Exhibit 99.1

Approaching Capital in a Recessionary Environment

Phil Cavatoni, Chief Strategy Officer

October 1, 2009

2

Certain statements made by management during this call and webcast constitute "forward-looking

statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are

not guarantees of future performance. Risks and uncertainties are inherent in our future performance.

Many factors could cause our actual results, performance or achievements, or industry results, to be

materially different from any future results, performance or achievements expressed or implied by such

forward looking-statements. These factors are discussed in detail in our Annual Report on Form 10-K and in

our other filings with the SEC, which you access through the investor relations section of Alpha’s website or

the SEC website. Given these risks and uncertainties, prospective and current investors are cautioned not to

place undue reliance on such forward-looking statements. We make forward-looking statements based on

currently available information, and we assume no obligation to update the statements made today or

contained in our Annual Report or other filings due to changes in underlying factors, new information,

future developments, or otherwise, except as required by law.

statements" within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements are

not guarantees of future performance. Risks and uncertainties are inherent in our future performance.

Many factors could cause our actual results, performance or achievements, or industry results, to be

materially different from any future results, performance or achievements expressed or implied by such

forward looking-statements. These factors are discussed in detail in our Annual Report on Form 10-K and in

our other filings with the SEC, which you access through the investor relations section of Alpha’s website or

the SEC website. Given these risks and uncertainties, prospective and current investors are cautioned not to

place undue reliance on such forward-looking statements. We make forward-looking statements based on

currently available information, and we assume no obligation to update the statements made today or

contained in our Annual Report or other filings due to changes in underlying factors, new information,

future developments, or otherwise, except as required by law.

3

v Headwinds in 2009

v Lower industrial demand for electricity

v Decreased demand for metallurgical coal

v Reduced net coal exports from the U.S.

v Coal-to-gas switching for electricity generation driven by low gas prices

v Milder-than-normal weather

v Demand for metallurgical coal recovering

v U.S. steel inventories at service centers bottomed at 25-30 year lows

v U.S. capacity utilization less than 45% in 1H09

v U.S. capacity utilization has been increasing for several weeks, now approaching 60%

v Investor focus on near-term international demand for metallurgical coal

v China met coal imports up significantly YOY, driving up spot prices in Asia

v Asian demand reduces availability of Australian coking coal in Atlantic Basin

v Steel production can be expected to recover in Europe, Brazil and the United States

which will increase demand for Appalachian coking coal

which will increase demand for Appalachian coking coal

v Valuations for metallurgical coal assets reflect investors’ enthusiasm

Source: WSA , Credit Suisse research

4

v Challenging market for domestic steam coal

v U.S. electricity generation down 4% YTD; coal-fired generation down +10%

v Nationwide inventory of 180-190 million equates to greater than 65 days of burn

v Annualized run-rate of production cutbacks total ~100 million tons

v Today’s spot prices force some high cost, uneconomic production from the market

v Domestic steam coal is currently out of favor

v Domestic steam coal poised for eventual recovery

v U.S. entering a period of “easy comps”

v Evidence of economic recovery mounting

v Forward prices indicate that low-priced natural gas won’t last—switching could reverse

v Return to normal weather likely

v Today’s steam coal market could offer attractive investment opportunity

v Asia expected to drive long-term growth in steam coal demand

v Global coal consumption rose approximately 40% between 2000 and 2008

v China’s 2010 coal demand expected to be 3 billion tons (BTs), growing to 5 BTs in 2030

v Worldwide coal demand is forecast to rise from 7.4 BTs in 2010 to 9.9 BTs in 2030

v How should a U.S. company position itself to benefit from this growth?

Source: EIA, Stifel Nicolaus research, internal analysis

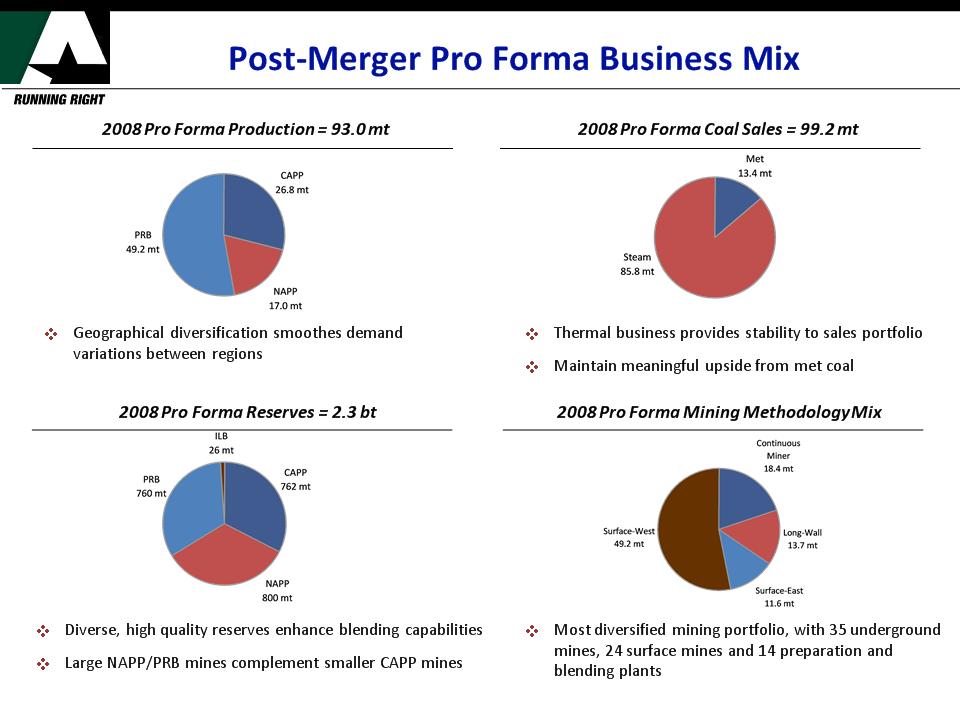

Foundation Coal - A Practical Example

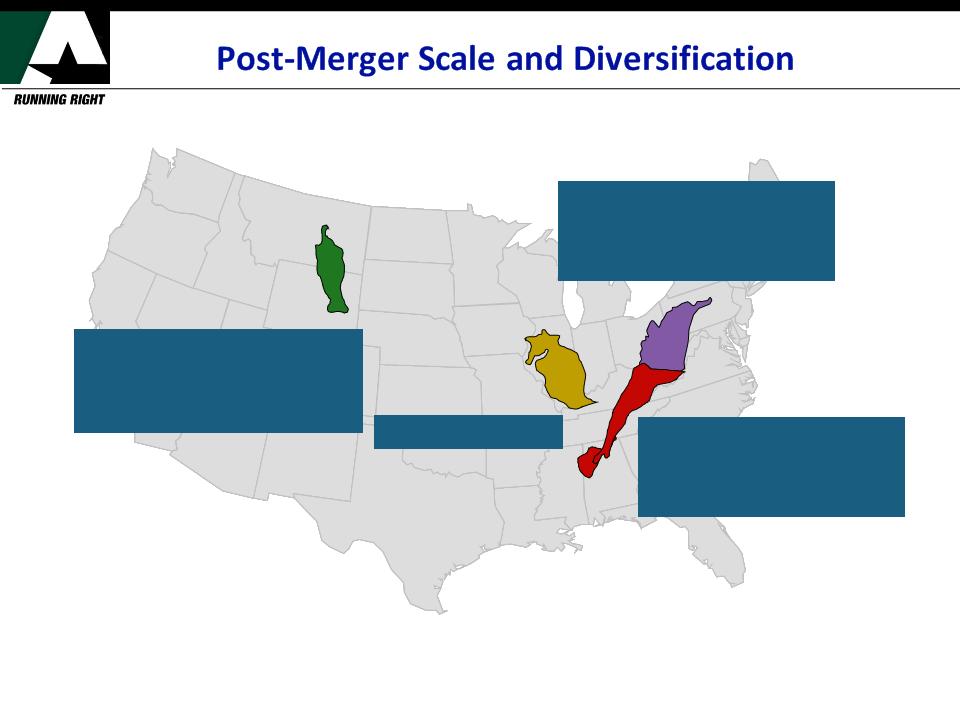

Pre-merger

6

v Large number of small mines

v Limited number of organic projects

v 600 MTs of reserves

v Cyclically volatile earnings

v Concentrated in CAPP

Post-merger

ü Added large mines with long lives in NAPP, PRB

ü Organic potential in NAPP, CAPP including new met

ü 2.3 BTs of reserves

ü Positioned to mitigate volatility through diversification

ü Most geographically diverse domestic producer

v Limited scale

ü Third largest U.S. producer by most metrics

Strategic Fit

From a strategic perspective, the merger significantly strengthened Alpha’s

business model and positioning in the domestic industry

business model and positioning in the domestic industry

Source: internal projections

Northern Appalachia

Central Appalachia

Illinois Basin

Powder River Basin

Production Capacity | 55.0 |

2008 Shipments | 49.2 |

Reserves | 760 |

Reserves | 26 |

Production Capacity | 17.3 |

2008 Shipments | 17.9 |

Reserves | 800 |

Production Capacity | 25.0 |

2008 Shipments | 32.1 |

Reserves | 762 |

Note: Figures pro forma as of 12/31/08.

7

8

14%

86%

20%

15%

12%

53%

29%

18%

53%

35%

32%

32%

1%

Source: internal projections

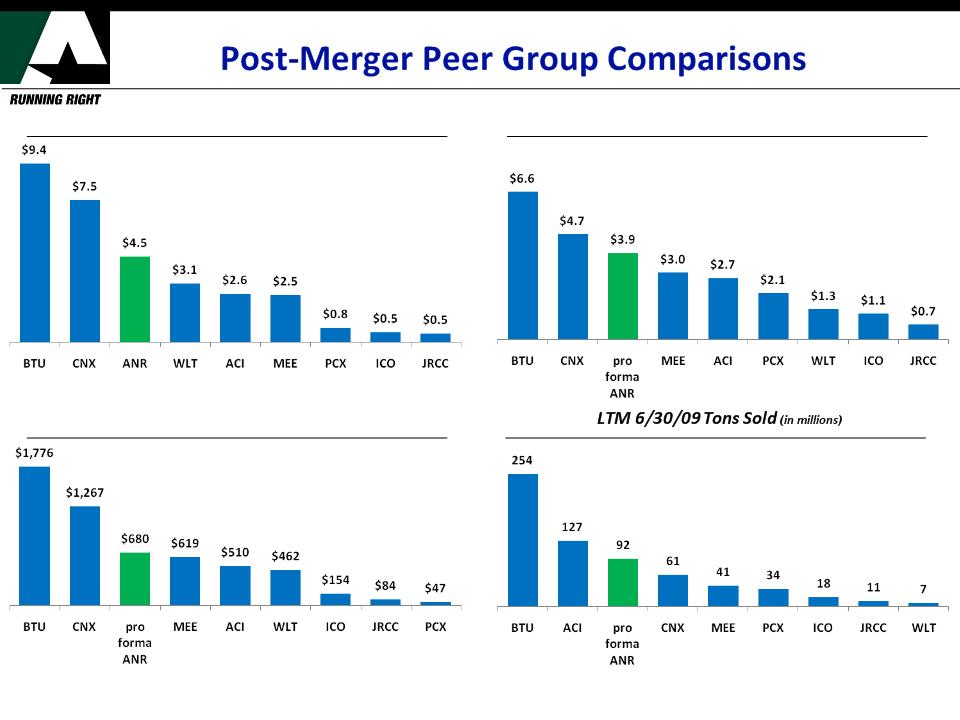

Source: Public filings and company press releases.

(1) Market data as of 9/9/09.

(2) Based on Alpha Natural Resources, Inc. reported EBITDA and Foundation Coal Holdings, Inc. adjusted EBITDA as reported in Form 10-Qs for the quarterly periods ended June 30, 2009, both of which are available on our

website at www.alphanr.com.

(1) Market data as of 9/9/09.

(2) Based on Alpha Natural Resources, Inc. reported EBITDA and Foundation Coal Holdings, Inc. adjusted EBITDA as reported in Form 10-Qs for the quarterly periods ended June 30, 2009, both of which are available on our

website at www.alphanr.com.

Market Capitalization(1) ($ in billions)

LTM 6/30/09 Revenue ($ in billions)

LTM 6/30/09 EBITDA(2) ($ in millions)

9

Foundation Coal - A Practical Example (con’t)

10

v Similar corporate cultures

v Complimentary management teams

v Compatible workforces

v Robust and replicable integration process

v Shared mission, vision and values unite the combined organization

The ability to manage the integration in terms of scope, process, operations and personnel

was given careful consideration in advance, and execution has gone according to plan.

was given careful consideration in advance, and execution has gone according to plan.

Manageability

Foundation Coal - A Practical Example

11

Alpha emerged from the transaction well-positioned for the future.

ü Strong post-closing liquidity of approximately $1 billion

ü Approximately $500 million in cash

ü Highly hedged book of business

ü Low leverage ratio at 1.3x debt-to-EBITDA

ü Favorable terms on remaining debt

ü Able to entertain future M&A or organic growth opportunities, or both

Empirical evidence suggests that greater scale and diversification will be accorded higher

valuation multiples in the coal mining industry.

valuation multiples in the coal mining industry.

While we had a view going into the transaction, investors will judge the appropriateness

of the valuation and return characteristics of the Alpha/Foundation merger.

of the valuation and return characteristics of the Alpha/Foundation merger.

End State

Valuation/Return

12

Build or buy?

Metallurgical or steam?

Which geographic region?

13

v Business cycle

v Market valuations

v Expected returns and cash flows

v Speed of implementation

v Potential synergies

v Marketing considerations

The decision to grow internally or through acquisition will be

determined by:

determined by:

14

This decision will be heavily dependent on our current and forward

-looking view of the markets

-looking view of the markets

v Met coal assets have been bid up in expectation

of a strong recovery

of a strong recovery

v Met coal is a scarce resource that can command

strong margins in a healthy market

strong margins in a healthy market

v Steam coal remains out of favor

v Current prices for eastern steam coal are under

the cost of production for a significant portion of

Central Appalachian production

the cost of production for a significant portion of

Central Appalachian production

v Currently bloated inventories are anticipated to

correct and demand for thermal coal is

projected to rebound over time

correct and demand for thermal coal is

projected to rebound over time

v Political and permitting pressures on CAPP

production could limit supply in the future

production could limit supply in the future

This decision will be guided by a balance of factors, including

diversification, opportunity set, market view, and possible synergies

diversification, opportunity set, market view, and possible synergies

v If thermal coal demand recovers and CAPP

production gradually declines, CAPP opportunities

could make sense

production gradually declines, CAPP opportunities

could make sense

v Permitting and MTR challenges limit CAPP volumes

v Current prices below production costs forcing high-

cost production out of the market

cost production out of the market

v Are bankrupt assets attractive—probably not

v NAPP is attractive, but opportunity set is limited

v As CAPP declines ILB, PRB & WBIT can fill demand

v ILB is attractive with large reserves, low-costs and

transportation advantages

transportation advantages

v PRB is the fastest growing region in the U.S.

v ~ ½ of new coal-fired generation to rely on PRB

v Now out of favor due to prices and utility

inventories, PRB & WBIT could hold promise

inventories, PRB & WBIT could hold promise

v Global demand growth will be driven by Asia, so

international opportunities are significant, but

logistics, culture & politics must be considered

international opportunities are significant, but

logistics, culture & politics must be considered