UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

| | |

Investment Company Act file number 811-21609 |

Salomon Brothers Variable Rate Strategic Fund Inc.

|

| (Exact name of registrant as specified in charter) |

| | |

| 125 Broad Street, New York, NY | | 10004 |

| (Address of principal executive offices) | | (Zip code) |

Robert I. Frenkel, Esq.

C/o Citigroup Asset Management

300 First Stamford Place, 4th Floor

Stamford, CT 06902

|

| (Name and address of agent for service) |

Registrant’s telephone number, including area code: (800) 725-6666

Date of fiscal year end: September 30

Date of reporting period: September 30, 2005

| ITEM 1. | REPORT TO STOCKHOLDERS. |

The Annual Report to Stockholders is filed herewith.

EXPERIENCE

ANNUAL REPORT

SEPTEMBER 30, 2005

Salomon Brothers

Variable Rate Strategic Fund Inc.

INVESTMENT PRODUCTS: NOT FDIC INSURED Ÿ NO BANK GUARANTEE Ÿ MAY LOSE VALUE

Salomon Brothers Variable Rate Strategic Fund Inc.

Annual Report • September 30, 2005

What’s

Inside

Fund Objective

The Fund’s investment objective is to maintain a high level of current income.

Letter from the Chairman

R. JAY GERKEN, CFA

Chairman and Chief Executive Officer

Dear Shareholder,

There was no shortage of potential threats to the U.S. economy during the reporting period. These included record high oil prices, rising short-term interest rates, the devastation inflicted by Hurricanes Katrina and Rita, geopolitical issues, and falling consumer confidence. However, the economy proved to be surprisingly resilient during the fiscal year of this report. Fourth quarter 2004 and first quarter 2005 gross domestic product (“GDP”)i growth was 3.8% and second quarter GDP growth was 3.3%, another solid advance. This marked nine consecutive quarters in which GDP grew 3.0% or more.

The Federal Reserve Board (“Fed”)ii continued to raise interest rates over the period in an attempt to ward off inflation. After raising rates in June, August, and September 2004, the Fed increased its target for the federal funds rateiii in 0.25% increments eight additional times. All told, the Fed’s 11 rate hikes have brought the target for the federal funds rate from 1.00% to 3.75% by the end of the period of this report. This also represents the longest sustained Fed tightening cycle since 1977-1979. Following the end of the Fund’s reporting period, at its November meeting, the Fed once again raised the target rate by 0.25% to 4.00%.

During much of the reporting period, the fixed income market confounded investors as short-term interest rates rose in concert with the Fed rate tightening, while longer-term rates, surprisingly, declined. When the period began, the federal funds target rate was 1.75% and the yield on the 10-year Treasury was 4.21%. When the reporting period ended, the federal funds rate had risen to 3.75%. Due to a spike in September, the 10-year yield finished the period at 4.29%, slightly higher than when the period began, but still lower than its yield of 4.62% when the Fed began its tightening cycle on June 30, 2004. Looking at the one-year period

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 1

as a whole, the overall bond market, as measured by the Lehman Brothers Aggregate Bond Indexiv returned 2.80%.

The high yield market experienced several periods of volatility during the reporting period. After a strong start, high yield bonds fell sharply in March and April 2005 as investors became concerned over the bond downgrades for General Motors and Ford Motor Company. However, the high yield market then rallied as the uncertainty surrounding the downgrades lifted and investors searched for incremental yield. Over the one-year period, the Citigroup High Yield Market Indexv returned 6.49%.

During the one-year period, emerging markets debt, as represented by the JPMorgan Emerging Markets Bond Index Global (“EMBI Global”)vi returned 14.00%. Improving country fundamentals and strong market technicals outweighed the downward pressure exerted throughout the period by Fed tightening. In addition, continued strength in commodity prices, including metals, agriculture, and oil, supported many emerging market countries.

Please read on for a more detailed look at prevailing economic and market conditions during the Fund’s most recent fiscal year and to learn how those conditions have affected Fund performance.

Special Shareholder Notice

On June 24, 2005, Citigroup Inc. (“Citigroup”) announced that it has signed a definitive agreement under which Citigroup will sell substantially all of its worldwide asset management business to Legg Mason, Inc. (“Legg Mason”).

As part of this transaction, Salomon Brothers Asset Management Inc (the “Manager”), currently an indirect wholly owned subsidiary of Citigroup, would become an indirect wholly owned subsidiary of Legg Mason. The Manager is the investment manager to the Fund.

The transaction is subject to certain regulatory approvals, as well as other customary conditions to closing. Subject to such approvals and the satisfaction of the other conditions, Citigroup expects the transaction to be completed later this year.

Under the Investment Company Act of 1940, consummation of the transaction will result in the automatic termination of the investment advisory contract between the Fund and the Manager. Therefore the Fund’s Board of Directors has approved a new investment advisory contract between the Fund and the Manager to become effective upon the closing of the sale to Legg Mason. The new investment advisory contract has been presented to shareholders for their approval.

Information About Your Fund

As you may be aware, several issues in the mutual fund industry have recently come under the scrutiny of federal and state regulators. The Fund’s Manager and some of its affiliates

2 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

have received requests for information from various government regulators regarding market timing, late trading, fees, and other mutual fund issues in connection with various investigations. The regulators appear to be examining, among other things, open-end fund’s response to market timing and shareholder exchange activity, including compliance with prospectus disclosure related to these subjects. The Fund has been informed that the Manager and its affiliates are responding to those information requests, but are not in a position to predict the outcome of these requests and investigations.

Important information concerning the Fund and its Manager with regard to recent regulatory developments is contained in the Notes to the Financial Statements included in this report.

As always, thank you for your confidence in our stewardship of your assets. We look forward to helping you continue to meet your financial goals.

Sincerely,

R. Jay Gerken, CFA

Chairman and Chief Executive Officer

November 1, 2005

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 3

Manager Overview

Investment Grade Market Review

During the 12 months ended September 30, 2005, markets were primarily driven by Fed activity, employment and inflation data and rising energy costs, exacerbated near period end by the devastating impact of Hurricane Katrina on the U.S. Gulf Coast. The Fed’s eight “measured” 25-basis-pointvii hikes during the period brought the federal funds rate to 3.75% from 1.75% by the end of the period. Following the end of the Fund’s reporting period, at its November meeting, the Fed once again raised the target rate by 0.25% to 4.00%. This exerted upward pressure on short-term bond yields, driving 2-year yields up about 156 basis points during the 12 months covered by this report. However, in what Fed Chairman Alan Greenspan termed a “conundrum,” long-term bond yields did not begin to rise and, in fact, continued to decline. Ten-year yields visited levels well below 4.00% during the 12 months of this report before leveling approximately 30 basis points lower by the end of the period. This sharp rise in short-term yields and continued decline in long-term yields resulted in the extensive yield curveviii flattening seen during the period.

As the market fully expected each 25-basis-point hike in the federal funds rate during the period — thanks to the Fed’s well-advertised intentions to raise rates at a measured pace — investors spent much of the period dissecting language from the Fed for clues on its assessment of the U.S. economy and the pace of rate hikes. The Fed reiterated throughout the year that it would increase rates “at a pace that is likely to be measured” and, starting in June 2004, added that, “the Committee will respond to changes in economic prospects as needed to fulfill its obligation to maintain price stability.” In its most recent statement (from the September 20th meeting), the Fed noted that core inflation remained low and long-term inflation expectations remained “contained” (even if the language was downgraded from the “well contained” language used at prior meetings).

Slowing global growth, rising inflation and surging oil prices undoubtedly restrained economic activity during the period, with GDP declining year-over-year to 3.8% growth in first quarter 2005 (from first quarter 2004’s 4.5% pace) and to 3.4% growth in second quarter 2005 (from second quarter 2004’s 3.5%). Although growth remained strong throughout the period, fears of potential slowing, combined with increasing inflation, drove markets. Oil prices, which breached $70 per barrel before the reporting period’s end, continue to cast a pall on growth and consumer spending expectations. This was particularly true in the latter half of the period, as investors assessed the potential impact on U.S. economic growth of Hurricanes Katrina and Rita, inflation and the pace of interest rates caused growth indicators to turn increasingly mixed. For example, the U.S. labor market began to pick up in early 2004 and continued to improve through most of the Fund’s most recent fiscal year, although the pace of improvement remained uneven from month to month. Unemployment fell through the majority of the period, declining from 5.4% in September 2004 to 4.9% in August 2005. However, most recent unemployment numbers skyrocketed, even if not as much as expected, in the wake of Hurricane Katrina, and the unemployment rate rose to 5.1% in September. Industrial production and retail sales also

4 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

remained positive through most of the period, even considering the volatility in the auto sector as General Motors and Ford were successively downgraded by three major credit rating agencies to below investment grade. Again, however, as with employment, industrial production and retail sales data turned negative near the reporting period’s end as the effects of Hurricane Katrina roiled through the economy, reductions in auto production hit the market and the highly successful automotive dealer incentive packages offered through the summer came to an end.

Core inflation rates remained relatively subdued throughout the period, with only first quarter 2005 seeing moderate increases, despite growing inflationary pressure from continually high and rising energy prices. Despite some volatility month to month, Core Consumer Price Index (CPI) inflation remained constant year-over-year, and core Producer Price Index (PPI) edged up only 0.7% in September 2005 versus September 2004. The core PCE deflator, which is the Fed’s preferred measure of inflation, increased 0.9% year-over-year in the latest August reading.

High Yield Market Review

During the 12 months ended September 30, 2005, the high yield market, as represented by the Citigroup High Yield Market Index, returned 6.49%. High yield debt markets rallied from the start of the period in September 2004 through the remainder of 2004 as investors gained confidence that inflation was contained and the Fed would continue to raise rates at a “measured pace.” Reduced U.S. Treasury market volatility, combined with the continued low interest rate environment, set a positive tone for high yield, engendering generally positive mutual fund flows and contributing both to the record number of deals that came to market during 2004 and strong demand for higher yielding assets. Additionally, default rates reached 20-year lows as the improving economy and the low interest rate environment enabled companies to extend their debt maturities and improve their liquidity.

Rising oil prices, weak equity markets and isolated hawkish comments from the Fed regarding inflation led the market down in the first few months of 2005. The steady stream of negative auto sector headlines through Spring 2005, including General Motor’s unexpected negative earnings warning in mid-March and Ford’s reduced earnings guidance and second quarter production cuts announced in late April, reintroduced investor fears of both companies’ potential downgrades to high yield status. This caused spreads to widen dramatically within the auto sector and across fixed income credit markets. Markets began recovering in mid-May on stronger technicals, positive economic developments and S&P and Fitch’s long-anticipated downgrades of Ford and GM to non-investment grade. The rating agencies’ actions removed some of the uncertainty in the market surrounding the credits’ ultimate resting places, allowing both high yield and investment grade investors to shore up their positions.

Improving technicals, better overall demand and the relative absence of further negative headlines continued to buoy markets through June and July, despite a stronger new issue

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 5

calendar in June and renewed outflows from high yield mutual funds. Resurgent investor risk appetites on the back of strong U.S. economic news and positive 2Q earnings announcements also contributed to positive performance, allowing markets to outperform despite the July 7th terrorist bombings in London (and the July 21st reprise) and weaker consumer sentiment.

However, higher-than-expected August new issuance, combined with stronger inflation, increasingly mixed economic data and rising energy prices, slowed activity near the end of the reporting period, although low trading volumes and light issuance in the latter half of August (ahead of the Labor Day holiday) kept markets in positive territory. High yield markets continued to decline through September end, registering the first month of negative performance since April 2005, as volatility in the auto sector, higher energy costs, rising inflation and fears of a potentially slowing economy in the aftermath of Hurricane Katrina converged with abundant new supply and continued retail outflows following the Labor Day holiday.

Based on the 7.85% yieldix of the Citigroup High Market Yield Index as of September 30, 2005, we believe high-yield bonds continued to offer competitive yields relative to U. S. Treasury notes.x However, high-yield issues are subject to additional risks, such as the increased possibility of default because of their lower credit quality, and yields and prices will fluctuate.

Emerging Markets Debt Review

Emerging markets debt returned 14.00% during the 12 months ended September 30, 2005, as represented by the EMBI Global. Strong country fundamentals and market technicals offset the downward pressure exerted by increases in the federal funds rate throughout the 12 months of this report and credit contagion from the auto sector during the volatile Spring of 2005. Continued progress on political and economic reform in many emerging countries and the generally positive macro environment supported broad credit quality improvements across emerging markets during the 12 months of this report.

Sovereign debt markets achieved positive momentum at the start of the period of this report after recovering from depressed levels earlier in 2004 and rallied through the remainder of the year. Positive returns were supported by strong underlying country fundamentals, commodity prices strength (particularly in metals, agriculture and oil) and relatively low U.S. Treasury market volatility. Emerging debt continued to trend positive during the first two months of 2005 despite concerns over the path of U.S. interest rates, risks of higher inflation and new bond issuance weighing on the market. However, indications of potentially more aggressive tightening (50-basis-point increments) from the Fed and increasingly prominent inflation worries led the market down in March, broadly in line with the U.S. Treasury market. Emerging debt markets remained under pressure in early April as spillover from volatile credit markets, with the highly visible troubles in the auto sector, worsened technicals.

6 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Markets turned again by mid-April and followed a generally upward trajectory through the remainder of the period as U.S. Treasury market volatility declined, the U.S. equity market recovered and country fundamentals remained broadly supportive. Although sovereign market volatility trended upward near the end of the period of this report, emerging markets proved relatively resilient, boosted by strong investor demand for greater risk assets despite the early July terrorist bombings in London, continued political noise in key emerging countries and increasing volatility in U.S. Treasuries.

Spreads tightened 174 basis points during the 12-month period ended September 30, 2005, closing at 235 basis points over U.S. Treasuries. Of note, sovereign spreads tightened 67 basis points alone during the month of June 2005 due primarily to index rebalancing with the conclusion of the Argentine bond exchange. Over the period of this report, 12-month return volatility stood at 4.69%,xi substantially below long-term, historical levels of approximately 16%.

Performance Review

Since the Fund’s inception on October 26, 2004 through September 30, 2005, the Salomon Brothers Variable Rate Strategic Fund Inc. returned –9.82%, based on its New York Stock Exchange (“NYSE”) market price and 7.06% based on its net asset value (“NAV”)xii per share. In comparison, the Fund’s unmanaged benchmark, the Lehman Brothers Aggregate Bond Index returned 1.94% 10/31/04-9/30/05 month-end only. The Lipper Global Income Closed-End Funds Category Averagexiii increased 6.09% from October 31, 2004 through September 30, 2005. Please note that Lipper performance returns are based on a Fund’s NAV.

During the period ended September 30, 2005, the Fund made distributions to shareholders totaling $0.8975 per share, (which may have included a return of capital). The performance table shows the Fund’s September 30, 2005 total return based on its NAV and market price as of September 30, 2005. Past performance is no guarantee of future results.

| | | | | |

| Fund Performance as of September 30, 2005 (unaudited) | |

| | |

Price

Per Share | | | | 10/26/04-9/30/05

Total Return | |

| | | | | | |

$19.47 (NAV) | | | | 7.06 | % |

|

|

$17.16 (Market Price) | | | | -9.82 | % |

|

|

| | | | |

| All figures represent past performance and are not a guarantee of future results. |

|

| Total returns are based on changes in NAV or market price, respectively. Total returns assume the reinvestment of all distributions, including returns of capital, if any, in additional shares. |

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 7

Factors Influencing Fund Performance

Although the Fund maintained a higher allocation to emerging markets debt during the early part of the period of this report, we decreased our allocation to emerging markets toward the period’s end based on relative value. As emerging markets spreads continued to narrow toward historical levels, we reallocated assets into U.S. high yield, which saw spreads widening. We also increased our overall exposure to U.S. investment grade debt, particularly mortgage-backed securities, since the Fund’s inception.

Finally, we gradually decreased interest rate sensitivity (i.e., duration) throughout the reporting period as rates rose on the short end of the curve and maintained a high average credit quality throughout the reporting period, which helped to insulate the Fund from net asset value (“NAV”) volatility during periods of credit weakness while maintaining overall yield.

Looking for Additional Information?

The Fund is traded under the symbol “GFY” and its closing market price is available in most newspapers under the NYSE listings. The daily NAV is available on-line under symbol XGFYX. Barron’s and The Wall Street Journal’s Monday editions carry closed-end fund tables that provide additional information. In addition, the Fund issues a quarterly press release that can be found on most major financial websites as well as www.citigroupam.com.

In a continuing effort to provide information concerning the Fund, shareholders may call 1-888-777-0102 or 1-800-SALOMON (toll free), Monday through Friday from 8:00 a.m. to 6:00 p.m. Eastern Time, for the Fund’s current NAV, market price, and other information.

Thank you for your investment in the Salomon Brothers Variable Rate Strategic Fund Inc. As ever, we appreciate that you have chosen us to manage your assets and we remain focused on achieving the Fund’s investment goals.

Sincerely,

| | | | |

| |  | |  |

| Peter J. Wilby | | James E. Craige | | Roger Lavan |

| President | | Portfolio Manager | | Portfolio Manager |

| | |

| |  | |  |

| David Torchia | | Beth A. Semmel | | David Scott |

| Portfolio Manager | | Portfolio Manager | | Portfolio Manager |

October 27, 2005

8 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

The information provided is not intended to be a forecast of future events, a guarantee of future results or investment advice. Views expressed may differ from those of the firm as a whole.

RISKS: The Fund is a non-diversified, closed-end management investment company designed primarily as a long-term investment and not as a trading vehicle. The Fund is not intended to be a complete investment program and, due to the uncertainty inherent in all investments, there can be no assurance that the Fund will achieve its investment objective. Your Common Shares at any point in time may be worth less than you invested, even after taking into account the reinvestment of Fund distributions. The Fund may invest in high-yield and foreign securities, including emerging markets, which involve risks beyond those inherently in solely higher-rated and domestic investments. High-yield bonds involve greater credit and liquidity risks than investment grade bonds. Investing in foreign securities is subject to certain risks not associated with domestic investing, such as currency fluctuations, and changes in political and economic conditions. These risks are magnified in emerging or developing markets. Derivatives, such as options or futures, can be illiquid and harder to value, especially in declining markets. A small investment in certain derivatives may have a potentially large impact on the Fund’s performance. As interest rates rise, bond prices fall, reducing the value of the Fund’s share price.

All index performance reflects no deduction for fees, expenses or taxes. Please note that an investor cannot invest directly in an index.

| i | | Gross domestic product is a market value of goods and services produced by labor and property in a given country. |

| ii | | The Federal Reserve Board is responsible for the formulation of a policy designed to promote economic growth, full employment, stable prices, and a sustainable pattern of international trade and payments. |

| iii | | The federal funds rate is the interest rate that banks with excess reserves at a Federal Reserve district bank charge other banks that need overnight loans. |

| iv | | The Lehman Brothers Aggregate Bond Index is a broad-based bond index comprised of Government, Corporate, Mortgage and Asset-backed issues, rated investment grade or higher, and having at least one year to maturity. |

| v | | The Citigroup High Yield Market Index is a broad-based unmanaged index of high yield securities. |

| vi | | JPMorgan Emerging Markets Bond Index Global (“EMBI Global”) tracks total returns for U.S. dollar denominated debt instruments issued by emerging market sovereign and quasi-sovereign entities: Brady bonds, loans, Eurobonds, and local market instruments. Countries covered are Algeria, Argentina, Brazil, Bulgaria, Chile, China, Colombia, Cote d’Ivoire, Croatia, Ecuador, Greece, Hungary, Lebanon, Malaysia, Mexico, Morocco, Nigeria, Panama, Peru, the Philippines, Poland, Russia, South Africa, South Korea, Thailand, Turkey and Venezuela. |

| vii | | A basis point is one one-hundredth (1/100 or 0.01) of one percent. |

| viii | | The yield curve is the graphical depiction of the relationship between the yield on bonds of the same credit quality but different maturities. |

| ix | | As measured by the yield on the Citigroup High Yield Market Index as of the reporting period’s close. |

| x | | Yields are subject to change and will fluctuate. |

| xii | | NAV is calculated by subtracting total liabilities from the closing value of all securities held by the Fund (plus all other assets) and dividing the result (total net assets) by the total number of the common shares outstanding. The NAV fluctuates with changes in the market prices of securities in which the Fund has invested. However, the price at which an investor may buy or sell shares of the Fund is at the Fund’s market price as determined by supply of and demand for the Fund’s shares. |

| xiii | | Lipper, Inc. is a major independent mutual-fund tracking organization. Returns are based on the time period from October 31, 2004 through September 30, 2005, including the reinvestment of distributions, including returns of capital, if any, calculated among the 9 funds in the Fund’s Lipper category, and excluding sales charges. |

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 9

Fund at a Glance (unaudited)

10 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Schedule of Investments (September 30, 2005)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

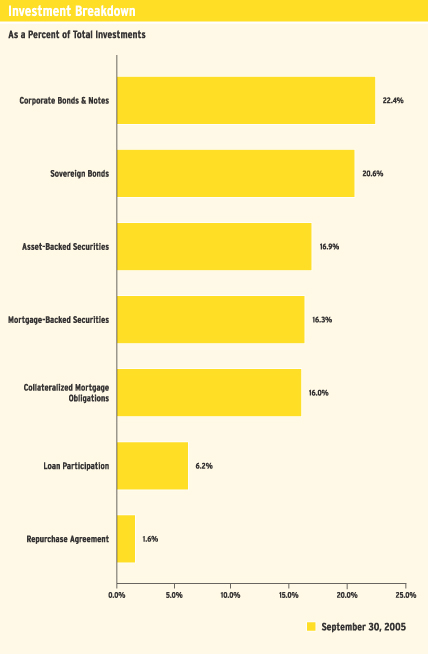

| | CORPORATE BONDS & NOTES — 22.4% | |

| | Advertising — 0.2% | |

| $ | 100,000 | | Bear Creek Corp., Senior Notes, 9.000% due 3/1/13 (a) | | $ | 104,000 | |

| | 375,000 | | Vertis Inc., Senior Second Lien Secured Notes, 9.750% due 4/1/09 | | | 389,063 | |

|

|

|

| | | | Total Advertising | | | 493,063 | |

|

|

|

| | Aerospace/Defense — 0.4% | |

| | 100,000 | | DRS Technologies Inc., Senior Subordinated Notes, 6.875% due 11/1/13 | | | 97,000 | |

| | 250,000 | | L-3 Communications Corp., Senior Subordinated Notes, 7.625% due 6/15/12 | | | 263,750 | |

| | 225,000 | | Moog Inc., Senior Subordinated Notes, 6.250% due 1/15/15 | | | 227,250 | |

| | 375,000 | | Sequa Corp., Senior Notes, Series B, 8.875% due 4/1/08 | | | 391,875 | |

|

|

|

| | | | Total Aerospace/Defense | | | 979,875 | |

|

|

|

| | Airlines — 0.0% | |

| | 100,000 | | Continental Airlines Inc., Senior Notes, 8.000% due 12/15/05 | | | 99,750 | |

|

|

|

| | Apparel — 0.2% | |

| | | | Levi Strauss & Co., Senior Notes: | | | | |

| | 25,000 | | 8.254% due 4/1/12 (b) | | | 25,063 | |

| | 25,000 | | 12.250% due 12/15/12 | | | 27,750 | |

| | 275,000 | | 9.750% due 1/15/15 | | | 281,875 | |

| | 125,000 | | Oxford Industries Inc., Senior Notes, 8.875% due 6/1/11 | | | 130,625 | |

|

|

|

| | | | Total Apparel | | | 465,313 | |

|

|

|

| | Auto Manufacturers — 0.5% | |

| | | | Ford Motor Co.: | | | | |

| | 50,000 | | Debentures, 6.625% due 10/1/28 | | | 36,375 | |

| | 850,000 | | Notes, 7.450% due 7/16/31 | | | 667,250 | |

| | | | General Motors Corp., Senior Debentures: | | | | |

| | 50,000 | | 8.250% due 7/15/23 | | | 39,125 | |

| | 410,000 | | 8.375% due 7/15/33 | | | 321,850 | |

|

|

|

| | | | Total Auto Manufacturers | | | 1,064,600 | |

|

|

|

| | Auto Parts & Equipment — 0.1% | |

| | 50,000 | | Delphi Corp., Notes, 6.500% due 8/15/13 (c) | | | 33,750 | |

| | 100,000 | | Tenneco Automotive Inc., Senior Subordinated Notes, 8.625% due 11/15/14 | | | 101,250 | |

| | 125,000 | | TRW Automotive Inc., Senior Notes, 9.375% due 2/15/13 | | | 136,250 | |

|

|

|

| | | | Total Auto Parts & Equipment | | | 271,250 | |

|

|

|

| | Beverages — 0.1% | |

| | 225,000 | | Constellation Brands Inc., Senior Subordinated Notes, Series B,

8.125% due 1/15/12 | | | 238,781 | |

|

|

|

| | Building Materials — 0.4% | |

| | | | Associated Materials Inc.: | | | | |

| | 200,000 | | Senior Discount Notes, step bond to yield 15.752% due 3/1/14 | | | 101,000 | |

| | 100,000 | | Senior Subordinated Notes, 9.750% due 4/15/12 | | | 97,250 | |

| | 500,000 | | Goodman Global Holding Co. Inc., Senior Notes, 6.410% due 6/15/12 (a)(b) | | | 491,250 | |

| | 225,000 | | Nortek Inc., Senior Subordinated Notes, 8.500% due 9/1/14 | | | 208,125 | |

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 11

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Building Materials — 0.4% (continued) | |

| $ | 125,000 | | Texas Industries, Inc., Senior Notes, 7.250% due 7/15/13 (a) | | $ | 130,625 | |

|

|

|

| | | | Total Building Materials | | | 1,028,250 | |

|

|

|

| | Chemicals — 1.3% | |

| | 200,000 | | Borden U.S. Finance Corp./Nova Scotia Finance ULC, Second Priority Senior Secured Notes, 9.000% due 7/15/14 (a) | | | 204,000 | |

| | 175,000 | | Compass Minerals Group Inc., Senior Subordinated Notes,

10.000% due 8/15/11 | | | 190,750 | |

| | 200,000 | | Equistar Chemicals LP/Equistar Funding Corp., Senior Notes,

10.625% due 5/1/11 | | | 219,000 | |

| | 200,000 | | New Market Corp., Senior Notes, 8.875% due 5/1/10 | | | 210,750 | |

| | | | Huntsman International LLC, Senior Subordinated Notes: | | | | |

| | 152,000 | | 10.125% due 7/1/09 | | | 157,130 | |

| | 75,000 | | 7.375% due 1/1/15 (a) | | | 72,188 | |

| | 100,000 | | Innophos Inc., Senior Subordinated Notes, 8.875% due 8/15/14 (a) | | | 102,750 | |

| | 125,000 | | ISP Holdings Inc., Senior Secured Notes, Series B, 10.625% due 12/15/09 | | | 132,812 | |

| | 375,000 | | Lyondell Chemical Co., Senior Secured Notes, 10.500% due 6/1/13 | | | 425,625 | |

| | 200,000 | | Nalco Co., Senior Subordinated Notes, 8.875% due 11/15/13 | | | 206,250 | |

| | 225,000 | | PQ Corp., Senior Subordinated Notes, 7.500% due 2/15/13 (a) | | | 219,375 | |

| | 200,000 | | Resolution Performance Products Inc., Senior Subordinated Notes,

13.500% due 11/15/10 | | | 213,500 | |

| | 225,000 | | Rhodia SA, Senior Notes, 7.625% due 6/1/10 | | | 220,500 | |

| | 300,000 | | Westlake Chemical Corp., Senior Notes, 8.750% due 7/15/11 | | | 324,750 | |

|

|

|

| | | | Total Chemicals | | | 2,899,380 | |

|

|

|

| | Commercial Services — 0.3% | |

| | 100,000 | | Allied Security Escrow Corp., Senior Subordinated Notes,

11.375% due 7/15/11 | | | 99,750 | |

| | | | Cenveo Corp.: | | | | |

| | 125,000 | | Senior Notes, 9.625% due 3/15/12 | | | 134,688 | |

| | 100,000 | | Senior Subordinated Notes, 7.875% due 12/1/13 | | | 97,000 | |

| | 425,000 | | Iron Mountain Inc., Senior Subordinated Notes, 8.625% due 4/1/13 | | | 447,312 | |

|

|

|

| | | | Total Commercial Services | | | 778,750 | |

|

|

|

| | Computers — 0.2% | |

| | 125,000 | | Seagate Technology HDD Holdings, Senior Notes, 8.000% due 5/15/09 | | | 131,875 | |

| | 50,000 | | SunGard Data Systems Inc., Senior Notes, 9.125% due 8/15/13 (a) | | | 52,063 | |

| | 225,000 | | Unisys Corp., Senior Notes, 6.875% due 3/15/10 | | | 218,250 | |

|

|

|

| | | | Total Computers | | | 402,188 | |

|

|

|

| | Containers & Packaging — 0.1% | |

| | 225,000 | | JSG Funding PLC, Senior Notes, 9.625% due 10/1/12 | | | 227,250 | |

|

|

|

| | Diversified Financial Services — 4.3% | |

| | 400,000 | | Alamosa Delaware Inc., Senior Notes, 11.000% due 7/31/10 | | | 453,000 | |

| | 188,000 | | BCP Crystal U.S. Holdings Corp., Senior Subordinated Notes,

9.625% due 6/15/14 | | | 210,090 | |

| | 100,000 | | CCM Merger Inc., Notes, 8.000% due 8/1/13 (a) | | | 101,375 | |

See Notes to Financial Statements.

12 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Diversified Financial Services — 4.3% (continued) | |

| | | | Ford Motor Credit Co., Notes: | | | | |

| $ | 3,000,000 | | 5.169% due 1/15/10 (b) | | $ | 2,736,531 | |

| | 175,000 | | 7.000% due 10/1/13 | | | 162,528 | |

| | | | General Motors Acceptance Corp.: | | | | |

| | 50,000 | | Bonds, 8.000% due 11/1/31 | | | 43,768 | |

| | | | Notes: | | | | |

| | 25,000 | | 7.250% due 3/2/11 | | | 23,272 | |

| | 4,000,000 | | 6.070% due 12/1/14 (b) | | | 3,369,592 | |

| | 500,000 | | 6.750% due 12/1/14 | | | 435,631 | |

| | 125,000 | | Global Cash Access LLC/Global Cash Finance Corp., Senior Subordinated Notes, 8.750% due 3/15/12 | | | 135,000 | |

| | 2,000,000 | | Residential Capital Corp., Notes, 5.385% due 6/29/07 (a)(b) | | | 2,017,544 | |

| | 325,000 | | Vanguard Health Holdings Co. I LLC, Senior Discount Notes, step bond to yield 9.731% due 10/1/15 | | | 237,250 | |

|

|

|

| | | | Total Diversified Financial Services | | | 9,925,581 | |

|

|

|

| | Electric — 0.9% | |

| | | | AES Corp., Senior Notes: | | | | |

| | 375,000 | | 9.375% due 9/15/10 | | | 415,312 | |

| | 25,000 | | 8.875% due 2/15/11 | | | 27,250 | |

| | 500,000 | | Calpine Corp., Second Priority Senior Secured Notes, 8.500% due 7/15/10 (a) | | | 360,000 | |

| | 375,000 | | Edison Mission Energy, Senior Notes, 9.875% due 4/15/11 | | | 446,250 | |

| | 348,000 | | NRG Energy Inc., Second Priority Senior Secured Notes, 8.000% due 12/15/13 | | | 372,360 | |

| | | | Reliant Energy Inc., Senior Secured Notes: | | | | |

| | 250,000 | | 9.250% due 7/15/10 | | | 272,500 | |

| | 200,000 | | 9.500% due 7/15/13 | | | 222,000 | |

|

|

|

| | | | Total Electric | | | 2,115,672 | |

|

|

|

| | Entertainment — 0.8% | |

| | 250,000 | | Choctaw Resort Development Enterprise, Senior Notes,

7.250% due 11/15/19 (a) | | | 252,187 | |

| | 350,000 | | Cinemark Inc., Senior Discount Notes, step bond to yield

10.033% due 3/15/14 | | | 246,750 | |

| | 125,000 | | Herbst Gaming Inc., Senior Subordinated Notes, 7.000% due 11/15/14 | | | 125,469 | |

| | 225,000 | | Isle of Capri Casinos Inc., Senior Subordinated Notes, 7.000% due 3/1/14 | | | 216,844 | |

| | 200,000 | | Mohegan Tribal Gaming Authority, Senior Subordinated Notes,

6.875% due 2/15/15 | | | 205,000 | |

| | 250,000 | | Penn National Gaming Inc., Senior Subordinated Notes, 6.750% due 3/1/15 | | | 246,250 | |

| | 200,000 | | Pinnacle Entertainment Inc., Senior Subordinated Notes, 8.250% due 3/15/12 | | | 201,000 | |

| | 200,000 | | Scientific Games Corp., Series A, 6.250% due 12/15/12 | | | 200,000 | |

| | | | Six Flags Inc., Senior Notes: | | | | |

| | 200,000 | | 9.750% due 4/15/13 | | | 198,000 | |

| | 25,000 | | 9.625% due 6/1/14 | | | 24,750 | |

|

|

|

| | | | Total Entertainment | | | 1,916,250 | |

|

|

|

| | Environmental Control — 0.3% | |

| | 125,000 | | Aleris International Inc., Series B, Senior Secured Notes,

10.375% due 10/15/10 | | | 138,438 | |

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 13

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Environmental Control — 0.3% (continued) | |

| | | | Allied Waste North America Inc.: | | | | |

| $ | 175,000 | | Senior Notes, 7.250% due 3/15/15 (a) | | $ | 173,250 | |

| | 167,000 | | Senior Secured Notes, Series B, 9.250% due 9/1/12 | | | 181,612 | |

| | 225,000 | | Allied Waste North America, Inc., Senior Notes, 7.875% due 4/15/13 | | | 230,625 | |

|

|

|

| | | | Total Environmental Control | | | 723,925 | |

|

|

|

| | Food — 0.4% | |

| | 125,000 | | Del Monte Corp., Senior Subordinated Notes, 8.625% due 12/15/12 | | | 135,000 | |

| | 200,000 | | Doane Pet Care Co., Senior Notes, 10.750% due 3/1/10 | | | 219,000 | |

| | 250,000 | | Dole Food Co. Inc., Debentures, 8.750% due 7/15/13 | | | 268,750 | |

| | 125,000 | | Pinnacle Foods Holding Corp., Senior Subordinated Notes, 8.250% due 12/1/13 | | | 118,750 | |

| | 90,000 | | United Agri Products Inc., Senior Notes, 8.250% due 12/15/11 | | | 95,400 | |

|

|

|

| | | | Total Food | | | 836,900 | |

|

|

|

| | Forest Products & Paper — 0.4% | |

| | | | Appleton Papers Inc.: | | | | |

| | 100,000 | | Senior Notes, 8.125% due 6/15/11 | | | 98,500 | |

| | 125,000 | | Senior Subordinated Notes, Series B, 9.750% due 6/15/14 | | | 120,625 | |

| | 225,000 | | Boise Cascade, LLC/Boise Cascade Finance Corp., Senior Subordinated Notes, Series B, 7.125% due 10/15/14 (a) | | | 214,313 | |

| | 200,000 | | Buckeye Technologies Inc., Senior Notes, 8.500% due 10/1/13 | | | 204,000 | |

| | 100,000 | | Domtar Inc., Notes, 7.125% due 8/15/15 | | | 92,187 | |

| | 200,000 | | Norske Skog Canada Ltd., Senior Notes, Series D, 8.625% due 6/15/11 | | | 202,000 | |

|

|

|

| | | | Total Forest Products & Paper | | | 931,625 | |

|

|

|

| | Health Care – Product — 0.1% | |

| | 125,000 | | Accellent Corp., Senior Subordinated Notes, Series B, 10.000% due 7/15/12 | | | 136,250 | |

|

|

|

| | Health Care – Services — 0.9% | |

| | 225,000 | | Community Health Systems Inc., Senior Subordinated Notes,

6.500% due 12/15/12 | | | 226,688 | |

| | 225,000 | | DaVita Inc., Senior Subordinated Notes, 7.250% due 3/15/15 | | | 229,219 | |

| | 200,000 | | Extendicare Health Services Inc., Senior Subordinated Notes,

6.875% due 5/1/14 | | | 198,000 | |

| | | | HCA Inc.: | | | | |

| | 200,000 | | Debentures, 7.050% due 12/1/27 | | | 189,902 | |

| | 250,000 | | Senior Notes, 6.375% due 1/15/15 | | | 248,588 | |

| | 375,000 | | IASIS Healthcare LLC/IASIS Capital Corp., Senior Subordinated Notes,

8.750% due 6/15/14 | | | 390,937 | |

| | 100,000 | | InSight Health Services Holdings Corp., Senior Secured Notes,

9.174% due 11/1/11 (a)(b) | | | 98,000 | |

| | 100,000 | | National Mentor Inc., Senior Subordinated Notes, 9.625% due 12/1/12 (a) | | | 105,000 | |

| | 375,000 | | Tenet Healthcare Corp., Senior Notes, 9.875% due 7/1/14 | | | 393,750 | |

|

|

|

| | | | Total Health Care-Services | | | 2,080,084 | |

|

|

|

| | Holding Companies – Diversified — 0.1% | |

| | 125,000 | | Nell AF SARL, Senior Notes, 8.375% due 8/15/15 (a) | | | 122,813 | |

|

|

|

See Notes to Financial Statements.

14 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Home Furnishings — 0.1% | |

| $ | 225,000 | | Norcraft Cos. LP/Norcraft Finance Corp., Senior Subordinated Notes,

9.000% due 11/1/11 | | $ | 234,000 | |

| | 125,000 | | Sealy Mattress Co., Senior Subordinated Notes, 8.250% due 6/15/14 | | | 126,250 | |

|

|

|

| | | | Total Home Furnishings | | | 360,250 | |

|

|

|

| | Household Products/Wares — 0.1% | |

| | 200,000 | | Playtex Products Inc., Senior Subordinated Notes, 9.375% due 6/1/11 | | | 209,750 | |

|

|

|

| | Insurance — 0.2% | |

| | 500,000 | | Stingray Pass-Through Trust Certificates, MTN,

5.902% due 1/12/15 (a) | | | 499,267 | |

|

|

|

| | Internet — 0.1% | |

| | 225,000 | | FTD Inc., Senior Subordinated Notes, 7.750% due 2/15/14 | | | 226,688 | |

|

|

|

| | Leisure Time — 0.2% | |

| | 125,000 | | AMF Bowling Worldwide Inc., Senior Subordinated Notes,

10.000% due 3/1/10 | | | 125,000 | |

| | 100,000 | | Equinox Holdings Inc., Senior Notes, 9.000% due 12/15/09 | | | 103,125 | |

| | 125,000 | | Riddell Bell Holdings Inc., Senior Subordinated Notes, 8.375% due 10/1/12 | | | 123,750 | |

|

|

|

| | | | Total Leisure Time | | | 351,875 | |

|

|

|

| | Lodging — 0.8% | |

| | 375,000 | | Boyd Gaming Corp., Senior Subordinated Notes, 7.750% due 12/15/12 | | | 396,094 | |

| | | | Gaylord Entertainment Co., Senior Notes: | | | | |

| | 25,000 | | 8.000% due 11/15/13 | | | 26,375 | |

| | 125,000 | | 6.750% due 11/15/14 | | | 121,562 | |

| | 250,000 | | Las Vegas Sands Corp., Senior Notes, 6.375% due 2/15/15 (a) | | | 242,500 | |

| | 150,000 | | Kerzner International Ltd., Senior Subordinated Notes, 6.750% due 10/1/15 (a) | | | 146,063 | |

| | 500,000 | | MGM MIRAGE Inc., Senior Notes, 6.750% due 9/1/12 | | | 510,625 | |

| | 375,000 | | Station Casinos Inc., Senior Subordinated Notes, 6.875% due 3/1/16 | | | 382,031 | |

|

|

|

| | | | Total Lodging | | | 1,825,250 | |

|

|

|

| | Machinery — 0.1% | |

| | 198,000 | | Dresser-Rand Group Inc., Senior Subordinated Notes,

7.375% due 11/1/14 (a) | | | 206,415 | |

|

|

|

| | Machinery – Construction & Mining — 0.1% | |

| | 300,000 | | Terex Corp., Senior Subordinated Notes, 7.375% due 1/15/14 | | | 304,500 | |

|

|

|

| | Media — 2.0% | |

| | 225,000 | | Cadmus Communications Corp., Senior Subordinated Notes,

8.375% due 6/15/14 | | | 233,437 | |

| | 497,250 | | CCH I LLC, Senior Secured Notes, 11.000% due 10/1/15 (a) | | | 487,305 | |

| | 225,000 | | Charter Communications Holdings II LLC/Charter Communications Holdings II Capital Corp., Senior Notes, 10.250% due 9/15/10 | | | 231,750 | |

| | 225,000 | | Charter Communications Operating LLC, Second Lien Senior Notes,

8.375% due 4/30/14 (a) | | | 227,250 | |

| | | | CSC Holdings Inc.: | | | | |

| | 75,000 | | Debentures, Series B, 8.125% due 8/15/09 | | | 75,938 | |

| | 125,000 | | Senior Debentures, 7.625% due 7/15/18 | | | 117,500 | |

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 15

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Media — 2.0% (continued) | |

| $ | 250,000 | | Senior Notes, Series B, 8.125% due 7/15/09 | | $ | 253,125 | |

| | | | Dex Media Inc., Discount Notes: | | | | |

| | 500,000 | | step bond to yield 8.389% due 11/15/13 | | | 396,250 | |

| | 75,000 | | step bond to yield 8.389% due 11/15/13 | | | 59,438 | |

| | 81,000 | | DirecTV Holdings LLC/DirecTV Financing Co., Senior Notes, 8.375% due 3/15/13 | | | 88,796 | |

| | 375,000 | | DirecTV Holdings/Finance, Senior Notes, 6.375% due 6/15/15 (a) | | | 374,062 | |

| | 375,000 | | EchoStar DBS Corp., Senior Notes, 6.625% due 10/1/14 | | | 373,125 | |

| | 225,000 | | Emmis Communications Corp., Senior Notes, Class A,

9.745% due 6/15/12 (b) | | | 227,812 | |

| | 325,000 | | LodgeNet Entertainment Corp., Senior Subordinated Debentures,

9.500% due 6/15/13 | | | 357,500 | |

| | 75,000 | | Mediacom Broadband LLC, Senior Notes, 11.000% due 7/15/13 | | | 81,188 | |

| | 125,000 | | Mediacom LLC/Mediacom Capital Corp., Senior Notes, 9.500% due 1/15/13 | | | 124,687 | |

| | 200,000 | | Salem Communications Holding Corp., Senior Subordinated Notes, Series B, 9.000% due 7/1/11 | | | 214,250 | |

| | 225,000 | | Sinclair Broadcast Group Inc., Senior Subordinated Notes,

8.000% due 3/15/12 | | | 231,469 | |

| | 225,000 | | Yell Finance BV, Senior Notes, 10.750% due 8/1/11 | | | 247,500 | |

| | 250,000 | | Young Broadcasting Inc., Senior Subordinated Notes, 10.000% due 3/1/11 | | | 237,500 | |

|

|

|

| | | | Total Media | | | 4,639,882 | |

|

|

|

| | Metal Fabricate/Hardware — 0.1% | |

| | 125,000 | | Mueller Group Inc., Senior Subordinated Notes, 10.000% due 5/1/12 | | | 133,125 | |

|

|

|

| | Mining — 0.2% | |

| | 200,000 | | Corporacion Nacional del Cobre-Codelco, Notes, 5.500% due 10/15/13 (a) | | | 207,188 | |

| | 225,000 | | Novelis Inc., Senior Notes, 7.250% due 2/15/15 (a) | | | 213,750 | |

|

|

|

| | | | Total Mining | | | 420,938 | |

|

|

|

| | Miscellaneous Manufacturing — 0.2% | |

| | 125,000 | | Blount Inc., Senior Subordinated Notes, 8.875% due 8/1/12 | | | 133,750 | |

| | 125,000 | | Invensys PLC, Senior Notes, 9.875% due 3/15/11 (a) | | | 124,844 | |

| | 200,000 | | KI Holdings Inc., Senior Discount Notes, step bond to yield

9.582% due 11/15/14 | | | 137,500 | |

| | 75,000 | | Park-Ohio Industries Inc., Senior Subordinated Notes, 8.375% due 11/15/14 (a) | | | 65,437 | |

|

|

|

| | | | Total Miscellaneous Manufacturing | | | 461,531 | |

|

|

|

| | Office Furnishings — 0.1% | |

| | 125,000 | | Interface Inc., Senior Notes, 7.300% due 4/1/08 | | | 125,625 | |

|

|

|

| | Oil & Gas — 1.0% | |

| | | | Chesapeake Energy Corp., Senior Notes: | | | | |

| | 50,000 | | 6.375% due 6/15/15 (a) | | | 50,500 | |

| | 375,000 | | 6.875% due 1/15/16 | | | 386,250 | |

| | 250,000 | | EXCO Resources Inc., Senior Notes, 7.250% due 1/15/11 | | | 260,000 | |

| | 450,000 | | Kerr-McGee Corp., Senior Secured Notes, 7.000% due 11/1/11 | | | 452,250 | |

| | 475,000 | | Petronas Capital Ltd., 7.875% due 5/22/22 (a) | | | 591,135 | |

| | 200,000 | | Stone Energy Corp., Senior Subordinated Notes, 8.250% due 12/15/11 | | | 211,000 | |

See Notes to Financial Statements.

16 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Oil & Gas — 1.0% (continued) | |

| $ | 250,000 | | Vintage Petroleum Inc., Senior Subordinated Notes, 7.875% due 5/15/11 | | $ | 262,500 | |

|

|

|

| | | | Total Oil & Gas | | | 2,213,635 | |

|

|

|

| | Oil & Gas Services — 0.3% | |

| | 250,000 | | Hanover Compressor Co., Senior Notes, 9.000% due 6/1/14 | | | 279,063 | |

| | 225,000 | | Key Energy Services, Inc., Senior Notes, 6.375% due 5/1/13 | | | 225,000 | |

| | 200,000 | | Universal Compression Inc., Senior Notes, 7.250% due 5/15/10 | | | 208,000 | |

|

|

|

| | | | Total Oil & Gas Services | | | 712,063 | |

|

|

|

| | Packaging & Containers — 0.6% | |

| | 125,000 | | Anchor Glass Container Corp., Senior Secured Notes, 11.000% due 2/15/13 (c) | | | 80,625 | |

| | 200,000 | | Berry Plastics Corp., Senior Subordinated Notes, 10.750% due 7/15/12 | | | 216,000 | |

| | 225,000 | | Graphic Packaging International Corp., Senior Subordinated Notes,

9.500% due 8/15/13 | | | 212,625 | |

| | 375,000 | | Owens-Illinois Inc., Debentures, 7.500% due 5/15/10 | | | 382,500 | |

| | 125,000 | | Plastipak Holdings Inc., Senior Notes, 10.750% due 9/1/11 | | | 136,875 | |

| | 125,000 | | Pliant Corp., Senior Secured Second Lien Notes, 11.125% due 9/1/09 | | | 108,125 | |

| | 375,000 | | Smurfit-Stone Container Enterprises Inc., Senior Notes, 8.375% due 7/1/12 | | | 358,125 | |

|

|

|

| | | | Total Packaging & Containers | | | 1,494,875 | |

|

|

|

| | Pharmaceuticals — 0.1% | |

| | 125,000 | | Warner Chilcott Corp., 8.750% due 2/1/15 (a) | | | 120,625 | |

|

|

|

| | Pipelines — 1.0% | |

| | | | Dynergy Holding Inc.: | | | | |

| | 200,000 | | Debentures, 7.625% due 10/15/26 | | | 186,000 | |

| | 500,000 | | Senior Notes, 6.875% due 4/1/11 | | | 491,250 | |

| | | | El Paso Corp., MTN: | | | | |

| | 375,000 | | 7.375% due 12/15/12 | | | 378,750 | |

| | 300,000 | | 7.750% due 1/15/32 | | | 303,750 | |

| | 225,000 | | Holly Energy Partners LP, Senior Notes, 6.250% due 3/1/15 (a) | | | 223,875 | |

| | 500,000 | | Williams Cos. Inc., Notes, 8.750% due 3/15/32 | | | 592,500 | |

|

|

|

| | | | Total Pipelines | | | 2,176,125 | |

|

|

|

| | Real Estate Investment Trust — 0.7% | |

| | 375,000 | | Felcor Lodging LP, Senior Notes, 9.000% due 6/1/11 | | | 409,687 | |

| | 425,000 | | Host Marriott LP, Senior Notes, 7.125% due 11/1/13 | | | 436,156 | |

| | 425,000 | | iStar Financial Inc., Senior Notes, 5.150% due 3/1/12 | | | 415,680 | |

| | 250,000 | | MeriStar Hospitality Corp., Senior Notes, 9.125% due 1/15/11 | | | 266,250 | |

|

|

|

| | | | Total Real Estate Investment Trust | | | 1,527,773 | |

|

|

|

| | Retail — 0.7% | | | | |

| | 225,000 | | Carrols Corp., Senior Subordinated Notes, 9.000% due 1/15/13 (a) | | | 229,500 | |

| | 225,000 | | CSK Auto Inc., Senior Subordinated Notes, 7.000% due 1/15/14 | | | 211,500 | |

| | 125,000 | | Eye Care Centers of America Inc., Senior Subordinated Notes,

10.750% due 2/15/15 (a) | | | 118,125 | |

| | 100,000 | | Finlay Fine Jewelry Corp., Senior Notes, 8.375% due 6/1/12 | | | 85,125 | |

| | 125,000 | | General Nutrition Centers Inc., Senior Subordinated Notes,

8.500% due 12/1/10 | | | 107,187 | |

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 17

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Retail — 0.7% (continued) | | | | |

| $ | 225,000 | | Jafra Cosmetics International Inc./Distribuidora Comercial Jafra SA de CV,

Senior Subordinated Notes, 10.750% due 5/15/11 | | $ | 250,875 | |

| | 225,000 | | Jean Coutu Group Inc., Senior Subordinated Notes, 8.500% due 8/1/14 | | | 225,000 | |

| | 75,000 | | Neiman Marcus Group Inc., Senior Subordinated Notes,

Series A, 10.375% due 10/15/15 (a) | | | 75,000 | |

| | | | Rite Aid Corp.: | | | | |

| | 175,000 | | 7.500% due 1/15/15 | | | 168,000 | |

| | 50,000 | | Notes, 6.125% due 12/15/08 (a) | | | 47,750 | |

|

|

|

| | | | Total Retail | | | 1,518,062 | |

|

|

|

| | Semiconductors — 0.2% | | | | |

| | 400,000 | | Amkor Technology Inc., Senior Notes, 9.250% due 2/15/08 | | | 377,000 | |

|

|

|

| | Telecommunications — 1.4% | | | | |

| | 250,000 | | American Tower Corp., Senior Notes, 7.125% due 10/15/12 | | | 263,750 | |

| | 175,000 | | AT&T Corp., Senior Notes, 9.750% due 11/15/31 | | | 222,469 | |

| | | | Centennial Communications Corp./Cellular Operating Co. LLC, Senior Notes: | | | | |

| | 125,000 | | 10.125% due 6/15/13 | | | 141,250 | |

| | 75,000 | | 8.125% due 2/1/14 | | | 79,687 | |

| | 50,000 | | Intelsat Bermuda Ltd., Senior Notes, 8.695% due 1/15/12 (a)(b) | | | 51,125 | |

| | 275,000 | | Intelsat Ltd., Senior Discount Notes, step bond to yield 9.447% due 2/1/15 (a) | | | 182,875 | |

| | 125,000 | | IWO Holdings Inc., Secured Notes, 7.349% due 1/15/12 (b) | | | 130,625 | |

| | 500,000 | | Lucent Technologies Inc., Debentures, 6.450% due 3/15/29 | | | 440,000 | |

| | 10,000 | | MCI Inc., Senior Notes, 8.735% due 5/1/14 | | | 11,175 | |

| | 75,000 | | PanAmSat Corp., Senior Notes, 9.000% due 8/15/14 | | | 79,500 | |

| | 1,000,000 | | Qwest Corp., Senior Notes, 7.120% due 6/15/13 (a)(b) | | | 1,045,000 | |

| | 200,000 | | SBA Communications Corp., Senior Notes, 8.500% due 12/1/12 | | | 218,500 | |

| | 125,000 | | UbiquiTel Operating Co., Senior Notes, 9.875% due 3/1/11 | | | 139,375 | |

| | 175,000 | | US Unwired Inc., Second Priority Secured Notes, Series B, 10.000% due 6/15/12 | | | 202,125 | |

|

|

|

| | | | Total Telecommunications | | | 3,207,456 | |

|

|

|

| | Textiles — 0.1% | | | | |

| | 225,000 | | Collins & Aikman Floor Covering Inc., Senior Subordinated Notes,

Series B, 9.750% due 2/15/10 | | | 218,250 | |

| | | | Simmons Bedding Co.: | | | | |

| | 50,000 | | Senior Discount Notes, step bond to yield 13.508% due 12/15/14 (a) | | | 26,750 | |

| | 100,000 | | Senior Subordinated Notes, 7.875% due 1/15/14 | | | 92,500 | |

|

|

|

| | | | Total Textiles | | | 337,500 | |

|

|

|

| | | | TOTAL CORPORATE BONDS & NOTES

(Cost — $52,340,681) | | | 51,187,760 | |

|

|

|

| | ASSET-BACKED SECURITIES — 16.9% | | | | |

| | Home Equity — 16.9% | | | | |

| | | | Aegis Asset-Backed Securities Trust: | | | | |

| | 422,220 | | Series 2004-5N, 5.000% due 12/25/34 (a) | | | 418,720 | |

| | 1,052,014 | | Series 2004-6N, 4.750% due 3/25/35 (a) | | | 1,046,261 | |

| | 508,707 | | Series 2005-1N, Class N1, 4.250% due 3/25/35 (a) | | | 506,158 | |

See Notes to Financial Statements.

18 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Home Equity — 16.9% (continued) | | | | |

| | | | Ameriquest Mortgage Securities, Inc: | | | | |

| $ | 1,500,000 | | Series 2004-R08, Class M10, 6.330% due 9/25/34 (a)(b) | | $ | 1,415,677 | |

| | 3,000,000 | | Series 2004-R1, Class M10, 5.831% due 2/25/34 (a)(b) | | | 2,985,938 | |

| | 2,000,000 | | Argent Securities Inc., Series 2004-W8, Class M10, 7.330% due 5/25/34 (b) | | | 1,964,689 | |

| | | | Countrywide Asset-Backed Certificates: | | | | |

| | 163,046 | | Series 2004-05N, Class N1, 5.500% due 10/25/35 (a) | | | 162,491 | |

| | 615,891 | | Series 2004-11N, Class N, 5.250% due 4/25/36 (a) | | | 612,822 | |

| | 500,000 | | First Franklin Mortgage Loan Trust NIM, Series 2004-FF10, Class N2,

6.000% due 11/26/34 (a)(d) | | | 490,000 | |

| | 3,000,000 | | Fremont Home Loan Trust, Series 2004-D, Class M5,

4.830% due 11/25/34 (b) | | | 3,016,152 | |

| | | | GSAMP Trust: | | | | |

| | 1,500,000 | | Series 2004-OPT, Class B1, 5.430% due 11/25/34 (b) | | | 1,507,698 | |

| | 305,497 | | Series 2005-OPTN, 5.000% due 11/25/34 (a) | | | 305,223 | |

| | 6,864,847 | | Lehman XS Trust, Series 2005-1, Class 2A2, 4.660% due 7/25/35 (b)(d) | | | 6,790,712 | |

| | 858,344 | | Long Beach Asset Holdings Corp., Series 2004-06, Class N2,

7.500% due 11/25/34 (a) | | | 789,140 | |

| | 266,006 | | Merrill Lynch Mortgage Investors Inc., Series 2005-WM1N, Class N1,

5.000% due 9/25/35 (a) | | | 263,660 | |

| | | | Morgan Stanley Asset Backed Securities Capital I: | | | | |

| | 2,000,000 | | Series 2004-HE9, Class M6, 5.080% due 11/25/34 (b) | | | 2,025,103 | |

| | 1,000,000 | | Series 2004-OP1, Class M5, 4.880% due 11/25/34 (b) | | | 1,013,775 | |

| | | | Novastar Home Equity Loan: | | | | |

| | 1,500,000 | | Series 2004-4, Class M4, 4.930% due 3/25/35 (b) | | | 1,501,938 | |

| | 2,000,000 | | Series 2005-2, Class M11, 6.830% due 10/25/35 (b) | | | 1,801,250 | |

| | 1,500,000 | | Option One Mortgage Loan Trust, Series 2004-2, Class M7, 7.330% due 5/25/34 (b) | | | 1,464,617 | |

| | 2,000,000 | | Park Place Securities Inc., Series 2004-WWF1, Class M4, 4.930% due 2/25/35 (b) | | | 2,044,965 | |

| | | | Park Place Securities NIM Trust: | | | | |

| | 1,500,000 | | Series 2004-WWF1, Class B, 6.290% due 1/25/35 (a) | | | 1,496,250 | |

| | 679,871 | | Series 2005-WHQ2, Class A, 5.192% due 5/25/35 (a) | | | 679,021 | |

| | | | Sail Net Interest Margin Notes: | | | | |

| | 466,148 | | Series 2004-02A, Class A, 5.500% due 3/27/34 (a) | | | 466,465 | |

| | 360,802 | | Series 2004-10A, Class B, 7.000% due 11/27/34 (a) | | | 345,243 | |

| | | | Series 2004-11A: | | | | |

| | 178,069 | | Class A2, 4.750% due 1/27/35 (a) | | | 177,285 | |

| | 242,948 | | Class B, 7.500% due 1/27/35 (a) | | | 237,871 | |

| | | | Series 2004-BN2A: | | | | |

| | 222,486 | | Class A, 5.000% due 12/27/34 (a) | | | 222,236 | |

| | 315,017 | | Class B, 7.000% due 12/27/34 (a) | | | 243,130 | |

| | | | Series 2005-1A: | | | | |

| | 110,467 | | Class A, 4.250% due 2/27/35 (a) | | | 109,913 | |

| | 334,153 | | Class B, 7.500% due 2/27/35 (a) | | | 325,799 | |

| | 2,260,000 | | Structured Asset Investment Loan Trust, Series 2004-9, Class M4,

5.130% due 10/25/34 (b) | | | 2,276,282 | |

|

|

|

| | | | TOTAL ASSET-BACKED SECURITIES

(Cost — $38,527,781) | | | 38,706,484 | |

|

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 19

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | COLLATERALIZED MORTGAGE OBLIGATIONS — 16.0% | | | | |

| | | | Federal Home Loan Mortgage Corp. (FHLMC): | | | | |

| $ | 7,730,567 | | Series 2638, Class DI, PAC IO, 5.000% due 5/15/23 (e) | | $ | 1,337,467 | |

| | 8,272,889 | | Series 2639, Class UI, PAC-1 IO, 5.000% due 3/15/22 (e) | | | 1,269,463 | |

| | 18,296,310 | | Series 2645, Class IW, PAC IO, 5.000% due 7/15/26 (e) | | | 2,007,885 | |

| | 19,076,152 | | Series 2684, Class PI, PAC, IO, 5.000% due 5/15/23 (e) | | | 1,454,825 | |

| | 13,436,745 | | Series 2777, Class PI, PAC, IO, 5.000% due 5/15/24 | | | 1,137,369 | |

| | 7,826,193 | | Series 2839, Class TX, PAC, IO, 5.000% due 1/15/19 (e) | | | 1,228,142 | |

| | 7,543,000 | | Series 2866, Class IC, PAC, IO, 5.000% due 1/15/24 (e) | | | 1,008,323 | |

| | 2,614,595 | | Series 2927, Class 0Q, PAC-1, IO, 5.000% due 8/15/19 | | | 166,342 | |

| | | | Federal National Mortgage Association (FNMA): | | | | |

| | 17,605,639 | | Series 337, Class 2, IO, 5.000% due 6/1/33 (e) | | | 3,788,312 | |

| | 7,886,027 | | Series 339, Class 30, IO, 5.500% due 7/1/18 (b) | | | 1,358,015 | |

| | 720,067 | | Homestar NIM Trust, Series 2004-6, Class A1, 5.500% due 1/25/35 (a) | | | 720,854 | |

| | 5,990,200 | | Indymac Index Mortgage Loan Trust, Series 2005-AR21, Class 4A1,

5.474% due 10/25/35 (e) | | | 6,012,663 | |

| | | | Structured Asset Securities Corp.: | | | | |

| | 855,552 | | Series 1998-2, Class M1, 4.930% due 2/25/28 (b) | | | 856,314 | |

| | 353,907 | | Series 1998-3, Class M1, 4.830% due 3/25/28 (b) | | | 354,284 | |

| | 650,707 | | Series 1998-8, Class M1, 4.770% due 8/25/28 (b) | | | 651,375 | |

| | 13,107,353 | | Series 2005-RF3, Class 2A, 4.648% due 6/25/35 (a)(b)(e) | | | 13,344,924 | |

|

|

|

| | | | TOTAL COLLATERALIZED MORTGAGE OBLIGATIONS

(Cost — $35,521,545) | | | 36,696,557 | |

|

|

|

| | LOAN PARTICIPATIONS (b)(f) — 6.2% | | | | |

| | Auto Parts & Equipment — 0.5% | | | | |

| | 1,000,000 | | Delphi Corp., Term Loan, Tranche B, 10.300% due 6/14/11

(JPMorgan Chase & Co.) (c) | | | 1,021,172 | |

|

|

|

| | Electric — 0.7% | | | | |

| | | | Reliant Energy, Inc., Term Loan, Tranche B: | | | | |

| | 1,384,615 | | 6.089% due 4/30/10 (Bank of America) | | | 1,393,640 | |

| | 107,885 | | 6.205% due 4/30/10 (Bank of America) | | | 108,588 | |

|

|

|

| | | | Total Electric | | | 1,502,228 | |

|

|

|

| | Energy — 0.4% | | | | |

| | 1,000,000 | | Key Energy Services Inc., Term Loan, Tranche B,

0.000% due 7/29/12 (Lehman Brothers Inc.) | | | 1,016,875 | |

|

|

|

| | Entertainment — 0.3% | | | | |

| | 750,000 | | BLB Worldwide Holdings Inc., Term Loan, 7.830% due 8/15/12

(Merrill Lynch) | | | 762,188 | |

|

|

|

| | Forest Products & Paper — 0.4% | | | | |

| | | | New Page Corp., Term Loan, Tranche B: | | | | |

| | 533,333 | | 6 Month Tranche, 6.492% due 5/2/11 (Goldman Sachs) | | | 541,333 | |

| | 466,667 | | 2 Month Tranche, 6.680% due 5/2/11 (Goldman Sachs) | | | 473,667 | |

|

|

|

| | | | Total Forest Products & Paper | | | 1,015,000 | |

|

|

|

| | Health Care – Services — 0.4% | | | | |

| | 1,000,000 | | DaVita Inc., Term Loan, Tranche B, 1.000% due 6/25/12

(JPMorgan Chase & Co.) (e) | | | 1,016,042 | |

|

|

|

See Notes to Financial Statements.

20 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount | | Security | | Value | |

| | | | | | | | |

| | Media — 1.3% | | | | |

| $ | 988,746 | | Charter Communications Holdings LLC, Term Loan, Tranche B,

6.930% due 4/27/11 (JPMorgan Chase & Co.) | | $ | 994,596 | |

| | | | DirecTV Holdings LLC, Term Loan, Tranche B: | | | | |

| | 500,000 | | 5.385% due 4/13/13 (Bank of America) | | | 506,302 | |

| | 500,000 | | 5.289% due 4/13/13 (Bank of America) | | | 506,302 | |

| | 1,000,000 | | Spanish Broadcasting Systems, Term Loan, Second Lien,

7.510% due 6/8/13 (Lehman Brothers, Inc.) | | | 1,015,625 | |

|

|

|

| | | | Total Media | | | 3,022,825 | |

|

|

|

| | Metal Fabricate/Hardware — 0.5% | | | | |

| | 1,000,000 | | Mueller Group Inc., Term Loans, 1.000% due 10/3/12 (Bank of America) (e) | | | 1,017,625 | |

|

|

|

| | Oil & Gas — 0.6% | | | | |

| | | | Kerr-McGee Corp. Term Loan: | | | | |

| | 997,500 | | Tranche B, 6.310% due 5/24/11 (JPMorgan Chase & Co.) | | | 1,003,672 | |

| | 350,000 | | Tranche X, 6.110% due 5/24/07 (JPMorgan Chase & Co.) | | | 351,469 | |

|

|

|

| | | | Total Oil & Gas | | | 1,355,141 | |

|

|

|

| | Resorts/Casinos — 0.4% | | | | |

| | | | Venetian Casino Resort LLC, Term Loan: | | | | |

| | 170,940 | | Tranche B, 5.461% due 6/15/11 (Bank of Nova Scotia) | | | 172,636 | |

| | 829,060 | | Tranche L, 5.240% due 6/15/11 (Bank of Nova Scotia) | | | 837,286 | |

|

|

|

| | | | Total Resorts/Casinos | | | 1,009,922 | |

|

|

|

| | Telecommunications — 0.7% | | | | |

| | 1,500,000 | | UPC Broadband Inc. Term Loan, Tranche H2,

6.004% due 3/15/12 (Toronto Dominion Bank) | | | 1,518,281 | |

|

|

|

| | | | TOTAL LOAN PARTICIPATIONS

(Cost — $14,106,702) | | | 14,257,299 | |

|

|

|

| | MORTGAGE-BACKED SECURITIES — 16.3% | | | | |

| | FHLMC — 9.1% | | | | |

| | | | Federal Home Loan Mortgage Corp. (FHLMC), Gold: | | | | |

| | 3,147,551 | | 6.000% due 2/1/33 (e) | | | 3,204,009 | |

| | 7,562,432 | | 6.500% due 11/1/34 (e) | | | 7,779,376 | |

| | 9,764,911 | | 5.500% due 6/1/35 (e) | | | 9,772,845 | |

|

|

|

| | | | Total FHLMC | | | 20,756,230 | |

|

|

|

| | FNMA — 7.2% | | | | |

| | | | Federal National Mortgage Association (FNMA): | | | | |

| | 6,635,552 | | 6.000% due 5/1/33 (e) | | | 6,749,611 | |

| | 9,744,072 | | 5.500% due 4/1/35 (e) | | | 9,745,898 | |

|

|

|

| | | | Total FNMA | | | 16,495,509 | |

|

|

|

| | | | TOTAL MORTGAGE-BACKED SECURITIES

(Cost — $37,775,267) | | | 37,251,739 | |

|

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 21

Schedule of Investments (September 30, 2005) (continued)

| | | | | | |

| | |

Face

Amount† | | Security | | Value | |

| | | | | | | |

| SOVEREIGN BONDS — 20.6% | | | | |

| Argentina — 0.7% | | | | |

| | | Republic of Argentina: | | | | |

| 1,050,000 | | 4.005% due 8/3/12 (b) | | $ | 957,402 | |

| 1,351,796ARS | | 5.830% due 12/31/33 | | | 574,446 | |

| 270,000 | | step bond to yield 8.870% due 12/31/38 | | | 106,853 | |

|

|

| | | Total Argentina | | | 1,638,701 | |

|

|

| Brazil — 4.6% | | | | |

| 10,747,197 | | Federative Republic of Brazil, DCB, Series L, 4.313% due 4/15/12 (b) | | | 10,596,065 | |

|

|

| Bulgaria — 0.3% | | | | |

| 575,000 | | Republic of Bulgaria, 8.250% due 1/15/15 (a) | | | 708,688 | |

|

|

| Chile — 0.3% | | | | |

| 675,000 | | Republic of Chile, 5.500% due 1/15/13 | | | 704,699 | |

|

|

| Colombia — 1.0% | | | | |

| | | Republic of Colombia: | | | | |

| 440,000 | | 10.375% due 1/28/33 | | | 575,300 | |

| 1,275,000 | | 10.750% due 1/15/13 | | | 1,604,269 | |

| 75,000 | | MTN, 11.750% due 2/25/20 | | | 104,662 | |

|

|

| | | Total Colombia | | | 2,284,231 | |

|

|

| Ecuador — 0.3% | |

| 720,000 | | Republic of Ecuador, step bond to yield 10.521% due 8/15/30 (a) | | | 681,120 | |

|

|

| El Salvador — 0.1% | |

| 275,000 | | Republic of El Salvador, 7.750% due 1/24/23 (a) | | | 309,375 | |

|

|

| Malaysia — 0.2% | |

| 450,000 | | Federation of Malaysia, 7.500% due 7/15/11 | | | 511,097 | |

|

|

| Mexico — 4.3% | |

| | | United Mexican States: | | | | |

| 780,000 | | 11.375% due 9/15/16 | | | 1,153,620 | |

| 2,700,000 | | 8.125% due 12/30/19 | | | 3,283,875 | |

| 275,000 | | Bonds, Series XW, 10.375% due 2/17/09 | | | 321,819 | |

| | | MTN: | | | | |

| 275,000 | | 8.300% due 8/15/31 | | | 343,750 | |

| | | Series A: | | | | |

| 1,730,000 | | 6.375% due 1/16/13 | | | 1,845,478 | |

| 925,000 | | 8.000% due 9/24/22 | | | 1,123,875 | |

| 1,125,000 | | 7.500% due 4/8/33 | | | 1,305,000 | |

| 5,077,500MXN | | Series MI10, 9.500% due 12/18/14 | | | 498,139 | |

|

|

| | | Total Mexico | | | 9,875,556 | |

|

|

| Panama — 0.8% | |

| | | Republic of Panama: | | | | |

| 100,000 | | 7.250% due 3/15/15 | | | 109,375 | |

| 600,000 | | 9.375% due 1/16/23 | | | 760,500 | |

| 859,073 | | PDI, 4.688% due 7/17/16 (b) | | | 839,743 | |

|

|

| | | Total Panama | | | 1,709,618 | |

|

|

See Notes to Financial Statements.

22 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Schedule of Investments (September 30, 2005) (continued)

| | | | | | |

| | |

Face

Amount† | | Security | | Value | |

| | | | | | | |

| Peru — 0.9% | |

| | | Republic of Peru: | | | | |

| 150,000 | | 7.350% due 7/21/25 | | $ | 159,750 | |

| 145,000 | | 9.125% due 2/21/12 | | | 174,362 | |

| 1,862,000 | | FLIRB, 5.000% due 3/7/17 (b) | | | 1,801,485 | |

|

|

| | | Total Peru | | | 2,135,597 | |

|

|

| Philippines — 0.9% | |

| | | Republic of the Philippines: | | | | |

| 125,000 | | 8.250% due 1/15/14 | | | 130,075 | |

| 1,575,000 | | 9.875% due 1/15/19 | | | 1,762,031 | |

| 125,000 | | 10.625% due 3/16/25 | | | 146,169 | |

| 100,000 | | 9.500% due 2/2/30 | | | 106,935 | |

|

|

| | | Total Philippines | | | 2,145,210 | |

|

|

| Poland — 0.1% | |

| 225,000 | | Republic of Poland, 5.250% due 1/15/14 | | | 232,031 | |

|

|

| Russia — 2.7% | |

| | | Russian Federation: | | | | |

| 650,000 | | 11.000% due 7/24/18 (a) | | | 992,875 | |

| 2,700,000 | | 12.750% due 6/24/28 (a) | | | 5,096,250 | |

|

|

| | | Total Russia | | | 6,089,125 | |

|

|

| South Africa — 0.3% | | | | |

| | | Republic of South Africa: | | | | |

| 125,000 | | 9.125% due 5/19/09 | | | 142,656 | |

| 575,000 | | 6.500% due 6/2/14 | | | 631,782 | |

|

|

| | | Total South Africa | | | 774,438 | |

|

|

| Turkey — 1.5% | |

| | | Republic of Turkey: | | | | |

| 300,000 | | 7.250% due 3/15/15 | | | 316,500 | |

| 425,000 | | 7.000% due 6/5/20 | | | 420,750 | |

| 250,000 | | 11.875% due 1/15/30 | | | 367,500 | |

| 1,850,000 | | Collective Action Securities, 9.500% due 1/15/14 | | | 2,238,500 | |

|

|

| | | Total Turkey | | | 3,343,250 | |

|

|

| Ukraine — 0.3% | |

| 575,000 | | Republic of Ukraine, 7.650% due 6/11/13 (a) | | | 634,656 | |

|

|

| Uruguay — 0.2% | |

| | | Republic of Uruguay, Benchmark Bonds: | | | | |

| 175,000 | | 7.250% due 2/15/11 | | | 183,094 | |

| 250,000 | | 7.500% due 3/15/15 | | | 256,250 | |

|

|

| | | Total Uruguay | | | 439,344 | |

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 23

Schedule of Investments (September 30, 2005) (continued)

| | | | | | | |

| | |

Face

Amount† | | Security | | Value | |

| | | | | | | | |

| | Venezuela — 1.1% | |

| | | | Bolivarian Republic of Venezuela: | | | | |

| | | | Collective Action Securities: | | | | |

| | 375,000 | | Global Bonds, 7.650% due 4/21/25 | | $ | 380,437 | |

| | 1,450,000 | | 4.640% due 4/20/11 (a)(b) | | | 1,439,125 | |

| | 500,000 | | 10.750% due 9/19/13 | | | 625,250 | |

|

|

|

| | | | Total Venezuela | | | 2,444,812 | |

|

|

|

| | | | TOTAL SOVEREIGN BONDS

(Cost — $44,302,099) | | | 47,257,613 | |

|

|

|

| | | | TOTAL INVESTMENTS BEFORE SHORT-TERM INVESTMENT

(Cost — $222,574,075) | | | 225,357,452 | |

|

|

|

| | |

Face

Amount | | | | | |

| | SHORT-TERM INVESTMENT — 1.6% | |

| | Repurchase Agreement — 1.6% | |

| $ | 3,704,000 | | Interest in $603,193,000 joint tri-party repurchase agreement dated 9/30/05 with Merrill Lynch, Pierce, Fenner & Smith Inc., 3.810% due 10/3/05; Proceeds at maturity — $3,705,176; (Fully collateralized by U.S. government agency obligations, 4.125% to 8.875% due 8/15/08 to 7/15/20;

Market value — $3,778,099)

(Cost — $3,704,000) (e) | | | 3,704,000 | |

|

|

|

| | | | TOTAL INVESTMENTS — 100.0% (Cost — $226,278,075#) | | $ | 229,061,452 | |

|

|

|

| † | | Face amount is denominated in U.S. dollars unless otherwise indicated. |

| (a) | | Security is exempt from registration under Rule 144A of the Securities Act of 1933. This security may be resold in transactions that are exempt from registration, normally to qualified institutional buyers. This security has been deemed liquid pursuant to guidelines approved by the Board of Directors unless otherwise noted. |

| (b) | | Variable rate securities. Interest rates disclosed are those which are in effect at September 30, 2005. |

| (c) | | Security is currently in default. |

| (d) | | Securities are fair valued at September 30, 2005 in accordance with the policies adopted by the Board of Directors (see note 1). |

| (e) | | All or a portion of this security is segregated for extended settlements, swap transactions, and reverse repurchase agreements. |

| (f) | | Participation interest was acquired through the financial institutions indicated parenthetically. |

| # | | Aggregate cost for federal income tax purposes is $226,573,609. |

| | | | |

Abbreviations used in this schedule:

|

| ARS | | — | | Argentine Peso |

| DCB | | — | | Debt Conversion Bond |

| FLIRB | | — | | Front-Loaded Interest Reduction Bonds |

| GSAMP | | — | | Goldman Sachs Mortgage Securities Corporation |

| IO | | — | | Interest Only |

| MTN | | — | | Medium-Term Note |

| MXN | | — | | Mexican Peso |

| NIM | | — | | Net Interest Margin |

| PAC | | — | | Planned Amortization Cost |

| PDI | | — | | Past Due Interest |

See Notes to Financial Statements.

24 Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report

Statement of Assets and Liabilities (September 30, 2005)

| | | | |

| ASSETS: | | | | |

Investments, at value (Cost — $226,278,075) | | $ | 229,061,452 | |

Cash | | | 169,784 | |

Interest receivable | | | 3,491,720 | |

Receivable for securities sold | | | 2,019,180 | |

Unrealized appreciation on interest rate swaps | | | 1,420,600 | |

Deposits with brokers for reverse repurchase agreement | | | 696,000 | |

Due from Manager | | | 57,803 | |

Prepaid expenses | | | 8,081 | |

|

|

Total Assets | | | 236,924,620 | |

|

|

| LIABILITIES: | | | | |

Payable for open reverse repurchase agreement (Notes 1 and 3) | | | 68,098,000 | |

Payable for securities purchased | | | 5,236,316 | |

Payable on interest rate swaps contracts (Note 3) | | | 1,077,904 | |

Interest payable (Note 3) | | | 163,044 | |

Management fee payable | | | 141,044 | |

Directors’ fees payable | | | 967 | |

Payable for open spot currency contracts | | | 101 | |

Accrued expenses | | | 141,155 | |

|

|

Total Liabilities | | | 74,858,531 | |

|

|

Total Net Assets | | $ | 162,066,089 | |

|

|

| NET ASSETS: | | | | |

Par value ($0.001 par value, 100,000,000 shares authorized; 8,323,434 shares outstanding) | | $ | 8,323 | |

Paid-in capital in excess of par value | | | 158,195,188 | |

Overdistributed net investment income | | | (7,473 | ) |

Accumulated net realized loss on investments, futures contracts, interest rate swap

contracts and foreign currency transactions | | | (333,732 | ) |

Net unrealized appreciation on investments, interest rate swap contracts and foreign currency transactions | | | 4,203,783 | |

|

|

Total Net Assets | | $ | 162,066,089 | |

|

|

Shares Outstanding | | | 8,323,434 | |

|

|

Net Asset Value | | | $19.47 | |

|

|

See Notes to Financial Statements.

Salomon Brothers Variable Rate Strategic Fund Inc. 2005 Annual Report 25

Statement of Operations (For the period ended September 30, 2005†)

| | | | |

| INVESTMENT INCOME: | | | | |

Interest | | $ | 9,538,879 | |

|

|

| EXPENSES: | | | | |

Management fee (Note 2) | | | 1,265,958 | |

Interest expense (Note 3) | | | 837,196 | |

Audit and tax | | | 55,879 | |

Custody fees | | | 49,415 | |

Shareholder reports | | | 43,700 | |

Legal fees | | | 43,625 | |

Directors’ fees | | | 43,452 | |

Transfer agent fees | | | 24,128 | |

Stock exchange listing | | | 18,466 | |

Insurance | | | 2,863 | |

Miscellaneous expenses | | | 5,802 | |

|

|

Total Expenses | | | 2,390,484 | |

|

|

Net Investment Income | | | 7,148,395 | |

|

|

REALIZED AND UNREALIZED GAIN (LOSS) ON INVESTMENTS,

FUTURES CONTRACTS, INTEREST RATE SWAP CONTRACTS

AND FOREIGN CURRENCY TRANSACTIONS (NOTES 1 AND 3): | | | | |

Net Realized Gain (Loss) From: | | | | |

Investments | | | 141,346 | |

Futures contracts | | | 122,748 | |

Interest rate swap contracts | | | (715,309 | ) |

Foreign currency transactions | | | (2,232 | ) |

|

|

Net Realized Loss | | | (453,447 | ) |

|

|

Change in Net Unrealized Appreciation/Depreciation From: | | | | |

Investments | | | 2,783,377 | |

Interest rate swap contracts | | | 1,420,600 | |