Filed by: Gold Kist Holdings Inc.

Pursuant to Rule 425 under the Securities Act of 1933

Commission File No. 333-116066

Subject Company: Gold Kist Inc.

Commission File No.: 002-62681

Date: June 1, 2004

A copy of a slide presentation to be used in meetings with certain members of Gold Kist Inc. is being filed as Appendix A to this filing. Appendix A is incorporated herein by reference.

The proposed conversion will be submitted to members of Gold Kist for their consideration, and Gold Kist Holdings Inc. has filed with the Securities and Exchange Commission a registration statement on Form S-4 relating to the conversion. Members of Gold Kist are urged to read the registration statement and the accompanying documents when they become available. These documents contain important information about the conversion and will be available for free on the SEC web site at www.sec.gov.

Appendix A

Appendix A

Welcome Gold Kist Members

The material in this presentation contains “forward-looking statements” as defined in Section 27A of the Securities Act and Section 21E of the Securities Exchange Act, including those statements regarding the amounts of patronage earnings to be distributed to Gold Kist’s members for fiscal periods not yet completed, the proposed conversion, initial public offering and use of proceeds therefrom and the benefits of the conversion, including our ability to grow, access other financial resources, strengthen our financial position and build stockholder value. You should read these statements carefully because they discuss future expectations, contain projections or our results of operations or financial condition and/or state other forward-looking information. These statements may also involve risks and uncertainties that could cause our actual results of operations or financial condition to materially differ from our expectations in this presentation. For example, although approved by our Board of Directors, the conversion is required to be approved by the members of Gold Kist and is subject to the satisfaction of other conditions, including the completion of the initial public offering by Gold Kist Holdings Inc. Other risks to our completion of the conversion include market conditions for corporate equity securities generally, for the securities of poultry and other protein and agribusiness companies and for the common stock being offered by Gold Kist Holdings, in particular. In addition, in its sole discretion, the Board of Directors may amend the plan of conversion or terminate or withdraw the plan of conversion or the initial public offering at any time. There can be no assurances that the conversion and the initial public offering will be completed. When reviewing and considering this presentation, you should also keep in mind the risk factors and other cautionary statements contained in our presentations made with the Securities and Exchange Commission.

Any forward-looking statements in this presentation are based on certain assumptions and analyses made by us in light of our experience and perception of historical trends, current conditions, expected future developments and other factors that we believe are appropriate under the current circumstances. However, events may occur in the future that we are unable to accurately predict, or over which we have no control. Forward-looking statements are not a guarantee of future performance and actual results or developments may differ materially from expectations. You are therefore cautioned not to place undue reliance on such forward-looking statements. We do not intend to update any forward-looking statements contained in this presentation.

The proposed conversion will be submitted to members of Gold Kist for their consideration, and Gold Kist Holdings Inc. has filed with the Securities and Exchange Commission a registration statement on Form S-4 relating to the conversion. You are urged to read the registration

statement and the accompanying documents when they become available. These documents contain important information about the conversion and will be available for free on the SEC web site at www.sec.gov. A finalized version of this document will be provided to you later this summer.

Since 1998, our goals have been to:

Focus on our core business - Poultry

Build a financially strong company

Find a way to return equity to members

Your Board unanimously agreed to present to members this proposal to:

Convert from a Cooperative Association to a For-Profit Corporation

Conduct an Initial Public Offering

The proposal allows Gold Kist to:

Be a financially stronger and more flexible company

Create liquidity for equity holders

Window of Opportunity

June 1, 2004

Registration Statement Filed with Securities and Exchange Commission www.sec.gov

Proceeds from the offering will be used to:

Pay cash to members

Pay down part of the debt

Address other corporate needs

(such as expand further processing, new equipment and facilities)

What will it mean to you?

What will it mean to you?

Cash and

Stock in the New Gold Kist

The allocation of value in the New Gold Kist will be based on:

Your Notified Equity Position up to the date of conversion

Your business with Gold Kist during last 5 fiscal years

The market value of the company

Each Current Member Will Receive in Cash and in new Gold Kist stock

The Full Value of Notified Equity + Premium

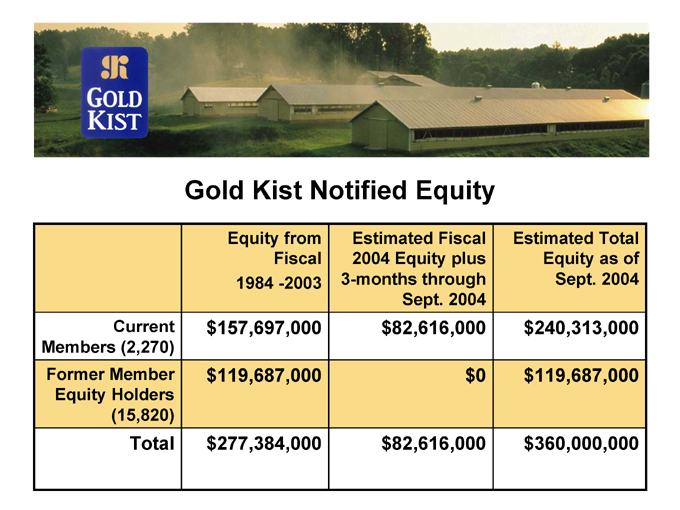

Gold Kist Notified Equity

Equity from Fiscal 1984 -2003 Estimated Fiscal 2004 Equity plus 3-months through Sept. 2004 Estimated Total Equity as of Sept. 2004

Current Members (2,270) $157,697,000 $82,616,000 $240,313,000

Former Member Equity Holders (15,820) $119,687,000 $0 $119,687,000

Total $277,384,000 $82,616,000 $360,000,000

We expect the value of Gold Kist as a for-profit company to exceed the value of notified equity.

This additional value will create a Premium, which as directed by the Gold Kist Bylaws will be distributed to current members in addition to Notified Equity.

The value of this premium will depend on a number of factors.

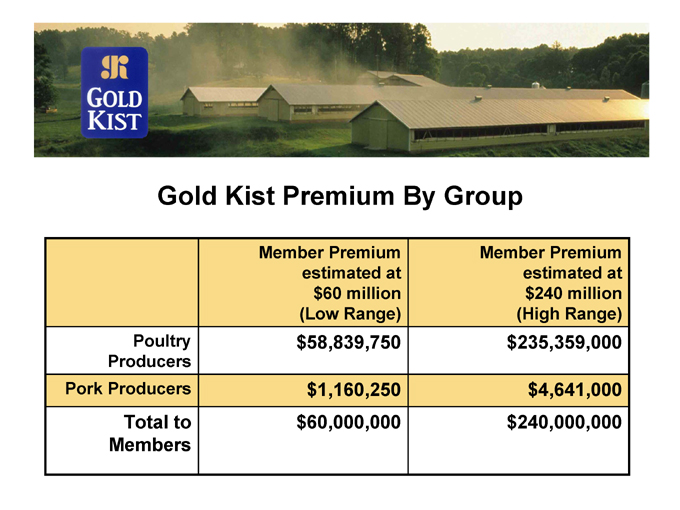

Gold Kist Premium By Group

Member Premium estimated at $60 million (Low Range) Member Premium estimated at $240 million (High Range)

Poultry Producers $58,839,750 $235,359,000

Pork Producers $1,160,250 $4,641,000

Total to Members $60,000,000 $240,000,000

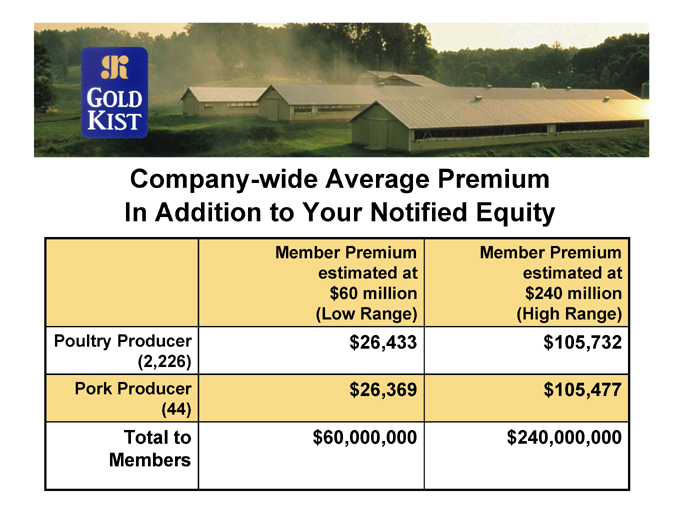

Company-wide Average Premium In Addition to Your Notified Equity

Member Premium estimated at $60 million (Low Range) Member Premium estimated at $240 million (High Range)

Poultry Producer (2,226) $26,433 $105,732

Pork Producer (44) $26,369 $105,477

Total to Members $60,000,000 $240,000,000

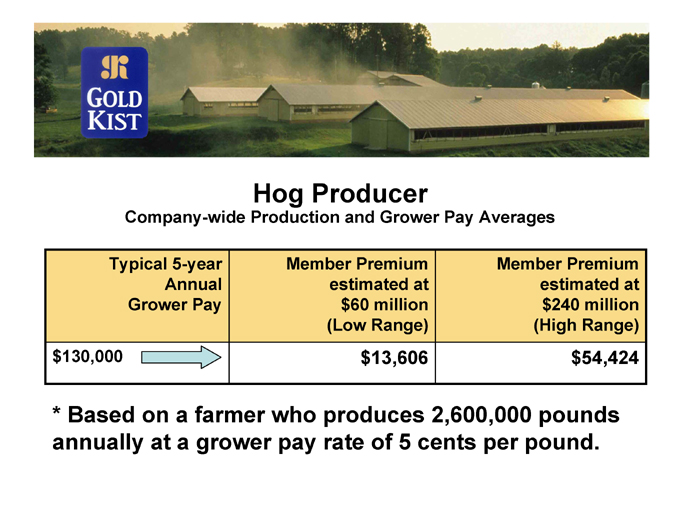

Hog Producer

Company-wide Production and Grower Pay Averages

Typical 5-year Annual Grower Pay Member Premium estimated at $60 million (Low Range) Member Premium estimated at $240 million (High Range)

$130,000 $13,606 $54,424

* Based on a farmer who produces 2,600,000 pounds annually at a grower pay rate of 5 cents per pound.

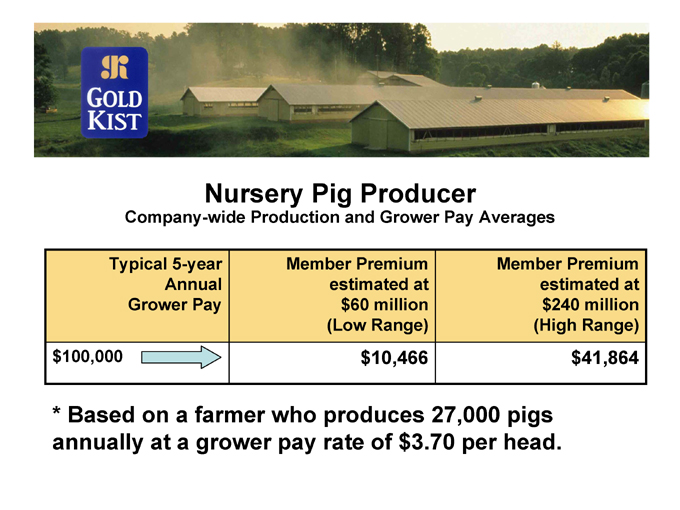

Nursery Pig Producer

Company-wide Production and Grower Pay Averages

Typical 5-year Annual Grower Pay Member Premium estimated at $60 million (Low Range) Member Premium estimated at $240 million (High Range)

$100,000 $10,466 $41,864

* Based on a farmer who produces 27,000 pigs annually at a grower pay rate of $3.70 per head.

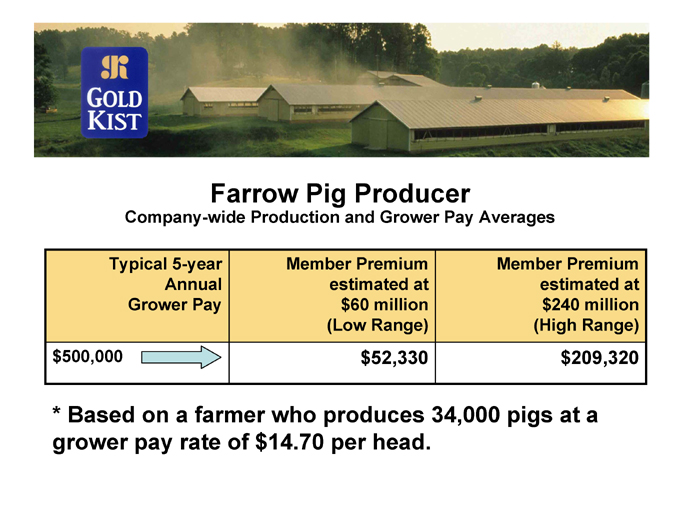

Farrow Pig Producer

Company-wide Production and Grower Pay Averages

Typical 5-year Annual Grower Pay Member Premium estimated at $60 million (Low Range) Member Premium estimated at $240 million (High Range)

$500,000 $52,330 $209,320

* Based on a farmer who produces 34,000 pigs at a grower pay rate of $14.70 per head.

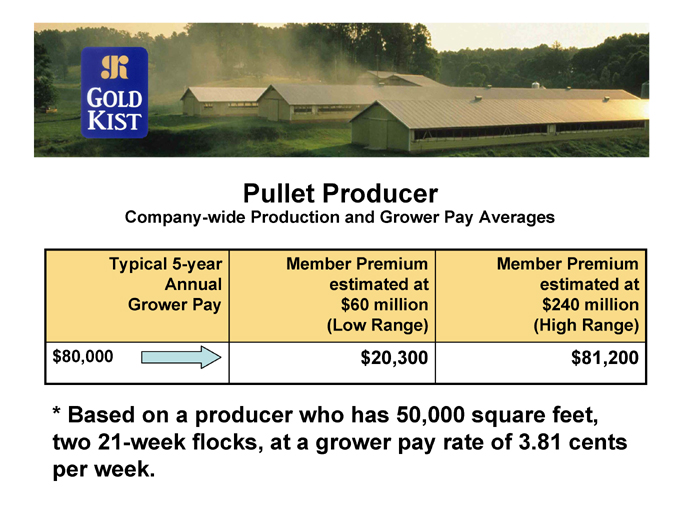

Pullet Producer

Company-wide Production and Grower Pay Averages

Typical 5-year Annual Grower Pay Member Premium estimated at $60 million (Low Range) Member Premium estimated at $240 million (High Range)

$80,000 $20,300 $81,200

* Based on a producer who has 50,000 square feet, two 21-week flocks, at a grower pay rate of 3.81 cents per week.

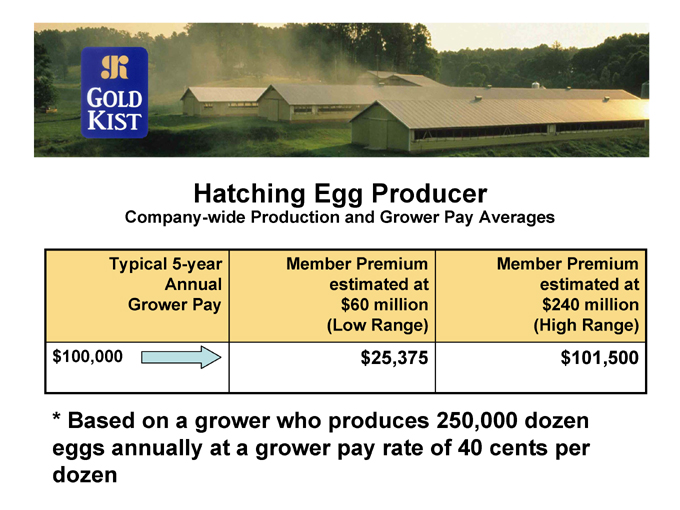

Hatching Egg Producer

Company-wide Production and Grower Pay Averages

Typical 5-year Annual Grower Pay Member Premium estimated at $60 million (Low Range) Member Premium estimated at $240 million (High Range)

$100,000 $25,375 $101,500

* Based on a grower who produces 250,000 dozen eggs annually at a grower pay rate of 40 cents per dozen

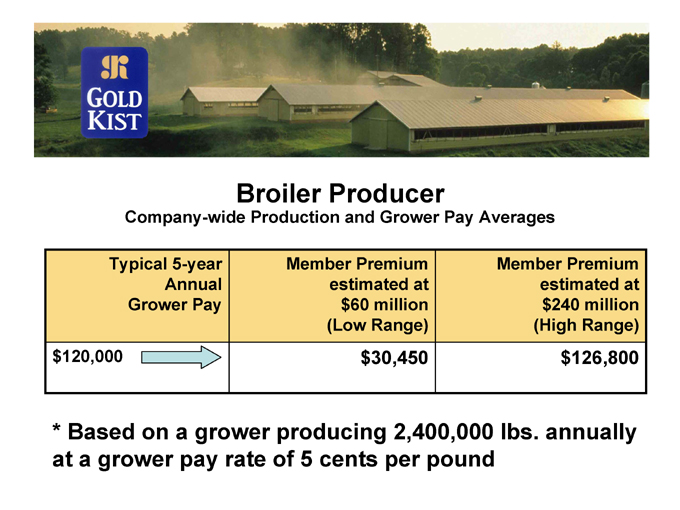

Broiler Producer

Company-wide Production and Grower Pay Averages

Typical 5-year Annual Grower Pay Member Premium estimated at $60 million (Low Range) Member Premium estimated at $240 million (High Range)

$120,000 $30,450 $126,800

* Based on a grower producing 2,400,000 lbs. annually at a grower pay rate of 5 cents per pound

Summary

Each Current Member Will Receive in Cash and in new Gold Kist stock

The Full Value of Notifed Equity + Premium

August 2004

You will receive a packet containing:

Disclosure statement-prospectus

A statement of notified equity including notified equity allocated for fiscal 2004

Your 2004 patronage refund

A ballot

A form on which you may elect to receive some portion in cash

Quiet Period

Gold Kist Information Line 770-393-5359

It’s Your Choice.

QUESTIONS?

Thank You for Attending.

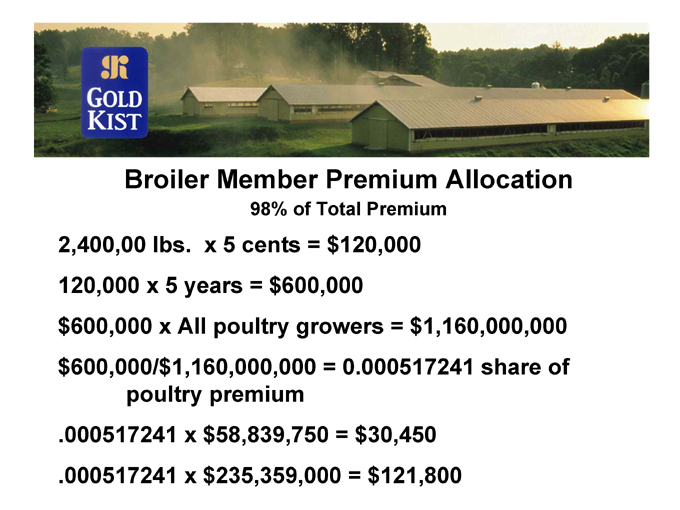

Broiler Member Premium Allocation

98% of Total Premium

2,400,00 lbs. x 5 cents = $120,000 120,000 x 5 years = $600,000 $600,000 x All poultry growers = $1,160,000,000 $600,000/$1,160,000,000 = 0.000517241 share of poultry premium .000517241 x $58,839,750 = $30,450 .000517241 x $235,359,000 = $121,800

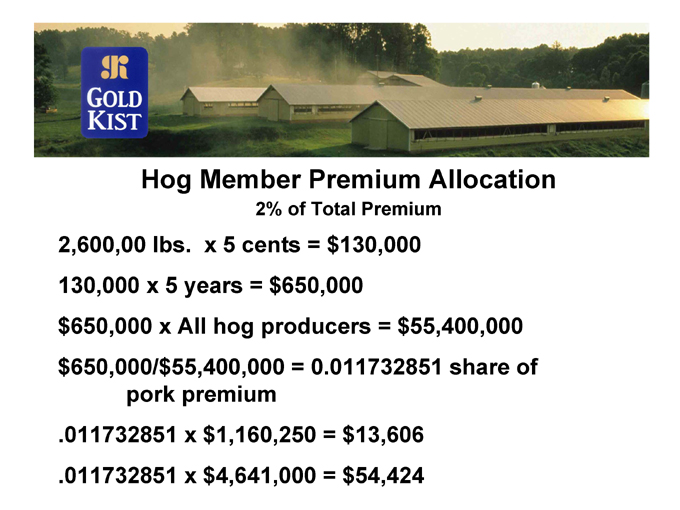

Hog Member Premium Allocation

2% of Total Premium

2,600,00 lbs. x 5 cents = $130,000 130,000 x 5 years = $650,000 $650,000 x All hog producers = $55,400,000 $650,000/$55,400,000 = 0.011732851 share of pork premium .011732851 x $1,160,250 = $13,606 ..011732851 x $4,641,000 = $54,424