UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 6-K

REPORT OF FOREIGN PRIVATE ISSUER PURSUANT TO RULE 13A-16 OR 15D-16 UNDER THE

SECURITIES EXCHANGE ACT OF 1934

For the month of May, 2019

Commission File Number 32297

CPFL Energy Incorporated

(Translation of Registrant's name into English)

Rodovia Engenheiro Miguel Noel Nascentes Burnier, km 2,5, parte

CEP 13088-140 - Parque São Quirino, Campinas - SP

Federative Republic of Brazil

CEP 13088-140 - Parque São Quirino, Campinas - SP

Federative Republic of Brazil

(Address of principal executive office)

Indicate by check mark whether the registrant files or will file annual reports under cover Form 20-F or Form 40-F. Form 20-F ___X___ Form 40-F _______

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): [ ]

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): [ ]

If "Yes" is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-_________________

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(1): [ ]

Indicate by check mark if the registrant is submitting the Form 6-K in paper as permitted by Regulation S-T Rule 101(b)(7): [ ]

Indicate by check mark whether the registrant by furnishing the information contained in this Form is also thereby furnishing the information to the Commission pursuant to Rule 12g3-2(b) under the Securities Exchange Act of 1934.

Yes _______ No ___X____If "Yes" is marked, indicate below the file number assigned to the registrant in connection with Rule 12g3-2(b): 82-_________________

.

Campinas, May 7, 2019 – CPFL Energia S.A. (B3: CPFE3 and NYSE: CPL), announces its1Q19 results.The financial and operational information herein, unless otherwise indicated, is presented on a consolidated basis and is in accordance with the applicable legislation. Comparisons are relative to 1Q18, unless otherwise stated.

CPFL ENERGIA ANNOUNCES ITS 1Q19 RESULTS

Indicators (R$ Million) | 1Q19 | 1Q18 | Var. |

Sales within the Concession Area - GWh | 17,731 | 17,185 | 3.2% |

Captive Market | 12,407 | 11,983 | 3.5% |

Free Client | 5,323 | 5,201 | 2.3% |

Gross Operating Revenue | 10,788 | 9,637 | 11.9% |

Net Operating Revenue | 7,127 | 6,375 | 11.8% |

EBITDA(1) | 1,531 | 1,366 | 12.1% |

Net Income | 570 | 419 | 36.0% |

Investments(2) | 445 | 426 | 4.6% |

|

|

|

|

Notes:

(1) EBITDA is calculated from the sum of net income, taxes, financial result, depreciation/amortization, as CVM Instruction no. 527/12. See the calculation in item 4.6 of this report;

(2) Includes investments related to the transmission segment; according to the requirements of IFRIC 15, it was recorded as “Contractual Asset of Transmission Companies” (in other credits). Does not include special obligations.

1Q19 HIGHLIGHTS

• Increase of3.2% in sales within the concession area, highlighting the growths of the residential (+8.4%) and commercial (+5.1%) classes;

• EBITDAofR$ 1,531 million, growth of12.1%;

• Net IncomeofR$ 570 million, growth of36.0%;

• Net debt ofR$ 14.9 billionand leverage of2.70x Net Debt/EBITDA;

• Investments ofR$ 445 million;

• CPFL Paulista’s tariff adjustment, in Apr-19: (i) increase of9.63% of the parcel B, from R$ 2,310 million to R$ 2,532 million, and (ii) average effect of+8.66% to be perceived by the consumers.

| 1Q19 Results | May 7, 2019 |

INDEX

| 1) MESSAGE FROM THE CEO | 4 |

| 2) ENERGY SALES | 5 |

| 2.1) Sales within the Distributors Concession Area | 5 |

| 2.1.1) Sales by Segment Concession Area | 6 |

| 2.1.2) Sales to the Captive Market | 6 |

| 2.1.3) Free Clients | 7 |

| 2.2) Generation Installed Capacity | 7 |

| 3) INFORMATION ON INTEREST IN COMPANIES AND CRITERIA OF FINANCIAL STATEMENTS | |

| CONSOLIDATION | 8 |

| 3.1) Consolidation of CPFL Renováveis Financial Statements | 10 |

| 3.2) Consolidation of RGE Sul Financial Statements | 10 |

| 3.3) Economic-Financial Performance Presentation | 10 |

| 3.4) Consolidation of Transmission Companies | 10 |

| 4) ECONOMIC-FINANCIAL PERFORMANCE | 11 |

| 4.1) Opening of economic-financial performance by business segment | 11 |

| 4.2) Sectoral Financial Assets and Liabilities | 12 |

| 4.3) Operating Revenue | 12 |

| 4.4) Cost of Electric Energy | 13 |

| 4.5) Operating Costs and Expenses | 14 |

| 4.6) EBITDA | 15 |

| 4.7) Financial Result | 16 |

| 4.8) Net Income | 17 |

| 5) INDEBTEDNESS | 18 |

| 5.1) Debt (IFRS) | 18 |

| 5.1.1) Debt Amortization Schedule in IFRS (Mar-19) | 19 |

| 5.2) Debt in Financial Covenants Criteria | 20 |

| 5.2.1) Indexation and Debt Cost in Financial Covenants Criteria | 20 |

| 5.2.2) Net Debt in Financial Covenants Criteria and Leverage | 21 |

| 6) INVESTMENTS | 21 |

| 6.1) Actual Investments | 21 |

| 6.2) Investments Forecasts | 22 |

| 7) ALLOCATION OF RESULTS | 23 |

| 8) STOCK MARKETS | 23 |

| 8.1) Stock Performance | 23 |

| 8.2) Daily Average Volume | 24 |

| 9) CORPORATE GOVERNANCE | 25 |

| 10) SHAREHOLDERS STRUCTURE | 26 |

| 11) PERFORMANCE OF THE BUSINESS SEGMENTS | 27 |

| 11.1) Distribution Segment | 27 |

| 11.1.1) Economic-Financial Performance | 27 |

| 11.1.1.1) Sectoral Financial Assets and Liabilities | 27 |

| 11.1.1.2) Operating Revenue | 28 |

| 11.1.1.3) Cost of Electric Energy | 29 |

| 11.1.1.4) Operating Costs and Expenses | 30 |

| 11.1.1.5) EBITDA | 32 |

Page 2 de 57

| 1Q19 Results | May 7, 2019 |

| 11.1.1.6) Financial Result | 32 |

| 11.1.1.7) Net Income | 33 |

| 11.1.2) Tariff Events | 33 |

| 11.1.3) Operating Performance of Distribution | 35 |

| 11.2) Commercialization and Services Segments | 36 |

| 11.2.1) Commercialization Segment | 36 |

| 11.2.2) Services Segment | 37 |

| 11.3) Conventional Generation Segment | 38 |

| 11.3.1) Economic-Financial Performance | 38 |

| 11.3.1.1) Operating Revenue | 38 |

| 11.3.1.2) Cost of Electric Power | 38 |

| 11.3.1.3) Operating Costs and Expenses | 39 |

| 11.3.1.4) Equity Income | 40 |

| 11.3.1.5) EBITDA | 41 |

| 11.3.1.6) Financial Result | 41 |

| 11.3.1.7) Net Income | 42 |

| 11.4) CPFL Renováveis | 42 |

| 11.4.1) Economic-Financial Performance | 42 |

| 11.4.1.1) Operating Revenue | 43 |

| 11.4.1.2) Cost of Electric Power | 43 |

| 11.4.1.3) Operating Costs and Expenses | 43 |

| 11.4.1.4) EBITDA | 44 |

| 11.4.1.5) Financial Result | 45 |

| 11.4.1.6) Net Income | 45 |

| 11.4.2) Status of Generation Projects 100% Participation | 45 |

| 12) ATTACHMENTS | 47 |

| 12.1) Statement of Assets CPFL Energia | 47 |

| 12.2) Statement of Liabilities CPFL Energia | 48 |

| 12.3) Income Statement CPFL Energia | 49 |

| 12.4) Cash Flow CPFL Energia | 50 |

| 12.5) Income Statement Conventional Generation Segment | 51 |

| 12.6) Income Statement CPFL Renováveis | 52 |

| 12.7) Income Statement Distribution Segment | 53 |

| 12.8) Economic-Financial Performance by Distributor | 54 |

| 12.9) Sales within the Concession Area by Distributor (In GWh) | 55 |

| 12.10) Sales to the Captive Market by Distributor (in GWh) | 56 |

| 12.11) Reconciliation of Net Debt/EBITDA Pro Forma ratio of CPFL Energia for purposes of financial | |

| covenants calculation | 57 |

Page 3 de 57

| 1Q19 Results | May 7, 2019 |

1) MESSAGE FROM THE CEO

The results from CPFL Group in the first quarter of 2019 reflected the growth of energy sales, as well as our discipline in cost and expense management.

The distribution segment had an increase in energy sales (+3.2%) in 1Q19. Residential and commercial classes registered market variations of +8.4% and +5.1%, respectively, reflecting the increase in temperature, mainly in the first two months of 2019. The industrial class registered market variation of -0.9%, still reflecting the slow recovery of economy activity.

CPFL group’s operating cash generation, measured by EBITDA, reached R$ 1,531 million in 1Q19 (+12.1%). We highlight the distribution segment, whose EBITDA reached R$ 980 million in 1Q19 (+23.6%), mainly reflecting the results coming from the conclusion of the tariff revision process (4th cycle) of CPFL Paulista, RGE Sul (both in April 2018) and RGE (in June 2018).

We continue working on value initiatives and in our investment plan (around R$ 11.9 billion for the next five years, being R$ 2.2 billion for 2019), with financial discipline, efforts and commitment of our teams. We invested R$ 445 million in 1Q19.

CPFL Energia’s capital structure and consolidated leverage remained at adequate levels. The Company’s net debt reached 2.70 times EBITDA at the end of the quarter, under the criteria to measure our financial covenants, lower than in the previous quarter.

Finally, CPFL’s management remains optimistic about the advances of the Brazilian electricity sector and remains confident in its business platform, which is increasingly prepared and well positioned to face the challenges and opportunities in the country.

Gustavo Estrella

CEO of CPFL Energia

Page 4 de 57

| 1Q19 Results | May 7, 2019 |

2) ENERGY SALES

2.1) Sales within the Distributors’ Concession Area

Sales within the Concession Area - GWh | |||

| 1Q19 | 1Q18 | Var. |

Captive Market | 12,407 | 11,983 | 3.5% |

Free Client | 5,323 | 5,201 | 2.3% |

Total | 17,731 | 17,185 | 3.2% |

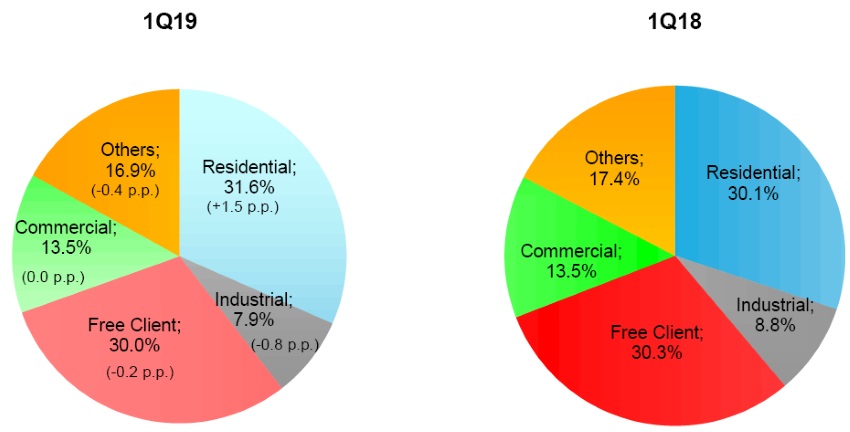

In 1Q19, sales within the concession area, achieved by the distribution segment, totaled 17,731 GWh, an increase of 3.2%. Sales to the captive market totaled 12,407 GWh in 1Q19, an increase of 3.5%. The quantity of energy, in GWh, which corresponds to the consumption of free clients in the concession area of group’s distributors, billed through the Tariff for the Usage of the Distribution System (TUSD), reached 5,323 GWh in 1Q19, an increase of 2.3%.

Sales within the Concession Area - GWh | ||||

| 1Q19 | 1Q18 | Var. | Part. |

Residential | 5,604 | 5,172 | 8.4% | 31.6% |

Industrial | 5,943 | 5,994 | -0.9% | 33.5% |

Commercial | 3,094 | 2,945 | 5.1% | 17.5% |

Others | 3,090 | 3,074 | 0.5% | 17.4% |

Total | 17,731 | 17,185 | 3.2% | 100.0% |

Note: The tables with sales within the concession area by distributor are attached to this report in item 12.9.

Noteworthy in 1Q19, in the concession area:

· Residential and Commercial classes (31.6% and 17.5% of total sales, respectively): increases of 8.4% and 5.1%, respectively. Highlights for residential class of CPFL Piratininga (+8.9%), RGE (+8.6%) and CPFL Santa Cruz (+9.4%). Highlights for commercial class of CPFL Paulista (+5.7%), CPFL Piratininga (+7.0%) and CPFL Santa Cruz (+9.0%). This result was due to the increase in temperature, mainly in the first two months of 2019.

· Industrial class (33.5% of total sales): reduction of 0.9%, reflecting the low economic activity.

Page 5 de 57

| 1Q19 Results | May 7, 2019 |

2.1.1) Sales by Segment – Concession Area

Note: in parentheses, the variation in percentage points from 1Q18 to 1Q19.

2.1.2) Sales to the Captive Market

Sales to the Captive Market - GWh | |||

| 1Q19 | 1Q18 | Var. |

Residential | 5,604 | 5,172 | 8.4% |

Industrial | 1,402 | 1,504 | -6.8% |

Commercial | 2,398 | 2,323 | 3.2% |

Others | 3,004 | 2,984 | 0.7% |

Total | 12,407 | 11,983 | 3.5% |

Note: The tables with captive market sales by distributor are attached to this report in item 12.10.

Sales to the captive market totaled 12,407 GWh in 1Q19, an increase of 3.5% (424 GWh), mainly due to the performance of the residential class (+8.4%); the performance of industrial (-6.8%) and commercial (+3.2%) classes, reflects the migration of customers to the free market.

Page 6 de 57

| 1Q19 Results | May 7, 2019 |

2.1.3) Free Clients

Free Client - GWh | |||

| 1Q19 | 1Q18 | Var. |

Industrial | 4,541 | 4,490 | 1.1% |

Commercial | 697 | 622 | 12.0% |

Others | 86 | 90 | -4.2% |

Total | 5,323 | 5,201 | 2.3% |

Free Client by Distributor - GWh | |||

| 1Q19 | 1Q18 | Var. |

CPFL Paulista | 2,515 | 2,434 | 3.3% |

CPFL Piratininga | 1,479 | 1,529 | -3.3% |

RGE | 1,152 | 1,093 | 5.4% |

CPFL Santa Cruz | 177 | 145 | 21.9% |

Total | 5,323 | 5,201 | 2.3% |

2.2) Generation Installed Capacity

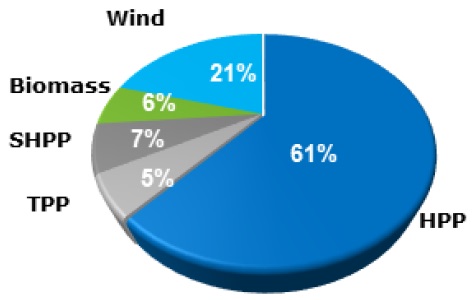

In 1Q19, the Generation installed capacity of CPFL Energia group, considering the proportional stake in each project, is of 3,272 MW.

Generation Installed Capacity

Total: 3,272 MW

Note: Take into account CPFL Energia’s 51.56% stake in CPFL Renováveis.

Page 7 de 57

| 1Q19 Results | May 7, 2019 |

3) INFORMATION ON INTEREST IN COMPANIES AND CRITERIA OF FINANCIAL STATEMENTS CONSOLIDATION

The interests directly or indirectly held by CPFL Energia in its subsidiaries and jointly-owned entities are described below. Except for: (i) the jointly-owned entities ENERCAN, BAESA, Foz do Chapecó and EPASA, that, as from January 1, 2013 are no longer proportionally consolidated in the Company’s financial statements, being their assets, liabilities and results accounted for using the equity method of accounting, and (ii) the investment in Investco S.A. recorded at cost by the subsidiary Paulista Lajeado, the other units are fully consolidated.

As of March 31, 2019 and 2019, the participation of non-controlling interests stated in the consolidated statements refers to the third-party interests in the subsidiaries CERAN, Paulista Lajeado and CPFL Renováveis.

Since November 1st, 2016 CPFL Energia is considering the full consolidation of RGE Sul.

Energy distribution | Company Type | Equity Interest | Location (State) | Number of municipalities | Approximate number of consumers | Concession term | End of the concession |

Companhia Paulista de Força e Luz ("CPFL Paulista") | Publicly-quoted corporation | Direct | Countryside of São Paulo | 234 | 4,516 | 30 years | November 2027 |

Companhia Piratininga de Força e Luz ("CPFL Piratininga") | Publicly-quoted corporation | Direct | Countryside and seaside of São Paulo | 27 | 1,760 | 30 years | October 2028 |

RGE Sul Distribuidora de Energia S.A. ("RGE") (a) | Publicly-quoted corporation | Direct and Indirect | Countryside of Rio Grande do Sul | 381 | 2,888 | 30 years | November 2027 |

Companhia Jaguari de Energia ("CPFL Santa Cruz") | Private corporation | Direct | Countryside of São Paulo, Paraná and Minas Gerais | 45 | 458 | 30 years | July 2045 |

Note:

(a) On December 31, 2018, was approved the grouping of the concessions of the distribution companies RGE Sul Distribuidora de Energia S.A. (“RGE Sul”) and Rio Grande Energia S.A. (“RGE”), considering RGE Sul as the Merging Company and RGE as the Merged Company;

Energy generation (conventional and renewable sources) | Company Type | Equity Interest | Location (State) | Number of plants / type of energy | Installed capacity | |

Total | CPFL participation | |||||

CPFL Geração de Energia S.A. ("CPFL Geração") | Publicly-quoted corporation | Direct | São Paulo and Goiás | 3 Hydroelectric (b) | 1,295 | 678 |

CERAN - Companhia Energética Rio das Antas ("CERAN") | Private corporation | Indirect | Rio Grande do Sul | 3 Hydroelectric | 360 | 234 |

Foz do Chapecó Energia S.A. ("Foz do Chapecó") | Private corporation | Indirect | Santa Catarina and | 1 Hydroelectric | 855 | 436 |

Campos Novos Energia S.A. ("ENERCAN") | Private corporation | Indirect | Santa Catarina | 1 Hydroelectric | 880 | 429 |

BAESA - Energética Barra Grande S.A. ("BAESA") | Publicly-quoted corporation | Indirect | Santa Catarina and | 1 Hydroelectric | 690 | 173 |

Centrais Elétricas da Paraíba S.A. ("EPASA") | Private corporation | Indirect | Paraíba | 2 Thermoelectric | 342 | 182 |

Paulista Lajeado Energia S.A. ("Paulista Lajeado") | Private corporation | Indirect | Tocantins | 1 Hydroelectric | 903 | 38 |

CPFL Energias Renováveis S.A. ("CPFL Renováveis") | Publicly-quoted corporation | Indirect | See chapter 11.4.2 | See chapter 11.4.2 | See chapter 11.4.2 | See chapter 11.4.2 |

CPFL Centrais Geradoras Ltda. ("CPFL Centrais Geradoras") | Limited company | Direct | São Paulo and Minas Gerais | 6 MHPPs | 4 | 4 |

Transmission | Company Type | Core activity | Equity Interest | |||

CPFL Transmissão Piracicaba S.A. ("CPFL Piracicaba") | Privately-held corporation | Electric energy transmission services | Indirect 100% | |||

CPFL Transmissão Morro Agudo S.A. ("CPFL Morro Agudo") | Privately-held corporation | Electric energy transmission services | Indirect 100% | |||

CPFL Transmissão Maracanaú S.A. ("CPFL Maracanaú") | Privately-held corporation | Electric energy transmission services | Indirect 100% | |||

CPFL Transmissão Sul I S.A. ("CPFL Sul I") | Privately-held corporation | Electric energy transmission services | Indirect 100% | |||

CPFL Transmissão Sul II S.A. ("CPFL Sul II") | Privately-held corporation | Electric energy transmission services | Indirect 100% | |||

Notes:

(b) CPFL Geração holds 51.54% of the assured power and power of the Serra da Mesa HPP, whose concession belongs to Furnas. The Cariobinha HPP and the Carioba TPP projects are deactivated pending the position of the Ministry of Mines and Energy on the anticipated closure of its concession and are not included in the table;

(c) The joint venture Chapecoense fully consolidates the interim financial statements of its direct subsidiary, Foz de Chapecó;

(d) Paulista Lajeado has a 7% participation in the installed power of Investco S.A. (5.94% share of its capital).

Page 8 de 57

| 1Q19 Results | May 7, 2019 |

Energy commercialization | Company Type | Core activity | Equity Interest |

CPFL Comercialização Brasil S.A. ("CPFL Brasil") | Private corporation | Energy commercialization | Direct |

Clion Assessoria e Comercialização de Energia Elétrica Ltda. ("CPFL Meridional") | Limited company | Commercialization and provision of energy services | Indirect |

CPFL Comercialização Cone Sul S.A. ("CPFL Cone Sul") | Private corporation | Energy commercialization | Indirect |

CPFL Planalto Ltda. ("CPFL Planalto") | Limited company | Energy commercialization | Direct |

CPFL Brasil Varejista S.A. ("CPFL Brasil Varejista") | Private corporation | Energy commercialization | Indirect |

Services | Company Type | Core activity | Equity Interest |

CPFL Serviços, Equipamentos, Industria e Comércio S.A. ("CPFL Serviços") | Private corporation | Manufacturing, commercialization, rental and maintenance of electro-mechanical equipment and service provision | Direct |

NECT Serviços Administrativos Ltda. ("Nect") | Limited company | Provision of administrative services | Direct |

CPFL Atende Centro de Contatos e Atendimento Ltda. ("CPFL Atende") | Limited company | Provision of telephone answering services | Direct |

CPFL Total Serviços Administrativos Ltda. ("CPFL Total") | Limited company | Billing and collection services | Direct |

CPFL Eficiência Energética S.A. ("CPFL Eficiência") | Private corporation | Management in Energy Efficiency | Direct |

TI Nect Serviços de Informática Ltda. ("Authi") | Limited company | IT services | Direct |

CPFL GD S.A. ("CPFL GD") | Private corporation | Electric energy generation services | Indirect |

Others | Company Type | Core activity | Equity Interest |

CPFL Jaguari de Geração de Energia Ltda. ("Jaguari Geração") | Limited company | Venture capital company | Direct |

Chapecoense Geração S.A. ("Chapecoense") | Private corporation | Venture capital company | Indirect |

Sul Geradora Participações S.A. ("Sul Geradora") | Private corporation | Venture capital company | Indirect |

CPFL Telecom S.A. ("CPFL Telecom") | Private corporation | Telecommunication services | Direct |

Page 9 de 57

| 1Q19 Results | May 7, 2019 |

3.1) Consolidation of CPFL Renováveis Financial Statements

On March 31, 2019, CPFL Energia indirectly held 51.56% of CPFL Renováveis, through its subsidiary CPFL Geração. CPFL Renováveis has been fully consolidated (100%, line by line), in CPFL Energia’s financial statements since August 1, 2011, and the interest held by the non-controlling shareholders has been mentioned bellow the net income line (in the Financial Statements), as “Non-Controlling Shareholders’ Interest”, and in the Shareholders Equity (in the Balance Sheet) in the line with the same name.

3.2) Consolidation of RGE Sul Financial Statements

On March 31, 2019, CPFL Energia held the following stake in the capital stock of RGE Sul: 89.0107%, directly, and 10.9893%, indirectly, through CPFL Brasil. RGE Sul has been fully consolidated (100%, line by line), in CPFL Energia’s financial statements since November 1st, 2016.

3.3) Economic-Financial Performance Presentation

In accordance with U.S. SEC (Securities and Exchange Commission) guidelines and pursuant to items 100(a) and (b) of Regulation G, with the disclosure of 4Q16/2016 results, in order to avoid the disclosure of non-GAAP measures, we no longer disclose the economic-financial performance considering the proportional consolidation of the generation projects and the adjustment of the numbers for non-recurring items, focusing the disclosure in the IFRS criterion. Only in chapter 5, of Indebtedness, we continue presenting the information in the financial covenants criterion, considering that the proper reconciliation with the numbers in the IFRS criterion are presented in item 12.11 of this report.

3.4) Consolidation of Transmission Companies

As of 4Q17, the subsidiaries CPFL Transmissão Piracicaba and CPFL Transmissão Morro Agudo are consolidated in the financial statements of the segment "Conventional Generation".

Page 10 de 57

| 1Q19 Results | May 7, 2019 |

4) ECONOMIC-FINANCIAL PERFORMANCE

Consolidated Income Statement - CPFL ENERGIA (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Gross Operating Revenue | 10,788 | 9,637 | 11.9% |

Net Operating Revenue | 7,127 | 6,375 | 11.8% |

Cost of Electric Power | (4,484) | (4,014) | 11.7% |

Operating Costs & Expenses | (1,603) | (1,470) | 9.0% |

EBIT | 1,041 | 891 | 16.9% |

EBITDA1 | 1,531 | 1,366 | 12.1% |

Financial Income (Expense) | (220) | (308) | -28.4% |

Income Before Taxes | 906 | 668 | 35.6% |

Net Income | 570 | 419 | 36.0% |

Note: (1) EBITDA is calculated from the sum of net income, taxes, financial result and depreciation/amortization, according to CVM Instruction no. 527/12. See the calculation in item 4.6 of this report.

4.1) Opening of economic-financial performance by business segment

Income Statement by business segment - CPFL Energia (R$ million) | ||||||||||||||||

|

| Distribution |

| Conventional Generation |

| Renewable Generation |

| Commerciali-zation |

| Services |

| Others |

| Eliminations |

| Total |

1Q19 | ||||||||||||||||

Net operating revenue | 5,936 | 269 | 334 | 760 | 146 | - | (318) | 7,127 | ||||||||

Operating costs and expenses |

| (4,957) |

| (51) |

| (142) |

| (730) |

| (110) |

| (11) |

| 318 |

| (5,682) |

Depreciation e amortization | (192) | (30) | (161) | (1) | (6) | (16) | - | (404) | ||||||||

Income from electric energy service |

| 788 |

| 188 |

| 31 |

| 30 |

| 30 |

| (27) |

| - |

| 1,041 |

Equity accounting | - | 86 | - | - | - | - | - | 86 | ||||||||

EBITDA |

| 980 |

| 304 |

| 192 |

| 31 |

| 36 |

| (11) |

| - |

| 1,531 |

Financial result | (60) | (44) | (112) | (8) | 0 | 3 | - | (220) | ||||||||

Income (loss) before taxes | 728 | 230 | (80) | 22 | 30 | (24) | - | 906 | ||||||||

Income tax and social contribution | (263) | (46) | (13) | (8) | (7) | 0 | - | (336) | ||||||||

Net income (loss) |

| 465 |

| 184 |

| (93) |

| 15 |

| 23 |

| (24) |

| - |

| 570 |

1Q18 | ||||||||||||||||

Net operating revenue | 5,201 | 281 | 384 | 710 | 112 | - | (313) | 6,375 | ||||||||

Operating costs and expenses |

| (4,408) |

| (42) |

| (156) |

| (702) |

| (89) |

| (9) |

| 313 |

| (5,094) |

Depreciation e amortization | (181) | (30) | (158) | (1) | (6) | (16) | - | (390) | ||||||||

Income from electric energy service |

| 612 |

| 210 |

| 70 |

| 7 |

| 17 |

| (25) |

| - |

| 891 |

Equity accounting | - | 85 | - | - | - | - | - | 85 | ||||||||

EBITDA |

| 792 |

| 325 |

| 228 |

| 8 |

| 23 |

| (9) |

| - |

| 1,366 |

Financial result | (105) | (68) | (129) | (7) | (0) | 2 | - | (308) | ||||||||

Income (loss) before taxes | 507 | 227 | (59) | (0) | 17 | (23) | - | 668 | ||||||||

Income tax and social contribution | (187) | (45) | (13) | (0) | (4) | 0 | - | (249) | ||||||||

Net income (loss) |

| 321 |

| 182 |

| (73) |

| (0) |

| 13 |

| (23) |

| - |

| 419 |

Variation | ||||||||||||||||

Net operating revenue | 14.1% | -4.3% | -12.9% | 7.1% | 30.4% | - | 1.8% | 11.8% | ||||||||

Operating costs and expenses |

| 12.4% |

| 23.2% |

| -8.7% |

| 3.9% |

| 23.3% |

| 15.8% |

| 1.8% |

| 11.6% |

Depreciation e amortization | 6.4% | -1.5% | 1.8% | -15.1% | 7.2% | 0.0% | - | 3.7% | ||||||||

Income from electric energy service |

| 28.7% |

| -10.1% |

| -55.1% |

| 321.5% |

| 75.1% |

| 5.9% |

| - |

| 16.9% |

Equity accounting | - | 0.5% | - | - | - | - | - | 0.5% | ||||||||

EBITDA |

| 23.6% |

| -6.5% |

| -15.7% |

| 295.0% |

| 58.5% |

| 15.8% |

| - |

| 12.1% |

Financial result | -43.1% | -35.1% | -13.5% | 5.9% | - | 42.2% | - | -28.4% | ||||||||

Income (loss) before taxes | 43.6% | 1.3% | 35.7% | - | 80.0% | 3.1% | - | 35.6% | ||||||||

Income tax and social contribution | 40.9% | 1.1% | -4.7% | 2480.8% | 86.2% | -79.3% | - | 35.0% | ||||||||

Net income (loss) |

| 45.1% |

| 1.4% |

| 28.3% |

| - |

| 78.1% |

| 4.1% |

| - |

| 36.0% |

Page 11 de 57

| 1Q19 Results | May 7, 2019 |

Note: an analysis of the economic-financial performance by business segment is presented in chapter 11.

4.2) Sectoral Financial Assets and Liabilities

In 1Q19, it was accounted the totalsectoral financial liabilities in the amount of R$ 324 million, compared to the totalsectoral financial assets in the amount of R$ 374 million in 1Q18, a variation of R$ 697 million.

On March 31, 2019, the balance of these sectoral financial assets and liabilities was positive in R$ 1,212 million, compared to a positive balance of R$ 1,508 million on December 31, 2018 and a positive balance of R$ 596 million on March 31, 2018.

As established by the applicable regulation, any sectoral financial assets or liabilities shall be included in the tariffs of the distributors in their respective annual tariff events.

4.3) Operating Revenue

In 1Q19, gross operating revenue reached R$ 10,788 million, representing an increase of 11.9% (R$ 1,150 million). Deductions from the gross operating revenue was of R$ 3,660 million in 1Q19, representing an increase of 12.2% (R$ 397 million). Net operating revenue reached R$ 7,127 million in 1Q19, registering an increase of 11.8% (R$ 753 million).

The main factors that affected the net operating revenue were:

· Increase of revenues in the Distribution segment, in the amount of R$ 735 million (for more details, see item 11.1.1.2);

· Increase of revenues in the Commercialization segment, in the amount of R$ 50 million;

· Increase of revenues in the Services segment, in the amount of R$ 34 million;

Partially offset by:

· Reduction of revenues in the Renewable Generation segment, in the amount of R$ 49 million;

· Reduction of revenues in the Conventional Generation segment, in the amount of R$ 12 million;

· Reduction of R$ 6 million, due to eliminations.

Page 12 de 57

| 1Q19 Results | May 7, 2019 |

4.4) Cost of Electric Energy

Cost of Electric Energy (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Cost of Electric Power Purchased for Resale | |||

Energy from Itaipu Binacional | 657 | 558 | 17.7% |

PROINFA | 105 | 86 | 22.1% |

Energy Purchased through Auction in the Regulated Environment, Bilateral Contracts and Energy Purchased in the Spot Market | 3,572 | 2,975 | 20.1% |

PIS and COFINS Tax Credit | (382) | (318) | 20.0% |

Total | 3,953 | 3,301 | 19.7% |

|

| ||

Charges for the Use of the Transmission and Distribution System |

|

| |

Basic Network Charges | 498 | 567 | -12.2% |

Itaipu Transmission Charges | 67 | 62 | 7.0% |

Connection Charges | 47 | 32 | 47.3% |

Charges for the Use of the Distribution System | 13 | 10 | 35.5% |

System Service Usage Charges - ESS | (41) | 47 | - |

Reserve Energy Charges - EER | - | 66 | -100.0% |

PIS and COFINS Tax Credit | (53) | (72) | -26.2% |

Total | 531 | 712 | -25.4% |

|

| ||

Cost of Electric Energy | 4,484 | 4,014 | 11.7% |

In 1Q19, the cost of electric energy, comprising the purchase of electricity for resale and charges for the use of the distribution and transmission system, amounted to R$ 4,484 million, registering an increase of 11.7% (R$ 470 million).

The factors that explain these variations follow below:

· The cost of electric power purchased for resale reached R$ 3,953 million in 1Q19, an increase of 19.7% (R$ 651 million), due to the following factors:

(i) Increase of 20.1% (R$ 597 million) in the cost of energy purchased through auction in the regulated environment, bilateral contracts and energy purchased in the spot market, due to the increases of 9.8% in the average purchase price (R$ 211.19/MWh in 1Q19 vs. R$ 192.33/MWh in 1Q18) and of 9.3% (1,446 GWh) in the volume of purchased energy;

(i) Increase of 17.7% (R$ 99 million) in the cost of energy from Itaipu, due to the increase of 18.5% in the average purchase price (R$ 241.63/MWh in 1Q19 vs. R$ 203.86/MWh in 1Q18), partially offset by the reduction of 0.7% (19 GWh) in the volume of purchased energy;

(ii) Increase of 22.1% (R$ 19 million) in the amount of PROINFA cost, due to the increases of 21.7% in the average purchase price (R$ 407.84/MWh in 1Q19 vs. R$ 335.19/MWh in 1Q18) and of 0.3% (1 GWh) in the volume of purchased energy;

Partially offset by:

(iii) Reduction of 20.0% (R$ 64 million) in PIS and COFINS tax credits (cost reducer), generated from the energy purchase;

Page 13 de 57

| 1Q19 Results | May 7, 2019 |

· Charges for the use of the transmission and distribution system reached R$ 531 million in 1Q19, a reduction of 25.4% (R$ 181 million), due to the following factors:

(i) Variation of R$ 88 million in the System Service Usage Charges – ESS, from an expense of R$ 47 million in 1Q18 to a revenue of R$ 41 million in 1Q19;

(ii) Reduction of 12.2% (R$ 69 million) in the basic network charges;

(iii) Reserve Energy Charges – EER of R$ 66 million in 1Q18;

Partially offset by:

(iv) Reduction of 26.2% (R$ 19 million) in PIS and COFINS tax credits (cost reducer), generated from the charges;

(v) Increase of 47.3% (R$ 15 million) in charges for connection;

(vi) Increase of 7.0% (R$ 4 million) in Itaipu transmission charges;

(vii) Increase of 35.5% (R$ 3 million) in charges for usage of the distribution system.

4.5) Operating Costs and Expenses

Operating costs and expenses reached R$ 1,603 million in 1Q19, compared to R$ 1,470 million in 1Q18, an increase of 9.0% (R$ 133 million).

The factors that explain these variations follow below:

PMSO

Reported PMSO (R$ million) | ||||

| 1Q19 | 1Q18 | Variation | |

| R$ MM | % | ||

Reported PMSO |

|

|

|

|

Personnel | (348) | (338) | (10) | 3.0% |

Material | (67) | (63) | (4) | 6.8% |

Outsourced Services | (165) | (181) | 16 | -8.8% |

Other Operating Costs/Expenses | (175) | (106) | (69) | 65.6% |

Allowance for doubtful accounts | (69) | (26) | (42) | 159.7% |

Legal and judicial expenses | (32) | (12) | (20) | 160.8% |

Others | (75) | (67) | (7) | 11.2% |

Total Reported PMSO | (755) | (687) | (68) | 9.9% |

The PMSO item reached R$ 755 million in 1Q19, compared to R$ 687 million in 1Q18, an increase of 9.9% (R$ 68 million), due to the following factors:

(i) | Personnel - increase of 3.0% (R$ 10 million), mainly due to the collective bargaining agreement – wages and benefits; |

(ii) | Material - increase of 6.8% (R$ 4 million), due to the increase in maintenance of the fleet, lines and networks (R$ 8 million), partially offset by the reduction in maintenance of machinery, equipment and others (R$ 5 million); |

(iii) | Outsourced services - reduction of 8.8% (R$ 16 million), mainly due to the primarization of services (R$ 27 million), partially offset by the maintenance of substations (R$ 8 million) and services related to electric energy billing (R$ 3 million); |

(iv) | Other operational costs/expenses-increase of 65.6% (R$ 69 million), mainly due to: |

ü Increase of 159.7% (R$ 42 million) in allowance for doubtful account; |

Page 14 de 57

| 1Q19 Results | May 7, 2019 |

ü Increase of 160.8% (R$ 20 million) in legal and judicial expenses;

ü Other effects (R$ 7 million).

Other operating costs and expenses

Other operating costs and expenses reached R$ 848 million in 1Q19, compared to R$ 783 million in 1Q18, registering an increase of 8.2% (R$ 65 million), due to the following factors:

· Increase of 12.1% (R$ 45 million) inCosts of Building the Infrastructure item;

· Increase of 4.3% (R$ 14 million) inDepreciation and Amortization item;

· Increase of 25.2% (R$ 6 million) inPrivate Pension Fund item, due to the registration of the impacts of the 2019 actuarial report;

· Increase of 0.8% (R$ 1 million) inAmortization of Intangible of Concession Asset item.

4.6) EBITDA

In 1Q19,EBITDA reached R$ 1,531 million, compared to R$ 1,366 million in 1Q18, registering an increase of 12.1% (R$ 165 million).

EBITDA is calculated according to CVM Instruction no. 527/12 and showed in the table below:

EBITDA and Net Income conciliation (R$ million) | |||

| 1Q19 | 1Q18 | Var. |

Net Income | 570 | 419 | 36.0% |

De preciation and Amortization | 405 | 390 | |

Financial Result | 220 | 308 | |

Income Tax / Social Contribution | 336 | 249 | |

EBITDA | 1,531 | 1,366 | 12.1% |

Page 15 de 57

| 1Q19 Results | May 7, 2019 |

4.7) Financial Result

Financial Result (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Revenues | |||

Income from Financial Investments | 49 | 66 | -26.8% |

Additions and Late Payment Fines | 75 | 70 | 8.3% |

Fiscal Credits Update | 1 | 3 | -51.7% |

Judicial Deposits Update | 9 | 9 | 1.1% |

Monetary and Foreign Exchange Updates | 8 | 23 | -63.7% |

Discount on Purchase of ICMS Credit | 7 | 7 | 2.1% |

Sectoral Financial Assets Update | 28 | 7 | 287.5% |

PIS and COFINS - over Other Financial Revenues | (10) | (12) | -11.0% |

Others | 40 | 25 | 61.3% |

Total | 207 | 197 | 4.8% |

|

| ||

Expenses |

|

| |

Debt Charges | (295) | (343) | -14.0% |

Monetary and Foreign Exchange Updates | (85) | (119) | -28.3% |

(-) Capitalized Interest | 6 | 6 | -10.0% |

Sectoral Financial Liabilities Update | - | (5) | -100.0% |

Use of Public Asset | (2) | (4) | -49.3% |

Others | (50) | (40) | 23.9% |

Total | (427) | (505) | -15.5% |

|

| ||

Financial Result | (220) | (308) | -28.4% |

In 1Q19,net financial expense was of R$ 220 million, a reduction of 28.4% (R$ 87 million) compared to the net financial expense of R$ 308 million reported in 1Q18.

The items explaining these variations in Financial Result are as follows:

· Financial Revenues: increase of 4.8% (R$ 9 million), from R$ 197 million in 1Q18 to R$ 207 million in 1Q19, mainly due to the following factors:

(i) Increase of 287.5% (R$ 20 million) insectoral financial assets update;

(ii) Increase of 61.3% (R$ 15 million) inother financial revenues;

(iii) Increase of 8.3% (R$ 6 million) inadditions and late payment fines;

(iv) Reduction of 11.0% (R$ 1 million) inPIS and COFINS over Interest on Own Capital (revenue reducer);

Partially offset by:

(v) Reduction of 26.8% (R$ 18 million) in theincome from financial investments, due to the reduction in the average balance of investments;

(vi) Reduction of 63.7% (R$ 14 million) in themonetary and foreign exchange updates, due to the reductions: (a) of R$ 11 million in revenues from fines, interest and monetary adjustment relating to installment payments made by consumers, and (b) of R$ 7 million in gains with the zero-cost collar derivative1; partially offset by the increases (c) of R$ 3million in other monetary and foreign exchange updates, and (d) of R$ 1 million in the update of the balance of tariff subsidies, as determined by ANEEL;

1In 2015, subsidiary CPFL Geração contracted US$ denominated put and call options, involving the same financial institution as counterpart, and which on a combined basis are characterized as an operation usually known as zero-cost collar. The contracting of this operation does not involve any kind of speculation, inasmuch as it is aimed at minimizing any negative impacts on future revenues of the joint venture ENERCAN, which has electric energy sale agreements with annual restatement of part of the tariff based on the variation in the US$. In addition, according to Management’s view, the scenario was favorable for contracting this type of financial instrument, considering the high volatility implicit in dollar options and the fact that there was no initial cost for same.

Page 16 de 57

| 1Q19 Results | May 7, 2019 |

(vii) Reduction of 51.7% (R$ 1 million) infiscal credits update.

· Financial Expenses: reduction of 15.5% (R$ 78 million), from R$ 505 million in 1Q18 to R$ 427 million in 1Q19, mainly due to the following factors:

(i) Reduction of 14.0% (R$ 48 million) ofdebt charges in local currency, due to the reduction in the average balance of debt;

(ii) Reduction of 28.3% (R$ 34 million) in themonetary and foreign exchange updates, due to: (a) the mark-to-market positive effect for financial operations under Law 4,131 – non-cash effect (R$ 33 million), and (b) the reduction of debt charges in foreign currency, with swap to CDI interbank rate (R$ 1 million);

(iii) Sectoral financial liabilities update in 1Q18, in the amount of R$ 5 million;

(iv) Reduction of 49.3% (R$ 2 million) in thefinancial expenses with the Use of Public Asset (UBP).

Partially offset by:

(v) Increase of 23.9% (R$ 10 million) inother financial expenses;

(vi) Reduction of 10.0% (R$ 1 million) incapitalized interest (expense reducer).

4.8) Net Income

Net incomewas of R$ 570 million in 1Q19, registering an increase of 36.0% (R$ 151 million) if compared to the net income of R$ 419 million observed in 1Q18.

Page 17 de 57

| 1Q19 Results | May 7, 2019 |

5) INDEBTEDNESS

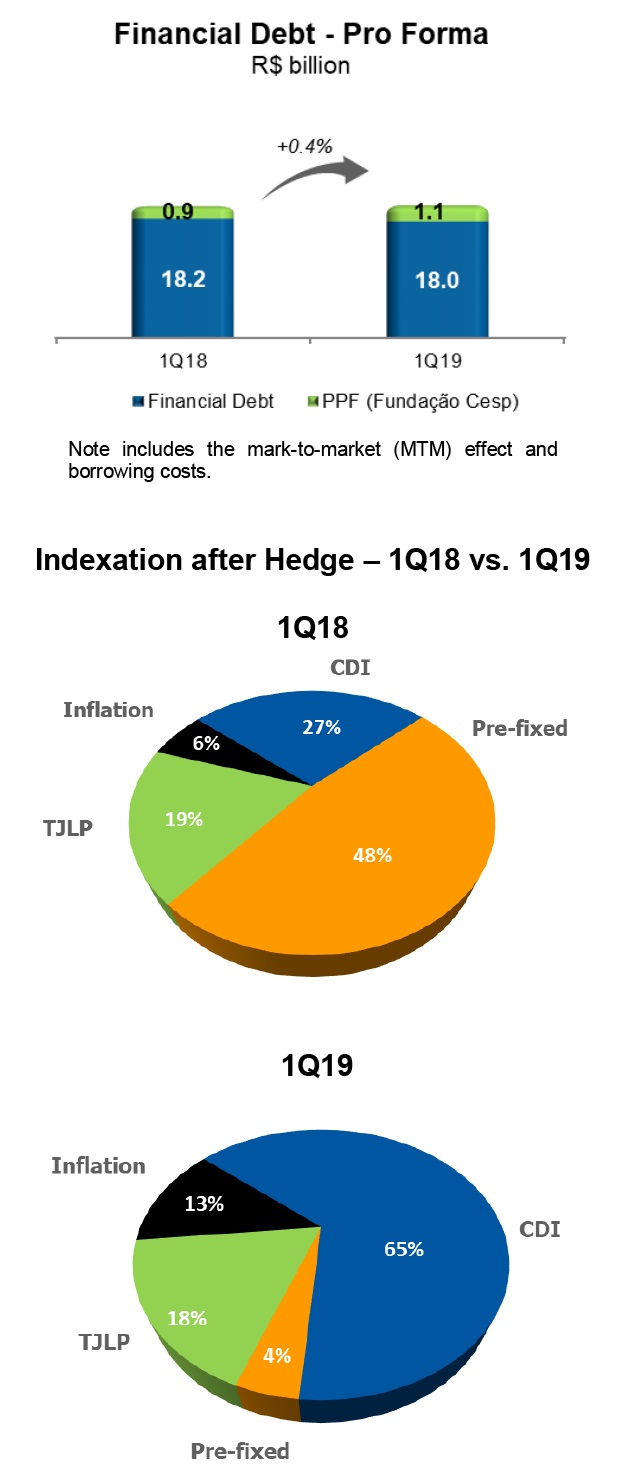

5.1) Debt (IFRS)

Note: for debt linked to foreign currency (24.0% of total in 1Q19), swap operations are contracted, aiming the protection of the foreign exchange and the rate linked to the contract.

Page 18 de 57

| 1Q19 Results | May 7, 2019 |

Net Debt in IFRS

IFRS | R$ Million | 1Q19 | 1Q18 | Var. % |

Financial Debt (including hedge) | (19,891) | (20,427) | -2.6% |

(+) Available Funds | 3,441 | 3,029 | 13.6% |

(=) Net Debt | (16,450) | (17,398) | -5.4% |

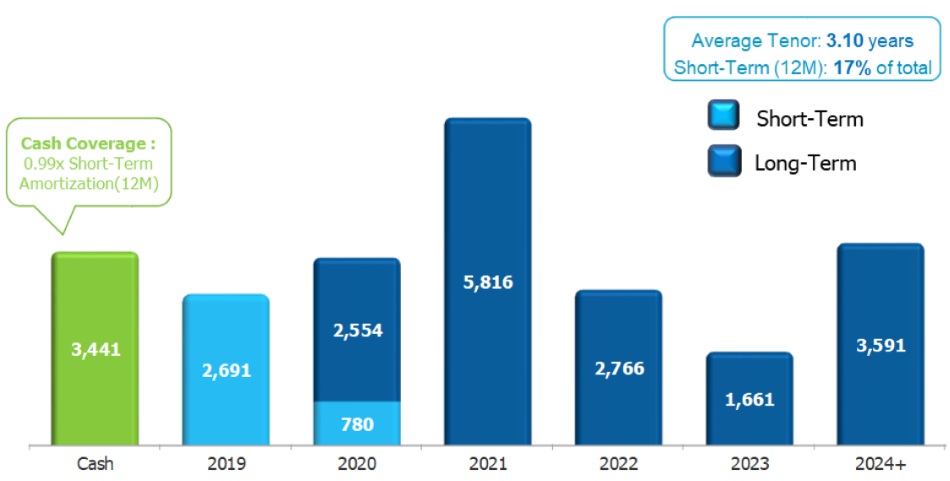

5.1.1) Debt Amortization Schedule in IFRS (Mar-19)

CPFL Energia has a large market access to liquidity sources through diversified funding alternatives, either through local market financing lines such as debenture issues, BNDES and other development banks, or through financing lines in the foreign market. This access to credit for the CPFL group is currently strengthened by the support of its shareholding structure, as State Grid gives greater robustness to CPFL group in financial market.

Notes:

1) Considers only the principal of the debt of R$ 19,859 million. In order to reach the value of debt in IFRS, of R$ 19,891 million, should be included charges and the mark-to-market (MTM) effect and cost with funding;

2) Short-term (April 2019 – March 2020) = R$ 3,471 million.

The cash position at the end of 1Q19 had a coverage ratio of0.99x the amortizations of the next 12 months, enough to honor all amortization commitments until the beginning of 2020. The average amortization term, calculated from this schedule, is of3.10 years.

Page 19 de 57

| 1Q19 Results | May 7, 2019 |

Gross Debt Cost1 in IFRS criteria

Note: (1) as of 2Q17, CPFL Energia started to calculate its debt average cost considering the end of the period, to better reflect the variations on interest rates.

5.2) Debt in Financial Covenants Criteria

5.2.1) Indexation and Debt Cost in Financial Covenants Criteria

Indexation1 After Hedge2 in Financial Covenants Criteria – 1Q18 vs. 1Q19

1) Considering proportional consolidation of CPFL Renováveis, CERAN, ENERCAN, Foz do Chapecó and EPASA;

2) For debt linked to foreign currency (26.5% of total), swap operations are contracted, aiming the protection of the foreign exchange and the rate linked to the contract.

Page 20 de 57

| 1Q19 Results | May 7, 2019 |

5.2.2) Net Debt in Financial Covenants Criteria and Leverage

In 1Q19 Proforma Net Debt totaledR$ 14,902 million, a reduction of4.4% compared to net debt position at the end of 1Q18, in the amount ofR$ 15,585 million.

Covenant Criteria (*) - R$ Million | 1Q19 | 1Q18 | Var. |

Financial Debt (including hedge)1 | (18,048) | (18,241) | -1.1% |

(+) Available Funds | 3,145 | 2,656 | 18.4% |

(=) Net Debt | (14,902) | (15,585) | -4.4% |

EBITDA Proforma2 | 5,515 | 4,708 | 17.2% |

Net Debt / EBITDA | 2.70 | 3.31 | -18.4% |

1) Considering proportional consolidation of CPFL Renováveis, CERAN, ENERCAN, Foz do Chapecó and EPASA;

2) Proforma EBITDA in the financial covenants criteria: adjusted according to equivalent participation of CPFL Energia in each of its subsidiaries, with the inclusion of regulatory assets and liabilities and the historical EBITDA of newly acquired projects.

In line with the criteria for calculation of financial covenants of loan agreements with financial institutions, net debt is adjusted according to the equivalent stake of CPFL Energia in each of its subsidiaries. Also, include in the calculation of Proforma EBITDA the effects of historic EBITDA of newly acquired projects. Considering that the Proforma Net Debt totaledR$ 14,902 million and Proforma EBITDA in the last 12 months reachedR$ 5,515 million, the ratio Proforma Net Debt / EBITDA at the end of 1Q19 reached2.70x.

6) INVESTMENTS

6.1) Actual Investments

Investments (R$ Million) | |||

Segment | 1Q19 | 1Q18 | Var. |

Distribution | 404 | 366 | 10.1% |

Generation - Conventional | 1 | 1 | 16.0% |

Transmission1 | 0 | 0 | -68.2% |

Generation - Renewable | 33 | 44 | -26.2% |

Commercialization | 1 | 1 | -24.3% |

Services and Others2 | 7 | 13 | -44.5% |

Total | 445 | 426 | 4.6% |

Note:

1) Investments related to the transmission segment, according to IFRIC 15, are recorded as “Contractual Asset of Transmission Companies” (in other credits). Investments of R$ 55 thousands in 1Q19 and R$ 172 thousands in 1Q18.

2) Others – basically refer to assets and transactions that are not related to the listed segments.

In 1Q19, investments were R$ 445 million, an increase of 4.6%, compared to R$ 426 million registered in 1Q18. We highlight investments made by CPFL Energia in the Distribution segment:

a. Expansion and strengthening of the electric system;

b. Electricity system maintenance and improvements;

c. Operational infrastructure;

d. Upgrade of management and operational support systems;

e. Customer help services;

f. Research and development programs;

Page 21 de 57

| 1Q19 Results | May 7, 2019 |

6.2) Investments Forecasts

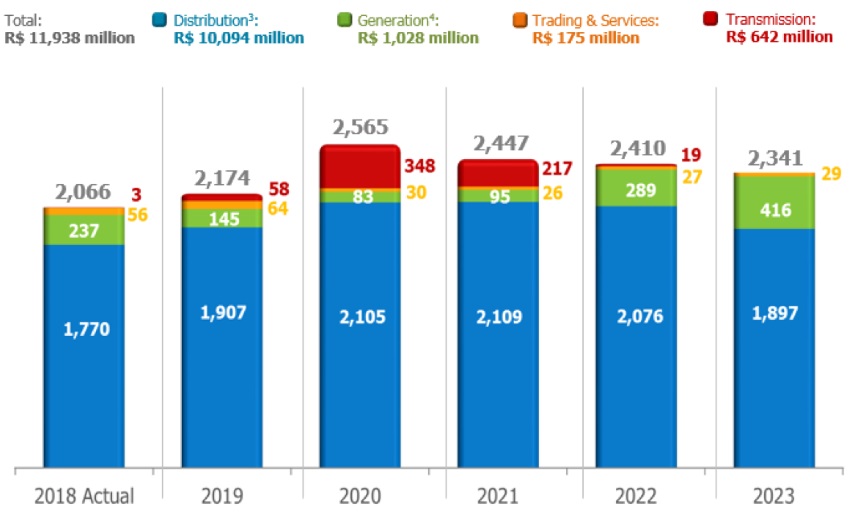

On November 30, 2018, CPFL Energia’s Board of Directors approved Board of Executive Officers’ proposal for 2019 Annual Budget and 2020/2023 Multiannual Plan for the Company, which was previously discussed by the Budget and Corporate Finance Commission.

Investments Forecasts (R$ million)1

Notes:

1) Constant currency;

2) Investment Plan released in 4Q18/2018 Earnings Release, from March 2019;

3) Disregard investments in Special Obligations (among other items financed by consumers);

4) Conventional + Renewable.

Page 22 de 57

| 1Q19 Results | May 7, 2019 |

7) ALLOCATION OF RESULTS

The Company’s Bylaws require the distribution of at least 25% of net income adjusted according to law, as dividends to its shareholders. The proposal for allocation of net income from the fiscal year is shown below:

| Thousands of R$ |

Net income of the fiscal year - Individual | 2,058,040 |

Realization of comprehensive income | 25,117 |

Adjustments from previous years - IFRS 9/CPC 48 adoption | (82,607) |

Reversion of statutory reserve - concession financial asset | 826,600 |

Net income base for allocation | 2,827,151 |

Legal reserve | (102,902) |

Statutory reserve - working capital reinforcement | (2,235,465) |

Minimum mandatory dividend | (488,785) |

Minimum Mandatory Dividend (25%)

At the Annual General Shareholders’ Meeting (AGM), held on April 30, 2019, at 10:00 a.m., among other matters, it was declared the distribution and it was approved the payment of dividends by the Company, in the amount ofR$ 488,784,574.40 (four hundred and eighty-eight million, seven hundred and eighty-four thousand, five hundred and seventy-four reais and forty centavos), equivalent toR$ 0.480182232 per common share issued by the Company.

Pursuant to paragraph 3 of article 205 of Law No. 6,404/76, the payment of dividends will be made in one single installment, untilDecember 31, 2019, in a specific date to be informed in due course to the shareholders and to the market, without monetary update or incurring interest between the declaration date and the effective payment date.

Shareholders owning shares on April 30, 2019 will be entitled to receive the dividends. Shares will be traded “ex-dividend” at the Brazilian Stock Exchange (B3 S.A. – Brasil, Bolsa, Balcão, or “B3”) and at the New York Stock Exchange (NYSE) as of May 2, 2019.

Statutory Reserve – Working Capital Reinforcement

For this fiscal year, considering the current macro scenario with an incipient economic recovery, and also considering the uncertainties regarding hydrology, the Company’s Management proposed the allocation of R$ 2.235 million to the statutory reserve - working capital reinforcement.

8) STOCK MARKETS

CPFL Energia is listed on both the B3 (Novo Mercado) and the New York Stock Exchange (NYSE) (ADR Level III), segments with the highest levels of corporate governance.

Page 23 de 57

| 1Q19 Results | May 7, 2019 |

B3 | NYSE | ||||||

Date | CPFE3 (R$) | IEE | IBOV | Date | CPL (US$) | DJBr20 | Dow Jones |

03/31/2019 | R$ 30.48 | 57,449 | 95,415 | 03/31/2019 | $ 15.52 | 23,618 | 25,929 |

12/31/2018 | R$ 28.85 | 49,266 | 87,887 | 12/31/2018 | $ 14.80 | 22,007 | 23,327 |

03/31/2018 | R$ 24.91 | 41,445 | 85,366 | 03/31/2018 | $ 15.00 | 25,170 | 24,103 |

QoQ | 5.6% | 16.6% | 8.6% | QoQ | 4.9% | 7.3% | 11.2% |

YoY | 22.4% | 38.6% | 11.8% | YoY | 3.5% | -6.2% | 7.6% |

On March 31, 2019, CPFL Energia’s shares closed at R$ 30.48 per share on the B3 and US$ 15.52 per ADR on the NYSE, an appreciation in the quarter of 5.6% and 4.7%, respectively. Considering the variation in the last 12 months, the shares and ADRs presented an appreciation of 22.4% on the B3 and of 3.5% on the NYSE.

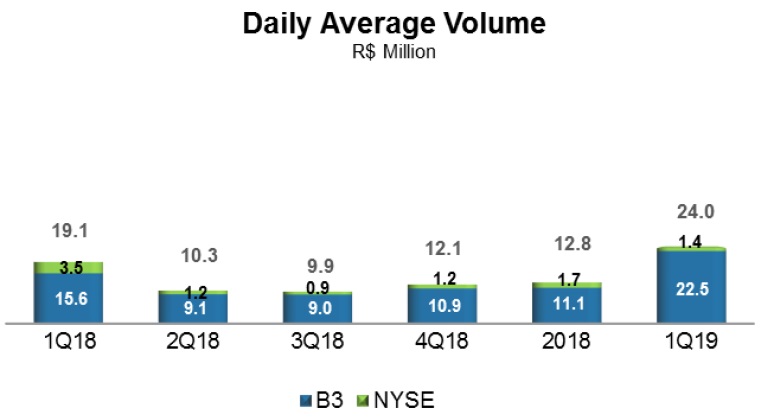

8.2) Daily Average Volume

The daily trading volume in 1Q19 averaged R$ 24.0 million, of which R$ 22.5 million on the B3 and R$ 1.4 million on the NYSE, representing a reduction of 25.5% in relation to 1Q18. The number of trades on the B3 decreased by 13.0%.

Note: Considers the sum of the average daily volume on the B3 and NYSE.

Page 24 de 57

| 1Q19 Results | May 7, 2019 |

9) CORPORATE GOVERNANCE

The corporate governance model adopted by CPFL Energia and its subsidiaries is based on the principles of transparency, equity, accountability and corporate responsibility.

In 2018, CPFL marked 14 years since being listed on the B3 and the New York Stock Exchange (“NYSE”). With more than 100 years of history in Brazil, the Company’s shares are listed on theNovo MercadoSpecial Listing Segment of the B3 with Level III ADRs, special segments for companies that comply with corporate governance best practices. All CPFL shares are common shares, entitling all shareholders the right to vote, as well as the tag along right with same conditions granted to the seller, in case of an offer which results in control transference.

CPFL’s Management is composed of the Board of Directors (“Board”), its decision-making authority, and the Board of Executive Officers, its executive body. The Board is responsible for defining the strategic business direction of the holding company and subsidiaries, and is composed of 9 members (of which 2 independent members), with terms of one year, eligible for reelection.

The Internal Regulation of the Board establishes the procedures for evaluating the directors, under the leadership of the Chairman, as well as their main duties and rights.

The Board set up three advisory committees (Management Processes, Risks and Sustainability, People Management and Related Parties), which support the Board in its decisions and monitor relevant and strategic themes, such as people and risk management, sustainability, the surveillance of internal audits, analysis of transactions with parties that are related to controlling shareholders and handling of incidents recorded through complaint hotlines and ethical conduct channels. Furthermore, 2 advisory commissions were setad hoc, as foreseen in the Internal Regulation: Strategy and Finance and Budget, which support the Board in subjects related to the strategic plan, as well as the budget follow-up.

The Board of Executive Officers is composed of 1 Chief Executive Officer and 9 Vice Presidents, with terms of two years, eligible for reelection, responsible for executing the strategy of CPFL Energia and its subsidiaries as defined by the Board of Directors in line with corporate governance guidelines. To ensure alignment of governance practices, Executive Officers sit on the Boards of Directors of companies that form the CPFL group and nominate their respective executive officers.

CPFL has a permanent Fiscal Council, composed of 3 members, that also exercises the duties of Audit Committee, in line with Sarbanes-Oxley Law (SOX), applicable to foreign companies listed on U.S. stock exchanges.

The guidelines and documents on corporate governance are available at the Investor Relations website http://www.cpfl.com.br/ir.

Page 25 de 57

| 1Q19 Results | May 7, 2019 |

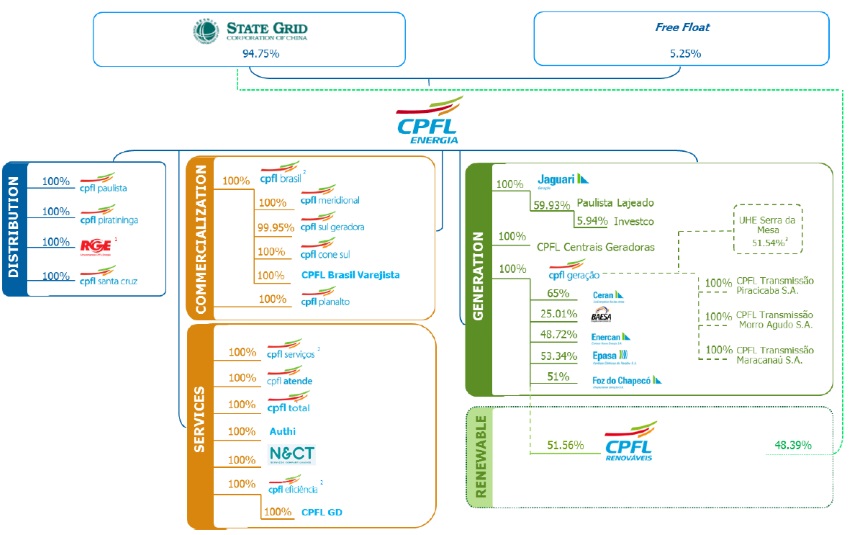

10) SHAREHOLDERS STRUCTURE

CPFL Energia is a holding company that owns stake in other companies. State Grid Corporation of China (SGCC) controls CPFL Energia through its subsidiaries State Grid International Development Co., Ltd, State Grid International Development Limited (SGID), International Grid Holdings Limited, State Grid Brazil Power Participações S.A. (SGBP) and ESC Energia S.A.:

Reference date: 03/31/2019

Notes:

(1) RGE is held by CPFL Energia (89.0107%) and CPFL Brasil (10.9893%).

(2) CPFL Soluções = CPFL Brasil + CPFL Serviços + CPFL Eficiência;

(3) 51.54% stake of the availability of power and energy of Serra da Mesa HPP, regarding the Power Purchase Agreement between CPFL Geração and Furnas;

Page 26 de 57

| 1Q19 Results | May 7, 2019 |

11) PERFORMANCE OF THE BUSINESS SEGMENTS

11.1) Distribution Segment

11.1.1) Economic-Financial Performance

Consolidated Income Statement - Distribution (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Gross Operating Revenue | 9,446 | 8,329 | 13.4% |

Net Operating Revenue | 5,936 | 5,201 | 14.1% |

Cost of Electric Power | (3,877) | (3,451) | 12.4% |

Operating Costs & Expenses | (1,271) | (1,138) | 11.7% |

EBIT | 788 | 612 | 28.7% |

EBITDA(1) | 980 | 792 | 23.6% |

Financial Income (Expense) | (60) | (105) | -43.1% |

Income Before Taxes | 728 | 507 | 43.6% |

Net Income | 465 | 321 | 45.1% |

Note:

(1) EBITDA (IFRS) is calculated from the sum of net income, taxes, financial result and depreciation/amortization, as CVM Instruction no. 527/12.

11.1.1.1) Sectoral Financial Assets and Liabilities

In 1Q19, totalsectoral financial liabilities accounted for R$ 324 million, a variation of R$ 697 million if compared to 1Q18, whensectoral financial assets amounted to R$ 374 million.

On March 31, 2019, the balance of sectoral financial assets and liabilities was positive in R$ 1,212 million, compared to a positive balance of R$ 1,508 million on December 31, 2018 and a positive balance of R$ 596 million on March 31, 2018.

As established by the applicable regulation, any sectoral financial assets or liabilities shall be included in the tariffs of the distributors in their respective annual tariff events.

Page 27 de 57

| 1Q19 Results | May 7, 2019 |

11.1.1.2) Operating Revenue

Operating Revenue (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Gross Operating Revenue | |||

Revenue with Energy Sales (Captive + TUSD) | 8,567 | 6,950 | 23.3% |

Short-term Electric Energy | 243 | 115 | 111.6% |

Revenue from Building the Infrastructure of the Concession | 415 | 370 | 12.1% |

Sectoral Financial Assets and Liabilities | (324) | 374 | - |

CDE Resources - Low-income and Other Tariff Subsidies | 429 | 377 | 13.8% |

Adjustments to the Concession's Financial Asset | 64 | 65 | -0.6% |

Other Revenues and Income | 52 | 79 | -34.3% |

Total | 9,446 | 8,329 | 13.4% |

|

| ||

Deductions from the Gross Operating Revenue |

|

| |

ICMS Tax | (1,740) | (1,400) | 24.2% |

PIS and COFINS Taxes | (794) | (736) | 7.9% |

CDE Sector Charge | (998) | (898) | 11.1% |

R&D and Energy Efficiency Program | (55) | (48) | 16.3% |

PROINFA | (39) | (35) | 10.1% |

Tariff Flags and Others | 122 | (7) | - |

Others | (7) | (5) | 26.4% |

Total | (3,510) | (3,129) | 12.2% |

|

| ||

Net Operating Revenue | 5,936 | 5,201 | 14.1% |

In 1Q19, gross operating revenue amounted to R$ 9,446 million, an increase of 13.4% (R$ 1,117 million), due to the following factors:

· | Increase of 23.3% (R$ 1,617 million) in the revenue with energy sales (captive + free clients), due to: (i) the positive average tariff adjustment in the distribution companies for the period between 1Q18 and 1Q19 (highlight for the average increases of 16.90% in CPFL Paulista and 22.47% in RGE Sul, in April 2018, of 20.58% in RGE, in June 2018, and of 19.25% in CPFL Piratininga, in October 2018); and (ii) the increase of 3.2% in the sales volume within the concession area; |

· | Increase of 111.6% (R$ 128 million) in Short-term Electric Energy; |

· | Increase of 13.8% (R$ 52 million) in tariff subsidies (CDE resources); |

· | Increase of 12.1% (R$ 45 million) in revenue from building the infrastructure of the concession; |

Partially offset by:

· | Variation of R$ 697 million in the Sectoral Financial Assets/Liabilities, from a sectoral financial asset of R$ 374 million in 1Q18 to a sectoral financial liability of R$ 324 million in 1Q19; |

· | Reduction of 34.3% (R$ 27 million) in Other Revenues and Income. |

Deductions from the gross operating revenue were R$ 3,510 million in 1Q19, representing an increase of 12.2% (R$ 381 million), due to the following factors:

Page 28 de 57

| 1Q19 Results | May 7, 2019 |

· Increase of 24.2% (R$ 340 million) in ICMS tax;

· Increase of 11.1% (R$ 100 million) in the CDE sector charge;

· Increase of 7.9% (R$ 58 million) in PIS and COFINS taxes;

· Increase of 16.3% (R$ 8 million) in the R&D and Energy Efficiency Program.

· Increase of 10.1% (R$ 4 million) in the PROINFA;

· Increase of 26.4% (R$ 1 million) in other deductions from the gross operating revenue;

Partially offset by the following factor:

· Variation of R$ 129 million in tariff flags approved by the CCEE, from an expense of R$ 7 million in 1Q18 to a revenue of R$ 122 million in 1Q19.

Net operating revenue reached R$ 5,936 million in 1Q19, representing an increase of 14.1% (R$ 735 million).

11.1.1.3) Cost of Electric Energy

Cost of Electric Energy (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Cost of Electric Power Purchased for Resale | |||

Energy from Itaipu Binacional | 657 | 558 | 17.7% |

PROINFA | 105 | 86 | 22.1% |

Energy Purchased through Auction in the Regulated Environment, Bilateral Contracts and Energy Purchased in the Spot Market | 2,932 | 2,384 | 23.0% |

PIS and COFINS Tax Credit | (324) | (265) | 22.1% |

Total | 3,370 | 2,764 | 22.0% |

|

| ||

Charges for the Use of the Transmission and Distribution System |

|

| |

Basic Network Charges | 479 | 549 | -12.7% |

Itaipu Transmission Charges | 67 | 62 | 7.0% |

Connection Charges | 45 | 30 | 53.0% |

Charges for the Use of the Distribution System | 9 | 5 | 60.4% |

System Service Usage Charges - ESS | (41) | 47 | - |

Reserve Energy Charges - EER | - | 66 | - |

PIS and COFINS Tax Credit | (52) | (71) | -27.7% |

Total | 507 | 687 | -26.2% |

|

| ||

Cost of Electric Energy | 3,877 | 3,451 | 12.4% |

In 1Q19, the cost of electric energy, comprising the purchase of electricity for resale and charges for the use of the distribution and transmission system, amounted to R$ 3,877 million, representing an increase of 12.4% (R$ 426 million):

· Thecost of electric power purchased for resale was R$ 3,370 million in 1Q19, representing an increase of 22.0% (R$ 607 million), due to the following factors:

(i) Increase of 23.0% (R$ 548 million) in thecost of energy purchased through auction in the regulated environment, bilateral contracts and energy purchased in the spot market, due to the increases of 10.4% in the average purchase price (from R$ 213.51/MWh in 1Q18 to R$ 235.78/MWh in 1Q19) and of 11.3% (1,267 GWh) in thevolume of purchased energy;

Page 29 de 57

| 1Q19 Results | May 7, 2019 |

(ii) Increase of 17.7% (R$ 99 million) in thecost of energy fromItaipu, due to theincrease of 18.5% in the average purchase price (from R$ 203.86/MWh in 1Q18 to R$ 241.63/MWh in 1Q19), partially offset by the reduction of 0.7% (19 GWh) in the volume of purchased energy;

(iii) Increase of 22.1% (R$ 19 million) in thecost of the Proinfa, due to theincreases of 21.9% in the average purchase price (from R$ 335.19/MWh in 1Q18 to R$ 408.60/MWh in 1Q19) and of 0.1% (1 GWh) in the volume of purchased energy;

Partially offset by:

(iv) Increase of 22.1% (R$ 59 million) inPIS and Cofins tax credit (cost reducer), generated from the energy purchase.

· Charges for the use of the transmission and distribution system reached R$ 507 million in 1Q19, representing a reduction of 26.2% (R$ 180 million), due to the following factors:

(i) Variation of R$ 88 million in theSystem Service Usage Charges – ESS, from an expense of R$ 47 million in 1Q18 to a revenue of R$ 41 million in 1Q19;

(ii) Reduction of 12.7% (R$ 70 million) incharges for basic network;

(iii) Reserve Energy Charges – EER in 1Q18, in the amount of R$ 66 million;

Partially offset by:

(iv) Reduction of 27.7% (R$ 20 million) inPIS and Cofins tax credit (cost reducer), generated from the charges;

(v) Increase of 53.0% (R$ 16 million) inconnection charges;

(vi) Increase of 7.0% (R$ 4 million) in theItaipu transmission charges;

(vii) Increase of 60.4% (R$ 3 million) in theusage of the distribution system charges.

11.1.1.4) Operating Costs and Expenses

Operating costs and expenses reached R$ 1,271 million in 1Q19, compared to R$ 1,138 million in 1Q18, an increase of 11.7% (R$ 133 million).

Page 30 de 57

| 1Q19 Results | May 7, 2019 |

The factors that explain these variations follow below:

PMSO

Reported PMSO (R$ million) | ||||

| 1Q19 | 1Q18 | Variation | |

| R$ MM | % | ||

Reported PMSO |

|

|

|

|

Personnel | (226) | (224) | (2) | 1.0% |

Material | (46) | (40) | (6) | 14.7% |

Outsourced Services | (207) | (206) | (0) | 0.1% |

Other Operating Costs/Expenses | (158) | (95) | (63) | 67.0% |

Allowance for doubtful accounts | (68) | (26) | (42) | 159.9% |

Legal and judicial expenses | (31) | (11) | (19) | 166.6% |

Others | (59) | (57) | (2) | 4.2% |

Total Reported PMSO | (637) | (565) | (72) | 12.7% |

In 1Q19,PMSO reached R$ 637 million, an increase of 12.7% (R$ 72 million), compared to R$ 565 million in 1Q18.

Personnel– increase of 1.0% (R$ 2 million), mainly due to the collective bargaining agreement – wages and benefits;

Material– increase of 14.7% (R$ 6 million), mainly due to the increases in the replacement of material to the maintenance of lines and grid (R$ 3 million) and in the fleet maintenance (R$ 2 million);

Third party services – increase of 0.1% (R$ 0.2 million);

Other operating costs/expenses – increase of 67.0% (R$ 63 million), due to the increases in the following items: (a) allowance for doubtful accounts (R$ 42 million), (b) legal and judicial expenses (R$ 19 million), and (c) other costs/expenses (R$ 2 million).

Other operating costs and expenses

In 1Q19, other operating costs and expenses reached R$ 635 million, compared to R$ 573 million in 1Q18, registering an increase of 10.8% (R$ 62 million), with the variations below:

(i) | Increase of 12.1% (R$ 45 million) incost of building the concession´s infrastructure. This item, which reached R$ 415 million in 1Q19, does not affect results, since it has its counterpart in “operating revenue”; |

(ii) | Increase of 6.9% (R$ 12 million) inDepreciation and Amortization item; |

(iii) | Increase of 25.3% (R$ 6 million) inPrivate Pension Fund item, due to the registration of the impacts of the 2019 actuarial report. |

Page 31 de 57

| 1Q19 Results | May 7, 2019 |

11.1.1.5) EBITDA

EBITDAtotaled R$ 980 million in 1Q19, compared to R$ 792 million in 1Q18, an increase of 23.6% (R$ 187 million).

Conciliation of Net Income and EBITDA (R$ million) | |||

| 1Q19 | 1Q18 | Var. |

Net income | 465 | 321 | 45.1% |

Depreciation and Amortization | 192 | 181 |

|

Financial Results | 60 | 105 |

|

Income Tax /Social Contribution | 263 | 187 |

|

EBITDA | 980 | 792 | 23.6% |

11.1.1.6) Financial Result

Financial Result (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Revenues | |||

Income from Financial Investments | 17 | 24 | -28.6% |

Additions and Late Payment Fines | 74 | 68 | 9.1% |

Fiscal Credits Update | 1 | 2 | -43.8% |

Judicial Deposits Update | 9 | 9 | 1.2% |

Monetary and Foreign Exchange Updates | 8 | 18 | -55.5% |

Discount on Purchase of ICMS Credit | 7 | 7 | 2.1% |

Sectoral Financial Assets Update | 28 | 7 | 287.5% |

PIS and COFINS - over Other Financial Revenues | (9) | (9) | -6.0% |

Others | 10 | 11 | -9.4% |

Total | 145 | 136 | 6.4% |

|

| ||

Expenses |

|

| |

Debt Charges | (140) | (145) | -3.3% |

Monetary and Foreign Exchange Updates | (59) | (75) | -22.0% |

(-) Capitalized Interest | 6 | 4 | 48.4% |

Sectoral Financial Liabilities Update | - | (5) | -100.0% |

Others | (12) | (20) | -42.8% |

Total | (205) | (241) | -15.1% |

|

| ||

Financial Result | (60) | (105) | -43.1% |

In 1Q19, the net financial result recorded a net financial expense of R$ 60 million, a reduction of 43.1% (R$ 45 million). The items explaining these changes are as follows:

Page 32 de 57

| 1Q19 Results | May 7, 2019 |

· Financial Revenue: increase of 6.4% (R$ 9 million), from R$ 136 million in 1Q18 to R$ 145 million in 1Q19, mainly due to the following factors:

(i) | Increase of 287.5% (R$ 20 million) insectoral financial assets update; |

(ii) | Increase of 9.1% (R$ 6 million) inlate payment interest and fines; |

(iii) | Reduction of 6.0% (R$ 1 million) inPIS and Cofins on financial revenues (revenue reducer); |

Partially offset by:

(iv) | Reduction of 55.5% (R$ 10 million) inadjustments for inflation and exchange rate changes, due to (a) the reduction of R$ 11 million in revenues from fines, interest and monetary adjustment relating to installment payments made by consumers; partially offset by the increase (b) of R$ 1 million in the adjustment of the balance of tariff subsidies, as determined by Aneel; |

(v) | Reduction of 28.6% (R$ 7 million) in theincome from financial investments, due to the lower average balance of investments; |

(vi) | Reduction of 43.8% (R$ 1 million) infiscal credits update; |

(vii) | Reduction of 9.4% (R$ 1 million) inother financial revenues. |

· Financial Expense: reduction of 15.1% (R$ 36 million), from R$ 241 million in 1Q18 to R$ 205 million in 1Q19, mainly due to the following factors:

(i) | Reduction of 22.0% (R$ 17 million) inadjustments for inflation and exchange rate changes, due to: (a) the mark-to-market positive effect for financial operations under Law 4,131 – non-cash effect (R$ 21 million); partially offset by (b) the increase of debt charges in foreign currency, with swap to CDI interbank rate (R$ 5 million); |

(ii) | Reduction of 42.8% (R$ 9 million) inother financial expenses; |

(iii) | Reduction of 3.3% (R$ 5 million) in interest on debt in local currency; |

(iv) | Sectoral financial liabilities update in 1Q18, in the amount of R$ 5 million; |

(v) | Increase of 48.4% (R$ 2 million) incapitalized interest (expense reducer). |

11.1.1.7) Net Income

Net Incometotaled R$ 465 million in 1Q19, compared to R$ 321 million in 1Q18, an increase of 45.1% (R$ 145 million).

11.1.2) Tariff Events

Reference dates

Tariff Process Dates | |

Distributor | Date |

CPFL Santa Cruz | March 22nd |

CPFL Paulista | April 8th |

New RGE | June 19th |

CPFL Piratininga | October 23rd |

Page 33 de 57

| 1Q19 Results | May 7, 2019 |

Tariff Revision | |||

Distributor | Periodicity | Next Revision | Cycle |

CPFL Piratininga | Every 4 years | October 2019 | 5thPTRC |

CPFL Santa Cruz | Every 5 years | March 2021 | 5th PTRC |

CPFL Paulista | Every 5 years | April 2023 | 5th PTRC |

New RGE | Every 5 years | June 2023 | 5th PTRC |

Annual tariff adjustments of October 2018, March 2019 and April 2019

| CPFL Piratininga | CPFL Santa Cruz | CPFL Paulista |

Ratifying Resolution | 2,472 | 2,522 | 2,526 |

Adjustment | 20.01% | 13.70% | 12.02% |

Parcel A | 7.07% | 1.12% | 0.78% |

Parcel B | 1.76% | 0.90% | 2.17% |

Financial Components | 11.18% | 11.68% | 9.07% |

Effect on consumer billings | 19.25% | 13.31% | 8.66% |

Date of entry into force | 10/23/2018 | 03/22/2019 | 04/08/2019 |

Periodic tariff reviews occurred in 2018

| RGE Sul | RGE |

Ratifying Resolution | 2,385 | 2,401 |

Adjustment | 18.44% | 21.27% |

Parcel A | 6.79% | 6.11% |

Parcel B | 4.77% | 9.45% |

Financial Components | 6.88% | 5.71% |

Effect on consumer billings | 22.47% | 20.58% |

Date of entry into force | 04/19/2018 | 06/19/2018 |

Page 34 de 57

| 1Q19 Results | May 7, 2019 |

4th Periodic Tariff Review Cycle | RGE Sul | RGE |

Date | Apr-18 | Jun-18 |

Gross Regulatory Asset Base (A) | 3,605 | 4,374 |

Depreciation Rate (B) | 3.87% | 3.74% |

Depreciation Quota (C = A x B) | 140 | 164 |

Net Regulatory Asset Base (D) | 2,389 | 3,032 |

Pre-tax WACC (E) | 12.26% | 12.26% |

Cost of Capital (F = D x E) | 290 | 372 |

Special Obligations (G) | 5 | 8 |

Regulatory EBITDA (H = C + F + G) | 435 | 543 |

OPEX = CAOM + CAIMI (I) | 438 | 523 |

Parcel B (J = H + I) | 872 | 1,066 |

Productivity Index Parcel B ( K ) | 0.98% | 1.07% |

Quality Incentive Mechanism ( L) | -0.71% | 0.05% |

Parcel B with adjusts (M = J * (K - L) | 870 | 1,054 |

Other Revenues (N) | 19 | 28 |

Adjusted Parcel B (O = M - N) | 851 | 1,026 |

Parcel A (P) | 2,653 | 2,816 |

Required Revenue (Q = O + P) | 3,504 | 3,842 |

On April 17, 2018, ANEEL approved the result of the fourth Periodic Tariff Review of distributor RGE Sul. The average effect to be perceived by the consumers was 22.47% and details can be found in the table above.

RGE

On June 19, 2018, ANEEL approved the result of the fourth Periodic Tariff Review of distributor RGE Sul. The average effect to be perceived by the consumers was 20.58% and details can be found in the table above.

11.1.3) Operating Performance of Distribution

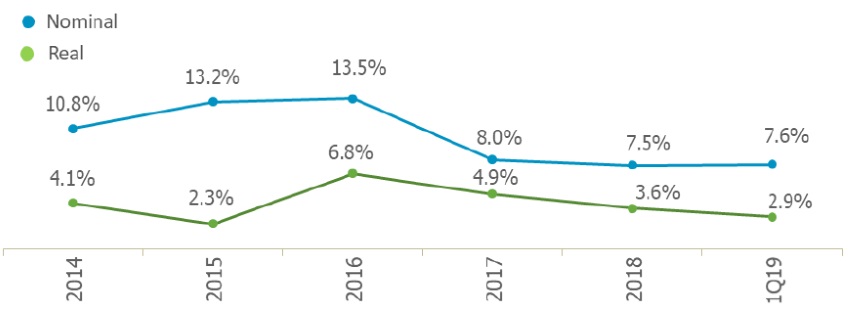

Below we are presenting the results achieved by the distribution companies with regard to the main indicators that measure the quality and reliability of their supply of electric energy. The SAIDI (System Average Interruption Duration Index) measures the average duration, in hours, of interruption per consumer per year. The SAIFI (System Average Interruption Frequency Index) measures the average number of interruptions per consumer per year.

SAIDI and SAIFI Indicators | ||||||||||||||||||||

Distributor | SAIDI (hours) | SAIFI (interruptions) | ||||||||||||||||||

2014 | 2015 | 2016 | 2017 | 1Q18 | 2Q18 | 3Q18 | 2018 | 1Q19 | ANEEL1 | 2014 | 2015 | 2016 | 2017 | 1Q18 | 2Q18 | 3Q18 | 2018 | 1Q19 | ANEEL1 | |

CPFL Paulista | 6.92 | 7.76 | 7.62 | 7.14 | 6.90 | 6.50 | 6.25 | 6.17 | 6.46 | 7.38 | 4.87 | 4.89 | 5.00 | 4.94 | 4.76 | 4.46 | 4.13 | 4.03 | 4.16 | 6.33 |

CPFL Piratininga | 6.98 | 7.24 | 8.44² | 6.97 | 6.37 | 5.93 | 6.01 | 5.92 | 6.40 | 6.74 | 4.19 | 4.31 | 3.97² | 4.45 | 4.13 | 3.61 | 3.71 | 3.87 | 4.31 | 5.82 |

RGE | 18.28 | 17.47 | 16.82 | 14.83 | 13.74 | 13.46 | 13.15 | 14.44 | 14.95 | 11.48 | 9.01 | 8.37 | 8.44 | 7.68 | 7.09 | 6.71 | 6.28 | 6.10 | 6.27 | 8.50 |

CPFL Santa Cruz |

|

|

| 6.20 | 5.80 | 5.61 | 5.61 | 6.01 | 6.21 | 8.75 |

|

|

| 5.12 | 5.26 | 4.98 | 4.89 | 5.09 | 4.84 | 7.88 |

1) Limit of the Regulatory Agency (ANEEL);

2) In the previous disclosures, we reported a SAIDI of 6.97 and a SAIFI of 3.80 for CPFL Piratininga in 2016. This number excluded the effect of a CTEEP transmission failure during a storm. However, a decision by ANEEL determined that this effect was included in the SAIDI and SAIFI statistics, so that we corrected the values, as shown in the table.

Page 35 de 57

| 1Q19 Results | May 7, 2019 |

The annualized values of SAIDI and SAIFI for the first quarter of 2019 presented lower results than the annualized values for the same period of 2018 (-0.6% in the SAIDI and -9.3% in the SAIFI) in the consolidated of the distributors. In the annualized view by distributor, there was a reduction of 6.5% in the SAIDI and 12.6% in the SAIFI of CPFL Paulista. CPFL Santa Cruz and RGE reduced the SAIFI by 8.0% and 11.3%, respectively.

As regards RGE Sul specifically, the recovery plan for technical indicators remains Rural, Troncal and Urban pruning, treatment of major primary, secondary and damage recidivism, programming of services for testing and maintenance in substations and transmission lines, carry out termovision and ultrasound inspections in distribution networks, substations and transmission lines. In addition, part of the maintenance plan, improvements and extensions of the existing structure, with the forecast of exchanges of posts, capacity adjustment, modernization of substations, and installation of remote control and control equipment. This plan is part of a continuous improvement that is already under development. In addition to the significant investments being made, the significant reduction of these investments has already been observed.

Since 2019, the RGE and RGE Sul concessions have been unified, becoming a single distributor for the purpose of calculating technical indicators.

Losses

Find below the performance of CPFL distribution companies throughout the last quarters:

12M Accumulated Losses1 | Total Losses | |||||

1Q18 | 2Q18 | 3Q18 | 4Q18 | 1Q19 | ANEEL | |

CPFL Energia | 8.82% | 9.02% | 8.86% | 9.03% | 8.84% | 8.30% |

CPFL Paulista | 8.93% | 9.10% | 8.87% | 9.13% | 8.86% | 8.37% |

CPFL Piratininga | 7.72% | 7.87% | 7.79% | 7.94% | 7.69% | 6.92% |

RGE | 9.45% | 9.73% | 9.71% | 9.70% | 9.78% | 9.11% |

CPFL Santa Cruz | 8.65% | 8.84% | 8.09% | 8.56% | 7.82% | 7.58% |

Notes:

1) The figures above were adequate to a better comparison with the regulatory losses trajectory defined by the Regulatory Agency (ANEEL). In CPFL Piratininga, RGE and RGE Sul, high-voltage customers were disregarded.

The consolidated losses index of CPFL Energia was of 8.84% in 1Q19, compared to 9.03% in 4Q18, a reduction of 0.19 p.p. Compared to 1Q18 (8.82%), there was an increase of 0.02 p.p.

11.2) Commercialization and Services Segments

11.2.1) Commercialization Segment

Consolidated Income Statement - Commercialization (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Net Operating Revenue | 760 | 710 | 7.1% |

EBITDA(1) | 31 | 8 | 295.0% |

Net Loss | �� 15 | (0) | - |

Note:

(1) EBITDA is calculated from the sum of net income, taxes, financial result and depreciation/amortization.

Page 36 de 57

| 1Q19 Results | May 7, 2019 |

Operating Revenue

In 1Q19, net operating revenue reached R$ 760 million, representing an increase of 7.1% (R$ 50 million).

EBITDA

In 1Q19, EBITDA totaled R$ 31 million, compared to R$ 8 million in 1Q18, an increase of 295.0% (R$ 23 million).

Net Income

In 1Q19, net income was of R$ 15 million, compared to a net loss of R$ 0.4 million in 1Q18, a variation of R$ 15 million.

11.2.2) Services Segment

Consolidated Income Statement - Services (R$ Million) | |||

| 1Q19 | 1Q18 | Var. |

Net Operating Revenue | 146 | 112 | 30.4% |

EBITDA(1) | 36 | 23 | 58.5% |

Net Income | 23 | 13 | 78.1% |

Note:

(1) EBITDA is calculated from the sum of net income, taxes, financial result and depreciation/amortization.

Operating Revenue

In 1Q19, net operating revenue reached R$ 146 million, representing an increase of 30.4% (R$ 34 million).

EBITDA

In 1Q19, EBITDA totaled R$ 36 million, compared to R$ 23 million in 1Q18, an increase of 58.5% (R$ 13 million).

Net Income

In 1Q19, net income was of R$ 23 million, compared to a net income of R$ 13 million in 1Q18, an increase of 78.1% (R$ 10 million).

Page 37 de 57

| 1Q19 Results | May 7, 2019 |

11.3) Conventional Generation Segment

11.3.1) Economic-Financial Performance

Consolidated Income Statement - Conventional Generation (R$ million) | |||

| 1Q19 | 1Q18 | Var. |

Gross Operating Revenue | 301 | 308 | -2.3% |

Net Operating Revenue | 269 | 281 | -4.3% |

Cost of Electric Power | (29) | (19) | 57.4% |

Operating Costs & Expenses | (52) | (53) | -2.6% |

EBIT | 188 | 210 | -10.1% |

EBITDA | 304 | 325 | -6.5% |

Financial Income (Expense) | (44) | (68) | -35.1% |

Income Before Taxes | 230 | 227 | 1.3% |

Net Income | 184 | 182 | 1.4% |

Nota:

(1) EBITDA is calculated from the sum of net income, taxes, financial result and depreciation/amortization.

11.3.1.1) Operating Revenue

In the analysis presented in this report we consider the migration of the transmission companies CPFL Piracicaba and CPFL Morro Agudo from “Others” to “Conventional Generation” segment.

In 1Q19,Gross Operating Revenuereached R$ 301 million, a reduction of 2.3% (R$ 7 million).Net Operating Revenue was of R$ 269 million,registering a reduction of 4.3% (R$ 12 million).

The main factors that affected the net operating revenue are:

- Reduction of R$ 10 million in other operating revenues;

- Reduction of R$ 1 million in the revenue with the power supply from Jaguari Geração;

- Reduction of R$ 1 million in the revenue with the power supply from CPFL Centrais Geradoras;

Partially offset by:

- Increase of 1.7% (R$ 3 million) in the revenue with the power supply to CPFL Paulista and CPFL Piratininga;