Sands China Ltd. (Incorporated in the Cayman Islands with limited liability) Stock Code: 1928 INTERIM REPORT 2010

Exhibit 99.1 Contents 1. Overview 2 1.1 Financial Highlights 2 1.2 Interim Dividend 2 2. Management Discussion and Analysis 3 3. Corporate Governance 15 3.1 Corporate Governance Practices 15 3.2 Board and Board Committees Composition 15 3.3 Director Remuneration 17 3.4 Internal Controls 17 3.5 Audit Committee Review 17 3.6 Re-appointment of PricewaterhouseCoopers 17 3.7 Loan Agreement Disclosure 17 3.8 Disclosure of Interests 18 3.9 Share Option Scheme 20 3.10 Purchase, Sale or Redemption of the Company's Listed Shares 22 4. Condensed Consolidated Interim Financial Information 23 4.1 Report on Review of Condensed Consolidated Interim Financial Information 23 4.2 Condensed Consolidated Interim Financial Information 25 4.3 Notes to the Condensed Consolidated Interim Financial Information 31 5. Corporate Information 54 6. Contact Us 55 7. Glossary 56

| Sands China Ltd. |

|

Overview

Financial Highlights

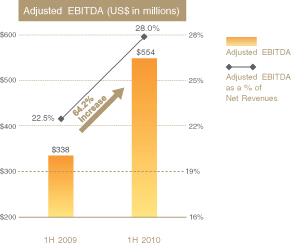

We generated an all-time half year record of US$554.4 million (HK$4,314.7 million) of adjusted EBITDA across all our Group properties, an increase of 64.2% compared to US$337.7 million (HK$2,617.2 million) in the first half of 2009.

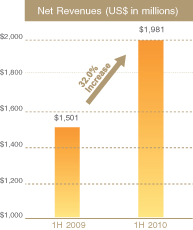

Total net revenues for the Group increased 32.0% to US$1,980.5 million (HK$15,413.6 million) in the first half of 2010, compared to US$1,500.6 million (HK$11,629.7 million) in the first half of 2009.

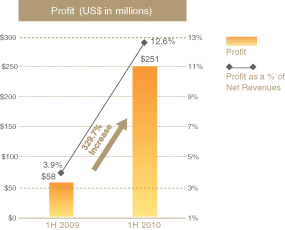

Profit for the Group increased 329.7% to US$250.5 million (HK$1,949.6 million) in the first half of 2010, compared to US$58.3 million (HK$451.8 million) in the first half of 2009.

Interim Dividend

The Board does not declare any interim dividend for the Reporting Period.

| Note: | The translation of US$ amounts into HK$ amounts has been made at the rate of US$1.00 to HK$7.7827 (six months ended June 30, 2009: US$1.00 to HK$7.750) for the purposes of illustration only. |

2

| Interim Report 2010 |

|

Management Discussion and Analysis

Results of Operations

We are pleased to present our unaudited consolidated results of the Group for the six months ended June 30, 2010 compared to the six months ended June 30, 2009.

Net Revenues

Net revenues were US$1,980.5 million for the six months ended June 30, 2010, an increase of US$479.9 million, or 32.0%, compared to US$1,500.6 million for the six months ended June 30, 2009. Net revenues increased

primarily due to an increase in net casino revenues, driven by strong visitation resulting in part from marketing initiatives such as the launch of the Sands Rewards Club, a stable macroeconomic environment in China, as well as management’s focus on driving the high-margin mass market gaming segment, while continuing to provide luxury amenities and high service levels to our VIP premium and junket players.

Our net revenues consisted of the following:

| Six months ended June 30, | |||||||

| 2010 | 2009 | Percent Change | |||||

| (US$ in millions, except percentages) | |||||||

Casino | 1,768.5 | 1,317.1 | 34.3% | ||||

Rooms | 67.5 | 55.5 | 21.6% | ||||

Food and beverage | 34.9 | 25.4 | 37.4% | ||||

Mall | 54.5 | 64.1 | (15.0)% | ||||

Convention, ferry, retail and other | 55.1 | 38.4 | 43.5% | ||||

Total net revenues | 1,980.5 | 1,500.6 | 32.0% | ||||

Our net casino revenues for the six months ended June 30, 2010 were US$1,768.5 million, an increase of US$451.4 million, or 34.3%, compared to US$1,317.1 million for the six months ended June 30, 2009. Net casino

revenues of the Sands Macao, The Venetian Macao and The Plaza Macao increased by US$123.2 million, US$181.1 million and US$147.1 million respectively, due to the factors mentioned above.

3

| Sands China Ltd. |

|

Management Discussion and Analysis

The following table summarizes the results of our casino activity:

| Six months ended June 30, | |||||||

| 2010 | 2009 | Change | |||||

| (US$ in millions, except percentages and points) | |||||||

Sands Macao | |||||||

Total net casino revenues | 572.1 | 448.9 | 27.4% | ||||

Non-rolling chip table games drop | 1,193.1 | 1,208.4 | (1.3)% | ||||

Non-rolling chip table games win percentage | 20.5% | 19.1% | 1.4 pts | ||||

Rolling chip volume | 13,627.8 | 9,845.3 | 38.4% | ||||

Rolling chip win percentage | 3.1% | 2.7% | 0.4 pts | ||||

Slot handle | 769.1 | 577.2 | 33.2% | ||||

Slot hold percentage | 5.8% | 6.7% | (0.9) pts | ||||

The Venetian Macao | |||||||

Total net casino revenues | 974.4 | 793.3 | 22.8% | ||||

Non-rolling chip table games drop | 1,819.6 | 1,623.3 | 12.1% | ||||

Non-rolling chip table games win percentage | 25.0% | 23.2% | 1.8 pts | ||||

Rolling chip volume | 19,815.3 | 18,590.1 | 6.6% | ||||

Rolling chip win percentage | 3.1% | 2.7% | 0.4 pts | ||||

Slot handle | 1,372.3 | 1,093.8 | 25.5% | ||||

Slot hold percentage | 7.2% | 7.5% | (0.3) pts | ||||

The Plaza Macao | |||||||

Total net casino revenues | 222.1 | 75.0 | 196.1% | ||||

Non-rolling chip table games drop | 194.6 | 167.5 | 16.2% | ||||

Non-rolling chip table games win percentage | 26.8% | 25.2% | 1.6 pts | ||||

Rolling chip volume | 8,562.9 | 1,125.2 | 661.0% | ||||

Rolling chip win percentage | 2.8% | 3.2% | (0.4) pts | ||||

Slot handle | 256.3 | 100.0 | 156.3% | ||||

Slot hold percentage | 5.6% | 5.7% | (0.1) pts | ||||

4

| Interim Report 2010 |

|

Management Discussion and Analysis

Net room revenues for the six months ended June 30, 2010 were US$67.5 million, an increase of US$12.0 million, or 21.6%, compared to US$55.5 million for the six months ended June 30, 2009. The increase was primarily driven by continued economic recovery from the global economic downturn

in 2009 as well as a continued focus on promotions such as the Winter, Spring & Summer Packages and incentive schemes given to selected wholesalers.

The following table summarizes our room activity. The suites at the Sands Macao are primarily provided to gaming patrons on a complimentary basis and therefore related statistics have not been included.

| Six months ended June 30, | |||||||

| 2010 | 2009 | Change | |||||

| (US$, except percentages and points) | |||||||

The Venetian Macao | |||||||

Gross room revenues (in millions) | 95.3 | 79.5 | 19.9% | ||||

Average daily rate | 203 | 209 | (2.9)% | ||||

Occupancy rate | 92.4% | 76.7% | 15.7 pts | ||||

Revenue per available room | 187 | 160 | 16.9% | ||||

The Plaza Macao | |||||||

Gross room revenues (in millions) | 13.5 | 7.9 | 70.9% | ||||

Average daily rate | 288 | 293 | (1.7)% | ||||

Occupancy rate | 71.0% | 41.5% | 29.5 pts | ||||

Revenue per available room | 204 | 122 | 67.2% | ||||

Note: Information in this table takes into account rooms provided to customers on a complimentary basis that are recorded at discounted rates.

Net food and beverage revenues for the six months ended June 30, 2010 were US$34.9 million, an increase of US$9.5 million, or 37.4%, compared to US$25.4 million for the six months ended June 30, 2009. The increase was primarily due to the growth in banquet operations as a result of more group business and wedding banquets. In addition, other food and beverage outlets also experienced better performance as a result of improved hotel occupancy.

Mall revenues for the six months ended June 30, 2010 were US$54.5 million, a decrease of US$9.6 million, or 15.0%, compared to US$64.1

million for the six months ended June 30, 2009. The decrease was primarily due to lower occupancy and rent restructuring for certain retailers.

Net convention, ferry, retail and other revenue for the six months ended June 30, 2010 were US$55.1 million, an increase of US$16.7 million, or 43.5%, compared to US$38.4 million for the six months ended June 30, 2009. The increase was primarily attributable to an increase in ferry revenue resulting from an increase in the number of sailings and higher occupancy and an increase in entertainment revenue due to an increase in arena events.

5

| Sands China Ltd. |

|

Management Discussion and Analysis

Operating Expenses

Operating expenses were US$1,659.6 million for the six months ended June 30, 2010, an increase of US$271.3 million, or 19.5%, compared to US$1,388.3 million for the six months ended June 30, 2009. The increase in operating expenses was primarily attributable to the increase in total

gaming tax and premiums as a result of increased gaming revenue, the expansion of our ferry service operations, as well as increases in general and administrative expense, corporate expense and loss on disposal of property and equipment, partially offset by a decrease in pre-opening expenses.

Our operating expenses consisted of the following:

| Six months ended June 30, | |||||||

| 2010 | 2009 | Percent Change | |||||

| (US$ in millions, except percentages) | |||||||

Casino | 1,161.2 | 916.2 | 26.7% | ||||

Rooms | 12.4 | 14.0 | (11.4)% | ||||

Food and beverage | 24.7 | 22.7 | 8.8% | ||||

Mall | 13.7 | 16.8 | (18.5)% | ||||

Convention, ferry, retail and other | 71.1 | 59.7 | 19.1% | ||||

Provision for doubtful accounts | 19.4 | 18.7 | 3.7% | ||||

General and administrative expense | 128.6 | 115.9 | 11.0% | ||||

Corporate expense | 13.6 | 4.7 | 189.4% | ||||

Pre-opening expense | 12.2 | 52.4 | (76.7)% | ||||

Depreciation and amortization | 163.3 | 162.4 | 0.6% | ||||

Loss on disposal of property and equipment | 29.4 | 4.9 | 500.0% | ||||

Fair value losses on financial assets at fair value through | 1.4 | — | — | ||||

Net foreign exchange losses | 8.4 | 0.1 | 8,300.0% | ||||

Total operating expenses | 1,659.6 | 1,388.3 | 19.5% | ||||

Casino expenses for the six months ended June 30, 2010 were US$1,161.2 million, an increase of US$245.0 million, or 26.7%, compared to US$916.2 million for the six months ended June 30, 2009. The increase was primarily due to the increase in total gaming tax and gaming premiums of US$239.1 million as a result of higher casino revenues.

Room expenses for the six months ended June 30, 2010 were US$12.4 million, a decrease of US$1.6 million, or 11.4%, compared to US$14.0 million for the six months ended June 30, 2009. Payroll expenses and hotel supplies decreased by US$4.9 million driven by our cost savings initiatives.

These decreases were partially offset by increases in the management fee to Four Seasons Hotel Management due to higher revenue, outside services for laundry, and travel agent commission of US$2.9 million due to the increase in occupancy.

Food and beverage expenses for the six months ended June 30, 2010 were US$24.7 million, an increase of US$2.0 million, or 8.8%, compared to US$22.7 million for the six months ended June 30, 2009. The increase was driven by the increase in cost of sales of US$2.3 million associated with the increase in food and beverage revenues.

6

| Interim Report 2010 |

|

Management Discussion and Analysis

Mall expenses for the six months ended June 30, 2010 were US$13.7 million, a decrease of US$3.1 million, or 18.5%, compared to US$16.8 million for the six months ended June 30, 2009. The decrease was primarily attributable to the decrease of common area maintenance costs, payroll expenses, utilities, contract labor and special events of US$2.8 million.

Convention, ferry, retail and other expenses for the six months ended June 30, 2010 were US$71.1 million, an increase of US$11.4 million, or 19.1%, compared to US$59.7 million for the six months ended June 30, 2009. The increase was primarily attributable to an increase in ferry expenses of US$9.8 million and an increase of US$3.2 million related to the contract entertainment mainly for Cotai Arena events at The Venetian Macao. These increases were partially offset by a reduction in payroll expenses of US$1.0 million, primarily resulting from management’s continued focus on driving operational efficiencies at the various properties.

Provision for doubtful accounts was US$19.4 million for the six months ended June 30, 2010, an increase of US$0.7 million or 3.7%, compared to US$18.7 million for the six months ended June 30, 2009.

General and administrative expenses were US$128.6 million for the six months ended June 30, 2010, an increase of US$12.7 million, or 11.0%, compared to US$115.9 million for the six months ended June 30, 2009. The increase was primarily attributable to bonus expenses, marketing expenses and utilities expenses of US$22.7 million. The increase was partially offset by a decrease of US$9.8 million driven by reductions in payroll expenses and transportation costs as a result of management’s continued focus on driving operational efficiencies throughout the various properties.

Corporate expenses were US$13.6 million for the six months ended June 30, 2010, an increase of US$8.9 million, or 189.4%, compared to US$4.7 million for the six months ended June 30, 2009. The increase was the result of royalty fees of US$10.0 million payable to Las Vegas Sands, LLC under the terms of the Second Trademark Sublicense Agreement entered into on November 8, 2009.

Pre-opening expenses were US$12.2 million for the six months ended June 30, 2010, a decrease of US$40.2 million, or 76.7%, compared to US$52.4 million for the six months ended June 30, 2009. Pre-opening expenses for the six months ended June 30, 2010 were primarily related to costs associated with the suspension of construction at Parcels 5 and 6, as well as costs related to the Four Seasons Service Apartment. Pre-opening expenses for the six months ended June 30, 2009 were primarily related to costs associated with the suspension of construction at Parcels 5 and 6.

Depreciation and amortization expense was US$163.3 million for the six months ended June 30, 2010, an increase of US$0.9 million, or 0.6%, compared to US$162.4 million for the six months ended June 30, 2009.

Loss on disposal of property and equipment was US$29.4 million for the six months ended June 30, 2010, an increase of US$24.5 million or 500.0% compared to US$4.9 million for the six months ended June 30, 2009. The increase was primarily related to the disposition of construction materials from construction sites at Parcels 5 and 6.

Net foreign exchange losses for the six months ended June 30, 2010 were US$8.4 million, primarily associated with U.S. dollar denominated debt held in Macao. This compares with net foreign exchange losses of US$0.1 million for the six months ended June 30, 2009.

7

| Sands China Ltd. |

|

Management Discussion and Analysis

Adjusted EBITDA(1)

Adjusted EBITDA for the six months ended June 30, 2010 was US$554.4 million, an increase of US$216.7 million, or 64.2%, compared to US$337.7 million for the six months ended June 30, 2009. This strong performance was driven by a significant increase in net casino revenues as a result of management’s focus on both driving the high-margin mass market gaming

segment as well as continuing to provide high service levels to our VIP premium and junket players. In addition, the management team continued to focus on driving operational efficiencies throughout both gaming and non-gaming areas of the business, driving further improvement in adjusted EBITDA.

The following table summarizes information related to our operations:

| Six months ended June 30, | ||||||||

| 2010 | 2009 | Percent Change | ||||||

| (US$ in millions, except percentages) | ||||||||

Adjusted EBITDA: | ||||||||

The Venetian Macao | 362.6 | 229.2 | 58.2% | |||||

Sands Macao | 150.4 | 111.3 | 35.1% | |||||

The Plaza Macao | 52.4 | 9.3 | 463.4% | |||||

Ferry and other operations | (11.0 | ) | (12.2 | ) | (9.8)% | |||

| 554.4 | 337.7 | 64.2% | ||||||

Note: The comparative figures have been reclassified to conform to the presentation of the current period.

Interest Expense

The following table summarizes information related to interest expense:

| Six months ended June 30, | ||||||||

| 2010 | 2009 | Percent change | ||||||

| (US$ in millions, except percentages) | ||||||||

Interest and other finance cost | 82.9 | 58.7 | 41.2% | |||||

Less — capitalized interest | (11.4 | ) | (4.6 | ) | 147.8% | |||

Interest expense, net | 71.5 | 54.0 | 32.4% | |||||

| (1) | Adjusted EBITDA is profit before interest, income taxes, depreciation and amortization (net of amortization of show production costs), pre-opening expense, net foreign exchange losses or gains, loss or gain on disposal of property and equipment, corporate expense, share-based compensation and fair value losses or gains on financial assets at fair value through profit or loss. With respect to adjusted EBITDA for each of our properties, we make allocations of the shared support expenses based on revenue attributable to each property. Adjusted EBITDA is used by management as the primary measure of operating performance of our Group’s properties and to compare the operating performance of our Group’s properties with |

that of its competitors. However, adjusted EBITDA should not be considered in isolation; construed as an alternative to profit or operating profit; as an indicator of our IFRS operating performance, other combined operations or cash flow data; or as an alternative to cash flow as a measure of liquidity. Adjusted EBITDA presented in the report may not be comparable to other similarly titled measures of other companies. In addition, our adjusted EBITDA presented in the report may differ from adjusted EBITDA presented by Las Vegas Sands Corp. (“LVS”) for its Macao segment in its filings with the U.S. Securities and Exchange Commission. |

8

| Interim Report 2010 |

|

Management Discussion and Analysis

Interest and other finance cost for the six months ended June 30, 2010 was US$82.9 million, an increase of US$24.2 million, or 41.2%, compared to US$58.7 million for the six months ended June 30, 2009. The increase was primarily a result of an increase in the weighted average interest rate driven by an increase in the credit spread on the Macao Credit Facility. The US$6.8 million increase in capitalized interest was primarily due to the recommencement of construction activities at Parcels 5 and 6 in May 2010.

Profit for the Period

Profit for the six months ended June 30, 2010 was US$250.5 million, an increase of US$192.2 million, or 329.7%, compared to US$58.3 million for the six months ended June 30, 2009.

Liquidity and Capital Resources

Historically, we have funded our operations through cash generated from our operations and our debt financings, as well as financial support from

LVS and its subsidiaries (excluding our Group) prior to the Global Offering.

On May 17, 2010, Venetian Orient Limited (“VOL”) entered into a credit agreement (the “VOL Credit Facility”) providing for up to US$1.75 billion (or equivalent in HK$ or MOP), which consists of a US$750.0 million term loan (the “VOL Term Facility”) that was fully drawn on July 16, 2010, a US$750.0 million delayed draw term loan available for 18 months after closing (the “VOL Delayed Draw Facility”) and a US$250.0 million revolving facility available until April 17, 2015 (the “VOL Revolving Facility”). As at June 30, 2010, the Company had not drawn any amounts under the VOL Revolving Facility.

As at June 30, 2010, we had cash and cash equivalents of US$673.8 million, restricted cash of US$25.0 million and short term deposits of US$173.5 million.

Cash Flows — Summary

Our cash flows consisted of the following:

| Six months ended June 30, | ||||||

| 2010 | 2009 | |||||

| (US$ in millions) | ||||||

Net cash generated from operating activities | 584.9 | 298.8 | ||||

Net cash used in investing activities | (288.3 | ) | (244.5 | ) | ||

Net cash used in financing activities | (528.6 | ) | (131.2 | ) | ||

Net decrease in cash and cash equivalents | (232.0 | ) | (76.8 | ) | ||

Cash and cash equivalents at beginning of the period | 908.3 | 417.8 | ||||

Effect of exchange rate on cash and cash equivalents | (2.6 | ) | (0.3 | ) | ||

Cash and cash equivalents at end of the period | 673.8 | 340.6 | ||||

9

| Sands China Ltd. |

|

Management Discussion and Analysis

Cash Flows — Operating Activities

We derive most of our operating cash flows from our casino, hotel room and retail mall operations.

Net cash generated from operating activities for the six months ended June 30, 2010 was US$584.9 million, an increase of US$286.1 million, or 95.7%, as compared to US$298.8 million for the six months ended June 30, 2009. The increase in net cash generated from operating activities was primarily due to an increase in profit before tax and improved working capital.

Cash Flows — Investing Activities

Net cash used in investing activities for the six months ended June 30, 2010 was US$288.3 million, which primarily consisted of capital expenditures and purchases of US$173.9 million of short term deposits. Capital expenditures amounted to US$112.4 million, including US$68.1

million for Parcels 5 and 6 of our Cotai Strip development and US$37.3 million for our operations mainly at The Venetian Macao and The Plaza Macao.

Cash Flows — Financing Activities

For the six months ended June 30, 2010, net cash flows used in financing activities were US$528.6 million, primarily attributable to US$392.6 million in repayment of borrowings under our credit facilities, interest paid of US$63.0 million, and financing costs paid of US$56.1 million.

Capital Expenditures

Capital expenditures were used primarily for new projects and to renovate, upgrade and maintain existing properties. Set forth below is historical information on our capital expenditures, excluding capitalized interest and construction payables:

| Six months ended June 30, | ||||||

| 2010 | 2009 | |||||

| (US$ in millions) | ||||||

The Venetian Macao | 18.0 | 7.8 | ||||

Sands Macao | 1.9 | 4.7 | ||||

The Plaza Macao | 15.0 | 128.1 | ||||

Ferry and other operations | 2.4 | 15.9 | ||||

Parcels 5 and 6 | 68.1 | 53.6 | ||||

Other developments | 7.0 | 0.1 | ||||

Total capital expenditures | 112.4 | 210.2 | ||||

Our capital expenditure plans are significant. We recommenced construction activities on Parcels 5 and 6 in May 2010 to complete Phases I and II. We intend to fully fund the development and construction costs

related to Phases I and II with at least US$500.0 million of the proceeds from the Global Offering, up to US$1.75 billion from the VOL Credit Facility and, to the extent necessary, cash flow from existing and future operations.

10

| Interim Report 2010 |

|

Management Discussion and Analysis

We expect to commence construction of Phase III at a future date as demand and market conditions warrant. As at June 30, 2010, we had capitalized construction costs of US$2.03 billion on the development of Parcels 5 and 6 including land, and we expect to spend an additional US$2.1 billion to complete Phases I and II.

These investment plans are preliminary and subject to change based upon the execution of our business plan, the progress of our capital projects, market conditions and the outlook on future business conditions.

Capital Commitments

Future commitments for property and equipment that are not recorded in the financial statements herein are as follows:

| As at June 30, 2010 | | As at December 31, 2009 | | |||

| (US$ in millions) | ||||||

Contracted but not provided for | 479.9 | 162.1 | ||||

Authorized but not contracted for | 1,364.2 | 1,708.2 | ||||

| 1,844.1 | 1,870.3 | |||||

Interim Dividend

The Board does not recommend the payment of an interim dividend for the six months ended June 30, 2010.

Pledge of Fixed Assets

We have pledged a substantial portion of our fixed assets to secure our loan facilities. We have pledged buildings; building, land and leasehold improvements; furniture, fittings and equipment; construction in progress; ferries and vehicles with an aggregate net book value of approximately US$5.35 billion as at June 30, 2010 (December 31, 2009: US$3.68 billion).

Contingent Liabilities and Risk Factors

The Group has contingent liabilities arising in the ordinary course of business. Management has made certain estimates for potential litigation costs based upon consultation with legal counsel and believes that no significant loss will be incurred beyond the amounts provided for as at June 30, 2010. Actual results could differ from these estimates; however, in the opinion of management, it is not anticipated that any material liabilities will arise from the contingent liabilities.

11

| Sands China Ltd. |

|

Management Discussion and Analysis

The land concession for Parcels 5 and 6 was published in Macao’s Official Gazette on May 12, 2010. We will subsequently negotiate the land concession for Parcels 7 and 8. Based on historical experience with the Macao Government with respect to the Group’s land concessions for the Sands Macao and Parcels 1, 2, 3, 5 and 6, management believes that the land concession for Parcels 7 and 8 will be granted. However, if the Group does not obtain the land concession, the Group could forfeit all or a substantial part of its US$102.3 million in construction costs incurred for the development of Parcels 7 and 8 as at June 30, 2010.

The Group had commenced pre-construction on Parcel 3, and had capitalized costs of approximately US$35.5 million as at June 30, 2010. Under the revised terms of the land concession approved by the Macao Government on August 20, 2009 that covers Parcel 3, the Group is required to complete the development of Parcel 3 by April 17, 2013. The land concession for Parcels 5 and 6 contains a similar requirement that the corresponding development be completed by May 2014. Management believes that if the Group is unable to complete the developments by the respective deadlines, it will likely be able to obtain an extension from the Macao Government. However, no assurances can be given that an extension will be granted. If the Group is not able to meet the deadlines and those deadlines are not extended, the Macao Government has the

right to unilaterally terminate the land concessions and the Group could lose its investment in, and right to operate, any properties developed under the land concessions for Parcels 3 and 5 and 6 without compensation to the Group.

Capital Risk Management

The Group’s primary objective when managing capital is to safeguard the Group’s ability to continue as a going concern in order to provide returns for Shareholders and benefits for other stakeholders, by pricing products and services commensurately with the level of risk.

The capital structure of the Group consists of debt, which includes interest bearing borrowings (including current and non-current bank loans as shown in Note 9 to the consolidated interim financial information), cash and cash equivalents, investments (short-term cash deposits with maturities over 90 days) and equity attributable to Shareholders, comprising issued share capital and reserves. The Group actively and regularly reviews and manages its capital structure to maintain the net debt-to-capital ratio (gearing ratio) at an appropriate level based on its assessment of the current risk and circumstances. This ratio is calculated as net debt divided by total capital. Net debt is calculated as interest bearing borrowings less cash and cash equivalents and investments. Total capital is calculated as equity as shown in the consolidated balance sheet plus net debt:

| As at June 30, 2010 | | As at December 31, 2009 | | |||

| (US$ in millions, except percentages) | ||||||

Interest bearing borrowings | 2,379.4 | 2,818.8 | ||||

Less: cash and cash equivalents | (673.8 | ) | (908.3 | ) | ||

Less: investments (short-term cash deposits with maturities over 90 days) | (173.5 | ) | — | |||

Net debt | 1,532.2 | 1,910.5 | ||||

Total equity | 3,943.9 | 3,698.9 | ||||

Total capital | 5,476.1 | 5,609.4 | ||||

Gearing ratio | 28.0% | 34.1% | ||||

12

| Interim Report 2010 |

|

Management Discussion and Analysis

Foreign exchange risk

The Group’s foreign currency transactions are mainly denominated in US$. The majority of assets and liabilities are denominated in US$, HK$ and MOP, and there are no significant assets and liabilities denominated in other currencies. The Group is subject to foreign exchange rate risk arising from future commercial transactions and recognized assets and liabilities that are denominated in a currency other than MOP, which is the functional currency of major operating companies within the Group. The Group currently does not have a foreign currency hedging policy.

Business Review and Prospects

Our business strategy is to continue to successfully execute our Cotai Strip developments and to leverage our integrated resort business model to create Asia’s premier gaming, leisure and convention destination. The Company continues to execute on the strategies outlined in our 2009 Annual Report. These strategies have proven to be successful in the first half of 2010 and we are confident they will continue to be so throughout the rest of the year.

We are making solid progress on the development of our integrated resort on Parcels 5 and 6 on Cotai. We recommenced construction of the project in May 2010 and entered into the VOL Credit Facility on May 17, 2010. Upon completion of Phases I and II, the integrated resort is expected to feature approximately 6,000 luxury and mid- scale hotel rooms, approximately 300,000 square feet of gaming space, approximately 1.2 million square feet of retail, entertainment and dining facilities, exhibition and conference facilities and a multipurpose theater.

Due to matters beyond the Company’s control, we have faced challenges acquiring the construction labor that we need quickly enough to be able to meet our original development and opening deadlines. We estimate that it will take approximately sixteen months to complete Phase I once we have sufficient labor to ramp up our construction activity to requisite levels. We currently expect to open Phase I of the project in the fourth quarter of 2011. Phase II, is expected to open six months thereafter.

On August 26, 2010, the Board approved an increase in the budget for the development of the integrated resort on Parcels 5 and 6 of approximately US$100.0 million. The additional funds will be used for, amongst other things, improving and updating the design and fit-out of the casino and hotel rooms and enhancing the layout of the convention, exhibition and meeting room spaces, along with some additional costs associated with the suspension of the project between November 2008 and May 2010. The Directors believe that the Company has sufficient funds available to be able to fund this budget increase.

The Directors removed Mr. Steven Craig Jacobs from the Board on July 23, 2010 and also terminated his employment as the Company’s Chief Executive Officer, President and Executive Director. Mr. Michael Alan Leven, President and Chief Operating Officer of our controlling shareholder, LVS, was appointed our Acting Chief Executive Officer on July 23, 2010. He will serve in this position until such time as a permanent Chief Executive Officer is found. Mr. Leven served as a Special Advisor to the Board from October 14, 2009 until his appointment as an Executive Director on July 27, 2010. Mr. Leven brings with him extensive experience in the gaming and hospitality industries.

13

| Sands China Ltd. |

|

Management Discussion and Analysis

On July 27, 2010 the Board approved the appointment of Mr. Edward M. Tracy and Mr. David R. Sisk. Mr. Tracy will serve as the Company’s President and Chief Operating Officer. Mr. Sisk will serve as the Company’s Executive Vice President, Chief Casino Officer. Both executives bring many years of development and operations experience to the Company.

Human Resources

As at June 30, 2010, our team member profile was as follows:

Number of full-time team members: | 14,766 | |

Average age: | 37 | |

Average years of service: | 3.52 | |

Gender Ratio: | Male 45.08% | |

| Female 54.92% | ||

Number of nationalities in | 32 | |

Total number of nationalities: | 48 |

Save as disclosed in this 2010 Interim Report, there have been no material changes to the information disclosed in the 2009 Annual Report in respect of the remuneration of employees, remuneration policies, bonus and share option schemes and staff development.

Environment

We recognize the impact our business has on the environment and we continue to strive to achieve the goals we have set ourselves in the areas of resource conservation and reducing our environmental foot print. We encourage and are grateful to those Shareholders who have elected to receive our annual and interim reports via electronic means, thereby reducing the need to print hard copies of our reports. Should you wish to start receiving an electronic copy of our annual and interim reports, please refer to page 55 of this report for more information.

To minimize the impact on our environment, this 2010 Interim Report is printed on recycled paper using soy based inks.

Awards

We are particularly pleased to report that the Company has continued to receive various prestigious awards during 2010 including:

| LACP 2009 Annual Report Vision Awards, Overall, GOLD | |

LACP 2009 Annual Report Vision Awards, Best Report Financials, BRONZE | ||

| International ARC Awards Competition, 2009 Annual Report, Cover Photo/Design (Hotel & Casino), GOLD Award | |

International ARC Awards Competition, 2009 Annual Report, Financial Data (Hotel & Casino), SILVER Award | ||

2010 Business Traveler Asia-Pacific Readers’ Poll, Best Business Hotel in Macao | ||

FinanceAsia Business Travel Poll Awards 2009, Best Hotel in Macao | ||

TTG China Travel Awards 2009, Best Meeting and Conventions Hotel in Macao | ||

The 5th China Hotel Starlight Award, TOP 10 MICE Hotels of China | ||

International Gaming Awards, Casino Interior Design | ||

Forbes Travel Guide 2010, Four-Star Lodging award, Sands Macao |

14

| Interim Report 2010 |

|

Corporate Governance

Corporate Governance Practices

The Company is committed to the maintenance of good corporate governance practices and procedures. In the Corporate Governance Report of April 14, 2010, which was published in our 2009 Annual Report, we reported that the Company has devised its own corporate governance guidelines, which incorporate most of the policies, principles and practices set out in the Code on Corporate Governance Practices (the “CG Code”) contained in Appendix 14 of the Rules Governing the Listing of Securities (the “Listing Rules”) on The Stock Exchange of Hong Kong Limited (the “Stock Exchange”). Except as disclosed below, the Company has fully complied with all the code provisions and certain recommended best practices set out in the CG Code throughout the six months ended June 30, 2010.

In the Corporate Governance Report of April 14, 2010 we had also reported on six deviations from the provisions of the CG Code. Set out below is an update on these deviations:

Code Provision

| A.1.1 | The Board is pleased to report that it meets regularly at least once every quarter. The Board has already exceeded the suggested minimum number of meetings in 2010. |

| A.1.7 | The Board is pleased to report that it has established a procedure to enable directors, upon reasonable request, to seek independent professional advice, in appropriate circumstances, at the Company’s expense. |

| C.2.1 | The Directors are pleased to report that they meet regularly and conduct a review of the effectiveness of the system of internal control of the Company and its subsidiaries. The review covers all material controls, including financial, operational and compliance controls and risk management functions. |

| C.2.2 | The Directors are pleased to report that they consider the Company’s accounting and financial reporting teams to be adequately resourced and qualified. |

| D.1.2 | The Board is currently reviewing and discussing those functions reserved to the Board and those delegated to management. We look forward to providing an update on this matter in our 2010 Annual Report. |

| D.2.2 | The Board will shortly be amending the terms of reference of the LVSC Announcements Committee to require the committee to report back to the Board on their decisions or recommendations. We look forward to providing an update on this matter in our 2010 Annual Report. |

As reported on page 82 of our 2009 Annual Report, the Company has devised its own securities trading code for securities transactions (the “Company Code”) by the Directors and relevant employees who are likely to be in possession of unpublished price-sensitive information of the Company on terms no less exacting than the Model Code for Securities Transactions by Directors of Listed Issuers as set out in Appendix 10 of the Listing Rules (the “Model Code”). Following specific enquiry by the Company, all Directors save for Mr. Steven Craig Jacobs who was removed as Executive Director on July 23, 2010 and cannot be reached to obtain his confirmation up to the date of this report, have confirmed that they have complied with the required standard set out in the Company Code during the six months ended June 30, 2010.

Board and Board Committees Composition

During the first half of 2010, there were two changes to the composition of the Board:

| • | Mr. Stephen John Weaver, an Executive Director and the Company’s Chief Development Officer, retired at the Annual General Meeting of the Company on June 19, 2010 and did not offer himself for re-election. |

| • | Mr. Toh Hup Hock, the Company’s Executive Vice President and Chief Financial Officer, was appointed an Executive Director with effect from June 30, 2010. As an Executive Director, Mr. Toh does not receive any emoluments for his position on the Board and his appointment is not governed by a service contract. Mr. Toh will serve as an Executive Director of the Company without any specific term, however he is subject to retirement by rotation and re-election in accordance with the articles of association of the Company. |

15

| Sands China Ltd. |

|

Corporate Governance

As at June 30, 2010, the composition of the Board was as follows:

Non-executive Directors |

Sheldon Gary Adelson |

Jeffrey Howard Schwartz |

Irwin Abe Siegel |

Independent Non-executive Directors |

Iain Ferguson Bruce |

Chiang Yun |

David Muir Turnbull |

Executive Directors |

Steven Craig Jacobs |

Toh Hup Hock |

The composition of the Board Committees as at June 30, 2010 was as follows:

Audit Committee |

Iain Ferguson Bruce (Chairman) |

Irwin Abe Siegel |

Chiang Yun |

Remuneration Committee |

David Muir Turnbull (Chairman) |

Iain Ferguson Bruce |

Jeffrey Howard Schwartz |

LVSC Announcements Committee |

Steven Craig Jacobs (Chairman) |

Iain Ferguson Bruce |

David Muir Turnbull |

Since June 30, 2010, there have been additional changes to the Board. In order to provide our Shareholders with the most up to date information on the Company, the most recent changes to the Board of the Company are detailed below:

| • | On July 23, 2010, Mr. Steven Craig Jacobs, the Company’s Chief Executive Officer, President and Executive Director, was removed from office by the Board. |

| • | On July 27, 2010, Mr. Michael Alan Leven, the Company’s Special Advisor to the Board and our Acting Chief Executive Officer, was appointed an Executive Director. His position as a Special Adviser to the Board was simultaneously dissolved on that date. As an Executive Director, Mr. Leven does not receive any emoluments for his position on the Board and his appointment is not governed by a service contract. Mr. Leven will serve for an initial period of 3 years and is subject to retirement by rotation and re-election in accordance with the articles of association of the Company. |

As at the date of this 2010 Interim Report, the composition of the Board was as follows:

Non-executive Directors |

Sheldon Gary Adelson |

Jeffrey Howard Schwartz |

Irwin Abe Siegel |

Independent Non-executive Directors |

Iain Ferguson Bruce |

Chiang Yun |

David Muir Turnbull |

Executive Directors |

Michael Alan Leven |

Toh Hup Hock |

In addition, two new committees of the Board were formed on July 27, 2010 — the CEO Search Committee and the Transitional Advisory Committee. We look forward to providing additional information and reporting on the work of these two committees in our 2010 Annual Report.

On August 26, 2010 Ms. Anne Maree Salt replaced Mr. Luis Nuno Mesquita de Melo as Joint Company Secretary.

16

| Interim Report 2010 |

|

Corporate Governance

Director Remuneration

On April 14, 2010, on the recommendation of the Remuneration Committee, the Board resolved to increase the fees paid to Non-executive Directors for their participation on the Board on the basis that, in their view,

the considerable responsibilities of the Non-executive Directors were not adequately compensated under the remuneration terms then in existence. The revised fees paid to Non-executive Directors as of April 14, 2010 are set out below:

Position | Annual Fee | |||

Independent Non-executive Director or Non-executive Director | US$ | 75,000.00 | ||

Chairman of Audit Committee, being also an Independent Non-executive Director | US$ | 25,000.00 | ||

Chairman of Remuneration Committee, whether an Independent Non-executive Director or | US$ | 25,000.00 | ||

Internal Controls

During the six months ended June 30, 2010, the Audit Committee met twice to consider the effectiveness and adequacy of the Company’s internal control system. On both occasions, the Audit Committee received a report from the Company’s Internal Audit Department and no significant areas of concern that might affect Shareholders were noted. Details of the standards, processes and effectiveness of the Company’s internal control system can be found on pages 84 to 85 of the 2009 Annual Report.

Audit Committee Review

The Audit Committee has reviewed the accounting policies adopted by the Group and the unaudited condensed consolidated interim financial information for the six months ended June 30, 2010. All of the Audit Committee members are Non-executive Directors, with the Chairman and one other member possessing the appropriate professional qualifications or accounting or related financial management experience. None of the members of the Audit Committee is a former partner of the Company’s existing external auditor.

Re-appointment of PricewaterhouseCoopers

At the Company’s Annual General Meeting held on June 19, 2010, Shareholders approved the re-appointment of PricewaterhouseCoopers as the Company’s external auditors for the financial year ending December 31, 2010.

Loan Agreement Disclosure

On May 17, 2010, VOL, a wholly-owned subsidiary of the Company, as borrower, entered into a credit agreement pursuant to which a syndicate of banks and financial institutions agreed to grant certain term loan facilities and revolving loan facilities amounting to US$1.75 billion (the “Credit Facility”). The facilities will be used to pay for project costs and as working capital and for general corporate purposes associated with the construction of the Company’s integrated resort being developed by VOL opposite The Venetian Macao and The Plaza Macao on Parcels 5 and 6. The maturity date of all the loans will be the earlier of June 16, 2015 and the fifth anniversary of the initial borrowing date.

The Credit Agreement imposes a specific performance obligation on our controlling Shareholder, LVS. Under the Credit Agreement, it would constitute an event of default if there is any sale, pledge or other transfer of

17

| Sands China Ltd. |

|

Corporate Governance

securities whereby LVS and/or its affiliates cease to own, directly or indirectly, in the aggregate at least 35% of the voting securities of the Company (a “Change of Control”).

Upon the occurrence of an event of default, including a Change of Control, that is continuing, the Administrative Agent may, or at the request of the lenders holding more than 50% of the sum of the aggregate principal amount of all loans outstanding under the Credit Agreement and any available undrawn commitments of all lenders thereunder, by written notice to VOL declare that all or any portion of (a) the aggregate principal amount of all outstanding loans and accrued but unpaid interest on the loans; (b) an amount equal to the maximum amount that may at any time be drawn under any letters of credit then outstanding; and (c) all other

obligations, in each case, outstanding under the Credit Agreement be immediately due and payable. In addition, upon the occurrence and continuation of an event of default, the obligation of each lender to make any loan or issue any letters of credit shall terminate.

Disclosure of Interests

Interests of Directors and Chief Executives

The interests/short positions of each of the Directors and Chief Executives in the shares, underlying shares and debentures of the Company and any of the Company’s associated corporations (within the meaning of Part XV of the SFO) as at June 30, 2010, as recorded in the register required to be kept under Section 352 of Part XV of the SFO, are set out in the table and explanatory notes below:

Name of Director | Company | Nature of Interest | Number of ordinary shares | Approximate percentage of shareholding interest | ||||

Sheldon Gary Adelson | Company | Interest in a controlled corporation | 5,657,814,855(L) | 70.3% | ||||

Steven Craig Jacobs | Company | Beneficial Owner | 2,500,000(L)(6) | 0.03% | ||||

Toh Hup Hock | Company | Beneficial Owner | 1,078,000(L)(7) | 0.01% | ||||

Name of Director | Associated Corporation | Nature of Interest | Number of Securities | Approximate percentage of shareholding interest | ||||

Sheldon Gary Adelson | LVS | Beneficial Owner | 218,544,122(L)(1) | 33.08% | ||||

| LVS | Family Interest | 213,345,002(L)(2) | 32.29% | |||||

| 5,250,000(L)(3) | 56.21% | |||||||

Jeffrey Howard Schwartz | LVS | Beneficial owner | 114,917(L)(4) | 0.02% | ||||

Irwin Abe Siegel | LVS | Beneficial owner | 51,870(L)(5) | 0.01% | ||||

Steven Craig Jacobs | LVS | Beneficial owner | 658,530(L)(6) | 0.10% | ||||

Toh Hup Hock | LVS | Beneficial owner | 69,000(L)(7) | 0.01% | ||||

The letter “L” denotes the person’s long position in such securities.

| (1) | This amount includes (a) 100 shares of LVS’s common stock, (b) 5,948 shares of restricted stock of which 1,983 shares are vested, (c) 255,362 vested and exercisable options to purchase 255,362 shares of LVS’s common stock, (d) 5,623,125 shares of LVS’s common stock held by the Sheldon G. Adelson 2005 Family |

Trust over which Mr. Adelson, as trustee, retains sole dispositive and voting control, (e) 382,280 shares of LVS’s common stock owned by the Dr. Miriam and Sheldon G. Adelson Charitable Trust over which Mr. Adelson, as trustee, retains sole voting and dispositive power, (f) 15,246,471 shares of LVS’s common stock owned by the Sheldon G. Adelson November 2008 Two Year LVS Annuity Trust over which Mr. Adelson, as trustee, retains sole dispositive control, (g) 44,922,412 shares of LVS’s common stock |

18

| Interim Report 2010 |

|

Corporate Governance

owned by the Sheldon G. Adelson December 2008 Three Year LVS Annuity Trust over which Mr. Adelson, as trustee, retains sole dispositive control, (h) 11,471,421 shares of LVS’s common stock owned by the Sheldon G. Adelson February 2009 Two Year LVS Annuity Trust over which Mr. Adelson, as trustee, retains sole dispositive control, (i) 23,336,445 shares of LVS’s common stock owned by the Sheldon G. Adelson February 2009 Three Year LVS Annuity Trust over which Mr. Adelson, as trustee, retains sole dispositive control, (j) 28,546,985 shares of LVS’s common stock owned by the Sheldon G. Adelson October 2009 Two Year LVS Annuity Trust over which Mr. Adelson, as trustee, retains sole dispositive control, (k) 29,105,939 shares of LVS’s common stock held by the Sheldon G. Adelson October 2009 Three Year LVS Annuity Trust over which Mr. Adelson, as trustee, retains sole dispositive control, (l) 32,000,000 shares of LVS’s common stock held by the Sheldon G. Adelson June 28, 2010 Two Year LVS Annuity Trust over which Mr. Adelson, as trustee, retains sole dispositive control, (m) 27,005,967 shares of LVS’s common stock held by the Sheldon G. Adelson June 29, 2010 Two Year LVS Annuity Trust over which Mr. Adelson, as trustee, retains sole dispositive control, and (n) 641,667 unvested options to purchase 641,667 shares of LVS’s common stock. Mr. Adelson and his wife together are entitled to control the exercise of one-third or more of the voting power at stockholders’ meetings of LVS. LVS’s interests in our Company are set out below. |

| (2) | This amount includes (a) 53,363,636 shares of LVS’s common stock held by Dr. Miriam Adelson, (b) 13,692,516 shares of LVS’s common stock held by the ESBT S Trust over which Dr. Adelson, as trustee, retains sole voting control, (c) 13,692,516 shares of LVS’s common stock held by the ESBT Y Trust over which Dr. Adelson, as trustee, retains sole voting control, (d) 13,692,517 shares of LVS’s common stock held by the QSST A Trust over which Dr. Adelson, as trustee, retains sole voting control, (e) 13,692,517 shares of LVS’s common stock held by the QSST M Trust over which Dr. Adelson, as trustee, retains sole voting control, (f) 5,144,415 shares of LVS’s common stock held by the Sheldon G. Adelson 2004 Remainder Trust over which Dr. Adelson, as trustee, retains sole voting control, (g) 12,566,710 shares of LVS’s common stock owned by Adfam Investment Company LLC over which Dr. Adelson, as co-manager, shares voting and dispositive control with Mr. Adelson and (h) warrants to purchase 87,500,175 shares of LVS’s common stock that are exercisable. |

| (3) | Dr. Adelson holds 5,250,000 shares of preferred stock. |

| (4) | This amount includes (a) 7,273 shares of restricted stock of which 5,268 shares are vested and (b) 107,644 options to purchase 107,644 shares of LVS’s common stock of which 16,528 options are vested and exercisable. |

| (5) | This amount includes (a) 1,000 shares of LVS’s common stock, (b) 10,770 shares of restricted stock of which 8,765 shares are vested and (c) 40,100 options to purchase 40,100 shares of LVS’s common stock, of which 9,100 options are vested and exercisable. |

| (6) | This amount includes (a) 2,500,000 unvested options to purchase 2,500,000 shares of the Company, (b) 352,280 shares of LVS’s common stock and (c) 306,250 unvested options to purchase 306,250 shares of LVS’s common stock. |

| (7) | This amount includes (a) 78,000 shares of the Company, (b) 1,000,000 unvested options to purchase 1,000,000 shares of the Company, (c) 9,000 shares of LVS’s common stock and (d) 60,000 options to purchase 60,000 shares of LVS’s common stock, of which 22,500 options are vested and exercisable. |

None of the Directors or the Chief Executive had short positions in respect of shares, underlying shares and debentures of the Company and its associated corporations (within the meaning of Part XV of the SFO) as at June 30, 2010.

Save as disclosed above, so far as was known to any Director, as at June 30, 2010, none of the Directors or the Chief Executive of the Company had, pursuant to Divisions 7 and 8 of Part XV of the SFO, nor were they taken or deemed to have under such provisions of the SFO, any interest or short position in any shares or underlying shares or interest in debentures of the Company or any of its associated corporations (within the meaning of Part XV of the SFO) that were required to be notified to the Company and the Stock Exchange, or any interests which were required, pursuant to Section 352 of the SFO, to be entered into the register referred to therein, or any interests which were required, pursuant to the Model Code, to be notified to the Company and the Stock Exchange.

As at June 30, 2010, saved as disclosed above, none of the Directors nor the Chief Executive of the Company (including their spouses and children under 18 years of age) had any interest in, or had been granted, or exercised, any rights to subscribe for Shares (or warrants or debentures, if applicable) of the Company and its associated corporations within the meaning of the SFO.

19

| Sands China Ltd. |

|

Corporate Governance

Interests of Substantial Shareholders

The interests/short positions of substantial Shareholders in the shares and underlying shares of the Company as at June 30, 2010, as recorded in the register required to be kept under Section 336 of Part XV of the SFO, are set out in the table and explanatory notes below:

The Company had been notified of the following substantial Shareholders’ interests in the shares as at June 30, 2010:

Name of Substantial Shareholder | Capacity/Nature of interest | Number of shares interested | % of issued share capital | |||

Sheldon Gary Adelson | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

Las Vegas Sands Corp. | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

Las Vegas Sands, LLC | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

Venetian Casino Resort, LLC | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

LVS (Nevada) International Holdings, Inc. | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

LVS Dutch Finance CV | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

LVS Dutch Holding BV | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

LVS Dutch Intermediate Holding BV | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

Venetian Venture Development Intermediate I | Interest in a controlled corporation | 5,657,814,885 | 70.30(L) | |||

Venetian Venture Development Intermediate II | Beneficial owner | 5,657,814,885 | 70.30(L) | |||

As at June 30, 2010, the Company had not been notified of any short positions being held by any substantial shareholder in the shares or underlying shares of the Company.

Interests of Any Other Persons

Save as disclosed above, as at June 30, 2010, the Company had not been notified of any persons who had interests or short positions in the shares or underlying shares of the Company, as recorded in the register required to be kept under Section 336 of Part XV of the SFO.

Share Option Scheme

On November 8, 2009, our Company adopted the Share Option Scheme for the purpose of attracting able persons to enter and remain in the employment of our Group. The Share Option Scheme also provides a means whereby employees, directors and consultants of our Group can

acquire and maintain share ownership, thereby strengthening their commitment to the welfare of our Group and promoting an identity of interest between Shareholders and these persons. For more information on the Share Option Scheme, please refer to pages 100 and 101 of our 2009 Annual Report or pages VII-22 to VII-33 of our Prospectus.

During the Reporting Period, the Company granted 20,376,100 options under the Share Option Scheme on March 31, 2010 and May 11, 2010 to a director and various members of the senior management of the Group. As at June 30, 2010, 566,700 options had lapsed in accordance with the terms of the Share Option Scheme due to resignations or terminations.

20

| Interim Report 2010 |

|

Corporate Governance

Details of the grant of share options and a summary of movements of the outstanding share options during the period under the Share Option Scheme were as follows:

| Number of options | ||||||||||||||||||

| Date of grant | Outstanding as at January 1, 2010 | Granted during Reporting Period | Exercised during Reporting Period | Lapsed during Reporting Period | Cancelled during Reporting Period | Outstanding as at June 30, 2010 | Validity period | Vesting Period | Subscription price per share | |||||||||

March 31, 2010 | — | 17,876,100 | — | 566,700 | — | 17,309,400 | Ten (10) years | 25% will vest on each of | HK$12.40 | |||||||||

May 11, 2010 | — | 2,500,000 | — | — | — | 2,500,000 | Ten (10) years | 50% will vest on each of January 1, 2011 and January 1, 2012 | HK$11.83 | |||||||||

Total: | — | 20,376,100 | — | 566,700 | — | 19,809,400 | ||||||||||||

21

| Sands China Ltd. |

|

Corporate Governance

The closing prices of the Shares immediately before the grant of options on March 31, 2010 and May 11, 2010 were HK$12.10 and HK$11.28 respectively.

Among the options granted above, a total of 2,500,000 options were granted to Mr. Steven Craig Jacobs, an Executive Director, on May 11, 2010. It should be noted that as at the Latest Practicable Date, these options had lapsed due to Mr. Jacobs’ termination.

Save as disclosed herein, no options were granted under the Share Option Scheme or any share option scheme of the Group as at June 30, 2010.

The Company estimates the fair value of options granted using the Black-Scholes option-pricing model. The weighted average fair value of options granted during the Reporting Period, measured as at the date of grant, was approximately US$1.03.

Significant estimates and assumptions are required to be made in determining the parameters for applying the Black-Scholes option-pricing model, including estimates and assumptions regarding the risk-free rate of return, expected dividend yield and volatility of the underlying shares and

the expected life of the options. These estimates and assumptions could have a material effect on the determination of the fair value of the share options and the amount of such equity awards expected to vest, which may in turn significantly impact the determination of the share- based compensation expense. The following assumptions were used to derive the fair values:

Weighted average volatility | 73.6% | |

Expected term (in years) | 6.2 | |

Risk-free rate | 2.0% | |

Expected dividends | — |

Purchase, Sale or Redemption of the Company’s Listed Shares

There was no purchase, sale or redemption of the Company’s listed shares by the Company or any of its subsidiaries during the six months ended June 30, 2010.

By order of the Board of Directors

Sands China Ltd.

Sheldon Gary Adelson

Chairman of the Board

Macao, August 26, 2010

22

| Interim Report 2010 |

|

Report on Review of Condensed Consolidated Interim Financial Information

To the Board of Directors of Sands China Ltd.

(incorporated in the Cayman Islands with limited liability)

Introduction

We have reviewed the condensed consolidated interim financial information set out on pages 25 to 53, which comprises the consolidated balance sheet of Sands China Ltd. (the “Company”) and its subsidiaries (together, the “Group”) as at June 30, 2010 and the related consolidated income statement, the consolidated statement of comprehensive income, the consolidated statement of changes in equity and the condensed consolidated statement of cash flows for the six-month period then ended, and a summary of significant accounting policies and other explanatory notes. The Rules Governing the Listing of Securities on The Stock Exchange of Hong Kong Limited require the preparation of a report on interim financial information to be in compliance with the relevant provisions thereof and International Accounting Standard 34 “Interim Financial Reporting”. The directors of the Company are responsible for the preparation and presentation of this condensed consolidated interim financial information in accordance with International Accounting Standard 34 “Interim Financial Reporting”. Our responsibility is to express a conclusion on this condensed consolidated interim financial information based on our review and to report our conclusion solely to you, as a body, in accordance with our agreed terms of engagement and for no other purpose. We do not assume responsibility towards or accept liability to any other person for the contents of this report.

Scope of review

We conducted our review in accordance with International Standard on Review Engagements 2410, “Review of Interim Financial Information Performed by the Independent Auditor of the Entity”. A review of interim financial information consists of making inquiries, primarily of persons responsible for financial and accounting matters, and applying analytical and other review procedures. A review is substantially less in scope than an audit conducted in accordance with International Standards on Auditing and consequently does not enable us to obtain assurance that we would become aware of all significant matters that might be identified in an audit. Accordingly, we do not express an audit opinion.

23

| Sands China Ltd. |

|

Report on Review of Condensed Consolidated Interim Financial Information

Conclusion

Based on our review, nothing has come to our attention that causes us to believe that the condensed consolidated interim financial information is not prepared, in all material respects, in accordance with International Accounting Standard 34 “Interim Financial Reporting”.

PricewaterhouseCoopers

Certified Public Accountants

Hong Kong, August 26, 2010

24

| Interim Report 2010 |

|

Consolidated Balance Sheet

| As at June 30, 2010 | | As at December 31, 2009 | | |||||||

| US$’000 | ||||||||||

| Note | (Unaudited | ) | (Audited, as restated) |

| ||||||

ASSETS | ||||||||||

Non-current assets | ||||||||||

Investment properties, net | 764,626 | 748,743 | ||||||||

Property and equipment, net | 5 | 5,414,194 | 5,525,057 | |||||||

Intangible assets, net | 38,050 | 41,005 | ||||||||

Deferred income tax assets | 96 | 113 | ||||||||

Financial assets at fair value through profit or loss | 114 | 1,529 | ||||||||

Other assets, net | 41,360 | 48,794 | ||||||||

Trade and other receivables and prepayments, net | 28,946 | 31,955 | ||||||||

Total non-current assets | 6,287,386 | 6,397,196 | ||||||||

Current assets | ||||||||||

Inventories | 8,307 | 9,630 | ||||||||

Trade and other receivables and prepayments, net | 6 | 282,803 | 295,400 | |||||||

Investments | 7 | 173,461 | — | |||||||

Restricted cash | 25,041 | 17,172 | ||||||||

Cash and cash equivalents | 673,763 | 908,334 | ||||||||

Total current assets | 1,163,375 | 1,230,536 | ||||||||

Total assets | 7,450,761 | 7,627,732 | ||||||||

The notes on pages 31 to 53 form an integral part of this condensed consolidated interim financial information.

25

| Sands China Ltd. |

|

Consolidated Balance Sheet

| As at June 30, 2010 | | As at December 31, 2009 | | |||||||

| US$’000 | ||||||||||

| Note | (Unaudited | ) | (Audited, as restated) | | ||||||

EQUITY | ||||||||||

Capital and reserves attributable to equity holders | ||||||||||

Share capital | 8 | 80,479 | 80,479 | |||||||

Reserves | 3,863,381 | 3,618,415 | ||||||||

Total equity | 3,943,860 | 3,698,894 | ||||||||

LIABILITIES | ||||||||||

Non-current liabilities | ||||||||||

Trade and other payables | 14,794 | 12,570 | ||||||||

Borrowings | 9 | 2,324,213 | 2,950,849 | |||||||

Total non-current liabilities | 2,339,007 | 2,963,419 | ||||||||

Current liabilities | ||||||||||

Trade and other payables | 10 | 860,990 | 828,791 | |||||||

Current income tax liabilities | 242 | 172 | ||||||||

Borrowings | 9 | 306,662 | 136,456 | |||||||

Total current liabilities | 1,167,894 | 965,419 | ||||||||

Total liabilities | 3,506,901 | 3,928,838 | ||||||||

Total equity and liabilities | 7,450,761 | 7,627,732 | ||||||||

Net current (liabilities)/assets | (4,519 | ) | 265,117 | |||||||

Total assets less current liabilities | 6,282,867 | 6,662,313 | ||||||||

Approved by the Board of Directors on August 26, 2010 and signed on behalf of the Board by

Michael Alan Leven | Toh Hup Hock | |

Director | Director |

The notes on pages 31 to 53 form an integral part of this condensed consolidated interim financial information.

26

| Interim Report 2010 |

|

Consolidated Income Statement

| Six months ended June 30, | ||||||||||

| 2010 | 2009 | |||||||||

| US$’000, except per share data | ||||||||||

| Note | (Unaudited | ) | (Audited, as restated) |

| ||||||

Net revenues | 11 | 1,980,499 | 1,500,587 | |||||||

Gaming tax | (872,525 | ) | (633,417 | ) | ||||||

Inventories consumed | (20,507 | ) | (20,408 | ) | ||||||

Employee benefit expenses | (223,039 | ) | (232,856 | ) | ||||||

Depreciation and amortization | (163,339 | ) | (162,362 | ) | ||||||

Gaming promoter/agency commissions | (109,177 | ) | (86,827 | ) | ||||||

Other expenses | (270,984 | ) | (252,459 | ) | ||||||

Operating profit | 320,928 | 112,258 | ||||||||

Interest income | 1,175 | 281 | ||||||||

Interest expense, net of amounts capitalized | (71,450 | ) | (54,026 | ) | ||||||

Profit before income tax | 250,653 | 58,513 | ||||||||

Income tax expense | 12 | (153 | ) | (167 | ) | |||||

Profit for the period and attributable to | 250,500 | 58,346 | ||||||||

Dividends | 13 | — | — | |||||||

Earnings per share for profit attributable to | ||||||||||

Basic and diluted | 14 | US3.11 cents | US0.93 cents | |||||||

The notes on pages 31 to 53 form an integral part of this condensed consolidated interim financial information.

27

| Sands China Ltd. |

|

Consolidated Statement of Comprehensive Income

| Six months ended June 30, | ||||||

| 2010 | 2009 | |||||

| US$’000 | ||||||

| (Unaudited | ) | (Audited, as restated) | | |||

Profit for the period attributable to equity holders of the Company | 250,500 | 58,346 | ||||

Other comprehensive (loss)/income, net of tax: | ||||||

Currency translation differences | (13,969 | ) | 182 | |||

Total comprehensive income for the period attributable to | 236,531 | 58,528 | ||||

The notes on pages 31 to 53 form an integral part of this condensed consolidated interim financial information.

28

| Interim Report 2010 |

|

Consolidated Statement of Changes in Equity

| Share-based | Currency | ||||||||||||||||||

| Capital | Share | Statutory | compensation | translation | Retained | ||||||||||||||

| Share capital | reserve | premium | reserve | reserve | reserve | earnings | Total | ||||||||||||

| US$’000

(Audited, as restated) |

| ||||||||||||||||||

For the six months ended June 30, 2009 | |||||||||||||||||||

Balance at December 31, 2008, | — | 80,049 | — | 6,222 | 17,538 | 5,632 | 1,140,093 | 1,249,534 | |||||||||||

Effect on adoption of IAS17 Amendment | — | — | — | — | — | — | 12,322 | 12,322 | |||||||||||

Balance at December 31, 2008, as restated | — | 80,049 | — | 6,222 | 17,538 | 5,632 | 1,152,415 | 1,261,856 | |||||||||||

Total comprehensive income | — | — | — | — | — | 182 | 58,346 | 58,528 | |||||||||||

Share-based compensation charged by LVS | — | — | — | — | 3,849 | — | — | 3,849 | |||||||||||

Transfer to statutory reserve | — | — | — | 93 | — | — | (93 | ) | — | ||||||||||

Balance at June 30, 2009 | — | 80,049 | — | 6,315 | 21,387 | 5,814 | 1,210,668 | 1,324,233 | |||||||||||

| (Unaudited) | |||||||||||||||||||

For the six months ended June 30, 2010 | |||||||||||||||||||

Balance at December 31, 2009, | 80,479 | 87,435 | 2,127,537 | 6,315 | 26,051 | 3,739 | 1,353,836 | 3,685,392 | |||||||||||

Effect on adoption of IAS17 Amendment | — | — | — | — | — | — | 13,502 | 13,502 | |||||||||||

Balance at December 31, 2009, as restated | 80,479 | 87,435 | 2,127,537 | 6,315 | 26,051 | 3,739 | 1,367,338 | 3,698,894 | |||||||||||

Total comprehensive income | — | — | — | — | — | (13,969 | ) | 250,500 | 236,531 | ||||||||||

Share-based compensation of the Company | — | — | — | — | 2,374 | — | — | 2,374 | |||||||||||

Share-based compensation charged by LVS | — | — | — | — | 6,061 | — | — | 6,061 | |||||||||||

Balance at June 30, 2010 | 80,479 | 87,435 | 2,127,537 | 6,315 | 34,486 | (10,230 | ) | 1,617,838 | 3,943,860 | ||||||||||

The notes on pages 31 to 53 form an integral part of this condensed consolidated interim financial information.

29

| Sands China Ltd. |

|

Condensed Consolidated Statement of Cash Flows

| Six months ended June 30, | ||||||

| 2010 | 2009 | |||||

| US$’000 | ||||||

| (Unaudited | ) | (Audited, as restated) | | |||

Net cash generated from operating activities | 584,949 | 298,828 | ||||

Net cash used in investing activities | (288,270 | ) | (244,495 | ) | ||

Net cash used in financing activities | (528,641 | ) | (131,160 | ) | ||

Net decrease in cash and cash equivalents | (231,962 | ) | (76,827 | ) | ||

Cash and cash equivalents at beginning of the period | 908,334 | 417,769 | ||||

Effect of exchange rate on cash and cash equivalents | (2,609 | ) | (322 | ) | ||

Cash and cash equivalents at end of the period | 673,763 | 340,620 | ||||

The notes on pages 31 to 53 form an integral part of this condensed consolidated interim financial information.

30

| Interim Report 2010 |

|

Notes to the Condensed Consolidated Interim Financial Information

| 1. | General information |

Principal activities

Sands China Ltd. (the “Company”) and its subsidiaries (collectively the “Group”) is principally engaged in the development and operation of integrated resorts and other ancillary services (the “Gaming and Other Related Operations”) in the Macao Special Administrative Region of the People’s Republic of China (“Macao”).

The Company was incorporated in the Cayman Islands on July 15, 2009 as an exempted company with limited liability under the Companies Law, Cap 22 (Law 3 of 1961, as consolidated and revised) of the Cayman Islands. The address of the Company’s registered office is Walkers Corporate Services Limited, Walker House, 87 Mary Street, George Town, Grand Cayman KY1-9005, Cayman Islands. The Company’s principal place of business in Hong Kong registered under Part XI of the Hong Kong Companies Ordinance at Level 28, Three Pacific Place, 1 Queen’s Road East, Hong Kong.

The Group owns and operates the Sands Macao, the first Las Vegas-style casino in Macao, pursuant to a 20-year gaming subconcession.

The Group also owns and operates The Venetian Macao Resort Hotel (“The Venetian Macao”), which anchors the Cotai Strip, the Group’s master-planned development of integrated resort properties in Macao.

In August 2008, the Group opened the Four Seasons Hotel, the Plaza Casino, the Shoppes at Four Seasons (together with the Paiza Mansions opened in July 2009 and the apart-hotel tower, referred to as “The Plaza Macao”). The Plaza Macao is located adjacent to The Venetian Macao.

The Group’s other ancillary services include ferry operations and other related operations.

The Company’s shares were listed on the Main Board of the Stock Exchange on November 30, 2009.

The unaudited condensed consolidated interim financial information (the “Interim Financial Information”) is presented in United States dollars (“US$”), unless otherwise stated. The Interim Financial Information was approved and authorized for issue by the Board of Directors of the Company on August 26, 2010.

This Interim Financial Information has not been audited.

| 2. | Basis of preparation |

The Interim Financial Information for the six months ended June 30, 2010 has been prepared in accordance with the International Accounting Standard (“IAS”) 34 ‘Interim Financial Reporting’ issued by the International Accounting Standard Board (“IASB”) and the applicable disclosure requirements of Appendix 16 to the Listing Rules. It should be read in conjunction with the Group’s annual financial statements for the year ended December 31, 2009, which were prepared in accordance with International Financial Reporting Standards (“IFRS”).

31

| Sands China Ltd. |

|

Notes to the Condensed Consolidated Interim Financial Information

| 3. | Changes in accounting policies and disclosures |

The accounting policies adopted in the preparation of the Interim Financial Information for the six months ended June 30, 2010 are consistent with those adopted and as described in the Group’s annual financial statements for the year ended December 31, 2009, except for the adoption of new standards and interpretations as of January 1, 2010, noted below which are relevant to the Group.

IAS 17 (amendment), ‘Leases’ (effective from January 1, 2010). The amendment is part of the IASB’s annual improvements project published in April 2009 and the Group has applied IAS 17 (amendment) from January 1, 2010. The adoption of IAS 17 (amendment) resulted in retrospective adjustments of leasehold interests in land from operating lease to finance lease, and finance lease liabilities on leasehold interests in land, and the consequential adjustments on investment properties, property and equipment, operating lease amortization, finance lease depreciation, interest expense and related interest capitalization. The effect of the adoption is set out in Note 18 to the Group’s Interim Financial Information.

International Financial Reporting Interpretations Committee (“IFRIC”) 17 ‘Distribution of non-cash assets to owners’ (effective on or after July 1, 2009), provides guidance on accounting for arrangements whereby an entity distributes non- cash assets to shareholders either as a distribution of reserves or as dividends. IFRS 5 has also been amended to require that assets are classified as held for distribution only when they are available for distribution in their present condition and the distribution is highly probable. The adoption of IFRIC 17 has no material impact on the Group’s Interim Financial Information.

IAS 27 (revised), ‘Consolidated and separate financial statements’, (effective from July 1, 2009). The revised standard requires the effects of all transactions with minority interest to be recorded in equity if there is no change in control and these transactions will no longer result in goodwill or gains and losses. The standard also specifies the accounting when control is lost. Any remaining interest in the entity is re-measured to fair value, and a gain or loss is recognized in the consolidated income statement. The Group adopted IAS 27 (revised) prospectively to transactions with minority interest from January 1, 2010 and the adoption of IAS 27 (revised) has no material impact on the Group’s Interim Financial Information.

IFRS 3 (revised), ‘Business combinations’ (effective from July 1, 2009). The revised standard continues to apply the acquisition method to business combinations, with some significant changes. For example, all payments to purchase a business are to be recorded at fair value at the acquisition date, with contingent payments classified as debt subsequently re-measured through the consolidated income statement. There is a choice on an acquisition-by-acquisition basis to measure the non-controlling interest in the acquiree either at fair vale or at the non-controlling interest’s proportionate share of the acquiree’s net assets. All acquisition-related costs should be expensed. The Group adopted IFRS 3 (revised) prospectively to all business combinations from January 1, 2010 and the adoption of IFRS 3 (revised) has no material impact on the Group’s Interim Financial Information.

IAS 38 (amendment), ‘Intangible Assets’ (effective from July 1, 2009), clarifies guidance in measuring the fair value of an intangible asset acquired in a business combination and it permits the grouping of intangible assets as a single asset if each asset has similar useful economic lives. The amendment has no material impact on the Group’s Interim Financial Information.

32

| Interim Report 2010 |

|

Notes to the Condensed Consolidated Interim Financial Information

| 3. | Changes in accounting policies and disclosures (continued) |

IFRS 5 (amendment), ‘Measurement of non-current assets (or disposal groups) classified as held for sale’, provides clarification that IFRS 5 specifies the disclosures required in respect of non-current assets (or disposal groups) classified as held for sale or discontinued operations. It also clarifies that the general requirements of IAS 1 still apply, particularly paragraph 15 (to achieve a fair presentation) and paragraph 125 (sources of estimation uncertainty) of IAS 1. The Group adopted IFRS 5 (amendment) from January 1, 2010 and the amendment has no material impact on the Group’s Interim Financial Information.