As filed with the Securities and Exchange Commission on April 9, 2010

| | Registration No. 333-164641 |

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington D.C. 20549

___________

AMENDMENT NO. 1 TO FORM S-4

REGISTRATION STATEMENT

UNDER THE SECURITIES ACT OF 1933

___________

Peninsula Gaming, LLC*

(Exact name of registrant as specified in its charter)

Delaware (State or other jurisdiction of incorporation or organization) | 7900 (Primary Standard Industrial Classification Code Number) | 20-0800583 (I.R.S. Employer Identification Number) |

___________

301 Bell Street

Dubuque, Iowa 52001

(563) 690-4975

(Address, including zip code, and telephone number, including area code, of registrants’ principal executive offices)

___________

M. Brent Stevens

Peninsula Gaming, LLC

301 Bell Street

Dubuque, Iowa 52001

(563) 690-4975

(Name, Address, Including Zip Code, and Telephone Number,

Including Area Code, of Agent for Service)

With Copies to:

Nazim Zilkha, Esq.

White & Case LLP

1155 Avenue of the Americas

New York, New York 10036

(212) 819-8200

* The companies listed on the next page are also included in this Form S-4 Registration Statement as additional Registrants.

___________

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effective date of this registration statement.

If the securities being registered on this Form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G, check the following box: o

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act.

Large Accelerated Filer o Accelerated Filer o Non-Accelerated Filer x Smaller reporting company o

If applicable, place an X in the box to designate the appropriate rule provision relied upon in conducting this transaction:

Exchange Act Rule 13e-4(i) (Cross-Border Issuer Tender Offer) o

Exchange Act Rule 14d-1(d) (Cross-Border Third Party Tender Offer) o

CALCULATION OF REGISTRATION FEE

Title of each class of securities to be registered | Amount to be registered | Proposed maximum offering price per note | Proposed maximum aggregate offering price (1) | Amount of registration fee |

8 3/8% Senior Secured Notes due 2015 | | | | |

10 3/4% Senior Unsecured Notes due 2017 | | | | |

Guarantees of 8 3/8% Senior Secured Notes due 2015 (2) | | | | |

Guarantees of 10 3/4% Senior Unsecured Notes due 2017 (2) | | | | |

| (1) | Estimated solely for the purposes of calculating the registration fee in accordance with Rule 457(f) under the Securities Act. |

(2) No additional registration fee is due for guarantees pursuant to Rule 457(n) under the Securities Act.

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until the registration statement shall become effective on such date as the Securities and Exchange Commission, acting pursuant to said Section 8(a), may determine.

ADDITIONAL REGISTRANTS

| Exact name of additional registrants as specified in their charter* | State or other jurisdiction of incorporation or organization | I.R.S. Employer Identification Number |

| | |

The Old Evangeline Downs, L.L.C. | | |

| | |

| | |

| | |

| * | The address and telephone number for each of the additional registrants is c/o Peninsula Gaming, LLC, 301 Bell Street, Dubuque, Iowa 52001, (563) 690-4800. The primary standard industrial classification number for each of the additional registrants is 7900. |

The information in this prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any jurisdiction where the offer or sale is not permitted.

Subject to Completion, dated April 9, 2010

PROSPECTUS

PENINSULA GAMING, LLC

PENINSULA GAMING CORP.

Offer to Exchange

$240,000,000

8 3/8% Senior Secured Notes due 2015

and

$305,000,000

10 3/4% Senior Unsecured Notes due 2017

We are offering to exchange, upon the terms and subject to the conditions set forth in this prospectus and the accompanying letter of transmittal, our new registered 8⅜% Senior Secured Notes due 2015 (the “secured exchange notes”) for all of our outstanding unregistered 8⅜% Senior Secured Notes due 2015 (the “secured outstanding notes”) and our new registered 10 3/4% Senior Unsecured Notes due 2017 (the “unsecured exchange notes”) for all of our outstanding unregistered 10 3/4% Senior Unsecured Notes due 2017 (the “unsecured outstanding notes”). In this prospectus, the term “outstanding notes” refers collectively to the secured outstanding notes and the unsecured outstanding notes and the term “exchange notes” refers collectively to the secured exchange notes and the unsecured exchange notes. We sometimes refer to the outstanding notes and the exchange notes collectively as the “Notes.” Exchange notes will be issued in denominations of $2,000 principal amount and integral multiples of $1,000 in exchange for outstanding notes in minimum denominations of $2,000 and integral multiples of $1,000. The CUSIP numbers for the secured outstanding notes are 707132AG1, 707132AH9 and U70601AA4. The CUSIP numbers for the unsecured outstanding notes are 707132AK2, 707132AL0 and U70601AB2.

Material terms of the exchange offer:

| · | The terms of the exchange notes we will issue in the exchange offer will be substantially identical to the terms of the outstanding notes, except that transfer restrictions and registration rights relating to the outstanding notes will not apply to the exchange notes. |

| · | The exchange offer expires at 5:00 p.m., New York City time, on , 2010, unless extended. |

| · | The exchange offer is subject only to the conditions that the exchange offer will not violate any applicable law or any interpretation of applicable law by the staff of the Securities and Exchange Commission (the “SEC”). |

| · | All outstanding notes that are validly tendered and not validly withdrawn prior to the expiration of the exchange offer will be exchanged. |

| · | Tenders of outstanding notes may be withdrawn at any time before 5:00 p.m., New York City time, on the expiration date of the exchange offer. |

| · | We will not receive any proceeds from the exchange offer. |

| · | There is no established trading market for the exchange notes, and we do not intend to apply for listing of the exchange notes on any securities exchange. |

| · | Any outstanding notes not validly tendered will remain subject to existing transfer restrictions. |

| · | The exchange of exchange notes for outstanding notes will not be a taxable transaction for U.S. federal income tax purposes, but you should see the discussion under the heading “Certain U.S. Federal Income Tax Consequences” on page 142 for more information. |

| · | We can amend or terminate the exchange offer. |

For a discussion of factors that you should consider before you participate in the exchange offer, see “Risk Factors” beginning on page 11 of this prospectus.

Neither the SEC nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2010.

TABLE OF CONTENTS

| |

| 1 |

| 11 |

| 26 |

| 27 |

| 28 |

| 31 |

| 33 |

| 45 |

| 54 |

| 65 |

| 67 |

| 75 |

| 77 |

| 78 |

| 111 |

| 140 |

| 146 |

| 147 |

| 147 |

| 147 |

| F-1 |

________________

Each broker-dealer that receives exchange notes for its own account pursuant to the exchange offer must acknowledge that it will deliver a prospectus in connection with any resale of such exchange notes. The letter of transmittal relating to the exchange offer states that by so acknowledging and by delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933, as amended (the “Securities Act”). This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of exchange notes received in exchange for outstanding notes where such outstanding notes were acquired by such broker-dealer as a result of market-making activities or other trading activiti es. We have agreed that, for a period of up to 90 days after the consummation of the exchange offer, we will make this prospectus available to any broker-dealer, at such broker-dealer’s request, for use in connection with any such resale. See “Plan of Distribution.”

________________

YOU SHOULD RELY ONLY ON THE INFORMATION CONTAINED IN THIS PROSPECTUS. WE HAVE NOT AUTHORIZED ANY DEALER, SALESPERSON, OR OTHER PERSON TO GIVE ANY INFORMATION OR REPRESENT ANYTHING NOT CONTAINED IN THIS PROSPECTUS OR THE ACCOMPANYING LETTER OF TRANSMITTAL. YOU MUST NOT RELY ON ANY UNAUTHORIZED INFORMATION. THIS PROSPECTUS AND THE ACCOMPANYING LETTER OF TRANSMITTAL DO NOT OFFER TO SELL OR ASK YOU TO BUY ANY SECURITIES IN ANY JURISDICTION WHERE IT IS UNLAWFUL. THE INFORMATION CONTAINED IN THIS PROSPECTUS IS ACCURATE ONLY AS OF THE DATE OF THIS PROSPECTUS, REGARDLESS OF THE TIME OF DELIVERY OF THIS PROSPECTUS OR OF ANY SALE OF THE NOTES.

NOTICE TO NEW HAMPSHIRE RESIDENTS

NEITHER THE FACT THAT A REGISTRATION STATEMENT OR AN APPLICATION FOR A LICENSE HAS BEEN FILED UNDER CHAPTER 421-B OF THE NEW HAMPSHIRE REVISED STATUTES ANNOTATED (“RSA 421-B”) WITH THE STATE OF NEW HAMPSHIRE NOR THE FACT THAT A SECURITY IS EFFECTIVELY REGISTERED OR A PERSON IS LICENSED IN THE STATE OF NEW HAMPSHIRE CONSTITUTES A FINDING BY THE SECRETARY OF STATE THAT ANY DOCUMENT FILED UNDER RSA 421-B IS TRUE, COMPLETE AND NOT MISLEADING. NEITHER ANY SUCH FACT NOR THE FACT THAT AN EXEMPTION OR EXCEPTION IS AVAILABLE FOR A SECURITY OR A TRANSACTION MEANS THAT THE SECRETARY OF STATE HAS PASSED IN ANY WAY UPON THE MERITS OR QUALIFICATIONS OF, OR RECOMMENDED OR GIVEN APPROVAL TO, ANY PERSON, SECURITY OR TRANSACTION. IT IS UNLAWFUL TO MAKE, OR CAUSE TO BE MADE, TO ANY PROSPECTIVE PURCHASER, CUSTOMER OR CLIENT ANY REPRESENTATION INCONSISTENT WITH THE PROVISIONS OF THIS PARAGRAPH.

________________

INDUSTRY AND MARKET DATA

Unless otherwise indicated, information contained in this prospectus concerning our business lines, our industry and its segments and related markets and our general expectations concerning our industry and its segments and related markets are based on management estimates. Such estimates are derived from publicly available information released by third-party sources, as well as data from our internal research and on assumptions made by us based on such data, which we believe to be reasonable, and our knowledge of such industry and markets.

While we believe that the industry and similar data presented herein that is derived from information released by third-party sources is accurate, we have not independently verified this information and cannot guarantee its accuracy. Industry and market data involve risks and uncertainties and are subject to change based on various factors, including those discussed under the caption “Risk Factors.”

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This prospectus includes “forward-looking statements” within the meaning of the federal securities laws. These statements relate to analyses and other information which are based on forecasts of future results and estimates of amounts not yet determinable. These statements also relate to our future prospects, developments and business strategies. These forward-looking statements are identified by their use of terms and phrases such as “anticipate,” “believe,” “could,” “would,” “estimate,” “expect,” “intend,” “may,” “plan,” “predict,” “project,” “will,” “likely,” “continue” and similar terms and phrases, including references to assumptions. The forwar d-looking information contained in this prospectus is generally located under the headings “Prospectus Summary,” “Risk Factors,” “Capitalization,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and “Business,” but may be found in other locations as well. These forward-looking statements generally relate to our strategies, plans and objectives for future operations and are based upon management's current beliefs or estimates of future results or trends. Although we believe that our plans, intentions and expectations reflected in or suggested by such forward-looking statements are reasonable, they are inherently subject to risks, uncertainties and assumptions. Accordingly, there can be no assurance that such plans, intentions or expectations will be achieved or that any trends noted in this prospectus will continue. We caution you that any forward-looking statement reflects only our belief at the time the statement is made. You should read this prospectus completely and with the understanding that actual future results may be materially different from what we expect. We do not plan to update forward-looking statements even though our situation may change in the future.

Specific factors that might cause actual results to differ from our expectations, might cause us to modify our plans or objectives, may affect our ability to pay timely amounts due under the exchange notes and/or may affect the value of the exchange notes, include, but are not limited to:

| | • | the availability and adequacy of our cash flows to satisfy our obligations, including payment obligations under the exchange notes and the PGL Credit Facility (as defined herein) and additional funds required to support capital improvements and developments; |

| | • | economic, competitive, demographic, business and other conditions in our local and regional markets; |

| | • | actions taken or omitted to be taken by third parties, including customers, suppliers, competitors, members and shareholders, as well as legislative, regulatory, judicial and other governmental authorities; |

| | • | changes in business strategy, capital improvements, development plans, including those due to environmental remediation concerns, or changes in personnel or their compensation, including federal, state and local minimum wage requirements; |

| | • | the loss of any license or permit, including the failure to obtain an unconditional renewal of a required gaming license on a timely basis; |

| | • | the loss of the ability of Diamond Jo, LLC, a Delaware limited liability company (“DJL”), or Diamond Jo Worth, LLC, a Delaware limited liability company (“DJW”), to conduct its gaming operations in the event the electorates in Dubuque County and Worth County, respectively, do not vote to continue gaming in Dubuque County and Worth County, Iowa, respectively; |

| | • | the termination of our operating agreement with the Dubuque Racing Association and/or the Worth County Development Authority or the failure of either such organization to continue as our “qualified sponsoring organization;” |

| | • | the loss or temporary closure of our facilities due to casualty, weather, mechanical failure or any extended or extraordinary repairs, maintenance or inspection that may be required; |

| | • | changes in federal or state tax obligations; |

| | • | potential exposure to environmental liabilities, changes or developments in the laws, regulations or taxes in the gaming or horse racing industry or a decline in the public acceptance of gaming or horse racing and other unforeseen difficulties associated with our operations; |

| | • | adverse circumstances, changes, developments or events relating to or resulting from our ownership and control of DJL, The Old Evangeline Downs, L.L.C., a Louisiana limited liability company (“EVD”), DJW and Belle of Orleans, L.L.C., a Louisiana limited liability company (“ABC”); and |

| | • | other factors discussed in our filings with the SEC. |

This summary highlights information contained in this prospectus. It does not contain all of the information that may be important to you. You should read this entire prospectus carefully, including the sections captioned “Risk Factors,” “Unaudited Pro Forma Condensed Combined Financial Information” and “Capitalization” and the audited and unaudited condensed financial statements and the notes thereto contained in this prospectus before making an investment decision.

In this prospectus, the terms “PGL,” “Company,” “we,” “us” and “our” refer to Peninsula Gaming, LLC and its subsidiaries, as the context may require.

Overview

We are a casino entertainment company with gaming operations in local markets in Iowa and Louisiana. Founded in 1999, we seek to develop quality gaming operations in highly protected markets and currently own and operate four facilities. We developed and built three of our gaming operations, comprised of the Diamond Jo in Dubuque, Iowa, the Diamond Jo Worth in Worth County, Iowa and the Evangeline Downs in Opelousas, Louisiana. On October 22, 2009, we acquired our fourth property, the Amelia Belle riverboat casino located in Amelia, Louisiana (the “Amelia Belle Casino” or “ABC”).

The following summarizes certain features of our gaming properties as of December 31, 2009:

| | Diamond Jo | Evangeline Downs | Diamond Jo Worth | Amelia Belle |

| Opened | December 2008 (replacing previous facility operating since 1994) | December 2003 | April 2006 (expansion completed in April 2007) | May 2007 (acquired in October 2009) |

Location | Dubuque, Iowa | Opelousas, Louisiana | Northwood, Iowa | Amelia, Louisiana |

Size | 188,000 square feet (“sq. ft.”) | 120,000 sq. ft. | 107,213 sq. ft. | 61,728 sq. ft. |

Gaming | • 985 slots • 19 table games | • 1,424 slots • 980 horse capacity | • 959 slots • 22 table games | • 842 slots • 17 table games |

Amenities | • 800 person capacity entertainment venue • 30-lane bowling center • 132-seat steakhouse • 184-seat buffet • 124-seat sports bar • 50-seat deli/coffee shop | • Seasonal thoroughbred and quarter horse horses • four off-track betting parlors • 94-seat steakhouse • 348-seat buffet • 90-seat cafe | • 400-seat entertainment venue • 190-seat buffet • 114-seat steakhouse • 7 table poker room • 45-seat Burger King • Subway restaurant • Third-party 102-room hotel | • 153 seat full service buffet |

Parking | 1,763 parking spaces | 2,447 parking spaces | 1,300 parking spaces | 655 parking spaces |

Operating Strategy

Our operating strategy focuses on three main areas:

| | • | Capitalizing on our recently constructed, state-of-the-art principal entertainment venues. With the exception of the Amelia Belle Casino, all of our facilities are land-based and have been constructed from the ground up within the last six years, including the Diamond Jo in Dubuque, Iowa, which opened to the public in December 2008 to replace our former riverboat facility located there. At each of our facilities, our team members are dedicated to providing exceptional guest service. In addition, our management team continues its focus on delivering a tailored mix of slot machines and other games as well as offering high quality, comprehensive dining and entertainment amenities for the local markets that we serve. We believe the quality of o ur venues and dedicated service is what differentiates us from our competitors. |

| | • | Targeted data base marketing. Most of our revenue comes from guests located within 100 miles of our facilities. The Amelia Belle Casino benefits from a strong local market and is strategically located in southern Louisiana, south of New Orleans and Baton Rouge. We utilize targeted database marketing strategies to increase visitation and maximize game play and profitability of each guest at our venues through customized incentives and marketing for various levels of play. Our “rewards loyalty” program rewards our guests based on their level of play and offers a variety of rewards ranging from free-play on our slot machines to complimentary food to events offered through our many amenities. Our disciplined approach to our database marketin g has continued to drive business while maintaining strong operating margins. |

| | • | Branded advertising. We utilize focused advertising dollars on select outdoor, print and television advertising within our markets to create a high level of local brand recognition. The Diamond Jo brand was established over 15 years ago in Dubuque and its association with being a quality local market establishment was instrumental in opening the Diamond Jo Worth in Worth County, Iowa. Evangeline Downs in Opelousas, Louisiana first began racing operations in the area in 1967, and we are able to carry that brand recognition to our several off-track betting/video poker operations within a broader area around Evangeline Downs. |

Business Strengths

Highly Protected Markets. Our properties are located in markets with limited direct competition. Currently, there are no new riverboat or racino gaming licenses available in Louisiana and, although there are four license applications currently pending in Iowa, we do not anticipate any of these new licenses, if granted, having a material impact on our properties. Therefore, the competitive landscape across the Company’s target markets is expected to remain favorable. In central Louisiana, Evangeline Downs is the only racino within a l20-mile radius and the only gaming facility within a 50-mile radius. Among its nearest competitors, Evangeline Downs is differentiated by its diverse suite of quality amenities and ease of access. &# 160;In Worth County, Iowa, Diamond Jo Worth is the only casino within a 90-mile radius. In Dubuque, we compete with a dog-track/casino located approximately three miles away. However, our newly completed, $82 million state-of-the-art facility, with its favorable location at the confluence of three major regional highways and within the Port of Dubuque, allows it to capture a greater market share. At the Amelia Belle Casino, the closest gaming facility is located 35 miles to the northwest; however, the Amelia Belle Casino is the closest facility to the southern Louisiana regional population centers of Morgan City, Houma and Thibodaux, Louisiana.

Emphasis on Slot Play. We emphasize slot machine wagering, which we believe is typically both the highest margin and most predictable component of the gaming industry. Slot machines do not have the staffing requirements of table games and, typically, have less volatility in revenues over an extended period of time than the table game side of the casino business. We believe that this affords us a more stable and predictable revenue stream, as well as consistently strong margins.

Low Maintenance Capital Expenditures. All of our properties were recently built or renovated and, we believe, will require minimal maintenance capital expenditures over the next few years to remain operational and competitive. We opened our new facility at the Diamond Jo in Dubuque in December 2008 at a cost of approximately $82 million. The Diamond Jo Worth opened in April 2006 and an expansion of the property was completed in April 2007 at a total cost of approximately $74 million. Evangeline Downs opened in December 2003 at a cost of approximately $130 million. We are currently in the final stages of a $7.5 million renovation of the Amelia Belle Casino.

Strategically Diverse Property Base. We believe that we benefit from the diverse locations of our properties. On a pro forma basis, for 2009, Evangeline Downs, Diamond Jo, Diamond Jo Worth and Amelia Belle generated 37%, 22%, 26% and 15% of our net revenues, respectively. In addition, all of the properties are located far enough away from each other such that they do not materially overlap in customer base, yet are close enough within their respective regions to enjoy certain operational synergies.

Proven and Experienced Management Team. Our senior management team is comprised of four individuals with extensive operating and development experience at our gaming properties, and in other regional and national (i.e., Atlantic City and Las Vegas) markets. Our team has established a track record for managing large development projects to completion on time and within budget. The senior management team is supported by experienced general managers local to each property.

Business Structure

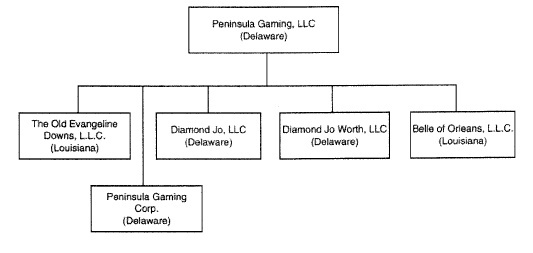

PGL is a holding company with no independent operations whose primary assets are its equity interests in the following wholly owned subsidiaries:

| | • | DJL, which owns and operates the Diamond Jo casino in Dubuque, Iowa; |

| | • | EVD, which owns and operates the Evangeline Downs Racetrack and Casino, or “racino,” in St. Landry Parish, Louisiana, and four off-track betting parlors (“OTB”) in Louisiana; |

| | • | DJW, which owns and operates the Diamond Jo Worth casino in Worth County, Iowa; and |

| | • | ABC, which owns and operates the Amelia Belle Casino in Amelia, Louisiana. |

PGL is a wholly owned subsidiary of Peninsula Gaming Partners, LLC (“PGP”). PGL’s other subsidiary is Peninsula Gaming Corp. (“PGC”), which has no assets or operations but serves as a co-issuer of the Notes.

Related Transactions

On June 18, 2009, PGP and AB Casino Acquisition LLC, a Delaware limited liability company (“AB Acquisition”) that was formed by PGL in order to effect the Amelia Belle Acquisition (as described below), entered into a definitive purchase agreement (the “Amelia Belle Purchase Agreement”) with Columbia Properties New Orleans, L.L.C. to purchase 100% of the outstanding limited liability company interests of ABC (the “Amelia Belle Acquisition”). On October 22, 2009, the Amelia Belle Acquisition was consummated for $104.0 million, plus $2.2 million in estimated working capital which shall be adjusted for actual working capital balances subsequent to closing. PGL and PGC (collectively, the “Issuers”) issued the outstanding notes in an aggregate principal amount of $545.0 milli on (the “Notes Issuance”), the net proceeds of which were used, among other things, to fund the purchase price of ABC, to redeem all of PGL’s existing 8 3/8% senior secured notes due 2012 (the “PGL Notes”), to redeem all of DJW’s existing 11% senior secured notes due 2012 (the “DJW Notes”), to redeem all of EVD’s existing 13% senior notes due 2010 (the “EVD Notes”) and to reduce outstanding borrowings under our senior credit facility.

Concurrently with the consummation of the Amelia Belle Acquisition, AB Acquisition merged with and into PGL (with PGL surviving) and ABC became a wholly-owned subsidiary of PGL. Following consummation of the Amelia Belle Acquisition, Diamond Jo Worth Holdings, LLC and Diamond Jo Worth Corp., subsidiaries of PGL, were dissolved.

On October 29, 2009, we amended and restated our senior secured credit facility (the “Original Credit Facility”) with Wells Fargo Foothill, Inc., as arranger and agent, to provide for, among other things, (i) an extension of the maturity date from January 15, 2012 to January 15, 2014, (ii) the inclusion of ABC as a borrower thereunder, (iii) a reduction in the maximum revolver amount from $65.0 million to $58.5 million, (iv) the re-adjustment of minimum EBITDA requirements, and (v) additional flexibility for the borrowers with respect to certain negative covenants (as amended and restated, the “PGL Credit Facility”). For more information on the PGL Credit Facility, see “Description of Certain Indebtedness.”

Set forth below is the current organizational structure of PGL and its subsidiaries.

Principal Executive Office

Our principal executive office is located at 301 Bell Street, Dubuque, Iowa 52001, and our telephone number at this address is (563) 690-4975.

Purpose of the Exchange Offer

On August 6, 2009, we sold, through a private placement exempt from the registration requirements of the Securities Act, $240,000,000 of aggregate principal amount of our secured outstanding notes and $305,000,000 of aggregate principal amount of our unsecured outstanding notes.

Simultaneously with the private placement, we entered into a registration rights agreement with the initial purchasers of the outstanding notes. Under the registration rights agreement, we are required to use our reasonable best efforts to cause a registration statement for substantially identical notes, which will be issued in exchange for the outstanding notes, to become effective within 270 days of issuance of the outstanding notes. You may exchange your outstanding notes for exchange notes in this exchange offer.

We did not register the outstanding notes under the Securities Act or any state securities law, nor do we intend to after the exchange offer. As a result, the outstanding notes may only be transferred in limited circumstances under the securities laws. If the holders of the outstanding notes do not exchange their outstanding notes in the exchange offer, they lose their right to have the outstanding notes registered under the Securities Act, subject to certain limitations. Anyone who still holds outstanding notes after the exchange offer may be unable to resell their outstanding notes.

We believe, however, that holders of the exchange notes may resell the exchange notes without complying with the registration and prospectus delivery provisions of the Securities Act, if they meet certain conditions. You should read the discussion under the headings “—Summary of The Exchange Offer,” “—Summary of The Exchange Notes” and “The Exchange Offer” for further information regarding the exchange offer, the exchange notes and resales of the exchange notes.

Summary of The Exchange Offer

The following is a summary of the principal terms of the exchange offer. A more detailed description is contained in this prospectus under the section entitled “The Exchange Offer.”

| The Exchange Offer | We are offering to exchange all of our outstanding notes for exchange notes. The terms of the exchange notes and outstanding notes are substantially identical in all respects, including principal amount at maturity, interest rate and maturity, except that the exchange notes are in general freely transferable and are not subject to any covenant regarding registration under the Securities Act. To be exchanged, an outstanding note must be properly tendered and accepted. Unless we terminate the exchange offer, all outstanding notes that are validly tendered and not validly withdrawn will be exchanged. We will issue the exchange notes promptly after the expiration of the exchange offer. |

Expiration Date | The exchange offer will remain open for at least 20 full business days and will expire at 5:00 p.m., New York City time, on , 2010, unless we decide to extend this expiration date. In that case, the phrase “expiration date” will mean the latest date and time to which we extend the exchange offer. |

Conditions to the Exchange Offer | We may terminate or amend the exchange offer if: • any legal proceeding or government action materially impairs our ability to complete the exchange offer, or • any SEC rule, regulation or interpretation materially impairs the exchange offer. We may waive any or all of these conditions. At this time, there are no adverse proceedings, actions or developments pending or, to our knowledge, threatened, and no governmental approvals are necessary to complete the exchange offer. The exchange offer is not conditioned upon any minimum principal amount of outstanding notes tendered. |

| Withdrawal Rights | You may withdraw the tender of your outstanding notes at any time before the expiration date. Any outstanding notes not accepted by us for exchange for any reason will be returned to you at our expense as soon as practicable after withdrawal or termination of the exchange offer. |

| The Registration Rights Agreement | You have the right to exchange your outstanding notes for exchange notes with substantially identical terms. This exchange offer is being made to satisfy these rights. Except in limited circumstances described under “The Exchange Offer—Background and Purpose of the Exchange Offer,” after the exchange offer is complete, you will no longer be entitled to any exchange or registration rights with respect to your outstanding notes. |

| Resales of the Exchange Notes | We believe that the exchange notes issued in the exchange offer may be offered for resale, resold and otherwise transferred by you without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that: • you are acquiring the exchange notes in the ordinary course of your business; • you are not participating, do not intend to participate and have no arrangement or understanding with any person to participate in the distribution of the exchange notes; and • you are not an "affiliate" of our company or any of our subsidiaries, as that term is defined in Rule 405 of the Securities Act. See "The Exchange Offer—Resale of the Exchange Notes." The SEC, however, has not considered this exchange offer in the context of a no-action letter, and we cannot be sure that the staff of the SEC would make the same determination with this exchange offer as it has in other circumstances. Furthermore, if you do not meet the above conditions, you may incur liability under the Securities Act. We do not assume, or indemnify you against, this liability. Each broker-dealer that is issued exchange notes in the exchange offer for its own account in exchange for outstanding notes which were acquired by it as a result of market-making or other trading activities must acknowledge that it will deliver a prospectus meeting the requirements of the Securities Act in connection with any resale of the exchange notes issued in the exchange offer. A broker-dealer may use this prospectus for an offer to resell, resale or other retransfer of the exchange notes issued to it in the exchange offer. The exchange offer is not being made to, nor will we accept surrenders for exchange from, the following: • holders of ourstanding notes in any jurisdiction in which this exchange offer or the acceptance of the exchange offer would not be in compliance with the applicable securities or "blue sky" laws of that jurisdiction, and • holders of outstanding notes who are “affiliates” of our company or any of our subsidiaries. |

Procedures for Tendering | If you wish to tender outstanding notes, you must (a)(1) complete, sign and date the letter of transmittal, or a facsimile of it, according to its instructions and (2) send the letter of transmittal, together with your outstanding notes to be exchanged and other required documentation, to U.S. Bank National Association, who is the exchange agent (the “Exchange Agent”), at the address provided in the letter of transmittal; or (b) tender through DTC pursuant to DTC’s Automated Tender Offer Program, or ATOP system. The letter of transmittal or a valid agent’s message through ATOP must be received by the Exchange Agent by 5:00 p.m., New York City time, on the expiration date. See “The Exchange Offer—Procedures for Tendering,” and “—Book-Entry Tender.” ;By executing the letter of transmittal, you are representing to us that you are acquiring the exchange notes in the ordinary course of your business, that you are not participating, do not intend to participate and have no arrangement or understanding with any person to participate in the distribution of exchange notes, and that you are not an “affiliate” of ours. See “The Exchange Offer—Procedures for Tendering,” and “—Book-Entry Tender.” Do not send letters of transmittal and certificates representing outstanding notes to us. Send these documents only to the Exchange Agent. See “The Exchange Offer—Procedures for Tendering” for more information. |

Special Procedures for Beneficial Owners | If you are the beneficial owner of book-entry interests and your name does not appear on a security position listing of DTC as the holder of the book-entry interests or if you are a beneficial owner whose outstanding notes are registered in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender your outstanding notes in the exchange offer, you should contact the registered holder promptly and instruct the registered holder to tender on your behalf. If you are a beneficial owner and wish to tender on your own behalf, you must, before completing and executing the letter of transmittal and delivering your outstanding notes, either make appropriate arrangements to register ownership of the outstanding notes in your name or obtain a properly completed bond power from the registered holder. See “The Exchange Offer—Procedure if the Outstanding Notes Are Not Registered in Your Name,” and “—Beneficial Owner Instructions to Holders of Outstanding Notes.” The transfer of registered ownership may take considerable time and may not be possible to complete before the expiration date. |

| Guaranteed Delivery Procedures | If you wish to tender your outstanding notes and the certificates for your outstanding notes are not immediately available, time will not permit your outstanding notes or other required documents to reach the Exchange Agent on or prior to the expiration date, or you cannot complete the procedures for delivery by book-entry transfer on time, then before the expiration date you may tender your outstanding notes as described in this prospectus under the heading “The Exchange Offer—Guaranteed Delivery Procedures.” |

| Failure to Tender Outstanding Notes | If you are eligible to participate in the exchange offer and you do not tender your outstanding notes, you will not have any further registration or exchange rights and your outstanding notes will continue to have restrictions on transfer. Outstanding notes may not be offered or sold, unless registered under the Securities Act and applicable state securities laws or under an exemption from the Securities Act and applicable state securities laws. We do not currently plan to register the outstanding notes under the Securities Act after the completion of the exchange offer. Accordingly, the liquidity of the market for the outstanding notes could be adversely affected. |

| | In addition, after the consummation of the exchange offer, it is anticipated that the outstanding principal amount at maturity of the outstanding notes available for trading will be significantly reduced. The reduced float will adversely affect the liquidity and market price of the outstanding notes. A smaller outstanding principal amount at maturity of notes available for trading may also tend to make the price more volatile. |

Acceptance of Outstanding Notes and Delivery of Exchange Notes | In general, we will accept any and all outstanding notes that are properly tendered in the exchange offer and not withdrawn before 5:00 p.m., New York City time, on the expiration date. The exchange offer will be considered consummated when we, as soon as practicable after the expiration date, accept for exchange the outstanding notes tendered, deliver them to the trustee for cancellation and issue the exchange notes. We will deliver the exchange notes as soon as practicable after the expiration date. Any outstanding notes not accepted by us for exchange for any reason will be returned to you at our expense promptly after the expiration or termination of the exchange offer. |

| Interest on the Outstanding Notes | Interest will not be paid on outstanding notes that are tendered and accepted for exchange in the exchange offer. |

| Listing of the Exchange Notes | We do not intend to have the outstanding notes or the exchange notes listed on any securities exchange or arrange for quotation on any automated dealer quotation system. |

| Federal Income Tax Considerations | We believe that the exchange of exchange notes for outstanding notes will not be a taxable event for U.S. federal income tax purposes. Please see “Certain U.S. Federal Income Tax Consequences” for more information. |

| Appraisal Rights | You do not have any appraisal or dissenters’ rights in connection with this exchange offer. |

| Use of Proceeds | We will not receive any proceeds from the issuance of the exchange notes in the exchange offer. |

| Fees and Expenses | We will pay all of the expenses incident to the exchange offer. |

| Exchange Agent | U.S. Bank National Association is serving as the exchange agent in connection with the exchange offer. Its address and telephone number are set forth in “The Exchange Offer—Exchange Agent.” |

Please review the information in the section captioned “The Exchange Offer” for more detailed information concerning the exchange offer.

Summary of the Exchange Notes

The form and terms of the exchange notes are the same as the form and terms of the outstanding notes, except that the exchange notes will be registered under the Securities Act. As a result, the exchange notes will not bear legends restricting their transfer and will not contain the registration rights and liquidated damage provisions contained in the outstanding notes. The exchange notes represent the same debt as the outstanding notes. The outstanding notes and the exchange notes are governed by the same indentures.

| Peninsula Gaming, LLC, a Delaware limited liability company, and Peninsula Gaming Corp., a Delaware corporation and a direct wholly-owned subsidiary of PGL. |

| $240.0 million aggregate principal amount of 8⅜% Senior Secured Notes due 2015, which have been registered under the Securities Act. $305.0 million aggregate principal amount of 10¾% Senior Unsecured Notes due 2017, which have been registered under the Securities Act. The exchange notes will evidence the same debt as the outstanding notes and will be issued under, and entitled to the benefits of, the same indentures. The terms of the exchange notes are the same as the terms of the outstanding notes in all material respects except that the exchange notes: • have been registered under the Securities Act; • bear a different CUSIP number from the outstanding notes; • do not include rights to registration under the Securities Act; and • do not contain transfer restrictions applicable to the outstanding notes. |

| Secured exchange notes: August 15, 2015 Unsecured exchange notes: August 15, 2017 |

| We will pay interest on the secured exchange notes semi-annually at the rate of 8⅜% per year, payable in cash, on August 15 and February 15 of each year, beginning on February 15, 2010. We will pay interest on the unsecured exchange notes semi-annually at the rate of 10¾% per year, payable in cash, on August 15 and February 15 of each year, beginning on February 15, 2010. |

| The secured exchange notes and the unsecured exchange notes will be guaranteed on a senior secured basis and a senior unsecured basis, respectively, by all of PGL’s existing and future domestic restricted subsidiaries other than PGC, which will be a co-Issuer of the exchange notes. |

| The secured exchange notes and its related guarantees will be secured by a security interest in our current and future assets (other than certain excluded assets) and by a pledge of 100% of the equity interests of PGL. The lien on the collateral that secures the secured exchange notes and the guarantees will be junior in priority relative to the liens securing any of our existing or future senior credit facilities pursuant to an intercreditor agreement. See “Description of Secured Notes—Security.” Accordingly, the secured exchange notes and related guarantees will be effectively subordinated to our existing or future senior secured credit facilities to the extent of the value of the assets securing such indebtedness. |

| The secured exchange notes will be our senior secured obligations, will rank pari passu in right of payment with all of our existing and future senior indebtedness and will rank senior in right of payment to all of our existing and future subordinated indebtedness. The unsecured exchange notes will be our senior unsecured obligations, will rank pari passu in right of payment with all of our existing and future senior indebtedness and will rank senior in right of payment to all of our existing and future subordinated indebtedness. The unsecured exchange notes will be effectively subordinated to our senior secured indebtedness, including the secured exchange notes and our existing and future senior credit facilities, to the extent of the value of the assets that secure such indebtedness. |

| On or after August 15, 2012, we will have the right to redeem all or some of the secured exchange notes at the redemption prices described in this prospectus, plus accrued and unpaid interest, if any, to the applicable date of redemption. See “Description of Secured Notes—Redemption—At the Option of the Issuers.” On or after August 15, 2013, we will have the right to redeem all or some of the unsecured exchange notes at the redemption prices described in this prospectus, plus accrued and unpaid interest, if any, to the applicable date of redemption. See “Description of Unsecured Notes—Redemption—At the Option of the Issuers.” |

Equity Clawback; Make- Whole Redemption | Prior to August 15, 2011, we may redeem from time to time up to 35% of the aggregate principal amount of the secured exchange notes at a redemption price equal to 108.375% plus accrued and unpaid interest, if any, to the applicable redemption date with the proceeds of any equity offering. Prior to August 15, 2012, we may redeem the secured exchange notes, in whole or in part, at a make-whole redemption price as described in this prospectus, plus accrued and unpaid interest, if any, to the applicable redemption date. See “Description of Secured Notes—Redemption—Equity Clawback” and “—Make-Whole Redemption,” respectively. Prior to August 15, 2012, we may redeem from time to time up to 35% of the aggregate principal amount of the unsecured exchange notes at a redemption price equal to 110.775% plus accrued and unpaid interest, if any, to the applicable redemption date with the proceeds of any equity offering. Prior to August 15, 2013, we may redeem the unsecured exchange notes, in whole or in part, at a make-whole redemption price as described in this prospectus, plus accrued and unpaid interest, if any, to the applicable redemption date. See “Description of Unsecured Notes—Redemption—Equity Clawback” and “—Make-Whole Redemption,” respectively. |

Required Regulatory Redemption | The Notes will be subject to mandatory disposition or redemption following certain determinations by applicable racing and gaming regulatory authorities. See “Description of Secured Notes—Required Regulatory Redemption” and “Description of Unsecured Notes—Redemption—Required Regulatory Redemption.” |

| Change of Control Offer | If a change of control occurs, the holders of the Notes will have the right to require us to purchase their Notes at 101% of the principal amount plus accrued and unpaid interest, if any, to the date of repurchase. See “Description of Secured Notes—Repurchase Upon Change of Control” and “Description of Unsecured Notes—Repurchase Upon Change of Control.” |

| If we sell assets or an event of loss occurs and the proceeds are not applied as required under the Indentures (as defined below), we may have to use the proceeds to offer to purchase some of the Notes at 100% of the principal amount, plus accrued and unpaid interest, if any, to the date of repurchase. See “Description of Secured Notes—Certain Covenants—Limitation on Asset Sales” and “Description of Unsecured Notes—Certain Covenants—Limitation on Assets Sales.” |

Certain Indenture Provisions | The indenture governing the secured exchange notes (the “Secured Notes Indenture”) and the indenture governing the unsecured exchange notes (the “Unsecured Notes Indenture” and, together with the Secured Notes Indenture, the “Indentures”) limits our ability and the ability of our restricted subsidiaries to, among other things; • incur more debt; • redeem stock; • pay dividends or make other distributions to PGP; • issue stock of restricted subsidiaries; • make investments; • create liens; • enter into transactions with affiliates; • merge or consolidate; and • transfer or sell assets. In addition, the Indentures prohibit PGC from holding any assets, becoming liable for any obligations (other than the Notes and borrowings under the PGL Credit Facility) or engaging in any business activities. These covenants are subject to a number of important exceptions. See “Description of Secured Note—Certain Covenants” and “Description of Unsecured Notes—Certain Covenants.” |

| The exchange notes will initially be issued in minimum denominations of $2,000. The exchange notes will be represented by permanent global notes in fully registered form, deposited with a custodian for and registered in the name of a nominee of DTC. Beneficial interests in the global notes will be shown on, and transfers thereof will be effected only through, records maintained by DTC and its participations. |

| U.S. Bank National Association. |

| The exchange notes will be, and the Indentures are, governed by the laws of the State of New York. |

| Because the outstanding notes were issued with original issue discount, or “OID,” for U.S. federal income tax purposes, the exchange notes will be treated as having been issued with OID. In addition to the stated interest on the exchange notes, holders of exchange notes that are U.S. persons for U.S. federal income tax purposes will be required to include the amounts representing the OID in gross income on a constant yield basis in advance of receipt of the cash payments to which such income is attributable. For additional information, see “Certain U.S. Federal Tax Consequences—Tax Consequences to U.S. Holders.” |

| You should consider carefully all of the information set forth in this prospectus and, in particular, you should evaluate the specific factors under “Risk Factors.” |

You should consider carefully the information set forth in this section along with all the other information provided to you in this prospectus before tendering your outstanding notes for exchange notes in the exchange offer.

Risks Relating to the Exchange Notes

Substantial Indebtedness – Our substantial level of indebtedness could adversely affect our financial condition and prevent us from fulfilling our obligations under the exchange notes and our other indebtedness.

We have substantial indebtedness. As of December 31, 2009, we had approximately $539.5 million of total debt outstanding. We and our subsidiaries will be permitted under the Indentures to incur additional indebtedness in the future. If new debt were to be incurred in the future, the related risks could intensify.

Our substantial indebtedness could have important consequences to you and significant effects on our business. For example, it could:

| • | make it more difficult for us to satisfy our obligations under the exchange notes and our other indebtedness; |

| • | result in an event of default if we fail to satisfy our obligations under the exchange notes or our other indebtedness or fail to comply with the financial and other restrictive covenants contained in the Indentures or the PGL Credit Facility, which event of default could result in all of our indebtedness becoming immediately due and payable and could permit our lenders to foreclose on our assets securing such indebtedness; |

| • | require us to dedicate a substantial portion of our cash flow from our business operations to pay our indebtedness, thereby reducing the availability of cash flow to fund working capital, capital expenditures, development projects, general operational requirements and other purposes; |

| • | limit our ability to obtain additional financing to fund our working capital requirements, capital expenditures, debt service, costs to complete the various development projects at DJL, DJW, EVD and ABC and general corporate or other obligations; |

| | |

| • | limit our flexibility in planning for, or reacting to, changes in our business and the industry in which we operate; |

| | |

| • | increase our vulnerability to and limiting our ability to react to changing market conditions, changes in our industry and economic downturns; |

| • | increase our interest expense if there is a rise in interest rates, because a portion of our borrowings may be under our senior credit facilities and, as such, we will have interest rate periods with short-term durations (typically 30 to 180 days) that require ongoing resetting at the then current rates of interest; and |

| | |

| • | place us at a competitive disadvantage compared to competitors that are not as highly leveraged. |

| | |

We expect to obtain the funds to pay our expenses and to pay the amounts due under the exchange notes, the PGL Credit Facility and our other debt primarily from our operations. Our ability to meet our expenses and make these payments thus depends on our future performance, which will be affected by financial, business, economic and other factors, many of which we cannot control. Our business may not generate sufficient cash flow from operations in the future and our currently anticipated growth in revenue and cash flow may not be realized, either or both of which could result in our being unable to pay amounts due under our indebtedness, including the exchange notes, or to fund other liquidity needs. If we do not have sufficient cash flow from operations, we may be required to refinance all or part of our then existing debt (including th e exchange notes), sell assets, reduce or delay capital expenditures or borrow more money. We cannot assure you that we will be able to accomplish any of these alternatives on terms acceptable to us, or at all. In addition, the terms of existing or future debt agreements, including the PGL Credit Facility and the Indentures, may restrict us from adopting any of these alternatives. The failure to generate sufficient cash flow or to achieve any of these alternatives could materially adversely affect the value of the exchange notes and our ability to pay the amounts due under the exchange notes.

Distributions from Subsidiaries – Our ability to make payments under the exchange notes and service our other debt depends on cash flow from our subsidiaries.

We will depend on distributions or other intercompany transfers of funds from our subsidiaries to make payments under the exchange notes and service our other debt. Distributions and intercompany transfers of funds to us from our subsidiaries will depend on:

• their earnings;

• covenants contained in our and their debt agreements, including our existing and any future senior secured credit facilities and the

Indentures;

• covenants contained in other agreements to which we or our subsidiaries are or may become subject;

• business and tax considerations; and

• applicable law, including laws regarding the payment of dividends and distributions.

We cannot assure you that the operating results of our subsidiaries at any given time will be sufficient to make distributions or other payments to us or that any distributions and/or payments will be adequate to pay any amounts due under the exchange notes or our other indebtedness.

Fraudulent Transfer – Under certain circumstances, a court could cancel the guarantees of our subsidiaries.

Unless designated as an unrestricted subsidiary, each domestic subsidiary we form or acquire will be required to guarantee the exchange notes and, solely in the case of a domestic subsidiary that is required to guarantee the secured exchange notes, grant a security interest in certain of its assets (junior to the security interest granted to the lenders under the PGL Credit Facility) to secure its guarantee. Although these guarantees will provide you with a direct claim against the subsidiary guarantors, under federal bankruptcy law and comparable provisions of state fraudulent transfer laws, under certain circumstances a court could void (i.e., cancel) a guarantee and, with respect to the secured exchange notes, the security interest in the guarantor’s assets securing the se cured exchange notes and order the return of any payments made under its guarantee and, with respect to the secured exchange notes, any payments made from any foreclosure of such assets to the guarantor or to a fund for the benefit of its other creditors.

A court might take these actions if it found that when the guarantor entered into its guarantee (or, in some jurisdictions, when payments became due on its guarantee), (i) it received less than reasonably equivalent value or fair consideration for its guarantee, and (ii) any of the following conditions was then satisfied;

| • | the guarantor was insolvent or rendered insolvent by reason of incurring its obligations under its guarantee; |

| • | the guarantor was engaged in a business or transaction for which its remaining assets constituted unreasonably small capital; or |

| • | the guarantor intended to incur, or believed (or reasonably should have believed) that it would incur, debts beyond its ability to pay as those debts matured. |

In applying these factors, a court would likely find that a guarantor did not receive fair consideration or reasonably equivalent value for its guarantee, except to the extent that it benefited directly or indirectly from the Notes Issuance in respect of which its guarantee was given. The determination of whether a subsidiary was or was rendered “insolvent” would vary depending on the law of the jurisdiction being applied. Generally, an entity would be considered insolvent if the sum of its debts (including contingent or unliquidated debts) is greater than all of its property at a fair valuation or if the present fair salable value of its assets is less than the amount that will be required to pay its probable liability on its existing debts (including contingent or unliquidated debts) as they become absolute and matured.

A court might also void a guarantor’s guarantee and with respect to the secured exchange notes, the security interest in its assets securing the secured exchange notes, if the court concluded that the guarantor entered into the guarantee with actual intent to hinder, delay, or defraud creditors. If a court voided a guarantor’s guarantee, a holder of exchange notes would no longer have a claim against that subsidiary and in the case where such holder holds the secured exchange notes, any such assets, and the claims of creditors of such subsidiary would be entitled to be paid in full prior to payments, if any, being made to us to satisfy any claims under the exchange notes. There can be no assurance that such assets of any guarantor whose guarantee in respect of the secured exchange notes was not voided would be sufficient to p ay amounts then due under the secured exchange notes.

Bankruptcy Considerations Regarding the Corporate Form of our Member – We are uncertain how the bankruptcy of our member would affect our ability to continue to operate.

PGP is our sole managing member. Generally, limited liability companies (“LLCs”) are intended to provide both the limited liability of the corporate form for their members and certain advantages of partnerships, including “pass-through” income tax treatment for members, and thus have attributes of both corporations and partnerships, LLCs and their members have been involved in relatively few bankruptcy cases as debtors, and there has been little reported judicial authority addressing bankruptcy issues as they pertain to LLCs. There is some authority that the bankruptcy of a partnership’s general partner may lead to the winding up or dissolution of the partnership. It is possible that a bankruptcy court might hold, by analogy, that an LLC member’s bankruptcy would have a similar effect on a LLC. In the absence of judicial precedent, there can be no assurance as to the effect that the bankruptcy of PGP might have on our ability or the ability of our operating subsidiaries to continue in business.

Restrictive Covenants – The Indentures and the PGL Credit Facility contain covenants that significantly restrict our operations.

The Indentures and the agreement governing the PGL Credit Facility contain, and any other future debt agreements may contain, numerous covenants imposing financial and operating restrictions on our business. These restrictions may affect our ability to operate our business, may limit our ability to take advantage of potential business opportunities as they arise and may adversely affect the conduct of our current business. These covenants place restrictions on our ability and the ability of our restricted subsidiaries to, among other things:

| • | pay dividends, redeem stock or make other distributions or restricted payments; |

| • | incur indebtedness or issue preferred membership interests; |

| • | make certain investments; |

| • | agree to payment restrictions affecting the restricted subsidiaries; |

| • | sell or otherwise transfer or dispose of assets, including equity interests of our restricted subsidiaries; |

| • | enter into transactions with our affiliates; |

| • | designate our subsidiaries as unrestricted subsidiaries; and |

| • | use the proceeds of permitted sales of our assets. |

Our existing senior secured credit facility also requires, and future senior secured credit facilities may require, us to meet a number of financial ratios and tests. Compliance with these financial ratios and tests may adversely affect our ability to adequately finance our operations or capital needs in the future or to pursue attractive business opportunities that may arise in the future. Our ability to meet these ratios and tests and to comply with other provisions governing our indebtedness may be adversely affected by our operations and by changes in economic or business conditions or other events beyond our control. Our failure to comply with our debt-related obligations could result in an event of default under our other indebtedness and if such other indebtedness is accelerated, in whole or in part, could result in an event of de fault under the Indentures.

Change of Control – Our ability to repurchase the exchange notes upon a change of control may be limited.

Upon the occurrence of specific change of control events, we will be required to offer to repurchase all outstanding Notes at 101% of the principal amount, plus accrued and unpaid interest to the date of repurchase. The lenders under the PGL Credit Facility will have the right to accelerate the indebtedness thereunder upon a change of control. Any of our future debt agreements may contain a similar provision. However, we may not have sufficient funds at the time of the change of control to make the required repurchase of Notes or repayment of our other indebtedness. The terms of the PGL Credit Facility also will limit our ability to purchase your Notes until all debt under the PGL Credit Facility is paid in full, all letters of credit issued thereunder are cash collateralized or paid or discharged in full and all commitments to extend cr edit thereunder are terminated. Any of our future debt agreements may contain similar restrictions. If we fail to repurchase any exchange notes submitted in a change of control offer, it would constitute an event of default under the Indentures, which would, in turn, constitute an event of default under the PGL Credit Facility and could constitute an event of default under our other indebtedness, even if the change of control itself would not cause a default. Important corporate events, such as takeovers, recapitalizations or similar transactions, may not constitute a change of control under the Indentures and thus not permit the holders of the exchange notes to require us to repurchase or redeem the exchange notes. See “Description of Secured Notes—Redemption,” “—Repurchase Upon Change of Control” and “—Certain Covenants—Limitation on Asset Sales” and “Description of Unsecured Notes—Redemption,” “—Repurchase Upon Chang e of Control” and “—Certain Covenants—Limitation on Asset Sales.”

Required Regulatory Redemption – Noteholders may be required to be licensed by a gaming authority and, if not so licensed, their Notes will be subject to redemption.

We are required to notify the Iowa Racing and Gaming Commission and the Louisiana Gaming Control Board and the Louisiana State Racing Commission as to the identity of, and may be required to submit background information regarding, each owner, partner or any other person who has a beneficial interest of five percent or more, direct or indirect, in the Company. The Iowa Racing and Gaming Commission, the Louisiana Gaming Control Board and the Louisiana State Racing Commission may also request that we provide them with a list of persons holding beneficial ownership interests in the Company of less than five percent. For purposes of these rules, “beneficial interest” includes all direct and indirect forms of ownership or control, voting power or investment power held through any contract, lien, lease, partnership, stockholding, s yndication, joint venture, understanding, relationship, present or reversionary right, title or interest, or otherwise. The Iowa Racing and Gaming Commission, the Louisiana Gaming Control Board and the Louisiana State Racing Commission may determine that holders of the exchange notes have a “beneficial interest” in the Company.

If any gaming, racing or liquor agencies, including the Iowa Racing and Gaming Commission, the Louisiana Gaming Control Board or the Louisiana State Racing Commission, requires any person, including a record or beneficial owner of the exchange notes, to be licensed, qualified or found suitable, that person must apply for a license, qualification or finding of suitability within the time period specified by the gaming authority. The person would be required to pay all costs of obtaining a license, qualification or finding of suitability. If you are unable or unwilling to obtain such license, qualification or finding of suitability, such agencies and authorities may not grant us or, if already granted, may suspend or revoke our licenses unless we terminate our relationship with you. Under these circumstances, we would be required to repurc hase your exchange notes. There can be no assurance that we will have sufficient funds or otherwise will be able to repurchase any or all of your exchange notes. See “Description of Secured Notes—Redemption—Required Regulatory Redemption” and “Description of Unsecured Notes—Redemption—Required Regulatory Redemption” for more information about regulatory redemptions affecting the exchange notes.

The exchange notes will be issued with original issue discount for U.S. federal income tax purposes.

Because the outstanding notes were issued with OID for U.S. federal income tax purposes, the exchange notes will be treated as having been issued with OID. Therefore, in addition to the stated interest on the exchange notes, holders of exchange notes that are U.S. persons for U.S. federal income tax purposes will be required to include the amounts representing the OID in gross income on a constant yield basis in advance of receipt of the cash payments to which such income is attributable. See “Certain U.S. Federal Income Tax Consequences.”

Risk Factors Relating to Collateral Securing the Secured Exchange Notes

Value of Collateral – The fair market value of the collateral securing the secured exchange notes may not be sufficient to pay the amounts owed under the secured exchange notes. As a result, holders of the secured exchange notes may not receive full payment on their secured exchange notes following an event of default.

The proceeds of any sale of collateral securing the secured exchange notes following an event of default with respect thereto may not be sufficient to satisfy, and may be substantially less than, amounts due on the secured exchange notes. No appraisal has been made of the collateral.

The value of the collateral in the event of liquidation will depend upon market and economic conditions, the availability of buyers and similar factors. The collateral does not include contracts, agreements, licenses (including gaming and liquor licenses) and other rights that by their express terms prohibit the assignment thereof or the grant of a security interest therein. Some of these may be material to us and such exclusion could have a material adverse effect on the value of the collateral. By its nature, some or all of the collateral may not have a readily ascertainable market value or may not be saleable or, if saleable, there may be substantial delays in its liquidation. To the extent that liens, security interests and other rights granted to other parties (including the lenders under the PGL Credit Facility) encumber assets own ed by us, those parties have or may exercise rights and remedies with respect to the property subject to their liens that could adversely affect the value of that collateral and the ability of the trustee under the Secured Notes Indenture (the “Secured Notes Trustee”) or the holders thereof to realize or foreclose on that collateral. Consequently, we cannot assure investors in the secured exchange notes that liquidating the collateral securing the secured exchange notes would produce proceeds in an amount sufficient to pay any amounts due under the secured exchange notes after also satisfying the obligations to pay any creditors with prior claims on the collateral. In addition, under the intercreditor agreement between the Secured Notes Trustee and the lenders under the PGL Credit Facility, described below, the right of the lenders to exercise remedies with respect to the collateral could delay liquidation of the collateral. The gaming licensing process, along with bankruptcy laws and other laws relating to foreclosure and sale, as discussed below, also could substantially delay or prevent the ability of the Secured Notes Trustee or any holder of the secured exchange notes to obtain the benefit of any collateral securing the secured exchange notes. Such delays could have a material adverse effect on the value of the collateral.

The Secured Notes Indenture and the agreements governing our other secured indebtedness also permit us to designate one or more of our restricted subsidiaries as an unrestricted subsidiary. If we designate a restricted subsidiary as an unrestricted subsidiary, all of the liens on any collateral owned by the unrestricted subsidiary or any of its subsidiaries and any guarantees of the secured exchange notes by the unrestricted subsidiary or any of its subsidiaries will be released under the Secured Notes Indenture but not necessarily under the PGL Credit Facility. Designation of an unrestricted subsidiary will reduce the aggregate value of the collateral securing the secured exchange notes to the extent that liens on the assets of the unrestricted subsidiary and its subsidiaries are released. In addition, the creditors of the unrestricted subsidiary and its subsidiaries will have a prior claim (ahead of the secured exchange notes) on the assets of such unrestricted subsidiary and its subsidiaries.

If the proceeds of any sale of collateral are not sufficient to repay all amounts due on the secured exchange notes, the holders of the secured exchange notes (to the extent not repaid from the proceeds of the sale of the collateral), would have only an unsecured claim against our remaining assets.

Lien Subordination – The right of holders of the secured exchange notes to receive payments thereon from proceeds from the sale of collateral securing the secured exchange notes will be effectively subordinated to payments under the PGL Credit Facility to the extent of the collateral securing such credit facility due to the contractual subordination of the liens on the collateral securing the secured exchange notes to those on such collateral that secures such credit facility and subject to the prior claim of purchase money lenders and holders of mechanics’ liens and other permitted liens.

The security interests securing the secured exchange notes and the related guarantees will be contractually subordinated to security interests securing $115 million (which may be increased by $15 million per gaming property that we acquire or construct or in which we invest) in aggregate principal amount of indebtedness that may be incurred under the PGL Credit Facility, pursuant to an intercreditor agreement between Secured Notes Trustee and the lender or lenders under the PGL Credit Facility (or their agent). In addition, lenders of furniture, fixtures and equipment financing and other purchase money indebtedness will have a security interest in the assets securing that indebtedness, although those assets, so long as they secure only such indebtedness, will not secure the se cured exchange notes. As a result, upon any distribution to our creditors, whether or not in bankruptcy, liquidation, reorganization or similar proceedings, or following acceleration of our indebtedness or an event of default under such indebtedness, the lenders under the PGL Credit Facility and the lenders of furniture, fixtures and equipment financing and other purchase money indebtedness will be entitled to be repaid in full from the proceeds of the assets securing such indebtedness before any payment is made to any holder of the secured exchange notes from such proceeds. It is likely that the liquidation of the collateral securing the secured exchange notes would not produce proceeds in an amount sufficient to pay the amounts due on the secured exchange notes after also satisfying the obligations to pay the PGL Credit Facility lenders and purchase money lenders. If the proceeds of any sale of collateral are not sufficient to repay all amounts due on the secured exchange notes, the holders of the secured exchange notes (to the extent not repaid from the proceeds of the sale of the collateral) would have only an unsecured claim against our remaining assets.

In addition, Louisiana law provides contractors, subcontractors and material suppliers with a lien on the property improved by their services or supplies in order to secure their right to be paid. If these parties are not paid in full, they may seek foreclosure on their liens. In Louisiana, the priority of all mechanics’ liens related to a particular construction project relate back to the date on which construction of the project first commenced by any contractor. Accordingly, contractors, subcontractors and suppliers providing goods and services in connection with the construction of the racino who after recordation of the security interests securing the secured exchange notes otherwise comply with the applicable requirements of Louisiana law may have a lien on the racino that is senior in priority to the security interests secur ing the secured exchange notes until they are paid in full. In the event of a liquidation, proceeds from the sale of collateral will be used to pay the holders of any mechanics’ liens then in existence before holders of the secured exchange notes.

The liens on collateral securing the secured exchange notes may also be subject to other liens thereon pursuant to the Secured Notes Indenture. Consequently, the ability of the holders of the secured exchange notes to foreclose upon such collateral or receive any proceeds thereof may be subject to the rights of the holders of such permitted liens.

None of our unrestricted domestic subsidiaries or any foreign subsidiaries that we may designate, form or acquire will guarantee the secured exchange notes. If any of our unrestricted domestic subsidiaries or foreign subsidiaries becomes insolvent, liquidates, reorganizes, dissolves or otherwise winds up, holders of its indebtedness and its trade creditors generally will be entitled to payment on their claims from the assets of such subsidiary before any of those assets would be made available to us.

Limited Remedies – The right of holders of the secured exchange notes to exercise remedies with respect to the collateral securing the secured exchange notes will be limited by an intercreditor agreement between the Secured Notes Trustee and the lenders under the PGL Credit Facility.