Exhibit 99.(a)(5)(xi)

| EFiled: Aug 13 2010 4:50PM EDT |

| Transaction ID 32664521 |

| Case No. 5720- |

| [SEAL] |

IN THE COURT OF CHANCERY IN THE STATE OF DELAWARE

KYLE HABINIAK, Individually and on Behalf | ) |

|

of All Others Similarly Situated, | ) |

|

| ) |

|

Plaintiff, | ) |

|

| ) |

|

v. | ) | Civil Action No. |

| ) |

|

HOWARD S. COHEN, RICHARD S. | ) |

|

GRANT, GEORGE R. JUDD, CHARLES H. | ) |

|

MCELREA, RICHARD B. MARCHESE, | ) |

|

STEVEN F. MAYER, ALAN H. | ) |

|

SCHUMACHER, MARK A. SUWYN, | ) |

|

ROBERT G. WARDEN, RICHARD | ) |

|

WARNER, BLUELINX HOLDINGS INC., | ) |

|

CERBERUS ABP INVESTOR LLC, and | ) |

|

CERBERUS CAPITAL MANAGEMENT, | ) |

|

L.P. | ) |

|

| ) |

|

Defendants. | ) |

|

VERIFIED COMPLAINT

Plaintiff Kyle Habiniak (“Plaintiff”), individually and as a class action on behalf of all others similarly situated, alleges upon knowledge as to Plaintiff’s own acts and upon information and belief as to all other matters, as follows:

SUMMARY OF THE ACTION

1. This is a stockholder class action brought by Plaintiff on Plaintiff’s behalf and on behalf of the public shareholders of BlueLinx Holdings, Inc. (“BlueLinx” or the “Company”) against BlueLinx, the Board of Directors of BlueLinx, BlueLinx’s controlling shareholder Cerberus ABP Investor LLC (“CAI”), and Cerberus Capital Management, L.P. (“Cerberus”), which controls CAI. CAI owns 55.39% of the outstanding common stock of BlueLinx, and has made a tender offer to BlueLinx to acquire the balance of BlueLinx’s common stock for $3.40 per share, to be followed by a back-end merger at the same price (the “Proposed Transaction”).

2. The tender offer is fundamentally inadequate and is an attempt by CAI and Cerberus to squeeze out BlueLinx’s shareholders upon a downturn in BlueLinx’s share price. BlueLinx has experienced recent trading prices nearly double the $3.40 per share offer,.

3. CAI and Cerberus control BlueLinx’s Board of Directors. BlueLinx’s Board Chairman, Howard S. Cohen (“Cohen”) was a senior advisor to Cerberus. Director Steven F. Mayer (“Mayer”) is a managing director of Cerberus, director Mark A. Suwyn (“Suwyn”) has acted as a senior member of Cerberus’ operations team and as an advisor to Cerberus, director Robert G. Warden (“Warden”) is a managing director of Cerberus, and director Richard Warner (“Warner”) is a consultant for Cerberus. Given Cerberus’ control of CAI, it is not surprising that the special committee created by the Board was apparently not granted the authority to defend against the Proposed Transaction or seek alternatives to it.

4. Moreover, Cerberus and CAI have failed to provide all material information to BlueLinx’s shareholders in connection with the tender offer. On or about August 2, 2010, the Cerberus and CAI commenced the tender offer and filed a Schedule TO document with the U.S. Securities and Exchange Commission (“SEC”). This filing fails to provide BlueLinx shareholder with basic material information, including but not limited to why the $3.40 per share offer is fair to BlueLinx shareholders. Without this information, BlueLinx shareholders are unable to make intelligent, rational, and informed decisions about whether to tender their shares.

5. The tender offer is set to expire on August 27, 2010. In the absence of equitable relief, the Proposed Transaction will go forward on inadequate terms through a coercive process that is designed to ensure the sale of BlueLinx to CAI on terms preferential to CAI that subvert the interests of the public stockholders of BlueLinx.

PARTIES

6. Plaintiff is, and has been at all times relevant hereto, a BlueLinx shareholder.

7. Defendant BlueLinx is a Delaware corporation with its principal place of business located at 4300 Wildwood Parkway, Atlanta, Georgia. According to the Company’s May 7, 2010 quarterly report filed with the SEC, there were over 32 million shares of BlueLinx’s common stock outstanding. BlueLinx is publicly traded on the New York Stock Exchange under the ticker “BXC.”

8. Defendant Cohen is, and has been at all times relevant hereto, a member of the Company’s Board. Defendant Cohen is Board Chairman.

9. Defendant Richard S. Grant (“Grant”) is, and has been at all times relevant hereto, a member of the Company’s Board.

10. Defendant George R. Judd (“Judd”) is, and has been at all times relevant hereto, a member of the Company’s Board.

11. Defendant Charles H. McElrea (“McElrea”) is, and has been at all times relevant hereto, a member of the Company’s Board.

12. Defendant Richard B. Marchese (“Marchese”) is, and has been at all times relevant hereto, a member of the Company’s Board.

13. Defendant Mayer is, and has been at all times relevant hereto, a member of the Company’s Board.

14. Defendant Alan H Schumacher (“Schumacher”) is, and has been at all times relevant hereto, a member of the Company’s Board.

15. Defendant Suwyn is, and has been at all times relevant hereto, a member of the Company’s Board.

16. Defendant Warden is, and has been at all times relevant hereto, a member of the Company��s Board.

17. Defendant Warner is, and has been at all times relevant hereto, a member of the Company’s Board.

18. The Defendants listed in paragraphs 10 through 19 are collectively referred to as the “Individual Defendants.”

19. Defendant CAI is BlueLinx’s controlling shareholder, which is itself controlled by Cerberus.

20. Defendant Cerberus is one of the world’s largest private investment firms.

FACTUAL ALLEGATIONS

21. BlueLinx is a distributor of building products in the United States. The Company operates in all of the metropolitan areas in the United States. As of January 2, 2010, BlueLinx distributed more than 10,000 products to approximately 11,500 customers through its network of more than 70 warehouses and third-party operated warehouses. The Company distributes products in two categories: structural products and specialty products. BlueLinx’s customers include building materials dealers, industrial users of building products, manufactured housing builders and home improvement centers. BlueLinx purchases products from over 750 vendors and serve as a national distributor for a number of its suppliers.

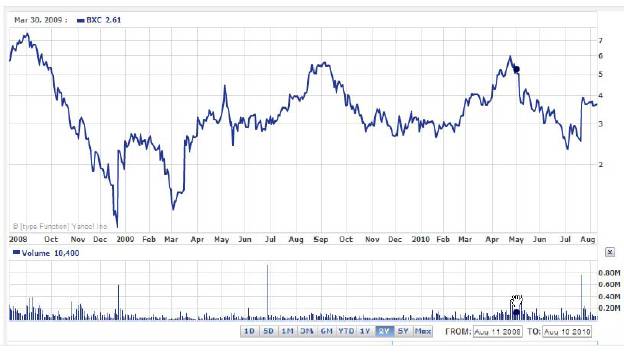

22. BlueLinx has historically performed well for its shareholders, trading at a peak of $7.21 per share before the recent economic recession.

23. Despite recent difficulties caused by the global recession and a recent decline in stock prices, the long-term prospects for BlueLinx’s services and finances are favorable. For example, analysts estimate a 110% growth rate for fiscal year 2011.(1)

24. This Company’s potential is further bolstered by the first quarter 2010 results. In a May 6, 2010 release, the Company stated:

Revenues increased 6% to $431.1 million from $407.1 million for the same period a year ago. Overall unit volume rose 1.4% compared to the year-ago period.

Gross profit for the first quarter totaled $52.3 million, up 18% from $44.3 million in the prior-year period. Gross margins increased to 12.1% from the 10.9% generated in the year earlier period. The improvement in margins was due to the Company’s continued focus on margin improvement, wood-based product pricing and an increase in sales through the warehouse channel.

(1) http://moneycentral.msn.com/investor/invsub/analyst/earnest.asp?Page=EarningsGrowthRate s&Symbol=BXC (last visited July 22, 2010).

25. The Company’s second quarter 2010 results were just as promising, as the Company stated:

ATLANTA, Aug. 5, 2010 (GLOBE NEWSWIRE) — BlueLinx Holdings Inc. (NYSE:BXC), a leading distributor of building products in North America, today reported financial results for the second quarter ended July 3, 2010.

Revenues increased 27.7% to $540.8 million from $423.5 million for the same period a year ago. The increase reflects a 45.1% increase in structural product sales and a 14.4% increase in specialty product sales. Overall unit volume rose 11.9% compared to the year-ago period. The Company incurred a net loss of $3.4 million, or $0.11 per diluted share for the second quarter of 2010, compared with net profit of $0.6 million, or $0.02 per diluted share, for the second quarter of 2009, which benefited from $19.4 million in pre-tax net gains from significant special items.

Gross profit for the second quarter totaled $64.1 million, up 32.8% from $48.3 million in the prior-year period. Gross margins increased to 11.9% from the 11.4% generated in the year earlier period. Total operating expenses increased $22.8 million, or 60.4% from the same period a year ago, which benefited from $20.5 million in net gains from significant special items. Reported operating income for the quarter was $3.6 million, compared with an operating profit of $10.6 million a year ago.

“The second-quarter business climate was characterized by unprecedented volatility in the structural wood-based products market and a sluggish recovery of demand for products related to new home construction.” said BlueLinx President and CEO George Judd. “Despite this challenging environment, we performed well as we grew our unit volume by 11.9% and increased our gross profit by 32.8%. We also remained focused on cost management reducing our selling, general and administrative expenses to 10.6% of sales.

26. Yet, despite this promising outlook for the Company, CAI seeks to squeeze out BlueLinx’s shareholders with the Proposed Acquisition. On July 21, 2010, on behalf of Cerberus and CAI, BlueLinx’s own Board Member wrote to BlueLinx’s Board, pitching the Proposed Acquisition:

Gentlemen:

Cerberus ABP Investor LLC (“CAI”) is pleased to advise you that it intends to commence a tender offer for all of the outstanding shares of common stock of BlueLinx Holdings Inc. (“BlueLinx” or the “Company”) not owned by CAI, at a purchase price of $3.40 per share in cash. This represents a premium of approximately 35.5% over the closing price on July 21, 2010, and a 16.8% premium

over the volume-weighted average closing price for the last 30 trading days. In our view, this price represents a fair price to BlueLinx’s stockholders.

The tender offer will be conditioned upon, among other things, the tender of a majority of shares not owned by CAI or by the directors or officers of the Company and, unless waived, CAI owning at least 90% of the outstanding BlueLinx common stock as a result of the tender or otherwise. Any shares not acquired in the tender offer are expected to be acquired in a subsequent merger transaction at the same cash price per share. The tender offer is not subject to any financing or due diligence condition.

We believe that our offer to acquire the shares of BlueLinx not owned by CAI represents a unique opportunity for BlueLinx’s stockholders to realize the value of their shares at a significant premium to BlueLinx’s current and recent stock price. As the longtime majority stockholder of BlueLinx, we wish to acknowledge your dedicated efforts as board members of the Company and to express our appreciation for the significant contribution that the board members of BlueLinx have made to the Company in the challenging business and economic environment of the past few years.

In considering our tender offer, you should be aware that in our capacity as a stockholder we are interested only in acquiring the BlueLinx shares not already owned by us and that in our capacity as a stockholder we have no current interest in selling our stake in BlueLinx nor would we currently expect, in our capacity as a stockholder, to vote in favor of any alternative sale, merger or similar transaction involving BlueLinx other than the transaction outlined here.

CAI has not had any substantive discussions or negotiations with members of the Company’s management regarding their ability to “roll” their BlueLinx shares or stock options, or regarding any changes to existing employment agreements, equity incentive plans or benefit arrangements, in connection with the tender offer. However, at the appropriate time, we may explore, and discuss with management, any or all such topics.

CAI does not expect the tender offer and merger to result in a change of control under the Company’s existing revolving credit facility or mortgage debt financing.

We intend to commence our tender offer within approximately seven days. CAI believes it would be appropriate for the Company’s board of directors to form a special committee consisting of independent directors not affiliated with CAI to consider CAI’s tender offer and to make a recommendation to the Company’s stockholders with respect thereto. In addition, CAI encourages the special committee to retain its own legal and financial advisors to assist in its review of our tender offer and the development of its recommendation.

We will file a Schedule 13D amendment, and as such, we feel compelled to issue a press release, a copy of which is attached for your information. We expect to make

the release public prior to the opening of the New York Stock Exchange on July 22, 2010.

Very truly yours, |

| |

|

| |

CERBERUS ABP INVESTOR LLC |

| |

|

|

|

By: | /s/ Steven F. Mayer |

|

27. Conveniently, Defendant Mayer was preaching to the choir, as BlueLinx’s Board Chairman himself, Defendant Cohen, as well as Board Members Suwyn, Warden and Warner each have close ties and affiliations with Cerberus.

28. Then, on July 22, 2010, the Company, via Defendant Judd, timidly described the tender offer and equivocated about the creation of an independent special committee to review the tender offer, something which should be automatic:

Last night the BlueLinx Board of Directors received notice from our largest shareholder, Cerberus, ABP Investor LLC (“Cerberus” or CAI”) that it intends to make a tender offer for the shares of BlueLinx stock it does not own for $3.40 in cash per share. As Cerberus will be releasing a press release this morning, I wanted to communicate to you personally.

In situations like this, it is typical to form a special committee consisting of independent directors not affiliated with Cerberus, to consider its tender offer and to make a recommendation to the Company’s stockholders. We will provide further information when the BlueLinx Board makes a determination about whether to form a special committee and any recommendation made by that committee or the full Board.

There can be no assurance the proposal from Cerberus will be approved.

For all employees, I expect no change for you, our customers and our vendors. It is important we stay focused on serving our customers better than anyone else in the industry. Everything will be business as usual. Please stay focused on our jobs, and doing our jobs safely.

Thank you for your support.

29. Given Cerberus’ control of BlueLinx’s Board of Directors, including its Board Chairman, Defendant Cohen, any purported special committee is window dressing. The Proposed

Acquisition is a foregone conclusion. Indeed, in the July 22, 2010 release, the Proposed Acquisition is described accordingly:

NEW YORK, July 22 /PRNewswire/ — Cerberus ABP Investor LLC (“CAI”), an affiliate of Cerberus Capital Management, L.P. (“Cerberus”), today announced that it intends to make a tender offer for all of the outstanding publicly held shares of BlueLinx Holdings Inc. (NYSE:BXC - News) (“BlueLinx” or the “Company”) not owned by CAI. Based on shares outstanding as of May 7, 2010, CAI currently owns 55.39% of the outstanding common stock of BlueLinx. CAI intends to offer to acquire the balance of BlueLinx’s common stock for $3.40 per share in cash, representing a premium of approximately 35.5% over the closing price on July 21, 2010, and a 16.8% premium over the volume-weighted average closing price for the last 30 trading days.

CAI believes that the offer to acquire the shares of BlueLinx not owned by CAI represents a unique opportunity for BlueLinx’s stockholders to realize the value of their shares at a significant premium to BlueLinx’s current and recent stock price. CAI intends to commence the offer within approximately seven days.

The tender offer will be conditioned upon, among other things, the tender of a majority of shares not owned by CAI or by the directors or officers of the Company and, unless waived, CAI owning at least 90% of the outstanding BlueLinx common stock as a result of the tender or otherwise. Any shares not acquired in the tender offer are expected to be acquired in a subsequent merger transaction at the same cash price per share. The tender offer is not subject to any financing or due diligence condition. The aggregate consideration for the outstanding BlueLinx shares (excluding shares outstanding following exercise of in-the-money options) would be approximately $49.6 million.

In a letter sent to the Board of Directors of BlueLinx yesterday, CAI stated that in its capacity as a stockholder of BlueLinx it was interested only in acquiring the BlueLinx shares not already owned by it and that in its capacity as a stockholder it has no current interest in selling its stake in BlueLinx nor would it currently expect, in its capacity as a stockholder, to vote in favor of any alternative sale, merger or similar transaction.

30. On or about July 27, 2010, BlueLinx issued a press release announcing that the Board had formed a special committee, which is comprised of Marchese Schumacher, and Grant. Nevertheless, CAI and the directors of BlueLinx all have clear and material conflicts of interest in the Proposed Acquisition as CAI is the controlling and dominant shareholder of the Company, and thereby dominates, controls, and/or has the power to influence the entire Board of BlueLinx as well

as the Company’s proxy machinery. CAI is acting to better its own interests at the expense of BlueLinx’s public minority shareholders. It is in a position to dictate the terms of the Proposed Acquisition, and the remaining directors of the Company are beholden to CAI for their positions and the perquisites which they enjoy therefrom and cannot represent or protect the interest of the Company’s minority shareholders with impartiality and vigor.

31. Simply put, the Proposed Acquisition is in furtherance of a wrongful plan by CAI and Cerberus, with the acquiescence of its appointed directors, to take the Company private, which, if not enjoined, will result in the elimination of the public stockholders of BlueLinx in a transaction that is inherently unfair to them and that is the product of the defendants’ conflict of interest and breach of fiduciary duties, as described herein. More particularly, the transaction is in violation of the Individual Defendants’ fiduciary duties and has been timed and structured unfairly in that:

(a) The Proposed Acquisition is designed and intended to eliminate members of the Class as stockholders of the Company for consideration which the Individual Defendants know or should know is grossly unfair and inadequate;

(b) CAI, by virtue of, among other things, its ownership and voting power, controls and dominates the Board of BlueLinx;

(c) The Individual Defendants have unique knowledge of the Company and have access to information denied or unavailable to the Class. Without all material information, Class members are unable to determine whether the price offered in the transaction is fair; and

(d) CAI has violated its duty of fair dealing by manipulating the timing of the transaction to benefit itself at the expense of plaintiffs and the Class.

32. In sum, CAI is engaging in self-dealing and not acting in good faith toward Plaintiff and the other members of the Class. By reason of the foregoing, defendants have breached and are breaching their fiduciary duties to the members of the Class.

The Tender Offer Materials Are Misleading and Omit Material Information

33. On or about August 2, 2010, CAI commenced the tender offer and, in connection, the Defendants filed a TO document with the SEC. The TO document purports to provide BlueLinx shareholders with material information about the tender offer so that they are able to make informed, rational, and intelligent decisions about whether to tender their shares. However, the tender offer materials fall far short of providing this information, omitting many material details, including but not limited to:

(a) The tender offer materials neglect to provide any rigorous or meaningful analysis as to why the $3.40 per share offer price is fair or as to the basis for the price, including any basis for how Cerberus determined the price;

(b) Although the tender offer materials include a cursory market premium justification for the $3.40 per share offer, the materials neglect to address why $3.40 is actually a “fair price,” especially given the Company’s demonstrated growth potential;

(c) Likewise, although the tender offer materials neglect to include Cerberus’ analysis of the “value of certain of the Company’s assets” in terms of the Company’s total enterprise value. As Cerberus itself acknowledges in the portion of the tender offer materials that discuss appraisal rights, “Any judicial determination of the fair value could be based upon considerations other than or in addition to the market value of the Shares, including, among other things, asset values and earning capacity”;

(d) Moreover, the tender offer materials neglect to adequately explain why Cerberus “believes that the liquidation value of the Company is irrelevant to a determination as to whether the Offer is fair to unaffiliated stockholders”;

(e) The tender offer materials neglect to provide the true value of BlueLinx’s assets, including the actual value of the Company’s real estate holdings; and

(f) The tender offer materials neglect to provide other information regarding BlueLinx’s value, such as appraisals or valuation materials of BlueLinx prepared or provided to any of the Defendants.

34. These and other omissions from the tender offer materials deprive Plaintiff and the class from making informed, rational, and intelligent decisions as to whether they should tender their shares in the tender offer. Without adequate corrective disclosures, Plaintiff and the class face irreparable harm and have no adequate remedy at law.

CLASS ACTION ALLEGATIONS

35. Plaintiff brings this action individually and as a class action on behalf of all holders of BlueLinx stock who are being and will be harmed by defendants’ actions described below (the “Class”). Excluded from the Class are defendants herein and any person, firm, trust, corporation, or other entity related to or affiliated with any defendants.

36. This action is properly maintainable as a class action under Delaware Court of Chancery Rule 23.

37. The Class is so numerous that joinder of all members is impracticable. There are over 32 million outstanding shares of BlueLinx common stock. These shares are held by hundreds, if not thousands, of beneficial holders.

38. There are questions of law and fact which are common to the Class and which predominate over questions affecting any individual Class member. The common questions include, inter alia, the following:

(i) whether defendants have breached their fiduciary duties of undivided loyalty and good faith with respect to plaintiffs and the other members of the Class in connection with the Proposed Acquisition;

(ii) whether the Individual Defendants and CAI and Cerberus are unjustly enriching themselves and other insiders or affiliates of CAI and Cerberus;

(iii) whether CAI, as the controlling and dominating shareholder of BlueLinx, has breached and is breaching its fiduciary duties to the BlueLinx public minority shareholders by making an unfair and inadequate offer to take the Company private and in failing to disclose material information to the Company’s minority shareholders;

(iv) whether defendants have breached any of their other fiduciary duties to plaintiffs and the other members of the Class in connection with the Proposed Acquisition, including the duties of candor, good faith, honesty and fair dealing; and

(v) whether plaintiffs and the other members of the Class would suffer irreparable injury were the transaction complained of herein consummated.

39. Plaintiffs claims are typical of the claims of the other members of the Class and plaintiff does not have any interests adverse to the Class.

40. Plaintiff is an adequate representative of the Class, has retained competent counsel experienced in litigation of this nature and will fairly and adequately protect the interests of the Class.

41. The prosecution of separate actions by individual members of the Class would create a risk of inconsistent or varying adjudications with respect to individual members of the Class which would establish incompatible standards of conduct for the party opposing the Class.

42. Plaintiff anticipates that there will be no difficulty in the management of this litigation. A class action is superior to other available methods for the fair and efficient adjudication of this controversy.

43. Defendants have acted on grounds generally applicable to the Class with respect to the matters complained of herein, thereby making appropriate the relief sought herein with respect to the Class as a whole.

CAUSE OF ACTION

Breach of Fiduciary Duty and Aiding and Abetting

Against All Defendants

44. Plaintiff repeats and realleges each allegation set forth herein.

45. Defendants are structuring their discussions concerning and timing of announcements of the Proposed Acquisition to benefit themselves and/or their colleagues to the detriment of BlueLinx public minority shareholders, and/or are aiding and abetting therein. Instead of attempting to maximize shareholder value for BlueLinx shareholders, the defendants have taken actions in violation of applicable state law which will only serve their own interests, while sacrificing the interests of BlueLinx public shareholders, and/or are aiding and abetting therein.

46. Defendant CAI owes fiduciary duties to Plaintiff and the Class as a majority and controlling shareholder of BlueLinx. The Individual Defendants owe fiduciary duties to Plaintiff and the Class as directors of BlueLinx.

47. CAI and the Individual Defendants were and are under a duty:

(a) to fully inform themselves of the market value of BlueLinx before taking, or agreeing to refrain from taking, action;

(b) to act in the interests of BlueLinx public shareholders;

(c) refrain from advancing their own interests, or those of other defendants, at the expense of Plaintiff and the Class;

(d) to obtain the best financial and other terms when the Company’s independent existence will be materially altered by a transaction; and

(e) to act in accordance with their fundamental duties of due care, loyalty, candor, independence, and good faith.

48. By the acts, transactions and courses of conduct alleged herein, defendants, individually and as part of a common plan and scheme, in breach of their fiduciary duties to Plaintiff and the other members of the Class, are implementing and abiding by a process that will deprive Plaintiff and other members of the Class of a fair process and the true value of their investment in BlueLinx.

49. By reason of the foregoing acts, practices and course of conduct, the defendants failed to exercise the required care and diligence in the exercise of their fiduciary obligations toward plaintiffs and the other BlueLinx public stockholders. The Defendants have also failed to abide by their fiduciary duties of candor which requires, inter alia, that they provide all material information to BlueLinx’s shareholders about the tender offer.

50. BlueLinx and CAI have aided and abetted the other defendants’ breaches of fiduciary duty by the conduct alleged above.

51. In light of the foregoing, Plaintiff demands that CAI and the Individual Defendants, as their fiduciary obligations require, immediately:

(a) act independently so that the interests of BlueLinx public stockholders will be protected, including, but not limited to, the retention of truly independent advisors and/or the appointment of a truly independent Special Committee;

(b) adequately ensure that no conflicts of interest exist between defendants’ own interests and their fiduciary obligation to maximize stockholder value or, if such conflicts exist, to ensure that all conflicts be resolved in the best interests of BlueLinx public stockholders;

(c) provide corrective disclosures that remedy the omission of material information from the tender offer materials and that enable BlueLinx shareholders to make intelligent, informed, and rational decisions on whether to tender their shares; and

(d) otherwise ensure that Plaintiff and the other members of the Class receive a fair process and fair price in connection with any transaction involving BlueLinx, including full and fair disclosure of all material information.

52. As a result of defendants’ failure to take such steps to date, Plaintiff and the other members of the Class have been and will be damaged in that they have been and will be prevented from obtaining a fair process or fair price for their shares.

53. Defendants are not acting in good faith toward Plaintiff and the other members of the Class, and have breached and are continuing to breach their fiduciary duties to Plaintiff and the members of the Class.

54. As a result of defendants’ unlawful actions, Plaintiff and the other members of the Class will be irreparably harmed in that they will not receive a fair process or fair value for BlueLinx assets and business. Unless the defendants’ actions are enjoined by the Court, defendants will continue to breach their fiduciary duties owed to Plaintiff and the members of the Class, and will engage in a process that inhibits the maximization of shareholder value. Moreover, unless the defendants’ actions are enjoined by the Court, BlueLinx shareholders will be unable to make intelligent, informed, and rational decisions about whether to tender their shares.

55. Plaintiff and the other members of the Class have no adequate remedy at law.

PRAYER FOR RELIEF

WHEREFORE, Plaintiff demands injunctive relief, in their favor and in favor of the Class and against defendants as follows:

A. Declaring that this action is properly maintainable as a class action;

B. Declaring and decreeing that the proposed tender offer is coercive, was entered into in by CAI in breach of its fiduciary duties and those of the Individual Defendants and that the tender offer is therefore unlawful and should be enjoined;

C. Enjoining defendants, their agents, counsel, employees and all persons acting in concert with them from consummating the Proposed Acquisition, unless and until the Company adopts and implements a procedure or process to obtain a transaction providing the highest possible value for shareholders; and unless and until the defendants provide corrective disclosures to remedy the omission of material information from the tender offer materials that deprives BlueLinx shareholders from making intelligent, informed, and rational decisions about whether to tender their shares;

D. Directing the Individual Defendants to exercise their fiduciary duties to obtain a transaction which is in the best interests of the Company’s shareholders until the process for the sale or auction of the Company is completed and the best possible consideration is obtained for BlueLinx public shareholders;

E. Rescinding, to the extent already implemented, the Proposed Acquisition or the tender offer or any of the terms thereof;

F. Awarding Plaintiff the costs and disbursements of this action, including reasonable attorneys’ and experts’ fees; and

G. Granting such other and further equitable relief as this Court may deem just and proper.

| /s/ Joel Friedlander |

| Joel Friedlander (#3163) |

| Sean M. Brennecke (#4686) |

| BOUCHARD MARGULES & FRIEDLANDER, P.A. |

| 222 Delaware Avenue, Suite 1400 |

| Wilmington, DE 19801 |

| (302) 573-3500 |

| Attorneys for Plaintiff |

OF COUNSEL:

ROBBINS GELLER RUDMAN

& DOWD LLP

Stuart A. Davidson

Cullin A. O’brien

120 E. Palmetto Park Road, Suite 500

Boca Raton, FL 33432

(561) 750-3000

ROBBINS GELLER RUDMAN

& DOWD LLP

David Wissbroecker

655 West Broadway, Suite 1900

San Diego, CA 92101

(619) 231-1058

RYAN & MANISKAS, LLP

RICHARD A. MANISKAS

995 Old Eagle School Road, Suite 311

Wayne, PA 19087

(877) 316-3218

DATED: August 13, 2010