UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

----------------------------------------------------------------

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT

OF REGISTERED MANAGEMENT

INVESTMENT COMPANIES

Investment Company Act file number 811-21593

----------------------------------------------------------------

KAYNE ANDERSON ENERGY

INFRASTRUCTURE FUND, INC.

(Exact name of registrant as specified in charter)

----------------------------------------------------------------

717 Texas Avenue, Suite 2200, Houston, Texas | | 77002 |

(Address of principal executive offices) | | (Zip code) |

Michael J. O’Neil

KA Fund Advisors, LLC, 717 Texas Avenue, Suite 2200, Houston, Texas 77002

(Name and address of agent for service)

----------------------------------------------------------------

Registrant’s telephone number, including area code: (713) 493-2020

Date of fiscal year end: November 30, 2024

Date of reporting period: November 30, 2024

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. § 3507.

Item 1. Reports to Stockholders.

The report of Kayne Anderson Energy Infrastructure Fund, Inc. (the “Registrant”) to stockholders for the fiscal year ended November 30, 2024 is attached below.

CONTENTS

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS: This report of Kayne Anderson Energy Infrastructure Fund, Inc. (the “Company”) contains “forward-looking statements” as defined under the U.S. federal securities laws. Generally, the words “believe,” “expect,” “intend,” “estimate,” “anticipate,” “project,” “will” and similar expressions identify forward-looking statements, which generally are not historical in nature. Forward-looking statements are subject to certain risks and uncertainties that could cause actual results to materially differ from the Company’s historical experience and its present expectations or projections indicated in any forward-looking statements. These risks include, but are not limited to, changes in economic and political conditions; regulatory and legal changes; energy infrastructure company industry risk; leverage risk; valuation risk; interest rate risk; tax risk; and other risks discussed in the Company’s filings with the Securities and Exchange Commission (“SEC”). You should not place undue reliance on forward-looking statements, which speak only as of the date they are made. The Company undertakes no obligation to update or revise any forward-looking statements made herein. There is no assurance that the Company’s investment objectives will be attained.

All investments in securities involve risks, including the possible loss of principal. The value of an investment in the Company could be volatile, and you could suffer losses of some or a substantial portion of the amount invested. The Company’s concentration of investments in energy infrastructure companies subjects it to the risks of midstream, renewable infrastructure and utility entities and the energy sector, including the risks of declines in energy and commodity prices, decreases in energy demand, adverse weather conditions, natural or other disasters, changes in government regulation, and changes in tax laws. Leverage creates risks that may adversely affect return, including the likelihood of greater volatility of net asset value and market price of common shares and fluctuations in distribution rates, which increases a stockholder’s risk of loss.

Performance data quoted in this report represent past performance and are for the stated time period only. Past performance is not a guarantee of future results. Current performance may be lower or higher than that shown based on market fluctuations from the end of the reported period.

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

Disclosure Pursuant to Rule 8b-16 under the Investment Company Act of 1940

Rule 8b-16 Disclosure

The following information in this annual report is a summary of certain changes since December 1, 2023. This information may not reflect all the changes that have occurred since you purchased shares of the Company.

Rule 8b-16 under the Investment Company Act of 1940, as amended, requires that we disclose certain information to stockholders in our annual report. That disclosure is included in this report as follows:

(1) information about our dividend investment plan is included on pages 83-85;

(2) information about our investment objectives and policies is included on page 50. There were no material changes to our investment objectives and policies that were not approved by stockholders;

(3) information regarding the principal risk factors associated with an investment in the Company is included on pages 51-76. There were no material changes to those risk factors;

(4) there were no changes to our charter or by-laws that were not approved by stockholders that delay or prevent a change of control; and

(5) Harrison J. Little, Executive Vice President of the Company, was made a portfolio manager of the Company effective February 5, 2024. James C. Baker, Jr. continues to be a portfolio manager of the Company, and Messrs. Baker and Little are the persons primarily responsible for the day-to-day management of the Company’s investment portfolio.

1

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

LETTER TO STOCKHOLDERS

December 18, 2024

Dear Fellow Stockholders,

Fiscal 2024 was an exceptional year for KYN. In fact, the Company’s Net Asset Return resulted in the best annual performance in KYN’s twenty-year history!(1)

Looking forward, we are excited about the Company’s next twenty years — KYN remains a very efficient vehicle for investors to gain exposure to energy infrastructure, a subsector that we believe is well positioned to generate attractive returns for years to come. Further, KYN’s emphasis on making cash distributions to stockholders and its positive structural attributes are key points of differentiation relative to other energy infrastructure-focused investment alternatives. As investors in the market-leading energy infrastructure closed-end fund, KYN’s stockholders will continue to benefit from the Company’s size and scale, trading liquidity and “best in class” access to the capital markets.

Some of KYN’s key accomplishments during fiscal 2024 include:

• Generated a Net Asset Return of 57%;(1)

• Generated a Market Return of 75%;(2)

• Increased its distribution by 14%;(3)

• Increased the frequency of its distribution payments to monthly (from quarterly); and

• Successfully integrated KMF and realized operating synergies.(4)

Fiscal 2024 was an inflection point in investors’ recognition of the stockholder-friendly actions implemented over the last few years by the midstream sector. It has been very rewarding to see midstream companies’ stock prices respond to this change in market perception. KYN’s performance during fiscal 2024 is particularly gratifying given our team’s multi-year efforts to ensure the Company’s corporate structure, investment objective, portfolio positioning, and balance sheet were aligned to enable KYN to take advantage of the favorable market setup.

It has been an exceptional four-year recovery from the challenges presented during fiscal 2020. Our Net Asset Return was 214% over this period (33% on an annualized basis) and we increased distributions to stockholders by 60%.(1),(5) Notwithstanding these strong results, we believe the energy infrastructure sector remains a compelling investment opportunity. Infrastructure assets, which serve as the backbone for the energy and power industries, play a critical role in the global economy. Put simply, these “must run” assets enable society’s modern way of life. This role will become even more vital as A.I.’s involvement in our day-to-day lives increases. KYN’s portfolio investments are well positioned to benefit from expected domestic natural gas and power demand growth in the coming years. Further, we believe the new U.S. presidential administration, which has made “energy dominance” one of its primary agenda items, will provide a constructive backdrop for KYN’s targeted investment areas.

Distribution and Stock Price Performance

We understand how important distributions are to our investors, and one of our objectives is to provide investors with an attractive distribution. Our recent switch to paying monthly distributions was a tangible step forward to differentiate the Company from other energy infrastructure focused-investment alternatives. Based on KYN’s stock price as of November 30th, KYN’s distribution rate was 7.0% at the end of fiscal 2024.(6)

2

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

LETTER TO STOCKHOLDERS

In September, we announced a $0.02 per share increase in KYN’s quarterly distribution (to $0.24 per share), which represented a 9.1% increase compared to the prior quarter’s distribution.(7) In October, we announced that distributions would increase in frequency and be paid monthly, instead of quarterly, beginning in November 2024. This $0.08 per share monthly distribution was equivalent to KYN’s prior quarterly rate of $0.24 per share ($0.96 per share annualized). Our long-term goal is to steadily increase KYN’s distribution over time as supported by the Company’s operating results.

KYN’s Market Return, which is based on stock price performance rather than changes in net asset value, was an incredible 75% during fiscal 2024!(2) We are extremely pleased with the narrowing of KYN’s price-to-NAV discount during the year. KYN’s stock price ended the year at a 9.0% discount to NAV compared to an 18.5% discount at the beginning of the year. Favorable market conditions for midstream companies created a tailwind for KYN, as did the stockholder-friendly actions we have taken over the last several years. We do not plan to rest on our laurels in 2025 — we will continue to proactively engage with investors to outline our favorable outlook for the energy infrastructure sector and highlight KYN’s positive attributes.

Investment Mandate and Performance

The Company’s structure provides meaningful flexibility in pursuit of its investment mandate, which is to invest in a portfolio of North American-focused energy infrastructure companies. Most of the portfolio is comprised of investments in midstream companies. The remainder is a mix of investments in energy companies and power infrastructure companies.(8) We believe this portfolio composition has the potential to generate superior risk-adjusted returns over the longer term and capitalize on the sector’s key macro trends. Importantly, we can quickly modify subsector allocations based on market conditions and relative valuations.

We benchmark the Company’s performance against the Alerian Midstream Energy Index (“AMNA”). This index best captures KYN’s target investment universe and is aligned with our goal of being the premier investment vehicle for investors to gain exposure to the midstream sector. For the fiscal year, KYN’s Net Asset Return was 57.1%, which was approximately 400 basis points higher than the AMNA’s 53.1% return.(1) We believe this outperformance speaks to our value-added portfolio management and the benefits of KYN’s structure. We are pleased to have achieved these results while proactively managing KYN’s balance sheet and utilizing a lower-than-targeted amount of leverage for most of the year.

Portfolio

At fiscal year-end, KYN’s portfolio was comprised of 31 investments in 29 companies. Approximately 95% of the portfolio was invested in common equity with the remainder invested in preferred equity and debt.

The large majority of KYN’s portfolio is invested in midstream master limited partnerships (“MLPs”) and midstream C-Corps. Importantly, KYN has no constraints on its ability to invest in MLPs (this flexibility results from KYN’s structure as a taxable entity). Said differently, KYN can invest in the companies that are best positioned to generate attractive returns and is not forced to make investment decisions based on fund-level structural constraints. Further, the Company has a small allocation to privately held midstream companies (approximately 2% of the portfolio). We believe KYN — due to its permanent capital base — is particularly well positioned to make long-term investments in private energy infrastructure businesses and we are actively looking to increase KYN’s exposure to these types of investments. KYN’s flexibility is an important point of distinction relative to certain peer funds and passive investment products where

3

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

LETTER TO STOCKHOLDERS

structure (or investment mandate) constrains portfolio composition. Without such constraints, KYN can dynamically allocate its portfolio across the full spectrum of energy infrastructure businesses in both public and private markets, which is not the case for most of the Company’s peers.

The chart below highlights KYN’s exposure to the different energy subsectors.

Fiscal 2024 Market Review

Broader equity markets rallied through our fiscal year, with the S&P 500 Index closing at a record high (up 33.9%) despite ongoing concerns of higher inflation, stagnating economic growth, shifting monetary policy, uncertainty surrounding the U.S. election, and a fragile geopolitical backdrop. The midstream sector was a star performer during the year relative to the broader markets, with the AMNA returning 53.1%. At the outset of fiscal 2024, we anticipated an overall constructive backdrop for North American energy infrastructure, despite market volatility leading up to the presidential election and persistent global tensions. While we were correct in this bullish outlook for midstream, the extent of the rally this year exceeded our expectations.

Throughout the year, we became more bullish on natural gas-focused infrastructure companies as we recognized the A.I.-driven natural gas and power demand story and its impact on midstream companies and certain utilities. Midstream C-Corps were the first stocks in the midstream sector to rally as investors sought to capitalize on this theme. KYN’s midstream portfolio was well positioned for this and enjoyed strong returns. During the last few months of the year, we tactically began to rotate our midstream positioning to increase exposure to midstream MLPs (and reduce C-Corp exposure). We took this action because we believe the valuation disparity between C-Corps and MLPs has widened to unjustified levels — particularly given how well positioned certain midstream MLPs are to benefit from domestic natural gas demand growth trends. This valuation gap began to correct itself during November, and it is a trend that we expect to continue into fiscal 2025.

4

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

LETTER TO STOCKHOLDERS

Utilities were also among the best performing market sectors, up 36.5% as measured by the XLU, benefiting in part from bullish A.I.-related themes mentioned above. We believe domestic power demand growth over the next 5 to 10 years will result in higher (and more durable) earnings growth for many companies in the power sector. Utilities also benefited from a “catch up trade” during 2024 — the prior year was one of the poorest in terms of relative market performance in the sector’s history. Energy companies underperformed during fiscal 2024 (up 16.8% as measured by the XLE), with commodity price weakness and a deteriorating crude oil narrative serving as headwinds for these companies.

| | Total Returns |

| | | Equity Market Indices | | Energy Indices | | KYN(1) |

| | | S&P 500 | | DJIA | | NASDAQ | | AMNA(11) | | XLU(12) | | KRII(13) | | XLE(14) | | |

Fiscal Q4(9) | | 7.2 | % | | 8.5 | % | | 8.7 | % | | 21.6 | % | | 9.4 | % | | (4.7 | )% | | 5.5 | % | | 22.4 | % |

Fiscal 2024(10) | | 33.9 | % | | 27.2 | % | | 36.1 | % | | 53.1 | % | | 36.5 | % | | 3.4 | % | | 16.8 | % | | 57.1 | % |

Fiscal 2025 Outlook

We are optimistic about the outlook for energy infrastructure in 2025, driven by accelerating demand trends, favorable policies and a strong regulatory backdrop for the domestic energy and power sectors. In particular, we expect continued growth in natural gas production, midstream infrastructure, and liquefied natural gas (“LNG”) exports, with a supportive environment for long-term investment in energy markets.

Broader Markets Outlook

While the energy infrastructure outlook remains positive, we are maintaining a balanced approach at KYN, prioritizing liquidity and moderate leverage as we navigate potential financial market challenges. We anticipate some near-term market volatility as investors evaluate policy developments and their potential impacts. We remain attentive to the possibility of higher inflation and interest rates, as well as “tail risks” tied to elevated geopolitical tensions and uncertainty surrounding proposed changes to tax, trade, immigration, and other policies under the new administration.

Energy Commodities Outlook

For energy commodities, we expect policy to be favorable for long-term investment decisions by the major energy companies and domestic E&P companies, as the runway for fossil fuels appears much more certain. We are cautious, however, about the short-term outlook for crude oil prices, as global oil markets appear to be oversupplied. While OPEC+ will likely try to defend prices at around $70 per barrel we believe the risk in oil prices is skewed to the downside, barring a major disruption to supply. Meanwhile, our outlook for natural gas prices is bullish as incremental demand from data centers and industrial re-shoring should bolster prices and stimulate domestic production growth. Additionally, lifting the LNG permitting pause, an action the new administration is expected take in early 2025, should create positive momentum for new LNG liquefaction plants over the next few years. We expect domestic LNG exports to more than double from current levels over the next decade.

5

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

LETTER TO STOCKHOLDERS

Midstream Outlook

Our outlook for the midstream sector is constructive. We believe the playbook of consistent operating results, execution of “return of capital” strategies (in the form of increasing dividends and stock buybacks), and steady cash flow growth will continue to be a winning formula. Because of these attributes, combined with a supportive regulatory backdrop and growth prospects that appear to be more durable (due to the macro themes we have discussed in this letter), we believe the midstream sector will continue to attract attention from investors. Further, there is little doubt the opportunity set has grown for the midstream sector. Execution will be key as will striking a balance between growth initiatives and shareholders’ return of capital expectations.

Notwithstanding these positive points, the magnitude of this year’s performance has “pulled forward” some of the excess returns we previously believed midstream equities could generate over a five-year investment horizon. Valuations remain attractive in our view, and we believe the sector has the potential to generate annual returns in the “low teens” area over the next five years.(15) We consider this return outlook to be compelling given the defensive attributes of these businesses.

Power Infrastructure Outlook

The economic super trend around power demand is driven by the growing need for reliable, scalable infrastructure to support the proliferation of data centers, industrial re-shoring, and the broader energy transition. As these trends accelerate in the back half of this decade, the demand for power will step up, creating tremendous requirements for investment in both traditional and renewable power infrastructure. This is a constructive backdrop for investments in the sector, particularly within businesses poised to benefit from the expanding energy needs of industrial users and consumers alike. We believe that the combination of policy support and increased demand should provide a solid foundation for long-term growth and value creation in power infrastructure.

Why Invest in KYN?

For investors that share our conviction in the long-term trends discussed in this letter, we believe KYN — with its flexible investment mandate, permanent capital base, and expertise providing capital solutions to both public and private companies — is a very attractive means to gain exposure to the North American energy infrastructure sector in an income-producing vehicle. The Company provides this exposure in an easy-to-own structure — daily liquidity via its NYSE listing, an attractive monthly distribution, and the tax simplicity of a single Form 1099.

Our highly experienced management team is laser-focused on ways to add value. Examples include active portfolio management, optimization of KYN’s balance sheet and vigilant risk management. We expect the next few years will be a “stock pickers market” in the energy infrastructure sector. This plays to our strengths and we relish the opportunity for our investment team to add differentiated value for KYN’s investors. Further, our team has done a commendable job managing KYN’s capitalization — from opportunistically refinancing debt and preferred stock at favorable long-term interest rates to dynamically managing leverage levels given the market backdrop. Those efforts will continue in fiscal 2025, and we believe it is an additional way we can augment investor returns.

6

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

LETTER TO STOCKHOLDERS

In summary, we are confident the stage is set for a successful 2025 and beyond. We appreciate the trust you have placed in us and are grateful for your support. We value the opportunity to connect with our fellow stockholders and encourage you to reach out with any questions, comments or feedback. Your insights are important to us, and we look forward to hearing from you.

Sincerely,

James C. Baker, Jr.

Chairman of the Board

President and Chief Executive Officer

For more information:

cef@kayneanderson.com // 877.657.3863

www.kaynefunds.com

7

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

LETTER TO STOCKHOLDERS

| | | | | | | | | | | | | | | | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | |

| | Actual events and conditions may differ materially from the assumptions used to establish this return estimate (“target returns”). Target returns are neither a guarantee nor a prediction or projection of future performance and there can be no assurance that the target returns will be achieved. Target returns for individual investments may be either greater or less than the target return. A broad range of risks could cause KYN to fail to meet its investment objectives and/or these target returns. The target returns for midstream equities set forth herein should not be viewed as an indicator of likely performance returns to investors. While subject to numerous assumptions, the primary considerations incorporated into these target returns are estimated dividend yields of 4% to 6%, estimated annual growth in dividends & cash flows of 5% to 7%, and estimated annual “excess” free cash flow of 0% to 3%. After incorporating the impacts of fees, expenses and leverage, Kayne Anderson views KYN as having the potential to generate similar annual returns on a net basis for investors. There is no guarantee that the facts on which such assumptions are based will materialize as anticipated. |

8

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

PORTFOLIO SUMMARY

(UNAUDITED)

Portfolio of Long-Term Investments by Category

Top 10 Holdings by Issuer(1)

Holding | | Category | | Percent of Long-Term

Investments as of

November 30, |

2024 | | 2023 |

1. | | Energy Transfer LP | | Midstream Energy Company | | 10.4 | % | | 10.0 | % |

2. | | Enterprise Products Partners L.P. | | Midstream Energy Company | | 10.1 | | | 10.9 | |

3. | | The Williams Companies, Inc. | | Midstream Energy Company | | 9.8 | | | 7.9 | |

4. | | MPLX LP | | Midstream Energy Company | | 9.0 | | | 9.3 | |

5. | | Targa Resources Corp. | | Midstream Energy Company | | 7.2 | | | 7.3 | |

6. | | ONEOK, Inc. | | Midstream Energy Company | | 7.1 | | | 6.7 | |

7. | | Cheniere Energy, Inc. | | Midstream Energy Company | | 6.4 | | | 7.1 | |

8. | | Kinder Morgan, Inc. | | Midstream Energy Company | | 6.0 | | | 3.6 | |

9. | | Western Midstream Partners, LP | | Midstream Energy Company | | 4.2 | | | 4.0 | |

10. | | Plains All American Pipeline, L.P. | | Midstream Energy Company | | 3.8 | | | 6.6 | (2) |

9

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

Company Overview

Kayne Anderson Energy Infrastructure Fund, Inc. (the “Company” or “KYN”) is a non-diversified, closed-end fund that commenced operations in September 2004. Our investment objective is to provide a high after-tax total return with an emphasis on making cash distributions to stockholders. We intend to achieve our investment objective by investing at least 80% of our total assets in the securities of Energy Infrastructure Companies. Please refer to the Glossary of Key Terms for the meaning of capitalized terms not otherwise defined herein.

As of November 30, 2024, we had total assets of $3.6 billion, net assets applicable to our common stockholders of $2.5 billion (net asset value of $15.03 per share) and 169.1 million shares of common stock outstanding.

Results of Operations — For the Three Months Ended November 30, 2024

Investment Income. Investment income totaled $22.2 million for the quarter. We received $40.4 million of dividends and distributions. We estimated that $18.2 million of the dividends and distributions received were return of capital distributions and/or distribution in excess of cost basis.

Operating Expenses. Operating expenses totaled $19.6 million, including $10.7 million of investment management fees (net of fee waivers), $5.9 million of interest expense, $1.8 million of preferred stock distributions and $1.2 million of other operating expenses.

Net Investment Income. Our net investment income was $2.6 million and included a current tax expense of $0.1 million and a deferred tax benefit of $0.1 million.

Net Realized Gains. We had net realized gains of $29.8 million, consisting of realized gains from long term investments of $37.3 million, a current tax expense of $7.2 million and a deferred tax expense of $0.3 million.

Net Change in Unrealized Gains. We had a net increase in our unrealized gains of $432.4 million. The net change consisted of an $547.7 million increase in unrealized gains on investments and a deferred tax expense of $115.3 million.

Net Increase in Net Assets Resulting from Operations. As a result of the above, we had a net increase in net assets resulting from operations of $464.8 million.

Results of Operations — For the Fiscal Year Ended November 30, 2024

Investment Income. Investment income totaled $83.4 million for the fiscal year. We received $155.1 million of dividends and distributions. We estimated that $71.7 million of the dividends and distributions received were return of capital distributions and/or distributions in excess of cost basis. Return of capital and distributions in excess of cost basis increased by $3.7 million (net) during the year due to 2023 tax reporting information that we received in fiscal 2024. Interest income for the year was less than $0.1 million.

Operating Expenses. Operating expenses totaled $69.6 million, including $37.0 million of investment management fees (net of fee waivers), $21.4 million of interest expense, $6.9 million of preferred stock distributions and $4.3 million of other operating expenses.

Net Investment Income. Our net investment income totaled $12.8 million and included a current tax expense of $0.5 million and a deferred tax expense of $0.5 million.

10

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

Net Realized Gains. We had net realized gains from our investments of $154.2 million, consisting of realized gains from long term investments of $195.5 million, $0.4 million of realized gains from securities sold short, a current tax expense of $20.5 million and a deferred tax expense of $21.2 million.

Net Change in Unrealized Gains. We had a net increase in unrealized gains of $762.7 million. The net change consisted of a $969.2 million increase in our unrealized gains on investments and a deferred tax expense of $206.5 million.

Net Increase in Net Assets Resulting from Operations. As a result of the above, we had a net increase in net assets resulting from operations of $929.7 million.

Management Discussion of Fund Performance

See Letter to Stockholders for a more fulsome discussion of the Company’s performance during the fiscal year ended November 30, 2024.

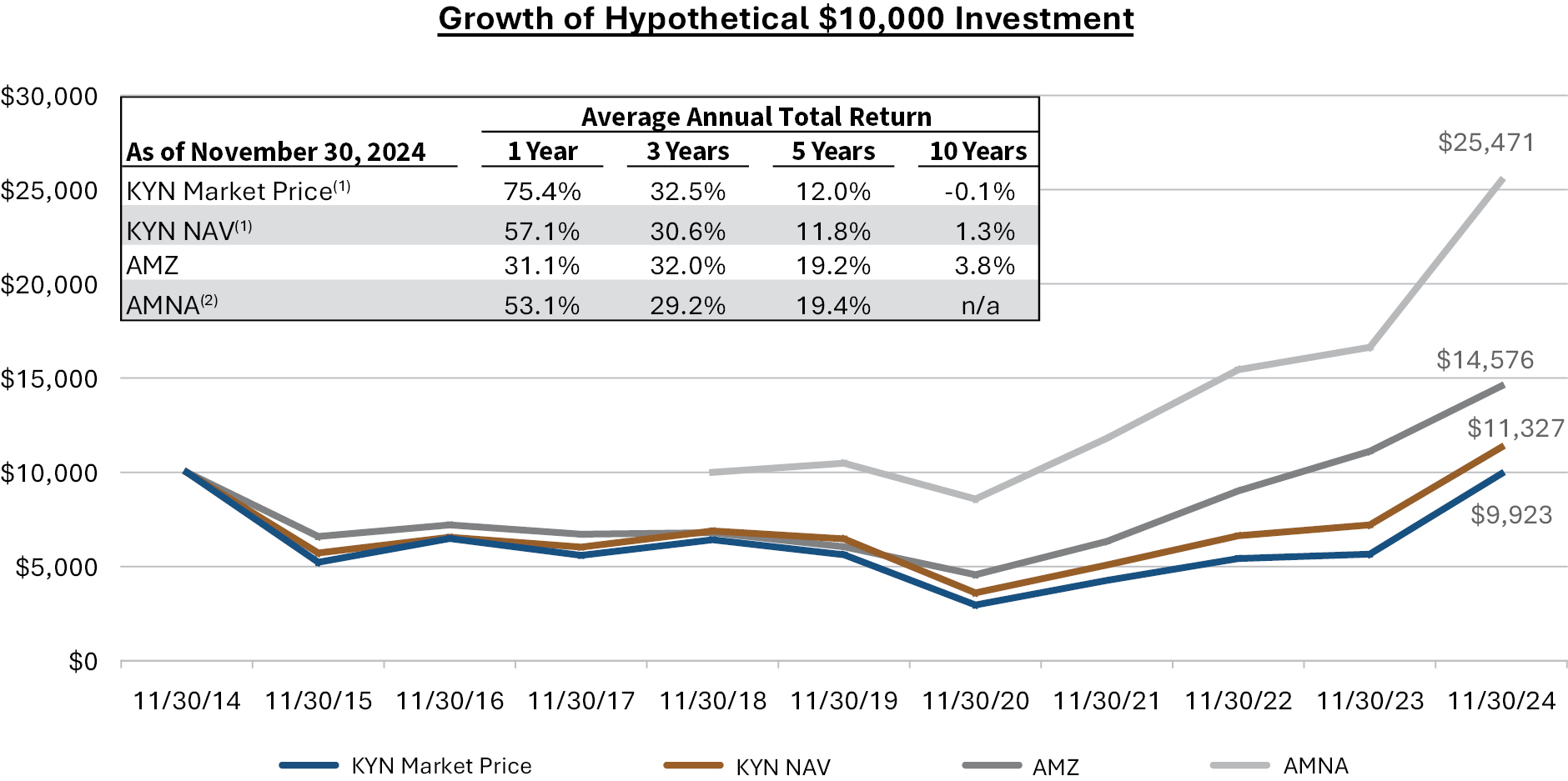

The below graph illustrates the hypothetical growth of $10,000 based upon the total return performance of the Company’s common share price (“KYN Market Price”) and net asset value per share price (“KYN NAV”) for the 10-year period ended November 30, 2024 as compared to the total return of the Alerian MLP Index (“AMZ”).

11

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

The table and graph do not reflect any deduction for taxes that a shareholder may pay on distributions or the disposition of Company shares. Index performance is shown for illustrative purposes only and does not reflect any fees, expenses or sales charges. It is not possible to invest directly in an index.

Performance data quoted represents past performance and is no guarantee of future results. Current performance may be lower or higher than that shown based on market fluctuations from the end of the reported period.

The AMZ is an index of energy infrastructure Master Limited Partnerships (MLPs). The AMZ is a capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities.

The AMNA is a broad-based composite of North American energy infrastructure companies (which includes both MLPs and taxable corporations). The AMNA is a capped, float-adjusted, capitalization-weighted index, whose constituents earn the majority of their cash flow from midstream activities involving energy commodities.

Distributions to Common Stockholders

On October 10, 2024, KYN announced a transition to monthly distributions and declared monthly distributions of $0.08 per common share payable November 29, 2024, December 31, 2024 and January 31, 2025. This monthly distribution is equivalent to the $0.24 per share quarterly distribution that was last paid by KYN on October 7, 2024. Payment of future distributions is subject to the approval of KYN’s Board of Directors, as well as meeting the covenants of our debt agreements and terms of our preferred stock. It is the Company’s intention to declare monthly payments each month beginning with the monthly payment expected to be made in February 2025.

The Board of Directors considers several items in setting our distributions to common stockholders including net distributable income (as defined below), realized and unrealized gains and expected returns for portfolio investments.

Net distributable income (“NDI”) is the amount of income received by us from our portfolio investments less operating expenses, subject to certain adjustments as described below. NDI is not a financial measure under the accounting principles generally accepted in the United States of America (“GAAP”). Refer to the Reconciliation of NDI to GAAP section for a reconciliation of this measure to our results reported under GAAP.

For the purposes of calculating NDI, income from portfolio investments includes (a) cash dividends and distributions, (b) paid-in-kind dividends received (i.e., stock dividends), (c) interest income from debt securities and (d) net premiums received from the sale of covered calls.

For the purposes of calculating NDI, operating expenses include (a) investment management fees paid to our investment adviser, (b) other expenses (mostly comprised of fees paid to other service providers), (c) interest expense and preferred stock distributions and (d) current and deferred income tax expense/benefit on net investment income/loss.

12

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

Net Distributable Income (NDI)

(amounts in millions, except for per share amounts)

| | Three Months

Ended

November 30,

2024 | | Fiscal Year

Ended

November 30,

2024 |

Distributions and Other Income from Investments | | | | | | | | |

Dividends and Distributions | | $ | 40.4 | | | $ | 155.1 | |

Expenses | | | | | | | | |

Net Investment Management Fee | | | (10.7 | ) | | | (37.0 | ) |

Other Expenses | | | (1.2 | ) | | | (4.3 | ) |

Interest Expense | | | (5.9 | ) | | | (21.4 | ) |

Preferred Stock Distributions | | | (1.8 | ) | | | (6.9 | ) |

Income Tax Expense, net | | | — | | | | (1.0 | ) |

Net Distributable Income (NDI) | | $ | 20.8 | | | $ | 84.5 | |

Weighted Shares Outstanding | | | 169.1 | | | | 169.1 | |

NDI per Weighted Share Outstanding | | $ | 0.123 | | | $ | 0.500 | |

Reconciliation of NDI to GAAP

The difference between distributions and other income from investments in the NDI calculation and total investment income as reported in our Statement of Operations is reconciled as follows:

• A significant portion of the cash distributions received from our investments is characterized as return of capital. For GAAP purposes, return of capital distributions are excluded from investment income, whereas the NDI calculation includes the return of capital portion of such distributions.

• GAAP recognizes distributions received from our investments that exceed the cost basis of our securities to be realized gains and are therefore excluded from investment income, whereas the NDI calculation includes these distributions.

• We may sell covered call option contracts to generate income or to reduce our ownership of certain securities that we hold. In some cases, we are able to repurchase these call option contracts at a price less than the call premium that we received, thereby generating a profit. The premium we receive from selling call options, less (i) the premium that we pay to repurchase such call option contracts and (ii) the amount by which the market price of an underlying security is above the strike price at the time a new call option is written (if any), is included in NDI. For GAAP purposes, premiums received from call option contracts sold are not included in investment income. See Note 2 — Significant Accounting Policies for the GAAP treatment of option contracts.

Liquidity and Capital Resources

At November 30, 2024, we had total leverage outstanding of $631 million, which represented 18% of total assets. Currently, we intend to utilize leverage in an amount that represents approximately 20% of our total assets. Total leverage was comprised of $68 million of borrowings outstanding under our unsecured revolving credit facility (the “Credit Facility”), $410 million of senior unsecured notes (“Notes”) and $153 million of mandatory redeemable preferred stock (“MRP Shares”). As of November 30, 2024, we had $13 million of short term investments in money market funds. As of January 24, 2024, we had $64 million of borrowings outstanding under our Credit Facility and we had $1 million of short term investments in money market funds.

13

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

MANAGEMENT DISCUSSION

(UNAUDITED)

Our Credit Facility has a total commitment of $135 million and matures on February 20, 2025. The interest rate on borrowings under the Credit Facility may vary between the secured overnight financing rate (“SOFR”) plus 1.40% and SOFR plus 2.25%, depending on our asset coverage ratios. We pay a fee of 0.20% per annum on any unused amounts of the Credit Facility. We have initiated the renewal process for this facility and anticipate renewing at the same commitment level or higher in February 2025.

On May 22, 2024, we repaid $25 million of our $50 million unsecured term loan (the “Term Loan”), which represented the floating rate portion of the Term Loan (interest rate of SOFR plus 1.40%). On August 6, 2024, upon the maturity date of the Term Loan, we repaid the remaining $25 million of fixed rate borrowings (interest rate of 1.735%) and the Term Loan was terminated.

As of November 30, 2024, we had $410 million of Notes outstanding that mature between 2025 and 2036 and we had $153 million of MRP Shares outstanding that are subject to mandatory redemption between 2026 and 2032. We expect to refinance upcoming 2025 Notes maturities with borrowings under our Credit Facility, additional issuances of Notes, cash on hand or some combination thereof.

On September 18, 2024, we issued $70 million of new Notes and $30 million of new MRP Shares. The Notes issuance was comprised of two series: (1) $30 million of Series YY Notes with a 5.19% fixed rate due September 18, 2031 and (2) $40 million of Series ZZ Notes with a 5.45% fixed rate due September 18, 2036. The MRP Shares issuance was $30 million of Series X MRP Shares with a 5.49% fixed dividend rate and a mandatory redemption date of September 18, 2029. On September 20, 2024, we repaid the entire $20 million of Series V floating rate MRP Shares at liquidation value plus accumulated but unpaid dividends through the date of redemption. On November 29, 2024, we repaid the entire $9.5 million of Series U fixed rate MRP Shares at liquidation value plus accumulated but unpaid dividends through the date of redemption.

At November 30, 2024, our asset coverage ratios under the Investment Company Act of 1940, as amended (“1940 Act”), were 664% for debt and 503% for total leverage (debt plus preferred stock). We target asset coverage ratios that give us the ability to withstand declines in the market value of the securities we hold before breaching the financial covenants in our leverage (we often refer to this as our “downside cushion”). At this time, we target asset coverage ratios that provide approximately 50% to 55% of downside cushion relative to our financial covenants. Our leverage targets are dependent on market conditions as well as certain other factors and may vary from time to time.

As of November 30, 2024, our total leverage consisted of 81% of fixed rate obligations and 19% of floating rate obligations. At such date, the weighted average interest/dividend rate on our total leverage was 4.92%.

14

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2024

(amounts in 000’s)

Description | | No. of

Shares/Units | | Value |

Long-Term Investments — 139.0% | | | | | |

Equity Investments(1) — 138.6% | | | | | |

Midstream Energy Company(2) — 131.4% | | | | | |

Antero Midstream Corporation | | 2,218 | | $ | 35,428 |

Archrock, Inc. | | 1,132 | | | 29,002 |

Aris Water Solutions, Inc. | | 644 | | | 17,317 |

Cheniere Energy, Inc. | | 1,016 | | | 227,668 |

DT Midstream, Inc. | | 531 | | | 56,350 |

Enbridge Inc.(3) | | 2,977 | | | 129,141 |

Energy Transfer LP | | 18,568 | | | 368,764 |

Enterprise Products Partners L.P. | | 10,357 | | | 356,608 |

Hess Midstream LP | | 1,632 | | | 61,863 |

Kinder Morgan, Inc. | | 7,545 | | | 213,303 |

Kinetik Holdings Inc. | | 632 | | | 37,319 |

MPLX LP | | 3,904 | | | 201,693 |

MPLX LP — Convertible Preferred Units(4)(5)(6) | | 2,255 | | | 116,513 |

ONEOK, Inc. | | 2,217 | | | 251,880 |

Pembina Pipeline Corporation(3) | | 3,167 | | | 131,013 |

Plains All American Pipeline, L.P. | | 7,105 | | | 132,658 |

Sentinel Midstream Highline JV Holdings LLC(4)(5)(7)(8) | | 1,500 | | | 38,250 |

South Bow Corporation(3)(9) | | 393 | | | 10,245 |

Streamline Innovations Holdings, Inc. — Series C Preferred Shares(4)(5)(8)(10)(11) | | 5,500 | | | 35,750 |

Targa Resources Corp. | | 1,248 | | | 255,029 |

TC Energy Corporation(3)(9) | | 2,606 | | | 127,501 |

Venture Global LNG, Inc. — Series A Preferred Shares(5)(12) | | 10,000 | | | 10,363 |

The Williams Companies, Inc. | | 5,910 | | | 345,840 |

Western Midstream Partners, LP | | 3,675 | | | 149,600 |

| | | | | | 3,339,098 |

Utility Company(2) — 4.1% | | | | | |

Entergy Corporation | | 202 | | | 31,575 |

Sempra Energy | | 770 | | | 72,104 |

| | | | | | 103,679 |

Other — 1.7% | | | | | |

Air Products and Chemicals, Inc. | | 87 | | | 29,175 |

Linde plc(3) | | 32 | | | 14,577 |

| | | | | | 43,752 |

Energy Company(2) — 1.4% | | | | | |

Shell plc — ADR(3)(13) | | 558 | | | 36,110 |

Total Equity Investments — (Cost — $2,409,530) | | | | | 3,522,639 |

See accompanying notes to financial statements.

15

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2024

(amounts in 000’s)

Description | | Interest

Rate | | Maturity

Date | | Principal

Amount | | Value |

Debt Investments — 0.4% | | | | | | | | | | | |

Midstream Energy Company(2) — 0.2% | | | | | | | | | | | |

South Bow Corporation(3)(5) | | 7.500% | | 3/1/55 | | $ | 5,000 | | $ | 5,233 | |

| | | | | | | | | | | | |

Utility Company(2) — 0.2% | | | | | | | | | | | |

PG&E Corporation | | 7.375 | | 3/15/55 | | | 5,000 | | | 5,167 | |

Total Debt Investments (Cost — $10,335) | | | | | | | | | | 10,400 | |

Total Long-Term Investments (Cost — $2,419,865) | | | 3,533,039 | |

| | | | | | | | | | | | |

| | | | | | | | No. of

Shares/Units | | | | |

Short-Term Investment — Money Market Fund — 0.5% | | | | | | | |

First American Money Market Fund Treasury Obligations Fund — Class X Shares, 4.55%(14) (Cost — $12,680) | | | 12,680 | | | 12,680 | |

Total Investments — 139.5% (Cost — $2,432,545) | | | | | | 3,545,719 | |

| | | | | | | | |

Debt | | | | | | (477,654 | ) |

Mandatory Redeemable Preferred Stock at Liquidation Value | | | | | | (153,603 | ) |

Current Income Tax Liability, net | | | | | | (433 | ) |

Deferred Income Tax Liability, net | | | | | | (362,983 | ) |

Other Liabilities in Excess of Other Assets | | | | | | (9,559 | ) |

Net Assets Applicable to Common Stockholders | | | | | $ | 2,541,487 | |

See accompanying notes to financial statements.

16

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

SCHEDULE OF INVESTMENTS

NOVEMBER 30, 2024

(amounts in 000’s)

As of November 30, 2024, the Company’s geographic allocation was as follows:

Geographic Location | | % of Long-Term

Investments |

United States | | 87.2% |

Canada | | 11.4% |

Europe/U.K. | | 1.4% |

See accompanying notes to financial statements.

17

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

STATEMENT OF ASSETS AND LIABILITIES

NOVEMBER 30, 2024

(amounts in 000’s, except share and per share amounts)

ASSETS | | | | |

Investments at fair value: | | | | |

Non-affiliated (Cost — $2,365,028) | | $ | 3,459,039 | |

Affiliated (Cost — $54,837) | | | 74,000 | |

Short-term investments (Cost — $12,680) | | | 12,680 | |

Receivable for securities sold | | | 2,753 | |

Dividends and distributions receivable (Cost — $2,650) | | | 2,661 | |

Deferred credit facility offering costs and other assets | | | 615 | |

Total Assets | | | 3,551,748 | |

| | | | | |

LIABILITIES | | | | |

Investment management fee payable, net | | | 10,659 | |

Accrued directors’ fees | | | 298 | |

Accrued expenses and other liabilities | | | 8,707 | |

Current income tax liability | | | 433 | |

Deferred income tax liability, net | | | 362,983 | |

Credit facility | | | 68,000 | |

Notes | | | 409,654 | |

Unamortized notes issuance costs | | | (2,725 | ) |

Mandatory redeemable preferred stock, $25.00 liquidation value per share (6,144,117 shares issued and outstanding) | | | 153,603 | |

Unamortized mandatory redeemable preferred stock issuance costs | | | (1,351 | ) |

Total Liabilities | | | 1,010,261 | |

NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS | | $ | 2,541,487 | |

NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS CONSIST OF | | | | |

Common stock, $0.001 par value (169,126,038 shares issued and outstanding, 193,855,883 shares authorized) | | $ | 169 | |

Paid-in capital | | | 2,609,492 | |

Total distributable earnings (loss) | | | (68,174 | ) |

NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS | | $ | 2,541,487 | |

NET ASSET VALUE PER COMMON SHARE | | $ | 15.03 | |

See accompanying notes to financial statements.

18

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

STATEMENT OF OPERATIONS

FOR THE FISCAL YEAR ENDED NOVEMBER 30, 2024

(amounts in 000’s)

INVESTMENT INCOME | | | | |

Income | | | | |

Dividends and distributions | | | | |

Non-affiliated investments | | $ | 149,855 | |

Affiliated investments | | | 4,633 | |

Money market mutual funds | | | 570 | |

Total dividends and distributions (after foreign taxes withheld of $2,396) | | | 155,058 | |

Return of capital | | | (69,777) | |

Distributions in excess of cost basis | | | (1,950 | ) |

Net dividends and distributions | | | 83,331 | |

Interest income | | | | |

Non-affiliated investments | | | 23 | |

Total Investment Income | | | 83,354 | |

| | | | | |

Expenses | | | | |

Investment management fees | | | 38,214 | |

Professional fees | | | 1,212 | |

Directors’ fees | | | 1,203 | |

Administration fees | | | 590 | |

Reports to stockholders | | | 341 | |

Insurance | | | 323 | |

Stock exchange listing fees | | | 216 | |

Custodian fees | | | 122 | |

Other expenses | | | 300 | |

Total Expenses — before fee waiver, interest expense, preferred distributions and taxes | | | 42,521 | |

Investment management fee waiver | | | (1,226 | ) |

Interest expense including amortization of offering costs | | | 21,412 | |

Distributions on mandatory redeemable preferred stock including amortization of offering costs | | | 6,914 | |

Total Expenses — before taxes | | | 69,621 | |

Net Investment Income — Before Taxes | | | 13,733 | |

Current income tax expense | | | (449 | ) |

Deferred income tax expense | | | (468 | ) |

Net Investment Income | | | 12,816 | |

| | | | | |

REALIZED AND UNREALIZED GAINS (LOSSES) | | | | |

Net Realized Gains (Losses) | | | | |

Investments — non-affiliated | | | 195,606 | |

Foreign currency transactions | | | (112 | ) |

Securities sold short | | | 364 | |

Current income tax expense | | | (20,453 | ) |

Deferred income tax expense | | | (21,268 | ) |

Net Realized Gains (Losses) | | | 154,137 | |

| | | | | |

Net Change in Unrealized Gains (Losses) | | | | |

Investments — non-affiliated | | | 950,847 | |

Investments — affiliated | | | 18,318 | |

Foreign currency translations | | | 7 | |

Deferred income tax expense | | | (206,452 | ) |

Net Change in Unrealized Gains (Losses) | | | 762,720 | |

Net Realized and Unrealized Gains (Losses) | | | 916,857 | |

NET INCREASE IN NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS

RESULTING FROM OPERATIONS | | $ | 929,673 | |

See accompanying notes to financial statements.

19

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

STATEMENT OF CHANGES IN NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS

(amounts in 000’s, except share amounts)

| | For the Fiscal Year Ended

November 30, |

| | | 2024 | | 2023 |

OPERATIONS | | | | | | | | |

Net investment income, net of tax(1) | | $ | 12,816 | | | $ | 17,123 | |

Net realized gains, net of tax | | | 154,137 | | | | 107,024 | |

Net change in unrealized gains (losses), net of tax | | | 762,720 | | | | (11,560 | ) |

Net Increase in Net Assets Resulting from Operations | | | 929,673 | | | | 112,587 | |

DIVIDENDS AND DISTRIBUTIONS TO COMMON STOCKHOLDERS(1)(2) | | | | | | | | |

Dividends | | | (165,744 | ) | | | (112,989 | ) |

Distributions — return of capital | | | — | | | | — | |

Dividends and Distributions to Common Stockholders | | | (165,744 | ) | | | (112,989 | ) |

CAPITAL STOCK TRANSACTIONS | | | | | | | | |

Issuance of 32,994,508 shares of common stock in connection with the merger of Kayne Anderson NextGen Energy & Infrastructure, Inc. | | | — | | | | 330,599 | |

Offering expenses associated with the issuance of common stock in merger | | | — | | | | (661 | )(3) |

Net Increase in Net Assets Applicable to Common Stockholders from Capital Stock Transactions | | | — | | | | 329,938 | |

Total Increase in Net Assets Applicable to Common Stockholders | | | 763,929 | | | | 329,536 | |

NET ASSETS APPLICABLE TO COMMON STOCKHOLDERS | | | | | | | | |

Beginning of year | | | 1,777,558 | | | | 1,448,022 | |

End of year | | $ | 2,541,487 | | | $ | 1,777,558 | |

See accompanying notes to financial statements.

20

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

STATEMENT OF CASH FLOWS

FOR THE FISCAL YEAR ENDED NOVEMBER 30, 2024

(amounts in 000’s)

CASH FLOWS FROM OPERATING ACTIVITIES | | | | |

Net increase in net assets resulting from operations | | $ | 929,673 | |

Adjustments to reconcile net increase in net assets resulting from operations to net cash provided by operating activities: | | | | |

Return of capital distributions | | | 69,777 | |

Distributions in excess of cost basis | | | 1,950 | |

Net realized gains (excluding foreign currency transactions) | | | (195,606 | ) |

Net realized gains on securities sold short | | | (364 | ) |

Net change in unrealized gains (excluding foreign currency translations) | | | (969,165 | ) |

Purchase of long-term investments | | | (1,447,296 | ) |

Proceeds from sale of long-term investments | | | 1,421,512 | |

Proceeds from securities sold short | | | 144,765 | |

Purchase of securities to cover securities sold short | | | (144,401 | ) |

Purchase of short-term investments, net | | | (12,680 | ) |

Amortization of deferred debt offering costs | | | 1,202 | |

Amortization of mandatory redeemable preferred stock offering costs | | | 503 | |

Decrease in deposits with brokers | | | 250 | |

Increase in receivable for securities sold | | | (2,753 | ) |

Decrease in dividends and distributions receivable | | | 557 | |

Decrease in current income tax receivable | | | 8,710 | |

Increase in other assets | | | (35 | ) |

Decrease in payable for securities purchased | | | (5,001 | ) |

Increase in investment management fee payable | | | 3,694 | |

Increase in accrued directors’ fees | | | 34 | |

Increase in accrued expenses and other liabilities | | | 1,452 | |

Increase in current income tax liability | | | 433 | |

Increase in deferred income tax liability | | | 228,187 | |

Net Cash Provided by Operating Activities | | | 35,398 | |

CASH FLOWS FROM FINANCING ACTIVITIES | | | | |

Increase in borrowings under credit facility | | | 59,000 | |

Costs associated with credit facility | | | (667 | ) |

Decrease in borrowings under term loan | | | (50,000 | ) |

Proceeds from notes issuance | | | 170,000 | |

Redemption of notes | | | (47,025 | ) |

Costs associated with notes issuance | | | (1,731 | ) |

Proceeds from issuance of mandatory redeemable preferred stock | | | 30,000 | |

Redemption of mandatory redeemable preferred stock | | | (29,491 | ) |

Costs associated with offering of mandatory redeemable preferred stock | | | (329 | ) |

Cash distributions paid to common stockholders | | | (165,744 | ) |

Net Cash Used in Financing Activities | | | (35,987 | ) |

NET CHANGE IN CASH | | | (589 | ) |

CASH — BEGINNING OF YEAR | | | 589 | |

CASH — END OF YEAR | | $ | — | |

During the fiscal year ended November 30, 2024, interest paid related to debt obligations was $18,578 and income tax paid was $11,759 (net of refunds received).

See accompanying notes to financial statements.

21

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| | For the Fiscal Year Ended November 30, |

2024 | | 2023 | | 2022 |

Per Share of Common Stock(1) | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 10.51 | | | $ | 10.64 | | | $ | 8.91 | |

Net investment income (loss)(2) | | | 0.08 | | | | 0.12 | | | | 0.07 | |

Net realized and unrealized gain (loss) | | | 5.42 | | | | 0.59 | | | | 2.44 | |

Total income (loss) from operations | | | 5.50 | | | | 0.71 | | | | 2.51 | |

Common dividends(3) | | | (0.98 | ) | | | (0.83 | ) | | | (0.78 | ) |

Common distributions — return of capital(3) | | | — | | | | — | | | | — | |

Total dividends and distributions — common | | | (0.98 | ) | | | (0.83 | ) | | | (0.78 | ) |

Offering expenses associated with the issuance of common stock | | | — | | | | (0.01 | )(4) | | | — | |

Effect of issuance of common stock | | | — | | | | — | | | | — | |

Effect of shares issued in reinvestment of dividends and distributions | | | — | | | | — | | | | — | |

Total capital stock transactions | | | — | | | | — | | | | — | |

Net asset value, end of period | | $ | 15.03 | | | $ | 10.51 | | | $ | 10.64 | |

Market value per share of common stock, end of period | | $ | 13.68 | | | $ | 8.57 | | | $ | 9.04 | |

Total investment return based on common stock market value(5) | | | 75.4 | % | | | 4.3 | % | | | 27.2 | % |

Total investment return based on net asset value(6) | | | 57.1 | % | | | 8.7 | % | | | 30.5 | % |

Supplemental Data and Ratios(7) | | | | | | | | | | | | |

Net assets applicable to common stockholders, end of period | | $ | 2,541,487 | | | $ | 1,777,558 | | | $ | 1,448,022 | |

Ratio of expenses to average net assets | | | | | | | | | | | | |

Management fees (net of fee waiver) | | | 1.9 | % | | | 1.9 | % | | | 2.0 | % |

Other expenses | | | 0.2 | | | | 0.2 | | | | 0.2 | |

Subtotal | | | 2.1 | | | | 2.1 | | | | 2.2 | |

Interest expense and distributions on mandatory redeemable preferred stock(2) | | | 1.4 | | | | 1.5 | | | | 1.2 | |

Income tax expense(8) | | | 12.5 | % | | | 1.9 | | | | 6.1 | |

Total expenses | | | 16.0 | % | | | 5.5 | % | | | 9.5 | % |

Ratio of net investment income (loss) to average net assets(2) | | | 0.6 | % | | | 1.2 | % | | | 0.7 | % |

Net increase (decrease) in net assets to common stockholders resulting from operations to average net assets | | | 46.7 | % | | | 8.0 | % | | | 24.1 | % |

Portfolio turnover rate | | | 51.7 | % | | | 48.8 | % | | | 28.2 | % |

Average net assets | | $ | 1,992,389 | | | $ | 1,399,694 | | | $ | 1,344,102 | |

Notes outstanding, end of period(9) | | $ | 409,654 | | | $ | 286,679 | | | $ | 260,789 | |

Borrowings under credit facilities, end of period(9) | | $ | 68,000 | | | $ | 9,000 | | | $ | — | |

Term loan outstanding, end of period(9) | | $ | — | | | $ | 50,000 | | | $ | 50,000 | |

Mandatory redeemable preferred stock, end of period(9) | | $ | 153,603 | | | $ | 153,094 | | | $ | 111,603 | |

Average shares of common stock outstanding | | | 169,126,038 | | | | 137,758,656 | | | | 133,664,106 | |

Asset coverage of total debt(10) | | | 664.2 | % | | | 658.5 | % | | | 601.8 | % |

Asset coverage of total leverage (debt and preferred stock)(11) | | | 502.6 | % | | | 456.4 | % | | | 442.8 | % |

Average amount of borrowings per share of common stock during the period(1) | | $ | 2.39 | | | $ | 2.30 | | | $ | 2.79 | |

See accompanying notes to financial statements.

22

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| | For the Fiscal Year Ended November 30, |

| | | 2021 | | 2020 | | 2019 | | 2018 |

Per Share of Common Stock(1) | | | | | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 6.90 | | | $ | 13.89 | | | $ | 16.37 | | | $ | 15.90 | |

Net investment income (loss)(2) | | | (0.08 | ) | | | (0.34 | ) | | | (0.26 | ) | | | (0.45 | ) |

Net realized and unrealized gain (loss) | | | 2.74 | | | | (5.87 | ) | | | (0.75 | ) | | | 2.74 | |

Total income (loss) from operations | | | 2.66 | | | | (6.21 | ) | | | (1.01 | ) | | | 2.29 | |

Common dividends(3) | | | — | | | | — | | | | — | | | | (1.80 | ) |

Common distributions — return of capital(3) | | | (0.65 | ) | | | (0.78 | ) | | | (1.47 | ) | | | — | |

Total dividends and distributions — common | | | (0.65 | ) | | | (0.78 | ) | | | (1.47 | ) | | | (1.80 | ) |

Offering expenses associated with the issuance of

common stock | | | — | | | | — | | | | — | | | | (0.01 | )(12) |

Effect of issuance of common stock | | | — | | | | — | | | | — | | | | — | |

Effect of shares issued in reinvestment of dividends and distributions | | | — | | | | — | | | | — | | | | (0.01 | ) |

Total capital stock transactions | | | — | | | | — | | | | — | | | | (0.02 | ) |

Net asset value, end of period | | $ | 8.91 | | | $ | 6.90 | | | $ | 13.89 | | | $ | 16.37 | |

Market value per share of common stock,

end of period | | $ | 7.77 | | | $ | 5.89 | | | $ | 12.55 | | | $ | 15.85 | |

Total investment return based on common stock market value(5) | | | 44.0 | % | | | (47.3 | )% | | | (12.4 | )% | | | 14.8 | % |

Total investment return based on net asset value(6) | | | 41.0 | % | | | (44.3 | )% | | | (6.1 | )% | | | 14.2 | % |

Supplemental Data and Ratios(7) | | | | | | | | | | | | | | | | |

Net assets applicable to common stockholders, end of period | | $ | 1,126,479 | | | $ | 872,914 | | | $ | 1,755,216 | | | $ | 2,066,269 | |

Ratio of expenses to average net assets | | | | | | | | | | | | | | | | |

Management fees (net of fee waiver) | | | 1.8 | % | | | 2.3 | % | | | 2.3 | % | | | 2.3 | % |

Other expenses | | | 0.3 | | | | 0.3 | | | | 0.1 | | | | 0.2 | |

Subtotal | | | 2.1 | | | | 2.6 | | | | 2.4 | | | | 2.5 | |

Interest expense and distributions on mandatory redeemable preferred stock(2) | | | 1.3 | | | | 3.6 | | | | 2.1 | | | | 1.9 | |

Income tax expense(8) | | | 5.1 | | | | — | | | | — | | | | — | |

Total expenses | | | 8.5 | % | | | 6.2 | % | | | 4.5 | % | | | 4.4 | % |

Ratio of net investment income (loss) to average net assets(2) | | | (0.9 | )% | | | (4.0 | )% | | | (1.6 | )% | | | (2.5 | )% |

Net increase (decrease) in net assets to common stockholders resulting from operations to average net assets | | | 31.4 | % | | | (73.8 | )% | | | (6.3 | )% | | | 10.8 | % |

Portfolio turnover rate | | | 50.8 | % | | | 22.3 | % | | | 22.0 | % | | | 25.8 | % |

Average net assets | | $ | 1,068,396 | | | $ | 1,063,404 | | | $ | 2,032,591 | | | $ | 2,127,407 | |

Notes outstanding, end of period(9) | | $ | 209,686 | | | $ | 173,260 | | | $ | 596,000 | | | $ | 716,000 | |

Borrowings under credit facilities, end of period(9) | | $ | 63,000 | | | $ | 62,000 | | | $ | 35,000 | | | $ | 39,000 | |

Term loan outstanding, end of period(9) | | $ | 50,000 | | | $ | — | | | $ | 60,000 | | | $ | 60,000 | |

Mandatory redeemable preferred stock,

end of period(9) | | $ | 101,670 | | | $ | 136,633 | | | $ | 317,000 | | | $ | 317,000 | |

Average shares of common stock outstanding | | | 126,447,554 | | | | 126,420,698 | | | | 126,326,087 | | | | 118,725,060 | |

Asset coverage of total debt(10) | | | 480.6 | % | | | 529.1 | % | | | 399.9 | % | | | 392.4 | % |

Asset coverage of total leverage (debt and preferred stock)(11) | | | 365.5 | % | | | 334.7 | % | | | 274.1 | % | | | 282.5 | % |

Average amount of borrowings per share of common stock during the period(1) | | $ | 2.43 | | | $ | 2.88 | | | $ | 6.09 | | | $ | 6.52 | |

See accompanying notes to financial statements.

23

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

| | For the Fiscal Year Ended November 30, |

| | | 2017 | | 2016 | | 2015 |

Per Share of Common Stock(1) | | | | | | | | | | | | |

Net asset value, beginning of period | | $ | 19.18 | | | $ | 19.20 | | | $ | 36.71 | |

Net investment income (loss)(2) | | | (0.45 | ) | | | (0.61 | ) | | | (0.53 | ) |

Net realized and unrealized gain (loss) | | | (0.92 | ) | | | 2.80 | | | | (14.39 | ) |

Total income (loss) from operations | | | (1.37 | ) | | | 2.19 | | | | (14.92 | ) |

Common dividends(3) | | | (0.53 | ) | | | — | | | | (2.15 | ) |

Common distributions — return of capital(3) | | | (1.37 | ) | | | (2.20 | ) | | | (0.48 | ) |

Total dividends and distributions — common | | | (1.90 | ) | | | (2.20 | ) | | | (2.63 | ) |

Offering expenses associated with the issuance of common stock | | | — | | | | — | | | | — | |

Effect of issuance of common stock | | | — | | | | — | | | | 0.03 | |

Effect of shares issued in reinvestment of dividends and distributions | | | (0.01 | ) | | | (0.01 | ) | | | 0.01 | |

Total capital stock transactions | | | (0.01 | ) | | | (0.01 | ) | | | 0.04 | |

Net asset value, end of period | | $ | 15.90 | | | $ | 19.18 | | | $ | 19.20 | |

Market value per share of common stock, end of period | | $ | 15.32 | | | $ | 19.72 | | | $ | 18.23 | |

Total investment return based on common stock market value(5) | | | (13.8 | )% | | | 24.1 | % | | | (47.7 | )% |

Total investment return based on net asset value(6) | | | (8.0 | )% | | | 14.6 | % | | | (42.8 | )% |

Supplemental Data and Ratios(7) | | | | | | | | | | | | |

Net assets applicable to common stockholders, end of period | | $ | 1,826,173 | | | $ | 2,180,781 | | | $ | 2,141,602 | |

Ratio of expenses to average net assets | | | | | | | | | | | | |

Management fees (net of fee waiver) | | | 2.5 | % | | | 2.5 | % | | | 2.6 | % |

Other expenses | | | 0.1 | | | | 0.2 | | | | 0.1 | |

Subtotal | | | 2.6 | | | | 2.7 | | | | 2.7 | |

Interest expense and distributions on mandatory redeemable preferred stock(2) | | | 2.0 | | | | 2.8 | | | | 2.4 | |

Income tax expense(8) | | | — | | | | 7.9 | | | | — | |

Total expenses | | | 4.6 | % | | | 13.4 | % | | | 5.1 | % |

Ratio of net investment income (loss) to average net assets(2) | | | (2.4 | )% | | | (3.4 | )% | | | (1.8 | )% |

Net increase (decrease) in net assets to common stockholders resulting from operations to average net assets | | | (7.5 | )% | | | 12.5 | % | | | (51.7 | )% |

Portfolio turnover rate | | | 17.6 | % | | | 14.5 | % | | | 17.1 | % |

Average net assets | | $ | 2,128,965 | | | $ | 2,031,206 | | | $ | 3,195,445 | |

Notes outstanding, end of period(9) | | $ | 747,000 | | | $ | 767,000 | | | $ | 1,031,000 | |

Borrowings under credit facilities, end of period(9) | | $ | — | | | $ | 43,000 | | | $ | — | |

Term loan outstanding, end of period(9) | | $ | — | | | $ | — | | | $ | — | |

Mandatory redeemable preferred stock, end of period(9) | | $ | 292,000 | | | $ | 300,000 | | | $ | 464,000 | |

Average shares of common stock outstanding | | | 114,292,056 | | | | 112,967,480 | | | | 110,809,350 | |

Asset coverage of total debt(10) | | | 383.6 | % | | | 406.3 | % | | | 352.7 | % |

Asset coverage of total leverage (debt and preferred stock)(11) | | | 275.8 | % | | | 296.5 | % | | | 243.3 | % |

Average amount of borrowings per share of common stock during the period(1) | | $ | 7.03 | | | $ | 7.06 | | | $ | 11.95 | |

See accompanying notes to financial statements.

24

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

FINANCIAL HIGHLIGHTS

(amounts in 000’s, except share and per share amounts)

See accompanying notes to financial statements.

25

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

(amounts in 000’s, except share and per share amounts)

1. Organization

Kayne Anderson Energy Infrastructure Fund, Inc. (the “Company” or “KYN”) was organized as a Maryland corporation on June 4, 2004, and is a non-diversified, closed-end management investment company registered under the Investment Company Act of 1940, as amended (the “1940 Act”). The Company’s investment objective is to provide a high after-tax total return with an emphasis on making cash distributions to shareholders. The Company intends to achieve this objective by investing at least 80% of its total assets in the securities of Energy Infrastructure Companies. The Company commenced operations on September 28, 2004. The Company’s shares of common stock are listed on the New York Stock Exchange, Inc. (“NYSE”) under the symbol “KYN.” For more information about the Company’s investment objective, policies and principal risks, see Investment Objective, Policies and Risks.

On November 13, 2023, KYN completed its merger with Kayne Anderson NextGen Energy & Infrastructure, Inc. (“KMF”). Pursuant to the terms of the merger agreement, KMF was merged with and into KYN, and KMF stockholders received either newly issued common stock of KYN or cash. The merger qualified as a tax-free reorganization under Section 368(a) of the Internal Revenue Code.

On August 1, 2024, a class action complaint was filed in the Circuit Court for Baltimore County against KMF and the members of its board of directors, as defendants, for alleged breaches of fiduciary duties arising from the merger of KMF and KYN. The Company is defending this litigation because it is the surviving entity from that merger. The Company believes the allegations in this complaint are without merit and intends to vigorously defend this action. The Company does not anticipate that this action will have a material impact on the Company or result in material losses.

2. Significant Accounting Policies

The following is a summary of the significant accounting policies that the Company uses to prepare its financial statements in accordance with accounting principles generally accepted in the United States of America (“GAAP”). The Company is an investment company and follows accounting and reporting guidance of the Financial Accounting Standards Board (FASB) Accounting Standards Codification (ASC) Topic 946 — “Financial Services — Investment Companies.”

A. Use of Estimates — The preparation of financial statements in conformity with GAAP requires management to make estimates and assumptions that affect the reported amount of assets and liabilities and disclosure of contingent assets and liabilities as of the date of the financial statements and the reported amounts of income and expenses during the period. Actual results could differ materially from those estimates.

B. Cash and Cash Equivalents — Cash and cash equivalents include short-term, liquid investments with an original maturity of three months or less and include money market fund accounts.

C. Calculation of Net Asset Value — The Company determines its net asset value on a daily basis and reports its net asset value on its website. Net asset value is computed by dividing the value of the Company’s assets (including accrued interest and distributions and current and deferred income tax assets), less all of its liabilities (including accrued expenses, distributions payable, current and deferred accrued income taxes, and any borrowings) and the liquidation value of any outstanding preferred stock, by the total number of common shares outstanding.

D. Investment Valuation — Pursuant to Rule 2a-5, the Company’s Board of Directors (the “Board”) has designated KA Fund Advisors, LLC (“KAFA“), the Company’s investment adviser, as the “Valuation Designee” to perform fair value determinations of the Company’s portfolio holdings, subject to oversight by and periodic reporting to the Board. The Valuation Designee determines the fair value of the Company’s portfolio holdings in accordance with the Company’s valuation program, as adopted by the Board.

26

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

(amounts in 000’s, except share and per share amounts)

Readily marketable portfolio securities listed on any exchange (including a foreign exchange) other than the NASDAQ Stock Market, Inc. (“NASDAQ”) are valued, except as indicated below, at the last sale price on the business day as of which such value is being determined. If there has been no sale on such day, the securities are valued at the mean of the most recent bid and ask prices on such day. Securities admitted to trade on the NASDAQ are valued at the NASDAQ official closing price. Portfolio securities traded on more than one securities exchange are valued at the last sale price on the business day as of which such value is being determined at the close of the exchange representing the principal market for such securities. The value of foreign securities traded outside of the Americas may be adjusted to reflect events occurring after a foreign exchange closes that may affect the value of the foreign security. In such cases, these foreign securities are valued by an independent pricing service and are categorized as Level 2 securities for purposes of the fair value hierarchy. See Note 3 — Fair Value.

Equity securities traded in the over-the-counter market, but excluding securities admitted to trading on the NASDAQ, are valued at the closing bid prices. Debt securities that are considered bonds are valued by using the bid price provided by an independent pricing service or, if such prices are not available or in the judgment of KAFA such prices are stale or do not represent fair value, by an independent broker. For debt securities that are considered bank loans, the fair market value is determined by using the bid price provided by the agent or syndicate bank or principal market maker. When price quotes for securities are not available, or such prices are stale or do not represent fair value in the judgment of KAFA, fair market value will be determined using the Company’s valuation process for securities that are privately issued or otherwise restricted as to resale.

Exchange-traded options and futures contracts are valued at the last sales price at the close of trading in the market where such contracts are principally traded or, if there was no sale on the applicable exchange on such day, at the mean between the quoted bid and ask price as of the close of such exchange.

The Company may hold securities that are privately issued or otherwise restricted as to resale. For these securities, as well as any security for which (a) reliable market quotations are not available in the judgment of KAFA, or (b) the independent pricing service or independent broker does not provide prices or provides a price that in the judgment of KAFA is stale or does not represent fair value, each shall be valued in a manner that most fairly reflects fair value of the security on the valuation date.

For the fiscal year ended November 30, 2024, unless otherwise determined by the Valuation Designee, the following valuation process was used for such securities:

• Valuation Designee. The applicable investments are valued monthly by KAFA, as the Valuation Designee, with new investments valued at the time such investment was made. The applicable investments are valued by senior professionals of KAFA who comprise KAFA’s valuation committee. KAFA will specify the titles of the persons responsible for determining the fair value of Company investments, including by specifying the particular functions for which they are responsible, and will reasonably segregate fair value determinations from the portfolio management of the Company such that the portfolio manager(s) may not determine, or effectively determine by exerting substantial influence on, the fair values ascribed to portfolio investments.

• Valuation Firm. Quarterly, a third-party valuation firm engaged by KAFA reviews the valuation methodologies and calculations employed for these securities, unless the aggregate fair value of such security is less than 0.1% of the Company’s total assets.

At November 30, 2024, the Company held 7.5% of its net assets applicable to common stockholders (5.4% of total assets) in securities that were fair valued pursuant to these procedures (Level 3 securities). The aggregate fair value of these securities at November 30, 2024, was $190,513. See Note 3 — Fair Value and Note 7 — Restricted Securities.

27

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

(amounts in 000’s, except share and per share amounts)

E. Security Transactions — Security transactions are accounted for on the date securities are purchased or sold (trade date). Realized gains and losses are calculated using the specific identification cost basis method for GAAP purposes. For tax purposes, the Company utilizes the average cost method to compute the adjusted tax cost basis of its MLP securities.

F. Return of Capital Estimates — Dividends and distributions received from the Company’s investments generally are comprised of income and return of capital. At the time such dividends and distributions are received, the Company estimates the amount of such payments that is considered investment income and the amount that is considered a return of capital. The Company estimates the return of capital portion of dividends and distributions received from investments based on historical information available and other information provided by certain investments. Return of capital estimates are adjusted to actual in the subsequent fiscal year when final tax reporting information related to the Company’s investments is received.

The return of capital portion of the distributions is a reduction to investment income that results in an equivalent reduction in the cost basis of the associated investments and increases net realized gains (losses) and net change in unrealized gains (losses). If the distributions received by the Company exceed its cost basis (i.e., its cost basis has been reduced to zero), the distributions are treated as realized gains.

The Company includes all distributions received on its Statement of Operations and reduces its investment income by (i) the estimated return of capital and (ii) the distributions in excess of cost basis, if any. Distributions received that were in excess of cost basis were treated as realized gains.

In accordance with GAAP, the return of capital cost basis reductions for the Company’s investments are limited to the total amount of the cash distributions received from such investments.

The following table sets forth the Company’s estimated return of capital portion of the dividends and distributions received from its investments that were not treated as distributions in excess of cost basis.

| | For the

Fiscal Year

Ended

November 30,

2024 |

Dividends and distributions (before foreign taxes withheld of $2,396 and excluding distributions in excess of cost basis) | | $ | 155,504 | |

Dividends and distributions — % return of capital | | | 45 | % |

Return of capital — attributable to net realized gains (losses) | | $ | 4,162 | |

Return of capital — attributable to net change in unrealized gains (losses) | | | 65,615 | |

Total return of capital | | $ | 69,777 | |

For the fiscal year ended November 30, 2024, the Company estimated the return of capital portion of dividends and distributions received to be $64,494 (41%). During the fiscal year ended November 30, 2024, the Company increased its return of capital estimate for the year by $5,283 due to 2023 tax reporting information received by the Company in fiscal 2024. As a result, the return of capital percentage for the fiscal year ended November 30, 2024 was 45%. In addition, for the fiscal year ended November 30, 2024, the Company estimated the cash distributions received that were in excess of cost basis to be $3,511. Distributions in excess of cost basis for the fiscal year ended November 30, 2024 were decreased by $1,561 due to 2023 tax reporting information received by the Company in fiscal 2024.

28

KAYNE ANDERSON ENERGY INFRASTRUCTURE FUND, INC.

NOTES TO FINANCIAL STATEMENTS

(amounts in 000’s, except share and per share amounts)