QuickLinks -- Click here to rapidly navigate through this documentAs filed with the Securities and Exchange Commission on May 25, 2004.

Registration No. 333- •

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM F-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

INMARSAT FINANCE PLC

(Exact name of co-registrant as

specified in their charters) |

England and Wales

(State or other jurisdiction of

incorporation or organization) |

|

4899

(Primary Standard Industrial

Classification Code Number) |

|

98–0425688

(I.R.S. Employer

Identification Number) |

SEE TABLE OF ADDITIONAL REGISTRANTS BELOW |

Inmarsat Group Limited

99 City Road, London EC1Y 1AX, United Kingdom; +44 (0)20 7728 1000

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

CT Corporation Systems

111 Eighth Avenue, 13th Floor, New York, NY 10011 +1 212 894 8600

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copy to:

John W. Connolly III

Clifford Chance Limited Liability Partnership

10 Upper Bank Street, London E14 5JJ, United Kingdom; +44 (0)20 7006 1000

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this Registration Statement.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

THE CO-REGISTRANTS HEREBY AMEND THIS REGISTRATION STATEMENT ON SUCH DATE OR DATES AS MAY BE NECESSARY TO DELAY ITS EFFECTIVE DATE UNTIL THE CO-REGISTRANTS SHALL FILE A FURTHER AMENDMENT WHICH SPECIFICALLY STATES THAT THIS REGISTRATION STATEMENT SHALL THEREAFTER BECOME EFFECTIVE IN ACCORDANCE WITH SECTION 8(A) OF THE SECURITIES ACT OR UNTIL THE REGISTRATION STATEMENT SHALL BECOME EFFECTIVE ON SUCH DATE AS THE SECURITIES AND EXCHANGE COMMISSION, ACTING PURSUANT TO SAID SECTION 8(A), MAY DETERMINE.

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of

Securities to be Registered

| | Amount to

be Registered

| | Proposed Maximum

Offering Price

Per Share

| | Proposed Maximum

Aggregate

Offering Price(2)

| | Amount of

Registration Fee

|

|---|

|

| 75/8% Senior Notes due 2012 | | $477,500,000 | | 100% | | $477,500,000 | | $60,499.25 |

| Guarantees of 75/8% Senior Notes due 2012(1) | | — | | — | | — | | —(3) |

|

- (1)

- The issuers of the guarantees are listed below in the Table of Additional Registrants.

- (2)

- Estimated solely for the purpose of calculating the registration fee pursuant to Rule 457(f) under the Securities Act of 1933.

- (3)

- In accordance with Rule 457(n) of the Securities Act, no separate fee for the registration of the guarantees is required.

TABLE OF ADDITIONAL REGISTRANTS

Exact Name of Additional Registrant

as Specified in Its Charter

| | State or Other Jurisdiction of

Incorporation or Organization

| | I.R.S. Emoployer

Identification Number

|

|---|

| Inmarsat Group Limited | | England and Wales | | 98–0425689 |

| Inmarsat Investments Limited | | England and Wales | | 98–0425691 |

| Inmarsat Ventures Limited | | England and Wales | | 98–0425692 |

| Inmarsat Limited | | England and Wales | | 98–0425693 |

| Inmarsat Leasing (Two) Limited | | England and Wales | | 98–0425694 |

| Inmarsat Launch Company Limited | | Isle of Man | | 98–0425695 |

- (1)

- The address and telephone number for each of the additional registrants, other than Inmarsat Launch Company Limited, is 99 City Road, London EC1Y 1AX, United Kingdom, +44 (0)20 7728 1000. The address and telephone number for Inmarsat Launch Company Limited is 15–19 Athol Street, Douglas, Isle of Man, IM1 1LB, +44(0)16 2463 8300.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

PROSPECTUS

SUBJECT TO COMPLETION. DATED MAY 25, 2004.

Inmarsat Finance plc

a public limited company incorporated under the laws of England and Wales and a direct subsidiary of

Inmarsat Group Limited, the parent guarantor of the notes and the indirect parent company of

Exchange Offer for

75/8% Senior Notes due 2012

This is an offer by Inmarsat Finance plc to exchange any 75/8% Senior Notes due 2012 that you now hold, for newly issued 75/8% Senior Notes due 2012. This offer will expire at 5:00 p.m. New York City time on , , unless we extend the offer. You must tender your existing notes by this deadline in order to receive the new notes. If we decide to extend the offer, we do not currently intend to extend the expiration period beyond .

We may redeem some or all of the new notes at any time at our option on the terms set forth in this prospectus. We will be required to redeem a portion of each of the new notes upon the occurrence of specified events and on the terms described in this prospectus.

See "Risk Factors" beginning on page 16 for a description of the business and financial risks associated with the new notes.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , .

TABLE OF CONTENTS

| | Page

|

|---|

| FORWARD-LOOKING STATEMENTS | | ii |

PRESENTATION OF FINANCIAL INFORMATION AND CERTAIN OTHER DATA |

|

iv |

PROSPECTUS SUMMARY |

|

1 |

RISK FACTORS |

|

16 |

CAPITALIZATION |

|

34 |

UNAUDITED PRO FORMA COMBINED FINANCIAL DATA |

|

35 |

EXCHANGE RATES |

|

45 |

SELECTED HISTORICAL CONSOLIDATED FINANCIAL DATA |

|

46 |

OPERATING AND FINANCIAL REVIEW AND PROSPECTS |

|

51 |

THE MOBILE SATELLITE COMMUNICATIONS SERVICES INDUSTRY |

|

74 |

BUSINESS |

|

76 |

REGULATION |

|

98 |

DIRECTORS, SENIOR MANAGEMENT AND EMPLOYEES |

|

108 |

PRINCIPAL SHAREHOLDERS |

|

116 |

MATERIAL CONTRACTS |

|

122 |

DESCRIPTION OF CERTAIN FINANCING ARRANGEMENTS |

|

137 |

CERTAIN RELATIONSHIPS AND RELATED PARTY TRANSACTIONS |

|

153 |

DESCRIPTION OF THE NOTES |

|

154 |

THE EXCHANGE OFFER |

|

217 |

TAX CONSIDERATIONS |

|

227 |

ERISA AND OTHER CONSIDERATIONS |

|

234 |

PLAN OF DISTRIBUTION |

|

236 |

ENFORCEMENT OF JUDGMENTS |

|

237 |

LEGAL MATTERS |

|

240 |

EXPERTS |

|

240 |

WHERE YOU CAN FIND MORE INFORMATION |

|

240 |

LISTING INFORMATION |

|

242 |

INDEX TO FINANCIAL STATEMENTS |

|

F-1 |

We refer to the 75/8% Senior Notes due 2012 in this prospectus as the notes. Unless we indicate differently, when we use the terms "notes" and "new notes," in this prospectus, we mean the new notes that we intend to issue to you if you exchange your existing notes.

i

FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements. These forward-looking statements include all matters that are not historical facts. Statements containing the words "believe," "expect," "intend," "plan," "may," "estimate" or, in each case, their negative and words of similar meaning are forward-looking.

By their nature, forward-looking statements involve risks and uncertainties because they relate to events and depend on circumstances that may or may not occur in the future. We caution you that forward-looking statements are not guarantees of future performance and that our actual financial condition, results of operations and cash flows, and the development of the industry in which we operate, may differ materially from those made in or suggested by the forward-looking statements contained in this prospectus. In addition, even if our financial condition, results of operations and cash flows, and the development of the industry in which we operate, are consistent with the forward-looking statements contained in this prospectus, those results or developments may not be indicative of results or developments in subsequent periods. Important facts that could cause our actual results of operations, financial condition or cash flows, or development of the industry in which we operate, to differ from our current expectations include, but are not limited to:

- •

- our reliance on third-party distributors to market and sell our services effectively;

- •

- our dependence on five master distributors, who generate a significant portion of our revenues;

- •

- our possible inability to offset declining revenues from voice services with revenues from data services;

- •

- significant competition from other operators;

- •

- our possible inability to retain orbital positions or sufficient rights to the L-band spectrum required to operate our satellite system to its expected capacity;

- •

- applications by our competitors to use L-band spectrum for terrestrial services leading to interference with our services;

- •

- factors beyond our control with respect to the manufacture and supply of user terminals by third parties;

- •

- possible operational failures of the Thuraya satellite, which could adversely affect our ability to deliver Regional BGAN services;

- •

- possible restrictions on our access to the U.S. market in the future pursuant to the U.S. ORBIT Act;

- •

- our possible inability to recruit and retain the necessary management or employees;

- •

- the significant operational risks relating to our satellite network;

- •

- the significant risks related to the timely manufacture and launch of our Inmarsat-4 satellites;

- •

- our possible inability to obtain launch and in-orbit insurance to cover our satellites;

- •

- the possibility that new technologies could render our technologies obsolete;

- •

- the possible adverse impact of increasing regulation relating to the transmission of our satellite signals and the provision of our services in certain countries;

- •

- the possible adverse impact of additional governmental regulation;

- •

- our possible inability to protect our intellectual property; and

ii

- •

- the possible adverse impact of our substantial leverage and ability to meet significant debt service obligations.

As a consequence, our current plans, anticipated actions and future financial condition, results of operations and cash flows, as well as the anticipated development of the industry in which we operate, may differ from those expressed in any forward-looking statements made by us or on our behalf. We urge you to read this prospectus, including the sections entitled "Risk Factors," "Operating and Financial Review and Prospects" and "Business" for a more complete discussion of the factors that could affect our future performance and the industry in which we operate. These factors and this cautionary statement expressly qualify all forward-looking statements.

Following this exchange offer, we will be subject to the reporting requirements of the Securities Exchange Act of 1934, or the Exchange Act, as amended, and will be required to make periodic reports to the SEC about us and our business which will be publicly available. In addition, we are subject to the ongoing reporting requirements of the Luxembourg Stock Exchange. Apart from any requirements pursuant to these laws and rules, we have no obligation to update publicly or revise any forward-looking statements in this prospectus, whether as a result of new information, future events or otherwise. You are cautioned not to rely unduly on forward-looking statements when evaluating the information presented in this prospectus.

iii

PRESENTATION OF FINANCIAL INFORMATION AND CERTAIN OTHER DATA

Financial Data

Unless otherwise indicated, all historical consolidated and pro forma combined financial information included herein has been prepared in accordance with UK GAAP, with a reconcilliation to U.S. GAAP of certain key financial data. UK GAAP differs in certain significant respects from U.S. GAAP. For a discussion of the principal differences between UK GAAP and U.S. GAAP as they apply to us, see Note 32 to the consolidated financial statements of Inmarsat Group Limited, Note 32 to the consolidated financial statements of Inmarsat Investments Limited, Note 31 to the consolidated financial statements of Inmarsat Ventures Limited, Note 29 to the financial statements of Inmarsat Limited, Note 18 to the financial statements of Inmarsat Leasing (Two) Limited, Note 7 to the financial statements of Inmarsat Launch Company Limited, Note 7 to the financial statements of Inmarsat Finance plc and Note 3 to the Unaudited Pro Forma Combined Financial Data, in each case included elsewhere in this prospectus.

Some of the financial information in this prospectus has been rounded and, as a result, the totals of the data presented in this prospectus may vary slightly from the actual arithmetic totals of such information.

Non-GAAP Financial Measures

EBITDA from continuing operations

EBITDA from continuing operations and the related ratios presented in this prospectus are supplemental measures of our performance and liquidity that are not required by, or presented in accordance with, UK GAAP or U.S. GAAP. Furthermore, EBITDA from continuing operations is not a measurement of our financial performance or liquidity under UK GAAP or U.S. GAAP and should not be considered as an alternative to net income, operating income or any other performance measures derived in accordance with UK GAAP or U.S. GAAP or as an alternative to cash flow from operating activities as a measure of our liquidity.

We believe EBITDA from continuing operations facilitates operating performance comparisons from period to period and company to company by eliminating potential differences caused by variations in capital structures (affecting interest expense), tax positions (such as the impact on periods or companies of changes in effective tax rates or net operating losses) and the age and book depreciation of tangible assets (affecting relative depreciation expense). We also present EBITDA from continuing operations because we believe it is frequently used by securities analysts, investors and other interested parties in evaluating similar issuers, the vast majority of which present EBITDA from continuing operations when reporting their results. Finally, we present EBITDA from continuing operations as a supplemental measure of our ability to service our debt.

Nevertheless, EBITDA from continuing operations has limitations as an analytical tool, and you should not consider it in isolation from, or as a substitute for analysis of, our results of operations, as reported under UK GAAP or U.S. GAAP. Some of these limitations are:

- •

- it does not reflect our cash expenditures or future requirements for capital expenditures or contractual commitments;

- •

- it does not reflect changes in, or cash requirements for, our working capital needs;

- •

- it does not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt;

iv

- •

- although depreciation and amortization are non-cash charges, the assets being depreciated and amortized will often have to be replaced in the future, and EBITDA measures do not reflect any cash requirements for such replacements;

- •

- it is not adjusted for all non-cash income or expense items that are reflected in our statements of cash flows; and

- •

- other companies in our industry may calculate this measure differently than we do, limiting its usefulness as a comparative measure.

Because of these limitations, EBITDA from continuing operations should not be considered as a measure of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our UK GAAP results and using EBITDA measures only supplementally. See "Unaudited Pro Forma Combined Financial Data" and "Operating and Financial Review and Prospects" and the consolidated financial statements of our predecessor contained elsewhere in this prospectus.

Aggregated 2003 Financial Information

On December 17, 2003 Inmarsat Investments Limited's offer to acquire all of the shares of Inmarsat Ventures Limited became unconditional and we account for the acquisition of Inmarsat Ventures Limited from that date. Inmarsat Ventures Limited and its consolidated subsidiaries prior to the acquisition are referred to as the "predecessor." Inmarsat Group Limited and its consolidated subsidiaries, from and after the acquisition of Inmarsat Ventures Limited, are referred to as the "successor."

Our results for the year ended December 31, 2003 are presented in this prospectus on an aggregated basis. Aggregated data is derived by adding amounts for our predecessor for the period from January 1, 2003 to (and including) December 17, 2003 and for the successor for the period from (but excluding) December 17, 2003 to December 31, 2003. We have aggregated the information to provide investors with 2003 data for a full year period. However, data for the successor period includes the effect of purchase accounting related to the acquisition and therefore is not directly comparable with predecessor data for prior periods. You should note that aggregated data is a non-GAAP financial measure.

Unless otherwise stated in this prospectus, all references to our results for the year ended December 31, 2003 refer to the aggregated data for 2003 discussed above.

Trademarks

The names "Inmarsat," "BGAN" and "Swift64," as well as the Inmarsat logo and Fleet logo, are our principal trademarks. Other significant trademarks include the name "Universal Calling" and its devices.

"Inmarsat" is owned by the International Maritime Satellite Organization and licensed to Inmarsat Limited and Inmarsat Ventures Limited pursuant to a perpetual, irrevocable license. All other trademarks listed above are owned by Inmarsat (IP) Company Limited, a subsidiary of Inmarsat Ventures Limited. All of those trademarks are either registered or registration is pending in our key markets.

CNN is an end user of our services. "CNN" is owned by Cable News Network LP, a Time Warner Company. All rights reserved.

v

PROSPECTUS SUMMARY

This summary highlights selected information about the exchange offer and us. It does not contain all the information that may be important to you. You should read the entire prospectus, including the financial information and the related Notes and the risks of investing in the notes under the "Risk Factors" section, before making an investment decision. Unless indicated herein or the context indicates otherwise, the information contained in this prospectus gives effect to the transactions described under "Unaudited Pro Forma Combined Financial Data."

In this prospectus, references to "we," "us" and "our" are to Inmarsat Group Limited, its subsidiaries (including Inmarsat Finance plc) and its predecessor (Inmarsat Ventures Limited), except that on the cover page, references to "we," "us" and "our" refer only to Inmarsat Group Limited. References to the "Issuer" are to Inmarsat Finance plc, the issuer of the notes. References to the "parent guarantor" are to Inmarsat Group Limited.

Our Business

We are a leading provider of global mobile satellite communications services. We have been designing, implementing and operating satellite networks for over 23 years. From our fleet of nine geostationary satellites, we provide a wide range of voice and data services, including telephony, fax, video, email and intranet and internet access. End users of our services operate at sea, on land and in the air, and include enterprise-level users, such as Maersk (one of the world's largest shipping firms), Shell, CNN, BBC, British Airways, governments and governmental agencies including the UK Ministry of Defence, and international aid organizations such as the International Red Cross. Our business is characterized by steady revenues and cash flows and, during each of the ten years ended December 31, 2003, our EBITDA exceeded $250 million. Our revenues and EBITDA from continuing operations for the year ended December 31, 2003 were $504.5 million and $336.6 million (66.7% of our revenues), respectively.

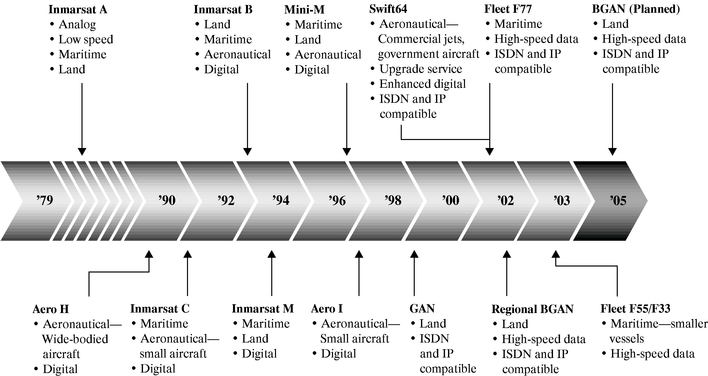

We own and operate all of our satellites. We have a successful launch and operating record, and have never experienced a satellite failure at launch or in orbit. Our current fleet of satellites includes four Inmarsat-2 satellites, which were launched in the early 1990s, and five Inmarsat-3 satellites, which were launched between 1996 and 1998. We currently anticipate that our Inmarsat-2 and Inmarsat-3 satellites will remain in commercial operation beyond their design lives, until between 2007-2011 and 2010-2014, respectively. We currently intend to launch two next-generation Inmarsat-4 satellites during the second half of 2004 and in 2005. The Inmarsat-4 satellites will extend the commercial life of our satellite fleet to beyond 2017, and will serve as the platform for the introduction of next-generation higher-bandwidth services, such as broadband global area network, or BGAN, which will offer more sophisticated and significantly faster communication to end users.

We provide our mobile satellite services to the maritime, land and aeronautical sectors. During the year ended December 31, 2003, the maritime, land and aeronautical sectors of our business accounted for 48.7%, 32.4% and 2.6% of our revenues, respectively. Our services are available at transmission rates of up to 64 kilobits per second and, through our recently-introduced Regional BGAN service, of up to 144 kilobits per second. The launch of our Inmarsat-4 satellites and the introduction of our BGAN services will allow us to offer a more sophisticated range of high-bandwidth services, including internet access, videoconferencing, local area network, or LAN, access and other services, all at speeds of up to 432 kilobits per second.

We also lease excess capacity on our satellites. During the year ended December 31, 2003, approximately 12.1% of our total revenues was attributable to leases, typically to governmental entities, including the U.S. Navy.

1

We sell our mobile satellite communications services to distributors, who then provide services to end users, either directly or indirectly through other distributors or service providers. Our 26 master distributors are affiliated with some of the largest incumbent communications companies in the world, and include affiliates of Telenor, KPN, Telstra and France Telecom. As at December 31, 2003, a global network of approximately 400 distributors and service providers, including our 26 master distributors, distributed our mobile satellite communications services to end users in approximately 170 countries on six continents.

Key Strengths

We believe we have the following key strengths:

- •

- Established market leader with strong market positions. We are a leading provider of mobile satellite communications services, with particularly strong positions in the maritime and data sectors of the market. In the maritime sector, we believe we are the leading provider of global mobile satellite services, with 2002 revenues in excess of 30 times those of our nearest competitor. Our market-leading position in the maritime sector is underpinned by our role as the sole provider of satellite services required for the operation of the Global Maritime Distress and Safety System, or GMDSS, and by maritime sector regulations that require all cargo vessels over 300 gross tons and all passenger vessels, irrespective of size, which travel in international waters to carry distress and safety terminals that use our services. We believe we are also the market leader in the provision of high-speed data services to the maritime and land sectors, with 2002 data revenues of more than 15 times those of our nearest competitor. To our knowledge, our global mobile satellite data services, which are currently offered at transmission rates of up to 64 kilobits per second and, with respect to Regional BGAN, up to 144 kilobits per second, are the only such global mobile satellite services offered by any provider at transmission rates in excess of 10 kilobits per second.

- •

- Established infrastructure and distribution network. We own and operate a fleet of nine geostationary satellites, using L-band spectrum to provide a comprehensive range of voice and data services with a global reach (excluding the extreme polar regions). We also have access to or own land earth stations in 31 locations. This infrastructure enables us to offer global mobile satellite services at data transmission rates well in excess of our competitors. We believe that no competitor is likely to introduce global mobile satellite services at data transmission rates comparable to ours in the short- to medium-term in light of the limited availability of suitable spectrum and the cost and lead-time required to replicate our in-orbit and terrestrial infrastructure. In addition, we believe establishing a distribution network comparable to ours would require significant lead-time. It is possible, however, that a regional competitor could introduce comparable services in the medium-term.

- •

- Established base of enterprise-level users. As at December 31, 2003, over 295,000 Inmarsat terminals were registered to access our services, of which approximately 59.8% had been active during the previous twelve months. Multiple end users access many of these terminals (for example, those installed on ships and airplanes). We believe this relatively large installed base of terminals contributes to stable revenues, particularly in the maritime market, because the cost and time required to switch to a competing system could be substantial. We also believe our established base of enterprise-level users leaves us well-placed to capture increasing demand for high-speed mobile data communications.

- •

- High and stable EBITDA margins. Historically, we have benefited from a large and established base of enterprise-level users with stable communications needs, particularly in the maritime sector. This installed base has helped us to generate stable EBITDA. In each of the past ten years, we have generated EBITDA of over $250 million and, in each financial year since we

2

became a private company in 1999, our EBITDA margins (EBITDA as a percentage of revenues) have exceeded 63%. Our annual maintenance and other capital expenditures (excluding costs associated with our Inmarsat-4 program and next-generation services) ranged from $13.1 million to $40.5 million between 2000 to 2003.

- •

- Service reliability and technical excellence. We have over 23 years of experience in designing, implementing and operating global mobile satellite communications networks and have a track record of quality and reliability. We have not experienced a satellite failure during the 84 satellite years in aggregate that our satellite fleet has operated. In addition, during each of the three years ended December 31, 2003, our satellite network was available more than 99.99% of the time. We believe that our reliability is particularly attractive to enterprise-level users who require mission critical communications support to operate their businesses. We also enjoy a reputation for technical innovation. We have pioneered a series of innovations in satellite communications services, in particular by making higher-speed data transmission services available to smaller and lighter mobile terminals, and have optimized the use of our spectrum with advanced digital signal processing technologies. Our Regional BGAN service (which we launched in 2002), represents the next step in our development of higher-bandwidth services and enhances our competitive position in relation to data services.

Our Strategy

Strategy

Our goal is to continue to be a leading provider of global mobile satellite communications services by increasing our penetration of our core voice and data services markets, introducing new services and entering new end user markets. We plan to achieve our goal by:

- •

- Continuing to focus on core maritime and land sectors. Our goal is to retain and increase sales to existing enterprise-level users in the maritime and land sectors. We will continue to leverage our leading position in the maritime sector by cooperating with our master distributors to encourage existing enterprise-level users to take up additional services. For example, we work with our distributors to design programs that incentivize merchant and passenger shipping enterprise-level users to install pay phones and other terminals on ships, increasing access for crew and/or passengers to email, instant messaging, the internet and corporate intranets. In the land sector, our high-speed global area network, or GAN, service, offers a seamless extension to corporate networks for email, internet access, remote office connectivity and document transfer. Enhancing end user access to our services increases our traffic and revenues.

- •

- Focusing on high-bandwidth data services. We intend to continue to focus on high-bandwidth data services, where growth in demand in our primary market sectors is expected to exceed growth in demand for voice services. In 1999, we introduced a higher-speed GAN service compatible with Integrated Services Digital Network, or ISDN, and Internet Protocol, or IP, standards. Media, aid organizations and military in Iraq and Afghanistan have used this service extensively. We also recently introduced a Regional BGAN service targeted at land-based users, and offering data transmission at rates of up to 144 kilobits per second. Our next-generation BGAN product (when introduced), will offer a more sophisticated range of high-bandwidth solutions, including internet access, videoconferencing, LAN access and all our other services at data transmission rates of up to 432 kilobits per second (which compares favorably with 384 kilobits per second transmission rates typically offered by terrestrial third-generation wireless services). Our higher-bandwidth mobile data services are compatible with terrestrial communications services, including third-generation wireless services.

- •

- Launching our next-generation Inmarsat-4 satellites. We currently intend to launch two Inmarsat-4 satellites during the second half of 2004 and in 2005. We have also commissioned a third

3

Inmarsat-4 satellite to hold as a ground spare. When launched, the Inmarsat-4 satellites, which individually will be approximately 60 times more powerful than an Inmarsat-3 satellite, will extend the commercial life of our satellite fleet, increase our capacity and enable us to deliver higher-bandwidth services offering sophisticated and significantly faster communication to end users. Our Inmarsat-4 satellites and next-generation services, which we will offer via laptop computer-sized terminals, should help us to remain at the forefront of technological developments within our industry.

- •

- Continuing our conservative management approach. Our goal is to manage the risks associated with our business. During 2002, we generated substantially all of our revenues using four of our five Inmarsat-3 satellites. Our fifth Inmarsat-3 satellite and, to a lesser extent our Inmarsat-2 satellites, provide redundant in-orbit capacity to cover potential satellite anomalies and allow us to generate revenues by leasing spare capacity. As part of our conservative approach to risk management, we have procured a third Inmarsat-4 satellite to serve as a ground spare. In addition, we currently maintain in-orbit insurance on our Inmarsat-3 satellites (excluding the first loss), which will remain in place until the successful launch of an Inmarsat-4 satellite. We also intend to obtain launch and in-orbit insurance for our Inmarsat-4 satellites.

- •

- Focus on de-leveraging. One of our key priorities will be to reduce our debt levels. To do so, upon completion of our Inmarsat-4 program, we will focus on reducing debt with available cash flows. Following completion of our Inmarsat-4 program, we expect our cash available for debt service to increase significantly as our capital expenditure should then be limited to maintenance capital expenditure.

The Acquisition and Financing

Acquisition

Effective as of December 17, 2003, Inmarsat Investments Limited, a company formed by funds advised by Apax Partners and funds advised by Permira, acquired all of the issued and outstanding share capital of Inmarsat Ventures Limited. The transaction, or the acquisition, was completed by way of a scheme of arrangement under the UK Companies Act 1985.

Under the scheme of arrangement, Inmarsat Investments Limited paid a purchase price of approximately $1.5 billion to the shareholders of Inmarsat Ventures Limited. Certain existing shareholders including Telenor, COMSAT and KDDI, or "rollover shareholders," chose to reinvest in the continuing business, and now own in aggregate approximately 42.6% of the outstanding share capital of Inmarsat Group Holdings Limited, the ultimate parent company of Inmarsat Investments Limited and Inmarsat Group Limited. In addition, certain members of our management (including our chairman) own 4.0% of the outstanding share capital of Inmarsat Group Holdings Limited in connection with the acquisition. Funds advised by Apax Partners and funds advised by Permira collectively own the remaining 51.7% of the outstanding share capital of Inmarsat Group Holdings Limited.

You should read the section titled "Principal Shareholders" for more detailed information regarding our shareholders following the acquisition.

Financing of the Acquisition

The purchase price for the acquisition, as well as related fees and expenses, were financed with a combination of funding provided by funds advised by Apax Partners and funds advised by Permira, the rollover shareholders and certain members of our management, and with external debt financing.

4

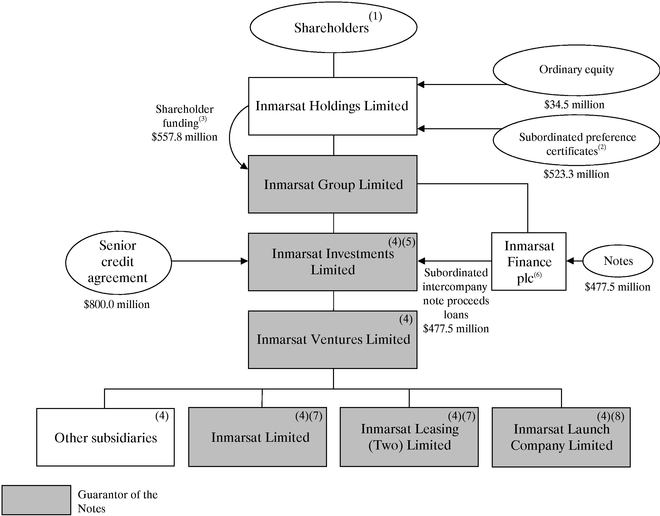

Shareholder Funding

Funds advised by Apax Partners and funds advised by Permira, the rollover shareholders and certain members of our management contributed $653.3 million of the acquisition purchase price in the form of ordinary equity ($34.5 million) and subordinated preference certificates ($618.8 million) at the Inmarsat Group Holdings Limited and Inmarsat Holdings Limited levels, respectively. The proceeds of the subordinated preference certificates were loaned by Inmarsat Holdings Limited to Inmarsat Group Limited, pursuant to the subordinated intercompany shareholder funding loan. A portion ($95.5 million) of that funding was repaid (together with interest) with the proceeds of the additional notes discussed below.

External Debt Financing

In addition to the shareholder funding described above, Inmarsat Group Holdings Limited, Inmarsat Investments Limited and certain subsidiaries of Inmarsat Investments Limited, entered into a senior credit agreement with Barclays Capital (the investment banking division of Barclays Bank PLC), Credit Suisse First Boston and The Royal Bank of Scotland plc, as mandated lead arrangers. At the closing of the acquisition, Inmarsat Investments Limited borrowed an aggregate of $800 million of term loans under the senior credit agreement. In addition, the senior credit agreement provides for a $100 million capital expenditure facility and a $75 million working capital facility. As at the date of this prospectus, no amounts had been drawn under either the capital expenditure facility or the working capital facility.

Also in connection with the acquisition, Inmarsat Investments Limited and Credit Suisse First Boston, Barclays Capital (the investment banking division of Barclays Bank PLC) and The Royal Bank of Scotland entered into a subordinated loan agreement, or the bridge loan, pursuant to which Inmarsat Investments Limited borrowed $365 million. The bridge loan was repaid in full with the proceeds of the offering of the January 2004 notes discussed below.

Issuance of the January 2004 Notes and the Additional Notes

As of the date hereof, Inmarsat Finance plc has issued a total of $477,500,000 75/8% senior notes in two tranches:

- •

- On February 3, 2004, Inmarsat Finance plc issued $375,000,000 75/8% senior notes, which we refer to as the January 2004 notes. We used the gross proceeds of the offering of the January 2004 notes to make a subordinated intercompany note proceeds loan to Inmarsat Investments Limited. Inmarsat Investments Limited used the proceeds of that subordinated intercompany note proceeds loan to pay accrued interest and principal on the bridge loan, and to pay fees and expenses of the offering of the January 2004 notes.

- •

- On April 30, 2004, Inmarsat Finance plc issued $102,500,000 75/8% senior notes, which we refer to as the additional notes. We used the gross proceeds of the offering of the additional notes (excluding accrued interest, which we will retain, pending payment in September 2004) to make a second subordinated intercompany note proceeds loan to Inmarsat Investments Limited. Inmarsat Investments Limited used the gross proceeds of the second subordinated intercompany note proceeds loan to (i) repay $95.5 million of principal and $4.5 million of interest on the subordinated intercompany shareholder funding loan and (ii) pay fees and expenses of the offering of the additional notes. Thereafter, the proceeds from the repayment of the subordinated intercompany shareholder funding loan were used to repurchase or otherwise retire an equal amount of the subordinated preference certificates.

We refer in this prospectus to the January 2004 notes and the additional notes collectively as the existing notes. We are offering you new notes in exchange for your existing notes.

5

Summary Corporate and Financial Structure

The following table sets forth a summary of our corporate and financing structure following (i) the acquisition and related financing transactions and (ii) the offering of the notes and the use of proceeds therefrom. Please refer to "Principal Shareholders," "Description of Certain Financing Arrangements" and "Description of the Notes" for more information.

- (1)

- The shareholders hold their equity interests in the group through Inmarsat Group Holdings Limited, the ultimate parent company of the group. Inmarsat Group Holdings Limited owns all of the outstanding shares of Inmarsat Holdings Limited. For more information regarding our shareholders, see "Principal Shareholders."

- (2)

- See "Description of Certain Financing Arrangements—Subordinated Preference Certificates."

- (3)

- Comprised of $34.5 million of ordinary equity and $523.3 million of subordinated intercompany shareholder funding loan. See "Description of Certain Financing Arrangements—Subordinated Intercompany Shareholder Funding Loan."

- (4)

- Each of Inmarsat Investments Limited, Inmarsat Ventures Limited, Inmarsat Limited, Inmarsat Leasing (Two) Limited, Inmarsat Launch Company Limited and certain of our other subsidiaries are borrowers and/or guarantors under the senior credit agreement. Please see "Description of Certain Financing Arrangements—Senior Credit Agreement."

- (5)

- The shares of Inmarsat Ventures Limited are charged, on a first priority basis, to secure the obligations of Inmarsat Investments Limited under the senior credit agreement. Holders of the notes benefit from a second priority charge over those shares.

- (6)

- Inmarsat Finance plc is a special purpose finance subsidiary whose only significant assets are the subordinated intercompany note proceeds loans.

- (7)

- During the year ended December 31, 2003, Inmarsat Limited and Inmarsat Leasing (Two) Limited collectively accounted for approximately 96.4% of our consolidated revenue and approximately 107.6% of our EBITDA from continuing operations. As

6

at December 31, 2003, Inmarsat Limited and Inmarsat Leasing (Two) Limited collectively accounted for 76.0% of our total assets less intangible assets.

- (8)

- Inmarsat Launch Company Limited was formed on December 4, 2003. Inmarsat Launch Company Limited will be assigned our contracts related to the launch of our Inmarsat-4 satellites and will be the beneficiary of our Inmarsat-4 launch insurance (when obtained).

Our Address

Our principal executive offices are located at 99 City Road, London EC1Y 1AX, United Kingdom, and our telephone number is +44 (0)20 7728 1000. The website of Inmarsat Group Limited iswww.inmarsat.com. This reference to this website is an inactive textual reference only. None of the information contained on this website is incorporated in this prospectus.

7

The Exchange Offer

| Notes Offered for Exchange | | We are offering up to $477,500,000 in aggregate principal amount of our new 75/8% Senior Notes due 2012 in exchange for an equal aggregate principal amount of our existing 75/8% Senior Notes due 2012 on a one-for-one basis. The new notes have substantially the same terms as the existing notes you currently hold, except that we have registered the new notes under the U.S. Securities Act of 1933, as amended, which we refer to as the Securities Act, and therefore will be freely tradable and will not contain the provisions for an increase in the interest rate related to defaults in our agreement to execute this exchange offer. |

The Exchange Offer |

|

We are offering to exchange $1,000 principal amount of new notes for each $1,000 principal amount of your existing notes. In order for you to exchange your existing notes, you must tender them properly and we must accept them. We will exchange all existing notes that you tender validly and do not withdraw from tender. |

Ability to Resell Notes |

|

We believe that you may offer for resale, resell and otherwise transfer the new notes issued in the exchange offer without compliance with the registration and prospectus delivery provisions of the Securities Act if: |

|

|

• |

you acquire the new notes in the exchange offer in the ordinary course of your business; |

|

|

• |

you are not participating, do not intend to participate and have no arrangement with any person to participate in the distribution of new notes we issue to you in the exchange offer; |

|

|

• |

you are not an affiliate of Inmarsat Finance plc; and |

|

|

• |

you are not a broker-dealer tendering existing notes that you acquired directly from us for your own account. |

|

|

By tendering your existing notes as described below, you will be making representations to this effect. See "The Exchange Offer—Representations We Need From You Before You May Participate in the Exchange Offer." |

Those Excluded from the Exchange Offer |

|

You may not participate in the exchange offer if you are: |

|

|

• |

a holder of existing notes in any jurisdiction in which the exchange offer is not, or your acceptance will not be, legal under the applicable securities or "blue sky" laws of that jurisdiction, or |

|

|

• |

a holder of existing notes who is an affiliate of Inmarsat Finance plc. |

Consequences of Failure to Exchange Your Existing Notes |

|

After the exchange offer is complete, you will no longer be entitled to exchange your existing notes for new notes. If you do not exchange your existing notes for new notes in the exchange offer, your existing notes will continue to have the restrictions on transfer contained in the existing notes and in the indenture governing the existing notes. In general, your existing notes may not be offered or sold unless registered under the Securities Act, unless there is an exemption from, or unless the transaction is not governed by, the Securities Act and applicable state "blue sky" securities laws. We have no plans to register your existing notes under the Securities Act. |

| | | | | |

8

Expiration Date |

|

The exchange offer expires at 5:00 p.m., New York City time, on , , the expiration date, unless we extend the offer. If we decide to extend the offer, we do not currently intend to extend the expiration period beyond , . |

Conditions to the Exchange Offer |

|

The exchange offer has customary conditions that we may waive. There is no minimum amount of existing notes that holders must tender for us to complete the exchange offer. |

Procedures for Tendering Your Existing Notes |

|

If you wish to tender your existing notes for exchange in the exchange offer, you or the custodial entity through which you hold your existing notes must send to The Bank of New York before the exchange agent, on or before the expiration date of the exchange offer: |

|

|

• |

a properly completed and executed letter of transmittal, which you have received with this prospectus, together with your existing notes and any other documentation that the letter of transmittal requests; and |

|

|

• |

for holders who hold their positions through the Depositary Trust Company, which we refer to as DTC: |

|

|

|

• |

an agent's message from DTC stating that the tendering participant agrees to be bound by the letter of transmittal and the terms of the exchange offer; |

|

|

|

• |

your existing notes by timely confirmation of book-entry transfer through DTC; and |

|

|

|

• |

all other documents that the letter of transmittal requires. |

|

|

Holders who hold their positions through Euroclear and Clearstream, Luxembourg must adhere to the procedures described in "The Exchange Offer—Procedures for Tendering Your Existing Notes." |

Special Procedures for Beneficial Owners |

|

If you beneficially own existing notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender your existing notes in the exchange offer, you should contact the registered holder promptly and instruct the registered holder to tender on your behalf. |

| | | | | |

9

Guaranteed Delivery Procedures for Tendering Existing Notes |

|

If you wish to tender your existing notes, and the existing notes are not immediately available, or time will not permit your existing notes or other required documents to reach The Bank of New York the expiration date, or the procedure for book-entry transfer cannot be completed on a timely basis, you may tender your existing notes according to the guaranteed delivery procedures set forth under "The Exchange Offer—Guaranteed Delivery Procedures." |

Withdrawal Rights |

|

You may withdraw the tender of your existing notes at any time prior to 5:00 p.m., New York City time, on the expiration date. |

U.S. Tax Considerations |

|

The exchange of existing notes for the new notes will not be treated as a taxable transaction for U.S. federal income tax purposes. Rather, the notes you receive in the exchange offer will be treated as a continuation of your investment in the existing notes. For additional information regarding U.S. federal income tax considerations, you should read the discussion under "Tax Considerations—U.S. Taxation." |

Use of Proceeds |

|

We will not receive any proceeds from the issuance of the notes in the exchange offer. We will pay all expenses incidental to the exchange offer. |

Exchange Agent |

|

The Bank of New York is serving as the exchange agent. Its address, telephone number and facsimile number are: |

|

|

|

|

The Bank of New York

101 Barclay Street

Floor 7E

Corporate Trust Operations

Reorganization Unit

New York, New York 10286

Telephone: +1 212 815 5788

Fax: +1 212 298 1915

Attention: William Buckley |

Please review the information under the heading "The Exchange Offer" for more detailed information concerning the exchange offer.

10

The Notes

The summary below describes the principal terms of the notes and the guarantees relating to the notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The "Description of the Notes" section of this prospectus contains a more detailed description of the terms and conditions of the notes, including the definitions of certain terms used in this summary.

| Issuer | | Inmarsat Finance plc. |

Parent Guarantor |

|

Inmarsat Group Limited. |

Subsidiary Guarantors |

|

Inmarsat Investments Limited, Inmarsat Ventures Limited, Inmarsat Limited, Inmarsat Leasing (Two) Limited, Inmarsat Launch Company Limited and certain future subsidiaries of the parent guarantor. |

The Notes |

|

The terms of the new notes will be identical in all material respects to the terms of the existing notes, except that the new notes have been registered and therefore will not contain transfer restrictions and will not contain the provisions for an increase in the interest rate related to defaults in our agreement to carry out this exchange offer. |

Maturity Date |

|

June 30, 2012. |

Interest Payment Dates |

|

Semi-annually on March 1 and September 1 of each year, commencing on September 1, 2004. Interest will accrue from February 3, 2004 (the issue date of the January 2004 notes). |

Ranking, Guarantees and Security |

|

The Notes |

|

|

The notes are senior obligations of the issuer and are its only debt (save for any additional notes issued by it in the future). The notes are effectively subordinated to all obligations of the subsidiaries of the parent guarantor that do not guarantee the notes. |

|

|

The issuer is a finance subsidiary which does not conduct any operations, and its only significant assets are the subordinated intercompany note proceeds loans. |

|

|

The issuer and the trustee are party to a pledge agreement pursuant to which the issuer has pledged as security for its obligations under the notes the subordinated intercompany note proceeds loans. |

| | | |

11

|

|

The Parent Guarantee |

|

|

The parent guarantee of the notes: |

|

|

• is a general unsecured obligation of the parent guarantor; |

|

|

• rankspari passu in right of payment with all unsubordinated indebtedness and other obligations of the parent guarantor; and |

|

|

• ranks senior in right of payment with any future subordinated indebtedness of the parent guarantor. |

|

|

The parent guarantor is a holding company which does not conduct any operations, and its only assets are the shares of Inmarsat Finance plc and of Inmarsat Investments Limited (whose only significant asset is the shares of Inmarsat Ventures Limited). |

|

|

The parent guarantee is effectively subordinated to all obligations of the subsidiaries of the parent guarantor that do not guarantee the notes. |

|

|

The Subsidiary Guarantees |

|

|

The subsidiary guarantees of the notes: |

|

|

• are the general obligations of each subsidiary guarantor; |

|

|

• are unsecured (save for the second-ranking charge over the shares of Inmarsat Ventures Limited, referred to below); |

|

|

• are subordinated in right of payment to all existing and future senior debt (as defined in "Description of the Notes") of such subsidiary guarantor; and |

|

|

• arepari passu in right of payment with any future senior subordinated debt of such subsidiary guarantor. |

|

|

The guarantee of each subsidiary guarantor provides that it will not mature (and no amount will become due or payable thereunder) until a payment event of default under the notes has occurred and (i) 179 days have elapsed or (ii) certain other events, including certain insolvency events related to the relevant guarantor, occur. |

|

|

The subsidiary guarantees are contractually subordinated in right of payment to all senior debt of the subsidiary guarantors and effectively subordinated to all obligations of the subsidiaries of Inmarsat Group Limited that do not guarantee the notes. |

|

|

Inmarsat Investments Limited's guarantee of the notes are secured by a second-ranking charge over the shares of Inmarsat Ventures Limited. |

| | | |

12

|

|

Release of guarantees and security |

|

|

The guarantees and the second-ranking charge will be released in certain circumstances, including in connection with certain sales of the shares of Inmarsat Ventures Limited by a receiver or other insolvency agent appointed by the lenders under the senior credit agreement. |

|

|

See "Description of the Notes—Guarantees—Release of Guarantees" and "—Security—Release of Security." |

|

|

Impact of subordination |

|

|

As of December 31, 2003, on a pro forma basis as described under "Unaudited Pro Forma Combined Financial Data," the subsidiary guarantees would have been contractually subordinated to $800.0 million of our subsidiary guarantors' senior debt, and the notes and the guarantees would have been effectively subordinated to $76.1 million of obligations of our non-guarantor subsidiaries. This amount principally relates to deferred tax liabilities of Inmarsat Leasing Limited. |

Optional Redemption |

|

The issuer may redeem some or all of the notes at any time, at a redemption price equal to 100% of principal amount thereof plus a make-whole premium as of, and accrued and unpaid interest up to, the redemption date. For a description of how to calculate the make-whole premium, see "Description of the Notes—Optional Redemption." |

|

|

The issuer may redeem up to 35% of the aggregate principal amount of the notes outstanding prior to March 1, 2007 at a redemption price of (expressed as a percentage of the principal amount) of 107.625%, plus accrued and unpaid interest, with the proceeds of certain equity offerings. The issuer may make that redemption only if, after the redemption, at least $243.75 million (65% of the aggregate principal amount of the January 2004 notes) remains outstanding. |

|

|

In addition, the issuer may redeem some or all of the notes after March 1, 2008 at the redemption price described in the section entitled "Description of the Notes—Optional Redemption." |

Tax Redemption |

|

The issuer may redeem the notes in whole, but not in part, at any time, following certain changes in tax laws or their interpretation. If the issuer decides to redeem the notes following such change, the issuer must redeem the notes at a price equal to the principal amount of the notes plus accrued and unpaid interest to the date of redemption. See "Description of the Notes—Tax Redemption." |

| | | |

13

Mandatory Offers |

|

Upon certain change of control events, each holder of the notes may require us to repurchase all or a portion of its notes at a price equal to 101% of the principal amount thereof, plus accrued and unpaid interest to the date of repurchase. See "Description of the Notes—Repurchase at the Option of Holders—Change of Control." |

|

|

The issuer is also required to offer to repurchase the notes with the excess proceeds, if any, following certain asset sales and certain recoveries under the insurance policies relating to our satellites. The repurchase price will be equal to 100% of the principal amount of the notes, plus accrued and unpaid interest to the date of repurchase. See "Description of the Notes—Repurchase at the Option of Holders—Asset Sales and Events of Loss." |

Covenants |

|

The issuer, the guarantors and the trustee are parties to an indenture relating to the notes. The indenture limits, among other things, the ability of the parent guarantor and its restricted subsidiaries to: |

|

|

• incur additional indebtedness and issue preferred shares; |

|

|

• make certain restricted payments and investments; |

|

|

• transfer or sell assets; |

|

|

• create certain liens; |

|

|

• create restrictions on the ability of our restricted subsidiaries to pay dividends or other payments to us; |

|

|

• issue guarantees of indebtedness by our restricted subsidiaries; |

|

|

• enter into sale and leaseback transactions; |

|

|

• issue or sell shares of our restricted subsidiaries; |

|

|

• merge, consolidate, amalgamate or combine with other entities; |

|

|

• designate restricted subsidiaries as unrestricted subsidiaries; and |

|

|

• engage in any business other than a permitted business. |

|

|

In addition, the indenture requires the parent guarantor and its restricted subsidiaries to maintain certain launch and in-orbit insurance for their Inmarsat-3 and Inmarsat-4 satellites. |

|

|

Each of the covenants is subject to a number of important exceptions and qualifications. See "Description of the Notes—Certain Covenants." |

Form of Notes |

|

The notes were initially issued in the form of one or more global notes deposited with, and registered in the name of, DTC (or its nominee). |

| | | |

14

|

|

Ownership of interests in the global notes, and the book-entry interests therein, are available only to persons who have accounts with DTC or persons that may hold interests through either of them. Book-entry interests are shown on, and transfers thereof will be effected only through, records maintained in book-entry form by DTC and its respective participants. Except as set out under the section "Book Entry, Delivery and Form—Exchange of Global Notes for Definitive Registered Notes," participants in DTC are not entitled to receive physical delivery of notes in definitive form or to have notes issued and registered in their names and, while the notes are in global form, are not considered the owners or holders thereof under the indenture. See "Book Entry, Delivery and Form." |

Market |

|

We cannot assure you that a liquid market for the new notes will develop or be maintained. |

Listing |

|

The existing notes are listed on the Luxembourg Stock Exchange, and the existing notes are designated for trading on the PORTAL market. We intend to list the new notes on the Luxembourg Stock Exchange. |

Trustee |

|

The Bank of New York. |

Listing Agent and Luxembourg Paying

Agent |

|

The Bank of New York (Luxembourg) S.A. |

Governing law of the notes |

|

New York law. |

Risk Factors

You should refer to "Risk Factors" beginning on page 16 for an explanation of certain risks involved in investing in the notes.

15

RISK FACTORS

In addition to the other information in this prospectus, you should carefully consider the risks described below before deciding whether to invest in the notes.

Risks Relating to Our Business

We rely on third-party distributors to sell our services to end users and to determine the prices at which those services are sold. If our distributors and service providers were to fail to market or distribute our services effectively or to offer our services at prices which are competitive, our revenues, profitability, liquidity and brand image could be adversely affected.

We sell our services exclusively to third-party distributors, the majority of whom operate the land earth stations that transmit and receive those services to and from our satellites. These distributors then market and distribute our services to end users, either directly or through other distributors and service providers.

Pursuant to our arrangements with our distributors:

- •

- we do not set the prices end users pay for our services;

- •

- we cannot contract with end users of our services; and

- •

- except with respect to our next-generation services and in other very limited circumstances, we are not permitted to have a direct contractual relationship with any third party for distribution of our services, other than with the distributors that operate land earth stations that transmit and receive our services (other than Regional BGAN), whom we refer to as our master distributors.

As a result of these arrangements, we are dependent on the performance of our master distributors to generate substantially all of our revenues. If our master distributors were to fail to market or distribute our services effectively, or if they offered our services at prices which were not competitive, our revenues, profitability, liquidity and brand image could be adversely affected.

In December 2003, we completed negotiation of a commercial framework agreement, which governs our relationship with each of our distributors upon signing, and a new distribution agreement, which governs our relationship with all of our master distributors for a five-year term that commenced on April 15, 2004. We are currently completing a regulatory review of the terms of the agreements. As a result of that review, if any changes to the agreements are identified as being required, then, with the agreement of our master distributors, certain provisions of the agreements may need to be modified.

Sales to five of our master distributors represent a significant portion of our revenues and the loss of any of these distributors could adversely affect our revenues, profitability and liquidity.

As of December 31, 2003, we had 26 master distributors. For the year ended December 31, 2003, our five largest master distributors (measured by the volume of traffic on our network) were Stratos Global, Telenor, Xantic (a joint venture between KPN and Telstra), France Telecom Mobile Satellite Communications and KDDI. Sales to these five master distributors represented over 80% of our revenue during the year ended December 31, 2003. Any further consolidation among our master distributors would likely increase our reliance on a few key distributors of our services. The loss of any of these distributors, or the failure by any of them to market or distribute our services effectively, could cause end users to seek alternative service providers, which could adversely affect our revenues, profitability or liquidity.

16

We may not be able to offset declining revenues from voice services with revenues from data services.

Since 1999, our revenues from voice services (across each of our market sectors) have been declining, in part driven by less expensive voice services offered by our competitors. During the same period, voice revenue declines have been offset by increasing revenues from data services (which have not been subject to the same pricing pressures). Recently, however, the increase in our data revenues in the maritime sector has not completely offset voice revenue declines. Our future profitability depends, in part, on our ability to offset declining revenues from voice services with revenues from data services. If revenues from our data services do not continue to increase at a rate sufficient to offset the decline in revenues from our voice services, our total future revenues will be adversely affected.

The global communications industry is highly competitive. It is likely that we will face significant competition in the future from other network operators, which may adversely affect end user take-up of our services and affect our revenues.

The global communications industry is highly competitive. We face competition from a number of communications technologies in the various target markets for our services. It is likely that we will continue to face significant competition from other network operators in some or all of our target market segments in the future, particularly from satellite network operators. Competition from Iridium and Globalstar, two global satellite network operators, has been increasing, particularly with respect to voice and low-speed data services. In addition, we also face competition for voice and low-speed data services from Thuraya and (to a lesser extent) other regional mobile satellite network operators, which has influenced the price at which our distributors and service providers offer our services. Thuraya's satellites are also capable of delivering high speed data services comparable to our next generation services, although only on a regional basis. Communications providers who operate private networks using very small aperture terminals, or VSATs, are also increasingly targeting users of mobile satellite services. Furthermore, the gradual extension of terrestrial wireline and wireless communications networks to areas not currently served by them may reduce demand for our services in those areas. If we fail to offer services that compete effectively, we may experience lower end user take-up which would have an adverse impact on our revenues, profitability and liquidity.

We may not retain sufficient rights to the spectrum required to operate our satellite system to its expected capacity.

We must retain rights to use sufficient L-band spectrum necessary for the transmission of signals between our satellites and end user terminals. Our right to spectrum is granted on an annual basis and evaluated and established, in part, through two annual, regional multilateral meetings of satellite operators—one for operators whose satellites cover North America, and a second for those which cover Europe, Africa, Asia and the Pacific. Since 1999, the North American operators have been unable to agree new spectrum allocations and rights have been frozen at 1999 levels. Additionally, Mobile Satellite Ventures, or MSV, has recently challenged our right to some of our current North American spectrum, claiming that MSV loaned us that spectrum in 1999. We have rejected that claim, and we believe the appropriate forum for spectrum allocation would be the next round of multilateral coordination meetings of North American operators. Competition for spectrum from new operators or services (for example, ancillary terrestrial components, or ATC services) could make it more difficult for us to retain rights to spectrum. If we were unable to retain sufficient rights to spectrum, our ability to provide our services in the future would be limited, which would have an adverse effect on our business and results of operations. We cannot assure you that we will be able to retain sufficient rights to spectrum in the future.

17

Applications by our competitors to use L-band spectrum for terrestrial services or on an ancillary basis could interfere with our services.

On January 29, 2003, the Federal Communications Commission, or FCC, promulgated a general ruling that mobile satellite service spectrum, including the L-band spectrum we use to operate our services, could be used by mobile satellite service operators to integrate ATC services into their satellite networks in order to provide combined terrestrial and satellite communications services to mobile terminals in the United States. The implementation of ATC services by other mobile satellite service operators in the United States or other countries may result in increased competition for the right to use L-band spectrum, and such competition may make it difficult for us to obtain or retain spectrum resources we require for our existing and future services. In addition, the FCC's decision to permit ATC services was based on certain assumptions, particularly relating to the level of interference that the provision of ATC services would likely cause to operators of other services, such as us, who use the L-band spectrum. One of our competitors, Mobile Satellite Ventures, has submitted applications to the FCC for authority to use L-band spectrum assigned to its satellite network to provide ATC services. If the FCC's assumptions with respect to the use of mobile satellite service spectrum for ATC services prove inaccurate, or a significant level of ATC services is provided in the United States, the provision of ATC services could interfere with our satellites and user terminals, which may adversely impact our services. For example, the use of certain L-band spectrum to provide ATC services in the United States could interfere with our satellites providing communications services outside the United States where the satellites' "footprint" overlaps the United States. Such interference could limit our ability to provide services that are transmitted through any satellite visible to the United States. Three of our Inmarsat-3 satellites are visible to the United States. In addition, users of our terminals in the United States could suffer interruptions to our services if they try to use their terminals near land earth stations used to provide ATC services.

Additionally, Mobile Satellite Ventures has petitioned the FCC to reconsider its ATC service rules in order to relax certain technical requirements applicable to ATC operations, and its pending ATC applications seek certain variancies or waivers of the ATC technical rules. Grant of these requests would result in increased interference into our satellite network and to mobile terminals communicating with our network. We therefore have opposed these Mobile Satellite Ventures requests for relaxation of the ATC technical rules. However, we cannot predict how the FCC will act on these requests, nor can we assure you that an FCC grant of any request for relaxation of the ATC technical rules would not have a material adverse effect on our business or results of operations.

Other jurisdictions are considering, and could implement, similar regulatory regimes in the future.

Any or all of the preceding could have a material adverse effect on our revenues, profitability or liquidity.

We rely on third parties to manufacture and supply terminals used to access our existing services, and as a result, we cannot control the availability of terminals.

Terminals used to access our existing services are built by a limited number of independent manufacturers. Although we provide manufacturers with key performance specifications for the terminals, these manufacturers could:

- •

- reduce production of, or cease to manufacture, terminals that access our services;

- •

- manufacture terminals with defects that fail to perform to our specifications;

- •

- fail to build or upgrade terminals that meet end users' requirements within our target market segments;

- •

- fail to meet delivery schedules or to market or distribute terminals effectively; or

18

- •

- sell our terminals at prices that end users or potential end users do not consider attractive.

Any of the foregoing could adversely affect the ability of our distributors to sell our services, which, in turn, could adversely affect our revenues, profitability and liquidity, as well as our brand image.

We rely on Thuraya to provide leased satellite capacity for our Regional BGAN service, and factors beyond our control with respect to the Thuraya satellite could affect our Regional BGAN revenues. Our Regional BGAN revenues could be affected by the operational failure of our land earth station in Fucino, Italy.

We lease capacity on a Thuraya satellite to provide our Regional BGAN service. The Thuraya satellite, like all satellites, could experience technical and operational failures which would adversely affect our ability to provide our Regional BGAN service. Furthermore, the lease can be terminated following consultation, if we become insolvent. A loss of access to the Thuraya satellite could adversely affect our revenue and/or our brand image and make it more difficult to market our Regional BGAN or future BGAN services.

We land satellite transmission of our Regional BGAN services exclusively at our land earth station in Fucino, Italy. Our Regional BGAN revenues would be adversely affected by the operational failure of the Fucino land earth station.

Our access to the U.S. market may be restricted under the terms of the ORBIT Act.

In the United States, we are subject to the Open-market Reorganization for the Betterment of International Telecommunications Act, or ORBIT Act. Under the terms of the ORBIT Act, we must conduct an initial public offering, or IPO, before June 30, 2004 or, at the discretion of the FCC, December 31, 2004. The FCC directed us to file within 30 days after conducting our IPO a demonstration that the IPO is in compliance with the ORBIT Act. We have submitted a filing with the FCC asserting that the acquisition, together with the offering of the notes, the associated listing of the notes on the Luxembourg Stock Exchange and the planned registration of the notes with the SEC, satisfy the intent and objectives of these ORBIT Act requirements. The FCC placed our submission on public notice and invited interested third parties to file oppositions or comments no later than April 5, 2004. SES Americom and Mobile Satellite Ventures have opposed our filing. We filed our response to the opposition filing within the required FCC timetable of April 20, 2004. We requested in our response that the FCC extend our IPO deadline from June 30, 2004 to December 31, 2004. SES Americom and Mobile Satellite Ventures filed replies to our response as required on or before April 30, 2004. We can provide no assurance that the FCC will find that we have met these requirements of the ORBIT Act. If the FCC determines that we failed to meet these requirements of the ORBIT Act within the specified time period, the ORBIT Act requires the FCC to deny or impose limitations or conditions upon the licenses granted to our distributors or service providers to provide certain services to, from or within the United States, and to revoke or impose limitations or conditions on previous licenses to provide such services. If the FCC revokes our distributor or service provider licenses, we would be unable to provide the bulk of our services to, from or within the United States. In addition, if the FCC determines that we failed to comply with the terms of the ORBIT Act, the FCC would be required to deny our distributors or service providers a license to provide our next-generation services, including BGAN, to, from or within the United States. In addition, we would be unable to land signals from our satellites within the United States for a number of our services. Any revocation or imposition of limitations or conditions on the terms of the licenses our distributors rely on to sell our current or next-generation services would impede the development of our business in the United States and would have an adverse effect on our revenues.

19

We may not be able to recruit and retain the number and caliber of management or employees necessary for our business, which may adversely affect our revenues and profitability.

Technological competence and innovation is critical to our business and depends, to a significant degree, on the work of technically skilled employees. Competition for the services of these types of employees is intense. We may not be able to attract and retain these employees. If we are unable to attract and retain adequate technically skilled employees, including the development and provision of our higher-bandwidth services, our competitive position could be materially adversely affected.

Furthermore, following the acquisition, we might suffer the loss of management or employees whom we will need to replace. If we are unable to replace them, our competitive position could be materially adversely affected.

We have recently had a senior management change, and we are currently implementing a business review, including a reduction in the number of our employees. These events could affect our ability to retain the services of key employees in the future.

Risks Relating to Our Technology and the Operation and Development of Our Network

Our satellites and satellites systems are subject to significant operational risks while in orbit which, if they were to occur, could adversely affect our revenues, profitability and liquidity.

Satellites are subject to significant operational risk while in orbit. These risks include malfunctions, commonly referred to as anomalies, that have occurred in our satellites and the satellites of other operators as a result of various factors, such as satellite manufacturers' errors, problems with the power or control systems of the satellites and general failures resulting from operating satellites in the harsh environment of space.