As filed with the Securities and Exchange Commission on June 22, 2004

Registration No. 333-

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

CARROLS HOLDINGS CORPORATION

(Exact Name of Registrant as Specified in its Charter)

| | | | |

| Delaware | | 5812 | | 16-1287774 |

(State or Other Jurisdiction of Incorporation or Organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification No.) |

968 James Street

Syracuse, New York 13203

(315) 424-0513

(Address, Including Zip Code, and Telephone Number, Including Area Code, of Registrant’s Principal Executive Offices)

Joseph A. Zirkman, Esq.

Vice-President, General Counsel

c/o Carrols Corporation

968 James Street

Syracuse, New York 13203

(315) 424-0513

(Name, Address Including Zip Code and Telephone Number, Including Area Code, of Agent For Service)

SEE TABLE OF ADDITIONAL REGISTRANTS

Copies to:

| | |

Wayne A. Wald, Esq. Katten Muchin Zavis Rosenman 575 Madison Avenue New York, New York 10022 (212) 940-8800 | | Risë B. Norman, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017 (212) 455-2000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after the effective date of this Registration Statement.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. ¨

CALCULATION OF REGISTRATION FEE

| | | | | | |

Title of Each Class of Securities to be Registered | | Proposed Maximum Aggregate Offering Price (1) | | Amount of Registration Fee |

Enhanced Yield Securities (EYSs) (2) | | | | | | |

Shares of Class A Common Stock, par value $0.01 per share (3) | | | | | | |

% Senior Subordinated Notes (4) | | | | | | |

Subsidiary Guarantees of % Senior Subordinated Notes (5) | | | | | | |

Total | | $ | 475,000,000 | | $ | 60,183 |

| (1) | Estimated solely for the purpose of calculating the amount of registration fee pursuant to Rule 457(o) under the Securities Act of 1933, as amended. |

| (2) | The EYSs represent shares of the Class A common stock and $ million aggregate principal amount of % senior subordinated notes of Carrols Holdings Corporation (“Carrols Holdings”), including EYSs subject to the underwriters’ over-allotment option to purchase additional EYSs, and an indeterminate number of EYSs of the same series which may be received by holders of EYSs in the future on one or more occasions in replacement of the EYSs being offered hereby in the event of a subsequent issuance of EYSs, upon an automatic exchange of portions of the notes for identical portions of such additional notes as discussed in note (4) below. |

| (3) | Includes shares of Class A common stock subject to the underwriters’ over-allotment option to purchase additional EYSs. |

| (4) | Includes $ million aggregate principal amount of Carrols Holdings’ % senior subordinated notes issued in the form of EYSs, which are subject to the underwriters’ over-allotment option to purchase additional EYSs. In addition, $ million aggregate principal amount of senior subordinated notes will be sold separately, not in the form of EYSs, to the public in connection with this offering. Also includes an indeterminate principal amount of senior subordinated notes of the same series as the senior subordinated notes, which will be received by holders of notes in the future on one or more occasions in the event of a subsequent issuance of EYSs, upon an automatic exchange of portions of the notes for identical portions of such additional notes. |

| (5) | Each of the subsidiary guarantors listed in the Table of Additional Registrants on the next page will guarantee the notes being registered hereby. Pursuant to Rule 457(n) under the Securities Act of 1933, no separate fee for the guarantees is payable. |

The Registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANTS

| | | | | | |

Exact Name of Registrant Guarantor as Specified in its Charter

| | State or Other Jurisdiction of Incorporation or Organization

| | Primary Standard Industrial Classification Code Number

| | I.R.S. Employer Identification Number

|

| Carrols Corporation | | Delaware | | 5812 | | 16-0958146 |

| Cabana Bevco LLC | | Texas | | 5810 | | 74-2974628 |

| Cabana Beverages, Inc. | | Texas | | 5810 | | 74-2616290 |

| Carrols J.G. Corp. | | Delaware | | 5812 | | 16-1440019 |

| Carrols Realty Holdings Corp. | | Delaware | | 6500 | | 16-1443701 |

| Carrols Realty I Corp. | | Delaware | | 6500 | | 16-1440018 |

| Carrols Realty II Corp. | | Delaware | | 6500 | | 16-1440017 |

| Get Real, Inc. | | Delaware | | 5810 | | 06-1387866 |

| Pollo Franchise, Inc. | | Florida | | 5812 | | 65-0446291 |

| Pollo Operations, Inc. | | Florida | | 5812 | | 65-0446289 |

| Quanta Advertising Corp. | | New York | | 7310 | | 16-1033405 |

| Taco Cabana, Inc. | | Delaware | | 5810 | | 74-2201241 |

| TC Bevco LLC | | Texas | | 5810 | | 74-2974633 |

| TC Lease Holdings III, V and VI, Inc. | | Texas | | 6500 | | 74-2642647 |

| T.C. Management, Inc. | | Delaware | | 5810 | | 74-2686352 |

| Texas Taco Cabana, L.P. | | Texas | | 5810 | | 74-2686346 |

| TP Acquisition Corp. | | Texas | | 5810 | | 74-2673996 |

The address, including zip code, of the principal executive offices of each additional registrant is: 968 James Street, Syracuse, New York 13203. Their telephone number at that address is (315) 424-0513.

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities, and we are not soliciting offers to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion, dated June 22, 2004

CARROLS HOLDINGS CORPORATION

Enhanced Yield Securities (EYSs)

representing

shares of Class A common stock and

$ % senior subordinated notes due 2016

and

$ % senior subordinated notes due 2016

This is our initial public offering of EYSs and senior subordinated notes. We are offering EYSs representing shares of our Class A common stock and $ million aggregate principal amount of our % senior subordinated notes due 2016. Each EYS initially represents:

| | • | | one share of our Class A common stock; and |

| | • | | a % senior subordinated note with $ principal amount. |

We are also selling separately, not in the form of EYSs, an additional $ million aggregate principal amount of % senior subordinated notes due 2016, which we refer to in this prospectus as the separate notes. Purchasers of the separate notes may not also purchase EYSs in this offering. The completion of the offering of the separate notes is a condition to our sale of the EYSs, and the completion of the offering of the EYSs is a condition to our sale of the separate notes. In addition, the completion of the internal corporate transactions described herein is a condition to our offering of the EYSs and the separate notes, and the completion of the offering of the EYSs and the separate notes is a condition to the consummation of the internal corporate transactions.

The notes mature on , 2016. We may defer or may be required to defer interest payments on the notes under specified circumstances and subject to the limitations described in “Description of Notes — Terms of the Notes — Interest Deferral” on page 122 and “Description of Other Indebtedness – New Credit Facility” on page 110. Deferred interest on the notes will bear interest quarterly at a rate equal to the stated annual rate of interest on the notes divided by four.

Upon a subsequent issuance by us of EYSs or additional notes of the same series, a portion of your notes may be automatically exchanged for an identical principal amount of the notes issued in such subsequent issuance, and in that event your EYSs or separate notes will be replaced with new EYSs or new notes. In addition to the notes offered hereby, the registration statement of which this prospectus is a part also registers the notes and new EYSs to be issued upon any such subsequent issuance. For more information regarding these automatic exchanges and the effect they may have on your investment, see “Description of Notes — Covenants Relating to EYSs — Procedures Relating to Subsequent Issuance” on page 129 and “Material U.S. Federal Income Tax Consequences — Consequences to U.S. Holders — Notes — Additional Issuances” on page 161.

Holders of EYSs will have the right to separate the EYSs into the shares of our Class A common stock and the notes represented thereby at any time after the earlier of 45 days from the closing of this offering or the occurrence of a change of control. Similarly, any holder of shares of our Class A common stock and notes may, unless the EYSs have automatically separated, combine the applicable number of shares of Class A common stock and principal amount of notes to form EYSs. Separation of all of the EYSs will occur automatically upon the occurrence of certain events described in this prospectus.

We will apply to list the EYSs on the under the symbol “ .” We anticipate that the initial public offering price will be between $ and $ per EYS and the public offering price of the separate notes will be 100% of their stated principal amount.

Investing in the EYSs, shares of our Class A common stock and/or the notes involves risks.Risk Factors begin on page 30.

| | | | | | | | | | | |

| | | Per EYS(1)

| | Total

| | Per Separate Note

| | Total

|

Public Offering Price | | $ | | | $ | | | % | | $ | |

Underwriting Discount | | $ | | | $ | | | % | | $ | |

Proceeds to Carrols Holdings Corporation (before expenses)(2) | | $ | | | $ | | | % | | $ | |

| (1) | Consists of $ allocated to each note, which represents 100% of its stated principal amount, and $ allocated to each share of Class A common stock. |

| (2) | Approximately $ million of these proceeds will be paid to the existing stockholders, including certain members of management. |

We have granted the underwriters an option to purchase up to an aggregate of additional EYSs on the same terms and conditions as set forth above to cover over-allotments, if any. To the extent we sell more EYSs in connection with the over-allotment option, the cash proceeds to certain of the existing stockholders will be greater.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

Lehman Brothers, on behalf of the underwriters, expects to deliver the EYSs and the separate notes on or about , 2004.

LEHMAN BROTHERS

, 2004

TABLE OF CONTENTS

You should rely only upon the information contained in this prospectus. We have not, and the underwriters have not, authorized any other person to provide you with different information. If anyone provides you with different or inconsistent information, you should not rely on it. We are not, and the underwriters are not, making an offer to sell these securities in any jurisdiction where the offer or sale is not permitted. You should assume the information appearing in this prospectus is accurate only as of the date on the front cover of this prospectus. Our business, financial condition, results of operations and prospects may have changed since that date.

Industry and Market Data

In this prospectus we refer to information and statistics regarding the food industry. Unless otherwise indicated, all U.S. restaurant industry data in this prospectus is from the Technomic Information Services (Technomic) 2004 report entitled “Technomic Top 100: Update and Analysis of the Largest U.S. Chain Restaurant Companies.” We believe that this source is reliable, but we have not independently verified its information and cannot guarantee its accuracy or completeness. The information and statistics we have used from Technomic reflect rounding adjustments.

Burger King® is a registered trademark and service mark and Whopper® is a registered trademark of Burger King Brands, Inc., a wholly-owned subsidiary of Burger King Corporation, or BKC. Neither BKC nor any of its subsidiaries, affiliates, officers, directors, agents, employees, accountants or attorneys are in any way participating in, approving or endorsing this offering, any of the underwriting or accounting procedures used in this offering, or any representations made in connection with this offering. The grant by BKC of any franchise or other rights to us is not intended as, and should not be interpreted as, an express or implied approval, endorsement or adoption of any statement regarding financial or other performance which may be contained in this prospectus. All financial information has been prepared by us and is our sole responsibility.

Any review by BKC of this prospectus or the information included in this prospectus has been conducted solely for the benefit of BKC to determine conformance with BKC internal policies, and not to benefit or protect any other person. No investor should interpret such review by BKC as an internal approval, endorsement, acceptance or adoption of any representation, warranty or covenant contained in this prospectus.

i

The enforcement or waiver of any obligation of Carrols Corporation under any agreement between Carrols Corporation and BKC or BKC affiliates is a matter of BKC or BKC affiliates’ sole discretion. No investor should rely on any representation, assumption or belief that BKC or BKC affiliates will enforce or waive particular obligations of Carrols Corporation under those agreements.

Through and including , 2004 (the 25th day after the date of this prospectus), all dealers effecting transactions in the EYSs and separate notes, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

ii

SUMMARY

The following is a summary of the principal features of this offering of EYSs and separate notes and should be read together with the more detailed information and financial data and statements contained elsewhere in this prospectus.

Throughout this prospectus, we refer to Carrols Holdings Corporation, a Delaware corporation, as “Carrols Holdings” and, together with its consolidated operations, as “we,” “our” and “us,” unless otherwise indicated. Any reference to “Carrols” refers to our wholly-owned subsidiary, Carrols Corporation, a Delaware corporation, and its consolidated operations, unless otherwise indicated. We are a holding company and have no direct operations. Our principal assets are the capital stock of Carrols and any intercompany notes owed to Carrols Holdings, all of which will be pledged to the creditors under the new credit facility, as described more fully below.

We use a 52-53 week fiscal year ending on the Sunday closest to December 31. For convenience, the dating of the financial information in this prospectus has been labeled as of, and for the years ended, December 31, 1999, 2000, 2001, 2002 and 2003. Similarly, all references herein to the three months ended March 30, 2003 and March 28, 2004 are referred to as the three months ended March 31, 2003 and 2004, respectively.

Throughout this prospectus, we use the terms “EBITDA” and “EBITDA margins” because we believe they are useful financial indicators for measuring operating results as well as the ability to service and/or incur indebtedness. They should not be considered as an alternative to net income as a measure of operating results or to cash flows as a measure of liquidity in accordance with generally accepted accounting principles. EBITDA is not necessarily comparable to other similarly titled captions of other companies due to differences in methods of calculation. Management believes the most directly comparable measure to EBITDA calculated in accordance with GAAP is net income (loss). See Reconciliation of Non-GAAP Financial Measures on page 60.

Carrols Holdings Corporation

Company Overview

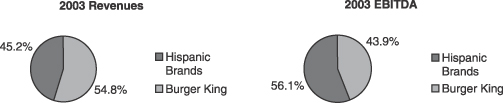

We are one of the largest restaurant companies in the United States operating 534 restaurants in 16 states as of March 31, 2004. We operate three restaurant brands that provide balance through diversification of our restaurant concepts and geographic dispersion. We own and operate two regional restaurant companies, Taco Cabana® and Pollo Tropical® (together referred to by us as our Hispanic Brands). We are also the largest Burger King® franchisee in the world and have operated Burger King restaurants since 1976. For the year ended December 31, 2003, we had total revenues of $645.0 million and EBITDA of $83.7 million.

The following charts reflect total revenues and EBITDA generated by our Hispanic Brands and Burger King restaurants for the year ended December 31, 2003 which illustrate our balance and diversity:

1

Hispanic Brands. We entered the quick-casual restaurant segment in 1998 with our acquisition of Pollo Tropical, Inc. and we subsequently acquired Taco Cabana, Inc. in late 2000. As of March 31, 2004, our Hispanic Brands were comprised of 183 company-owned and 33 franchised restaurants.

Taco Cabana—Our Taco Cabana restaurants combine generous portions of fresh, premium quality Tex-Mex and traditional Mexican style food in a festive setting with the convenience and value of quick-service restaurants. Menu items include flame-grilled beef and chicken fajitas, quesadillas, traditional Mexican and American breakfasts, other Tex-Mex dishes and fresh-made flour tortillas. Unlike many of our competitors, most menu items are made fresh daily in each of our Taco Cabana restaurants. Our Taco Cabana restaurants also offer a distinctive salsa bar as well as a variety of beverage choices, including margaritas and beer. Taco Cabana pioneered the Mexican patio café concept with its first restaurant in San Antonio, Texas in 1978. As of March 31, 2004, we owned and operated 123 Taco Cabana restaurants located in Texas and Oklahoma and franchised nine Taco Cabana restaurants. For the year ended December 31, 2003, our Taco Cabana restaurants generated total revenues of $181.5 million and EBITDA of $24.4 million. In addition, for 2003, our Taco Cabana restaurants generated average annual sales per restaurant of $1.5 million and average EBITDA per restaurant of $0.2 million.

Pollo Tropical—Our Pollo Tropical restaurants feature fresh grilled chicken marinated in a proprietary blend of tropical fruit juices and spices and authentic “made from scratch” side dishes. Our menu emphasizes freshness and quality with a focus on flavorful chicken served “hot off the grill.” Pollo Tropical restaurants combine high quality, distinctive menu items and an inviting tropical setting with the convenience and value of quick-service restaurants. Most menu items are made fresh daily in each of our Pollo Tropical restaurants. Pollo Tropical opened its first company-owned restaurant in 1988 in Miami. As of March 31, 2004, we owned and operated a total of 60 restaurants, 51 of which were located in south Florida under the trade name Pollo Tropical, and nine of which were located in central Florida under the trade name TropiGrill®. We also franchised 24 Pollo Tropical restaurants as of March 31, 2004, 19 of which were located in Puerto Rico, four in Ecuador and one in Miami. Since our acquisition of Pollo Tropical, we have expanded the brand by over 65% by opening 24 new company-owned restaurants. For the year ended December 31, 2003, our Pollo Tropical restaurants generated total revenues of $110.2 million and EBITDA of $22.6 million. In addition, for 2003, our Pollo Tropical restaurants generated average annual sales per restaurant of $1.8 million, which we believe is among the highest in the quick-casual segment, and average EBITDA per restaurant of $0.4 million.

Burger King. Burger King is the second largest hamburger restaurant chain in the world and we are the largest Burger King franchisee in the world. Burger King restaurants feature flame-broiled hamburgers and other sandwiches, the most popular of which is the WHOPPER® sandwich. The WHOPPER® is a large, flame-broiled hamburger on a toasted bun garnished with mayonnaise, lettuce, onions, pickles and tomatoes. Burger King restaurants offer hamburgers, cheeseburgers, chicken and fish sandwiches, breakfast items, french fried potatoes, onion rings, salads, shakes, desserts, and a variety of soft drinks and other beverages. In addition, promotional menu items are introduced periodically for limited periods. Burger King continually seeks to develop new products to enhance the menu of its restaurants. As of March 31, 2004, we operated 351 Burger King restaurants located in 13 Northeastern, Midwestern and Southeastern states. For the year ended December 31, 2003, our Burger King restaurants generated total revenues of $353.3 million and EBITDA of $36.8 million. In addition, for 2003, our Burger King restaurants generated average annual sales per restaurant of $1.0 million and average EBITDA per restaurant of $0.1 million.

The Industry

Total restaurant industry revenues in the United States for 2003 were $291.9 billion, an increase of 3.4% over 2002. The U.S. restaurant industry is comprised of five major segments: quick-service, quick-casual, family/mid-scale, casual dining and fine dining restaurants. Sales in the overall restaurant industry are projected to increase at a compound annual growth rate of 4.8% between 2003 and 2008.

2

The emerging quick-casual restaurant segment, which includes our Hispanic Brands, combines the convenience of quick-service restaurants with the menu variety, use of fresh ingredients, upscale decor and food quality of casual dining. We believe that the quick-casual restaurant segment is one of the fastest growing segments of the restaurant industry. Sales growth in 2003 of quick-casual chains in the Top 100 restaurant chains was 9.1% as compared to 5.1% for the overall Top 100 restaurant chains, which includes all five major segments.

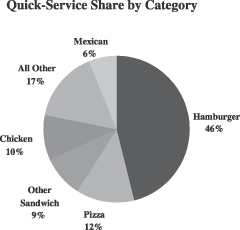

The quick-service restaurant segment is the largest segment of the U.S. restaurant industry. Technomic identifies eight major types of quick-service restaurants in the United States: hamburger; pizza/pasta; chicken; other sandwich; Mexican; ice cream/yogurt; donut and cafeteria/buffet. Sales at quick-service restaurants in the United States were $144.1 billion in 2003, representing 49% of total U.S. restaurant industry sales. The hamburger segment of the U.S. quick-service restaurant segment, which includes our Burger King restaurants, generated revenues of $50.7 billion in 2003 making it the largest segment of the U.S. quick-service restaurant market. Sales in the hamburger segment are projected to increase at a compound annual growth rate of 3.5% between 2003 and 2008. We believe that the quick-service restaurant segment meets consumers’ desire for a convenient, reasonably priced restaurant experience.

Competitive Strengths

We attribute our success in the quick-casual and quick-service restaurant segments to the following competitive strengths:

Strong Brand Names. We believe our restaurant concepts are highly recognized brands in their market areas.

| | • | | Hispanic Brands—Taco Cabana and Pollo Tropical are among the most highly recognized quick-casual restaurant brands in their respective core markets. Of the 123 Taco Cabana restaurants we owned and operated as of March 31, 2004, 117 were concentrated in five major Texas markets: San Antonio, Houston, Dallas/Fort Worth, Austin and El Paso. All of the 60 Pollo Tropical restaurants we owned and operated as of March 31, 2004 were located in four counties in south and central Florida. We believe that the following factors have contributed to the success of our Hispanic Brands: |

| | • | strong brand awareness in their respective core markets; |

| | • | high quality, freshly prepared food; |

| | • | high frequency of visits and loyalty by core customers; and |

| | • | distinctive menu offerings that capitalize on the growing consumer preference for variety and ethnic foods. |

| | • | | Burger King—Since its introduction in 1954, the Burger King brand has become one of the most recognized brands in the restaurant industry. Each year Burger King spends between 4% and 5% of total system sales on advertising (a total of $2.3 billion over the past five years) to sustain and increase this high brand awareness. We believe that strong brand recognition, combined with food quality, value and convenience of Burger King restaurants, provide opportunities for growth for the Burger King brand. |

Stable and Diversified Cash Flows. We believe that the stability of our operating cash flows is due to the proven success of our restaurant concepts, the high degree of customer awareness of our brands and our consistent focus on effective restaurant operations. Over the past five years, our EBITDA margins have ranged between 12.6% and 14.4% and averaged 13.5%. We also believe that multiple concepts operating in diverse geographic areas enable us to capitalize on regions that have rapidly growing populations and to further reduce our dependence on the economic performance of any one particular region or restaurant concept. Taco Cabana, with its restaurants primarily located in Texas, and Pollo Tropical, with its restaurants primarily located in Florida, have provided us with geographic and concept diversity. In addition, our Burger King restaurants are geographically dispersed over 13 states in the Northeast, Southeast and Midwest regions.

3

Well Positioned to Continue to Capitalize on Growing Population in Our Core Markets. Due primarily to our acquisition of Taco Cabana in late 2000 as well as the development of new Taco Cabana and Pollo Tropical restaurants over the past five years, total revenues generated by our Hispanic Brands have increased from $83.8 million in 1999 to $291.7 million in 2003. During this time frame, total EBITDA generated by our Hispanic Brands has increased over 250% from $18.5 million in 1999 to $47.0 million in 2003. As of March 31, 2004, we collectively owned and operated or franchised more than 200 restaurants under our Hispanic Brands. Our Hispanic Brand restaurants are concentrated in two regions: Texas and Florida. We expect sales from these restaurants to benefit from the continued population growth in these regions and from the growth of the U.S. Hispanic population, both of which are expected to exceed the national average. According to the U.S. Census Bureau, the U.S. population is forecast to grow by 4.1% from 2005 to 2010 and the population in Texas and Florida is forecast to grow by 6.4% and 6.7%, respectively, during that same period.In addition, the growth of the Hispanic population is expected to outpace overall population growth and increase from 11.8% of the total U.S. population in 2000 to 18.2% by 2025.

Largest Burger King Franchisee. We are the largest Burger King franchisee in the world. We believe that our leadership position, together with our experienced management team, effective management information systems, and a comprehensive infrastructure enable us to operate more efficiently and better enhance restaurant margins and overall performance levels than most other Burger King franchisees. These strengths also enable us to selectively acquire additional Burger King restaurants, continue to develop new restaurants and leverage this expertise across our Hispanic Brands.

Experienced Management Team. Our senior management has extensive experience in the restaurant industry and has a long and successful history of developing, acquiring and operating quick-service and quick-casual restaurants. Management has successfully integrated the acquisitions of Taco Cabana and Pollo Tropical. We believe that our senior management team’s experience in operating restaurants and knowledge of the demographic and other characteristics of our core markets provide us with a competitive advantage.

Business Strategy

Our business strategy is to continue to increase revenues and cash flows through the development of new restaurants and selective acquisitions. Our business strategy also includes improvements in sales at our restaurants through our marketing and product development activities and through our operating efficiencies as a result of our training and sophisticated management information systems. We also may have opportunities to expand our Hispanic Brands in additional markets through franchising and other arrangements. Our strategy is based on the following components:

Leverage Strong Brand Names. We realize significant benefits as an owner and operator of the Taco Cabana and Pollo Tropical restaurant concepts and as a Burger King franchisee. These benefits are the result of the following:

| | • | | strong recognition of the Taco Cabana and Pollo Tropical brands in their core markets; |

| | • | | ability to manage brand awareness, marketing and product development for our Hispanic Brands; |

| | • | | widespread recognition of the Burger King brand and flagship WHOPPER® product supported by a national advertising program; and |

| | • | | ability to capitalize on Burger King’s product development capabilities. |

Grow Sales and Continue to Improve Operating Efficiencies. We maintain a disciplined commitment to increasing the profitability of our existing restaurants. Our strategy is to grow sales in our existing restaurants by continuing to develop new products for our Hispanic Brands, developing and enhancing the efficiency and quality of our proprietary advertising and promotional programs and improving the customer experience at all of

4

our restaurants. Our large base of restaurants, skilled management team and sophisticated management information and operating systems enable us to optimize operating efficiencies for our restaurants. We are able to control restaurant labor and food costs, effectively manage our restaurant operations and ensure consistent application of operating controls through the use of our sophisticated management information and point-of-sale systems. Our size and, in the case of Burger King, the size of the Burger King system enable us to realize benefits from improved bargaining power for purchasing and cost management initiatives. We believe these factors provide the basis for increased restaurant level and company profitability.

Open Additional Restaurants. We believe that many of our existing markets continue to provide opportunities for the development of new Taco Cabana, Pollo Tropical and Burger King restaurants. Our staff of real estate and development professionals are responsible for new restaurant development. Before developing a new restaurant, we conduct an extensive site selection and evaluation process that includes in-depth demographic, market and financial analyses. By selectively increasing the number of restaurants we operate in a particular market, we can increase brand awareness and effectively leverage our management oversight, corporate infrastructure and local marketing expenditures.

We believe there are further growth opportunities for our Hispanic Brands. We plan to open new restaurants in our existing markets which may be either free-standing buildings or restaurants contained within strip shopping centers (in-line restaurants) to further leverage our existing brand awareness. Operating in-line restaurants allows us to selectively expand our brand penetration and visibility in certain of our existing markets, while doing so at a lower cost than developing a restaurant as a free-standing building. We also believe that there may be opportunities to further expand these brands beyond their current core regions of Texas and south and central Florida.

We believe there may be opportunities to expand the number of Burger King restaurants we operate through selective acquisitions from other franchisees and through development of new restaurants in our existing markets. We believe that selective acquisitions of additional Burger King restaurants would result in operating efficiencies from our proven abilities to reduce operating costs and achieve increased economies of scale by leveraging our infrastructure and operating systems.

Explore Franchising and Other Arrangements. We may consider expanding our Hispanic Brands into new markets through franchising and other arrangements, such as joint ventures, which would provide us with additional cash flows through royalties, franchise and other fees. We believe this strategy will allow us to test new markets for future expansion without incurring significant capital expenditures required for developing new company owned and operated restaurants.

5

The Transactions

In connection with this offering, we will:

| | • | | effect a reclassification of our existing common stock and a number of other internal corporate transactions; |

| | • | | enter into a $ million new credit facility; and |

| | • | | conduct a tender offer and consent solicitation to repurchase all of Carrols’ 9 1/2% senior subordinated notes. |

The closing of this offering is conditioned upon our completion of these transactions.

We estimate that we will sell EYSs and an additional $ million aggregate principal amount of separate notes as part of this offering. The completion of the offering of the separate notes is a condition to our sale of the EYSs, and the completion of the offering of the EYSs is a condition to our sale of the separate notes. Assuming an initial public offering price of $ per EYS, which represents the midpoint of the range set forth on the cover page of this prospectus, and 100% of the stated principal amount of each separate note, we estimate that we will receive aggregate net proceeds of $ million from this offering of EYSs and separate notes, after deducting underwriting discounts, commissions and other estimated transaction expenses.

We will use these net proceeds, together with $ million of borrowings under the new credit facility, as follows:

| | • | | $ million to repurchase shares of our existing common stock (and options to purchase shares of our existing common stock) from the existing stockholders, including certain members of management; |

| | • | | $ million to repay all outstanding borrowings under the existing credit facility; |

| | • | | $ million to repurchase all of Carrols’ 9 1/2% senior subordinated notes in the tender offer or through a redemption; |

| | • | | $ million to paybonuses and other payments to certain members of management upon the completion of this offering; and |

| | • | | $ million to pay related fees and expenses. |

If the underwriters exercise their over-allotment option with respect to the EYSs in full, we will use all of the net proceeds we receive from the sale of additional EYSs under the over-allotment option ($ million) to repurchase shares of our existing common stock (and options to purchase shares of our existing common stock) held by certain of the existing stockholders, including certain members of management.

We refer to the offering of the EYSs and the separate notes, our internal corporate transactions, the entering into of the new credit facility, the tender offer and consent solicitation, the repurchases of our existing common stock and stock options from the existing stockholders, the repayment in full of the existing credit facility and the retirement of Carrols’ 9 1/2% senior subordinated notes collectively as the “transactions.” Each of the transactions described above is conditioned upon our completion of each of the other transactions.

Internal Corporate Transactions

Prior to the commencement of this offering, we will amend our current certificate of incorporation and long-term incentive plans to provide for a single class of authorized common stock and to convert all outstanding stock options to purchase each of Carrols Holdings’ Taco Cabana class of common stock and Carrols Holdings’ Pollo Tropical class of common stock into options to purchase only Carrols Holdings’ Carrols class of common stock, which we refer to in this prospectus as our “existing common stock.”

6

Concurrently with the closing of this offering, we will repurchase an aggregate of shares of our existing common stock from Madison Dearborn Capital Partners, L.P. and Madison Dearborn Capital Partners II, L.P., together, Madison Dearborn, and BIB Holdings (Bermuda) Ltd., which we refer to collectively in this prospectus as the “existing financial investors.” In addition, we will repurchase an aggregate of shares of our existing common stock from certain of our directors and officers, and repurchase options to purchase an aggregate of shares of our existing common stock from certain of our directors, officers and current and former key employees.

In connection with this offering, we will reclassify our existing common stock into two classes of common stock: Class A common stock and Class B common stock. The shares of our existing common stock held by the existing stockholders and not repurchased by us in connection with this offering will be reclassified into shares of Class B common stock. Options to purchase our existing common stock held by the existing stockholders and not repurchased by us in connection with this offering will be exchanged for restricted shares of our Class B common stock to be issued under a newly-adopted restricted stock plan. In this prospectus, we refer to all of the foregoing transactions as our “internal corporate transactions.”

New Credit Facility

Concurrently with the closing of this offering, Carrols will repay all outstanding borrowings due to the current lenders under its senior secured credit facility, which we refer to in this prospectus as the “existing credit facility,” and will amend and restate the existing credit facility with a new syndicate of lenders, including Lehman Brothers as lead arranger and bookrunner. In this prospectus, we refer to this amended and restated senior secured credit facility as the “new credit facility.” The new credit facility will be comprised of a secured revolving credit facility in a total principal amount of up to $ million (including amounts reserved for letters of credit) and a term loan facility consisting of senior secured notes in an aggregate principal amount of $ million. A portion of the new credit facility ($ million) will be reserved to fund capital expenditures for new restaurant development. While the new credit facility will permit us to pay dividends on our shares of Class A common stock and Class B common stock and interest to holders of the notes, it will contain significant restrictions on our ability to do so, and on our subsidiaries’ ability to make dividend and interest payments to us. The revolving credit facility will have a -year maturity and the term loan facility will have a -year maturity. See “Description of Other Indebtedness—New Credit Facility.”

Tender Offer and Consent Solicitation

In connection with this offering, we will commence a tender offer and consent solicitation with respect to all of Carrols’ outstanding 9 1/2% senior subordinated notes due 2008 for an expected total consideration of $ million. In this prospectus, we refer to these notes as “Carrols’ 9 1/2% senior subordinated notes.” As of March 31, 2004, $170 million aggregate principal amount of Carrols’ 9 1/2% senior subordinated notes were outstanding. The closing of this offering will be conditioned upon the receipt of the tender and consent of at least a majority in aggregate principal amount of Carrols’ 9 1/2% senior subordinated notes outstanding in order to delete the restrictive covenants contained in the indenture governing those notes, and the consummation of the tender offer and consent solicitation will be conditioned upon the closing of this offering. Holders that provide consents will be obligated to tender and holders who tender will be obligated to consent. After we receive the required consents, we intend to enter into a supplemental indenture to remove the restrictive covenants contained in the indenture to facilitate this offering. We cannot assure you that the tender offer and consent solicitation will be consummated on the terms described above. If any notes are not tendered pursuant to the tender offer, we intend to redeem such outstanding notes. The notes are redeemable at our option on or after December 1, 2003 at a price of 104.75% of the principal amount if redeemed before December 1, 2004. We will use a portion of the net proceeds from this offering and borrowings under the new credit facility to pay for Carrols’ 9 1/2% senior subordinated notes accepted for purchase in the tender offer and consent solicitation or redeemed after this offering.

7

The Existing Stockholders

The existing financial investors and certain of our directors, officers and current and former key employees are the owners of all our outstanding existing common stock (and, in the case of our directors, officers and current and former key employees, outstanding options to purchase our existing common stock) prior to this offering. In this prospectus, we refer to these owners as the “existing stockholders.” As discussed above, the existing stockholders will be selling an aggregate of shares of our existing common stock (and options to purchase shares of our existing common stock) to us for $ million, which we will purchase with a portion of the proceeds of this offering, or shares of our existing common stock (and options to purchase shares of our existing common stock) for $ million if the underwriters exercise their over-allotment option with respect to the EYSs.

Following the completion of our internal corporate transactions and upon the consummation of the other transactions, we anticipate that the existing financial investors will own an aggregate of shares of our outstanding Class B common stock, representing approximately % of our outstanding capital stock, or an aggregate of shares representing approximately % of our outstanding capital stock, if the underwriters’ over-allotment option with respect to the EYSs is exercised in full. In addition, we anticipate that the other existing stockholders will own an aggregate of shares of our outstanding Class B common stock, representing approximately % of our outstanding capital stock, or an aggregate of shares representing approximately % of our outstanding capital stock, if the underwriters’ over-allotment option with respect to the EYSs is exercised in full.

Exchange Rights of Class B Common Stockholders

After the expiration of a 180-day lock-up period, the holders of our Class B common stock will have rights to exchange their Class B common stock for EYSs or, if the EYSs have been automatically separated or if the Class A common stock is listed for separate trading on a stock exchange, Class A common stock, subject to certain restrictions. Following the consummation of the transactions and through the maturity date of the notes, and subject to the lock-up period, each share of Class B common stock will be exchangeable into EYSs at a fixed rate of shares of Class B common stock for one EYS. If the EYSs have automatically separated or if the shares of our Class A common stock are listed for separate trading on a stock exchange, the holders of the Class B common stock may convert each share of Class B common stock into one share of Class A common stock. Following this offering, we expect that there will be shares of Class B common stock (or shares of Class B common stock if the underwriters exercise their over-allotment option with respect to the EYSs in full) exchangeable into EYSs (or EYSs if the underwriters exercise their over-allotment option in full). Subject to limited exceptions, until the second anniversary of the consummation of this offering, the amended and restated stockholders agreement to be entered into among the Class B stockholders will restrict the holders of our Class B common stock from exercising their exchange rights if following the exchange the holders of our Class B common stock would hold less than 10% of the outstanding shares of our capital stock in the aggregate. For a more complete description of this exchange right and the terms of our Class A common stock and Class B common stock, see “Description of Capital Stock.”

8

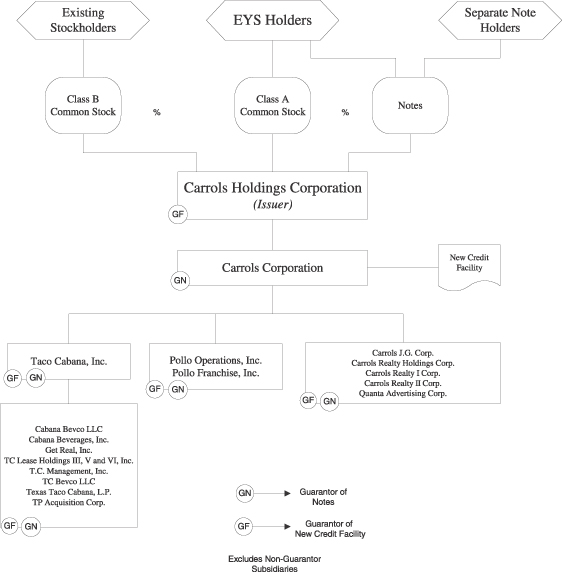

Our Corporate Structure After this Offering

The following chart reflects our corporate structure immediately after this offering (without giving effect to the exercise of the underwriters’ over-allotment option with respect to the EYSs), including percentages of voting control:

9

General Information About This Prospectus

Throughout this prospectus, unless otherwise noted, we have assumed:

| | • | | no exercise of the underwriters’ over-allotment option with respect to the EYSs; |

| | • | | the reclassification of our existing common stock (and options to purchase our existing common stock); |

| | • | | that the 10% of our outstanding capital stock that the existing stockholders must continue to hold for two years following the consummation of this offering is calculated on a fully-diluted basis; |

| | • | | the purchase of all of Carrols’ 9 1/2%senior subordinated notes in the tender offer and consent solicitation for aggregate consideration of $ million, including accrued and unpaid interest to the tender purchase date; |

| | • | | a % annual interest rate on the notes, which is subject to change depending on market conditions prior to the pricing date; and |

| | • | | an initial public offering price of $ per EYS (which represents the midpoint of the range set forth on the cover page of this prospectus) comprised of $ allocated to one share of Class A common stock and $ (100% of the stated principal amount) allocated to each note, and 100% of the stated principal amount of each separate note. |

Unless the context otherwise requires, references in this prospectus to this “offering” refer collectively to the offering of EYSs, including the shares of Class A common stock and notes represented by such EYSs, and $ million aggregate principal amount of separate notes.

Recent Developments

We restated our financial statements, including applicable footnotes, for periods ended prior to December 31, 2003 to report real estate transactions for 86 restaurants consummated during 1991 to 2000 as financing transactions under SFAS No. 98, “Accounting for Leases”, rather than as sale/leaseback transactions.

The restatement was due to lease provisions in certain of our sale/leaseback transactions, which in our opinion have minimal commercial impact upon the relevant terms of the leases. Had we been aware of the potential impact of these provisions upon our financial statements, we believe that both we and the respective lessors would have agreed to exclude those provisions from each lease without affecting any of the material terms of such leases. We may amend these leases in the future to address these provisions and to qualify them for treatment as operating leases as originally intended. However, we cannot assure you as to when or whether any or all of such leases will be amended.

The impact of the restatement was to record on our balance sheets the property and equipment of the restaurants subject to these transactions and record the proceeds from these transactions (including the gains previously deferred) as a form of debt financing. The restatement also impacted our financial results by increasing the depreciation expense for the property and equipment subject to these transactions and recharacterizing the lease payments previously accounted for as rent expense for these restaurants as principal repayments and interest expense. The restatement had no impact on our liquidity and net cash flows. In addition, there was no impact on sale/leaseback transactions that were consummated in 2002 and 2003.

As a result of the restatement, we were in default related to certain required financial leverage ratios and other covenants under the existing credit facility. We obtained a waiver from our senior secured lenders of any

10

prior non-compliance and defaults resulting from the restatement. In addition, the existing credit facility was amended to exclude all adjustments resulting from this restatement on our financial covenant requirements and to treat on a prospective basis the specified leases as if no restatement or recharacterization had occurred.

See Note 2 to the consolidated financial statements included elsewhere in this prospectus for a complete discussion of the restatement. Amounts affected by the restatement that appear in this prospectus have also been restated.

Our Corporate Information

Our principal executive office is located at 968 James Street, Syracuse, New York 13203, and our telephone number is (315) 424-0513. Our internet address iswww.carrols.com. www.carrols.com is a textual reference only, meaning that the information contained on the website is not part of this prospectus and is not incorporated in this prospectus by reference. Carrols Holdings is a Delaware corporation, incorporated in 1986.

11

The Offering

Summary of the EYSs and Notes

We are offering EYSs at an initial public offering price of $ per EYS, which represents the midpoint of the range set forth on the cover page of this prospectus, and $ million aggregate principal amount of separate notes at an assumed initial public offering price of 100% of their stated principal amount. The completion of the offering of separate notes is a condition to our sale of the EYSs and the completion of the offering of EYSs is a condition to our sale of the separate notes. In addition, no purchaser, including the existing stockholders or any affiliate of such purchaser, is permitted to purchase both EYSs and separate notes in this offering. Unless the context requires otherwise, the EYSs and the Class A common stock and notes represented by the EYSs, together with the separate notes, are referred to in this prospectus as the “offered securities.”

What are EYSs?

EYSs are securities comprised of Class A common stock and notes.

Each EYS initially represents:

| | • | | one share of our Class A common stock; and |

| | • | | a % note with $ principal amount. |

The ratio of Class A common stock to principal amount of notes represented by an EYS is subject to change in the event of a stock split, recombination or reclassification of our Class A common stock. For example, if we effect a two-for-one stock split, from and after the effective date of the stock split, each EYS will represent two shares of Class A common stock and the same principal amount of notes as it previously represented. Similarly, if thereafter we elect to effect a two-for-one combination, from and after the effective date of the combination, each EYS will represent one share of Class A common stock and the same principal amount of notes as it previously represented. Likewise, if we effect a recombination or reclassification of our Class A common stock, each EYS will thereafter represent the appropriate number of shares of Class A common stock on a recombined or reclassified basis, as applicable, and the same principal amount of notes as it previously represented. If additional notes are issued and such notes are issued with original issue discount, referred to as OID, or if we issue notes subsequent to an issuance of notes with OID, a portion of each holder’s notes, whether held as separate notes or in the form of EYSs, will be exchanged without any further action on the part of the holder for a portion of the additional notes, so that each holder of separate notes or EYSs, as the case may be, will thereafter own indivisible note units comprised of the original notes and the additional notes in the same aggregate principal amount as such holder held prior to the automatic exchange. The principal amount of the original note and the additional note in each indivisible note unit will be identical. Accordingly, following an automatic exchange of notes, each note represented by an EYS and each separate note will consist of an indivisible note unit with an aggregate principal amount equal to the aggregate principal amount of the original note immediately prior to such exchange.

What payments can I expect to receive as a holder of EYSs or separate notes?

Assuming we make our scheduled interest payments on the notes, and pay dividends in the amount contemplated by the dividend policy to be adopted by our board of directors upon consummation of this offering, holders of the EYSs will receive in the aggregate approximately $ per year in interest on the notes and dividends on the Class A common stock represented by each EYS, and holders of the separate notes will receive $ per year per $ principal amount of their notes. We expect to make interest and dividend payments quarterly on the day of each , , and to holders of record on the day or, if such day is not a business day, on the immediately preceding business day of such month.

You will be entitled to receive quarterly interest payments at an annual rate of % of the aggregate principal amount of notes or, in the case of notes represented by EYSs, approximately $ per EYS per

12

year, subject to our right to defer interest payments on the notes for an aggregate period not to exceed eight quarters prior to , 2009 and on up to four occasions after , 2009 for up to two quarters per occasion, so long as in each case we are not otherwise in default under the indenture governing the notes. The new credit facility will contain provisions that will require us under certain circumstances to defer interest payments on the notes pursuant to our option under the indenture to defer such payments. For a detailed description of these circumstances, see “Description of Notes—Terms of the Notes—Interest Deferral” and “Description of Other Indebtedness—New Credit Facility.”

Holders of the EYSs will also receive quarterly dividend payments on the shares of our Class A common stock represented by the EYSs, if and to the extent dividends are declared by our board of directors and permitted by applicable law and the terms of our then existing indebtedness. Specifically, the indenture governing the notes and the new credit facility will restrict our ability to declare and pay dividends on our Class A common stock as described under “Dividend Policy,” “Description of Notes” and “Description of Other Indebtedness—New Credit Facility.” Upon the closing of this offering, our board of directors is expected to adopt a dividend policy which contemplates that, subject to applicable law and the terms of our then existing indebtedness, initial annual dividends will be approximately $ per share of our Class A common stock and Class B common stock. However, our board of directors may, in its discretion, modify or repeal this dividend policy. We cannot assure you that we will pay dividends at this level in the future, if at all. Any dividends paid to one class of our common stock must be paid to the other.

Will my rights as a holder of EYSs be any different than the rights of a beneficial owner of separately held Class A common stock and notes?

No. As a holder of EYSs you are the beneficial owner of the Class A common stock and notes represented by your EYSs. As such, through your broker or bank and The Depository Trust Company, or DTC, you will have exactly the same rights, privileges and preferences, including voting rights, rights to receive distributions, rights and preferences in the event of a default under the indenture governing the notes, ranking upon bankruptcy and rights to receive communications and notices as a beneficial owner of separately held Class A common stock and notes, as applicable, would have through its broker or bank and DTC.

Do I have voting rights as a holder of EYSs?

EYSs have no voting rights separate and apart from the underlying securities. As a holder of EYSs, you will be able to vote with respect to the underlying shares of Class A common stock. The existing stockholders, through their ownership of shares of Class B common stock, will own % of the voting power of our common stock outstanding immediately following the offering of the EYSs (or % if the over-allotment option with respect to the EYSs is exercised in full). Shares of our Class A common stock and shares of our Class B common stock are entitled to the same voting rights per share and vote together as a single class on all matters with respect to which holders are entitled to vote.

Will the EYSs be listed on an exchange?

Yes. We will apply to have our EYSs listed on the under the symbol “ .” Listing is subject to our fulfillment of all of the requirements of the , including the distribution of the EYSs to a minimum number of public holders.

Will the shares of our Class A common stock and the notes represented by the EYSs be separately listed on an exchange?

No. The notes represented by the EYSs and the separate notes will not be listed on any exchange. Our shares of Class A common stock will not be listed for separate trading on the unless and until a sufficient number of

13

shares are held separately and not in the form of EYSs and other conditions for listing on the have been satisfied as may be necessary to satisfy applicable listing requirements. If more than the required number of our outstanding shares of Class A common stock are no longer held in the form of EYSs and other conditions for listing on the have been satisfied for a period of 30 consecutive trading days, we will apply to list the shares of our Class A common stock for separate trading on the . The Class A common stock and notes represented by the EYSs will be freely tradable without restriction or further registration under the Securities Act, unless they are purchased by “affiliates” as that term is defined in Rule 144 under the Securities Act.

Will the separate notes be the same as the notes issued as a component of the EYSs?

Yes. The separate notes will be identical to the notes represented by EYSs, will have the same CUSIP number, and will be part of the same series of notes and issued under the same indenture. Accordingly, holders of separate notes and holders of notes represented by EYSs will vote together as a single class, in proportion to the aggregate principal amount of notes they hold, on all matters on which holders of notes are entitled to vote under the indenture governing the notes.

In what form will the offered securities be issued?

The offered securities will be issued in book-entry form only. This means that you will not be a registered holder of EYSs or the securities represented by the EYSs, or the separate notes, and you will not receive a certificate for your EYSs or the securities represented by your EYSs or the separate notes. You must rely on your broker, bank or other DTC nominee that will maintain your book-entry position to receive the benefits and exercise the rights of a holder of the offered securities.

Can I separate my EYSs into shares of Class A common stock and notes or combine shares of Class A common stock and notes to form EYSs?

Yes. Holders of any EYSs may at any time after the earlier of 45 days from the date of the closing of this offering or the occurrence of a change of control, through their broker, bank or other DTC nominee, separate the EYSs into the shares of our Class A common stock and the notes represented thereby. Similarly, unless the EYSs have previously been automatically separated, any holder of shares of our Class A common stock and notes may, at any time, through his or her broker, bank or other DTC nominee, combine the applicable number of shares of Class A common stock and principal amount of notes to form EYSs. Separation and combination of EYSs will occur promptly in accordance with DTC’s procedures and upon receipt of instructions from your broker and may involve transaction fees charged by your broker and/or financial intermediary. See “Description of EYSs—Book-Entry Settlement and Clearance—Separation and Combination.”

Will my EYSs automatically separate into shares of common stock and notes upon the occurrence of certain events?

Yes. Separation of all of the EYSs will occur automatically upon the occurrence of any redemption of the notes, whether in whole or in part, upon the maturity of the notes, upon the continuance of a payment default for 90 days under the indenture governing the notes or upon certain bankruptcy events.

What will happen if we issue additional EYSs or notes of the same series in the future?

We may in the future sell additional EYSs and/or notes of the same series, which will have terms that are identical to those of the EYSs or notes being sold in this offering. Additional EYSs will represent the same proportion of Class A common stock and notes as are represented by the then outstanding EYSs. In addition, we will be required to issue additional EYSs in the future upon the exercise of exchange rights by the holders of our Class B common stock. If we issue notes in the future (whether or not in the form of EYSs) and these notes are

14

sold with OID for U.S. federal income tax purposes, holders of the notes outstanding prior to such issuance and purchasers of the newly issued notes will automatically exchange among themselves a portion of the notes they hold so that immediately following such automatic exchange, each holder of notes will own a pro rata portion of the new notes and the old notes. The aggregate principal amount of new notes and old notes held by any holder after the exchange will be the same as the aggregate principal amount of the notes held by such holder prior to the exchange. Accordingly, following an automatic exchange of notes, each note will consist of an indivisible note unit with an aggregate principal amount equal to the aggregate principal amount of the original note immediately prior to such exchange. This exchange will be effected automatically, without any action by the holders, through the facilities of DTC. DTC has advised us that the implementation of this automatic exchange may cause a delay in the settlement of trades for up to 24 hours. See “Description of EYSs—Book Entry Settlement and Clearance—Procedures Relating to Subsequent Issuances.”

Other than potential tax and bankruptcy implications and subject to market perception, we do not believe that the automatic exchange will affect the economic attributes of your investment in our EYSs or notes. The tax and bankruptcy implications of an automatic exchange are summarized below and are described in more detail in “Risk Factors—Risks Relating to the EYSs, the Shares of Class A Common Stock and the Notes” and “Material U.S. Federal Income Tax Consequences—Consequences to U.S. Holders—Notes—Additional Issuances.”

This automatic exchange should not impair the rights you might otherwise have to assert a claim under applicable securities laws against us or the underwriters with respect to the full amount of notes purchased by you.

What are the U.S. federal income tax consequences of an investment in the EYSs?

Certain of the U.S. federal income tax consequences of an investment in EYSs are uncertain. We intend to treat the purchase of EYSs in this offering as the purchase of shares of our Class A common stock and notes and, by purchasing EYSs, you will agree to such treatment. You must allocate the purchase price of the EYSs between the shares of our Class A common stock and the notes in proportion to their respective initial fair market values, which will establish your initial tax basis in the shares of our Class A common stock and the notes. We expect to report the initial fair market value of each share of our Class A common stock as $ and the initial fair market value of each $ principal amount of the notes as $ , and by purchasing EYSs, you will agree to such allocation. If this allocation is not respected, our interest deductions may be reduced or your income inclusions (on account of interest) may be increased.

We intend to treat the notes included in the EYSs as debt for U.S. federal income tax purposes, and we intend to deduct interest on such notes for tax purposes. Such position is subject to challenge by the IRS. If the notes are treated as equity rather than debt for U.S. federal income tax purposes, then the stated interest on the notes could be treated as dividends, and interest on the notes would not be deductible by us for U.S. federal income tax purposes, which could significantly reduce our future after-tax cash flow and adversely affect our ability to make interest and dividend payments. In addition, if the notes are treated as equity, payments on the notes to foreign holders generally would be subject to U.S. federal withholding taxes, and we could be liable for withholding taxes that were not collected on our prior interest payments to foreign holders. Payments to foreign holders would not be grossed-up on account of any such taxes.

Dividends paid on our Class A common stock through 2008 are expected to qualify for taxation to non-corporate EYS holders at long-term capital gain rates. Interest income on the notes will be taxable to U.S. individuals at ordinary income tax rates.

What are the U.S. federal income tax consequences of a subsequent issuance of notes?

The U.S. federal income tax consequences to you of the subsequent issuance of notes with OID upon a subsequent offering by us of EYSs or notes of the same series are uncertain.

15

The indenture governing the notes will provide that, in the event there is a subsequent issuance of notes and such notes are issued with OID or are issued after an issuance of notes with OID, each holder of EYSs or separate notes, as the case may be, agrees that a portion of such holder’s notes will be exchanged for a portion of the notes acquired by the holders of such subsequently issued notes, as described above. As a result of these exchanges, the OID associated with the issuance of the new notes will be effectively spread among all holders of notes on a pro rata basis, which may adversely affect your tax treatment, as described below.

We intend to take the position that any subsequent issuance of notes, whether or not such notes are issued with OID, will not result in a taxable exchange of your notes for U.S. federal income tax purposes, but because of a lack of legal authority on point (1) our counsel is unable to opine on the matter and (2) there can be no assurance that the IRS will not assert that such a subsequent issuance of notes should be treated as a taxable exchange of a portion of your notes, whether held separately or in the form of EYSs, for a portion of the notes subsequently issued. In that event, you generally would have to recognize the gain (if any) realized by you on such exchange, but any loss realized by you on the exchange would most likely be disallowed. Your initial tax basis in the notes deemed to have been received in the exchange would equal the fair market value of such notes on the date of the deemed exchange (increased to reflect any disallowed loss), and your holding period for such notes would begin on the day after the deemed exchange.

Regardless of whether the exchange of notes is treated as a taxable event, such exchange could result in holders having to include OID in their taxable income prior to the receipt of cash. Following any subsequent issuance of notes with OID (or any issuance of notes thereafter), we (and our agents) will report any OID on the subsequently issued notes ratably among all holders of EYSs and separate notes, and each holder of EYSs and separate notes will, by purchasing EYSs or notes, agree to report OID in a manner consistent with this approach. However, the IRS might assert that any OID should be reported only to the persons that initially acquired such subsequently issued notes (and their transferees), and may challenge your reporting OID on your tax returns.

Immediately following an exchange of notes, we will file a Current Report on Form 8-K (or any other applicable form) to announce and quantify any changes in OID attributable to the notes.

Because there is no statutory, judicial or administrative authority directly addressing the tax treatment of the EYSs or instruments similar to the EYSs, we urge you to consult your own tax advisor concerning the tax consequences to you of an investment in the EYSs. For additional information, see “Material U.S. Federal Income Tax Consequences.”

What is the initial and prospective accounting treatment of the EYSs?

There is no explicit guidance under generally accepted accounting principles regarding the accounting and financial reporting of unit securities, such as the EYSs, comprised of common stock and notes. Any accounting treatment followed by us for the EYSs may be subject to future scrutiny and challenge. Authoritative accounting bodies such as the FASB, EITF or SEC may issue future guidance, rules or interpretations which may require us to adjust our accounting treatment for the EYSs. For our interpretation of the accounting treatment based on existing guidance available, see “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Significant Accounting Policies.”

16

Summary of the Common Stock

Issuer | Carrols Holdings Corporation |

Shares of Class A common stock represented by EYSs | shares, or shares if the underwriters exercise their over-allotment option with respect to the EYSs in full. |

Shares of Class B common stock to be outstanding following the offering | shares, or shares if the underwriters exercise their over-allotment option with respect to the EYSs in full. |

Voting rights | Subject to applicable law, each outstanding share of our Class A common stock and Class B common stock will carry one vote per share and, as a general matter, will vote together as a single class. |

Dividends | You and the holders of our Class B common stock will receive quarterly dividends on the shares of our common stock if, and to the extent, dividends are declared by our board of directors and permitted by applicable law and the terms of our then outstanding indebtedness. Specifically, the indenture governing the notes and the new credit facility both will restrict our ability to declare and pay dividends on our common stock as described in detail under “Dividend Policy.” Upon the closing of this offering, our board of directors is expected to adopt a dividend policy which contemplates that, subject to applicable law and the terms of our then existing indebtedness, initial annual dividends will be approximately $ per share of our common stock. Any time a dividend is paid to the holders of our Class A common stock, holders of our Class B common stock will be paid a dividend equal to the amount per share paid to holders of Class A common stock. Our board of directors may, in its discretion, modify or repeal this dividend policy. We cannot assure you that we will pay dividends at this level in the future, if at all. |

Dividend payment dates | If declared, dividends will be paid quarterly on the day of each , , and to holders of record on the day or, if such day is not a business day, on the immediately preceding business day of such month. |

Listing | Our shares of Class A common stock will not be listed for separate trading on the unless and until a sufficient number of shares are held separately and not in the form of EYSs and other conditions for listing on as may be necessary are satisfied. If more than the required number of our outstanding shares of Class A common stock are no longer held in the form of EYSs and other conditions for listing on are satisfied for a period of 30 consecutive trading days, we will apply to list the shares of our Class A common stock for separate trading on the . The notes and Class A common stock represented by the EYSs will be freely tradable without restriction or further registration under the Securities Act, unless they are purchased by “affiliates” as that term is defined in Rule 144 under the Securities Act. Our shares of Class B common stock will not be listed for separate trading and will have limitations on their transferability. |

17

Rights to exchange shares of Class B common stock for EYSs or shares of Class A common stock | After the expiration of a 180-day lock-up period, the holders of our Class B common stock will have rights to exchange their Class B common stock for EYSs or, if the EYSs have been automatically separated or if the Class A common stock is listed for separate trading on a stock exchange, Class A common stock, subject to certain restrictions. For a complete description of this exchange right and the terms of our Class A common stock and Class B common stock, see “Description of Capital Stock.” |

18

Summary of Notes

When we refer to the notes in this prospectus, we are referring to the notes represented by the EYSs and the separate notes.

Issuer | Carrols Holdings Corporation |

Notes represented by EYSs being offered to the public | $ million aggregate principal amount (or $ million aggregate principal amount if the underwriters exercise their over-allotment option with respect to the EYSs in full). |

Notes being offered to the public separately, not in the form of EYSs | $ million aggregate principal amount. |

Notes to be outstanding following the offering | $ million aggregate principal amount (or $ million aggregate principal amount if the underwriters exercise their over-allotment option with respect to the EYSs in full). |

Interest rate | % per year. |

Interest payment dates | Interest on the notes will be payable quarterly in arrears on the day of each , , and commencing , 2004 to holders of record on the day or, if such day is not a business day, on the immediately preceding business day of such month. |

Maturity date | The notes will mature on , 2016. |

Interest deferral | We may, at our election, subject to certain restrictions, defer interest payments on the notes. We may defer interest payments prior to , 2009 on one or more occasions during this period for up to an aggregate period of eight quarters. In addition, after , 2009, we may, subject to certain restrictions, defer interest payments on the notes on up to four occasions for up to two quarters per occasion. However, we may not defer interest on more than one occasion after , 2009 unless and until all previously deferred interest (and interest on deferred interest) has been paid in full. The new credit facility will contain provisions that will require us under certain circumstances to defer interest payments on the notes pursuant to our option under the indenture to defer such payments. |

| | Deferred interest on the notes will bear interest at the same rate per annum as the stated rate of interest applicable to the notes, compounded quarterly, until paid in full. At the end of any interest deferral period, we will be obligated to resume quarterly payments of interest on the notes, including interest on deferred interest. All interest deferred prior to , 2009, must be repaid by us on or prior to , 2009. All interest deferred after , 2009, must be repaid by us on or before maturity. |

19

| | During any interest deferral period and so long as any deferred interest or interest on deferred interest remains outstanding, we will not be permitted to make any payment of dividends on our common stock. |

| | For a detailed description of interest deferral provisions of the indenture see “Description of Notes—Terms of the Notes—Interest Deferral.��� |

| | In the event that interest payments on the notes are deferred, you would be required to recognize interest income for U.S. federal income tax purposes even if you do not currently receive the related cash interest payments. |

Ranking | The notes will be unsecured and |

| | • | subordinated in right of payment to all of our existing and future senior indebtedness, including our guarantee under the new credit facility; |

| | • | equal in right of payment to our other existing and future senior subordinated indebtedness; and |

| | • | effectively subordinated to all indebtedness of our existing and future subsidiaries that are not guarantors of the notes. |

| | As of March 31, 2004, after giving pro forma effect to the transactions, we would have had approximately $ million of total consolidated indebtedness, of which $ million would have been senior to the notes. |