UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-Q

| [X] | QUARTERLY REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the quarterly period ended September 30, 2012

Or

[ ] TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES

EXCHANGE ACT OF 1934

For the transition period from _________ to _____________

Commission file number: 000-51139

TWO RIVERS WATER COMPANY

(Exact name of registrant as specified in its charter)

| Colorado | | 13-4228144 |

| State or other jurisdiction of incorporation or organization | | I.R.S. Employer Identification No. |

| | 2000 South Colorado Boulevard, Tower 1, Suite 3100, Denver, CO 80222 | |

| | (Address of principal executive offices) (Zip Code) | |

| | | |

| | Registrant’s telephone number, including area code: (303) 222-1000 | |

| | | |

| | Securities registered pursuant to Section 12(b) of the Act: | |

| Title of each class registered | | Name of each exchange on which registered |

| Not Applicable | | Not Applicable |

| | Securities registered pursuant to Section 12(g) of the Act: | |

| | Common Stock (Title of class) | |

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes |X| No |_|

Indicate by check mark whether the registrant has submitted electronically and posted on its corporate Web site, if any, every Interactive Data file required to be submitted and posted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit and post such files).

Yes |X| No |_|

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer” and “smaller reporting company” in Rule 12b-2 of the Exchange Act. (Check One).

| Large accelerated filer | [___] | | Accelerated filer | [___] |

Non-accelerated filer (Do not check if a smaller reporting company) | [___] | | Smaller reporting company | [ X ] |

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act).

Yes |_| No |X|

As of November 5, 2012 there were 24,124,682 shares outstanding of the registrant's Common Stock.

| | | Page |

| Item 1 | Financial Statements (Unaudited) | |

| | Condensed Consolidated Balance Sheets September 30, 2012 and December 31, 2011 | 1 |

| | | 2 |

| | | 3 |

| | | 4 |

| Item 2 | | 26 |

| Item 3 | | 32 |

| Item 4 | | 32 |

| |

| Item 1 | Legal Proceedings | 33 |

| Item 2 | Unregistered Sales of Equity Securities and Use of Proceeds | 33 |

| Item 3 | Defaults Upon Senior Securities – Not Applicable | |

| Item 4 | Mine Safety Disclosures – Not Applicable | |

| Item 5 | Other Information – Not Applicable | |

| Item 6 | | 34 |

| | | 35 |

TWO RIVERS WATER COMPANY AND SUBSIDIARIES

Condensed Consolidated Balance Sheets (In Thousands)

| | | | | | December 31, 2011 | |

| | | Sept 30, 2012 | | | Restated | |

| | | (Unaudited) | | | (Derived from Audit) | |

| ASSETS: | | | | | | |

| Current Assets: | | | | | | |

| Cash and cash equivalents | | $ | 228 | | | $ | 777 | |

| Marketable securities, available for sale | | | - | | | | 137 | |

| Advances and accounts receivable | | | 352 | | | | 87 | |

| Farm product | | | 464 | | | | 43 | |

| Deposits and other current assets | | | 111 | | | | 20 | |

| Total Current Assets | | | 1,155 | | | | 1,064 | |

| Property, equipment and software, net | | | 2,633 | | | | 1,129 | |

| Other Assets | | | | | | | | |

| Debt issuance costs, net | | | 460 | | | | 663 | |

| Land | | | 3,664 | | | | 2,968 | |

| Water rights and infrastructure | | | 29,738 | | | | 28,786 | |

| Dam and water infrastructure construction in progress | | | 53 | | | | 848 | |

| Total Other Assets | | | 33,915 | | | | 33,265 | |

| TOTAL ASSETS | | $ | 37,703 | | | $ | 35,458 | |

| | | | | | | | | |

| LIABILITIES & STOCKHOLDERS' EQUITY: | | | | | | | | |

| Current Liabilities: | | | | | | | | |

| Accounts payable | | $ | 411 | | | $ | 631 | |

| Current portion of notes payable | | | 10,681 | | | | 32 | |

| Accrued liabilities | | | 1,137 | | | | 495 | |

| Total Current Liabilities | | | 12,229 | | | | 1,158 | |

| Notes Payable - Long Term | | | 8,083 | | | | 12,104 | |

| Total Liabilities | | | 20,312 | | | | 13,262 | |

| Commitments & Contingencies (Notes 2, 3, 5, 6) | | | | | | | | |

| Stockholders' Equity: | | | | | | | | |

| Common stock, $0.001 par value, 100,000,000 shares authorized, 23,934,682 and 23,258,494 shares issued and outstanding at September 30, 2012 and December 31, 2011, respectively | | | 24 | | | | 23 | |

| Additional paid-in capital | | | 44,681 | | | | 39,847 | |

| Accumulated Comprehensive (Loss) | | | - | | | | (51 | ) |

| Accumulated (deficit) | | | (29,472 | ) | | | (19,785 | ) |

| Total Two Rivers Water Company Shareholders' Equity | | | 15,233 | | | | 20,034 | |

| Noncontrolling interest in subsidiary | | | 2,158 | | | | 2,162 | |

| Total Stockholders' Equity | | | 17,391 | | | | 22,196 | |

| TOTAL LIABILITIES & STOCKHOLDERS' EQUITY | | $ | 37,703 | | | $ | 35,458 | |

The accompanying notes to condensed consolidated financial statements are an integral part of these statements.

Two Rivers Water Company -- September 30, 2012 -- 10Q

TWO RIVERS WATER COMANY AND SUBSIDIARIES

| | | Three Months Ended Sept 30, | | | Nine Months Ended Sept 30, | |

| | | 2012 | | | 2011 | | | 2012 | | | 2011 | |

| Revenue | | | | | | | | | | | | |

| Member assessments | | $ | - | | | $ | 25 | | | $ | 36 | | | $ | 73 | |

| Water | | | 34 | | | | - | | | | 34 | | | | - | |

| Farm | | | 381 | | | | - | | | | 381 | | | | - | |

| Other | | | (6 | ) | | | - | | | | 5 | | | | - | |

| Revenue - Net | | | 409 | | | | 25 | | | | 456 | | | | 73 | |

| Direct cost of revenue | | | 280 | | | | - | | | | 280 | | | | - | |

| Gross Margin | | | 129 | | | | 25 | | | | 176 | | | | 73 | |

| Operating Expenses: | | | | | | | | | | | | | | | | |

General and administrative | | | 2,018 | | | | 1,932 | | | | 6,649 | | | | 4,769 | |

| Depreciation and amortization | | | 107 | | | | 24 | | | | 235 | | | | 73 | |

| Total operating expenses | | | 2,125 | | | | 1,956 | | | | 6,884 | | | | 4,842 | |

| (Loss) from operations | | | (1,996 | ) | | | (1,931 | ) | | | (6,708 | ) | | | (4,769 | ) |

| Other income (expense) | | | | | | | | | | | | | | | | |

| Interest expense, net | | | (1,028 | ) | | | (251 | ) | | | (2,589 | ) | | | (634 | ) |

| Gain (Loss) from previous non-controlling interest | | | - | | | | - | | | | - | | | | - | |

| Warrant Expense | | | (18 | ) | | | - | | | | (315 | ) | | | - | |

| Gain (Loss) on extinguishment of notes payable | | | - | | | | 384 | | | | - | | | | 196 | |

| Other income (expense) | | | (45 | ) | | | (18 | ) | | | (81 | ) | | | (10 | ) |

| Total other income (expense) | | | (1,091 | ) | | | 115 | | | | (2,985 | ) | | | (448 | ) |

| Net (Loss) from continuing operations before taxes | | | (3,087 | ) | | | (1,816 | ) | | | (9,693 | ) | | | (5,217 | ) |

| Income tax (provision) benefit | | | - | | | | - | | | | - | | | | - | |

| Net (Loss) from continuing operations | | | (3,087 | ) | | | (1,816 | ) | | | (9,693 | ) | | | (5,217 | ) |

| Discontinued Operations (Note 1) | | | | | | | | | | | | | | | | |

| Loss from operations of discontinued real estate and mortgage business | | | - | | | | (100 | ) | | | - | | | | (131 | ) |

| Income tax (provision) benefit from discontinued operations | | | - | | | | - | | | | - | | | | - | |

| (Loss) on discontinued operations | | | - | | | | (100 | ) | | | - | | | | (131 | ) |

| Net (Loss) | | | (3,087 | ) | | | (1,916 | ) | | | (9,693 | ) | | | (5,348 | ) |

| Net loss (income) attributable to the noncontrolling interest (Note 2) | | | 8 | | | | 7 | | | | 4 | | | | (18 | ) |

| Net (Loss) attributable to Two Rivers Water Company | | $ | (3,079 | ) | | $ | (1,909 | ) | | $ | (9,689 | ) | | $ | (5,366 | ) |

| (Loss) Per Share - Basic and Dilutive: | | | | | | | | | | | | | | | | |

| (Loss) from continuing operations | | $ | (0.13 | ) | | $ | (0.08 | ) | | $ | (0.41 | ) | | $ | (0.24 | ) |

| (Loss) from discontinued operations | | | - | | | | - | | | | - | | | | - | |

| Total | | $ | (0.13 | ) | | $ | (0.08 | ) | | $ | (0.41 | ) | | $ | (0.24 | ) |

| Weighted Average Shares Outstanding: | | | | | | | | | | | | | | | | |

| Basic and Dilutive | | | 23,910 | | | | 22,054 | | | | 23,564 | | | | 21,832 | |

The accompanying notes to condensed consolidated financial statements are an integral part of these statements.

Two Rivers Water Company -- September 30, 2012 -- 10Q

TWO RIVERS WATER COMPANY AND SUBSIDIARIES

| | | For the nine months ended Sept 30, | |

| | | 2012 | | | 2011 | |

| Cash Flows from Operating Activities: | | | | | | |

| Net (Loss) | | $ | (9,689 | ) | | $ | (5,348 | ) |

| Adjustments to reconcile net income or (loss) to net cash (used in) operating activities: | | | | | |

| Depreciation (including discontinued operations) | | | 235 | | | | 73 | |

| Amortization of debt issuance costs and pre-paids | | | 1,402 | | | | 55 | |

| (Gain) Loss on extinguishment of notes payables | | | - | | | | (196 | ) |

| (Gain) Loss on sale of investments and assets held | | | - | | | | 131 | |

| Stock based compensation and warrant expense | | | 3,051 | | | | 2,103 | |

| Stock for services | | | 742 | | | | 559 | |

| Net change in operating assets and liabilities: | | | | | | | | |

| Decrease (increase) in advances & accounts receivable | | | (265 | ) | | | (31 | ) |

| (Increase) in farm product | | | (421 | ) | | | (26 | ) |

| (Increase) decrease in deposits, prepaid expenses and other assets | | | (83 | ) | | | (28 | ) |

| Investments | | | (8 | ) | | | - | |

| Decrease in long term mortgage | | | - | | | | 128 | |

| (Decrease) Increase in accounts payable | | | (220 | ) | | | (38 | ) |

| Increase (decrease) in accrued liabilities and interest | | | 1,081 | | | | 198 | |

| Net Cash (Used in) Operating Activities | | | (4,175 | ) | | | (2,420 | ) |

| Cash Flows from Investing Activities: | | | | | | | | |

| Purchase of property, equipment and software | | | (722 | ) | | | (978 | ) |

| Purchase of land, water shares, infrastructure | | | (748 | ) | | | (1,032 | ) |

| (Purchase) Sale of securities available for resale | | | 68 | | | | (149 | ) |

| Construction in Progress | | | - | | | | (20 | ) |

| Net Cash (Used in) Investing Activities | | | (1,402 | ) | | | (2,179 | ) |

| Cash Flows from Financing Activities: | | | | | | | | |

| Proceeds from issuance of convertible notes | | | - | | | | 7,332 | |

| Proceeds from issuance of bridge loans | | | 3,994 | | | | - | |

| Payment of offering costs | | | (45 | ) | | | (653 | ) |

| Payment on notes payable | | | (38 | ) | | | (1,292 | ) |

| Payment for settlement of note payable | | | - | | | | (105 | ) |

| Proceeds from long-term debt | | | 1,117 | | | | - | |

| Options and warrants exercised | | | - | | | | 613 | |

| Net Cash Provided by Financing Activities | | | 5,028 | | | | 5,895 | |

| Net (Decrease) Increase in Cash & Cash Equivalents | | | (549 | ) | | | 1,296 | |

| Beginning Cash & Cash Equivalents | | | 777 | | | | 645 | |

| Ending Cash & Cash Equivalents | | $ | 228 | | | $ | 1,941 | |

| | | | | | | | | |

| Supplemental Disclosure of Cash Flow Information | | | | | | | | |

| Cash paid for interest | | $ | 689 | | | $ | 353 | |

| Common stock issued in conjunction with extinguishment of notes payable | | $ | - | | | $ | 3,056 | |

| Acquisition of Orlando Reservoir for Seller financed note payable | | $ | - | | | $ | 187 | |

| Stock & warrants for debt issuance costs | | $ | 315 | | | $ | 3,406 | |

| Equipment purchases financed | | $ | 97 | | | $ | 146 | |

The accompanying notes to condensed consolidated financial statements are an integral part of these statements Two Rivers Water Company -- September 30, 2012 -- 10Q

TWO RIVERS WATER COMPANY AND SUBSIDIARIES

For the Nine Months Ended September 30, 2012 and September 30, 2011

(Unaudited)

NOTE 1 – ORGANIZATION AND BUSINESS

GENERAL

The following is a summary of some of the information contained in this document. Unless the context requires otherwise, references in this document to “Two Rivers Water Company,” “Two Rivers,” or the “Company” is to Two Rivers Water Company and its subsidiaries.

Two Rivers Water Company acquires and develops high yield irrigated farmland and the associated water rights in the Arkansas River watershed, particularly along the Huerfano and Cucharas Rivers and the Bessemer Ditch, in Southeastern Colorado.

The Company has acquired 4,915 acres of farmland and associated water rights in the watershed of the Huerfano and Cucharas Rivers. In order to develop and maximize the value of the farmland and the water rights, the Company also acquires reservoirs and interests in mutual irrigation companies. The Company owns a 91% interest in the Huerfano Cucharas Irrigation Company, a mutual irrigation company. The Company also purchased the Orlando Reservoir and Butte Valley water rights on the Huerfano River in February 2011. In June 2012, the Company purchased certain assets, including crops in the ground, farmland and water rights from Dionisio Farms, an operating farm enterprise irrigated by the Bessemer Ditch from the main stem of the Arkansas River. The Company has also agreed to purchase facilities, equipment and the produce business which is integrated with Dionisio Farms.

Two Rivers Water Company plans to operate two core businesses: (i) conventional crop production from high yield irrigated farmland and (ii) water supply to municipal markets in Huerfano County and the Front Range of Colorado. The Company’s current crop production consists of high-value, human-consumption vegetable crops, exchange-trade grains (feed corn) and silage.

The Company currently has the right and the physical capability to store 15,000 acre-feet (“AF”) of water1 within the Huerfano and Cucharas Rivers watershed.

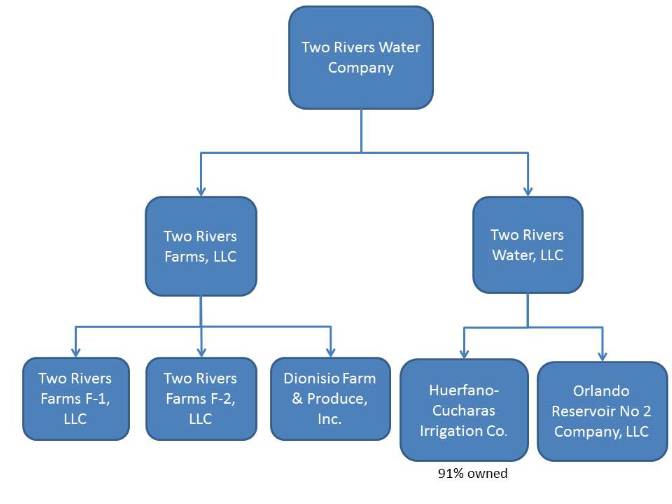

Two Rivers Water Company Corporate Organization

The Company’s organizational structure is illustrated in the chart below. Two Rivers Water Company is the parent company and owns 100% of Two Rivers Farms, LLC and Two Rivers Water, LLC. Two Rivers Farms owns 100% of Two Rivers Farms F-1, LLC, Two Rivers Farms F-2, LLC and Dionisio Farms & Produce, Inc. Two Rivers Farms also owns unencumbered farmland that will eventually be redeveloped and brought into production. Two Rivers Water, LLC owns 91% of the Huerfano-Cucharas Irrigation Company (sometimes referred to elsewhere in this quarterly report as the “HCIC”) and 100% of the Orlando Reservoir No. 2 Company LLC (the “Orlando”).

Two Rivers Water Company -- September 30, 2012 -- 10Q

Two Rivers Farms, LLC (“Farms”) – Our Farming Business

In order to put its water rights and facilities to productive use, the Company formed Farms to manage farms in proximity to our water distribution facilities and has undertaken a program of redeveloping the land, introducing modern agricultural and water management practices including deep plowing, laser leveling and installing efficient irrigation facilities.

The Company acquires farmland and associated, established and strategic water rights. Acquisitions include currently operating and producing farms as well as farmland that has not been cultivated for many years. For the non-operating land, Two Rivers will make capital improvements to rehabilitate the farm and maximize the beneficial use of the associated water rights.

During the 2010 growing season, approximately 440 acres of the Company’s land were farmed, primarily for wheat and feed corn, to determine the fertility of the soil and the most efficient and cost effective means of irrigation.

1 An acre-foot of water is the amount of water required to cover one acre to a depth of one foot. An acre-foot of water contains 325,851 gallons, generally considered enough water to supply two average households for a year.

Two Rivers Water Company -- September 30, 2012 -- 10Q

During 2011, the Company increased the farmable acreage to 713 acres. However, because of the extensive drought in the area and because redevelopment of the Orlando and Phase I reconstruction of the Cucharas Reservoirs had not been completed; Farms made the decision to not produce crops on this acreage.

During the current growing season, the Company is growing, harvesting and selling a variety of crops from 405 acres irrigated from the Bessemer Ditch and is also growing roughly 130 acres of sorghum irrigated from the water rights acquired with the Orlando.

Two Rivers Farms F-1, LLC (“F-1”) and Two Rivers Farms F-2, LLC (“F-2”)

On January 21, 2011 the Company formed F-1 to hold certain farming assets and as an entity to raise convertible debt financing for the Company’s expansion of our farming business. In February 2011, F-1 sold $2,000,000 in 5% per annum, 3-year convertible promissory notes that also participates in 1/3 of the crop profit from the related land. Proceeds from these notes were used to improve irrigation systems, pay for the farmland and retire a portion of the seller carry-back debt from the purchase of the HCIC. This allowed water available through the HCIC to be used to irrigate the F-1 farms without other encumbrances.

On April 5, 2011 the Company formed F-2 to hold certain farming and water assets and as an entity to raise additional convertible debt for the Company’s expansion of our farming business. Proceeds from the notes that were sold in summer 2011, were used to acquire the Orlando and additional farmland and to install irrigation systems.

Both F-1 and F-2 lease their farmland and farming assets to Farms as the operator of the Company’s farming business. The farms are managed by our employees who are supported, as necessary, by contract seasonal farm workers.

Butte Valley Farms

Through multiple transactions, the Company has acquired irrigable farmland and water rights in the Butte Valley. This farmland is, and will continue to be, served by irrigation through the Orlando.

Approximately 1,500 acres of irrigable farmland in the Butte Valley acquired by the Company in connection with the Orlando purchase (the “Lascar-Butte Acres”) is subject to a conditional right to a repurchase by the sellers. The repurchase option is for $1.00 but is only effective on or after September 7, 2021 and only if the sellers have previously offered to purchase from the Company at least 2,500 SFE (single family equivalent) Taps, and tendered payment of a $6,500 Water Resource Fee per SFE Tap pursuant to an agreement. Also, the sellers of Orlando have the right after twenty years to repurchase Lascar-Butte Acres for $2,000 per acre.

In 2011 and 2012, the Company made substantial improvements to the Lascar-Butte Acres to restore the farmable land and enhance the associated water rights. These improvements include but are not limited to installing an irrigation system, rebuilding the outlet works and diversion structure at the Orlando Reservoir, rebuilding the Orlando Ditch, laser leveling the farm land, purchasing nearby land, making filings with the water courts to enhance the water rights, and planting sorghum for harvest. These improvements allowed the Company to commence farming on the Lascar-Butte Acres in 2012 with a crop of sorghum. As of September 30, 2012, the Company expended $2,357,000 in rebuilding and preparing the Lascar-Butte Acres for farming and developing the associated water rights. The Company believes these substantial improvements satisfy certain obligations under, and terminate, an additional Seller’s option to re-purchase the Lascar-Butte Acres. The seller had an option to repurchase the Lascar-Butte Acres by September 7, 2013, if the Company did not use its best efforts to complete substantial improvements to the Lascar-Butte Acres, or if the Company did not commence farming on Lascar-Butte Acres.

Two Rivers Water Company -- September 30, 2012 -- 10Q

Dionisio Farms & Produce, Inc. (“DFP”)

On June 15, 2012, the Company acquired certain land and water rights from Dionisio Produce and Farms, LLC (an unrelated party) and affiliated entities (“Dionisio”). The Company purchased 146 acres of high yield irrigable farmland, and the accompanying 146 shares of Bessemer Ditch Company, a senior water right holder on the main stem of the Arkansas River, and two supplemental ground water wells. Further, the Company entered into leases for an additional 279 irrigable acres, of which 83 acres are subject to a 20 year lease. Dionisio has been producing vegetable crops for over 70 years and has well-established commercial relationships for the sale and distribution of its crops. The Company is operating these acquired assets under the Dionisio name and has entered into employment agreements with members of the Dionisio family to maintain the experience and skill in producing and marketing of the vegetable crops.

On August 11, 2012, the Company formed DFP to hold the Dionisio purchase and subsequent purchases.

Two Rivers Water, LLC (“TR Water”) – our Water Business

During 2011, the Company formed TR Water to secure additional water rights, rehabilitate water diversion, conveyance and storage facilities and to develop one or more special water districts.

Colorado adheres to the Prior Appropriation Doctrine, which provides for a seniority-based allocation system for water which is often described as “first in time, first in right.” This system is administered by the Office of the State Engineer within the Colorado Division of Water Resources (“DWR”) based on judicial water decrees that define the type of use, seniority and volumetric limit of a water right. On each tributary, DWR has full-time and seasonal personnel who monitor the flow in the river and allocate the water to individual water rights based on seniority. Daily information about river conditions and the resulting designation of which water rights are “in priority” are posted on the Internet. Our farmers maintain regular contact with the local water commissioner to optimize the use of the Company’s water rights.

Direct flow rights are generally senior to storage rights, because direct diversion generally preceded the development of storage reservoirs. However, direct flow rights typically do not divert early in the spring (before the irrigation season begins), so lower priority storage rights are often exercised to store water early in the season. The Arkansas River basin below Pueblo Reservoir also operates a Winter Storage Program that re-allocates winter direct flow rights to storage in reservoirs from November 15 to March 15 each year. Because the Company completed needed physical renovations to both the Orlando and the Cucharas Reservoirs in early 2012, we expect to be able to participate in the Winter Storage Program and store water in both reservoirs for later irrigation use on our farms beginning this year.

Two Rivers Water Company -- September 30, 2012 -- 10Q

The Company also has the right to divert from the natural flows of the Huerfano and Cucharas rivers, the two rivers, in excess of 50 cubic feet per second which historically yields 15,000 AF of water annually, subject to river conditions and competing uses. The historic average of 15,000 AF of water is derived from a number of sources. That sum represents the middle of a range of annual water yield which are affected by the changes in weather and resulting hydrology. A wet year estimate of the yield from our direct flow water rights is approximately 18,000 AF. A dry year estimate would be closer to 12,000 AF. In estimating water supply yield, the dry-average-wet method offers a reasonable range of expected diversion. An exception is made, however, for conditions of extreme drought, which has characterized several years of the most recent decade. In addition, the current year is likely to be classified as an extremely dry year. The 15,000 AF of long-term average yield from our direct diversion rights is based on a 50+ year period of record and also relies on historic studies of these rights by a variety of engineers at various times. Our expectation is that the future conditions will be similar to the past, with cycles of wet, average and dry conditions. In order to ameliorate the effects of such variations in the yield of our direct flow water rights, the Company has developed and will continue to develop water storage reservoirs and also plans to develop sustainable, supplemental groundwater resources in the Huerfano/Cucharas watershed. The Company believes that a fully integrated system consisting of annually variable precipitation, a portfolio of direct diversion and storage rights, back-up groundwater production capability, and our storage and distribution facilities will create a reliable, sustainable water supply to support our expanding farming business.

The Company is engaged in refurbishing the water management facilities of the HCIC and the Orlando infrastructure. When the Company’s reservoirs are fully restored, they will have the physical capability and the associated rights to store in excess of 70,000 acre-feet of water.

TR Bessemer, LLC (“Bessemer”)

TR Bessemer, LLC ("Bessemer") was formed on June 6, 2012 as a wholly owned subsidiary of TR Water to acquire Bessemer Ditch Company shares associated with productive farmland. Bessemer’s first acquisition (146 shares) occurred on June 15, 2012 with the acquisition of Dionisio, as discussed above. Upon additional funding in DFP, the Bessemer Ditch Company shares and associated farmland is planned to be transferred to DFP. The Company plans to purchase, lease, improve and farm additional acreage under the Bessemer Ditch and Bessemer is intended to be the holder of the associated water rights, wells and contracts.

The Huerfano-Cucharas Irrigation Company (the “HCIC”)

In order to supply its farms with irrigation water, the Company began to acquire shares in the HCIC in order to develop and put to use their historic water rights on the two rivers. At the time the HCIC was formed in 1944, the water in the two rivers was continuously augmented by groundwater pumped from coal mines that operated in the watershed. The augmented and natural flow of the rivers, along with the water rights and facilities of the HCIC were sufficient to provide reliable irrigation water for the HCIC mutual company’s shareholders and their expanding farm enterprises. However, in the years following World War II, the mines began to cease production and, therefore, stopped pumping groundwater out of the mine shafts and into the river channels. As a result of the reduction in downstream flow in the rivers, the extent of farming in the watershed could no longer be reliably irrigated. In some years, crops failed for lack of late summer irrigation water and, over time, once thriving farms withered. Because of such failures and the reduced flow in the rivers, the shareholders of the HCIC were unable or unwilling to adequately maintain the water diversion, conveyance and storage facilities. Therefore, at the time the Company decided to invest in the Huerfano/Cucharas watershed, the shares in HCIC had become less valuable and the residual farming in the area had reverted primarily to pasture and dry grazing.

Beginning in 2009, the Company systematically acquired shares in the HCIC and, as of December 31, 2010, had acquired 91% of the shares, which it continues to own. The shares were acquired from willing sellers in a series of negotiated transactions for cash, seller-financing and the Company’s common shares. As the controlling shareholder, the Company currently operates the HCIC and has undertaken a long-term program to refurbish and restore the water management facilities.

Two Rivers Water Company -- September 30, 2012 -- 10Q

Orlando Reservoir No. 2 Company, LLC (the “Orlando”)

The Orlando is a Colorado limited liability company originally formed to divert water from the Huerfano River for storage in the Orlando Reservoir to be re-timed and used for irrigation of farmland in Huerfano and Pueblo Counties. At the time the Company began investing in the Huerfano/Cucharas watershed, the Orlando owned an historic diversion structure, a conveyance system and a reservoir and also owned a small amount of irrigable farmland. However, the water facilities were in deteriorated condition. Beginning in January, 2011, through a series of transactions, the latest of which closed on September 7, 2011, the Company acquired 100% ownership of the Orlando (through its wholly-owned subsidiary, TR Water) for a combination of cash, stock and seller-financing. Promptly following the acquisition, the Company began the program for refurbishing the facilities to restore their operating efficiency. During the quarter ended June 30, 2012, the Company completed projects to refurbish the Orlando irrigation infrastructure; these projects were partially funded through long-term loans to the Company from the Colorado Water Conservation Board.

The Orlando assets include not only the reservoir, but also the most senior direct flow water right on the Huerfano River (the #1 priority), along with the #9 priority and miscellaneous junior water rights. These water rights are now integrated with the Company’s other water rights on the Huerfano and Cucharas River to optimize the natural water supply. In addition, the water storage rights and the physical storage reservoirs are critical to water supply reliability in the watershed, because the storage system allows the natural spring runoff from snowmelt to be captured and re-timed for delivery to irrigate crops throughout the growing season. Coupled with the Company’s distribution facilities and farmland, these water diversion and storage rights are expected to provide consistent supplies to irrigate and grow our crops.

Discontinued Operations

In early 2009, the Company (then named Navidec Financial Services, Inc.) discontinued its short-term real estate lending and development in an effort to reduce its exposure to credit risk. The wind down of discontinued operations was completed by December 31, 2011.

Management plans for funding future operations

During the nine months ended September 30, 2012, the Company placed a $3,994,000 bridge loan (the “Bridge Loan”) with a group of private lenders, including the Company’s CEO who lent $994,000 of the total. The Bridge Loan is unsecured, pays monthly interest at 12% per annum, with $200,000 due October 31, 2012 and the remainder due May 31, 2013. The holders of the Bridge Loan also received one share of the Company’s stock for each $10 of loan principal, and the principal of the Bridge Loan is convertible into the Company’s common stock under certain conditions. The Company anticipates retiring any portion of the Bridge Loan not converted to common stock from the proceeds of a take-out equity financing currently under development.

As of September 30, 2012, the Company had $228,000 in demand deposits. These funds, along with proceeds from crop sales, the anticipated additional debt and equity financing are expected to provide sufficient capital to implement the Company’s business plans through 2013.

Two Rivers Water Company -- September 30, 2012 -- 10Q

NOTE 2 – RESTATEMENT AND SUMMARY OF SIGNIFICANT ACCOUNTING POLICIES

Restatement

We have restated the results for the period ended December 31, 2011, which were reported originally in our Form 10-K filed with the United States Securities and Exchange Commission (the “SEC”) on March 8, 2012.

During the recently completed review of the Company’s filing, the SEC recommended enhanced disclosure. Based, in part, on the SEC’s review, the Company has adopted guidance from ASC 470-20 as it relates to its Series B convertible debt. Previously the Company did not account for the beneficial conversion feature of the Series B debt. For the year ended December 31, 2011, the beneficial conversion feature increased the Company’s paid in capital and increased the discount on the Series B note by $1,490,000.

Below is detail on the December 31, 2011 restatement.

Two Rivers Water Company -- September 30, 2012 -- 10Q

| Consolidated Balance Sheet (in thousands) | | December 31, | |

| | | 2011 | | | CHANGE | | | 2011 RESTATED | |

| ASSETS: | | | | | | | | | |

| Current Assets: | | | | | | | | | |

| Cash and cash equivalents | | $ | 777 | | | | | | $ | 777 | |

| Marketable securities, available for sale | | | 137 | | | | | | | 137 | |

| Advances and accounts receivable | | | 87 | | | | | | | 87 | |

| Farm product | | | 43 | | | | | | | 43 | |

| Deposits and other current assets | | | 20 | | | | | | | 20 | |

| Total Current Assets | | | 1,064 | | | | | | | 1,064 | |

| | | | | | | | | | | | |

| Property, equipment and software, net | | | 1,129 | | | | | | | 1,129 | |

| | | | | | | | | | | | |

| Other Assets | | | | | | | | | | | |

| Debt issuance costs | | | 663 | | | | | | | 663 | |

| Land (Note 2) | | | 2,968 | | | | | | | 2,968 | |

| Water rights and infrastructure | | | 28,786 | | | | | | | 28,786 | |

| Options on real estate and water shares | | | - | | | | | | | - | |

| Dam and water infrastructure construction in progress | | | 848 | | | | | | | 848 | |

| Discontinued operations - assets held for sale | | | - | | | | | | | - | |

| Total Other Assets | | | 33,265 | | | | | | | 33,265 | |

| TOTAL ASSETS | | $ | 35,458 | | | | | | $ | 35,458 | |

| | | | | | | | | | | | |

| LIABILITIES & STOCKHOLDERS' EQUITY: | | | | | | | | | | | |

| Current Liabilities: | | | | | | | | | | | |

| Accounts payable | | $ | 631 | | | | | | $ | 631 | |

| Current portion of notes payable | | | 32 | | | | | | | 32 | |

| Accrued liabilities | | | 495 | | | | | | | 495 | |

| Total Current Liabilities | | | 1,158 | | | | | | | 1,158 | |

| Notes Payable - Long Term | | | 13,508 | | | | (1,404 | ) | | | 12,104 | |

| Total Liabilities | | | 14,666 | | | | (1,404 | ) | | | 13,262 | |

| | | | | | | | | | | | | |

| Stockholders' Equity: | | | | | | | | | | | | |

| Common stock, $0.001 par value, 100,000,000 shares authorized, 23,258,494 and 19,782,916 shares issued and outstanding at December 31, 2011 and 2010, respectively | | | 23 | | | | | | | | 23 | |

| Additional paid-in capital | | | 38,357 | | | | 1,490 | | | | 39,847 | |

| Accumulated Comprehensive (Loss) | | | (51 | ) | | | | | | | (51 | ) |

| Accumulated (deficit) | | | (19,699 | ) | | | (86 | ) | | | (19,785 | ) |

| Total Two Rivers Water Company Shareholders' Equity | | | 18,630 | | | | 1,404 | | | | 20,034 | |

| Noncontrolling interest in subsidiary | | | 2,162 | | | | | | | | 2,162 | |

| Total Stockholders' Equity | | | 20,792 | | | | | | | | 22,196 | |

| TOTAL LIABILITIES & STOCKHOLDERS' EQUITY | | $ | 35,458 | | | | | | | $ | 35,458 | |

Two Rivers Water Company -- September 30, 2012 -- 10Q

Principles of Consolidation

The accompanying consolidated financial statements include the accounts of Two Rivers Water Company and its subsidiaries, Farms, F-1, F-2, DFP, TR Water, the HCIC, the Orlando, Bessemer and discontinued operations. All significant inter-company balances and transactions have been eliminated in consolidation. The Company has completed the termination of the discontinued operations.

Non-controlling Interest

The Company owns 91% of the HCIC, so the results for the HCIC are consolidated in the Company’s financial statements. As of September 30, 2012, the non-controlling members’ equity in the HCIC (the remaining 9% ownership interests) was $2,158,000.

Below is the breakdown of the non-controlling interests’ share of gains (losses).

| | | For the three months ended, | | | For the nine months ended, | |

| | | Sept 30, 2012 | | | Sept 30, 2011 | | | Sept 30, 2012 | | | Sept 30, 2011 | |

| HCIC | | $ | (8,000 | ) | | $ | (7,000 | ) | | $ | (4,000 | ) | | $ | 18,000 | |

The non-controlling interests’ shares are assessed their pro-rata share of expected expenses to operate the HCIC.

Reclassification

Certain amounts previously reported have been reclassified to conform to the current presentation.

Use of Estimates

The preparation of financial statements in conformity with generally accepted accounting principles in the United States requires management to make estimates and assumptions. These estimates and assumptions affect the reported amounts of assets and liabilities, disclosure of contingent assets and liabilities at the date of the financial statements and the reported amounts of revenues and expenses during the reported period. Actual results could differ materially from those estimates.

Fair Value of Measurements and Disclosures

Fair Value of Assets and Liabilities Acquired

Fair value is the price that would be received from the sale of an asset or paid to transfer a liability (i.e., an exit price) in the principal or most advantageous market in an orderly transaction between market participants. In determining fair value, the accounting standards establish a three-level hierarchy that distinguishes between (i) market data obtained or developed from independent sources (i.e., observable data inputs) and (ii) a reporting entity’s own data and assumptions that market participants would use in pricing an asset or liability (i.e., unobservable data inputs). Financial assets and financial liabilities measured and reported at fair value are classified in one of the following categories, in order of priority of observability and objectivity of pricing inputs:

| | • Level 1 – Fair value based on quoted prices in active markets for identical assets or liabilities. |

Two Rivers Water Company -- September 30, 2012 -- 10Q

| | • Level 2 – Fair value based on significant directly observable data (other than Level 1 quoted prices) or significant indirectly observable data through corroboration with observable market data. Inputs would normally be (i) quoted prices in active markets for similar assets or liabilities, (ii) quoted prices in inactive markets for identical or similar assets or liabilities or (iii) information derived from or corroborated by observable market data. |

| | • Level 3 – Fair value based on prices or valuation techniques that require significant unobservable data inputs. Inputs would normally be a reporting entity’s own data and judgments about assumptions that market participants would use in pricing the asset or liability. |

The fair value measurement level for an asset or liability is based on the lowest level of any input that is significant to the fair value measurement. Valuation techniques should maximize the use of observable inputs and minimize the use of unobservable inputs to the extent possible.

Recurring Fair Value Measurements:

The carrying value of the Company’s financial assets and financial liabilities is their cost, which may differ from fair value. The carrying value of cash held as demand deposits, money market and certificates of deposit, accounts receivable, short-term borrowings, accounts payable and accrued liabilities approximated their fair value. Marketable securities are valued at Level 1 due to readily available market quotes. The fair value of the Company’s long-term debt, including the current portion, approximate its carrying value.

Revenue Recognition

Farm Revenues

Revenues from farming operations are recognized when resulting crops are sold into the market. All direct expenses related to farming operations are capitalized as farm product and recognized as a direct cost of sale upon the sale of the crops.

Water Revenues

Current water revenues are from the sale of water arising under water rights owned by the HCIC to farmers in the HCIC service area who are not affiliated with the Company. Water revenues are recognized when the water is invoiced at the established rate per acre foot of water consumed.

Member Assessments

Once per year the HCIC board estimates that company’s expenses, less anticipated water revenues, and establishes an annual assessment per ownership share. One-half of the member assessment is recorded in the second quarter of the calendar year and the other one-half of the member assessment is recorded in the fourth quarter of the calendar year. Assessments paid by Two Rivers Water Company to the HCIC are eliminated in consolidation of our financial statements.

The HCIC does not reserve against any unpaid assessments. Assessments due, but unpaid, are secured by the member’s shares of the HCIC. The value of this ownership is significantly greater than the annual assessments. If assessments are not paid, after proper notifications to the delinquent party and a set time, the shares are offered at the amount of assessments due including interest and fees.

Two Rivers Water Company -- September 30, 2012 -- 10Q

Farm Product – Inventory

Costs directly associated with growing crops are capitalized as farm product and recognized as a direct cost of sale upon the sale of the crops. At the end of each quarter, the Company receives a field report from its farmers to ascertain that the value of the Farm Inputs is not in excess of market value, based on an estimate of costs incurred to date and costs needed to complete the crop and recognize the review. Market value is determined by estimating expected yield times the current market price of the crop.

Seasonality

Our main source of revenue is from the sale of produce, grains and animal grain feed. There might be some revenue recognized in the first and second calendar quarter from winter harvest, for example parsnips. However, the majority of our revenue occurs in the third and fourth calendar quarter.

Net Income (Loss) per Share

Basic net income per share is computed by dividing net income (loss) attributed to the Company available to common shareholders for the period by the weighted average number of common shares outstanding for the period. Diluted net income (loss) per share is computed by dividing the net income for the period by the weighted average number of common and potential common shares outstanding during the period.

The dilutive effect of 4,115,474 restricted stock units (“RSUs”), 1,727,562 options and 2,653,424 warrants at December 31, 2011, and the dilutive effect of 7,844,282 RSUs, 1,749,532 options, 3,053,424 warrants and 9,263,531 conversion rights at September 30, 2012 has not been included in the determination of diluted earnings per share because, under ASC 260 their exercise would be anti-dilutive.

Comprehensive Income (Loss)

Comprehensive income (loss) excludes net income or loss and changes in equity from the market price variations in securities held by the Company. Since these securities are classified as “available for sale” any unrecognized gain or loss is shown in Other Comprehensive Income (Loss) section in the Statement of Changes in Stockholders’ Equity. At December 31, 2011 and September 30, 2012 the Company had $51,000 and $-0-, respectively, in unrecognized loss.

At December 31, 2011 and September 30, 2012, the Company held $137,000 and $-0-, respectively, in highly liquid gold-based ETFs. For financial statement presentation, this amount is included in marketable securities available for sale.

Recently issued Accounting Pronouncements

Goodwill Impairment Testing

In September 2011, the FASB issued guidance to amend and simplify the rules related to testing goodwill for impairment. The revised guidance allows an entity to make an initial qualitative evaluation, based on the entity’s events and circumstances, to determine whether it is more likely than not that the fair value of a reporting unit is less than its carrying amount. The results of this qualitative assessment determine whether it is necessary to perform the currently required two-step impairment test. The new guidance is effective now and has been adopted by the Company. The adoption of this guidance is not expected to have a material impact on the Company’s consolidated financial statements.

Two Rivers Water Company -- September 30, 2012 -- 10Q

Presentation of Comprehensive Income

In June 2011, the FASB issued ASU No. 2011-05, Presentation of Comprehensive Income. The issuance of ASU 2011-5 was intended to improve the comparability, consistency and transparency of financial reporting and to increase the prominence of items reported in other comprehensive income. This guidance is effective now. The Company’s adoption of this guidance is not expected to have a material impact on the Company’s consolidated financial statements.

Disclosures about Offsetting Assets and Liabilities

In December 2011, FASB issued ASU No. 2011-11, Disclosures about Offsetting Assets and Liabilities which requires an entity to disclose information about offsetting and related arrangements to enable financial statement user to understand the effect of those arrangements on its financial position. This ASU is effective for periods beginning on or after January 1, 2013. At the present, the adoption of this guidance is not expected to have a material impact on the Company’s consolidated financial statements.

There were various other accounting standards and interpretations issued in 2012 and 2011, none of which is expected to have a material impact on the Company’s financial position, operations or cash flows.

NOTE 3 – NOTES PAYABLE

HCIC Seller Carryback Notes

Beginning on September 17, 2009, the Company began acquiring shares in the HCIC and related land from HCIC shareholders. As part of these transactions, many of the sellers financed the acquisitions by accepting notes payable from the Company and HCIC. As of December 31, 2011 and September 30, 2012, these loans totaled $7,362,000. The notes carry interest at 6% per annum, interest payable monthly, the principal amounts due at various dates from February 1, 2013 through September 30, 2015, and are collateralized by the HCIC shares and land. As of September 30, 2012, due to a maturity on the seller financed notes being within 12 months, $6,587,000 of the $7,364,000 is classified as a current portion of long-term debt.

As of September 30, 2012, of the $7,364,000 in seller carry back notes, $2,114,000 provides the holders the right to convert some or all of debt into the Company’s common stock at $1/share to $1.25/share. Each of the holders of such conversion rights can convert anytime until the related note is paid.

During the year ended December 31, 2011, the Company exchanged $1,575,000 in HCIC debt into 722,222 shares of the Company’s common stock, a cash payment of $37,500, and $37,500 in an unsecured note, which note was paid in 2012. The fair market value of the consideration paid by the Company to induce the exchange exceeded the face amount of the debt by $272,000. An expense due to loss on extinguishment of note payable of $272,000 was recognized due to the difference between the stock price conversion and the fair market value of the Company’s common stock.

Two Rivers Water Company -- September 30, 2012 -- 10Q

During the year ended December 31, 2011, the Company offered holders of HCIC notes the option of an early payoff in exchange for a discount on the face amount of the note. A total of $189,000 of notes was retired early and a gain on forgiveness of the HCIC notes of $84,000 was recognized and is netted against the loss on extinguishment of note payables mentioned above in the statement of operations.

Orlando Note

On January 28, 2011, the Company purchased water storage rights and direct flow water diversion rights from the Orlando Reservoir No. 2 Company, LLC (the “Orlando”) for $3,100,000, which consisted of a cash payment of $100,000 and a Company note payable to the seller in the amount of $3,000,000.

However, in July 2011, the Company substantially restructured the transaction resulting in the Company acquiring the Orlando for (i) 650,000 shares of the Company’s common stock, (ii) a $1,412,500 cash payment, and (iii) a seller carryback note of $187,500 at 7% per annum with principal and interest due on January 28, 2014. For purposes of the transaction, the Company shares were valued at $1,557,000. Upon the completion of the Orlando purchase, the Company engaged a water research firm to perform a valuation of the Orlando. The valuation report (which took into account the rehabilitation project then nearing completion) was issued on January 16, 2012 with an approximate value of $5,195,000.

Series A & B Notes

In February 2011 the Company closed a $2,000,000 Series A convertible debt offering to finance the land, water rights, improvements, and farm equipment for F-1. The debt pays interest at 6% per annum to maturity on March 31, 2014 plus one-third of the F-1 crop profit. The crop profit participation will be recognized as an interest expense upon the sale of the F-1 crop. Holders of the debt have the right to convert its principal into Company common stock at $2.50/share. Because conversion at $2.50/share would be accretive to the Company, no additional beneficial interest has been recorded in favor of the debt.

As noted above, one-third of crop profit will be recognized as an interest expense upon the sale of the crop. The crop profit is defined as crop revenue less the direct cost of growing and cultivating the crop. Direct costs includes all cost to prepare for planting, planting, caring for the crops planted, harvesting and delivering the crop to market. Further, the crop profit is only from the 500 acres of farmland that secures the Series A debt.

In August 2011, the Company closed a $5,332,000 Series B convertible debt offering to finance the land, water rights, and improvements for F-2. The debt pays interest at 6% per annum to maturity on June 30, 2014 plus 10% of the net crop revenue from land owned by F-2. The crop profit participation will be recognized as an interest expense upon the sale of the F-2 crop. Net-crop revenue is defined as the gross selling price of the crops less basis. Basis is the difference between the futures price for a commodity and the local cash price offered by grain buyers. It reflects the cost of marketing grain from one point of sale to another point of sale. The net-crop revenue is paid on crops that are produced on the farmland that secures the Series B debt, approximately 1,200 acres.

Holders of the Series B debt also have the right to convert its principal into Company common stock at $2.50/share.

The conversion option on the Series A and Series B Notes cannot be separated from their respective notes. However, in conjunction with the Series B Notes, the Company issued 2,132,800 warrants to purchase the Company common stock at $2.50/share through December 31, 2012. Further, in connection with the placement of the Series A and Series B Notes, the Company also issued 171,000 warrants to purchase the Company’s common stock at $2.50/share to three broker-dealers; those warrants have an expiration of September 30, 2014. The fair value of the warrants issued was computed at $1,675,000 for the debt holder warrants. This amount was recorded as a discount on the note and is accreted over the life of the note to interest expense utilizing the effective-interest method. There is an additional $149,000 for the broker dealer warrants, which warrants were issued as partial compensation for the successful completion of the Series B placement. These warrants are amortized over the life of the warrants and recognized as interest expense.

Two Rivers Water Company -- September 30, 2012 -- 10Q

For the year ended December 31, 2011, the Company also recorded a beneficial conversion amount with Series B. After accounting for the fair value of the warrants at $0.7854/share, the adjusted and effective Series B conversion rate is $1.7146/share. Taking into account the various closing dates of the Series B and the respective stock price of our common stock at each closing, the value of the beneficial conversion feature is $1,490,000. This amount was recorded as a discount on the note and is accreted over the life of the note to interest expense utilizing the effective-interest method. The Company estimated the effective interest rate to be 46% per annum.

Below is a summary of Series B discount and accretion:

| | | Beginning balance | | | 2011 discount accretion | | | 9 months 2012 accretion | | | Net | |

| Face | | $ | 5,332,000 | | | | | | | | | $ | 5,332,000 | |

| Warrant fair value | | | (1,675,000 | ) | | | 245,000 | | | | 673,000 | | | | (2,247,000 | ) |

| Beneficial conversion | | | (1,490,000 | ) |

| Net | | $ | 2,167,000 | | | | 245,000 | | | | 673,000 | | | $ | 3,085,000 | |

Bridge Loan

During the quarter ended March 31, 2012, the Company closed a short-term bridge financing (the “Bridge Loan”) in the total amount of $3,994,000. The Company’s CEO participated as a lender in the Bridge Loan in the amount of $994,000. The Bridge Loan pays monthly interest at 12% per annum with $200,000 due on October 31, 2012 and the remainder due on May 31, 2013. The Bridge Loan holders also received one share of the Company’s stock for each $10 of Bridge Loan participation. Participants in the Bridge Loan have the option of converting the principal into the Company’s common stock at the price offered in a take-out equity financing which the Company plans to complete. In conjunction with the closing of the Bridge Loan, the Company issued 400,000 shares of its common stock to the Bridge Loan holders. The fair value of the shares issued was determined to be $655,000, which is recorded as a debt discount being amortized on a straight-line basis over the term of the related Bridge Loan.

In October 2012, the Company obtained extensions to May 31, 2013 on $3,794,000 of the principal. In exchange for these extensions, the terms remain the same and the Company will issue the note holders restricted stock of the Company computed by multiplying the face amount of the note by 10% and dividing by $1.75 (per share). These shares will be issued in the quarter ending December 31, 2012 and the cost will be amortized from November 1, 2012 to May 31, 2013 on a straight line basis.

Colorado Water Conservation Loan

On March 5, 2012 the Company closed long-term financing with the Colorado Department of Natural Resources, Colorado Water Conservation Board in the amount of $1,185,000 (the “CWCB Loan”). This loan partially finances the rehabilitation of the Cucharas Reservoir to bring it into safety compliance with the Colorado State Engineers office. Further, the CWCB Loan assisted with the rehabilitation of the Orlando facilities. There was a $12,000 service fee due upon closing. This amount is being amortized over the expected life of the CWCB Loan which is 20 years with interest fixed at 2.5% per annum.

Two Rivers Water Company -- September 30, 2012 -- 10Q

First National Bank of Pueblo (FNB) – Dionisio Purchase

The cost of the Dionisio land/water acquisition was $1,500,000, of which $900,000 was financed by FNB and $600,000 was paid in cash. The purchase price has been allocated to land for $513,000; building for $35,000, and $952,000 to water rights representing the purchase of the Bessemer Ditch Company (“BIDC”) shares. The Company has agreed to purchase facilities, equipment and the produce business which is integrated with Dionisio Farms for an additional $1,500,000.

The terms of the FNB loan is at 1% above the base rate on corporate loans posted by at least 75% of the nation’s 30 largest banks known as the Wall Street Journal Prime Rate (3.25% as of September 30, 2012), subject to a minimum of 6% per annum. The FNB loan is secured by the Dionisio assets which include 146 shares of the BIDC. There are five annual payments of $76,000 due each December 15 commencing December 15, 2012. A balloon payment of all accrued interest and outstanding principal is due June 15, 2017.

Below is a summary of the Company’s debt:

| Note | | Sept 30, 2012 principal balance | | | Sept 30, 2012 accrued interest | | | Interest rate | | Security |

| Mutual Ditch seller carry back | | $ | 7,364,000 | | | $ | - | | | | 6 | % | Shares in the Mutual Ditch Company |

| Orlando purchase | | | 187,000 | | | | 13,800 | | | | 7 | % | 188 acres of land |

| Convertible debt Series A | | | 2,000,000 | | | | 75,000 | | | | 6 | % | F-1 assets |

| Convertible debt Series B | | | 5,332,000 | | | | 159,500 | | | | 6 | % | F-2 assets |

| Bridge Loan | | | 3,994,000 | | | | 150,000 | | | | 12 | % | Unsecured |

| CWCB | | | 1,117,000 | | | | 13,000 | | | | 2.5 | % | Certain Orlando and Farmland assets |

| FNB - Dionisio Farm | | | 900,000 | | | | 2,000 | | | | (1 | ) | Dionisio farmland and 146.4 shares of Bessemer Irrigating Ditch Company Stock, well permits |

| Equipment loans | | | 199,000 | | | | 700 | | | | 5 - 8 | % | Specific equipment |

| Total | | | 21,093,000 | | | $ | 414,000 | | | | | | |

| Less: Current portion | | | (10,681,000 | ) | | | | | | | | | |

| Net long term due before discounts | | | 10,412,000 | | | | | | | | | | |

| Less: Discount on Series B | | | (2,247,000 | ) | | | | | | | | | |

| Less: Discount on Bridge Loan | | | (82,000 | ) | | | | | | | | | |

| Long Term portion | | $ | 8,083,000 | | | | | | | | | | |

Two Rivers Water Company -- September 30, 2012 -- 10Q

NOTE 4 – INFORMATION ON BUSINESS SEGMENTS

We organize our business segments based on the nature of the products and services offered. We focus on the farming business and water business with Two Rivers Water Company as the parent company. Therefore, we report our segments by these lines of businesses: Farms and Water. Farms contain all of our farming business (Farms, F-1, F-2, DFP). Water contains our Water Business (HCIC and Orlando).

In the following tables of financial data, the total of the operating results of these business segments is reconciled, as appropriate, to the corresponding consolidated amount. There are some corporate expenses that were not allocated to the business segments, and these expenses are contained in the “Total Operating Expenses” under Two Rivers Water Company.

While the Parent is not a separable reportable operating segment, there are some corporate expenses that were not allocated to the business segments, and these expenses are contained in the “Total Operating Expenses” under Parent. Further, segment allocations may differ from those on the face of the income statement.

Two Rivers Water Company -- September 30, 2012 -- 10Q

Operating results for each of the segments of the Company are as follows (in thousands):

| | | For the nine months ended Sept 30, 2012 | | | For the nine months ended Sept 30, 2011 | |

| | | Parent | | | Farms | | | Water | | | Discontinued Operations | | | Total | | | Parent | | | Farms | | | Water | | | Discontinued Operations | | | Total | |

| Revenue | | $ | - | | | | 381 | | | | 75 | | | | - | | | | 456 | | | $ | - | | | | 1 | | | | 72 | | | | - | | | | 73 | |

| Less: direct cost of revenue | | | - | | | | 280 | | | | - | | | | - | | | | 280 | | | | - | | | | - | | | | - | | | | - | | | | - | |

| Gross Margin | | | - | | | | 101 | | | | 75 | | | | - | | | | 176 | | | | - | | | | 1 | | | | 72 | | | | - | | | | 73 | |

| Total Operating Expenses | | | 5,494 | | | | 676 | | | | 714 | | | | - | | | | 6,884 | | | | (4,059 | ) | | | (483 | ) | | | (299 | ) | | | - | | | | (4,841 | ) |

| Total Other Income/(Expense) | | | (1,645 | ) | | | (1,009 | ) | | | (331 | ) | | | - | | | | (2,985 | ) | | | 3 | | | | 238 | | | | (689 | ) | | | - | | | | (448 | ) |

| Net (Loss) Income from continuing operations before income taxes | | | (7,139 | ) | | | (1,584 | ) | | | (970 | ) | | | - | | | | (9,693 | ) | | | (4,056 | ) | | | (244 | ) | | | (916 | ) | | | - | | | | (5,216 | ) |

| Income Taxes (Expense)/Credit | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | |

| Net Income (Loss) from continuing operations | | | (7,139 | ) | | | (1,584 | ) | | | (970 | ) | | | - | | | | (9,693 | ) | | | (4,056 | ) | | | (244 | ) | | | (916 | ) | | | - | | | | (5,216 | ) |

| Discontinued operations: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (Loss) from operations of discontinued real estate and mortgage business | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | (131 | ) | | | (131 | ) |

| Income tax benefit | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | |

| Loss on discontinued operations | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | - | | | | (131 | ) | | | (131 | ) |

| Non-controlling interest | | | - | | | | - | | | | 4 | | | | - | | | | 4 | | | | - | | | | - | | | | (17 | ) | | | - | | | | (17 | ) |

| Net (Loss) Income | | $ | (7,139 | ) | | | (1,584 | ) | | | (966 | ) | | | - | | | | (9,689 | ) | | $ | (4,056 | ) | | | (244 | ) | | | (933 | ) | | | (131 | ) | | | (5,364 | ) |

| Segment assets | | $ | 711 | | | | 9,791 | | | | 27,201 | | | | - | | | | 37,703 | | | $ | 2,876 | | | | 5,542 | | | | 26,298 | | | | 6 | | | | 34,722 | |

Two Rivers Water Company -- September 30, 2012 -- 10Q

NOTE 5 – EQUITY TRANSACTIONS

Common Stock

During the nine months ended September 30, 2011 the Company had the following common stock transactions:

| · | During February 70,000 shares of our common stock were issued in exchange for consulting services. |

| · | In March, 2011 a total of 722,000 shares were issued to a creditor of the Company, as payment in full for the debt in the amount of $1,575,000. At the time of the transaction, the fair value of the Company’s common stock exceeded the amount of debt retired, which resulted in a loss from debt retirement of $272,000. |

| · | During April, 2011 we issued 100,000 shares of our common stock in exchange for consulting services. |

During the nine months ended September 30, 2012 the Company had the following common stock transactions:

| · | In January, 2012 the Company issued 50,000 shares of our common stock to the independent members of the Board in exchange for Board of Director services rendered in 2011. |

| · | In January, 2012 the Company issued 125,000 shares to cover 125,000 Restricted Stock Units (“RSUs”) issued to an non-executive employee under the 2011 Plan in exchange for his surrender of 250,000 options (strike price of $2.00/share) under the 2005 Plan. |

| · | In January, 2012 100,000 RSU shares, as part of an overall grant of 700,000 shares, were issued to the Company’s CFO pursuant to the 2011 Plan. |

| · | In January, 2012 200,000 shares, as part of an overall grant of 400,000 shares, were issued to a former member of the Board of Directors. |

| · | In February, 2012 the Company issued 83,330 shares to our investor relations consultants as partial payment for their services. |

| · | In March, 2012 the Company issued 400,000 shares to participating lenders in consideration of the Bridge Loan. |

| · | In April 2012, the Company issued 25,000 RSU shares to the estate of a previous employee under our 2011 Plan. |

| · | In June 2012, the Company issued 166,666 RSU shares of the total grant of 700,000 shares pursuant to the CFO’s employment agreement and to the 2011 Plan. |

| · | In June 2012, the Company issued 200,000 RSU shares to complete a grant of 400,000 shares to a former member of the Board of Directors. |

| · | In June 2012, the Company issued 50,000 shares to a key vendor, as partial payment for services performed. |

| · | In June 2012, the Company issued 166,666 RSU shares to a board member for consulting services performed from April 1, 2012 through June 30, 2012. |

| · | In June 2012, the Company issued 100,000 shares through the exercise of warrants. |

| · | In September 2012, the Company issued 50,000 shares to a key vendor, as partial payment for services performed. |

Two Rivers Water Company -- September 30, 2012 -- 10Q

Stock Incentive Plans

The Company previously had a 2005 Stock Option Plan (“2005 Plan”) that was superseded by the Two Rivers 2011 Long-Term Stock Incentive Plan (“2011 Plan”). Upon the Company’s shareholder adoption of the 2011 Plan, the 2005 Plan stopped issuance of any further grants, except for grants previously committed by agreement.

Under the 2005 Plan, we have the following stock options issued and outstanding:

| Optionee | Company Relationship | | Shares | | | Date of Grant | | | Vesting Date | | | Performance Requirement | | | Expiration Date | | Exercise Price - Exercised toDate | |

| Howard Farkas | Former Director | | | 1,023,200 | | | Jul 2006 | | | Jul 2006 | | | Satisfied | | | Jul 2016 | | $ | 1.25 | | - | |

| Empl-oyees | Employee | | | 40,000 | | | Apr 2011 | | | | (1) | | | | (2) | | | Apr 2021 | | $ | 3.00 | | - | |

| Wallick Associates | Consultant | | | 600,000 | | | | (3) | | | | (3) | | | Satisfied | | | | (3) | | $ | 1.25 | | - | |

| | | | | 1,663,200 | | | | | | | | | | | | | | | | | | | | | | |

| Exercisable September 30, 2012 | | | 1,636,533 | | | | | | | | | | | | | | | | | | | | | | |

| Notes: | | | | | | | | | | | | | | | | | | | | | | | | | | |

| (1) Vests 1/3 at the end of each 12 months from Date of Grant | | | |

| (2) Satisfactory employee performance during vesting period | | | |

| (3) Various grant dates of during 2011 and 2012. When granted, the options immediately vested. Expiration is 5 years from the date of grant. | | | |

If all of the options were exercised, $2,149,000 would be collected by the Company and yield an average share price of $1.29.

During the nine months ended September 30, 2012, the Company issued 204,480 options under the 2005 Plan and pursuant to a prior written agreement with a financial consultant. The options have a strike of $1.25/share. Of the 204,480 options, 83,333 options were issued in conjunction with a successful debt placement; the fair value is being amortized over the three-year life of the associated debt, or $3,000 per quarter which is recognized as interest expense. The remaining 121,147 options issued in 2012 were for current services; therefore the fair value of $44,000 was expensed to consulting expense.

Option Valuation Process

The fair value of each option award is estimated on the date of grant. To calculate the fair value of options, the Company uses the Black-Scholes model employing the following variables:

| Expected stock price volatility | 78% |

| Risk-free interest rate | 2.64% |

| Expected option life (years) | 2.2 to 5.2 |

| Expected annual dividend yield | 0% |

Two Rivers Water Company -- September 30, 2012 -- 10Q

The Company arrived at the foregoing estimate of volatility of the Company’s common stock based on observation of pricing volatility of the publicly-traded stocks of other entities in a similar line of business for a period commensurate with the contractual term of the underlying options and used weekly intervals for price observations. The Company will continue to consider the volatilities of those other stocks unless circumstances change such that the identified entities are no longer similar to the Company or until there is sufficient information available to substitute the Company’s own stock price volatility. The risk-free rate for periods within the expected term of the options is based on the U.S. Treasury yield curve in effect at the time of grant. The Company believes these estimates and assumptions are reasonable. However, these estimates and assumptions may change in the future based on actual experience as well as market conditions.

Under the 2011 Plan, we have issued the following Restricted Stock Units (RSUs):

| Grantee | Company Relationship | RSUs issued | Date of Grant | Vesting Date | Performance Requirement | Exercised to Date |

| John McKowen | Chairman/CEO | 2,480,948 | Oct 2010 | (1) | (2) | - |

| 1,400,000 | Jan 2012 | (1) | (3) | - |

| Gary Barber | President/COO | 1,000,000 | Oct 2010 | (1) | (2) | - |

| 1,400,000 | Jan 2012 | (1) | (3) | - |

| Wayne Harding | CFO | 700,000 | Oct 2010 | (1) | (2) | 366,666 |

| 500,000 | Jan 2012 | (1) | (3) | - |

| John Stroh | Director | 220,236 | Oct 2010 | Jan 2011 | n/a | 220,236 |

| Jolee Henry | Prior Director | 400,000 | Oct 2010 | Jan 2011 | n/a | 400,000 |

| Employees (5) | Past & Present Employees | 558,570 | Various | (1) | (4) | 150,000 |

| | | 8,659,754 | | | | 1,136,902 |

| Notes: |

| Above table does not show those shares that were cancelled or returned. |

| (1) Vests 1/3 at the end of each 12 months from Date of Grant |

| (2) Subject to employer deferral and employment agreement, if applicable |

| (3) Vests 1/3 when the Company's common stock is listed on a National Exchange and attains closing bid of $3 per share, a second 1/3 when the share price attains $6 per share, and the final 1/3 when the share price attains $9 per share, respectively |

| (4) Satisfactory employee performance during vesting period |

| (5) A total of ten current and past employees are in this group |

The 2011 Plan has a total of 10,000,000 shares available for grants. With 9,684,754 RSUs and options granted, and 1,025,000 RSUs cancelled, there is a balance of 1,340,246 shares available for grants under the 2011 Plan.

The Company can issue stock awards and options for nonemployee services. If stock is granted, the Company values the stock using an average of the closing price of the Company’s stock over the period that the service was rendered. If options are granted, the Company uses the Black-Scholes model for determining fair value. The parameters for the Black-Scholes model are detailed later in this Note.

It is estimated that $6,497,000 in stock-based compensation expense will be fully amortized by December 31, 2015.

Two Rivers Water Company -- September 30, 2012 -- 10Q

The stock-based compensation expense was $1,015,000 for the three months ended September 30, 2012 and $3,051,000 for the nine months ended September 30, 2012.

The stock-based compensation expense was $646,000 for the three months ended September 30, 2011 and $2,103,000 for the nine months ended September 30, 2011.

Warrants

On January 27, 2012, our Board of Directors authorized an extension of the expiration date of 100,000 warrants to purchase the Company’s common stock at $1.00/share held by the Elevation Fund. The former expiration date was December 31, 2011, and the expiration date was extended to June 30, 2012. The extension was granted in consideration of the Elevation Fund’s assistance with the Company’s capital financing. Due to the extension of the warrant expiration date, a new fair value calculation was performed using the Black-Scholes method. Based on this calculation, an expense of $55,000 was recognized for the three months ended June 30, 2012. The Elevation Fund’s 100,000 warrants were exercised by June 30, 2012.

As of September 30, 2012, the Company has outstanding the following warrants to purchase common stock:

| Grantee | Company Relationship | | Shares | | Date of Grant | Vesting Date | | Expiration Date | | Exercise Price |

| Holders of Series B Debt | Investors | | | 2,132,800 | | Aug 2011 | Aug 2011 | | Dec 2013 | | $ | 2.50 | |

| Broker Dealer Series B Debt | Placement Agent | | | 170,624 | | Aug 2011 | Aug 2011 | | Sep 2014 | | $ | 2.50 | |

| Boenning Scattergood | Financial Advisor | | | 250,000 | | May 2011 | May 2011 | | May 2016 | | $ | 2.00 | |

| Investor Group | Investors | | | 300,000 | | Feb 2012 | Mar 2012 | | | (1) | | | (1 | ) |

| Wedbush Securities | Financial Advisor | | | 200,000 | | June 2012 | June 2012 | | June 2017 | | $ | 1.20 | |

| Total | | | | 3,053,424 | | | | | | | | | | | |

| (1) These warrants are priced at the same price per share as the expected equity offering and expire one year after the completion of the expected equity offering. | | |

Conversion Rights:

As of September 30, 2012, through the Company’s various capital raising activities, we have issued the following rights to convert debt into the Company’s common stock as follows:

Two Rivers Water Company -- September 30, 2012 -- 10Q

| Grantee | Company Relationship | | Shares | | | Date of Grant | | | Vesting Date | | | Expiration Date | | | Exercise Price |

| HCIC Debt holders | Creditors | | | 2,336,731 | | | | 2010 | | | | 2010 | | | | (1) | | | | (1 | ) |

| Holders of Series A Debt | Investors | | | 800,000 | | | Feb 2011 | | | Feb 2011 | | | Mar 2014 | | | $ | 2.50 | |

| Holders of Series B Debt | Investors | | | 2,132,800 | | | Aug 2011 | | | Aug 2011 | | | Jun 2014 | | | $ | 2.50 | |

| Holders of Bridge Loan | Investors | | | (2 | ) | | Feb 2012 | | | Feb 2012 | | | | (3) | | | | (3 | ) |

(1) Expiration is when the note is due which is between January and October 2013. Exercise price is from $1.00 to $1.25/share. (2) The holders have the right to convert notes at a price discussed in Note 3 so the number of shares issued will be $3,994,000 divided by price per share. (3) These conversion rights are priced at the same price per share as the expected equity offering and expire one year after the completion of the expected equity offering. | | |

NOTE 6 – SUBSEQUENT EVENTS

In October 2012, the Company obtained extensions to May 31, 2013 on $3,794,000 of the principal of the Bridge Loans. In exchange for these extensions, the terms remain the same and the Company will issue the note holders restricted stock of the Company computed by multiplying the face amount of the note by 10% and dividing by $1.75 (per share). These shares will be issued in the quarter ending December 31, 2012 and the cost will be amortized from November 1, 2012 to May 31, 2013 on a straight line basis.

During October 2012, the Company’s wholly owned subsidiary, DFP, issued a private placement offering up to $5,000,000 of preferred shares in Dionisio Farms & Produce, Inc. As of November 5, 2012, DFP has closed on $3,250,000.

On November 2, 2012, the Company completed its acquisition of Dionisio Produce and Farms, LLC and its affiliated entities through the payment of $900,000 and a seller carry-back promissory note of $600,000 (“Seller Note”). The Seller Note is due in five years, carries interest at 6%, and is payable quarterly. No principal is due until the note matures. The Seller Note is secured by certain farm equipment, that was purchased in this transaction. The assets acquired from Dionisio Produce and Farms, LLC and its affiliated entities will be transferred to DFP.

Two Rivers Water Company -- September 30, 2012 -- 10Q

Note about Forward-Looking Statements

This Form 10-Q contains forward-looking statements, such as statements relating to our financial condition, results of operations, plans, objectives, future performance and business operations. These statements relate to expectations concerning matters that are not historical facts. These forward-looking statements reflect our current views and expectations based largely upon the information currently available to us and are subject to inherent risks and uncertainties. Although we believe our expectations are based on reasonable assumptions, they are not guarantees of future performance and there are a number of important factors that could cause actual results to differ materially from those expressed or implied by such forward-looking statements. By making these forward-looking statements, we do not undertake to update them in any manner except as may be required by our disclosure obligations in filings we make with the Securities and Exchange Commission under the Federal securities laws. Our actual results may differ materially from our forward-looking statements.

Overview

The following Management’s Discussion and Analysis (“MD&A”) is intended to help the reader understand our results of operations and financial condition and should be read in conjunction with the accompanying financial statements and the notes thereto and the financial statements and the notes thereto contained in our 2011 Annual Report on Form 10-K (the “2011 Annual Report”).

The following section focuses on the key indicators reviewed by management in evaluating our financial condition and operating performance, including the following:

| · | Revenue generated from our core businesses. |

| · | Expenses associated with acquiring and developing our business. |

| · | Availability of cash to continue growing our business. |

Our MD&A section includes the following items:

| · | Our Business – The Company’s plans and expectations. |

| · | Results of Operations – our financial results from the three months and nine months ended September 30, 2012 versus September 30, 2011. |

| · | Liquidity, Capital Resources and Financial Position – discussion of our current and expected financial position and liquidity detail. |

| · | Critical Accounting Policies and Use of Estimates – a summary of applicable accounting policies to our business. |