As filed with the Securities and Exchange Commission on December 7, 2006

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number: 811-21631

RMK Advantage Income Fund, Inc.

(Exact name of Registrant as specified in charter)

Morgan Keegan Tower

Fifty North Front Street

Memphis, Tennessee 38103

(Address of principal executive offices) (Zip code)

Allen B. Morgan, Jr.

Morgan Keegan Tower

Fifty North Front Street

Memphis, Tennessee 38103

(Name and address of agent for service)

Registrant’s telephone number, including area code: (901) 524-4100

with copies to:

Arthur J. Brown, Esq.

Kirkpatrick & Lockhart Nicholson Graham LLP

1601 K Street, N.W.

Washington, D.C. 20006

Date of fiscal year end: March 31, 2007

Date of reporting period: September 30, 2006

Item 1. Reports to Stockholders.

The following is a copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “1940 Act”) (17 CFR 270.30e-1):

TABLEOF CONTENTS

There is no assurance that the Funds will achieve their investment objectives. The Funds are subject to market risk, which include the possibilities that the market values of the securities owned by the Funds will decline or that the shares of the Funds will trade at lower prices in the market. Accordingly, you can lose money investing in the Funds.

| | | | |

| NOT FDIC INSURED | | MAY LOSE VALUE | | NO BANK GUARANTEE |

i

LETTER TO STOCKHOLDERS

Dear Stockholder,

We are pleased to present the enclosed combined semi-annual report for RMK Advantage Income Fund, Inc., RMK High Income Fund, Inc., RMK Multi-Sector High Income Fund, Inc. and RMK Strategic Income Fund, Inc. (each, a “Fund” and collectively, the “Funds”). In this report, you will find information on each Fund’s investment objective and strategy and learn how your investment performed during the six months ended September 30, 2006. The portfolio manager will also provide an overview of the market conditions and discuss some of the factors that affected investment performance during the reporting period. In addition, this report includes each Fund’s unaudited financial statements and each Fund’s portfolio of investments as of September 30, 2006.

As always, we appreciate your continued support of the Regions Morgan Keegan closed-end funds. We remain committed to helping you pursue your financial goals through investments in our fund family. You have our commitment to bring you the highest level of disciplined decision making and personal service to meet your financial needs. If you have any questions about the Funds, please call us toll-free at 800-564-2188.

Sincerely,

Brian B. Sullivan, CFA

President and Chief Investment Officer

Morgan Asset Management, Inc.

November 21, 2006

1

[THIS PAGE INTENTIONALLY LEFT BLANK]

2

RMK ADVANTAGE INCOME FUND, INC.

OBJECTIVE & STRATEGY

RMK Advantage Income Fund, Inc. seeks a high level of current income. The Fund seeks capital growth as a secondary investment objective when consistent with its primary investment objective. The Fund invests a majority of its total assets in below investment grade debt securities (commonly referred to as “junk bonds”) that offer attractive yield and capital appreciation potential. The Fund may also invest in investment grade debt securities, up to 15% of its total assets in foreign debt and foreign equity securities and up to 25% of its total assets in domestic equity securities, including common and preferred stocks. The Fund invests in a wide range of below investment grade debt securities, including corporate bonds, mortgage-backed and asset-backed securities and municipal and foreign government obligations, as well as securities of companies in bankruptcy reorganization proceedings or otherwise in the process of debt restructuring. (Below investment grade debt securities are rated Ba1 or lower by Moody’s Investors Service, Inc., BB+ or lower by Standard & Poor’s Ratings Group, comparably rated by another nationally recognized statistical rating organization or, if unrated, determined by the Fund’s investment adviser to be of comparable quality.)

INVESTMENT RISKS: Bond funds tend to experience smaller fluctuations in value than stock funds. However, investors in any bond fund should anticipate fluctuations in price. Bond prices and the value of bond funds decline as interest rates rise. Longer-term funds generally are more vulnerable to interest rate risk than shorter-term funds. Below investment grade bonds involve greater credit risk, which is the risk that the issuer will not make interest or principal payments when due. An economic downturn or period of rising interest rates could adversely affect the ability of issuers, especially issuers of below investment grade debt, to service primary obligations and an unanticipated default could cause the Fund to experience a reduction in value of its shares. The value of U.S. and foreign equity securities in which the Fund invests will change based on changes in a company’s financial condition and in overall market and economic conditions. Leverage creates an opportunity for an increased return to common stockholders, but unless the income and capital appreciation, if any, on securities acquired with leverage proceeds exceed the costs of the leverage, the use of leverage will diminish the investment performance of the Fund’s shares. Use of leverage may also increase the likelihood that the net asset value of the Fund and market value of its common shares will be more volatile, and the yield and total return to common stockholders will tend to fluctuate more in response to changes in interest rates and creditworthiness.

3

RMK ADVANTAGE INCOME FUND, INC.

MANAGEMENT DISCUSSIONOF FUND PERFORMANCE

During the first half of RMK Advantage Income Fund, Inc.’s fiscal year 2007, which ended September 30, 2006, the Fund had a total return of 11.19%, based on market price and reinvested dividends. For the six months ended September 30, 2006, the Fund had a total return of 3.06%, based on net asset value and reinvested dividends. For the six months ended September 30, 2006, the Lehman Brothers Ba U.S. High Yield Index1 had a total return of 4.12%. The Fund’s strong market performance is a reflection of investor’s desire for cash distributions as well as the stability of the Fund’s net asset value offered by a very diverse portfolio.

During the first six months of the 2007 fiscal year, corporate high yield debt and common stocks were the best performing asset categories. Credit spreads (the yield premium required for risky assets over riskless assets such as U.S. Treasuries) contracted, or shrank significantly in the corporate sector providing meaningful outperformance for corporate securities. In the asset-backed sector, however, concerns over the slow down in housing and real estate in general caused credit spreads to expand and acted to depress overall performance from our portfolio of mortgage related securities. Asset-backed bonds secured by aircraft leases, medical equipment leases and ship leases continued to perform very well.

During the same period, we made substantial allocation shifts away from home equity loans and into collateralized loan obligations focusing specifically on packages of senior secured corporate loans, both domestic and international. Further allocation shifts will focus on moving out of some floating rate assets and into more fixed rate assets as we expect the Federal Reserve to begin lowering short term rates at some point in 2007.

James C. Kelsoe, Jr., CFA

Senior Portfolio Manager

Morgan Asset Management, Inc.

Market forecasts provided in this report may not necessarily come to pass. There is no assurance that the Fund will achieve its investment objectives. These views are subject to change at any time based upon market or other conditions, and Morgan Asset Management, Inc. disclaims any responsibility to update such views. The Fund is subject to market risk, which include the possibilities that the market values of the securities owned by the Fund will decline or that shares of the Fund will trade at lower prices in the market. Accordingly, you can lose money investing in the Fund.

4

RMK ADVANTAGE INCOME FUND, INC.

INDEX DESCRIPTION

| 1 | | The Lehman Brothers Ba U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt. Pay-in-kind (PIK) bonds, Eurobonds and debt issues from countries designated as emerging markets (e.g., Argentina, Brazil, Venezuela, etc.) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-emerging countries are included. Original issue zeroes, step-up coupon structures and 144As are also included. The index is unmanaged, and unlike the fund, is not affected by cashflows or trading and other expenses. It is not possible to invest directly in an index. |

5

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIO STATISTICS†

AS OF SEPTEMBER 30, 2006

| | |

Average Credit Quality | | BB |

Current Yield | | 10.19% |

Yield to Maturity | | 12.03% |

Duration | | 4.27 Years |

Average Effective Maturity | | 5.69 Years |

Percentage of Leveraged Assets | | 26% |

Total Number of Holdings | | 273 |

| † | | The Fund’s composition is subject to change. |

CREDIT QUALITY†

AS OF SEPTEMBER 30, 2006

| | | | | | |

| %OFTOTALINVESTMENTS | | %OFTOTALINVESTMENTS |

AAA | | 1.8% | | CCC | | 17.8% |

AA | | 0.8% | | CC | | 2.7% |

BBB | | 17.2% | | C | | 0.4% |

BB | | 23.8% | | D | | 0.9% |

B | | 13.6% | | Not Rated | | 21.0% |

| | | | | | |

|

| | | | | Total | | 100.0% |

| † | | The Fund’s composition is subject to change. |

ASSET ALLOCATION†

AS OF SEPTEMBER 30, 2006

| | |

| %OFTOTALINVESTMENTS |

Corporate Bonds | | 32.4% |

Collateralized Debt Obligations | | 16.4% |

Collateralized Mortgage Obligations | | 13.9% |

Equipment Leases | | 11.5% |

Home Equity Loans | | 9.7% |

Common Stock | | 9.2% |

Preferred Stock | | 2.8% |

Certificate-Backed Obligations | | 2.2% |

Short-Term Investments | | 1.3% |

Other | | 0.6% |

| | |

|

Total | | 100.0% |

| † | | The Fund’s composition is subject to change. |

6

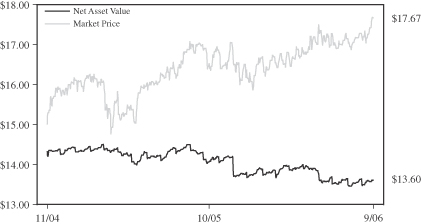

RMK ADVANTAGE INCOME FUND, INC.

NAV & MARKET PRICE HISTORY*

The graph below illustrates the net asset value and market price history of RMK Advantage Income Fund, Inc. (NYSE: RMA) from the commencement of investment operations on November 8, 2004 to September 30, 2006.

| * | | Net asset value is calculated every day that the New York Stock Exchange is open as of the close of trading (normally 4:00 p.m. Eastern Time) by taking the closing market value of all portfolio securities, cash and other assets owned, subtracting all liabilities, then dividing the result (total net assets) by the total number of shares outstanding. The market price is the last reported price at which a share of the Fund was sold on the New York Stock Exchange. |

PERFORMANCE INFORMATION

| | | | | | | | | |

| | | AVERAGE ANNUAL TOTAL RETURNS | |

| AS OF SEPTEMBER 30, 2006 | | SIX

MONTHS* | | | 1

YEAR | | | COMMENCEMENT

OF INVESTMENT

OPERATIONS1 | |

| MARKET VALUE | | 11.19 | % | | 19.37 | % | | 22.56 | % |

| NET ASSET VALUE | | 3.06 | % | | 9.04 | % | | 9.36 | % |

LEHMAN BROTHERS BA

HIGH YIELD INDEX2 | | 4.12 | % | | 6.67 | % | | 5.66 | % |

| * | | Not annualized for periods less than one year. |

7

RMK ADVANTAGE INCOME FUND, INC.

| 1 | | The Fund commenced investment operations on November 8, 2004. |

| 2 | | The Lehman Brothers Ba U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt. Pay-in-kind (PIK) bonds, Eurobonds and debt issues from countries designated as emerging markets (e.g., Argentina, Brazil, Venezuela, etc.) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-emerging countries are included. Original issue zeroes, step-up coupon structures and 144As are also included. The index is unmanaged, and unlike the fund, is not affected by cashflows or trading and other expenses. It is not possible to invest directly in an index. |

Performance data quoted represents past performance which is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund performance changes over time and current performance may be lower or higher than what is stated. For the most recent performance, call toll-free 800-564-2188. Total returns assume an investment at the common share market price or net asset value at the beginning of the period, reinvestment of all dividends and distributions for the period in accordance with the Fund’s dividend reinvestment plan, and sale of all shares at the closing market price (excluding any commissions) or net asset value at the end of the period. Returns shown do not reflect the deduction of taxes that a stockholder would pay on Fund distributions or on the sale of Fund shares.

8

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount | | | | Description | | Value (b) |

| | Asset Backed Securities–Investment Grade–12.7% of Net Assets | | | |

| | | | | | Collateralized Debt Obligations–8.4% | | | |

| $ | 2,000,000 | | | | Alesco Preferred 11A, 8.291% 12/23/36 (a) | | $ | 1,999,800 |

| | 1,913,862 | | | | E-Trade 2004-1A COM1, 2.000% 1/10/40 | | | 1,933,000 |

| | 6,000,000 | | | | Palmer Square 2A CN, 12.000% 11/2/45 (a) | | | 5,940,000 |

| | 4,200,000 | | | | Restructured Asset Backed 2003-3A A3, 6.143% 1/29/22 (a) | | | 3,719,478 |

| | 6,000,000 | | | | Taberna Preferred Funding Ltd. 2006-6A COM, 6.100% 12/6/36 (a) | | | 5,948,400 |

| | 4,000,000 | | | | Taberna Preferred Funding, Ltd 2006-7A C1,

Zero Coupon Bond 2/5/37 (a) | | | 3,936,000 |

| | 2,000,000 | | | | Trapeza 2006-10A D2, 8.700% 6/6/41 (a) | | | 2,000,000 |

| | 2,000,000 | | | | Trapeza CDO LLC 2006-10A, Zero Coupon Bond 6/6/41 | | | 1,920,000 |

| | 3,000,000 | | | | TSAR 16A E, 8.830% 5/19/45 (a) | | | 2,925,000 |

| | 4,777,255 | | | | Witherspoon 2004-1A COM1, 7.500% 9/15/39 | | | 4,657,823 |

| | | | | | | |

|

|

| | | | | | | | | 34,979,501 |

| | | | | | | |

|

|

| | | | | | Equipment Leases–1.2% | | | |

| | 3,883,658 | | | | Aviation Capital 2005-3A C1, 8.580% 12/25/35 (a) | | | 3,961,331 |

| | 3,000,000 | | | | United Capital Aviation Trust 2005-1 B1A,

Zero Coupon Bond 7/15/31 (a) | | | 959,040 |

| | | | | | | |

|

|

| | | | | | | | | 4,920,371 |

| | | | | | | |

|

|

| | | | | | Home Equity Loans–3.1% | | | |

| | 7,613,000 | | | | Ace Securities 2004-HE3 M11, 8.830% 11/25/34 | | | 6,927,830 |

| | 2,119,000 | | | | Asset Backed Securities Corp Home Equity 2005-HE1 M10,

6.788% 3/25/35 | | | 1,968,678 |

| | 2,681,000 | | | | Bear Stearns 2004-HE9 M7B, 9.330% 11/25/34 | | | 2,386,090 |

| | 2,000,000 | | | | Soundview 2005-A B1, 8.330% 4/25/35 (a) | | | 1,600,000 |

| | | | | | | |

|

|

| | | | | | | | | 12,882,598 |

| | | | | | | |

|

|

| | | | | | Total Asset Backed Securities–Investment Grade

(cost $52,012,777) | | | 52,782,470 |

| | | | | | | |

|

|

| | Asset Backed Securities–Below Investment Grade or Unrated–41.2% of Net Assets |

| | | | | | Certificate-Backed Obligations–2.9% | | | |

| | 2,000,000 | | | | Preferred Term Securities II, 12.000% 5/22/33 (a) | | | 1,349,880 |

| | 2,000,000 | | | | Preferred Term Securities XXI, 10.000% 3/22/38 (a) | | | 1,974,960 |

| | 1,000,000 | | | | Preferred Term Securities XXII, Zero Coupon Bond 9/22/36 (a) | | | 988,570 |

| | 5,000,000 | | | | Preferred Term Securities XXII, Zero Coupon Bond 9/22/36 (a) | | | 4,963,200 |

| | 3,000,000 | | | | Preferred Term Securities XXIII, Zero Coupon Bond 12/22/36 (a) | | | 2,964,000 |

| | | | | | | |

|

|

| | | | | | | | | 12,240,610 |

| | | | | | | |

|

|

| | | | | | Collateralized Debt Obligations–13.6% | | | |

| | 2,000,000 | | | | 801 Grand CDO 06-1 LLC, 11.390% 9/20/16 (a) | | | 1,965,000 |

| | 4,000,000 | | | | Acacia CDO, Ltd. 10A, Zero Coupon Bond 9/7/46 (a) | | | 1,824,400 |

| | 5,000,000 | | | | Aladdin CDO 2006-3A, 10.390% 10/31/13 (a) | | | 2,350,000 |

| | 2,000,000 | | | | Arlington Street CDO 1A B, 8.970% 6/10/12 (a) | | | 1,730,000 |

9

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount | | | | Description | | Value (b) |

| | Asset Backed Securities–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Collateralized Debt Obligations (continued) | | | |

| $ | 4,000,000 | | | | Attentus CDO Ltd. 2006-2A COM, Zero Coupon Bond 10/9/41 | | $ | 3,888,000 |

| | 2,773,473 | | | | Cigna CDO Limited 2000-1A B1, 6.520% 8/28/12 (a) | | | 2,081,852 |

| | 3,000,000 | | | | Diversified Asset Securitization 2 1A B1, 9.712% 9/15/35 (a) | | | 1,590,000 |

| | 3,000,000 | | | | Dryden Leveraged Loan CDO 2005-9A DFN,

Zero Coupon Bond 9/20/19 | | | 2,550,000 |

| | 4,000,000 | | | | GSC Partners CDO Fund Ltd 2006-7A COM1, 5.075% 5/25/20 (a) | | | 3,987,200 |

| | 3,909,018 | | | | Hewett’s Island 2004-1A COM, 9.000% 12/15/16 | | | 3,772,203 |

| | 2,000,000 | | | | Jazz CDO BV III-A EB, Zero Coupon Bond 9/20/14 (a) | | | 1,974,440 |

| | 9,000,000 | | | | Kenmore Street Synthetic CDO 2006-1A, 10.390% 4/30/14 (a) | | | 4,140,000 |

| | 1,000,000 | | | | Knollwood CDO Ltd. 2006-2A E, 11.488% 7/13/46 (a) | | | 1,000,000 |

| | 2,000,000 | | | | Knollwood CDO Ltd. 2006-2A SN, Zero Coupon Bond 7/13/46 | | | 1,840,000 |

| | 4,000,000 | | | | Kodiak CDO 2006-1A COMB, 3.712% 8/7/37 (a) | | | 3,600,000 |

| | 2,000,000 | | | | Millstone III CDO Ltd, 4.300% 7/5/46 | | | 1,940,000 |

| | 3,863,935 | | | | MKP 4A CS, 2.000% 7/12/40 (a) | | | 3,722,515 |

| | 5,000,000 | | | | OFSI Fund 2006-1A COM1, 5.400% 3/20/40 (a) | | | 5,000,000 |

| | 3,000,000 | | | | Rosedale CLO Ltd I-A II, 5.146% 5/31/36 (a) | | | 2,880,000 |

| | 3,000,000 | | | | Tropic CDO Corp. 2006-5A C1, Zero Coupon Bond 7/15/36 | | | 2,841,000 |

| | 2,000,000 | | | | Veritas 2006-2, 15.000% 7/11/20 (a) | | | 1,920,000 |

| | | | | | | |

|

|

| | | | | | | | | 56,596,610 |

| | | | | | | |

|

|

| | | | | | Collateralized Loan Obligations–0.2% | | | |

| | 1,000,000 | | | | Flagship CLO 2005-4I, Zero Coupon Bond 6/1/17 | | | 946,250 |

| | | | | | | |

|

|

| | | | | | Equipment Leases–14.3% | | | |

| | 6,085,100 | | | | Aerco Limited 1X C1, 6.680% 7/15/23 | | | 2,388,402 |

| | 4,235,094 | | | | Aerco Limited 2A B2, 6.380% 7/15/25 (a) | | | 2,075,196 |

| | 7,342,333 | | | | Aerco Limited 2A C2, 7.380% 7/15/25 (a) | | | 2,349,546 |

| | 14,250,000 | | | | Aircraft Finance Trust 1999-1A A1, 5.810% 5/15/24 | | | 10,081,875 |

| | 5,000,000 | | | | Airplanes Pass Through Trust 2001-1A A9, 5.880% 3/15/19 | | | 3,256,250 |

| | 969,186 | | | | DVI Receivables 2001-2 A3, 3.519% 11/8/31 | | | 746,274 |

| | 2,060,781 | | | | DVI Receivables 2001-2 A4, 4.613% 11/11/09 | | | 1,607,409 |

| | 7,023,203 | | | | DVI Receivables 2002-1 A3A, 5.680% 6/11/10 | | | 4,003,225 |

| | 1,627,123 | | | | DVI Receivables 2002-2 C, 4.340% 9/12/10 | | | 878,647 |

| | 1,912,817 | | | | DVI Receivables 2003-1 A3A, 5.830% 3/14/11 | | | 1,625,895 |

| | 17,000,000 | | | | Lease Investment Flight Trust 1 A1, 5.720% 7/15/31 | | | 12,112,500 |

| | 5,000,000 | | | | Pegasus Aviation Lease 1999-1A A2, 6.300% 3/25/29 | | | 2,175,000 |

| | 6,000,000 | | | | Pegasus Aviation Lease 1999-1A B1, 6.300% 3/25/29 (a) | | | 1,313,580 |

| | 3,687,467 | | | | Pegasus Aviation Lease 2000-1 A1, 5.955% 3/25/15 (a) | | | 2,359,979 |

| | 20,700,000 | | | | Pegasus Aviation Lease 2001-1A A1, 5.810% 5/10/31 (a) | | | 12,678,750 |

| | | | | | | |

|

|

| | | | | | | | | 59,652,528 |

| | | | | | | |

|

|

| | | | | | Franchise Loans–0.2% | | | |

| | 1,617,000 | | | | Falcon Franchise Loan 2001-1 F, 6.500% 1/5/23 | | | 957,021 |

| | | | | | | |

|

|

10

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount | | | | Description | | Value (b) |

| | Asset Backed Securities–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Home Equity Loans–9.9% | | | |

| $ | 2,000,000 | | | | Ace Securities 2005-HE2 B1, 8.580% 4/25/35 (a) | | $ | 1,640,000 |

| | 3,000,000 | | | | Ace Securities 2005-HE6 B1, 8.330% 10/25/35 (a) | | | 2,340,000 |

| | 2,000,000 | | | | Asset Backed Securities Corp Home Equity 2006-HE4 M9,

7.830% 5/25/36 (a) | | | 1,788,440 |

| | 7,038,000 | | | | Equifirst Mortgage 2004-3 B2, 6.521% 12/25/34 (a) | | | 6,123,060 |

| | 1,000,000 | | | | Equifirst Mortgage 2005-1 B3, 6.268% 4/25/35 (a) | | | 822,500 |

| | 2,000,000 | | | | Master Asset Backed Securities Trust 2005-FRE1 M10,

7.830% 10/25/35 (a) | | | 1,620,000 |

| | 4,000,000 | | | | Meritage Asset Holdings NIM 2005-2 N4, 7.500% 11/25/35 (a) | | | 2,960,000 |

| | 2,000,000 | | | | Merrill Lynch Mortgage 2005-SL1 B5, 8.830% 6/25/35 (a) | | | 1,760,000 |

| | 2,000,000 | | | | Nomura Home Equity Loan Inc. 2005-HE1 B1, 7.780% 9/25/35 | | | 1,775,000 |

| | 3,000,000 | | | | Structured Asset 2005-S6 B3, 7.830% 11/25/35 (a) | | | 2,486,250 |

| | 4,548,535 | | | | Terwin Mortgage 2005-11 1B7, 5.000% 11/25/36 (a) | | | 3,798,027 |

| | | | | | Terwin Mortgage 2005-3SL B6, 11.500% 3/25/35 interest-only strips | | | 815,728 |

| | 2,070,801 | | | | Terwin Mortgage 2005-7SL, 9.203% 7/25/35 (a) | | | 1,804,186 |

| | 4,000,000 | | | | Terwin Mortgage 2005-R1, 5.000% 12/28/36 (a) | | | 2,970,000 |

| | 4,500,000 | | | | Terwin Mortgage 2006-1 2B5, 5.000% 1/25/37 (a) | | | 3,681,000 |

| | 6,000,000 | | | | Terwin Mortgage 2006-R3, 6.290% 7/25/37(a) | | | 4,904,400 |

| | | | | | | |

|

|

| | | | | | | | | 41,288,591 |

| | | | | | | |

|

|

| | | | | | Manufactured Housing Loans–0.1% | | | |

| | 896,130 | | | | Bombardier Capital 1998-B M2, 7.310% 10/15/28 | | | 17,923 |

| | 482,121 | | | | Bombardier Capital 2001-A M2, 8.265% 12/15/30 | | | 106,066 |

| | | | | | | |

|

|

| | | | | | | | | 123,989 |

| | | | | | | |

|

|

| | | | | | Total Asset Backed Securities–Below Investment Grade

or Unrated (cost $179,547,359) | | | 171,805,599 |

| | | | | | | |

|

|

| | Corporate Bonds–Investment Grade–2.0% of Net Assets | | | |

| | | | | | Special Purpose Entity–2.0% | | | |

| | 2,000,000 | | | | Barton Springs 2005-1-C1, 8.690% 12/20/10 (a) | | | 1,760,000 |

| | 4,000,000 | | | | Duane Park I, Zero Coupon Bond 6/27/16 (a) | | | 4,000,000 |

| | 3,000,000 | | | | Lincoln Park Ref Link 01-1, 8.905% 7/30/31 (a) | | | 2,670,000 |

| | | | | | | |

|

|

| | | | | | Total Corporate Bonds–Investment Grade

(cost $8,463,022) | | | 8,430,000 |

| | | | | | | |

|

|

| | Corporate Bonds–Below Investment Grade or Unrated–41.5% of Net Assets | | | |

| | | | | | Apparel–1.1% | | | |

| | 4,435,000 | | | | Rafaella Apparel, 11.250% 6/15/11 (a) | | | 4,357,387 |

| | | | | | | |

|

|

| | | | | | Appliances–0.6% | | | |

| | 2,535,000 | | | | Windmere-Durable, 10.000% 7/31/08 | | | 2,535,000 |

| | | | | | | |

|

|

11

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount | | | | Description | | Value (b) |

| | Corporate Bonds–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Automotives–3.7% | | | |

| $ | 2,225,000 | | | | Cooper Standard Auto, 8.375% 12/15/14 | | $ | 1,635,375 |

| | 2,225,000 | | | | Dana Corporation, Zero Coupon Bond 1/15/15 in default (c) | | | 1,457,375 |

| | 1,388,000 | | | | Dana Corporation, Zero Coupon Bond 3/15/10 in default (c) | | | 964,660 |

| | 925,000 | | | | Delco Remy International Inc, 11.000% 5/1/09 | | | 444,000 |

| | 1,325,000 | | | | Delphi Corporation, Zero Coupon Bond 5/1/29 in default (c) | | | 1,119,625 |

| | 1,350,000 | | | | Dura Operating, 8.625% 4/15/12 | | | 534,937 |

| | 1,650,000 | | | | Dura Operating, 9.000% 5/1/09 | | | 70,125 |

| | 1,550,000 | | | | Federal-Mogul Co, Zero Coupon Bond 1/15/09 in default (c) | | | 891,250 |

| | 2,550,000 | | | | Ford Motor, 7.450% 7/16/31 | | | 1,969,875 |

| | 250,000 | | | | Ford Motor, 9.980% 2/15/47 | | | 217,500 |

| | 2,525,000 | | | | General Motors, 8.375% 7/15/33 | | | 2,184,125 |

| | 400,000 | | | | Metaldyne Corp., 10.000% 11/1/13 | | | 404,000 |

| | 3,750,000 | | | | Metaldyne Corp., 11.000% 6/15/12 | | | 3,375,000 |

| | | | | | | |

|

|

| | | | | | | | | 15,267,847 |

| | | | | | | |

|

|

| | | | | | Basic Materials–2.1% | | | |

| | 4,410,000 | | | | Edgen Acquisition, 9.875% 2/1/11 | | | 4,365,900 |

| | 2,375,000 | | | | FMG Finance, 10.625% 9/1/16 (a) | | | 2,280,000 |

| | 2,533,000 | | | | Millar Western, 7.750% 11/15/13 | | | 2,102,390 |

| | | | | | | |

|

|

| | | | | | | | | 8,748,290 |

| | | | | | | |

|

|

| | | | | | Building & Construction–0.7% | | | |

| | 600,000 | | | | William Lyon Homes, 7.625% 12/15/12 | | | 484,500 |

| | 1,700,000 | | | | Owens Corning, Zero Coupon Bond 8/1/18 in default (c) | | | 871,250 |

| | 1,700,000 | | | | Tech Olympic USA, Inc, 10.375% 7/1/12 | | | 1,470,500 |

| | | | | | | |

|

|

| | | | | | | | | 2,826,250 |

| | | | | | | |

|

|

| | | | | | Communications–1.0% | | | |

| | 4,350,000 | | | | CCH I Holdings LLC, 11.750% 5/15/14 | | | 3,099,375 |

| | 967,000 | | | | CCH I Holdings LLC, 11.000% 10/1/15 | | | 879,970 |

| | 350,000 | | | | Penton Media, 10.375% 6/15/11 | | | 344,750 |

| | | | | | | |

|

|

| | | | | | | | | 4,324,095 |

| | | | | | | |

|

|

| | | | | | Consulting Services–1.1% | | | |

| | 2,000,000 | | | | MSX International, 11.000% 10/15/07 | | | 1,920,000 |

| | 4,000,000 | | | | MSX International, 11.375% 1/15/08 | | | 2,868,480 |

| | | | | | | |

|

|

| | | | | | | | | 4,788,480 |

| | | | | | | |

|

|

| | | | | | Electronics–0.4% | | | |

| | 1,800,000 | | | | Motors and Gears, 10.750% 11/15/06 | | | 1,789,735 |

| | | | | | | |

|

|

| | | | | | Energy–1.8% | | | |

| | 2,425,000 | | | | Neptune Marine, 10.920% 9/7/09 (a) | | | 2,443,188 |

12

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount | | | | Description | | Value (b) |

| | Corporate Bonds–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Energy (continued) | | | |

| $ | 5,050,000 | | | | Paramount Resources Ltd, 8.500% 1/31/13* | | $ | 5,062,625 |

| | | | | | | |

|

|

| | | | | | | | | 7,505,813 |

| | | | | | | |

|

|

| | | | | | Finance–1.0% | | | |

| | 3,225,000 | | | | Advanta Capital Trust I, 8.990% 12/17/26 | | | 3,265,312 |

| | 875,000 | | | | Altra Industrial Motion, 9.000% 12/1/11 | | | 892,500 |

| | | | | | | |

|

|

| | | | | | | | | 4,157,812 |

| | | | | | | |

|

|

| | | | | | Food–1.0% | | | |

| | 1,950,000 | | | | Eurofresh Inc, 11.500% 1/15/13 (a) | | | 1,901,250 |

| | 3,200,000 | | | | Merisant, 9.500% 7/15/13 | | | 2,048,000 |

| | | | | | | |

|

|

| | | | | | | | | 3,949,250 |

| | | | | | | |

|

|

| | | | | | Garden Products–0.3% | | | |

| | 1,460,000 | | | | Ames True Temper, 10.000% 7/15/12 | | | 1,251,950 |

| | | | | | | |

|

|

| | | | | | Health Care–0.9% | | | |

| | 3,500,000 | | | | Healthsouth Corp, 11.418% 6/15/14 (a) | | | 3,570,000 |

| | | | | | | |

|

|

| | | | | | Human Resources–0.4% | | | |

| | 1,850,000 | | | | Comforce Operating, 12.000% 12/1/07 | | | 1,845,560 |

| | | | | | | |

|

|

| | | | | | Industrial–5.9% | | | |

| | 3,235,000 | | | | Advanced Lighting Technologies, 11.000% 3/31/09 | | | 3,218,825 |

| | 4,000,000 | | | | Consolidated Container, 10.125% 7/15/09 | | | 3,820,000 |

| | 1,120,000 | | | | Constar International, 11.000% 12/1/12 | | | 974,400 |

| | 3,228,000 | | | | Continental Global Group, 9.000% 10/1/08 | | | 3,134,517 |

| | 950,000 | | | | Corp Durango SA, 8.500% 12/31/12 | | | 883,500 |

| | 1,800,000 | | | | Home Products International, 9.625% 5/15/08 | | | 1,170,000 |

| | 2,800,000 | | | | IMAX Corp, 9.625% 12/1/10 | | | 2,667,000 |

| | 1,675,000 | | | | Spectrum Brands, 8.500% 10/1/13 | | | 1,448,875 |

| | 1,270,000 | | | | Trimas Corp., 9.875% 6/15/12 | | | 1,174,750 |

| | 1,225,000 | | | | VITRO S.A., 12.750% 11/1/13 (a) | | | 1,280,125 |

| | 675,000 | | | | Wolverine Tube, 10.500% 4/1/09 | | | 594,000 |

| | 3,675,000 | | | | Wolverine Tube, 7.375% 8/1/08 (a) | | | 3,123,750 |

| | 1,125,000 | | | | Wornick Company, 10.875% 7/15/11 | | | 1,119,375 |

| | | | | | | |

|

|

| | | | | | | | | 24,609,117 |

| | | | | | | |

|

|

| | | | | | Investment Companies–0.3% | | | |

| | 1,250,000 | | | | Reg Diversified Funding, 10.000% 1/25/36 (a) | | | 1,250,000 |

| | | | | | | |

|

|

| | | | | | Manufacturing–4.3% | | | |

| | 4,500,000 | | | | BGF Industries, 10.250% 1/15/09 | | | 4,235,625 |

| | 2,200,000 | | | | Elgin National Industries, 11.000% 11/1/07 | | | 2,200,770 |

| | 3,900,000 | | | | GSI Group, 12.000% 5/15/13 (a) | | | 4,173,000 |

| | 3,545,000 | | | | JB Poindexter, 8.750% 3/15/14 | | | 2,924,625 |

13

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount | | | | Description | | Value (b) |

| | Corporate Bonds–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Manufacturing (continued) | | | |

| $ | 3,475,000 | | | | Maax Corp, 9.750% 6/15/12 | | $ | 2,745,250 |

| | 1,700,000 | | | | Terphane Holding Corp, 12.500% 6/15/09 (a) | | | 1,700,000 |

| | | | | | | |

|

|

| | | | | | | | | 17,979,270 |

| | | | | | | |

|

|

| | | | | | Medical Products–0.4% | | | |

| | 5,055,000 | | | | Insight Health Services, 9.875% 11/1/11 | | | 1,731,337 |

| | | | | | | |

|

|

| | | | | | Retail–1.8% | | | |

| | 950,000 | | | | Jo-Ann Stores, 7.500% 3/1/12 | | | 826,500 |

| | 400,000 | | | | Lazydays RV Center, 11.750% 5/15/12 | | | 384,000 |

| | 1,150,000 | | | | Nebraska Book Company, 8.625% 3/15/12 | | | 1,078,125 |

| | 1,518,000 | | | | Star Gas Partner, 10.250% 2/15/13 | | | 1,540,770 |

| | 4,350,000 | | | | Uno Restaurant, 10.000% 2/15/11 (a) | | | 3,632,250 |

| | | | | | | |

|

|

| | | | | | | | | 7,461,645 |

| | | | | | | |

|

|

| | | | | | Special Purpose Entity–6.6% | | | |

| | 9,333,333 | | | | Dow Jones CDX HY T4, 10.500% 12/29/09 (a) | | | 9,403,333 |

| | 2,500,000 | | | | Eirles Two Limited 262, 5.372% 8/3/21 | | | 2,500,000 |

| | 3,500,000 | | | | Eirles Two Limited 263, 5.372% 8/3/21 | | | 3,500,000 |

| | 5,000,000 | | | | INCAPS Funding II, Zero Coupon Bond 1/15/34 (a) | | | 4,500,000 |

| | 1,320,000 | | | | Interactive Health, 7.250% 4/1/11 (a) | | | 1,062,600 |

| | 2,100,000 | | | | Milacron Escrow Corp, 11.500% 5/15/11 | | | 1,995,000 |

| | 2,000,000 | | | | North Street Referenced Linked Notes 2000-1A D1, 8.085% 4/28/11 (a) | | | 900,000 |

| | 3,500,000 | | | | North Street Referenced Linked Notes 2000-1A, 7.235% 4/28/11 (a) | | | 2,730,000 |

| | 850,000 | | | | PCA LLC/PCA Finance Corp, 14.000% 6/1/09 (a) | | | 858,500 |

| | | | | | | |

|

|

| | | | | | | | | 27,449,433 |

| | | | | | | |

|

|

| | | | | | Technology–1.3% | | | |

| | 3,350,000 | | | | Danka Business Systems, 11.000% 6/15/10 | | | 3,082,000 |

| | 1,450,000 | | | | Spheris Inc, 11.000% 12/15/12 (a) | | | 1,359,375 |

| | 875,000 | | | | Unisys Corp, 8.000% 10/15/12 | | | 818,125 |

| | | | | | | |

|

|

| | | | | | | | | 5,259,500 |

| | | | | | | |

|

|

| | | | | | Telecommunications–2.0% | | | |

| | 3,350,000 | | | | Broadview Networks Holdings, 11.375% 9/1/12 (a) | | | 3,408,625 |

| | 675,000 | | | | Iridium LLC/Capital Corp, Zero Coupon Bond

7/15/09 in default (c) | | | 182,250 |

| | 4,175,000 | | | | Primus Telecommunications, 8.000% 1/15/14 | | | 2,609,375 |

| | 2,400,000 | | | | Securus Technologies, 11.000% 9/1/11 | | | 2,052,000 |

| | | | | | | |

|

|

| | | | | | | | | 8,252,250 |

| | | | | | | |

|

|

| | | | | | Tobacco–0.6% | | | |

| | 2,915,000 | | | | North Atlantic Trading, 9.250% 3/1/12 | | | 2,521,475 |

| | | | | | | |

|

|

14

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount | | | | Description | | Value (b) |

| | Corporate Bonds–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Transportation–0.9% | | | |

| $ | 3,875,000 | | | | Sea Containers Ltd, 10.750% 10/15/06* | | $ | 3,850,219 |

| | | | | | | |

|

|

| | | | | | Travel–1.3% | | | |

| | 5,675,000 | | | | Worldspan Financial, 11.655% 2/15/11 | | | 5,582,781 |

| | | | | | | |

|

|

| | | | | | Total Corporate Bonds–Below Investment Grade or Unrated (cost $179,971,449) | | | 172,864,496 |

| | | | | | | |

|

|

| | Mortgage Backed Securities–Investment Grade–2.9% of Net Assets | | | |

| | | | | | Collateralized Mortgage Obligations–2.9% | | | |

| | | | | | Harborview Mortgage 2004-8 X, 1.243% 11/19/34

interest-only strips | | | 2,517,798 |

| | 1,998,918 | | | | Harborview Mortgage 2006-4 B11, 7.080% 10/19/35 (a) | | | 1,956,441 |

| | 1,000,000 | | | | Indymac Index NIM Corp 2006-AR6 N2,

8.833% 6/25/46 (a) | | | 1,000,000 |

| | 3,000,000 | | | | Park Place Securities 2005-WCW2 M10, 7.830% 7/25/35 | | | 2,670,000 |

| | 2,000,000 | | | | Park Place Securities 2005-WHQ3 M11, 7.830% 6/25/35 | | | 1,735,000 |

| | 2,415,450 | | | | Sail Net Interest Margin Notes 2004-7A B,

6.750% 8/27/34 (a) | | | 2,378,059 |

| | | | | | | |

|

|

| | | | | | Total Mortgage Backed Securities–Investment Grade (cost $14,621,571) | | | 12,257,298 |

| | | | | | | |

|

|

| | Mortgage Backed Securities–Below Investment Grade or Unrated–15.7% of Net Assets |

| | | | | | Collateralized Mortgage Obligations–15.7% | | | |

| | 2,994,394 | | | | Countrywide Alternative Loan Trust 2005-51 B3, 6.580% 11/20/35 | | | 2,350,600 |

| | 3,991,006 | | | | Countrywide Alternative Loan Trust 2005-56 B3,

6.580% 11/25/35 (a) | | | 3,122,962 |

| | 1,985,386 | | | | Countrywide Alternative Loan Trust 2006-OA1 B2, 7.330% 3/20/46 | | | 1,111,816 |

| | 3,000,000 | | | | First Franklin Mortgage 2005-FFH3 B4, 7.330% 9/25/35 (a) | | | 2,208,750 |

| | 3,000,000 | | | | Greenwich 2005-3 N2, 2.000% 6/27/35 (a) | | | 1,878,900 |

| | 8,000,000 | | | | Greenwich 2005-4 N-2, Zero Coupon Bond 7/27/45 (a) | | | 4,600,000 |

| | 4,000,000 | | | | Greenwich 2005-6A N3, Zero Coupon Bond 11/27/45 (a) | | | 3,400,000 |

| | 2,000,000 | | | | GSAMP Trust 2004-AR1 B5, 5.000% 6/25/34 (a) | | | 1,825,620 |

| | 1,999,878 | | | | Harborview Mortgage 2005-15 B10, 7.080% 10/20/45 | | | 1,591,783 |

| | 3,956,338 | | | | Harborview Mortgage 2006-4 B11, 7.080% 5/19/47 (a) | | | 2,433,148 |

| | 1,000,000 | | | | Indymac Index NIM Corp 2006-AR6 N3, 8.833% 6/25/46 (a) | | | 942,970 |

| | 5,000,000 | | | | Long Beach Asset Holdings 2005-WL1 N4, 7.500% 6/25/45 (a) | | | 4,250,000 |

| | 1,902,625 | | | | Long Beach Mortgage 2001-3 M3, 8.143% 9/25/31 | | | 456,630 |

| | 1,393,846 | | | | Long Beach Mortgage 2001-4 M2, 6.980% 3/25/32 | | | 1,125,578 |

| | 2,000,000 | | | | Long Beach Mortgage Loan Trust 2005-2 B2, 8.080% 4/25/35 (a) | | | 1,713,120 |

| | 2,043,150 | | | | Park Place Securities 2005-WCW1 B, 5.000% 9/25/35 (a) | | | 1,884,806 |

| | 3,800,000 | | | | Park Place Securities 2005-WCW1 M11, 7.830% 9/25/35 | | | 3,078,000 |

| | 3,000,000 | | | | Park Place Securities 2005-WCW3, 7.830% 8/25/35 (a) | | | 2,430,000 |

| | 3,000,000 | | | | Park Place Securities 2005-WHQ1 M10, 7.830% 3/25/35 (a) | | | 2,666,250 |

15

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount/

Shares | | | | Description | | Value (b) |

| | Mortgage Backed Securities–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Collateralized Mortgage Obligations (continued) | | | |

| $ | 2,000,000 | | | | Park Place Securities 2005-WHQ4, 7.830% 9/25/35 (a) | | $ | 1,400,000 |

| | 2,000,000 | | | | Popular 2005-4 B2, 7.830% 9/25/35 (a) | | | 1,800,000 |

| | 5,250,000 | | | | Residential 2005-RS4 B2, 8.330% 4/25/35 (a) | | | 4,372,253 |

| | 3,938,000 | | | | Residential 2005-RS4 B3, 8.330% 4/25/35 (a) | | | 3,103,656 |

| | 1,381,829 | | | | Sasco Net Interest Margin Trust 2004-6XS B, 5.000% 3/28/34 (a) | | | 1,292,010 |

| | 2,000,000 | | | | Soundview 2005-1 B3, 8.580% 4/25/35 (a) | | | 1,560,000 |

| | 2,591,000 | | | | Soundview 2005-2 B3, 8.330% 7/25/35 (a) | | | 2,098,710 |

| | 1,972,000 | | | | Soundview 2005-B M14, 7.650% 5/25/35 (a) | | | 1,197,951 |

| | 2,573,000 | | | | Structured Asset 2004-S2 B, 6.000% 6/25/34 (a) | | | 2,404,443 |

| | 2,139,000 | | | | Structured Asset 2004-S4 B3, 5.000% 12/25/34 (a) | | | 1,628,014 |

| | 2,000,000 | | | | Structured Asset 2005-AR1 B2, 7.330% 9/25/35 (a) | | | 1,510,000 |

| | | | | | | |

|

|

| | | | | | Total Mortgage Backed Securities–Below Investment Grade

or Unrated (cost $66,136,563) | | | 65,437,970 |

| | | | | | | |

|

|

| | Municipal Securities–0.2% of Net Assets | | | |

| | 1,250,000 | | | | Pima County Arizona IDA Health Care, Zero Coupon Bond 11/15/32 | | | 700,000 |

| | | | | | | |

|

|

| | | | | | Total Municipal Securities

(cost $783,722) | | | 700,000 |

| | | | | | | |

|

|

| | Common Stocks–12.3% of Net Assets | | | |

| | 35,200 | | | | Alpha Natural Resources, Inc. (c) | | | 554,752 |

| | 38,800 | | | | American Capital Strategies, Ltd. | | | 1,531,436 |

| | 11,700 | | | | Anadarko Petroleum Corporation | | | 512,811 |

| | 23,300 | | | | Aqua America, Inc. | | | 511,202 |

| | 28,900 | | | | AVX Corporation | | | 511,241 |

| | 61,500 | | | | Cascade Microtech, Inc. (c) | | | 765,675 |

| | 12,700 | | | | Caterpillar Inc. (d) | | | 835,660 |

| | 18,000 | | | | Cemex, S.A. de C.V. (d) | | | 541,440 |

| | 17,600 | | | | Chiquita Brands International, Inc. | | | 235,488 |

| | 46,700 | | | | Citizens Communications Company | | | 655,668 |

| | 6,600 | | | | Companhia de Saneamento Básico do Estado de São Paulo | | | 198,660 |

| | 60,300 | | | | Compass Diversified Trust | | | 922,590 |

| | 29,000 | | | | Consolidated Communications Illinois Holdings, Inc. | | | 542,590 |

| | 17,100 | | | | Cytec Industries Inc. (d) | | | 950,589 |

| | 33,300 | | | | Direct General Corporation | | | 448,218 |

| | 12,900 | | | | Edison International | | | 537,156 |

| | 30,900 | | | | ENSCO International Incorporated | | | 1,354,347 |

| | 24,100 | | | | Enterprise Products Partners L.P. | | | 644,675 |

| | 18,800 | | | | FairPoint Communications, Inc. | | | 327,120 |

| | 41,500 | | | | Famous Dave’s of America, Inc. (c) | | | 630,800 |

| | 32,100 | | | | Fording Canadian Coal Trust | | | 851,613 |

| | 17,000 | | | | Helix Energy Solutions Group, Inc. (c) | | | 567,800 |

16

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | |

| Shares | | | | Description | | Value (b) |

| Common Stocks (continued) | | | |

| 75,600 | | | | Horizon Offshore, Inc. | | $ | 1,292,760 |

| 71,000 | | | | Infocrossing, Inc. (c) | | | 952,110 |

| 142,100 | | | | InPhonic, Inc. (c)(d) | | | 1,125,432 |

| 111,695 | | | | Intermet Corporation (c) | | | 893,560 |

| 3,200 | | | | International Coal Group, Inc. (c) | | | 13,504 |

| 14,100 | | | | Iowa Telecommunications Services, Inc. | | | 279,039 |

| 6,800 | | | | J.C. Penney Company, Inc. | | | 465,052 |

| 20,400 | | | | Kinder Morgan Energy Partners, L.P. | | | 895,152 |

| 32,800 | | | | KKR Financial Corp. | | | 804,912 |

| 18,400 | | | | L-3 Communications Holdings, Inc. | | | 1,441,272 |

| 47,200 | | | | Macquarie Infrastructure Company Trust | | | 1,471,696 |

| 11,000 | | | | Magellan Midstream Partners, L.P. | | | 405,900 |

| 19,100 | | | | Masco Corporation (d) | | | 523,722 |

| 17,200 | | | | McDermott International, Inc. (c) | | | 718,960 |

| 77,800 | | | | MCG Capital Corporation | | | 1,270,474 |

| 37,900 | | | | Mittal Steel Company N.V. | | | 1,316,646 |

| 27,600 | | | | Motorola, Inc. (d) | | | 690,000 |

| 86,400 | | | | Nam Tai Electronics, Inc. | | | 1,061,856 |

| 91,900 | | | | Ness Technologies, Inc. (c) | | | 1,226,865 |

| 38,200 | | | | New York Community Bancorp, Inc. | | | 625,716 |

| 46,900 | | | | Optimal Group Inc. (c) (d) | | | 551,544 |

| 34,000 | | | | Pacific Sunwear of California, Inc. (c) | | | 512,720 |

| 15,500 | | | | Peabody Energy Corporation | | | 570,090 |

| 667 | | | | Providence Washington Insurance Companies (c) | | | 67 |

| 41,400 | | | | Regal Entertainment Group | | | 820,548 |

| 23,600 | | | | RTI International Metals, Inc. (c) | | | 1,028,488 |

| 14,600 | | | | Sanderson Farms, Inc. (d) | | | 472,456 |

| 18,100 | | | | Sasol Limited | | | 595,309 |

| 25,190 | | | | Ship Finance International Limited | | | 501,281 |

| 17,200 | | | | Stage Stores, Inc. (d) | | | 504,648 |

| 192,452 | | | | Star Gas Partners, L.P. (c) | | | 479,205 |

| 31,000 | | | | Superior Energy Services, Inc. (c) | | | 814,060 |

| 120,167 | | | | Taiwan Semiconductor Manufacturing Company Ltd. | | | 1,153,603 |

| 131,770 | | | | Technology Investment Capital Corporation (c) | | | 1,927,795 |

| 13,200 | | | | Tenaris S.A. | | | 467,016 |

| 12,800 | | | | The Dow Chemical Company | | | 498,944 |

| 1,900 | | | | The First Marblehead Corporation (d) | | | 131,594 |

| 30,500 | | | | The Home Depot, Inc. | | | 1,106,235 |

| 14,300 | | | | The Timken Company | | | 425,854 |

| 92,550 | | | | Trustreet Properties Inc. | | | 1,157,801 |

| 26,600 | | | | Tsakos Energy Navigation Limited | | | 1,186,360 |

| 33,600 | | | | Valero Energy Corporation (d) | | | 1,729,392 |

| 13,900 | | | | Valero L.P. | | | 695,000 |

| 11,000 | | | | Washington Mutual, Inc. | | | 478,170 |

17

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | | |

Principal

Amount/

Shares | | | | Description | | Value (b) | |

| | Common Stocks (continued) | | | | |

| | 103,400 | | | | Windstream Corporation | | $ | 1,363,846 | |

| | | | | | | |

|

|

|

| | | | | | Total Common Stocks

(cost $52,340,734) | | | 51,278,185 | |

| | | | | | | |

|

|

|

| | Preferred Stocks–3.9% of Net Assets | | | | |

| | 4,000 | | | | Baker Street Funding (a) | | | 3,880,000 | |

| | 1,000 | | | | Baker Street Funding 2006-1 (a) | | | 940,000 | |

| | 3,000 | | | | Credit Genesis CLO 2005 (a) | | | 2,970,000 | |

| | 2,000 | | | | Hewett’s Island II CDO (a) | | | 1,980,000 | |

| | 67,000 | | | | Indymac Indx CI-1 Corp (a) | | | 1,820,859 | |

| | 2,000 | | | | Marquette Park CLO (a) | | | 1,960,000 | |

| | 2,975 | | | | Motient Corporation | | | 2,506,437 | |

| | | | | | | |

|

|

|

| | | | | | Total Preferred Stocks

(cost $16,033,903) | | | 16,057,296 | |

| | | | | | | |

|

|

|

| | Corporate Loans–0.1% of Net Assets | | | | |

| $ | 400,000 | | | | ICO North America, 7.500% 8/15/09 | | | 492,000 | |

| | | | | | | |

|

|

|

| | | | | | Total Corporate Loans

(cost $400,000) | | | 492,000 | |

| | | | | | | |

|

|

|

| | Eurodollar Time Deposits–1.7% of Net Assets | | | | |

| | | | | | State Street Bank & Trust Company Eurodollar time deposits dated September 29, 2006 4.050% maturing at $7,097,395 on October 2, 2006. | | | 7,095,000 | |

| | | | | | | |

|

|

|

| | | | | | Total Investments–134.2% of Net Assets

(cost $576,483,477) | | | 559,200,314 | |

| | | | | | | |

|

|

|

| | | | | | Other Assets and Liabilities, net–(34.2)% of Net Assets | | | (142,380,424 | ) |

| | | | | | | |

|

|

|

| | | | | | Net Assets | | $ | 416,819,890 | |

| | | | | | | |

|

|

|

18

RMK ADVANTAGE INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | |

Call Options Written

September 30, 2006 | | |

| | | |

Number of

Contracts | | | | Common Stooks/Expiration Date/Exercise Price | | Value (b) |

| 17 | | | | Caterpillar, Inc./October/65 | | $ | 3,655 |

| 11 | | | | Cemex, S.A. de C.V./October/30 | | | 1,210 |

| 26 | | | | Cytec Industries, Inc./October/55 | | | 5,460 |

| 16 | | | | Inphonic, Inc./October/7.50 | | | 1,040 |

| 16 | | | | Masco Corporation/October/25 | | | 4,560 |

| 8 | | | | Motorola, Inc./October/25 | | | 808 |

| 17 | | | | Optimal Group Inc./October/15 | | | 595 |

| 11 | | | | Sanderson Farms, Inc./October/35 | | | 330 |

| 9 | | | | Stage Stores Inc./October/30 | | | 1,035 |

| 8 | | | | The First Marblehead Corporation/October/65 | | | 3,680 |

| 33 | | | | Valero Energy Corporation/October/50 | | | 8,745 |

| | | | | | |

|

|

| | | | | Total Call Options Written

(Premiums Received $25,463) | | $ | 31,118 |

| | | | | | |

|

|

| (a) | | Securities sold within the terms of a private placement memorandum, exempt from registration under Rule 144A under the Securities Act of 1933, as amended, and may be resold in transactions exempt from registration, normally to qualified institutional buyers. Pursuant to guidelines adopted by the Board of Directors, these issues have been determined to be liquid by Morgan Asset Management, Inc., the fund’s investment adviser. |

| (b) | | See Note 2 of accompanying Notes to the Financial Statements regarding investment valuations. |

| (c) | | Non-income producing securities. |

| (d) | | A portion or all of the security is pledged as collateral for call options written. |

| * | | These securiities are classified as Yankee Bonds, which are U.S. dollar denominated bonds issued in the United States by a foreign entity. |

The notes to the financial statements are an integral part of, and should be read in conjunction with, the financial statements.

19

[THIS PAGE INTENTIONALLY LEFT BLANK]

20

RMK HIGH INCOME FUND, INC.

OBJECTIVE & STRATEGY

RMK High Income Fund, Inc. seeks a high level of current income. The Fund seeks capital growth as a secondary investment objective when consistent with its primary investment objective. The Fund invests a majority of its total assets in below investment grade debt securities (commonly referred to as “junk bonds”) that offer attractive yield and capital appreciation potential. The Fund may also invest in investment grade debt securities, up to 15% of its total assets in foreign debt and foreign equity securities and up to 25% of its total assets in domestic equity securities, including common and preferred stocks. The Fund invests in a wide range of below investment grade debt securities, including corporate bonds, mortgage-backed and asset-backed securities and municipal and foreign government obligations, as well as securities of companies in bankruptcy reorganization proceedings or otherwise in the process of debt restructuring. (Below investment grade debt securities are rated Ba1 or lower by Moody’s Investors Service, Inc., BB+ or lower by Standard & Poor’s Ratings Group, comparably rated by another nationally recognized statistical rating organization or, if unrated, determined by the Fund’s investment adviser to be of comparable quality.)

INVESTMENT RISKS: Bond funds tend to experience smaller fluctuations in value than stock funds. However, investors in any bond fund should anticipate fluctuations in price. Bond prices and the value of bond funds decline as interest rates rise. Longer-term funds generally are more vulnerable to interest rate risk than shorter-term funds. Below investment grade bonds involve greater credit risk, which is the risk that the issuer will not make interest or principal payments when due. An economic downturn or period of rising interest rates could adversely affect the ability of issuers, especially issuers of below investment grade debt, to service primary obligations and an unanticipated default could cause the Fund to experience a reduction in value of its shares. The value of U.S. and foreign equity securities in which the Fund invests will change based on changes in a company’s financial condition and in overall market and economic conditions. Leverage creates an opportunity for an increased return to common stockholders, but unless the income and capital appreciation, if any, on securities acquired with leverage proceeds exceed the costs of the leverage, the use of leverage will diminish the investment performance of the Fund’s shares. Use of leverage may also increase the likelihood that the net asset value of the Fund and market value of its common shares will be more volatile, and the yield and total return to common stockholders will tend to fluctuate more in response to changes in interest rates and credit worthiness.

21

RMK HIGH INCOME FUND, INC.

MANAGEMENT DISCUSSIONOF FUND PERFORMANCE

During the first half of RMK High Income Fund, Inc.’s fiscal year 2007, which ended September 30, 2006, the Fund had a total return of 10.91%, based on market price and reinvested dividends. For the six months ended September 30, 2006, the Fund had a total return of 3.49%, based on net asset value and reinvested dividends. For the six months ended September 30, 2006, the Lehman Brothers Ba U.S. High Yield Index1 had a total return of 4.12%. The Fund’s strong market performance is a reflection of investor’s desire for cash distributions as well as the stability of the Fund’s net asset value offered by a very diverse portfolio.

During the first six months of the 2007 fiscal year, corporate high yield debt and common stocks were the best performing asset categories. Credit spreads (the yield premium required for risky assets over riskless assets such as U.S. Treasuries) contracted, or shrank significantly in the corporate sector providing meaningful outperformance for corporate securities. In the asset-backed sector, however, concerns over the slow down in housing and real estate in general caused credit spreads to expand and acted to depress overall performance from our portfolio of mortgage related securities. Asset-backed bonds secured by aircraft leases, medical equipment leases and ship leases continued to perform very well.

During the same period, we made substantial allocation shifts away from home equity loans and into collateralized loan obligations focusing specifically on packages of senior secured corporate loans, both domestic and international. Further allocation shifts will focus on moving out of some floating rate assets and into more fixed rate assets as we expect the Federal Reserve to begin lowering short term rates at some point in 2007.

James C. Kelsoe, Jr., CFA

Senior Portfolio Manager

Morgan Asset Management, Inc.

Market forecasts provided in this report may not necessarily come to pass. There is no assurance that the Fund will achieve its investment objectives. These views are subject to change at any time based upon market or other conditions, and Morgan Asset Management, Inc. disclaims any responsibility to update such views. The Fund is subject to market risk, which include the possibilities that the market values of the securities owned by the Fund will decline or that shares of the Fund will trade at lower prices in the market. Accordingly, you can lose money investing in the Fund.

22

RMK HIGH INCOME FUND, INC.

INDEX DESCRIPTION

| 1 | | The Lehman Brothers Ba U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt. Pay-in-kind (PIK) bonds, Eurobonds and debt issues from countries designated as emerging markets (e.g., Argentina, Brazil, Venezuela, etc.) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-emerging countries are included. Original issue zeroes, step-up coupon structures and 144As are also included. The index is unmanaged, and unlike the fund, is not affected by cashflows or trading and other expenses. It is not possible to invest directly in an index. |

23

RMK HIGH INCOME FUND, INC.

PORTFOLIO STATISTICS†

AS OF SEPTEMBER 30, 2006

| | |

Average Credit Quality | | BB- |

Current Yield | | 9.78% |

Yield to Maturity | | 11.62% |

Duration | | 4.53 Years |

Average Effective Maturity | | 6.03 Years |

Percentage of Leveraged Assets | | 27% |

Total Number of Holdings | | 273 |

| † | | The Fund’s composition is subject to change. |

CREDIT QUALITY†

AS OF SEPTEMBER 30, 2006

| | | | | | |

| %OFTOTALINVESTMENTS | | %OFTOTALINVESTMENTS |

AAA | | 2.6% | | CCC | | 19.1% |

AA | | 0.3% | | CC | | 2.4% |

BBB | | 15.5% | | C | | 0.2% |

BB | | 25.1% | | D | | 1.2% |

B | | 13.7% | | Not Rated | | 19.9% |

| | | | | | |

|

| | | Total | | 100.0% |

| † | | The Fund’s composition is subject to change. |

ASSET ALLOCATION†

AS OF SEPTEMBER 30, 2006

| | |

| %OFTOTALINVESTMENTS |

Corporate Bonds | | 31.2% |

Collateralized Mortgage Obligations | | 15.6% |

Collateralized Debt Obligations | | 15.1% |

Equipment Leases | | 13.1% |

Common Stock | | 9.2% |

Home Equity Loans | | 7.3% |

Preferred Stock | | 2.3% |

Certificate-Backed Obligations | | 1.8% |

Short-Term Investments | | 1.8% |

Commercial Loans | | 1.1% |

Franchise Loans | | 1.0% |

Other | | 0.5% |

| | |

|

Total | | 100.0% |

| † | | The Fund’s composition is subject to change. |

24

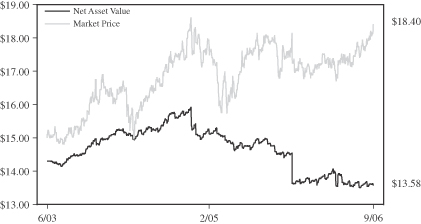

RMK HIGH INCOME FUND, INC.

NAV & MARKET PRICE HISTORY*

The graph below illustrates the net asset value and market price history of RMK High Income Fund, Inc. (NYSE: RMH) from the commencement of investment operations on June 24, 2003 to September 30, 2006.

| * | | Net asset value is calculated every day that the New York Stock Exchange is open as of the close of trading (normally 4:00 p.m. Eastern Time) by taking the closing market value of all portfolio securities, cash and other assets owned, subtracting all liabilities, then dividing the result (total net assets) by the total number of shares outstanding. The market price is the last reported price at which a share of the Fund was sold on the New York Stock Exchange. |

PERFORMANCE INFORMATION

| | | | | | | | | |

| | | AVERAGE ANNUAL TOTAL RETURNS | |

| AS OF SEPTEMBER 30, 2006 | | SIX MONTHS* | | | 1 YEAR | | | COMMENCEMENT

OF INVESTMENT

OPERATIONS1 | |

| MARKET VALUE | | 10.91 | % | | 19.87 | % | | 22.16 | % |

| NET ASSET VALUE | | 3.49 | % | | 7.53 | % | | 12.90 | % |

LEHMAN BROTHERS BA

HIGH YIELD INDEX2 | | 4.12 | % | | 6.67 | % | | 7.87 | % |

| * | Not annualized for periods less than one year. |

25

RMK HIGH INCOME FUND, INC.

| 1 | | The Fund commenced investment operations on June 24, 2003. |

| 2 | | The Lehman Brothers Ba U.S. High Yield Index covers the universe of fixed rate, non-investment grade debt. Pay-in-kind (PIK) bonds, Eurobonds and debt issues from countries designated as emerging markets (e.g., Argentina, Brazil, Venezuela, etc.) are excluded, but Canadian and global bonds (SEC registered) of issuers in non-emerging countries are included. Original issue zeroes, step-up coupon structures and 144As are also included. The index is unmanaged, and unlike the fund, is not affected by cashflows or trading and other expenses. It is not possible to invest directly in an index. |

Performance data quoted represents past performance which is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Fund performance changes over time and current performance may be lower or higher than what is stated. For the most recent performance, call toll-free 800-564-2188. Total returns assume an investment at the common share market price or net asset value at the beginning of the period, reinvestment of all dividends and distributions for the period in accordance with the Fund’s dividend reinvestment plan, and sale of all shares at the closing market price (excluding any commissions) or net asset value at the end of the period. Returns shown do not reflect the deduction of taxes that a stockholder would pay on Fund distributions or on the sale of Fund shares.

26

RMK HIGH INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount

| | | | Description | | Value (b) |

| | Asset Backed Securities–Investment Grade–9.0% of Net Assets | | | |

| | | | | | Collateralized Debt Obligations–6.4% | | | |

| $ | 5,000,000 | | | | Commodore 1A C, 7.970% 2/28/37 (a) | | $ | 2,650,000 |

| | 1,913,862 | | | | E-Trade 2004-1A COM1, 2.000% 1/10/40 | | | 1,933,001 |

| | 2,000,000 | | | | Linker Finance PLC 16A E, 8.752% 5/19/45 (a) | | | 1,950,000 |

| | 3,000,000 | | | | Palmer Square 2A CN, 12.000% 11/2/45 (a) | | | 2,970,000 |

| | 4,000,000 | | | | Taberna Preferred Funding 2006-6A COM,

Zero Coupon Bond 12/5/36 (a) | | | 3,965,600 |

| | 3,000,000 | | | | Taberna Preferred Funding, Ltd 2006-7A C1,

Zero Coupon Bond 2/5/37 (a) | | | 2,952,000 |

| | 1,500,000 | | | | Trapeza CDO LLC 2006-10A, Zero Coupon Bond 6/6/41 | | | 1,440,000 |

| | 2,000,000 | | | | Trapeza CDO LLC, 8.70% 6/6/41 (a) | | | 2,000,000 |

| | | | | | | |

|

|

| | | | | | | | | 19,860,601 |

| | | | | | | |

|

|

| | | | | | Equipment Leases–1.3% | | | |

| | 2,912,743 | | | | Aviation Capital 2005-3A C1, 8.573% 12/25/35 (a) | | | 2,970,998 |

| | 3,000,000 | | | | United Capital Aviation Trust 2005-1 B1A,

Zero Coupon Bond 7/15/31 (a) | | | 959,040 |

| | | | | | | |

|

|

| | | | | | | | | 3,930,038 |

| | | | | | | |

|

|

| | | | | | Franchise Loans–0.2% | | | |

| | | | | | Atherton Franchisee 1999-A AX, 1.082% 3/15/19

interest-only strips (a) | | | 534,899 |

| | | | | | | |

|

|

| | | | | | Home Equity Loans–1.1% | | | |

| | 871,300 | | | | Ameriquest Mortgage 2003-8 MV6, 9.073% 10/25/33 | | | 882,323 |

| | 1,000,000 | | | | Asset Backed Securities 2005-HE1 M10, 8.323% 3/25/35 | | | 929,060 |

| | 2,000,000 | | | | Soundview 2005-A B1, 8.323% 4/25/35 (a) | | | 1,600,000 |

| | | | | | | |

|

|

| | | | | | | | | 3,411,383 |

| | | | | | | |

|

|

| | | | | | Total Asset Backed Securities–Investment Grade

(cost $28,847,199) | | | 27,736,921 |

| | | | | | | |

|

|

| | Asset Backed Securities–Below Investment Grade or Unrated–45.1% of Net Assets |

| | | | | | Certificate-Backed Obligations–2.5% | | | |

| | 1,000,000 | | | | Preferred Term Securities II, 12.000% 5/22/33 (a) | | | 674,940 |

| | 1,000,000 | | | | Preferred Term Securities XXI, 10.000% 3/22/38 (a) | | | 987,480 |

| | 4,000,000 | | | | Preferred Term Securities XXII, Zero Coupon Bond 9/22/36 (a) | | | 3,970,560 |

| | 2,000,000 | | | | Preferred Term Securities XXIII, Zero Coupon Bond 12/22/36 (a) | | | 1,976,000 |

| | | | | | | |

|

|

| | | | | | | | | 7,608,980 |

| | | | | | | |

|

|

| | | | | | Collateralized Debt Obligations–14.2% | | | |

| | 1,000,000 | | | | 801 Grand CDO 06-1 LLC, 11.390% 9/20/16 (a) | | | 982,500 |

| | 2,000,000 | | | | Acacia CDO, Ltd. 10A, Zero Coupon Bond 9/7/46 (a) | | | 912,200 |

| | 3,000,000 | | | | Aladdin CDO 2006-3A, 10.390% 10/31/13 (a) | | | 1,410,000 |

| | 2,000,000 | | | | Arlington Street CDO 1A B, 8.970% 6/10/12 (a) | | | 1,730,000 |

27

RMK HIGH INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount

| | | | Description | | Value (b) |

| | Asset Backed Securities–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Collateralized Debt Obligations (continued) | | | |

| $ | 3,000,000 | | | | Attentus CDO Ltd. 2006-2A COM, Zero Coupon Bond 10/9/41 | | $ | 2,916,000 |

| | 1,664,084 | | | | Cigna CDO Limited 2000-1A B1, 6.520% 8/28/12 (a) | | | 1,249,111 |

| | 3,000,000 | | | | Diversified Asset Securitization 2 1A B1, 9.712% 9/15/35 (a) | | | 1,590,000 |

| | 3,000,000 | | | | Dryden Leveraged Loan CDO 2005-9A DFN, Zero Coupon Bond 9/20/19 | | | 2,550,000 |

| | 3,000,000 | | | | GSC Partners CDO Fund Ltd 2006-7A COM1, 5.075% 5/25/20 (a) | | | 2,990,400 |

| | 2,931,764 | | | | Hewett’s Island 2004-1A COM, 9.000% 12/15/16 | | | 2,829,152 |

| | 2,000,000 | | | | Jazz CDO BV III-A EB, 10.713% 9/26/14 (a) | | | 1,974,440 |

| | 5,000,000 | | | | Kenmore Street Synthetic CDO 2006-1A, 10.390% 4/30/14 (a) | | | 2,300,000 |

| | 1,000,000 | | | | Knollwood CDO Ltd. 2006-2A E, 11.488% 7/13/46 (a) | | | 1,000,000 |

| | 2,000,000 | | | | Knollwood CDO Ltd. 2006-2A SN, Zero Coupon Bond 7/13/46 | | | 1,840,000 |

| | 4,000,000 | | | | Kodiak CDO 2006-1A COMB, Zero Coupon Bond 8/7/37 (a) | | | 3,600,000 |

| | 1,000,000 | | | | Marquette Park CLO, 10.000% 7/12/20 (a) | | | 980,000 |

| | 2,000,000 | | | | Millstone III CDO Ltd, Zero Coupon Bond 7/5/46 | | | 1,940,000 |

| | 1,931,858 | | | | MKP 4A CS, 2.000% 7/12/40 (a) | | | 1,861,152 |

| | 3,000,000 | | | | OFSI Fund 2006-1A COM1, 2.000% 9/20/19 (a) | | | 3,000,000 |

| | 2,000,000 | | | | Rosedale CLO Ltd I-A II, 5.146% 7/26/21 (a) | | | 1,920,000 |

| | 2,000,000 | | | | Tropic CDO Corp. 2006-5A C1, Zero Coupon Bond 7/15/36 | | | 1,894,000 |

| | 2,000,000 | | | | Veritas 2006-2A, 15.000% 7/11/21 (a) | | | 1,920,000 |

| | | | | | | |

|

|

| | | | | | | | | 43,388,955 |

| | | | | | | |

|

|

| | | | | | Collateralized Loan Obligations–0.3% | | | |

| | 1,000,000 | | | | Flagship CLO 2005-4I, Zero Coupon Bond 6/1/17 | | | 946,250 |

| | | | | | | |

|

|

| | | | | | Commercial Loans–1.6% | | | |

| | 84,068 | | | | CS First Boston 1995-WF1 G, 8.570% 12/21/27 | | | 80,693 |

| | 1,967,335 | | | | Lehman Brothers-UBS Commercial Mortgage 2001-C7 S,

5.868% 11/15/33 | | | 1,101,983 |

| | 2,000,000 | | | | Merrill Lynch Mortgage 1998-C1 F, 6.250% 11/15/26 | | | 1,190,420 |

| | 2,000,000 | | | | North Street Referenced Linked Notes 2000-1A,

6.876% 4/28/11 (a) | | | 1,560,000 |

| | 2,000,000 | | | | North Street Referenced Linked Notes 2000-1A D1,

7.726% 4/28/11 (a) | | | 900,000 |

| | | | | | | |

|

|

| | | | | | | | | 4,833,096 |

| | | | | | | |

|

|

| | | | | | Equipment Leases–16.5% | | | |

| | 5,215,800 | | | | Aerco Limited 1X C1, 6.549% 7/15/23 | | | 2,047,202 |

| | 4,235,094 | | | | Aerco Limited 2A B2, 6.380% 7/15/25 (a) | | | 2,075,196 |

| | 7,021,106 | | | | Aerco Limited 2A C2, 7.249% 7/15/25 (a) | | | 2,246,754 |

| | 10,000,000 | | | | Aircraft Finance Trust 1999-1A A1, 5.679% 5/15/24 (a) | | | 7,075,000 |

| | 5,000,000 | | | | Airplanes Pass Through Trust 2001-1A A9, 5.749% 3/15/19 | | | 3,256,250 |

| | 861,499 | | | | DVI Receivables 2001-2 A3, 3.519% 11/8/31 | | | 663,354 |

| | 1,208,992 | | | | DVI Receivables 2001-2 A4, 4.613% 11/11/09 | | | 943,013 |

28

RMK HIGH INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount

| | | | Description | | Value (b) |

| | Asset Backed Securities–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Equipment Leases (continued) | | | |

| $ | 4,592,094 | | | | DVI Receivables 2002-1 A3A, 5.520% 6/11/10 | | $ | 2,617,493 |

| | 1,434,613 | | | | DVI Receivables 2003-1 A3A, 5.830% 3/14/11 | | | 1,219,421 |

| | 16,000,000 | | | | Lease Investment Flight Trust 1 A1, 5.589% 7/15/31 | | | 11,400,000 |

| | 5,000,000 | | | | Pegasus Aviation Lease 1999-1A A2, 6.300% 3/25/29 (a) | | | 2,175,000 |

| | 1,000,000 | | | | Pegasus Aviation Lease 1999-1A B1, 6.300% 3/25/29 (a) | | | 218,930 |

| | 3,687,467 | | | | Pegasus Aviation Lease 2000-1 A1, 5.948% 3/25/15 (a) | | | 2,359,979 |

| | 20,000,000 | | | | Pegasus Aviation Lease 2001-1A A1, 5.655% 3/25/30 (a) | | | 12,250,000 |

| | 3,517,584 | | | | Pegasus Aviation Lease 2001-1A B1, 6.670% 5/10/31 (a) | | | 105,528 |

| | 1,758,792 | | | | Pegasus Aviation Lease 2001-1A B2, 7.270% 5/10/31 (a) | | | 52,764 |

| | | | | | | |

|

|

| | | | | | | | | 50,705,884 |

| | | | | | | |

|

|

| | | | | | Franchise Loans–1.2% | | | |

| | 1,000,000 | | | | Falcon Franchise Loan 2001-1 F, 6.500% 1/5/23 | | | 591,850 |

| | 3,548,000 | | | | Falcon Franchise Loan 2003-1 D, 7.836% 1/5/25 (a) | | | 3,201,705 |

| | | | | | | |

|

|

| | | | | | | | | 3,793,555 |

| | | | | | | |

|

|

| | | | | | Home Equity Loans–8.8% | | | |

| | 1,500,000 | | | | Ace Securities 2005-HE2 B1, 8.573% 4/25/35 (a) | | | 1,230,000 |

| | 2,000,000 | | | | Ace Securities 2005-HE6 B1, 8.323% 10/25/35 (a) | | | 1,560,000 |

| | 2,000,000 | | | | Ace Securities 2005-SL1 B1, 6.000% 6/25/35 (a) | | | 1,720,000 |

| | 661,176 | | | | Amresco Residential Securities 1999-1 B, 9.323% 11/25/29 | | | 638,530 |

| | 2,000,000 | | | | Asset Backed Securities Corp Home Equity 2006-HE4 M9,

7.823% 5/25/36 (a) | | | 1,788,440 |

| | 2,649,475 | | | | Delta Funding Home Equity 2000-1 B, 8.090% 5/15/30 | | | 1,086,576 |

| | 1,000,000 | | | | Equifirst Mortgage 2005-1 B3, 8.573% 4/25/35 (a) | | | 822,500 |

| | 2,000,000 | | | | First Franklin Mortgage 2004-FFH4 B1, 6.762% 1/25/35 (a) | | | 1,755,520 |

| | 3,000,000 | | | | Meritage Asset Holdings NIM 2005-2 N4, 7.500% 11/25/35 (a) | | | 2,220,000 |

| | 2,000,000 | | | | Merrill Lynch Mortgage 2005-SL1 B5, 8.823% 6/25/35 (a) | | | 1,760,000 |

| | 2,000,000 | | | | Nomura Home Equity Loan Inc. 2005-HE1 B1, 7.773% 9/25/35 | | | 1,775,000 |

| | 1,305,646 | | | | Structured Asset 2003-S A, 7.500% 12/28/33 (a) | | | 913,952 |

| | 2,729,121 | | | | Terwin Mortgage 2005-11SL B7, 5.000% 11/25/36 (a) | | | 2,278,816 |

| | | | | | Terwin Mortgage 2005-3SL B6, 11.500% 3/25/35 interest-only strips | | | 326,291 |

| | 1,800,697 | | | | Terwin Mortgage 2005-7SL, 6.500% 7/25/35 (a) | | | 1,568,857 |

| | 3,000,000 | | | | Terwin Mortgage 2005-R1, 5.000% 12/28/36 (a) | | | 2,227,500 |

| | 4,000,000 | | | | Terwin Mortgage 2006-R3, 6.290% 6/26/37(a) | | | 3,269,600 |

| | | | | | | |

|

|

| | | | | | | | | 26,941,582 |

| | | | | | | |

|

|

| | | | | | Total Asset Backed Securities–Below Investment Grade

or Unrated (cost $144,969,728) | | | 138,218,302 |

| | | | | | | |

|

|

29

RMK HIGH INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount

| | | | Description | | Value (b) |

| | Corporate Bonds–Investment Grade–1.9% of Net Assets | | | |

| | | | | | Special Purpose Entity–1.9% | | | |

| $ | 4,000,000 | | | | Duane Park I, Zero Coupon Bond 6/27/16 (a) | | $ | 4,000,000 |

| | 2,000,000 | | | | Lincoln Park Ref Link 01-1, 8.905% 7/30/31 (a) | | | 1,780,000 |

| | | | | | | |

|

|

| | | | | | Total Corporate Bonds–Investment Grade

(cost $5,780,460) | | | 5,780,000 |

| | | | | | | |

|

|

| | Corporate Bonds–Below Investment Grade or Unrated–40.5% of Net Assets | | | |

| | | | | | Apparel–1.1% | | | |

| | 3,475,000 | | | | Rafaella Apparel, 11.250% 6/15/11 (a) | | | 3,414,187 |

| | | | | | | |

|

|

| | | | | | Appliances–0.6% | | | |

| | 1,943,000 | | | | Windmere-Durable, 10.000% 7/31/08 | | | 1,943,000 |

| | | | | | | |

|

|

| | | | | | Automotive–3.8% | | | |

| | 1,725,000 | | | | Cooper Standard Auto, 8.375% 12/15/14 | | | 1,267,875 |

| | 1,750,000 | | | | Dana Corporation, Zero Coupon Bond 1/15/15 in default (c) | | | 1,146,250 |

| | 1,125,000 | | | | Dana Corporation, Zero Coupon Bond 3/15/10 in default (c) | | | 781,875 |

| | 725,000 | | | | Delco Remy International Inc, 11.000% 5/1/09 | | | 348,000 |

| | 900,000 | | | | Delphi Corporation, Zero Coupon Bond 5/1/29 in default (c) | | | 760,500 |

| | 1,025,000 | | | | Dura Operating, 8.625% 4/15/12 | | | 406,156 |

| | 1,350,000 | | | | Dura Operating, 9.000% 5/1/09 | | | 57,375 |

| | 1,250,000 | | | | Federal-Mogul, Zero Coupon Bond 1/15/09 in default (c) | | | 718,750 |

| | 1,950,000 | | | | Ford Motor, 7.450% 7/16/31 | | | 1,506,375 |

| | 175,000 | | | | Ford Motor, 9.980% 2/15/47 | | | 152,250 |

| | 1,825,000 | | | | General Motors, 8.375% 7/15/33 | | | 1,578,625 |

| | 275,000 | | | | Metaldyne Corp., 10.000% 11/1/13 | | | 277,750 |

| | 3,075,000 | | | | Metaldyne Corp., 11.000% 6/15/12 | | | 2,767,500 |

| | | | | | | |

|

|

| | | | | | | | | 11,769,281 |

| | | | | | | |

|

|

| | | | | | Basic Materials–2.3% | | | |

| | 3,625,000 | | | | Edgen Acquisition, 9.875% 2/1/11 | | | 3,588,750 |

| | 1,825,000 | | | | FMG Finance, 10.625% 9/1/16 (a) | | | 1,752,000 |

| | 2,075,000 | | | | Millar Western, 7.750% 11/15/13 | | | 1,722,250 |

| | | | | | | |

|

|

| | | | | | | | | 7,063,000 |

| | | | | | | |

|

|

| | | | | | Building & Construction–0.7% | | | |

| | 450,000 | | | | William Lyon Homes, 7.625% 12/15/12 | | | 363,375 |

| | 1,350,000 | | | | Owens Corning, Zero Coupon Bond 8/1/18 in default (c) | | | 691,875 |

| | 1,275,000 | | | | Tech Olympic USA, Inc., 10.375% 7/1/12 | | | 1,102,875 |

| | | | | | | |

|

|

| | | | | | | | | 2,158,125 |

| | | | | | | |

|

|

| | | | | | Communications–1.2% | | | |

| | 3,850,000 | | | | CCH I Holdings LLC, 11.750% 5/15/11 | | | 2,743,125 |

| | 771,000 | | | | CCH I Holdings, 11.000% 10/1/15 | | | 701,610 |

| | 300,000 | | | | Penton Media, 10.375% 6/15/11 | | | 295,500 |

| | | | | | | |

|

|

| | | | | | | | | 3,740,235 |

| | | | | | | |

|

|

30

RMK HIGH INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount

| | | | Description | | Value (b) |

| | Corporate Bonds–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Consulting Services–1.2% | | | |

| $ | 2,300,000 | | | | MSX International, 11.375% 1/15/08 | | $ | 1,649,376 |

| | 2,000,000 | | | | MSX International, 11.000% 10/15/07 | | | 1,920,000 |

| | | | | | | |

|

|

| | | | | | | | | 3,569,376 |

| | | | | | | |

|

|

| | | | | | Electronics–0.5% | | | |

| | 1,600,000 | | | | Motors and Gears, 10.750% 11/15/06 | | | 1,596,285 |

| | | | | | | |

|

|

| | | | | | Energy–1.9% | | | |

| | 1,900,000 | | | | Neptune Marine Invest, 10.920% 9/7/09 (a) | | | 1,914,250 |

| | 3,900,000 | | | | Paramount Resources Ltd, 8.500% 1/31/13* | | | 3,909,750 |

| | | | | | | |

|

|

| | | | | | | | | 5,824,000 |

| | | | | | | |

|

|

| | | | | | Finance–0.8% | | | |

| | 2,500,000 | | | | Advanta Capital Trust I, 8.990% 12/17/26 | | | 2,531,250 |

| | | | | | | |

|

|

| | | | | | Food–1.0% | | | |

| | 1,525,000 | | | | Eurofresh Inc, 11.500% 1/15/13 (a) | | | 1,486,875 |

| | 2,300,000 | | | | Merisant, 9.500% 7/15/13 | | | 1,472,000 |

| | | | | | | |

|

|

| | | | | | | | | 2,958,875 |

| | | | | | | |

|

|

| | | | | | Garden Products–0.3% | | | |

| | 965,000 | | | | Ames True Temper, 10.000% 7/15/12 | | | 827,488 |

| | | | | | | |

|

|

| | | | | | Human Resources–0.5% | | | |

| | 1,500,000 | | | | Comforce Operating, 12.000% 12/1/07 | | | 1,496,400 |

| | | | | | | |

|

|

| | | | | | Industrial–7.7% | | | |

| | 2,550,000 | | | | Advanced Lighting Technologies, 11.000% 3/31/09 | | | 2,537,250 |

| | 3,000,000 | | | | Consolidated Container, 10.125% 7/15/09 | | | 2,865,000 |

| | 825,000 | | | | Constar International, 11.000% 12/1/12 | | | 717,750 |

| | 2,500,000 | | | | Continental Global Group, 9.000% 10/1/08 | | | 2,427,600 |

| | 750,000 | | | | Corp Durango SA, 8.500% 12/31/12 | | | 697,500 |

| | 3,075,000 | | | | GSI Group, 12.000% 5/15/13 (a) | | | 3,290,250 |

| | 1,400,000 | | | | Home Products International, 9.625% 5/15/08 | | | 910,000 |

| | 2,125,000 | | | | IMAX Corp, 9.625% 12/1/10 | | | 2,024,062 |

| | 1,325,000 | | | | Spectrum Brands, 8.500% 10/1/13 | | | 1,146,125 |

| | 1,350,000 | | | | Terphane Holding Corp, 12.500% 6/15/09 (a) | | | 1,350,000 |

| | 1,050,000 | | | | Trimas Corp., 9.875% 6/15/12 | | | 971,250 |

| | 975,000 | | | | VITRO S.A., 11.750% 11/1/13 (a) | | | 1,018,875 |

| | 2,775,000 | | | | Wolverine Tube, 7.375% 8/1/08 (a) | | | 2,358,750 |

| | 500,000 | | | | Wolvernine Tube, 10.500% 4/1/09 | | | 440,000 |

| | 900,000 | | | | Wornick Company, 10.875% 7/15/11 | | | 895,500 |

| | | | | | | |

|

|

| | | | | | | | | 23,649,912 |

| | | | | | | |

|

|

| | | | | | Manufacturing–3.1% | | | |

| | 3,520,000 | | | | BGF Industries, 10.250% 1/15/09 | | | 3,313,200 |

31

RMK HIGH INCOME FUND, INC.

PORTFOLIOOF INVESTMENTS

SEPTEMBER 30, 2006 (UNAUDITED)

| | | | | | | | |

Principal

Amount

| | | | Description | | Value (b) |

| | Corporate Bonds–Below Investment Grade or Unrated (continued) | | | |

| | | | | | Manufacturing (continued) | | | |

| $ | 1,725,000 | | | | Elgin National Industries, 11.000% 11/1/07 | | $ | 1,725,604 |

| | 2,725,000 | | | | Maax Corp, 9.750% 6/15/12 | | | 2,152,750 |

| | 2,725,000 | | | | JB Poindexter & Co., 8.750% 3/15/14 | | | 2,248,125 |

| | | | | | | |

|

|

| | | | | | | | | 9,439,679 |

| | | | | | | |

|

|

| | | | | | Health Care–1.4% | | | |

| | 2,750,000 | | | | Healthsouth Corp, 11.418% 6/15/14 (a) | | | 2,805,000 |

| | 4,000,000 | | | | Insight Health Services, 9.875% 11/1/11 | | | 1,370,000 |

| | | | | | | |

|

|

| | | | | | | | | 4,175,000 |

| | | | | | | |

|

|

| | | | | | Retail–1.9% | | | |