As filed pursuant to Rule 424(b)(3) under the Securities Act of 1933. Registration Number 333-144235 |

PROSPECTUS

WEST COAST CAR COMPANY

8,750,000 Shares of Common Stock

4,375,000 Shares of Common Stock

Underlying Warrants

Offered by Selling Stockholders

The selling stockholders identified in this prospectus are offering for sale from time to time up to 13,125,000 shares of our common stock, including 4,375,000 shares they may acquire on exercise of warrants. The common stock and warrants were issued to the selling stockholders in a private placement completed on May 15, 2007. The warrants expire on May 15, 2012 and have an exercise price of $2.60 per share, as adjusted.

The selling stockholders may offer all or part of their shares for resale from time to time through public or private transactions, at either prevailing market prices or at privately negotiated prices. We will not receive any of the proceeds from the sales of the shares by the selling stockholders. To the extent the warrants are exercised, if at all, we will receive the exercise price for those warrants. We will pay all of the registration expenses incurred in connection with this offering (estimated to be $192,118), but the selling stockholders will pay all of the selling commissions, brokerage fees and related expenses.

Our common stock is quoted on the National Association of Securities Dealers Over-the-Counter Bulletin Board under the symbol "WCSC.OB". As of June 22, 2007, the last reported bid price of our common stock was $3.50 per share and the last reported ask price was $4.50 per share.

There is a limited market in our common stock. The shares are being offered by the selling stockholders in anticipation of the development of a secondary trading market in our common stock. We cannot give you any assurance that an active trading market in our common stock will develop, or if an active market does develop, that it will continue.

Investing in our common stock involves a high degree of risk. See “Risk Factors” beginning on page 12 for a discussion of certain risk factors that you should consider.

You should read the entire prospectus before making an investment decision.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is July 16, 2007

3

TABLE OF CONTENTS

| About This Prospectus | 5 | |

| Cautionary Note Regarding Forward Looking Statements | ||

| and Other Information Contained in this Prospectus | 5 | |

| Prospectus Summary | 7 | |

| Risk Factors | 12 | |

| Use of Proceeds | 26 | |

| Selected Consolidated Financial Data | 27 | |

| Management's Discussion and Analysis of Financial Condition | ||

| and Results of Operations | 28 | |

| Quantitative and Qualitative Disclosure About Market Risk | 33 | |

| Business | 34 | |

| Properties | 52 | |

| Legal Proceedings | 53 | |

| Market Price of and Dividends on our Common Stock | ||

| And Related Stockholder Matters | 53 | |

| Security Ownership of Certain Beneficial Owners and Management | 56 | |

| Directors and Executive Officers | 57 | |

| Executive Compensation | 60 | |

| Certain Relationships and Related Transactions | 63 | |

| Selling Stockholders | 64 | |

| Plan of Distribution | 67 | |

| Description of Our Securities | 69 | |

| Changes in and Disagreements with Accountants | 71 | |

| Where You Can Find More Information | 72 | |

| Legal Matters | 72 | |

| Experts | 72 | |

| Financial Statements | F-1 |

4

ABOUT THIS PROSPECTUS

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. The selling stockholders are offering to sell and seeking offers to buy shares of our common stock, including shares they acquire upon exercise of their warrants, only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of our common stock. The prospectus will be updated and updated prospectuses made available for delivery to the extent required by the federal securities laws.

No person is authorized in connection with this prospectus to give any information or to make any representations about us, the selling stockholders, the securities or any matter discussed in this prospectus, other than the information and representations contained in this prospectus. If any other information or representation is given or made, such information or representation may not be relied upon as having been authorized by us or any selling stockholder. This prospectus does not constitute an offer to sell, or a solicitation of an offer to buy the securities in any circumstances under which the offer or solicitation is unlawful. Neither the delivery of this prospectus nor any distribution of securities in accordance with this prospectus shall, under any circumstances, imply that there has been no change in our affairs since the date of this prospectus. The prospectus will be updated and updated prospectuses made available for delivery to the extent required by the federal securities laws.

CAUTIONARY NOTE REGARDING FORWARD-LOOKING STATEMENTS AND OTHER INFORMATION CONTAINED IN THIS PROSPECTUS

This prospectus contains some forward-looking statements. Forward-looking statements give our current expectations or forecasts of future events. You can identify these statements by the fact that they do not relate strictly to historical or current facts. Forward-looking statements involve risks and uncertainties. Forward-looking statements include statements regarding, among other things, (a) our projected sales, profitability, and cash flows, (b) our growth strategies, (c) anticipated trends in our industries, (d) our future financing plans and (e) our anticipated needs for working capital. They are generally identifiable by use of the words "may," "will," "should," "anticipate," "estimate," "plans," “potential," "projects," "continuing," "ongoing," "expects," "management believes," "we believe," "we intend" or the negative of these words or other variations on these words or comparable terminology. These statements may be found under "Management's Discussion and Analysis of Financial Condition and Results of Operations" and "Business," as well as in this prospectus generally. In particular, these include statements relating to future actions, prospective products or product approvals, future performance or results of current and anticipated products, sales efforts, expenses, the outcome of contingencies such as legal proceedings, and financial results.

Any or all of our forward-looking statements in this report may turn out to be inaccurate. They can be affected by inaccurate assumptions we might make or by known or unknown risks or uncertainties. Consequently, no forward-looking statement can be guaranteed. Actual future results may vary materially as a result of various factors, including, without limitation, the risks outlined under "Risk Factors" and matters described in this prospectus generally. In light of these risks and uncertainties, there can be no assurance that the forward-looking statements contained in this filing will in fact occur. You should not place undue reliance on these forward-looking statements.

5

The forward-looking statements speak only as of the date on which they are made, and, except to the extent required by federal securities laws, we undertake no obligation to publicly update any forward-looking statements, whether as the result of new information, future events, or otherwise.

Currency

Unless otherwise noted, all currency figures in this filing are in U.S.dollars. References to "yuan" or "RMB" are to the Chinese yuan (also known as the Renminbi). According to www.Xe.com as of June 26, 2007, $1 = 7.61650 yuan.

6

PROSPECTUS SUMMARY

This summary highlights information contained elsewhere in this prospectus. This summary does not contain all of the information you should consider before investing in our common stock. You should read the entire prospectus, including "Risk Factors" and the consolidated financial statements and the related notes before making an investment decision. Except as otherwise specifically stated or unless the context otherwise requires, the “Company,” we," "our" and "us" refers collectively to West Coast Car Company, a Delaware corporation and its subsidiaries, Shengtai Holding Inc., a New Jersey Corporation and Weifang Shengtai Pharmaceutical Co., Ltd, a wholly foreign-owned entity organized under the laws of the People's Republic of China (“PRC”).

THE COMPANY

Business Overview

We are engaged in the business of manufacturing and supplying pharmaceutical grade glucose products for medicinal purposes and other glucose and starch products used for the food and beverage industry and for industrial production primarily in the People's Republic of China (“PRC”). Our business is conducted through our indirect wholly-owned subsidiary Weifang Shengtai Pharmaceutical Co., Ltd. (“Weifang Shengtai”).

Approximately 92% of our sales revenues for the fiscal year ended June 30, 2006 were derived from sales made to the pharmaceutical industry.

Approximately 85% of our sales revenues for the fiscal year ended June 30, 2006 were derived from the PRC, with approximately 15% of our sales derived from the international market.

Corporate History

West Coast Car Company (“WCCC”) was incorporated in Delaware in March 2004 and commenced operations in Temecula, California in November 2004 doing business as So Cal Car Company. Until July 2006, WCCC was a pre-owned retail automobile dealership in Southern California, operating as a "traditional" pre-owned dealership, whereby it sought out vehicles from various sources, such as auctions, private parties and wholesalers and then sold the vehicles to the general public. The Company was unable to achieve a profit and did not renew its lease when it expired at the end of July 2006.

WCCC had limited operations and generated no revenue for the year ended December 31, 2006 and revenue of $30,318 for the year ended December 31, 2005

On September 26, 2005, WCCC registered as a public reporting company by filing a Form 10-SB with the Securities and Exchange Commission under Section12(g) of the Securities Exchange Act of 1934, as amended. (the “Exchange Act”). On January 12, 2007 WCCC’s common stock was available for quotation on the Over the Counter Bulletin Board under the symbol "WCSC.”

7

On February 4, 1999, Weifang Shengtai was established in Changle County, Weifang City, Shandong Province, PRC. Mr. Qingtai Liu and Weifang Shengtai’s management were the original shareholders.

In February 1999, Weifang Shengtai acquired for $775,000 all the assets of Weifang Fifth Pharmaceutical Plant, a former PRC state-owned enterprise (who had defaulted on a bank loan of approximately $5 million and which had its pledged assets taken over by the lending bank).

On February 27, 2006, Shengtai Holding Inc., a New Jersey corporation (“SHI”), was formed by Messrs. Qingtai Liu and Chenghai Du as a holding company for Weifang Shengtai.

On June 20, 2006, SHI acquired all of the outstanding shares of Weifang Shengtai from Mr. Qingtai Liu and Bio-One, Inc. SHI acquired Mr. Qingtai Liu’s 49% equity interest in Weifang Shengtai for approximately RMB 15 million (approximately $1,920,000) and acquired Bio-One’s 51% equity interest in Weifang Shengtai for $1,000,000 as well as a return of $4,180,000 worth of preferred stock of Bio-One. As a result of this acquisition, Weifang Shengtai became a wholly foreign owned entity or “WFOE” and obtained the requisite approval of the local branch of the Ministry of Commerce in the City of Weifang on June 21, 2006. Its business term is 20 years starting on February 10, 2004, the date of approval of a previous joint venture which was not pursued. Weifang Shengtai’s registered capital is RMB32 million (approximately $3.92 million) of which $1,925,996 was required to be contributed by June 21, 2007. This amount has already been sent to Weifang Shengtai from the proceeds raised under the share purchase agreement described below.

Share Exchange Agreement

On May 15, 2007, WCCC entered into a share exchange agreement with the stockholders of SHI, under which Messrs. Qingtai Liu and Chenghai Du, holders of all of the issued and outstanding shares of common stock of SHI, exchanged all of their shares of SHI for 8,212,500 and 912,500, respectively, newly-issued shares of common stock of WCCC. The newly issued shares represented approximately 91% of the then outstanding shares of WCCC. The share exchange transaction closed on May 15, 2007. As a result of the share exchange SHI became a direct wholly-owned subsidiary of WCCC and Weifang Shengtai became an indirect wholly-owned subsidiary.

In connection with the share exchange, WCCC’s former directors, Daniel Drummond and Alex Ferries, appointed Mr. Qingtai Liu as Chief Executive Officer and President, and as a director of WCCC and appointed Yongqiang Wang as a director and thereafter resigned as directors and officers of WCCC, subject to the filing and dissemination of Schedule 14f-1. WCCC filed an information statement with the SEC on May 4, 2007, relating to the change in control of WCCC’s Board of Directors containing the information required under Rule 14f-1 of the Securities Exchange Act of 1934, as amended and on May 4, 2007. WCCC distributed that information statement to all holders of record of its common stock. After the closing of the share exchange, there occurred a change in control in the Board of Directors with Messrs. Qingtai Liu and Yongqiang Wang constituting the sole members of the Board of Directors.

8

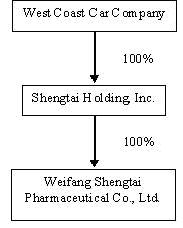

Corporate Structure

As a result of the consummation of the share exchange on May 15, 2007, our corporate structure is as follows:

The Share Purchase Agreement

On May 15, 2007, we entered into and closed on a share purchase agreement with nineteen accredited investors (who are the selling stockholders named in this prospectus (the “Selling Stockholders”) who purchased from us for $2.00 per share (or an aggregate purchase price of $17,500,000) an aggregate of 8,750,000 shares of common stock and 4,375,000 attached five year warrants with an exercise price of $2.60 per share, as adjusted. We received net cash proceeds of approximately $15,323,000 from this financing. The closing of the transaction contemplated by the share purchase agreement occurred immediately following the closing of the share exchange. Brill Securities, Inc. acted as placement agent for the share purchase and received $875,000 as a placement fee, an additional $175,000 for non accountable expenses and are entitled to receive warrants to purchase 109,375 shares of common stock. We are registering for resale in this prospectus 13,125,000 shares of common stock which represents all of 8,750,000 shares of common stock purchased by the Selling Stockholders and all of the 4,375,000 shares of common stock issuable on exercise of the warrants. For additional disclosure relating to the terms of the share purchase agreement, reference is made to “BUSINESS - Corporate History.”

Executive Offices

Our executive offices are located at 45 Old Millstone Drive, Unit #6, East Windsor, NJ 08520, and its telephone number is (609) 426-8996.

9

THE OFFERING

The Offering

This prospectus relates to (i) 8,750,000 shares of common stock and (ii) 4,375,000 shares of common stock underlying warrants attached to the shares of common stock. These shares and attached warrants were purchased by the Selling Stockholders pursuant to the share purchase agreement entered into on May 15, 2007 and may be offered for sale by the Selling Stockholders from time to time.

| Common stock outstanding prior to Offering | 18,875,000 | |

| Common stock offered by the Company | 0 shares | |

| Total shares of common stock offered by Selling Stockholders | 13,125,000 (includes 4,375,000 shares underlying the warrants attached to the shares purchased by the Selling Stockholders in the May 15, 2007 private placement.) | |

| Common stock to be outstanding after the offering (assuming all warrants have been exercised) | 23,250,000 | |

| Use of Proceeds | We will not receive any of the proceeds from the sale of the shares owned by the Selling Stockholders. However, we will receive the net proceeds from any exercise of the warrants to acquire up to 4,375,000 shares offered under this prospectus. We intend to use any proceeds received from the exercise of warrants for working capital and other general corporate purposes. We cannot assure you that any of the warrants will ever be exercised. | |

| Our OTC Bulletin Board Trading Symbol | WCSC.OB | |

| Risk Factors | See "Risk Factors" beginning on page 12 and other information included in this prospectus for a discussion of factors you should consider before deciding to invest in shares of our common stock. |

Background

On May 15, 2007, we entered into a share purchase agreement under which the Selling Stockholders purchased from us, for $2.00 per share or an aggregate purchase price of $17,500,000, an aggregate of 8,750,000 shares of common stock and 4,375,000 attached warrants. This financing closed on May 15, 2007 and we received approximately $15,323,000 as net proceeds. Under the terms of the share purchase agreement, which granted the investors certain registration rights with respect to the shares of common stock which they purchased as well as the shares underlying the warrants purchased, we are required to file an initial registration statement on Form S-1 (or such other form as may be applicable) covering those shares.

10

Reference is made to “Selling Stockholders - Background” in this prospectus for disclosure relating to our obligations, as set forth in share purchase agreement, to register the shares (and the shares underlying the warrants) and the circumstances in which we may be required to pay liquidated damages for failing to comply with those obligations.

Plan of Distribution

This offering is not being underwritten. The Selling Stockholders directly, through agents designated by them from time to time or through brokers or dealers also to be designated, may sell their shares from time to time, in or through privately negotiated transactions, or in one or more transactions, including block transactions, on the OTC Bulletin Board or on any stock exchange on which the shares may be listed in the future pursuant to and in accordance with the applicable rules of such exchange or otherwise. The selling price of the shares may be at market prices prevailing at the time of sale, at prices related to such prevailing market prices or at negotiated prices. To the extent required, the specific shares to be sold, the names of the Selling Stockholders, the respective purchase prices and public offering prices, the names of any such agent, broker or dealer and any applicable commission or discounts with respect to a particular offer will be described in an accompanying prospectus. In addition, any securities covered by this prospectus which qualify for sale pursuant to Rule 144 may be sold under Rule 144 rather than pursuant to this prospectus. We will keep this prospectus current until the expiration dates of the warrants (May 15, 2012), even if the warrants which underlie certain shares of our common stock subject to this prospectus are out of the money.

We will not receive any proceeds from sales of shares by the Selling Stockholders. However, if any of the Selling Stockholders decide to exercise their warrants, we will receive the net proceeds of the exercise of outstanding warrants held by the Selling Stockholders. The warrants do not provide for cashless exercise. We intend to use any proceeds we receive from the exercise of warrants for working capital and other general corporate purposes. We cannot assure you that any of the warrants ever be exercised.

We will pay all expenses of registration incurred in connection with this offering (estimated to be $192,118), but the Selling Stockholders will pay all of the selling commissions, brokerage fees and related expenses. We have agreed to indemnify the Selling Stockholders against certain liabilities, including liabilities under the Securities Act.

The Selling Stockholders and any broker-dealers or agents that participate with the Selling Stockholders in the distribution of any of the shares may be deemed to be “underwriters” within the meaning of the Securities Act, and any commissions received by them and any profit on the resale of the shares purchased by them may be deemed to be underwriting commissions or discounts under the Securities Act.

11

An investment in our common stock involves a high degree of risk. You should carefully consider the risks described below and the other information contained in this prospectus before deciding to invest in our common stock.

Risks related to doing business in the People’s Republic of China

Our business operations are conducted primarily in the PRC. Because Chinese laws, regulations and policies are continually changing, our Chinese operations will face several risks summarized below.

Our ability to operate in the PRC may be harmed by changes in its laws and regulations

Our offices and manufacturing plants are located in the PRC and the production, sale and distribution of our products are subject to PRC rules and regulations. In particular, the manufacture and supply of pharmaceutical grade and medicinal products are subject to the PRC rules and regulations, such as the Good Practice in the Manufacturing and Quality Control of Drugs (as amended in 1998) as promulgated by the PRC State Food and Drug Administration on March 18, 1999 and the PRC Medical Products Governance Law. In addition, because we operate a cornstarch production facility which produces waste water and we are subject to the environmental rules and regulations such as the Integrated Wastewater Discharge Standard (GB8978-1996).

The PRC only recently has afforded provincial and local economic autonomy and permitted private economic activities. The PRC government has exercised and continues to exercise substantial control over virtually every sector of the PRC economy through regulation and state ownership.

Our ability to operate in the PRC may be harmed by changes in its laws and regulations, including those relating to manufacturing, taxation, import and export tariffs, environmental regulations, land use rights, property and other matters.

Our production and manufacturing facility is subject to PRC regulation and environmental laws. The PRC government has been active in regulating the pharmaceutical and medicinal goods industry. Our business and products are subject to government regulations mandating the use of good manufacturing practices. Changes in these laws or regulations in the PRC, or other countries we sell into, that govern or apply to our operations could have a materially adverse effect on our business. For example, the law could change so as to prohibit the use of certain chemical agents in our products. If such chemical agents are found in our products, then such a change would reduce our productivity of that product.

We are a state-licensed corporation. If we were to lose our state-licensed status, we would no longer be able to manufacture our products in the PRC.

There is no assurance that PRC economic reforms will not adversely affect our operations in the future

As a developing nation, the PRC's economy is more volatile than that of developed Western industrial economies. It differs significantly from that of the U.S. or a Western European country in such respects as structure, level of development, capital reinvestment, resource allocation and self-sufficiency. Only in recent years has the PRC economy moved from what had been a command economy through the 1970s to one that during the 1990s encouraged substantial private economic activity. Although the PRC government still owns the majority of productive assets in the PRC, in the past several years the government has implemented economic reform measures that emphasize decentralization and encourage private economic activity.

12

In 1993, the Constitution of the PRC was amended to reinforce such economic reforms. The trends of the 1990s indicate that future policies of the Chinese government will emphasize greater utilization of market forces. The PRC government has confirmed that economic development will follow the model of a market economy. For example, in 1999 the Government announced plans to amend the Chinese Constitution to recognize private property, although private business will officially remain subordinated to the state-owned companies, which are the mainstay of the Chinese economy. However, there can be no assurance that, under some circumstances, the government's pursuit of economic reforms will not be restrained or curtailed. Actions by the central government of the PRC could have a significant adverse effect on economic conditions in the country as a whole and on the economic prospects for our Chinese operations. Economic reforms could either benefit or damage our operations and profitability. Some of the things that could have this effect are: (i) level of government involvement in the economy; (ii) control of foreign exchange; (iii) methods of allocating resources; (iv) international trade restrictions; and (v) international conflict.

Under the present direction, we believe that the PRC will continue to strengthen its economic and trading relationships with foreign countries and business development in the PRC will follow market forces. While we believe that this trend will continue, there can be no assurance that this will be the case. A change in policies by the PRC government could adversely affect our interests by, among other factors: changes in laws, regulations or the interpretation thereof, confiscatory taxation, restrictions on currency conversion, imports or sources of supplies, or the expropriation or nationalization of private enterprises and could require us to divest ourselves of any interest we then hold in Chinese properties or businesses.

Although the PRC government has been pursuing economic reform policies for more than two decades, there is no assurance that the government will continue to pursue these policies or that these policies may not be significantly changed, especially in the event of a change in leadership, social or political disruption, or other circumstances affecting the PRC's political, economic and social life.

Because these economic reform measures may be inconsistent, ineffectual or temporary, there are no assurances that:

| · | we will be able to capitalize on economic reforms; |

| · | the Chinese government will continue its pursuit of economic reform policies; |

| · | the economic policies, even if pursued, will be successful; |

| · | economic policies will not be significantly altered from time to time; and |

| · | business operations in the PRC will not become subject to the risk of nationalization. |

13

Anti-inflation measures may be ineffective or harm our ability to do business in the PRC

Since 1979, the PRC government has reformed its economic system. Because many reforms are unprecedented or experimental, they are expected to be refined and improved. Other political, economic and social factors, such as political changes, changes in the rates of economic growth, unemployment or inflation, or in the disparities in per capita wealth between regions within the PRC, could lead to further readjustment of the reform measures. This refining and readjustment process may instead negatively affect our operations and there is guarantee that it will be effective.

Over the last few years, the PRC's economy has registered a high growth rate. During the past ten years, the rate of inflation in the PRC has been as high as 20.7% and as low as -2.2%. Recently, there have been indications that rates of inflation have increased. In response, the PRC government recently has taken measures to curb this excessively expansive economy. These corrective measures were designed to restrict the availability of credit or regulate growth and contain inflation. These measures have included devaluations of the PRC currency, the Renminbi (RMB), restrictions on the availability of domestic credit, reducing the purchasing capability of certain of its customers, and limited re-centralization of the approval process for purchases of some foreign products. These austerity measures alone may not succeed in slowing down the economy's excessive expansion or control inflation, and may result in severe dislocations in the PRC economy. The PRC government may adopt additional measures to further combat inflation, including the establishment of freezes or restraints on certain projects or markets. Such measures could harm the market for our products and inhibit our ability to conduct business in the PRC.

The PRC’s legal and judicial system may not adequately protect our business and operations and the rights of foreign investors

The PRC legal and judicial system may negatively impact foreign investors. In 1982, the National People's Congress amended the Constitution of China to authorize foreign investment and guarantee the "lawful rights and interests" of foreign investors in the PRC. However, the PRC's system of laws is not yet comprehensive. The legal and judicial systems in the PRC are still rudimentary, and enforcement of existing laws is inconsistent. Many judges in the PRC lack the depth of legal training and experience that would be expected of a judge in a more developed country. Because the PRC judiciary is relatively inexperienced in enforcing the laws that do exist, anticipation of judicial decision-making is more uncertain than would be expected in a more developed country. It may be impossible to obtain swift and equitable enforcement of laws that do exist, or to obtain enforcement of the judgment of one court by a court of another jurisdiction. The PRC's legal system is based on the civil law regime, that is, it is based on written statutes; a decision by one judge does not set a legal precedent that is required to be followed by judges in other cases. In addition, the interpretation of Chinese laws may be varied to reflect domestic political changes.

The promulgation of new laws, changes to existing laws and the pre-emption of local regulations by national laws may adversely affect foreign investors. However, the trend of legislation over the last 20 years has significantly enhanced the protection of foreign investment and allowed for more control by foreign parties of their investments in Chinese enterprises. There can be no assurance that a change in leadership, social or political disruption, or unforeseen circumstances affecting the PRC's political, economic or social life, will not affect the PRC government's ability to continue to support and pursue these reforms. Such a shift could have a material adverse effect on our business and prospects.

14

The practical effect of the PRC legal system on our business operations in the PRC can be viewed from two separate but intertwined considerations. First, as a matter of substantive law, the Foreign Invested Enterprise laws provide significant protection from government interference. In addition, these laws guarantee the full enjoyment of the benefits of corporate Articles and contracts to Foreign Invested Enterprise participants. These laws, however, do impose standards concerning corporate formation and governance, which are qualitatively different from the general corporation laws of the United States. Similarly, the PRC accounting laws mandate accounting practices, which are not consistent with U.S. generally accepted accounting principles. PRC’s accounting laws require that an annual "statutory audit" be performed in accordance with PRC accounting standards and that the books of account of Foreign Invested Enterprises are maintained in accordance with Chinese accounting laws. Article 14 of the People's Republic of China Wholly Foreign-Owned Enterprise Law requires a wholly foreign-owned enterprise to submit certain periodic fiscal reports and statements to designated financial and tax authorities, at the risk of business license revocation. Weifang Shengtai is a wholly foreign owned enterprise. Second, while the enforcement of substantive rights may appear less clear than United States procedures, the Foreign Invested Enterprises and Wholly Foreign-Owned Enterprises are Chinese registered companies, which enjoy the same status as other Chinese registered companies in business-to-business dispute resolution.

Since the Articles of Association of Weifang Shengtai do not provide for the resolution of disputes business, the parties are free to proceed to either the Chinese courts or if they are in agreement, to arbitration.

Any award rendered by an arbitration tribunal is enforceable in accordance with the United Nations Convention on the Recognition and Enforcement of Foreign Arbitral Awards (1958). Therefore, as a practical matter, although no assurances can be given, the Chinese legal infrastructure, while different in operation from its United States counterpart, should not present any significant impediment to the operation of Foreign Invested Enterprises.

In addition, some of our present and future executive officers and our directors, most notably, Mr. Qingtai Liu, Mr. Yongqiang Wang and Mr. Yizhao Zhang, may be residents of the PRC and not of the United States, and substantially all the assets of these persons are located outside the U.S. As a result, it could be difficult for investors to effect service of process in the United States, or to enforce a judgment obtained in the United States against us or any of these persons.

The PRC laws and regulations governing our current business operations are sometimes vague and uncertain. There are substantial uncertainties regarding the interpretation and application of PRC laws and regulations, including but not limited to the laws and regulations governing our business, or the enforcement and performance of our arrangements with customers in the event of the imposition of statutory liens, death, bankruptcy and criminal proceedings. We and any future subsidiaries are considered foreign persons or foreign funded enterprises under PRC laws, and as a result, we are required to comply with PRC laws and regulations. These laws and regulations are sometimes vague and may be subject to future changes, and their official interpretation and enforcement may involve substantial uncertainty. The effectiveness of newly enacted laws, regulations or amendments may be delayed, resulting in detrimental reliance by foreign investors. New laws and regulations that affect existing and proposed future businesses may also be applied retroactively. We cannot predict what effect the interpretation of existing or new PRC laws or regulations may have on our business.

15

Governmental control of currency conversion may affect the value of your investment.

The majority of our revenues will be settled in Renminbi and U.S. dollars, and any future restrictions on currency exchanges may limit our ability to use revenue generated in Renminbi to fund any future business activities outside the PRC or to make dividend or other payments in U.S. dollars. Although the Chinese government introduced regulations in 1996 to allow greater convertibility of the Renminbi for current account transactions, significant restrictions still remain, including primarily the restriction that foreign-invested enterprises like us may only buy, sell or remit foreign currencies after providing valid commercial documents, at those banks in the PRC authorized to conduct foreign exchange business.

In addition, conversion of Renminbi for capital account items, including direct investment and loans, is subject to governmental approval in the PRC, and companies are required to open and maintain separate foreign exchange accounts for capital account items. We cannot be certain that the PRC regulatory authorities will not impose more stringent restrictions on the convertibility of the Renminbi.

The value of our securities and your ability to receive dividends may be affected by the foreign exchange rate between U.S. dollars and Renminbi and the PRC government’s control over the Renminbi.

The value of our common stock will be affected by the foreign exchange rate between U.S. dollars and Renminbi, and between those currencies and other currencies in which our sales may be denominated. For example, to the extent that we need to convert U.S. dollars into Renminbi for our operational needs and should the Renminbi appreciate against the U.S. dollar at that time, our financial position, the business of the Company, and the price of our common stock may be harmed. Conversely, if we decide to convert our Renminbi into U.S. dollars for the purpose of declaring dividends on our common stock or for other business purposes and the U.S. dollar appreciates against the Renminbi, the U.S. dollar equivalent of our earnings from our subsidiary in the PRC would be reduced.

The PRC government imposes controls on the convertibility of Renminbi into foreign currencies and, in certain cases, the remittance of currency out of the PRC. We receive substantially all of our revenues in Renminbi which is currently not a freely convertible currency. Shortages in the availability of foreign currency may restrict our ability to remit sufficient foreign currency to pay dividends, or otherwise satisfy foreign currency dominated obligations. Under existing PRC foreign exchange regulations, payments of current account items, including profit distributions, interest payments and expenditures from the transaction, can be made in foreign currencies without prior approval from the PRC State Administration of Foreign Exchange by complying with certain procedural requirements. However, approval from appropriate governmental authorities is required where RMB is to be converted into foreign currency and remitted out of the PRC to pay capital expenses, such as the repayment of bank loans denominated in foreign currencies.

The PRC government may also at its discretion restrict access in the future to foreign currencies for current account transactions. If the foreign exchange control system prevents us from obtaining sufficient foreign currency to satisfy our currency demands, we may not be able to pay certain expenses as they come due.

16

The fluctuation of the Renminbi may materially and adversely affect your investment.

The value of the Renminbi against the U.S. Dollar and other currencies may fluctuate and is affected by, among other things, changes in the PRC's political and economic conditions. As we rely almost entirely on revenues earned in the PRC since most of our sales occur in the PRC, any significant revaluation of the Renminbi may materially and adversely affect our cash flows, revenues and financial condition. For example, to the extent that we need to convert U.S. Dollars we receive from an offering of our securities into Renminbi for our operations, appreciation of the Renminbi against the U.S. Dollar could have a material adverse effect on our business, financial condition and results of operations. Conversely, if we decide to convert our Renminbi into U.S. Dollars for the purpose of making payments for dividends on our common shares or for other business purposes and the U.S. Dollar appreciates against the Renminbi, the U.S. Dollar equivalent of the Renminbi we convert would be reduced. In addition, the depreciation of significant U.S. Dollar denominated assets could result in a charge to our income statement and a reduction in the value of these assets.

On July 21, 2005, the PRC government changed its decade-old policy of pegging the value of the Renminbi to the U.S. Dollar. Under the new policy, the Renminbi is permitted to fluctuate within a narrow and managed band against a basket of certain foreign currencies. This change in policy has resulted in an approximately 2.0% appreciation of the Renminbi against the U.S. Dollar. While the international reaction to the Renminbi revaluation has generally been positive, there remains significant international pressure on the PRC government to adopt an even more flexible currency policy, which could result in a further and more significant appreciation of the Renminbi against the U.S. Dollar.

Recent SAFE Regulations may restrict our ability to remit profits out of the PRC as dividends

Recent PRC State Administration of Foreign Exchange ("SAFE") Regulations regarding offshore financing activities by PRC residents have undergone a number of changes which may increase the administrative burden we face. The failure by our stockholders who are PRC residents to make any required applications and filings pursuant to such regulations may prevent us from being able to distribute profits and could expose us and our PRC resident stockholders to liability under PRC law.

SAFE issued a public notice ("October Notice") effective from November 1, 2005, which requires registration with SAFE by the PRC resident stockholders of any foreign holding company of a PRC entity. The Company is a foreign holding company of a PRC entity. Without registration, the PRC entity cannot remit any of its profits out of the PRC as dividends or otherwise; however, it is uncertain how the October Notice will be interpreted or implemented regarding specific documentation requirements for a foreign holding company formed prior to the effective date of the October Notice, such as in our case. In addition, the October Notice requires that any monies remitted to PRC residents outside of the PRC be returned within 180 days; however, there is no indication of what the penalty will be for failure to comply or if stockholder non-compliance will be considered to be a violation of the October Notice by us or otherwise affect us.

In the event that the proper procedures are not followed under the SAFE October Notice, we could lose the ability to remit monies outside of the PRC and would therefore be unable to pay dividends or make other distributions. Our PRC resident stockholders could be subject to fines, other sanctions and even criminal liabilities under the PRC Foreign Exchange Administrative Regulations promulgated January 29, 1996, as amended.

17

Risks related to our business

We give no assurances that any plans for future expansion will be implemented or that they will be successful.

While we have expansion plans, which include building a cornstarch manufacturing plant (which is already partly completed and operational), upgrading our existing glucose manufacturing facility and expanding our sales overseas, there is no guarantee that such plans will be implemented or that they will be successful. These plans are subject to, among other things, their feasibility to meet the challenges we face, our ability to arrange for sufficient funding and the ability to hire qualified and capable employees to carry out these expansion plans.

We have a limited operating history and limited historical financial information upon which you may evaluate our performance.

Our operating subsidiary, Weifang Shengtai, was incorporated in 1999 and our operations have been largely confined to the PRC. In addition, while we have had some experience in managing a cornstarch manufacturing facility, we may not be adequately prepared to manage and operate a larger and more modern facility.

We are in our early stages of development and face risks associated with a new company in a growth industry. We may not successfully address these risks and uncertainties or successfully implement our operating strategies. If we fail to do so, it could materially harm our business to the point of having to cease operations and could impair the value of our common stock to the point investors may lose their entire investment. Even if we accomplish these objectives, we may not generate positive cash flows or the profits we anticipate in the future.

Although our revenues have grown rapidly since our inception from the growing demand for our glucose products, we cannot assure you that we will maintain our profitability or that we will not incur net losses in the future. We expect that our operating expenses will increase as we expand. Any significant failure to realize anticipated revenue growth could result in significant operating losses. We will continue to encounter risks and difficulties frequently experienced by companies at a similar stage of development, including our potential failure to:

| · | expand our product offerings and maintain the high quality of our products; |

| · | manage our expanding operations, including the integration of any future acquisitions; |

| · | obtain sufficient working capital to support our expansion and to fill customers' orders in time; |

| · | maintain adequate control of our expenses; |

| · | implement our product development, marketing, sales, and acquisition strategies and adapt and modify them as needed; and |

| · | anticipate and adapt to changing conditions in the dextrose monohydrate and glucose products markets in which we operate as well as the impact of any changes in government regulation, mergers and acquisitions involving our competitors, technological developments and other significant competitive and market dynamics. |

18

If we are not successful in addressing any or all of these risks, our business may be materially and adversely affected.

Because we are a relatively new company, we may not be experienced enough to address all the risks in our business or in our expansion including successfully operating our new cornstarch manufacturing plant. If we are unable to anticipate and react to such risks, our business may be materially and adversely affected.

We will face a lot of competition, some of which may be from companies which may be better capitalized and more experienced than us.

We face competition from other domestic and global manufacturers and suppliers of pharmaceutical grade dextrose monohydrate and glucose. Although we view ourselves in a favorable position vis-à-vis our competition, some of the other companies that sell into our markets may be more successful than us and/or have more experience and money that we do. This additional experience and money may enable our competitors to produce more cost-effective products and market their products with more success than we are able to, which would decrease our sales. We expect that we will be required to continue to invest in product development and productivity improvements to compete effectively in our markets. However, we cannot give assure you that we can successfully remain competitive. If our competitors developed a more efficient product or undertook more aggressive and costly marketing campaigns than us this could have a material adverse effect on our business, results of operations or financial condition.

A slowdown in the PRC economy may adversely affect our operations.

As all of our operations are conducted in the PRC and most of all of our revenues are generated from sales in the PRC, a slowdown or other adverse developments in the PRC economy could materially and adversely affect our customers, demand for our products and our business. Although the PRC economy has grown significantly in recent years, we cannot assure you that such growth will continue. While we believe the demand for our products is not dependent on the health of the economy, we do not know how sensitive we are to a slowdown in economic growth or other adverse changes in the PRC economy. A slowdown in overall economic growth, an economic downturn or recession or other adverse economic developments in the PRC may materially reduce the demand for our products and materially and adversely affect our business.

Our major competitors may be better able than us to successfully endure downturns in our sector. In periods of reduced demand for our products, we can either choose to maintain market share by reducing our selling prices to meet competition or maintain selling prices, which would likely sacrifice market share. Sales and overall profitability would be reduced under either scenario. In addition, we cannot assure you that additional competitors will not enter our existing markets, or that we will be able to compete successfully against existing or new competition.

Inflation in the PRC could negatively affect our profitability and growth.

While the PRC economy has experienced rapid growth, such growth has been uneven among various sectors of the economy and in different geographical areas of the country. Rapid economic growth can lead to growth in the money supply and rising inflation. If prices for our products rise at a rate that is insufficient to compensate for the rise in the costs of supplies, it may have an adverse effect on profitability. In order to control inflation in the past, the PRC government has imposed controls on bank credits, limits on loans for fixed assets and restrictions on state bank lending. Such an austere policy can lead to a slowing of economic growth. In October 2004, the People's Bank of China, the PRC's central bank, raised interest rates for the first time in nearly a decade and indicated in a statement that the measure was prompted by inflationary concerns in the PRC economy. Repeated rises in interest rates by the central bank would likely slow economic activity in the PRC which could, in turn, materially increase our costs and also reduce demand for our products.

19

A widespread health problem in the PRC could negatively affect our operations

A renewed outbreak of SARS or another widespread public health problem in the PRC, such as bird flu, where a major portion of the Company's revenue is derived, could have an adverse effect on our operations. Our operations may be impacted by a number of health-related factors, including quarantines or closures of some offices that would adversely disrupt our operations. Any of the foregoing events or other unforeseen consequences of public health problems could adversely affect our operations.

Enforcement against us or our directors and officers may be difficult

Because our principal assets are located outside of the U.S. and almost all our directors and officers reside outside of the U.S., it may be difficult for you to enforce your rights based on U.S. Federal securities laws against us and our officers and some directors or to enforce a U.S. court judgment against us or them in the PRC.

In addition, our operating subsidiary is located in the PRC and substantially all of its assets are located outside of the U.S. It may therefore be difficult for investors in the U.S. to enforce their legal rights based on the civil liability provisions of the U.S. Federal securities laws against us in the courts of either the U.S. or the PRC and, even if civil judgments are obtained in U.S. courts, to enforce such judgments in PRC courts. Further, it is unclear if extradition treaties now in effect between the U.S. and the PRC would permit effective enforcement against us or our officers and directors of criminal penalties under the U.S. Federal securities laws or otherwise.

We may have difficulty establishing adequate management, legal and financial controls in the PRC.

The PRC historically has not adopted a western style of management and financial reporting concepts and practices, as well as in modern banking, computer and other control systems. We may have difficulty in hiring and retaining a sufficient number of qualified employees to work in the PRC. As a result of these factors, we may experience difficulty in establishing management, legal and financial controls, collecting financial data and preparing financial statements, books of account and corporate records and instituting business practices that meet Western standards.

Inadequate funding for our capital expenditure may affect our growth and profitability

Our sales revenues have increased from $19,999,826, for the fiscal year ended June 30, 2004 to $36,029,179 for the fiscal year ended June 30, 2006. Our continued growth is dependent upon our ability to raise capital from outside sources. Our ability to obtain financing will depend upon a number of factors, including:

| · | our financial condition and results of operations; |

20

| · | the condition of the PRC economy and the healthcare sector in the PRC; |

| · | conditions in relevant financial markets; and |

| · | relevant PRC laws regulating the same. |

If we are unable to obtain financing, as needed, on a timely basis and on acceptable terms to our investors or lenders, our financial position, competitive position, growth and profitability may be adversely affected.

We may not be able to effectively control and manage our growth.

If our business and markets grow and develop, it will be necessary for us to finance and manage expansion in an orderly fashion. We may not have the requisite experience to manage and operate a larger, more modern cornstarch manufacturing plant and a bigger glucose production line. In addition, we may face challenges in managing expanding product offerings and in integrating acquired businesses with our own. These events would increase demands on our existing management, workforce and facilities. Failure to satisfy these increased demands could interrupt or adversely affect our operations and cause production backlogs, longer product development time frames and administrative inefficiencies.

Significant fluctuations in raw material prices may have a material adverse effect on us

We do not have any long-term supply contracts with our raw materials suppliers. Any significant fluctuation in price of our raw materials could have a material adverse effect on the manufacturing cost of our products. We are subject to market conditions and although raw materials are generally available and we have not experienced any raw material shortage in the past, we cannot assure you that the necessary materials will continue to be available to us at prices currently in effect or acceptable to us.

We may have limited options in the short-term for alternative supply if our suppliers fail for any reason, including their business failure or financial difficulties, to continue the supply of raw materials. Moreover, identifying and accessing alternative sources may increase our costs.

Although we are in the corn-producing region in the Shandong province, there is no guarantee that we will not face a shortage of corn because of some natural calamity or other reason.

We have also mitigated the risks of a shortage in cornstarch by managing a cornstarch-producing company, Shouguang Shengtai Starch Company, and implemented a vertical integration manufacturing program, which includes building our own cornstarch processing plant, which plant is now operational. This will not only lower production costs and improve profit margins, it will also allow Weifang Shengtai to produce higher quality, lower-cost cornstarch. We cannot guarantee these measures will be effective in eradicating all risks attendant to the supply of raw materials. In the event our cost of materials is increased, we may have to raise prices of our products, making us less competitive price-wise.

21

We may not be able to adjust our product prices, especially in the short-term, to recover the costs of any increases in raw materials. Our future profitability may be adversely affected to the extent we are unable to pass on higher raw material costs to our customers.

We may be exposed to intellectual property infringement and other claims by third parties, which, if successful, could cause us to pay significant damage awards and incur other costs.

Our success also depends in large part on our ability to use and develop our technology and know-how without infringing the intellectual property rights of third parties. We believe that the technology we use is not protected by any patent or intellectual property rights. As litigation becomes more common in the PRC in resolving commercial disputes, we face a higher risk of being the subject of intellectual property infringement claims. The validity and scope of claims relating to the manufacturing of pharmaceutical grade products and cornstarch involve complex technical, legal and factual questions and analysis and, therefore, may be highly uncertain. The defense and prosecution of intellectual property suits, patent opposition proceedings and related legal and administrative proceedings can be both costly and time consuming and may significantly divert the efforts and resources of our technical and management personnel. An adverse determination in any such litigation or proceedings to which we may become a party could subject us to significant liability, including damage awards, to third parties, require us to seek licenses from third parties, to pay ongoing royalties, or to redesign our products or subject us to injunctions preventing the manufacture and sale of our products. Protracted litigation could also result in our customers or potential customers deferring or limiting their purchase or use of our products until resolution of such litigation. Further, we do not have adequate product liability insurance coverage against defective products as our products are manufactured according to fairly basic formulas. Any disputes so far have been resolved through friendly negotiations. There is no guarantee that we will not be involved in any legal proceedings should such negotiations fail one day.

Potential environmental liability could have a material adverse effect on our operations and financial condition.

To the knowledge of management, neither the production nor the sale of our products constitute activities, or generate materials in a material manner, that requires our operation to comply with the PRC environmental laws. Although it has not been alleged by PRC government officials that we have violated any current environmental regulations, we cannot assure you that the PRC government will not amend the current PRC environmental protection laws and regulations. Our business and operating results may be materially and adversely affected if we were to be held liable for violating existing environmental regulations or if we were to increase expenditures to comply with environmental regulations affecting our operations.

We rely on Mr. Qingtai Liu, our Chief Executive Officer and President, for the management of our business, and the loss of his services may significantly harm our business and prospects.

We depend, to a large extent, on the abilities and participation of our current management team, but have a particular reliance upon Mr. Qingtai Liu, our Chief Executive Officer and President for the direction of our business. The loss of the services of Mr. Liu, for any reason, may have a material adverse effect on our business and prospects. We cannot assure you that the services of Mr. Liu will continue to be available to us, or that we will be able to find a suitable replacement for Mr. Liu. We have not entered into an employment contract with Mr. Liu. We do not have key man insurance on Mr. Qingtai Liu. If Mr. Liu dies and we are unable to replace Mr. Liu for a prolonged period of time, we may be unable to carry out our long term business plan and our future prospect for growth, and our business, may be harmed.

22

We may not be able to hire and retain qualified personnel to support our growth and if we are unable to retain or hire such personnel in the future, our ability to improve our products and implement our business objectives could be adversely affected.

Our future success depends heavily upon the continuing services of the members of our senior management team, in particular our Chief Executive Officer and President, Mr. Qingtai Liu. If one or more of our senior executives or other key personnel is/are unable or unwilling to continue in his/her/their present positions, we may not be able to replace them easily or at all, and our business may be disrupted and our financial condition and results of operations may be materially and adversely affected. Competition for senior management and personnel is intense, the pool of qualified candidates is very limited, and we may not be able to retain the services of our senior executives or senior personnel, or attract and retain high-quality senior executives or senior personnel in the future. This failure could materially and adversely affect our future growth and financial condition.

We may not have adequate internal accounting controls. While we have certain internal procedures in our budgeting, forecasting and in the management and allocation of funds, our internal controls may not be adequate.

We are constantly striving to improve our internal accounting controls. With the appointment of our new Chief Financial Officer, Mr. Yizhao Zhang, we hope to develop an adequate internal accounting control to budget, forecast, manage and allocate our funds and account for them. There is no guarantee that such improvements will be adequate or successful or that such improvements will be carried out on a timely basis. If we do not have adequate internal accounting controls, we may not be able to appropriately budget, forecast and manage our funds, we may also be unable to prepare accurate accounts on a timely basis to meet our continuing financial reporting obligations and we may not be able to satisfy our obligations under US securities laws.

Standards for compliance with Section 404 of the Sarbanes-Oxley Act Of 2002 are uncertain, and if we fail to comply in a timely manner, our business could be harmed and our stock price could decline.

Rules adopted by the SEC pursuant to Section 404 of the Sarbanes-Oxley Act of 2002 require annual assessment of our internal control over financial reporting, and attestation of this assessment by our company's independent registered public accountants. The SEC extended the compliance dates for non-accelerated filers, as defined by the SEC. Accordingly, we believe that the annual assessment of our internal controls requirement will first apply to our annual report for the 2007 fiscal year and the attestation requirement of management's assessment by our independent registered public accountants will first apply to our annual report for the 2008 fiscal year. The standards that must be met for management to assess the internal control over financial reporting as effective are new and complex, and require significant documentation, testing and possible remediation to meet the detailed standards. We may encounter problems or delays in completing activities necessary to make an assessment of our internal control over financial reporting. In addition, the attestation process by our independent registered public accountants is new and we may encounter problems or delays in completing the implementation of any requested improvements and receiving an attestation of our assessment by our independent registered public accountants. If we cannot assess our internal control over financial reporting as effective, or our independent registered public accountants are unable to provide an unqualified attestation report on such assessment, investor confidence and share value may be negatively impacted.

23

We have inadequate insurance coverage

We do not presently maintain product liability insurance, and our property and equipment insurance does not cover the full value of our property and equipment, which leaves us with exposure in the event of loss or damage to our properties or claims filed against us.

We currently do not carry any product liability or other similar insurance. We cannot assure you that we would not face liability in the event of the failure of any of our products. This is particularly true given our plan to significantly expand our sales into international markets, like the United States, where product liability claims are more prevalent.

Except for property and automobile insurance, we do not have other insurance such as business liability or disruption insurance coverage for our operations in the PRC.

We do not maintain a reserve fund for warranty or defective products claims. Our costs could substantially increase if we experience a significant number of warranty claims. We have not established any reserve funds for potential warranty claims since historically we have experienced few warranty claims for our products so that the costs associated with our warranty claims have been low. If we experience an increase in warranty claims or if our repair and replacement costs associated with warranty claims increase significantly, it would have a material adverse effect on our financial condition and results of operations.

Rule 415

WE MAY NOT BE ABLE TO REGISTER ALL OF THE SHARES (AND THE SHARES UNDERLYING THE ATTACHED WARRANTS) PURCHASED UNDER THE SHARE PURCHASE AGREEMENT ENTERED INTO IN MAY 2007. THIS MAY REQUIRE US TO PAY THE INVESTORS LIQUIDATED DAMAGES AS SET FORTH THEREIN.

Reference is made to “Selling Stockholders - Background” in this prospectus for disclosure relating to our obligation to register the shares (and the shares underlying the warrants) set forth in share purchase agreement and the circumstances in which we may be required to pay liquidated damages for failing to comply with our obligations set forth therein.

Risks related to an investment in our common stock

Our Chief Executive Officer and President controls us through his position and stock ownership and his interests may differ from other stockholders

Our Chief Executive Officer and President, Mr. Qingtai Liu, beneficially owns approximately 41.15% of our common stock. As a result, although Mr. Liu is not the holder of a majority of the outstanding shares, Mr. Liu may be able to influence the outcome of stockholder votes on various matters, including the election of directors and extraordinary corporate transactions, including business combinations. Mr. Liu's interests may differ from other stockholders.

24

We do not intend to pay cash dividends in the foreseeable future

We currently intend to retain all future earnings for use in the operation and expansion of our business. We do not intend to pay any cash dividends in the foreseeable future but will review this policy as circumstances dictate. Should we decide in the future to do so, as a holding company, our ability to pay dividends and meet other obligations depends upon the receipt of dividends or other payments from our operating subsidiary based in the PRC, Weifang Shengtai. Our operating subsidiary, from time to time, may be subject to restrictions on its ability to make distributions to us, including as a result of restrictions on the conversion of local currency into U.S. dollars or other hard currency and other regulatory restrictions. See “Risks related to doing business in the People’s Republic of China”.

There is currently a very limited trading market for our common stock

Our common stock has been quoted on the over-the-counter Bulletin Board since January 2007. Because we were formerly a shell company, our bid and ask quotations have not regularly appeared on the OTC Bulletin Board for any consistent period of time. There is a limited trading market for our common stock and our common stock may never be included for trading on any stock exchange or through any other quotation system, including, without limitation, the NASDAQ Stock Market. You may not be able to sell your shares due to the absence of an established trading market.

Our common stock is subject to the Penny Stock Regulations

Our common stock is, and will continue to be subject to the SEC's "penny stock" rules to the extent that the price remains less than $5.00. Those rules, which require delivery of a schedule explaining the penny stock market and the associated risks before any sale, may further limit your ability to sell your shares.

The SEC has adopted regulations which generally define "penny stock" to be an equity security that has a market price of less than $5.00 per share. Our common stock, when and if a trading market develops, may fall within the definition of penny stock and subject to rules that impose additional sales practice requirements on broker-dealers who sell such securities to persons other than established customers and accredited investors (generally those with assets in excess of $1,000,000, or annual incomes exceeding $200,000 or $300,000, together with their spouse).

For transactions covered by these rules, the broker-dealer must make a special suitability determination for the purchase of such securities and have received the purchaser's prior written consent to the transaction. Additionally, for any transaction, other than exempt transactions, involving a penny stock, the rules require the delivery, prior to the transaction, of a risk disclosure document mandated by the Commission relating to the penny stock market. The broker-dealer also must disclose the commissions payable to both the broker-dealer and the registered representative, current quotations for the securities and, if the broker-dealer is the sole market-maker, the broker-dealer must disclose this fact and the broker-dealer's presumed control over the market. Finally, monthly statements must be sent disclosing recent price information for the penny stock held in the account and information on the limited market in penny stocks. Consequently, the "penny stock" rules may restrict the ability of broker-dealers to sell our common stock and may affect the ability of investors to sell their common stock in the secondary market.

25

Our common stock is illiquid and subject to price volatility unrelated to our operations

The market price of our common stock could fluctuate substantially due to a variety of factors, including market perception of our ability to achieve our planned growth, quarterly operating results of other companies in the same industry, trading volume in our common stock, changes in general conditions in the economy and the financial markets or other developments affecting our competitors or us. In addition, the stock market is subject to extreme price and volume fluctuations. This volatility has had a significant effect on the market price of securities issued by many companies for reasons unrelated to their operating performance and could have the same effect on our common stock.

A large number of shares of common stock will be issuable for future sale which will dilute the ownership percentage of our current holders of common stock. Under the terms of the share purchase agreement entered into on May 15, 2007 we are required to register for public resale 8,750,000 shares (as well as 4,375,000 shares issuable on exercise of the attached warrants) and the availability for public resale of those shares may depress our stock price.

Also as a result, there will be a significant number of new shares of common stock on the market in addition to the current public float. Sales of substantial amounts of common stock, or the perception that such sales could occur, and the existence of warrants to purchase shares of common stock at prices that may be below the then current market price of the common stock, could adversely affect the market price of our common stock and could impair our ability to raise capital through the sale of our equity securities.

USE OF PROCEEDS

We will not receive any of the proceeds from any sales of the shares offered for sale and sold under this prospectus by the Selling Stockholders. We will receive proceeds from the issuance of shares of our common stock on the exercise, if any, of the 4,375,000 warrants issued to the Selling Stockholders in connection with our private placement completed on May 15, 2007. The warrants expire on May 15, 2012 and are exercisable at $2.60 per share, as adjusted. If all of these outstanding warrants are exercised for cash, we would receive aggregate net proceeds of approximately $11,375,000. The terms of the warrants do not provide for cashless exercise. We intend to use the net proceeds from the exercise of warrants, if any, for working capital and other general corporate purposes. We cannot assure you that any of the warrants will ever be exercised for cash, if at all.

26

The following selected consolidated statement of operations data contains consolidated statement of operations data for the nine months ended March 31, 2007 and 2006 (unaudited) and each of the years in the five-year period ended June 30, 2006 and the consolidated balance sheet data as of March 31, 2007 and 2006 (unaudited) and year-end for each of the years in the five-year period ended June 30, 2006. The consolidated statement of operations data and balance sheet data were derived from the audited consolidated financial statements, except for data for the periods ended and as of March 31, 2007 and 2006 and the fiscal years ended June 30, 2002 and June 30, 2003 which are unaudited. Such financial data should be read in conjunction with the consolidated financial statements and the notes to the consolidated financial statements starting on page F-1 and with “Management’s Discussion and Analysis of Financial Condition and Results of Operations.”

Nine Months Ended March 31, | Year Ended June 30, | |||||||||||||||||||||

Consolidated Statements of Operations | 2006 | 2007 | 2002 | 2003 | 2004 | 2005 | 2006 | |||||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (unaudited) | (audited) | (audited) | (audited) | ||||||||||||||||

| Sales revenue | $ | 25,714,509 | $ | 35,472,898 | $ | 14,407,510 | $ | 10,493,234 | $ | 19,999,826 | $ | 24,860,399 | $ | 36,029,179 | ||||||||

| Cost of good sold | (19,900,781 | ) | (26,694,321 | ) | (12,409,927 | ) | (8,666,872 | ) | (16,487,240 | ) | (19,557,743 | ) | (27,568,092 | ) | ||||||||

| Gross profit | $ | 5,813,728 | $ | 8,778,577 | 1,997,583 | 1,826,362 | $ | $3,512,586 | $ | 5,302,656 | $ | 8,461,087 | ||||||||||

| Selling, general and administrative expenses | 2,820,492 | 2,989,524 | 1,398,366 | 1,868,727 | 2,474,813 | 3,242,330 | 3,831,778 | |||||||||||||||

| Operating Income | $ | 2,993,236 | $ | 5,789,053 | $ | 599,217 | $ | (42,365 | ) | $ | 1,037,773 | $ | 2,060,326 | $ | 4,629,309 | |||||||

| Other net income | (372,271 | ) | (404,830 | ) | (40,492 | ) | 193,279 | (550,196 | ) | (445,169 | ) | (418,398 | ) | |||||||||

| Income before Income taxes | $ | 2,620,965 | $ | 5,384,223 | 558,725 | 150,914 | $ | $487,577 | $ | 1,615,157 | $ | 4,210,911 | ||||||||||

| Provision for Income Taxes | $ | - | $ | (518,128 | ) | (184,379 | ) | (49,463 | ) | - | - | - | ||||||||||

| Net income | 2,620,965 | $ | 4,866,095 | $ | 374,346 | $ | 101,451 | $ | 487,577 | $ | 1,615,157 | $ | 4,210,911 | |||||||||

| Foreign Currency Translation Adjustment | $ | 154,589 | $ | 377,729 | ||||||||||||||||||

| Comprehensive Income | 2,755,554 | 5,243,824 | ||||||||||||||||||||

| Basic and diluted net income per common share | $ | 0.14 | 0.26 | 0.03 | 0.09 | 0.22 | ||||||||||||||||

| Basic weighted average common shares outstanding | 18,875,000 | 18,875,000 | 18,875,000 | 18,875,000 | 18,875,000 | |||||||||||||||||

| Diluted weighted average common shares outstanding | 18,875,000 | 18,875,000 | 18,875,000 | 18,875,000 | 18,875,000 | |||||||||||||||||

As of March 31, | Year Ended June 30, | ||||||||||||||||||

Consolidated Balance Sheets | 2007 | 2002 | 2003 | 2004 | 2005 | 2006 | |||||||||||||

| (unaudited) | (unaudited) | (unaudited) | (audited) | (audited) | (audited) | ||||||||||||||

| Current Assets | $ | 18,175,670 | $ | 3,372,924 | $ | 5,076,919 | $ | 7,900,644 | $ | 11,981,783 | $ | 12,149,634 | |||||||

| Total Assets | 50,328,161 | 7,389,886 | 11,787,828 | 17,644,345 | 23,672,498 | 31,271,457 | |||||||||||||

| Current Liabilities | 37,841,793 | 6,710,902 | 8,597,754 | 14,447,904 | 19,564,316 | 23,612,427 | |||||||||||||

| Total Liabilities | 38,426,907 | 6,710,902 | 11,007,393 | 16,141,904 | 20,411,316 | 24,614,027 | |||||||||||||

| Total Stockholders’ Equity | 11,901,254 | 678,984 | 780,455 | 1,502,441 | 3,261,182 | 6,657,430 | |||||||||||||

27

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Overview

We are, through our subsidiaries, SHI and Weifang Shengtai, engaged in the manufacture and supply of pharmaceutical grade glucose used for medical purposes, as well as glucose and starch products for the food and beverage industry and for industrial production primarily in the PRC.

Dextrose, a form of glucose is one of the most important carbohydrates and is the chief source of energy in the human body. As such it is used in a wide array of pharmaceutical products such as transfusions and intravenous drips.

In addition to our pharmaceutical glucose series of products, we also produce other medicinal product lines and glucose and starch products such as industrial glucose, syrup, starch, avermectins, dextrin, maltose and maltitol, which are used for food, beverage and industrial production.

Result of Operations

The following table shows the operating results for the nine months ended March 31, 2007 the nine months ended March 31, 2006.

Nine Months ended March 31, 2006 | Nine Months ended March 31, 2007 | ||||||

| Sales revenue | 25,714,509 | 35,472,898 | |||||

| Cost of goods sold | 19,900,781 | 26,694,321 | |||||

| Gross profit | 5,813,728 | 8,778,577 | |||||

| Selling,General and Administrative expenses | 2,820,492 | 2,989,524 | |||||

| Operating income | 2,993,236 | 5,789,053 | |||||

| Other net income | (372,271 | ) | (404,830 | ) | |||

| Income before Income Taxes | 2,620,965 | 5,384,223 | |||||

| Provision for Income Taxes | - | 518,128 | |||||

| Net income | 2,620,965 | 4,866,095 | |||||