SCHEDULE 14A

(Rule 14a-101)

INFORMATION REQUIRED IN PROXY STATEMENT

SCHEDULE 14A INFORMATION

PROXY STATEMENT PURSUANT TO SECTION 14(a) OF

THE SECURITIES EXCHANGE ACT OF 1934

(Amendment No. )

Filed by the Registrant [ ]

Filed by a Party Other than the Registrant [x]

Check the Appropriate Box:

[ ] Preliminary Proxy Statement

[ ] Confidential, for Use of the Commission Only (as permitted by

Rule 14a-6(e)(2))

[ ] Definitive Proxy Statement

[x] Definitive Additional Materials

[ ] Soliciting Material Pursuant to Rule 14a-11(c) or Rule 14a-12

ECHO THERAPEUTICS, INC.

(Name of registrant as specified in its charter)

Platinum Partners Value Arbitrage Fund L.P.

Platinum Long Term Growth VII, LLC

Platinum Partners Liquid Opportunity Master Fund L.P.

Platinum-Montaur Life Sciences, LLC

Platinum Management (NY) LLC

Platinum Liquid Opportunity Management (NY) LLC

Mark Nordlicht

Uri Landesman

Shepard M. Goldberg

(Name of person(s) filing proxy statement, if other than the registrant)

Payment of Filing Fee (Check the Appropriate Box):

[x] No fee required.

[ ] Fee computed on table below per Exchange Act Rules 14a-6(i)(1) and 0-11.

(1) Title of each class of securities to which transaction applies:

(2) Aggregate number of securities to which transaction applies:

(3) Per unit price or other underlying value of transaction computed pursuant to

Exchange Act Rule 0-11 (set forth the amount on which the filing fee is

calculated and state how it is determined):

(4) Proposed maximum aggregate value of transaction:

(5) Total fee paid:

[ ] Fee paid previously with preliminary materials:

[ ] Check box if any part of the fee is offset as provided by Exchange Act

Rule 0-11(a)(2) and identify the filing for which the offsetting fee was paid previously. Identify the previous

filing by registration statement number, or the form or schedule and the date of its filing.

(1) Amount Previously Paid:

(2) Form, Schedule or Registration Statement no.:

(3) Filing Party:

(4) Date Filed:

Platinum Management (NY) LLC, together with the other participants named herein (collectively, “Platinum”), has made a definitive filing with the Securities and Exchange Commission of a proxy statement and an accompanying GOLD proxy card to be used to solicit votes for the election of Platinum’s highly-qualified director nominee at the upcoming 2014 annual meeting of stockholders of Echo Therapeutics, Inc.

On May 30, 2014, Platinum issued the following presentation to stockholders:

WHY REAL CHANGE IS NEEDED NOW AT ECHO THERAPEUTICS, INC. LET’S END THE ERA OF UNDERPERFORMANCE AT ECHO – VOTE THE GOLD PROXY CARD

TABLE OF CONTENTS Pages 3-5 Platinum – Who We Are Pages 6-16 How We Got Here Pages 17-25 Echo’s Track Record of Underperformance Pages 26-35 Platinum - Our Nominee is Highly Qualified, Our Interests Are Aligned, Do Not Be Misled by Echo Page 36 Conclusion *

PLATINUM MANAGEMENT: WHO WE ARE *

WHO WE ARE Platinum is a New York based investment management group with more than $1.3 Billion in assets under management We are the largest stockholder in Echo, owning almost 20% of the Company’s stock Platinum is a long-term investor having made our first investment in Echo in 2007. We have invested more than $18.6M into Echo Platinum was founded in 2003 by Mark Nordlicht, who has more than twenty years of asset management experience Platinum has a long history of working constructively with management teams and board members at Platinum portfolio companies Platinum has been the only source of non-dilutive financing for Echo in years. Only we have recently paid above-market prices to Echo *

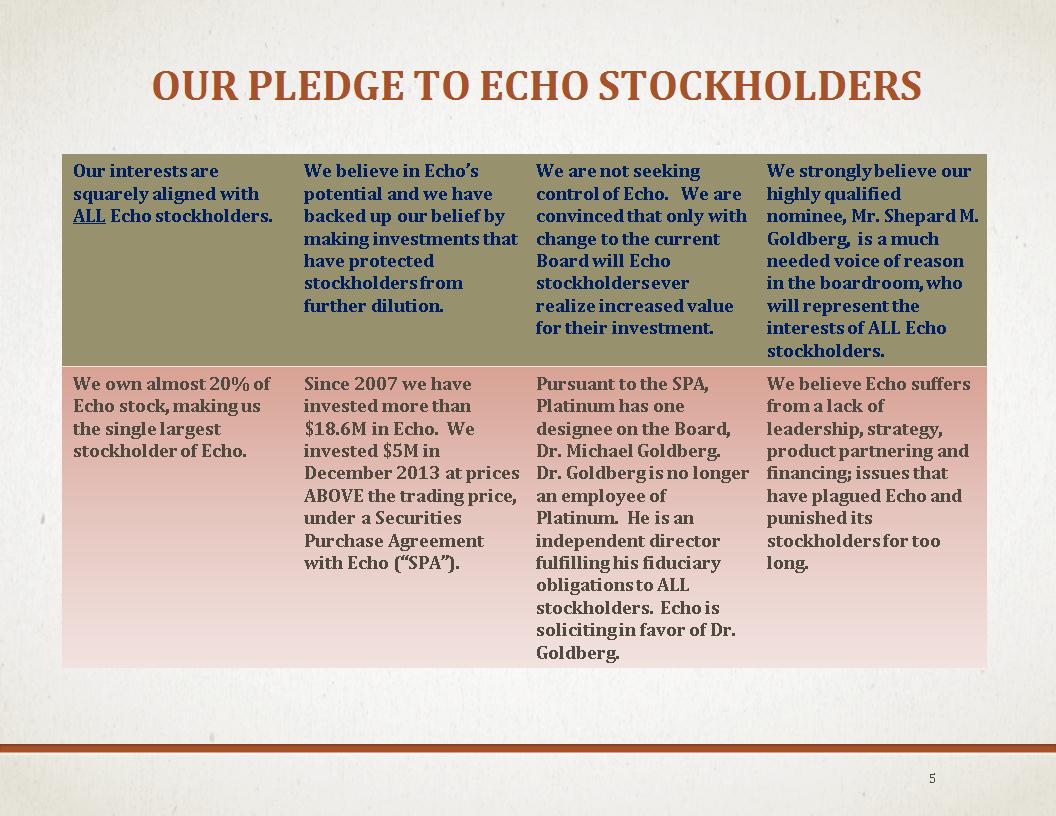

OUR PLEDGE TO ECHO STOCKHOLDERS Our interests are squarely aligned with ALL Echo stockholders. We believe in Echo’s potential and we have backed up our belief by making investments that have protected stockholders from further dilution. We are not seeking control of Echo. We are convinced that only with change to the current Board will Echo stockholders ever realize increased value for their investment. We strongly believe our highly qualified nominee, Mr. Shepard M. Goldberg, is a much needed voice of reason in the boardroom, who will represent the interests of ALL Echo stockholders. We own almost 20% of Echo stock, making us the single largest stockholder of Echo. Since 2007 we have invested more than $18.6M in Echo. We invested $5M in December 2013 at prices ABOVE the trading price, under a Securities Purchase Agreement with Echo (“SPA”). Pursuant to the SPA, Platinum has one designee on the Board, Dr. Michael Goldberg. Dr. Goldberg is no longer an employee of Platinum. He is an independent director fulfilling his fiduciary obligations to ALL stockholders. Echo is soliciting in favor of Dr. Goldberg. We believe Echo suffers from a lack of leadership, strategy, product partnering and financing; issues that have plagued Echo and punished its stockholders for too long. *

PLATINUM : How We Got Here *

ECHO AND ITS BOARD HAVE LOST THE CONFIDENCE OF THE INVESTING PUBLIC Platinum Strongly Believes the Restoration of Investor Confidence in Echo and the Best Path Forward for Echo and its Stockholders Begins with the Election of Our Nominee to the Board. We believe Echo suffers from numerous issues that help explain its downward stock spiral. Echo stock closed at an ALL TIME low of $1.58 on May 27, 2014: Failure of Leadership Deficient and Unclear Corporate Strategy Poor Execution Slow to Find a Partner for its Products Excessive Cost of Capital through Poorly Constructed Dilutive Financings Slow to Act and Ineffective Board *

BACKGROUND Platinum is a long-term investor in Echo, having made our first investment in 2007. We have invested more than $18.6M into Echo. We believe in the Company and in unlocking its awesome potential. After initially being denied access to speak to the independent members of the Board, the Company eventually agreed to engage with us. After private discussions failed, we reluctantly began our public campaign in August of 2013 as soon as it became clear to us that ONLY through public stockholder pressure would the Board take any substantial action. We believe we have been proven correct. On August 30, 2013, we sent a letter to the Board outlining concrete steps Echo should take to stop the destruction of stockholder value. We encourage stockholders to view this letter at http://www.sec.gov/Archives/edgar/data/1031927/000101359413000471/echo13da-083013.htm *

PLATINUM’S PLAN TO UNLOCK VALUE AT ECHO Endless months of Board inaction forced us to publicly announce in 2013 a multi-point plan carefully targeted to address the shortfalls in leadership, strategy, product partnering and financing that have plagued Echo and punished its stockholders through dilution and rampant loss of market value. Our August 30th plan to reverse the destruction of stockholder value included: Immediately remove two incumbent directors and appoint two new directors; Remove ineffective directors and replaces them with professionals who bring key industry experience and informed investor community insight to a Board that has proven incapable of developing Echo's potentially groundbreaking CGM Technology and in communicating with the shareholder base Enter into a partnership for the development and manufacture of the CGM product in mainland China; Present a uniquely valuable opportunity to team with an offshore partner who will bear the burden of developing and marketing the CGM Technology on economically favorable terms Engage a consulting firm to review the Issuer’s product and business development positioning; Engage a premier consulting firm to help the new Board establish and implement a sorely needed strategic vision Hire a new & permanent CEO; Retain a leading recruiting firm to hire a gifted permanent CEO with bona fide medical device development credentials who is not tainted by service on the current underperforming Board Not enter into further financings until the closing of the mainland China transaction, at which time Platinum(and co-investors approved by the board of directors) would invest an additional $10 million in shares of Common Stock at an agreed upon price. Offer financing at a premium to share price that will halt the dilution that has battered the shareholder owners of Echo *

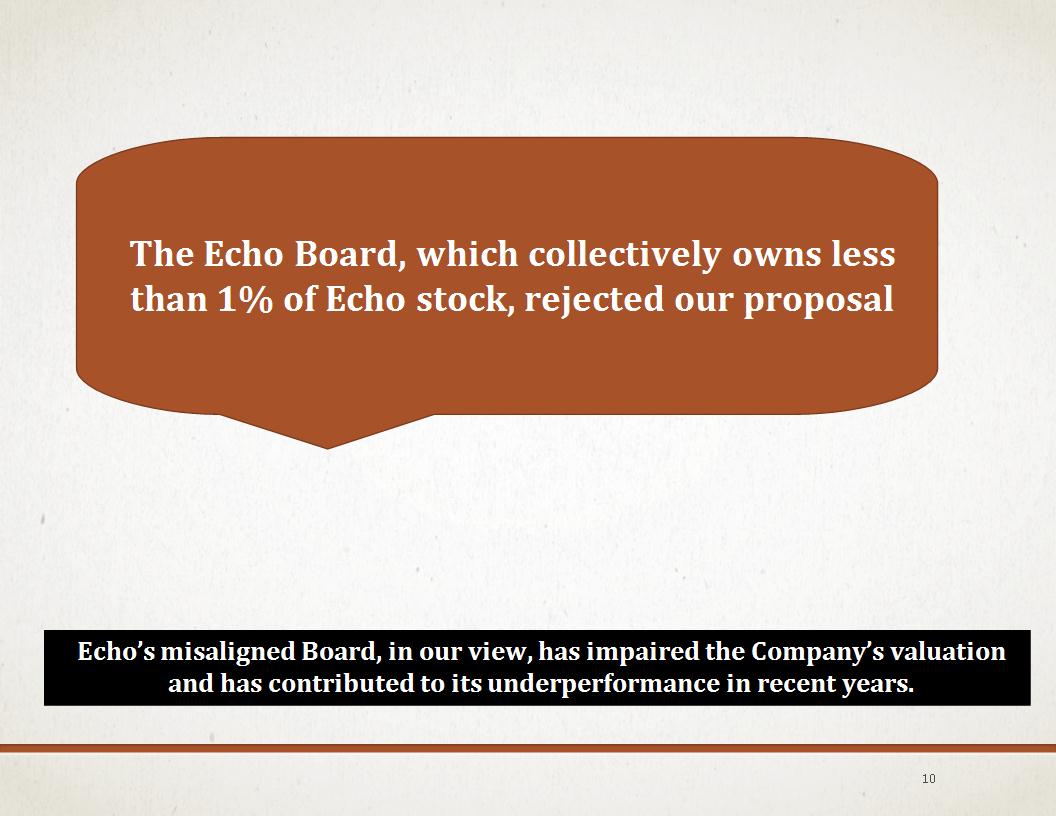

The Echo Board, which collectively owns less than 1% of Echo stock, rejected our proposal Echo’s misaligned Board, in our view, has impaired the Company’s valuation and has contributed to its underperformance in recent years. *

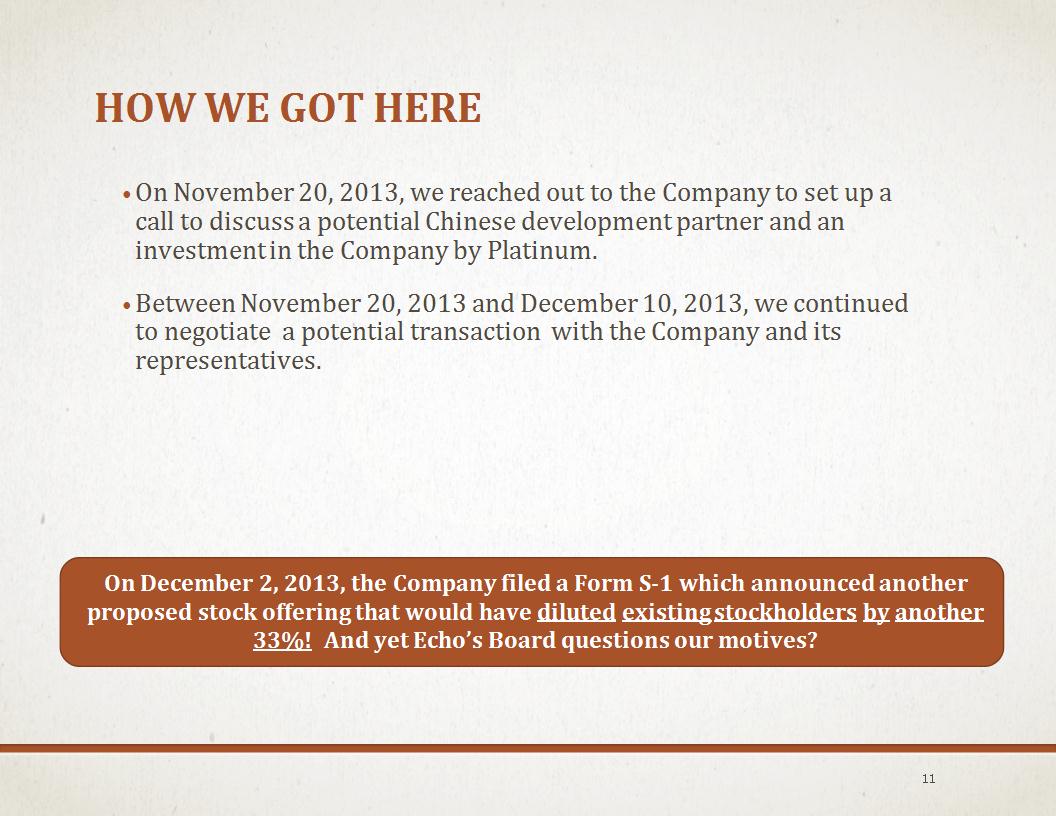

HOW WE GOT HERE On November 20, 2013, we reached out to the Company to set up a call to discuss a potential Chinese development partner and an investment in the Company by Platinum. Between November 20, 2013 and December 10, 2013, we continued to negotiate a potential transaction with the Company and its representatives. On December 2, 2013, the Company filed a Form S-1 which announced another proposed stock offering that would have diluted existing stockholders by another 33%! And yet Echo’s Board questions our motives? *

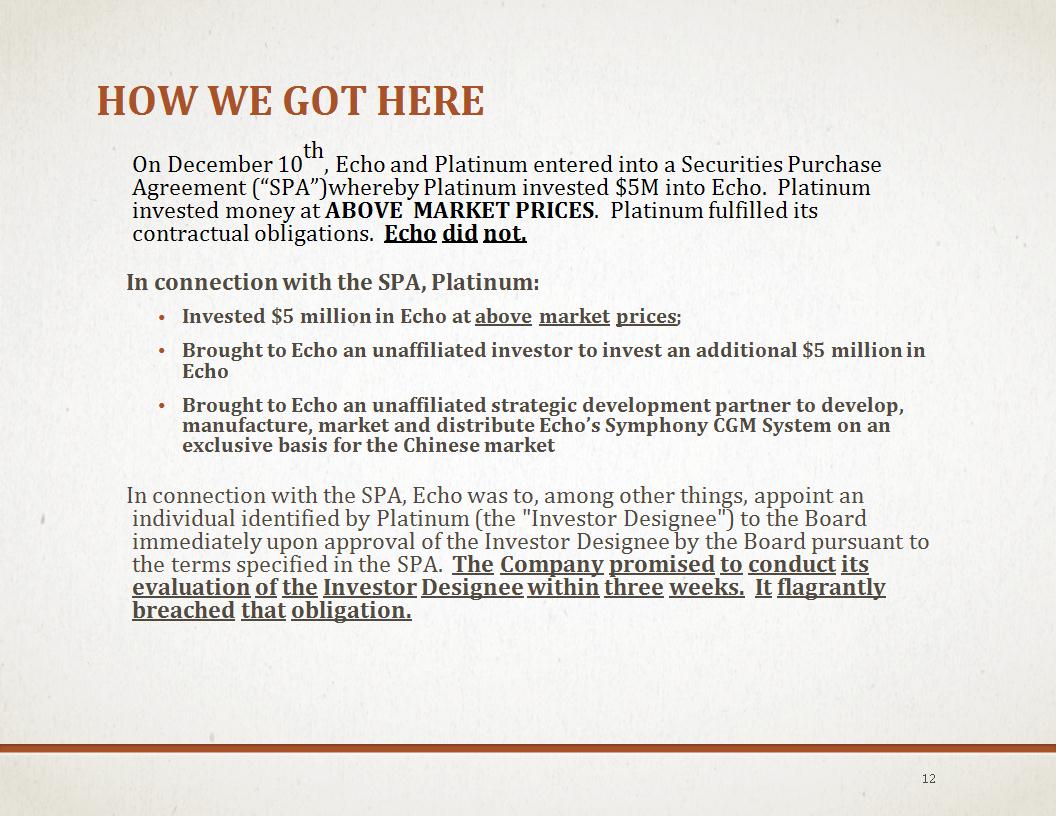

HOW WE GOT HERE On December 10th, Echo and Platinum entered into a Securities Purchase Agreement (“SPA”)whereby Platinum invested $5M into Echo. Platinum invested money at ABOVE MARKET PRICES. Platinum fulfilled its contractual obligations. Echo did not. In connection with the SPA, Platinum: Invested $5 million in Echo at above market prices; Brought to Echo an unaffiliated investor to invest an additional $5 million in Echo Brought to Echo an unaffiliated strategic development partner to develop, manufacture, market and distribute Echo’s Symphony CGM System on an exclusive basis for the Chinese market In connection with the SPA, Echo was to, among other things, appoint an individual identified by Platinum (the "Investor Designee") to the Board immediately upon approval of the Investor Designee by the Board pursuant to the terms specified in the SPA. The Company promised to conduct its evaluation of the Investor Designee within three weeks. It flagrantly breached that obligation. *

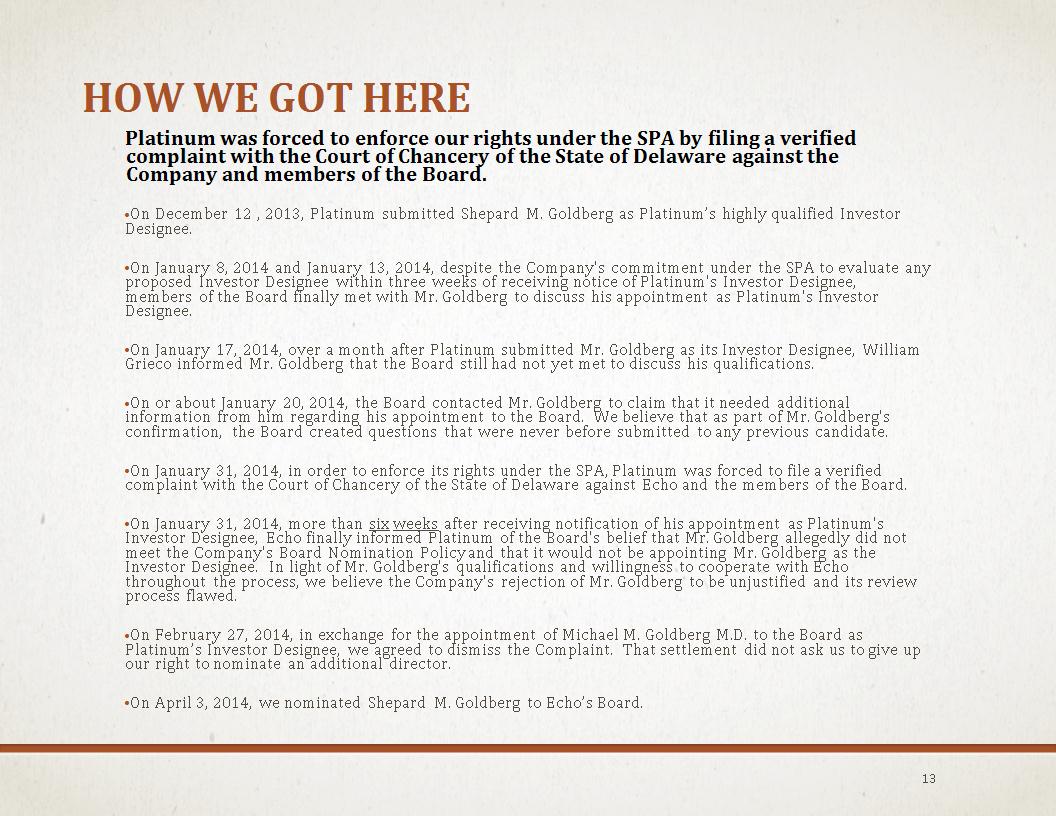

HOW WE GOT HERE Platinum was forced to enforce our rights under the SPA by filing a verified complaint with the Court of Chancery of the State of Delaware against the Company and members of the Board. On December 12 , 2013, Platinum submitted Shepard M. Goldberg as Platinum’s highly qualified Investor Designee. On January 8, 2014 and January 13, 2014, despite the Company's commitment under the SPA to evaluate any proposed Investor Designee within three weeks of receiving notice of Platinum's Investor Designee, members of the Board finally met with Mr. Goldberg to discuss his appointment as Platinum's Investor Designee. On January 17, 2014, over a month after Platinum submitted Mr. Goldberg as its Investor Designee, William Grieco informed Mr. Goldberg that the Board still had not yet met to discuss his qualifications. On or about January 20, 2014, the Board contacted Mr. Goldberg to claim that it needed additional information from him regarding his appointment to the Board. We believe that as part of Mr. Goldberg's confirmation, the Board created questions that were never before submitted to any previous candidate. On January 31, 2014, in order to enforce its rights under the SPA, Platinum was forced to file a verified complaint with the Court of Chancery of the State of Delaware against Echo and the members of the Board. On January 31, 2014, more than six weeks after receiving notification of his appointment as Platinum's Investor Designee, Echo finally informed Platinum of the Board's belief that Mr. Goldberg allegedly did not meet the Company's Board Nomination Policy and that it would not be appointing Mr. Goldberg as the Investor Designee. In light of Mr. Goldberg's qualifications and willingness to cooperate with Echo throughout the process, we believe the Company's rejection of Mr. Goldberg to be unjustified and its review process flawed. On February 27, 2014, in exchange for the appointment of Michael M. Goldberg M.D. to the Board as Platinum’s Investor Designee, we agreed to dismiss the Complaint. That settlement did not ask us to give up our right to nominate an additional director. On April 3, 2014, we nominated Shepard M. Goldberg to Echo’s Board. *

WE BELIEVE THE ECHO BOARD’S RESPONSE TO OUR NOMINATION OF SHEPARD M. GOLDBERG IS JUST ANOTHER REASON TO VOTE FOR CHANGE AT ECHO THERAPEUTICS *

WE BELIEVE ECHO’S RECENT ACTIONS VIOLATED SEC RULES Despite the valid nomination of Mr. Shepard Goldberg to Echo’s Board on April 3, 2014, we believe Echo ignored SEC Rules by not filing a preliminary proxy statement with the SEC in connection with a proxy contest . Our nomination was publicly disclosed to Echo stockholders in a SC13D/A on April 8, 2014: ITEM 4.Purpose of Transaction. Item 4 is hereby amended to add the following: On April 3, 2014, PPVA delivered a letter to the Corporate Secretary of the Issuer nominating Shepard M. Goldberg for election to the Board of Directors of the Issuer (the “Board”) at the 2014 annual meeting of stockholders of the Issuer, or any other meeting of stockholders held in lieu thereof, and any adjournments, postponements, reschedulings or continuations thereof (the “Annual Meeting”). Mr. Goldberg has been nominated for the seat on the Board currently occupied by Robert F. Doman. On April 15, 2014, Echo improperly filed a definitive proxy statement with the SEC (with no mention of our nomination) and began distributing proxy material and soliciting votes for an annual meeting which they scheduled for May 20, 2014. What does this escapade say about Robert Doman’s leadership style? *

WE BELIEVE ECHO’S RECENT ACTIONS VIOLATED SEC RULES On April 22, Echo announced they would set a new record and meeting date and also said: “In light of Platinum’s decision to move forward with its proxy contest and solicit proxies in connection with Echo’s 2014 Annual Meeting, Echo will be filing revised proxy materials with the SEC commenting on Platinum’s opposing solicitation.” On April 24, 2014 Echo finally had to file a preliminary proxy statement complying with the law. Platinum is incredulous, that with multiple law firms and a proxy solicitor retained , Echo was continuing to act as if was unaware of its obligation to file a preliminary proxy statement with the SEC in connection with a contested proxy contest. Moreover, Echo’s stated rationale for finally deciding to abide by SEC rules is insulting to stockholders. Echo used this opportunity to delay their Annual Meeting by 30 days. *

Echo’s Track Record of Underperformance *

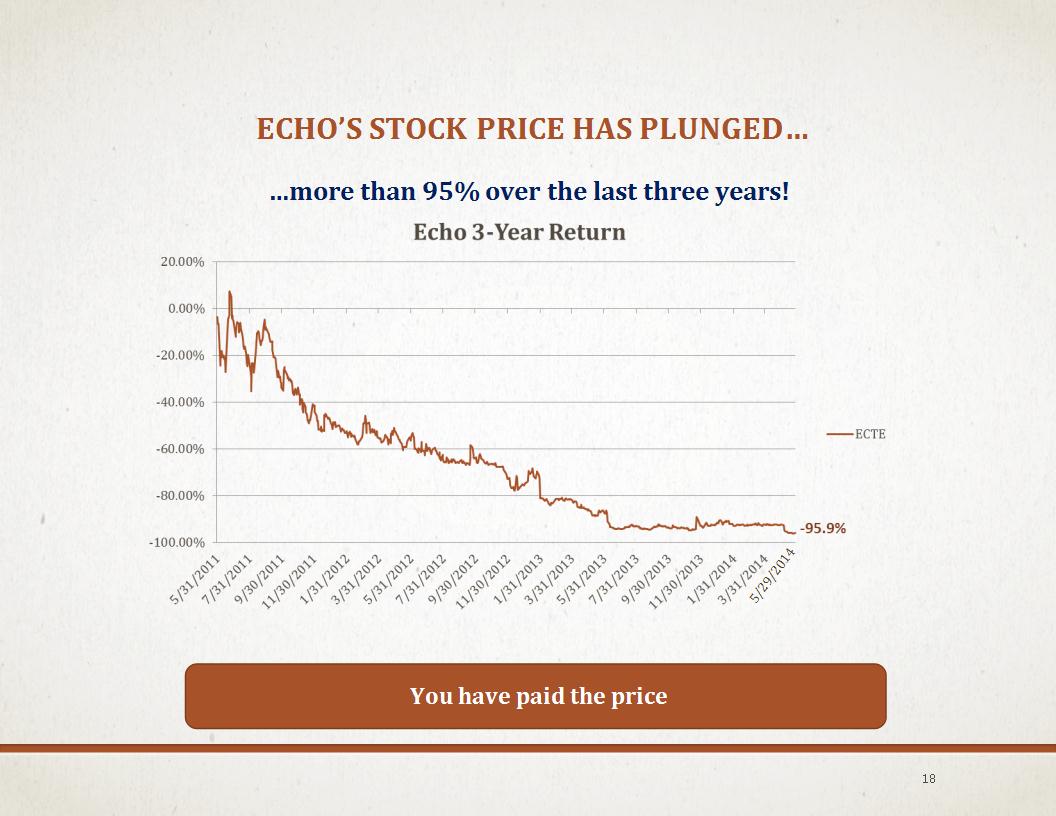

ECHO’S STOCK PRICE HAS PLUNGED… …more than 95% over the last three years! 5/29/2014 * You have paid the price

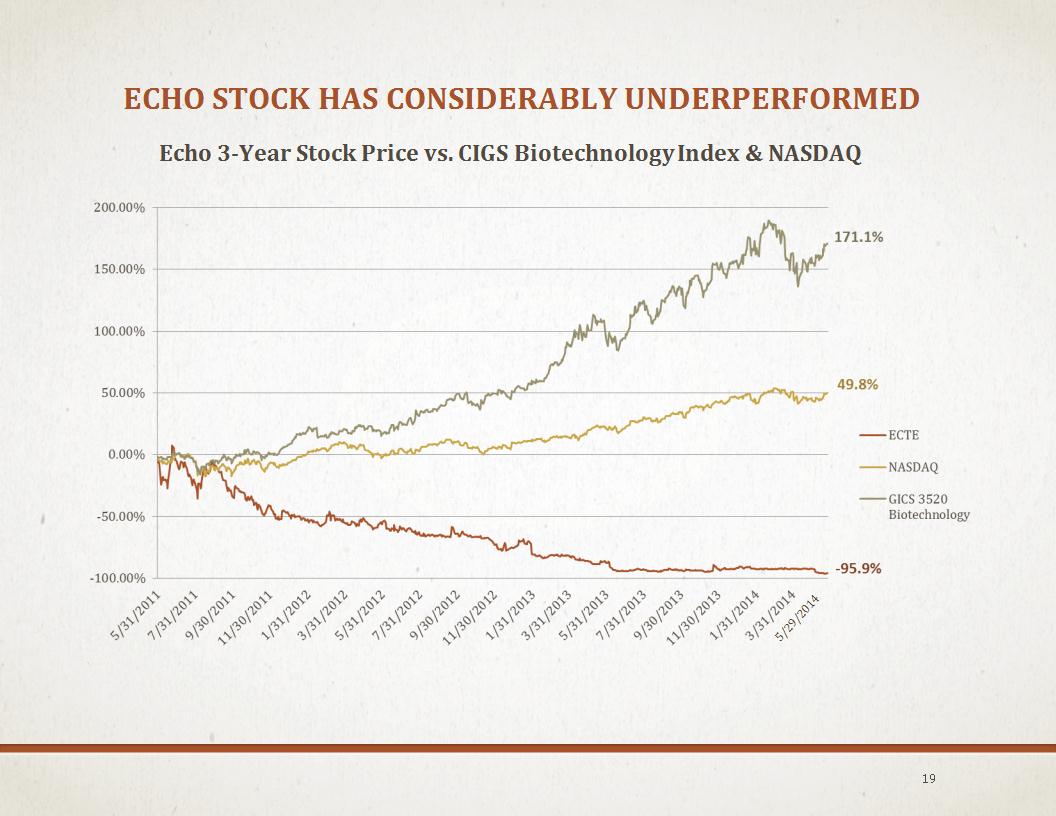

ECHO STOCK HAS CONSIDERABLY UNDERPERFORMED Echo 3-Year Stock Price vs. CIGS Biotechnology Index & NASDAQ 5/29/2014 *

SINCE ROBERT DOMAN WAS NAMED “INTERIM” CEO NINE MONTHS AGO, ECHO HAS DROPPED ANOTHER 34% AND UNDERPERFORMED VS. ALL RELEVANT INDEXES… *

…YET DOMAN, LIKE THE REST OF THE BOARD, HAS BEEN HIGHLY COMPENSATED… Robert Doman has collected over $300,000 in compensation during the Board’s “search” for a permanent CEO in our estimation. After initially receiving $2,500 a day for his services, he now continues to collect $8,000 per week. He presides over a Board, and its various committees, whose members met more than 35 times and collected over $274,000 in fees and awards in 2013. *

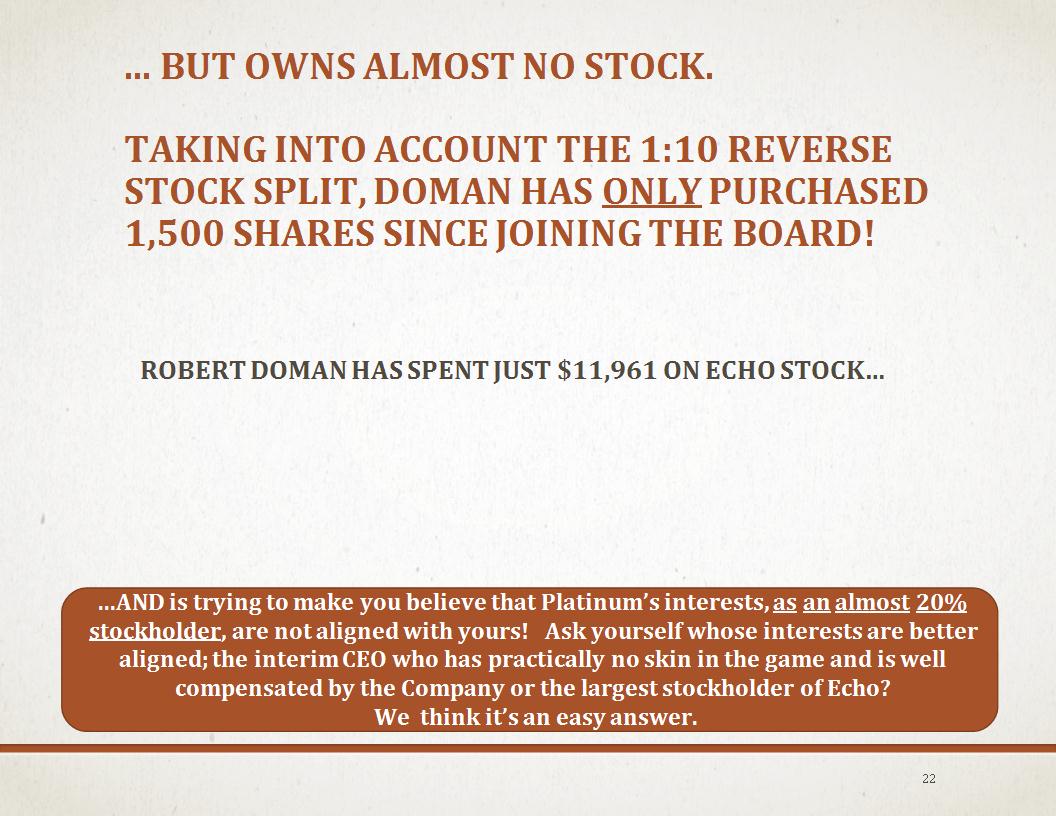

... BUT OWNS ALMOST NO STOCK. TAKING INTO ACCOUNT THE 1:10 REVERSE STOCK SPLIT, DOMAN HAS ONLY PURCHASED 1,500 SHARES SINCE JOINING THE BOARD! ROBERT DOMAN HAS SPENT JUST $11,961 ON ECHO STOCK… ...AND is trying to make you believe that Platinum’s interests, as an almost 20% stockholder, are not aligned with yours! Ask yourself whose interests are better aligned; the interim CEO who has practically no skin in the game and is well compensated by the Company or the largest stockholder of Echo? We think it’s an easy answer. *

PLATINUM BELIEVES THE ELECTION OF OUR NOMINEE IS VITAL TO PROTECTING THE FUTURE VALUE OF YOUR INVESTMENT Failure of leadership Deficient or unclear corporate strategy Poor execution Lethargic in seeking a partner for its products Excessive cost of capital through poorly constructed dilutive financings Slow and ineffective Board Purposeful and petty exclusion of Dr. Goldberg, the newest Board member We believe the Echo Board have been poor stewards of your investment: *

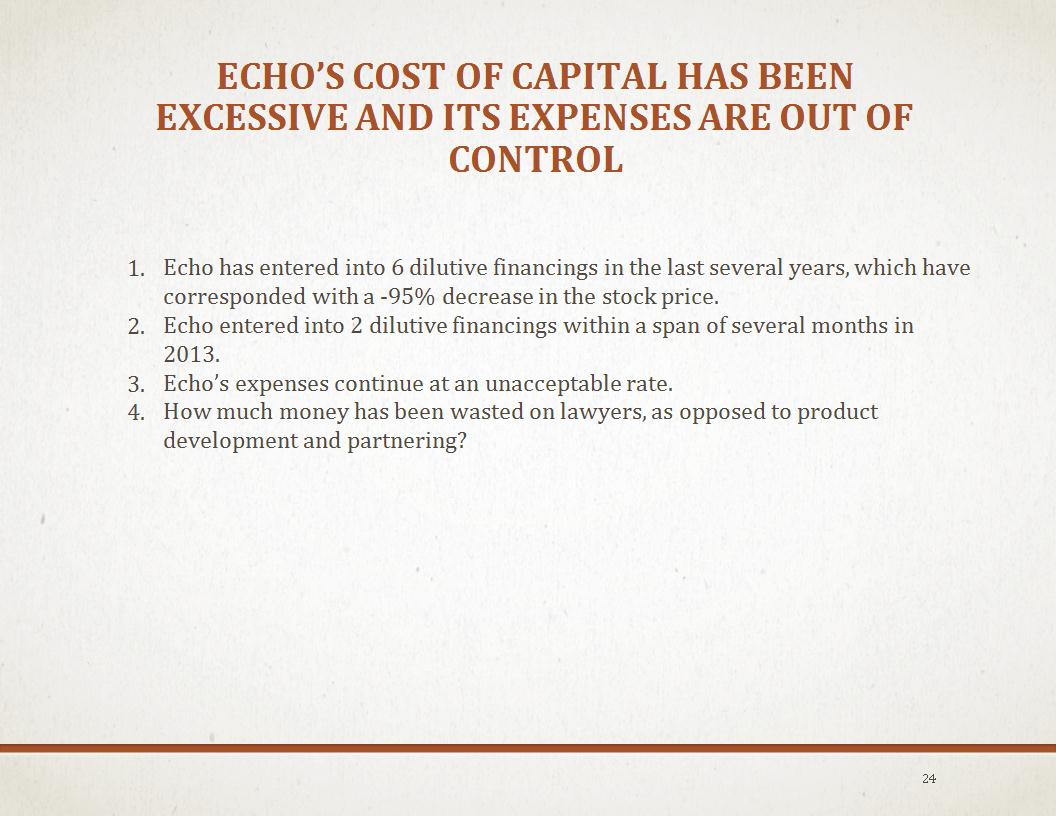

ECHO’S COST OF CAPITAL HAS BEEN EXCESSIVE AND ITS EXPENSES ARE OUT OF CONTROL Echo has entered into 6 dilutive financings in the last several years, which have corresponded with a -95% decrease in the stock price. Echo entered into 2 dilutive financings within a span of several months in 2013. Echo’s expenses continue at an unacceptable rate. How much money has been wasted on lawyers, as opposed to product development and partnering? *

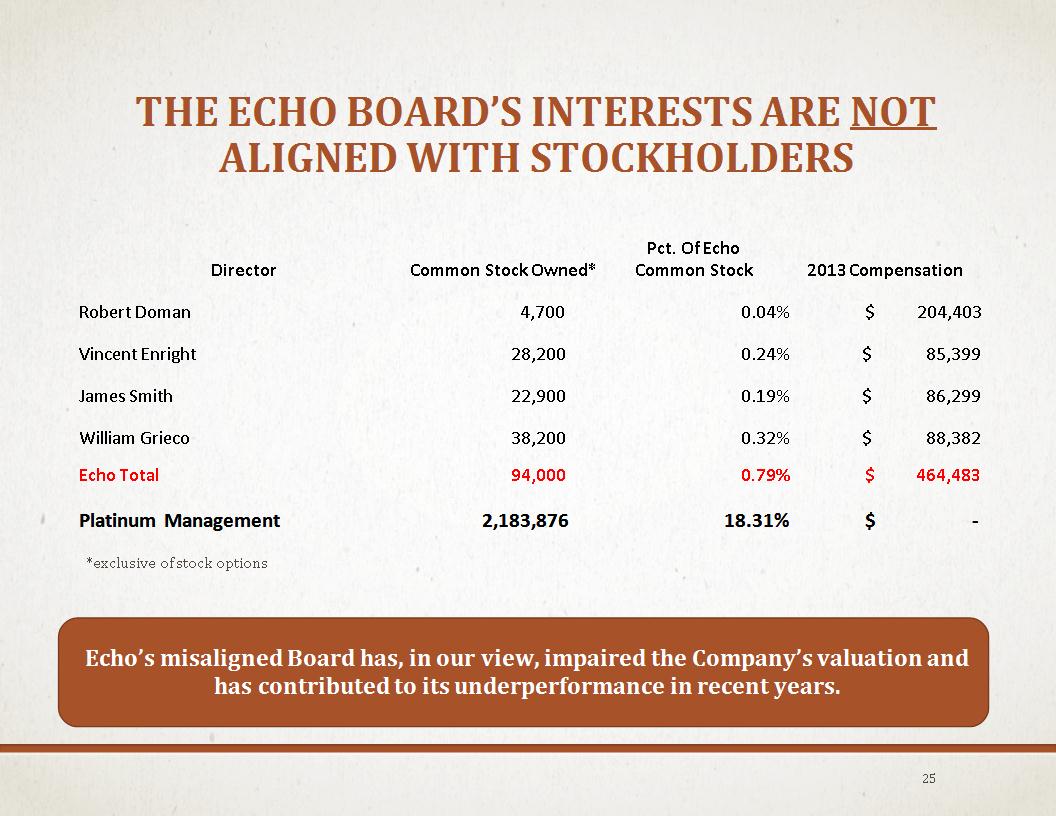

THE ECHO BOARD’S INTERESTS ARE NOT ALIGNED WITH STOCKHOLDERS Echo’s misaligned Board has, in our view, impaired the Company’s valuation and has contributed to its underperformance in recent years. * Director Common Stock Owned* Pct. Of Echo Common Stock 2013 Compensation Robert Doman 4,700 0.04% $ 204,403 Vincent Enright 28,200 0.24% $ 85,399 James Smith 22,900 0.19% $ 86,299 William Grieco 38,200 0.32% $ 88,382 Echo Total 94,000 0.79% $ 464,483 Platinum Management 2,183,876 18.31% $ - *exclusive of stock options

* PLATINUM : Our Nominee is Highly Qualified Our Interests are Aligned with all Stockholders DO NOT BE MISLED BY ECHO

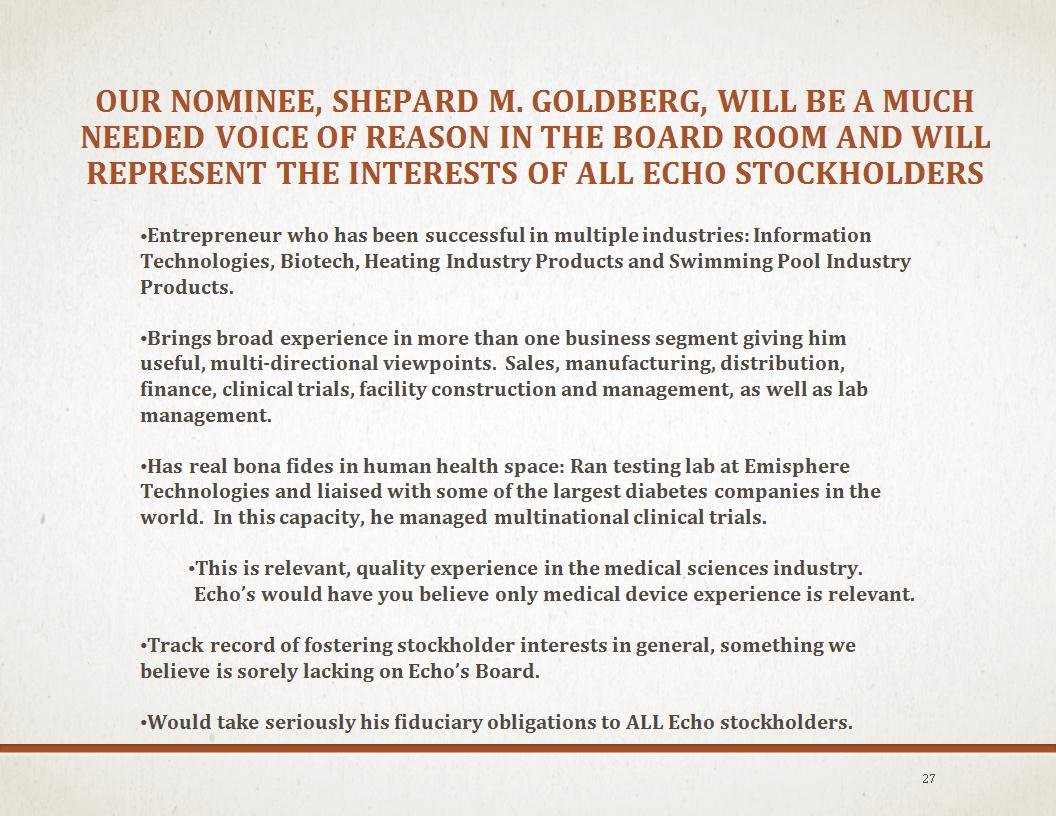

OUR NOMINEE, SHEPARD M. GOLDBERG, WILL BE A MUCH NEEDED VOICE OF REASON IN THE BOARD ROOM AND WILL REPRESENT THE INTERESTS OF ALL ECHO STOCKHOLDERS Entrepreneur who has been successful in multiple industries: Information Technologies, Biotech, Heating Industry Products and Swimming Pool Industry Products. Brings broad experience in more than one business segment giving him useful, multi-directional viewpoints. Sales, manufacturing, distribution, finance, clinical trials, facility construction and management, as well as lab management. Has real bona fides in human health space: Ran testing lab at Emisphere Technologies and liaised with some of the largest diabetes companies in the world. In this capacity, he managed multinational clinical trials. This is relevant, quality experience in the medical sciences industry. Echo’s would have you believe only medical device experience is relevant. Track record of fostering stockholder interests in general, something we believe is sorely lacking on Echo’s Board. Would take seriously his fiduciary obligations to ALL Echo stockholders. *

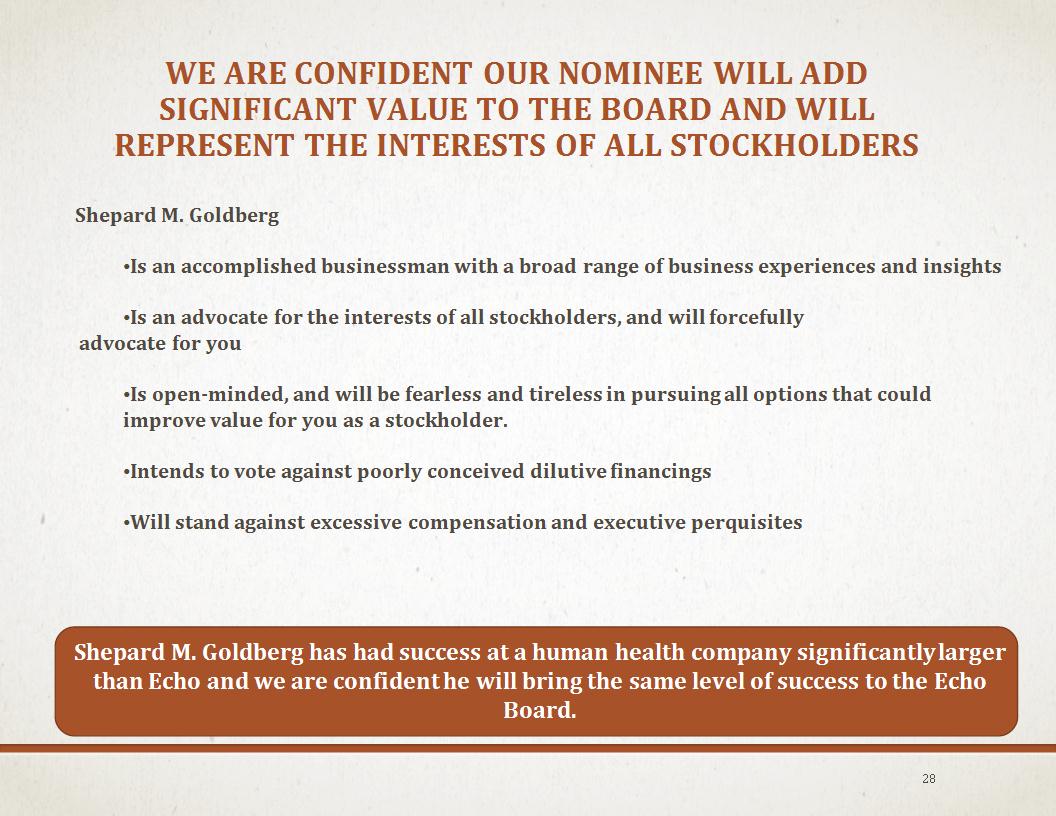

WE ARE CONFIDENT OUR NOMINEE WILL ADD SIGNIFICANT VALUE TO THE BOARD AND WILL REPRESENT THE INTERESTS OF ALL STOCKHOLDERS Shepard M. Goldberg Is an accomplished businessman with a broad range of business experiences and insights Is an advocate for the interests of all stockholders, and will forcefully advocate for you Is open-minded, and will be fearless and tireless in pursuing all options that could improve value for you as a stockholder. Intends to vote against poorly conceived dilutive financings Will stand against excessive compensation and executive perquisites Shepard M. Goldberg has had success at a human health company significantly larger than Echo and we are confident he will bring the same level of success to the Echo Board. *

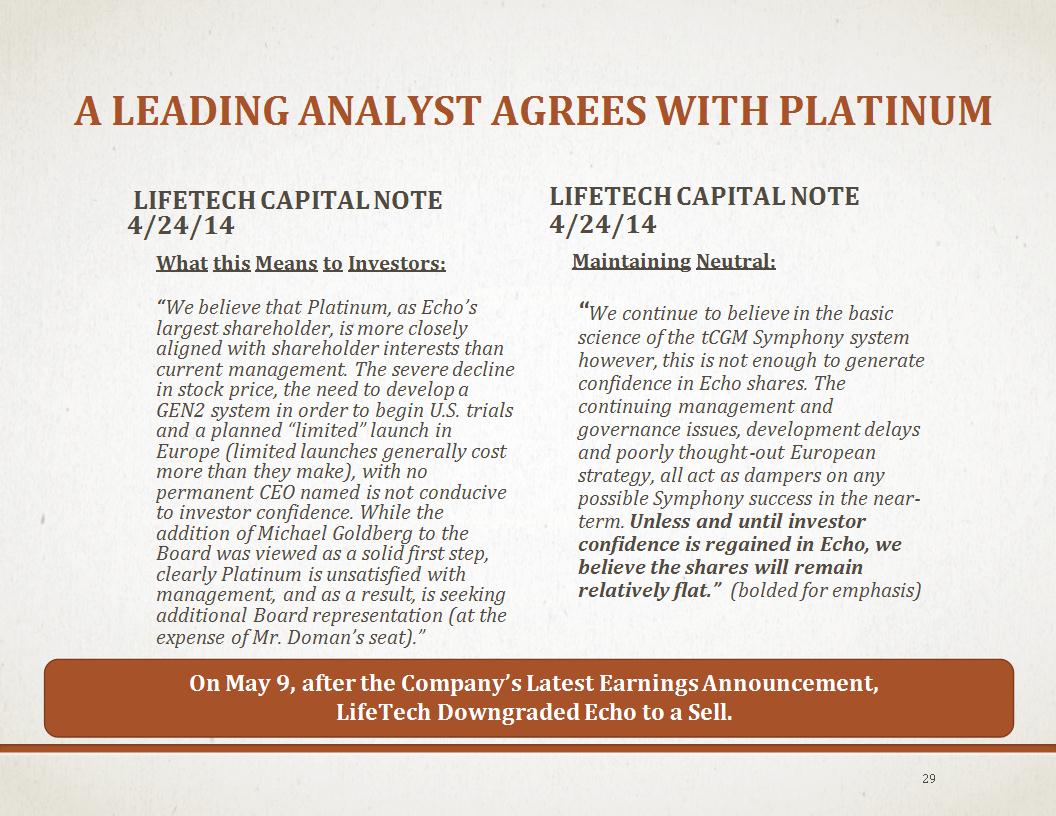

A LEADING ANALYST AGREES WITH PLATINUM LIFETECH CAPITAL NOTE 4/24/14 What this Means to Investors: “We believe that Platinum, as Echo’s largest shareholder, is more closely aligned with shareholder interests than current management. The severe decline in stock price, the need to develop a GEN2 system in order to begin U.S. trials and a planned “limited” launch in Europe (limited launches generally cost more than they make), with no permanent CEO named is not conducive to investor confidence. While the addition of Michael Goldberg to the Board was viewed as a solid first step, clearly Platinum is unsatisfied with management, and as a result, is seeking additional Board representation (at the expense of Mr. Doman’s seat).” LIFETECH CAPITAL NOTE 4/24/14 Maintaining Neutral: “We continue to believe in the basic science of the tCGM Symphony system however, this is not enough to generate confidence in Echo shares. The continuing management and governance issues, development delays and poorly thought-out European strategy, all act as dampers on any possible Symphony success in the near-term. Unless and until investor confidence is regained in Echo, we believe the shares will remain relatively flat.” (bolded for emphasis) On May 9, after the Company’s Latest Earnings Announcement, LifeTech Downgraded Echo to a Sell. *

ANALYST ALSO SAYS… “PROXY BATTLE IS LAST CHANCE FOR INVESTORS “ ON MAY 28TH LIFETECH CAPITAL ALSO STATED, “Echo Board Remains Tone-Deaf: We note with some irony that after a disastrous 2 years where Echo’s stock declined 95% due to multiple poorly executed financings, including an incredibly ill-timed 1 for 10 reverse-split, the Board of Directors is objecting to giving their 20% majority shareholder an additional seat on the board claiming they would not represent all shareholders. Perhaps not, but we believe Platinum Management would represent more shareholders than have been represented in the past. Investors should note that should Platinum fail to gain the board seat at the June 19th shareholder meeting, it is possible they could sell their shares in the open market further depressing the share price.” *

PLATINUM’S IMMEDIATE GOALS IN RESTORING VALUE TO ECHO Immediately find a new and permanent CEO. We publicly urged this Board to find a new CEO back in August of 2013, which they acknowledged was underway. Nine months later there is still no CEO. And, in fact, only two months ago, Echo admitted to having suspended their search and were only beginning to reinitiate their efforts. Analyze optimal ways for the Company to raise capital. We believe there is a stark contrast between Echo’s dilutive philosophy for raising capital and what we consider to be more stockholder-friendly methods. Engage top quality strategic consultant to assist Board in reviewing alternatives to maximize value. Emphasize partnering and push to commercialize products. Cut costs at Board level. Will bring an needed sense of urgency and voice of reason to the Board room. *

We believe in an effort to mislead shareholders, Echo has called into question the veracity and truthfulness of many of our ideas and statements and would have stockholders believe that we have not been genuine in our concerns. Nothing could be further from the truth! WE BELIEVE THE ECHO BOARD’S MISLEADING PROXY CAMPAIGN IS JUST ANOTHER REASON TO VOTE FOR CHANGE AT ECHO THERAPEUTICS *

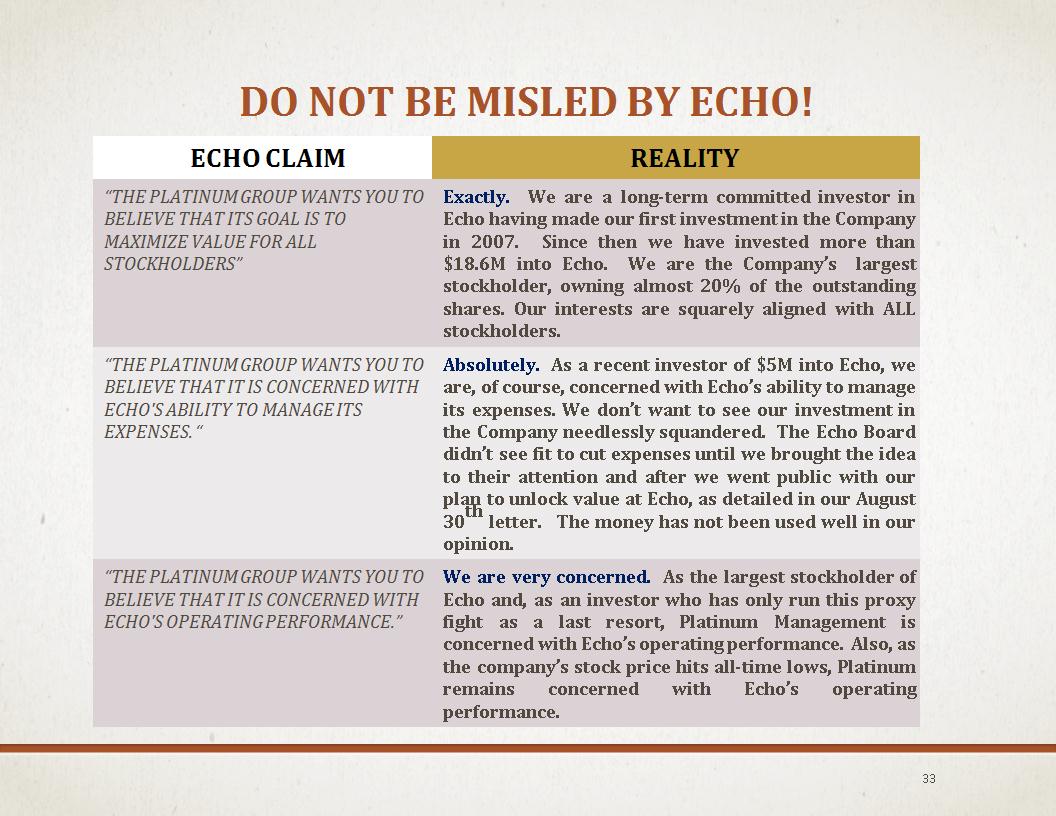

DO NOT BE MISLED BY ECHO! ECHO CLAIM REALITY “THE PLATINUM GROUP WANTS YOU TO BELIEVE THAT ITS GOAL IS TO MAXIMIZE VALUE FOR ALL STOCKHOLDERS” Exactly. We are a long-term committed investor in Echo having made our first investment in the Company in 2007. Since then we have invested more than $18.6M into Echo. We are the Company’s largest stockholder, owning almost 20% of the outstanding shares. Our interests are squarely aligned with ALL stockholders. “THE PLATINUM GROUP WANTS YOU TO BELIEVE THAT IT IS CONCERNED WITH ECHO'S ABILITY TO MANAGE ITS EXPENSES. “ Absolutely. As a recent investor of $5M into Echo, we are, of course, concerned with Echo’s ability to manage its expenses. We don’t want to see our investment in the Company needlessly squandered. The Echo Board didn’t see fit to cut expenses until we brought the idea to their attention and after we went public with our plan to unlock value at Echo, as detailed in our August 30th letter. The money has not been used well in our opinion. “THE PLATINUM GROUP WANTS YOU TO BELIEVE THAT IT IS CONCERNED WITH ECHO'S OPERATING PERFORMANCE.” We are very concerned. As the largest stockholder of Echo and, as an investor who has only run this proxy fight as a last resort, Platinum Management is concerned with Echo’s operating performance. Also, as the company’s stock price hits all-time lows, Platinum remains concerned with Echo’s operating performance. *

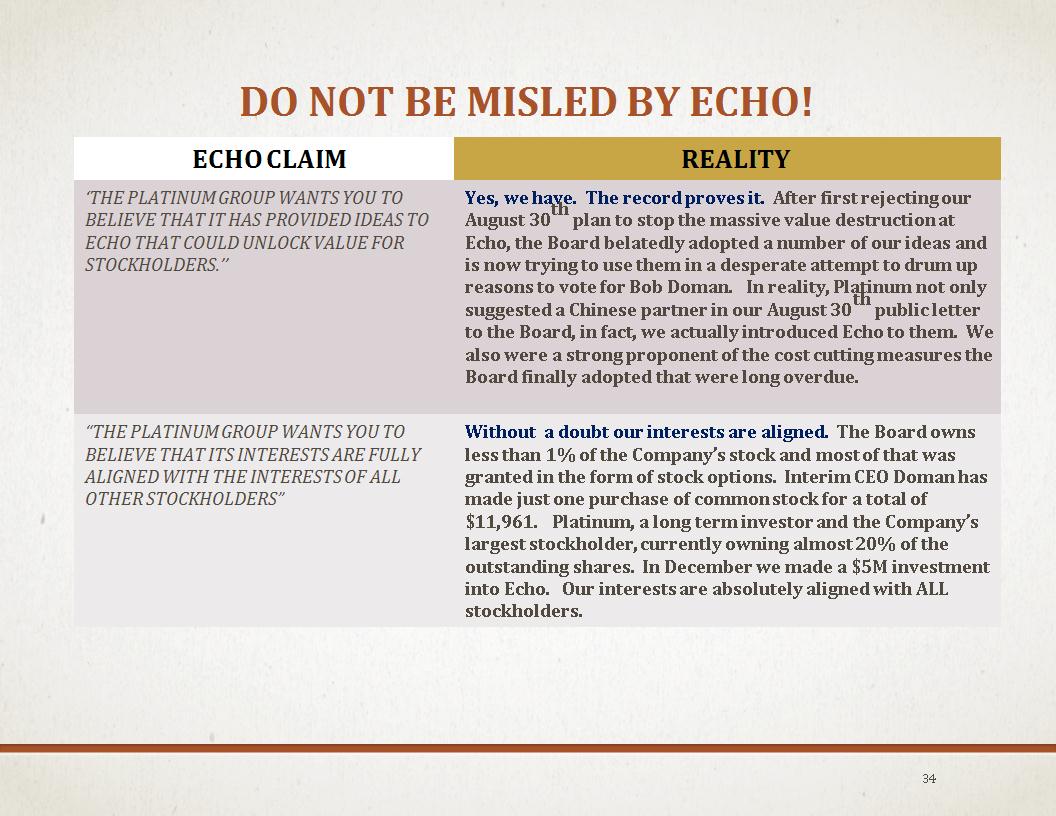

DO NOT BE MISLED BY ECHO! ECHO CLAIM REALITY ‘THE PLATINUM GROUP WANTS YOU TO BELIEVE THAT IT HAS PROVIDED IDEAS TO ECHO THAT COULD UNLOCK VALUE FOR STOCKHOLDERS.’’ Yes, we have. The record proves it. After first rejecting our August 30th plan to stop the massive value destruction at Echo, the Board belatedly adopted a number of our ideas and is now trying to use them in a desperate attempt to drum up reasons to vote for Bob Doman. In reality, Platinum not only suggested a Chinese partner in our August 30th public letter to the Board, in fact, we actually introduced Echo to them. We also were a strong proponent of the cost cutting measures the Board finally adopted that were long overdue. “THE PLATINUM GROUP WANTS YOU TO BELIEVE THAT ITS INTERESTS ARE FULLY ALIGNED WITH THE INTERESTS OF ALL OTHER STOCKHOLDERS” Without a doubt our interests are aligned. The Board owns less than 1% of the Company’s stock and most of that was granted in the form of stock options. Interim CEO Doman has made just one purchase of common stock for a total of $11,961. Platinum, a long term investor and the Company’s largest stockholder, currently owning almost 20% of the outstanding shares. In December we made a $5M investment into Echo. Our interests are absolutely aligned with ALL stockholders. *

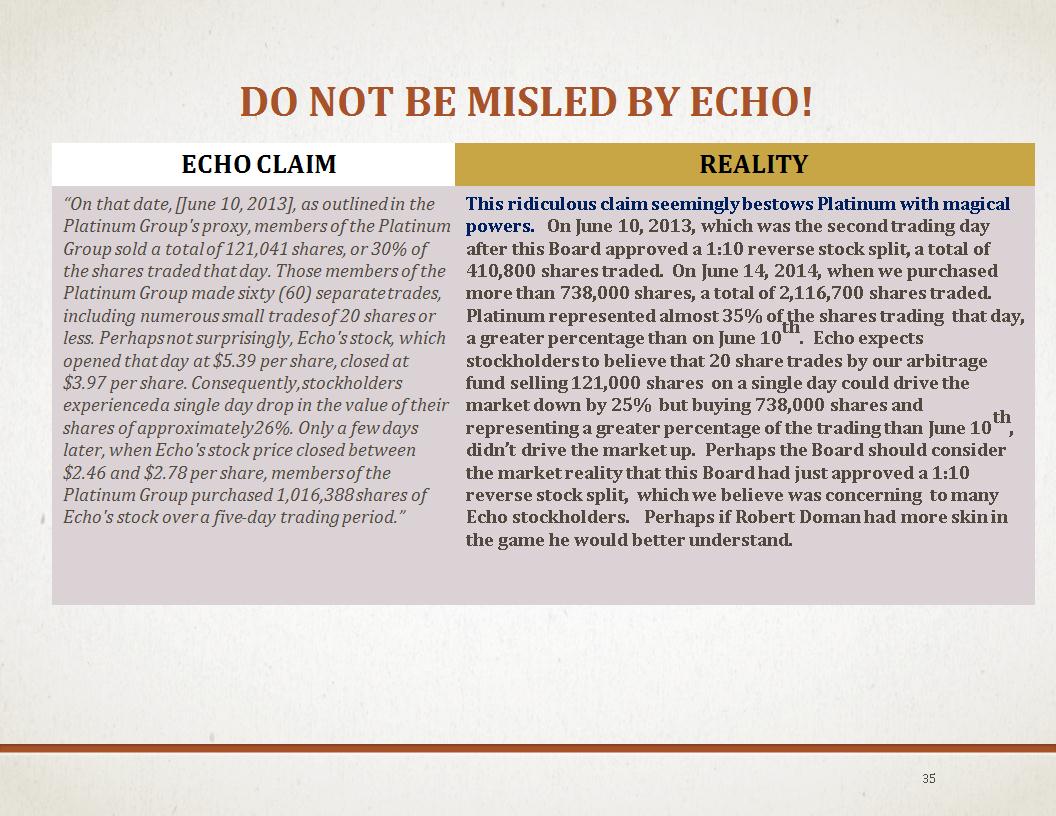

DO NOT BE MISLED BY ECHO! ECHO CLAIM REALITY “On that date, [June 10, 2013], as outlined in the Platinum Group's proxy, members of the Platinum Group sold a total of 121,041 shares, or 30% of the shares traded that day. Those members of the Platinum Group made sixty (60) separate trades, including numerous small trades of 20 shares or less. Perhaps not surprisingly, Echo's stock, which opened that day at $5.39 per share, closed at $3.97 per share. Consequently, stockholders experienced a single day drop in the value of their shares of approximately 26%. Only a few days later, when Echo's stock price closed between $2.46 and $2.78 per share, members of the Platinum Group purchased 1,016,388 shares of Echo's stock over a five-day trading period.” This ridiculous claim seemingly bestows Platinum with magical powers. On June 10, 2013, which was the second trading day after this Board approved a 1:10 reverse stock split, a total of 410,800 shares traded. On June 14, 2014, when we purchased more than 738,000 shares, a total of 2,116,700 shares traded. Platinum represented almost 35% of the shares trading that day, a greater percentage than on June 10th. Echo expects stockholders to believe that 20 share trades by our arbitrage fund selling 121,000 shares on a single day could drive the market down by 25% but buying 738,000 shares and representing a greater percentage of the trading than June 10th, didn’t drive the market up. Perhaps the Board should consider the market reality that this Board had just approved a 1:10 reverse stock split, which we believe was concerning to many Echo stockholders. Perhaps if Robert Doman had more skin in the game he would better understand. *

CONCLUSION LET’S END THE ERA OF UNDERPERFORMANCE AT ECHO THERAPEUTICS. WE URGE ALL ECHO STOCKHOLDERS TO VOTE THE GOLD PROXY CARD FOR REAL CHANGE NOW AT ECHO THERAPEUTICS. THANK YOU FOR YOUR SUPPORT. *