SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 20-F-A-2

| REGISTRATION STATEMENT PURSUANT TO SECTION 12(b) OR (g) OF THE SECURITIES EXCHANGE ACT OF 1934 |

OR

| ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 For the Fiscal Year Ended December 31, 2005 |

OR

| TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 [NO FEE REQUIRED] |

OR

| SHELL COMPANY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 [NO FEE REQUIRED] |

For the transition period from to

Commission file number – 0-50822

NORTHWESTERN MINERAL VENTURES INC.

(Exact name of Registrant as specified in its charter)

NORTHWESTERN MINERAL VENTURES INC.

(Translation of Registrant’s name into English)

Province of Ontario, Canada

(Jurisdiction of incorporation or organization)

36 Toronto Street

Suite 1000

Toronto, Ontario M5C 2C5

(Address of principal executive offices)

Securities registered or to be registered pursuant to Section 12(g) of the Act:

Common Shares

(Title of Class)

Securities for which there is a reporting obligation pursuant to Section 15(d) of the Act:

None

(Title of Class)

Indicate the number of outstanding shares of each of the issuer’s classes of capital or common shares as of the close of the period covered by the annual report.

80,226,090

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes ![]() . No

. No ![]() .

.

If this report is an annual or transition report, indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934. Yes ![]() . No

. No ![]() .

.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ![]() . No

. No ![]() .

.

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of ‘‘accelerated filer and large accelerated filer’’ in Rule 12b-2 of the Exchange Act. (Check one)

Large accelerated filer ![]() . Accelerated filer

. Accelerated filer ![]() . Non-accelerated filer

. Non-accelerated filer ![]() .

.

Indicate by check mark which financial statement item the Registrant has elected to follow. Item 17 ![]() . Item 18

. Item 18 ![]()

If this is an annual report, indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes. ![]() . No

. No ![]() .

.

All references herein are to Canadian dollars. Reference is made to ‘‘Item 3. Key Information.’’ for exchange rate information for the Canadian Dollar.

TABLE OF CONTENTS

i

ii

iii

PART I1

Item 1. Identity of Directors, Senior Management and Advisers.

Not Applicable.

Item 2. Offer Statistics and Expected Timetable.

Not applicable.

Item 3. Key Information.

All dollar amounts in this Annual Report are expressed in Canadian dollars. The following tables set forth the exchange rates for one Canadian dollar expressed in terms of one U.S. dollar for the years 2001-2005 and for the period December 31, 2005 through May 31, 2006.

| YEAR | AVERAGE | |||||

| 2001 | .6579 | |||||

| 2002 | .6776 | |||||

| 2003 | .7186 | |||||

| 2004 | .7702 | |||||

| 2005 | .8276 | |||||

| LOW | HIGH | |||||||||||

| May 2006 | .8903 | .9100 | ||||||||||

| April 2006 | .8534 | .8926 | ||||||||||

| March 2006 | .8531 | .8834 | ||||||||||

| February 2006 | .8638 | .8771 | ||||||||||

| January 2006 | .8528 | .8744 | ||||||||||

| December 2005 | .8521 | .8690 | ||||||||||

The exchange rates are based upon the noon buying rate in New York City for cable transfers in foreign currencies as certified for customs purposes by the Federal Reserve Bank of New York. At June 27, 2006, one Canadian dollar, as quoted by Reuters and other sources at 4 P.M. Eastern Time for New York foreign exchange selling rates (for bank transactions of at least $1,000,000), equaled $.8909 in U.S. dollars. (Source: The Wall Street Journal)

| A. | Selected Financial Data. |

Following is selected financial data of the Company, expressed in Canadian dollars, for the period from the Company’s incorporation on September 26, 2003 through December 31, 2005, the date of its audited consolidated financial statements, which were prepared in accordance with Canadian generally accepted accounting principles (‘‘Canadian GAAP’’), which differ substantially from United States generally accepted accounting principles (‘‘US GAAP’’). Reference is made to Note 15 to the audited consolidated financial statements for the period ended December 31, 2005, which is contained below in ‘‘Item 18. Financial Statements.’’ Note 15 provides a description of the differences between Canadian and United States generally accepted accounting principles, and how these differences could affect the Company’s financial statements. On July 27, 2004 the Company completed a 2 for 1 stock split, pursuant to which each issued Share of the Company was subdivided into two Shares. On September 6, 2005, the Company completed an additional 2 for 1 stock split, pursuant to which each issued Share of the Company was subdivided into two Shares. The outstanding warrants and stock options were also sub-divided at the same ratio as the common shares. Shares and per Share amounts in this Annual Report and in the Selected Financial Data have been retroactively adjusted to reflect the stock splits.

| 1 | The information contained in this Amendment is current as of the beginning of July 2006. |

1

CANADIAN GAAP

Can $

| Three Month Period ended March 31, 2006 (unaudited) $ | Three Month Period ended March 31, 2005 (unaudited) $ | Year Ended December 31, 2005 (audited) $ | Year Ended December 31, 2004 (audited) $ | Period from September 26, 2003 to December 31, 2003 (audited) $ | ||||||||||||||||||||||||||

| Revenues | — | — | — | — | — | |||||||||||||||||||||||||

| Loss for the Period | 280,119 | 135,479 | 1,780,074 | 1,121,460 | 33,097 | |||||||||||||||||||||||||

| Loss Per Share | 0.00 | 0.00 | 0.02 | 0.02 | 0.0 | |||||||||||||||||||||||||

| Cash Flows from Operating Activities | (257,791 | ) | (348,225 | ) | (851,997 | ) | (587,006 | ) | (23,097 | ) | ||||||||||||||||||||

| Cash Flows from Investing Activities | (692,828 | ) | (237,347 | ) | (707,330 | ) | (735,006 | ) | — | |||||||||||||||||||||

| Total Assets | 3,242,203 | 2,086,254 | 2,856,700 | 1,896,035 | 172,413 | |||||||||||||||||||||||||

| Current Assets | 1,366,352 | 1,114,825 | 1,774,293 | 1,161,660 | 172,413 | |||||||||||||||||||||||||

| Liabilities | 176,286 | 21,773 | 170,817 | 197,625 | 10,000 | |||||||||||||||||||||||||

| Share Capital | 6,280,667 | 3,354,517 | 5,620,514 | 2,852,967 | 195,510 | |||||||||||||||||||||||||

| Deficit | 3,214,750 | 1,290,036 | 2,934,631 | 1,154,557 | 33,097 | |||||||||||||||||||||||||

| Shareholders’ Equity | 3,065,917 | 2,064,481 | 2,685,883 | 1,698,410 | 162,413 | |||||||||||||||||||||||||

The following table sets forth how the Selected Financial Data presented above would be presented under US GAAP for the fiscal years ended December 31, 2005 and December 31, 2004, and the period from September 26, 2003 through December 31, 2003:

US GAAP

Can $

| Year ended December 31, 2005 (audited) $ | Year ended December 31, 2004 (audited) $ | Period from September 26, 2003 to December 31, 2003 (audited) $ | ||||||||||||||||

| Loss for the Period | 2,170,175 | 1,852,260 | 33,097 | |||||||||||||||

| Loss Per Share | 0.03 | 0.03 | 0.00 | |||||||||||||||

| Cash Flows from Operating Activities | (1,554,381 | ) | (1,317,806 | ) | (23,097 | ) | ||||||||||||

| Cash Flows From Investing Activities | (707,330 | ) | (735,006 | ) | — | |||||||||||||

| Total Assets | 1,780,999 | 1,165,235 | 172,413 | |||||||||||||||

| Deficit | 4,055,532 | 1,885,357 | 33,097 | |||||||||||||||

| B. | Capitalization and Indebtedness. |

Not applicable.

| C. | Reasons for the Offer and Use of Proceeds. |

Not applicable.

| D. | Risk Factors. |

2

RISK FACTORS AFFECTING THE COMPANY

The business of the Company entails significant risks, and an investment in the Shares should be considered highly speculative for a variety of reasons. An investment in the Shares should only be undertaken by persons who have sufficient financial resources to enable them to assume such risks. In addition to the usual risks associated with investment in a business, the following is a general description of significant risk factors, which should be considered.

We Have No Ongoing Mining Operations, None of our Mineral Properties Contain a Known Commercially Mineable Mineral Deposit, We Have Never Received Any Revenues From Mining Operations, and Our Chances of Reaching the Development Stage on Any of our Properties are Remote. Since our inception, we have never engaged in any mining operations and the Company has not generated any revenues from mining operations. Our activities have been limited to the highly speculative business of acquiring and exploring properties in the hope that commercial quantities of gold, uranium or other minerals, will be discovered. At the present time, none of our properties contain a known commercially mineable mineral deposit. We believe that the probability of our reaching the development stage on any of our properties is remote for a number of reasons. The exploration for and development of mineral deposits involves significant risks, which even a combination of careful evaluation, experience and knowledge may not eliminate. While the discovery of an ore body may result in substantial rewards, few properties, which are explored, are ultimately developed into producing mines. Major expenses may be required to locate and establish mineral reserves, to develop metallurgical processes and to construct mining and processing facilities at a particular site. Whether a mineral deposit will be commercially viable depends on a number of factors, including, but not limited to the following: the particular attributes of the deposit, such as size, grade and proximity to infrastructure; metal prices, which are highly cyclical; and government regulations, including regulations relating to prices, taxes, royalties, land tenure, land use, importing and exporting of minerals and environmental protection. Because so few properties which are explored ever become producing mines, investors must be prepared for the possibility that we will be unsuccessful and that they could lose their entire investment.

In the remote possibility that we place any of our properties into production, of which there can be no assurance, we would face numerous risks associated with mining operations. These risks include adverse environmental conditions, industrial accidents, labor disputes, unusual or unexpected geological conditions, ground or slope failures, cave-ins, changes in the regulatory environment and natural phenomena such as inclement weather conditions, floods and earthquakes, and the inability to maintain the infrastructure for our production activities. Mining and mining exploration is risky, presenting potentially dangerous conditions for workers. Large, heavy equipment and machinery is used and toxic substances are utilized and encountered in exploration, extraction, and processing. Misuse and accidents could result in serious injury and death to personnel. Such events could be caused by numerous factors including faulty equipment, unsafe practices, explosions, fires, natural phenomenon (such as lightning, mudslides, cave-ins, etc.), which may be impossible to avoid and protect against. In the event of any such misuse, accidents or natural disasters, personnel could be injured and killed, and mining operations suspended or terminated. In addition, any future development activities, of which there can be no assurance, would depend, to one degree or another, on adequate infrastructure. Reliable roads, bridges, power sources and water supply are important factors, which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could make it very difficult, if not impossible, to engage in any development activities and force us to incur expenses that we had not planned on spending.

We Will Need to Raise Substantial Funding in Order to Carry Out Our Activities. The Company has substantial financial obligations, including exploration funding requirements and purchase payment obligations, relating to its existing property interests. It will be necessary in the near and over the long term to raise substantial funds to maintain existing property interests, acquire, explore, and if warranted, develop mineral properties. In addition, in the event it is determined that any of our properties contain a commercially mineable mineral deposit, of which there can be no assurance, it is anticipated the Company would require substantial funds to place such property into production.

3

However, there can be no assurance we would be able to raise the necessary funds. Reference is made to ‘‘Item 4. Information on the Company. D. Property, Plants and Equipment’’ and Item 5. Operating and Financial Review and Prospects. F. Tabular Disclosure of Contractual Obligations’’ for a description of the Company’s financial commitments relating to its various property interests. In our audited consolidated financial statements for the year ended December 31, 2005, our auditors expressed substantial doubt as to our ability to continue as a going concern. In May 2006, the Company raised gross proceeds of approximately $17.9 million in a private offering of its securities. Although the funds raised in May 2006 will allow the Company to meet its existing financial obligations over the next 24 months, there is no assurance that in the future we will be able to raise the necessary funds on acceptable terms, or at all. If we do not raise these funds, investors could lose their investment. If we are able to raise these funds, it is likely that investors will experience dilution of their interests, which could result in a decrease in the value of their Shares.

Lack of Revenue Producing Operations. Since inception, the Company has not generated any revenues from mining operations. As of December 31, 2005, the Company had an accumulated deficit of $2,934,631. Accordingly, the Company’s business operations are subject to all of the risks inherent in companies without cash flow or earnings. The future earnings, if any, and cash flow, if any, from operations of the Company are dependent, in part, on its ability to locate properties containing commercially mineable mineral deposits, of which there can be no assurance.

We Could Lose our Interests in our Properties if Minimum Annual Work is Not Conducted. and Option Payments are not Made. In order to maintain our interests in all of our various properties, the Company is required to complete certain annual work commitments on each property and make certain option or purchase payments In the event such work is not completed or the required payments are not made, the Company could lose its interest in that property. Reference is made to ‘‘Item 4. Information on the Company. D. Property, Plants and Equipment.’’ for a description of the Company’s work and payment commitments on its various properties.

Title To Our Mining Properties Has Not Been Verified. Although the title to the properties in which the Company holds interests were reviewed by or on behalf of us, and title opinions were delivered to us, no assurances can be given that there are no title defects affecting such properties. Title insurance generally is not available for mining claims in Canada, and that our ability to ensure that it has obtained secure claim to individual mineral properties or mining concessions may be severely constrained. The Company has not conducted surveys of the claims in which it holds direct or indirect interests; therefore, the precise area and location of such claims may be in doubt. Accordingly, the properties may be subject to prior unregistered liens, agreements, transfers or claims, including native land claims, and title may be affected by, among other things, undetected defects. In addition, the Company may be unable to operate its properties as permitted or to enforce its rights with respect to its properties.

The Value of our Mineral Properties is Dependent Upon Commodity Prices Which Can Fluctuate Widely. The price of our Shares, our financial results and exploration, development and mining activities may in the future be significantly adversely affected by declines in the price of gold, copper, or other minerals. Gold, uranium, copper, and other mineral prices fluctuate, like many resource commodities, and are affected by numerous factors beyond the Company’s control such as the sale or purchase of such commodities by various central banks and financial institutions, interest rates, exchange rates, inflation or deflation, fluctuation in the value of the United States dollar and foreign currencies, global and regional supply and demand, and the political and economic conditions of major gold, uranium, copper or other mineral-producing countries throughout the world. Although the prices of gold, copper or other minerals have increased in recent years, and future price declines could cause continued development of and commercial production from the Company’s properties to be impracticable. Depending on the price of gold, copper, uranium or other minerals, cash flow from mining operations may not be sufficient and the Company could be forced to discontinue production and may lose its interest in, or may be forced to sell, some of its properties. Future production from the Company’s mining properties is dependent on gold and uranium or other mineral prices that are adequate to make these properties economic.

4

In addition to adversely affecting the Company’s reserve estimates and its financial condition, declining commodity prices can impact operations by requiring a reassessment of the feasibility of a particular project. Such a reassessment may be the result of a management decision or may be required under financing arrangements related to a particular project. Even if the project is ultimately determined to be economically viable, the need to conduct such a reassessment may cause substantial delays or may interrupt operations until the reassessment can be completed.

We Are Not Engaged in Mining Operations; In the Event We Engage in Mining Operations in the Future, We Would Face Substantial Regulation. We are not engaged in any mining operations at the present time and there can be no assurance we will ever engage in any mining operations in the future. All of our current activities are exploratory in nature.There can be no assurance, that we will discover any precious or base metals, establish the feasability of mining a deposit, or, if warranted, develop a property to production and maintain production activities, either alone or as a joint venture participant. Furthermore, there can be no assurance that we would be able to sell either the deposit or the Company on acceptable terms. Mining operations in Canada are subject to federal, provincial and local laws relating to the protection of the environment, including laws regulating the removal of natural resources from the ground and the discharge of materials into the environment. Mining operations are also subject to federal, provincial and local laws which seek to maintain health and safety standards by regulating the design and use of mining methods and equipment. Various permits from government bodies are required for mining operations to be conducted; no assurance can be given that such permits will be received. No assurance can be given that environmental standards imposed by federal, provincial or local authorities will not be changed with material adverse effect on the Company’s activities. Moreover, compliance with such laws may cause substantial delays and require capital outlays in excess of those anticipated, thus causing an adverse effect on the Company. Additionally, the Company may be subject to liability for pollution or other environmental damage which it may elect not to insure against due to prohibitive premium costs and other reasons.

Titles to the Mexican Properties in which the Company has an Interest are not Registered in the Name of the Company, Which may Result in Potential Title Disputes Having a Negative Impact on the Company. All of the agreements under which the Company may earn interests in properties have either been registered or been submitted for registration with the Mexican Public Registry of Mining, but title relating to the properties in which the Company may earn its interests are held in the names of parties other than the Company. Any of such properties may become the subject of an agreement which conflicts with the agreement pursuant to which the Company may earn its interest, in which case the Company may incur expenses in resolving any dispute relating to its interest in such property and such a dispute could result in the delay or indefinite postponement of further exploration and development of properties with the possible loss of such properties.

The Properties in Which the Company has Interests in Mexico are Subject to Changes in Governmental Laws, Regulations, Economic Conditions or Shifts in Political Attitudes or Stability in Mexico. The Company has property interests that are located in Mexico. Any changes in governmental laws, regulations, economic conditions or shifts in political attitudes or stability in Mexico are beyond the control of the Company and may adversely affect its business. Reference is made to ‘‘Item 4. Information on the Company – Business Overview – Regulation of Mining Industry – Mexico.’’

Mexican Foreign Investment and Income Tax Laws apply to the Company. Corporations in Mexico are taxed only by the Federal Government. Mexico has a general system for taxing corporate income, ensuring that all of a corporation’s earnings are taxed only once, in the fiscal year in which profits are obtained. There are two federal taxes in Mexico that apply to the Picachos Project; an asset tax and a corporate income tax. Corporations have to pay a federal tax on assets at 1.8% of the average value of assets less certain liabilities. Corporate income tax is credited against this tax. Mexican corporate taxes are calculated based on gross revenue deductions for all refining and smelting charges, direct operating costs, and all head office general and administrative costs; and depreciation deductions. The 2005 corporate tax rate in Mexico is 30%.

5

Foreign currency fluctuations and inflationary pressures may have a negative impact on the Company’s financial position and results. The Company’s property interests in Mexico make it subject to foreign currency fluctuations and inflationary pressures which may adversely affect the Company’s financial position and results. As the Company maintains its accounts in Canadian and US dollars, any appreciation in Mexican currency against the Canadian or US dollar will increase our costs of carrying out operations in Mexico. Further, any decrease in the US dollar against the Canadian dollar will result in a loss on our books to the extent we hold funds in US dollars. The steps taken by management to address foreign currency fluctuations may not eliminate all adverse effects and, accordingly, the Company may suffer losses due to adverse foreign currency fluctuations. The Company also bears the risk of incurring losses occasioned as a result of inflation in Mexico.

Regulation of Mining Operations in Mexico is Very Extensive. Regulatory requirements to which the Company is subject to in Mexico include certain permits that require periodic or annual renewal with governmental and regulatory authorities. In addition, the Company is required to comply with existing permit conditions. Although the Company believes that it is currently in full compliance with existing permit conditions, and although its permits have been renewed by governmental and regulatory authorities in the past, there are no assurances that the applicable governmental and regulatory authorities will renew the permits as they expire, or that pending or future permit applications will be granted, or that existing permits will not be revoked. In the event that the required permits are not granted or renewed in a timely manner, or in the event that governmental and regulatory authorities determine that the Company is not in compliance with its existing permits, the Company may be forced to suspend operations.

Risks related to the Company’s Foreign Investments and Operations. The Company conducts exploration activities in Canada, Mexico and Niger. The Company’s foreign mining investments are subject to the risks normally associated with the conduct of business in foreign countries. The occurrence of one or more of these risks could have a material and adverse effect on the Company’s earnings or the viability of its affected foreign operations, which could have a material and adverse effect on the Company’s future cash flows, results of operations and financial condition.

Risks may include, among others, labor disputes, invalidation of governmental orders and permits, corruption, uncertain political and economic environments, war, civil disturbances and terrorist actions, arbitrary changes in laws or policies of particular countries, foreign taxation, delays in obtaining or the inability to obtain necessary governmental permits, opposition to mining from environmental or other non-governmental organizations, limitations on foreign ownership, limitations on the repatriation of earnings, limitations on gold exports and increased financing costs. These risks may limit or disrupt the Company’s projects, restrict the movement of funds or result in the deprivation of contract rights or the taking of property by nationalization or expropriation without fair compensation.

There is a Risk that we will be Unable to Compete for Mineral Properties, Investment Funds and Technical Expertise. Significant and increasing competition exists for the limited number of gold, uranium, and other precious metal acquisition opportunities available in North, South and Central America and elsewhere in the world. As a result of this competition, some of which is with large, established mining companies with substantially greater financial and technical resources than us, we may be unable to acquire additional attractive precious metal mining properties on terms we consider acceptable. Moreover, this competition makes it more difficult for us to attract and retain mining experts, and to secure financing for our operations. Accordingly, there can be no assurance that our exploration and acquisition programs will be successful or result in any commercial mining operation.

We Do Not Have Insurance; We Will Not be Able to Insure Against All Possible Risks. The Company’s business is subject to a number of risks and hazards generally, including adverse environmental conditions, industrial accidents, labor disputes, unusual or unexpected geological conditions, ground or slope failures, cave-ins, changes in the regulatory environment and natural phenomena such as inclement weather conditions, floods and earthquakes. Such occurrences could result in damage to mineral properties or production facilities, personal injury or death, environmental damage to the Company’s properties or the properties of others, delays, monetary losses and possible

6

legal liability. Although the Company intends to obtain insurance to protect against certain risks in such amounts as it considers to be reasonable, it does not have any insurance at the present time. If and when insurance is obtained, of which there can be no assurance, the insurance will not cover all the potential risks associated with a mining company’s operations. Moreover, the Company may also be unable to maintain insurance to cover these risks at economically feasible premiums. Insurance coverage may not continue to be available or may not be adequate to cover any resulting liability. Moreover, insurance against risks such as environmental pollution or other hazards as a result of exploration and production is not generally available to the Company or to other companies in the mining industry on acceptable terms. The Company might also become subject to liability for pollution or other hazards which may not be insured against or which the Company may elect not to insure against because of premium costs or other reasons. Losses from these events may cause the Company to incur significant costs that could have a material adverse effect upon its financial performance and results of operations. Should a catastrophic event arise, investors could lose their entire investment.

If We are Unable to Maintain the Infrastructure for Our Exploration Activities, We Could be Adversely Affected. Our exploration activities depend, to one degree or another, on adequate infrastructure. Reliable roads, bridges, power sources and water supply are important factors which affect capital and operating costs. Unusual or infrequent weather phenomena, sabotage, government or other interference in the maintenance or provision of such infrastructure could adversely affect the Company’s exploration activities and its financial condition.

Management May Be Subject to Conflicts of Interest Due to Affiliations with Other Resource Companies. Because some of our directors and officers serve as officers and/or directors of other resource exploration companies which are themselves engaged in the search for additional opportunities, situations may arise where these persons are presented with, or identify, resource exploration opportunities that may be or perceived to be in competition with us for exploration opportunities. Since all of our officers and directors have a financial interest in other resource issuers to which they owe a fiduciary duty, it is likely our management may never be financially disinterested in such potential conflict of interest situations. It is likely that these other companies will be in competition with us for properties, funds, and personnel. Although it is anticipated that such potential conflicts will be dealt with in accordance with corporate and common law of the Province of Ontario, there can be no assurance any conflicts will be dealt with in a way that is best for the Company.

Although directors are required to declare and refrain from voting on any matter in which such directors may have a conflict of interest in accordance with the procedures set forth in the Business Corporations Act (Ontario) and other applicable laws, this could result in a situation where it will be difficult to have a totally disinterested board of directors deciding on a matter.

Our Management May Not Be Subject to U.S. Legal Process. The enforcement by investors of civil liabilities under the United States federal securities laws may be adversely affected by the fact that all of our officers and directors are neither citizens nor residents of the United States. There can be no assurance that (a) U.S. stockholders will be able to effect service of process within the United States upon such persons, (b) U.S. stockholders will be able to enforce, in United States courts, judgments against such persons obtained in such courts predicated upon the civil liability provisions of United States federal securities laws, (c) appropriate foreign courts would enforce judgments of United States courts obtained in actions against such persons predicated upon the civil liability provisions of the federal securities laws, and (d) the appropriate foreign courts would enforce, in original actions, liabilities against such persons predicated solely upon the United States federal securities laws.

Prices for Precious Metals such as Gold are Volatile and Could Decline. Historically, gold prices have fluctuated, so that there is no assurance, even if substantial quantities of gold are discovered, that we can make a profit. The prices of uranium, precious and base metals fluctuate on a daily basis and have experienced volatile and significant price movements over short periods of time. Prices are affected by numerous factors beyond our control, including international economic and political trends, expectations of inflation, currency exchange fluctuations (specifically, the U.S. dollar relative to

7

other currencies), interest rates, central bank transactions, world supply for precious and base metals, international investments, monetary systems, and global or regional consumption patterns (such as the development of gold coin programs), speculative activities and increased worldwide production due to improved mining and production methods. The effect of these factors cannot be accurately predicted, and the combination of these factors may result in us not receiving adequate returns on invested capital or the investments retaining their respective values. There is no assurance that the price of gold and of other precious and base metals will be high enough so that our properties, assuming that we ever discover substantial quantities of gold, could be mined at a profit.

Our Stock will be a Penny Stock which Imposes Significant Restrictions on Broker-Dealers Recommending the Stock For Purchase. The Securities and Exchange Commission (SEC) has adopted regulations that define ‘‘penny stock’’ to include common stock that has a market price of less than $5.00 per share, subject to certain exceptions. These rules include the following requirements: broker-dealers must deliver, prior to the transaction, a disclosure schedule prepared by the SEC relating to the penny stock market; broker-dealers must disclose the commissions payable to the broker-dealer and its registered representative; broker-dealers must disclose current quotations for the securities; if a broker-dealer is the sole market-maker, the broker-dealer must disclose this fact and the broker-dealer’s presumed control over the market; and a broker-dealer must furnish its customers with monthly statements disclosing recent price information for all penny stocks held in the customers’ account and information on the limited market in penny stocks. Additional sales practice requirements are imposed on broker-dealers who sell penny stocks to persons other than established customers and accredited investors. For these types of transactions, the broker-dealer must make a special suitability determination for the purchaser and must have received the purchaser’s written consent to the transaction prior to sale. If our Shares become subject to these penny stock rules these disclosure requirements may have the effect of reducing the level of trading activity in the secondary market for the Shares, if such trading market should ever develop, of which there can be no assurance. Accordingly, this may result in a lack of liquidity in the Shares and you may be unable to sell your Shares on terms you consider reasonable.

Our Stock Price Could be Volatile. The market price of our Shares, like that of the common shares of many other natural resource companies, has been and is likely to remain highly volatile. Results of exploration activities, the price of gold, copper, uranium, and other precious metals, period-to-period fluctuations in our operating results, changes in estimates of the Company’s performance by securities analysts, market conditions for shares of natural resource companies in general, and other factors beyond the control of the Company, could have a significant, adverse impact on the market price of the Shares.

We Do Not Plan to Pay Any Dividends in the Foreseeable Future. The Company has never paid a dividend and it is unlikely that the Company will declare or pay a dividend until warranted based upon the factors outlined below. The declaration, amount and date of distribution of any dividends in the future will be decided by the Board of Directors from time-to-time, based upon, and subject to, the Company’s earnings, financial requirements and other conditions prevailing at the time.

At June 30, 2006 the Company Had Only One Full-Time Consultant Acting in a Management Capacity. At June 30, 2006, the Company had two management consultants, each acting in their respective capacities as Chairman of the Board of Directors and President and CEO. Mr. Kabir Ahmed who acted as the Company’s Chairman and Mr. Marek Kreczmer acts as the Company’s President and CEO. Messrs. Ahmed and Kreczmer were the Company’s only full-time service providers. Mr. Ahmed resigned from all of his positions with the Company, including its Board of Directors on or about July 7, 2006. Mr. Errol Farr, our Chief Financial Officer, works for the Company on a part-time basis, devoting approximately ten to fifteen hours a month on the Company’s affairs. Upon the resignation of Mr. Ahmed, Mr. Kreczmer will be the Company’s only full-time service provider. The loss of Mr. Kreczmer, for any reason, or our inability to attract and retain additional highly skilled employees, may adversely affect our business and future operations. We do not carry key-man insurance on any members of our management

Future Sales of Common Shares by Existing Shareholders. Sales of a large number of our Shares in the public markets, or the potential for such sales, could decrease the trading price of the Shares

8

and could impair the Company’s ability to raise capital through future sales of Shares. The Company has previously issued Shares at an effective price per share which is lower than the effective price of the Shares in the Company’s public offering of its Shares completed in February 2004. Accordingly, certain shareholders of the Company have an investment profit in the Shares that they may seek to liquidate.

Item 4. Information on the Company.

| A. | History and Development of the Company. |

The Company was incorporated under the laws of the Province of Ontario, Canada on September 26, 2003.

The principal business office of the Company is located at 36 Toronto Street, Suite 1000, Toronto, Ontario M5C 2C5 Canada. Its telephone number is (416) 367-6875. The Company does not have an agent in the United States.

Its registered and records office is located at 200 King Street West, Suite 2300, Toronto, Ontario M5H 3W5 Canada. Its telephone number is (416) 595-2300.

| B. | Business Overview*. |

| • | See Glossary on pages 39-42 for terms used throughout this Annual Report. |

Forward-Looking Statements

Safe Harbor Statement under the United States Private Securities Litigation Reform Act of 1995: Except for the statements of historical fact contained herein, the information presented constitutes ‘‘forward-looking statements’’ within the meaning of the Private Securities Litigation Reform Act of 1995. Often, but not always, forward-looking statements can be identified by the use of words such as ‘‘plans’’, ‘‘expects’’, ‘‘budget’’, ‘‘scheduled’’, ‘‘estimates’’, ‘‘forecasts’’, ‘‘intends’’, ‘‘anticipates’’, ‘‘believes’’, or variation of such words and phrases that refer to certain actions, events or results to be taken, occur or achieved. Forward-looking statements involve known and unknown risks, uncertainties and other factors which may cause the actual results, performance or achievements of the Company to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, among others, the actual results of exploration activities, the estimation or realization of mineral reserves and resources, capital expenditures, costs and timing of the development of new deposits, requirements for additional capital, future prices of gold, possible variations in ore grade or recovery rates, failure of plant, equipment or processes to operate as anticipated, accidents, labor disputes and other risks of the mining industry, delays in obtaining governmental approvals, permits or financing or in the completion of development or construction activities, currency fluctuations, title disputes or claims limitations on insurance coverage and the timing and possible outcome of pending litigation, as well as those factors discussed under Item 3 in the section entitled ‘‘Risk Factors’’. Although the Company has attempted to identify important factors that could cause actual actions, events or results to differ materially from those described in forward-looking statements, there may be other factors that cause actions, events or results not to be as anticipated, estimated or intended. There can be no assurance that such statements will prove to be accurate as actual results and future events could differ materially from those anticipated in such statements. Accordingly, readers should not place undue reliance on forward-looking statements.

General

The Company was founded on September 26, 2003 to explore for precious and base metals and uranium. The Company is currently focused on properties with potential gold and silver deposits, and uranium. The Company is an exploration stage company and is not engaged in any mining operations, and there can be no assurance it will ever engage in mining operations. To date, its only mining interests are (i) an option to acquire a 100% interest in properties in Mexico’s Durango state (the

9

‘‘Picachos Project’’), (ii) the acquisition in March 2006 of the right to explore two uranium properties in the Republic of Niger, Africa, (iii) an option to acquire up to a 65% interest in the North Rae Uranium Project, Northern Quebec, Canada, (iv) an option to acquire a 75% interest in the Waterbury Project, which consists of nine uranium claims in the Athabasca Basin, Saskatchewan, Canada, and (v) a Letter of Intent dated June 9, 2006 granting it the right to conduct due diligence and to potentially enter into an option agreement to acquire the Saguenay Uranium Property, located in Charlevoix County, Quebec. In December 2005 the Company acquired an option to acquire a 100% interest of the Firefly Project, in the La Sal uranium district in southeastern Utah, but in June 2006 decided to let the option lapse. In addition, during the year ended December 31, 2005 the Company dropped its option to acquire a 50% interest in the Bear Project, Longtom Property, located in the Northwest Territories, Canada because it wanted to concentrate more of its resources on the Picachos Project, which it believed had more potential. The Company had spent approximately $600,000 on the Bear Project. Reference is made to ‘‘Item 4. Information on the Company. D. Property, Plants and Equipment.’’ for a detailed description of the Company’s mining interests.

There can be no assurance that a commercially mineable mineral deposit exists on any of these properties.

On May 11, 2006 Mr. Marek Kreczmer, the Company’s President, assumed the position of Chief Executive Officer. Mr. Kabir Ahmed, formerly the Chief Executive Officer, was appointed Chairman of the Company’s Board of Directors. On May 25, 2006, Mr. Wayne Beach, Jon North, and J. Scott Waldie resigned from the Board of Directors and were replaced by Anton Esterhuizen, Simon Lawrence, and Joseph D. Horne. On or about July 7, 2006 Mr. Kabir Ahmed intends to resign from the Company’s Board of Directors. Reference is made to ‘‘Item 6. Directors, Senior Management and Employees.’’

Description of Mining Industry

Our business is highly speculative. We are exploring for base and precious metals and other mineral resources. Ore is rock containing particles of a particular mineral (and possibly other minerals which can be recovered and sold), which rock can be legally extracted, and then processed to recover the minerals which can be sold at a profit. Although mineral exploration is a time consuming and expensive process with no assurance of success, the process is straight forward. First, we acquire the rights to enable us to explore for, and if warranted, extract and remove ore so that it can be refined and sold on the open market to dealers. Second, we explore for precious and base metals by examining the soil, rocks on the surface, and by drilling into the ground to retrieve underground rock samples, which can then be analyzed. This work is undertaken in staged programs, with each successive stage built upon the information gained in prior stages. If exploration programs discover what appears to be an area which may be able to be profitably mined, we will focus our activities on determining whether that is feasible, while at the same time continuing the exploratory activities to further delineate the location and size of this potential ore body. Things that will be analyzed by us in making a determination of whether we have a deposit which can be feasibly mined at a profit include:

| 1. | The amount of mineralization which has been established, and the likelihood of increasing the size of the mineralized deposit through additional drilling; |

| 2. | The expected mining dilution; |

| 3. | The expected recovery rates in processing; |

| 4. | The cost of mining the deposit; |

| 5. | The cost of processing the ore to separate the gold or uranium from the host rocks, including refining the precious or base metals; |

| 6. | The costs to construct, maintain, and operate mining and processing activities; |

| 7. | Other costs associated with operations including permit and reclamation costs upon cessation of operations; |

| 8. | The costs of capital; |

10

| 9. | The costs involved in acquiring and maintaining the property; and |

| 10. | The price of the precious or base minerals. For example, the price of one ounce of gold for the years 2001-2005 ranged from a low of $271 U.S. in 2001, to a high of $536.50 U.S. in 2005. At June 28, 2006, the price of gold was $582.75 U.S. per ounce2 .. The price of one pound of uranium for the years 2001-2005 ranged from a low of $7.25 U.S. in 2001, to a high of $36.25 U.S. in 2005. At June 26, 2006, the price of uranium was $45.50 U.S. per pound. |

Our analysis will rely upon the estimates the plans of geologists mining engineers, metallurgists and others.

If we determine that we have a feasible mining project, we will consider pursuing alternative courses of action, including:

| • | seeking to sell the deposit or the Company to third parties; |

| • | entering into a joint venture with larger mining company to mine the deposit; or |

| • | placing the property into production ourselves. |

There can be no assurance, that we will discover any precious or base metals, establish the feasability of mining a deposit, or, if warranted, develop a property to production and maintain production activities, either alone or as a joint venture participant. Furthermore, there can be no assurance that we would be able to sell either the deposit or the Company on acceptable terms, or at all, enter into such a joint venture on acceptable terms, or be able to place a property into production ourselves. If we do enter actual mining operations, which is unlikely in the near future, our operations will be subject to various factors and risks generally affecting the mining industry, many of which are beyond our control. These include the price of precious or base metals declining, the possibility that a change in laws respecting the environment could make operations unfeasible, or our ability to conduct mining operations could be adversely affected by government regulation. Reference is made to ‘‘Item. 3. Key Information. D. Risk Factors.’’

Regulation of Mining Industry

Canada

Although each province of Canada has its own regulations for the mining industry, generally the following is true. Prior to commencing any exploration activities in Canada, and depending on the provincial jurisdiction, the Company or the party intending to carry out a work program on a mineral property may be required to apply to the appropriate local government agencies for a number of permits or licenses related to mineral exploration activities. These permits or licenses may include water and surface use permits, occupation permits, fire permits, and timber permits. Prior to being issued the various permits or licenses, the applicant may have to file a detailed work plan with the applicable government agency. Permits are issued on the basis of the work plan submitted and approved by the governing agency. Additional work on a given mineral property or a significant change in the nature of the work to be completed would require an amendment to the original permit or license.

As part of the permit or licensing requirements, the applicant is required to post an environmental reclamation bond in respect to the work to be carried out on the mineral property. The amount of such bond is determined by the amount and nature of the work proposed by the applicant. The amount of a bond may also be increased with increased levels of development on the property.

The Company has or will make application to the appropriate agencies for permits and licenses relating to those properties upon which the Company intends to carry out work during the 2006 exploration season. For those mineral properties in which the Company has an interest but is not the operator of the work programs, application for the required permits and licenses and the posting of the reclamation bonds will be made by the party entitled to carry out exploration work on the property. The Company believes that it is currently in compliance with all applicable environmental laws and regulations in Canada.

| 2 | Based upon the Average Spot Price of Gold, London PM fix. |

11

Mexico

The exploration and exploitation of minerals in Mexico may be carried out by Mexican citizens or Mexican companies incorporated under Mexican law by means of obtaining exploration and exploitation concessions. Exploration concessions are granted by the Mexican federal government for a period of six years from the date of their recording in the Public Registry of Mining and are not renewable. Holders of exploration concessions may, prior to the expiration of such exploration concessions, apply for one or more exploitation concessions covering all or part of the area covered by one exploration concession. Failure to apply prior to the expiration of the term of the exploration concession will result in termination of the concession. An exploitation concession has a term of 50 years, generally renewable for a further 50 years upon application within five years prior to the expiration of such concession. Both exploration and exploitation concessions are subject to annual work requirements and payment of surface taxes which are assessed and levied on a semiannual basis. Such concessions may be transferred or assigned by their holders, but such transfers or assignments must comply with the requirements established by the Mexican Mining Law and be registered before the Public Registry of Mining in order to be valid against third parties.

Mineral exploration and exploitation concessions may also be obtained by foreign citizens or foreign corporations, in this latter case, through the establishment of a branch or subsidiary in Mexico, and in the case of foreign citizens, provided that they comply with certain requirements set forth in the Foreign Investment Law. Foreign citizens are required to apply for the corresponding authorization before the Ministry of Foreign Affairs and register their investment in the National Registry of Foreign Investment. In the case of a branch of foreign corporations, in addition to registration in the National Registry of Foreign Investment, additional authorization from the Ministry of Economy is required in order to obtain subsequent registration in the corresponding local Public Registry of Commerce.

Mexican mining law does not require payment of finder’s fees or royalties to the Government, except for a discovery premium in connection with national mineral reserves, concessions in marine zones and claims or allotments contracted directly from the Council of Mineral Resources. None of the property interests held by the Company are under such fee regime. However, holders of exploration and exploitation concessions are required to pay surface taxes which are assessed and levied on a semi-annual basis.

Republic of Niger

There are four types of licenses available for companies and individuals interested in exploration and development of mineral resources. A Prospecting Authorization gives the holder the right to search for one or a number of minerals. It is non-exclusive and confers to the holder any rights to an exclusive exploration permit within the limits and time validity of the Authorization.

Prospecting Authorizations are valid for one year, renewable indefinitely for one year periods. Only surface prospecting is permitted, including remote sensing techniques. The objective of the prospecting program must be stated in the application, although there are no fee or land holding requirements.

An Exploration Permit is valid for three-years, renewable for two further three-year periods subject to certain land holding reduction criteria and field works. The area held under a permit cannot exceed 2,000 km² in a rectangular block.

An Exploration Permit confers to the holder the right to dispose of any minerals obtained during exploration and test work, and also confers the right to a Mining Permit if a viable reserve is discovered. Applications must stipulate the minerals sought (additional minerals can be included later), and a time and expenditure schedule. A variable fee (CFA F 300.000) is tied to the permit, and holders are required to submit progress reports to the Government on their activities.

A Mining Permit will be granted in the case of successful exploration, subject to the right of the Government to participate in the project. A ‘small mine’ permit is valid for five years, renewable 3 times for five-year periods, while a ‘large mine’ permit lasts for 20 years initially, renewable 2 times per period of 10 years. Further extensions are possible if commercial reserves remain.

12

Companies applying for Mining Permits must conform to Nigerien Company law. The Government requires an initial 10% share in the mining project, free of all costs, which can be later increased to a maximum of 30 % through share purchases. Fees for mining permits are around $1,400 and $2,000 for small and large mining permits respectively.

The fourth type of license is the Authorization for Small-Scale Mining, and it concerns artisanal level of production.

The Government of Niger has stated that it welcomes overseas private investment as a key to relaunching its national economy, and its mining code contains a number of incentives for potential investors. These include income tax holidays and many exemptions (customs duty exemption, exemption in some cases from value-added tax, the right to remit dividends freely) equal opportunities for overseas and national investors, and guaranteed freedom from nationalization or expropriation.

Mining companies are subject to a number of fees and taxes:

Annual area fees are related to the licenses except to the prospecting authorization.

Mining royalties are payable at a rate of 5.5% of the final selling price of the mineral commodity produced. Royalties are, however, deductible from income tax, which is levied at a rate of 35% after the deduction of operating and production costs. Small mines enjoy a two-year income tax holiday, while for large mines this period extends to five years from the start of commercial production. Dividends distributed to share holders attract a 16% capital gains tax. Other charges include stamp duty, public notary fees, value added tax and social security contributions for employees.

Customs duties are not charged on equipment imported for use for direct mining operations, or temporarily for exploration programs. Mineral products may be exported free of duty.

Niger uses the CFA francs, which is tied to the Euros and is fully convertible (1 Euro = 656 Fcfa). Foreign exchange regulations are very liberal, although with the requirement that overseas transactions must be authorized by the Ministry of Finance and made through a registered bank.

| C. | Organizational Structure. |

The Company has one inactive U.S. subsidiary.

| D. | Property, Plants and Equipment. |

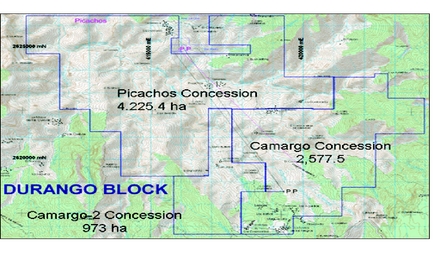

| A. | Picachos Project, Durango State, Mexico |

In July 2004, the Company entered into an option agreement with RNC Gold Inc. (‘‘RNC’’) to acquire a 50% interest in two silver-gold properties in Mexico’s Durango and Sinaloa provinces (the ‘‘Picachos Project’’). Subsequently, in October 2005, the Company amended its option agreement to acquire the remaining 50% interest in the Picachos Project. The Picachos property portfolio originally included the 7,700-hectare (19,000-acre) silver-gold Picachos property area in Durango State and the 17,800-hectare (43,900-acre) Tango gold claims in Sinaloa State. In 2005 the Company decided to focus its exploration on the 7,700 hectare silver-gold Picachos Property, so on November 17, 2005 the Company dropped its interest in the Tango gold claims in Sinaloa State.

In order to earn its initial 50% interest in the Picachos Project, the Company must expend $1,500,000 in exploration expenditures on or before December 31, 2006. To March 31, 2006, the Company has spent approximately $786,000 in exploration expenditures on the project and is expected to spend approximately $1 million during the balance of the year. Also, as part of the Picachos Option Agreement, the Company must by July 2007 generate a feasibility study for the production of a minimum of 25,000 ounces of gold per year (‘‘Feasibility Study’’).

Subsequently, in October 2005, the Company amended its agreement with RNC to acquire an option to acquire a 100% interest in the Picachos Project. After the Company earns a 50% interest in the project, the Company will be granted the right to acquire RNC’s remaining 50% stake in the Picachos Project. The purchase price for acquiring the remaining 50% interest would be $20,000,000, payable as follows:

13

| 1. | $3,000,000 at the time the Feasibility Study is completed; |

| 2. | $9,000,000 at the Commencement of Commercial Production |

| 3. | $2,000,000 on each of the first through fourth anniversaries of the Commencement of Commercial Production. |

In addition, the Company issued RNC 200,000 Shares. To retain its acquisition rights, the Company must keep the claims comprising the Picachos Project in good standing by undertaking minimum work commitments of approximately $50,000 annually.

Kabir Ahmed, currently the Chairman of the Company’s Board of Directors, was a director of RNC at the time the original option agreement was entered into in 2004, but he has resigned his position as a director of RNC during 2005, prior to the October 2005 amendment to the option agreement.

The properties comprising the Picachos Project do not contain a known commercially mineable mineral deposit and the Company’s proposed exploration programs are exploratory in nature.

14

Property Description, Location and Access

The following information regarding the Picachos Project’s location, access, history, planned exploration activities, and related topics are summarized from a report titled ‘‘A Technical Review of the Picachos Silver-Gold Prospects, Western Durango State, Mexico for Northwestern Mineral Ventures Inc.,’’ prepared by Watts, Griffis and McOuat Limited (‘‘WGM’’), Consulting Geologists and Engineers, and dated November 24, 2004 (the ‘‘WGM Report’’). There is no known commercially mineable mineral deposit on any of the properties comprising the Picachos Project.

The Picachos area is located in the western portion of Durango State, 100 kilometers west-southwest of the state capital, Durango. It is situated within the Zona Minera La Ventana of the Sierra Madre Occidental Mountains. The exploration concessions or licenses are owned by Minera Tango S.A. de CV. (‘‘Tango’’), a Mexican corporation, which is 75% owned by RNC Gold Inc. (‘‘RNC’’), and 25% owned by Minera Camargo S.A. de C.V. (‘‘Camargo’’), a Mexican company. Prior to Tango acquiring the licenses, Camargo acquired the licenses based on the presence of a large number of old native silver-gold mine workings and a favorable geological setting. Most of the mine workings were enlarged as a result of the interest of the early Spanish settlers.

The Los Cochis prospect portion of the property is located just below the village of La Mesa de Los Negros, about 5 kilometers from the main regional highway between Durango and Mazatlan, the capital of neighboring Sinaloa State. It is on the south central part of the ‘‘Camargo’’ concession, part of a larger land package in the southeastern quadrant of a caldera complex in the Western Sierra Madre.

According to the WGM Report, the Picachos concession (4,225.4 hectares) was registered with SECOFI (the Mexican Mining Recorder) July 12, 1999 by Camargo. Camargo is a private Mexican corporation, owned 80% by Michelle Robinson, MASc, P.Eng., and 20% by Jose Vargas Gaytan, a Mexican prospector. The legal survey was completed and filed September 6, 1999. The legal survey for the Camargo concession (2,577.5 hectares) was filed with SECOFI on May 16, 2002. Legal title was recorded for both claims on July 9, 2002.

15

Temperatures are subject to seasonal variations, which are largely dependent on elevation. Above 2,000 meters, the climate is drier and temperatures range from over 30°C in summer to below freezing at night in the winter with some snowfall. Below 2,000 meters, the climate gradually becomes more hot and humid, with temperatures ranging from 10°C in winter to 38°C in summer. Irrespective of season, nightfall can bring substantial drops in temperature. The rainy season is from July to October.

According to the WGM Report, there is a ready supply of labor in the immediate area of the prospects. People living in the Picachos area are mainly farmers, cattle ranchers, and fruit growers. A 230 KV electrical transmission line runs parallel to Highway 40. Neveros is connected to the power grid via a branch line. The village of La Mesa de Los Negros has grid electricity and a telephone.

The Picachos Property covers small past silver and gold producers and several significant silver/gold showings that remain to be fully explored. Camargo and Tango have carried out a significant amount of ground work, including geochemical sampling and two drill holes.

Based on its comparisons with other mines and mineral deposits in the Sierra Madre, including the Tayoltita Mine located a short distance to the north, the WGM Report concluded that the Picachos area has the potential to host an economically significant silver-gold deposit. In addition, the silver-gold values found on the property demonstrate a potential for bulk tonnage scale mineralization. However, there is no known commercially mineable mineral deposit on any of the properties comprising the Picachos Project and the Company’s proposed exploration programs are exploratory in nature.

Summary of 2004 Minimum Work Exploration Program and Budget

In 2004, the Company completed a limited work program of trenching, soil sampling and geochemistry analysis on both of its silver-gold properties in Mexico. The limited work program, which was completed in December 2004, was required as part of the Company’s minimum work commitments to keep all of the claims in good standing. The Company expended approximately $50,000 towards the limited work program.

Summary of First Phase 2005 Exploration Program

In 2004, the geological and engineering firm of Watts, Griffis and McOuat Limited (‘‘WGM’’), proposed a first phase exploration program costing $526,000 for the Company. This first phase exploration program consisted of additional land acquisition; the acquisition and study of remote sensing imagery; a fixed-wing airborne magnetometer survey; hand trenching, soil geochemical surveying and sampling at three of the most prospective targets for gold (El Toro, Los Cochis and Guadalupe targets); and preparations for underground development and diamond drilling at a fourth site, the El Pino target.

The Company’s first phase exploration program was completed during the third quarter of 2005, at a cost of $620,980. The Company completed all aspects of the WGM first phase exploration program — but has postponed the airborne survey and preparations for underground development at El Pino, which will be carried out in the Company’s second phase exploration program, which is expected to cost $1.0 million.

The results of the first phase exploration program have been generally positive. Results are available for 7,056 samples from Los Cochis, El Toro and Guadalupe. The highest gold values to date were returned from the El Toro samples, which define a strong polymetallic geochemical anomaly. Several of these samples contained in excess of 500 ppb gold, and values of 2,424 ppb gold occurred in soils near the previous mine workings. This discovery at El Toro is in addition to the large Los Cochis anomaly, which returned the highest silver values to date and has already been identified by the Company as a compelling drill target.

Summary of Proposed Second Phase 2005-2006 Exploration Program

The Company is expected to prepare a second phase exploration program, costing $1.0 million, which is expected to be completed by December 30, 2006. The second phase exploration program will

16

be designed to further develop the Los Cochis, El Toro and Guadalupe targets; airborne survey of the Picachos properties; and underground development of the El Pino target. The Company intends to fully fund the second phase exploration program from its existing working capital. In order to retain its option interest in the Picachos Project, the Company must expend an additional $1.0 million in exploration by December 30, 2006.

Management of Picachos Project

Michelle Robinson, MASc, P.Eng., a professional engineer, is the person responsible for overseeing and carrying out the Company’s exploration programs on the Picachos Project in Mexico.

| B. | Uranium Concession, Niger, Africa |

On March 8, 2006 the Company completed the acquisition of two uranium concessions in Niger, Africa. These concessions, the In Gall Concession and the Irhazer Concession, cover a total 4,000 square kilometers (988,000 acres) and were selected for their favorable geology, exploration potential and strategic location — situated in the same stratigraphy as two operating uranium mines which together yield almost 10% of worldwide production, according to the International Atomic Energy Agency, a division of the United Nations. The Company’s objective in applying for the uranium concessions in the Republic of Niger is to minimize its exploration risk by attempting to diversify the Company’s property portfolio.

The Company was required to file a formal concession application for with the Ministry of Mines & Energy, Niger. The work commitments have been negotiated with the Director of Mines and the application was thereafter referred to the Minister of Mines & Energy for review. After its approval by the Minister of Mines & Energy the application was then forwarded to the Ministers Council for formal approval.

The concessions were granted to the Company for a period of thirty years. Under the terms of the concessions, the Company is required to spend a total of $4.4 million U.S. on exploration of the concessions over the next three years, as set forth below:

| YEAR | AMOUNT FOR EACH PROPERTY | TOTAL FOR YEAR | ||||||||||

| Year 1 | $ | 200,000 US | $ | 400,000 US | ||||||||

| Year 2 | $ | 600,000 US | $ | 1,200,000 US | ||||||||

| Year 3 | $ | 1,400,000 US | $ | 2,800,000 US | ||||||||

The Company’s concessions provide it with the right to dispose of any minerals obtained during exploration and test work, and also confers on the Company the right to a mining permit, if a viable reserve is discovered.

The Government of Niger is automatically granted an initial ten (10%) percent non-participating interest in the project. In addition, the Government of Niger can subscribe to a maximum twenty (20%) percent interest of the operating company to be formed to develop the properties. In the event the Government of Niger does not subscribe for its 20% interest at the time of incorporation, it will lose its right to subscribe for such interest.

A Mining Convention signed on March 8, 2006 by the Company and the Government of Niger guarantees for thirty years the stability of administrative, judicial, fiscal, customs, financial, economic and social conditions during the duration of the Convention , covering both exploration and exploitation activities.

The Company had prepared a ‘‘Technical Evaluation Report 43-101, Northwestern Mineral Ventures Inc., Uranium Properties, Niger, West Africa,’’ dated March 9, 2006, prepared by Claude Jobin, P.Eng. M.Sc., and El Hamet Mai Ousmane, Ph.D. (‘‘Irhazer and In Gall Technical Report’’).

Property Description

The Irhazer and In Gall concessions are located in the Agades area, department of Techirozrine, Niger. Each concession consists of approximately two thousand (2,000) square kilometers. The rainy

17

season is from June to September with annual rainfall averaging 93 millimeters in Agades. The temperature ranges from 15 degrees Centigrade to 40 degrees centigrade.

Access to Properties

The properties may be accessed from the capital, Niamey, by paved road up to In Gall village and from there by four wheel drive vehicles. In addition, a flight may be taken from Niamey to Arlit, from where the properties can be accessed by four wheel drive vehicles.

Work Program and Budget for the First Three-Year Period

The Irhazer and In Gall Technical Report has recommended a three-year exploration program for the two concessions, costing each a total of $2,200,000 U.S., which the Company intends to follow. According to the Irhazer and In Gall Technical Report, the work program and budget is the same for both properties. The proposed exploration programs are as follows:

The first work program will include an airborne high sensitivity magnetic/gamma ray survey of 5,000 kilometers, along lines 200 meters apart, with a ground follow up of the anomalies.

| FIRST YEAR EXPENSES | $US | |||||

| Contribution to technical training | $ | 20,000 | ||||

| Wages of expatriate personnel | 15,000 | |||||

| Wages of local personnel | 30,000 | |||||

| Airborne Survey 5,000 km x $14 | 70,000 | |||||

| Vehicle | 15,000 | |||||

| Equipment | 10,000 | |||||

| Office, field camp | 10,000 | |||||

| Travel, communication | 10,000 | |||||

| Consumables, fuel | 10,000 | |||||

| Miscellaneous | 10,000 | |||||

| TOTAL: | $ | 200,000 | ||||

The second year work program will include 6000 meters of reverse circulation drilling at an average depth of 400 meters; samples will be assayed for uranium and multi elements.

| SECOND YEAR EXPENSES | $US | |||||

| Contribution to technical training | $ | 20,000 | ||||

| Wages of expatriate personnel | 40,000 | |||||

| Wages of local personnel | 30,000 | |||||

| Reverse circulation drilling 6,000 m x $50 | 300,000 | |||||

| Down hole radiometric 6,000 x $10 | 60,000 | |||||

| Chemical assays 6,500 x $8 | 52,000 | |||||

| Vehicle | 15,000 | |||||

| Equipment | 15,000 | |||||

| Office, field camp | 15,000 | |||||

| Travel and communications | 15,000 | |||||

| Consumables, fuel | 15,000 | |||||

| Miscellaneous | 23,000 | |||||

| TOTAL: | $ | 600,000 | ||||

18

The third year program could include 15,500 meters of drilling if encouraging results were obtained from the previous year

| THIRD YEAR EXPENSES | $US | |||||

| Contributions to technical training | $ | 20,000 | ||||

| Wages of expatriate personnel | 70,000 | |||||

| Wages of local personnel | 75,000 | |||||

| Reverse circulation drilling 15,500 m x $50 | 775,000 | |||||

| Down hole radiometric 15,500 m x $10 | 155,000 | |||||

| Chemical assays 16,500 x $8 | 132,000 | |||||

| Equipment | 25,000 | |||||

| Office, field camp | 40,000 | |||||

| Travel and communications | 30,000 | |||||

| Consumables, fuel | 25,000 | |||||

| Miscellaneous | 53,000 | |||||

| TOTAL: | $ | 1,400,000 | ||||

The Company intends to pay for the exploration programs from its working capital.

The Company’s President and CEO, Marek Kreczmer, will be supervising the exploration activities through an exploration team composed of Nigerien geologists and expatriate technical professionals.

History

There is no history of exploration on the Irhazer or In Gall concessions. Uranium was first discovered in Niger in 1957. Since that time there have been a number of uranium discoveries, with two open pit mines and one underground mine established. The established mines are located approximately 150 kilometers from the Company’s concessions. However, there can be no assurance that there is a commercially mineable deposit of uranium on any of the Company’s properties. The Company’s activities will be exploratory in nature.

There is no known commercially mineable mineral deposit on either the Irhazer or In Gall concessions.

| C. | Waterbury Uranium Project, Saskatchewan, Canada |

Pursuant to an agreement dated November 9, 2005 with Canalaska Ventures Ltd. (‘‘Canalaska’’), the Company acquired an option to acquire up to a 75% interest in the Waterbury Uranium Project, Saskatchewan, Canada (‘‘Waterbury Project’’). The Waterbury Project covers 12,417 hectares and includes nine prospective uranium claims located in the Althabasca Basin, Saskatchewan, Canada.

To acquire the 75% interest in the Waterbury Project, the Company would first acquire a 50% interest, with options to acquire additional 10% and 15% interests.

To acquire the initial 50% interest, the Company is required to (i) make cash payments to Canalaska of $150,000, by April 1, 2008, (ii) issue Canalaska a total of 300,000 Shares by April 1, 2007, (iii) incur $2,000,000 of exploration expenditures by April 1, 2008, and (iv) grant Canalaska a 3% net smelter royalty (‘‘NSR’’) on any production, if any, from the Waterbury Project, as set forth below.

19

The Company is required to pay Canalaska $150,000 as follows:

| On or prior to the earlier of December 9, 2005 and the date the agreement was signed | $25,000 | ||

| On or prior to April 1, 2006 | $25,000 | ||

| On or prior to April 1, 2007 | $50,000 | ||

| On or prior to April 1, 2008 | $50,000 | ||

The Company is required to issue Canalaska 300,000 Shares, as follows:

| On or prior to the earlier of December 9, 2005 and the date the agreement is signed | 100,000 Shares | ||

| On or prior to April 1, 2006 | 100,000 Shares | ||

| On or prior to April 1, 2007 | 100,000 Shares | ||

In addition, the Company is required to incur a total of $2,000,000 in exploration expenditures on the Waterbury Project as follows:

| On or prior to April 1, 2006 | $500,000 | ||

| On or prior to April 1, 2007 | $750,000 | ||

| On or prior to April 1, 2008 | $750,000 | ||

Upon the Company satisfying the above requirements, it will have acquired a 50% interest in the Waterbury Project.

As of June 28, 2006 the Company has made all requirements payments and share issuances to Canalaska.

To acquire an additional 10% interest in the Waterbury Project (60% interest in total), the Company will be required to incur an additional $2,000,000 in exploration expenditures within two years of acquiring the 50% interest, with a minimum expenditure of $500,000 in each year.

To acquire an additional 15% interest (75% interest in total), the Company will be required to (i) complete a feasibility study on the Waterbury Project within two years of acquiring the 60% interest (‘‘Development Stage’’), (ii) issue Canalaska 200,000 Shares, (iii) and incur a minimum of $500,000 in annual exploration expenditures for two years. The Company may extend the Development Stage for two years by paying Canalaska a fee of $250,000 in advance for each year of extension.

Upon the Company acquiring its 50% interest in the Waterbury Project, the Company and Canalaska will be deemed to have formed a joint venture, with Canalaska acting as the operator of the joint venture. If the Company increases its interest to 60%, it will be become the operator of the Waterbury Project at that time. After the formation of the joint venture, the party’s obligations to financially contribute to the joint venture will be based upon their respective ownership interests. If any party’s interest in the joint venture falls below 10%, then that party’s interest will revert to a 3% NSR, which in the case of Canalaska, would be in addition to its existing 3% NSR, for a total NSR of 6%.

Location and Access

The Waterbury Project is located in the eastern portion of the Athabasca Basin in Saskatchewan, Canada. The nine mineral claims are located seven miles (12 kilometers) east of the Cigar Lake Deposit and six miles (10 kilometers) south of the Midwest Mine.

Private roads maintained by major uranium producers traverse the property area and provide access to the property, as do numerous drill roads. Daily air service and a provincial highway also serve the area.

20

Climate