EXHIBIT 99.3

NextSource Materials Inc.

Management’s Discussion and Analysis (MD&A)

For the years ended June 30, 2021, and 2020

Expressed in US Dollars

| 1 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING INFORMATION

Certain statements contained in this document constitute forward-looking information within the meaning of applicable Canadian securities legislation. Generally, forward-looking information can be identified by the use of forward-looking terminology such as “plans,” “expects,” or “does not expect,” “is expected,” “budget,” “scheduled,” “goal,” “estimates,” “forecasts,” “intends,” “anticipates,” or “does not anticipate,” or “believes” or variations of such words and phrases or statements that certain actions, events or results “may,” “could,” “would,” “might,” or “will be taken,” “occur,” or “be achieved”.

Forward-looking information includes, but is not limited to, information with respect to certain expectations regarding obtaining necessary permits; construction timelines and costs; anticipated production volumes; anticipated operating costs and capital spending; supply, demand and pricing outlook in the graphite market; sources of funding for the Molo Graphite Mine and the Green Giant Vanadium Project; exploration drill results; metallurgical drill results; environmental assessment and rehabilitation costs and amounts of certain other commitments; and the Company’s business objectives and targeted milestones (and timing thereof).

Forward-looking information is subject to known and unknown risks, uncertainties and other factors that may cause the actual results, level of activity, performance or achievements of the Company to be materially different from those expressed or implied by such forward-looking information. Such factors include, among others; uncertainty due to the Covid-19 Pandemic; development projects are uncertain, and it is possible that actual capital and operating costs and economic returns will differ significantly from those estimated for a project prior to production; the Company’s development and exploration projects are in the African country of Madagascar and are subject to country political and regulatory risks; economic dependence on the Molo Graphite Mine; additional permits and licenses are necessary to complete the development of the Molo Graphite Mine; fluctuations in the market price of graphite and other metals may adversely affect and the value of the Company’s securities, revenue projections and the ability of the Company to develop Phase 2 of the Molo Graphite Mine; estimates of mineral resources and mineral reserves may not be realized; the Company may not have access to sufficient capital to develop Phase 2 of the Molo Graphite Mine and value-added processing facilities; the Company has a limited operating history and expects to incur operating losses for the foreseeable future; due to the speculative nature of mineral property exploration, there is substantial risk that the Company’s assets will not go into commercial production and the business will fail; mining companies are increasingly required to consider and provide benefits to the communities and countries in which they operate, and are subject to extensive environmental, health and safety laws and regulations; because of the inherent dangers involved in mineral exploration, there is a risk that the Company may incur liability or damages as the Company conducts business; the Company has no insurance for environmental problems; should the Company lose the services of key executives, the Company’s financial condition and proposed expansion may be negatively impacted; because access to the Company’s properties may be restricted by inclement weather or proper infrastructure, its exploration programs are likely to experience delays; climate change and related regulatory responses may impact the Company’s business; compliance with changing regulation of corporate governance and public disclosure will result in additional expenses and pose challenges for management; tax risks; because from time to time the Company holds a significant portion of cash reserves in Canadian dollars, the Company may experience losses due to foreign exchange translations; the Company’s business is subject to anti-corruption and anti-bribery laws, a breach or violation of which could lead to civil and criminal fines and penalties, loss of licenses or permits and reputational harm; the Company is exposed to general economic conditions, which could have a material adverse impact on its business, operating results and financial condition; the market price for the Common Shares is particularly volatile given the Company’s status as a company with a small public float, limited operating history and lack of profits which could lead to wide fluctuations in the market price for the Common Shares; the Company does not intend to pay dividends in the foreseeable future; and the Company’s ability to meet other factors listed from time to time in the Company’s continuous disclosure documents, including but not limited to, the Annual Information Form (AIF).

Forward-looking information is based on the reasonable assumptions, estimates, analysis and opinions of management and/or “qualified persons” (as such term is defined under National Instrument 43-101 – Standards of Disclosure for Mineral Projects (““NI 43-101”)) made in light of their experience and their perception of trends, current conditions and expected developments, as well as other factors that management and/or qualified persons believe to be relevant and reasonable in the circumstances at the date that such statements are made, but which may prove to be incorrect. Although the Company believes that the assumptions and expectations reflected in such forward-looking information are reasonable, undue reliance should not be placed on forward-looking information because the Company can give no assurance that such expectations will prove to be correct. In addition to the assumptions discussed herein the material assumptions upon which such forward-looking statements are based include, among others, that: the Company will be successful in its financing activities; the demand for graphite will develop as anticipated; graphite prices will remain at or attain levels that would make the Molo Graphite Mine economic; that any proposed operating and capital plans will not be disrupted by operational issues, title issues, loss of permits, environmental concerns, power supply, labour disturbances, financing requirements or adverse weather conditions; the Company will continue to have the ability to attract and retain skilled staff; and there are no material unanticipated variations in the cost of energy or supplies. Readers are cautioned that the foregoing list is not exhaustive of all factors and assumptions which may have been used. Although the Company has attempted to identify important factors that could cause actual results to differ materially from those contained in forward-looking information, there may be other factors that cause results not to be as anticipated, estimated or intended. There can be no assurance that such information will prove to be accurate, as actual results and future events could differ materially from those anticipated in such information. Accordingly, readers should not place undue reliance on forward-looking information. The forward-looking information contained herein is presented for the purposes of assisting investors in understanding the Company’s expected financial and operating performance and the Company’s plans and objectives and may not be appropriate for other purposes.

The Company does not undertake to update any forward-looking information, except in accordance with applicable securities laws.

This MD&A includes market, industry and economic data and projections obtained from various publicly available sources and other sources believed by the Company to be true. Although the Company believes these to be reliable, it has not independently verified the information from third party sources, or analyzed or verified the underlying reports relied upon or referred to by the third parties, or ascertained the underlying economic and other assumptions relied upon by the third parties. The Company believes that the market, industry and economic data and projections are accurate and that the estimates and assumptions are reasonable, but there can be no assurance as to their accuracy or completeness. The accuracy and completeness of the market, industry and economic data and projections in this MD&A are not guaranteed and the Company does not make any representation as to the accuracy or completeness of such information.

| 2 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

INTRODUCTION

This Management’s Discussion and Analysis (MD&A) dated September 28, 2021 of NextSource Materials Inc. (“NextSource”, “we”, “our” or “the Company”) should be read in conjunction with Company’s audited consolidated financial statements for the years ended June 30, 2021 and 2020 that were prepared in accordance with International Financial Reporting Standards (“IFRS”) issued by International Accounting Standards Board (“IASB”) (the “Annual Financial Statements”).

The Annual Financial Statements and this MD&A are presented United States dollars (“USD” or “$”). Certain information in this MD&A is presented in Canadian dollars (“CAD$”). The term “NSR” stands for net smelter royalty. The term “tpa” stands for tonnes per annum. Additional information relating to the Company is available on the Canadian Securities Administrators’ (the “CSA”) SEDAR website at www.sedar.com and on the United States Securities and Exchange Commission’s (the “SEC”) website at www.sec.gov.

EXECUTIVE SUMMARY

NextSource was continued under the Canada Business Corporations Act from the State of Minnesota to Canada on December 27, 2017 and has a fiscal year end of June 30. The Company’s registered head office and primary location of records is 130 King Street West, Exchange Tower, Suite 1940, Toronto, Ontario Canada, M5X 2A2. The Company’s common shares are listed on the Toronto Stock Exchange (the “TSX”) under the symbol “NEXT” and the OTCQB under the symbol “NSRCF”.

NextSource is principally engaged in the development of mineral resources and value-added processing of flake graphite and other minerals into materials used in the manufacturing of batteries and other applications. The Company accepts the risks which are inherent to mineral exploration and development programs and exposure to the cyclical nature of mineral and commodity prices. These risks are discussed in greater detail in the Risk Factors section of this MD&A.

The Company does not currently operate any mines and has not completed the construction of any mines. No commercial revenue has been generated to date.

On February 15, 2019, the Company obtained a mining permit for its Molo Graphite Mine, located in Madagascar. On February 8, 2021, the Company announced a binding financing package totaling USD$29.5 million for the construction of Phase 1 of the Molo Graphite Mine. On March 29, 2021, the Company initiated the construction process for the mine with the awarding of the engineering, procurement, and construction management contract.

Site works are expected to begin in late 2021 and commissioning of the plant is expected to begin in May 2022 followed by a ramp up to the Phase 1 processing plant capacity of 240,000 tpa of ore over a period of two to three months. At full Phase 1 capacity, the Molo Graphite Mine is expected to produce approximately 17,000 tpa of high-quality SuperFlake® graphite concentrate.

The Company has initiated a technical study for a Molo Graphite Mine Phase 2 production capacity expansion to target 150,000 tonnes per annum (“tpa”) of SuperFlake®. The Company has also initiated technical study related to its Green Giant Vanadium Project and in collaboration with its partners, has initiated a technical study related to value-added processing facilities capable of producing coated, spheronized and purified graphite.

Corporate Structure

NextSource owns 100% of NextSource Materials (Mauritius) Ltd. (“MATMAU”), a Mauritius subsidiary, and 2391938 Ontario Inc., an Ontario Company. MATMAU owns 100% of NextSource Minerals (Mauritius) Ltd. (“MINMAU”), a Mauritius subsidiary, NextSource Graphite (Mauritius) Ltd (“GRAMAU”), a Mauritius subsidiary, and NextSource Materials (Madagascar) SARLU (“MATMAD”), a Madagascar subsidiary. MINMAU owns 100% of NextSource Minerals (Madagascar) SARLU (“MINMAD”), a Madagascar subsidiary. GRAMAU owns 100% of ERG (Madagascar) SARLU (“ERGMAD”), a Madagascar.

Canada |

|

|

|

|

|

|

|

|

|

|

| NextSource Materials Inc. |

|

| |||||

|

|

|

| 100.0% |

| 100.0% |

|

|

|

|

|

|

|

|

| 2391938 Ontario Inc. |

| ||

Mauritius |

|

|

|

|

|

|

|

|

|

|

| NextSource Materials (Mauritius) Ltd. |

|

| |||||

|

|

|

|

|

|

| "MATMAU" |

|

|

|

| 100% |

|

|

| 100% |

|

|

|

NextSource Graphite (Mauritius) Ltd. |

|

| NextSource Minerals (Mauritius) Ltd. | ||||||

|

|

| "GRAMAU" |

|

|

|

|

| "MINMAU" |

Madagascar |

|

| 100% |

|

|

|

|

| |

|

|

| NextSource Materials (Madagascar) SARLU |

|

|

| |||

|

|

|

|

|

| "MATMAD" |

|

|

|

| 100% |

|

|

|

|

| 100% |

|

|

ERG (Madagascar) SARLU |

|

| NextSource Minerals (Madagascar) SARLU | ||||||

|

|

| "ERGMAD" |

|

|

|

|

| "MINMAD" |

| 3 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

Dividends and Distributions

The Company has yet to pay any dividends since inception and is unlikely to do so in the immediate or foreseeable future.

Employees and Contractors

The Company relies on the geological and industry expertise of its management team and engages contractors to complete certain aspects of its mine development, mineral exploration and evaluation programs, and development of value-added processing facilities.

As of June 30, 2021, in addition to the Board of Directors, President & Chief Executive Officer, Chief Financial Officer, Chief Operating Officer and SVP Corporate Development, the Company had 2 employees. Certain professional, administrative, mine development and mineral exploration and evaluation services are provided to the Company by independent contractors, including corporations and/or individuals who may be officers or directors of NextSource. No assurance can be given that qualified employees can be retained by NextSource when necessary.

Cautionary Note about Operating Losses

As of June 30, 2021, the Company had incurred recurring operating losses resulting in an accumulated deficit of $146,893,550. We anticipate incurring further operating losses until the completion of construction and successful commissioning of Phase 1 of the Molo Graphite Mine.

Operating cash flows from Phase 1 of the Molo Graphite Mine are not expected to be sufficient to fund the construction of the Phase 2 capacity expansion and construction of value-added processing facilities. Our future financial results are uncertain due to a number of factors, some of which are outside our Company’s control. These factors include, but are not limited to: (a) our ability to complete construction of Phase 1 of the Molo Graphite Mine on time and on budget; (b) our ability to raise funding to cover potential working capital shortfalls, subsequent Molo Graphite Mine capacity expansions, the construction of value-added processing facilities, the completion of new mineral exploration and evaluation programs, and the potential acquisition of new mineral exploration and evaluation projects; (c) the market price for graphite and vanadium, which could impact expected revenues following the commissioning of the Molo Graphite Mine; (d) the results of the exploration programs and metallurgical analysis of our mineral properties; (e) the political instability and/or environmental regulations that may adversely impact construction and operating costs for the Molo Graphite Mine and our ability to operate in Madagascar; and (f) our ability to find joint venture and/or off-take partners in order to advance the development of our mineral properties and value-added processing facilities. Any future equity financing will cause existing shareholders to experience dilution of their ownership interest in our Company.

If operating cash flows from the Molo Graphite Mine are insufficient to fund operations and we are not successful in raising additional financing, we anticipate the Company will not be able to proceed with all or part of its existing business plan. In which case the Company may decide to discontinue or modify the current business plan and seek other business opportunities. As a public company, the Company needs to maintain periodic filings with the appropriate regulatory authorities and will continue to incur legal, accounting, administrative and listing costs. In the event the Company cannot raise additional capital to sustain operations, and cannot find other business opportunities, we may be forced to discontinue the business. We do not have any specific alternative business opportunities under consideration and have not planned for any such contingency.

GENERAL DEVELOPMENT OF THE BUSINESS

Strategy

The Company is focused on becoming a key producer of raw and value-added materials used in the manufacturing of batteries and other applications. To achieve this, the Company’s strategy is to:

| · | Deliver on growth expectations by developing and operating mining projects and value-added materials processing facilities that will generate long-term free cash flows |

| · | Build and maintain a high-quality project pipeline to ensure we advance and develop successful projects |

| · | Adhere to the highest environmental, social and governance standards |

Three-Year History

On August 17, 2018, the Company closed a non-brokered private placement offering of 2,105,927 units at a price of $0.53 (CAD$0.70) per unit for aggregate gross proceeds of $1,120,385 (CAD$1,474,149). Each unit consisted of one common share and one-half common share purchase warrant, with each warrant exercisable into one common share at an exercise price of $0.76 (CAD$1.00) for a period of two years.

| 4 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

On October 16, 2018, the Company announced the signing of an Offtake Agreement with the primary graphite supplier to a major Japanese electric vehicle anode producer. The Offtake Agreement is for a period of ten (10) years and activates on the commencement of commercial production at the Molo project, with an automatic renewal for an additional five (5) years. The Japanese Partner will have the exclusive right to import and sell SuperFlake® graphite concentrate in Japan. Provided that commercial production commences within 3 years, following the ramp up period, the Japanese Partner will purchase 20,000 tonnes of SuperFlake® graphite per annum. Product prices will be negotiated on a per order basis between the parties and will be based on the floating market prices (FOB basis) prevailing in the region.

On February 15, 2019, the Company announced the Madagascar Government granted a 40-year mining license for the Molo Graphite Mine and that the mining license does not limit mining to any specific volume.

On March 7, 2019, the Company closed a non-brokered private placement offering of 1,608,643 common shares at a price of $0.80 (CAD$1.10) per common share for aggregate gross proceeds of $1,323,630 (CAD$1,769,507).

On April 11, 2019, the Company announced it had received the Global Environmental Permit for the Molo Graphite Mine from the Madagascar Ministry of Environment’s Office National pour l’Environnement (the National Office for the Environment; or “ONE”). This follows the completion of the Environmental & Social Impact Assessment (“ESIA”) and Relocation Action Plan (“RAP”) to International Finance Corporation (IFC) performance standards and World Bank standards, the completion of local and regional stakeholder and community engagement, and the completion of negotiations and signed agreements with all potentially affected land occupants to accept compensation for any affected crops and grazing land and relocation if needed.

On September 27, 2019, the Company reported the results of a new Feasibility Study (“FS”) for its 100%-owned Molo Graphite Project in southern Madagascar. The FS outlines a phased development approach with Phase 1 producing 17,000 tonnes per annum (“tpa”) over the first two years of production and Phase 2 producing a total of 45,000 tpa by year 3. Over the modelled life of mine (30 years), the production plants will have a pre-tax internal rate of return (“IRR”) of 43.1%, and a post-tax IRR of 36.2%. The pre-tax Net Present Value (“NPV”) at 8% discount rate will be US$237.1M, and the post-tax NPV will be US$184.3M. The FS results are summarized in further detail in the Mineral Development Projects section.

On October 24, 2019, the Company announced the successful registration of Molo SuperFlake® as a trademark in Canada. The successful registration of this trademark means that NextSource has the exclusive right to brand all of its natural flake graphite sold in Canada as Molo SuperFlake® from its Molo Graphite Project in Madagascar.

On October 25, 2019, the Company closed a non-brokered private placement offering of 2,907,777 units at a price of $0.34 (CAD$0.45) per unit for aggregate gross proceeds of $998,620 (CAD$1,308,500). Each unit consisted of one common share and one-half common share purchase warrant, with each warrant exercisable into one common share at an exercise price of $0.70 (CAD$0.90) for a period of two years. There were no finder’s fees in relation to the private placement.

On September 27, 2019, Quentin Yarie resigned as a director of the Company.

On December 2, 2019, Christopher Kruba and David McNeely became directors of the Company.

On January 23, 2020, John Sanderson and Dalton Larson resigned as directors of the Company and Dean Comand was appointed as Chair of the Board of Directors.

On April 9, 2020, the Company announced that it executed a Letter of Agreement (“LOI”) with its Japanese offtake partner and a leading Chinese processor of graphite anode material to collaborate on the construction of a value-add, battery anode plant in a jurisdiction that is proximal to the Company’s Molo Graphite Mine project in Madagascar.

On July 2, 2020, the Company completed a non-brokered private placement of 6,157,887 units at a price of $0.24 (CAD$0.325) per unit for gross proceeds of $1,476,571 (CAD$2,001,310). Each unit consisted of one common share of the Company and one-half of one common share purchase warrant, with each full warrant entitling the holder to acquire one additional common share of the Company at a price of $0.48 (CAD$0.65) per share for a period of 24 months. No finder fees or commissions were paid in association with the private placement. In connection with the non-brokered private placement, the Company incurred $9,293 in share issuance costs.

On July 20, 2020, Brett Whalen became a director of the Company. On August 24, 2020, the Company announced the appointment of Brett Whalen as Chair of the Board of Directors.

| 5 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

On February 8, 2021, the Company announced that it entered into a binding agreement with Vision Blue Resources Limited (“Vision Blue”) to provide a financing package (the “Financing Package”) for total gross proceeds of USD$29.5M. The proceeds of the Financing Package will be used to complete construction of Phase 1 of the Company’s Molo Graphite Mine. The Financing Package consisted of an initial private placement of $6.0 million that was completed on March 15, 2021, a second private placement for $12.5 million that was completed on May 19, 2021, and a royalty financing that was completed on June 28, 2021, when the Company received an initial $8.0 million, less a $1.5 million royalty financing fee, and will receive another $3.0 million once it has reached 80% of capital expenditures related to the construction of the Molo Graphite Mine. The Molo Graphite Mine will be subject to minimum royalty payments and a 3.0% royalty. The Green Giant Vanadium Project will be subject to a 1.0% royalty. In connection with the initial private placement, the Company granted Vision Blue the right to appoint two directors to the Board of the Company. The Chairman of Vision Blue, Sir Mick Davis, was appointed as Chair of the Board of Directors of the Company on March 15, 2021. The second Vision Blue appointee, Ian Pearce, was appointed to the Board of Directors of the Company on July 14, 2021. Vision Blue was granted a right of first refusal to finance the Phase 2 expansion of the Molo Graphite Mine, and if Vision Blue holds common shares representing at least 10% of the issued and outstanding common shares, a right to participate in future equity financings on the same terms as such financing to maintain its ownership percentage in the Company. Vision Blue is subject to a 1-year lock-up from the closing of the Initial Private Placement with a periodic release schedule. In addition, each of the Directors and Officers of the Company have agreed to similar lock-up periods for the securities they hold.

On March 15, 2021, the Company completed the initial private placement with Vision Blue consisting of 12,000,000 common shares at a price of CAD$0.65 per share for total gross proceeds of $6,000,000 (CAD$7,800,000). In connection with the non-brokered private placement, the Company incurred $16,367 in share issuance costs. The Company also announced the appointment of Mick Davis as Chair of the Board of Directors.

On March 29, 2021, the Company announced the initiation of the construction process for the Molo Graphite Mine in Madagascar with the awarding of the engineering, procurement, and construction management contract.

On April 12, 2021, the Company announced a binding partnership agreement to construct and operate its own turnkey spheronized and purified graphite (“SPG”) production facility. SPG is a key component of lithium-ion batteries such as those used in electric vehicle (“EV”) and hybrid vehicle applications. The partnership involves Japanese and Chinese companies that currently operate their own SPG facilities that provide SPG to leading Japanese lithium-ion battery makers that are within the supply chains of Tesla and other major EV automotive companies. Proposed locations for the facility include South Africa, Europe, or North America. The Company will determine the initial production capacity and will then initiate a technical study to determine capital and operating costs for the proposed locations. Construction of one or more of these SPG production facilities will be subject to obtaining a positive technical study and securing sufficient funding for construction and initial working capital. Commissioning of the first SPG production facility is being targeted for Q4 2022. The Chinese partner will design and develop the process flowsheets, source all necessary graphite processing equipment, and will provide all the necessary training and operational know-how necessary for the production SPG material. In return, the Chinese partner will receive a 3% licensing fee based on the total annual sales value of anode material sold. The Japanese partner will leverage its sales relationships and will act as NextSource’s exclusive agent for sales, marketing and trading of anode battery materials sold to OEM anode suppliers and to OEMs directly. In return, the Japanese partner will receive a 5% sales commission based on the total annual sales value of anode battery material sold.

On May 11, 2021, the Company announced it initiated the procurement of processing plant equipment for the Molo Graphite Mine.

On May 19, 2021, the Company completed the second private placement with Vision Blue consisting of 23,214,286 units at a price of CAD$0.65 per unit for total gross proceeds of $12,500,000 (CAD$15,089,286). Each unit consisted of one common share of the Company and one common share purchase warrant, with each warrant entitling the holder to acquire one additional common share of the Company at a price of CAD$1.00 per share for a period of 24 months. No finder fees or commissions were paid in association with the private placement. In connection with the non-brokered private placement, the Company incurred $87,788 in share issuance costs.

On May 25, 2021, the Company announced that following a multi-year verification process, thyssenkrupp entered into a long-term partnership with NextSource and signed an offtake agreement to secure SuperFlake® graphite concentrate for their refractories/foundries, expandable graphite (graphite foil) and battery anode production businesses. The key highlights are:

| · | Commercial agreement for the sale of 35,000 tpa of SuperFlake® graphite concentrate from the Molo mine |

| · | 10-year term with an automatic 5-year extension |

| · | Products under the agreement pertain to refractory, battery anode production and expandable graphite (graphite foil) markets |

| · | Geographical regions include, but are not limited to, Europe, the UK, North America, Mexico, China and South Korea |

| · | Minimum 7,300 tpa during Phase 1 initial production |

| · | Ramp up to 35,000 tpa in Phase 2 |

| · | Shipments in Phase 1 will be used to verify run-of-mill production to trigger the larger volume expansion |

On June 23, 2021, the Company announced the initiation of a technical study for a Phase 2 production capacity to target 150,000 tpa of SuperFlake® for its Molo Graphite Mine in Madagascar. This is an increase from the 2019 Feasibility Study hat considered a Phase 2 production capacity of 45,000 tpa. The new minimum targeted capacity was determined after recent discussions with our flake graphite offtake partners and with our partnership for the construction of a battery anode facility (“BAF”) to produce spheronized and purified graphite (“SPG”). The purpose of the technical study is to determine the project economics pertaining to this increase in targeted production for Phase 2.

On June 28, 2021, the Company received the royalty funding from Vision Blue consisting of $8.0 million, less a US$1.5 million royalty financing fee. The Company will receive a further $3.0 million upon achieving 80% of capital expenditures related to the construction of the mine, which is expected to be reached on or around December 31, 2021. In return for the royalty funding, the Company will pay to Vision Blue the greater of: (i) US$1.65 million per annum or (ii) 3% of the gross revenues from SuperFlake® concentrate sales (the “GSR”). Once Vision Blue has received a cumulative royalty payment of US$16.5 million, the GSR will be calculated as 3% of the gross revenues from the Company’s SuperFlake® sales. NextSource will have the option at any time to reduce the GSR to 2.25% upon payment to Vision Blue of US$20 million. The Company may delay the first-year minimum repayments, which will become subject to accrued interest of 15% per annum. Vision Blue will also receive a royalty of 1.0% of the gross revenues from sales of vanadium pentoxide (“V2O5”) from the Green Giant Vanadium Project for a period of 15 years following commencement of production of V2O5.

| 6 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

On July 14, 2021, the Company announced the appointment of Ian Pearce to the Board of Directors and the resignation of David McNeely as a Director of the Company.

On July 22, 2021, the Company announce that it has been accepted as a member of both the European Battery Alliance (“EBA”) and the European Raw Materials Alliance (“ERMA”).

On September 8, 2021, the Company announced it intends to assess emerging opportunities to accelerate expansion through the potential acquisition and development of additional metals and mineral assets that are expected to play a vital role in clean energy technologies.

MINERAL DEVELOPMENT PROJECTS

The following section contains “forward-looking statements” and “forward-looking information” within the meaning of applicable securities laws. The Company continues to monitor the implications of the Covid-19 Pandemic. The manner and extent that the pandemic, and measures taken as a result of the pandemic by governments and others, will affect the Company in ways that cannot be predicted with certainty. See the Cautionary Statement Regarding Forward-Looking Information and Uncertainty due to the Covid-19 Pandemic in this MD&A for a discussion of assumptions and risks relating to such statements and information and a discussion of certain risks facing the Company relating to the pandemic.

Molo Graphite Mine, Southern Madagascar Region, Madagascar

Overview and Project Plan

The Molo Graphite Mine project is located near the town of Fotadrevo in the Province of Toliara, Madagascar.

On February 15, 2019, the Company announced the Madagascar Government granted a 40-year mining license for the Molo Graphite Mine and that the mining license does not limit mining to any specific volume.

On March 29, 2021, the Company announced the initiation of the construction process for the Molo Graphite Mine in Madagascar with the awarding of the engineering, procurement, and construction management contract.

On May 11, 2021, the Company announced it initiated the procurement of processing plant equipment for the Molo Graphite Mine.

| 7 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

Total construction costs excluding working capital have been estimated at $21.7 million. All construction activities are expected to be completed by June 30, 2022. As of June 30, 2021, the Company had already incurred $3.6 million in capital costs and the remaining construction costs were estimated at approximately $18.4 million, mine working capital requirements were estimated at approximately $1.3 million, and general and administrative expenditures until June 30, 2022 were estimated at $3.0 million. As part of the royalty financing agreement, the Company will receive a further $3.0 million from Vision Blue upon achieving 80% of capital expenditures related to the construction of the mine, which is expected to be reached on or around December 31, 2021. As a result, the Company believes its capital resources will be sufficient to complete construction of the mine and to fund mine working capital and general and administrative expenditures.

The processing plant equipment is currently being assembled offshore and is expected to begin arriving in Madagascar in late 2021 and will then be transported overland and installed at the mine site in Q1 2022. Mine-site construction activities are expected to begin in late 2021. Open pit pre-production mining activities are expected to begin in Q1 2022. Commissioning of the plant is expected to begin in May 2022, followed by a ramp up over a period of two to three months to the Phase 1 nameplate capacity of 240,000 tpa of ore. At full Phase 1 capacity, the Molo Graphite Mine is expected to produce approximately 17,000 tpa of high-quality SuperFlake® graphite concentrate.

The application for all necessary permits to construct and operate the mine, including water use, facilities construction, mineral processing, transportation, export, and labour have been initiated and are expected to be obtained as they are required.

The following is a rendering of the completed Phase 1 processing plant:

Phase 2 Expansion

On June 23, 2021, the Company announced the initiation of a technical study for a Phase 2 production capacity to target 150,000 tpa of SuperFlake® for its Molo Graphite Mine in Madagascar. This is an increase from the 2019 Feasibility Study, which considered a Phase 2 production capacity of 45,000 tpa.

The expanded Phase 2 production capacity was determined after recent discussions with our flake graphite offtake partners and with our partnership for the construction of a value-added processing facility to produce spheronized graphite (“SPG”). The purpose of the technical study is to determine the project economics for the expanded Phase 2.

Construction of the Phase 2 expansion is expected to begin after completion of Phase 1 and is subject to the technical report supporting positive economics and obtaining sufficient funding to complete construction.

Global market for and supply of flake graphite

Benchmark Intelligence estimated that global flake graphite demand in 2020 was approximately 900,000 tonnes and is expected to increase significantly over the next ten years due to increasing demand for lithium-ion batteries used in electric vehicles. A rule of thumb is that approximately 1.1 tonnes of flake graphite (2,500 lbs) is required for each 1GWh of electric vehicle capacity. Benchmark Intelligence has further estimated that global battery manufacturing capacity in 2020 was approximately 755 GWh and is set to increase by 2030 to 3,400 GWh through the construction of up to 200 new gigafactories. As a result, global flake graphite demand in 2030 is estimated at approximately 4,000,000 tonnes, which exceeds the existing global supply.

| 8 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

Benchmark Intelligence estimated that the global flake graphite market was in relative balance in recent years but has moved from an oversupply of 226,000 tpa in 2018 to a deficit of approximately 60,000 tpa in 2021. Flake graphite demand is forecast to exceed global supply by approximately 430,000 tpa by 2026 and increasing to approximately 1,888,000 tpa by 2030. The supply response for natural flake graphite is expected to be constrained by technical challenges, capital costs, development timelines and operating economics. The supply response for synthetic flake graphite is expected to be constrained by the economics and availability of petroleum needle coke, which is its primary raw material feedstock for synthetic graphite and is also in demand for use in the steel making industry.

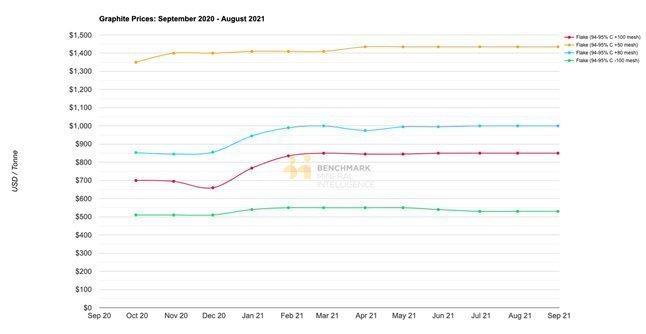

As an industrial mineral, flake graphite pricing is determined by three factors: 1) flake size, 2) carbon purity and 3) industry-specific technical attributes of the flakes. Flake sizing is broadly classified into four ranges: small (-100 mesh, or <75µm) medium (-80 to 100 mesh, or 75µm to 180µm), large (-50 to 80 mesh, or 180µm to 300µm), and extra-large or jumbo (+50 mesh, or >300µm). These flake sizes are in turn classified by carbon content (“C”), and are typically sold in ranges of 88-93% C, 94-95% C, and 95-97% C. The specific technical attributes of the flakes are then defined by end-user parameters such as expansion coefficient, thermal and electrical conductivity, and charge-discharge stability and efficiency. Larger flake size is generally sold at a premium to smaller flake sizes, and higher purity products (e.g., above 94%) are sold at a premium to lower purity products. Pricing is further impacted by the regional location of supply.

Transactions in the flake graphite market are generally based on private negotiations between buyers and sellers, as a result there is no spot or forward market. Research companies such as Benchmark Mineral Intelligence (“Benchmark”) and Roskill Information Services (“Roskill”) estimate current and historical pricing based on their proprietary market research and publish forward estimates for select grades and product types. Benchmark has estimated the following average FOB China 94-95% C flake graphite market prices for different mesh sizes during the past 12 months. Benchmark has not estimated the flake graphite market prices for 96-98% C flake graphite, which is the yield expected to be produced by the Molo Graphite Mine and is typically sold at a premium to 94-95% C flake graphite.

Sales, Marketing and Offtakes of SuperFlake® Graphite

Independent testing by various third-party end users of flake graphite was announced by the Company in 2015 that confirmed that flake graphite concentrates from the Molo Graphite Mine meets or exceeds quality requirements for all major end-markets of natural flake graphite. The major end-markets for flake graphite include refractories, graphite anode materials used in lithium-ion batteries, specialty graphite foils used as essential components in the chemical, aeronautical and fire-retardant industries, and graphene used in high-end ink and substrate applications.

The Feasibility Study confirmed that Molo flake graphite concentrate has an excellent flake size distribution that is well above the global average, with 46.4% classified as +80 mesh (large), +65 mesh (extra-large) and +48 mesh (jumbo) mesh in flake size, which includes 23.6% as +48 mesh and greater in flake size. The concentrate also has excellent thermal expansion, can be upgraded to 99.97% purity and contains no deleterious substances and has high crystallinity.

In response, NextSource has registered SuperFlake® as a trademark for the Molo flake graphite concentrate in the United States, Canada, Japan, South Korea, U.K. and the European Union. These are the top demand markets for flake graphite and the countries where NextSource intends to sell its SuperFlake® graphite material.

| 9 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

The Company expects to sell most of the flake graphite produced at the Molo Graphite Mine through offtakes with several key customers.

On October 16, 2018, the Company announced a binding offtake agreement for the supply of SuperFlake® graphite concentrate with a prominent Japanese Trading Company that is a primary supplier of flake graphite to a major Japanese electric vehicle anode producer. To protect certain confidential aspects of the agreement, the Japanese Trading Company and the Japanese electric vehicle anode producer requested not to be identified. The key highlights are:

| · | Offtake is for a period of ten (10) years, beginning at the start of commercial production at the Molo Graphite Mine, with an automatic renewal for an additional five (5) years. |

| · | Exclusive right to import and sell SuperFlake® graphite concentrate in Japan. |

| · | Provided that commercial production commences within 3 years, following the ramp up period, the Japanese Partner will purchase 20,000 tonnes of SuperFlake® graphite per annum. |

| · | Product prices will be negotiated on a per order basis between the parties and will be based on the market prices (FOB basis) prevailing in the region. |

On May 25, 2021, the Company announced that following a multi-year verification process, thyssenkrupp entered into a long-term partnership with NextSource and signed an offtake agreement to secure SuperFlake® graphite concentrate for their refractories/foundries, expandable graphite (graphite foil) and battery anode production businesses. The key highlights are:

| · | Commercial agreement for the sale of 35,000 tpa of SuperFlake® graphite concentrate from the Molo mine |

| · | 10-year term with an automatic 5-year extension |

| · | Products under the agreement pertain to refractory, battery anode production and expandable graphite (graphite foil) markets |

| · | Geographical regions include, but are not limited to, Europe, the UK, North America, Mexico, China and South Korea |

| · | Minimum 7,300 tpa during Phase 1 initial production |

| · | Ramp up to 35,000 tpa in Phase 2 |

| · | Shipments in Phase 1 will be used to verify run-of-mill production to trigger the larger volume expansion |

Royalty

On June 28, 2021, the Company received the royalty funding from Vision Blue consisting of $8.0 million, less a US$1.5 million royalty financing fee. The Company will receive a further $3.0 million upon achieving 80% of capital expenditures related to the construction of the mine, which is expected to be reached on or around December 31, 2021. In return for the royalty funding, the Company will pay to Vision Blue the greater of: (i) US$1.65 million per annum or (ii) 3% of the gross revenues from SuperFlake® concentrate sales (the “GSR”). Once Vision Blue has received a cumulative royalty payment of US$16.5 million, the GSR will be calculated as 3% of the gross revenues from the Company’s SuperFlake® sales. NextSource will have the option at any time to reduce the GSR to 2.25% upon payment to Vision Blue of US$20 million. The Company may delay each individual minimum payments for a period of 12 months, whereby each deferred payment will be subject to accrued interest of 15% per annum. At this time, the Company expects to defer the minimum payments and as a result, the first minimum payment is expected to be completed on June 30, 2023.

Exploration and Evaluation

The Molo Graphite Project is one of seven surficial graphite trends discovered and drill tested by NextSource in late 2011 and announced to the market in early January 2012. The Molo deposit itself occurs in a flat, sparsely populated and dry savannah grassland region that has easy access via a network of seasonal secondary roads.

The Molo Graphite Project graphitic zone consists of multi-folded graphitic strata at surface with an exposed strike length of over two kilometres. Outcrop mapping and trenching on the Molo Graphite Project has shown the surface geology to be dominated by resistant ridges of graphitic schist and graphitic gneiss, as well as abundant graphitic schist float. Geological modeling has shown that the Molo Graphite Project deposit consists of various zones of mineralized graphitic gneiss, with a barren footwall composed of garnetiferous gneiss. The host rock of the mineralized zones on the Molo Graphite Project is graphitic gneiss.

Resource delineation, drilling and trenching on the Molo Graphite Project took place between May and November of 2012. This resulted in a maiden mineral resource estimate that formed the basis for the Company’s Preliminary Economic Assessment (the “PEA”), which was undertaken by DRA Mineral Projects and released in 2013.

The positive outcome of the PEA led NextSource to undertake another phase of exploratory drilling and sampling in 2014 to upgrade the deposit and its contained mineral resources to mineral reserves. The process included an additional 32 diamond drill holes (totaling 2,063 metres) and 9 trenches (totaling 1,876 metres). The entire database upon which the upgraded resource estimate was based contained 80 drill holes (totaling 11,660 metres) and 35 trenches (totaling 8,492 metres). This mineral resource formed the basis of the first feasibility study, which was released in February 2015, and for the September 2019 Feasibility Study.

The resource remains open along strike and to depth. The Company does not have any immediate plans to complete any further drilling to expand the resource.

| 10 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

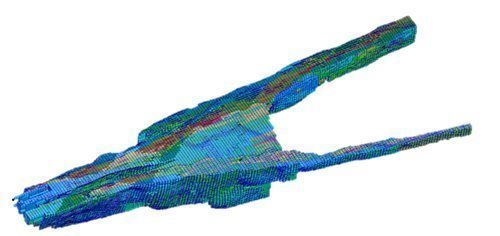

Resource and Reserve Estimate

The current mineral resource estimate for the Molo Graphite Project is summarised below consisting of the resource categories, the tonnage, the carbon grade (“C%”) and the contained graphite (“C”) tonnage. A cut-off grade of 4% C was used for the “higher grade” zones and 2% C for the “lower grade” zones. The mineral resources are classified in the Measured, Indicated and Inferred categories as defined by the Canadian Institute of Mining, Metallurgy and Petroleum definition standards.

Classification | Tonnage (Mt) | Grade (C%) | Graphite (C Mt) |

Measured | 23.62 | 6.32% | 1.49 |

Indicated | 76.75 | 6.25% | 4.80 |

Measured & Indicated | 100.37 | 6.30% | 6.29 |

Inferred | 40.91 | 5.78% | 2.36 |

The Mineral Resources above are inclusive of the Mineral Reserves below.

Classification | Tonnage (Mt) | Grade (C%) |

Proven | 14.17 | 7.00% |

Probable | 8.37 | 7.04% |

Proven & Probable | 22.44 | 7.02% |

Readers are cautioned to refer to the 2019 Feasibility Study for all the material assumptions, qualifications and verification procedures relating to the current mineral resource and mineral reserve estimate for the Molo Graphite Project.

The following is a graphical representation of the shape of the mineral resource, which has been extracted from the 2019 Feasibility Study.

History

On December 14, 2011, the Company entered into a Definitive Joint Venture Agreement (“JVA”) with Malagasy Minerals Limited (“Malagasy”), a public company listed on the Australian Stock Exchange, to acquire a 75% interest in a property package for the exploration and development of industrial minerals, including graphite, vanadium and 25 other minerals. The land position consisted of 2,119 permits covering 827.7 square kilometers and is mostly adjacent towards the south and east with the Company’s 100% owned Green Giant Vanadium Project. Pursuant to the JVA, the Company paid $2,261,690 and issued 750,000 common shares that were valued at $1,350,000.

On April 16, 2014, the Company signed a Sale and Purchase Agreement and a Mineral Rights Agreement (together “the Agreements”) with Malagasy to acquire the remaining 25% interest, subject to Malagasy retaining a 1.5% net smelter royalty. Pursuant to the Agreements, the Company paid $364,480 (CAD$400,000), issued 250,000 common shares subject to a 12-month voluntary vesting period that were valued at $325,000 and issued 350,000 common share purchase warrants, which were valued at $320,950 using Black‑Scholes, with an exercise price of $0.14 and an expiry date of April 15, 2019. On May 20, 2015, upon completion of a bankable feasibility study (“BFS”) for the Molo Graphite Property, the Company paid $546,000 (CAD$700,000) and issued 100,000 common shares, which were valued at $100,000. A further cash payment of approximately $771,510 (CAD$1,000,000) will be due within five days of the commencement of commercial production. The Company also acquired a 100% interest in the industrial mineral rights on approximately 1 ½ additional claim blocks covering 10,811 hectares adjoining the east side of the Molo Graphite Property. Prior to becoming a Director of the Company, Brett Whalen purchased an option to acquire the 1.5% NSR from Malagasy, upon the mine achieving commercial production, in return for a further payment to Malagasy.

| 11 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

The Molo Graphite Project is located within Exploration Permit #3432 (“PR 3432”) as issued by the Bureau de Cadastre Minier de Madagascar (“BCMM”) pursuant to the Mining Code 1999 (as amended) and its implementing decrees. The Molo Graphite Project exploration permit PR 3432 is currently held under the name of our Madagascar subsidiary, which has paid all taxes and administrative fees to the Madagascar government and its mining ministry with respect to all the mining permits held in country. These taxes and administrative fee payments have been acknowledged and accepted by the Madagascar government.

On June 1, 2017, we released the results of an updated Molo Feasibility Study utilizing a fully modular approach which was based on the FEED Study and subsequent detailed engineering studies.

During fiscal 2017, the Company applied to the BCMM to have the exploration permit for the Molo Graphite Project converted into a mining permit.

Following an Environmental Legal Review and an Environmental and Social Screening Assessment, which provided crucial information to align the project’s development and design with international best practice on sustainable project development, the Company completed a comprehensive Environmental and Social Impact Assessment (“ESIA”), which was developed to local Madagascar (“Malagasy”), Equator Principles, World Bank and International Finance Corporation (“IFC”) standards. The ESIA was submitted to the Office National d’Environment (“ONE”) (the Madagascar Environment Ministry) during fiscal 2018.

On February 15, 2019, the Company announced the Madagascar Government granted a 40-year mining license for the Molo Graphite Mine and that the mining license does not limit mining to any specific volume.

On April 11, 2019, the Company announced it had received the Global Environmental Permit (“GEP”) for the Molo Graphite Mine from the Madagascar Ministry of Environment’s Office National pour l’Environnement (the National Office for the Environment; or “ONE”). The GEP was based on ESIA and a Relocation Action Plan (“RAP”) that involved the completion of local and regional stakeholder and community engagement, and the completion of negotiations and signed agreements with all potentially affected land occupants to accept compensation for any affected crops and grazing land and relocation if needed.

On September 27, 2019, the Company reported the results of an updated Feasibility Study (“FS”) consisting of two phases:

PHASE 1: Production of 17,000 tpa of graphite concentrate

The first phase of production will consist of a fully operational and sustainable graphite mine with a permanent processing plant capable of processing 240,000 tpa of ore producing approximately 17,000 tpa of graphite concentrate per year over a 30-year life of mine. The estimated capital costs for Phase 1 including contingencies were estimated at US$21.0 million and construction was expected to take approximately 12 months to complete. Phase 1 costs including contingency and working capital were estimated at US$24.1 million.

PHASE 2: Production expansion to 45,000 tpa of graphite concentrate in Year 3

Phase 2 assumes that Phase 1 is achieved and operates for two years followed by the completion of the Phase 2 expansion in the third year resulting in a combined 720,000 tpa of ore producing 45,000 tpa of graphite concentrate per year over a 30-year life of mine. The Phase 2 expansion is based on the construction of two additional Phase 1 processing plant modules over a construction period of 12 months. Phase 2 capital costs including all Phase 1 capital costs and contingency were estimated at US$60.1 million. Phase 2 capital costs including all Phase 1 capital costs, contingency and working capital were estimated at US$67.4 million. Additional sustaining capital for equipment replacement over the 30-year life of mine and closure costs was estimated at $3.3 million.

On February 8, 2021, the Company announced that it entered into a binding agreement with Vision Blue to provide the Financing Package for total gross proceeds of USD$29.5M. The proceeds of the Financing Package will be used to complete construction of Phase 1 of the Company’s Molo Graphite Mine. The Financing Package consisted of an initial private placement of $6.0 million that was completed on March 15, 2021, a second private placement for $12.5 million that was completed on May 19, 2021, and a royalty financing agreement that was completed on June 28, 2021, when the Company received an initial $8.0 million, less a $1.5 million royalty financing fee, and will receive another $3.0 million once it has reached 80% of capital expenditures related to the construction of the Molo Graphite Mine. The Molo Graphite Mine will be subject to minimum royalty payments and a 3.0% royalty. Vision Blue was granted a right of first refusal to finance the Phase 2 expansion of the Molo Graphite Mine.

On March 29, 2021, the Company announced the initiation of the construction process for the Molo Graphite Mine in Madagascar with the awarding of the engineering, procurement, and construction management contract.

On May 11, 2021, the Company announced it initiated the procurement of processing plant equipment, which will be assembled offshore then shipped to Madagascar in late 2021.

| 12 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

Feasibility Study Summary

On September 27, 2019, the Company reported the results of an updated Feasibility Study (“FS”) consisting of two phases. Phase 1 consisted of production of 17,000 tpa of finished SuperFlake® concentrate for the first two years of production, followed by an expansion to Phase 2 production of 45,000 tpa. The FS considered mine capital equipment and mining costs, as well as the 12-month rolling flake graphite pricing on a Freight-on-Board (“FOB”) China basis, supplied by UK-based battery mineral commodities research firm, Benchmark Minerals Intelligence. The FS incorporated the procurement of all mining equipment, off-site modular fabrication and assembly, factory acceptance testing, module disassembly, shipping, plant infrastructure construction, onsite module re-assembly, commissioning, project contingencies and working capital. All capital and operating costs expressed for Phase 1 are accurate to +/- 10%, and Phase 2 are accurate to +/- 12.5%.

Description |

| Phase 1 and 2 |

| |||||

|

| Pre-Tax |

|

| Post-Tax |

| ||

NPV (8% Discount Cash Flow)(1)(2) |

| $237.1 million |

|

| $184.3 million |

| ||

IRR (1)(2) |

|

| 43.1 | % |

|

| 36.2 | % |

Payback (2) |

| 3.4 years |

|

| 3.8 years |

| ||

Capital cost (“CAPEX”) |

| $ | 60,082,340 |

|

|

|

|

|

Owners Contingency |

| $ | 6,670,430 |

|

|

|

|

|

On-site Mining Costs (“OPEX”) per tonne of concentrate, (year 3 onward) |

| $ | 82.69 |

|

|

|

|

|

On-site Processing Costs (“OPEX”) per tonne of concentrate, (year 3 onward) |

| $ | 270.27 |

|

|

|

|

|

Transportation per tonne of concentrate (mine site to Madagascar Port year 3 onward) |

| $ | 133.01 |

|

|

|

|

|

Average annual production of concentrate |

| 45,136 tonne |

|

|

|

|

| |

Life of Mine (“LOM”) |

| 30 years |

|

|

|

|

| |

Graphite concentrate sale price (US$/tonne at Start Up - 2017) |

| $ | 1,208 |

|

|

|

|

|

Average Head Grade |

|

| 7.1 | % |

|

|

|

|

Average ore mined per annum over Life of Mine |

| 720,000 tonne |

|

|

|

|

| |

Average stripping ratio |

| 0.53:1 |

|

|

|

|

| |

Average carbon recovery |

|

| 88.30 | % |

|

|

|

|

Notes:

(1) Assumes Project is financed with 100% equity. Unless otherwise noted, all monetary figures presented are expressed in US dollars (USD).

(2) CAPEX includes process equipment, civil & infrastructure, mining, buildings, electrical infrastructure, project & construction services. Values shown are based on real graphite sales pricing

CAPEX and Working Capital |

| Phase 1 (240ktpa) |

|

| Phase 1 and 2 (720ktpa) |

| ||

Process Equipment |

| $ | 8,438,609 |

|

| $ | 25,315,827 |

|

Civil & Infrastructure |

| $ | 2,103,672 |

|

| $ | 6,661,016 |

|

Tailings |

| $ | 0.00 |

|

| $ | 0.00 |

|

Mining |

| $ | 2,574,143 |

|

| $ | 4,913,341 |

|

Buildings |

| $ | 1,154,609 |

|

| $ | 2,886,523 |

|

Electrical Infrastructure |

| $ | 128,804 |

|

| $ | 386,412 |

|

Project Services/EPCM |

| $ | 931,481 |

|

| $ | 2,794,445 |

|

Construction Services |

| $ | 1,474,775 |

|

| $ | 3,686,937 |

|

Indirect Costs |

| $ | 372,750 |

|

| $ | 1,118,250 |

|

Environmental & Permitting costs |

| $ | 729,827 |

|

| $ | 1,459,655 |

|

Owner’s Costs |

| $ | 1,197,000 |

|

| $ | 4,189,500 |

|

Sub-total |

| $ | 19,105,673 |

|

| $ | 53,411,909 |

|

Contingency (10%/12.5%) |

| $ | 1,910,567 |

|

| $ | 6,676,488 |

|

3 Months Working Capital |

| $ | 3,100,000 |

|

| $ | 7,300,000 |

|

CAPEX AND WORKING CAPITAL TOTAL |

| $ | 24,116,241 |

|

| $ | 67,388,398 |

|

Sustaining CAPEX over Life of Mine |

|

|

|

|

| $ | 3,300,000 |

|

| 13 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

Operating Costs |

| Phase 1 |

|

| Phase 2 |

| ||

|

| Operating cost |

| |||||

Mining (US$/T) |

|

| 102.81 |

|

|

| 65.34 |

|

Processing (US$/T) |

|

| 265.82 |

|

|

| 265.82 |

|

Trucking to local port / Ft. Dauphin (US$/T) |

|

| 133.01 |

|

|

| 133.01 |

|

General and Administration (US$/T) |

|

| 64.29 |

|

|

| 50.00 |

|

TOTAL |

| $ | 565.93 |

|

| $ | 514.17 |

|

The 2019 Feasibility Study technical report has been filed under the Company’s profile and on SEDAR at www.sedar.com, and is posted on NextSource’s website at www.nextsourcematerials.com. Please see “Molo Feasibility Study, National Instrument 43-101 Technical Report on the Molo Graphite Project located near the village of Fotadrevo in the Province of Toliara, Madagascar Prepared by Erudite Strategies (Pty) Ltd” dated May 31, 2019 for certain other details and assumptions relating to the above mineral resource and reserve estimates and data verification procedures.

The 2019 Feasibility Study was prepared in accordance with National Instrument 43-101 standards by Mr. Johann de Bruin, Pr. Eng. Mr. de Bruin is the Qualified Person who verified the technical data using industry acceptable standards and signed off on the relevant sections in the 43-101 report filed on SEDAR.

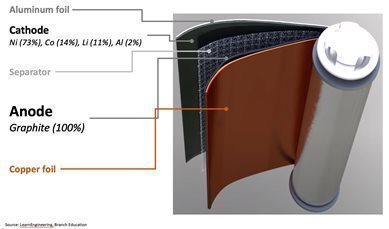

VALUE-ADDED MATERIAL PROCESSING FACILITY

The Company is currently evaluating the construction of value-added processing facilities that can convert flake graphite into spheronized and purified graphite (“SPG”) and coated spheronized graphite (“CSPG”). The coated spheronized purified graphite is then sold to battery manufacturers, where it is rolled into an anode and is assembled with other components into a finished battery. The following is a representation of a conversion process and the typical battery with the approximate composition of the primary components:

The SPG and CSPG produced from the value-added processing facilities can be sold at significantly greater prices per tonne than flake graphite. Transactions in the SPG and CSPG market are generally based on private negotiations between buyers and sellers, as a result there is no spot or forward market. Research companies such as Benchmark and Roskill estimate current and historical pricing based on their proprietary market research and publish forward estimates for select grades and product types. According to Roskill, the average price of CSPG imported into China in 2019 and 2020 were USD$7,157 per tonne and USD$7,307 per tonne, respectively.

On April 12, 2021, the Company announced a binding partnership agreement to construct and operate its own turnkey spheronized and purified graphite (“SPG”) production facility. SPG is a key component of lithium-ion batteries such as those used in electric vehicle (“EV”) and hybrid vehicle applications. The partnership involves Japanese and Chinese companies that currently operate their own SPG and CSPG facilities that provide SPG and CSPG to leading Japanese lithium-ion battery makers that are within the supply chains of Tesla and other major EV automotive companies.

| 14 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

| · | The Chinese partner will design and develop the process flowsheets, source all necessary graphite processing equipment, and will provide all the necessary training and operational know-how necessary for the production SPG material. In return, the Chinese partner will receive a 3% licensing fee based on the total annual sales value of anode material sold. |

|

|

|

| · | The Japanese partner will leverage its sales relationships and will act as NextSource’s exclusive agent for sales, marketing and trading of battery (graphite) anode material sold to OEM anode suppliers and to OEMs directly. In return, the Japanese partner will receive a 5% sales commission based on the total annual sales value of anode battery material sold. |

The Company is currently working with its partners to determine the initial production capacity and will complete a technical study to determine capital and operating costs based on proposed locations. Proposed locations for the value-added facility include South Africa, Europe, or North America.

Construction of one or more of these SPG production facilities will be subject to obtaining a positive technical study and securing sufficient funding for construction and initial working capital. Completion of the technical report is expected in late 2021 with a construction decision in early 2022. Construction of the first value-added production facility could begin in mid-2022 followed by commissioning in late 2022.

MINERAL EXPLORATION PROJECTS

Green Giant Vanadium Project, Province of Toliara, Madagascar

Overview and Project Plan

The Green Giant Vanadium Project is located 15 kilometres from the Molo Graphite Project and hosts a large sedimentary-hosted vanadium deposit.

Since early 2012, the Company has focused its efforts on the Molo Graphite Project and as such only limited work has been completed on the Green Giant Vanadium Project since that time.

The Company plans to complete additional metallurgical evaluation of the property during the next 12 months to establish a mineral processing flow sheet.

Royalty

On June 28, 2021, the Company received the royalty funding from Vision Blue for the construction of the Molo Graphite Mine. As part of the royalty agreement, Vision Blue will receive a royalty of 1.0% of the gross revenues from sales of vanadium pentoxide (“V2O5”) from the Green Giant Vanadium Project for a period of 15 years following commencement of production of V2O5.

History

In 2007, the Company entered into a joint venture agreement with Madagascar Minerals and Resources SARL (“MMR”) to acquire a 75% interest in the Green Giant property. Pursuant to the agreement, the Company paid $765,000 in cash, issued 250,000 common shares and issued 100,000 common share purchase warrants, which have now expired.

On July 9, 2009, the Company acquired the remaining 25% interest by paying $100,000. MMR retains a 2% NSR. The first 1% NSR can be acquired at the Company’s option by paying $500,000 in cash or common shares and the second 1% NSR can be acquired at the Company’s option by paying $1,000,000 in cash or common shares.

The Green Giant property is located within exploration permits issued by the Bureau de Cadastre Minier de Madagascar (“BCMM”) pursuant to the Mining Code 1999 (as amended) and its implementing decrees. The Green Giant property exploration permits are currently held under the name of our Madagascar subsidiary.

Exploration and Evaluation

A comprehensive diamond-drill program confirmed five vanadium-bearing trends on the property. The Jaky and Manga trends were deemed the most prospective and were the focus of the 2009 and 2010 drill programs. The complete exploration program included of 131 diamond drill holes totalling 21,957 metres, 140 trenches totalling 17,105 metres, 11,035 soil samples and 7,843-line kilometres of airborne surveys.

The exploration work resulted in a National Instrument 43-101 compliant (NI 43-101) resource estimate dated January 14, 2011.

| 15 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

Mineral Resource Estimate

The current mineral resource estimate for the Green Giant Project is summarised below consisting of the resource categories, the tonnage, the vanadium grade (“V2O5%”) and the contained vanadium (“V2O5”) pounds. A cut-off grade of 0.5% V2O5 was used. The mineral resources are classified in the Indicated and Inferred categories as defined by the Canadian Institute of Mining, Metallurgy and Petroleum definition standards.

Classification | Tonnage (Mt) | Grade (V2O5%) | V2O5 (million pounds) |

Indicated | 49.5 | 0.693% | 756.3 |

Inferred | 9.7 | 0.632% | 134.5 |

Readers are cautioned to refer to the technical study for certain other details and assumptions relating to the above mineral resource and reserve estimates and data verification procedures.

The Technical Report for the Green Giant Project has been filed under the Company’s profile and on SEDAR at www.sedar.com, and is posted on NextSource’s website at www.nextsourcematerials.com. Please see “Green Giant Project, Fotadrevo, Province of Toliara, Madagascar, Technical Report Update NI 43-101. Prepared by AGP Mining Consultants” dated January 14, 2011 for certain other details and assumptions relating to the above mineral resource estimates and data verification procedures.

Sagar Project, Labrador Trough Region, Quebec, Canada

Overview and Project Plan

In 2006, the Company purchased from Virginia Mines Inc. (“Virginia”) a 100% interest in 369 claims located in northern Quebec, Canada. Virginia retains a 2% net smelter royalty (“NSR”) on certain claims within the property. Other unrelated parties also retain a 1% NSR and a 0.5% NSR on certain claims within the property, of which half of the 1% NSR can be acquired by the Company by paying $200,000 and half of the 0.5% NSR can be acquired by the Company by paying $100,000.

Since early 2012, the Company has focused its efforts on the Molo Graphite Project and as such only minimal work has been completed on the Sagar Property since that time.

As of June 30, 2021, the Sagar property consisted of 184 claims covering a total area of 8,539.58 ha.

The Company does not have any immediate plans to complete any further exploration on this property.

| 16 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

RESULTS OF OPERATIONS

Financial Results for the year ended June 30, 2021 and 2020

|

| For the year ended |

|

| For the year ended |

|

| For the year ended |

| |||

|

| June 30, |

|

| June 30, |

|

| June 30, |

| |||

|

| 2021 |

|

| 2020 |

|

| 2019 |

| |||

Revenues |

| $ | - |

|

| $ | - |

|

| $ | - |

|

Mine development expenses |

|

|

|

|

|

|

|

|

|

|

|

|

Mineral claims (Madagascar) |

|

| 3,335 |

|

|

| 93,954 |

|

|

| 81,969 |

|

Payroll and benefits |

|

| - |

|

|

| - |

|

|

| 13,490 |

|

Engineering and metallurgical (Canada, South Africa) |

|

| 38,598 |

|

|

| 64,850 |

|

|

| 171,210 |

|

Consulting fees (Madagascar) |

|

| 265,635 |

|

|

| - |

|

|

| 686,212 |

|

Travel |

|

| 16,100 |

|

|

| 20,452 |

|

|

| 12,587 |

|

Commercial production success fee |

|

| - |

|

|

| - |

|

|

| - |

|

Total mine development expenses |

|

| 323,668 |

|

|

| 179,256 |

|

|

| 965,468 |

|

Exploration and evaluation expenses |

|

|

|

|

|

|

|

|

|

|

|

|

Mineral claims (Canada) |

|

| 15,335 |

|

|

| 6,623 |

|

|

| 15,469 |

|

Mineral claims (Madagascar) |

|

| 4,449 |

|

|

| 50,000 |

|

|

| 39,875 |

|

Exploration Camp and Admin (Madagascar) |

|

| 27,031 |

|

|

| 9,487 |

|

|

| 82,582 |

|

Total exploration and evaluation expenses |

|

| 46,815 |

|

|

| 66,110 |

|

|

| 137,926 |

|

General and administrative expenses |

|

|

|

|

|

|

|

|

|

|

|

|

Payroll and benefits |

|

| 483,519 |

|

|

| 436,337 |

|

|

| 459,553 |

|

Consulting Fees |

|

| 383,841 |

|

|

| 358,503 |

|

|

| 368,345 |

|

Legal Fees |

|

| 99,316 |

|

|

| 29,344 |

|

|

| 239,366 |

|

Professional Fees |

|

| 155,108 |

|

|

| 95,397 |

|

|

| 111,711 |

|

Public filing expenses |

|

| 131,923 |

|

|

| 72,137 |

|

|

| 87,093 |

|

Travel expenses |

|

| 23,399 |

|

|

| 34,004 |

|

|

| 140,414 |

|

Investor relation expenses |

|

| 31,610 |

|

|

| 22,993 |

|

|

| 49,711 |

|

Insurance expenses |

|

| 30,816 |

|

|

| 22,624 |

|

|

| 18,315 |

|

Rent expenses |

|

| 19,857 |

|

|

| 19,111 |

|

|

| 34,303 |

|

Office and admin |

|

| 37,412 |

|

|

| 23,637 |

|

|

| 24,704 |

|

Total general and administrative expenses |

|

| 1,396,801 |

|

|

| 1,114,087 |

|

|

| 1,533,515 |

|

Share-based compensation |

|

| 3,744,172 |

|

|

| - |

|

|

| 651,692 |

|

Amortization of plant and equipment |

|

| 6,592 |

|

|

| 6,053 |

|

|

| - |

|

Finance costs |

|

| 1,317 |

|

|

| - |

|

|

| - |

|

Foreign currency translation (gain) loss |

|

| 101,252 |

|

|

| 3,552 |

|

|

| (4,565 | ) |

Interest (income) |

|

| (104 | ) |

|

| - |

|

|

| - |

|

Interest expense |

|

| 273 |

|

|

| 2,098 |

|

|

| - |

|

Royalty Fee |

|

| - |

|

|

| - |

|

|

| - |

|

Flow through provision (gain) or loss |

|

| (146,814 | ) |

|

| - |

|

|

| - |

|

Foreign taxes |

|

| 92 |

|

|

| 772 |

|

|

| - |

|

Sub-total before other items |

|

| 5,474,064 |

|

|

| 1,371,928 |

|

|

| 3,284,036 |

|

Change in value of warrant liability |

|

| 36,486,420 |

|

|

| (386,940 | ) |

|

| (73,532 | ) |

Government assistance |

|

| - |

|

|

| (7,353 | ) |

|

| - |

|

Net loss for the year |

|

| (41,960,484 | ) |

|

| (977,635 | ) |

|

| (3,210,504 | ) |

Other comprehensive income |

|

|

|

|

|

|

|

|

|

|

|

|

Items that will be reclassified subsequently to net loss |

|

|

|

|

|

|

|

|

|

|

|

|

Translation adjustment for foreign operations |

|

| 134,639 |

|

|

| 3,196 |

|

|

| 41,713 |

|

Net loss and comprehensive loss for the year |

| $ | (41,825,845 | ) |

| $ | (974,439 | ) |

| $ | (3,168,791 | ) |

| 17 |

NEXTSOURCE MATERIALS INC.

MANAGEMENT’S DISCUSSION AND ANALYSIS

For the years ended June 30, 2021, and 2020

Overall Performance

The Company has two operating segments, consisting of the development of mining operations in Madagascar and the exploration and evaluation of mineral resources in Madagascar and Canada. During the year ended June 30, 2021, the Company incurred a net loss and comprehensive loss of $41,825,845 (2020: net loss and comprehensive loss of $974,439). Highlights include completing a $29.5 million financing package and the initiation of mine development and construction activities for Phase 1 of the Molo Graphite Mine.

Mine Development Expenses