Exhibit 99.2

Disclaimer

Certain statements included or incorporated by reference in this document may constitute forward looking statements or financial outlooks under applicable securities legislation. Such forward looking statements or information typically contain statements with words such as "anticipate", "believe", "expect", "plan", "intend", "estimate", "propose", or similar words suggesting future outcomes or statements regarding an outlook. Forward looking statements or information in this document may include, but are not limited to: capital expenditures and Vermilion’s ability to fund such expenditures; Vermilion’s additional debt capacity providing it with additional working capital; the flexibility of Vermilion’s capital program and operations; business strategies and objectives; operational and financial performance; estimated volumes of reserves and resources; petroleum and natural gas sales; future production levels and the timing thereof, including Vermilion’s 2019 guidance, and rates of average annual production growth; the effect of changes in crude oil and natural gas prices, changes in exchange rates and significant declines in production or sales volumes due to unforeseen circumstances; the effect of possible changes in critical accounting estimates; statements regarding the growth and size of Vermilion’s future project inventory, and the wells expected to be drilled in 2019; exploration and development plans and the timing thereof; Vermilion’s ability to reduce its debt, including its ability to redeem senior unsecured notes prior to maturity; statements regarding Vermilion’s hedging program, its plans to add to its hedging positions, and the anticipated impact of Vermilion’s hedging program on project economics and free cash flows; the potential financial impact of climate-related risks; acquisition and disposition plans and the timing thereof; operating and other expenses, including the payment and amount of future dividends; royalty and income tax rates and Vermilion’s expectations regarding future taxes and taxability; and the timing of regulatory proceedings and approvals.

Such forward looking statements or information are based on a number of assumptions, all or any of which may prove to be incorrect. In addition to any other assumptions identified in this document, assumptions have been made regarding, among other things: the ability of Vermilion to obtain equipment, services and supplies in a timely manner to carry out its activities in Canada and internationally; the ability of Vermilion to market crude oil, natural gas liquids, and natural gas successfully to current and new customers; the timing and costs of pipeline and storage facility construction and expansion and the ability to secure adequate product transportation; the timely receipt of required regulatory approvals; the ability of Vermilion to obtain financing on acceptable terms; foreign currency exchange rates and interest rates; future crude oil, natural gas liquids, and natural gas prices; and management’s expectations relating to the timing and results of exploration and development activities.

Although Vermilion believes that the expectations reflected in such forward looking statements or information are reasonable, undue reliance should not be placed on forward looking statements because Vermilion can give no assurance that such expectations will prove to be correct. Financial outlooks are provided for the purpose of understanding Vermilion’s financial position and business objectives, and the information may not be appropriate for other purposes. Forward looking statements or information are based on current expectations, estimates, and projections that involve a number of risks and uncertainties which could cause actual results to differ materially from those anticipated by Vermilion and described in the forward looking statements or information. These risks and uncertainties include, but are not limited to: the ability of management to execute its business plan; the risks of the oil and gas industry, both domestically and internationally, such as operational risks in exploring for, developing and producing crude oil, natural gas liquids, and natural gas; risks and uncertainties involving geology of crude oil, natural gas liquids, and natural gas deposits; risks inherent in Vermilion's marketing operations, including credit risk; the uncertainty of reserves estimates and reserves life and estimates of resources and associated expenditures; the uncertainty of estimates and projections relating to production and associated expenditures; potential delays or changes in plans with respect to exploration or development projects; Vermilion's ability to enter into or renew leases on acceptable terms; fluctuations in crude oil, natural gas liquids, and natural gas prices, foreign currency exchange rates and interest rates; health, safety, and environmental risks; uncertainties as to the availability and cost of financing; the ability of Vermilion to add production and reserves through exploration and development activities; the possibility that government policies or laws may change or governmental approvals may be delayed or withheld; uncertainty in amounts and timing of royalty payments; risks associated with existing and potential future law suits and regulatory actions against Vermilion; and other risks and uncertainties described elsewhere in this document or in Vermilion's other filings with Canadian securities regulatory authorities.

The forward looking statements or information contained in this document are made as of the date hereof and Vermilion undertakes no obligation to update publicly or revise any forward looking statements or information, whether as a result of new information, future events, or otherwise, unless required by applicable securities laws.

All crude oil and natural gas reserve and resource information contained in this document has been prepared and presented in accordance with National Instrument 51-101 Standards of Disclosure for Oil and Gas Activities and the Canadian Oil and Gas Evaluation Handbook. Reserves estimates have been made assuming that development of each property in respect of which the estimate is made will occur, without regard to the likely availability of funding required for such development. The actual crude oil and natural gas reserves and future production will be greater than or less than the estimates provided in this document.

Natural gas volumes have been converted on the basis of six thousand cubic feet of natural gas to one barrel of oil equivalent. Barrels of oil equivalent (boe) may be misleading, particularly if used in isolation. A boe conversion ratio of six thousand cubic feet to one barrel of oil is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead.

Financial data contained within this document are reported in Canadian dollars, unless otherwise stated.

Vermilion Energy Inc. ■ Page 1■ 2018 Management’s Discussion and Analysis

Abbreviations

| $M | thousand dollars |

| $MM | million dollars |

| AECO | the daily average benchmark price for natural gas at the AECO ‘C’ hub in Alberta |

| bbl(s) | barrel(s) |

| bbls/d | barrels per day |

| boe | barrel of oil equivalent, including: crude oil, condensate, natural gas liquids, and natural gas (converted on the basis of one boe for six mcf of natural gas) |

| boe/d | barrel of oil equivalent per day |

| GJ | gigajoules |

| LSB | light sour blend crude oil reference price |

| mbbls | thousand barrels |

| mcf | thousand cubic feet |

| mmcf/d | million cubic feet per day |

| NBP | the reference price paid for natural gas in the United Kingdom at the National Balancing Point Virtual Trading Point. |

| NGLs | natural gas liquids, which includes butane, propane, and ethane |

| PRRT | Petroleum Resource Rent Tax, a profit based tax levied on petroleum projects in Australia |

| tCO2e | tonnes of carbon dioxide equivalent |

| TTF | the price for natural gas in the Netherlands, quoted in megawatt hours of natural gas, at the Title Transfer Facility Virtual Trading Point |

| WTI | West Texas Intermediate, the reference price paid for crude oil of standard grade in US dollars at Cushing, Oklahoma |

Vermilion Energy Inc. ■ Page 2■ 2018 Management’s Discussion and Analysis

Management's Discussion and Analysis

The following is Management’s Discussion and Analysis (“MD&A”), dated February 27, 2019, of Vermilion Energy Inc.’s (“Vermilion”, “we”, “our”, “us” or the “Company”) operating and financial results as at and for the three months and year ended December 31, 2018 compared with the corresponding periods in the prior year.

This discussion should be read in conjunction with the audited consolidated financial statements for the year ended December 31, 2018 and 2017, together with the accompanying notes. Additional information relating to Vermilion, including its Annual Information Form, is available on SEDAR at www.sedar.com or on Vermilion’s website at www.vermilionenergy.com.

The audited consolidated financial statements for the year ended December 31, 2018 and comparative information have been prepared in Canadian dollars and in accordance with International Financial Reporting Standards (“IFRS” or, alternatively, “GAAP”) as issued by the International Accounting Standards Board ("IASB").

This MD&A includes references to certain financial and performance measures which do not have standardized meanings prescribed by IFRS. These measures include:

| • | Fund flows from operations: Fund flows from operations is a measure of profit or loss in accordance with IFRS 8 “Operating Segments”. Please see "Segmented Information" in the "Notes to the Consolidated Financial Statements" for a reconciliation of fund flows from operations to net earnings. We analyze fund flows from operations both on a consolidated basis and on a business unit basis in order to assess the contribution of each business unit to our ability to generate income necessary to pay dividends, repay debt, fund asset retirement obligations and make capital investments. |

| • | Net debt: Net debt is a capital management measure in accordance with IAS 1 "Presentation of Financial Statements". Net debt is comprised of long-term debt plus current liabilities less current assets and represents Vermilion's net financing obligations after adjusting for the timing of working capital fluctuations. Net debt excludes lease obligations which are secured by a corresponding right-of-use asset. Please see "Capital disclosures" in the "Notes to the Consolidated Financial Statements" for additional information. |

| • | Netbacks: Netbacks are per boe and per mcf performance measures used in the analysis of operational activities. We assess netbacks both on a consolidated basis and on a business unit basis in order to compare and assess the operational and financial performance of each business unit versus other business units and also versus third party crude oil and natural gas producers. |

In addition, this MD&A includes references to certain financial measures which are not specified, defined, or determined under IFRS and are therefore considered non-GAAP financial measures. These non-GAAP financial measures are unlikely to be comparable to similar financial measures presented by other issuers. For a full description of these non-GAAP financial measures and a reconciliation of these measures to their most directly comparable GAAP measures, please refer to “Non-GAAP Financial Measures”.

Condensate Presentation

We report our condensate production in Canada and the Netherlands business units within the crude oil and condensate production line. We believe that this presentation better reflects the historical and forecasted pricing for condensate, which is more closely correlated with crude oil pricing than with pricing for propane, butane and ethane (collectively “NGLs” for the purposes of this report).

Vermilion Energy Inc. ■ Page 3■ 2018 Management’s Discussion and Analysis

Guidance

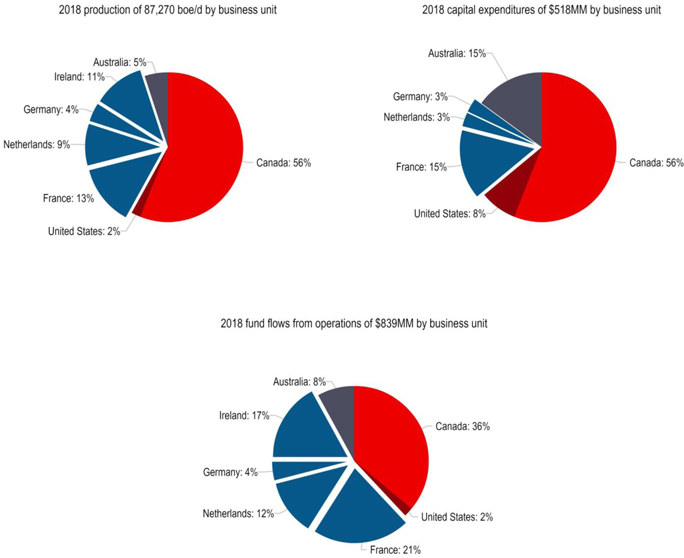

On October 30, 2017, we released our 2018 capital expenditure guidance of $315 million and associated production guidance of between 74,500 to 76,500 boe/d. On January 15, 2018, we increased our capital expenditure guidance to $325 million and production guidance to between 75,000 to 77,500 boe/d to reflect the post-closing impact of the acquisition of a private southeast Saskatchewan and southwest Manitoba light oil producer. On April 16, 2018, we increased our capital expenditure guidance to $430 million and production guidance to between 86,000 to 90,000 boe/d to reflect the post-closing impact of the acquisition of Spartan Energy Corp. On July 30, 2018, we increased our capital expenditure guidance to $500 million to reflect the acceleration of our Australia drilling campaign into Q4 2018, and to a lesser extent to account for the impact of foreign exchange fluctuations on our Canadian dollar capital levels. On October 25, 2018, we increased our capital expenditure guidance to $510 million to reflect additional capital activity associated with the assets acquired in the Powder River Basin in August of 2018. Actual 2018 capital spending of $518 million was within 2% of our guidance and 2018 average production of 87,270 boe/d was within 1% of the mid-point of our guidance range.

On October 25, 2018, we released our 2019 capital budget and related guidance. The 2019 total budget and production guidance remain unchanged, although we have deferred some activity to later in the year and reallocated capital between business units, the breakdown of which can be found in our corporate presentation located on our website.

The following table summarizes our guidance:

| | | Date | | Capital Expenditures ($MM) | | | Production (boe/d) | |

| 2018 Guidance | | | | | | | | | | |

| 2018 Guidance | | October 30, 2017 | | | 315 | | | | 74,500 to 76,500 | |

| 2018 Guidance | | January 15, 2018 | | | 325 | | | | 75,000 to 77,500 | |

| 2018 Guidance | | April 16, 2018 | | | 430 | | | | 86,000 to 90,000 | |

| 2018 Guidance | | July 30, 2018 | | | 500 | | | | 86,000 to 90,000 | |

| 2018 Guidance | | October 25, 2018 | | | 510 | | | | 86,000 to 90,000 | |

| 2018 Actual Results | | | | | 518 | | | | 87,270 | |

| 2019 Guidance | | | | | | | | | | |

| 2019 Guidance | | October 25, 2018 | | | 530 | | | | 101,000 to 106,000 | |

Vermilion Energy Inc. ■ Page 4■ 2018 Management’s Discussion and Analysis

Vermilion's Business

Vermilion is a Calgary, Alberta based international oil and gas producer focused on the acquisition, exploration, development, and optimization of producing properties in North America, Europe, and Australia. We manage our business through our Calgary head office and our international business unit offices. This MD&A separately discusses each of our business units in addition to our corporate segment.

Vermilion Energy Inc. ■ Page 5■ 2018 Management’s Discussion and Analysis

Consolidated Results Overview

| | | Q4 2018 | | | Q3 2018 | | | Q4 2017 | | | Q4/18 vs.

Q3/18 | | Q4/18 vs.

Q4/17 | | 2018 | | | 2017 | | | 2018 vs.

2017 |

| Production | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil and condensate (bbls/d) | | | 47,678 | | | | 47,152 | | | | 27,830 | | | 1% | | 71% | | | 39,182 | | | | 27,721 | | | 41% |

| NGLs (bbls/d) | | | 7,815 | | | | 6,839 | | | | 5,279 | | | 14% | | 48% | | | 6,366 | | | | 4,194 | | | 52% |

| Natural gas (mmcf/d) | | | 276.77 | | | | 253.38 | | | | 238.27 | | | 9% | | 16% | | | 250.33 | | | | 216.64 | | | 16% |

| Total (boe/d) | | | 101,621 | | | | 96,222 | | | | 72,821 | | | 6% | | 40% | | | 87,270 | | | | 68,021 | | | 28% |

| Sales | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil and condensate (bbls/d) | | | 47,620 | | | | 46,368 | | | | 27,638 | | | 3% | | 72% | | | 38,741 | | | | 27,483 | | | 41% |

| NGLs (bbls/d) | | | 7,815 | | | | 6,839 | | | | 5,279 | | | 14% | | 48% | | | 6,366 | | | | 4,194 | | | 52% |

| Natural gas (mmcf/d) | | | 276.77 | | | | 253.38 | | | | 238.27 | | | 9% | | 16% | | | 250.33 | | | | 216.64 | | | 16% |

| Total (boe/d) | | | 101,563 | | | | 95,437 | | | | 72,628 | | | 6% | | 40% | | | 86,829 | | | | 67,784 | | | 28% |

| Build in inventory (mbbls) | | | 5 | | | | 73 | | | | 18 | | | | | | | | 160 | | | | 87 | | | |

| Financial metrics | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Fund flows from operations ($M) | | | 222,342 | | | | 260,705 | | | | 181,253 | | | (15)% | | 23% | | | 838,652 | | | | 602,565 | | | 39% |

| Per share ($/basic share) | | | 1.46 | | | | 1.71 | | | | 1.49 | | | (15)% | | (2)% | | | 5.96 | | | | 5.00 | | | 19% |

| Net earnings | | | 323,373 | | | | (15,099 | ) | | | 8,645 | | | N/A | | 3,641% | | | 271,650 | | | | 62,258 | | | 336% |

| Per share ($/basic share) | | | 2.12 | | | | (0.10 | ) | | | 0.07 | | | N/A | | 2,929% | | | 1.93 | | | | 0.52 | | | 271% |

| Net debt ($M) | | | 1,929,529 | | | | 2,034,086 | | | | 1,371,790 | | | (5)% | | 41% | | | 1,929,529 | | | | 1,371,790 | | | 41% |

| Cash dividends ($/share) | | | 0.690 | | | | 0.690 | | | | 0.645 | | | —% | | 7% | | | 2.715 | | | | 2.580 | | | 5% |

| Activity | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital expenditures ($M) | | | 163,580 | | | | 146,185 | | | | 74,303 | | | 12% | | 120% | | | 518,214 | | | | 320,449 | | | 62% |

| Acquisitions ($M) | | | 2,689 | | | | 198,173 | | | | 3,048 | | | | | | | | 1,759,425 | | | | 27,637 | | | |

| Gross wells drilled | | | 73.00 | | | | 65.00 | | | | 8.00 | | | | | | | | 185.00 | | | | 56.00 | | | |

| Net wells drilled | | | 45.08 | | | | 58.97 | | | | 6.00 | | | | | | | | 147.93 | | | | 46.58 | | | |

| Financial performance review |

Q4 2018 vs. Q3 2018

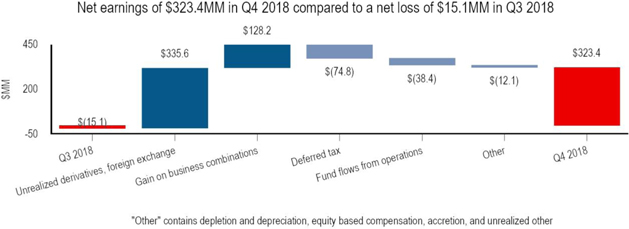

| • | We recorded net earnings for Q4 2018 of $323.4 million ($2.12/basic share) compared to a net loss of $15.1 million ($0.10/basic share) in Q3 2018. This net earnings growth was primarily attributable to a $348.9 million increase in unrealized gains on derivative instruments and a $128.2 million gain recorded on business combinations. These increases were partially offset by a $38.4 million decrease in fund flows from operations. |

Vermilion Energy Inc. ■ Page 6■ 2018 Management’s Discussion and Analysis

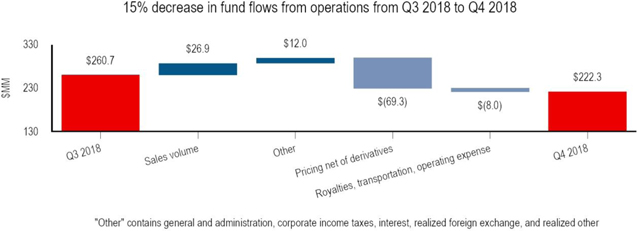

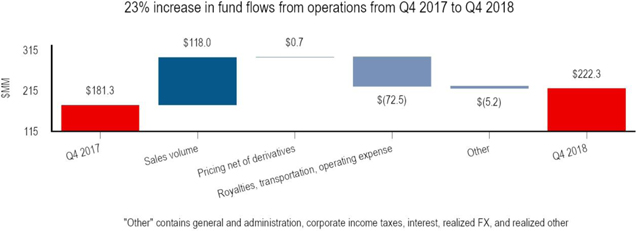

| • | We generated fund flows from operations of $222.3 million during Q4 2018, a decrease of 15% from Q3 2018. This quarter-over-quarter decrease was primarily due to weaker crude oil prices during the current period, including a 48% decrease in in the Edmonton sweet index. The diversified nature of our production somewhat mitigated this 48% decrease in the Edmonton sweet index as illustrated by an attenuated 23% decrease in our crude oil and condensate realized price and a 16% decrease in our consolidated realized price. |

Q4 2018 vs. Q4 2017

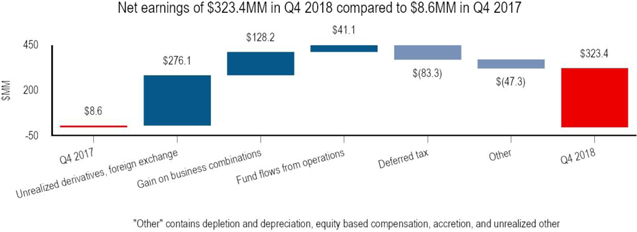

| • | We recorded net earnings for Q4 2018 of $323.4 million ($2.12/basic share) compared to net earnings of $8.6 million ($0.07/basic share) in Q4 2017. The net earnings growth was the result of a 23% increase in fund flows from operations driven by increased sales volumes in Q4 2018 as compared to Q4 2017, an increase in unrealized gain on derivative instruments ($193.1 million), and a $128.2 million gain on business combinations. |

Vermilion Energy Inc. ■ Page 7■ 2018 Management’s Discussion and Analysis

| • | Fund flows from operations increased 23% in Q4 2018 versus Q4 2017. This increase occurred due to higher sales volumes in Q4 2018 partially offset by increased royalties, transportation, and operating expense associated with these higher volumes. |

2018 vs. 2017

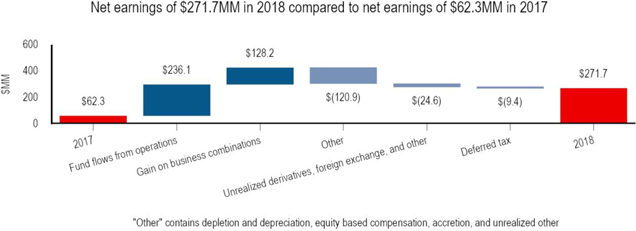

| • | For the year ended December 31, 2018, net earnings of $271.7 million compared to net earnings of $62.3 million in 2017. The increase in net earnings primarily resulted from a year-over-year increase in fund flows from operations of $236.1 million and a gain on business combinations of $128.2 million. These increases were partially offset by increased depletion and depreciation expense resulting from higher production volumes. |

Vermilion Energy Inc. ■ Page 8■ 2018 Management’s Discussion and Analysis

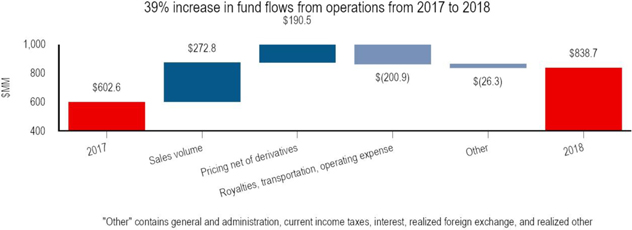

| • | Fund flows from operations increased 39% for the year ended December 31, 2018 versus 2017 due to increased sales volumes and higher realized pricing offset by an increase in royalties, transportation and operating expense. Our consolidated realized price increased by 19% from $44.41/boe to $52.95/boe due to an increase in our relative crude oil production and stronger crude oil and European gas pricing. Our sales volumes increased by 28% due to production increases in Canada, the Netherlands, and the United States. |

| • | On a per unit basis, fund flows from operations increased by 9% from $24.34/boe for the year ended December 31, 2017 to $26.47/boe in 2018. This increase reflects the improvement in our realized price per boe and includes a 25% decrease in per boe general and administration expenses as our overall expense decreased by 4% despite production growth. These decreases were partially offset by higher per unit costs for royalties (resulting from the stronger commodity price environment and higher royalty rates) and operating expenses. Per boe operating expenses increased by $1.47/boe from $9.79/boe in 2017 to $11.26/boe in 2018 due in part to a stronger Euro relative to the Canadian dollar in 2018 and increased expenses associated with higher value crude oil production in Canada. |

Q4 2018 vs. Q3 2018

| • | Consolidated average production of 101,621 boe/d during Q4 2018 increased 6% versus Q3 2018. The increase in production was primarily attributable to new wells brought on production in Canada, growth in the United States through an acquisition closed in Q3 2018, and a full quarter of production from wells brought on production in Q3 2018 in the Netherlands and Hungary. These production increases were partially offset by an 11% decrease in Australia resulting from a planned shutdown of the Wandoo field for maintenance and downtime associated with drilling. |

Q4 2018 vs. Q4 2017

| • | Consolidated average production of 101,621 boe/d in Q4 2018 represented an increase of 40% from Q4 2017 due to growth in Canada and the United States. In Canada, year-over-year growth was the result of both acquisitions and continued development of our Mannville condensate-rich resource play and southeast Saskatchewan light oil development. In the United States, production growth resulted from an acquisition in Q3 2018 and organic drilling activity. |

2018 vs. 2017

| • | For the year ended December 31, 2018, consolidated average production of 87,270 boe/d represented an increase of 28% from 2017 due to production growth in Canada, the United States, and the Netherlands. In Canada, production increased by 19,120 boe/d due to contributions from acquisitions and continued development of our Mannville condensate-rich resource play and southeast Saskatchewan light oil development. In the United States, production growth resulted from an acquisition in Q3 2018 and organic drilling activity. In the Netherlands, year-over-year production growth occurred following the receipt of production permits (the absence of which restricted production from certain wells in the comparable period in 2017). |

Vermilion Energy Inc. ■ Page 9■ 2018 Management’s Discussion and Analysis

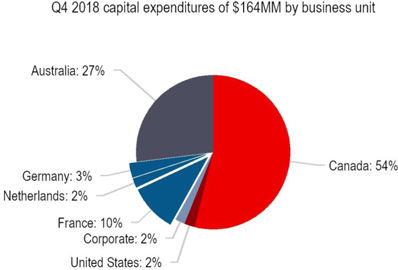

| • | For the three months ended December 31, 2018, capital expenditures of $163.6 million primarily related to activity in Canada and Australia. In Canada, capital expenditures of $90.2 million included the drilling of 72.0 (44.1 net) wells, primarily in southeast Saskatchewan. In Australia, capital expenditures of $43.8 million related to the two (2.0 net) well drilling program. |

Dividends

| • | Declared dividends of $0.23 per common share per month for Q4 2018, resulting in total dividends declared of $2.715 per common share for the year ended December 31, 2018. |

| • | In Q2 2018, we increased our monthly dividend by 7% resulting in a year-over-year increase in cash dividends. The Q2 2018 increase was our fourth dividend increase (previously Vermilion's distribution in the income trust era) since we began paying a distribution in 2003. |

Long-term debt and net debt

| • | Long-term debt increased from $1.3 billion as at December 31, 2017 to $1.8 billion as at December 31, 2018. This increase was primarily a result of increased borrowings on the revolving credit facility to fund acquisitions in 2018. These increases were coupled with the impact of the stronger US dollar on our US denominated Sr. Unsecured Notes. |

| • | Net debt increased to $1.9 billion as at December 31, 2018 from $1.4 billion at December 31, 2017, primarily due to acquisition activity in 2018, partially offset by a $115.6 million decrease in net current derivative liability at December 31, 2018 (from a net liability position of $60.9 million as at December 31, 2017 to a net asset position of $54.7 million). |

| • | The ratio of net debt to fund flows from operations remained consistent at 2.30 (2017 - 2.28) as the increase in net debt was offset by a partial year of contribution from the acquisitions that closed in 2018. |

Vermilion Energy Inc. ■ Page 10■ 2018 Management’s Discussion and Analysis

Commodity Prices

| | | Q4 2018 | | | Q3 2018 | | | Q4 2017 | | | Q4/18 vs.

Q3/18 | | Q4/18 vs.

Q4/17 | | 2018 | | | 2017 | | | 2018 vs.

2017 |

| Crude oil | | | | | | | | | | | | | | | | | | | | | | | | | | |

| WTI ($/bbl) | | | 77.71 | | | | 90.83 | | | | 70.43 | | | (14)% | | 10% | | | 83.94 | | | | 66.13 | | | 27% |

| WTI (US $/bbl) | | | 58.81 | | | | 69.50 | | | | 55.40 | | | (15)% | | 6% | | | 64.77 | | | | 50.95 | | | 27% |

| Edmonton Sweet index ($/bbl) | | | 42.96 | | | | 81.92 | | | | 68.98 | | | (48)% | | (38)% | | | 69.53 | | | | 62.94 | | | 10% |

| Edmonton Sweet index (US $/bbl) | | | 32.51 | | | | 62.68 | | | | 54.26 | | | (48)% | | (40)% | | | 53.65 | | | | 48.49 | | | 11% |

| Saskatchewan LSB index ($/bbl) | | | 58.18 | | | | 82.79 | | | | 68.70 | | | (30)% | | (15)% | | | 73.17 | | | | 62.10 | | | 18% |

| Saskatchewan LSB index (US $/bbl) | | | 44.03 | | | | 63.35 | | | | 54.04 | | | (30)% | | (19)% | | | 56.46 | | | | 47.85 | | | 18% |

| Dated Brent ($/bbl) | | | 89.54 | | | | 98.37 | | | | 78.05 | | | (9)% | | 15% | | | 92.07 | | | | 70.44 | | | 31% |

| Dated Brent (US $/bbl) | | | 67.76 | | | | 75.27 | | | | 61.39 | | | (10)% | | 10% | | | 71.04 | | | | 54.27 | | | 31% |

| Hardisty Heavy ($/bbl) | | | 15.28 | | | | 54.11 | | | | 49.19 | | | (72)% | | (69)% | | | 41.07 | | | | 45.67 | | | (10)% |

| Hardisty Heavy (US $/bbl) | | | 11.56 | | | | 41.40 | | | | 38.69 | | | (72)% | | (70)% | | | 31.69 | | | | 35.19 | | | (10)% |

| Natural gas | | | | | | | | | | | | | | | | | | | | | | | | | | |

| AECO ($/mcf) | | | 1.56 | | | | 1.19 | | | | 1.69 | | | 31% | | (8)% | | | 1.50 | | | | 2.16 | | | (31)% |

| NBP ($/mcf) | | | 11.03 | | | | 10.95 | | | | 8.70 | | | 1% | | 27% | | | 10.35 | | | | 7.49 | | | 38% |

| NBP (€/mcf) | | | 7.31 | | | | 7.20 | | | | 5.81 | | | 2% | | 26% | | | 6.76 | | | | 5.12 | | | 32% |

| TTF ($/mcf) | | | 10.91 | | | | 10.92 | | | | 8.36 | | | —% | | 31% | | | 10.23 | | | | 7.43 | | | 38% |

| TTF (€/mcf) | | | 7.23 | | | | 7.18 | | | | 5.58 | | | 1% | | 30% | | | 6.69 | | | | 5.07 | | | 32% |

| Henry Hub ($/mcf) | | | 4.82 | | | | 3.80 | | | | 3.73 | | | 27% | | 29% | | | 4.01 | | | | 4.04 | | | (1)% |

| Henry Hub (US $/mcf) | | | 3.65 | | | | 2.90 | | | | 2.93 | | | 26% | | 25% | | | 3.09 | | | | 3.11 | | | (1)% |

| Average exchange rates | | | | | | | | | | | | | | | | | | | | | | | | | | |

| CDN $/US $ | | | 1.32 | | | | 1.31 | | | | 1.27 | | | 1% | | 4% | | | 1.30 | | | | 1.30 | | | —% |

| CDN $/Euro | | | 1.51 | | | | 1.52 | | | | 1.50 | | | (1)% | | 1% | | | 1.53 | | | | 1.46 | | | 5% |

| Realized Prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil and condensate ($/bbl) | | | 66.19 | | | | 85.84 | | | | 74.12 | | | (23)% | | (11)% | | | 79.16 | | | | 67.00 | | | 18% |

| NGLs ($/bbl) | | | 25.69 | | | | 27.97 | | | | 29.28 | | | (8)% | | (12)% | | | 26.33 | | | | 25.00 | | | 5% |

| Natural gas ($/mcf) | | | 5.83 | | | | 5.35 | | | | 5.23 | | | 9% | | 11% | | | 5.45 | | | | 4.91 | | | 11% |

| Total ($/boe) | | | 48.90 | | | | 57.90 | | | | 47.49 | | | (16)% | | 3% | | | 52.95 | | | | 44.41 | | | 19% |

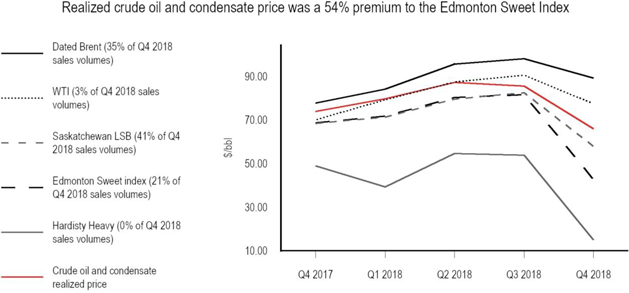

| • | Crude oil prices decreased throughout Q4 2018, driven by record global production levels and macroeconomic concerns. Quarter-over-quarter, WTI and Brent decreased by 14% and 9%, respectively, in Canadian dollar terms. Despite the end-of-year weakness in 2018, for the three months and year ended December 31, 2018, WTI increased 10% and 27%, respectively, in Canadian dollar terms versus the comparable periods in the prior year. Similarly, Brent increased 15% and 31%, respectively, in Canadian dollar terms for the three months and year ended December 31, 2018 versus the comparable periods in 2017. |

Vermilion Energy Inc. ■ Page 11■ 2018 Management’s Discussion and Analysis

| • | Western Canadian takeaway capacity constraints negatively impacted differentials in Q4 2018 versus Q3 2018; the Edmonton Sweet differential widened by $19.48/bbl, the Saskatchewan LSB differential widened by $14.78/bbl, and the Hardisty WCS differential widened by $19.15/bbl. |

| • | Vermilion's crude oil production benefits from light oil pricing and no exposure to significantly discounted heavy crude oil. Approximately 35% of our Q4 2018 crude oil and condensate production was priced at the Dated Brent index (which averaged a premium to WTI of US$8.95/bbl) while the remainder of our crude oil and condensate production was priced at the Saskatchewan LSB, Edmonton Sweet, and WTI indices. As a result, our Q4 2018 crude oil and condensate realized price of $66.19/bbl represented a 54% premium to the Edmonton Sweet index and a 333% premium to Hardisty Heavy. |

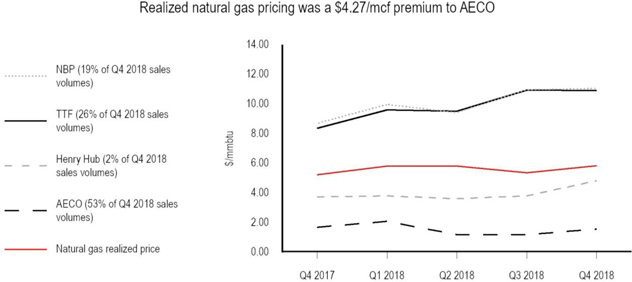

| • | European natural gas prices were relatively unchanged in Q4 2018 compared to Q3 2018. For the year ended December 31, 2018, TTF and NBP prices in Canadian dollar terms increased 38% compared to 2017. Competition from Asia for liquefied natural gas ("LNG") supply, strong demand from both the power sector and for storage injections, and surging carbon prices in the European Union, all played a role in 2018 price strength. |

| • | Natural gas prices at AECO increased by 31% in Q4 2018 as compared to Q3 2018. While the AECO gas market continues to face egress challenges, the seasonal shift from a summer quarter to a winter quarter drove stronger domestic gas demand. |

| • | For Q4 2018, average European natural gas prices represented a $9.41/mcf premium to AECO and a $6.15/mcf premium to Henry Hub pricing. Approximately 45% of our natural gas production in Q4 2018 benefited from this premium European pricing. As a result, our consolidated natural gas realized price was a $4.27/mcf premium to AECO and a $1.01/mcf premium to Henry Hub pricing. |

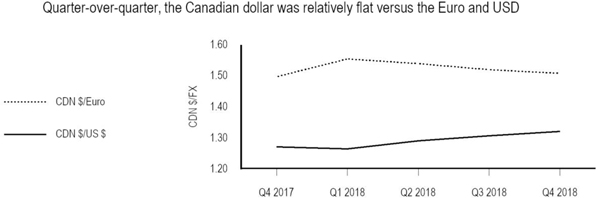

| • | For the three months ended December 31, 2018, the Canadian dollar weakened by 1% against the US dollar quarter-over-quarter. The annual average in 2018 was nearly unchanged versus 2017. |

| • | For the three months ended December 31, 2018, the Canadian dollar strengthened by 1% against the Euro quarter-over-quarter. The annual average in 2018 was 5% weaker versus 2017. |

Vermilion Energy Inc. ■ Page 12■ 2018 Management’s Discussion and Analysis

Canada Business Unit

Production and assets focused in West Pembina near Drayton Valley, Alberta and in southeast Saskatchewan and Manitoba.

| • | Potential for three significant resource plays sharing the same surface infrastructure in the West Pembina region in Alberta: |

| – | Mannville condensate-rich gas (2,400 - 2,700m depth) - in development phase |

| – | Cardium light oil (1,800m depth) - in development phase |

| – | Duvernay condensate-rich gas (3,200 - 3,400m depth) - no investment at present |

| • | Southeast Saskatchewan light oil development: |

| – | Targeting the Mississippian Midale (1,400 - 1,700m depth), Frobisher/Alida (1,200 - 1,400m depth) and Ratcliffe (1,800 - 1,900m) formations |

| Operational and financial review |

Canada business unit ($M except as indicated) | | Q4 2018 | | | Q3 2018 | | | Q4 2017 | | | Q4/18 vs.

Q3/18 | | Q4/18 vs.

Q4/17 | | 2018 | | | 2017 | | | 2018 vs.

2017 |

| Production and sales | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil and condensate (bbls/d) | | | 29,557 | | | | 28,477 | | | | 9,703 | | | 4% | | 205% | | | 21,154 | | | | 9,051 | | | 134% |

| NGLs (bbls/d) | | | 6,816 | | | | 6,126 | | | | 5,235 | | | 11% | | 30% | | | 5,914 | | | | 4,144 | | | 43% |

| Natural gas (mmcf/d) | | | 146.65 | | | | 136.77 | | | | 107.91 | | | 7% | | 36% | | | 129.37 | | | | 97.89 | | | 32% |

| Total (boe/d) | | | 60,814 | | | | 57,397 | | | | 32,923 | | | 6% | | 85% | | | 48,630 | | | | 29,510 | | | 65% |

| Production mix (% of total) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil and condensate | | | 49 | % | | | 50 | % | | | 29 | % | | | | | | | 43 | % | | | 31 | % | | |

| NGLs | | | 11 | % | | | 10 | % | | | 16 | % | | | | | | | 13 | % | | | 14 | % | | |

| Natural gas | | | 40 | % | | | 40 | % | | | 55 | % | | | | | | | 44 | % | | | 55 | % | | |

| Activity | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | | 90,211 | | | | 89,837 | | | | 26,865 | | | —% | | 236% | | | 277,857 | | | | 148,667 | | | 87% |

| Acquisitions | | | 12,233 | | | | 6,146 | | | | 788 | | | | | | | | 1,573,964 | | | | 22,011 | | | |

| Gross wells drilled | | | 72.00 | | | | 65.00 | | | | 6.00 | | | | | | | | 173.00 | | | | 44.00 | | | |

| Net wells drilled | | | 44.08 | | | | 58.97 | | | | 4.00 | | | | | | | | 135.93 | | | | 35.56 | | | |

| Financial results | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 186,308 | | | | 243,016 | | | | 94,522 | | | (23)% | | 97% | | | 671,172 | | | | 330,903 | | | 103% |

| Royalties | | | (25,584 | ) | | | (33,801 | ) | | | (9,301 | ) | | (24)% | | 175% | | | (84,696 | ) | | | (33,258 | ) | | 155% |

| Transportation | | | (11,129 | ) | | | (9,057 | ) | | | (4,836 | ) | | 23% | | 130% | | | (29,912 | ) | | | (17,368 | ) | | 72% |

| Operating | | | (62,064 | ) | | | (55,577 | ) | | | (22,356 | ) | | 12% | | 178% | | | (177,499 | ) | | | (80,444 | ) | | 121% |

| General and administration | | | (2,150 | ) | | | (1,316 | ) | | | (2,540 | ) | | 63% | | (15)% | | | (6,057 | ) | | | (9,604 | ) | | (37)% |

| Fund flows from operations | | | 85,381 | | | | 143,265 | | | | 55,489 | | | (40)% | | 54% | | | 373,008 | | | | 190,229 | | | 96% |

| Netbacks ($/boe) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 33.30 | | | | 46.02 | | | | 31.21 | | | (28)% | | 7% | | | 37.81 | | | | 30.72 | | | 23% |

| Royalties | | | (4.57 | ) | | | (6.40 | ) | | | (3.07 | ) | | (29)% | | 49% | | | (4.77 | ) | | | (3.09 | ) | | 54% |

| Transportation | | | (1.99 | ) | | | (1.72 | ) | | | (1.60 | ) | | 16% | | 24% | | | (1.69 | ) | | | (1.61 | ) | | 5% |

| Operating | | | (11.09 | ) | | | (10.52 | ) | | | (7.38 | ) | | 5% | | 50% | | | (10.00 | ) | | | (7.47 | ) | | 34% |

| General and administration | | | (0.38 | ) | | | (0.25 | ) | | | (0.84 | ) | | 52% | | (55)% | | | (0.34 | ) | | | (0.89 | ) | | (62)% |

| Fund flows from operations netback | | | 15.27 | | | | 27.13 | | | | 18.32 | | | (44)% | | (17)% | | | 21.01 | | | | 17.66 | | | 19% |

| Realized prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil and condensate ($/bbl) | | | 54.04 | | | | 79.86 | | | | 69.20 | | | (32)% | | (22)% | | | 70.16 | | | | 63.41 | | | 11% |

| NGLs ($/bbl) | | | 25.53 | | | | 27.82 | | | | 29.18 | | | (8)% | | (13)% | | | 26.20 | | | | 25.00 | | | 5% |

| Natural gas ($/mcf) | | | 1.73 | | | | 1.44 | | | | 1.88 | | | 20% | | (8)% | | | 1.54 | | | | 2.34 | | | (34)% |

| Total ($/boe) | | | 33.30 | | | | 46.02 | | | | 31.21 | | | (28)% | | 7% | | | 37.81 | | | | 30.72 | | | 23% |

| Reference prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| WTI (US $/bbl) | | | 58.81 | | | | 69.50 | | | | 55.40 | | | (15)% | | 6% | | | 64.77 | | | | 50.95 | | | 27% |

| Edmonton Sweet index ($/bbl) | | | 42.96 | | | | 81.92 | | | | 68.98 | | | (48)% | | (38)% | | | 69.53 | | | | 62.94 | | | 10% |

| Saskatchewan LSB index ($/bbl) | | | 58.18 | | | | 82.79 | | | | 68.70 | | | (30)% | | (15)% | | | 73.17 | | | | 62.10 | | | 18% |

| AECO ($/mcf) | | | 1.56 | | | | 1.19 | | | | 1.69 | | | 31% | | (8)% | | | 1.50 | | | | 2.16 | | | (31)% |

Vermilion Energy Inc. ■ Page 13■ 2018 Management’s Discussion and Analysis

Production

| • | Q4 2018 production increased 6% from the prior quarter due to strong operating performance and new well completions from our Saskatchewan and Alberta assets. Quarterly production increased 82% year-over-year primarily due to our acquisition of Spartan Energy Corp. in May 2018. |

| • | Production in Alberta averaged approximately 34,000 boe/d in Q4 2018, an increase of 4% quarter-over-quarter. |

| • | Production in Saskatchewan averaged approximately 26,800 boe/d in Q4 2018, an increase of 9% quarter-over-quarter. |

Activity review

| • | Vermilion drilled 43 (41.1 net) operated wells and participated in the drilling of 29 (2.9 net) non-operated wells in Canada during Q4 2018. |

Alberta

| – | In Q4 2018, we drilled or participated in nine (8.9 net) operated and two (0.4 net) non-operated wells, completed four (3.9 net) operated and three (0.8 net) non-operated wells, and brought on production four (4.0 net) operated and four (1.1 net) non-operated wells in Alberta. |

| – | In 2018, we drilled or participated in 27 (23.4 net) wells in Alberta, which included the drilling of 23 (20.7 net) Mannville wells. |

Saskatchewan

| – | In Q4 2018, we drilled or participated in 34 (32.3 net) operated wells and 27 (2.5 net) non-operated wells, completed 40 (37.3 net) operated and 26 (2.8 net) non-operated wells, and brought 51 (48.3 net) operated and 27 (3.2 net) non-operated wells on production. |

| – | In 2018, we drilled or participated in 146 (112.6 net) wells in Saskatchewan. |

| • | On May 28, 2018, Vermilion acquired 100% of the issued and outstanding common shares of Spartan, a publicly traded southeast Saskatchewan oil and gas producer. Consideration consisted of the issuance of 27.9 million Vermilion common shares valued at approximately $1.2 billion (based on the closing price per Vermilion common share of $44.30 on the Toronto Stock Exchange on May 28, 2018). Vermilion also assumed approximately $172 million of Spartan's outstanding debt at the time the transaction closed. |

Sales

| • | The realized price for our crude oil and condensate production in Canada is linked to WTI subject to market conditions in western Canada (as reflected by the Saskatchewan LSB index price in Saskatchewan and the Edmonton Sweet index price in Alberta). The realized price of our natural gas in Canada is based on the AECO index. |

| • | Q4 2018 sales per boe decreased 28% compared to Q3 2018 consistent with the decrease in crude oil and condensate pricing. Quarter-over-quarter, our crude oil and condensate production mix remained stable at approximately 50% of production. |

| • | For the year ended December 31, 2018, sales per boe increased versus 2017 due to increased Saskatchewan LSB and Edmonton Sweet index pricing coupled with an increased weighting towards higher-priced crude oil and condensate production. |

Royalties

| • | Royalties as a percentage of sales for the three months and year ended December 31, 2018 of 13.7% and 12.6%, respectively, increased from the comparable periods in 2017 due to the impact of the Spartan assets, which have higher associated royalty rates. |

Transportation

| • | Transportation expense for the three months and year ended December 31, 2018 increased on a per unit basis versus all comparable periods due to an increase in production that incurs higher transportation expense. |

Operating

| • | Operating expense increased in Q4 2018 versus Q3 2018 on both a dollar and per unit basis. On a dollar basis, this increase was due to higher production volumes and the per unit increase was caused by a favourable adjustment recorded in the prior quarter. |

| • | For the three months and year ended December 31, 2018, operating expense increased on both a dollar and per unit basis versus the comparable periods in 2017. On a dollar basis, the increase in operating expense was driven by higher production volumes during Q4 2018. On a per unit basis, the increase in operating expense was primarily attributable to the impact of production from the Spartan assets, which have higher associated per unit operating expense. |

Vermilion Energy Inc. ■ Page 14■ 2018 Management’s Discussion and Analysis

France Business Unit

| • | Largest oil producer in France, constituting approximately three-quarters of domestic oil production. |

| • | Low base decline producing assets comprised of large conventional oil fields with high working interests located in the Aquitaine and Paris Basins. |

| • | Identified inventory of workover, infill drilling, and secondary recovery opportunities. |

| Operational and financial review |

France business unit

($M except as indicated) | | Q4 2018 | | | Q3 2018 | | | Q4 2017 | | | Q4/18 vs.

Q3/18 | | Q4/18 vs.

Q4/17 | | 2018 | | | 2017 | | | 2018 vs.

2017 |

| Production | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil (bbls/d) | | | 11,317 | | | | 11,407 | | | | 11,215 | | | (1)% | | 1% | | | 11,362 | | | | 11,084 | | | 3% |

| Natural gas (mmcf/d) | | | 0.82 | | | | — | | | | — | | | 100% | | 100% | | | 0.21 | | | | — | | | 100% |

| Total (boe/d) | | | 11,454 | | | | 11,407 | | | | 11,215 | | | —% | | 2% | | | 11,396 | | | | 11,085 | | | 3% |

| Sales | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil (bbls/d) | | | 10,975 | | | | 11,482 | | | | 11,397 | | | (4)% | | (4)% | | | 11,012 | | | | 10,950 | | | 1% |

| Natural gas (mmcf/d) | | | 0.82 | | | | — | | | | — | | | 100% | | 100% | | | 0.21 | | | | — | | | 100% |

| Total (boe/d) | | | 11,111 | | | | 11,482 | | | | 11,397 | | | (3)% | | (3)% | | | 11,047 | | | | 10,950 | | | 1% |

| Inventory (mbbls) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Opening crude oil inventory | | | 293 | | | | 300 | | | | 214 | | | | | | | | 197 | | | | 148 | | | |

| Crude oil production | | | 1,041 | | | | 1,049 | | | | 1,032 | | | | | | | | 4,147 | | | | 4,046 | | | |

| Crude oil sales | | | (1,009 | ) | | | (1,056 | ) | | | (1,049 | ) | | | | | | | (4,019 | ) | | | (3,997 | ) | | |

| Closing crude oil inventory | | | 325 | | | | 293 | | | | 197 | | | | | | | | 325 | | | | 197 | | | |

| Activity | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | | 17,008 | | | | 15,779 | | | | 20,027 | | | 8% | | (15)% | | | 79,758 | | | | 73,381 | | | 9% |

| Gross wells drilled | | | — | | | | — | | | | 2.00 | | | | | | | | 5.00 | | | | 7.00 | | | |

| Net wells drilled | | | — | | | | — | | | | 2.00 | | | | | | | | 5.00 | | | | 7.00 | | | |

| Financial results | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 85,889 | | | | 100,840 | | | | 78,778 | | | (15)% | | 9% | | | 360,602 | | | | 268,103 | | | 35% |

| Royalties | | | (11,976 | ) | | | (12,765 | ) | | | (10,599 | ) | | (6)% | | 13% | | | (46,781 | ) | | | (28,565 | ) | | 64% |

| Transportation | | | (3,242 | ) | | | (2,013 | ) | | | (4,475 | ) | | 61% | | (28)% | | | (10,426 | ) | | | (14,627 | ) | | (29)% |

| Operating | | | (14,015 | ) | | | (13,733 | ) | | | (14,332 | ) | | 2% | | (2)% | | | (54,690 | ) | | | (51,002 | ) | | 7% |

| General and administration | | | (3,792 | ) | | | (3,365 | ) | | | (4,259 | ) | | 13% | | (11)% | | | (14,170 | ) | | | (13,585 | ) | | 4% |

| Current income taxes | | | (884 | ) | | | (6,913 | ) | | | (2,348 | ) | | (87)% | | (62)% | | | (15,084 | ) | | | (10,556 | ) | | 43% |

| Fund flows from operations | | | 51,980 | | | | 62,051 | | | | 42,765 | | | (16)% | | 22% | | | 219,451 | | | | 149,768 | | | 47% |

| Netbacks ($/boe) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 84.02 | | | | 95.46 | | | | 75.13 | | | (12)% | | 12% | | | 89.44 | | | | 67.08 | | | 33% |

| Royalties | | | (11.72 | ) | | | (12.08 | ) | | | (10.11 | ) | | (3)% | | 16% | | | (11.60 | ) | | | (7.15 | ) | | 62% |

| Transportation | | | (3.17 | ) | | | (1.91 | ) | | | (4.27 | ) | | 66% | | (26)% | | | (2.59 | ) | | | (3.66 | ) | | (29)% |

| Operating | | | (13.71 | ) | | | (13.00 | ) | | | (13.67 | ) | | 5% | | —% | | | (13.56 | ) | | | (12.76 | ) | | 6% |

| General and administration | | | (3.71 | ) | | | (3.19 | ) | | | (4.06 | ) | | 16% | | (9)% | | | (3.51 | ) | | | (3.40 | ) | | 3% |

| Current income taxes | | | (0.86 | ) | | | (6.54 | ) | | | (2.24 | ) | | (87)% | | (62)% | | | (3.74 | ) | | | (2.64 | ) | | 42% |

| Fund flows from operations netback | | | 50.85 | | | | 58.74 | | | | 40.78 | | | (13)% | | 25% | | | 54.44 | | | | 37.47 | | | 45% |

| Reference prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Dated Brent (US $/bbl) | | | 67.76 | | | | 75.27 | | | | 61.39 | | | (10)% | | 10% | | | 71.04 | | | | 54.27 | | | 31% |

| Dated Brent ($/bbl) | | | 89.54 | | | | 98.37 | | | | 78.05 | | | (9)% | | 15% | | | 92.07 | | | | 70.44 | | | 31% |

Vermilion Energy Inc. ■ Page 15■ 2018 Management’s Discussion and Analysis

Production

| • | Q4 2018 production increased slightly from the prior quarter due continued strong performance from the 2018 Champotran wells and continued workover success in the Aquitaine Basin. Production increased 2% year-over-year primarily due to production additions from our 2018 drilling program. |

Activity review

| • | Our 2018 capital program included the drilling and completion of two (2.0 net) Neocomian wells and three (3.0 net) Champotran wells in the first quarter of 2018. In addition to the drilling and completion activity, we continued our workover and optimization programs in the Aquitaine and Paris Basins throughout 2018. |

Sales

| • | Crude oil in France is priced with reference to Dated Brent. |

| • | Q4 2018 sales per boe decreased versus Q3 2018, consistent with the weakening in the Dated Brent reference price. |

| • | For the three months and year ended December 31, 2018 versus the comparable periods in the prior year, the increase in sales per boe was consistent with increases in the Dated Brent benchmark price. |

Royalties

| • | Royalties in France relate to two components: RCDM (levied on units of production and not subject to changes in commodity prices) and R31 (based on a percentage of sales). |

| • | Royalties as a percentage of sales was 13.9% in Q4 2018 compared to 12.7% in Q3 2018. This increase was due the impact of fixed per-unit RCDM royalties relative to lower revenues resulting from weaker commodity prices. |

| • | For the three months and year ended December 31, 2018, royalties as a percentage of sales of 13.9% and 13.0% increased from 13.5% and 10.7%, respectively, in the comparable periods in the prior year. These increases were due to the impact of a royalty rate increase enacted in 2017. |

Transportation

| • | Transportation expense increased in Q4 2018 compared to Q3 2018 due to higher pipeline and terminal maintenance work performed in Q4 2018. |

| • | Transportation expense for the three months and year ended December 31, 2018 decreased versus the comparable periods in the prior year, primarily due to the impact of IFRS 16 adoption in 2018. Please refer to "Recently Adopted Accounting Pronouncements" for additional information. |

Operating

| • | Operating expense in Q4 2018 was relatively consistent with Q3 2018 and Q4 2017 on a dollar basis. On a per unit basis, operating expense increased in Q4 2018 versus Q3 2018 due to the impact of fixed costs on lower sales volumes, which was a result of shipment timing. |

| • | For the year ended December 31, 2018, operating expense increased versus 2017 on both a dollar and per unit basis. These increases were primarily due to the impact of a stronger Euro versus the Canadian dollar, increased cost and usage of electricity, and higher maintenance activity in 2018. |

General and administration

| • | Fluctuations in general and administration expense for all comparable periods were due to the timing of expenditures and allocations from our corporate segment. |

Current income taxes

| • | In France, current income taxes are applied to taxable income, after eligible deductions, at a statutory rate of 34.4%. |

| • | Current income taxes for the year ended December 31, 2018 versus the comparative period were higher mainly due to higher Dated Brent prices resulting in increased sales. |

| • | Current income taxes for Q4 2018 versus Q3 2018 and Q4 2017 were lower due to increased tax deductions for depletion. |

| • | On December 21, 2017, the French Parliament approved the Finance Bill for 2018. The Finance Bill for 2018 provides for a progressive decrease of the French corporate income tax rate from 34.4% to 25.8% by 2022, with the first reduction planned for 2019 to 32.0%. |

Vermilion Energy Inc. ■ Page 16■ 2018 Management’s Discussion and Analysis

Netherlands Business Unit

| • | Entered the Netherlands in 2004. |

| • | Second largest onshore operator. |

| • | Interests include 26 onshore licenses (all operated) and 17 offshore licenses (all non-operated). |

| • | Licenses include more than 930,000 net acres of land, 90% of which is undeveloped. |

| Operational and financial review |

Netherlands business unit ($M except as indicated) | | Q4 2018 | | | Q3 2018 | | | Q4 2017 | | | Q4/18 vs.

Q3/18 | | Q4/18 vs.

Q4/17 | | 2018 | | | 2017 | | | 2018 vs.

2017 |

| Production and sales | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Condensate (bbls/d) | | | 112 | | | | 84 | | | | 105 | | | 33% | | 7% | | | 90 | | | | 90 | | | —% |

| Natural gas (mmcf/d) | | | 51.82 | | | | 44.37 | | | | 55.66 | | | 17% | | (7)% | | | 46.13 | | | | 40.54 | | | 14% |

| Total (boe/d) | | | 8,749 | | | | 7,479 | | | | 9,381 | | | 17% | | (7)% | | | 7,779 | | | | 6,847 | | | 14% |

| Activity | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | | 2,454 | | | | 5,056 | | | | 12,300 | | | (51)% | | (80)% | | | 17,483 | | | | 31,575 | | | (45)% |

| Acquisitions | | | (7,860 | ) | | | 2,874 | | | | (38 | ) | | | | | | | (2,087 | ) | | | (24 | ) | | |

| Gross wells drilled | | | — | | | | — | | | | — | | | | | | | | — | | | | 2.00 | | | |

| Net wells drilled | | | — | | | | — | | | | — | | | | | | | | — | | | | 1.02 | | | |

| Financial results | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 52,937 | | | | 41,793 | | | | 40,914 | | | 27% | | 29% | | | 165,916 | | | | 108,060 | | | 54% |

| Royalties | | | (537 | ) | | | (1,049 | ) | | | (647 | ) | | (49)% | | (17)% | | | (3,181 | ) | | | (1,722 | ) | | 85% |

| Operating | | | (6,765 | ) | | | (5,812 | ) | | | (6,981 | ) | | 16% | | (3)% | | | (26,681 | ) | | | (21,212 | ) | | 26% |

| General and administration | | | (709 | ) | | | (320 | ) | | | (546 | ) | | 122% | | 30% | | | (1,947 | ) | | | (2,212 | ) | | (12)% |

| Current income taxes | | | (7,492 | ) | | | 1,729 | | | | 6,975 | | | N/A | | N/A | | | (16,561 | ) | | | 3,331 | | | N/A |

| Fund flows from operations | | | 37,434 | | | | 36,341 | | | | 39,715 | | | 3% | | (6)% | | | 117,546 | | | | 86,245 | | | 36% |

| Netbacks ($/boe) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 65.77 | | | | 60.74 | | | | 47.41 | | | 8% | | 39% | | | 58.44 | | | | 43.24 | | | 35% |

| Royalties | | | (0.67 | ) | | | (1.52 | ) | | | (0.75 | ) | | (56)% | | (11)% | | | (1.12 | ) | | | (0.69 | ) | | 62% |

| Operating | | | (8.40 | ) | | | (8.45 | ) | | | (8.09 | ) | | (1)% | | 4% | | | (9.40 | ) | | | (8.49 | ) | | 11% |

| General and administration | | | (0.88 | ) | | | (0.47 | ) | | | (0.63 | ) | | 87% | | 40% | | | (0.69 | ) | | | (0.89 | ) | | (22)% |

| Current income taxes | | | (9.31 | ) | | | 2.51 | | | | 8.08 | | | N/A | | N/A | | | (5.83 | ) | | | 1.33 | | | N/A |

| Fund flows from operations netback | | | 46.51 | | | | 52.81 | | | | 46.02 | | | (12)% | | 1% | | | 41.40 | | | | 34.50 | | | 20% |

| Realized prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Condensate ($/bbl) | | | 69.95 | | | | 82.32 | | | | 66.38 | | | (15)% | | 5% | | | 74.85 | | | | 56.90 | | | 32% |

| Natural gas ($/mcf) | | | 10.95 | | | | 10.08 | | | | 7.87 | | | 9% | | 39% | | | 9.71 | | | | 7.18 | | | 35% |

| Total ($/boe) | | | 65.77 | | | | 60.74 | | | | 47.41 | | | 8% | | 39% | | | 58.44 | | | | 43.24 | | | 35% |

| Reference prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| TTF ($/mcf) | | | 10.91 | | | | 10.92 | | | | 8.36 | | | —% | | 31% | | | 10.23 | | | | 7.43 | | | 38% |

| TTF (€/mcf) | | | 7.23 | | | | 7.18 | | | | 5.58 | | | 1% | | 30% | | | 6.69 | | | | 5.07 | | | 32% |

Vermilion Energy Inc. ■ Page 17■ 2018 Management’s Discussion and Analysis

Production

| • | Q4 2018 production increased 17% from the prior quarter due to the contribution of a full quarter of production from the Eesveen-02 well (60% working interest), which we brought on production at a restricted rate of 10 mmcf/d net late in the third quarter of 2018. Production decreased 7% year-over-year primarily due to natural declines and permitting delays of certain drilling and workover activities, which impacted 2018 full-year volumes. |

Activity review

| • | Our 2018 capital activity was primarily focused on planned workovers, facilities maintenance, and advancing our drilling permits ahead of our 2019 drilling campaign. |

| • | In September 2018 we brought the Eesveen-02 well on production at a restricted rate of 10 mmcf/d net. |

| • | In Q4 2018 we consolidated working interests on some of our existing assets and added minor working interest ownerships in several non-operated offshore licenses. The acquisition contributed approximately 200 boe/d to our Q4 2018 production results. Consideration for the acquisition required no cash payment but included the assumption of the full ARO associated with the incremental working interest. The ARO is estimated at a PV10 of €20 million. At closing we received a cash payment and positive working capital totaling €5.8 million due to the transaction having an effective date of January 1, 2018. |

Sales

| • | The price of our natural gas in the Netherlands is based on the TTF index. |

| • | Q4 2018 sales increased on a dollar basis versus Q3 2018 due to higher sales volumes coupled with increased TTF commodity pricing. Sales for the year ended December 31, 2018 increased versus the same period in the prior year due to the stronger TTF reference price in 2018, as well as an increase in sold volumes in 2018. |

| • | For the three months and year ended December 31, 2018, sales per boe increased versus all comparable periods, consistent with increases in the TTF reference price. |

Royalties

| • | In the Netherlands, certain wells are subject to overriding royalties while some wells are subject to royalties that take effect only when specified production levels are exceeded. As such, royalty expense may fluctuate from period to period depending on the amount of production from those wells. Royalties in the three months and year ended December 31, 2018 represented 1.0% and 1.9% of sales, respectively. |

Transportation

| • | Our production in the Netherlands is not subject to transportation expense as gas is sold at the plant gate. |

Operating

| • | Q4 2018 operating expense increased on a dollar basis versus Q3 2018 due to a prior period adjustment booked in Q4 2018 relating to power usage, as well as increased permitting costs. On a per boe basis, operating expense was relatively consistent with the prior quarter as higher costs were offset by an increase in sales volumes. Operating expense on a per unit basis increased Q4 2018 versus Q4 2017 due to the impact of fixed costs over lower sales volumes. |

| • | For the year ended December 31, 2018, operating expense increased on a dollar basis versus the comparable period in 2017 primarily due to increased maintenance activity coupled with an unfavourable foreign exchange impact. On a per unit basis, operating expense increased due to the strengthening of the Euro versus the Canadian Dollar. |

General and administration

| • | Fluctuations in general and administration expense for all comparable periods were due to the timing of expenditures and allocations from our corporate segment. |

Current income taxes

| • | In the Netherlands, current income taxes are applied to taxable income, after eligible deductions and a 10% uplift deduction applied to operating expenses, eligible general and administration and tax deductions for depletion and asset retirement obligations, at a tax rate of 50%. |

| • | Current income taxes in Q4 2018 and for the year ended December 31, 2018 versus the comparative periods were higher mainly due to higher TTF prices and volumes resulting in increased sales and an increased tax deduction taken in Q4 2017 for future asset retirement obligations resulting from a reduction in the applicable discount rate assumption. |

| • | On December 18, 2018, the Dutch government approved the 2019 Tax Plan. The Bill provides for reduced corporate tax rates from 25.0% to 20.5% by 2021, with the first reduction planned for 2020 to 22.55%. Due to the tax regime applicable to natural gas producers in the Netherlands, the reduction to the corporate tax rate is not expected to have a material impact to Vermilion taxes in the Netherlands. |

Vermilion Energy Inc. ■ Page 18■ 2018 Management’s Discussion and Analysis

Germany Business Unit

| • | Entered Germany in 2014 through the acquisition of a non-operated natural gas producing property. |

| • | Executed a significant exploration license farm-in agreement in 2015 and acquired operated producing properties in 2016. |

| • | Producing assets consist of seven gas and eight oil producing fields with extensive infrastructure in place. |

| • | Significant land position of approximately 1.2 million net acres (97% undeveloped). |

| Operational and financial review |

Germany business unit ($M except as indicated) | | Q4 2018 | | | Q3 2018 | | | Q4 2017 | | | Q4/18 vs.

Q3/18 | | Q4/18 vs.

Q4/17 | | 2018 | | | 2017 | | | 2018 vs.

2017 |

| Production | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil (bbls/d) | | | 913 | | | | 1,019 | | | | 1,148 | | | (10)% | | (20)% | | | 1,004 | | | | 1,060 | | | (5)% |

| Natural gas (mmcf/d) | | | 16.94 | | | | 14.88 | | | | 18.19 | | | 14% | | (7)% | | | 15.66 | | | | 19.39 | | | (19)% |

| Total (boe/d) | | | 3,736 | | | | 3,498 | | | | 4,180 | | | 7% | | (11)% | | | 3,614 | | | | 4,291 | | | (16)% |

| Sales | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil (bbls/d) | | | 970 | | | | 929 | | | | 1,067 | | | 4% | | (9)% | | | 1,065 | | | | 993 | | | 7% |

| Natural gas (mmcf/d) | | | 16.94 | | | | 14.88 | | | | 20.12 | | | 14% | | (16)% | | | 15.66 | | | | 19.79 | | | (21)% |

| Total (boe/d) | | | 3,794 | | | | 3,408 | | | | 4,420 | | | 11% | | (14)% | | | 3,675 | | | | 4,292 | | | (14)% |

| Production mix (% of total) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil | | | 24 | % | | | 29 | % | | | 27 | % | | | | | | | 28 | % | | | 25 | % | | |

| Natural gas | | | 76 | % | | | 71 | % | | | 73 | % | | | | | | | 72 | % | | | 75 | % | | |

| Activity | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | | 4,580 | | | | 6,497 | | | | 5,279 | | | (30)% | | (13)% | | | 15,806 | | | | 9,531 | | | 66% |

| Acquisitions | | | 706 | | | | 959 | | | | — | | | | | | | | 1,665 | | | | — | | | |

| Financial results | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 21,897 | | | | 21,052 | | | | 18,898 | | | 4% | | 16% | | | 82,449 | | | | 68,696 | | | 20% |

| Royalties | | | (1,190 | ) | | | (2,448 | ) | | | (1,798 | ) | | (51)% | | (34)% | | | (6,626 | ) | | | (6,655 | ) | | —% |

| Transportation | | | (1,452 | ) | | | (1,191 | ) | | | (1,164 | ) | | 22% | | 25% | | | (6,420 | ) | | | (6,207 | ) | | 3% |

| Operating | | | (6,615 | ) | | | (4,863 | ) | | | (6,025 | ) | | 36% | | 10% | | | (23,048 | ) | | | (20,176 | ) | | 14% |

| General and administration | | | (2,308 | ) | | | (2,073 | ) | | | (2,080 | ) | | 11% | | 11% | | | (7,401 | ) | | | (7,767 | ) | | (5)% |

| Fund flows from operations | | | 10,332 | | | | 10,477 | | | | 7,831 | | | (1)% | | 32% | | | 38,954 | | | | 27,891 | | | 40% |

| Netbacks ($/boe) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 62.74 | | | | 67.15 | | | | 50.22 | | | (7)% | | 25% | | | 61.47 | | | | 44.37 | | | 39% |

| Royalties | | | (3.41 | ) | | | (7.81 | ) | | | (4.78 | ) | | (56)% | | (29)% | | | (4.94 | ) | | | (4.30 | ) | | 15% |

| Transportation | | | (4.16 | ) | | | (3.80 | ) | | | (3.09 | ) | | 9% | | 35% | | | (4.79 | ) | | | (4.01 | ) | | 19% |

| Operating | | | (18.95 | ) | | | (15.51 | ) | | | (16.01 | ) | | 22% | | 18% | | | (17.18 | ) | | | (13.03 | ) | | 32% |

| General and administration | | | (6.61 | ) | | | (6.61 | ) | | | (5.53 | ) | | —% | | 20% | | | (5.52 | ) | | | (5.02 | ) | | 10% |

| Fund flows from operations netback | | | 29.61 | | | | 33.42 | | | | 20.81 | | | (11)% | | 42% | | | 29.04 | | | | 18.01 | | | 61% |

| Realized prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil ($/bbl) | | | 75.53 | | | | 92.45 | | | | 72.58 | | | (18)% | | 4% | | | 84.14 | | | | 63.91 | | | 32% |

| Natural gas ($/mcf) | | | 9.72 | | | | 9.61 | | | | 7.07 | | | 1% | | 37% | | | 8.70 | | | | 6.38 | | | 36% |

| Total ($/boe) | | | 62.74 | | | | 67.15 | | | | 50.22 | | | (7)% | | 25% | | | 61.47 | | | | 44.37 | | | 39% |

| Reference prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Dated Brent (US $/bbl) | | | 67.76 | | | | 75.27 | | | | 61.39 | | | (10)% | | 10% | | | 71.04 | | | | 54.27 | | | 31% |

| Dated Brent ($/bbl) | | | 89.54 | | | | 98.37 | | | | 78.05 | | | (9)% | | 15% | | | 92.07 | | | | 70.44 | | | 31% |

| TTF ($/mcf) | | | 10.91 | | | | 10.92 | | | | 8.36 | | | —% | | 31% | | | 10.23 | | | | 7.43 | | | 38% |

| TTF (€/mcf) | | | 7.23 | | | | 7.18 | | | | 5.58 | | | 1% | | 30% | | | 6.69 | | | | 5.07 | | | 32% |

Vermilion Energy Inc. ■ Page 19■ 2018 Management’s Discussion and Analysis

Production

| • | Q4 2018 production increased 7% from the prior quarter due to the restoration of a non-operated gas processing facility in the prior quarter, partially offset by other minor unplanned downtime events on our non-operated oil assets. Production decreased 11% year-over-year due to downtime at a non-operated gas processing plant that began in the middle of Q2 2018 and continued through the middle of Q3 2018. |

Activity review

| • | Our 2018 capital program focused on permitting and other pre-drill activities associated with our first operated well in Germany, Burgmoor Z5 (46% working interest) in the Dümmersee-Uchte area, which we expect to drill in 2019, in addition to performing workovers opportunities on our operated asset base. |

Sales

| • | The price of our natural gas in Germany is based on the NCG and GPL indexes, which are both highly correlated to the TTF benchmark. Crude oil in Germany is priced with reference to Dated Brent. |

| • | Sales per boe for Q4 2018 decreased versus Q3 2018, and increased versus the comparable periods in 2017, consistent with fluctuations in crude oil and natural gas benchmark prices. |

| • | Sales per boe for 2018 increased versus 2017 due to the increase in crude oil and natural gas benchmark prices. |

Royalties

| • | Our production in Germany is subject to state and private royalties on sales after certain eligible deductions. |

| • | Royalties as a percentage of sales were lower in Q4 2018 versus Q3 2018 and Q4 2017 due to an annual rate adjustment recorded in Q4 2018. Royalties as a percentage of sales for the year ended December 31, 2018 were lower than the comparable period in the prior year due to increased production of crude oil with lower associated royalty rates. |

Transportation

| • | Transportation expense in Germany relates to costs incurred to deliver natural gas from the processing facility to the customer and deliver crude oil to the refinery. |

| • | Transportation expense in Q4 2018 was higher than Q3 2018 due to the impact of a favourable prior period adjustment recorded in Q3 2018. Transportation expense increased versus Q4 2017 due to higher volumes of crude oil transported in Q4 2018. |

| • | Transportation expense for the year ended December 31, 2018 increased slightly versus the comparable period in the prior year due to higher tariffs on crude oil transport in 2018. |

Operating

| • | Operating expense on a per unit basis in Q4 2018 was higher versus Q3 2018 due to higher activity levels at non-operated properties and increased gas processing fees. |

| • | Operating expense on a per unit basis increased for the three months and year ended December 31, 2018, versus the comparable periods in the prior year. The increase was primarily due to increased gas processing tariffs, the impact of fixed costs on lower volumes and the impact of a stronger Euro versus the Canadian dollar. |

General and administration

| • | Fluctuations in general and administration expense for all comparable periods were due to the timing of expenditures and allocations from our corporate segment. |

Current income taxes

| • | As a result of our tax pools in Germany, we do not expect to incur current income taxes for 2019 in the German Business Unit. This is subject to change in response to production variations, commodity price fluctuations, the timing of capital expenditures, and other eligible in-country adjustments. |

Vermilion Energy Inc. ■ Page 20■ 2018 Management’s Discussion and Analysis

Ireland Business Unit

| • | Entered Ireland in 2009 with an investment in the offshore Corrib gas field. |

| • | The Corrib gas field is located offshore northwest Ireland and comprises six offshore wells, offshore and onshore sales and transportation pipeline segments, as well as a natural gas processing facility. |

| • | In Q4 2018, Vermilion assumed operatorship of the Corrib Natural Gas Project (the "Corrib Project") and increased its ownership stake by 1.5% to 20% following the completion of a strategic partnership with Canada Pension Plan Investment Board (“CPPIB”). |

| Operational and financial review |

Ireland business unit ($M except as indicated) | | Q4 2018 | | | Q3 2018 | | | Q4 2017 | | | Q4/18 vs.

Q3/18 | | Q4/18 vs.

Q4/17 | | 2018 | | | 2017 | | | 2018 vs.

2017 |

| Production and sales | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Natural gas (mmcf/d) | | | 52.03 | | | | 51.38 | | | | 56.23 | | | 1% | | (7)% | | | 55.17 | | | | 58.43 | | | (6)% |

| Total (boe/d) | | | 8,672 | | | | 8,563 | | | | 9,372 | | | 1% | | (7)% | | | 9,195 | | | | 9,737 | | | (6)% |

| Activity | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | | 140 | | | | (50 | ) | | | 327 | | | N/A | | (57)% | | | 224 | | | | 551 | | | (59)% |

| Acquisitions | | | (5,572 | ) | | | — | | | | — | | | | | | | | (5,572 | ) | | | — | | | |

| Financial results | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 53,385 | | | | 50,228 | | | | 43,793 | | | 6% | | 22% | | | 205,150 | | | | 153,330 | | | 34% |

| Transportation | | | (1,115 | ) | | | (1,460 | ) | | | (1,496 | ) | | (24)% | | (25)% | | | (5,129 | ) | | | (5,205 | ) | | (1)% |

| Operating | | | (4,497 | ) | | | (3,354 | ) | | | (2,977 | ) | | 34% | | 51% | | | (15,366 | ) | | | (17,596 | ) | | (13)% |

| General and administration | | | (2,037 | ) | | | (3,597 | ) | | | (517 | ) | | (43)% | | 294% | | | (8,386 | ) | | | (2,320 | ) | | 261% |

| Fund flows from operations | | | 45,736 | | | | 41,817 | | | | 38,803 | | | 9% | | 18% | | | 176,269 | | | | 128,209 | | | 37% |

| Netbacks ($/boe) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 66.91 | | | | 63.76 | | | | 50.79 | | | 5% | | 32% | | | 61.12 | | | | 43.14 | | | 42% |

| Transportation | | | (1.40 | ) | | | (1.85 | ) | | | (1.74 | ) | | (24)% | | (20)% | | | (1.53 | ) | | | (1.46 | ) | | 5% |

| Operating | | | (5.64 | ) | | | (4.26 | ) | | | (3.45 | ) | | 32% | | 63% | | | (4.58 | ) | | | (4.95 | ) | | (7)% |

| General and administration | | | (2.55 | ) | | | (4.57 | ) | | | (0.60 | ) | | (44)% | | 325% | | | (2.50 | ) | | | (0.65 | ) | | 285% |

| Fund flows from operations netback | | | 57.32 | | | | 53.08 | | | | 45.00 | | | 8% | | 27% | | | 52.51 | | | | 36.08 | | | 46% |

| Reference prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| NBP ($/mcf) | | | 11.03 | | | | 10.95 | | | | 8.70 | | | 1% | | 27% | | | 10.35 | | | | 7.49 | | | 38% |

| NBP (€/mcf) | | | 7.31 | | | | 7.20 | | | | 5.81 | | | 2% | | 26% | | | 6.76 | | | | 5.12 | | | 32% |

Vermilion Energy Inc. ■ Page 21■ 2018 Management’s Discussion and Analysis

Production

| • | Q4 2018 production increased 1% from the prior quarter primarily due to the production contribution from the closing of our acquisition of an additional 1.5% working interest in the Corrib Project. Production also benefited from the absence of maintenance downtime that had occurred in Q3 2018, which was partially offset by natural decline. |

Activity review

| • | In December 2018, Vermilion acquired all of the issued and outstanding common shares of Shell E&P Ireland Limited, along with an incremental 1.5% working interest in the Corrib Project in Ireland from Nephin Energy Holdings Limited, a wholly owned subsidiary of CPPIB. The acquisition increased Vermilion's total ownership in Corrib to 20%. As part of this transaction, Vermilion assumed operatorship of the Corrib Project, providing us with day-to-day control over Corrib operations. |

Sales

| • | The price of our natural gas in Ireland is based on the NBP index. |

| • | Sales per boe for the three months and year ended December 31, 2018 increased versus all comparable periods consistent with increases in the NBP reference price. |

Royalties

| • | Our production in Ireland is not subject to royalties. |

Transportation

| • | Transportation expense in Ireland relates to payments under a ship-or-pay agreement related to the Corrib project. |

| • | Transportation expense for the three months ended December 31, 2018 decreased versus Q3 2018 and Q4 2017 due to a decrease in tariffs in Q4 2018. For the year ended December 31, 2018, transportation expense was consistent with the comparable period in 2017. |

Operating

| • | Q4 2018 operating expense was higher versus Q3 2018 and Q4 2017 due to an increase in offshore operations and terminal maintenance activity completed during Q4 2018. |

| • | For the year ended December 31, 2018, operating expense was lower versus the comparable period in 2017 due to higher offshore maintenance activities which occurred in 2017. |

General and administration

| • | The increase in general and administration expense versus all comparable periods is primarily due to transition costs associated with the aforementioned strategic partnership in Corrib. |

Current income taxes

| • | Given the significant level of investment in Corrib and the resulting tax pools, we do not expect to incur current income taxes in the Ireland Business Unit for the foreseeable future. |

Vermilion Energy Inc. ■ Page 22■ 2018 Management’s Discussion and Analysis

Australia Business Unit

| • | Entered Australia in 2005. |

| • | Hold a 100% operated working interest in the Wandoo field, located approximately 80 km offshore on the northwest shelf of Australia. |

| • | Production is operated from two off-shore platforms and originates from 20 producing wells including five dual lateral wells for a total of 25 producing laterals. |

| • | Wells that utilize horizontal legs (ranging in length from 500 to 3,000 plus metres) are located 600m below the seabed in approximately 55m of water depth. |

| Operational and financial review |

Australia business unit

($M except as indicated) | | Q4 2018 | | | Q3 2018 | | | Q4 2017 | | | Q4/18 vs.

Q3/18 | | Q4/18 vs.

Q4/17 | | 2018 | | | 2017 | | | 2018 vs.

2017 |

| Production | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil (bbls/d) | | | 4,174 | | | | 4,704 | | | | 4,993 | | | (11)% | | (16)% | | | 4,494 | | | | 5,770 | | | (22)% |

| Sales | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Crude oil (bbls/d) | | | 4,401 | | | | 3,935 | | | | 4,707 | | | 12% | | (7)% | | | 4,342 | | | | 5,717 | | | (24)% |

| Inventory (mbbls) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Opening crude oil inventory | | | 210 | | | | 139 | | | | 108 | | | | | | | | 134 | | | | 115 | | | |

| Crude oil production | | | 384 | | | | 433 | | | | 459 | | | | | | | | 1,640 | | | | 2,106 | | | |

| Crude oil sales | | | (405 | ) | | | (362 | ) | | | (433 | ) | | | | | | | (1,585 | ) | | | (2,087 | ) | | |

| Closing crude oil inventory | | | 189 | | | | 210 | | | | 134 | | | | | | | | 189 | | | | 134 | | | |

| Activity | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Capital expenditures | | | 43,760 | | | | 16,061 | | | | 7,192 | | | 172% | | 508% | | | 75,638 | | | | 29,942 | | | 153% |

| Financial results | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 39,351 | | | | 35,848 | | | | 36,086 | | | 10% | | 9% | | | 150,733 | | | | 154,391 | | | (2)% |

| Operating | | | (15,757 | ) | | | (11,585 | ) | | | (12,172 | ) | | 36% | | 29% | | | (53,199 | ) | | | (50,139 | ) | | 6% |

| General and administration | | | (1,391 | ) | | | (1,020 | ) | | | (3,193 | ) | | 36% | | (56)% | | | (4,918 | ) | | | (8,194 | ) | | (40)% |

| Current income taxes | | | 2,206 | | | | (3,101 | ) | | | (5,327 | ) | | N/A | | N/A | | | (11,419 | ) | | | (24,355 | ) | | (53)% |

| Fund flows from operations | | | 24,409 | | | | 20,142 | | | | 15,394 | | | 21% | | 59% | | | 81,197 | | | | 71,703 | | | 13% |

| Netbacks ($/boe) | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Sales | | | 97.19 | | | | 99.01 | | | | 83.32 | | | (2)% | | 17% | | | 95.11 | | | | 73.99 | | | 29% |

| Operating | | | (38.92 | ) | | | (32.00 | ) | | | (28.11 | ) | | 22% | | 38% | | | (33.57 | ) | | | (24.03 | ) | | 40% |

| General and administration | | | (3.44 | ) | | | (2.82 | ) | | | (7.37 | ) | | 22% | | (53)% | | | (3.10 | ) | | | (3.93 | ) | | (21)% |

| PRRT | | | 5.98 | | | | 0.70 | | | | (8.25 | ) | | 754% | | N/A | | | (3.04 | ) | | | (9.50 | ) | | (68)% |

| Corporate income taxes | | | (0.53 | ) | | | (9.27 | ) | | | (4.05 | ) | | (94)% | | (87)% | | | (4.16 | ) | | | (2.17 | ) | | 92% |

| Fund flows from operations netback | | | 60.28 | | | | 55.62 | | | | 35.54 | | | 8% | | 70% | | | 51.24 | | | | 34.36 | | | 49% |

| Reference prices | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Dated Brent (US $/bbl) | | | 67.76 | | | | 75.27 | | | | 61.39 | | | (10)% | | 10% | | | 71.04 | | | | 54.27 | | | 31% |

| Dated Brent ($/bbl) | | | 89.54 | | | | 98.37 | | | | 78.05 | | | (9)% | | 15% | | | 92.07 | | | | 70.44 | | | 31% |

Vermilion Energy Inc. ■ Page 23■ 2018 Management’s Discussion and Analysis

Production

| • | Q4 2018 production decreased 11% quarter-over-quarter and 16% year-over-year due to a planned shutdown of the Wandoo field for maintenance and other well downtime, including that which was associated with drilling two new wells. |

| • | Production volumes are managed within corporate targets while meeting customer demands and the requirements of long-term supply agreements. |

| • | We continue to plan for long-term annual production levels of approximately 6,000 bbls/d. |

Activity review

| • | In Q4 2018, we initiated our two (2.0 net) well drilling program, which was successfully completed in early 2019. The total cost of the program was $75 million, which was approximately $10 million over budget due to some minor drilling complications and weather-related delays. |

| • | We also continued to focus on adding value through asset optimization and proactive maintenance. |

Sales

| • | Crude oil in Australia is priced with reference to Dated Brent. |

| • | Q4 2018 sales per boe were consistent with Q3 2018, but higher sales volumes resulted in an increase in sales quarter-over-quarter. |

| • | Sales per boe for the three months and year ended December 31, 2018 increased versus the comparable periods in the prior year, consistent with increases in the Dated Brent reference price. |

Royalties and transportation