“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Manitex International, Inc. Corporate Presentation (NASDAQ:MNTX) November 2010 Exhibit 99.1 |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Forward Looking Statements and Non- GAAP Measures Safe Harbor Statement under the U.S. Private Securities Litigation Reform Act of 1995: This presentation contains statements that are forward-looking in nature which express the beliefs and expectations of management including statements regarding the Company’s expected results of operations or liquidity; statements concerning projections, predictions, expectations, estimates or forecasts as to our business, financial and operational results and future economic performance; and statements of management’s goals and objectives and other similar expressions concerning matters that are not historical facts. In some cases, you can identify forward-looking statements by terminology such as “anticipate,”“estimate,” “plan,” “project,” “continuing,” “ongoing,” “expect,” “we believe,” “we intend,” “may,” “will,” “should,” “could,” and similar expressions. Such statements are based on current plans, estimates and expectations and involve a number of known and unknown risks, uncertainties and other factors that could cause the Company's future results, performance or achievements to differ significantly from the results, performance or achievements expressed or implied by such forward looking statements. These factors and additional information are discussed in the Company's filings with the Securities and Exchange Commission and statements in this presentation should be evaluated in light of these important factors. Although we believe that these statements are based upon reasonable assumptions, we cannot guarantee future results. Forward looking statements speak only as of the date on which they are made, and the Company undertakes no obligation to update publicly or revise any forward-looking statement, whether as a result of new information, future developments or otherwise. Non-GAAP Measures: Manitex International from time to time refers to various non-GAAP (generally accepted accounting principles) financial measures in this presentation. Manitex believes that this information is useful to understanding its operating results without the impact of special items. See Manitex’s earnings releases on the Investor Relations section of our website www.manitexinternational.com for a description and/or reconciliation of these measures. 2 |

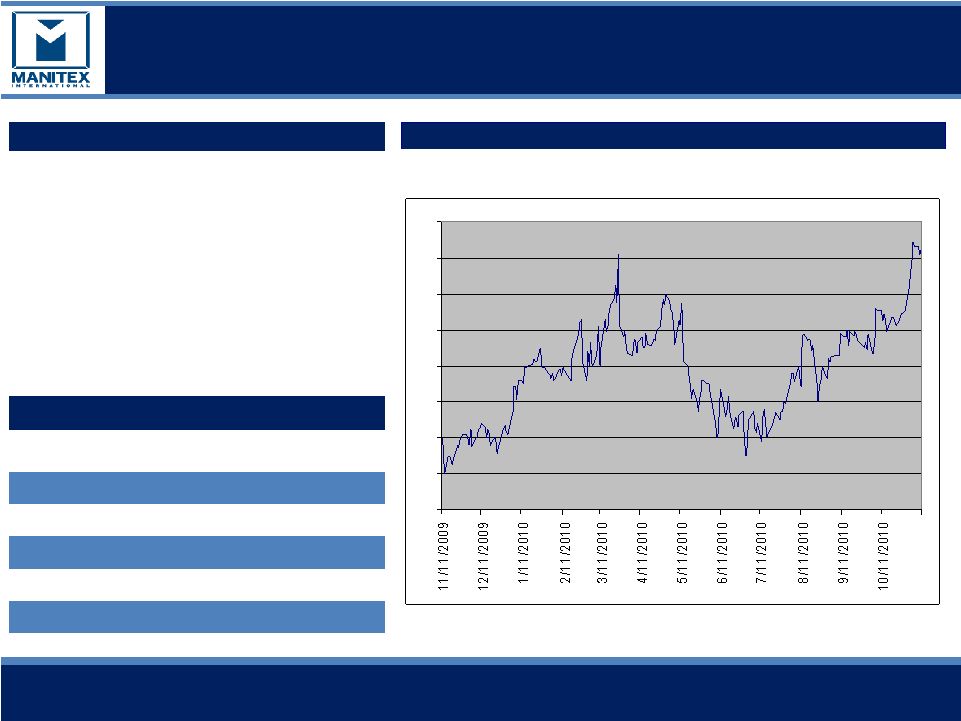

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Company Snapshot 3 LTM Share Price Performance Company Description Manitex International, Inc. provides engineered lifting solutions. The company operates through two segments, Lifting Equipment and Equipment Distribution. The Lifting Equipment segment designs, manufactures, and distributes boom trucks and crane products. The Equipment Distribution segment sells, services and distributes lifting equipment to end users. The company was formerly known as Veri-Tek International, Corp. and changed its name to Manitex International, Inc. in May 2008. Manitex International was founded in 1993 and is based in Bridgeview, Illinois. Financial Summary Total Enterprise Value (11/11/10): $67.0 million Market Cap (11/11/10): $33.3 million LTM Total Revenue (9/30/10): $81.3 million LTM Net Income (9/30/10): $5.0 million LTM EBITDA (9/30/10): 6.3 million Stock Price (11/11/10) $2.93 Ticker / Exchange: MNTX / NASDAQ 1.5 1.7 1.9 2.1 2.3 2.5 2.7 2.9 3.1 $2.93 |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation • Global provider of boom trucks, sign cranes and specialized material handling equipment primarily used in commercial, state, local and international government, and military applications • Major industries served include energy (extraction and processing), utilities, railroads, commercial building, rental fleets, cargo transportation, and infrastructure development – roads and bridges • Historically serving North American markets; recent international diversification and growth • Business Model based in part on an aggressive program of making accretive acquisitions of complementary businesses – High margin niche markets – Including two in 2009 (Badger and Load King) and CVS agreement in July 2010 – Rely on seller financing (favorable terms, limited covenants) Corporate Overview Manitex International 4 Manitex International Businesses |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation 5 Product Overview Manitex, Manitex Liftking, Badger, Load King • Badger Equipment has manufactured specialized earthmoving, railroad and material handling equipment since 1945 and has built over 10,000 units during its existence. • Manufacturer of a complete line of RT Forklifts, Special Mission Oriented Vehicles, Carriers, Heavy Material Handling Transporters and Steel Mill Equipment • Manitex specializes in engineered lifting equipment and its product family includes Manitex Boom Trucks, SkyCrane Aerial Platforms and Sign Cranes • Manufacturer of container handling equipment for the global port and inter-modal sectors. Products include reach stackers, laden and unladen container forklifts and straddle carriers |

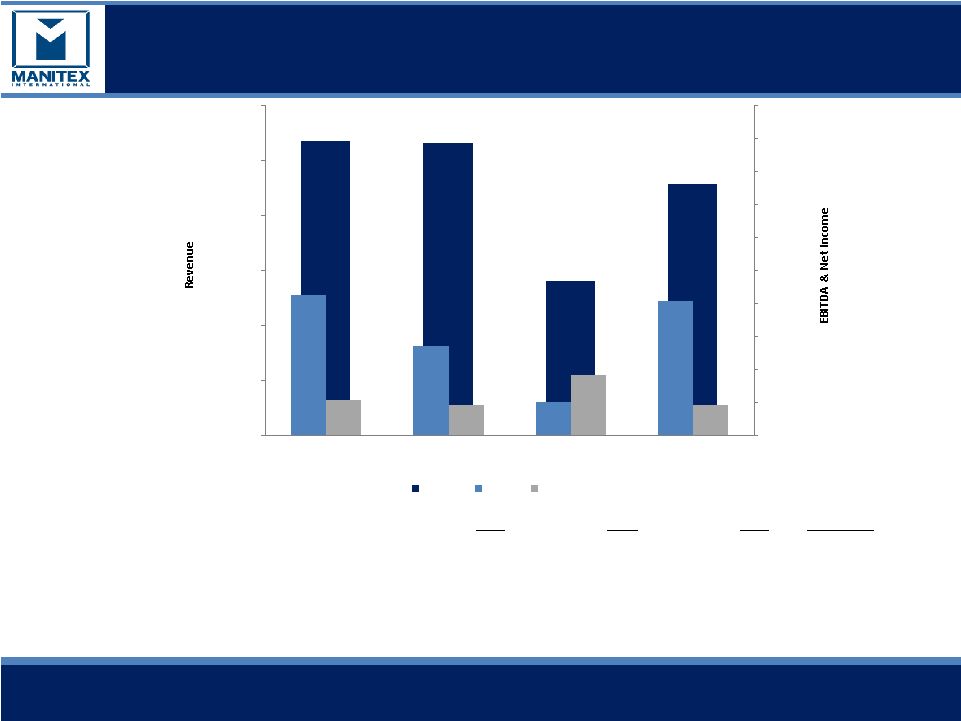

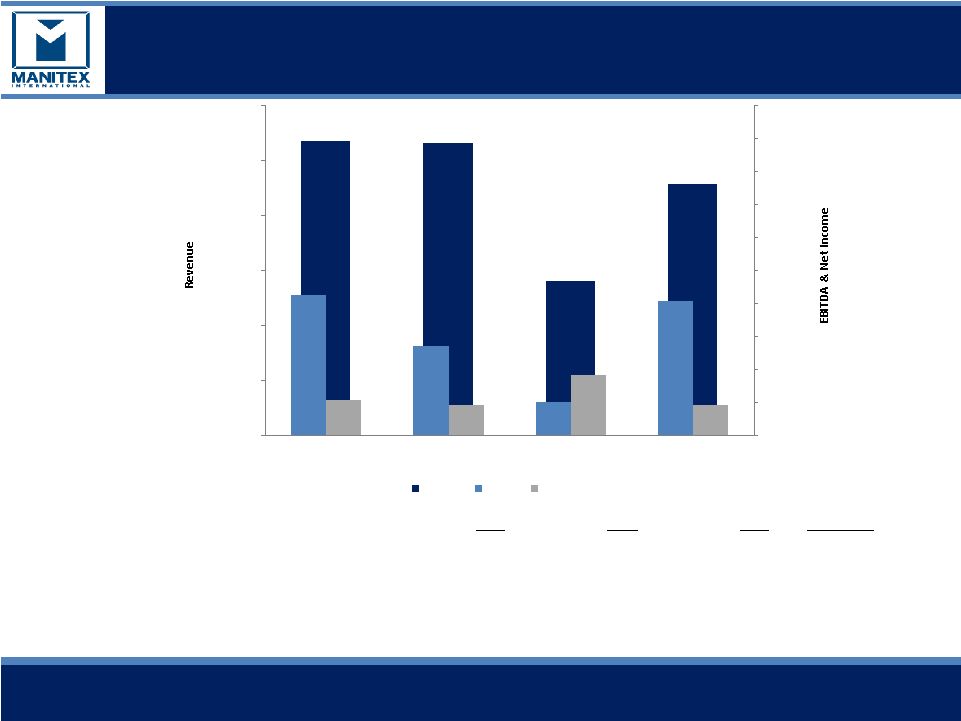

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Select Financial Data Note: Includes continuing operations only. •Includes gain on bargain purchase of $3,815 •**2010 est, based on 2010 nine months ytd plus estimated Q4 based on repeating Q3 revenue, gross profit, EBITDA and net income 6 (USD in thousands) $106,946 $106,341 $55,887 $91,200 $8,461 $5,416 $1,982 $8,100 $1,799 $3,639 $1,834 $2,126 $0 $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 2007 2008 2009 2010 est** $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 $18,000 $20,000 Revenue EBITDA Net Income $ in thousands, except percentages 2007 2008 2009 2010 est** Revenue $ 106,946 $ 106,341 $ 55,887 $ 91,200 Gross Margin 18.6% 16.4% 20.0% 23.6% EBITDA 8,461 5,416 1,982 8,100 EBITDA Margin (%) 7.9% 5.1% 3.5% 8.9% Net Income 2126 1,799 3,639 * 1834 |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Key Management Name & Title Experience David Langevin Chairman & CEO 20+ years principally with Terex Andrew Rooke President &COO 20+ years principally with Rolls Royce, GKN Sinter Metals, Off- Highway & Auto Divisions David Gransee CFO & Treasurer Formerly with Arthur Andersen, 15+ years with Eon Labs (formerly listed) Robert Litchev President – Material Handling & SVP International Distribution 10+ years principally with Terex Scott Rolston SVP Sales & Marketing – Manitex International 13+ years principally with Manitowoc 7 |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation 1) 2009 was a transformative year for Manitex – Two major acquisitions – Successfully developed new products for the utilities & railroad markets • Maintained R&D spend to continue developing innovative products – Major cost reductions • $12.4 m reduction in costs in 2009 compared to 2008: Manufacturing cost reduction 48% or $7.8m, SG&A, Corporate and R&D cost reduction of 34% or $4.6m 2) Experienced senior management – Senior management has over 70 years of collective experience from well-known industrial leaders such as Terex, Manitowoc, Rolls Royce, GKN Sinter Metals, Off-Highway and Auto Divisions and Genie 3) The Company has a global presence with more than 20,000 units operating worldwide spanning equipment dealerships throughout the country – High recurring revenue stream 24% of total sales (average 40% margin) 4) Growing market share – Increased penetration in oil and gas, power grid and rail – Rebounding military sales – Expanding international sales 5) Focused on earnings, cash flow and working capital management 8 Investment Highlights |

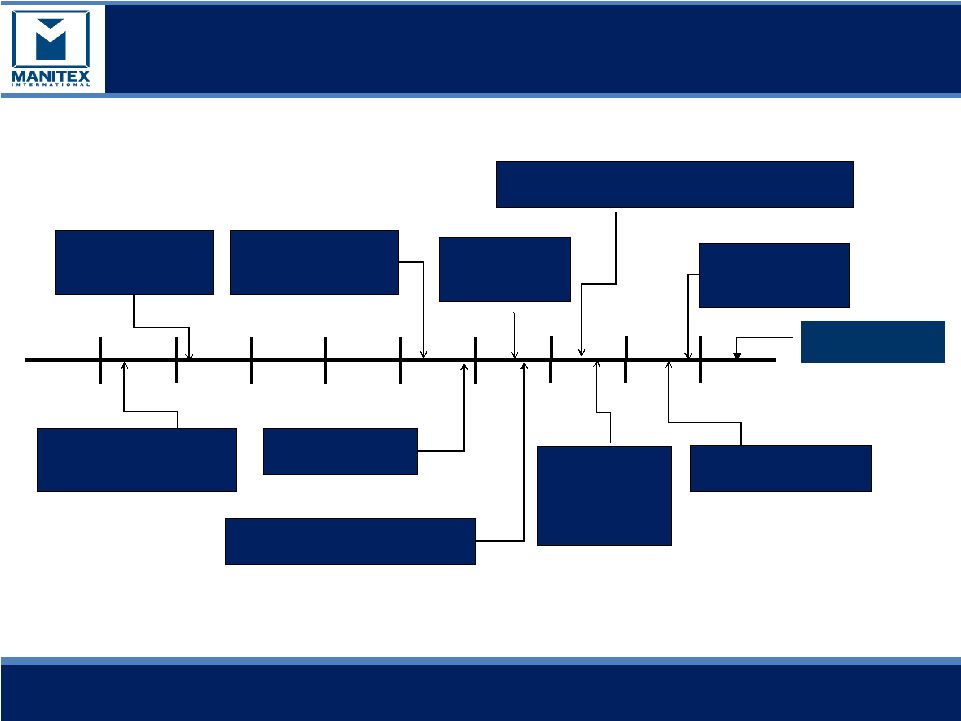

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation 9 Company Timeline March 2002: Manitowoc (NYSE:MTW) acquires Grove. January 2003: Manitowoc divests Manitex December 2009: Acquire Load King Trailers July 2009 Acquire Badger Equipment Co November 2006: Veri- Tek Acquires LiftKing July 2007: VCC acquires Noble forklift August 2007: Sale of assets and closure of legacy VCC business May 2008: Name changed to Manitex International and listed on Nasdaq (MNTX) October 2008: Crane & Machinery and Schaeff Forklift acquired July 2006: Manitex merges into Veri-Tek, Intl. (VCC) 2002 2003 2004 2005 2006 2007 2008 2009 2010 July 2010 :CVS Ferrari Operating Agreement |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation • Load King Trailers, an Elk Point, South Dakota-based manufacturer of specialized custom trailers and hauling systems typically used for transporting heavy equipment • Consideration of $3 million; Load King’s last five years average annual revenues were approximately $23 million • Niche product line, well-recognized quality brand name and accomplished management team Recent Acquisitions Highlights 10 • Badger Equipment Co, a Winona, Minnesota based manufacturer of specialized rough terrain cranes and material handling products • Stock purchase with consideration of $5.1m: Badgers last five years average annual revenues were approximately $8m • Developing new rough terrain crane line targeted for railroad, refinery and construction markets • Long standing brand recognition and crane legacy, with established railroad and municipality relationships |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Recent Acquisitions (subject to approval) CVS 11 • June 30 2010 MNTX entered into an agreement to operate, on an exclusive rental basis, the business of CVS SPA, commencing July 1 2010 • CVS SPA is located near Milan Italy and designs and manufactures a range of reach stackers and associated lifting equipment for the global container handling market • CVS had 2008 annual sales of $106m prior to the global downturn • The rental agreement has been filed with the Italian Court and includes an offer to purchase the business at the conclusion of the Italian insolvency process (“Concordato Preventivo”) Rental period could extend for up to two years • Sales and profits are consolidated into Manitex International from July 2010. No debt or liabilities of “old CVS” were assumed. As at July 1, CVS has a backlog of orders of approximately $10m • Acquisition is transformational: • Adds global product offering • European manufacturing and design • Adds scale • Above average growth profile sectors of containers / ports / inter- modal |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation • Recurring revenue of approximately 24% of total sales • Spares relate to swing drives, rotating components, and booms among others, many of which are proprietary – Serve additional brands – Service team for crane equipment Replacement Parts & Service Consistent Recurring Revenue 12 |

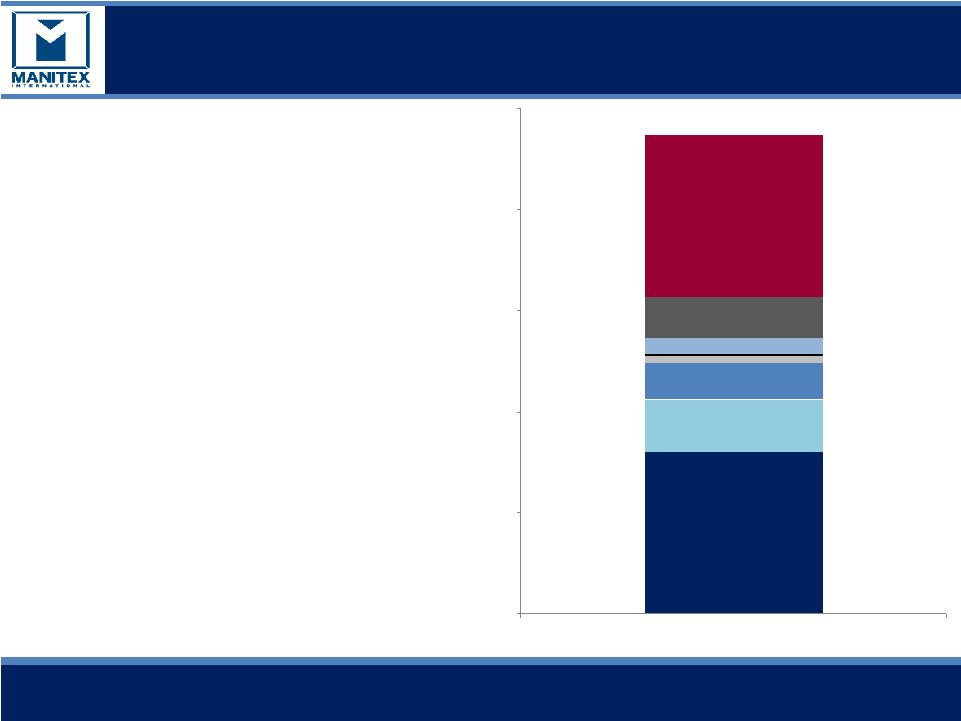

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Pro-forma Revenues • Pro-forma revenues are based on 2007 revenue numbers for each respective business, regardless of date of acquisition by Manitex International • We believe Pro-forma revenues are more representative of revenue opportunity than revenues in the current phase of the economic cycle 13 Manitex, $80.0 Liftking, $26.0 Crane & Machinery, $18.1 Schaeff, $3.3 Noble, $1.1 Badger, $8.0 LoadKing, $20.0 CVS Ferrari, $80.0 $0.0 $50.0 $100.0 $150.0 $200.0 $250.0 Pro-forma Annual Revenue |

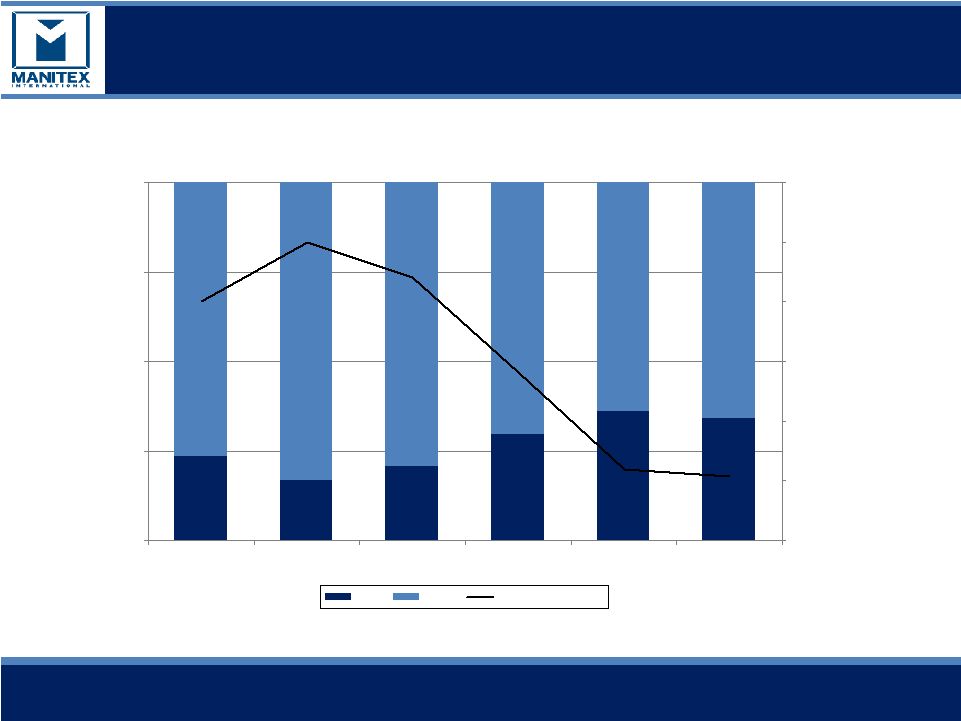

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation 14 Boom Truck Crane Market 23.4% 16.7% 20.8% 29.6% 36.1% 34.0% 76.6% 83.3% 79.2% 70.4% 63.9% 66.0% 0.0% 25.0% 50.0% 75.0% 100.0% 2005 2006 2007 2008 2009 2010 est Market Share 0 500 1000 1500 2000 2500 3000 Units Shipped MNTX Others Total Units Shipped Increased Market Share as Market Declined |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation • Management saw the state of the world as an opportunity to cut costs and grow the business through acquisition at a very modest cost, notwithstanding reductions in its core markets • $12.4 m reduction in costs in 2009 compared to 2008 • Management was successful in lowering costs to match decreases in sales; revenue decreased 47% from 2008-2009 • With outside financing unavailable our model of negotiating seller financing fit circumstances perfectly • 1 nine months 2010 gross margin 23.6%, $4.3m increase in EBITDA, revenue 62% higher • 1 nine months 2010 EBITDA margin of 8.8% was the best since 2007 15 2009/2010 Highlights Opportunistic Cost Cutting st st |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Select Financial Data Note: Includes continuing operations only. •Includes gain on bargain purchase of $3,815 •**2010 est, based on 2010 nine months ytd plus estimated Q4 based on repeating Q3 revenue, gross profit, EBITDA and net income 16 (USD in thousands) $106,946 $106,341 $55,887 $91,200 $8,461 $5,416 $1,982 $8,100 $1,799 $3,639 $1,834 $2,126 $0 $20,000 $40,000 $60,000 $80,000 $100,000 $120,000 2007 2008 2009 2010 est** $0 $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 $14,000 $16,000 $18,000 $20,000 Revenue EBITDA Net Income $ in thousands, except percentages 2007 2008 2009 2010 est** Revenue $ 106,946 $ 106,341 $ 55,887 $ 91,200 Gross Margin 18.6% 16.4% 20.0% 23.6% EBITDA 8,461 5,416 1,982 8,100 EBITDA Margin (%) 7.9% 5.1% 3.5% 8.9% Net Income 2126 1,799 3,639 * 1834 |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Growth Drivers – 2010 and Beyond • World wide improvements in GDP, economic recovery • Increased market penetration with product developments and innovative distribution • Leverage synergy with railroad industry • Developed products specifically for the following industries: Oil & Gas, Railroads, Power Grid & Wind Power • Any significant governmental infrastructure spending will be a potential spark to recovery for Manitex • International expansion – New dealership agreements reached in Middle East, Russia, & with Caterpillar Global Distribution Network – Achieved European CE Certification for 50 Ton Cranes in 2009. – Manitex International made its first international sales in 2008 and has identified new markets to accelerate future growth (Russian market potential is estimated to be double that of North America) – 2009 international sales were over 10% of revenue • CVS Ferrari is additive to the Company results 17 |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Recent Developments • May 27, 2009 – Announced $7.0 million in new orders including $5.0 million for commercial boom truck cranes for the owner-operated and rental markets and $2.0 million for Liftking military container handling forklifts. • July 10, 2009 – Acquired Badger Equipment Company for $3.0 million; adds another niche product line of rough terrain cranes and expands dealer network. • December 2, 2009 - Announced $7.6 million of orders received for 1 half of 2010 • December 31, 2009 - Acquired Load King Trailers • February 8, 2010 – Announced $4 million of orders for end of 1 half of 2010 • June 9, 2010 – Announced $5 million of orders for 2 half of 2010 • June 30, 2010 – Announced signing of exclusive Operating Agreement for business of CVS • August 5, 2010 – Announced $5 million of orders for 2010 for Manitex boom truck cranes for Canadian dealers 18 st nd st |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Summary Delivering sound operational and financial performance despite the historic economic and industry-specific challenges • Growing market share • Increased penetration in oil and gas, power grid and rail • Rebound in military sales • Penetration into rental markets and networks • International orders are increasing • We have successfully scaled our business to perform in the current market conditions through cost rationalization • Focused on earnings, cash flow and working capital management 19 |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Appendix 20 Manitex International, Inc. Corporate Presentation November 2010 |

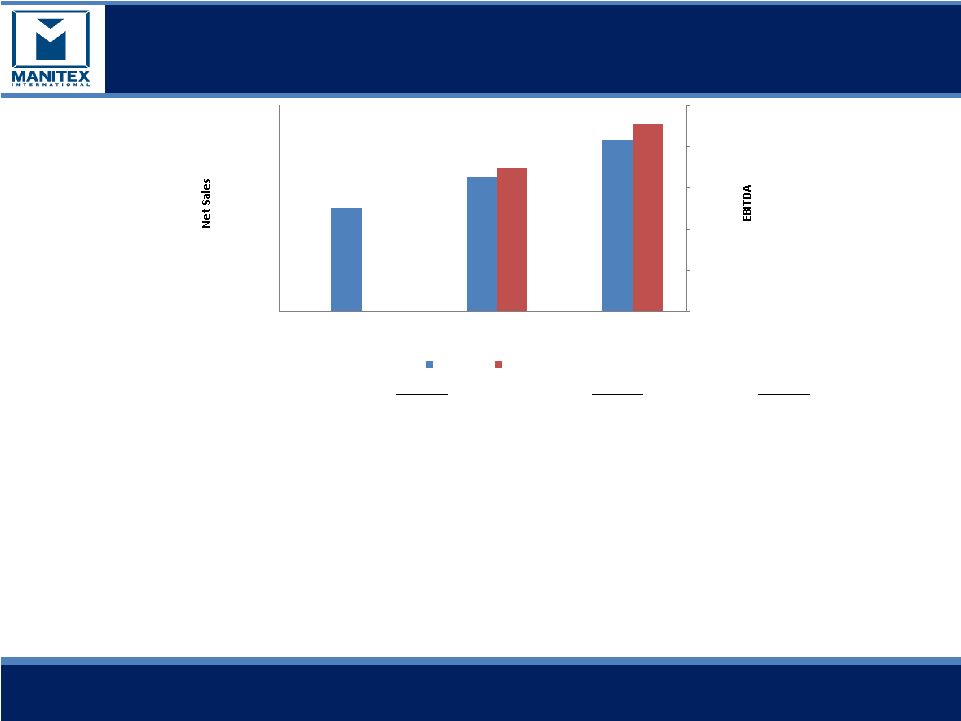

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Key Figures - Quarterly 21 USD thousands Q3-2009 Q2-2010 Q3-2010 Net sales $15,063 $19,502 $24,859 % change in Q3-2010 to prior period 65% 27% Gross profit 2,208 4,607 5,855 Gross margin % 14.7% 23.6% 23.6% Operating expenses 2946* 3,658 4,365 Net (loss) Income (147) 213 657 EBITDA -80 1,732 2,271 EBITDA % of Sales -0.5% 8.9% 9.1% Backlog ($ million) 22.3 24.9 32.8 * excludes bargain purchase gain of $0.9m $15,063 $19,502 $24,859 $1,732 $2,271 $0 $5,000 $10,000 $15,000 $20,000 $25,000 $30,000 Q3-2009 Q2-2010 Q3-2010 $0 $500 $1,000 $1,500 $2,000 $2,500 Net Sales EBITDA |

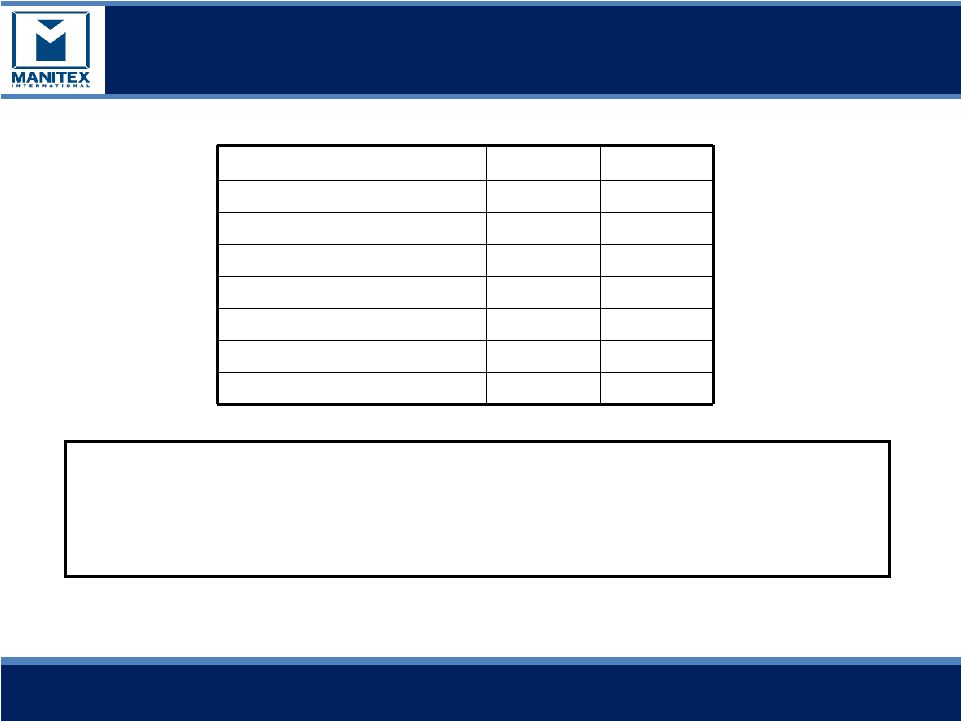

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Summarized Balance Sheet 22 Current assets $47,496 $40,147 $40,685 Fixed assets 10,955 11,804 5,878 Other long term assets 41,198 42,734 39,665 Total Assets $99,649 $94,685 $86,228 Current liabilities 17,875 14,569 17,062 Long term liabilities 39,749 39,688 34,152 Total Liabilities $57,624 $54,257 $51,214 Shareholders equity 42,025 40,428 35,014 Total liabilities & Shareholders equity $99,649 $94,685 $86,228 31-Dec-08 31-Dec-09 30-Sep-10 |

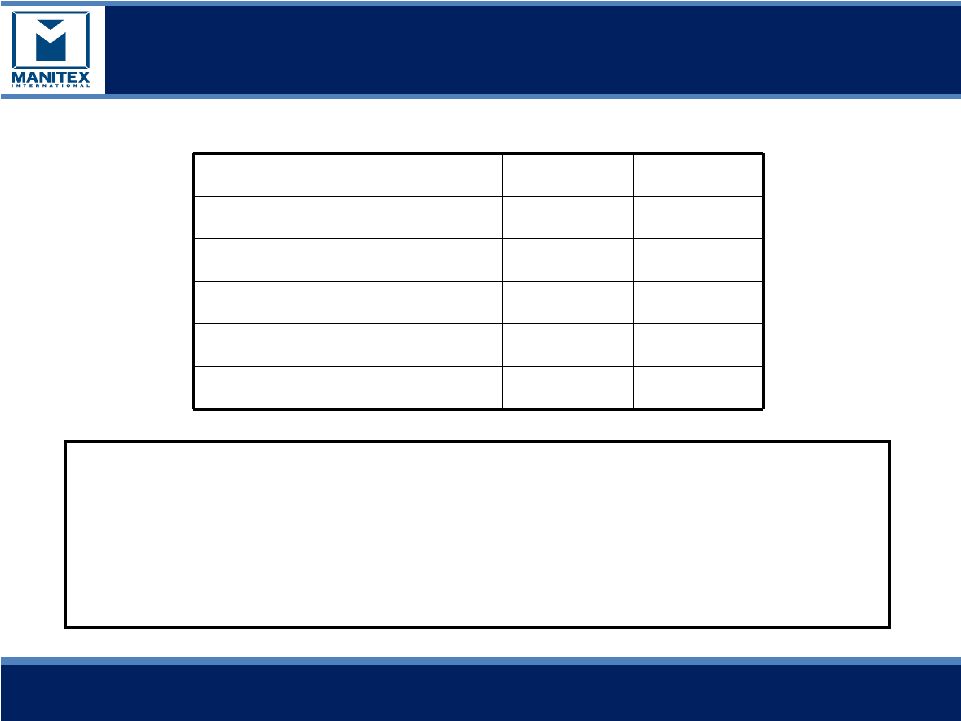

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Debt and Liquidity $000 Q3-2010 Q4-2009 Total Cash 217 287 Total Debt 33,745 33,511 Total Equity 42,025 40,428 Net capitalization 75,553 73,652 Net debt / capitalization 44.4% 45.1% Quarterly EBITDA 2,271 426 Quarterly EBITDA % of sales 9.1% 2.9% •Ebitda for Q3-2010 at 9.1% of sales is best performance by the Company •Debt reduction in Q3-2010 of $1.2m: •Revolver facility, based on available collateral at September 30, 2010 was $22.3m •Revolver availability at September 30, 2010 $3.2m •Net capitalization is the sum of debt plus equity minus cash. •Net debt is total debt less cash |

“Focused manufacturer of engineered lifting equipment “ Corporate Presentation Working Capital $000 Q3 2010 Q4 2009 Working Capital $29,621 $25,578 Days sales outstanding 62 67 Days payable outstanding 53 73 Inventory turns 2.7 1.7 Current ratio 2.7 2.8 •Increase in working capital Q3-2010 v Q4-2009 principally from increased accounts receivable ($6.0m) and inventory ($1.2m) and offset by increased accounts payable, accruals & other liabilities ($3.4) •Inventory increase from new businesses of CVS and NAEE •Continued strength of current ratio |