FBR Capital Markets Fall Investor Conference December 3, 2008 * * * * * * * ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* ********* Exhibit 99.1 |

1 Forward Looking Statements Safe Harbor Statement under the Private Securities Litigation Reform Act of 1995: Statements in this presentation regarding The Bancorp, Inc.’s business which are not historical facts are "forward-looking statements" that involve risks and uncertainties. These statements may be identified by the use of forward-looking terminology, including the words “may,” “believe,” “will,” “expect,” “anticipate,” “estimate,” “continue,” or similar words. For further discussion of these risks and uncertainties, see The Bancorp, Inc.’s filings with the SEC, including the “risk factors” section of The Bancorp Inc.’s Annual Report on Form10-K for the year ended December 31, 2007. These risks and uncertainties could cause actual results to differ materially from those projected in the forward-looking statements. The Bancorp, Inc. does not undertake to publicly revise or update forward-looking statements in this presentation to reflect events or circumstances that arise after the date of this presentation, except as may be required under applicable law. ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ******************** |

2 The Bancorp, Inc. - Overview An FDIC-insured commercial bank with a branchless deposit strategy that delivers a full array of commercial and consumer banking services both locally and nationally through private label banking products – Experienced senior management team with significant inside ownership – 300 Employees in 8 Offices – Highly scalable, national in scope, private label banking business focused on four lines of business where we have achieved market leadership position by providing sponsorship, integrated payment solutions, and banking services to firms outsized in comparison to us Health Care Wealth Management Merchant Processing Prepaid Issuing – Target market for commercial lending is the greater Philadelphia-Wilmington metropolitan area Consists of the 12 counties surrounding Philadelphia and Wilmington including Philadelphia, Delaware, Chester, Montgomery, Bucks and Lehigh Counties in Pennsylvania, New Castle County in Delaware and Mercer, Burlington, Camden, Ocean and Cape May Counties in New Jersey The Bancorp, Inc. is a Delaware corporation with a wholly owned subsidiary, The Bancorp Bank. |

3 Senior Management Highly experienced senior management team with an aggregate of over 140 years of experience providing middle market banking services – Management has a significant history together as most are former executives of a prior bank which was sold in November 1999 Inside ownership over 20.04% (fully diluted) Senior management has a significant ownership stake in the company Betsy Z. Cohen Chairman & Chief Executive Officer Frank M. Mastrangelo President & Chief Operating Officer (The Bancorp, Inc.) Martin F. Egan Senior Vice President & Chief Financial Officer Donald F. McGraw, Jr Executive Vice President & Chief Credit Officer Arthur M. Birenbaum Executive Vice President, Commercial Lending Scott R. Megargee Executive Vice President, Consumer Lending Peter Chiccino Chief Information Officer (The Bancorp Bank) Jeremy Kuiper Managing Director (Stored Value Solutions) |

4 Growth Engine DEPOSITS Private Label Banking: Capture stable, low-cost core deposits – Health Care – HSA / FSA / HRA – Merchant Processing – Prepaid Card Issuing – Asset Managers – DTC Eligible / ERISA Qualified account (MDA) – Safeharbor IRA Rollovers Generate low-cost core deposits through personal and business checking and savings accounts through the community bank – Check 21 / Remote Deposit Capture 1. For the quarter ended September 30, 2008 Net Interest Margin of 3.28% INCOME Non-Interest Income: Merchant Processing & Debit Issuing Fees LOANS Originates high-credit quality, well collateralized loans to local businesses and individuals – Commercial lending, commercial & residential real estate, construction lending Automobile Fleet Leasing Private Label Banking (National) – Asset Managers – generate consumer loans, HELOC’s, installment loans and securities backed loans ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* ********************* * 1 |

5 Growth Engine: Lines of Business: Deposits “Private-Label” Banking – Provider of private label banking services for non-bank businesses – Access large customer groups at low acquisition costs – Private label partners derive from our four main sources: Open-loop private label debit cards (prepaid cards) – Generated over $475 million in deposits as of 9/30/08 – 3rd largest open-loop debit issuer in the U.S. Western Union, IDT, H&R Block, Higher One – Largest agent bank gift card issuer in the U.S. Deluxe, Digital Insight – Extremely scalable operation - over 15 million active cards – Industry is expected to grow at a compound annual growth rate of over 32% between 2005 and 2009 Health Care – Scalable deposit gathering channel via HSA, HRA, and FSA accounts – Represents over $178 million in deposits as of 9/30/08 – 2nd largest FSA issuing portfolio in U.S. with over 1.8 million cards issued – 6 largest HSA custodian in U.S. with over 123,000 accounts – Currently 26 partners covering over 22 million insured lives Independence Blue Cross; Blue Cross Blue Shield of Louisiana , Wage Works, Evolution Benefits The Bancorp, Inc. employs a multi-channel growth strategy th |

6 Growth Engine: Lines of Business: Deposits Private Client – Deposit and asset gathering channel – Currently have 24 partners representing approximately $110 billion of assets under management Over 7,000 investment advisors serving more than 280,000 clients SEI Investments, Legg Mason – Master Demand Account (MDA) - DTC Registered / ERISA Qualified bank deposit account Trades on the DTC & NSCC like Money Market Mutual Fund FDIC insurance passed through to 401(k) participant Schwab, Matrix, Sunguard – Safeharbor IRA Rollovers Rollover Systems, WMSI Merchant Processing – Deposit gathering and non-interest income channel – 26 largest bank acquiring portfolio through 6/30/2008 – Annualized processing volume in excess of $5 billion – 3 party ACH originators, ISO Network (Independent Service Organizations) BillMatrix; BankServ, Cash Systems, TSYS, Planet Payments – Over 300 private label partners Remote Deposit Capture – Market leader in the industry Distributed over 300 scanners Processed over 170,000 transactions representing in excess of $600 million in deposits in 2008 The Bancorp, Inc. employs a multi-channel growth strategy th rd |

7 Deposits The Bancorp has leveraged its private label partnerships to grow core deposits Note: as of 9/30/08 |

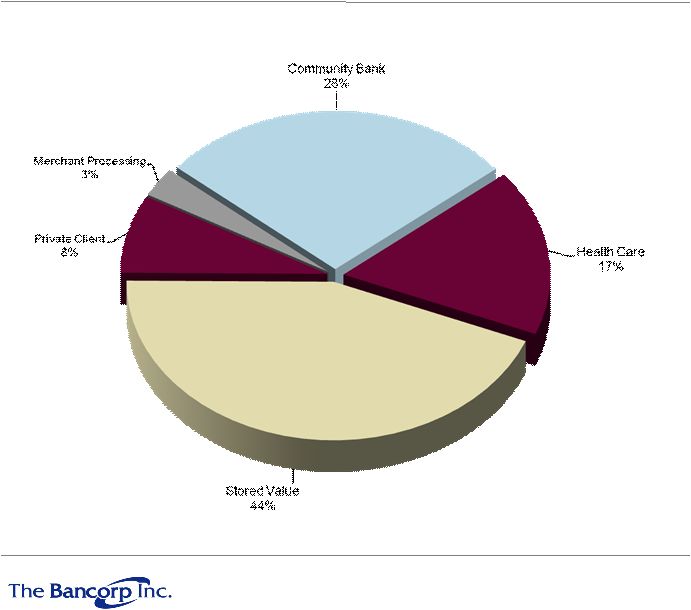

8 Deposits: Core By Lines of Business The Bancorp has leveraged its private label partnerships to grow core deposits Note: as of 9/30/08 |

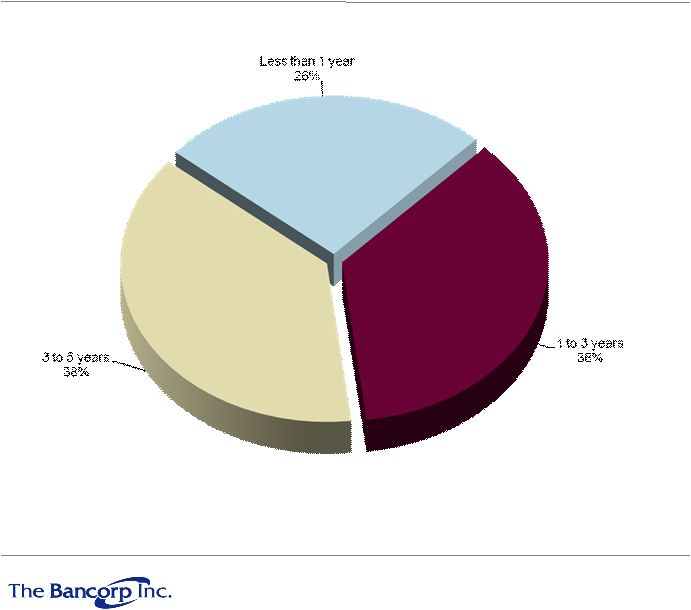

9 Deposits: Private Label Deposits by Remaining Contractual Term The Bancorp has long term (in many cases exclusive) agreements in place with its private label banking partners. 90% of agreements contain provisions to automatically renew at maturity. Note: as of 9/30/08 |

10 Growth Engine: Lines of Business: Loans Community Bank Offers traditional community banking products and services Leverages the business relationships developed during management team’s tenure in banking Targets highly fragmented Philadelphia-Wilmington banking market Leasing Portfolio – Automobile Fleet Leasing Portfolio Eastern Corridor Average Transaction – 8-15 automobiles – $350,000 Acquired Mears Leasing in January 2005 Private Client – Deposit and asset gathering channel – Currently have 24 partners representing approximately $110 billion of assets under management SEI Investments, Legg Mason – Generates consumer loans, HELOC’s, installment loans, and securities backed loans – Represents approximately 8% of loan portfolio at 09/30/08 The Bancorp, Inc. employs a multi-channel growth strategy |

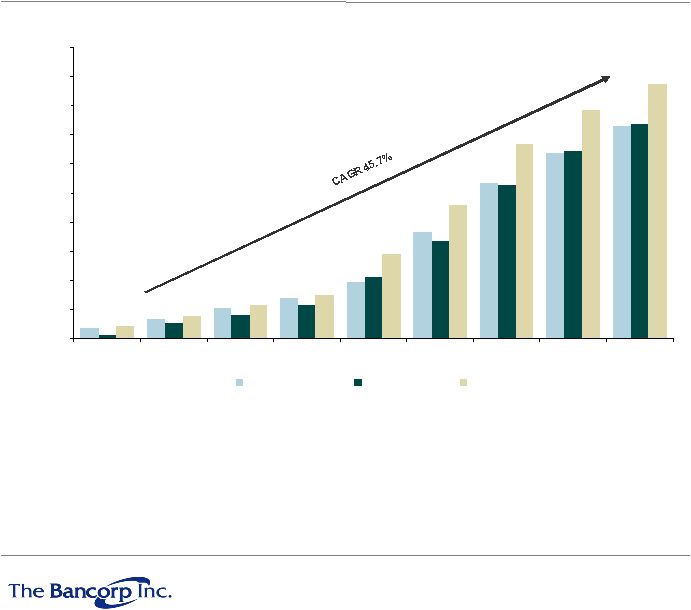

11 Loan Portfolio Growth Since 2000, The Bancorp has grown total loans at a compound annual growth rate of approximately 64% Proven track record at originating high quality community bank loans – Loan/deposit ratio currently stands at above 100% – NPA/Assets: 0.78% 2000 2001 2002 2003 2004 2005 2006 2007 Commercial 4,172 $ 30,250 $ 36,037 $ 53,130 $ 89,327 $ 119,654 $ 199,397 $ 325,166 $ Commercial Mortgage 1,149 37,939 71,016 89,772 140,755 190,153 327,639 369,124 Construction 318 4,441 9,400 29,026 97,239 168,149 275,079 307,614 Direct Financing Leases, net 20,352 25,405 30,958 38,405 44,795 81,162 92,947 89,519 Residential Mortgage 817 3,228 4,433 6,473 31,388 62,378 62,413 50,193 Consumer Loans and Other 1,149 4,336 10,815 14,989 24,894 61,017 108,374 144,882 Total Loans 27,957 $ 105,599 $ 162,659 $ 231,795 $ 428,398 $ 682,513 $ 1,065,849 $ 1,286,498 $ Supplemental loan data (1): 31-Dec-07 30-Sep-08 Construction 1-4 family $167,485 $158,310 Construction commercial, acquisition and development 140,129 173,781 $307,614 $332,091 (1) Prior to December 31, 2007 Construction loans were reported as a single line item. Note: as of 9/30/08 |

12 Credit Performance Nine months ended September 30, December 31, 2008 2007 2006 2005 2004 2003 (dollars in thousands) Balance in the allowance for loan and lease losses at beginning of period $ 10,233 $ 8,400 $ 5,513 $ 3,593 $ 1,991 $ 1,379 Loans charged-off: Commercial 734 2,545 8 123 10 - Lease financing 46 35 93 70 - 65 Construction 2,744 1,084 - - - - Consumer 9 8 - 2 20 9 Residential mortgage 192 - - - - - Total 3,725 3,672 101 195 30 74 Recoveries: Commercial 151 73 12 15 - 1 Lease financing 5 8 - - - - Construction - 10 - - - - Consumer 4 14 1 - - - Residential mortgage - - - - - - Total 160 105 13 15 - 1 Net charge-offs (recoveries) 3,565 3,567 88 180 30 73 Provision charged to operations 8,800 5,400 2,975 2,100 1,632 685 Balance in allowance for loan and lease losses at end of period $ 15,468 $ 10,233 $ 8,400 $ 5,513 $ 3,593 $ 1,991 Net charge-offs/average loans 0.26% 0.30% 0.01% 0.03% 0.01% 0.04% |

13 Acquisitions The Bancorp has utilized acquisitions to augment its organic growth strategy Stored Value Solutions Business Acquisition Mears Motor Livery Corp Acquisition Deal Overview Deal Overview Target Stored Value Solutions Business Target Mears Motor Livery Corp Seller Marshall Bankfirst Corporation Seller Investor Group Deal Type Financial Technology Company Deal Type Specialty Finance Company Announcement Date Announcement Date Announced Deal Value ($MM) 60.6 $ Announced Deal Value ($MM) 5.0 $ Status Completed Status Completed Completion Date Completion Date Deal Summary Deal Summary Consideration Breakout Consideration Breakout Cash ($MM) 48.5 $ Cash ($MM) 1.0 $ Common Stock ($MM) 12.1 $ Common Stock ($MM) 4.0 $ Common Stock Issued (shares) 722,733 Common Stock Issued (shares) 253,126 12/31/2004 1/3/2005 Wilmington, Del.-based Bancorp Inc. has acquired the Stored Value Solutions business of Minneapolis-based Marshall Bankfirst Corp. unit Sioux Falls, S.D.-based BankFirst. Stored Value Solutions provides customized and secure program development and issuing services to national stored value card program managers. Wilmington, Del.-based Bancorp Inc. has acquired Orlando, FL- based Mears Motor Livery Corporation from James C. Hartman and Arrow Holdings. Mears is an automobile leasing business. 7/13/2007 11/30/2007 |

14 Selected Financial Information For the three months ended For the year ended December 31, Operating Ratios 9/30/2008 2007 2006 2005 2004 2003 Return on average assets 0.06% 1.04% 1.19% 1.02% 0.79% 0.41% Return on average equity 0.92% 9.15% 8.90% 5.69% 3.94% 4.93% Net interest margin 3.28% 3.90% 4.32% 4.57% 3.86% 3.77% Efficiency ratio 72.20% 51.76% 51.72% 58.94% 80.78% 93.14% Book value per share $ 11.78 $ 12.01 $ 10.76 $ 9.80 $ 9.32 $ 6.43 Shareholders' equity (millions) $ 172.80 $ 176.30 $ 148.90 $ 134.90 $ 121.40 $ 21.70 |

15 Balance Sheet Growth Since 2000, The Bancorp has grown total assets at a compound annual growth rate of approximately 46% 86,166 1,750,495 $0 $200,000 $400,000 $600,000 $800,000 $1,000,000 $1,200,000 $1,400,000 $1,600,000 $1,800,000 $2,000,000 2000 2001 2002 2003 2004 2005 2006 2007 9/30/2008 Deposits Loans Assets |

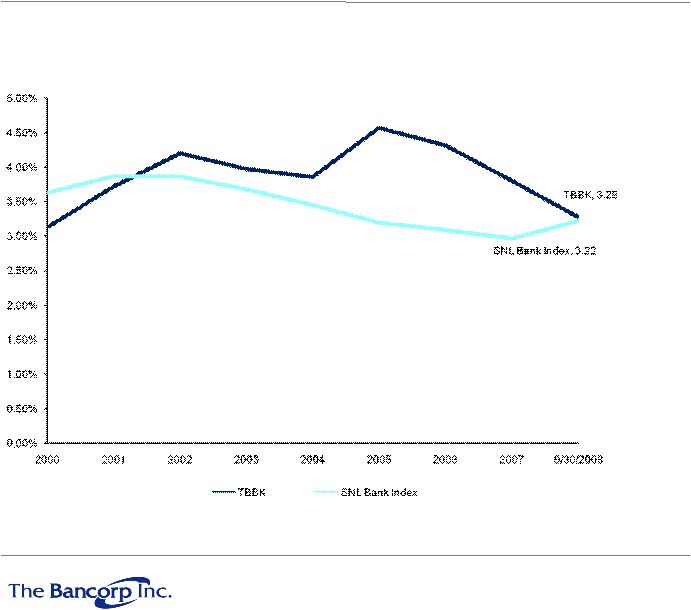

16 Net Interest Margin Strong loan growth coupled with the ability to leverage deposit relationships has translated into TBBK’s net interest margin |

17 Balance Sheet Unaudited company financial statements September 30, 2008 December 31, (unaudited) 2007 ASSETS 77,233 $ 21,121 $ 2,566 20,254 36,485 40,783 Total cash and cash equivalents 116,284 82,158 85,659 122,215 30,447 - 1,469,615 1,286,789 (15,468) (10,233) 1,454,147 1,276,556 7,009 6,660 7,539 9,686 50,135 50,173 11,256 12,006 18,466 8,928 Total assets 1,750,495 $ 1,568,382 $ LIABILITIES 451,652 $ 242,164 $ 618,293 622,090 361,561 390,684 27,623 23,380 Total deposits 1,459,129 1,278,318 3,249 3,846 100,000 90,000 Long term borrowings 28,250 - Subordinated debenture 13,401 13,401 2,796 4,865 1,353 1,693 Total liabilities 1,608,178 1,392,123 par value; issued and outstanding, 108,136 and 111,585 shares for September 30, 2008 and December 31, 2007, respectively value; issued and outstanding shares 14,563,919 and 14,560,470 for September 30, 2008 and December 31, 2007 , respectively 138,876 138,808 23,871 25,106 (4,547) (2,216) Total shareholders' equity 172,764 176,259 Total liabilities and shareholders' equity 1,780,942 $ 1,568,382 $ Investment securities, Held-to-maturity 14,563 14,560 Loans, net Intangible assets Premises and equipment, net Accrued interest receivable Goodwill Other liabilities SHAREHOLDERS' EQUITY Accrued interest payable Other assets Deposits Time deposits Demand (non-interest bearing) Savings, money market and interest checking Cash and due from banks Interest bearing deposits Federal funds sold Cash and cash equivalents (in thousands) Investment securities, available-for-sale Loans, net of deferred loan costs Allowance for loan and lease losses Accumulated other comprehensive loss Securities sold under agreements to repurchase Short term borrowings Time deposits, $100,000 and over Common stock - authorized, 20,000,000 shares of $1.00 par Retained earnings Additional paid-in capital Preferred stock -authorized 5,000,000 shares of $0.01 1 1 ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* ******************* * |

18 Current Initiatives For Future Growth Asset/Liability Generation – Affinity Group Relationships Continue to leverage the economies of scale of internally developed systems to provide banking products through affinity relationships – Stored Value Solutions Acquisition Capitalize on the non-interest income and low-cost core deposits generated through the business – Community Bank Continue to generate high quality loans and deposits in the highly fragmented Philadelphia/Wilmington marketplace Operations – Leverage internally developed software to provide online and traditional banking products and services Private label banking websites – Utilize third party service providers to capitalize on technical capabilities of selected vendors Other Initiatives Gain access to additional clearing platforms to increase distribution of the Master Demand Account, the NSCC / DTC settling bank depository product sold to retirement administrators and retail brokerage firms as a cash sweep vehicle Extend and expand the Prepaid relationships by offering clients commercial banking, EFT, acquiring, and other depository services not previously offered via the channel The Bancorp made significant investments to build or acquire platforms that will generate and support future growth |

19 Summary Experienced and proven management team Attractive growth opportunities in multiple lines of business Fee income and deposit growth through affinity, merchant processing, and debit issuing relationships *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** *********************** ********************** |