Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on July 9, 2004.

Registration No. 333–115996–11

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

AMENDMENT NO. 1

FORM F-4

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

| Concordia Bus Nordic AB (publ) (Exact name of registrant as specified in its charter) | ||||

(For co-registrants, please see "Table of co-registrants" on the following page) | ||||

Sweden (State or other jurisdiction of incorporation or organization) |

Not Applicable

(I.R.S. Employer Identification No.)

Solna Strandväg 78, SE-171 54,

Solna, Sweden 011 46 85 46 30 000

(Address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

4100

(Primary Standard Industrial Classification Code Number)

CT Corporation System

111 Eighth Avenue, New York, NY 10011 (212) 894-8600

(Address, including zip code, and telephone number, including

area code, of agent for service of process)

Copies of Communications to:

Robert S. Trefny, Esq.

Clifford Chance Limited Liability Partnership

10 Upper Bank Street London E14 5JJ United Kingdom

Approximate date of commencement of proposed sale to the public: As soon as possible after the effective date of this Registration Statement.

| Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per unit(1) | Proposed maximum aggregate offering price | Amount of registration fee | ||||

|---|---|---|---|---|---|---|---|---|

| 9.125% Senior Secured Notes Due August 1, 2009 | $157,326,000.00(2) | 100% | $157,326,000.00 | $19,933.20(3) | ||||

| Guarantee by Concordia Bus Nordic Holding AB | — | — | — | — | ||||

| Guarantee by Alpus AB | — | — | — | — | ||||

| Guarantee by Enköping-Bålsta Fastighetsbolag AB | — | — | — | — | ||||

| Guarantee by Interbus AB | — | — | — | — | ||||

| Guarantee by Malmfältens Omnibus AB | — | — | — | — | ||||

| Guarantee by Swebüs AB | — | — | — | — | ||||

| Guarantee by Swebus Busco AB | — | — | — | — | ||||

| Guarantee by Swebus Express AB | — | — | — | — | ||||

| Guarantee by Swebus Fastigheter AB | — | — | — | — | ||||

| Guarantee by Concordia Bus Finland Oy Ab | — | — | — | — | ||||

| Guarantee by Ingeniør M.O. Schøyens Bilcentraler AS | — | — | — | — | ||||

- (1)

- Estimated solely for the purpose of computing the amount of the registration fee.

- (2)

- The €130,000,000 face amount of the Senior Secured Notes has been translated into dollars at the rate of $1.2102 per €1.00, the noon buying rate for euro published by the Federal Reserve Bank of New York on May 26, 2004.

- (3)

- In accordance with Rule 457(f)(1) under the Securities Act of 1933, the filing fee has been calculated on the basis of the market value of the Notes to be received by the Registrants in the exchange offer using the noon buying rate for cable transfers of euros as reported by the Federal Reserve Bank of New York as of May 26, 2004 of $1.2102 per €1.00.

The registrant hereby amends the registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

| Name of Additional Registrant | State of Incorporation/ Formation | Primary Standard Industrial Classification Code | I.R.S. Employer Identification Number | |||

|---|---|---|---|---|---|---|

| Concordia Bus Nordic Holding AB | Sweden | 4100 | Not Applicable | |||

| Alpus AB | Sweden | 4100 | Not Applicable | |||

| Enköping-Bålsta Fastighetsbolag AB | Sweden | 4100 | Not Applicable | |||

| Interbus AB | Sweden | 4100 | Not Applicable | |||

| Malmfältens Omnibus AB | Sweden | 4100 | Not Applicable | |||

| Swebus AB | Sweden | 4100 | Not Applicable | |||

| Swebus Busco AB | Sweden | 4100 | Not Applicable | |||

| Swebus Express AB | Sweden | 4100 | Not Applicable | |||

| Swebus Fastigheter AB | Sweden | 4100 | Not Applicable | |||

| Concordia Bus Finland Oy Ab | Finland | 4100 | Not Applicable | |||

| Ingeniør M.O. Schøyens Bilcentraler AS | Norway | 4100 | Not Applicable |

Exchange Offer for

€130,000,000

Concordia Bus Nordic AB(publ)

9.125% Senior Secured Notes due August 1, 2009

Guaranteed by Concordia Bus Nordic Holding AB, Alpus AB, Enköping-Bålsta Fastighetsbolag AB, Interbus AB, Malmfältens Omnibus AB, Swebus AB, Swebus Busco AB, Swebus Express AB, Swebus Fastigheter AB, Concordia Bus Finland Oy Ab and Ingeniør M.O. Schøyens Bilcentraler AS

We are offering to exchange our 9.125% Senior Secured Notes due August 1, 2009, which we refer to as the Exchange Notes, for all of our 9.125% Senior Secured Notes due August 1, 2009, which we refer to as the Old Notes. An aggregate principal amount of €130,000,000 of the Old Notes are outstanding.

- •

- Exchange Offer Expiration Date

9:00 a.m. central European time on , 2004, unless extended. - •

- Exchange Ratio

You will receive €1,000 principal amount of Exchange Notes for each €1,000 principal amount of Old Notes that you validly tender. - •

- Withdrawal Rights

You may withdraw a tender of the Old Notes at any time prior to the expiration date.

- •

- Substantially Identical to Old Notes

The terms of the Exchange Notes are substantially identical to those of the Old Notes, except that you can freely trade the Exchange Notes in the United States. - •

- Ranking

The Exchange Notes will be senior secured debt of Concordia Bus Nordic AB (publ) ("Concordia"), ranking equally with all of its existing and future senior unsecured debt and senior in right of payment to its existing and future subordinated debt, if any.The Exchange Notes will rank senior to all of our future junior subordinated indebtedness.

As of July 9, 2004, there is no debt that is senior or effectively senior to the Exchange Notes.

- •

- Guarantees

Concordia Bus Nordic Holding AB and all subsidiaries of Concordia, other than minor dormant subsidiaries, have fully and unconditionally guaranteed the Exchange Notes. The guarantees are joint and several. - •

- Redemption

The Exchange Notes may be redeemed at any time on or after February 1, 2007 at the redemption prices listed under "Description of Notes—Optional Redemption." - •

- Listing

The Exchange Notes will be listed on the Luxembourg Stock Exchange. The Exchange Notes will not be listed on any U.S. exchange.

This investment involves risks. You should read "Risk Factors" beginning on page 17.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

Each broker-dealer that receives Exchange Notes for its own account in exchange for Old Notes, where those Old Notes were acquired by that broker-dealer as a result of its market-making activities and other trading activities, acknowledges that it will deliver a prospectus meeting the requirements of the Securities Act in connection with any resale of such Exchange Notes.

The date of this prospectus is , 2004.

You can obtain copies of documents described in, but not included or delivered with this prospectus, without charge to you upon written or oral request. You must address your request to Jan Seljemo, Chief Financial Officer, Concordia Bus Nordic AB (publ), Solna Strandväg 78, SE-171 54 Solna, Sweden. To obtain timely delivery, you must request the information no later than , 2004.

For a period of 180 days after the expiration date, we will promptly send additional copies of this prospectus and any amendment or supplement to it to any broker-dealer that requests additional copies of the prospectus in the letter of transmittal. Until , 2004, all dealers effecting transactions in the Exchange Notes, whether or not participating in the exchange offer, may be required to deliver a prospectus.

You should rely on the information contained in this prospectus. We have not authorized anyone to provide you with different information. We are not making an offer of these securities in any jurisdiction where the offer is not permitted.

WHERE YOU CAN FIND MORE INFORMATION

We have filed with the Securities and Exchange Commission a registration statement on Form F-4 under the Securities Act of 1933 to register the exchange offer contemplated in this prospectus. This prospectus, which forms a part of the registration statement, does not contain all of the information presented in the registration statement. For further information about us, the exchange offer and any document referred to in this prospectus, you should refer to the registration statement and its exhibits.

The registration statement, its exhibits and schedules, reports and other information that we have filed with or furnished to the Commission may be inspected and copied at the public reference facilities maintained by the Commission at Room 1024, Judiciary Plaza, 450 Fifth Street, N.W., Washington, D.C. 20549. You may also contact the Commission at 1-800-SEC-0330 and at its regional offices at 7 World Trade Center, 13th Floor, New York, New York, 10048 and at Citicorp Center, 500 West Madison Street, Suite 1400, Chicago, Illinois 60661-2511. You can obtain copies of this material by mail from the Public Reference section of the Commission, 450 Fifth Street, N.W., Washington, D.C., 20549, at prescribed rates.

ENFORCEMENT OF CERTAIN CIVIL LIABILITIES

Concordia is organized under the laws of Sweden and the Guarantors are organized under the laws of Sweden, Norway and Finland. All of our directors, executive officers and our subsidiaries and the independent auditors named in this prospectus are non-residents of the United States. As a result, it may not be possible for investors to effect service of process within the United States upon us or such persons or to enforce against any of them judgments of US courts predicated upon civil liabilities under US federal securities laws. Although we agree under the terms of the indenture relating to these Notes to accept service of process in the United States by an agent designated for such purpose, it may not be possible for investors to (i) effect service of process within the United

i

States upon our officers and directors and the independent auditors named herein and to (ii) realize in the United States upon judgments against such persons obtained in such courts predicated upon civil liabilities of such persons, including any judgments predicated upon US federal securities laws to the extent such judgments exceed such person's US assets. There is also doubt as to the enforceability in Sweden, Norway and Finland, in original actions or in actions for enforcement, of judgments of US courts predicted upon the civil liability provisions of the federal securities laws of the United States.

CURRENCY AND FINANCIAL STATEMENT PRESENTATION

Unless otherwise indicated, references in this prospectus to "SEK," "Swedish Krona" or "Swedish Kronor" are to the lawful currency of Sweden; references to "euro" or "€" are to the single currency of the participating Member States in the Third Stage of European Economic and Monetary Union of the Treaty Establishing the European Community, as amended from time to time; references to "Norwegian Kroner" or "NOK" are to the lawful currency of Norway; and references to "US dollars" or "$" are to the lawful currency of the United States of America.

We prepare our consolidated financial statements in Swedish Kronor. For information regarding recent rates of exchange between Swedish Kronor and US dollars, see the section "Exchange Rates."

The consolidated financial statements of Concordia Bus Nordic Holding AB are prepared in accordance with accounting principles generally accepted in Sweden ("Swedish GAAP"), which differ in certain respects from generally accepted accounting principles in certain other countries. The significant differences between Swedish GAAP and accounting principles generally accepted in the United States of America ("US GAAP") are discussed in Note 32 to the consolidated financial statements of Concordia Bus Nordic Holding AB included elsewhere in this prospectus.

ii

The following summary contains basic information about us and the exchange offer. Because this is a summary, it does not contain all the information that may be important to you. For a more complete understanding of the exchange offer, we encourage you to read this entire document, including Concordia Bus Nordic Holding AB's consolidated financial statements included herein and the notes thereto, and the documents we have referred you to.

The information set out in sections of this prospectus describing clearing arrangements is subject to any change in or reinterpretation of the rules, regulations and procedures of Euroclear or Clearstream, which we refer to as the clearing systems, currently in effect. Investors wishing to use the facilities of any of the clearing systems are advised to confirm the continued applicability of the rules, regulations and procedures of the relevant clearing system. We will have no responsibility or liability for any aspect of the records relating to, or payments made on account of, book-entry-interests held through the facilities of any clearing system or for maintaining, supervising or reviewing any records relating to these book-entry-interests.

Unless otherwise stated in this prospectus or unless the context otherwise requires, references to "Concordia," "we," "us" or "our" are to Concordia Bus Nordic AB and, as the context may require, its subsidiaries; references to "our indirect Parent" are to Concordia Bus AB (publ) and, as the context may require, its subsidiaries; references to "our direct Parent" or "the Parent Guarantor" are to Concordia Bus Nordic Holding AB and, as the context may require, its subsidiaries; references to "Swebus" are to Swebus AB; references to "Concordia Finland" are to Concordia Bus Finland Oy Ab; references to "SBC" are to Ingeniør M.O. Schøyens Bilcentraler AS; references to "SG" or the "Schøyen Group" are to Schøyen Gruppen AS; and references to "Bus Holdings" are to Bus Holdings S.a.r.l.

Overview

We provide public bus transportation services in Sweden, Norway and Finland, operating through our three main operating subsidiaries: Swebus, SBC and Concordia Finland, respectively. We also provide express bus and coach hire services. In Sweden, we currently operate 3,156 buses, and are the largest operator through Swebus, with an estimated market share of approximately 31.3% of the public bus transportation market (measured by the number of buses in operation). This market share data has been calculated based on the share of total number of buses, as provided by the relevant CPTA. In Norway, SBC currently operates 405 buses (of these 405 buses, 94 had been purchased pursuant to a contract entered into in January of 2004 and included in the February 29, 2004 year end totals, though these 94 buses were not delivered to SBC until March of 2004) and has an estimated 20% market share of the public bus transportation market in southeastern Norway, which includes Oslo and neighboring cities. This market share data has been calculated based on the share of total number of buses, as provided by the relevant CPTA. In Finland, Concordia Finland currently operates 347 buses and is the second largest operator in the greater Helsinki area with a market share of approximately 26%. This market share data has been calculated based on the relative number of contract kilometres. This information is made available at each tendering.

Previously, Concordia Bus Nordic Holding AB was named Interbus Finans AB and was a wholly owned subsidiary of Concordia Bus Nordic AB (publ), which was wholly owned by Concordia Bus AB. In January 2004, a reorganization was performed whereby Concordia Bus Nordic AB (publ) transferred to Concordia Bus AB its 100% share ownership of Interbus Finans AB. Concordia Bus AB then transferred its shares in Concordia Bus Nordic AB (publ) to Interbus Finans AB. Interbus Finans AB was then renamed Concordia Bus Nordic Holding AB.

1

Such reorganization had the effect of creating a new holding company for Concordia Bus Nordic AB (publ) from one of its dormant subsidiaries. Concordia Bus Nordic Holding AB is a non-operating holding company that has no assets other than its shares in Concordia Bus Nordic AB (publ).

For the year ended February 29, 2004, we had net revenue of SEK 4,761 million. We sustained operating losses of SEK 108 million for the year ended February 29, 2004, SEK 123 million for the year ended February 28, 2003 and SEK 115 million for the year ended February 28, 2002. We sustained net losses of SEK 171 million for the year ended February 29, 2004, SEK 179 million for the year ended February 28, 2003 and SEK 173 million for the year ended February 28, 2002.

Pursuant to an intercompany loan agreement entered into on February 28, 2002, as amended and restated as of the issue date, Concordia Bus AB provided a shareholder loan (the "Subordinated Shareholder Loan") to Concordia of SEK 501 million in aggregate principal amount, comprising a portion of the net proceeds of the Parent Notes issued in 2002. The current outstanding balance of the Subordinated Shareholder Loan is SEK 368 million. The terms of this Subordinated Shareholder Loan, as so amended and restated, provide that (i) interest accrues at a rate of 11% per annum, (ii) the loan is payable on demand and (iii) payments in respect of the Subordinated Shareholder Loan have been subordinated to our obligations under the Notes. The Subordinated Shareholder Loan will mature on February 14, 2010.

Our Address

Our principal executive office is located at Solna Strandväg 78, SE-171 54, Solna, Sweden, and our telephone number is +46 85 46 30 000. Our Internet address is www.concordiabus.com.

2

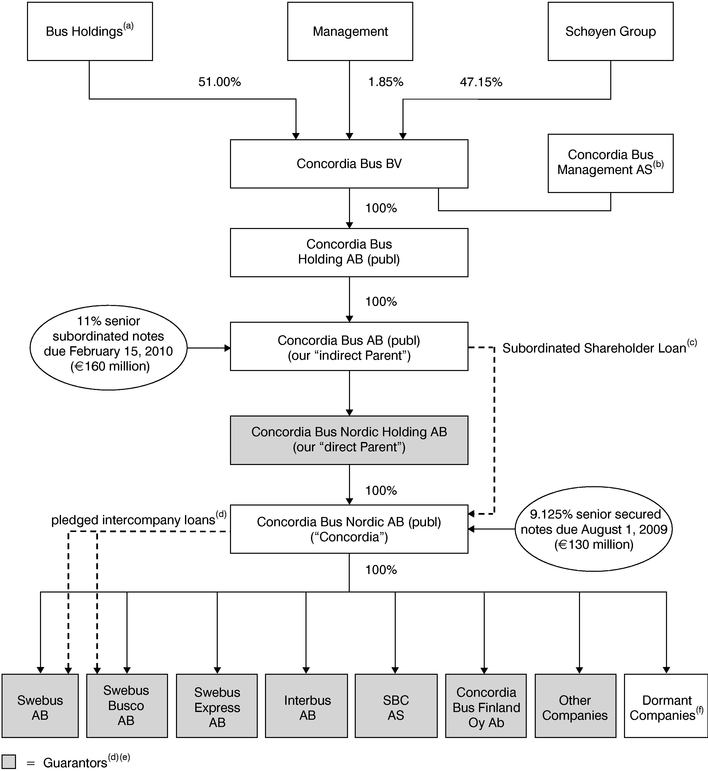

The following chart sets forth the corporate structure of Concordia.

- (a)

- Bus Holdings is an affiliate of Goldman Sachs International.

- (b)

- Under the terms of a management services agreement, Concordia Bus Management AS has agreed with Concordia Bus BV to provide specified management services to Concordia Bus BV and its subsidiaries. See "Principal Shareholders and Related Party Transactions" for a description of the management services agreement.

- (c)

- Pursuant to an intercompany loan agreement entered into on February 28, 2002, as amended and restated, Concordia Bus AB provided the Subordinated Shareholder Loan to Concordia of SEK 501 million in aggregate principal amount, comprising a portion of the net proceeds of the Parent Notes issued in 2002. The current outstanding balance of the Subordinated Shareholder Loan is SEK 368 million. The terms of this Subordinated Shareholder Loan, as so amended

3

and restated, provide that (i) interest accrues at a rate of 11% per annum, (ii) the loan is payable on demand and (iii) payments in respect of the Subordinated Shareholder Loan are subordinated to our obligations under the Notes. The Subordinated Shareholder Loan will mature on February 14, 2010.

- (d)

- The Notes benefit from (i) a pledge by our direct Parent of the shares in Concordia, (ii) a pledge by Concordia of the shares of all of its operating subsidiaries, (iii) certain other security, including a pledge by Swebus Busco AB of all of the buses it owns (with a book value at November 30, 2003, of approximately SEK 1.3 billion), which represents substantially all of the tangible fixed assets of Concordia and its operating subsidiaries, and a pledge by Swebus AB of a floating charge over its assets securing an amount up to SEK 100 million and (iv) a pledge by Concordia of certain secured intercompany loans to Swebus AB and Swebus Busco AB, in the amounts of SEK 200 million and SEK 800 million, respectively, pursuant to which a second ranking security interest over certain assets of those Guarantors has been granted to Concordia. The Indenture in respect of the Notes includes certain intercreditor arrangements between Concordia and the Trustee with respect to the Collateral securing such intercompany loans. The laws of certain jurisdictions may limit recovery over security constituting the Collateral. See "Risk Factors—Risks Related to the Notes—Enforcement of the Note Guarantees and the Collateral may be subject to certain limitations and will require satisfaction of certain conditions."

- (e)

- The Notes are guaranteed on a senior basis by all of Concordia's operating subsidiaries as well as by our direct Parent, Concordia Bus Nordic Holding AB (together, the "Guarantors"). These subsidiaries are: Swebus AB, Swebus Busco AB, Swebus Express AB, Interbus AB, Ingeniør M.O. Schøyens Bilcentraler AS, Concordia Bus Finland Oy Ab, Swebus Fastigheter AB, Alpus AB, Malmfältens Omnibus AB and Enköping-Bålsta Fastighetsbolag AB. The laws of certain jurisdictions may limit the enforceability of certain guarantees. See "Risk Factors—Risks Related to the Notes—Enforcement of the Note Guarantees and the Collateral may be subject to certain limitations and will require satisfaction of certain conditions."

- (f)

- These companies are dormant and have no material assets. Concordia has designated Arlanda Buss AB, Billingens Trafik AB, Enköping-Bålsta Trafik AB, Gävle Trafik AB, Hälsinge Wasatrafik AB, AB Härnösandsbuss, Karlstadsbuss AB, AB Kristinehamns Omnibusstrafik, Saltsjöbuss AB, Swebus Service AB, Swebus Västerås AB, Tumlare Buss AB, Wasabuss AB and Wasatrafik AB as unrestricted subsidiaries. These companies will not guarantee the Notes.

4

The exchange offer applies to the €130,000,000 aggregate principal amount at maturity of the Old Notes. The form and terms of the Exchange Notes are the same as the form and terms of the Old Notes except that the Exchange Notes have been registered under the Securities Act and, therefore, will not bear legends restricting their transfer. The Exchange Notes will be entitled to the benefits of the Indenture under which the Old Notes were issued. We sometimes refer to the Old Notes and the Exchange Notes collectively in this prospectus as the "Notes". You should read "Description of Notes" for additional information about the terms of the Notes.

| The Exchange Offer | We are offering to exchange each €1,000 principal amount of Exchange Notes for each €1,000 principal amount of Old Notes. As of the date hereof, Old Notes representing €130,000,000 aggregate principal amount at maturity are outstanding. | |||

To be exchanged, an outstanding Old Note must be properly tendered by you and accepted by us. All outstanding Old Notes that are validly tendered and not validly withdrawn will be exchanged. If you wish to tender your Old Notes for exchange in the exchange offer, you must send your response to the exchange agent on or prior to the expiration date. We will issue Exchange Notes on or promptly after the expiration of the exchange offer. | ||||

Resale of the Exchange Notes | Based on an interpretation by the staff of the Securities and Exchange Commission set forth in interpretive letters issued to third parties, we believe that the Exchange Notes may be offered for resale, resold and otherwise transferred by you, without compliance with the registration and prospectus delivery provisions of the Securities Act, if you are not our affiliate, the Exchange Notes issued in the exchange offer are being acquired by you in the normal course of business, you are not participating in the distribution of the Exchange Notes, you have no intention of participating in the distribution of Exchange Notes and you have no arrangement or understanding with any person to participate in the distribution of the Exchange Notes. | |||

Each broker-dealer that receives Exchange Notes for its own account in exchange for Old Notes, where those Old Notes were acquired by that broker-dealer as a result of its market-making activities or other trading activities, must acknowledge that it will deliver a prospectus meeting the requirements of the Securities Act in connection with any resale of such Exchange Notes. You should read "Plan of Distribution". If you are a broker-dealer who purchased Old Notes directly from us for resale, you may not participate in the exchange offer. | ||||

5

Registration Rights Agreements | We sold the Old Notes on January 16, 2004 in a private placement. In connection with the sale, we executed an Exchange and Registration Rights Agreement for the benefit of the purchasers under which we agreed to effect the exchange offer. You should read the information under the heading "Purpose and Effect" in "The Exchange Offer". | |||

Expiration Date | The exchange offer will expire at 9:00 a.m., central European time, , 2004, or at a later date and time to which it is extended. Any Old Notes not accepted for exchange for any reason or properly withdrawn will be returned without expense to you promptly after the expiration or termination of the exchange offer. | |||

Withdrawal | You may withdraw your tender of Old Notes during the exchange offer at any time prior to 9:00 a.m., central European time, on the expiration date. | |||

Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, some of which may be waived by us. You should read the information under the heading "Conditions" in "The Exchange Offer" for a description of these conditions. | |||

Procedures for Tendering Old Notes | Prior to tendering any Old Notes, you should read this prospectus and the letter of transmittal. In addition, you must comply with the procedures established by Euroclear and/or Clearstream, as the case may be, prior to the expiration date. By executing or agreeing to be bound by the letter of transmittal and by participating in the exchange offer, you will represent to us that, among other things, | |||

• | the Exchange Notes acquired under the terms of the exchange offer are being obtained by you in the ordinary course of your business, | |||

• | you do not intend to engage in a distribution of those Exchange Notes, | |||

• | you do not intend to engage in a distribution of those Exchange Notes, | |||

• | you do not have an arrangement or understanding with any person to participate in the distribution of those Exchange Notes, | |||

• | you are not an affiliate of us, and | |||

• | if you are a broker-dealer, you acquired the Old Notes as a result of market-making or other trading activities and will deliver a copy of this prospectus in connection with any resale of Exchange Notes. | |||

6

Under the terms of the Exchange and Registration Rights Agreement, we are required to file a registration statement for a "shelf" registration providing for the registration and sale on a continuous or delayed basis in respect of the Old Notes if existing interpretations of the Securities and Exchange Commission are changed so that the Exchange Notes received by you in the exchange offer are not or would not be, upon receipt, transferable by you (unless you are our affiliate) without restriction under the Securities Act. | ||||

Acceptance of Old Notes and Delivery of Exchange Notes | We will accept for exchange any and all Old Notes which you properly tender prior to 9:00 a.m., central European time, on the expiration date. We will issue the Exchange Notes promptly following the expiration date. | |||

Exchange Agent | Deutsche Bank AG London is serving as exchange agent for the exchange offer. They can be reached by telephone at +(44) 20-7545-8000 for more information. | |||

United States Tax Considerations | The exchange under the terms of the exchange offer will not be a taxable event for US federal income tax purposes. You should read the information under the heading "United States Federal Tax Considerations—Sale, Exchange, Retirement and Other Disposition of the Notes" in "Certain Tax Considerations". | |||

Effect of Not Tendering | If you choose not to tender your Old Notes, or if they are not accepted, the existing transfer restrictions will continue to apply. We do not have any further obligation to provide for the registration of the Old Notes under the Securities Act. Old Notes will, following consummation of the exchange offer, bear interest at the same rate as the Exchange Notes. | |||

7

Summary of Key Terms of the Exchange Notes

The Exchange Notes are registered under the Securities Act and accordingly are not subject to several restrictions on transfer applicable to the Old Notes. Except as provided in the previous sentence, the Exchange Notes have terms and conditions identical in all material respects to those of the Old Notes. Accordingly, the following description of the Notes applies equally to the Old Notes and the Exchange Notes.

| Issuer | Concordia Bus Nordic AB (publ), a Swedish limited liability company. | |

Notes Offered | €130 million principal amount of 9.125% Senior Secured Notes due August 1, 2009. | |

Guarantors | Each of our operating subsidiaries (currently Swebus AB, Swebus Busco AB, Swebus Express AB, Interbus AB, Ingeniør M.O. Schøyens Bilcentraler AS, Concordia Bus Finland Oy Ab, Swebus Fastigheter AB, Alpus AB, MalmFältens Omnibus AB and Enköping-Bålsta Fastighetsbolag AB, together, "Subsidiary Guarantors") and our direct Parent (together with the Subsidiary Guarantors, the "Guarantors") will guarantee the Notes on a senior basis (the "Subsidiary Guarantees" and the "Holding Guarantee," respectively, and together the "Note Guarantees"). Under the Indenture, other subsidiaries may also in the future be required to become Subsidiary Guarantors. Each future Subsidiary Guarantor will become a Guarantor upon execution of a supplemental indenture. For each future Guarantor, a supplemental listing prospectus will be filed with the Luxembourg Stock Exchange and notices will be published in accordance with the rules of the Luxembourg Stock Exchange and provided to the Trustee and the Collateral Agent. | |

Issue Price | 100%, plus accrued interest from January 22, 2004. | |

Maturity Date | August 1, 2009. | |

Sinking Fund | None. | |

Interest | Interest accrues at an annual rate of 9.125%. | |

Payment frequency: every six months on each February 1 and August 1. | ||

First payment August 1, 2004. | ||

Ranking of the Notes and Note Guarantees | The Notes will be our general obligations that rank senior in right of payment to our existing and future indebtedness that is expressly subordinated in right of payment to the Notes. The Notes will be at leastpari passu with all our existing and future unsecured liabilities that are not so subordinated and will effectively rank senior in right of payment to our unsecured liabilities with respect to the value of the Collateral securing the Notes and the Note Guarantees (subject to any priority rights for such unsecured liabilities pursuant to applicable law). As of July 9, 2004, there is no debt that ranks senior or effectively senior to the Exchange Notes. | |

8

The Note Guarantees will be general obligations of the respective Guarantors, ranking senior in right of payment to any existing and future indebtedness that is expressly subordinated in right of payment to such Note Guarantees. The Note Guarantees will be at leastpari passu with all existing and future unsecured liabilities of the respective Guarantors that are not so subordinated and will rank effectively senior in right of payment to the unsecured liabilities of those Guarantors with respect to the value of the Collateral securing the Note Guarantees (subject to any priority rights for such unsecured liabilities pursuant to applicable law). | ||

The Note Guarantees may be limited in amount and enforceability by applicable laws as described under "Risk Factors." | ||

Release of the Note Guarantees | A Note Guarantee given by a Guarantor may be released in certain circumstances, including: | |

(1) Upon repayment in full of the Notes; | ||

(2) upon a legal defeasance or covenant defeasance as described under the caption "Description of Notes—Defeasance;" | ||

(3) upon the designation by us of a Subsidiary Guarantor as an Unrestricted Subsidiary (for a definition of Unrestricted Subsidiary please see "Description of Notes—Certain Definitions—Unrestricted Subsidiary") in compliance with the terms of the Indenture; | ||

(4) upon the sale of a Subsidiary Guarantor in compliance with the terms of the Indenture (including the covenant described under the caption "Description of Notes—Certain Covenants—Limitation on sales of Assets and Subsidiary Stock") resulting in such Subsidiary Guarantor no longer being a Restricted Subsidiary, so long as (a) such Subsidiary Guarantor is simultaneously released from its obligations in respect of any of our other indebtedness or any indebtedness of any other Restricted Subsidiary and (b) the proceeds from such sale or disposition are used for the purposes permitted or required by the Indenture; or | ||

9

(5) upon release or discharge (other than as a result of the payment thereof), to the extent then existing, of the guarantee or security granted by a Subsidiary Guarantor that resulted in the issuance of the Subsidiary Guarantee pursuant to the covenant described under "Description of Notes—Certain Covenants—Limitations on Issuances of Guarantees of Indebtedness; Release of Guarantees." | ||

Security | The Notes will benefit from (i) a pledge by our direct Parent of the shares in Concordia, (ii) a pledge by Concordia of the shares of all of its operating subsidiaries, (iii) certain other security, including a pledge by Swebus Busco AB of all of the buses it owns (with a book value at February 29, 2004 of approximately SEK 1,268 million), which represents substantially all of the tangible fixed assets of Concordia and its operating subsidiaries, and a pledge by Swebus AB of a floating charge over its assets securing an amount up to SEK 100 million and (iv) a pledge by Concordia of certain secured intercompany loans (the "Guarantor Intercompany Loans") to Swebus AB and Swebus Busco AB, in the amounts of SEK 200 million and SEK 800 million, respectively, pursuant to which a second ranking security interest over certain assets of those Guarantors has been granted to Concordia. The Indenture in respect of the Notes will include certain intercreditor arrangements between Concordia and the Trustee with respect to the Collateral securing such intercompany loans. The enforceability of the Security and the amounts recoverable thereunder may be limited by applicable laws. See "Risk Factors—Risks Related to the Notes—Enforcement of the Note Guarantees and the Collateral may be subject to certain limitations and will require satisfaction of certain conditions." See "Description of Notes." | |

Optional Redemption | Before February 1, 2007, we may redeem up to 35% of the aggregate principal amount of the Notes with the proceeds of one or more public offerings of our or our ultimate parent company's (Concordia Bus BV's) equity at the redemption price listed under "Description of Notes—Optional Redemption." | |

On or after February 1, 2007, we may redeem some or all of the Notes at any time at the redemption prices listed under "Description of Notes—Optional Redemption." | ||

10

Repurchase at Option of Holders | If we experience specific kinds of changes of control, such as: a sale, conveyance or other disposition of all or substantially all of the assets of Concordia and its subsidiaries taken as a group, the liquidation or dissolution of any Parent Company, the Permitted Holders (as defined herein) hold less than 51% of the aggregate ordinary voting power of any Parent Company or Concordia prior to a Public Equity Offering (as defined herein) or after such a Public Equity Offering any person or group owns 35% of the aggregate ordinary voting power of any Parent Company or Concordia and their share exceeds that of the Permitted Holders, a majority of the members of the board of directors as of the Issue Date ceases to remain a majority, or upon merger, or if we sell certain assets without having met certain conditions, we must offer to repurchase the Notes at the prices listed under the headings "Change of Control Event" and "Asset Sales" in the section "Description of Notes." There is no other issue of debt of Concordia or its subsidiaries that would be redeemable or in default if a change of control were to occur. However, if a change of control were to occur, the lessor under our operating leases would have the right to terminate such operating leases. | |

Basic Covenants of Indenture | The Indenture governing the Notes appoints Deutsche Bank Trust Company Americas, as Trustee. The indenture, among other things, restricts our ability and the ability of our subsidiaries to: incur additional debt; pay or repurchase shares or junior debt; make investments; use assets as security in other transactions; enter into transactions with affiliates; issue or sell shares in subsidiaries; dispose of assets; or merge or consolidate with or into other companies. For more details, see "Description of Notes—Asset Sales" and "—Certain Covenants." | |

Regulatory Requirements | All regulatory requirements, including the requirements of U.S. federal securities laws and the regulatory requirements of Sweden, Norway and Finland, except for subsequent filings with the Central Bank of Sweden(Sw. Sveriges Riksbank)for payment statistics purposes, have been complied with and no further government approvals must be obtained in connection with the transaction. | |

Listing | The Notes are listed on the Luxembourg Stock Exchange. |

11

You should consider carefully all the information set forth in this prospectus and, in particular, should evaluate the specific factors involved with an investment in the Exchange Notes under the section "Risk Factors" beginning on page 17.

12

Summary Consolidated Historical Financial and Operating Data

Previously, Concordia Bus Nordic Holding AB was named Interbus Finans AB and was a wholly owned subsidiary of Concordia Bus Nordic AB (publ), which was wholly owned by Concordia Bus AB. In January 2004, a reorganization was performed whereby Concordia Bus Nordic AB (publ) transferred to Concordia Bus AB its 100% share ownership of Interbus Finans AB. Concordia Bus AB then transferred its shares in Concordia Bus Nordic AB (publ) to Interbus Finans AB. Interbus Finans AB was then renamed Concordia Bus Nordic Holding AB.

Such reorganization had the effect of creating a new holding company for Concordia Bus Nordic AB (publ) from one of its dormant subsidiaries. Concordia Bus Nordic Holding AB is a non-operating holding company that has no assets other than its shares in Concordia Bus Nordic AB (publ). Subsequent to the reorganization, the consolidated financial position, results of operations and cash flows of Concordia Bus Nordic AB (publ) are the same as that of Concordia Bus Nordic Holding AB. Since this was a reorganization of entities under common control, the consolidated financial statements contained in this prospectus are presented as if Concordia Bus Nordic Holding AB was in existence as the shareholder of Concordia Bus Nordic AB (publ) for all periods presented.

The following tables set forth summary consolidated financial data derived from audited financial statements of Concordia Bus Nordic Holding AB as of and for the years ended February 28, 2002, February 28, 2003 and February 29, 2004. This information should be read in conjunction with the sections "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the consolidated financial statements and the notes thereto included elsewhere in this prospectus.

The consolidated financial statements of Concordia Bus Nordic Holding AB have been prepared in accordance with Swedish GAAP, which differ in certain significant respects from US GAAP. The significant differences between Swedish GAAP and US GAAP are discussed in Note 32 to the consolidated financial statements of Concordia Bus Nordic Holding AB included elsewhere in this prospectus.

13

CONCORDIA BUS NORDIC HOLDING AB

SUMMARY CONSOLIDATED FINANCIAL AND OPERATING DATA

(in millions, except per share amounts and operating data)

| | As of and for the year ended | |||||||

|---|---|---|---|---|---|---|---|---|

| | February 28, | | ||||||

| | February 29, 2004 | |||||||

| | 2002 | 2003 | ||||||

| | SEK | SEK | SEK | |||||

| Statement of Operations | ||||||||

| Net revenue | 4,226 | 4,758 | 4,761 | |||||

| Operating expenses | (3,999 | ) | (4,505 | ) | (4,544 | ) | ||

| Gain (loss) on sale of fixed assets | 20 | (4 | ) | 6 | ||||

| Depreciation, amortization and impairments | (362 | ) | (372 | ) | (331 | ) | ||

| Operating loss | (115 | ) | (123 | ) | (108 | ) | ||

| Financial income and expense, net(a) | (104 | ) | (105 | ) | (146 | ) | ||

| Income taxes | 46 | 49 | 83 | |||||

| Net loss | (173 | ) | (179 | ) | (171 | ) | ||

| Net loss per share (in thousands of SEK) | (577 | ) | (596 | ) | (572 | ) | ||

| Balance Sheet Data | ||||||||

| Total fixed assets | 2,321 | 2,127 | 1,827 | |||||

| Of which: buses | 1,971 | 1,793 | 1,491 | |||||

| Total current assets | 1,035 | 757 | 1,024 | |||||

| Total shareholder's equity | 692 | 412 | 235 | |||||

| Total provisions | 269 | 198 | 146 | |||||

| Total non-current liabilities | 1,652 | 858 | 1,216 | |||||

| Total current liabilities | 743 | 1,416 | 1,254 | |||||

| Total debt | 1,691 | 1,497 | 1,589 | |||||

| Of which: Subordinated Shareholder Loan, net(b) | 631 | 494 | 368 | |||||

| Of which: senior debt(c) | 1,060 | 1,003 | 1,221 | |||||

| Cash Flow Data | ||||||||

| Cash flow from operations | 39 | (66 | ) | 24 | ||||

| Cash flow from investing activities | 274 | (136 | ) | (11 | ) | |||

| Cash flow from financing activities | (78 | ) | (95 | ) | 152 | |||

| Total capital expenditures | 43 | 216 | 32 | |||||

| Of which: capital expenditures on buses | 21 | 182 | 15 | |||||

| US GAAP: | ||||||||

| Net loss | (188 | ) | (168 | ) | (127 | ) | ||

| Basic and diluted loss per share (in thousands of SEK) | (626 | ) | (560 | ) | (425 | ) | ||

| Shareholder's equity, end of year | 1,231 | 952 | 826 | |||||

| Selected Operating Data | ||||||||

| Number of buses at year end: | ||||||||

| Owned and under financial leases | 2,866 | 2,793 | 2,591 | |||||

| Under operating leases | 784 | 1,156 | 1,317 | |||||

| Total buses operated at year end | 3,650 | 3,949 | 3,908 | |||||

| Average number of employees during the year | 6,924 | 7,484 | 7,512 | |||||

| Kilometers of service provided during the year (in thousands) | 249,169 | 270,404 | 257,672 | |||||

| Other Financial Data | ||||||||

| Operating lease rental expense | 230 | 350 | 388 | |||||

| Net present value of operating leases(d) | 748 | 1,003 | 957 | |||||

| Ratio of earnings to fixed charges under Swedish GAAP(e) | — | — | 0.0 | x | ||||

| Ratio of earnings to fixed charges under U.S. GAAP(e) | — | — | 0.3 | x | ||||

- (a)

- Includes financing costs and other financial charges and unrealized exchange rate gains and losses on loans denominated in foreign currency. The net foreign currency exchange gains and losses represented SEK 3 million, SEK 4 million and SEK (7) million for the years ended February 28, 2002 and 2003 and February 29, 2004, respectively.

(footnotes continued on following page)

14

- (b)

- The Subordinated Shareholder Loan, net, reflects the combination of the net balance of the initial subordinated loan of SEK 501 million and aggregate group contributions received by Concordia Bus AB (publ) from Concordia Bus Nordic Holding AB and its subsidiaries in exchange for tax losses from Concordia Bus AB (publ) and cash payments from Concordia Bus Nordic Holding AB to Concordia Bus AB (publ) relating to servicing the Parent Notes. For a description of the Subordinated Shareholder Loan, see "Description of Other Material Indebtedness—Subordinated Shareholder Loan from Our Indirect Parent."

- (c)

- Total senior debt includes long-term senior debt and the short-term portion of long-term senior debt including obligations under financial lease arrangements but excluding the Subordinated Shareholder Loan. Concordia Bus Nordic Holding AB believes that total senior debt is a useful supplement to total debt and other balance sheet data as it indicates the amount of debt Concordia Bus Nordic Holding AB owes that historically was rankedpari passu with the Notes.

- (d)

- Net present value of operating leases represents the net present value of future minimum lease payments for vehicles, real estate and certain other leased assets under operating lease arrangements.

- (e)

- Ratio of earnings to fixed charges is expressed as net income before taxation plus fixed charges (interest expenses, amortization of financing fees and the interest component of operating leases) divided by fixed charges. Earnings are inadequate to cover fixed charges by SEK 219 million under Swedish GAAP and by SEK 228 million under U.S. GAAP for the year ended February 28, 2002. For the year ended February 28, 2003 earnings were inadequate to cover fixed charges by SEK 228 million under Swedish GAAP and SEK 226 million under U.S. GAAP. See Exhibit 12.1 to this Form F-4.

15

RECONCILIATION OF CERTAIN FINANCIAL DATA TO ACCOUNTS OF CONCORDIA BUS AB

Concordia Bus AB (publ) is subject to certain provisions of the periodic reporting and other information requirements of the Exchange Act. The following table reconciles certain line items of the financial statements of Concordia Bus Nordic Holding AB with the corresponding line items of the accounts of Concordia Bus AB (publ). Amounts in each reconciling line item set forth below were recognized or incurred by Concordia Bus AB (publ) but were not recognized or incurred by Concordia Bus Nordic Holding AB.

| | As of and for the year ended | |||||||

|---|---|---|---|---|---|---|---|---|

| | February 28, | February 29, | ||||||

| | 2002 | 2003 | 2004 | |||||

| | SEK | SEK | SEK | |||||

Operating loss—Concordia Bus Nordic Holding AB | (115 | ) | (123 | ) | (108 | ) | ||

| Management charges, net | 3 | (15 | ) | (11 | ) | |||

| Professional fees to third parties(a) | (3 | ) | (2 | ) | (4 | ) | ||

| Goodwill amortization | (32 | ) | (32 | ) | (32 | ) | ||

| Operating loss—Concordia Bus AB | (147 | ) | (172 | ) | (155 | ) | ||

Financial income and expenses, net—Concordia Bus Nordic Holding AB | (104 | ) | (105 | ) | (146 | ) | ||

| Parent Notes interest | (108 | ) | (160 | ) | (161 | ) | ||

| Financial income in Concordia Bus AB | 5 | — | 1 | |||||

| Amortization of deferred financing costs | (7 | ) | (10 | ) | (10 | ) | ||

| Foreign exchange gains and losses on Parent Notes, net | — | (6 | ) | (15 | ) | |||

| Subordinated Shareholder Loan interest elimination, net | (3 | ) | 26 | 23 | ||||

| Financial interest income and expenses net—Concordia Bus AB | (217 | ) | (255 | ) | (308 | ) | ||

Total senior debt—Concordia Bus Nordic Holding AB(b) | 1,060 | 1,003 | 1,221 | |||||

| Parent Notes | 1,454 | 1,460 | 1,475 | |||||

| Total debt—Concordia Bus AB | 2,514 | 2,463 | 2,696 | |||||

Cash and bank balances—Concordia Bus Nordic Holding AB | 480 | 180 | 346 | |||||

| Cash and balances in Concordia Bus AB | — | 19 | — | |||||

| Utilized overdraft facility in Concordia Bus AB | (58 | ) | — | — | ||||

| Cash and bank balances—Concordia Bus AB | 422 | 199 | 346 | |||||

- (a)

- Third parties are entities not included in the Concordia Bus BV group of companies (as depicted under the caption "Summary—Corporate Structure").

- (b)

- Total senior debt includes long-term senior debt and the short-term portion of long term senior debt including obligations under financial lease arrangements but excluding the Subordinated Shareholder Loan.

16

Prior to investing in the Notes, prospective investors should consider the following risk factors, together with the other information set forth in this prospectus. This section of the prospectus describes important risks that may cause actual results or performance to differ materially from the results or performance described in the forward-looking statements throughout this prospectus.

Risks Related to the Notes

Concordia is a holding company with no revenue generating operations of its own.

Concordia is a holding company. Our principal asset is our investment in our subsidiaries. We conduct no business or operations except through direct and indirect subsidiaries. Our ability to service our indebtedness, including the Notes, is entirely dependent upon the receipt of funds from our subsidiaries by means of dividends, interest, intercompany loans or otherwise. The ability of our subsidiaries to make those funds available to us is subject to, among other things, applicable corporate and other laws and restrictions contained in agreements to which such subsidiaries may be subject. We cannot assure you that our subsidiaries will be in a position to make funds available to us. Although the indenture related to the Notes limits the ability of such subsidiaries to enter into consensual restrictions on their ability to pay dividends and make other payments to us, such limitations are subject to a number of significant qualifications. See the section "Description of Notes." Also, according to Swedish law, our subsidiaries may only pay dividends to us to the extent that they have distributable earnings. All of our subsidiaries, except for Concordia Bus Finland, have historically had distributable earnings. This could have a material adverse effect on our financial condition.

We expect that our direct Parent and our indirect Parent will seek to cause us to make funds available for interest payments under the Parent Notes.

We are a wholly-owned indirect subsidiary of our indirect Parent, which is required by the terms of the Parent Notes to make semi-annual interest payments on the Parent Notes, which bear interest at 11%. Currently, the total aggregate amount of Parent Notes outstanding is €160,000,000. Annual interest costs on the Parent Notes currently equal €17,600,000. A portion of the net proceeds received from the issuance of the Parent Notes was loaned to us by our indirect Parent pursuant to the Subordinated Shareholder Loan, which is a subordinated intercompany loan and which bears interest at a rate of 11% and matures on February 14, 2010. The current outstanding balance of the Subordinated Shareholder Loan is SEK 368 million. Payments made by us in respect of the Subordinated Shareholder Loan will not be sufficient to allow our indirect Parent to make interest payments on the Parent Notes. In addition to the payments we make in respect of the Subordinated Shareholder Loan, therefore, we expect that our direct Parent, which is entirely dependent upon the receipt of funds from us and our subsidiaries and whose interests may conflict with holders of the Notes, will seek for us to make funds available to it so that our indirect Parent may make interest payments on the Parent Notes. The terms of the Notes will permit us to make distributions to our Parents, whether in the form of dividends, distributions, advances or otherwise for the purpose of making these semi-annual interest payments. We intend to make such distributions to our Parents via dividends, by making interest payments on the Subordinated Shareholder Loan, or by repaying the principal on the Subordinated Shareholder Loan. However, according to Swedish law, we can only pay dividends to our Parents to the extent that we have distributable earnings. This could have a material adverse effect on our financial condition.

17

To service our debt, we will require a significant amount of cash. Our ability to generate cash depends on many factors beyond our control.

Our ability to make payments on and to refinance our debt, including the Notes, will depend on our subsidiaries' ability to generate cash in the future and our subsidiaries' ability to generate distributable earnings or other funds available for that purpose. We currently require €11,900,000 to service our debt on an annual basis and are not required to make any payments of principal prior to maturity. This, to a certain extent, is subject to general economic, financial, competitive and other factors that are beyond our control.

Based on our current level of operations and anticipated cost savings and operating improvements, we believe our cash flow from operations and available cash will be adequate to meet our future liquidity and debt service needs. However, we cannot assure you that (1) our business will generate sufficient cash flow from operations, particularly if our bus fleet grows more rapidly than anticipated, with the associated increase in operating lease costs, (2) currently anticipated cost savings, fleet management strategies and operating improvements will be realized on schedule, or at all or (3) future borrowings will be available to us in an amount sufficient to enable us to make required payments on, and redemptions of, our debt, including these Notes, or to fund our other liquidity needs.

We sustained operating losses of SEK 108 million for the year ended February 29, 2004, SEK 123 million for the year ended February 28, 2003 and SEK 115 million for the year ended February 28, 2002. We sustained net losses of SEK 171 million for the year ended February 29, 2004, SEK 179 million for the year ended February 28, 2003 and SEK 173 million for the year ended February 28, 2002,

We may need to refinance all or a portion of our and our subsidiaries' debt, including the Notes, on or before maturity. We may not be able to refinance any of such debt, including debt under the Notes, on commercially reasonable terms or at all, which could have a material adverse effect on our business.

Further, our indirect Parent's ability to make payments on the Parent Notes is currently wholly dependent upon our and our subsidiaries' ability to make payments in connection with the Subordinated Shareholder Loan, as well as our and our subsidiaries' ability to generate distributable earnings for that purpose. Although we believe that, after making payments permitted in respect of the Subordinated Shareholder Loan, we will have available distributable earnings to make payments in respect of the Parent Notes, we cannot assure you we will have sufficient distributable earnings to do so. Any failure to provide funds to our direct Parent sufficient to make interest payments on the Parent Notes could result in a default under the Parent Notes. A default on the Parent Notes could result in an insolvency of our indirect Parent, which would accelerate payment on the Notes in accordance with the terms of the indenture. Even if our indirect Parent did not suffer an insolvency, such default could limit our ability to obtain funding, which could have a material adverse effect on our business.

Our substantial leverage could adversely affect our ability to run our business.

We have now and will continue to have a significant amount of debt. As of February 29, 2004, our total consolidated debt was approximately SEK 1,589 million, of which total consolidated senior debt was approximately SEK 1,221 million and our shareholders equity was SEK 235 million. We also have substantial liabilities in the form of our operating lease payments. The present value of future lease payments for our operating lease liability for February 29, 2004 was SEK 957 million, SEK 1,003 million for the year ended February 28, 2003 and SEK 748 million for the year ended February 28, 2002.

18

In addition, we expect that our direct Parent and our indirect Parent will seek to cause us to make funds available to them, in excess of our obligations in respect of the Subordinated Shareholder Loan, in respect of our indirect Parent's interest payment obligations under the Parent Notes. See "Risk Factors—Risks Related to the Notes—Concordia is a holding company with no revenue generating operations of its own. We expect that our direct Parent and our indirect Parent will seek to cause us to make funds available for interest payments under the Parent Notes."

Our and our subsidiaries' substantial debt, and such need to provide funds to our direct Parent, could have important consequences for you. For example, it could among other things:

- •

- make it more difficult for us to satisfy our obligations under the Notes;

- •

- limit our ability to fund our working capital, capital expenditures and general corporate requirements;

- •

- limit our ability to borrow additional funds;

- •

- limit our ability to enter into operating leases for buses;

- •

- require us to dedicate a substantial portion of our cash flow from operations to payments on our debt, thereby reducing the funds available to us for other purposes;

- •

- make us more vulnerable to economic downturns; and

- •

- reduce our flexibility to respond to changing business and economic conditions.

In addition, we and our subsidiaries may be able to incur substantial additional debt in the future. The terms of the indenture restrict but do not fully prohibit us and our subsidiaries from borrowing after completion of this offering, and some of those borrowings may be secured. To the extent one or more of the Note Guarantees may be limited in value, or unenforceable, as a result of applicable laws, future borrowings by Subsidiary Guarantors will be effectively senior in right of payment to the Notes. Further, if new debt is added to our and our subsidiaries' current debt levels, the related risks that we and they now face could intensify.

Any of the foregoing could have a material adverse effect on our business, our ability to make payments under the Notes and our ability to continue presenting our financial statements under the assumption that we are a going concern.

The terms of our indebtedness restrict our corporate activities.

The Indenture under which the Notes will be issued, and the indenture under which the Parent Notes were issued, restrict, and in some cases prohibit, among other things, our and our subsidiaries' ability to:

- •

- incur additional debt;

- •

- make prepayments of certain debt;

- •

- pay dividends;

- •

- make investments;

- •

- engage in transactions with affiliates;

- •

- issue capital stock;

- •

- create liens;

- •

- sell assets; and

- •

- engage in mergers and consolidations.

19

A failure to comply with these covenants could result in a default under the Notes, which in turn could result in an event of default under our other indebtedness, or an event of default under the Parent Notes.

We may not have the ability to raise the funds necessary to finance the change of control offer or asset sale offers required by the indenture.

Upon the occurrence of specific kinds of change of control events, we will be required to offer to repurchase all outstanding Notes. Furthermore, a change of control may result in a default under and possibly acceleration of other senior debt we may incur. Also, if we or our subsidiaries sell assets we may, subject to conditions, be required to offer to repurchase Notes. It is possible, however, that we will not have sufficient funds at the time we are required to make such an offer to make the required repurchase of Notes. See the heading "Repurchase at the Option of Holders" in the section "Description of Notes."

Enforcement of the Note Guarantees and the Collateral may be subject to certain limitations and will require satisfaction of certain conditions.

Generally, claims of creditors of a subsidiary will have priority with respect to the assets of such subsidiary over the claims of creditors of its parent company. However, subject to the limitations and qualifications described below, holders of the Notes will have direct claims against the Guarantors under the Note Guarantees. Guarantors guaranteeing the Notes at closing include:

| Name | Jurisdiction of Incorporation | |

|---|---|---|

| Alpus AB | Sweden | |

| Concordia Bus Nordic Holding AB | Sweden | |

| Enköping-Bålsta Fastighetsbolag AB | Sweden | |

| Interbus AB | Sweden | |

| Malmfältens Omnibus AB | Sweden | |

| Swebus AB | Sweden | |

| Swebus Busco AB | Sweden | |

| Swebus Express AB | Sweden | |

| Swebus Fastigheter AB | Sweden | |

| Ingeniør M.O. Schøyens Bilcentraler AS | Norway | |

| Concordia Bus Finland Oy Ab | Finland |

Enforcement of the Note Guarantees and Collateral may be limited in certain circumstances. Any such limitation would, if applicable, effectively subordinate the Notes in right of payment to all indebtedness of the relevant Guarantor then existing irrespective of the granting of the Note Guarantee.

Swedish Subsidiary Guarantees and Collateral.

Enforcement of the Note Guarantees and Collateral may, in whole or in part, be limited to the extent that the undertaking by each respective subsidiary is deemed to be in conflict with the corporate interest of the respective subsidiary. The corporate interest shall be determined on the basis of whether the undertaking was made for business reasons so as to involve corporate benefit for the subsidiary and whether the guaranteed party is solvent for repayment of the secured amount at the time of providing the security. The absence of business reasons and corporate benefit would have the effect that the performance of the undertaking, or part thereof, would violate the Swedish Companies Act to the extent that it would result in a payment exceeding the distributable profit of the respective subsidiary at the time of providing the security. Upon such violation, the Note

20

Guarantees and Collateral would be invalid and any payments made thereunder would be subject to recovery at least to the extent they violate the above mentioned rules on corporate interest.

Finnish Subsidiary Guarantee and Collateral.

The granting of guarantees and security is restricted under the Finnish Companies Act. Enforcement of the Note Guarantees and Collateral issued or granted by Concordia Finland may, in whole or in part, be limited to the extent that the undertaking by such subsidiary is deemed to be in conflict with the limitations set out in the Finnish Companies Act, including the corporate interest of Concordia Finland. The determination shall be made,inter alia, on the basis of whether the undertaking was made for reasons so as to involve corporate benefit for (and be justified with grounds relating to the operations of) Concordia Finland and whether the guaranteed party is solvent for repayment of the guaranteed amount during the term of the undertaking. The absence of business reasons and corporate benefit would have the effect that the performance of the undertaking, or a part thereof, would violate the Finnish Companies Act. Any such violation would render the Note Guarantees and Collateral invalid and any payments made thereunder would be subject to recovery at least to the extent that they violate the Finnish Companies Act.

Norwegian Subsidiary Guarantee and Collateral.

The issuance of the Subsidiary Guarantee and the granting of the relevant security by the Norwegian subsidiary may be invalid under Norwegian law if such issuance and granting are not motivated by a legitimate business reason or corporate benefit for that subsidiary. In determining the sufficiency of the business reason or corporate benefit, a Norwegian court will consider whether or not the granting of the guarantee or security supported the object and the operations of that subsidiary. We believe sufficient corporate benefit exists with respect to the Note Guarantee and Collateral granted by the Norwegian subsidiary. However, there can be no certainty as to the sufficiency of the corporate benefit.

If we or our Swedish, Norwegian or Finnish operating subsidiaries incur substantial operating losses, we or they may be subject to liquidation under our respective national regimes.

The respective companies acts and insolvency and reorganization laws of Sweden, Norway and Finland apply to Concordia and its operating subsidiaries. Under these regimes, if losses reduce the equity of these entities or any of their subsidiaries (including Concordia itself on a stand-alone rather than a consolidated basis) to an amount less than 50% of its registered share capital, or (in Norway only) if the equity becomes inadequate compared to the risks and the size of its business, the directors of such entity would be obligated by law to convene a general shareholders meeting to resolve to liquidate such entity unless the directors were able to balance the amount of such equity and the registered share capital (in Sweden, within eight months of such meeting, and in Finland, within twelve months of such meeting) by (1) increasing the equity in an amount sufficient to achieve such balance and, in the Norwegian scheme, to ensure that its equity becomes adequate compared to the risks and the size of its business, or (2) reducing the share capital to pay off losses in an amount sufficient to achieve such balance. Due to these requirements, Concordia Finland converted portions of its shareholder loan from Concordia into a subordinated loan in July 2001 and in February 2003. In addition, if we are not successful in our cost-cutting initiatives and our losses continue, this may cause our equity to decrease sufficiently to require an equity increase or share capital reduction as described above. If we are unable to procure such an equity increase or share capital reduction, it would have an adverse effect on our ability to continue presenting our financial statements under the assumption that we are a going concern. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Operating Results—Critical Accounting Policies—Going-concern matters."

21

Your rights as a creditor may not be as strong under Swedish, Norwegian or Finnish insolvency laws as under other insolvency laws.

Under Swedish, Norwegian or Finnish law, there is no consolidation of bankruptcies of the assets and liabilities of a group of companies. Each individual company would thus be treated separately by a bankruptcy administrator appointed by the local district court. The assets of our subsidiaries would first be used to satisfy the debts of each respective subsidiary and only the remaining surplus (if any) of a subsidiary would benefit our creditors. As a result, your ability to protect your interests as a creditor of a parent of such subsidiary may not be as strong under Swedish, Norwegian or Finnish law as it would be under the laws of other countries.

Sweden

Under Swedish law, secured creditors enjoy a privileged position in bankruptcy and similar proceedings. Such provisions afford debtors and unsecured creditors only limited protection relative to the claims of secured creditors.

The security in the floating charges pledged by Swebus has a first priority interest in all tangible and intangible assets except for (i) real estate property and (ii) cash and bank deposits, unless the property is otherwise pledged, but after our debt to creditors with rights of set-off. However, after January 1, 2005, the pledged floating charges will attach to all of the relevant pledgor's assets (including real estate property, cash and bank deposits) due to amendments in Swedish insolvency law. According to the new rules, the floating charge will carry a general right of priority, which means that it may be enforced only in the event of bankruptcy or insolvent liquidation. Furthermore, the right of priority that will attach to the floating charge will be enforceable only against 55% of the value of the property remaining after distribution has been made to creditors with specific rights of priority.

The business reorganization laws of Sweden apply to Concordia. Under official business reorganization, creditors may under certain circumstances be forced to approve the terms of the business reorganization. During a business reorganization, Concordia will not be allowed to fulfill any obligations incurred before the reorganization without the permission of the administrator appointed by the local district court.

Council Regulation (EC) No 1346/2000 of 29 May 2000 on insolvency proceedings is applicable in Sweden. In certain circumstances, that regulation will govern determinations as to the appropriate jurisdiction and competent authority within the European Union with respect to insolvency proceedings.

Norway

Noteholders' rights with respect to the Note Guarantees and pledges of security from SBC may be compromised in an insolvency proceeding with respect to SBC.

The Norwegian Bankruptcy Act 1984 sets out two main procedures that can be followed in respect of a company being illiquid or insolvent: debt settlement proceedings (voluntary or compulsory) and bankruptcy. Only the subject company can apply for debt settlement proceedings.

The purpose of debt settlement proceedings is to give a debtor who is illiquid the opportunity to negotiate with its creditors for a voluntary composition or a compulsory composition under the protection of the courts. In such a proceeding, the court will appoint a debt settlement committee composed preferentially of creditors' representatives with a lawyer as chairman. If a voluntary debt settlement is opposed by any of the creditors, the alternatives are either compulsory debt settlement proceedings or bankruptcy. While in debt settlement proceedings a debtor is restricted with respect to carrying on its business but remains in charge of its business under the supervision

22

of the committee. As a general rule, during the first three months of debt settlement proceedings, a bankruptcy petition cannot be filed.

During the first six months of the debt settlement or bankruptcy proceedings, security may only be enforced with the consent of the debt settlement committee or the bankruptcy trustee (as the case may be).

In certain circumstances, liens by operation of law have priority ranking ahead of contractually agreed first priority pledges.

Finland

Under Finnish insolvency law, secured creditors enjoy a privileged position in bankruptcy and similar proceedings. Such provisions afford debtors and unsecured creditors only limited protection relative to the claims of secured creditors. In addition to the priority given to secured debts under Finnish insolvency law, in certain circumstances, liens by operation of law have priority ranking ahead of contractually agreed first priority pledges.

Pledges over specific assets and certain liens by operation of law have priority ranking ahead of pledged floating charges. Furthermore, in the event of bankruptcy proceedings, the proceeds remaining from the sale of assets subject to the floating charge, after payment to creditors with higher priority ranking, would be divided, with those remaining proceeds being paid (1) 50% to creditors whose claims are secured by the floating charge and (2) 50% to remaining creditors (including creditors secured by floating charge to the extent their claims are not satisfied pursuant to clause (1) above) pro rata in relation to the respective amounts of their claims.

The business reorganization laws of Finland restrict the actions that are allowed to be taken by either debtors or creditors during business reorganization proceedings.

Council Regulation (EC) No 1346/2000 of 29 May 2000 on insolvency proceedings is applicable in Finland. In certain circumstances, that regulation will govern determinations as to the appropriate jurisdiction and competent authority within the European Union with respect to insolvency proceedings.

Fraudulent conveyance laws of Sweden, Norway and Finland may protect our creditors to your disadvantage.

Sweden and Finland

Under Swedish and Finnish law relating to fraudulent conveyance, it is possible that other creditors may claim that payments to you under the Notes or the Note Guarantees or any recoveries with respect to the pledged Collateral should be voided as fraudulent conveyances.

Under Swedish and Finnish law, in the case of bankruptcy or company reorganization proceedings affecting us, the payments to you under the Notes or the Note Guarantees (of principal or interest or otherwise), which are made less than three months (or two years if effected to a related party) before the application for bankruptcy or company reorganization proceedings is filed with the competent court may, in certain situations, be recovered if the payment is carried out:

- •

- using unusual means of payment;

- •

- prematurely; or

- •

- in an amount which, in light of a debtor's financial position, is material.

Payments which are deemed to be customary are, however, permissible.

23

Furthermore, the security granted in respect of the Notes or the Note Guarantees, if granted less than three months (or two years, if effected to a related party) before the application for bankruptcy or company reorganization proceedings were filed with a competent court, may be recovered if the security was not a condition under such indebtedness or was not pledged without delay after our accrual of such indebtedness. Nonetheless, security provided that is deemed to be customary is permissible.

A Swedish or Finnish court could also determine that a fraudulent conveyance has taken place under the general provision on recovery whereby a payment to you under the Notes or the Note Guarantees or the pledging of the Collateral could be revoked if an agreement, transaction or other act, such as the issuance of the Notes or the Note Guarantees or the pledging of the Collateral is held to favor a creditor in an undue manner to the detriment of another creditor or to transfer property out of the reach of the creditors or to increase the debt to the detriment of the creditors, provided that:

- •

- the debtor was insolvent at the time the agreement, transaction or other act was concluded or the debtor became insolvent as a result of the transaction, by itself or combined with other circumstances; and

- •

- the other party knew or should have known of the insolvency or over-indebtedness or of the impact of such payment on the debtor's financing state as well as of the circumstances due to which the payment under the Notes or the Note Guarantees or the pledging of the Collateral was undue.

However, under Swedish and Finnish law, if such an agreement, transaction or other act is concluded earlier than five years before the application for bankruptcy or company reorganization was filed, the payment to you under the Notes or the Note Guarantees or the pledging of the Collateral could be revoked only if a party to the agreement, transaction or other act was someone related to the bankrupt or reorganized party, such as a group company.

Furthermore, under Finnish law, a gift may be recovered by the estate if it has been made within one year prior to the due date. A gift that has been given before this, but within three years prior to the due date may be recovered if it has been given to a person within the debtor's sphere of interest and it is not proven that the debtor was not excessively indebted nor became excessively indebted as a result of the gift. A transfer resulting from a sale, trade or any other agreement can likewise be recovered if it can be shown that the agreement was unbalanced to the extent that the transfer should be regarded as a gift.

Under Swedish law, a gift may be recovered by the estate if it has been made within six months prior to the date of application for bankruptcy or reorganization. A gift that has been given before this, but within one year prior to the date of application (or three years if effected to a related party) may be recovered if it is not proven that the debtor was not excessively indebted nor became excessively indebted as a result of the gift. A transfer resulting from a sale, trade or any other agreement can likewise be recovered if it can be shown that the agreement was unbalanced to the extent that the transfer should be regarded as a gift.

In addition, if any of our major subsidiaries in Sweden or Finland were to enter bankruptcy proceedings, a court in that jurisdiction could prevent our subsidiaries from making payments to us, thereby possibly impairing our ability to pay the amounts due under the Notes.

Norway

Under Norwegian insolvency laws, the granting of security interests and unusual payments can be voided if undertaken during the three-month period prior to the commencement of insolvency proceedings. There are also other preference provisions such as fraudulent conveyance rules that

24