Exhibit 99.2

Digital Realty Trust, Inc.

Fourth Quarter 2005

Supplemental Operating and Financial Data

December 31, 2005

This Supplemental Operating and Financial Data package is not an offer to sell or solicitation to buy securities of Digital Realty Trust, Inc. Any offers to sell or solicitation to buy securities of Digital Realty Trust, Inc. shall be made only by means of a prospectus approved for that purpose.

Table of Contents

| | | | |

| | | | | PAGE |

Corporate Data | | |

| | |

| | Corporate Information | | 3 |

| | Investor Information | | 4 |

| | Stock Performance | | 5 |

| | Ownership Structure | | 6 |

| |

Consolidated Financial Results | | |

| | |

| | Properties Acquired | | 7 |

| | Key Financial Data | | 8 |

| | Consolidated Balance Sheets | | 9 |

| | Consolidated and Combined Quarterly Statements of Operations | | 10 |

| | Funds From Operations | | 11 |

| | Adjusted Funds from Operations | | 12 |

| | Reconciliation of Earnings Before Interest, Taxes and Depreciation and Amortization | | 13 |

| | Capital Structure | | 14 |

| | Debt Summary | | 15 |

| | Debt Maturities | | 16 |

| |

Portfolio Data | | |

| | |

| | Occupancy Analysis | | 17 |

| | Major Tenants | | 18 |

| | Lease Expirations | | 19 |

| | Lease Distribution | | 20 |

| | Leasing Activity | | 21 |

| | Tenant Improvements and Leasing Commissions | | 22 |

| | Historical Capital Expenditures | | 23 |

| | Properties rename | | 24 |

| | Management Statements on Non-GAAP Supplemental Measures | | 25 |

This supplemental package contains forward-looking statements within the meaning of the federal securities laws. Such statements are based on management’s beliefs and assumptions made based on information currently available to management. Such statements are subject to risks, uncertainties and assumptions and are not guarantees of future performance and may be affected by known and unknown risks, trends, uncertainties and factors that are beyond our control. Should one or more of these risks or uncertainties materialize, or should underlying assumptions prove incorrect, actual results may vary materially from those anticipated, estimated or projected. Some of the risks and uncertainties that may cause our actual results, performance or achievements to differ materially from those expressed or implied by forward-looking statements include, among others, the following: adverse economic or real estate developments in our markets or technology related real estate; general and local economic conditions; defaults on or non-renewal of leases by tenants; increased interest rates and operating costs; our inability to manage growth effectively; our failure to obtain necessary outside financing; decreased rental rates or increased vacancy rates; difficulties in identifying properties to acquire and completing acquisitions; our failure to successfully operate acquired properties and operations; our failure to maintain our status as a REIT; possible adverse changes to tax laws; environmental uncertainties and risks related to natural disasters; financial market fluctuations; changes in foreign currency exchange rates; and changes in real estate and zoning laws and increases in real property tax rates. The risks included here are not exhaustive, and additional factors could adversely affect our business and financial performance. We discussed a number of additional material risks in our annual report on Form 10-K for the year ended December 31, 2004 and other filings with the Securities and Exchange Commission. Those risks continue to be relevant to our performance and financial condition. Moreover, we operate in a very competitive and rapidly changing environment. New risk factors emerge from time to time and it is not possible for management to predict all such risk factors, nor can it assess the impact of all such risk factors on the business or the extent to which any factor, or combination of factors, may cause actual results to differ materially from those contained in any forward-looking statements. We expressly disclaim any responsibility to update forward-looking statements, whether as a result of new information, future events or otherwise.

2

Corporate Information

Corporate Profile

Digital Realty Trust is firmly positioned at the crossroads of real estate and technology and focuses solely on the ownership of technology real estate:

| | • | | We own and operate properties that are critical to the operations of our tenants; |

| | • | | As of December 31, 2005, our portfolio is primarily located in 20 major metropolitan areas including 17 in the United States and three in Europe; |

| | • | | We concentrate on areas within the technology industry that we believe have growth potential. As such, we emphasize properties that provide the infrastructure for sectors such as corporate data centers, disaster recovery and business continuity, electronic commerce and the security of stored or transmitted electronic data. |

As of December 31, 2005, our 43 property portfolio, totaling 8.1 million square feet excluding approximately 1.1 million square feet of space held for development, consists mainly of highly improved properties containing specialized facilities that play a critical role in our tenants' operations and in the delivery of services to their customers. We maintain a significant focus on Internet gateway and data center properties that are located at the junction of major high-speed data networks that deliver Internet, data, voice, video, wireless and satellite services.

Our tenant base includes media, communications and technology-based businesses, Internet enterprises and Fortune 1000 companies. Our tenants' operations typically require specially designed and engineered facilities that maintain sophisticated security systems, robust and redundant power services, backup power systems, redundant air conditioning systems and advanced fire suppression systems.

Corporate Headquarters

| | |

| 560 Mission Street, Suite 2900 |

| San Francisco, California 94105 |

| Telephone: | | (415) 738-6500 |

| Facsimile: | | (415) 738-6501 |

| Web site: | | www.digitalrealtytrust.com |

Senior Management

| | |

| Richard A. Magnuson | | Executive Chairman |

| Michael F. Foust | | Chief Executive Officer |

| A. William Stein | | Chief Financial Officer and Chief Investment Officer |

| Scott E. Peterson | | Senior Vice President, Acquisitions |

| Christopher J. Crosby | | Senior Vice President, Sales |

Investor Relations

To request an Investor Relations package or be added to our e-mail distribution list, please contact us at:

Web site: www.digitalrealtytrust.com (Go to Information Request in the Investor Relations section)

This Supplemental Operating and Financial Data package supplements the information provided in our quarterly and annual reports filed with the Securities and Exchange Commission. Additional information about us and our properties is also available at our website www.digitalrealtytrust.com.

3

Investor Information

Analyst Coverage

| | |

| Credit Suisse | | Merrill Lynch |

| Jessica Tully | | Steve Sakwa |

| (404) 897-2820 | | (212) 449-0335 |

| |

| JMP Securities | | RBC Capital Markets |

| William Marks | | Jay Leupp |

| (415) 835-8944 | | (415) 633-8558 |

| |

| KeyBanc Capital Markets | | SmithBarney Citigroup |

| Srikanth Nagarajan | | Jonathan Litt |

| (917) 368-2280 | | (212) 816-0231 |

Quarterly Reporting Schedule

Quarterly results will be announced according to the following anticipated schedule:

| | |

| Fourth Quarter and Year End | | March 1, 2006 |

| |

| First Quarter 2006 | | To be decided. |

Stock Listing

The stock of Digital Realty Trust, Inc. is traded primarily on the New York Stock Exchange under the following symbols:

| | |

| Common Stock: | | DLR |

| Series A Preferred Stock: | | DLRPA |

| Series B Preferred Stock: | | DLRPB |

Note that symbols may vary by stock quote provider.

4

Stock Performance

The following summarizes recent activity of Digital Realty’scommon stock (DLR):

| | | | | | | | | | | | | | | | |

| | | 4th Quarter

2005 | | | 3rd Quarter

2005 | | | 2nd Quarter

2005 | | | 1st Quarter

2005 | |

High Price * | | $ | 24.70 | | | $ | 19.97 | | | $ | 17.49 | | | $ | 14.81 | |

Low Price * | | $ | 17.73 | | | $ | 16.80 | | | $ | 13.67 | | | $ | 12.50 | |

Closing Price, end of period * | | $ | 22.63 | | | $ | 18.00 | | | $ | 17.38 | | | $ | 14.37 | |

Average daily trading volume * | | | 134,046 | | | | 260,942 | | | | 94,248 | | | | 94,884 | |

Indicated dividend per share ** | | $ | 1.060 | | | $ | 0.975 | | | $ | 0.975 | | | $ | 0.975 | |

Closing dividend yield, end of period | | | 4.7 | % | | | 5.4 | % | | | 5.6 | % | | | 6.8 | % |

Closing shares and units outstanding (thousands), end of period | | | 59,017 | | | | 58,826 | | | | 52,943 | | | | 52,943 | |

Closing market value of shares and units outstanding (thousands), end of period | | $ | 1,335,554 | | | $ | 1,058,870 | | | $ | 920,145 | | | $ | 760,787 | |

The following summarizes recent activity of Digital Realty’sSeries A preferred stock (DLRPA):

| | | | | | | | | | | | | | | | |

| | | 4th Quarter

2005 | | | 3rd Quarter

2005 | | | 2nd Quarter

2005 | | | 2/9/05 to

3/31/05 | |

High Price * | | $ | 26.25 | | | $ | 26.60 | | | $ | 26.70 | | | $ | 26.63 | |

Low Price * | | $ | 24.89 | | | $ | 26.10 | | | $ | 25.85 | | | $ | 25.90 | |

Closing Price, end of period * | | $ | 25.30 | | | $ | 26.35 | | | $ | 25.97 | | | $ | 26.00 | |

Indicated dividend per share ** | | $ | 2.125 | | | $ | 2.125 | | | $ | 2.125 | | | $ | 2.125 | |

Closing dividend yield, end of period | | | 8.4 | % | | | 8.1 | % | | | 8.2 | % | | | 8.2 | % |

Closing shares outstanding (thousands), end of period | | | 4,140 | | | | 4,140 | | | | 4,140 | | | | 4,140 | |

Closing market value of shares outstanding (thousands), end of period | | $ | 104,742 | | | $ | 109,089 | | | $ | 107,516 | | | $ | 107,640 | |

The following summarizes recent activity of Digital Realty’sSeries B preferred stock (DLRPB):

| | | | | | | | |

| | | 4th Quarter

2005 | | | 7/26/05 to

9/30/05 | |

High Price * | | $ | 25.15 | | | $ | 25.55 | |

Low Price * | | $ | 23.65 | | | $ | 24.95 | |

Closing Price, end of period * | | $ | 24.21 | | | $ | 24.95 | |

Indicated dividend per share ** | | $ | 1.969 | | | $ | 1.969 | |

Closing dividend yield, end of period | | | 8.1 | % | | | 7.9 | % |

Closing shares outstanding (thousands), end of period | | | 2,530 | | | | 2,530 | |

Closing market value of shares outstanding (thousands), end of period | | $ | 61,251 | | | $ | 63,124 | |

| * | New York Stock Exchange trades only |

5

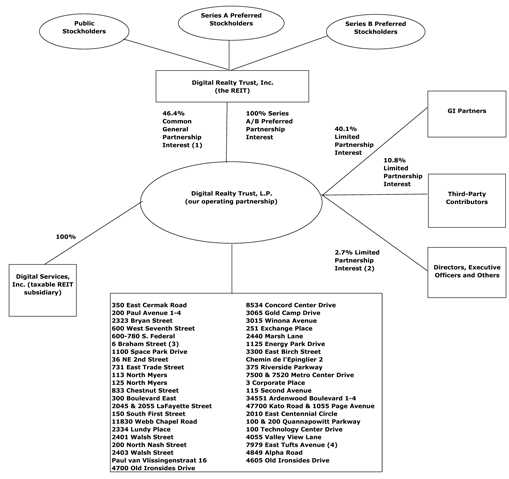

Digital Realty Trust, Inc.

Ownership Structure

As of December 31, 2005

| | | | | |

Partner | | # of Units (5) | | % Ownership (1) | |

Digital Realty Trust, Inc. | | 27,363,408 | | 46.4 | % |

GI Partners, LLC | | 23,699,359 | | 40.1 | % |

Cambay Tele.com, LLC (6) | | 5,903,124 | | 10.0 | % |

Wave Exchange, LLC (6) | | 32,722 | | 0.1 | % |

Pacific-Bryan Partners, L.P. (7) | | 395,665 | | 0.7 | % |

Directors, Executive Officers and Others | | 1,622,671 | | 2.7 | % |

| | | | | |

Total | | 59,016,949 | | 100.0 | % |

| | | | | |

| (1) | Excludes shares issuable with respect to stock options that have been granted but have not yet been exercised, and also excludes Class C units which have not yet vested. |

| (2) | Reflects limited partnership interests held by our officers and directors in the form of vested long-term incentive units. |

| (3) | This property is held through a taxable REIT subsidiary. |

| (4) | We indirectly own a 98% interest in a subsidiary that holds the fee simple interest in this property. An unrelated third party holds the remaining 2% interest in this subsidiary. |

| (5) | The total number of units includes 27,363,408 shares of common stock and 31,653,541 common units. |

| (6) | These third-party contributors received the units (along with cash and the operating partnership assuming debt) in exchange for their interests in 200 Paul Avenue 1-4, 1100 Space Park Drive, the eXchange colocation business and other specified assets and liabilities. |

| (7) | This third-party contributor received the units in exchange for a 10% minority interest in the 2323 Bryan Street property. |

6

Properties Acquired

For the three months ended December 31, 2005

| | | | | | | | | | | | | | | | |

Property | | Metropolitan Area | | Date Acquired | | Purchase

Price (in

millions) | | Net Rentable

Square Footage

of Property | | Total Square

Footage Held for

Redevelopment | | Percentage of

Total Rentable

Square Footage

of Property

Occupied (1) | | | Major Tenant(s) |

115 Second Avenue | | Boston | | October 2005 | | $ | 14.3 | | 12,500 | | 55,569 | | 0.0 | % | | N/A |

Chemin de l’Epinglier 2 | | Geneva, Switzerland | | November 2005 | | $ | 12.2 | | 59,190 | | — | | 100.0 | % | | PSI Net Realty Switze |

251 Exchange Place | | Northern Virginia | | November 2005 | | $ | 12.9 | | 70,982 | | — | | 100.0 | % | | Looking Glass Networks, Inc. |

7500 & 7520 Metro Center Drive | | Austin | | December 2005 | | $ | 13.5 | | 45,000 | | 74,962 | | 100.0 | % | | Electric Reliability Council of Texas |

3 Corporate Place | | New York | | December 2005 | | $ | 14.7 | | — | | 283,124 | | 0.0 | % | | N/A |

| | | | | | | | | | | | | | | | |

| | | | | | $ | 67.6 | | 187,672 | | 413,655 | | 93.3 | % | | |

| | | | | | | | | | | | | | | | |

| (1) | Excludes space held for redevelopment. |

7

Key Financial Data

(Dollars in thousands, except per share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | For the three months ended or as of | |

| | | 12/31/2005 | | | 9/30/2005 | | | 6/30/2005 | | | 3/31/2005 | | | 12/31/2004 | | | 9/30/2004 | | | 6/30/2004 | | | 3/31/2004 | |

Shares and Units | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Common Shares Outstanding | | | 27,363,408 | | | | 27,304,691 | | | | 21,421,300 | | | | 21,421,300 | | | | 21,421,300 | | | N/A | | | N/A | | | N/A | |

Common Units Outstanding | | | 31,653,541 | | | | 31,521,431 | | | | 31,521,431 | | | | 31,521,431 | | | | 31,521,431 | | | N/A | | | N/A | | | N/A | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Shares and Operating Partnership Units | | | 59,016,949 | | | | 58,826,122 | | | | 52,942,731 | | | | 52,942,731 | | | | 52,942,731 | | | N/A | | | N/A | | | N/A | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | |

Market Capitalization | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Market Value of Common Equity (1) | | $ | 1,335,554 | | | $ | 1,058,870 | | | $ | 920,145 | | | $ | 760,787 | | | $ | 713,139 | | | N/A | | | N/A | | | N/A | |

Stated Value of Preferred Equity | | | 166,750 | | | | 166,750 | | | | 103,500 | | | | 103,500 | | | | N/A | | | N/A | | | N/A | | | N/A | |

Total Debt | | | 749,067 | | | | 686,909 | | | | 765,687 | | | | 515,701 | | | | 519,498 | | | 551,351 | | | 473,896 | | | 318,199 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Market Capitalization | | $ | 2,251,371 | | | $ | 1,912,529 | | | $ | 1,789,332 | | | $ | 1,379,988 | | | $ | 1,232,637 | | | N/A | | | N/A | | | N/A | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Debt/Total Market Capitalization | | | 33.3 | % | | | 35.9 | % | | | 42.8 | % | | | 37.4 | % | | | 42.1 | % | | N/A | | | N/A | | | N/A | |

| | | | | | | | |

Selected Balance Sheet Data | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Book Value of Real Estate Assets before Depreciation | | | 1,258,510 | | | | 1,173,332 | | | | 1,099,699 | | | | 889,803 | | | | 818,392 | | | 675,204 | | | 602,805 | | | 433,123 | |

Total Assets | | | 1,529,170 | | | | 1,454,222 | | | | 1,368,256 | | | | 1,099,727 | | | | 1,013,287 | | | 822,189 | | | 731,237 | | | 513,968 | |

Total Liabilities | | | 880,228 | | | | 792,538 | | | | 856,617 | | | | 579,393 | | | | 584,229 | | | 593,699 | | | 509,684 | | | 346,545 | |

| | | | | | | | |

Selected Operating Data | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Revenue | | | 62,947 | | | | 56,556 | | | | 49,663 | | | | 39,643 | | | | 36,205 | | | 29,346 | | | 22,800 | | | 18,770 | |

Expenses (including interest expense) | | | 57,008 | | | | 50,507 | | | | 42,189 | | | | 34,748 | | | | 51,774 | | | 25,959 | | | 19,806 | | | 15,263 | |

Interest Expense | | | 10,988 | | | | 10,724 | | | | 9,289 | | | | 8,121 | | | | 8,657 | | | 7,926 | | | 4,065 | | | 3,813 | |

Net Income (Loss) | | | 4,602 | | | | 4,425 | | | | 4,335 | | | | 2,739 | | | | (5,359 | ) | | 3,359 | | | 3,096 | | | 3,461 | |

Net Income Available to Common Stockholders | | | 1,157 | | | | 1,326 | | | | 2,136 | | | | 1,468 | | | | — | | | — | | | — | | | — | |

| | | | | | | | |

Financial Ratios | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

EBITDA (2) | | | 30,949 | | | | 29,007 | | | | 25,753 | | | | 21,732 | | | | N/A | | | N/A | | | N/A | | | N/A | |

Adjusted EBITDA (2) | | | 35,731 | | | | 33,730 | | | | 31,091 | | | | 25,159 | | | | N/A | | | N/A | | | N/A | | | N/A | |

Cash interest expense (2) | | | 9,607 | | | | 9,947 | | | | 8,086 | | | | 7,416 | | | | N/A | | | N/A | | | N/A | | | N/A | |

Debt Service Coverage Ratio (2) | | | 3.7 | | | | 3.4 | | | | 3.8 | | | | 3.4 | | | | N/A | | | N/A | | | N/A | | | N/A | |

Fixed Charges (3) | | | 14,521 | | | | 15,019 | | | | 12,266 | | | | 10,525 | | | | N/A | | | N/A | | | N/A | | | N/A | |

Fixed Charge Coverage Ratio (3) | | | 2.5 | | | | 2.2 | | | | 2.5 | | | | 2.4 | | | | N/A | | | N/A | | | N/A | | | N/A | |

| | | | | | | | |

EPS, FFO and AFFO | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Basic Net Income (Loss) per common share | | $ | 0.04 | | | $ | 0.05 | | | $ | 0.10 | | | $ | 0.07 | | | $ | (0.30 | ) | | (4) N/A | | | N/A | | | N/A | |

Diluted Net Income (Loss) per common share | | $ | 0.04 | | | $ | 0.05 | | | $ | 0.10 | | | $ | 0.07 | | | $ | (0.30 | ) | | (4) N/A | | | N/A | | | N/A | |

Diluted FFO per share (5) | | $ | 0.36 | | | $ | 0.35 | | | $ | 0.37 | | | $ | 0.30 | | | $ | (0.17 | ) | | N/A | | | N/A | | | N/A | |

Diluted AFFO per share (5) | | $ | 0.26 | | | $ | 0.26 | | | $ | 0.31 | | | $ | 0.24 | | | | N/A | | | N/A | | | N/A | | | N/A | |

Dividends per share and common unit | | $ | 0.27 | | | $ | 0.24 | | | $ | 0.24 | | | $ | 0.24 | | | $ | 0.16 | | | N/A | | | N/A | | | N/A | |

Diluted FFO payout ratio (6) | | | 73.8 | % | | | 70.1 | % | | | 65.8 | % | | | 82.0 | % | | | N/A | | | N/A | | | N/A | | | N/A | |

Diluted AFFO payout ratio (6) | | | 101.5 | % | | | 93.6 | % | | | 79.9 | % | | | 100.0 | % | | | N/A | | | N/A | | | N/A | | | N/A | |

| | | | | | | | |

Portfolio Statistics | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Properties | | | 43 | | | | 38 | | | | 33 | | | | 26 | | | | 24 | | | 20 | | | 18 | | | 14 | |

Net rentable square feet | | | 8,051,212 | | | | 7,864,760 | | | | 7,791,110 | | | | 6,303,226 | | | | 5,652,700 | | | 4,796,996 | | | 4,252,058 | | | 2,989,266 | |

Square feet held for redevelopment (7) | | | 1,146,538 | | | | 731,663 | | | | 707,920 | | | | 107,563 | | | | — | | | — | | | — | | | — | |

Occupancy at end of quarter (8) | | | 93.9 | % | | | 93.2 | % | | | 93.0 | % | | | 88.9 | % | | | 88.4 | % | | 89.4 | % | | 89.3 | % | | 88.8 | % |

| (1) | Assuming 100% conversion of the limited partnership units in the operating partnership into shares of our common stock. |

| (2) | EBITDA is calculated as earnings before interest, taxes and depreciation. Adjusted EBITDA is EBITDA adjusted for preferred dividends and minority interests. Debt service coverage ratio is calculated as adjusted EBITDA divided by cash interest expense. For a definition of cash interest expense, see page 15. For a discussion of Adjusted EBITDA and EBITDA, see page 25. For a quantitative reconciliation of the differences between EBITDA and Adjusted EBITDA and net income, see page 13. |

| (3) | Calculated as Adjusted EBITDA divided by fixed charges. For a definition of fixed charges, see page 15. |

| (4) | The net loss per common share - basic and diluted is for the period from November 3, 2004 to December 31, 2004. This may not be comparable future net income (loss) per common share since it includes the effect of various IPO-related charges. |

| (5) | For a definition and discussion of FFO and AFFO, see page 25. For a quantitative reconciliation of the differences between FFO and net income, see page 11. For a quantitative reconciliation of the differences between FFO and AFFO, see page 12. |

| (6) | Calculated as dividend declared per common share divided by FFO or AFFO per common share - diluted. |

| (7) | Redevelopment space requires significant capital investment in order to develop datacenter facilities that are ready for use. Most often this is shell space. However, in certain circumstances this may include partially built datacenter space that was not completed by previous ownership and requires a large capital investment in order to build out the space. |

| (8) | Occupancy at end of quarter excludes space held for redevelopment. We completed a review of space held for development in the quarter ended September 30, 2005 and have not restated any occupancy statistics for March 31, 2005 and earlier periods. This will cause occupancy statistics for March 31, 2005 and earlier periods to not be comparable to occupancy statistics for later periods. |

Note: The Predecessor is not a legal entity; rather it is a combination of certain of the real estate subsidiaries of Global Innovation Partners, LLC, a Delaware limited liability company (GI Partners) along with an allocation of certain assets, liabilities, revenues and expenses of GI Partners related to the real estate held by such subsidiaries. The financial statements presented are the consolidated financial statements of the Company. The financial statements presented for periods prior to November 3, 2004 are the combined financial statements of the Predecessor.

8

Consolidated Balance Sheets

(in thousands, except share data)

| | | | | | | | |

| | | December 31,

2005 | | | December 31,

2004 | |

| | | (unaudited) | | | | |

ASSETS | | | | | | | | |

Investments in real estate | | | | | | | | |

Land | | $ | 191,961 | | | $ | 129,112 | |

Acquired ground lease | | | 1,477 | | | | 1,477 | |

Buildings and improvements | | | 941,115 | | | | 613,058 | |

Tenant improvements | | | 123,957 | | | | 74,745 | |

| | | | | | | | |

Investments in real estate | | | 1,258,510 | | | | 818,392 | |

Accumulated depreciation and amortization | | | (64,404 | ) | | | (30,980 | ) |

| | | | | | | | |

Net investments in real estate | | | 1,194,106 | | | | 787,412 | |

Cash and cash equivalents | | | 10,930 | | | | 4,557 | |

Accounts and other receivables, net | | | 7,587 | | | | 3,051 | |

Deferred rent | | | 25,094 | | | | 12,236 | |

Acquired above market leases, net | | | 48,237 | | | | 43,947 | |

Acquired in place lease value and deferred leasing costs, net | | | 201,141 | | | | 136,721 | |

Deferred financing costs, net | | | 7,659 | | | | 8,236 | |

Restricted cash | | | 22,123 | | | | 14,207 | |

Other assets | | | 12,293 | | | | 2,920 | |

| | | | | | | | |

Total Assets | | $ | 1,529,170 | | | $ | 1,013,287 | |

| | | | | | | | |

LIABILITIES AND STOCKHOLDERS’ EQUITY | | | | | | | | |

Notes payable under line of credit | | $ | 181,000 | | | $ | 44,000 | |

Mortgage loans | | | 568,067 | | | | 453,498 | |

Other secured loans | | | — | | | | 22,000 | |

Accounts payable and other accrued liabilities | | | 36,869 | | | | 12,789 | |

Accrued dividends and distributions | | | 15,639 | | | | 8,276 | |

Acquired below market leases, net | | | 67,177 | | | | 37,390 | |

Security deposits and prepaid rents | | | 11,476 | | | | 6,276 | |

| | | | | | | | |

Total Liabilities | | | 880,228 | | | | 584,229 | |

| | | | | | | | |

Commitments and contingencies | | | — | | | | — | |

Minority interests in consolidated joint ventures | | | 206 | | | | 997 | |

Minority interests in operating partnership | | | 262,239 | | | | 254,862 | |

Stockholders’ equity: | | | | | | | | |

Preferred Stock: $0.01 par value, 20,000,000 authorized: | | | | | | | | |

Series A Cumulative Redeemable Preferred Stock, 8.50%, $103,500,000 liquidation preference ($25.00 per share), 4,140,000 issued and outstanding | | | 99,297 | | | | — | |

Series B Cumulative Redeemable Preferred Stock, 7.875%, $63,250,000 liquidation preference ($25.00 per share), 2,530,000 issued and outstanding | | | 60,502 | | | | — | |

Common Stock; $0.01 par value: 100,000,000 authorized, 27,363,408 and 21,421,300 shares issued and outstanding as of December 31, 2005 and December 31, 2004 | | | 274 | | | | 214 | |

Additional paid-in capital | | | 252,562 | | | | 182,411 | |

Dividends in excess of earnings | | | (27,782 | ) | | | (9,517 | ) |

Accumulated other comprehensive income, net | | | 1,644 | | | | 91 | |

| | | | | | | | |

Total Stockholders’ Equity | | | 386,497 | | | | 173,199 | |

| | | | | | | | |

Total Liabilities and Stockholders’ Equity | | $ | 1,529,170 | | | $ | 1,013,287 | |

| | | | | | | | |

9

Consolidated and Combined Quarterly Statements of Operations

(unaudited and in thousands, except share data)

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended | |

| | | 12/31/2005 | | | 9/30/2005 | | | 6/30/2005 | | | 3/31/2005 | | | 12/31/2004 | | | 9/30/2004 | | | 6/30/2004 | | 3/31/2004 | |

Revenues | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Rental | | $ | 48,859 | | | $ | 45,065 | | | $ | 37,604 | | | $ | 32,691 | | | $ | 29,981 | | | $ | 24,666 | | | $ | 18,433 | | $ | 16,028 | |

Tenant reimbursements | | | 11,781 | | | | 11,040 | | | | 8,113 | | | | 6,520 | | | | 6,174 | | | | 4,658 | | | | 2,669 | | | 2,728 | |

Other | | | 2,307 | | | | 451 | | | | 3,946 | | | | 432 | | | | 50 | | | | 22 | | | | 1,698 | | | 14 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Revenues | | | 62,947 | | | | 56,556 | | | | 49,663 | | | | 39,643 | | | | 36,205 | | | | 29,346 | | | | 22,800 | | | 18,770 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Expenses | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Rental property operating and maintenance | | | 13,909 | | | | 12,385 | | | | 9,718 | | | | 7,145 | | | | 7,349 | | | | 5,336 | | | | 3,283 | | | 3,006 | |

Property taxes | | | 7,035 | | | | 6,241 | | | | 4,910 | | | | 3,681 | | | | 3,084 | | | | 2,417 | | | | 2,115 | | | 1,718 | |

Insurance | | | 905 | | | | 770 | | | | 530 | | | | 599 | | | | 696 | | | | 617 | | | | 321 | | | 241 | |

Interest | | | 10,988 | | | | 10,724 | | | | 9,289 | | | | 8,121 | | | | 8,657 | | | | 7,926 | | | | 4,065 | | | 3,813 | |

Asset management fees to related party | | | — | | | | — | | | | — | | | | — | | | | 266 | | | | 797 | | | | 796 | | | 796 | |

Depreciation and amortization | | | 18,804 | | | | 16,957 | | | | 14,328 | | | | 12,143 | | | | 10,576 | | | | 8,604 | | | | 6,711 | | | 5,507 | |

General and administrative | | | 4,425 | | | | 3,324 | | | | 2,453 | | | | 2,413 | | | | 20,774 | | | | 86 | | | | 65 | | | 92 | |

Loss from early extinguishment of debt | | | 896 | | | | — | | | | — | | | | 125 | | | | 283 | | | | — | | | | — | | | — | |

Other | | | 46 | | | | 106 | | | | 961 | | | | 521 | | | | 89 | | | | 176 | | | | 2,450 | | | 90 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Total Expenses | | | 57,008 | | | | 50,507 | | | | 42,189 | | | | 34,748 | | | | 51,774 | | | | 25,959 | | | | 19,806 | | | 15,263 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Income (loss) before minority interests | | | 5,939 | | | | 6,049 | | | | 7,474 | | | | 4,895 | | | | (15,569 | ) | | | 3,387 | | | | 2,994 | | | 3,507 | |

Minority interests in consolidated joint ventures | | | 1 | | | | 4 | | | | 4 | | | | 3 | | | | (4 | ) | | | (28 | ) | | | 102 | | | (46 | ) |

Minority interests in operating partnership | | | (1,338 | ) | | | (1,628 | ) | | | (3,143 | ) | | | (2,159 | ) | | | 10,214 | | | | — | | | | — | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | | 4,602 | | | | 4,425 | | | | 4,335 | | | | 2,739 | | | $ | (5,359 | ) | | $ | 3,359 | | | $ | 3,096 | | $ | 3,461 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Preferred stock dividends | | | (3,445 | ) | | | (3,099 | ) | | | (2,199 | ) | | | (1,271 | ) | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income available to common stockholders | | $ | 1,157 | | | $ | 1,326 | | | $ | 2,136 | | | $ | 1,468 | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) per common share - basic | | $ | 0.04 | | | $ | 0.05 | | | $ | 0.10 | | | $ | 0.07 | | | $ | (0.30 | )(1) | | | | | | | | | | | |

Net income (loss) per common share - diluted | | $ | 0.04 | | | $ | 0.05 | | | $ | 0.10 | | | $ | 0.07 | | | $ | (0.30 | )(1) | | | | | | | | | | | |

Weighted-average shares outstanding - basic | | | 27,314,190 | | | | 25,704,721 | | | | 21,421,300 | | | | 21,421,300 | | | | 20,770,875 | | | | | | | | | | | | |

Weighted-average shares outstanding - diluted | | | 27,656,496 | | | | 26,004,324 | | | | 21,584,913 | | | | 21,535,485 | | | | 20,770,875 | | | | | | | | | | | | |

Weighted-average fully diluted shares and units | | | 59,248,243 | | | | 57,525,755 | | | | 53,106,344 | | | | 53,056,916 | | | | 52,942,731 | | | | | | | | | | | | |

| (1) | The net loss per common share - basic and diluted is for the period from November 3, 2004 to December 31, 2004. This may not be comparable future net income (loss) per common share since it includes the effect of various IPO-related charges. |

10

Funds From Operations

(unaudited and in thousands, except share data)

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended |

| | | 12/31/2005 | | 9/30/2005 | | 6/30/2005 | | 3/31/2005 | | 12/31/2004 | | | 9/30/2004 | | 6/30/2004 | | 3/31/2004 |

Reconciliation of net income (loss) available to common stockholders to funds from operations: | | | | | | | | | | | | | | | | | | | | | | | | | |

Net income (loss) available to common stockholders | | $ | 1,157 | | $ | 1,326 | | $ | 2,136 | | $ | 1,468 | | $ | (5,359 | ) | | $ | 3,359 | | $ | 3,096 | | $ | 3,461 |

Adjustments: | | | | | | | | | | | | | | | | | | | | | | | | | |

Minority interests in operating partnership | | | 1,338 | | | 1,628 | | | 3,143 | | | 2,159 | | | (10,214 | ) | | | — | | | — | | | — |

Real estate related depreciation and amortization | | | 18,781 | | | 16,929 | | | 14,318 | | | 12,143 | | | 10,576 | | | | 8,604 | | | 6,711 | | | 5,507 |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Funds from operations available to common stockholders and unitholders (FFO) | | $ | 21,276 | | $ | 19,883 | | $ | 19,597 | | $ | 15,770 | | $ | (4,997 | ) | | $ | 11,963 | | $ | 9,807 | | $ | 8,968 |

| | | | | | | | | | | | | | | | | | | | | | | | | |

FFO per share: | | | | | | | | | | | | | | | | | | | | | | | | | |

Basic | | $ | 0.36 | | $ | 0.35 | | $ | 0.37 | | $ | 0.30 | | $ | (0.17 | )(1) | | | N/A | | | N/A | | | N/A |

Diluted | | $ | 0.36 | | $ | 0.35 | | $ | 0.37 | | $ | 0.30 | | $ | (0.17 | )(1) | | | N/A | | | N/A | | | N/A |

| | | | | | | | | | | | | | | | | | | | | | | | | |

Weighted-average shares outstanding - basic | | | 58,906 | | | 57,226 | | | 52,943 | | | 52,943 | | | 52,943 | | | | N/A | | | N/A | | | N/A |

Weighted-average shares outstanding - diluted | | | 59,248 | | | 57,526 | | | 53,106 | | | 53,057 | | | 52,943 | | | | N/A | | | N/A | | | N/A |

| (1) | The FFO per share - basic and diluted is for the period from November 3, 2004 to December 31, 2004. This may not be comparable future net income (loss) per common share since it includes the effect of various IPO-related charges. |

Note:For a definition and discussion of FFO, see page 25.

11

Adjusted Funds From Operations

(unaudited and in thousands)

| | | | | | | | | | | | | | | | |

| | | Three Months Ended | |

| | | 12/31/2005 | | | 9/30/2005 | | | 6/30/2005 | | | 3/31/2005 | |

Reconciliation of funds from operations (FFO) to adjusted funds from operations (AFFO): | | | | | | | | | | | | | | | | |

Funds from operations available to common stockholders and unitholders (FFO) | | $ | 21,276 | | | $ | 19,883 | | | $ | 19,597 | | | $ | 15,770 | |

Adjustments: | | | | | | | | | | | | | | | | |

Non real estate depreciation | | | 23 | | | | 28 | | | | 10 | | | | — | |

Amortization of deferred financing costs | | | 793 | | | | 790 | | | | 707 | | | | 675 | |

Non cash compensation | | | 335 | | | | 50 | | | | 44 | | | | 52 | |

Loss from early extinguishment of debt | | | 896 | | | | — | | | | — | | | | 125 | |

Straight line rents | | | (4,172 | ) | | | (3,815 | ) | | | (2,483 | ) | | | (2,553 | ) |

Above and below market rent amortization | | | (632 | ) | | | (416 | ) | | | (230 | ) | | | (439 | ) |

Capitalized leasing payroll | | | (105 | ) | | | (549 | ) | | | (127 | ) | | | — | |

Recurring capital expenditures and tenant improvements | | | (1,406 | ) | | | (240 | ) | | | (732 | ) | | | (519 | ) |

Capitalized leasing commissions | | | (1,535 | ) | | | (757 | ) | | | (579 | ) | | | (180 | ) |

| | | | | | | | | | | | | | | | |

Adjusted Funds from operations available to common stockholders and unitholders (AFFO) | | $ | 15,473 | | | $ | 14,974 | | | $ | 16,207 | | | $ | 12,931 | |

| | | | | | | | | | | | | | | | |

Note: For a definition and discussion of AFFO, see page 25. For a reconciliation of net income (loss) available to common stockholders to FFO, see page 11.

12

Reconciliation of Earnings Before Interest Taxes and Depreciation and Amortization

(unaudited and in thousands)

| | | | | | | | | | | | |

| | | Three Months Ended |

| | | 12/31/2005 | | 9/30/2005 | | 6/30/2005 | | 3/31/2005 |

Reconciliation of net income available to common stockholders to earnings before interest, taxes and depreciation and amortization (EBITDA) and Adjusted EBITDA(1) | | | | | | | | | | | | |

Net income available to common stockholders | | $ | 1,157 | | $ | 1,326 | | $ | 2,136 | | $ | 1,468 |

Add: Interest | | | 10,988 | | | 10,724 | | | 9,289 | | | 8,121 |

Depreciation and amortization | | | 18,804 | | | 16,957 | | | 14,328 | | | 12,143 |

| | | | | | | | | | | | |

EBITDA | | | 30,949 | | | 29,007 | | | 25,753 | | | 21,732 |

Minority interests | | | 1,337 | | | 1,624 | | | 3,139 | | | 2,156 |

Preferred stock dividends | | | 3,445 | | | 3,099 | | | 2,199 | | | 1,271 |

| | | | | | | | | | | | |

Adjusted EBITDA | | $ | 35,731 | | $ | 33,730 | | $ | 31,091 | | $ | 25,159 |

| | | | | | | | | | | | |

| (1) | For the definition and discussion of EBITDA and Adjusted EBITDA, see page 25. |

13

Capital Structure

As of December 31, 2005

Consolidated Debt and Equity

(in thousands)

| | | | | |

| | | | | December 31,

2005 |

Mortgage and Other Secured Loans Payable | | | | $ | 568,067 |

Unsecured Credit Facility | | | | | 181,000 |

| | | | | |

Total Debt | | | | $ | 749,067 |

| | | | | |

| | |

| | | Shares Outstanding | | Total

Liquidation

Preference |

Preferred Stock | | 6,670 | | $ | 166,750 |

| | |

| | | Shares & Units Outstanding | | Market

Value (1) |

Common Stock | | 27,363.4 | | $ | 619,234 |

Operating Partnership Units | | 31,653.5 | | | 716,320 |

| | | | | |

Total Common Equity | | 59,016.9 | | $ | 1,335,554 |

| | | | | |

Total Market Capitalization | | | | $ | 2,251,371 |

| | | | | |

| (1) | Value based on December 31, 2005 closing price of $22.63. |

14

Consolidated Debt Analysis

(in thousands)

| | | | | | | | | | | |

| | | Maturity Date | | Principal

Balance as of

December 31,

2005 | | % of Debt | | | Interest Rate

as of

December 31,

2005 | |

Floating Rate Debt | | | | | | | | | | | |

47700 Kato Road & 1055 Page Avenue-Mortgage | | December 31, 2006(2) | | | 17,540 | | 2.3 | % | | 6.09 | % |

Unsecured Credit Facility | | November 3, 2008 | | | 181,000 | | 24.2 | % | | 5.89 | % |

| | | | | | | | | | | |

Total Unhedged Floating Rate Debt | | | | | 198,540 | | 26.5 | % | | | |

Fixed Rate Mortgage Debt | | | | | | | | | | | |

Secured Term Debt | | November 11, 2014 | | | 152,918 | | 20.4 | % | | 5.65 | % |

350 East Cermak Road | | June 9, 2008(2) | | | 100,000 | | 13.4 | % | | 6.59 | %(4) |

2323 Bryan Street | | November 6, 2009 | | | 57,282 | | 7.6 | % | | 6.04 | % |

200 Paul Avenue 1-4 | | October 8, 2015 | | | 81,000 | | 10.8 | % | | 5.74 | % |

34551 Ardenwood Boulevard 1-4, 2334 Lundy Place, 2440 Marsh Lane | | August 9, 2006(3) | | | 43,000 | | 5.7 | % | | 5.98 | %(4) |

7979 East Tufts Avenue | | January 10, 2009 | | | 26,000 | | 3.5 | % | | 5.14 | % |

6 Braham Street | | October 31, 2009 | | | 22,490 | | 3.0 | % | | 6.85 | % |

4055 Valley View Lane | | January 1, 2009 | | | 21,150 | | 2.8 | % | | 5.74 | %(4) |

100 Technology Center Drive | | April 1, 2009 | | | 20,000 | | 2.7 | % | | 6.24 | %(4) |

1125 Energy Park Drive | | March 1, 2032 | | | 9,675 | | 1.3 | % | | 7.62 | % |

731 East Trade Street | | July 1, 2020 | | | 6,042 | | 0.8 | % | | 7.82 | % |

375 Riverside Parkway | | December 1, 2006(2) | | | 8,775 | | 1.2 | % | | 6.39 | %(4) |

| | | | | | | | | | | |

Total Fixed Rate Debt | | | | | 548,332 | | 73.2 | % | | | |

Loan premium—1125 Energy Park Drive and 731 East Trade Street | | | | | 2,195 | | 0.3 | % | | | |

| | | | | | | | | | | |

Total Consolidated Debt | | | | $ | 749,067 | | 100.0 | % | | | |

| | | | | | | | | | | |

Weighted average cost of debt (including interest rate swaps) | | | | | | | | | | 5.82 | % |

| | | | | | | | | | | |

| (1) | A one-year extension option is available. |

| (2) | Two one-year extensions are available. |

| (3) | A 13-month extension and a one-year extension are available. |

| (4) | Mortgage loans subject to interest rate swap agreements. The interest rates on the mortgage loans, adjusted for the interest rate swap agreements are as follows: |

| | | |

350 East Cermak Road | | 6.23 | % |

34551 Ardenwood Boulevard 1-4, 2334 Lundy Place, 2440 Marsh Lane | | 4.84 | % |

4055 Valley View Lane | | 4.95 | % |

100 Technology Center Drive | | 5.52 | % |

375 Riverside Parkway | | 5.18 | % |

Credit Facility

(in thousands)

| | | | | | | | | |

| | | Maximum

Available | | Available

as of December 31,

2005 | | Drawn |

Unsecured Credit Facility | | $ | 350,000 | | $ | 56,500 | | $ | 181,000 |

Financial Ratios

| | | |

EBITDA | | 30,949 | |

Adjusted EBITDA | | 35,731 | |

Total interest expense per income statement | | 10,988 | |

Less non cash interest | | 1,301 | |

| | | |

Cash interest expense (a) | | 9,607 | |

Debt service coverage ratio based on GAAP interest expense (b) | | 3.3 | |

Debt service coverage ratio based on cash interest expense (b) | | 3.7 | |

Scheduled debt principal payments and preferred dividends | | 4,914 | |

Total fixed charges | | 14,521 | |

Fixed charge coverage ratio based on GAAP interest expense (c) | | 2.2 | |

Fixed charge coverage ratio based on cash interest expense (c) | | 2.5 | |

Debt to total market capitalization (d) | | 33.3 | % |

Debt plus preferred stock to total market capitalization (e) | | 40.7 | % |

Pretax income to interest expense (f) | | 1.5 | |

| (a) | Cash interest expense relates to interest less amortized deferred financing fees and includes interest that we capitalized. We consider cash interest expense to be a useful measure of interest as it does not include non-cash based interest expense. |

| (b) | Adjusted EBITDA divided by interest expense. |

| (c) | Adjusted EBITDA divided by fixed charges. Fixed charges include interest expense as per a above and scheduled debt principal payments and preferred dividends. |

| (d) | Mortgage debt and other loans divided by mortgage debt and other loans plus the liquidation value of preferred stock and the market value of outstanding common stock and operating partnership units, assuming the conversion of operating partnership units into shares of our common stock. |

| (e) | Same as (d), except numerator includes preferred stock. |

| (f) | Calculated as income before minority interest and interest divided by interest expense. |

15

Debt Maturities

(in thousands)

| | | | | | | | | | | | | | |

Property | | 2006 | | 2007 | | 2008 | | 2009 | | 2010 | | Thereafter | | Total |

Secured Term Debt(1) | | 2,030 | | 2,150 | | 2,276 | | 2,410 | | 2,552 | | 141,500 | | 152,918 |

350 East Cermak Road(2) | | 506 | | 1,078 | | 98,416 | | — | | — | | — | | 100,000 |

2323 Bryan Street | | 703 | | 747 | | 784 | | 55,048 | | — | | — | | 57,282 |

34551 Ardenwood Boulevard 1-4, 2334 Lundy Place, 2440 Marsh Lane (3) | | 43,000 | | — | | — | | — | | — | | — | | 43,000 |

7979 East Tufts Avenue | | — | | — | | — | | 26,000 | | — | | — | | 26,000 |

6 Braham Street | | 1,947 | | 2,085 | | 2,230 | | 16,228 | | — | | — | | 22,490 |

4055 Valley View Lane | | 540 | | 540 | | 540 | | 19,530 | | — | | — | | 21,150 |

100 Technology Center Drive | | — | | — | | — | | 20,000 | | — | | — | | 20,000 |

47700 Kato Road & 1055 Page Avenue-Mortgage(2) | | 17,540 | | — | | — | | — | | — | | — | | 17,540 |

1125 Energy Park Drive | | 105 | | 114 | | 121 | | 132 | | 143 | | 9,060 | | 9,675 |

731 East Trade Street | | 160 | | 174 | | 189 | | 205 | | 235 | | 5,079 | | 6,042 |

375 Riverside Parkway(2) | | 8,775 | | — | | — | | — | | — | | — | | 8,775 |

200 Paul Avenue 1-4 | | — | | 231 | | 1,433 | | 1,533 | | 1,624 | | 76,179 | | 81,000 |

Unsecured Credit Facility | | — | | — | | 181,000 | | — | | — | | — | | 181,000 |

| | | | | | | | | | | | | | |

Total | | 75,306 | | 7,119 | | 286,989 | | 141,086 | | 4,554 | | 231,818 | | 746,872 |

| | | | | | | | | | | | | | |

The debt secured by our properties at December 31, 2005 had a weighted average term to initial maturity of approximately 5.0 years (approximately 5.7 years assuming exercise of extension options).

| (1) | This amount represents six mortgage loans secured by our interests in 36 NE 2nd Street, 3300 East Birch Street, 100 & 200 Quannapowitt Parkway, 300 Boulevard East, 4849 Alpha Road, and 11830 Webb Chapel Road. Each of these loans are cross-collateralized by the six properties. |

| (2) | Two one-year extensions are available. |

| (3) | A 13-month extension and a one-year extension are available. |

Note:Above amounts assume no exercise of extensions and total excludes $2,195 of Loan Premiums.

16

Occupancy Analysis

As of December 31, 2005

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | | | | | | | | Occupancy | | | Net Rentable

Square Feet as a % of | | | Annualized Rent as a % of | |

Property (1) | | Acquisition

date | | Metropolitan

Area | | Net

Rentable

Square

Feet | | Redevelopment

Space | | Annualized

Rent

($000) (2) | | As of

12/31/05 (3) | | | As of

9/30/05 (3) | | | As of

6/30/05 (3) | | | As of

3/31/05 | | | Property

Type | | | Total

Portfolio | | | Property

Type | | | Total

Portfolio | |

Internet Gateways | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

350 East Cermak Road | | May 2005 | | Chicago | | 870,183 | | 263,208 | | | 18,640 | | 92.2 | % | | 92.2 | % | | 82.6 | % | | N/A | % | | 31.1 | % | | 10.8 | | | 28.9 | % | | 12.0 | % |

200 Paul Avenue 1-4 | | Nov. 2004 | | San Francisco | | 494,608 | | 37,630 | | | 12,881 | | 95.8 | | | 93.8 | | | 93.7 | | | 83.4 | | | 17.7 | | | 6.1 | | | 20.0 | | | 8.3 | |

2323 Bryan Street | | Jan. 2002 | | Dallas | | 457,217 | | 19,890 | | | 8,455 | | 82.0 | | | 80.9 | | | 83.8 | | | 79.9 | | | 16.4 | | | 5.7 | | | 13.1 | | | 5.4 | |

600 West Seventh Street | | May 2004 | | Los Angeles | | 430,759 | | 59,319 | | | 7,858 | | 90.8 | | | 83.0 | | | 82.3 | | | 79.7 | | | 15.4 | | | 5.4 | | | 12.2 | | | 5.1 | |

600-780 S. Federal | | Sept. 2005 | | Chicago | | 161,547 | | — | | | 4,405 | | 84.1 | | | 84.1 | | | N/A | | | N/A | | | 5.8 | | | 2.0 | | | 6.8 | | | 2.8 | |

6 Braham Street | | July 2002 | | London, England | | 63,233 | | — | | | 3,816 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 2.3 | | | 0.8 | | | 5.9 | | | 2.5 | |

1100 Space Park Drive | | Nov. 2004 | | Silicon Valley | | 82,409 | | 85,542 | | | 3,598 | | 94.9 | | | 94.9 | | | 94.9 | | | 46.6 | | | 2.9 | | | 1.0 | | | 5.6 | | | 2.3 | |

36 NE 2nd Street | | Jan. 2002 | | Miami | | 162,140 | | — | | | 3,232 | | 81.2 | | | 81.2 | | | 81.2 | | | 81.2 | | | 5.8 | | | 2.0 | | | 5.0 | | | 2.1 | �� |

731 East Trade Street | | Aug. 2005 | | Charlotte | | 40,879 | | — | | | 1,007 | | 100.0 | | | 100.0 | | | N/A | | | N/A | | | 1.5 | | | 0.5 | | | 1.5 | | | 0.6 | |

113 North Myers | | Aug. 2005 | | Charlotte | | 18,717 | | 10,501 | | | 444 | | 100.0 | | | 100.0 | | | N/A | | | N/A | | | 0.7 | | | 0.2 | | | 0.7 | | | 0.3 | |

125 North Myers | | Aug. 2005 | | Charlotte | | 12,151 | | 13,242 | | | 229 | | 85.8 | | | 85.8 | | | N/A | | | N/A | | | 0.4 | | | 0.2 | | | 0.3 | | | 0.1 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | 2,793,843 | | 489,332 | | | 64,565 | | 90.2 | | | 88.8 | | | 86.1 | | | 80.9 | | | 100.0 | | | 34.7 | | | 100.0 | | | 41.5 | |

Data Centers | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

833 Chestnut Street | | March 2005 | | Philadelphia | | 535,098 | | 119,660 | | | 7,222 | | 91.5 | | | 91.3 | | | 93.3 | | | 91.5 | | | 16.4 | | | 6.6 | | | 12.9 | | | 4.7 | |

300 Boulevard East | | Nov. 2002 | | New York | | 311,950 | | — | | | 6,867 | | 87.4 | | | 87.4 | | | 87.4 | | | 87.4 | | | 9.6 | | | 3.9 | | | 12.2 | | | 4.4 | |

2045 & 2055 LaFayette Street | | May 2004 | | Silicon Valley | | 300,000 | | — | | | 5,940 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 9.2 | | | 3.7 | | | 10.6 | | | 3.8 | |

150 South First Street | | Sept. 2004 | | Silicon Valley | | 187,334 | | — | | | 4,750 | | 98.5 | | | 98.5 | | | 95.7 | | | 96.2 | | | 5.8 | | | 2.3 | | | 8.5 | | | 3.1 | |

11830 Webb Chapel Road | | Aug. 2004 | | Dallas | | 365,648 | | — | | | 4,689 | | 93.3 | | | 90.5 | | | 90.5 | | | 90.6 | | | 11.2 | | | 4.5 | | | 8.3 | | | 3.0 | |

2334 Lundy Place | | Dec. 2002 | | Silicon Valley | | 130,752 | | — | | | 3,932 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 4.0 | | | 1.6 | | | 7.0 | | | 2.5 | |

2401 Walsh Street | | June 2005 | | Silicon Valley | | 167,932 | | — | | | 3,028 | | 100.0 | | | 100.0 | | | 100.0 | | | N/A | | | 5.2 | | | 2.1 | | | 5.4 | | | 2.0 | |

200 North Nash Street | | June 2005 | | Los Angeles | | 113,606 | | — | | | 2,048 | | 100.0 | | | 100.0 | | | 100.0 | | | N/A | | | 3.5 | | | 1.4 | | | 3.6 | | | 1.3 | |

2403 Walsh Street | | June 2005 | | Silicon Valley | | 103,940 | | — | | | 1,874 | | 100.0 | | | 100.0 | | | 100.0 | | | N/A | | | 3.2 | | | 1.3 | | | 3.3 | | | 1.2 | |

Paul van Vlissingenstraat 16 | | Aug. 2005 | | Amsterdam, Netherlands | | 112,472 | | — | | | 1,658 | | 62.0 | | | 62.0 | | | N/A | | | N/A | | | 3.5 | | | 1.4 | | | 3.0 | | | 1.1 | |

4700 Old Ironsides Drive | | June 2005 | | Silicon Valley | | 90,139 | | — | | | 1,625 | | 100.0 | | | 100.0 | | | 100.0 | | | N/A | | | 2.8 | | | 1.1 | | | 2.9 | | | 1.0 | |

8534 Concord Center Drive | | June 2005 | | Denver | | 82,229 | | — | | | 1,521 | | 100.0 | | | 100.0 | | | 100.0 | | | N/A | | | 2.5 | | | 1.0 | | | 2.7 | | | 1.0 | |

3065 Gold Camp Drive | | Oct. 2004 | | Sacramento | | 62,957 | | — | | | 1,487 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 1.9 | | | 0.8 | | | 2.6 | | | 1.0 | |

3015 Winona Avenue | | Dec. 2004 | | Los Angeles | | 82,911 | | — | | | 1,414 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 2.5 | | | 1.0 | | | 2.5 | | | 0.9 | |

251 Exchange Place | | Nov. 2005 | | Northern Virginia | | 70,982 | | — | | | 1,374 | | 100.0 | | | N/A | | | N/A | | | N/A | | | 2.2 | | | 0.9 | | | 2.4 | | | 0.9 | |

2440 Marsh Lane | | Jan. 2003 | | Dallas | | 135,250 | | — | | | 1,353 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 4.2 | | | 1.7 | | | 2.4 | | | 0.9 | |

1125 Energy Park Drive | | March 2005 | | Minneapolis/St. Paul | | 88,134 | | — | | | 1,340 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 2.7 | | | 1.1 | | | 2.4 | | | 0.9 | |

3300 East Birch Street | | Aug. 2003 | | Los Angeles | | 68,807 | | — | | | 1,228 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 2.1 | | | 0.9 | | | 2.2 | | | 0.8 | |

Chemin de l’Epinglier 2 | | Nov. 2005 | | Geneva, Switzerland | | 59,190 | | — | | | 1,176 | | 100.0 | | | N/A | | | N/A | | | N/A | | | 1.8 | | | 0.7 | | | 2.1 | | | 0.8 | |

375 Riverside Parkway | | June 2003 | | Atlanta | | 126,300 | | 123,891 | | | 1,138 | | 100.0 | | | 100.0 | | | 100.0 | | | 50.5 | | | 3.9 | | | 1.6 | | | 2.0 | | | 0.7 | |

7500 & 7520 Metro Center Drive | | Dec. 2005 | | Austin | | 45,000 | | 74,962 | | | 551 | | 100.0 | | | N/A | | | N/A | | | N/A | | | 1.4 | | | 0.6 | | | 1.0 | | | 0.4 | |

3 Corporate Place | | Dec. 2005 | | New York | | — | | 283,124 | | | — | | 0.0 | | | N/A | | | N/A | | | N/A | | | — | | | — | | | — | | | — | |

115 Second Avenue | | Oct. 2005 | | Boston | | 12,500 | | 55,569 | | | — | | 0.0 | | | N/A | | | N/A | | | N/A | | | 0.4 | | | 0.2 | | | — | | | — | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | 3,253,131 | | 657,206 | | | 56,215 | | 94.9 | | | 94.4 | | | 95.9 | | | 89.1 | | | 100.0 | | | 40.4 | | | 100.0 | | | 36.4 | |

Technology Manufacturing | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

34551 Ardenwood Boulevard 1-4 | | Jan. 2003 | | Silicon Valley | | 307,657 | | — | | | 7,941 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 50.9 | | | 3.8 | | | 56.9 | | | 5.1 | |

47700 Kato Road & 1055 Page Avenue | | Sept. 2003 | | Silicon Valley | | 183,050 | | — | | | 3,472 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 30.3 | | | 2.3 | | | 24.9 | | | 2.2 | |

2010 East Centennial Circle | | May 2003 | | Phoenix | | 113,405 | | — | | | 2,549 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 18.8 | | | 1.4 | | | 18.2 | | | 1.7 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | 604,112 | | — | | | 13,962 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 7.5 | | | 100.0 | | | 9.0 | |

Technology Office | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

100 & 200 Quannapowitt Parkway | | June 2004 | | Boston | | 386,956 | | — | | | 5,989 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 27.6 | | | 4.8 | | | 29.6 | | | 3.9 | |

100 Technology Center Drive | | Feb. 2004 | | Boston | | 197,000 | | — | | | 3,743 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 14.1 | | | 2.5 | | | 18.5 | | | 2.4 | |

4055 Valley View Lane | | Sept. 2003 | | Dallas | | 240,065 | | — | | | 3,435 | | 94.3 | | | 94.3 | | | 94.3 | | | 94.6 | | | 17.1 | | | 3.0 | | | 17.0 | | | 2.2 | |

7979 East Tufts Avenue | | Oct. 2003 | | Denver | | 366,184 | | — | | | 3,286 | | 89.0 | | | 89.8 | | | 91.9 | | | 88.4 | | | 26.2 | | | 4.5 | | | 16.3 | | | 2.1 | |

4849 Alpha Road | | April 2004 | | Dallas | | 125,538 | | — | | | 2,263 | | 100.0 | | | 100.0 | | | 100.0 | | | 100.0 | | | 9.0 | | | 1.6 | | | 11.1 | | | 1.5 | |

4605 Old Ironsides Drive | | June 2005 | | Silicon Valley | | 84,383 | | — | | | 1,521 | | 100.0 | | | 100.0 | | | 100.0 | | | N/A | | | 6.0 | | | 1.0 | | | 7.5 | | | 1.0 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| | | | | | 1,400,126 | | — | | | 20,237 | | 96.1 | | | 96.4 | | | 96.9 | | | 95.8 | | | 100.0 | | | 17.4 | | | 100.0 | | | 13.1 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

Portfolio Total/Weighted Average | | | | | | 8,051,212 | | 1,146,538 | | $ | 154,979 | | 93.9 | % | | 93.2 | % | | 93.0 | % | | 88.9 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % | | 100.0 | % |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) | In the final quarter of 2005 we renamed our properties based on the address of each building. Please see page 24 for a list of the former names used in previous supplemental information presentations. |

| (2) | Annualized rent represents the monthly contractual rent under existing leases as of December 31, 2005 multiplied by 12. This amount reflects total base rent before any one-time or non-recurring rent abatements, but after annually recurring rent credits and is shown on a net basis; thus, for any tenant under a partial gross lease, the expense stop, or under a full gross lease, the current year operating expenses (which may be estimates as of such date), are subtracted from gross rent. |

| (3) | The December 31, 2005 occupancies excludes the redevelopment space in the column above. We completed a review of space held for development in the quarter ended September 30, 2005 and have not restated any occupancy statistics for March 31, 2005 and earlier periods. This will cause occupancy statistics for March 31, 2005 to not be comparable to occupancy statistics for later periods. |

17

Major Tenants

As of December 31, 2005

| | | | | | | | | | | | | | | | | |

| | | Tenant | | Number of

Locations | | Total Occupied

Square Feet (1) | | Percentage of

Net Rentable

Square Feet | | | Annualized

Rent ($000) | | Percentage of

Annualized

Rent | | | Weighted

Average

Remaining

Lease Term

in Months |

| 1 | | Savvis Communications (2) | | 9 | | 1,119,401 | | 13.9 | % | | $ | 22,775 | | 14.7 | % | | 126 |

| 2 | | Qwest Communications International, Inc. | | 10 | | 655,494 | | 8.1 | % | | | 17,359 | | 11.2 | % | | 112 |

| 3 | | Verio Inc. (3) | | 2 | | 238,051 | | 3.0 | % | | | 6,484 | | 4.2 | % | | 81 |

| 4 | | Comverse Network Systems | | 1 | | 367,033 | | 4.6 | % | | | 5,690 | | 3.7 | % | | 62 |

| 5 | | Equinix, Inc. | | 2 | | 324,354 | | 4.0 | % | | | 5,427 | | 3.5 | % | | 113 |

| 6 | | Abgenix (4) | | 1 | | 131,386 | | 1.6 | % | | | 5,146 | | 3.3 | % | | 64 |

| 7 | | AT&T (5) | | 7 | | 289,343 | | 3.6 | % | | | 4,785 | | 3.1 | % | | 86 |

| 8 | | AboveNet, Inc. | | 4 | | 154,215 | | 1.9 | % | | | 4,475 | | 2.9 | % | | 152 |

| 9 | | Leslie & Godwin (6) | | 1 | | 63,233 | | 0.8 | % | | | 3,816 | | 2.5 | % | | 48 |

| 10 | | Stone & Webster, Inc. (7) | | 1 | | 197,000 | | 2.4 | % | | | 3,743 | | 2.4 | % | | 87 |

| 11 | | Maxtor Corporation (8) | | 1 | | 183,050 | | 2.3 | % | | | 3,472 | | 2.2 | % | | 69 |

| 12 | | XO Communications, Inc. | | 6 | | 98,878 | | 1.2 | % | | | 2,913 | | 1.9 | % | | 109 |

| 13 | | VSNL Networks, Inc. | | 1 | | 59,289 | | 0.7 | % | | | 2,803 | | 1.8 | % | | 131 |

| 14 | | Thomas Jefferson University | | 1 | | 179,659 | | 2.2 | % | | | 2,626 | | 1.7 | % | | 57 |

| 15 | | ASM Lithography | | 1 | | 113,405 | | 1.4 | % | | | 2,549 | | 1.6 | % | | 134 |

| | | | | | | | | | | | | | | | | |

| | Total/Weighted Average | | | | 4,173,791 | | 51.7 | % | | $ | 94,063 | | 60.7 | % | | 102 |

| | | | | | | | | | | | | | | | | |

| (1) | Occupied square footage is defined as leases that have commenced on or before December 31, 2005. |

| (2) | Microsoft subleases 300,000 net rentable square feet (approximately $5.9 million of annualized rent) of this space and has the right to become tenant if the primary lessor defaults. |

| (3) | Verio is a wholly-owned subsidiary of Nippon Telegraph & Telephone. |

| (4) | Amgen signed an agreement to acquire Abgenix in December 2005. |

| (5) | SBC finalized the acquisition of AT&T in December 2005. |

| (6) | Leslie & Godwin is a United Kingdom subsidiary of AON Corporation. |

| (7) | Stone & Webster is a subsidiary of The Shaw Group. |

| (8) | Seagate Technology signed an agreement to acquire Maxtor in December 2005. |

18

Lease Expirations

As of December 31, 2005

| | | | | | | | | | | | | | | | | | | | | | |

Year | | Number of

Leases

Expiring | | Square

Footage of

Expiring

Leases | | Percentage of

Net Rentable

Square Feet | | | Annualized

Rent ($000) | | Percentage of

Annualized

Rent | | | Annualized

Rent Per

Occupied

Square Foot | | Annualized

Rent Per

Occupied

Square Foot

at Expiration | | Annualized

Rent at

Expiration

($000) |

Available | | | | 494,232 | | 6.1 | % | | $ | — | | 0.0 | % | | | | | | | | | |

2006 | | 62 | | 230,595 | | 2.9 | % | | | 3,605 | | 2.3 | % | | $ | 15.63 | | $ | 17.39 | | | 4,010 |

2007 | | 37 | | 149,890 | | 1.8 | % | | | 3,249 | | 2.1 | % | | | 21.68 | | | 23.82 | | | 3,571 |

2008 | | 53 | | 294,721 | | 3.7 | % | | | 5,825 | | 3.8 | % | | | 19.76 | | | 21.26 | | | 6,265 |

2009 | | 71 | | 506,940 | | 6.3 | % | | | 11,770 | | 7.6 | % | | | 23.22 | | | 25.69 | | | 13,024 |

2010 | | 71 | | 1,016,795 | | 12.6 | % | | | 22,086 | | 14.3 | % | | | 21.72 | | | 21.27 | | | 21,626 |

2011 | | 43 | | 1,201,911 | | 14.9 | % | | | 25,140 | | 16.2 | % | | | 20.92 | | | 23.76 | | | 28,553 |

2012 | | 11 | | 134,748 | | 1.7 | % | | | 2,655 | | 1.7 | % | | | 19.70 | | | 23.01 | | | 3,100 |

2013 | | 20 | | 705,167 | | 8.8 | % | | | 11,494 | | 7.4 | % | | | 16.30 | | | 19.50 | | | 13,751 |

2014 | | 22 | | 546,019 | | 6.8 | % | | | 9,446 | | 6.1 | % | | | 17.30 | | | 21.99 | | | 12,005 |

2015 | | 38 | | 1,414,282 | | 17.6 | % | | | 32,434 | | 20.9 | % | | | 22.93 | | | 31.59 | | | 44,680 |

Thereafter | | 31 | | 1,355,912 | | 16.8 | % | | | 27,275 | | 17.6 | % | | | 20.12 | | | 29.71 | | | 40,281 |

| | | | | | | | | | | | | | | | | | | | | | |

Portfolio Total / Weighted Average | | 459 | | 8,051,212 | | 100.0 | % | | $ | 154,979 | | 100.0 | % | | $ | 20.51 | | $ | 25.26 | | $ | 190,866 |

| | | | | | | | | | | | | | | | | | | | | | |

19

Lease Distribution

As of December 31, 2005

| | | | | | | | | | | | | | | | |

Square Feet Under Lease | | Number of

Leases | | Percentage

of All Leases | | | Total Net

Rentable

Square Feet | | Percentage of

Net Rentable

Square Feet | | | Annualized

Rent ($000) | | Percentage of

Annualized

Rent | |

Available | | | | | | | 494,232 | | 6.1 | % | | $ | — | | 0.0 | % |

2,500 or less | | 235 | | 51.2 | % | | 128,648 | | 1.6 | % | | | 5,070 | | 3.3 | % |

2,501 - 10,000 | | 90 | | 19.6 | % | | 479,993 | | 6.1 | % | | | 12,229 | | 7.9 | % |

10,001 - 20,000 | | 44 | | 9.6 | % | | 647,115 | | 8.0 | % | | | 13,730 | | 8.9 | % |

20,001 - 40,000 | | 37 | | 8.0 | % | | 1,006,201 | | 12.5 | % | | | 15,647 | | 10.1 | % |

40,001 - 100,000 | | 33 | | 7.2 | % | | 2,151,155 | | 26.7 | % | | | 47,421 | | 30.6 | % |

Greater than 100,000 | | 20 | | 4.4 | % | | 3,143,868 | | 39.0 | % | | | 60,882 | | 39.2 | % |

| | | | | | | | | | | | | | | | |

Portfolio Total | | 459 | | 100.0 | % | | 8,051,212 | | 100.0 | % | | $ | 154,979 | | 100.0 | % |

| | | | | | | | | | | | | | | | |

20

Leasing Activity

As of December 31, 2005

| | | | | | | |

| | | For the

Three Months

Ended

December 31,

2005 | | | % Leased | |

Occupied Square Feet as of September 30, 2005 | | 7,326,431 | | | | 93.2 | % |

Q4 2005 Acquisitions: | | | | | | | |

7500 & 7520 Metro Center Drive | | 45,000 | | | | | |

Chemin de l’Epinglier 2 | | 59,190 | | | | | |

3 Corporate Place | | — | | | | | |

251 Exchange Place | | 70,982 | | | | | |

115 Second Avenue | | — | | | | | |

| | | | | | | |

Occupied Square Feet including Q4 2005 Acquisitions | | 7,501,603 | | | | 93.2 | % |

Expirations | | (1,680 | ) | | | 0.0 | % |

New Leases | | 41,784 | | | | 0.5 | % |

Renewals | | 8,086 | | | | 0.1 | % |

Expansions/Remeasurements (1) | | 7,187 | | | | 0.1 | % |

Terminations | | — | | | | 0.0 | % |

| | | | | | | |

Occupied Square Feet as of December 31, 2005 | | 7,556,980 | | | | 93.9 | % |

| | | | | | | |

Cash Rent Growth (2) | | | | | | | |

Expiring Rate per Square Foot | | | | | $ | 18.99 | |

New / Renewed Rate per Square Foot | | | | | $ | 35.08 | |

Percentage Increase | | | | | | 84.9 | % |

GAAP Rent Growth (3) | | | | | | | |

Expiring Rate per Square Foot | | | | | $ | 24.50 | |

New / Renewed Rate per Square Foot | | | | | $ | 38.12 | |

Percentage Increase | | | | | | 55.6 | % |

Weighted Average Lease Term - New (in months) | | | | | | 104 | |

Weighted Average Lease Term - Renewal (in months) | | | | | | 43 | |

| (1) | Represents remeasuring of building to BOMA standards. |

| (2) | Represents the difference between (i) initial contractual rents on new and renewed leases and (ii) the cash rents on expiring leases immediately prior to the expiration or termination. |

| (3) | Represents estimated cash rent growth adjusted for straight-line rents in accordance with GAAP. |

21

Tenant Improvements and Leasing Commissions

As of December 31, 2005

| | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended | | Full Year |

| | | 12/31/2005 | | 9/30/2005 | | 6/30/2005 | | 3/31/2005 | | 2005 | | 2004 | | 2003 |

Renewals (1) | | | | | | | | | | | | | | | | | | | | | |

Number of renewals | | | 2 | | | 3 | | | 1 | | | 3 | | | 9 | | | 4 | | | 10 |

Square Feet | | | 8,086 | | | 8,109 | | | 4,517 | | | 12,295 | | | 33,007 | | | 19,079 | | | 78,172 |

Tenant improvement costs per square foot (2) | | $ | 1.14 | | $ | 9.67 | | $ | 20.00 | | $ | 3.93 | | $ | 6.86 | | $ | 15.06 | | $ | 1.83 |

Leasing commission costs per square foot (2) | | | 2.61 | | | 2.48 | | | 6.24 | | | 9.11 | | | 5.50 | | | 6.78 | | | 6.09 |

Total tenant improvement and leasing commission costs per square foot | | $ | 3.75 | | $ | 12.15 | | $ | 26.24 | | $ | 13.04 | | $ | 12.36 | | $ | 21.84 | | $ | 7.92 |

New Leases (3) | | | | | | | | | | | | | | | | | | | | | |

Number of leases | | | 16 | | | 23 | | | 18 | | | 6 | | | 63 | | | 34 | | | 18 |

Square Feet | | | 41,784 | | | 8,410 | | | 41,967 | | | 15,762 | | | 107,923 | | | 220,868 | | | 229,211 |

Tenant improvement costs per square foot (2) | | $ | 10.37 | | $ | 32.86 | | $ | 5.10 | | $ | 13.01 | | $ | 10.46 | | $ | 14.55 | | $ | 2.27 |

Leasing commission costs per square foot (2) | | | 26.28 | | | 21.38 | | | 8.58 | | | 4.54 | | | 15.84 | | | 10.08 | | | 12.55 |

Total tenant improvement and leasing commission costs per square foot | | $ | 36.65 | | $ | 54.24 | | $ | 13.68 | | $ | 17.55 | | $ | 26.30 | | $ | 24.63 | | $ | 14.82 |

Total (4) | | | | | | | | | | | | | | | | | | | | | |

Number of leases/renewals | | | 18 | | | 26 | | | 19 | | | 9 | | | 72 | | | 38 | | | 28 |

Square Feet | | | 49,870 | | | 16,519 | | | 46,484 | | | 28,057 | | | 140,930 | | | 239,947 | | | 307,383 |

Tenant improvement costs per square foot (2) | | $ | 8.87 | | $ | 21.47 | | $ | 6.55 | | $ | 9.03 | | $ | 9.62 | | $ | 14.59 | | $ | 2.16 |

Leasing commission costs per square foot (2) | | | 22.44 | | | 12.10 | | | 8.35 | | | 6.54 | | | 13.42 | | | 9.82 | | | 10.91 |

Total tenant improvement and leasing commission costs per square foot | | $ | 31.31 | | $ | 33.58 | | $ | 14.90 | | $ | 15.57 | | $ | 23.04 | | $ | 24.41 | | $ | 13.07 |

| (1) | Does not include retained tenants that have relocated to new space or expanded into new space. |

| (2) | Assumes all tenant improvement and leasing commissions are paid in the calendar year in which the lease commences, which may be different than the year in which they are actually paid. |

| (3) | Includes retained tenants that have relocated to new space or expanded into new space within our portfolio. |

| (4) | We recently acquired most of our properties which may make a period over period comparison difficult. For a list of the acquisition dates of our properties see page 17. |

22

Historical Capital Expenditures

As of December 31, 2005

| | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended | | Full Year |

| | | 12/31/2005 | | 9/30/2005 | | 6/30/2005 | | 3/31/2005 | | 2005 | | 2004 | | 2003 |

Recurring capital expenditures (1) (2) | | $ | 1,167,052 | | $ | 240,025 | | $ | 91,049 | | $ | 266,974 | | $ | 1,765,100 | | $ | 711,998 | | $ | 388,636 |

Non-recurring capital expenditures (2) | | $ | 1,689,757 | | $ | 1,766,579 | | $ | 1,604,007 | | $ | 1,352,219 | | $ | 6,412,562 | | $ | 2,168,837 | | $ | 765,587 |

Total net rentable square feet at period end | | | 8,051,212 | | | 7,864,760 | | | 7,791,110 | | | 6,303,226 | | | 8,051,212 | | | 5,652,700 | | | 2,792,266 |

Recurring capital expenditures per square foot | | $ | 0.14 | | $ | 0.03 | | $ | 0.01 | | $ | 0.04 | | $ | 0.22 | | $ | 0.13 | | $ | 0.14 |

Non-recurring capital expenditures per square foot | | $ | 0.21 | | $ | 0.22 | | $ | 0.21 | | $ | 0.21 | | $ | 0.80 | | $ | 0.38 | | $ | 0.27 |

| (1) | Recurring capital expenditures represents non-incremental building improvements required to maintain current revenues. Recurring capital expenditures do not include acquisition capital that was taken into consideration when underwriting the purchase of a building or which are incurred to bring a building up to “operating standard”. |

| (2) | We have acquired several properties in the past which may make a period over period comparison difficult. For a list of the acquisition dates of our properties see page 17. |

23

Properties rename

As of December 31, 2005

In the final quarter of 2005 we renamed our properties based on the address of each building. This table shows the names of buildings at December 31, 2005 and the names of those buildings in previous supplemental information disclosures.

| | |

Former name used in prior supplemental information

presentations. | | New name |

100 Technology Center Drive | | 100 Technology Center Drive |

1100 Space Park Drive | | 1100 Space Park Drive |

200 Paul Avenue | | 200 Paul Avenue 1-4 |

36 Northeast Second Street | | 36 NE 2nd Street |

833 Chestnut Street | | 833 Chestnut Street |

AboveNet Data Center | | 150 South First Street |

Ameriquest | | 8534 Concord Center Drive |

Amsterdam Data Center | | Paul van Vlissingenstraat 16 |

Ardenwood Corporate Park | | 34551 Ardenwood Boulevard 1-4 |

ASM Lithography Training Facility | | 2010 East Centennial Circle |

AT&T Web Hosting Facility | | 375 Riverside Parkway |

Brea Data Center | | 3300 East Birch Street |

Burbank Data Center | | 3015 Winona Avenue |

Camperdown House | | 6 Braham Street |

Carrier Center | | 600 West Seventh Street |

Charlotte 1 | | 731 East Trade Street |

Charlotte 2 | | 113 North Myers |

Charlotte 3 | | 125 North Myers |

Comverse Technology Building | | 100 & 200 Quannapowitt Parkway |

eBay Data Center | | 3065 Gold Camp Drive |

Granite Tower | | 4055 Valley View Lane |

Hudson Corporate Center | | 300 Boulevard East |

Lakeside Technology Center | | 350 East Cermak Road |

MAPP Building | | 1125 Energy Park Drive |

Maxtor Manufacturing Facility | | 47700 Kato Road & 1055 Page Avenue |

NTT/Verio Premier Data Center | | 2334 Lundy Place |

Printers’ Square | | 600-780 S. Federal |

Savvis Data Center 1 | | 2045 & 2055 LaFayette Street |

Savvis Data Center 2 | | 2401 Walsh Street |

Savvis Data Center 3 | | 200 North Nash Street |

Savvis Data Center 4 | | 2403 Walsh Street |

Savvis Data Center 5 | | 4700 Old Ironsides Drive |

Savvis Office Building | | 4605 Old Ironsides Drive |

Siemens Building | | 4849 Alpha Road |

Stanford Place II | | 7979 East Tufts Avenue |

Univision Tower | | 2323 Bryan Street |

VarTec Building | | 2440 Marsh Lane |

Webb at LBJ | | 11830 Webb Chapel Road |

24

MANAGEMENT STATEMENTS ON NON-GAAP SUPPLEMENTAL MEASURES

Funds from Operations:

We calculate Funds from Operations, or FFO, in accordance with the standards established by the National Association of Real Estate Investment Trusts, or NAREIT. FFO represents net income (loss) (computed in accordance with GAAP), excluding gains (or losses) from sales of property, real estate related depreciation and amortization (excluding amortization of deferred financing costs) and after adjustments for unconsolidated partnerships and joint ventures. Management uses FFO as a supplemental performance measure because, in excluding real estate related depreciation and amortization and gains and losses from property dispositions, it provides a performance measure that, when compared year over year, captures trends in occupancy rates, rental rates and operating costs. We also believe that, as a widely recognized measure of the performance of REITs, FFO will be used by investors as a basis to compare our operating performance with that of other REITs. However, because FFO excludes depreciation and amortization and captures neither the changes in the value of our properties that result from use or market conditions, nor the level of capital expenditures and leasing commissions necessary to maintain the operating performance of our properties, all of which have real economic effect and could materially impact our results from operations, the utility of FFO as a measure of our performance is limited. Other REITs may not calculate FFO in accordance with the NAREIT definition and, accordingly, our FFO may not be comparable to such other REITs’ FFO. Accordingly, FFO should be considered only as a supplement to net income as a measure of our performance.

Adjusted Funds From Operations:

We present adjusted funds from operations, or AFFO, as a supplemental operating measure because, when compared year over year, it assesses our ability to fund dividend and distribution requirements from our operating activities. We also believe that, as a widely recognized measure of the operations of REITs, AFFO will be used by investors as a basis to assess our ability to fund dividend payments in comparison to other REITs. We calculate adjusted funds from operations, or AFFO, by adding to or subtracting from FFO (i) non-real estate depreciation, (ii) amortization of deferred financing costs (iii) noncash compensation (iv) loss from early extinguishment of debt (v) straight line rents (vi) fair value of lease revenue amortization (vii) capitalized leasing payroll (viii) recurring tenant improvements and (ix) capitalized leasing commissions. Other equity REITs may not calculate AFFO in a consistent manner. Accordingly, our AFFO may not be comparable to other equity REITs’ AFFO. AFFO should be considered only as a supplement to net income computed in accordance with GAAP as a measure of our operations.

EBITDA and Adjusted EBITDA:

We believe that earnings before interest, income taxes, depreciation and amortization, or EBITDA and Adjusted EBITDA (as defined below), are useful supplemental performance measures because they allow investors to view our performance without the impact or noncash depreciation and amortization or the cost of debt and with respect to Adjusted EBITDA preferred dividends and minority interests. Adjusted EBITDA is EBITDA excluding minority interests and preferred stock dividends. In addition, we believe EBITDA and adjusted EBITDA are frequently used by securities analysts, investors and other interested parties in the evaluation of REITs. Because EBITDA and adjusted EBITDA are calculated before recurring cash charges including interest expense and income taxes, and are not adjusted for capital expenditures or other recurring cash requirements of our business, their utility as a measure of our performance is limited. Accordingly, EBITDA and Adjusted EBITDA should be considered only as supplements to net income (computed in accordance with GAAP) as a measure of our financial performance. Other equity REITs may calculate EBITDA and Adjusted EBITDA differently than we do; accordingly, our EBITDA and Adjusted EBITDA may not comparable to such other REITs’ EBITDA and Adjusted EBITDA.

25