INVESTOR PRESENTATION Exhibit 99.1 |

Certain statements contained in this presentation, including, without limitation, statements containing the words “believes”, “anticipates”, “intends”, “expects”, and words of similar import, constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933 and Section 21E of the Securities Exchange Act of 1934. Such forward looking statements involve known and unknown risks, uncertainties and other factors that may cause our actual results, performance or achievements to be materially different from any future results, performance or achievements expressed or implied by such forward-looking statements. Such factors include, among others, the following: general economic and business conditions in those areas in which we operate, demographic changes, competition, fluctuations in interest rates, changes in business strategy or development plans, changes in governmental regulation, credit quality, the availability of capital to fund the expansion of our business, economic, political and global changes arising from the war on terrorism, the conflict with Iraq and its aftermath, and other factors referenced in this presentation. When relying on forward-looking statements to make decisions with respect to our Company, investors and others are cautioned to consider these and other risks and uncertainties. We disclaim any obligation to update any such factors or to publicly announce the results of any revisions to any of the forward-looking statements contained herein to reflect future events or developments. Forward Looking Information 2 |

• One of the largest community banks headquartered in the high growth market of Las Vegas • Consistent, high performing institution – Five year CAGR of assets and net income of 26% and 24% respectively – Five year average ROE and ROA of 15.7% and 1.21% respectively – Year-end 2005 ROE and ROA of 11.4% and 1.43% respectively • Focus on business lending and relationship banking • Experienced management team with extensive Las Vegas experience • Successful in market acquisition in August 2005 and initial public offering in December 2004 – priced above initial filing range and was over 10x oversubscribed Key Investment Considerations Bellagio 3 |

Issuer: Community Bancorp NASDAQ Symbol: CBON Shares Outstanding (12/31/05): 7,374,712 Trading Range: $23.00 - $34.75 per Share Market Capitalization Range: $170 Million to $256 Million Lead Manager: Keefe, Bruyette & Woods, Inc. Co-Manager: D.A. Davidson & Co. Stock Summary 4 Commercial Real Estate Funded Property |

Company Overview • Community Bancorp is the bank holding company for Community Bank of Nevada serving the greater Las Vegas market with nine branches • Community Bank of Nevada, founded in 1995, is one of the largest community banks headquartered in the greater Las Vegas area • Profitable every year since 1995 • Provides a complete array of commercial banking products and services to small-to medium-sized businesses • On September 26, 2005 closed a $20 million private placement of trust preferred securities. • Trends in growth and profitability have continued into year-end 2005 with organic growth in assets of 26%, organic growth in deposits of 27%, and organic growth in loans of 39%. Post acquisition, assets have grown 56%, deposits 52% and loans 65%. ROE and ROA continues to be strong at 11.4% and 1.43% respectively. Corporate Headquarters 5 |

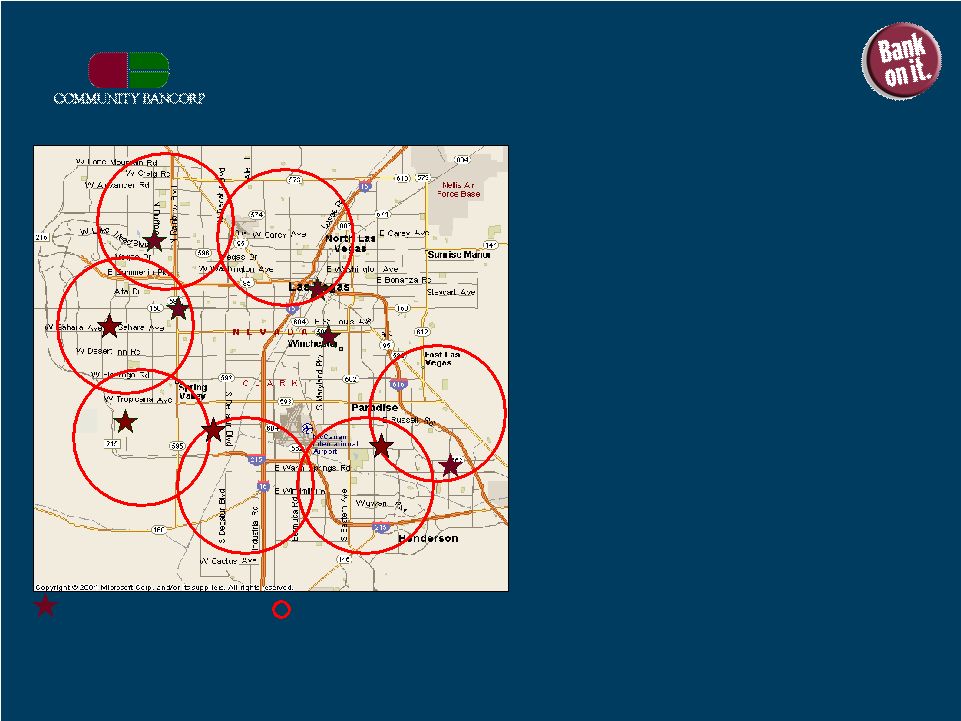

Branch Locations & Market Area •Nine full service offices located throughout the greater Las Vegas Area •One of the largest community banks in the greater Las Vegas Area • Between 2001 and 2005 Clark County’s population grew by approximately 5% per year compared to the national average of 1.2%* • By 2005 Clark County reached a population of 1,796,380 • According to FDIC, deposits in Clark County grew from $15 billion to $34 billion between June 2001 and June 2005, a compound annual growth rate of 22%. • Circled areas are expected growth areas for the market area * According to UNLV CBER Current Branch Locations Proposed Growth Areas 6 |

Deposit Market Share Source: SNL Securities at 6/30/05 (includes Bank of Commerce deposits) One of the largest community banks based in Las Vegas 7 |

• Continue as a public company • To capitalize on growth opportunities in Las Vegas and other rapidly expanding markets – Acquire other community banks in markets that offer regional continuity, such as the greater Las Vegas area or similar high-growth markets in Arizona and California – Planning the 10 th branch for the fall of 2006 and plans to open one additional branch per year through 2008 Growth Strategies World Market Center 8 |

Growth Strategies - Continued SBA Financed Property • Expand our commercial lending portfolio • Increase our SBA production from each of our three loan production offices in Las Vegas, Phoenix and San Diego • Continue to grow our commercial real estate lending and real estate lending. 9 |

Operating Strategies Commercial Real Estate Funded Property • Enhance our risk management function – Proactively manage sound procedures – Commit experienced human resources to this effort. In Q305 an experienced former bank regulator joined the management team to oversee this commitment to internal controls. • Maintain high asset quality by continuing to utilize rigorous loan underwriting standards and credit risk management practices • Continue to actively manage interest rate and market risks – Closely monitor volume and maturity of our rate sensitive assets to our interest sensitive liabilities 10 |

Operating Strategies- Continued • Expand commercial and industrial, as well as small business relationships • Diversify our revenue source – Increase number of products being sold to each of our client relationships 11 Commercial Real Estate Funded Property |

Experienced Management Team- Community Bancorp * Community Bancorp was founded in 2002 Management Position Edward M. Jamison Lawrence K. Scott Cathy Robinson Founder and Chief Executive Officer President and Chief Operating Officer EVP and Chief Financial Officer Years of Experience 33+ 20+ 25+ Years with CBON 10+ 3+ 10+ 12 |

Experienced Management Team- Community Bank of Nevada * Community Bank of Nevada was founded in 1995 Management Position Edward M. Jamison Lawrence K. Scott Cathy Robinson Don F. Bigger Cassandra Eisinger Bruce Ford Tom McGrath Rich Robinson Founder and Chief Executive Officer President and Chief Operating Officer EVP and Chief Financial Officer EVP and Chief Credit Administrator EVP and Chief Operations Officer EVP and Chief Credit Officer EVP and Chief Risk Manager Executive Vice President Years of Experience 33+ 20+ 25+ 20+ 26+ 21+ 30+ 35+ Years with CBON 10+ 3+ 10+ 2+ 1+ 1+ 1 1 13 |

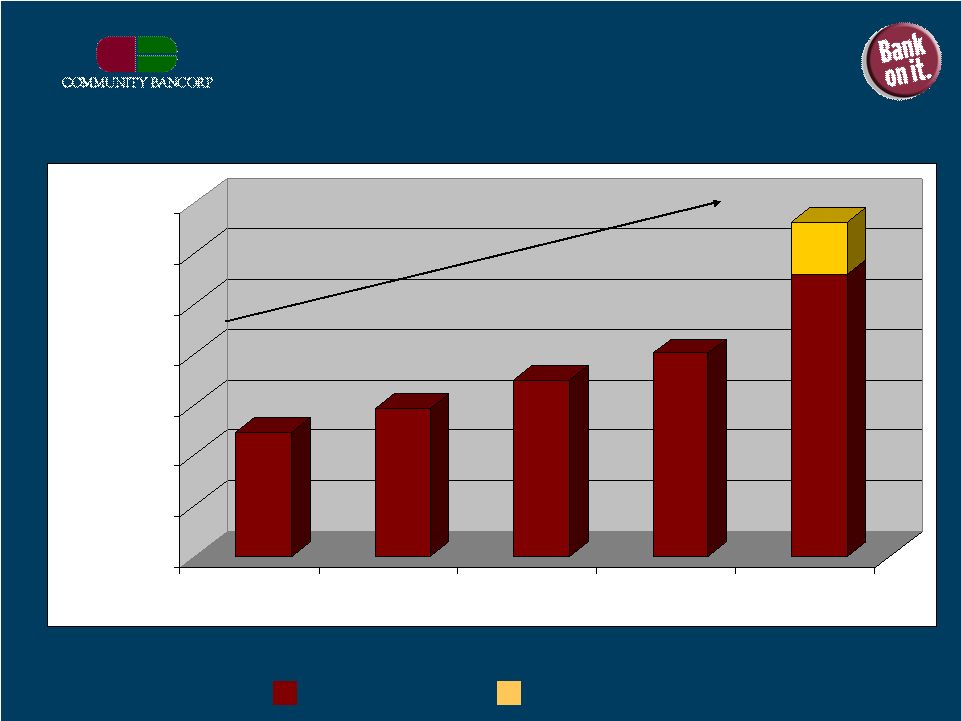

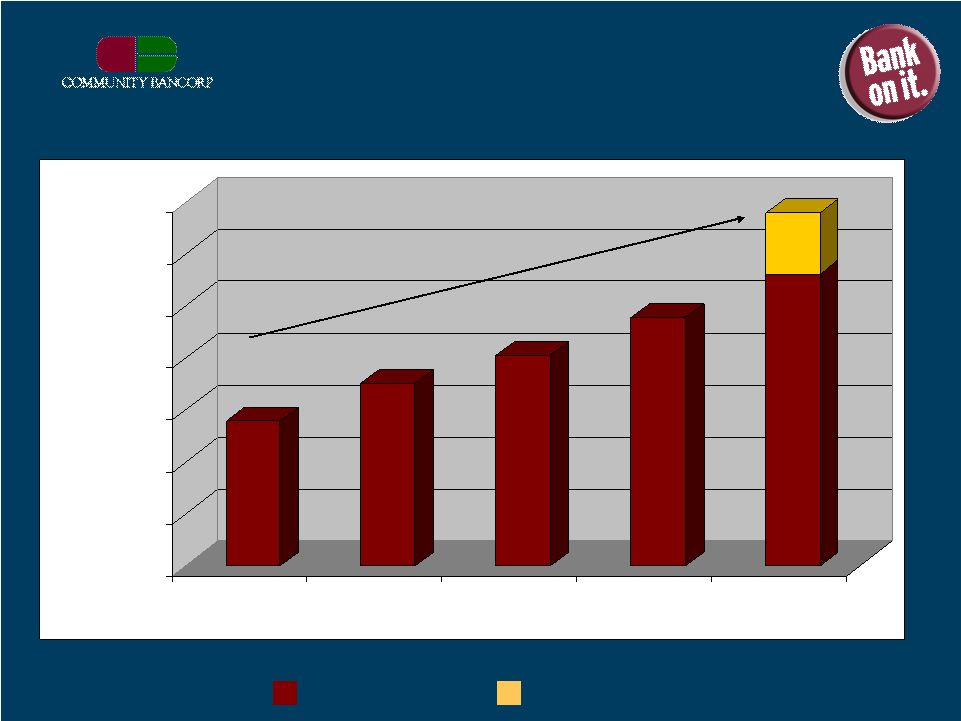

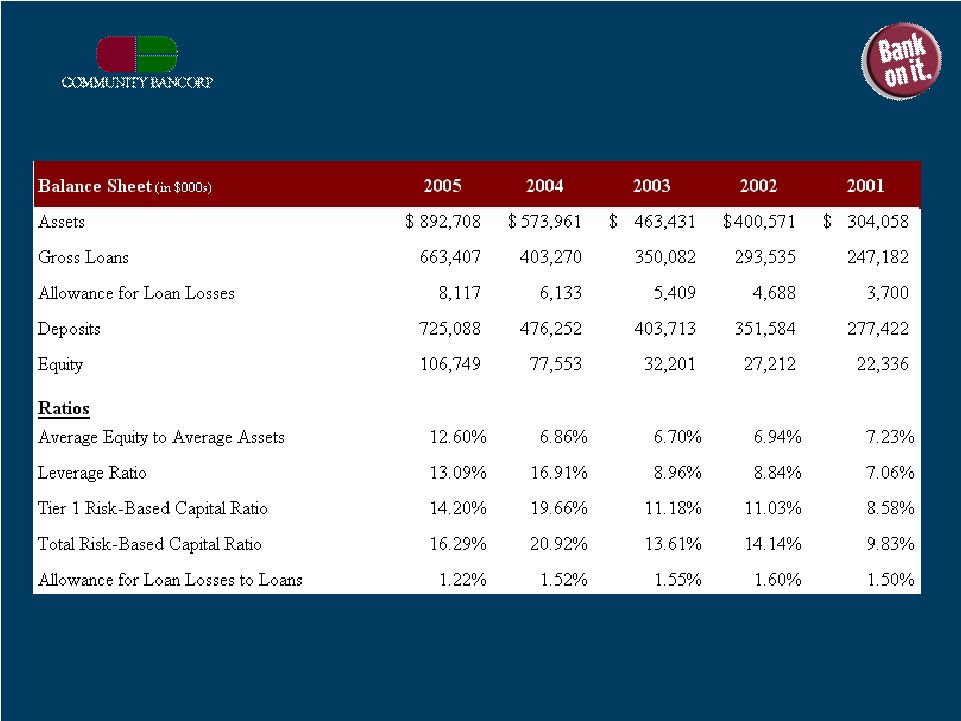

Strong Asset Growth $- $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 $800,000 $900,000 2001 2002 2003 2004 2005 $304,058 $400,571 $463,431 $892,708 ($000) 15 $573,961 $722,009 CAGR = 31% Organic Growth Acquisition Growth* * Based on fair value of assets acquired on August 26, 2005 |

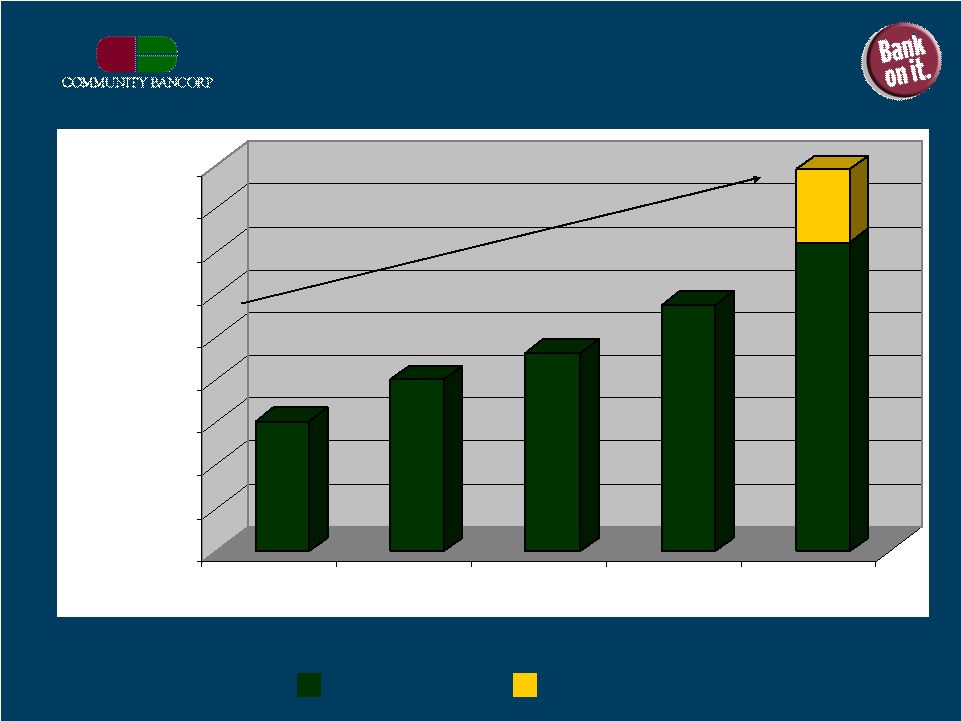

Loan Growth $0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 2001 2002 2003 2004 2005 CAGR = 28% ($000) $247,182 $293,535 $350,082 $663,407 $403,270 16 $559,349 Organic Growth Acquisition Growth |

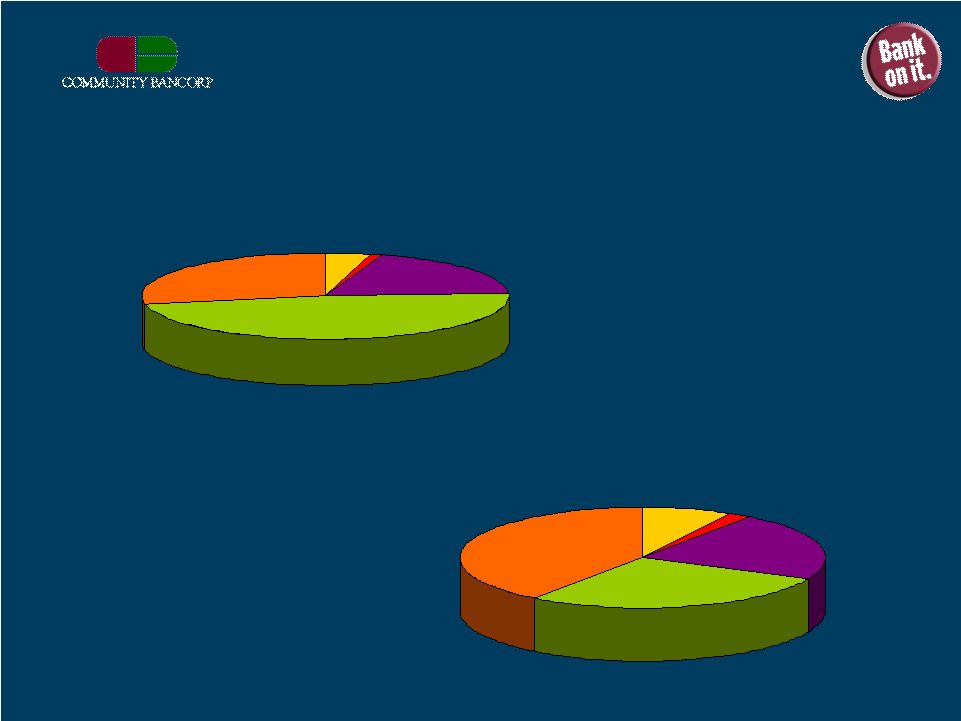

Loan Portfolio Matches the Marketplace 2001 2005 Commercial Real Estate 40% Construction 28% Commercial 22% Consumer & Other 2% Residential Real Estate 8% Construction 48% Commercial Real Estate 28% Consumer & Other 1% Residential Real Estate 4% Commercial 19% 17 |

Deposit Growth $0 $100,000 $200,000 $300,000 $400,000 $500,000 $600,000 $700,000 2001 2002 2003 2004 2005 ($000) CAGR = 27% $277,422 $351,584 $403,713 $476,252 $606,847 18 $725,088 Organic Growth Acquisition Growth |

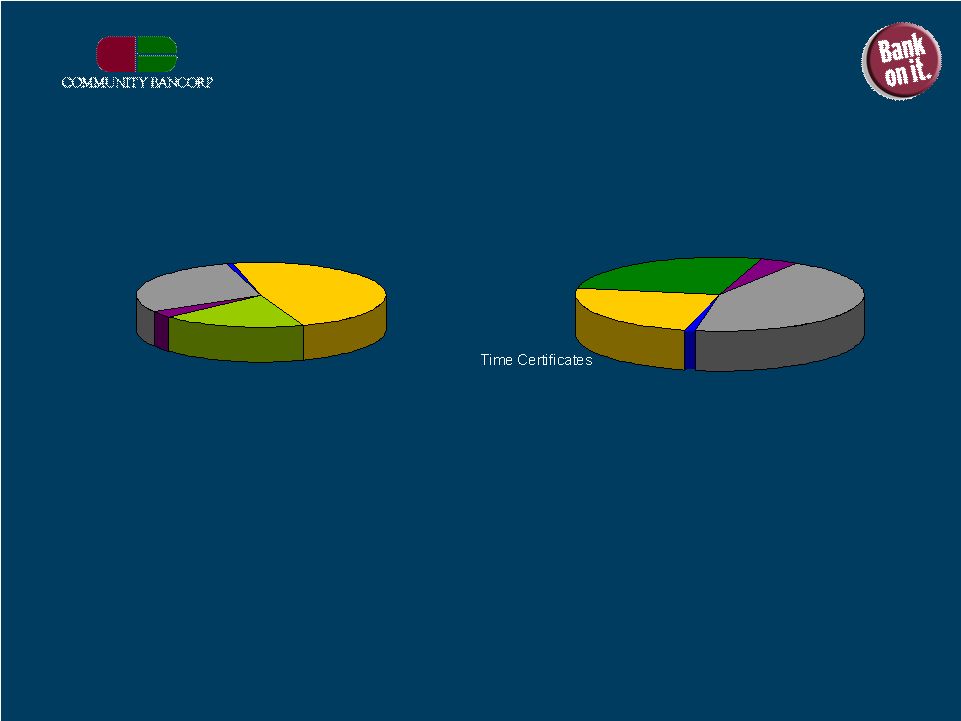

Improving Deposit Mix Interest Bearing Demand 3% Money Market 29% Savings 1% Time Certificates 48% Non-interest Bearing Demand 19% 2001 2005 Average balances for the year ended December 31, 2001 Cost of Deposits = 3.97% 19 Non-interest Bearing Demand 27% Interest Bearing Demand 4% Money Market 44% Savings 1% 24% Average balances for the year ending December 31, 2005 Cost of Deposits = 1.85% |

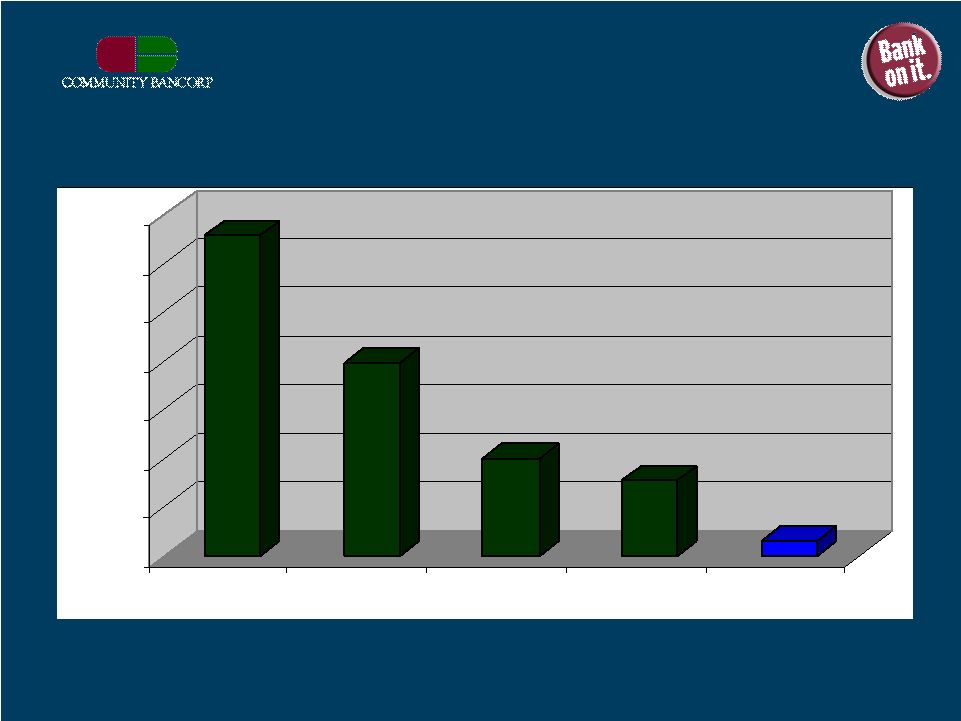

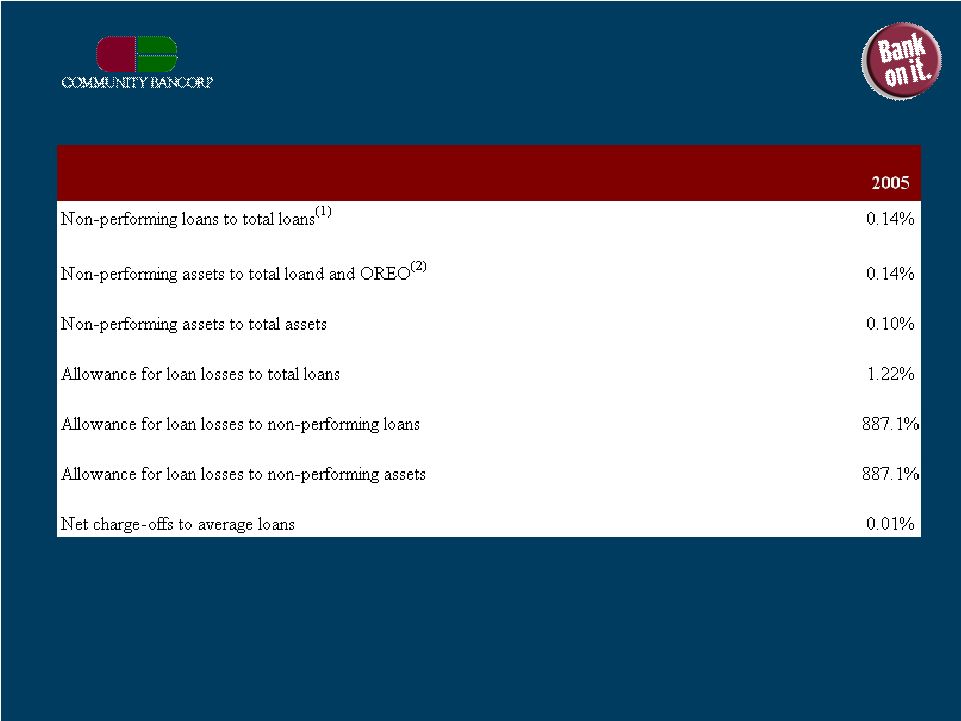

Improving Credit Quality NPAs to Loans & OREO 0.00% 0.50% 1.00% 1.50% 2.00% 2.50% 3.00% 3.50% 2001 2002 2003 2004 2005 ($000) 3.29% 1.99% 1.00% 0.78% 0.14% 20 |

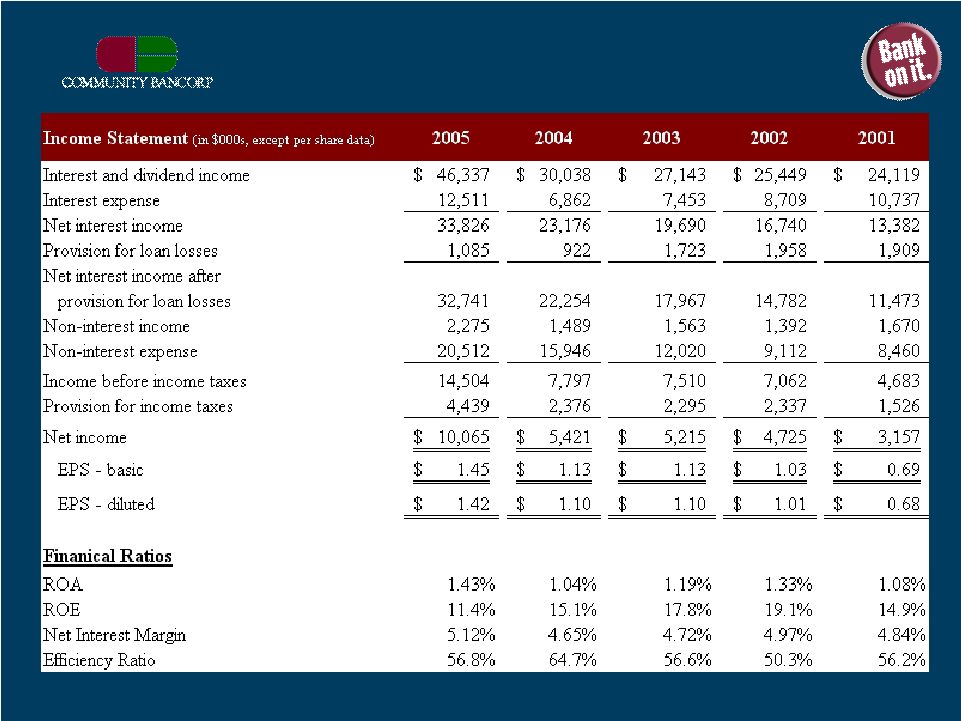

$- $2,000 $4,000 $6,000 $8,000 $10,000 $12,000 2001 2002 2003 2004 2005 Gains in Net Income ($000) $3,157 $4,725 $5,215 $5,421 $10,065 21 |

Consistently Profitable ROE 0.0% 2.0% 4.0% 6.0% 8.0% 10.0% 12.0% 14.0% 16.0% 18.0% 20.0% 2001 2002 2003 2004 2005 14.9% 19.1% 17.8% 15.1% 11.4% 22 |

Asset Quality (1) Non-performing loans are defined as loans that are past due 90 days or more plus loans placed in non-accrual status and restructured loans. (2) Non-performing assets are defined as loans that are past due 90 days or more, non-accrual loans plus other real estate owned. 25 |

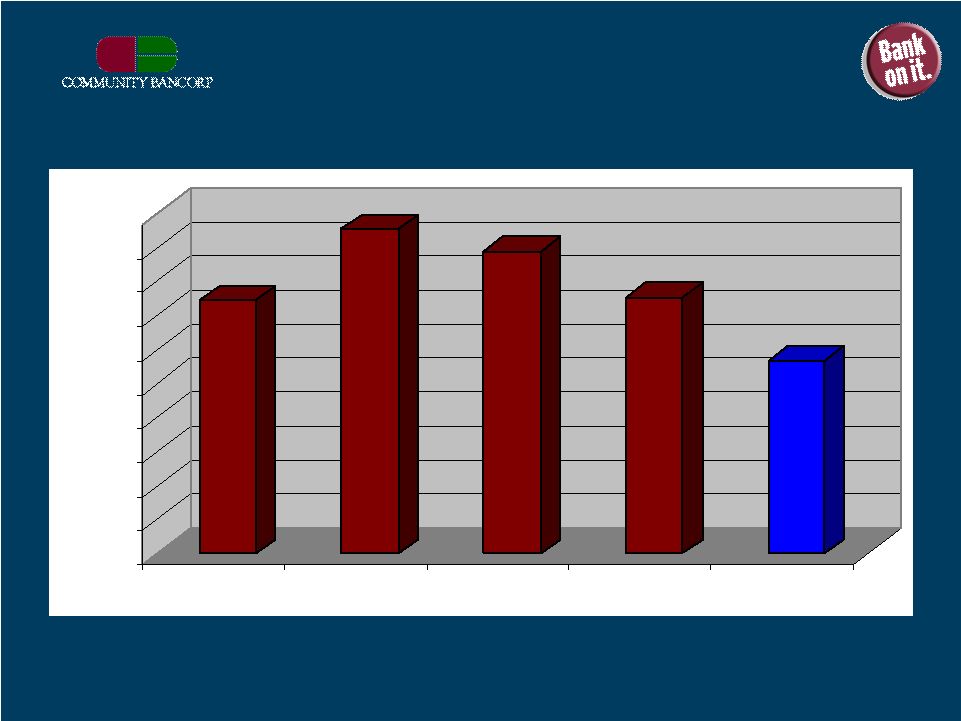

EPS - Diluted $- $0.20 $0.40 $0.60 $0.80 $1.00 $1.20 $1.40 $1.60 2001 2002 2003 2004 2005 CAGR = 20% $0.68 $1.01 $1.10 $1.10 $1.42 26 |

Summary • Strong balance sheet growth • Consistent profitability • High quality credit • Strong asset sensitive balance sheet 27 |

Investment Thesis • One of the largest community banks headquartered in the high growth market of Las Vegas • Excellent expansion opportunities in both Las Vegas and other high growth markets • Consistent, high performance institution – Five year CAGR of assets and net income of 26% and 24% respectively – Five year average ROE and ROA of 15.7% and 1.21% respectively • Focus on commercial banking and total client relationships • Experienced management team with over 205 years combined banking experience in the greater Las Vegas area 28 |