Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO CONSOLIDATED FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on April 4, 2005

Registration No. 333-115344

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 2

to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Huntsman Advanced Materials LLC

(Exact Name of Registrant as Specified in its Charter)

| Delaware (State or Other Jurisdiction of Incorporation or Organization) | 2800 (Primary Standard Industrial Classification Code Number) | 92-0194012 (I.R.S. Employer Identification Number) |

500 Huntsman Way

Salt Lake City, UT 84108

(801) 584-5700

(Address, Including Zip Code, and Telephone Number, Including Area Code,

of Registrant's Principal Executive Offices)

Samuel D. Scruggs, Esq.

Executive Vice President,

General Counsel and Secretary

Huntsman Advanced Materials LLC

500 Huntsman Way

Salt Lake City, UT 84108

(801) 584-5700

(Name, Address, Including Zip Code, and Telephone Number, Including Area Code, of Agent For Service)

Copy to:

Nathan W. Jones, Esq.

Stoel Rives LLP

201 South Main Street, Suite 1100

Salt Lake City, UT 84111

(801) 328-3131

| Exact Name of Additional Registrants* | Jurisdiction of Incorporation/Organization | Primary Standard Industrial Classification Code Number | I.R.S. Employer Identification Number | |||

|---|---|---|---|---|---|---|

| Huntsman Advanced Materials Americas Inc. | Delaware | 2800 | 52-2215309 | |||

| Huntsman Advanced Materials (Belgium) BVBA | Belgium | 2800 | 98-0407856 | |||

| Huntsman Advanced Materials (Deutschland) GmbH | Germany | 2800 | 98-0407436 | |||

| Huntsman Advanced Materials Holdings (UK) Limited | United Kingdom | 2800 | 98-0407410 | |||

| Huntsman Advanced Materials (Spain) S.L. | Spain | 2800 | 98-0407423 | |||

| Huntsman Advanced Materials (Switzerland) GmbH | Switzerland | 2800 | 98-0413260 | |||

| Huntsman Advanced Materials (UK) Limited | United Kingdom | 2800 | 98-0407414 | |||

| Vantico Group S.A. | Luxembourg | 2800 | — | |||

| Vantico International S.à.r.l. | Luxembourg | 2800 | 98-0407428 | |||

- *

- Address and telephone of principal executive offices are the same as those of Huntsman Advanced Materials LLC.

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this registration statement.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

The Registrants hereby amend this registration statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment that specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act or until this registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

Information contained herein is subject to completion or amendment. A registration statement relating to these securities has been filed with the Securities and Exchange Commission. These securities may not be sold nor may offers to buy be accepted prior to the time the registration statement becomes effective. This prospectus shall not constitute an offer to sell or the solicitation of an offer to buy nor shall there be any sale of these securities in any State in which such offer, solicitation or sale would be unlawful prior to registration or qualification under the securities laws of any such State.

Subject to Completion—Dated April 4, 2005

PROSPECTUS

![]()

Huntsman Advanced Materials LLC

Exchange Offer for

$250,000,000 11% Senior Secured Notes due 2010

and

$100,000,000 Senior Secured Floating Rate Notes due 2008

This exchange offer will expire at 5:00 p.m., New York City Time,

on , 2005, unless extended.

Terms of the exchange offer:

- •

- We will exchange all outstanding 11% Senior Secured Notes due 2010 ("old fixed rate notes") and all outstanding Senior Secured Floating Rate Notes due 2008 ("old floating rate notes" and, together with the old fixed rate notes, "old notes") that are validly tendered and not withdrawn prior to the expiration of the exchange offer.

- •

- You may withdraw tendered old notes at any time prior to the expiration of the exchange offer.

- •

- The exchange of old notes will not be a taxable event for United States federal income tax purposes.

- •

- The terms of the new 11% Senior Secured Notes due 2010 ("new fixed rate notes") and the new Senior Secured Floating Rate Notes due 2008 ("new floating rate notes" and, collectively with the new fixed rate notes, "new notes") to be issued in this exchange offer are substantially identical to the terms of the old notes, except for transfer restrictions and registration rights relating to the old notes.

- •

- We will not receive any proceeds from the exchange offer.

- •

- There is no existing market for the new notes, and we have not and will not apply for their listing on any securities exchange.

See the "Description of New Notes" section on page 98 for more information about the new notes to be issued in this exchange offer.

This investment involves risks. See the section entitled "Risk Factors" that begins on page 17 for a discussion of the risks that you should consider prior to tendering your old notes for exchange.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or the accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2005

Each broker-dealer that receives new notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of the new notes it receives. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act of 1933, as amended, which we refer to as the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of new notes received in exchange for old notes where such old notes were acquired by the broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 120 days after the consummation of the exchange offer, we will make this prospectus, as amended and supplemented, available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

The following summary highlights selected information from this prospectus and may not contain all the information that is important to you. This prospectus contains information regarding our business and detailed financial information. You should carefully read this entire document.

In this prospectus, the terms "AdMat," "Company," "our," "us" and "we" refer to Huntsman Advanced Materials LLC and, unless the context otherwise requires, its subsidiaries. In this prospectus, "AdMat Holdings" refers to Huntsman Advanced Materials Holdings LLC, "AdMat Investment" refers to Huntsman Advanced Materials Investment LLC, "HLLC" or "Huntsman LLC" refers to Huntsman LLC and, unless the context otherwise requires, its subsidiaries, "HIH" refers to Huntsman International Holdings LLC and, unless the context otherwise requires, its subsidiaries, "HI" refers to Huntsman International LLC and, unless the context otherwise requires, its subsidiaries, "HMP" refers to HMP Equity Holdings Corporation, "HGI" refers to Huntsman Group Inc., "Huntsman" or "Huntsman Corporation" refers to Huntsman Corporation and, unless the context otherwise requires, its subsidiaries, "MatlinPatterson" refers to MatlinPatterson Global Opportunities Partners L.P. and its affiliates, "Consolidated Press" refers to Consolidated Press Holdings Limited and its subsidiaries, "SISU" refers to SISU Capital Limited and its affiliates, "MGPE" refers to Morgan Grenfell Private Equity Limited and its affiliates, "Vantico" or "Predecessor Company" refers to Vantico Group S.A. and, unless the context otherwise requires, its subsidiaries, "Vantico International" refers to Vantico International S.à.r.l., and "Ciba" refers to Ciba Specialty Chemicals Holdings Inc. Where the context requires, references to the "Company," "we," "us" or "our" as of a date prior to June 30, 2003, the date of the AdMat Transaction (as defined below), are to Vantico.

In this prospectus, we refer to the old fixed rate notes and the new fixed rate notes collectively as "fixed rate notes," the old floating rate notes and the new floating rate notes collectively as "floating rate notes," the fixed rate notes and the floating rate notes collectively as "Senior Secured Notes" and the old notes and the new notes collectively as "notes." Unless otherwise indicated, references in this prospectus to "CHF" are to the lawful currency of Switzerland, references to "euro" or "€" are to the single currency of participating Member States in the Third Stage of European Economic and Monetary Union pursuant to the Treaty Establishing the European Community, references to "GBP Sterling" or "£" are to the lawful currency of the U.K. and references to "U.S. dollars" or "$" are to the lawful currency of the United States of America.

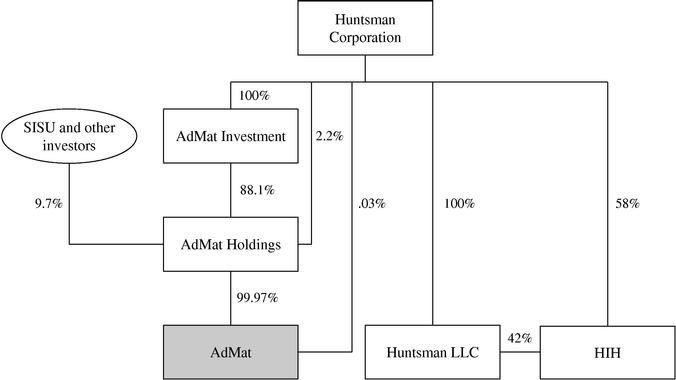

Our Company is a Delaware limited liability company, and substantially all of its membership interests are owned by Huntsman Advanced Materials Holdings LLC, a Delaware limited liability company ("AdMat Holdings"). The membership interests of AdMat Holdings are owned 88.1% by Huntsman Advanced Materials Investment LLC, a Delaware limited liability company ("AdMat Investment"), 2.2% by Huntsman Corporation and the balance of the membership interests are held by third parties, including SISU Capital Limited ("SISU"), a private investment firm based in London, U.K. All of the common and preferred membership interests in AdMat Investment are owned by Huntsman Corporation.

1

The following chart shows our current ownership structure.

In May 2000, a group led by MGPE acquired Ciba's former Performance Polymers business in a leveraged buyout transaction (the "2000 LBO"). The 2000 LBO was effected through Vantico. In 2001 and 2002, Vantico's business was adversely affected by a global downturn in the chemical industry, weakness in several of its key end-markets, including the aerospace, automotive and electronics markets, and a number of issues related to Vantico's separation from Ciba. In January 2003, Vantico reached agreement with its lenders under its senior secured credit facilities (the "Vantico Credit Facilities") to defer a payment due in December 2002 until its subsequent date of payment in January 2003. Additionally, the interest payment due on Vantico's 12% senior notes (the "Vantico Senior Notes") due in February 2003 was deferred. Vantico secured a waiver for the requirement to deliver covenant certificates to its senior lenders in respect of third and fourth quarter 2002 covenants and first quarter 2003 covenants, subject to the satisfaction of further conditions. The waiver was extended to June 30, 2003, while Vantico continued restructuring discussions with its stakeholders.

On June 30, 2003, MatlinPatterson, SISU, HGI, Huntsman Holdings and MGPE completed a restructuring and business combination involving Vantico, whereby ownership of the equity of Vantico was transferred to us in exchange for substantially all of the issued and outstanding Vantico Senior Notes and approximately $165 million of additional equity (the "AdMat Transaction"). In connection with the AdMat Transaction, we issued $250 million aggregate principal amount of fixed rate notes, and $100 million aggregate principal amount of floating rate notes at a discount of 2%, or for $98 million. Proceeds from the issuance of the Senior Secured Notes, along with a portion of the additional equity, were used to repay in full the Vantico Credit Facilities. Also in connection with the AdMat Transaction, we entered into a $60 million senior secured revolving credit facility (the "Revolving Credit Facility").

Prior to the AdMat Transaction, Vantico had three reportable business segments: Polymer Specialties, Electronics and Adhesives and Tooling. Each business segment developed, manufactured and marketed different products and services and was managed separately, as management at the time believed each required different technology and marketing strategies. In connection with the AdMat Transaction, we reorganized our operations and now have one reportable business segment.

2

Our principal executive offices are located at 500 Huntsman Way, Salt Lake City, Utah 84108 and our telephone number is 801-584-5700.

Overview

We are a leading global manufacturer and marketer of technologically advanced specialty chemicals used in a wide variety of industrial and consumer applications. Our business is characterized by the breadth of our product offering, our expertise in complex chemistry, our long-standing relationships with our key customers and our ability to develop and adapt our technology and our applications expertise for new markets and new applications. We operate 14 manufacturing facilities worldwide, with facilities in North America, Europe, Asia and South America. We provide our customers with the following:

- •

- Formulated polymer systems based on epoxy, polyurethane, acrylic and other materials,

- •

- Complex chemicals and additives, and

- •

- Basic and advanced epoxy resin compounds.

We derived approximately 46% of our revenues for the year ended December 31, 2004 from the sale of formulated polymer systems, 17% from complex chemicals and additives, 15% from advanced epoxy resin compounds and 22% from basic epoxy resin compounds. We are a global business serving customers in Europe, Africa and the Middle East ("EAME"); North, Central and South America (the "Americas"); and Asia, with sales in those regions constituting 53%, 25% and 22% of our total revenues, respectively, for the year ended December 31, 2004. Our revenues, net income and EBITDA (as defined in footnote (2) to Summary Consolidated Historical and Pro Forma Financial Information) were $1,162.4 million, $52.2 million and $186.1 million, respectively, for the year ended December 31, 2004.

Our products are used to address customer-specific application needs in a wide variety of applications, including adhesives, electrical and electronics materials, structural composites, surface technologies and tooling and modeling materials. Information with respect to revenues and specific end-markets is set forth in the following table. In many cases, our products are used either as replacements for traditional materials such as metals, wood, clay, glass, stone and ceramics, or where traditional materials do not meet demanding engineering specifications. We sell over 6,000 products to more than 5,000 customers.

| Applications | End-Markets | |

|---|---|---|

| Adhesives | aerospace, consumer/do-it-yourself ("DIY"), DVD, general industrial bonding, liquified natural gas ("LNG") transport, wind power generation | |

| Electrical and Electronics Materials | consumer and industrial electronics, electrical power generation and transmission; printed circuit boards | |

| Structural Composites | aerospace, electronic laminates, recreational sports equipment, wind power generation | |

| Surface Technologies | automotive, civil engineering, domestic appliance, food and beverage packaging, shipbuilding and marine maintenance | |

| Tooling and Modeling Materials | aerospace, automotive, industrial |

3

Adhesives

We produce innovative formulated polymer systems used as industrial and high-performance consumer adhesives based upon epoxy, polyurethane, acrylic and other materials, primarily marketed under theAraldite® brand name. Our adhesives are used to bond materials such as steel, aluminum, engineering plastics and structural composites. The sales of our adhesive systems have experienced rapid growth due to the continued substitution of adhesives for traditional joining techniques, such as welding and soldering, and the use of metal fasteners and clamps. We sell our adhesive products into industry-specific markets, the general industrial bonding market and the consumer DIY market. Our primary industry-specific markets are the aerospace, DVD, wind power generation and liquefied natural gas transport markets.

Electrical and Electronics Materials

We produce formulated polymer systems based on epoxy and polyurethane resins which are used to insulate, protect or shield both the environment from electrical current and electrical devices from the environment. We primarily sell our electrical products to customers in the electric power generation, transmission and distribution, consumer and industrial electronics, automotive and appliance markets. We believe we have a leading market position globally in epoxy-based electrical insulating materials.

We produce liquid formulated polymer systems used in the manufacture of soldermasks and inner layer resists for printed circuit boards. Soldermasks are permanent coatings, resistant to heat, chemicals and the environment, that allow various components and circuitry to be soldered to the surface of a printed circuit board. Inner layer resists are temporary photo-imageable materials that enable the generation of circuitry on the inner layers of printed circuit boards.

Structural Composites

We produce formulated polymer systems, complex chemicals and additives and basic and advanced epoxy resin compounds which are used to manufacture a variety of fiber-reinforced materials with enhanced structural properties, known as structural composites. Structural composites are lightweight, high-strength, rigid materials with high resistance to chemicals, moisture and high temperatures. We primarily sell our products to customers in the aerospace, automotive, wind power generation, recreational sports equipment and electronic laminates markets.

Surface Technologies

We produce formulated polymer systems, complex chemicals and additives and basic and advanced epoxy resin compounds to provide structural stability and broad application functionality, combined with overall economic efficiency, for a broad range of consumer and industrial coatings applications. These products are used to make coatings for the protection of steel and concrete substrates, such as floorings, metal furniture and appliances, buildings, the linings of storage tanks, food and beverage packaging, and the primer coat of automobile bodies and ships, among other applications. We are the world's third largest producer of basic liquid-epoxy resin ("BLR"), and its basic derivatives, the building blocks for epoxy-based products in coating applications. In addition, we are a leading manufacturer of complex chemicals and additives, such as curing agents, matting agents, accelerators, cross-linkers, and thermoplastic polyamides, which are used in combination with epoxy resins to impart properties such as chemical and abrasion resistance and improved surface appearance.

Tooling and Modeling Materials

We produce epoxy, polyurethane and acrylic-based formulated polymer systems used in the production of models, prototypes, patterns and molds and a variety of related products for design,

4

prototyping and short-run manufacture. Our products are used in the automotive, aerospace and industrial markets as productivity tools to quickly and efficiently create accurate prototypes and develop experimental models, primarily using computer-aided-design techniques. These products are valued for their resilience, heat resistance, dimensional stability, low shrinkage, ease of curing and ability to simulate the look and feel of a variety of materials. These characteristics have allowed our tooling and modeling materials to replace other materials traditionally used in these applications, such as wood, clay and engineering thermoplastics. Our products include photopolymers used in stereolithography ("SLA"), a process that combines computer-aided-design, laser technology and chemistry to permit a complex three-dimensional design to be rapidly replicated in finely-finished solid form.

5

Huntsman Corporation Initial Public Offering

On February 16, 2005, Huntsman Corporation, our parent corporation, completed initial public offerings of (i) 55,681,819 shares of its common stock sold by Huntsman Corporation and 13,579,546 shares of its common stock sold by a selling stockholder, in each case at a price to the public of $23 per share, and (ii) 5,750,000 shares of its 5% Mandatory Convertible Preferred Stock sold by Huntsman Corporation at a price to the public of $50 per share. Net proceeds to Huntsman Corporation from the offering were approximately $1,500 million, substantially all of which has been used to repay outstanding indebtedness of certain of Huntsman Corporation's subsidiaries, including HMP, HLLC and HIH.

| Securities Offered | $350,000,000 aggregate principal amount of new notes, consisting of $250,000,000 aggregate principal amount of new fixed rate notes and $100,000,000 aggregate principal amount of new floating rate notes, all of which have been registered under the Securities Act of 1933, as amended (the "Securities Act"). The terms of the new notes offered in the exchange offer are substantially identical to those of the old notes, except that certain transfer restrictions, registration rights and liquidated damages provisions relating to the old notes do not apply to the new registered notes. | |||

The Exchange Offer | We are offering to issue registered notes in exchange for a like principal amount and like denomination of our old notes. We are offering to issue these registered notes to satisfy our obligations under an exchange and registration rights agreement that we entered into with the initial purchasers of the old notes when we sold them in a transaction that was exempt from the registration requirements of the Securities Act. You may tender your old notes for exchange by following the procedures described under the heading "The Exchange Offer." | |||

Tenders; Expiration Date; Withdrawal | The exchange offer will expire at 5:00 p.m., New York City time, on , 2005, unless we extend it. If you decide to exchange your old notes for new notes, you must acknowledge that you are not engaging in, and do not intend to engage in, a distribution of the new notes. You may withdraw any notes that you tender for exchange at any time prior to , 2005. If we decide for any reason not to accept any old notes you have tendered for exchange, those notes will be returned to you without cost promptly after the expiration or termination of the exchange offer. See "The Exchange Offer—Terms of the Exchange Offer" and "—Withdrawal Rights" for a more complete description of the tender and withdrawal provisions. | |||

6

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions and we may terminate or amend the exchange offer if any of these conditions occur prior to the expiration of the exchange offer. These conditions include any change in applicable law or legal interpretation or governmental or regulatory actions that would impair our ability to proceed with the exchange offer, any general suspension or general limitation relating to trading of securities on any national securities exchange or the over-the-counter market or a declaration of war or other hostilities involving the United States. We may waive any of these conditions in our sole discretion. | |||

United States Federal Income Tax Consequences | The exchange of old notes for new notes in the exchange offer will not be a taxable transaction for United States federal income tax purposes. See "Material United States Federal Income Tax Consequences." | |||

Use of Proceeds | We will not receive any cash proceeds from the exchange offer. We will pay all expenses incident to the exchange offer. See "Use of Proceeds" for a discussion of the use of proceeds from the issuance of the old notes. | |||

Exchange Agent | Wells Fargo Bank, N.A. | |||

Consequences of Failure to Exchange | Old notes that are not tendered or that are tendered but not accepted will continue to be subject to the restrictions on transfer that are described in the legend on those notes. In general, you may offer or sell your old notes only if they are registered under, or offered or sold under an exemption from, the Securities Act and applicable state securities laws. We, however, will have no further obligation to register the old notes. If you do not participate in the exchange offer, the liquidity of your notes could be adversely affected. | |||

Consequences of Exchanging Your Old Notes | Based on interpretations of the SEC set forth in certain no-action letters issued to third parties, we believe that you may offer for resale, resell or otherwise transfer the new notes that we issue in the exchange offer without complying with the registration and prospectus delivery requirements of the Securities Act if you: | |||

• | acquire the new notes issued in the exchange offer in the ordinary course of your business; | |||

• | are not participating, do not intend to participate, and have no arrangement or understanding with anyone to participate, in the distribution of the new notes issued to you in the exchange offer; and | |||

• | are not an "affiliate" of our company as defined in Rule 405 of the Securities Act. | |||

7

If any of these conditions are not satisfied and you transfer any new notes issued to you in the exchange offer without delivering a proper prospectus or without qualifying for a registration exemption, you may incur liability under the Securities Act. We will not be responsible for, or indemnify you against, any liability you may incur. | ||||

Any broker-dealer that acquires new notes in the exchange offer for its own account in exchange for old notes which it acquired through market-making or other trading activities must acknowledge that it will deliver a prospectus when it resells or transfers any new notes. See "Plan of Distribution" for a description of the prospectus delivery obligations of broker-dealers in the exchange offer. | ||||

The terms of the new notes and those of the outstanding old notes are identical in all material respects, except:

- (1)

- the new notes will have been registered under the Securities Act;

- (2)

- the new notes will not contain transfer restrictions and registration rights that relate to the old notes; and

- (3)

- the new notes will not contain provisions relating to the payment of liquidated damages to be made to the holders of the old notes under circumstances related to the timing of the exchange offer.

A brief description of the material terms of the new notes follows:

| Issuer | Huntsman Advanced Materials LLC | |||

Notes Offered | $250,000,000 principal amount of 11% Senior Secured Notes due 2010. | |||

$100,000,000 principal amount of Senior Secured Floating Rate Notes due 2008. | ||||

Maturity | The fixed rate notes mature on July 15, 2010. The floating rate notes mature on July 15, 2008. | |||

Interest Rate | The fixed rate notes bear interest at a rate of 11% per annum (calculated using a 360-day year). The floating rate notes bear interest at a rate per annum equal to LIBOR plus 8.00%, provided that in no event will LIBOR be deemed to be less than 2.00%. Interest on the floating rate notes is reset semi-annually. | |||

Interest Payment Dates | January 15 and July 15, beginning on January 15, 2004. The old notes were sold with accrued interest from June 30, 2003. | |||

8

Original Issue Discount | The floating rate notes were issued with original issue discount for United States Federal income tax purposes and the new floating rate notes also will carry original issue discount. United States holders are required to include original issue discount in gross income for United States Federal income tax purposes over the term of the floating rate notes in advance of the receipt of cash payments to which such income is attributable. See "Description of New Notes—Principal, Maturity and Interest—Floating Rate Notes." | |||

Guarantees | The new notes initially will be guaranteed on a senior basis by our U.S. subsidiary and certain of our non-U.S. subsidiaries. See "Description of New Notes—Ranking and Guarantees." | |||

Security | The new notes initially will be secured by second priority liens (or a second priority position under the intercreditor agreement) on our assets and those of our subsidiaries that from time to time secure our obligations under our Revolving Credit Facility. Our Revolving Credit Facility is secured by first priority liens (or a first priority position under the intercreditor agreement) on those assets. See "Description of New Notes—Security." | |||

Intercreditor Agreement | The trustee, on behalf of the holders of the notes, and the bank agent, on behalf of the lenders under the Revolving Credit Facility, have entered into an intercreditor agreement which provides, among other things, that the bank agent, on behalf of the lenders under the Revolving Credit Facility, holds a first priority security interest (or a first priority position under the intercreditor agreement) in the shared collateral and, the trustee, on behalf of the holders of the notes, holds a second priority security interest (or a second priority position under the intercreditor agreement) in the shared collateral. The intercreditor agreement provides that, for so long as any obligations or commitments are outstanding under the Revolving Credit Facility, the bank agent will have the exclusive right to instruct the collateral agent to manage, perform and enforce the terms of the security documents relating to the collateral and to exercise and enforce all privileges, rights and remedies thereunder according to its direction. Further, the bank agent may, without the consent of the trustee or the holders of the notes, release any or all of the collateral securing both the Revolving Credit Facility and the notes, except in connection with the repayment of the Revolving Credit Facility or during the occurrence of an event of default under the indenture governing the notes, subject to certain limited exceptions. See "Description of New Notes—Intercreditor Agreement." | |||

9

Fall Away Event | In the event that the notes achieve investment grade ratings from both S&P and Moody's, the guarantees of, and the collateral pledged by, the non-U.S. guarantors will be released, subject to certain conditions. In connection with such a release, each pledge of shares of a released non-U.S. guarantor that continues to form part of the collateral securing the notes will be limited to a pledge of 65% of the shares of such released non-U.S. guarantor. See "Description of New Notes—Fall Away Event." | |||

Ranking | Our obligations and those of the guarantors with respect to the notes rank equally in right of payment with all of our and their senior obligations. The notes effectively rank senior in right of payment to all of our and their senior unsecured obligations to the extent of the value of the collateral securing the notes. Our obligations and those of the guarantors with respect to the notes effectively rank junior in right of payment to our and their obligations under the Revolving Credit Facility to the extent of the value of the assets securing such facility. The notes are structurally subordinated to the obligations of our subsidiaries that are not guarantors. See "Description of New Notes—Ranking and Guarantees." | |||

Optional Redemption | We may redeem all or a portion of the fixed rate notes at any time on or after July 15, 2007 at the redemption prices set forth under "Description of New Notes—Optional Redemption." Before July 15, 2007, we may redeem all or a portion of the fixed rate notes at 100% of their principal amount plus a "make whole" premium. | |||

We may redeem all or a portion of the floating rate notes at any time on or after July 15, 2005 at the redemption prices set forth under "Description of New Notes—Optional Redemption." Before July 15, 2005, we may redeem all or a portion of the floating rate notes at 100% of their principal amount plus a "make whole" premium. | ||||

See "Description of New Notes—Optional Redemption." | ||||

Optional Redemption after Certain Equity Offerings | At any time (which may be more than once) on or before July 15, 2006, we may redeem up to 35% of the aggregate principal amount of the fixed rate notes with the net cash proceeds of certain equity offerings, provided that: | |||

• | we pay 111% of the principal amount of the fixed rate notes, plus interest; | |||

• | we redeem the fixed rate notes within 120 days of completing the equity offering; and | |||

• | at least 60% of the aggregate principal amount of the fixed rate notes remains outstanding afterwards. | |||

10

At any time (which may be more than once) on or before July 15, 2005, we may redeem up to 35% of the aggregate principal amount of the floating rate notes with the net cash proceeds of certain equity offerings, provided that: | ||||

• | we pay 111% of the principal amount of the floating rate notes, plus interest; | |||

• | we redeem the floating rate notes within 120 days of completing the equity offering; and | |||

• | at least 60% of the aggregate principal amount of the floating rate notes remains outstanding afterwards. | |||

See "Description of New Notes—Optional Redemption." | ||||

Change of Control Offer | Upon the occurrence of a change of control, you will have the right to require us to repurchase all or a portion of your notes at a purchase price in cash equal to 101% of their principal amount, plus accrued and unpaid interest, if any, to the repurchase date. See "Description of New Notes—Repurchase at the Option of Holders upon a Change of Control." | |||

Asset Sale Proceeds | If we or our restricted subsidiaries engage in asset sales, we and such subsidiaries generally must either invest the net cash proceeds from such sales in the business within a period of time or we must make an offer to repurchase a principal amount of the notes equal to the excess net cash proceeds. The purchase price of the notes will be 100% of their principal amount, plus accrued and unpaid interest, if any, to the date of repurchase. See "Description of New Notes—Certain Covenants—Limitation on Asset Sales." | |||

Events of Loss | If we or our restricted subsidiaries experience events of loss at a time when there are not outstanding amounts as commitments under the Revolving Credit Facility, we and such subsidiaries generally must either invest the net loss proceeds from such events in the business within a period of time or we must make an offer to repurchase a principal amount of the notes equal to the excess net loss proceeds. The purchase price of the notes will be 100% of their principal amount, plus accrued and unpaid interest, if any, to the date of repurchase. See "Description of New Notes—Certain Covenants—Events of Loss." | |||

Certain Indenture Provisions | The indenture governing the notes contains covenants limiting our (and our restricted subsidiaries') ability to, among other things: | |||

• | incur additional debt; | |||

• | pay dividends, redeem stock or make other distributions; | |||

• | make certain other restricted payments; | |||

• | issue capital stock; | |||

11

• | make certain investments; | |||

• | create liens; | |||

• | enter into transactions with affiliates; | |||

• | enter into sale and leaseback transactions; | |||

• | merge or consolidate; and | |||

• | transfer and sell assets. | |||

These covenants are subject to a number of important qualifications and limitations. See "Description of New Notes—Certain Covenants." | ||||

Exchange Offer; Registration Rights | We have agreed to: | |||

• | file a registration statement for the new notes within 315 days after the issue date of the old notes; | |||

• | cause the registration statement to become effective within 375 days after the issue date of the old notes (the "effectiveness date"); and | |||

• | consummate the exchange offer within 420 days after the issue date of the old notes (the "completion date"). | |||

In addition, we have agreed, in certain circumstances, to file a "shelf registration statement" that would allow some or all of the old notes to be offered to the public. | ||||

If we fail to fulfill our obligations with respect to registration of the new notes (a "registration default"), the annual interest rate on the notes will increase by 0.25% during the first 90-day period during which the registration default continues, and will increase by an additional 0.25% for each subsequent 90-day period during which the registration default continues, up to a maximum increase of 1.0% over the interest rate that would otherwise apply to the notes; provided, however, that additional interest may not accrue with respect to more than one registration default at any one time. | ||||

We failed to cause the registration statement to become effective by the effectiveness date. Therefore, additional interest accrued on the notes from the effectiveness date until the date of this prospectus. In addition, we failed to complete the exchange offer by the completion date. Therefore, additional interest will accrue on the notes from the date of this prospectus until the exchange offer is completed. This additional interest will be paid to holders in cash on the same dates that we make other interest payments on the notes until all such additional interest has been paid. | ||||

12

Use of Proceeds | We will not receive any proceeds from the exchange offer. We used the net proceeds from the sale of the old notes, along with proceeds from an equity private placement and a capital infusion in connection with the AdMat Transaction, together with available cash balances, to repay in full the outstanding borrowings under the senior secured credit facilities of Vantico International and certain other outstanding indebtedness. See "Use of Proceeds." | |||

Risk Factors | You should carefully consider all the information set forth in this prospectus and, in particular, should evaluate the specific risk factors set forth under "Risk Factors" before participating in this exchange offer. | |||

Failure to Exchange Your Old Notes

The old notes which you do not tender or we do not accept will, following the exchange offer, continue to be restricted securities. Therefore, you may only transfer or resell them in a transaction registered under or exempt from the Securities Act and all applicable state securities laws. We will issue the new notes in exchange for the old notes under the exchange offer only following the satisfaction of the procedures and conditions described in the caption "The Exchange Offer."

Any old notes tendered and exchanged in the exchange offer will reduce the aggregate principal amount outstanding of the old notes. Because we anticipate that most holders of the old notes will elect to exchange their old notes, we expect that the liquidity of the markets, if any, for any old notes remaining after the completion of the exchange offer will be substantially limited.

As of December 31, 2004, we had no borrowings outstanding under the Revolving Credit Facility that ranked senior to the notes and had approximately $10.1 million of letters of credit issued and outstanding under the Revolving Credit Facility. We have no amortization payments due under the Revolving Credit Facility in 2005, and we have approximately $40 million due in total annual net interest payments on our total debt. As of December 31, 2004, our guarantors had no material outstanding third-party debt.

The agreements governing the Revolving Credit Facility and the indenture governing the notes limit our ability to incur additional debt. Consequently, we would be required to obtain amendments of the agreements and the indenture before we incurred any additional debt, other than the types of debt specifically identified in those documents as permitted. For more information, see "Description of Other Indebtedness" below.

13

Summary Consolidated Historical and Pro Forma Financial Information

The summary consolidated historical financial data presents Vantico's business as of the dates and for the periods indicated below. The summary consolidated pro forma statement of operations data for the year ended December 31, 2003, gives effect to the completion of the AdMat Transaction, including the issuance of the old notes and our acquisition of Vantico, as if such transactions occurred on January 1, 2003. The summary financial data set forth below should be read in conjunction with the audited and unaudited consolidated financial statements of Vantico, "Management's Discussion and Analysis of Financial Condition and Results of Operations," "Unaudited Pro Forma Financial Information" and "Selected Historical Financial Information" included elsewhere in this prospectus and, in each case, any notes thereto.

| | Summary Historical Financial Data | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | AdMat | Predecessor Company | |||||||||||||||

| | Year Ended December 31, 2004 | Year Ended December 31, 2003 Pro Forma(3) | Six Months Ended December 31, 2003 | Six Months Ended June 30, 2003 | Year Ended December 31, 2002 | ||||||||||||

| | (Dollars in Millions) | ||||||||||||||||

| Revenues | $ | 1,162.4 | $ | 1,049.6 | $ | 517.8 | $ | 531.8 | $ | 949.0 | |||||||

| Cost of goods sold | 869.5 | 823.5 | 410.8 | 412.7 | 707.0 | ||||||||||||

| Gross profit | 292.9 | 226.1 | 107.0 | 119.1 | 242.0 | ||||||||||||

| Expenses: | |||||||||||||||||

| Selling, general and administrative | 184.0 | 198.0 | 94.9 | 103.1 | 219.0 | ||||||||||||

| Research and development | 21.4 | 23.0 | 10.8 | 12.2 | 26.0 | ||||||||||||

| Impairment of long lived assets | — | — | — | — | 56.0 | ||||||||||||

| Litigation charges | — | — | — | — | — | ||||||||||||

| Legal and contract settlement (credits) charges, net | (8.5 | ) | 5.5 | — | 5.5 | (9.0 | ) | ||||||||||

| Reorganization costs | — | 27.5 | — | 27.5 | 22.0 | ||||||||||||

| Restructuring costs | 9.0 | — | — | — | — | ||||||||||||

| Other operating (income) expense(1) | (46.3 | ) | (20.0 | ) | (10.0 | ) | 23.8 | 1.0 | |||||||||

| Total expenses | 159.6 | 234.0 | 95.7 | 172.1 | 315.0 | ||||||||||||

| Operating income (loss) | 133.3 | (7.9 | ) | 11.3 | (53.0 | ) | (73.0 | ) | |||||||||

| Interest expense | (44.1 | ) | (41.7 | ) | (21.3 | ) | (36.3 | ) | (68.0 | ) | |||||||

| Income (loss) before income taxes | 89.2 | (49.6 | ) | (10.0 | ) | (89.3 | ) | (141.0 | ) | ||||||||

| Income tax benefit (expense) | (36.0 | ) | (7.3 | ) | (3.3 | ) | 11.4 | (7.0 | ) | ||||||||

| Minority interests in subsidiaries income | (1.0 | ) | — | — | — | ||||||||||||

| Income (loss) before accounting change | 52.2 | (56.9 | ) | (13.3 | ) | (77.9 | ) | (148.0 | ) | ||||||||

| Cumulative effect of accounting change | — | — | — | — | (3.0 | ) | |||||||||||

| Net income (loss) | 52.2 | (56.9 | ) | (13.3 | ) | (77.9 | ) | (151.0 | ) | ||||||||

| Interest expense, net | 44.1 | 41.7 | 21.3 | 36.3 | 68.0 | ||||||||||||

| Income tax (benefit) expense | 36.0 | 7.3 | 3.3 | (11.4 | ) | 7.0 | |||||||||||

| Depreciation and amortization | 53.8 | 56.1 | 27.3 | 28.8 | 59.0 | ||||||||||||

| EBITDA(2) | $ | 186.1 | $ | 48.2 | $ | 38.6 | $ | (24.2 | ) | $ | (17.0 | ) | |||||

| Balance Sheet Data (at period end): | |||||||||||||||||

| Total assets | $ | 938.9 | $ | 900.7 | $ | 900.7 | $ | 1,050.0 | |||||||||

| Total long-term debt | 348.7 | 348.3 | 348.3 | 648.0 | |||||||||||||

| Other Data: | |||||||||||||||||

| Capital expenditures | $ | 17.4 | $ | 11.8 | $ | 5.8 | $ | 6.0 | $ | 24.0 | |||||||

Notes to summary consolidated historical and pro forma financial information (dollars in millions):

- (1)

- In the historical periods, these amounts include the unrealized exchange gains/(losses) arising from the revaluation of non-functional currency denominated debt, realized exchange gains/(losses) arising from the sale of products and the purchase of raw materials, goods and services denominated in non-functional currencies and unrealized gains/(losses) arising from the revaluation of the current assets and liabilities held in non-functional currencies. In the pro forma period, the effect

14

of the revaluation of non-functional currency denominated debt has been eliminated as substantially all of such debt has been repaid in connection with the AdMat Transaction.

- (2)

- EBITDA is defined as net income (loss) before interest, income taxes, depreciation and amortization. We believe that EBITDA enhances an investor's understanding of our financial performance and our ability to satisfy principal and interest obligations with respect to our indebtedness. However, EBITDA should not be considered in isolation or viewed as a substitute for net income, cash flow from operations or other measures of performance as defined by GAAP. Moreover, EBITDA as used herein is not necessarily comparable to other similarly titled measures of other companies due to potential inconsistencies in the method of calculation. Our management uses EBITDA to assess financial performance and debt service capabilities. In assessing financial performance, our management reviews EBITDA as a general indicator of economic performance compared to prior periods. Because EBITDA excludes interest, income taxes, depreciation and amortization, EBITDA provides an indicator of general economic performance that is not affected by debt restructurings, fluctuations in interest rates or effective tax rates, or levels of depreciation and amortization. Accordingly, our management believes this type of measurement is useful for comparing general operating performance from period to period and making certain related management decisions. EBITDA is also used by securities analysts, lenders and others in their evaluation of different companies because it excludes certain items that can vary widely across different industries or among companies within the same industry. For example, interest expense can be highly dependent on a company's capital structure, debt levels and credit ratings. Therefore, the impact of interest expense on earnings can vary significantly among companies. In addition, the tax positions of companies can vary because of their differing abilities to take advantage of tax benefits and because of the tax policies of the various jurisdictions in which they operate. As a result, effective tax rates and tax expense can vary considerably among companies. Finally, companies employ productive assets of different ages and utilize different methods of acquiring and depreciating such assets. This can result in considerable variability in the relative costs of productive assets and the depreciation and amortization expense among companies. Our management also believes that our investors use EBITDA as a measure of our ability to service indebtedness as well as to fund capital expenditures and working capital requirements. Nevertheless, our management recognizes that there are material limitations associated with the use of EBITDA in the evaluation of our company as compared to net income, which reflects overall financial performance, including the effects of interest, income taxes, depreciation and amortization. EBITDA excludes interest expense. Because we have borrowed money in order to finance our operations, interest expense is a necessary element of our costs and ability to generate revenue. Therefore, any measure that excludes interest expense has material limitations. EBITDA also excludes taxes. Because the payment of taxes is a necessary element of our operations, any measure that excludes tax expense has material limitations. Finally, EBITDA excludes depreciation and amortization expense. Because we use capital assets, depreciation and amortization expense is a necessary element of our costs and ability to generate revenue. Therefore, any measure that excludes depreciation and amortization expense has material limitations. Our management compensates for the limitations of using EBITDA by using it to supplement GAAP results to provide a more complete understanding of the factors and trends affecting the business than GAAP results alone. Our management also uses other metrics to evaluate capital structure, tax planning and capital investment decisions. For example, our management uses credit ratings and net debt ratios to evaluate capital structure, effective tax rate by jurisdiction to evaluate tax planning, and payback period and internal rate of return to evaluate capital investments. Our management also uses trade working capital to evaluate its investment in accounts receivable and inventory, net of accounts payable.

15

- We believe that net income (loss) is the performance measure calculated and presented in accordance with GAAP that is most directly comparable to EBITDA and that cash provided by (used in) operating activities is the liquidity measure calculated and presented in accordance with GAAP that is most directly comparable to EBITDA. The following table reconciles EBITDA to our net income (loss) and to our cash provided by (used in) operations:

| | | | Predecessor Company | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, 2004 | Six Months Ended December 31, 2003 | Six Months Ended June 30, 2003 | Year Ended December 31, 2002 | |||||||||

| EBITDA | $ | 186.1 | $ | 38.6 | $ | (24.2 | ) | $ | (17.0 | ) | |||

| Depreciation and amortization expense | (53.8 | ) | (27.3 | ) | (28.8 | ) | (59.0 | ) | |||||

| Interest expense, net | (44.1 | ) | (21.3 | ) | (36.3 | ) | (68.0 | ) | |||||

| Income tax (expense) benefit | (36.0 | ) | (3.3 | ) | 11.4 | (7.0 | ) | ||||||

| Net income (loss) | 52.2 | (13.3 | ) | (77.9 | ) | (151.0 | ) | ||||||

Cumulative effect of accounting change | — | — | — | 3.0 | |||||||||

| Depreciation and amortization expense | 53.8 | 27.3 | 28.8 | 59.0 | |||||||||

| Impairment and non-cash restructuring charges | — | — | — | 56.0 | |||||||||

| Legal and contract settlement (credits) charges, net | — | — | — | (9.0 | ) | ||||||||

| Non-cash interest | 2.9 | 1.2 | — | 9.0 | |||||||||

| Deferred income taxes | 22.9 | 0.6 | (19.3 | ) | 5.0 | ||||||||

| Unrealized (gain) loss on foreign currency transactions | (44.9 | ) | (11.6 | ) | 23.8 | 1.0 | |||||||

| Litigation charges | — | — | — | — | |||||||||

| Other, net | 0.4 | 0.9 | 2.0 | (5.0 | ) | ||||||||

| Changes in operating assets and liabilities | (52.3 | ) | 7.1 | 43.9 | (9.0 | ) | |||||||

| Net cash provided by (used in) operating activities | 35.0 | 12.2 | 1.3 | (41.0 | ) | ||||||||

- Included in EBITDA are the following items:

Summary Historical Financial Data

| | AdMat | Predecessor Company | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, 2004 | Year Ended December 31, 2003 Pro Forma(3) | Six Months Ended December 31, 2003 | Six Months Ended June 30, 2003 | Year Ended December 31, 2002 | ||||||

| | (Dollars in Millions) | | | ||||||||

| Foreign currency effect of predecessor debt structure | — | — | — | (33.8 | ) | 14.0 | |||||

| Reorganization costs | — | (27.5 | ) | — | (27.5 | ) | (22.0 | ) | |||

| Restructuring costs | (9.0 | ) | — | — | — | — | |||||

| Legal and contract settlement credits (charges), net | 8.5 | (5.5 | ) | — | (5.5 | ) | 9.0 | ||||

| Asset impairment charges | — | — | — | — | (56.0 | ) | |||||

| Litigation charges | — | — | — | — | — | ||||||

- (3)

- See "Unaudited Pro Forma Financial Information" for discussion of the pro forma information.

16

You should carefully consider the risks described below in addition to all other information provided to you in this prospectus before participating in this exchange offer. Any of the following risks could materially and adversely affect our business, financial condition or results of operations.

Our substantial leverage and debt service obligations could harm our business or adversely affect our ability to meet our obligations, including our obligations under the notes.

We have a large amount of outstanding indebtedness. As of December 31, 2004, we had total debt of $350.4 million. There can be no assurance that we will be able to repay all our outstanding indebtedness, including our indebtedness under the notes, as it comes due and that we will not become insolvent.

Our high level of debt could have important consequences to holders of the notes, including the following:

- •

- we may have difficulty borrowing money in the future for working capital, capital expenditures, acquisitions or general corporate purposes;

- •

- we will need to use a large portion of our cash flow from operations to pay principal and interest on our debt, which will reduce the amount of cash available to us to finance our operations and other business activities;

- •

- we may have a much higher level of debt than certain of our competitors, which may put us at a competitive disadvantage; and

- •

- our debt level makes us more vulnerable to economic downturns and adverse developments in our business.

We and our subsidiaries may be able to incur substantial debt in the future. The terms of the instruments governing our debt will restrict, but not fully prohibit, us and our affiliates from doing so. If new debt is added to our debt described above, the related risks that we face could intensify.

Indebtedness under the Revolving Credit Facility and the floating rate notes will be subject to floating interest rates, which would result in our interest expense increasing if interest rates rise.

Indebtedness under the Revolving Credit Facility and the floating rate notes are subject to floating interest rates. Changes in economic conditions could result in higher interest rates, thereby increasing our interest expense and reducing funds available for operations or other purposes. Accordingly, we may experience economic losses and a negative impact on earnings as a result of interest rate fluctuations. Although we may use interest rate protection agreements from time to time to reduce our exposure to interest rate fluctuations in some cases, we may not elect or have the ability to implement hedges or, if we do implement them, they may not achieve the desired effect. See "Capitalization," "Description of Other Indebtedness" and "Description of New Notes."

A downgrade in the ratings of our debt securities could result in increased interest and other financial expenses related to our borrowings and could restrict our access to additional capital.

Standard and Poor's Ratings Services and Moody's Investors Service maintain credit ratings for our Company. Each of these ratings is currently below investment grade. Any decision by these or other ratings agencies to downgrade such ratings in the future could result in increased interest and other financial expenses relating to the future borrowings and could restrict our ability to obtain additional

17

financing on satisfactory terms. In addition, any downgrade could restrict our access to, and negatively impact the terms of, trade credit extended by our suppliers of raw materials.

Prices can be cyclical and may decrease due to supply and demand.

Many of our customers are in mature industries that have cyclical periods of expansion and contraction, which affect the demand for our products and can, during periods of contraction, put pressure on our ability to raise or maintain prices. Changes in the supply or demand for our products can harm the results of our business, particularly our sales of basic epoxy resins and their common derivatives.

Supply and pricing can also be affected by decreased demand in the markets we serve. For example, the recent declines in the electronics market have meant that integrated producers of laminates for the electronics market have seen their demand decrease. This has led at least one major producer of electronics laminates to sell basic epoxy resins normally consumed in the manufacture of its laminates into other markets, increasing supply and decreasing prices in these markets.

Many of the industries we serve have been consolidated into the hands of fewer participants in recent years. As a result, in many industries in which our products are used, such as aerospace, automotive and heavy electrical equipment manufacturing, there are only a few large potential customers for our products and may be fewer potential customers in the future. Where our customers are in consolidated industries, they may have greater bargaining power, decreasing our ability to raise or maintain our prices.

In addition, external factors beyond our control, such as general economic conditions, competitors' actions, international events and circumstances and governmental regulation in the United States and in other foreign jurisdictions can cause volatility in raw material prices, as well as fluctuations in demand for our products, product prices, volumes and margins.

Our operating margins may decrease if we cannot pass on to customers increased prices for the raw materials and energy we depend on or if prices for our products decrease faster than raw material prices.

The base petrochemical industry, which affects our raw material prices, historically has experienced alternating periods of tight supply, causing prices and profit margins to increase, followed by periods of substantial capacity increase, resulting in oversupply, declining prices, reduction in the use of existing production capacity and lower operating profit margins.

Bisphenol A and epichlorohydrin are key raw materials for our products, particularly in our coating systems and electrical insulating materials businesses. The cost of these materials, in the aggregate, generally represents a significant portion of our raw material costs. The prices and availability of these raw materials change with market conditions and may be highly volatile. In addition, the supplier for one of the raw materials, epichlorohydrin, is also a competitor in certain of our basic epoxy resin markets. We have generally been able to pass on changes in the prices of raw materials to our customers within three to six months after they come into effect. However, there have been, and may be in the future, periods of time during which raw material price increases cannot be passed on to customers. Even during periods in which raw material prices decrease, we may suffer decreasing operating profit margins, if raw material price reductions occur at a slower rate than the rate of decreases in the selling prices of our products. We typically do not enter into hedging arrangements with respect to prices of raw materials but we have entered into long-term supply contracts for raw materials. Any major change in the supply or price of these raw materials could harm our business, financial condition, results of operations or cash flows.

Energy costs can impact our profitability if they cannot be passed on to customers. Accurately predicting trends in energy costs is difficult to achieve as energy costs are, to a large extent, subject to

18

factors beyond our control—for example, political conditions in oil producing regions. Our energy costs have recently increased, particularly in North America. If our energy costs continue to rise, and we cannot pass these costs on to our customers, our profitability could be negatively affected. Additionally, rising energy costs may have a negative impact on our customers, which could reduce demand for our products and adversely affect our business, financial condition, results of operations or cash flows.

Our business may be harmed if we are unable to implement our business and cost reduction strategies.

Our future financial performance and success will largely depend on our ability to implement our business strategies successfully. We may not be able to successfully implement our business strategies. These strategies may not sustain or improve and may harm our results of operations in targeted sectors. In particular, we may be unable to lower our production costs, increase our manufacturing efficiency, enhance our current portfolio of products or capitalize on our status as a subsidiary of Huntsman.

Our business strategies are based on our assumptions about future demand for our products and the new products and applications we are developing, and on our continuing ability to produce our products profitably. Each of these factors depends, among other things, on our ability to:

- •

- finance our operating and product development activities, and to maintain high quality and efficient manufacturing operations;

- •

- relocate and close certain manufacturing facilities with minimal disruption to our operations;

- •

- access quality raw materials in a cost-effective and timely manner;

- •

- protect our intellectual property portfolio; and

- •

- retain and attract highly-skilled technical, marketing and managerial personnel.

We may be unable to implement on a timely basis our business strategies, including the reductions or rationalization that are part of our cost reduction strategy. In the process of implementing our business strategies, we may experience severe business disruption, loss of key personnel and difficulties with respect to the gathering and processing of accounting information. In addition, the costs involved in implementing our business strategies may be substantially greater than we currently anticipate. Any failure to develop, revise or implement our business strategies in a timely and effective manner may adversely effect our business, financial condition, results of operations or cash flows.

We have many competitors, some of whom have significantly greater resources than us.

We compete with a variety of other companies in the markets in which we operate, and those companies are different in each of the markets in which we operate. Our ability to compete effectively is based on a number of considerations, such as product innovation, product quality, service, distribution capability and price. The relative importance of these considerations is not consistent across the markets in which we operate. In the market for basic resins and their common derivatives, we compete on the basis of price and service with companies that are back-integrated into the key raw materials for basic resins, bisphenol A and epichlorohydrin, which we do not produce. This back-integration may give our competitors a market advantage in certain circumstances and in some markets. We purchase a material amount of our bisphenol A and epichlorohydrin, and some basic resins, from one or more of our competitors in the market for basic resins and their common derivatives, which may give those competitors a market advantage in certain circumstances. Since most of our products contain derivatives of basic resins, our ability to access supplies of bisphenol A, epichlorohydrin and basic resins at competitive prices is material to our ability to compete effectively. We may have insufficient financial resources in comparison to some of our competitors, some of whom are larger and have significantly greater financial and other resources than us, to respond to these

19

financial pressures and to continue to make investments in our business. In our other markets, we compete on the basis of product innovation, product quality and distribution capability.

Failure to keep up with the technological innovation could harm our profitability and cash flows.

Our operating results will depend to a significant extent on our ability to continue to introduce new products and applications that offer distinct value for our customers. In many of the industry sectors to which we sell our products, products become obsolete rapidly. As a result, rapid and frequent developments are needed in order to remain competitive and to minimize the effects of downward sales price pressure when a product matures. Likewise, manufacturers periodically introduce new generations of products or require new technological capacity to develop customized products. We expect to continue to identify, develop and market innovative products on a timely basis to replace existing products in order to maintain our profit margins and our competitive position. We intend to devote sizeable resources to the development of new technologically advanced products and to continue to devote a substantial amount of expenditures to the research, development and technology process functions of our business. However, we are unable to give assurance that:

- •

- we can always successfully develop new products and applications or bring them to market in a timely manner;

- •

- products or technologies developed by others will not render our offerings obsolete or non-competitive;

- •

- the market will accept our innovations; and

- •

- our competitors will not be able to produce our core non-patented products at a lower cost.

Key customers may switch to other suppliers if we are not technologically innovative and high switching costs for those customers may mean that it is difficult to regain them again until the end of the life cycle of the other suppliers' products, which may be several years.

Our operations are conducted globally and our results of operations are subject to currency translation risk and currency transaction risk.

We report our financial results in U.S. dollars. The financial condition and results of operations of each operating subsidiary are reported in the relevant local currency and are then translated into U.S. dollars at the applicable currency exchange rate for inclusion in our financial statements. Exchange rates between these currencies and U.S. dollars in recent years have fluctuated and may do so in the future. We generate the majority of our revenues in euros and U.S. dollars; however, we also incur a substantial proportion of our operating expenses in other currencies, including CHF and GBP Sterling. Any appreciation of the U.S. dollar against the euro and other world currencies may adversely affect sales as reported in U.S. dollars and also affect the comparability of our results between different financial periods; conversely, a weakening of the U.S. dollar particularly against the euro, may positively affect sales as reported in U.S. dollars. In addition, a weakening of the U.S. dollar versus the euro may make it possible for producers of resins whose costs are denominated in U.S. dollars to compete with us more effectively in Europe. Significant changes in the value of the euro, U.S. dollar, CHF and GBP Sterling relative to each other could also harm our financial condition and results of operations. Our business could also be adversely affected by a general or regional economic climate of price deflation, as such conditions could generally make it harder to repay our indebtedness, even if our indebtedness were hedged against currency risk.

In addition to currency translation risks, we incur a currency transaction risk whenever one of our operating subsidiaries enters into either a purchase or a sales transaction using a different currency from the currency in which it receives revenues. Given the volatility of exchange rates, there can be no assurance that we will be able to manage our currency transaction and/or translation risks effectively, or

20

that any volatility in currency exchange rates will not have a material adverse effect on our financial condition or results of operations or cash flows. Since most of our indebtedness is denominated in U.S. dollars, a strengthening of the U.S. dollar could make it more difficult for us to repay our indebtedness.

We are subject to many environmental and safety regulations that may result in unanticipated costs or liabilities.

We are subject to extensive federal, state, local and foreign laws, regulations, rules and ordinances relating to pollution, protection of the environment and the generation, storage, handling, transportation, treatment, disposal and remediation of hazardous substances and waste materials. In the ordinary course of business, we are subject to frequent environmental inspections and monitoring and occasional investigations by governmental enforcement authorities. In addition, our production facilities require operating permits that are subject to renewal, modification and, in certain circumstances, revocation. Actual or alleged violations of environmental laws or permit requirements could result in restrictions or prohibitions on plant operations, substantial civil or criminal sanctions, as well as, under some environmental laws, the assessment of strict liability and/or joint and several liability. Moreover, changes in environmental regulations could inhibit or interrupt our operations, or require us to modify our facilities or operations. Accordingly, environmental or regulatory matters may cause our Company to incur significant unanticipated losses, costs or liabilities.

In addition, we could incur significant expenditures in order to comply with existing or future environmental laws. Capital expenditures and costs relating to environmental or safety matters will be subject to evolving regulatory requirements and will depend on the timing of the promulgation and enforcement of specific standards which impose requirements on our operations. Therefore, we cannot assure you that capital expenditures and costs beyond those currently anticipated will not be required under existing or future environmental or safety laws. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Environmental Matters."

Furthermore, we may be liable for the costs of investigating and cleaning up environmental contamination on or from our properties or at off-site locations where we disposed of or arranged for the disposal or treatment of hazardous materials. Some of our manufacturing sites have an extended history of industrial chemical manufacturing and other uses, including on-site waste disposal. We cannot assure you that capital expenditures and costs beyond those currently anticipated will not be incurred to address all such known and unknown situations under existing and future environmental law. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Environmental Matters."

We handle and produce chemicals and other substances that may have adverse effects on human health or the environment.

Certain of our raw materials and finished products are highly regulated under environmental and industrial hygiene laws because of their potential toxicological impact on human health or the environment. Under such laws and other legal theories, individuals could seek payment of damages from us for alleged personal injury or property damage due to exposure to substances at our facilities or substances otherwise controlled by us. For example, a number of the substances used in our business are animal (Category II) carcinogens.

Environmental and industrial hygiene laws regulating hazardous substances are continually strengthened, and if a recharacterization of any of our products or raw materials occurs, the relevant material or product may be banned or we may incur substantial costs in order to comply with new requirements. Changes in these laws also may affect the marketability of our products. For instance,

21

such changes have been a key factor in the shift from solvent-based to solid-based products in our coating systems business.

Although we are not aware of any such current matters that we believe could be material to us, changes in these regulations, or claims related to exposure to potentially hazardous substances, could have a material adverse impact on us in the future.

As a global business, we are exposed to local business risks in several different countries which could harm our financial condition or results of operations.

We manufacture and distribute our products in many countries around the world, and one of our strategies is to expand outside our traditional European markets. We are, and may increasingly become, confronted with different political, social, legal and regulatory requirements in many jurisdictions which affect the cost of doing business. These include:

- •

- tariffs and trade barriers;

- •

- exchange controls;

- •

- requirements relating to withholding taxes on remittances and other payments by subsidiaries;

- •

- different regimes controlling the protection of our intellectual property;

- •

- restrictions on our ability to own or operate subsidiaries or acquire new businesses in these jurisdictions; and

- •

- restrictions on our ability to repatriate dividends from our subsidiaries.

Our international operations also expose us to different local political and business risks and challenges. For example:

- •

- we may be faced with political and social instability in countries in which we operate that could result in nationalization or seizure of our assets;

- •

- we are faced with potential difficulties in staffing and managing local operations; and

- •

- we have to design local solutions to manage credit risks of local customers and distributors.

Our expansion in emerging markets requires us to respond to rapid changes in market conditions in these countries. Our overall success as a global business depends, in part, upon our ability to succeed in differing economic, social and political conditions. We may not continue to succeed in developing and implementing policies and strategies that are effective in each location where we do business and failure to do so could harm our results of operations.

Several countries in which we operate have sophisticated tax regimes. As a result, changes in tax regulations, policy or enforcement in different countries could adversely affect our overall financial condition.

We depend on proprietary technologies and may be unable to adequately protect our intellectual property rights and may be subject to claims that we are infringing upon the rights of others.

Proprietary protection of our formulations, processes, apparatuses and other technology is important to our business. We rely upon unpatented proprietary expertise and continuing technological innovation and other trade secrets to develop and maintain our competitive position. Others may obtain knowledge of trade secrets through independent development or by other means.

To a lesser extent, we also rely on patents to protect our intellectual property. While a presumption of validity exists with respect to patents issued to us in the United States and other jurisdictions, there can be no assurance that any of our patents will not be challenged, invalidated,

22

circumvented or otherwise rendered unenforceable. The laws of many countries do not protect our intellectual property rights to the same extent as the laws of the United States. Furthermore, pending patent applications filed by us might not result in an issued patent. Even if patents are issued to us, they may not provide protection against competitors or against competitive technologies. The expiration of a patent can result in intense competition, particularly from generic producers, with consequent erosion of profit margins. The failure of our patents to protect our formulations, processes, apparatus, technology, trade secrets or proprietary know-how could hurt our business, financial condition and results of operations.

We have received communications asserting that certain of our products or their applications infringe on certain third-parties' proprietary rights. Such claims, with or without merit, could subject us to costly litigation and divert our technical and management personnel from their regular responsibilities. Furthermore, successful claims could cause us to suspend the manufacture of products using the contested inventions and could have a material adverse effect on our business, financial condition, operating results or cash flows.

Our products are often critical to our purchasers' products; therefore, we may be liable for damages arising from liability claims.

Many of our products, most notably those used in structural aerospace applications and those used in the electrical power generation and distribution equipment manufacturing industries, among others, provide attributes critical to the performance of our customers' products. Therefore, the sale of these products involves the risk of product liability claims if our products fail.