William E. Cooper

Attorney at Law

9630 Clayton Road

Saint Louis, Missouri 63124

314-581-4091 bcooper@alliedcos.com

November 29, 2013

Mr. John Reynolds

Assistant Director

Office of Beverages, Apparel and Mining

United States Securities and Exchange Commission

Division of Corporation Finance

Washington, D.C. 20549

| Re: | Rush Exploration Inc. Form 20-F for the Fiscal Year Ended December 31, 2012 Filed April 25, 2013 Comment Letter dated October 31, 2013 File No. 000-51337 |

Dear Mr. Reynolds:

As counsel for Rush Exploration Inc. (“Rush” or the “Company”), I have been asked to review your comments to the Form 20-F for the fiscal year ended January 31, 2013. We appreciate your review to assist and enhance the overall disclosure in our Exchange Act Filings. This letter sets forth the responses of the Company to the comments of the Staff of the Division of Corporation Finance of the Securities and Exchange Commission (“SEC”) dated October 31, 2013 with respect to the above referenced Form 20-F filing. The references to the comment letter have been shown in bold face for convenience, and the Company’s responses are set forth below the reference.

Please note all responses are outlined herein for convenience of the Staff, however upon approval, an amendment to Form 20-F for the Fiscal Year Ended December 31, 2012 will be filed to include updated disclosure contained herein.

FORM 20-F FOR THE YEAR ENDED DECEMBER 31, 2013

Comment:

Risk Factors, page 7

| 1. | Please disclose whether your sole officer and director has visited your claims, and if so, when and for how long. If he has not visited your claims, please add related risk factor disclosure. |

Mr. John Reynolds

United States Securities and Exchange Commission

Page 2

Response:

The Company respectfully directs the Staff to Risk Factors, Page 8 of the Form 20-F, specifically:

"3.Our properties have not been examined by a professional geologist or mining engineer and we have no known mineral reserves on any of our properties.Without mineral reserves we cannot generate income, and if we cannot generate income we will have to cease operations.

Without mineral reserves, we have nothing to economically remove. If we have nothing to economically remove from our property, we cannot generate income and in such a situation, we will have to cease operations which may result in the loss of an investment."

Acquisition of Interest, page 16

Comment:

| 2. | Please file as an exhibit, the agreements through which you acquired ownership or control of your mineral claims. Refer to Item 601(b)((10) of Regulation S-K |

Response:

The Company respectfully confirms to the Staff that in accordance with Item 601(b)(10)(ii)(A) and (B) of Regulation S-K, the annual report will be amended to include the May 26, 2012 Property Option Agreement (the "Agreement") by and between Rush Exploration Inc. and Knight Resources as an Exhibit.

Comment:

| 3. | We note you acquired your mining claims from Knight Resources. However the owners of the mining claims are listed as Horizon Exploration Inc. Please explain the relationship, if any, between these two companies and your property. |

Response:

The Company respectfully submits to the Staff that Knight Resources has represented that it has beneficial ownership and authority over the claims interest. Rush Exploration Inc. has no relationship with Horizon Exploration Inc. and is not privy to any relationship, if any, between Knight Resources and Horizon Exploration Inc.

Comment:

Description and Location of the Mudersbach Property, page 17

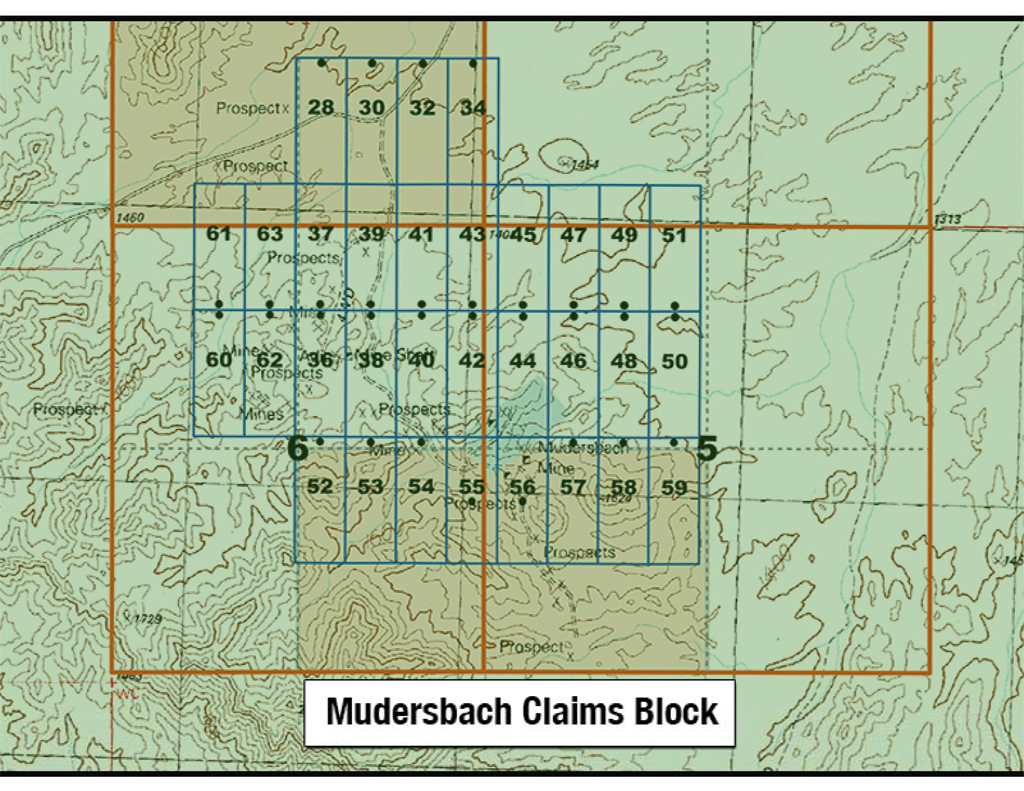

| 4. | We note your Mudersbach property consists of 32 unpatented mining claims and these claims cover a total acreage of 688 acres. We understand that the maximum acreage of a mining claim is 20.66 acres. Please explain this variance and modify your filing. |

Mr. John Reynolds

United States Securities and Exchange Commission

Page 3

Response:

The Company respectfully acknowledges that a clerical error existed in the Form 20-F wherein the total acreage of the mining claims was reflected as 688 acres and should have been reflected as approximately 639 acres. The mining claims PLO 34 AMC 411337, PLO 43 AMC 411346, PLO 45 AMC 411348, PLO 47 AMC 411350, PLO 49 AMC 411352 and PLO 51 AMC 411354 have a northern boundary which terminates on adjacent state land. Please see Mudersbach Claim Block Map attached hereto as Exhibit A. The Company does not have any surface or mineral rights on state property. The 20-F will be amended to reflect the attached map, amended acreage and notation regarding the 6 mineral claims for which the northern claim boundary is limited by the state lands.

Comment:

| 5. | Please disclose the following information for each of your properties: |

| · | Describe the process by which mineral rights are acquired at this location and the basis and duration of your mineral rights, surface rights, mining claims or concessions. |

Response:

The Company respectfully directs the Staff's attention to Page16 of the Form 20-F, specifically:

"Effective May 26, 2012, Rush Exploration Inc. (the “Company”) executed a Property Option Agreement (the “Agreement”), with Knight Resources (the “Optionor”) granting the Company the exclusive option to an undivided right, title and interest in the Mudersbach Property located in the Plomosa Mountain Range, La Paz County, Arizona (the “Property”). Simultaneous with the execution and delivery of the Agreement, the Company issued Fifty Million (50,000,000) Shares of its fully paid and non-assessable Restricted Common Stock"

If the Company performs its obligations as specified in the Agreement, it will retain control of the mineral rights. Further to the aforementioned, the mineral rights consist of unpatented federal land claims administered and regulated by the Bureau of Land Management (the “BLM”) under the Federal Land Policy and Management Act of 1976. These mineral rights will continue in perpetuity providing the applicable annual maintenance and filing fees are paid as required.

Comment:

| · | Please include certain identifying information, such as the property names, claim numbers, grant numbers, mining concession name or number, and dates of recording and expiration that is sufficient to enable the claims to be distinguished from other claims that may exist in the area of your properties. |

Response:

The Company respectfully acknowledges to the Staff that the Form 20-F will be amended to reflect the following identifying information for its mineral claims:

List of unpatented claims located in Sections 5, 6, 31, 32 of TS/6N, R17W G&SR B&M, La Paz County, Arizona

Mr. John Reynolds

United States Securities and Exchange Commission

Page 4

CLAIM NAME

PL028 | AMC NUMBER

411331 |

PL030 PL032 PL034 | 411333 41 I 33S 411337 |

| PL036 | 411339 |

| PL037 | 411340 |

| PL038 | 411341 |

| PL039 | 411342 |

| PL040 | 4II343 |

| PL041 | 411344 |

| PL042 | 41134S |

| PL043 | 411346 |

| PL044 | 411347 |

| PL045 | 411348 |

| PL046 | 411349 |

| PL047 | 4113SO |

| PL048 | 4113S1 |

| PL049 | 4113S2 |

| PLOSO | 4113S3 |

| PLOS1 | 4113S4 |

| PLOS2 | 413312 |

| PLOS3 | 413313 |

| PLOS4 | 413314 |

| PLOSS | 41331S |

| PLOS6 | 413316 |

| PLOS7 | 413317 |

| PLOSS | 413318 |

| PLOS9 | 413319 |

| PL060 | 413320 |

| PL061 | 413321 |

| PL062 | 413322 |

| PL063 | 413323 |

The claims were recorded on October 12, 2011. If annual maintenance fees and filing fees are paid as required, the claims may continue in perpetuity.

Comment:

| · | The conditions that must be met to retain your claims or leases, including quantification and timing of all necessary payments, annual maintenance fees, and disclose who is responsible for paying these fees. |

Response:

The Company respectfully submits the conditions to retain the mineral claims are specified in the Agreement. Further, the Company respectfully directs the Staff's attention to Page 17 of the Form 20-F, specifically:

Mr. John Reynolds

United States Securities and Exchange Commission

Page 5

"In order to earn a 100% interest in the Property, the Company must pay the Optionor and incur expenditures relating to exploration and mining operations in accordance with the following schedule: (i) on or before May 26, 2013, $20,000 CDN to Optionor and incur $100,000 CDN in expenditures incidental to the exploration and mining operations; (ii) on or before May 26, 2014, $20,000 to Optionor and an additional $100,000 in expenditures; (iii) on or before May 26, 2015, $40,000 to Optionor and an additional $200,000 in expenditures; (iv) on or before May 26, 2016, $60,000 to Optionor and an additional $300,000 in expenditures; and (v) on or before May 26, 2017, $60,000 to Optionor and incur an additional $300,000 in expenditures. Since our payment obligations are non-refundable, if we do not make all required payments, we will lose all payments made and our rights to the properties. If all said payments are made, then we will acquire all mining interests in the property subject to a 3% net smelter royalty. The Optionor retains a 3% royalty of the aggregate proceeds received by the Company from any smelter or other purchaser of any ores, concentrates, metals or other material of commercial value produced from the property, minus the cost of transportation of the ores, concentrates or metals, including related insurance, and smelting and refining charges, including penalties.

Both the Company and Optionor have the right to assign, sell, mortgage or pledge their rights in the Agreement or on the Property."

Further to the aforementioned, the Company respectfully acknowledges to the Staff that the Form 20-F will be amended to reflect the following information regarding the filing and payment of all maintenance/filing fees for the mining claims:

"Pursuant to the Agreement, the Optionor will keep the Property in good standing, free and clear of all liens and encumbrances during the Option period, subject to the Company performing its obligations. The Optionor is required to pay the annual maintenance and filing fees which include $140 per claim to be paid to the Bureau of Land Management (“BLM”) and recording fees of approximately $15 per claim to be paid to the respective county on or before September 1 of each year."

Comment:

| · | The area of your claims, either in hectares or in acres. |

Response:

The Company respectfully directs the Staff's attention to Page 17 of the Form 20-F, specifically:

"The 688 acre Mudersbach property consists of 32 unpatented mining claims in the Plomosa Mountain range in the northwest area of the State of Arizona, located at the historical Mudersbach Mine Camp (the "Mudersbach Property")."

Furthermore, please be advised the reference to “688 acre Mudersbach property consists of...” will be amended to read "639 acre Mudersbach property consists of..." Please refer to the Company's response to Comment 4 of this letter.

Mr. John Reynolds

United States Securities and Exchange Commission

Page 6

Comment:

| 6. | Please disclose the information required under paragraph (b) of Industry Guide 7 for all your material properties. For any properties identified that are not material, please include a statement to that effect, clarifying your intentions. For each material property, include the following information: |

| · | The location and means of access to your property, including the modes of transportation utilized to and from the property. |

Response:

At the time of filing the Annual Report, the Company had acquired the mineral rights to the Mudersbach Property. The Company respectfully acknowledges to the Staff that the Form 20-F will be amended to reflect the following regarding the location and means of access to and from the Property:

The Property is easily accessed via Plomosa Road and lies approximately 12 miles northeast of the town of Quartzite, Arizona and approximately 9 miles southwest of Bouse, Arizona. The gravel inroads which provide access to the property area are accessible with a 4 wheel drive vehicle. Certain areas may require an off road ATV or on foot access depending on the specific terrain.

Comment:

| · | Any conditions that must be met in order to obtain or retain title to the property, whether you have surface and/or mineral rights. |

Response:

The Company respectfully directs the Staff's attention to Page 17 of the Form 20-F for the conditions that must be met in order for the Company to obtain or retain title to the property, specifically:

" In order to earn a 100% interest in the Property, the Company must pay the Optionor and incur expenditures relating to exploration and mining operations in accordance with the following schedule: (i) on or before May 26, 2013, $20,000 CDN to Optionor and incur $100,000 CDN in expenditures incidental to the exploration and mining operations; (ii) on or before May 26, 2014, $20,000 to Optionor and an additional $100,000 in expenditures; (iii) on or before May 26, 2015, $40,000 to Optionor and an additional $200,000 in expenditures; (iv) on or before May 26, 2016, $60,000 to Optionor and an additional $300,000 in expenditures; and (v) on or before May 26, 2017, $60,000 to Optionor and incur an additional $300,000 in expenditures. Since our payment obligations are non-refundable, if we do not make all required payments, we will lose all payments made and our rights to the properties. If all said payments are made, then we will acquire all mining interests in the property subject to a 3% net smelter royalty. The Optionor retains a 3% royalty of the aggregate proceeds received by the Company from any smelter or other purchaser of any ores, concentrates, metals or other material of commercial value produced from the property, minus the cost of transportation of the ores, concentrates or metals, including related insurance, and smelting and refining charges, including penalties.

Mr. John Reynolds

United States Securities and Exchange Commission

Page 7

Both the Company and Optionor have the right to assign, sell, mortgage or pledge their rights in the Agreement or on the property."

The Company respectfully acknowledges to the Staff that the Form 20-F will be amended to reflect the following additional information regarding the conditions that must be met in order to obtain or retain title to the property and whether we have surface and/or mineral rights.

The Property claims are held as unpatented federal land claims administered under the Department of Interior, Bureau of Land Management under the Federal Land Policy and Management Act of 1976. In order to acquire an unpatented mineral claim the land must be open to mineral entry. Federal law specifies that a claim must be located or “staked” and site boundaries be distinctly and clearly marked to be readily identifiable on the ground in addition to filing the appropriate state and or federal documentation such as Location Notice, Claim Map, Notice of Non-liability for Labor and Materials Furnished, Notice of Intent to Hold Mining Claims, Maintenance Fee Payment and fees to secure the claim. The State may also establish additional requirements regarding the manner in which mining claims and sites are located and recorded. An unpatented mining claim on U.S. government lands establishes a claim to the locatable minerals (also referred to as stakeable minerals) on the land and the right of possession solely for mining purposes. No title to the land passes to the claimant. If a proven economic mineral deposit is developed, provisions of federal mining laws permit owners of unpatented mining claims to patent (to obtain title to) the claim.

The general administrative process by which the Company maintains control of its Property is to keep the Property Option Agreement in good standing in accordance with the terms of the Agreement. Upon satisfying the obligations in the Agreement, the Company will acquire a 100% right, title and interest in the Property subject to a 3% net smelter royalty with duration in perpetuity.

Required annual maintenance and filing fees include $140 per claim to be paid to the Bureau of Land Management (“BLM”) and recording fees of approximately $15 per claim to be paid to the respective county.

None of the Property claims have been legally surveyed. Although our legal access to unpatented Federal claims cannot be denied, staking or operating a mining claim does not provide the claim holder exclusive rights to the surface resources (unless a right was determined under Public Law 84-167) establish residency or block access to other users. Regulations managing the use and occupancy of the public lands for development of locatable mineral deposits by limiting such use or occupancy to that which is reasonably incident is found in 43 CFR 3715. These Regulations apply to public lands administered by BLM.

The Property interests in the Agreement are mineral rights.

Comment:

| · | A brief description of the rock formations and mineralization of existing or potential economic significance on the property. |

Mr. John Reynolds

United States Securities and Exchange Commission

Page 8

Response:

The Company has recently acquired the property option and is in the process of determining whether there is a potential to host economically viable mineralization. The Company respectfully directs the Staff's attention to Page 18, 15, and 17 of the Form 20-F as further outlined consecutively below:

"We recognize this property is a grass roots exploration opportunity. The Company’s objectives are to assess its geological merits to establish an exploration program to identify the potential for economically viable mineralization."

“No commercially viable mineral deposits may exist on our properties. Our plan of operations is to carry out geological analysis of our properties in order to ascertain whether they possess economically viable mineral deposits. We can provide no assurance to investors that our properties contain commercially viable deposits until appropriate exploratory work is done and an evaluation based on that work concludes further work programs are justified. At this time, we definitely have no known reserves on our properties.”

“This region's Lode and Placer gold has been heavily sought after since the 18th century, and based on historical records and data from former claim holders, the Company believes this property has the potential to host a commercial gold find”.

Further, the Company respectfully acknowledges to the Staff that the Form 20-F will be amended to reflect the following additional information regarding a description of the rock formations and mineralization of potential economic significance on the property.

The Property is part of the Plomosa Mining District and is located within the Basin and Range Geomorphologic Province, which comprises the southwestern third of the State of Arizona. The region is characterized by linear mountain ranges separated by down thrown, alluvium-filled basins. In southern Arizona, a "belt" of Precambrian metamorphic rocks (“core complex") ranges forms a transition zone between the younger, predominantly volcanic desert mountains of the south and the folded and faulted highlands of central Arizona. The Plomosa Mountains rise up just west of the Bouse Hills to the north and extend for tens of miles southward. The Plomosa Mountains form the eastern wall of the La Posa Plain and the western front-range to the Ranegras Plains for nearly its entire length. The northern half of the Plomosa Mountains is predominantly composed of Mesozoic sandstone, shale, conglomerate and limestone. Slightly younger Cretaceous to early-Tertiary sediments crop out along the northernmost point of the range and small outcrops of ancient Precambrian gneiss also occur in the area. Mesozoic-age intrusive rocks, chiefly granites, intrude the pre-Tertiary rocks and is believed

to be the source for much of the gold in the Plomosa Mountains.

A former surface and underground Cu-Fe-Ag-Au-Gypsum mine known as the Mudersbach Mine is located within the Property boundary. Past exploration has presented that the mineralization is a replacement deposit with ore in irregular and pocketry distribution copper, and iron sulfides are in a pyrometasomatic deposit, oxidized near the surface, with a garnet-epidote gangue and strong hematitic-copper carbonate gossan. The irregular deposit is in faulted and deformed metamorphosed Mesozoic limestone interbedded with schist and intruded by quartz monzonite.

Workings are relatively shallow with 2 shallow shafts, tunnels, and open cuts. This mine was worked intermittently from the early 1900's through 1930. It produced some 700 tons of ore averaging about 4.4% Cu, 0.67 oz. Ag/T, and 0.03 oz. Au/T. One carload of ore has been shipped, which the owner reported averaged 10.4% Cu and $1.00 in Au per ton (period values)(owner's identification and timeframe not specified).

Mr. John Reynolds

United States Securities and Exchange Commission

Page 9

Comment:

| · | A description of any work completed on the property and its present condition. |

| · | The details as to modernization and physical condition of the plant and equipment, including subsurface improvements and equipment. |

| · | A description of equipment, infrastructure, and other facilities. |

| · | The current state of exploration of the property. |

| · | The total costs incurred to date and all planned future costs. |

Response:

The Company respectfully acknowledges to the Staff that the Form 20-F will be amended to reflect the following:

The Property is a recent acquisition and hence the Company has not developed any exploration proposals nor completed any work, improvement or expenditure on the Property. There is currently no plant, equipment, infrastructure or other facilities on site.

Further, the Company respectfully directs the Staff to Page 18 of the Form 20-F for an estimate of planned future costs, specifically:

"We anticipate that we will incur through the end of our next fiscal year in connection with our current exploration plan for 2013:

| • | $100,000 in connection with exploration expenditures |

| • | $20,000 for property option payments for the Mudersbach Property." |

Comment:

| · | The source of power and water that can be utilized at the property. |

Response:

The Company respectfully submits to the Staff that there is currently no source of power and water on site. Power could be provided by portable diesel-powered generators. Non potable water may be sourceable on site for drilling, mining and milling purposes.

Comment:

| · | If applicable, provide a clear statement that the property is without known reserves and the proposed program is exploratory in nature. |

Mr. John Reynolds

United States Securities and Exchange Commission

Page 10

Response:

The Company respectfully directs the Staff to Risk Factors, Page 8 of the Form 20-F, specifically:

"3. Our properties have not been examined by a professional geologist or mining engineer and we have no known mineral reserves on any of our properties. Without mineral reserves we cannot generate income, and if we cannot generate income we will have to cease operations.Without mineral reserves, we have nothing to economically remove. If we have nothing to economically remove from our property, we cannot generate income and in such a situation, we will have to cease operations which may result in the loss of an investment."

The Company respectfully submits to the Staff that the amended 20-F will reflect the statement that any proposed work program is exploratory in nature.

Comment:

| 7. | On a related point, it appears you should also expand your disclosure concerning the exploration plans for the properties to address the following points: |

| · | Disclose a brief geological justification for each of the exploration projects written in non-technical language. |

| · | Give a breakdown of the exploration timetable and budget, including estimated amounts that will be required for each exploration activity, such as geophysics, geochemistry, surface sampling, drilling, etc. for each prospect. |

| · | If there is a phased program planned, briefly outline all phases. |

| · | If there are no current detailed plans to conduct exploration on the property, disclose this prominently. |

Response:

The Company respectfully submits to the Staff that there are currently no detailed plans to conduct exploration on this recently acquired property.

Comment:

| · | Disclose how the exploration program will be funded. |

Response:

The Company respectfully directs the Staff's attention to Page 21 of the Form 20-F as further outlined below.

"We shall require additional funding and we anticipate that such funding will be in the form of equity financing from the sale of our common stock."

Mr. John Reynolds

United States Securities and Exchange Commission

Page 11

Comment:

| · | Identify who will be conducting any proposed exploration work, and discuss what their qualifications are. |

Response:

The Company respectfully submits that the Mudersbach Property has been recently acquired and therefore we are not at the stage to discuss any proposed exploration work.

Comment:

| 8. | We recommend that a brief description of the QA/QC protocols be provided to inform investors regarding sample preparation, controls, custody, assay precision and accuracy as it relates to your exploration plans. This would apply to exploration and operational analytical procedures. |

Response:

The Company respectfully submits that the Mudersbach Property has been recently acquired and therefore we are not at the stage to provide further disclosure related to QA/QC protocols.

Comment:

| 9. | Detailed sampling provides the basis for the quality estimate or grade of your mineral discovery. Please provide a brief description of your sample collection, sample preparation, and the analytical procedures used to develop your analytical results. In addition, please disclose any Quality Assurance/Quality Control (QA/QC) protocols you have developed for your exploration program. These procedures would serve to inform potential investors regarding your sample collection and preparation, assay controls, sample custody, assay precision and accuracy procedures and protocols. |

Response:

The Company respectfully submits that the Mudersbach Property has been recently acquired and therefore we are not at the stage to provide further disclosure related to QA/QC protocols.

Comment:

| 10. | In the description of each exploration property, please provide a clear statement that the property is without known reserves and the proposed program is exploratory in nature to comply with the guidance in paragraph (b) (4) (i) of Industry Guide 7, applicable under the instructions to Item 4 of Form 20-F. |

Mr. John Reynolds

United States Securities and Exchange Commission

Page 12

Response:

The Company respectfully submits to the Staff that Item 4 of the Form 20-F will be amended to include:

"The Mudersbach Property is without known reserves and a proposed program, if any, will be exploratory in nature."

Comment:

| 11. | We note you are subject to permitting requirements of the Bureau of Land Management Detailed sampling provides the basis for the quality estimate or grade of your mineral discovery. Please provide a brief description of your sample collection, sample preparation, and the analytical procedures used to develop your analytical results. In addition, please disclose any Quality Assurance/Quality Control (QA/QC) protocols you have developed for your exploration program. These procedures would serve to inform potential investors regarding your sample collection and preparation, assay controls, sample custody, assay precision and accuracy procedures and protocols. |

Response:

The Company respectfully submits that the Mudersbach Property has been recently acquired and therefore we are not at the stage to provide further disclosure related to QA/QC protocols.

Closing Comments

Please see Exhibit B acknowledging that:

| · | the Company is responsible for the adequacy and accuracy of the disclosure in the filing; |

| · | staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| · | the Company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

Yours truly,

/s/ William E. Cooper

William E. Cooper

Mr. John Reynolds

United States Securities and Exchange Commission

Page 13

EXHIBIT A

Mr. John Reynolds

United States Securities and Exchange Commission

Page 14

EXHIBIT B

Rush Exploration Inc. respectfully acknowledges the following:

| · | the company is responsible for the adequacy and accuracy of the disclosure in the filing; |

| · | staff comments or changes to disclosure in response to staff comments do not foreclose the Commission from taking any action with respect to the filing; and |

| · | the company may not assert staff comments as a defense in any proceeding initiated by the Commission or any person under the federal securities laws of the United States. |

Very truly yours,

/s/ Kenneth Williams

Kenneth Williams

President