Exhibit 99.3

2007 Earnings Guidance January 12, 2007

Agenda

Introduction and Overview

– Chuck Raymond – Chairman, President & Chief Executive Officer

Commercial and Operations Outlook

– John Handy – Executive Vice President

Financial Outlook

– Mike Avara – Vice President, Investor Relations & Treasurer

Questions and Answers

Forward-Looking Statements

Risks, Uncertainties, Other Factors with Respect to “Forward-Looking Statements:”

Certain statements contained in this presentation constitute “forward-looking statements” within the meaning of the Private Securities Litigation Reform Act of 1995. Such statements that are not of historical fact constitute “forward-looking statements” and, accordingly, involve estimates, assumptions, judgments and uncertainties. There are a number of factors that could cause actual results or outcomes to differ materially from those addressed in the “forward-looking statements”. Such factors are detailed in the Horizon Lines, Inc.’s final prospectus filed with the Securities and Exchange Commission on November 17, 2006. Other factors may include changes in tax laws or their interpretation or application, adverse tax audits and other tax matters.

2007 Earnings Guidance

Chuck Raymond

Chairman, President & Chief Executive Officer

Introduction and Overview

2007 Outlook – Investing in the Future

Five new “Hunter-class” vessels

Maersk agreements extended to 2010

Horizon Edge initiative

Terminal and equipment improvements

Technology innovation and investment

Container fleet upgrades

”Red, White and Blue” strategic growth

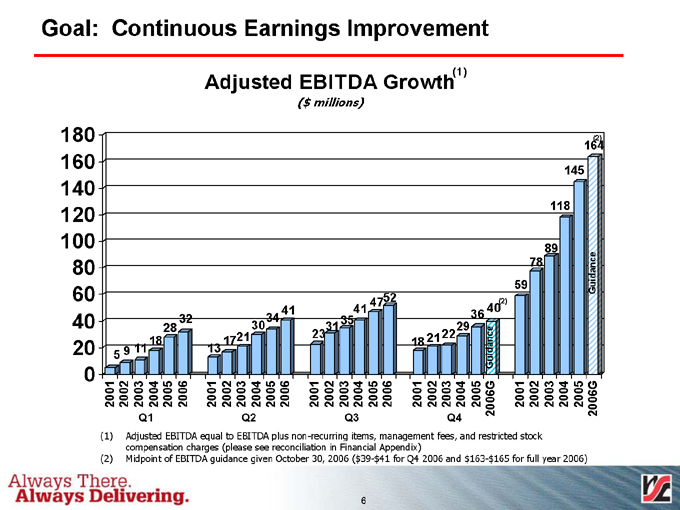

Goal: Continuous Earnings Improvement

(1)

Adjusted EBITDA Growth

($ millions)

180 160 140 120 100 80 60 40 20 0

28 32 18 5 9 11

41 3034 21 13 17

52 41 47 35 23 31 (2)

36 40 29 Guidance 18 2122 (2)

164 145 118 89 78 Guidance 59

2001 2002 2003 2004 2005 2006

2001 2002 2003 2004 2005 2006

2001 2002 2003 2004 2005 2006

2001 2002 2003 2004 2005 2006G

2001 2002 2003 2004 2005 2006G

Q1 Q2 Q3 Q4

(1) Adjusted EBITDA equal to EBITDA plus non-recurring items, management fees, and restricted stock compensation charges (please see reconciliation in Financial Appendix)

(2) Midpoint of EBITDA guidance given October 30, 2006 ($39-$41 for Q4 2006 and $163-$165 for full year 2006)

2007 Earnings Guidance

John Handy Executive Vice President

Commercial and Operations Outlook

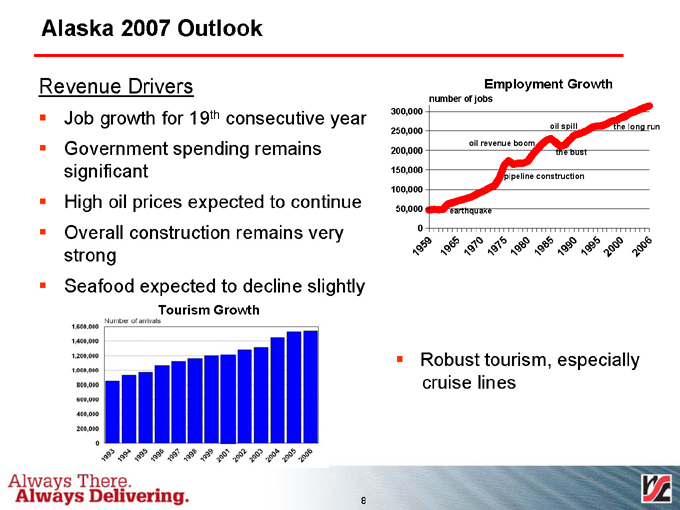

Alaska 2007 Outlook

Revenue Drivers

Job growth for 19th consecutive year

Government spending remains significant

High oil prices expected to continue

Overall construction remains very strong

Seafood expected to decline slightly

Tourism Growth

Employment Growth

number of jobs

300,000 250,000 200,000 150,000 100,000 50,000 0

19 59 19 65 19 70 19 75 19 80 19 85 19 90 19 9 5 2 00 0 20 06

Robust tourism, especially cruise lines

1,600,000 1,400,000 1,200,000 1,000,000 800,000 600,000 400,000 200,000 0

1993 1994 1995 1996 1997 1998 1999 2001 2002 2003 2004 2005 2006

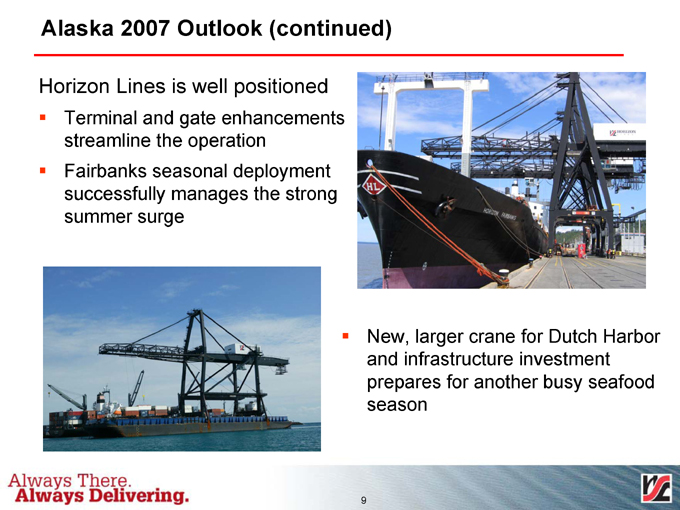

Alaska 2007 Outlook (continued)

Horizon Lines is well positioned

Terminal and gate enhancements streamline the operation

Fairbanks seasonal deployment successfully manages the strong summer surge

New, larger crane for Dutch Harbor and infrastructure investment prepares for another busy seafood season

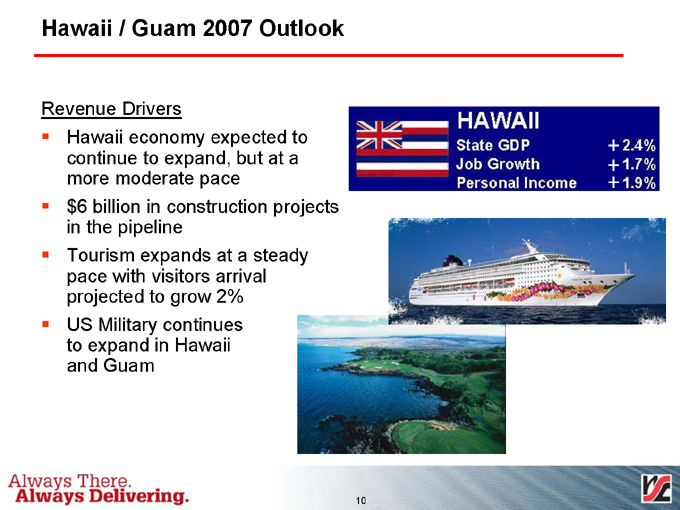

Hawaii / Guam 2007 Outlook

Revenue Drivers

Hawaii economy expected to continue to expand, but at a more moderate pace

$6 billion in construction projects in the pipeline

Tourism expands at a steady pace with visitors arrival projected to grow 2%

US Military continues to expand in Hawaii and Guam

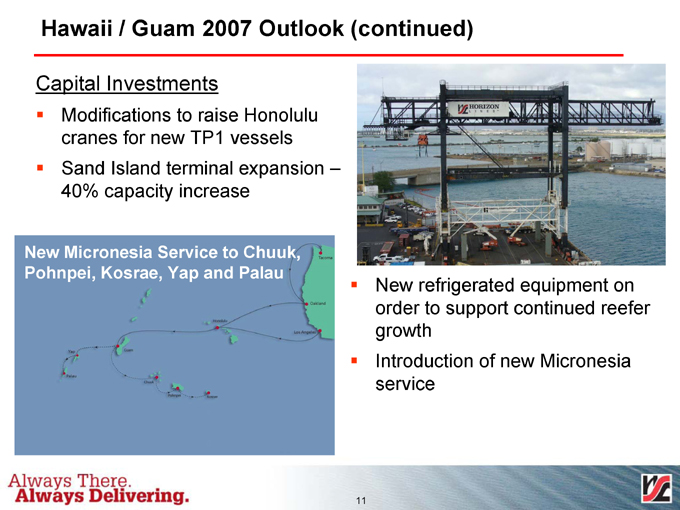

Hawaii / Guam 2007 Outlook (continued)

Capital Investments

Modifications to raise Honolulu cranes for new TP1 vessels

Sand Island terminal expansion – 40% capacity increase

New Micronesia Service to Chuuk, Pohnpei, Kosrae, Yap and Palau

New refrigerated equipment on order to support continued reefer growth

Introduction of new Micronesia service

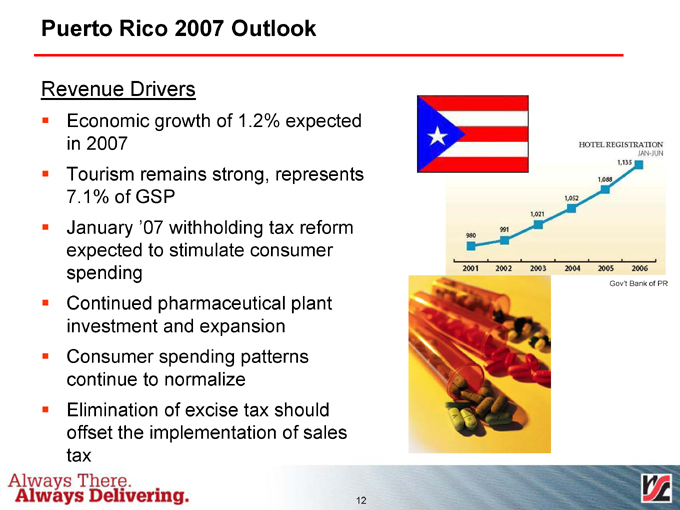

Puerto Rico 2007 Outlook

Revenue Drivers

Economic growth of 1.2% expected in 2007

Tourism remains strong, represents 7.1% of GSP

January ‘07 withholding tax reform expected to stimulate consumer spending

Continued pharmaceutical plant investment and expansion

Consumer spending patterns continue to normalize

Elimination of excise tax should offset the implementation of sales tax

HOTEL REGISTRATION JAN-JUN

980 991 1,021 1,052 1,088 1,135

2001 2002 2003 2004 2005 2006

Gov’t Bank of PR

Puerto Rico 2007 Outlook (continued)

Capital Investments

San Juan terminal realignment will lead to improved operating efficiency

New generation gate automation will improve turntimes and enhance customer service

New equipment strengthens the Horizon Lines value proposition with customers

Cost reductions in Puerto Rico operations leads to improved operating margins

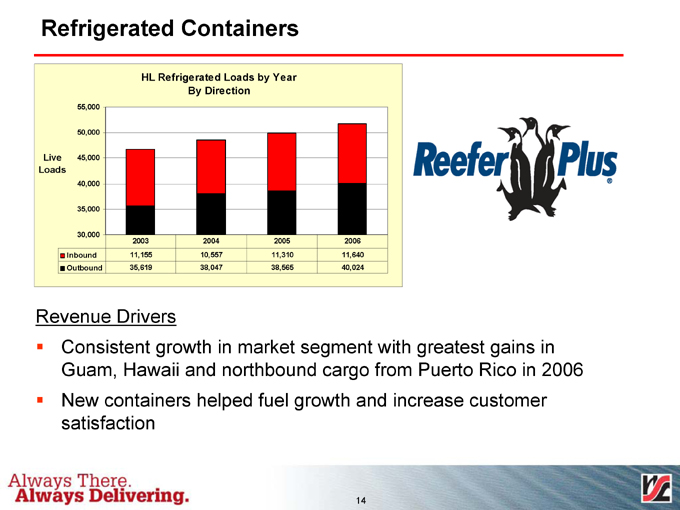

Refrigerated Containers

HL Refrigerated Loads by Year By Direction

Live Loads

55,000 50,000 45,000 40,000 35,000 30,000

2003 2004 2005 2006 Inbound 11,155 10,557 11,310 11,640

Outbound 35,619 38,047 38,565 40,024

Revenue Drivers

Consistent growth in market segment with greatest gains in Guam, Hawaii and northbound cargo from Puerto Rico in 2006

New containers helped fuel growth and increase customer satisfaction

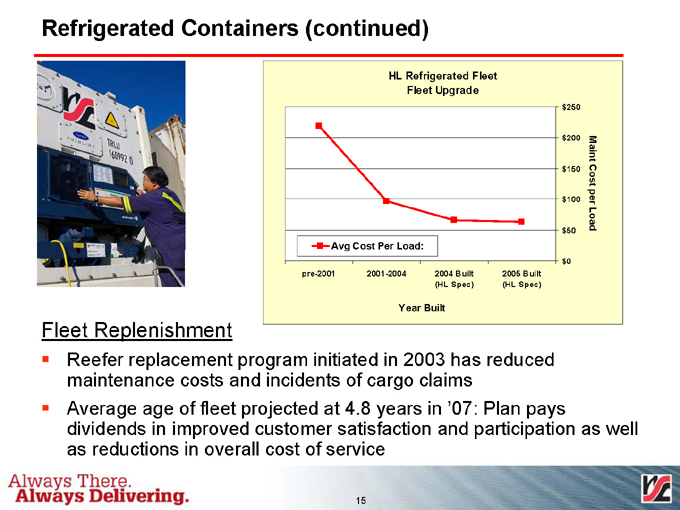

Refrigerated Containers (continued)

HL Refrigerated Fleet Fleet Upgrade

Avg Cost Per Load:

$250 $200 $150 $100 $50 $0

Maint Cost per Load

pre-2001 2001-2004 2004 Built 2005 Built (HL Spec)(HL Spec)

Year Built

Fleet Replenishment

Reefer replacement program initiated in 2003 has reduced maintenance costs and incidents of cargo claims

Average age of fleet projected at 4.8 years in ‘07: Plan pays dividends in improved customer satisfaction and participation as well as reductions in overall cost of service

Horizon TP1 (Transpacific 1) Significance

Replace older and smaller Jones Act vessels with new, less expensive to operate vessels in a capital efficient manner

Dedicate Jones Act vessels to serve only Jones Act markets, creating additional capacity and improving slot cost economics in our Hawaii and Puerto Rico trade lanes

Better serve customers’ needs as well as foster growth in the near term

New and improved TP1 service provides basis to extend agreements with Maersk, yielding stability and continued benefits through end of 2010

TP1 initiative is the first critical step in Horizon Lines’ fleet enhancement program that will generate long-term value for our customers and shareholders

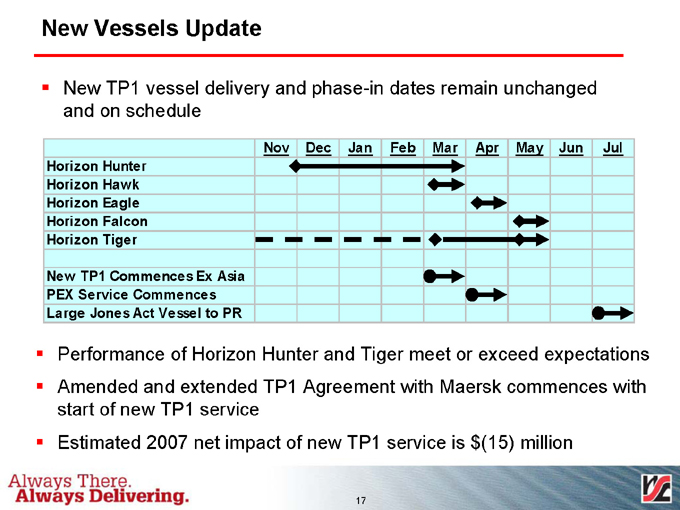

New Vessels Update

New TP1 vessel delivery and phase-in dates remain unchanged and on schedule

Horizon Hunter

Horizon Hawk

Horizon Eagle

Horizon Falcon

Horizon Tiger

New TP1 Commences Ex Asia

PEX Service Commences

Large Jones Act Vessel to PR

Nov Dec Jan Feb Mar Apr May Jun Jul

Performance of Horizon Hunter and Tiger meet or exceed expectations

Amended and extended TP1 Agreement with Maersk commences with start of new TP1 service

Estimated 2007 net impact of new TP1 service is $(15) million

Horizon Edge Significance

Edge will improve margin through better visibility into all company processes and cost drivers

Edge focus is always on customer satisfaction

Edge is also an investment in our most prized assets – our associates

Edge clarifies individual roles and responsibilities, provides training in new tools and systems, and provides clear performance expectations and accountabilities through coaching and mentoring activities

2006 Recap

All 2006 milestones achieved

Gross benefits / cost reduction ahead of plan = $3.9M vs. budget of $3.0M

2007 Savings Target

2007 net benefits projection remains at a minimum of $13M

Horizon Edge Significance (continued)

Current Sources of Benefits

Offshore Ports: Puerto Rico, Hawaii, and Alaska

Cost per lift reduced at all locations

Crane lifts per hour improved in all locations

Yard cost reductions in all locations

Crane operations and maintenance costs reduced in San Juan

Implementing in Guam, Kodiak, and Dutch Harbor in Q1 2007

Supply Chain

Web based equipment visibility tools implemented

Data integrity improvement process launched

Record number of containers returned to Asia for Maersk

Reduced cost per move over North America trucking network

Automated dispatch planning process implemented

Horizon Edge Significance (continued)

Current Sources of Benefits (cont.)

Sales

Sales performance metrics / tools implemented

System upgrades and pricing / sales tool enhancements in progress

Process alignment meetings being held

Domestic Ports

Kicked off ahead of schedule in Q4 2006

Tacoma is first of 6 domestic ports to be implemented in 2007

Horizon Edge Significance (continued)

2007 Focus = minimum of $13M of net savings / cost reduction

Equipment turntime / aging reduction program

Vessel fuel consumption reduction program

Order fulfillment process improvement

Domestic port implementation continues

Offshore port continues process improvements

Sales & Marketing revenue goals focus on integration of sales / operations goals and metrics

Inland truck / rail coordination

Organizational efficiency and process improvements

2007 Capital Outlook

Total outlook for capital expenditures in 2007 is $30M

‘‘Core” maintenance and replacement capital outlook is $14M

Level of spending in line with prior years and covers IT systems, vessel maintenance and upgrades, terminal equipment replacement and growth needs

”Strategic��� capital outlook is $16M to invest in the future in the following areas:

New TP1 Vessel Initial Capitalized Costs

Honolulu Terminal Infrastructure and Cranes

Dutch Harbor Crane

San Juan Terminal Infrastructure

2007 Dry-dock Expense

Total outlook for dry-dock cash expenditures in 2007 is $26M

9 vessels are scheduled to be dry-docked

2007 is higher than average due to regulatory timing

2005 - 6 DD vessels

2006 - 5 DD vessels

2008 per ABS will be 3 DD vessels

Phase in of new TP1 vessels will be used to cover drydock program for Hawaii/Guam vessels

2007 Earnings Guidance

Mike Avara

Vice President, Investor Relations & Treasurer

Financial Update

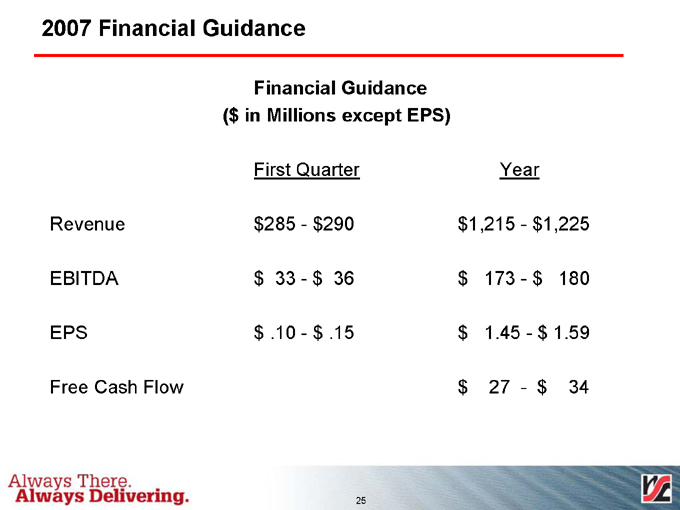

2007 Financial Guidance

Financial Guidance ($ in Millions except EPS)

Revenue EBITDA EPS Free Cash Flow

First Quarter $285 - $290 $ 33 - $ 36 $ .10 - $ .15

Year $1,215 - $1,225 $ 173 - $ 180 $ 1.45 - $ 1.59

$27 - $ 34

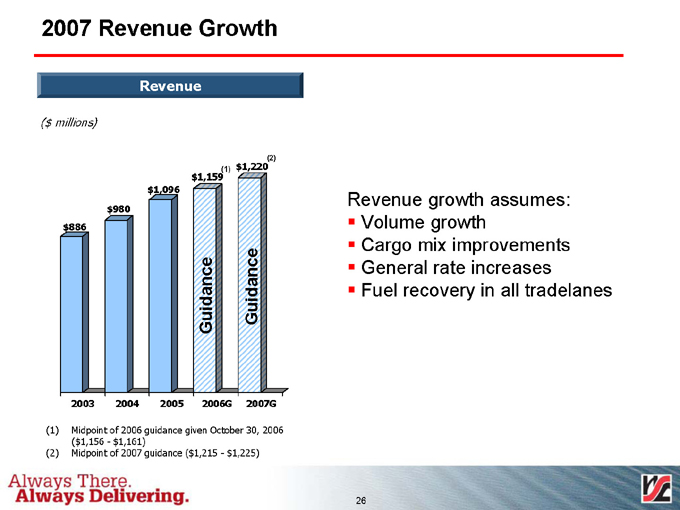

2007 Revenue Growth

Revenue

($ millions)

(2)

(1) $1,220 $1,159 $1,096 $980 $886

Guidance Guidance

2003 2004 2005 2006G 2007G

(1) Midpoint of 2006 guidance given October 30, 2006

($1,156 - $1,161)

(2) Midpoint of 2007 guidance ($1,215 - $1,225)

Revenue growth assumes:

Volume growth

Cargo mix improvements

General rate increases

Fuel recovery in all tradelanes

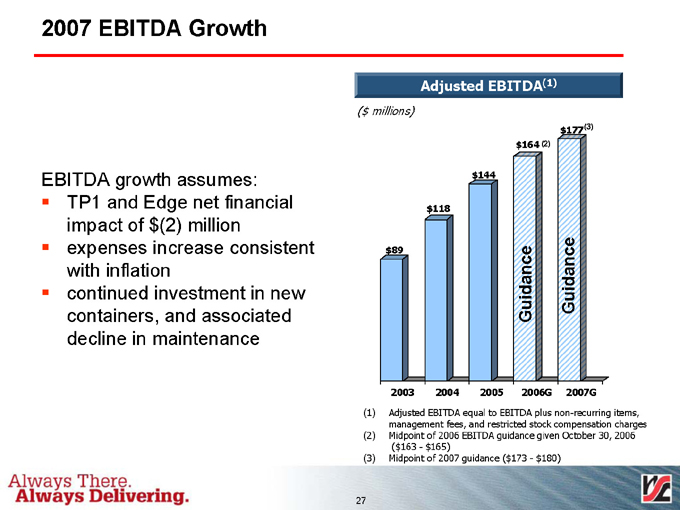

2007 EBITDA Growth

Adjusted EBITDA(1)

($ millions)

EBITDA growth assumes:

TP1 and Edge net financial impact of $(2) million

expenses increase consistent with inflation

continued investment in new containers, and associated decline in maintenance

$177(3) $164 (2)

$144

$118

$89 Guidance Guidance

2003 2004 2005 2006G 2007G

(1) Adjusted EBITDA equal to EBITDA plus non-recurring items, management fees, and restricted stock compensation charges

(2) Midpoint of 2006 EBITDA guidance given October 30, 2006 ($163 - $165)

(3) Midpoint of 2007 guidance ($173 - $180)

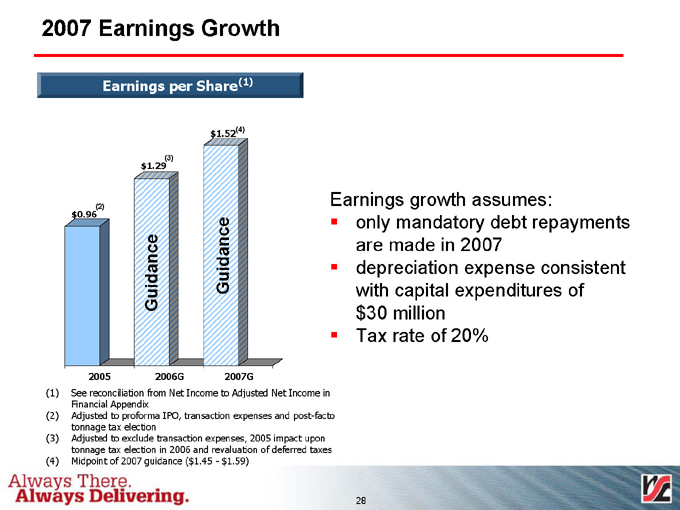

2007 Earnings Growth

Earnings per Share(1)

$1.52(4)

(3) $1.29

(2) $0.96

Guidance Guidance

2005 2006G 2007G

(1) See reconciliation from Net Income to Adjusted Net Income in Financial Appendix

(2) Adjusted to proforma IPO, transaction expenses and post-facto tonnage tax election

(3) Adjusted to exclude transaction expenses, 2005 impact upon tonnage tax election in 2006 and revaluation of deferred taxes

(4) Midpoint of 2007 guidance ($1.45 - $1.59)

Earnings growth assumes:

only mandatory debt repayments are made in 2007

depreciation expense consistent with capital expenditures of $30 million

Tax rate of 20%

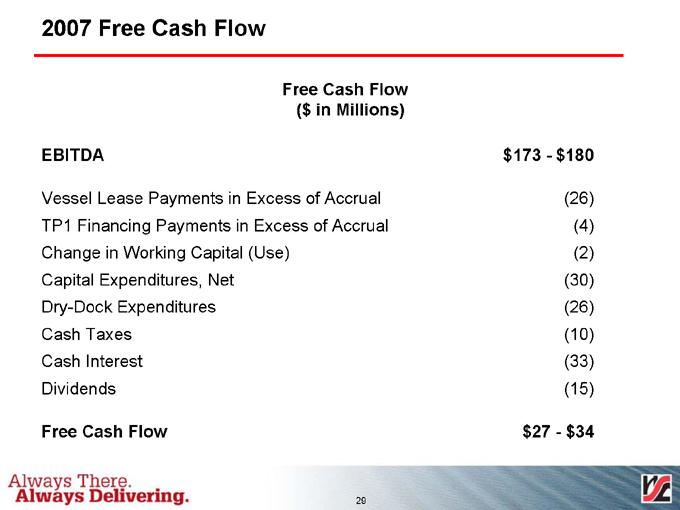

2007 Free Cash Flow

Free Cash Flow ($ in Millions)

EBITDA

Vessel Lease Payments in Excess of Accrual

TP1 Financing Payments in Excess of Accrual

Change in Working Capital (Use)

Capital Expenditures, Net

Dry-Dock Expenditures

Cash Taxes

Cash Interest

Dividends

Free Cash Flow

$173 - $180

(26) (4) (2) (30) (26) (10) (33) (15)

$27 - $34

2007 Earnings Guidance

Questions & Answers

Financial Appendix

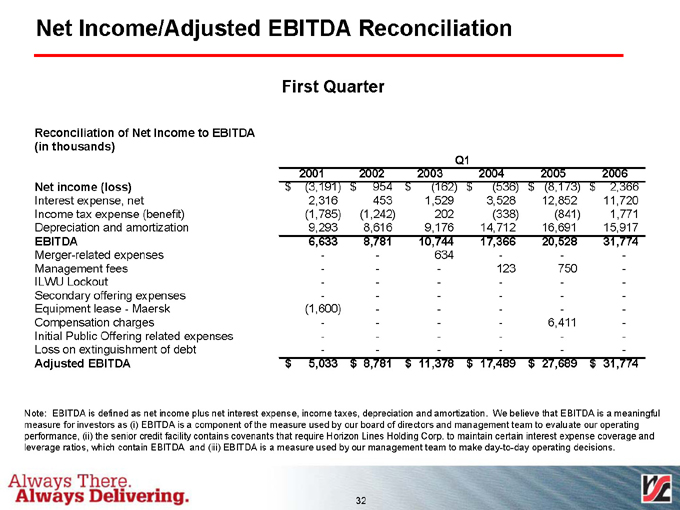

Net Income/Adjusted EBITDA Reconciliation

First Quarter

Reconciliation of Net Income to EBITDA

(in thousands)

Q1

2001

2002

2003

2004

2005

2006

Net income (loss)

$(3,191)

$954

$(162)

$(536)

$(8,173)

$2,366

Interest expense, net

2,316

453

1,529

3,528

12,852

11,720

Income tax expense (benefit)

(1,785)

(1,242)

202

(338)

(841)

1,771

Depreciation and amortization

9,293

8,616

9,176

14,712

16,691

15,917

EBITDA

6,633

8,781

10,744

17,366

20,528

31,774

Merger-related expenses

—

—

634

—

—

—

Management fees

—

—

—

123

750

—

ILWU Lockout

—

—

—

—

—

—

Secondary offering expenses

—

—

—

—

—

—

Equipment lease - Maersk

(1,600)

—

—

—

—

—

Compensation charges

—

—

—

—

6,411

—

Initial Public Offering related expenses

—

—

—

—

—

—

Loss on extinguishment of debt

—

—

—

—

—

—

Adjusted EBITDA

$5,033

$8,781

$11,378

$17,489

$27,689

$31,774

Note: EBITDA is defined as net income plus net interest expense, income taxes, depreciation and amortization. We believe that EBITDA is a meaningful measure for investors as (i) EBITDA is a component of the measure used by our board of directors and management team to evaluate our operating performance, (ii) the senior credit facility contains covenants that require Horizon Lines Holding Corp. to maintain certain interest expense coverage and leverage ratios, which contain EBITDA and (iii) EBITDA is a measure used by our management team to make day-to-day operating decisions.

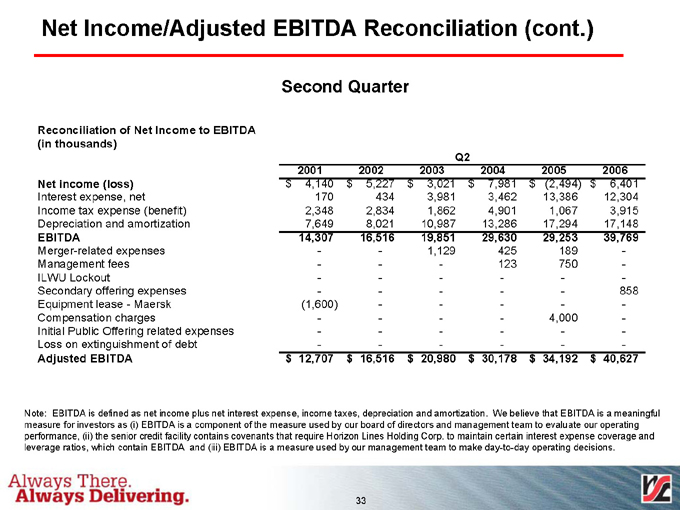

Net Income/Adjusted EBITDA Reconciliation (cont.)

Second Quarter

Reconciliation of Net Income to EBITDA

(in thousands)

Q2

2001

2002

2003

2004

2005

2006

Net income (loss)

$4,140

$5,227

$3,021

$7,981

$(2,494)

$6,401

Interest expense, net

170

434

3,981

3,462

13,386

12,304

Income tax expense (benefit)

2,348

2,834

1,862

4,901

1,067

3,915

Depreciation and amortization

7,649

8,021

10,987

13,286

17,294

17,148

EBITDA

14,307

16,516

19,851

29,630

29,253

39,769

Merger-related expenses

—

—

1,129

425

189

—

Management fees

—

—

—

123

750

—

ILWU Lockout

—

—

—

—

—

—

Secondary offering expenses

—

—

—

—

—

858

Equipment lease - Maersk

(1,600)

—

—

—

—

—

Compensation charges

—

—

—

—

4,000

—

Initial Public Offering related expenses

—

—

—

—

—

—

Loss on extinguishment of debt

—

—

—

—

—

—

Adjusted EBITDA

$12,707

$16,516

$20,980

$30,178

$34,192

$40,627

Note: EBITDA is defined as net income plus net interest expense, income taxes, depreciation and amortization. We believe that EBITDA is a meaningful measure for investors as (i) EBITDA is a component of the measure used by our board of directors and management team to evaluate our operating performance, (ii) the senior credit facility contains covenants that require Horizon Lines Holding Corp. to maintain certain interest expense coverage and leverage ratios, which contain EBITDA and (iii) EBITDA is a measure used by our management team to make day-to-day operating decisions.

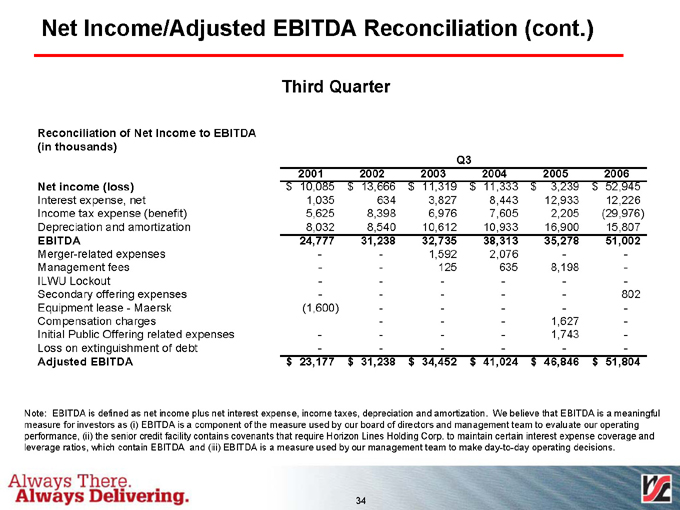

Net Income/Adjusted EBITDA Reconciliation (cont.)

Third Quarter

Reconciliation of Net Income to EBITDA

(in thousands)

Q3

2001

2002

2003

2004

2005

2006

Net income (loss)

$10,085

$13,666

$11,319

$11,333

$3,239

$52,945

Interest expense, net

1,035

634

3,827

8,443

12,933

12,226

Income tax expense (benefit)

5,625

8,398

6,976

7,605

2,205

(29,976)

Depreciation and amortization

8,032

8,540

10,612

10,933

16,900

15,807

EBITDA

24,777

31,238

32,735

38,313

35,278

51,002

Merger-related expenses

—

—

1,592

2,076

—

—

Management fees

—

—

125

635

8,198

—

ILWU Lockout

—

—

—

—

—

—

Secondary offering expenses

—

—

—

—

—

802

Equipment lease - Maersk

(1,600)

—

—

—

—

—

Compensation charges

—

—

—

1,627

—

Initial Public Offering related expenses

—

—

—

—

1,743

—

Loss on extinguishment of debt

—

—

—

—

—

—

Adjusted EBITDA

$23,177

$31,238

$34,452

$41,024

$46,846

$51,804

Note: EBITDA is defined as net income plus net interest expense, income taxes, depreciation and amortization. We believe that EBITDA is a meaningful measure for investors as (i) EBITDA is a component of the measure used by our board of directors and management team to evaluate our operating performance, (ii) the senior credit facility contains covenants that require Horizon Lines Holding Corp. to maintain certain interest expense coverage and leverage ratios, which contain EBITDA and (iii) EBITDA is a measure used by our management team to make day-to-day operating decisions.

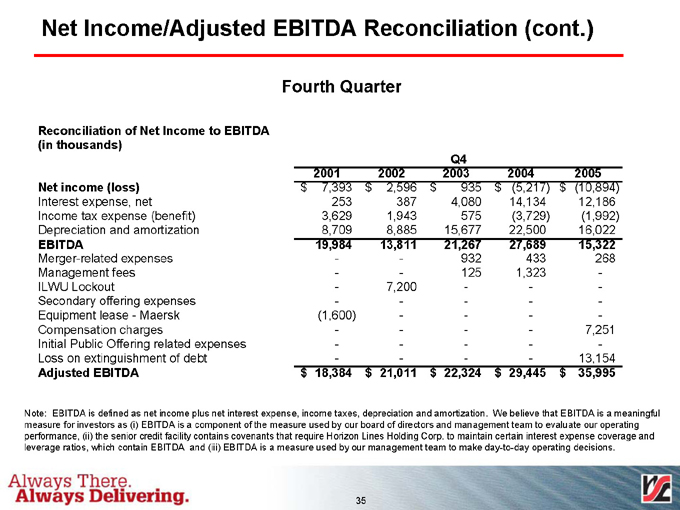

Net Income/Adjusted EBITDA Reconciliation (cont.)

Fourth Quarter

Reconciliation of Net Income to EBITDA

(in thousands)

Q4

2001

2002

2003

2004

2005

Net income (loss)

$7,393

$2,596

$935

$(5,217)

$(10,894)

Interest expense, net

253

387

4,080

14,134

12,186

Income tax expense (benefit)

3,629

1,943

575

(3,729)

(1,992)

Depreciation and amortization

8,709

8,885

15,677

22,500

16,022

EBITDA

19,984

13,811

21,267

27,689

15,322

Merger-related expenses

—

—

932

433

268

Management fees

—

—

125

1,323

—

ILWU Lockout

—

7,200

—

—

—

Secondary offering expenses

—

—

—

—

—

Equipment lease - Maersk

(1,600)

—

—

—

—

Compensation charges

—

—

—

—

7,251

Initial Public Offering related expenses

—

—

—

—

—

Loss on extinguishment of debt

—

—

—

—

13,154

Adjusted EBITDA

$18,384

$21,011

$22,324

$29,445

$35,995

Note: EBITDA is defined as net income plus net interest expense, income taxes, depreciation and amortization. We believe that EBITDA is a meaningful measure for investors as (i) EBITDA is a component of the measure used by our board of directors and management team to evaluate our operating performance, (ii) the senior credit facility contains covenants that require Horizon Lines Holding Corp. to maintain certain interest expense coverage and leverage ratios, which contain EBITDA and (iii) EBITDA is a measure used by our management team to make day-to-day operating decisions.

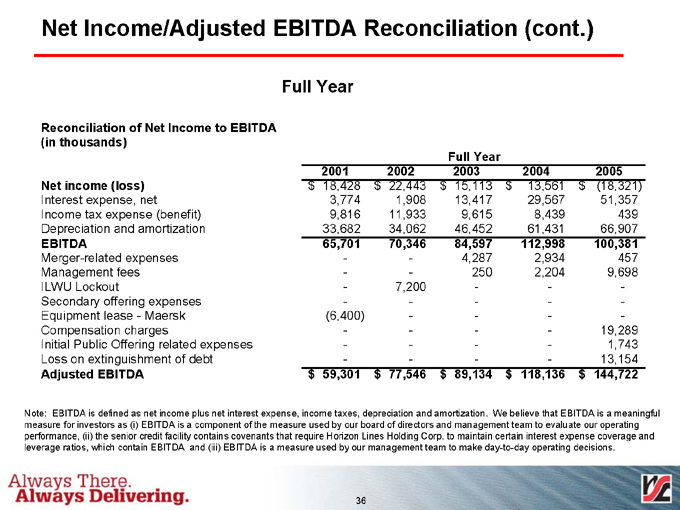

Net Income/Adjusted EBITDA Reconciliation (cont.)

Full Year

Reconciliation of Net Income to EBITDA

(in thousands)

Full Year

2001

2002

2003

2004

2005

Net income (loss)

$18,428

$22,443

$15,113

$13,561

$(18,321)

Interest expense, net

3,774

1,908

13,417

29,567

51,357

Income tax expense (benefit)

9,816

11,933

9,615

8,439

439

Depreciation and amortization

33,682

34,062

46,452

61,431

66,907

EBITDA

65,701

70,346

84,597

112,998

100,381

Merger-related expenses

—

—

4,287

2,934

457

Management fees

—

—

250

2,204

9,698

ILWU Lockout

—

7,200

—

—

—

Secondary offering expenses

—

—

—

—

—

Equipment lease - Maersk

(6,400)

—

—

—

—

Compensation charges

—

—

—

—

19,289

Initial Public Offering related expenses

—

—

—

—

1,743

Loss on extinguishment of debt

—

—

—

—

13,154

Adjusted EBITDA

$59,301

$77,546

$89,134

$118,136

$144,722

Note: EBITDA is defined as net income plus net interest expense, income taxes, depreciation and amortization. We believe that EBITDA is a meaningful measure for investors as (i) EBITDA is a component of the measure used by our board of directors and management team to evaluate our operating performance, (ii) the senior credit facility contains covenants that require Horizon Lines Holding Corp. to maintain certain interest expense coverage and leverage ratios, which contain EBITDA and (iii) EBITDA is a measure used by our management team to make day-to-day operating decisions.

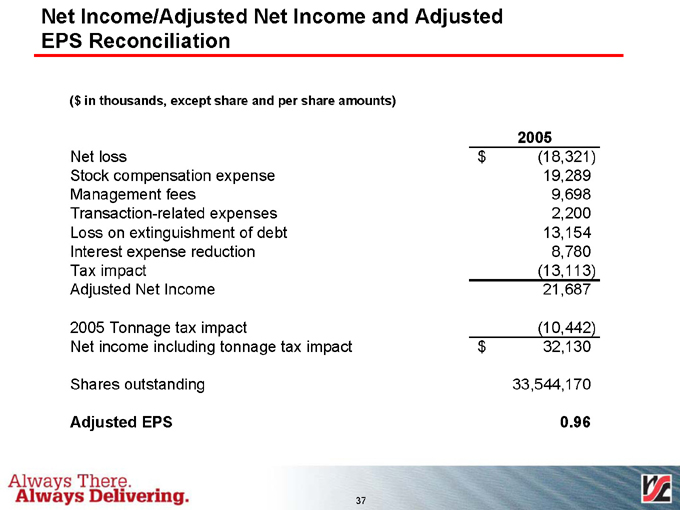

Net Income/Adjusted Net Income and Adjusted EPS Reconciliation

($ in thousands, except share and per share amounts)

2005

Net loss

$(18,321)

Stock compensation expense

19,289

Management fees

9,698

Transaction-related expenses

2,200

Loss on extinguishment of debt

13,154

Interest expense reduction

8,780

Tax impact

(13,113)

Adjusted Net Income

21,687

2005 Tonnage tax impact

(10,442)

Net income including tonnage tax impact

$32,130

Shares outstanding

33,544,170

Adjusted EPS

0.96

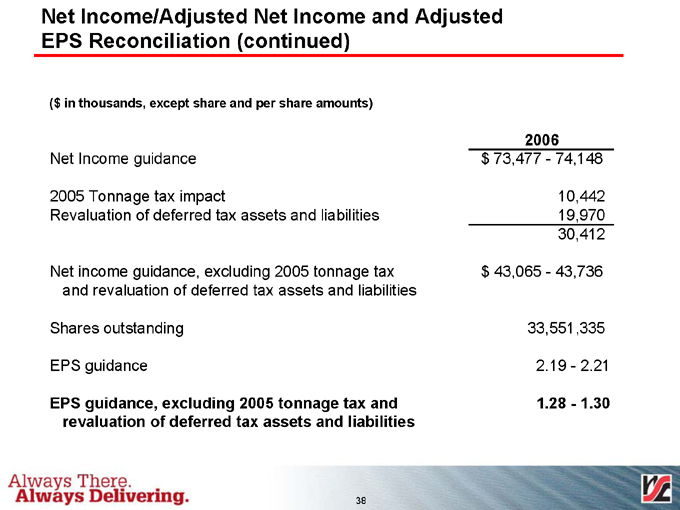

Net Income/Adjusted Net Income and Adjusted EPS Reconciliation (continued)

($ in thousands, except share and per share amounts)

Net Income guidance

2005 Tonnage tax impact

Revaluation of deferred tax assets and liabilities

Net income guidance, excluding 2005 tonnage tax and revaluation of deferred tax assets and liabilities

Shares outstanding

EPS guidance

EPS guidance, excluding 2005 tonnage tax and revaluation of deferred tax assets and liabilities

2006

$ 73,477 - 74,148

10,442 19,970

30,412

$ 43,065 - 43,736

33,551,335

2.19 - 2.21

1.28 - 1.30

40®