UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

x | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

| | |

For the quarterly period ended: March 31, 2008 |

| | |

Or |

| | |

o | TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number: 000-50983

ECOTALITY, INC.

(Exact name of registrant as specified in its charter)

Nevada | 68-0515422 |

| (State or other jurisdiction of incorporation or organization) | (I.R.S. Employer Identification No.) |

| | |

6821 E Thomas Road, Scottsdale, Arizona | 85251 |

| (Address of principal executive offices) | (Zip Code) |

(480) 219-5005

(Registrant’s telephone number, including area code)

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes x No o

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See the definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check One):

Large accelerated filer o | | Accelerated filer o | | Non-accelerated filer o (Do not check of a smaller reporting company) | | Smaller reporting company þ |

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes o No x

Indicate the number of shares outstanding of each of the issuer’s classes of common stock, as of May 15, 2008

124,732,861

ECOtality, Inc.

Table of Contents

| PART I - FINANCIAL INFORMATION | 3 |

| | |

| |

| | |

Condensed Consolidated Balance Sheet | |

| |

| Condensed Consolidated Statements of Operations | 4 |

| | |

Condensed Consolidated Statements of Cash Flows | |

| | |

| Notes to Condensed Consolidated Financial Statements | 6 |

| | |

Management’s Discussion and Analysis of Financial Condition and Results of Operation | |

| |

| Quantitative and Qualitative Disclosures about Market Risk | 31 |

| | |

| Controls and Procedures | 31 |

| | |

| PART II - OTHER INFORMATION | 32 |

| | |

| Legal Proceedings | 32 |

| | |

| Risk Factors | 32 |

| | |

Unregistered Sales of Equity Securities | |

| |

| Defaults Upon Senior Securities | 33 |

| | |

| Submission of Matters to a Vote of Security Holders | 33 |

| | |

Exhibits and Reports on Form 8-K | |

| | |

| SIGNATURES | 36 |

PART 1. FINANCIAL INFORMATION

ECOTALITY, INC.

CONDENSED CONSOLIDATED BALANCE SHEETS

(unaudited)

| | | March 31, 2008 | | December 31, 2007 | |

| | | (Unaudited) | | | |

Assets | | | | | |

| | | | | | |

| Current assets: | | | | | | | |

| Cash | | $ | 616,712 | | $ | 677,318 | |

| Certificates of deposit | | | 50,727 | | | 1,197,784 | |

Receivables, net of allowance for bad debt of $21,252 and $21,743 as of 03/31/08 and 12/31/07 respectively | | | 2,624,554 | | | 2,387,542 | |

Inventory, net of allowance for obsolescence of $48,000 and $293,934 as of 03/31/08 and 12/31/07 respectively | | | 1,075,647 | | | 1,791,174 | |

| Prepaid expenses and other current assets | | | 587,417 | | | 477,186 | |

| Total current assets | | | 4,955,057 | | | 6,531,004 | |

| | | | | | | | |

Fixed assets, net accumulated depreciation of $4,026,187 and $3,884,302 as of 03/31/08 and 12/31/07 respectively | | | 2,028,535 | | | 2,027,142 | |

| | | | | | | | |

| Goodwill | | | 3,095,878 | | | 3,095,878 | |

| | | | | | | | |

| Total assets | | $ | 10,079,470 | | $ | 11,654,025 | |

| | | | | | | | |

Liabilities and Stockholders’ Equity | | | | | | | |

| | | | | | | | |

| Current liabilities: | | | | | | | |

| Accounts payable | | $ | 1,202,100 | | $ | 1,317,916 | |

| Accrued liabilities | | | 770,709 | | | 670,746 | |

| Liability for purchase price | | | 4,245,600 | | | 4,075,000 | |

| Current portion of LT Debt, net of discount of $1,291,272 and 1,174,075 as of 03/31/08 and 12/31/07 respectively | | | 1,334,757 | | | 1,147,241 | |

| Total current liabilities | | | 7,553,168 | | | 7,210,903 | |

| | | | | | | | |

| Total LT Liabilities, net of discount of $1,935,140 and $2,494,910 as of 03/31/08 and 12/31/07 respectively | | | 1,532,791 | | | 1,808,314 | |

| | | | | | | | |

| Stockholders’ equity: | | | | | | | |

| Preferred stock, $0.001 par value, 200,000,000 shares | | | | | | | |

| authorized, no shares issued and outstanding | | | - | | | - | |

| Common stock, $0.001 par value, 300,000,000 shares | | | | | | | |

| authorized, 124,732,861 and 124,224,528 shares issued | | | | | | | |

| and outstanding as of 03/31/08 and 12/31/07, respectively | | | 124,733 | | | 124,225 | |

| Additional paid-in capital | | | 31,139,184 | | | 30,780,992 | |

| Retained deficit | | | (30,262,626 | ) | | (28,270,409 | ) |

| Accumulated Foreign Currency Translation Adjustments | | | (7,782 | ) | | - | |

| Total stockholders' equity | | | 993,510 | | | 2,634,808 | |

| | | | | | | | |

| Total liabilities and stockholders' equity | | $ | 10,079,470 | | $ | 11,654,025 | |

The accompanying notes are an integral part of these financial statements.

ECOTALITY, INC.

CONDENSED CONSOLIDATED STATEMENTS OF OPERATIONS

(unaudited)

| | | For the Three Months Ended | |

| | | March 31, | |

| | | 2008 | | 2007 | |

| | | (Unaudited) | |

| Revenue | | $ | 2,817,899 | | $ | - | |

| Cost of goods sold | | | 1,616,355 | | | - | |

| | | | | | | | |

| Gross profit | | $ | 1,201,544 | | $ | - | |

| | | | | | | | |

Expenses: | | | | | | | |

| Depreciation | | | 141,886 | | | 48,087 | |

| General and administrative expenses | | | 2,357,009 | | | 542,533 | |

| Research and development | | | 115,686 | | | 373,530 | |

| Settlement Expense | | | 0 | | | 1,800,000 | |

| Total expenses | | | 2,614,581 | | | 2,764,150 | |

| | | | | | | | |

| Operating loss | | | (1,413,037 | ) | | (2,764,150 | ) |

| | | | | | | | |

| Other income: | | | | | | | |

| Interest income | | | 8,150 | | | 21,743 | |

| Total other income | | | 8,150 | | | 21,743 | |

| | | | | | | | |

| Other expenses: | | | | | | | |

| Interest expense | | | 562,304 | | | 3,234 | |

| Loss on Disposal of Assets | | | 25,020 | | | - | |

| Accrued expense - Potential Registration Rights Penalty | | | | | | 3,001,493 | |

| Total other expenses | | | 587,324 | | | 3,004,727 | |

| | | | | | | | |

| Loss from operations before income taxes | | | ($1,992,211 | ) | | ($5,747,134 | ) |

| | | | | | | | |

| Provision for income taxes | | | - | | | - | |

| | | | | | | | |

| Net (loss) | | | ($1,992,211 | ) | | ($5,747,134 | ) |

| | | | | | | | |

| Weighted average number of | | | | | | | |

| common shares outstanding - basic and fully diluted | | | 124,469,621 | | | 110,066,566 | |

| | | | | | | | |

| Net (loss) per share-basic and fully diluted | | | ($0.02 | ) | | ($0.05 | ) |

The accompanying notes are an integral part of these financial statements.

ECOTALITY, INC.

CONDENSED CONSOLIDATED STATEMENTS OF CASH FLOWS

(unaudited)

| | | For the Three Months Ended | |

| | | March 31, | |

| | | 2008 | | 2007 | |

Cash flows from operating activities | | (unaudited) | |

| Net Income (loss) | | | ($1,992,211 | ) | | ($5,747,134 | ) |

| Adjustments to reconcile: | | | | | | | |

| Stock and options issued for services and compensation | | | 52,288 | | | - | |

| Shares issued for settlement | | | - | | | 1,200,000 | |

| Shares Accrued for registration penalty | | | | | | 3,001,493 | |

| Depreciation | | | 141,886 | | | 48,087 | |

| Amortization of stock issued for services | | | 91,413 | | | - | |

| Amortization of discount on notes payable | | | 442,573 | | | - | |

| Loss on disposal of assets | | | 25,020 | | | - | |

| Changes in operating assets and liabilities: | | | | | | | |

| Certificate of deposit | | | 1,147,057 | | | (21,743 | ) |

| Accounts Receivable | | | (230,248 | ) | | - | |

| Inventory | | | 690,503 | | | - | |

| Prepaid expenses and other | | | (116,995 | ) | | 5,543 | |

| Accounts Payable | | | (115,816 | ) | | (87,107 | ) |

| Accrued Liabilities | | | (42,836 | ) | | 1,183 | |

| Net cash provided (used) by operating activities | | | 92,634 | | | (1,599,678 | ) |

Cash flows from investing activities | | | | | | | |

| Purchase of fixed assets | | | (143,277 | ) | | (611,019 | ) |

| Net cash (used) by investing activities | | | (143,277 | ) | | (611,019 | ) |

| | | | | | | | |

Cash flows from financing activities | | | | | | | |

| Mortgage Payable | | | | | | 287,500 | |

| Payments on notes payable | | | (2,180 | ) | | - | |

| Net cash provided (used) by financing activities | | | (2,180 | ) | | 287,500 | |

| | | | | | | | |

| Effects of exchange rate changes | | | (7,782 | ) | | | |

| | | | | | | | |

| Net increase (decrease) in cash | | | (60,605 | ) | | (1,923,197 | ) |

| Cash - beginning | | | 677,318 | | | 5,047,968 | |

| Cash - ending | | | 616,712 | | | 3,124,771 | |

| | | | | | | | |

| Supplemental disclosures: | | | | | | | |

| Interest paid | | | 4,758 | | | 3,234 | |

| | | | | | | | |

| Non-cash transactions: | | | | | | | |

| Stock and options issued for services | | $ | 52,288 | | $ | - | |

| Shares of stock issued | | | 125,000 | | | - | |

| Number of options issued | | | 175,000 | | | - | |

| | | | | | | | |

| Stock issued for settlement | | $ | 0 | | $ | 1,200,000 | |

| Shares of stock issued | | | - | | | 1,500,000 | |

| | | | | | | | |

| Amortization of stock issued for services | | $ | 91,413 | | $ | 0 | |

| | | | | | | | |

| Amortization of discount on notes payable | | $ | 442,573 | | $ | 0 | |

| | | | | | | | |

| Note Payable conversted for common stock | | $ | 100,000 | | $ | 0 | |

| Shares of stock issued | | | 333,333 | | | - | |

The accompanying notes are an integral part of these financial statements.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS

(UNAUDITED)

Note 1 - History and organization of the company

The Company was organized April 21, 1999 (Date of Inception) under the laws of the State of Nevada, as Alchemy Enterprises, Ltd. The Company was initially authorized to issue 25,000 shares of its no par value common stock.

On October 29, 2002, the Company amended its articles of incorporation to increase its authorized capital to 25,000,000 shares with a par value of $0.001. On January 26, 2005, the Company amended its articles of incorporation again, increasing authorized capital to 100,000,000 shares of common stock with a par value of $0.001. On March 1, 2006, the Company amended its articles of incorporation, increasing authorized capital to 300,000,000 shares of common stock, each with a par value of $0.001, and 200,000,000 shares of preferred stock, each with a par value of $0.001.

On November 26, 2006, the Company amended its articles of incorporation to change its name from Alchemy Enterprises, Ltd. to ECOtality, Inc to better reflect its renewable energy strategy.

The former business of the Company was to market a private-label biodegradable product line. During the year ended December 31, 2006, the board of directors changed the Company’s focus toward developing an electric power cell technology.

On June 11, 2007, the Company acquired the assets of the FuelCellStore.com, a small web based seller of educational fuel cell products. The FuelCellStore.com product line includes demonstration kits, educational materials, fuel cell systems and component parts. It also offers consulting services on establishing educational programs for all levels of educational institutions. FuelCellStore.com now operates as a wholly owned subsidiary call ECOtality Stores, Inc. See note 3 for further information.

On October 1, 2007, the Company purchased certain assets of Innergy Power Corporation and its wholly owned subsidiary, Portable Energy De Mexico, S.A. DE C.V. Innergy Power Corporation designs and manufactures standard and custom solar-power and integrated solar-battery solutions for government, industrial and consumer applications. See note 3 for further information.

On November 6, 2007 the Company acquired all the outstanding capital stock of Electric Transportation Engineering Corporation, as well as its affiliated company The Clarity Group (collectively referred to as eTec). eTec designs fast-charge systems for material handling and airport ground support applications. eTec also tests and develops plug-in hybrids, advanced battery systems and hydrogen ICE conversions. See note 3 for further information.

On December 6, 2007 the Company acquired through eTec the Minit-Charger business of Edison Enterprises. Minit-Charger makes products that enable fast charging of lift trucks using revolutionary technologies. See note 3 for further information.

The consolidated financial statements as of March 31, 2008 include the accounts of ECOtality, Innergy Power Corporation, eTec, and Minit-Charger. All significant inter-company balances and transactions have been eliminated. ECOtality and its subsidiaries will collectively be referred herein as the “Company”.

Note 2 - Summary of Significant Accounting Policies

Use of estimates

Preparation of financial statements in conformity with generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts of assets and liabilities and disclosures of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenue and expenses during the reporting period. Significant estimates have been used by management in conjunction with the measurement of the valuation allowance relating to deferred tax assets and future cash flows associated with long-lived assets. Actual results could differ from those estimates.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Cash and cash equivalents

For financial statement presentation purposes, the Company considers short-term, highly liquid investments with original maturities of three months or less to be cash and cash equivalents.

Interest income is credited to cash balances as earned. For the quarter ended March 31, 2008 and 2007 interest income was $8,150 and $21,743, respectively.

Credit risks

Financial instruments that potentially subject the Company to concentrations of credit risk consist principally of cash deposits. The Company maintains cash and cash equivalent balances at financial institutions that are insured by the Federal Deposit Insurance Corporation up to $100,000. Deposits with these banks may exceed the amount of insurance provided on such deposits. At March 31, 2008 and 2007, the Company had approximately $226,500 and $5,061,281 in excess of FDIC insured limits, respectively.

Impairment of long-lived assets and intangible assets

The Company follows the provisions of SFAS No. 144, “Accounting for the Impairment or Disposal of Long-Lived Assets” and SFAS No. 142, “Goodwill and other intangible assets”, which addresses financial accounting and reporting for acquired goodwill and other intangible assets. Management regularly reviews property, equipment, intangibles and other long-lived assets for possible impairment. This review occurs quarterly, or more frequently if events or changes in circumstances indicate the carrying amount of the asset may not be recoverable. If there is indication of impairment, then management prepares an estimate of future cash flows expected to result from the use of the asset and its eventual disposition. If these cash flows are less than the carrying amount of the asset, an impairment loss is recognized to write down the asset to its estimated fair value. Management believes that the accounting estimate related to impairment of its property and equipment, is a “critical accounting estimate” because: (1) it is highly susceptible to change from period to period because it requires management to estimate fair value, which is based on assumptions about cash flows and discount rates; and (2) the impact that recognizing an impairment would have on the assets reported on our balance sheet, as well as net income, could be material. Management’s assumptions about cash flows and discount rates require significant judgment because actual revenues and expenses have fluctuated in the past and are expected to continue to do so. During the quarter ended March 31, 2008 and 2007, the Company had impairment expense of $0 and $0, respectively

Revenue recognition

The Company’s revenue recognition policies are in compliance with Staff Accounting Bulletin (SAB) 104. Revenue is recognized when a formal arrangement exists, the price is fixed or determinable, all obligations have been performed pursuant to the terms of the formal arrangement and collectibility is reasonably assured. The Company recognizes revenues on product sales, based on the terms of the customer agreement. The customer agreement takes the form of either a contract or a customer purchase order and each provide information with respect to the product or service being sold and the sales price. If the customer agreement does not have specific delivery or customer acceptance terms, revenue is recognized at the time of shipment of the product to the customer.

Management periodically reviews all product returns and evaluates the need for establishing either a reserve for product returns or a product warranty liability. As of March 31, 2008 and 2007, management has concluded that no reserve is required for product returns.

We warrant to our customers that our product and services are in good working order at the time of delivery. In our acquisition of Minit-Charger, we assumed a warranty reserve in relation to warranties of products. At the time of acquisition, the warranty reserve was $231,303 and as of March 31, 2008 the warranty reserve was $217,729. Management has concluded this warranty reserve to be adequate for future expenses relating to the warranty.

Accounts receivable

Accounts receivable are carried on a gross basis, with no discounting, less the allowance for doubtful accounts. Management estimates the allowance for doubtful accounts based on existing economic conditions, the financial conditions of the customers, and the amount and the age of past due accounts. Receivables are considered past due if full payment is not received by the contractual due date. Past due accounts are generally written off against the allowance for doubtful accounts only after all collection attempts have been exhausted. There is no collateral held by the Company for accounts receivable. The allowance for doubtful accounts was $21,252 and $21,743 as of March 31, 2008 and 2007, respectively.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Inventory

Inventory is valued at the lower of cost, determined on a first-in, first-out basis, or market. Inventory includes material, labor, and factory overhead required in the production of our products. Inventory obsolescence is examined on a regular basis. The allowance for obsolescence as of March 31, 2008 was $48,000.

Advertising costs

The Company expenses all costs of advertising as incurred. There were advertising costs of $15,454 and $0 included in general and administrative expenses for the quarter ended March 31, 2008 and 2007, respectively.

Research and development costs

Research and development costs are charged to expense when incurred. For the quarter ended March 31, 2008 and 2007, research and development costs were $115,686 and $373,530, respectively.

Contingencies

The Company is not currently a party to any pending or threatened legal proceedings. Based on information currently available, management is not aware of any matters that would have a material adverse effect on the Company’s financial condition, results of operations or cash flows.

Fair Value of Financial Instruments

The carrying amounts of the Company’s financial instruments, including cash and cash equivalents, accounts receivable, accounts payable, accrued expenses and notes payable approximate their fair values based on their short-term nature. Fair value estimates discussed herein are based upon certain market assumptions and pertinent information available to management as of March 31, 2008 and 2007. The respective carrying value of certain on-balance-sheet financial instruments approximated their fair values.

Loss per Common Share

Net loss per share is provided in accordance with Statement of Financial Accounting Standards No. 128 (SFAS #128), “Earnings Per Share”. We present basic loss per share (“EPS”) and diluted EPS on the face of statements of operations. Basic EPS is computed by dividing reported losses by the weighted average shares outstanding. Except where the result would be anti-dilutive to income from continuing operations, diluted earnings per share has been computed assuming the conversion of the convertible long-term debt and the elimination of the related interest expense, and the exercise of stock warrants. Loss per common share has been computed using the weighted average number of common shares outstanding during the year. For the quarter ended March 31, 2008 and 2007, the assumed conversion of convertible long-term debt and the exercise of stock warrants are anti-dilutive due to the Company’s net loss and were excluded in determining diluted loss per share.

Foreign Currency Translation

In 2008, a Company subsidiary, Protable Energy De Mexico operated outside the United States and their local currency is their functional currency. The functional currency is translated into U.S. dollars for balance sheet accounts using the period end rates in effect as of the balance sheet date and the average exchange rate for revenue and expense accounts for each respective period. The translation adjustments are deferred as a separate component of stockholders' equity, within other comprehensive loss, net of tax where applicable.

Stock-Based Compensation

The Company records stock-based compensation in accordance with SFAS No. 123R “Share Based Payments”, using the fair value method. All transactions in which goods or services are the consideration received for the issuance of equity instruments are accounted for based on Emerging Issues Task Force Issue No. 96-18, “Accounting for Equity Instruments That Are Issued to Other Than Employees for Acquiring, or in Conjunction with Selling, Goods or Services” using the fair value of the consideration received or the fair value of the equity instrument issued, whichever is more reliably measurable.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Property and Equipment

Property and equipment are recorded at historical cost. Minor additions and renewals are expensed in the year incurred. Major additions and renewals are capitalized and depreciated over their estimated useful lives. When property and equipment are retired or otherwise disposed of, the cost and accumulated depreciation are removed from the accounts and any resulting gain or loss is included in the results of operations for the respective period. The Company uses other depreciation methods (generally accelerated) for tax purposes where appropriate. The estimated useful lives for significant property and equipment categories are as follows:

| Equipment | 5-7 years |

| Buildings | 39 years |

Income Taxes

The Company has adopted the provisions of SFAS No. 109, “Accounting for Income Taxes" which requires recognition of deferred tax liabilities and assets for the expected future tax consequences of events that have been included in the financial statements or tax returns. Under this method, deferred tax liabilities and assets are determined based on the difference between the financial statement and tax basis of assets and liabilities using enacted tax rates in effect for the year in which the differences are expected to reverse. Deferred income tax expenses or benefits are based on the changes in the asset or liability each period. If available evidence suggests that it is more likely than not that some portion or all of the deferred tax assets will not be realized, a valuation allowance is required to reduce the deferred tax assets to the amount that is more likely than not to be realized. A valuation allowance is provided for those deferred tax assets for which the related benefits will likely not be realized. Future changes in such valuation allowance are included in the provision for deferred income taxes in the period of change.

Deferred income taxes may arise from temporary differences resulting from income and expense items reported for financial accounting and tax purposes in different periods. Deferred taxes are classified as current or non-current, depending on the classification of assets and liabilities to which they relate. Deferred taxes arising from temporary differences that are not related to an asset or liability are classified as current or non-current depending on the periods in which the temporary differences are expected to reverse.

The Company adopted FASB Interpretation Number. 48, Accounting for Uncertainty in Income Taxes, as of January 1, 2007. FIN 48 clarifies the accounting for uncertainty in income taxes recognized in the companies’ financial statements in accordance with FASB Statement No. 109, Accounting for Income Taxes. As a result, the Company applies a more-likely-than-not recognition threshold for all tax uncertainties. FIN 48 only allows the recognition of those tax benefits that have a greater than fifty percent likelihood of being sustained upon examination by the taxing authorities. As a result of implementing FIN 48, the Company reviewed its tax positions and determined there were no outstanding, or retroactive tax positions with less than a fifty percent likelihood of being sustained upon examination, therefore the implementation of this standard has not had a material affect on the Company.

The Company does not anticipate any significant changes to its total unrecognized tax benefits with the next twelve months. As of March 31, 2008 and 2007, no income tax expense has been incurred.

Dividends

The Company has not yet adopted any policy regarding payment of dividends. No dividends have been paid or declared since inception. For the foreseeable future, the Company intends to retain any earnings to finance the development and expansion of its business and it does not anticipate paying any cash dividends on its common stock. Any future determination to pay dividends will be at the discretion of the Board of Directors and will be dependent upon then existing conditions, including the Company’s financial condition and results of operations, capital requirements, contractual restrictions, business prospects and other factors that the board of directors considers relevant.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Segment reporting

SFAS No. 131, “Disclosures about Segments of an Enterprise and Related Information,” requires disclosures related to components of a company for which separate financial information is available that is evaluated regularly by a company’s chief operating decision maker in deciding the allocation of resources and assessing performance. Upon completion of FuelCellStores.com, Innergy Power Corporation, Electric Transportation Engineering Corporation (eTec) and eTec’s Minit-Charger business acquisitions from June through December 2007, the Company identified its segments based on the way management expects to organize the Company to assess performance and make operating decisions regarding the allocation of resources. In accordance with the criteria in SFAS No. 131, “Disclosure about Segments of an Enterprise and Related Information,” the Company has concluded it has three reportable segments for the quarter ended March 31, 2008; ECOtality/ECOtality Stores segment, Innergy Power segment and eTec segment. The ECOtality/ECOtality Stores segment is the online marketplace for fuel cell-related products and technologies with online distribution sites in the U.S., Japan, Russia, Italy and Portugal. The Innergy Power segment is comprised of the sale of solar batteries and other solar and battery powered devices to end-users. The eTec segment relates to sale of fast-charge systems for material handling and airport ground support applications to the testing and development of plug-in hybrids, advanced battery systems and hydrogen ICE conversions and consulting revenues. This segment also includes the Minit-Charger business which relates to the research, development and testing of advanced transportation and energy systems with a focus on alternative-fuel, hybrid and electric vehicles and infrastructures. eTec holds exclusive patent rights to the eTec SuperCharge™ and Minit-Charger systems - battery fast charge systems that allow for faster charging with less heat generation and longer battery life than conventional chargers. The Company has aggregated these subsidiaries into three reportable segments: ECOtality/Fuel Cell Store, eTec and Innergy.

Management is currently assessing how it evaluates segment performance, and currently utilize income (loss) from operations, excluding share-based compensation (benefits), depreciation and intangibles amortization and income taxes. There were no inter-segment sales during the quarter ended March 31, 2008.

Recent Accounting pronouncements

In December 2004, the FASB issued Financial Accounting Standards No. 123 (revised 2004) (“FAS 123R”), Share-Based Payments, FAS 123R replaces FAS No. 123, Accounting for Stock-Based Compensation, and supersedes APB Opinion No. 25, Accounting for Stock Issued to Employees. FAS 123R requires compensation expense, measured as the fair value at the grant date, related to share-based payment transactions to be recognized in the financial statements over the period that an employee provides service in exchange for the award. FAS 123R is effective January 1, 2006. The company has adopted this accounting standard, however the implementation of this standard did not have a material impact on the Company’s financial position, results of operations or cash flows.

In November 2004, FASB issued Financial Accounting Standards No. 151, Inventory Costing, an amendment amends the guidance in ARB No. 43, Chapter 4, "Inventory Pricing," to clarify the accounting for abnormal amounts such as wasted material. This Statement requires that those items be recognized as current-period charges regardless of whether they meet the criterion of "abnormal." The implementation of this standard did not have a material impact on the Company’s financial position, results of operations or cash flows for the quarters ended March 31, 2008 and 2007.

In September of 2006, the FASB issued SFAS No. 157 “Fair Value Measurements” (SFAS No. 157). SFAS No. 157 establishes a framework for measuring fair value under generally accepted accounting procedures and expands disclosures on fair value measurements. This statement applies under previously established valuation pronouncements and does not require the changing of any fair value measurements, though it may cause some valuation procedures to change. Under SFAS No. 157, fair value is established by the price that would be received to sell the item or the amount to be paid to transfer the liability of the asset as opposed to the price to be paid for the asset or received to transfer the liability. Further, it defines fair value as a market specific valuation as opposed to an entity specific valuation, though the statement does recognize that there may be instances when the low amount of market activity for a particular item or liability may challenge an entity’s ability to establish a market amount. In the instances that the item is restricted, this pronouncement states that the owner of the asset or liability should take into consideration what affects the restriction would have if viewed from the perspective of the buyer or assumer of the liability. This statement is effective for all assets valued in financial statements for fiscal years beginning after November 15, 2007. Although SFAS No. 157 applies to and amends the provisions of existing FASB and AICPA pronouncements, it does not, of itself, require any new fair value measurements, nor does it establish valuation standards. SFAS No. 157 applies to all other accounting pronouncements requiring or permitting fair value measurements, except for: SFAS No. 123(R), share-based payment and related pronouncements, the practicability exceptions to fair value determinations allowed by various other authoritative pronouncements, and AICPA Statements of Position 97-2 and 98-9 that deal with software revenue recognition. The Company is currently evaluating the impact of SFAS No. 157 to its financial position and result of operations.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

In July 2006, the FASB issued FASB Interpretation No. 48 “Accounting for Uncertain Tax Positions” (“FIN 48”). FIN 48 clarifies the accounting for uncertainty in income taxes recognized in an enterprise’s financial statements in accordance with FASB Statement No. 109 “Accounting for Income Taxes”. It prescribes a recognition threshold and measurement attribute for the financial statement recognition and measurement of a tax position taken or expected to be taken, in a tax return. FIN 48 also provides guidance on de-recognition, classification, interest and penalties, accounting in interim periods, disclosure, and transition. FIN 48 is effective for fiscal years beginning after December 15, 2006. The implementation of this standard did not have a material impact on the Company’s financial position, results of operations or cash flows for the quarter ended March 31, 2008.

In December 2007, FASB issued Statement of Financial Accounting Standards No. 141 (revised 2007) on Business Combinations. This guidance retains the fundamental requirements in Statement 141 that the acquisition method of accounting (which Statement 141 called the purchase method) be used for all business combinations and for an acquirer to be identified for each business combination. This Statement defines the acquirer as the entity that obtains control of one or more businesses in the business combination and establishes the acquisition date as the date that the acquirer achieves control. This guidance requires an acquirer to recognize the assets acquired, the liabilities assumed, and any non-controlling interest in the acquired at the acquisition date, measured at their fair values as of that date, with limited exceptions specified in the Statement. It replaces Statement 141’s cost-allocation process, which required the cost of an acquisition to be allocated to the individual assets acquired and liabilities assumed based on their estimated fair values. For example, Statement 141 required the acquirer to include the costs incurred to effect the acquisition (acquisition- related costs) in the cost of the acquisition that was allocated to the assets acquired and the liabilities assumed. This guidance requires those costs to be recognized separately from the acquisition. In addition, in accordance with Statement 141, restructuring costs that the acquirer expected but was not obligated to incur were recognized as if they were a liability assumed at the acquisition date. This guidance requires the acquirer to recognize those costs separately from the business combination. The Company has followed the above guidance in accounting for all acquisitions that happened in 2007.

Reclassifications

Certain reclassifications have been made to the prior years’ financial statements to conform to the current year presentation. These reclassifications had no effect on previously reported results of operations or retained earnings.

Year end

The Company has adopted December 31 as its fiscal year end.

Note 3 - Acquisitions and Goodwill

FuelCellStore.com acquisition

On June 11, 2007, the Company acquired the assets of the FuelCellStore.com, a small web based seller of educational fuel cell products. The FuelCellStore.com product line includes demonstration kits, educational materials, fuel cell systems and component parts. It also offers consulting services on establishing educational programs for all levels of educational institutions. FuelCellStore.com now operates as a wholly owned subsidiary call ECOtality Stores, Inc. The acquisition has been accounted for under the purchase accounting method pursuant to SFAS 141. Our consolidated financial statements for the year ended December 31, 2007 and the quarter ended March 31, 2008 include the financial results of ECOtality Stores, Inc. subsequent to the date of the acquisition.

The fair value of the transaction was $539,000. The company paid $350,000 in cash and issued 300,000 shares of common stock, which was valued at $189,000 based on the closing market price on the date of the agreement.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Innergy Power Corporation acquisition

On October 1, 2007, the Company acquired certain assets of the Innergy Power Corporation and its wholly owned subsidiary, Portable Energy De Mexico, S.A. DE C.V. Innergy Power Corporation designs and manufactures standard and custom solar-power and integrated solar-battery solutions for government, industrial and consumer applications. The acquisition has been accounted for under the purchase accounting method pursuant to SFAS 141. Our consolidated financial statements for the year ended December 31, 2007 and the quarter ended March 31, 2008 include the financial results of Innergy Power Corporation and its subsidiary subsequent to the date of the acquisition.

The fair market value of the transaction was $3,000,000. The Company issued 3,000,000 shares of the Company’s common stock for the acquisition. The Company guaranteed to the sellers that the shares would be worth $1 each ($3,000,000) during the 30-day period commencing 11 months from the closing date. If the shares are not worth $3,000,000, the company would be required to either issue additional shares such that the total shares are worth $3,000,000 at that time or pay cash to the seller so that the aggregate value of the 3,000,000 shares plus the cash given would equal $3,000,000.

The fair value of the 3,000,000 shares of common stock given, based on the closing price of the Company’s common stock on December 31, 2007, was $555,000. A liability for the balance of $2,445,000 has been recorded as a current liability for purchase price on the consolidated balance sheet as of December 31, 2007. This liability has been reduced to reflect the value of the closing price of the Company’s common stock of March 31, 2008 and the amount of the current liability for purchase price has been updated to $2,376,000 on the consolidated balance sheet at March 31, 2008.

eTec acquisition

On November 6, 2007, the Company acquired all the outstanding capital stock of Electric Transportation Engineering Corporation, as well as its affiliated company The Clarity Group (collectively referred to as eTec). eTec designs fast-charge systems for material handling and airport ground support applications. eTec also tests and develops plug-in hybrids, advanced battery systems and hydrogen ICE conversions. The acquisition has been accounted for under the purchase accounting method pursuant to SFAS 141. Our consolidated financial statements for the year ended December 31, 2007 and the quarter ended March 31, 2008 include the financial results of eTec subsequent to the date of the acquisition.

The fair market value of the transaction was $5,037,193. The Company paid $2,500,000 in cash, issued a $500,000 note payable, and issued 6,500,000 shares of the company’s common stock for the acquisition, which was valued at $1,820,000 based on the closing market price on the date of the agreement. The total value of the transaction also includes $217,193 in direct acquisition costs.

The $500,000 is payable in monthly installments of $50,000 beginning December of 2007. The note payable balance as of March 31, 2008 was $300,000.

The aggregate purchase price was allocated to the assets acquired and liabilities assumed on their preliminary estimated fair values at the date of the acquisition. The preliminary estimate of the excess of purchase price over the fair value of net tangible assets acquired was allocated to identifiable intangible assets and goodwill. In accordance with U.S. generally accepted accounting principles, we have up to twelve months from closing of the acquisition to finalize the valuation. The purchase price allocation is preliminary, pending finalization of our valuation of certain liabilities assumed. The following table summarizes the preliminary estimate of fair value of assets as part of the acquisition with eTec:

| | | 2007 | |

| Tangible assets acquired, net of liabilities assumed | | $ | 1,941,315 | |

| Goodwill | | | 3,095,878 | |

| | | $ | 5,037,193 | |

In accordance with SFAS No. 144, “Accounting for the impairment or disposal of long lived assets”, the Company reviewed the goodwill for impairment. Due to a proven track record of cash flows generated by the assets acquired, no impairment was taken during the year ended December 31, 2007. Impairment expense relating to this acquisition was $0 for the quarter ended March 31, 2008.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Minit-Charger acquisition

On December 6, 2007 the Company acquired through eTec the Minit-Charger business of Edison Enterprises. Minit-Charger makes products that enable fast charging of lift trucks using revolutionary technologies. The acquisition has been accounted for under the purchase accounting method pursuant to SFAS 141. Our consolidated financial statements for the year ended December 31, 2007 and the quarter ended March 31, 2008 include the financial results of Minit-Charger subsequent to the date of the acquisition.

The fair market value of the transaction was $3,000,000. The company paid $1,000,000 in cash and issued 2,000,000 shares of the company’s common stock for the acquisition. The company guaranteed to the sellers that the shares would be worth $1 each ($2,000,000) by the tenth day following the first anniversary date of the transaction. If the shares are not worth $2,000,000, the company would be required to either issue additional shares such that the total shares are worth $2,000,000 at that time or pay cash to the seller so that the aggregate value of the 2,000,000 shares plus the cash given would equal $2,000,000.

The fair value of the common stock given, based on the closing price of the Company’s common stock on December 31, 2007, was $370,000. A liability for the balance of $1,630,000 based on the December 31 closing price was recorded as a current liability for purchase price on the consolidated balance sheet as of December 31, 2007. This liability has been reduced to reflect the value of the closing price of the Company’s common stock of March 31, 2008 and the amount of the current liability for purchase price has been updated to $1,584,000 on the consolidated balance sheet at March 31, 2008.

Pro forma financial statements

The unaudited pro forma consolidated statement of operations for the quarters ended March 31, 2008 and 2007 combines the historical results of ECOtality, Inc and the unaudited pro forma results of the four companies acquired during 2007 and gives effect to the acquisitions as if they occurred on January 1, 2007. Pro forma adjustments have been made related to impairment of goodwill. The pro forma consolidated results do not purport to be indicative of results that would have occurred had the acquisition been in effect for the periods presented, nor do they claim to be indicative of the results that will be obtained in the future, and do not include any adjustments for cost savings or other synergies achieved in the consolidations of the companies.

The following table contains unaudited pro forma results for the quarters ended March 31, 2008 and 2007 as if the acquisitions had occurred on January 1, 2007:

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

| | | | Quarter Ended March 31, | | | | |

| | | | 2008 | | | | | | 2007 | | | | |

| | | | Reported | | | Pro Forma | | | Reported | | | Pro Forma | |

| Net Revenues | | $ | 2,817,899 | | $ | 2,817,899 | | $ | - | | $ | 3,268,073 | |

| Net Income (loss) | | | ($1,992,211 | ) | | ($1,992,211 | ) | | ($5,747,134 | ) | | ($6,332,549 | ) |

| Net (loss) per share-basic and fully diluted | | | ($0.02 | ) | | ($0.02 | ) | | ($0.05 | ) | | ($0.06 | ) |

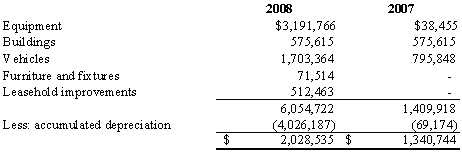

Note 4 - Fixed assets

Fixed assets as of March 31, 2008 and 2007 consisted of the following:

Depreciation expense totaled $141,886 and $48,087, for the quarters ended March 31, 2008 and 2007 respectively.

Note 5 - Notes payable

For the quarter ended March 31, 2007

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

On January 16, 2007, the Company purchased an office building for an aggregate price of $575,615. $287,959 in cash was paid and the remaining balance of $287,500 was structured as an interest-only loan. The loan bears an interest rate of 6.75% calculated annually, with monthly interest-only payments due beginning on February 16, 2007. The entire principal balance is due on or before January 16, 2012 and is recorded as a long-term note payable on the consolidated financial statements.

Interest expense totaled $3,234 for the quarter ended March 31, 2007.

As of March 31, 2007, there were no other outstanding notes payable.

For the quarter ended March 31, 2008

During 2007, the Company acquired a note payable in the acquisition of eTec. The note relates to a vehicle that was also acquired in the acquisition. As of March 31, 2008, $24,105 was owed on the note; $3,480 of which is due during 2008 with the remainder, $20,625 recorded as a long-term note payable on the consolidated financial statements.

During 2007, the Company incurred a $500,000 note payable to the previous owners of eTec through the acquisition of eTec. The loan is payable in ten monthly installments of $50,000 each. See note 3 for details. As of March 31, 2008, $300,000 was owed and recorded as long-term note payable on the consolidated financial statements.

In November and December of 2007, the Company received gross proceeds of $5,000,000 in exchange for a note payable of $5,882,356 as part of a private offering of 8% Secured Convertible Debentures (the “Debentures”). The debentures are convertible into common stock at $0.30 per share. The debentures are due beginning in May and June of 2008. 1/24th of the outstanding amount is due each month thereafter. In connection with these debentures, the Company issued debenture holders warrants (“the Warrants”) to purchase up to 9,803,925 shares of the Company’s common stock with an exercise price of $0.32. The warrants are exercisable immediately upon issue. The Warrants expire five years from the date of issue. The aggregate fair value of the Warrants equals $2,272,942 based on the Black-Scholes pricing model using the following assumptions: 3.39%-3.99% risk free rate, 162.69% volatility, strike price of $0.32, market price of $0.22-$0.32, no yield, and an expected life of 912 days. The gross proceeds received were bifurcated between the note payable and the warrants issued and a discount of $3,876,256 was recorded. The discount is being amortized over the loan term of two and one half years. As of March 31, 2008, a total of $649,844 had been amortized and recorded as interest expense and $3,226,412 remains as the unamortized discount. See note 7 for additional discussion regarding the issuance of warrants.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

The current portion of the debentures is recorded, net of a $1,291,272 discount, is $1,331,277 at March 31, 2008. The long-term portion of the debentures is recorded, net of a $1,935,140 discount, is $1,224,666 as of March 31, 2008.

Included in accrued liabilities is $114,051 of accrued interest relating to the debentures at March 31, 2008.

Interest expense totaled $562,304 for the quarter ended March 31, 2008.

Note 6 - Stockholders’ equity

There were 124,224,528 shares of common stock issued and outstanding at December 31, 2007.

During the year ended December 31, 2007, the Company issued 11,800,000 shares in four different acquisitions. See Note 3 for further information.

During the year ended December 31, 2007, the Company issued a total of 750,000 shares of common stock to employees as an incentive. The stock was valued at the current market price at the date of issue for a total of $316,000. Of this amount $91,000 was expensed and $225,000 was recorded as unamortized cost of stock issued for services to be amortized over the periods of the related agreements. During the quarter ended March 31, 2008, $56,250 has been amortized and $56,250 remains in unamortized cost of stock issued for services.

In January 2008, 175,000 shares of $0.001 common stock were issued to employees of eTec. The cost of issuance for these shares was recorded at $0.155, the close price of the stock on the date of grant and was charged to compensation expense.

In February 2008, BridgePointe Capital, one of the holders of the convertible debentures described in Note 5, converted $100,000 of debentures into 333,332 shares of $0.001 common stock at a conversion price of $0.30. This conversion was made in two equal installments, the first on February 1st, 2008 and the second on February 29th, 2008. As a result of these conversions, a reduction to the outstanding debenture balance in the amount of $100,000 and a corresponding reduction to the remaining discount on the debenture of $55,797 were recorded.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

During the year ended December 31, 2007, the Company signed an employment agreement with the CEO of the Company. The Company agreed to issue a total of 1,000,000 options for shares of common stock currently and issue another 1,000,000 options to him one year from the date of the agreement. The options issued in 2007 have a term of ten years and a strike price of $0.30. The aggregate fair value of the Warrants equals $281,300 based on the Black-Scholes pricing model using the following assumptions: 3.95% risk free rate, 162.69% volatility, strike price of $0.30, market price of $0.32, no yield, and an expected life of 5 years. This amount was recorded as unamortized cost of stock issued for services to be amortized over the two-year period of the agreement. During the quarter ended March 31, 2008, $35,163 has been amortized into expense and $222,696 remains in unamortized cost of stock issued for services. The options to be issued in 2008 were treated as earned equally over the two-year term of the agreement so that 208,334 of these options were earned as of March 31, 2008. Those options were valued using the Black-Scholes pricing model assuming 3.45% risk free rate, 179.04% volatility, strike and market price of $0.21 and were valued at $25,163. This amount was expensed during the quarter ended March 31, 2008. The remainder of the options will be expensed over the two-year term of the agreement as they are earned.

During the year ended December 31, 2007, the Company issued a total of 790,000 shares of common stock to consultants forservices. The stock was valued at the current market price at the date of issue for a total of $400,400. This amount was recorded as a prepaid expense for services to be amortized over the periods of the related agreements. During the quarter ended March 31, 2008, $47,275 has been amortized and $66,300 remains in prepaid expenses.

There were 124,732,861 shares of common stock issued and outstanding at March 31, 2008.

There is no preferred stock issued or outstanding as of March 31, 2008, or March 2007.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Note 7 - Options and Warrants

As of December, 2007, there were 8,799,982 options and warrants outstanding.

During the year ended December 31, 2007, the Company signed an employment agreement with the CEO of the Company. The Company agreed to issue a total of 1,000,000 options for shares of common stock currently and issue another 1,000,000 options to him one year from the date of the agreement. The options issued in 2007 have a term of ten years and a strike price of $0.30. The aggregate fair value of the Warrants equals $281,300 based on the Black-Scholes pricing model using the following assumptions: 3.95% risk free rate, 162.69% volatility, strike price of $0.30, market price of $0.32, no yield, and an expected life of 5 years. This amount was recorded as unamortized cost of stock issued for services to be amortized over the two-year period of the agreement. During the quarter ended March 31, 2008, $35,163 has been amortized into expense and $222,696 remains in unamortized cost of stock issued for services. The options to be issued in 2008 were treated as earned equally over the two-year term of the agreement so that 208,334 of these options were earned as of March 31, 2008. Those options were valued using the Black-Scholes pricing model assuming 3.45% risk free rate, 179.04% volatility, strike and market price of $0.21 and were valued at $25,163. This amount was expensed during the quarter ended March 31, 2008. The remainder of the options will be expensed over the two-year term of the agreement as they are earned.

As of March 31, 2008, there were 19,075,462 options and warrants outstanding.

The following is a summary of the status of the Company’s stock warrants:

| | | | Number | | | Weighted-Average | |

| | | | Of Shares | | | Exercise Price | |

| Outstanding at December 31, 2006 | | | 8,799,982 | | $ | 0.57 | |

| Granted | | | 11,753,925 | | $ | 0.31 | |

| Exercised | | | (1,478,445 | ) | $ | 0.35 | |

| Cancelled | | | 0 | | $ | 0.00 | |

| Outstanding at December 31,2007 | | | 19,075,462 | | $ | 0.42 | |

| Granted | | | 0 | | $ | 0.00 | |

| Exercised | | | 0 | | $ | 0.00 | |

| Cancelled | | | 0 | | $ | 0.00 | |

| Outstanding at March 31, 2008 | | | 19,075,462 | | $ | 0.42 | |

| | | | STOCK WARRANTS OUTSTANDING | |

| | | | | | Weighted-Average Remaining Contractual Life in Years | | | | |

$0.35 | | | 5,421,537 | | | 3.56 | | $ | 0.35 | |

$1.24 - $1.42 | | | 1,900,000 | | | 3.32 | | $ | 1.36 | |

$0.32 | | | 6,862,748 | | | 4.59 | | $ | 0.32 | |

$0.32 | | | 2,941,177 | | | 4.67 | | $ | 0.32 | |

$0.30 | | | 1,000,000 | | | 9.57 | | $ | 0.30 | |

$0.18 | | | 950,000 | | | 9.75 | | $ | 0.18(2 | ) |

| | | | 19,075,462 | | | 4.7 | | $ | 0.42 | |

| | | STOCK WARRANTS EXERCISABLE | |

| | | | | | | |

$0.35 | | | 5,421,537 | | $ | 0.35 | |

$1.24 - $1.42 | | | 1,900,000 | | $ | 1.36 | |

$0.32 | | | 6,862,748 | | $ | 0.32 | |

$0.32 | | | 2,941,177 | | $ | 0.32 | |

$0.30 | | | 1,000,000 | | $ | 0.30 | |

$0.18 | | | 950,000 | | $ | 0.18 | |

| | | | 19,075,462 | | $ | 0.42 | |

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Note 8 - Commitments and contingencies

As of March 31, 2008, the Company has seven leases in effect for operating space. Future obligations under these commitments are $161,631 for 2008, $119,400 for 2009, $109,450 for 2010, and $0 for 2011 and thereafter.

In June of 2006, the Company entered into a License Agreement with California Institute of Technology, whereby the Company obtained certain exclusive and non-exclusive intellectual property licenses pertaining to the development of an electronic fuel cell technology. The License Agreement carries an annual maintenance fee of $50,000, with the first payment due on or about June 12, 2009. The License Agreement carries a perpetual term, subject to default, infringement, expiration, revocation or unenforceability of the License Agreement and the licenses granted thereby.

Note 9 - Segment Reporting

SFAS No. 131, “Disclosures about Segments of an Enterprise and Related Information,” requires disclosures related to components of a company for which separate financial information is available that is evaluated regularly by a company’s chief operating decision maker in deciding the allocation of resources and assessing performance. Upon completion of FuelCellStores.com, Innergy Power Corporation, Electric Transportation Engineering Corporation (eTec) and eTec’s Minit-Charger business acquisitions from June through December 2007, the Company identified its segments based on the way management expects to organize the Company to assess performance and make operating decisions regarding the allocation of resources. In accordance with the criteria in SFAS No. 131, “Disclosure about Segments of an Enterprise and Related Information,” the Company has concluded it has three reportable segments for the quarter ended March 31, 2008; ECOtality/ECOtality Stores segment, Innergy Power segment and eTec segment. The ECOtality/ECOtality Stores segment is the online marketplace for fuel cell-related products and technologies with online distribution sites in the U.S., Japan, Russia, Italy and Portugal. The Innergy Power segment is comprised of the sale of solar batteries and other solar and battery powered devices to end-users. The eTec segment relates to sale of fast-charge systems for material handling and airport ground support applications to the testing and development of plug-in hybrids, advanced battery systems and hydrogen ICE conversions and consulting revenues. This segment also includes the Minit-Charger business which relates to the research, development and testing of advanced transportation and energy systems with a focus on alternative-fuel, hybrid and electric vehicles and infrastructures. eTec holds exclusive patent rights to the eTec SuperCharge™ and Minit-Charger systems - battery fast charge systems that allow for faster charging with less heat generation and longer battery life than conventional chargers. The Company has aggregated these subsidiaries into three reportable segments: ECOtality/Fuel Cell Store, eTec and Innergy.

Management is currently assessing how it evaluates segment performance, and currently utilize income (loss) from operations, excluding share-based compensation (benefits), depreciation and intangibles amortization and income taxes. There were no inter-segment sales during the quarter ended March 31, 2008.

The Company did not have separate segments for the quarter ended March 31, 2007.

ECOTALITY, INC.

NOTES TO CONDENSED CONSOLIDATED FINANCIAL STATEMENTS — (Continued)

Summarized financial information concerning the Company’s reportable segments for the quarter ended March 31, 2008 is as follows:

Quarter Ended | | | ECOtality/ | | | | | | eTec/ | | | | |

March 31, 2008 | | | Fuel Cell Store | | | Innergy | | | Minit-Charger | | | Total | |

| Total net operating revenues | | | 180,023 | | | 674,975 | | | 1,962,901 | | $ | 2,817,899 | |

| Depreciation and amortization | | | 35,494 | | | 10,284 | | | 96,108 | | | 141,886 | |

| Operating income (loss) | | | (1,352,057 | ) | | 37,207 | | | (98,187 | ) | | (1,413,038 | ) |

| Interest expense | | | (562,098 | ) | | - | | | (206 | ) | | (562,304 | ) |

| Interest income | | | 4,672 | | | 435 | | | 3,043 | | | 8,150 | |

| Loss on disposal of assets | | | - | | | - | | | (25,020 | ) | | (25,020 | ) |

| Income (loss) before income tax | | | (1,909,483 | ) | | 37,642 | | | (120,370 | ) | | (1,992,211 | ) |

| Income tax provision (benefit) | | | - | | | - | | | - | | | - | |

| Total assets | | | 4,802,388 | | | 649,958 | | | 4,627,123 | | | 10,079,469 | |

| Capital expenditures (including non-cash) | | | (694 | ) | | (7,396 | ) | | (135,187 | ) | | (143,277 | ) |

The following discussion and analysis provides information which management believes is relevant to an assessment and understanding of the Company’s results of operations and financial condition. The discussion should be read in conjunction with the Condensed Consolidated Financial Statements and the related notes thereto.

Forward-Looking Statements

This Quarterly Report contains forward-looking statements about our business, financial condition and prospects that reflect management’s assumptions and beliefs based on information currently available. We can give no assurance that the expectations indicated by such forward-looking statements will be realized. If any of our management’s assumptions should prove incorrect, or if any of the risks and uncertainties underlying such expectations should materialize, Ecotality’s actual results may differ materially from those indicated by the forward-looking statements.

The key factors that are not within our control and that may have a direct bearing on operating results include, but are not limited to, acceptance of our services, our ability to expand our customer base, managements’ ability to raise capital in the future, the retention of key employees and changes in the regulation of our industry.

There may be other risks and circumstances that management may be unable to predict. When used in this Quarterly Report, words such as, “believes,” “expects,” “intends,” “plans,” ”anticipates,” “estimates” and similar expressions are intended to identify forward-looking statements, although there may be certain forward-looking statements not accompanied by such expressions.

GENERAL

The following discussion and analysis provides information that management believes is relevant to an assessment and understanding of the Company’s results of operations and financial condition. The discussion should be read in conjunction with the Condensed Consolidated Financial Statements and the related notes thereto, contained elsewhere in this Form 10-Q.

Business Development and Summary

ECOtality, Inc. is a Nevada corporation that was incorporated in 1999. We are a renewable energy company that develops, acquires and operates companies in the clean technology sector that provide commercial solutions for today’s global energy challenges. Through strategic acquisitions, partnerships and technology innovations, we strive to advance the market applicability of clean electric technologies to become accepted alternatives to carbon-based fuel technologies. In 2007, through a number of platform acquisitions we transitioned from a development-stage company into a revenue producing company focused on providing renewable energy products and solutions.

We operate with a commercial “electro-centric” strategy, targeting only products and companies that are involved in the creation, storage, and/or delivery of clean or renewable electric power. This strategy has resulted in the development and acquisition of various operating companies and the establishment of solar, hydrogen, and energy storage divisions. We are developing a diverse technology product base that is linked through the ability to deliver comprehensive electro-centric energy alternatives and solutions for commercial customers seeking to implement greenhouse gas reduction programs (GRPs) and to prepare for the anticipated consumer and governmental moves to carbon caps and taxes. We also believe that by building a technologically diverse multi-product base we can mitigate the uncertainty of renewable energy demand and regulatory changes. With our primary focus on commercially advancing clean electro-centric technologies, we are focused on improving the world’s prevailing and most dominant energy system - electricity.

Our gross sales grew from $0 in 2006 to $2,588,658 for the year ended December 31, 2007 and $2,817,899 for the first quarter of 2008. The trailing twelve month performance of the companies acquired in 2007, coupled with the strong and quickly growing demand for clean and renewable energy technologies and products positions us to greatly expand our sales and market share in 2008 as indicated by our first quarter sales revenue amount. As most of our acquisitions occurred between October and December of 2007, our revenue amounts for 2007 reflect only the portion of sales while under our control.

The current operations of the Company consist of:

Hydrality™

Hydrality™ is our initial technology and is a complex reactor system that stores and delivers hydrogen on-demand using magnesium compounds and water. When used in conjunction with existing fuel cell technology, Hydrality emits only pure water and produces no harmful emissions. An electric power cell or fuel cell is an electrochemical device that combines hydrogen and oxygen to produce electric power without combustion.

The EPC/Hydrality technology, which was initially developed in conjunction with NASA’s Jet Propulsion Laboratory (JPL) and subsequently advanced by Arizona State University, Green Mountain Engineering and Airboss Aerospace, Inc., continues to have strong promise for a variety of commercial applications. While we initially sought to design and license a cost efficient Hydrality system for use in motorized vehicles and industrial equipment, we have identified several additional and promising applications for Hydrality that include stationary applications for remote power, back-up power systems, and large scale industrial and utility use.

We expect to derive revenue from technology license fees, technology transfer fees, fuel licensing fees and fees for the design, installation and technical support of Hydrality systems and by third parties.

Innergy Power Systems

Founded in 1989, Innergy Power Systems is a division of ECOtality, Inc. and is based in San Diego, California with a manufacturing facility in Tijuana, Mexico. Innergy is the only North American manufacturer of both renewable energy solar modules and thin-sealed rechargeable batteries, as its solar photovoltaic (PV) product line addresses the burgeoning worldwide demand for solar energy products and off-grid power. Innergy’s fiberglass reinforced panel (FRP) solar modules are designed to meet a broad range of applications for emergency preparedness and recreation, where quality, durability, rugged construction and light weight are important in the outdoor environment. Applications include logistics tracking, asset management systems, off-grid lighting, mobile communications, mobile computing, recreational vehicles, signaling devices and surveillance cameras.

Innergy and our wholly owned subsidiary, Portable Energy De Mexico, S.A. DE C.V., were acquired as platform acquisitions that provide us the ability to further expand our production and manufacturing of solar products and energy storage devices. We viewed this acquisition as the starting point of a major move to provide solar products and solutions for current and developing commercial markets. We expect that solar will become one of our four core technology groups and will contribute to our long and short-term earnings and revenue growth. Innergy is actively pursuing growth opportunities through product line expansion, joint ventures, acquisitions, and manufacturing contracts.

Electric Transportation Engineering Corporation (eTec)

Electric Transportation Engineering Corporation (eTec) was incorporated in Arizona in 1996 to support the development and installation of battery charging infrastructures for electric vehicles, and conducts research, development and testing of advanced transportation and energy systems. Specializing in alternative-fuel, hybrid and electric vehicles and infrastructures, eTec offers consulting, technical support and field services and is committed to developing and commercially advancing clean electric technologies with clear market advantages. eTec also holds exclusive patent rights for their flagship products, the eTec SuperCharge™ - battery fast-charge systems that allow for rapid charging while generating less heat and promoting longer battery life than conventional chargers. This technology was licensed to eTec from Norvic Traction in 1999. The eTec SuperCharge system is specifically designed for airport ground support equipment, neighborhood electric vehicle operations, and marine and transit systems. Since the acquisition of the technology, eTec has made considerable engineering and product advancements and is currently a leader in providing this clean electric fast charging technology to airports throughout North America.

eTec has a comparatively long history in clean and renewable technologies and has various standing contractual relationships as a test contractor and/or primary and consulting engineer for projects with the Department of Energy, several national research laboratories, national energy storage consortiums, and large electric utilities where they provide services in energy storage, monitoring, systems design and fabrication, product and vehicle testing, and product development. Their work has been in the areas of advanced battery technologies, fast charging technologies, hydrogen creation, storage and dispensing systems, electric vehicle systems, recharging stations, and coal gasification programs.

eTec was acquired as an expansion platform for its core expertise in battery technologies, fast charging systems, energy distribution infrastructure, and advanced vehicle technologies and testing, which includes electric vehicle (EV), hybrid electric vehicle (HEV), plug-in hybrid electric vehicle (PHEV) and hydrogen vehicle technologies. We believe that eTec and its subsidiaries will expand its core technologies through new product development, joint ventures, acquisitions and organic growth.

Edison MinitCharger

Edison MinitCharger was a subsidiary of Edison Source, a division of Edison International (the Southern California energy conglomerate). Edison originally acquired Norvic Traction Technology, which became Edison MinitCharger, for its unique fast charge and complex battery maintenance technologies that are primarily used in mobile material handling applications (forklifts, pallet jacks, etc.). Edison MinitCharger has been, and continues to be, one of the leaders in the mobile material handling industry. The core MinitCharger technology allows for material handling equipment to convert to electric power systems that can be charged quickly, conveniently and efficiently, thereby eliminating the need for propane or diesel-powered equipment or for backup batteries and costly change-out operations required with traditional straight-line charging. Following the initial acquisition of Norvic, Edison engineers completed many advancements of the technology and received numerous patents all of which were transferred to us in our acquisition. MinitCharger has a large customer base that consists of Fortune 500 companies and other corporate entities throughout North America.

Our acquisition of Edison MinitCharger greatly increased the size of our company and reunited the technologies and advancements that sprung from the original Norvic Traction technology: Edison’s MinitCharger and eTec’s SuperCharge products. It allows the unification of the underlying fast charging technology under a single engineering, manufacturing and sales entity and puts us in a leadership position in the rapidly growing clean technology sector of electric vehicle infrastructure technologies.

ECOtality Stores (dba Fuel Cell Store)

ECOtality Stores (dba Fuel Cell Store) is our wholly owned subsidiary and operates as our online retail division. Fuel Cell Store (www.fuelcellstore.com) is an e-commerce marketplace that offers consumers the widest array of fuel cell products from around the globe. Based in San Diego, California and with active international operations in Japan, Russia, Italy, and Portugal, Fuel Cell Store develops, manufacturers, and sells a diverse and comprehensive range of fuel cell products that includes fuel cell stacks, systems, component parts and educational materials. In addition to primary retail operations, Fuel Cell Store also offers consulting services for high schools, colleges, and leading research institutes and is available to host workshops, conferences and corporate events. Fuel Cell Store is the leading market place for fuel cell stack, component, and hydrogen storage manufacturers to unite with consumers and is an attractive source for hydrogen and fuel cell industry activity and direction.

Products

We currently offer the following products:

| | · | Energy engineering services (hydrogen, solar, battery, coal gasification, energy delivery infrastructure, etc…) |

| | · | eTec SuperCharge fast charge systems |

| | · | Minit-Charger fast charge systems |

| | · | Industrial battery systems |

| | · | Specialty solar solutions |

| | · | Specialty thin-sealed lead battery products |

| | · | Proprietary solar products for consumer, emergency response programs and remote power systems. |

| | · | Third-party hydrogen and education related products |

Customers

We have a strong base of commercial, industrial, institutional, governmental, and utility customers. As the move to renewable clean energy continues to advance, we believe that our positioning within the commercial sector gives us an advantage over companies who focus on consumer products or distribution. Our customer base includes many Fortune 500 companies, hundreds of colleges and universities, international research institutes, major electric utilities, the Department of Energy, the Department of Transportation, major industry research consortiums, vehicle manufacturers and original equipment manufacturers (OEM). By providing testing and engineering services, as well as being a product provider, we are on the cutting edge of technology and product development for the production, storage and delivery of renewable energy sources, which allows us to develop innovative product solutions for industry and government needs. Our customers use our products in industrial applications and for OEM applications.

We believe that commercial/industrial entities will be the early adopters of renewable energy technologies and products, precipitated by regulatory, financial, employee, and customer pressure. We also believe this sector will provide the most stable demand and will be less prone to overall economy or “fad” pressures. For the immediate future, we plan to focus our efforts and products on this high value added business sector.

Manufacturing

We have manufacturing facilities in Mexico operated under a Maquiladora program for the production of solar and battery products. The facility is highly labor-intensive. We have a high-value assembly operation in Phoenix, Arizona. Additionally, we have manufacturing agreements with third parties in Canada, Germany, and China.

We expect to expand our Mexican operations significantly in 2008, as well as the high-value manufacturing capability in Arizona. We are currently planning for new leased facilities in Mexico to handle our anticipated growth. Part of our anticipated growth plan would include more mechanized production systems, inclusive of International Organization for Standardization (ISO) quality and environmental certifications. We believe that our existing plant in Arizona has sufficient room for anticipated growth.

Research and Development

We devoted a large percentage of our 2007 research and development expenditures to the Hydrality project. This expenditure was with third-party technology and engineering partners such as NASA’s Jet Propulsion Laboratories (JPL) and others. We have determined that we will rationalize and capacitate our technology research and development expenditures at levels in-line with traditional operating technology companies based upon a reasonable percentage of revenues. Given the proven and commercially viable clean technology companies we acquired in 2007 and anticipate adding in 2008, we have determined we are well positioned with our strategy to grow through a combination of organic growth of existing operations and potential acquisitions of other mid-stage companies that are congruous with our clean electro-centric strategy.

We have determined that the vagaries of the hydrogen industry, the advancement of other renewable technologies to the commercial forefront, and the potentially long and expensive road to commercialization and profitability for hydrogen technologies necessitate that we prudently and significantly scale back our hydrogen research and development expenditures, and proceed only on the basis of joint development projects with third-parties or significantly subsidized development with potential licensees or federal grants.

Sales and Marketing