Use these links to rapidly review the document

TABLE OF CONTENTS

INDEX TO FINANCIAL STATEMENTS

As filed with the Securities and Exchange Commission on October 25, 2004

Registration No. 333-118675

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

Amendment No. 1

to

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

Medical Device Manufacturing, Inc.

(Exact name of registrant as specified in its charter)

| Colorado (State or other jurisdiction of incorporation or organization) | 3841 (Primary Standard Industrial Classification Code Number) | 91-2054669 (I.R.S. Employer Identification Number) |

200 West 7th Avenue

Collegeville, PA 19426-0992

(610) 489-0300

(Name, address, including zip code, and telephone number, including

area code, of registrant's principal executive offices)

Ron Sparks

President and Chief Executive Officer

200 West 7th Avenue

Collegeville, PA 19426-0992

(610) 489-0300

(Name, address, including zip code, and telephone number, including

area code, of agent for service)

With copies to:

Christopher J. Walsh, Esq.

Scott A. Berdan, Esq.

Hogan & Hartson L.L.P.

1200 Seventeenth Street, Suite 1500

Denver, CO 80202

(303) 899-7300

Approximate Date Of Commencement Of Proposed Sale To The Public:

As soon as practicable after the effective date of this Registration Statement.

If the securities being registered on this Form are to be offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment that specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF ADDITIONAL REGISTRANTS

| Exact Name of Registrant as Specified in its Charter(1) | State of Incorporation or Organization | Primary Standard Industrial Classified Code Number | I.R.S. Employer Identification Number | |||

|---|---|---|---|---|---|---|

| MedSource Technologies, Inc. | Delaware | 3841 | 52-2094496 | |||

| Noble-Met, Ltd. | Virginia | 3499 | 54-1480585 | |||

| UTI Corporation | Pennsylvania | 3317 | 23-1721795 | |||

| Spectrum Manufacturing, Inc. | Nevada | 3841 | 36-2997517 | |||

| American Technical Molding, Inc. | California | 3082 | 99-0266738 | |||

| UTI Holding Company | Delaware | 6719 | 51-0407158 | |||

| Micro-Guide, Inc. | California | 3496 | 95-1866997 | |||

| Venusa, Ltd. | New York | 3841 | 13-3029017 | |||

| MedSource Technologies, LLC | Delaware | 6719 | 41-1934170 | |||

| Brimfield Acquisition Corp. | Delaware | 3814 | 51-0386457 | |||

| Brimfield Precision LLC | Delaware | 6719 | 04-3457459 | |||

| Kelco Acquisition, LLC | Delaware | 3499 | 52-2139676 | |||

| Hayden Precision Industries, LLC | Delaware | 3841 | 16-1564447 | |||

| Portlyn, LLC | Delaware | 3841 | 02-0506852 | |||

| The Microspring Company, LLC | Delaware | 3841 | 04-3459102 | |||

| Tenax, LLC | Delaware | 3841 | 06-1567572 | |||

| Thermat Acquisition Corp. | Delaware | 3841 | 52-2235950 | |||

| MedSource Technologies Newton, Inc. | Delaware | 3841 | 41-1990432 | |||

| MedSource Technologies Pittsburgh, Inc. | Delaware | 3841 | 04-3710128 | |||

| MedSource Trenton, Inc. | Delaware | 3841 | 32-0000036 | |||

| National Wire & Stamping, Inc. | Colorado | 3841 | 84-0485552 | |||

| Cycam, Inc. | Pennsylvania | 3841 | 25-1567669 | |||

| ELX, Inc. | Pennsylvania | 3841 | 25-1711485 | |||

| Texcel, Inc. | Massachusetts | 3841 | 04-2973748 | |||

| G&D, Inc. | Colorado | 3496 | 84-0718817 |

- (1)

- The address and telephone number of each co-registrant's principal executive offices is 200 W. 7th Avenue, Collegeville, PA 19426, (610) 409-2225.

The information in this prospectus is not complete and may be changed. We may not complete the exchange offer and issue these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and we are not soliciting an offer to buy these securities in any state where the offer is not permitted.

SUBJECT TO COMPLETION, DATED OCTOBER 25, 2004

PROSPECTUS

$175,000,000

MEDICAL DEVICE MANUFACTURING, INC.

OFFER TO EXCHANGE ALL OF THE OUTSTANDING

SERIES A 10% SENIOR SUBORDINATED NOTES DUE 2012

FOR

SERIES B 10% SENIOR SUBORDINATED NOTES DUE 2012

THAT HAVE BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933

We are offering to exchange all of our outstanding Series A 10% senior subordinated notes due 2012, which we refer to as the old notes, for our registered Series B 10% senior subordinated notes due 2012, which we refer to as the exchange notes. We refer to the old notes and the exchange notes collectively as the notes. The terms of the exchange notes are substantially identical to the terms of the old notes to be exchanged, except that the exchange notes have been registered under the Securities Act of 1933, as amended, which we refer to as the Securities Act, and will thus not be entitled to registration rights and will not bear any legend restricting their transfer. The old notes are, and the exchange notes will be, jointly and severally, fully and unconditionally, guaranteed on a senior subordinated basis by each of our existing domestic subsidiaries and by all our future domestic subsidiaries that are not designated by us as unrestricted subsidiaries. The exchange notes and the guarantees rank junior to all of our and the applicable guarantors' existing and future senior indebtedness, including our new senior secured credit facility.

Material Terms of the Exchange Offer

- •

- The exchange offer will expire at .m., New York City time, on , 2004, unless extended.

- •

- All old notes that are validly tendered and not validly withdrawn will be exchanged.

- •

- You may withdraw tenders of old notes at any time prior to the expiration of the exchange offer.

- •

- If you fail to tender your old notes, you will continue to hold unregistered notes that you will not be able to transfer freely.

- •

- There is no established trading market for the exchange notes or the old notes. We do not intend to list the exchange notes on any securities exchange, and therefore no active public market is anticipated.

- •

- We will not receive any proceeds from the exchange offer.

Participating in this exchange offer involves risks. See "Risk Factors" beginning on page 16.

Any broker-dealer that holds old notes that were acquired by it for its own account as a result of market-making activities or other trading activities and who receives exchange notes pursuant to the exchange offer may be deemed to be an "underwriter" within the meaning of the Securities Act. Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an "underwriter" within the meaning of the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for old notes where such old notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We and the guarantors have agreed that, for a period of 180 days after the expiration date, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See "Plan of Distribution."

We are not making this exchange offer in any state or jurisdiction where it is not permitted.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2004.

Industry and market data used throughout this prospectus is based on independent industry publications, government publications, reports by market research firms and other published independent sources. Some data is also based on our good faith estimates, which are derived from our review of internal surveys and independent sources.

i

The following summary should be read in conjunction with, and is qualified in its entirety by, the more detailed information and financial statements (including the accompanying notes) appearing elsewhere in this prospectus. We encourage you to read this entire document, including "Risk Factors," and the documents to which we refer you before making an investment in the exchange notes.

Overview

On April 27, 2004, we entered into an Agreement and Plan of Merger pursuant to which, on June 30, 2004, we acquired MedSource by merging it with our wholly owned subsidiary, Pine Merger Corporation, a Delaware corporation, which merger resulted in MedSource and its subsidiaries becoming our wholly owned subsidiaries. As a result of our completion of the MedSource acquisition, we believe we are the largest provider of outsourced precision manufacturing and engineering services in our target markets of the medical device industry. We are focused on the leading companies in the medical device industry in the cardiovascular, endoscopy and orthopedic end markets. We offer our customers design and engineering, precision component manufacturing, device assembly and supply chain management services. We have extensive resources focused on providing our customers reliable, high quality, cost-efficient, integrated outsourced solutions. We often become the sole supplier of manufacturing and engineering services for the products we provide to our customers.

Our design and engineering, precision component manufacturing, device assembly and supply chain management services provide multiple strategic benefits to our customers. We help speed our customers' products to market, lower their manufacturing costs and enable our customers to focus on their core competencies, including research, sales and marketing.

We have developed long-term relationships with our largest customers and work closely with our customers in the design, testing, prototyping and production of their products. Many of the end products we produce for our customers are regulated by the U.S. Food & Drug Administration, or the FDA, which has stringent quality standards for manufacturers of medical devices.

We generate a recurring revenue base from a diverse range of products used in a number of cardiovascular, endoscopic and orthopedic applications. The majority of our net sales come from products we consider high value, single use products. These products are either regulated for single use, implanted into the body or considered too critical to be re-used. Our revenue base has grown through a combination of our customers' end market growth and their increased outsourcing of products to us.

1

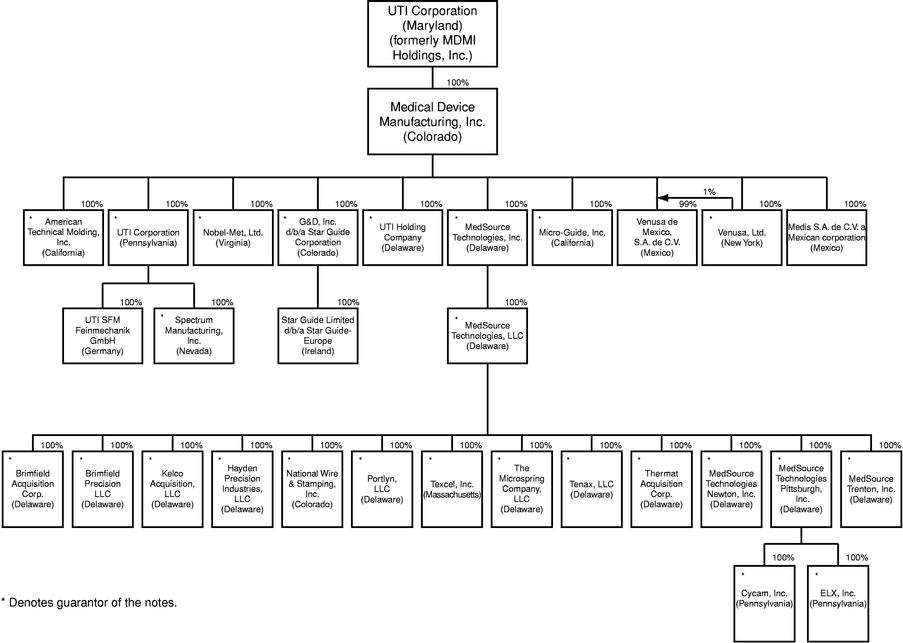

Our Organizational Structure

The following organizational chart shows the relationships among us, our parent, and our direct and indirect wholly owned subsidiaries, the jurisdictions of organization of each of which are shown parenthetically:

Industry Background

We believe our target market is represented by the amount of engineering and manufacturing services outsourced by the leading medical device companies to third-party manufacturers. Our target market is growing through a combination of growth in our customers' end markets and an increase in the amount of manufacturing and engineering services outsourced to third-party providers.

We believe that our targeted end markets are attractive based on their large size, growth, customer dynamics, competitive environment and need for high-quality engineering and manufacturing services. Based on published research reports from industry analysts such as Merrill Lynch Equity Research, Theta Reports and Frost & Sullivan, these end markets are projected to grow at 8%-13% per year from 2003 to 2008.

Many of the medical device companies in these end markets are increasingly utilizing third-party manufacturing and engineering providers as part of their business and manufacturing strategies. Medical device companies are choosing their strategic outsourcing partners based on the partner's ability to provide comprehensive precision manufacturing and engineering capabilities and deliver consistently high quality and highly reliable products at competitive prices. We believe medical device companies will continue to outsource manufacturing to third-party providers based on the: (1) desire of

2

medical device companies to accelerate time-to-market; (2) increasing complexity of manufacturing medical device products; (3) rationalization of medical device companies' existing manufacturing facilities; and (4) increasing focus by medical device companies on their core competencies of research, sales and marketing.

Competitive Strengths

Our competitive strengths make us a preferred strategic manufacturing partner for many of the leading medical device companies and position us for profitable growth. Our preferred provider status is evident through our long term customer relationships, sole source agreements and/or by official designation.

- •

- Market Leader. We believe we are the largest provider of outsourced precision manufacturing and engineering services in our target markets of the medical device industry, which enables us to invest significant resources in our infrastructure including manufacturing facilities, engineering expertise, proprietary processes and sales force.

- •

- Strong Relationships With Targeted Customers. We provide manufacturing and engineering services to the leading medical device companies worldwide in our targeted medical end markets of cardiology, endoscopy and orthopedics.

- •

- Preferred Supplier. We are the sole supplier of manufacturing and engineering services for a significant portion of the products we provide to our customers due to the high level of interaction necessary to design, develop and produce the high value medical devices on which we focus.

- •

- Breadth of Manufacturing and Engineering Capabilities. We provide a comprehensive range of manufacturing and engineering services, including design, testing, prototyping, production and device assembly, as well as global supply chain management services.

- •

- Strategic Locations. Our strategic locations allow us to facilitate speed to market, rapid prototyping, low cost assembly and overall customer familiarity.

- •

- Reputation for Quality. We believe our reputation and experience as a high quality manufacturer provide us with an advantage in winning new business as large medical device companies want to partner with a successful, proven manufacturer who has the systems and capabilities to ensure a high level of quality.

- •

- Experienced Management Team. We have a highly experienced management team at both the corporate and operational levels.

Business Strategy

Our objective is to grow profitably and strengthen our position as a leading provider of outsourced precision manufacturing and engineering services to the medical device industry through the following:

- •

- Increase Share Within Target Market Leaders. We are focused on increasing our share of revenues from the leading companies within our target markets.

- •

- Increase Manufacturing Efficiencies. We will continue to implement quality and manufacturing programs across all of our facilities to improve the cost structure of our manufacturing through the reduction of labor and overhead costs, tighter inventory controls and process improvement.

3

- •

- Expand Design and Prototyping Capabilities and Presence. We intend to grow revenues from design and prototyping services by continuing to invest in selected strategic locations. We believe being involved in the initial design and prototyping of medical devices positions us to capture the ongoing manufacturing business of these devices as they move to full production.

Investing in the notes involves risks. You should carefully consider the following risk factors and refer to the section captioned "Risk Factors" for an explanation of the material risks of participating in the exchange offer and investing in the notes. Specific factors that might cause actual results to differ from our expectations and that may affect our ability to pay timely amounts due under the notes or that may affect the value of the notes include, but are not limited to:

- •

- failure to successfully integrate MedSource or any future acquisition into our operations;

- •

- failure to realize the anticipated synergies from the MedSource acquisition;

- •

- our dependence on a few large customers for a significant portion of our revenue;

- •

- failure to continue to maintain or grow our business or successfully expand into new markets and products;

- •

- our obligations under our new senior secured credit facility and the notes;

- •

- downward fluctuations in our operating results, which could lead to an inadequacy of our cash flow to meet our operational and debt service requirements;

- •

- competitive pressures from our existing and potential competitors;

- •

- the unpredictable product cycles of the medical device manufacturing industry and uncertain demand for our manufacturing capabilities;

- •

- adverse trends or political, economic and regulatory changes affecting the medical device industry or our customers;

- •

- inability to recruit and retain experienced engineers and management personnel;

- •

- product liability claims and liability resulting from uninsured injury or death occurring at our facilities;

- •

- quality problems with our processes, products and services;

- •

- decreasing prices for our products or failure to reduce our expenses;

- •

- failure to respond to changes in technology and obsolescence of our manufacturing processes;

- •

- inability to protect our intellectual property and defend against infringement claims by third parties;

- •

- risks associated with our international operations;

- •

- our dependence on outside suppliers and subcontractors;

- •

- failure to obtain sufficient quantities of raw materials;

- •

- inability to access additional capital;

- •

- dependence on earnings of our operating subsidiaries and distributions of such earnings to us;

- •

- significant costs of compliance with, and liability from failure to comply with, environmental laws;

4

- •

- adverse determinations in lawsuits to which we are a party or legal or regulatory actions;

- •

- risks associated with the implementation of our new third-party enterprise resource planning system;

- •

- dependence on senior management;

- •

- inability to generate the cash needed to service our lease and debt obligations;

- •

- inability to restructure or refinance our leases or indebtedness if we are not able to meet our obligations under our leases and indebtedness;

- •

- inability to obtain all the funds necessary to purchase the notes upon a change of control;

- •

- fraudulent transfer statutes which may limit noteholders rights;

- •

- inability to develop an active trading market for the notes;

- •

- significant operating and financial restrictions imposed by our new senior secured credit facility and the indenture for the notes; and

- •

- other factors discussed under "Risk Factors" or elsewhere in this prospectus.

On April 27, 2004, we entered into an Agreement and Plan of Merger pursuant to which, on June 30, 2004, we acquired MedSource by merging it with our wholly owned subsidiary, Pine Merger Corporation, a Delaware Corporation, which merger resulted in MedSource and its subsidiaries becoming our wholly owned subsidiaries. Upon the consummation of the MedSource acquisition, our parent, UTI Corporation, a Maryland corporation, repurchased its outstanding Class C Redeemable Preferred Stock and paid accrued dividends to its holders of Class A 5% Convertible Preferred Stock and Class C Redeemable Preferred Stock. We also completed payment of approximately $9.2 million in respect of an earn-out obligation entered into in connection with our acquisition of Venusa, Ltd. and Venusa de Mexico, S.A. de C.V., referred to in this prospectus collectively as Venusa, in February, 2003.

We financed the foregoing transactions primarily with the proceeds from the issuance on June 30, 2004 of the notes, our new six-year $194.0 million senior secured term loan facility borrowed under our new senior secured credit facility, which also includes a five-year $40.0 million senior secured revolving credit facility, which was undrawn at the closing of the transactions consummated on June 30, 2004, and an $89.8 million equity investment in UTI by the DLJ Merchant Banking Buyers. See "The Transactions" elsewhere in this prospectus.

5

Founded in 1996, KRG Capital Partners, LLC, or KRG, is a Denver, Colorado based private equity firm that currently manages over $860 million of committed equity capital and equity co-investments. KRG specializes in acquiring and recapitalizing unique and profitable middle-market companies. The firm seeks investment opportunities with owners and operating managers who are committed to expanding their companies and becoming, industry leaders through a combination of internal growth and complementary add-on acquisitions. KRG initiated its involvement with UTI in 1999 and, together with its co-investors, provided the equity capital to support UTI's growth to date.

The DLJ Merchant Banking Buyers are part of DLJ Merchant Banking, a leading private equity investor that has a 19-year record of investing in leveraged buyouts and related transactions across a broad range of industries. DLJ Merchant Banking, with offices in New York, London, Houston and Buenos Aires, is part of Credit Suisse First Boston's Alternative Capital Division, which is one of the largest alternative asset managers in the world with more than $36 billion of assets under management. The Alternative Capital Division is comprised of $20 billion of private equity assets under management across a diverse family of funds, including leveraged buyout funds, mezzanine funds, real estate funds, venture capital funds, fund of funds and secondary funds, as well as more than $16 billion of assets under management through its hedge fund (both direct and fund of funds), leveraged loan and CDO businesses. Certain affiliates of the DLJ Merchant Banking Buyers initiated their involvement in UTI in 2000 and provided a combination of equity and debt financing to help support UTI's growth to date.

We were incorporated under the laws of the State of Colorado in May 2000 and became a wholly owned subsidiary of UTI Corporation, a Maryland Corporation (formerly known as MDMI Holdings, Inc.). MDMI Holdings, Inc. was organized in Colorado in July 1999 and conducted its own business and operations. Prior to our formation, MDMI Holdings, Inc. acquired our current wholly owned subsidiaries G&D Inc. d/b/a Star Guide and Noble-Met, Ltd. On the date of our formation, MDMI Holdings, Inc. became the first-tier holding company in our organizational structure. On February 23, 2001, MDMI Holdings, Inc. reincorporated by merger in Maryland and changed its name to UTI Corporation, which is today our parent and the first-tier holding company in our organizational structure. We maintain our principal executive offices at 200 West 7th Avenue, Collegeville, Pennsylvania 19426, and our telephone number is (610) 489-0300.

Unless the context indicates otherwise, (1) the terms the "Company," "MDMI," "we," "our" and "us" refer to Medical Device Manufacturing, Inc. and its subsidiaries, (2) the term "UTI" refers to our parent company and sole stockholder, UTI Corporation, a Maryland corporation formerly known as MDMI Holdings, Inc., (3) the term "MedSource" refers to MedSource Technologies, Inc., a Delaware corporation, and (4) the "DLJ Merchant Banking Buyers" refers to DLJ Merchant Banking Partners III, L.P., DLJ Offshore Partners III-1, C.V., DLJ Offshore Partners III-2, C.V., DLJ Offshore Partners III, C.V., DLJ MB Partners III GmbH & Co. KG, Millennium Partners II, L.P. and MBP III Plan Investors, L.P. Unless the context indicates otherwise, "on a pro forma basis" or "pro forma" means after giving effect to the transactions described under "The Transactions."

6

Summary of the Terms of the Exchange Offer

| Issue | $1,000 principal amount of exchange notes will be issued in exchange for each $1,000 principal amount of old notes validly tendered. | |||

Resale | Based upon interpretations by the staff of the Securities and Exchange Commission, or the SEC, set forth in no-action letters of Exxon Capital Holdings Corporation (available April 13, 1988), Morgan Stanley & Co. Incorporated (available June 5, 1991) and Shearman & Sterling (available July 2, 1993), we believe that exchange notes may be offered for resale, resold or otherwise transferred by you without compliance with the registration and prospectus delivery requirements of the Securities Act, unless you: | |||

• | are an "affiliate" of ours or any of the guarantors within the meaning of Rule 405 under the Securities Act; | |||

• | are a broker-dealer who purchased the old notes directly from us for resale under Rule 144A or any other available exemption under the Securities Act; | |||

• | acquired the exchange notes other than in the ordinary course of your business; or | |||

• | have an arrangement or understanding with any person to participate in the distribution of the notes within the meaning of the Securities Act. | |||

We have not submitted a no-action letter, however, and there can be no assurance that the SEC will make a similar determination with respect to the exchange offer. Furthermore, in order to participate in the exchange offer, you must make the representations set forth in the letter of transmittal that we are sending you with this prospectus. | ||||

Expiration Date | The exchange offer will expire at .m., New York City time, on , 2004, unless we in our sole discretion, extend it. We refer to this date, as it may be extended, as the expiration date. | |||

Conditions to the Exchange Offer | The exchange offer is subject to certain customary conditions, some of which may be waived by us. See "The Exchange Offer—Conditions to the Exchange Offer." | |||

7

Procedure for Tendering Old Notes | If you wish to accept the exchange offer, you must complete, sign and date the letter of transmittal, or a copy of the letter of transmittal, in accordance with the instructions contained in this prospectus and in the letter of transmittal, and mail or otherwise deliver the letter of transmittal, or the copy, together with the old notes and any other required documentation, to the exchange agent at the address set forth in this prospectus. If you are a person holding the old notes through The Depository Trust Company and wish to accept the exchange offer, you must do so through The Depository Trust Company's Automated Tender Offer Program, by which you will agree to be bound by the letter of transmittal. By executing or agreeing to be bound by the letter of transmittal, you will be making a number of important representations to us as described under "The Exchange Offer—Purpose and Effect." | |||

We will accept for exchange any and all old notes that are properly tendered in the exchange offer prior to the expiration date. The exchange notes issued in the exchange offer will be delivered promptly following the expiration date. See "The Exchange Offer—Terms of the Exchange Offer." | ||||

Special Procedures for Beneficial Owners | If you are the beneficial owner of old notes registered in the name of a broker, dealer, commercial bank, trust company or other nominee and wish to tender in the exchange offer, you should contact the person in whose name your notes are registered and promptly instruct the person to tender on your behalf. | |||

Guaranteed Delivery Procedures | If you wish to tender your old notes and time will not permit your required documents to reach the exchange agent by the expiration date, or the procedure for book-entry transfer cannot be completed on time, you may tender your old notes according to the guaranteed delivery procedures. For additional information, you should read the discussion under "Exchange Offer—Guaranteed Delivery Procedures." | |||

Withdrawal Rights | The tender of the old notes pursuant to the exchange offer may be withdrawn at any time prior to the expiration date. | |||

8

Acceptance of Old Notes and Delivery of Exchange Notes | Subject to customary conditions, we will accept old notes that are properly tendered in the exchange offer and not withdrawn prior to the expiration date. The exchange notes will be delivered as promptly as practicable following the expiration date. | |||

Consequence of Failure to Exchange | Old notes that are not tendered, or that are tendered but not accepted, will be subject to their existing transfer restrictions. In general, the old notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. The liquidity for and market price of the old notes could be adversely affected upon consummation of the exchange offer because the aggregate principal amount of the old notes outstanding will be reduced by the aggregate principal amount of old notes exchanged in the exchange offer, thereby potentially reducing the market in the old notes. Unless we are required by the registration rights agreements to file a "shelf" registration statement, generally we will have no further obligation to provide for registration under the Securities Act of such old notes. | |||

Registration Rights Agreement; Effect on Holders | We sold the old notes in a private placement in reliance on Section 4(2) of the Securities Act. The old notes were immediately resold by the initial purchasers in reliance on Rule 144A and Regulation S under the Securities Act. On June 30, 2004, we entered into a registration rights agreement with the initial purchasers of the old notes requiring us to make this exchange offer. The registration rights agreement also requires us to: | |||

• | use our best efforts to cause the registration statement filed with respect to the exchange offer to be declared effective by March 27, 2005; and | |||

• | consummate the exchange offer no later than 30 business days after the registration statement has been declared effective. | |||

See "The Exchange Offer—Purpose and Effect." If we do not do so, liquidated damages will be payable on the old notes. | ||||

9

Material United States Federal Income Tax Consequences | The exchange of old notes for exchange notes by tendering holders will not be a taxable exchange for federal income tax purposes, and such holders will not recognize any taxable gain or loss or any interest income for federal income tax purposes as a result of such exchange. See "Material United States Federal Income Tax Consequences." | |||

Exchange Agent | U.S. Bank National Association is serving as exchange agent in connection with the exchange offer. | |||

Use of Proceeds | We will not receive any proceeds from the exchange offer. | |||

Summary of the Terms of the Exchange Notes

The exchange offer relates to the exchange of up to $175.0 million principal amount of exchange notes for up to an equal principal amount of old notes. The form and terms of the exchange notes are substantially identical to the form and terms of the old notes, except the exchange notes will be registered under the Securities Act. Therefore, the exchange notes will not bear legends restricting their transfer. The exchange notes will evidence the same debt as the old notes (which they replace). The old notes and the exchange notes are governed by the same indenture. The summary below describes the principal terms of the exchange notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The "Description of Notes" section of this prospectus contains a more detailed description of the terms and conditions of the exchange notes.

| Issuer | Medical Device Manufacturing, Inc. | ||

Notes Offered | $175.0 million aggregate principal amount of Series B 10% senior subordinated notes due 2012. | ||

Maturity Date | July 15, 2012. | ||

Interest Rate and Payment Dates | The exchange notes will bear interest at the rate of 10% per year, payable in cash semi-annually, in arrears, on January 15 and July 15 of each year, commencing on January 15, 2005. Interest on the exchange notes will accrue from the last interest payment date on which interest was paid on the old notes surrendered for exchange therefor or, if no interest has been paid on the old notes, from the date of original issue of the old notes. | ||

Subsidiary Guarantees | The exchange notes will be jointly and severally, fully and unconditionally, guaranteed on a senior subordinated basis by all our existing domestic subsidiaries and by all our future domestic subsidiaries that are not designated by us as unrestricted subsidiaries. | ||

Ranking | The exchange notes and the guarantees will be our and the applicable guarantors' senior subordinated unsecured obligations and will be: | ||

• | junior in right of payment to all of our and such guarantors' existing and future senior indebtedness; | ||

10

• | equal in right of payment to all of our and such guarantors' existing and future senior subordinated indebtedness, including any old notes that are not exchanged in the exchange offer; and | ||

• | senior in right of payment to all of our and such guarantors' existing and future subordinated indebtedness. | ||

As of June 30, 2004, we and the subsidiary guarantors had outstanding an aggregate of approximately $194.0 million of indebtedness that was senior to the exchange notes. In addition, as of June 30, 2004, we and the subsidiary guarantors had the ability to incur up to $40.0 million of additional indebtedness under our revolving credit facility, which indebtedness, if incurred, would rank senior to the exchange notes. The old notes and the related subsidiary guarantees are our and the subsidiary guarantors only outstanding senior subordinated indebtedness. | |||

Optional Redemption | We may redeem the exchange notes, in whole or in part, on or after July 15, 2008, at the redemption prices set forth in this prospectus under the caption "Description of Notes—Optional Redemption." | ||

In addition, on or prior to July 15, 2007, we may redeem up to 35% of the aggregate principal amount of the exchange notes with the net proceeds of one or more qualified equity offerings. For more information, see "Description of Notes—Optional Redemption." | |||

Change of Control | If we experience a change of control, holders of the exchange notes will have the right to require us to repurchase the exchange notes at a purchase price of 101% of the principal amount of the exchange notes, plus accrued and unpaid interest to the date of the repurchase. See "Description of Notes—Repurchase at the Option of Holders." | ||

Restrictive Covenants | The indenture governing the exchange notes contains covenants that limit our and our subsidiaries' ability to, among other things: | ||

• | pay dividends, redeem capital stock and make other restricted payments and investments; | ||

• | incur additional debt or issue preferred stock; | ||

• | enter into agreements that restrict our subsidiaries from paying dividends or other distributions, making loans or otherwise transferring assets to us or to any other subsidiaries; | ||

• | create liens on assets; | ||

• | engage in transactions with affiliates; | ||

• | sell assets, including capital stock of subsidiaries; and | ||

• | merge, consolidate or sell all or substantially all of our assets and the assets of our subsidiaries. | ||

11

All of these limitations are subject to important exceptions and qualifications described under "Description of Notes—Certain Covenants." | |||

Registration Rights; Liquidated Damages | In connection with the offering of the old notes, we granted registration rights to holders of the old notes. We agreed to consummate an offer to exchange the old notes for the related series of exchange notes and to take other actions in connection with the exchange offer by the dates specified in the registration rights agreement. In addition, under certain circumstances, we may be required to file a shelf registration statement to cover resales of the old notes held by you. | ||

If we fail to take these actions with respect to the old notes by the dates specified in the registration rights agreement, we will pay liquidated damages to each holder of the old notes at a rate of 0.25% per annum with respect to the first 90-day period immediately following the occurrence of the first registration default. The rate of liquidated damages will increase by an additional 0.25% per annum with respect to each subsequent 90-day period until all registration defaults have been cured, up to a maximum liquidated damages rate of 1.0% per annum. Following the cure of all registration defaults, the accrual of liquidated damages will cease. | |||

Form of Exchange Notes | The exchange notes to be issued in the exchange offer will be represented by one or more global notes deposited with U.S. Bank National Association for the benefit of Depository Trust Company, or DTC. You will not receive exchange notes in certificated form unless one of the events set forth under the heading "Description of Notes—Form of Exchange Notes" occurs. Instead, beneficial interests in the exchange notes to be issued in the exchange offer will be shown on, and transfer of these interests will be effected only through, records maintained in book-entry form by DTC with respect to its participants. | ||

Absence of a Public Market for the Exchange Notes | The exchange notes are a new issue of securities for which there is currently no trading market. Although we expect the exchange notes to be eligible for trading in The PortalSM Market, a subsidiary of The Nasdaq Stock Market, Inc., referred to in this prospectus as The PORTAL Market, we cannot assure you that an active trading market for the exchange notes will develop or be sustained. The initial purchasers of the old notes advised us that they intended to make a market in the old notes after offering of such notes was completed. The initial purchasers of the old notes are not obligated, however, to make a market in the old notes or the exchange notes and any such market-making may be discontinued at any time at the sole discretion of the initial purchasers of the old notes. | ||

12

SUMMARY HISTORICAL AND PRO FORMA

CONDENSED CONSOLIDATED FINANCIAL DATA

The following table contains summary historical financial data for the twelve months ended December 31, 2003 and six months ended June 30, 2004 derived from our and MedSource's audited and unaudited consolidated financial statements included elsewhere in this prospectus and from MedSource's unaudited consolidated financial statements not included in this prospectus. The historical statement of operations data of MedSource have been adjusted from a June 30 fiscal year to a calendar year presentation to match our fiscal year end. We consummated the MedSource acquisition on June 30, 2004 and, as a result, the assets and liabilities of MedSource are recorded on our balance sheet as of the date of the MedSource acquisition and the results of operations of MedSource for June 30, 2004 are included in our results for that day. The table also contains summary unaudited pro forma financial data derived from the financial information set forth under "Unaudited Pro Forma Condensed Consolidated Financial Statements" included elsewhere in this prospectus. The unaudited pro forma condensed consolidated financial data do not purport to present our actual financial position or results of operations had the Transactions actually occurred on the date specified. The summary unaudited pro forma condensed consolidated statements of operations data for the twelve months ended December 31, 2003 and six months ended June 30, 2004 give effect to the Transactions as if they had occurred on January 1, 2003. The Transactions include:

- •

- the MedSource acquisition;

- •

- the payment of MedSource's indebtedness and accrued interest;

- •

- the payment of our old senior secured credit facility, our old senior subordinated indebtedness, UTI's senior indebtedness and accrued interest;

- •

- the payment of the Venusa earn-out;

- •

- the payment of dividends on UTI's Class A 5% Convertible Preferred Stock and Class C Redeemable Preferred Stock;

- •

- the repurchase of UTI's Class C Redeemable Preferred Stock;

- •

- the borrowings under our new senior secured credit facility;

- •

- the equity investment by the DLJ Merchant Banking Buyers in UTI;

- •

- the offering of the notes; and

- •

- the payment of fees and expenses related to the foregoing.

The summary pro forma data account for the MedSource acquisition using the purchase method of accounting, which requires that we adjust their assets and liabilities to their fair values. Such valuations are based upon available information and certain assumptions that we believe are reasonable. The total purchase price for the MedSource acquisition was allocated to our net assets based on preliminary estimates of fair value. The final purchase price allocation will be based on a formal valuation analysis and may include adjustments to the amounts shown here. A final valuation is in process. The result of the final allocation could be materially different from the preliminary allocation set forth in this prospectus.

You should read the summary historical and pro forma data set forth in the following table in conjunction with "The Transactions," "Capitalization," "Selected Historical Consolidated Financial Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations," the consolidated financial statements of MDMI and MedSource and the respective notes thereto, and the Unaudited Pro Forma Condensed Consolidated Financial Statements and the related notes thereto

13

included in this prospectus. In addition, future results may vary significantly from the results reflected in such statements due to certain factors beyond our control. See "Risk Factors."

We are a wholly owned subsidiary of UTI. UTI is a holding company with no operations and whose only asset is our capital stock. Proceeds from the issuance of indebtedness and sale of capital stock of UTI were used by us for acquisitions of subsidiaries. Accordingly, in compliance with provisions of Staff Accounting Bulletin 54 (Topic 5-J), the accompanying financial statements reflect the push down of UTI's indebtedness and related interest expense and UTI's equity. UTI allocates all interest and costs to us as all indebtedness has been pushed down. Management believes the methods of allocation are reasonable.

| | Historical | Pro Forma | Historical | Pro Forma | ||||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | MDMI | MedSource | | MDMI | MedSource | | ||||||||||||||

| | Twelve Months Ended December 31, 2003 | Twelve Months Ended December 28, 2003 | Twelve Months Ended December 31, 2003 | Six Months Ended June 30, 2004 | Interim Period Ended June 29, 2004 | Six Months Ended June 30, 2004 | ||||||||||||||

| | (dollars in thousands) | |||||||||||||||||||

| STATEMENT OF OPERATIONS DATA: | ||||||||||||||||||||

| Net Sales | $ | 174,223 | $ | 181,905 | $ | 353,692 | $ | 112,147 | $ | 94,301 | $ | 205,922 | ||||||||

| Gross Profit | 53,194 | 44,847 | 100,115 | 34,489 | 22,534 | 57,660 | ||||||||||||||

| Income (Loss) from Operations | 15,664 | (35,035 | ) | (18,771 | ) | 14,288 | 4,935 | 19,083 | ||||||||||||

| Net Loss | (14,804 | ) | (38,462 | ) | (61,894 | ) | (2,049 | ) | 3,445 | 3,526 | ||||||||||

| OTHER FINANCIAL DATA: | ||||||||||||||||||||

| Cash Flows Provided by (Used in) | ||||||||||||||||||||

| Operating Activities | $ | 14,392 | $ | 16,857 | $ | 5,081 | $ | 8,583 | ||||||||||||

| Investing Activities | (20,370 | ) | (10,349 | ) | (215,969 | ) | (4,320 | ) | ||||||||||||

| Financing Activities | 3,977 | (8,264 | ) | 219,074 | (3,683 | ) | ||||||||||||||

| Capital Expenditures | (6,371 | ) | (9,934 | ) | (16,305 | ) | (4,178 | ) | (4,757 | ) | (8,935 | ) | ||||||||

| Depreciation and Amortization | 11,591 | 9,672 | 20,263 | 6,003 | 4,411 | 10,354 | ||||||||||||||

| EBITDA(1) | 27,246 | (25,463 | ) | 1,383 | 17,026 | 9,431 | 29,552 | |||||||||||||

| | As of June 30, 2004 | ||

|---|---|---|---|

| | (in thousands) | ||

| BALANCE SHEET DATA: | |||

| Cash and Cash Equivalents | $ | 12,130 | |

| Total Assets | 600,531 | ||

| Total Debt | 369,035 | ||

| Redeemable and Convertible Preferred Stock | 60 | ||

| Stockholder's Equity | 141,617 | ||

- (1)

- We define EBITDA as net income (loss) before net interest expense, income tax expense, depreciation and amortization. Since EBITDA may not be calculated the same by all companies, this measure may not be comparable to similarly titled measures by other companies. We use EBITDA as a supplemental measure of our performance. EBITDA has limitations as an analytical tool, and you should not consider it in isolation, or as a substitute for analysis of our results as reported under GAAP. See "Non-GAAP Financial Measures" for a discussion of our use of EBITDA and certain limitations of EBITDA as a financial measure. EBITDA is calculated as follows for the periods presented:

| | Historical | Pro Forma | Historical | Pro Forma | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | MDMI | MedSource | | MDMI | MedSource | | |||||||||||||

| | Twelve Months Ended December 31, 2003 | Twelve Months Ended December 28, 2003 | Twelve Months Ended December 31, 2003 | Six Months Ended June 30, 2004 | Interim Period Ended June 29, 2004 | Six Months Ended June 30, 2004 | |||||||||||||

| | (dollars in thousands) | ||||||||||||||||||

| Net Income (Loss) | $ | (14,804 | ) | $ | (38,462 | ) | $ | (61,894 | ) | $ | (2,049 | ) | $ | 3,445 | $ | 3,526 | |||

| Interest Expense | 16,587 | 2,870 | 28,685 | 12,015 | 1,291 | 14,331 | |||||||||||||

| Income Tax Expense, net | 13,872 | 457 | 14,329 | 1,057 | 284 | 1,341 | |||||||||||||

| Depreciation and Amortization | 11,591 | 9,672 | 20,263 | 6,003 | 4,411 | 10,354 | |||||||||||||

| EBITDA | $ | 27,246 | $ | (25,463 | ) | $ | 1,383 | $ | 17,026 | $ | 9,431 | $ | 29,552 | ||||||

14

RATIO OF EARNINGS TO FIXED CHARGES

The following table sets forth our historical and pro forma ratios and deficiencies of earnings to fixed charges for the periods indicated and should be read in conjunction with "Selected Historical Consolidated Financial Data" included elsewhere in this prospectus ($ in thousands).

| | Period from Inception (July 2, 1999) to December 31, 1999 | | | | | | | | |||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | | | | | | Pro Forma | |||||||||||||||||

| | Twelve Months Ended December 31, | | |||||||||||||||||||||

| | Six Months Ended June 30, 2004 | Twelve Months Ended December 31, 2003 | Six Months Ended June 30, 2004 | ||||||||||||||||||||

| | 2000 | 2001 | 2002 | 2003 | |||||||||||||||||||

| Ratio of earnings to fixed charges | 1.5 | x | — | — | — | — | — | — | 1.3 | x | |||||||||||||

Deficiency of earnings to fixed charges | — | $ | 16,282 | $ | 8,502 | $ | 32,557 | $ | 932 | $ | 992 | $ | 47,565 | — | |||||||||

The following table sets forth our predecessor's historical ratios and deficiencies of earnings to fixed charges for the periods indicated and should be read in conjunction with "Selected Historical Consolidated Financial Data" included elsewhere in this prospectus ($ in thousands).

| | Twelve Months Ended December 31, 1999 | Five Months Ended May 31, 2000 | |||

|---|---|---|---|---|---|

| Ratio of earnings to fixed charges | 3.5x | — | |||

| Deficiency of earnings to fixed charges | — | $ | 16,840 | ||

15

An investment in the notes involves a high degree of risk. You should consider carefully the following risk factors, in addition to the other information set forth in this prospectus, before deciding to participate in the exchange offer. The factors set forth below, however, are generally applicable to the old notes as well as to the exchange notes.

Risks Related to Our Business

We may not successfully integrate MedSource or any subsequent acquisition target into our business and operations.

Prior to the consummation of the MedSource acquisition we and MedSource operated as separate entities. We may experience material negative consequences to our business, financial condition or results of operations if we cannot successfully integrate MedSource's operations with ours. The integration of companies that have previously been operated separately involves a number of risks, including, but not limited to:

- •

- demands on management related to the significant increase in the size of the business for which they are responsible;

- •

- diversion of management's attention from the management of daily operations to the integration of operations;

- •

- management of employee relations across facilities;

- •

- difficulties in the assimilation of different corporate cultures and practices, as well as in the assimilation and retention of broad and geographically dispersed personnel and operations;

- •

- difficulties and unanticipated expenses related to the integration of departments, systems (including accounting systems), technologies, books and records, procedures and controls (including internal accounting controls, procedures and policies), as well as in maintaining uniform standards, including environmental management systems;

- •

- expenses of any undisclosed or potential liabilities; and

- •

- ability to maintain our customers and MedSource's customers after the acquisition.

Successful integration of MedSource's operations with ours depends on our ability to manage the combined operations, to realize opportunities for revenue growth presented by broader product offerings and expanded geographic coverage and to eliminate redundant and excess costs. If our integration efforts are not successful, we may not be able to maintain the levels of revenues, earnings or operating efficiency that we and MedSource achieved or might achieve separately. In addition, the unaudited pro forma condensed consolidated financial data presented in this prospectus cover periods during which we were not under the same management and, therefore, may not be indicative of our future financial condition or operating results.

We will incur significant costs to achieve and may not be able to realize the anticipated savings, synergies or revenue enhancements from the MedSource acquisition.

Even if we are able to integrate successfully our operations with MedSource's operations, we may not be able to realize the cost savings, synergies or revenue enhancements that we anticipate from the integration, either in the amount or the time frame that we currently expect. Our ability to realize

16

anticipated cost savings, synergies and revenue enhancements may be affected by a number of factors, including, but not limited to:

- •

- our ability to effectively eliminate duplicative backoffice overhead and overlapping and redundant selling, general and administrative functions, rationalize manufacturing capacity and shift production to more economical facilities;

- •

- the anticipated utilization of cash resources on integration and implementation activities to achieve those cost savings, which could be greater than we currently expect and which could offset any such savings and other synergies resulting from the MedSource acquisition;

- •

- increases in other expenses, operating losses or problems unrelated to the MedSource acquisition, which may offset the cost savings and other synergies from the MedSource acquisition or divert resources intended to be used in the integration plan; and

- •

- our ability to avoid labor disruption in connection with the integration.

Because a significant portion of our net sales comes from a few large customers, any decrease in sales to these customers could harm our operating results.

The medical device industry is concentrated, with relatively few companies accounting for a large percentage of sales in the cardiology, endoscopy and orthopedic markets that we target. Accordingly, our net sales and profitability are highly dependent on our relationships with a limited number of large medical device companies. Pro forma for the twelve months ended December 31, 2003, our top 15 customers accounted for approximately 60% of our net sales. In particular, Johnson & Johnson and Boston Scientific each accounted for more than 10% of our net sales for the twelve months ended December 31, 2003 and six months ended June 30, 2004 on a pro forma basis. We are likely to continue to experience a high degree of customer concentration, particularly if there is further consolidation within the medical device industry. We cannot assure you that there will not be a loss or reduction in business from one or more of our major customers. For example, in 2002 we lost a start-up customer as a result of the customer's product not gaining market acceptance. In addition, we cannot assure you that net sales from customers that have accounted for significant net sales in the past, either individually or as a group, will reach or exceed historical levels in any future period. For example, Boston Scientific has recently informed us that it intends to transfer a number of products currently assembled by us to its own assembly operation in 2005 and the first half of 2006. For a detailed discussion of the Boston Scientific relationship, see "Management's Discussion and Analysis of Financial Condition and Results of Operations—Overview." The loss or a significant reduction of business from any of our major customers would adversely affect our results of operations.

Our substantial leverage and debt service obligations could harm our ability to operate our business, remain in compliance with debt covenants and make payments on our debt, including the notes.

We are highly leveraged and have significant debt service obligations under the notes and our new senior secured credit facility. As of June 30, 2004, we had total debt obligations of $369.0 million, of which approximately $2.0 million is due in one year. Pro forma for the twelve months ended December 31, 2003 and the six months ended June 30, 2004, our interest expense, net was approximately $28.7 million and $14.3 million, respectively. For a detailed discussion of our contractual cash obligations and other commercial commitments over the next several years and the new senior secured credit facility, refer to "Management's Discussion and Analysis of Financial Condition and Results of Operations—Contractual Obligations" and "Description of New Senior Secured Credit Facility."

If we are unable to meet our debt service obligations, we could be forced to restructure or refinance our obligations and seek additional equity financing or sell assets. We may be unable to restructure or refinance our obligations and obtain additional equity financing or sell assets on

17

satisfactory terms or at all. As a result, inability to meet our debt service obligations could cause us to default on those obligations. Many of our agreements governing the terms of our debt obligations contain restrictive covenants that limit our ability to take specific actions or require us not to allow specific events to occur and prescribe minimum financial maintenance requirements that we must meet. If we violate those restrictive covenants or fail to meet the minimum financial requirements contained in a lease or debt instrument, we would be in default under that instrument, which could, in turn, result in defaults under other leases and debt instruments. Any such defaults could materially impair our financial condition and liquidity.

The unpredictable product cycles of the medical device manufacturing industry and uncertain demand for our manufacturing, design and engineering capabilities and related services could cause our revenues to fluctuate.

Our target customer base of medical device companies operates in the medical device manufacturing industry, which is subject to rapid technological changes, short product life-cycles, frequent new product introductions and evolving industry standards, as well as economic cycles. If the market for our manufacturing, design and engineering capabilities does not grow as rapidly as forecasted by industry experts, our revenues could be less than expected. We also face the risk that changes in the medical device industry, for example, cost-cutting measures, changes to manufacturing techniques or production standards, could cause our manufacturing, design and engineering capabilities to lose widespread market acceptance. If our customers' products do not gain market acceptance or suffer because of competing products, unfavorable regulatory actions, alternative treatment methods or cures, product recalls or liability claims, they will no longer have the need for our capabilities and services and we may experience a decline in revenues. For example, the discovery and market acceptance of non-device treatments for specific medical conditions could make the medical devices used to treat those conditions obsolete. Shifts in our customers' market shares may also cause us to experience a decline in revenues. Our customers' markets, which include cardiology, endoscopy and orthopedics, and our markets are also subject to economic cycles and are likely to experience periods of economic decline in the future. Adverse economic conditions affecting the medical device manufacturing industry, in general, or the market for our manufacturing, design and engineering capabilities and services, in particular, could result in diminished sales, reduced profit margins and a disruption in our business. If our customers do not proceed with the production of devices in development because of their inability to obtain approval for those devices, changing market conditions or other reasons, our revenue could decline and therefore our results could suffer.

Our operating results may fluctuate, which may make it difficult to forecast our future performance.

Fluctuations in our operating results may cause uncertainty concerning our performance and prospects or may result in our failure to meet expectations. Our operating results have fluctuated in the past and are likely to fluctuate significantly in the future due to a variety of factors, which include, but are not limited to:

- •

- the fixed nature of a substantial percentage of our costs, which results in our operations being particularly sensitive to fluctuations in revenue;

- •

- changes in the relative portion of our revenue represented by our various products, which could result in reductions in our profits if the relative portion of our revenue represented by lower margin products increases;

- •

- introduction and market acceptance of our customers' new products and changes in demand for our customers' existing products;

- •

- the accuracy of our customers' forecasts of future production requirements;

- •

- timing of orders placed by our principal customers that account for a significant portion of our revenues;

- •

- timing of payments by customers;

18

- •

- price concessions as a result of pressure to compete;

- •

- cancellations by customers as a result of which we may recover only our costs plus our target markup;

- •

- availability of raw materials, including nitinol, elgiloy, tantalum, stainless steel, columbium, zirconium, titanium, gold, silver and platinum;

- •

- increased costs of raw materials, supplies or skilled labor;

- •

- effectiveness in managing our manufacturing processes; and

- •

- changes in competitive and economic conditions generally or in our customers' markets.

Investors should not rely on results of operations in any past period as an indication of what our results will be for any future period.

Our industry is very competitive; we may face competition from, and we may be unable to compete successfully against, new entrants and established companies with greater resources.

The medical device industry is very competitive and includes thousands of companies. As more medical device companies seek to outsource more of the design, prototyping and manufacturing of their products, we will face increasing competitive pressures to grow our business in order to maintain our competitive position, and we may encounter competition from and lose customers to other companies with design, technological and manufacturing capabilities similar to ours. Some of our potential competitors have greater name recognition, greater operating revenues, larger customer bases, longer customer relationships and greater financial, technical, personnel and marketing resources than we have. If we are unsuccessful competing with our competitors for our existing and prospective customers' business, we could lose business and our financial results could suffer.

We may not be able to continue to grow our business if the trend by medical device companies to outsource their manufacturing activities does not continue or if our customers decide to manufacture internally products that we currently provide.

Our design, manufacturing and assembly business has grown as a result of the increase over the past several years in medical device companies outsourcing these activities. We view the increasing use of outsourcing by medical device companies as an important component of our future growth strategy. While industry analysts expect the outsourcing trend to increase, our current and prospective customers continue to evaluate our capabilities against the merits of internal production. For example, recently Boston Scientific has informed us that it intends to transfer a number of products currently assembled by us to its own assembly operation in 2005 and the first half of 2006. Any substantial slowing of growth rates or decreases in outsourcing by medical device companies could cause our revenue to decline, and we may be limited in our ability or unable to continue to grow our business.

Also, as part of our growth strategy, we are seeking to accept full supply chain management and manufacturing responsibility for selected product lines from our customers and, in some cases, to acquire the related manufacturing assets from these customers. While we believe that product line transfers and asset acquisitions of this kind are becoming increasingly attractive to our customers, we have only consummated one of these transactions to date. We cannot be sure that opportunities of this nature will be available, especially if the trend toward outsourcing does not continue.

Our business may suffer if we are unable to recruit and retain the experienced engineers and management personnel that we need to compete in the medical device industry.

Our future success depends upon our ability to attract, retain and motivate highly skilled engineers and management personnel. We may not be successful in attracting new engineers or management

19

personnel or in retaining or motivating our existing personnel, which may lead to increased recruiting, relocation and compensation costs for such personnel. These increased costs may reduce our profit margins or make hiring new engineers impracticable. Some of our manufacturing processes are highly technical in nature. Our ability to maintain, expand or renew existing engagements with our customers, enter into new engagements and provide additional services to our existing customers depends on our ability to hire and retain engineers with the skills necessary to keep pace with continuing changes in the medical device industry. Competition for experienced engineers is intense. We compete with other companies in the medical device industry to recruit engineers. Our inability to hire additional qualified personnel may also require an increase in the workload for both existing and new personnel.

Our future success also depends on the personal efforts and abilities of the principal members of our senior management and engineering staff to provide strategic direction, manage our operations and maintain a cohesive and stable environment. In addition, our successful integration of acquired companies depends in part on our ability to retain senior management of the acquired companies. Although we have employment agreements with many of the members of our senior management staff, we do not have employment agreements with all of our key personnel, and the employment agreements we do have allow the employees to terminate them upon written notice. In addition, we do not carry key-man life insurance on any of our senior management.

Quality problems with our processes, products and services could harm our reputation for producing high quality products and erode our competitive advantage.

Quality is extremely important to us and our customers due to the serious and costly consequences of product failure. Many of our customers require us to adopt and comply with specific quality standards, and they periodically audit our performance. Our quality certifications are critical to the marketing success of our products and services. If we fail to meet these standards our reputation could be damaged, we could lose customers and our revenue could decline. Aside from specific customer standards, our success depends generally on our ability to manufacture to exact tolerances precision engineered components, subassemblies and finished devices from multiple materials. If our components fail to meet these standards or fail to adapt to evolving standards, our reputation as a manufacturer of high quality components could be harmed, our competitive advantage could be damaged, and we could lose customers and market share.

If we experience decreasing prices for our products and services and we are unable to reduce our expenses, our results of operations will suffer.

We may experience decreasing prices for the products and services we offer due to:

- •

- pricing pressure experienced by our customers from managed care organizations and other third-party payors;

- •

- increased market power of our customers as the medical device industry consolidates; and

- •

- increased competition among medical engineering and manufacturing services providers.

If the prices for our products and services decrease and we are unable to reduce our expenses, our results of operations will be adversely affected.

If we do not respond to changes in technology, our manufacturing, design and engineering processes may become obsolete and we may experience reduced sales and lose customers.

We use highly engineered, proprietary processes and highly sophisticated machining equipment to meet the critical specifications of our customers. Without the timely incorporation of new processes and enhancements, particularly relating to quality standards and cost-effective production, our manufacturing, design and engineering capabilities will likely become outdated, which could cause us to

20

lose customers and result in reduced revenues or profit margins. In addition, new or revised technologies could render our existing technology less competitive or obsolete or could reduce demand for our products and services. It is also possible that finished medical device products introduced by our customers may require fewer of our components or may require components that we lack the capabilities to manufacture or assemble. In addition, we may expend resources on developing new technologies that do not result in commercially viable processes for our business, which could adversely impact our margins and operating results.

Inability to obtain sufficient quantities of raw materials could cause delays in our production.

Our business depends on a continuous supply of raw materials. Raw materials needed for our business are susceptible to fluctuations in price and availability due to transportation costs, government regulations, price controls, change in economic climate or other unforeseen circumstances. Failure to maintain our supply of raw materials could cause production delays resulting in a loss of customers and a decline in revenue. Due to the supply and demand fundamentals of raw material used by us, we have occasionally experienced extended lead times on purchases and deliveries from our suppliers. Consequently, we have had to adjust our delivery schedule to customers. In addition, fluctuations in the cost of raw materials may increase our expenses and affect our operating results. The principal raw materials used in our business include stainless steel, tantalum, columbium, zirconium, titanium, nitinol, elgiloy, gold, silver and platinum. In particular, tantalum and nitinol are in limited supply. For wire fabrication, we purchase approximately 100% of our stainless steel wire from an independent, third-party supplier. The loss of this supplier could interrupt production and harm our business.

Our international operations are subject to a variety of risks that could adversely affect those operations and thus our profitability and operating results.

We have substantial international manufacturing operations in Europe and Mexico. We also receive a significant portion of our net sales from international sales, approximately half of which is generated by exports from our facilities in the United States and the other half of which is generated by sales from our international facilities. Although we take measures to minimize risks inherent to our international operations, the following risks may have a negative effect on our profitability and operating results, impair the performance of our foreign operations or otherwise disrupt our business:

- •

- fluctuations in the value of currencies could cause exchange rates to change and impact our profitability;

- •

- changes in labor conditions and difficulties in staffing and managing foreign operations, including labor unions, could lead to delays or disruptions in production or transportation of materials or our finished products;

- •

- greater difficulty in collecting accounts receivable and longer payment cycles, which can be more common in our international operations, could adversely impact our operating results over a particular fiscal period; and

- •

- changes in foreign regulations, export duties, taxation and limitations on imports or exports could increase our operational costs, impose fines or restrictions on our ability to carry on our business or expand our international operations.

We may expand into new markets and products and our expansion may not be successful.

We may expand into new markets through the development of new product applications based on our existing specialized manufacturing, design and engineering capabilities and services. These efforts could require us to make substantial investments, including significant research, development, engineering and capital expenditures for new, expanded or improved manufacturing facilities which

21

would divert resources from other aspects of our business. Expansion into new markets and products may be costly without resulting in any benefit to us. Specific risks in connection with expanding into new markets include the inability to transfer our quality standards into new products, the failure of customers in new markets to accept our products and price competition in new markets. If we choose to expand into new markets and are unsuccessful, our financial condition could be adversely affected and our business harmed.

We are subject to a variety of environmental laws that could be costly for us to comply with, and we could incur liability if we fail to comply with such laws or if we are responsible for releases of contaminants to the environment.

Federal, state and local laws impose various environmental controls on the management, handling, generation, manufacturing, transportation, storage, use and disposal of hazardous chemicals and other materials used or generated in the manufacturing of our products. If we fail to comply with any present or future environmental laws, we could be subject to fines, corrective action, other liabilities or the suspension of production. We have in the past paid civil penalties for violations of environmental laws. To date, such matters have not had a material adverse impact on our business or financial condition. We cannot assure you, however, that such matters will not have a material impact on us in the future.

In addition, conditions relating to our operations may require expenditures for clean-up of releases of hazardous chemicals into the environment. For example, our subsidiary, UTI Corporation, a Pennsylvania corporation, referred to herein as UTI Pennsylvania, has incurred liability for various cleanup matters related to the disposal of regulated wastes at third-party disposal sites, as has MedSource and companies it has acquired, which are now our subsidiaries through the MedSource acquisition. Further, we (including MedSource and its subsidiaries after the MedSource acquisition) have incurred liability with respect to contaminations at our and their current and former properties as a result of operations performed at these facilities. For example, we were required and continue to perform remediation as a result of leaks from underground storage tanks at our Collegeville, Pennsylvania facility. In addition, we may have future liability with respect to contamination at their current or former properties or with respect to third-party disposal sites. Although we do not anticipate that currently pending matters will have a material adverse effect on our results of operations and financial condition, we cannot assure you that these matters or others that arise in the future will not have such an effect.

Changes in environmental laws may result in costly compliance requirements or otherwise subject us to future liabilities. In addition, to the extent these changes affect our customers and require changes to their devices, our customers could have a reduced need for our products and services, and, as a result, our revenue could suffer.

Our inability to protect our intellectual property could result in a loss of our competitive advantage, and infringement claims by third parties could be costly and distracting to management.

We rely on a combination of patent, trade secret and trademark laws, confidentiality procedures and contractual provisions to protect our intellectual property. The steps we have taken or will take to protect our proprietary rights may not adequately deter unauthorized disclosure or misappropriation of our intellectual property, technical knowledge, practice or procedures. We may be required to spend significant resources to monitor our intellectual property rights, we may be unable to detect infringement of these rights and we may lose our competitive advantage associated with our intellectual property rights before we do so. Although we do not believe that any of our products, services or processes infringe the intellectual property rights of third parties, we may in the future be notified that we are infringing patent or other intellectual property rights of third parties. In the event of infringement of patent or other intellectual property rights, we may not be able to obtain licenses on commercially reasonable terms, if at all, and we may end up in litigation. The failure to obtain

22