Bob Currey – Chief Executive Officer

Steve Childers – Chief Financial Officer

Steve Jones – Vice President, Investor Relations

September 2007

1

Safe Harbor

2

Prospectus & Proxy

3

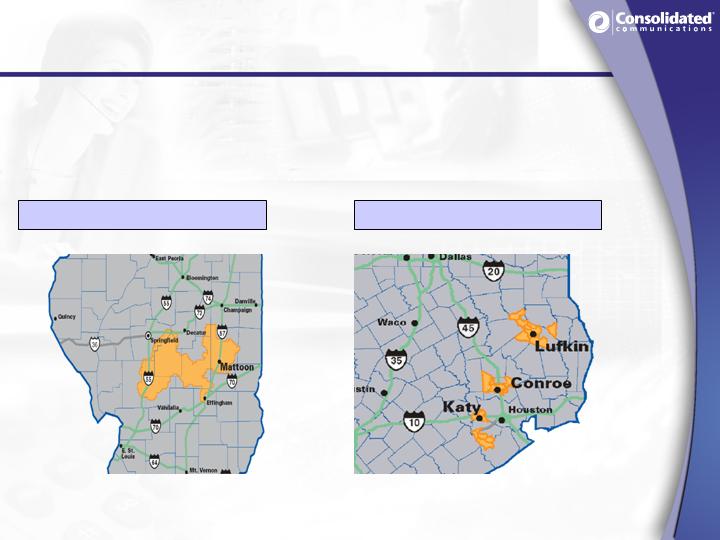

Company Overview

14th largest Independent Local Exchange Carrier in the U.S.

with operations in Illinois and Texas

Approximately 229,000 access lines, 58,000 DSL subscribers and 9,600

IPTV subscribers, representing over 296,000 total connections

Providing voice, video and data services

Triple play offerings in both Texas and Illinois

Announced acquisition of North Pittsburgh Systems, expect to close Q4

2007 or Q1 2008

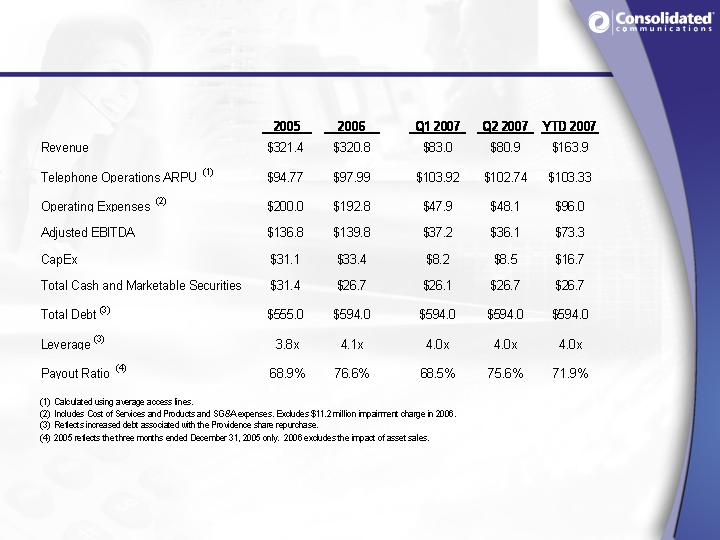

Year to date 2007 financial overview:

Revenues of $163.9 million

Adjusted EBITDA of $73.3 million

Cash Available to Pay Dividends of $28.0 million, with a dividend

payout ratio of 71.9%

4

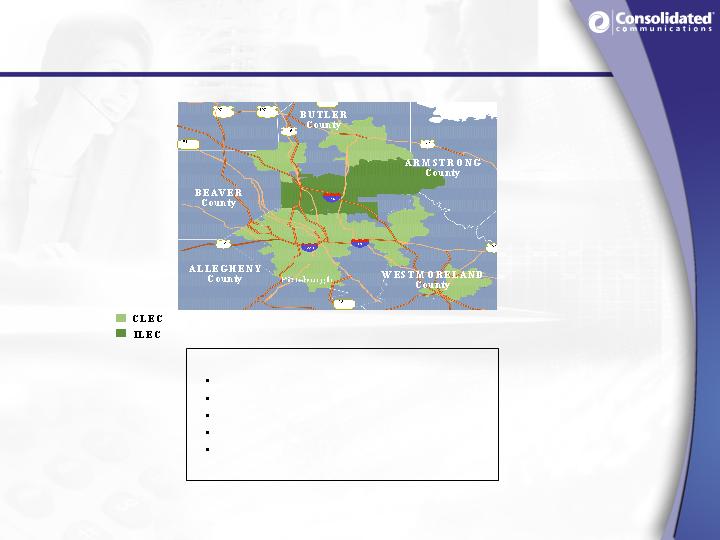

Operations in both Texas and Illinois

Illinois

Texas

Balance of both stable rural and growing suburban

markets

5

Marketing, customer service and technology initiatives have been

designed to minimize competitive traction

The company has successfully managed wireless competition since the

late 1980s

Cable operators - Charter and Mediacom in Illinois and Comcast and

Suddenlink in Texas

Only Mediacom has launched a voice product in CNSL’s markets

Managing Competition

CNSL’s strategy is to minimize competition from cable and

wireless companies by providing “sticky” bundled service

offerings and exemplary customer service

6

Favorable Regulatory Environment

Rate of return regulated at the federal level in both states

Elected incentive regulation at the state level in Texas and rate of

return in Illinois

Strong working relationships with the FCC and both state

commissions

Actively involved in both USF and access charge reform

7

Experienced & Operations-Focused

Management Team

Executive

Title

Telecom

Experience

Bob Currey

President & CEO

37 Years

Steve Childers

Chief Financial Officer

19 Years

Joe Dively

Sr. VP & President of IL

Telephone Ops

20 Years

Steve Shirar

Sr. VP & President of

Enterprise Units

22 Years

Bob Udell

Sr. VP & President of TX

Telephone Ops

19 Years

Chris Young

Chief Information Officer

19 Years

Richard Lumpkin

Chairman

46 Years

CCI Date of

Initial Hire

1990

1986

1991

1996

1993

1985

1963

8

Executing on our Strategy

9

Sustain

and grow

cash flow

Increase

revenue

per customer

Improve

operating

efficiency

Pursue selective

acquisitions

Maintain

effective capital

deployment

9

CNSL continues to focus on increasing revenues per

customer by driving service bundle subscriptions

Attractive product set including:

DSL

IPTV

Integrated voice products

First to offer the triple play in both its Illinois and Texas

markets, with over 90% of video subscribers selecting the

triple play

Bundling not only drives revenue per customer, but also

reduces line loss

Increasing Revenue per Customer with Bundling

10

DSL is a Key Component of the Bundle

Attractive, feature rich offering

Multiple speeds and price points

High-margin product

Nearly 100% self-installed

35.4% penetration of

primary residential lines

% of total

access lines

16.2%

18.1%

19.2%

20.9%

22.6%

24.1%

25.4%

11

IPTV Service in Illinois & Texas

A robust offering with over 200 all-digital channels,

premium movie packages and over a 1000 hours of

movies on demand

12

Video Drives Incremental Revenue Per Customer

IPTV enables the Triple Play offering

Incremental Product Rollout

Leverages existing resources and network

IP Backbone/ADSL 2+

Future CapEx is success based

Enhances the value of the bundle and deepen customer relationships

IPTV available in both Illinois and Texas

Illinois launched in 2005

Conroe & Katy, Texas launched in August 2006

Lufkin, Texas launched in March 2007

9,577 total video subscribers with 107,631 homes passed as of 6/30/2007

HDTV rolled out in Q2 in Texas and Q3 in Illinois

DVR to be rolled out in Q4 2007

13

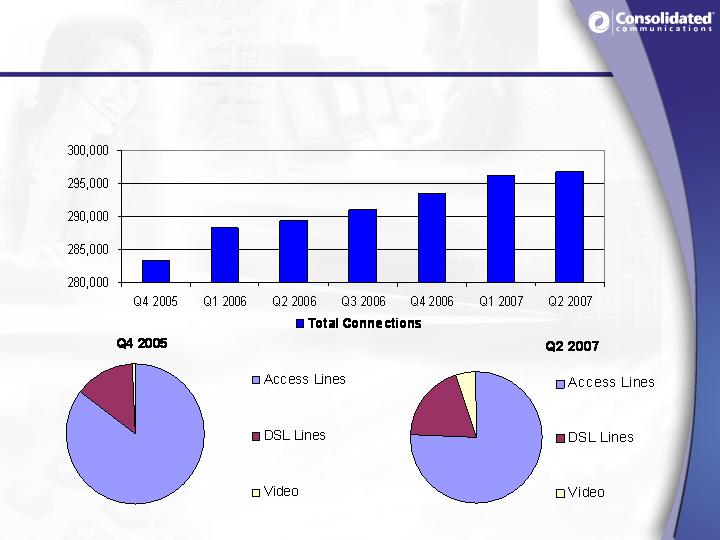

Stable Customer Base

CNSL’s total connections have grown by over 13,000 since

2005 and product mix has changed

14

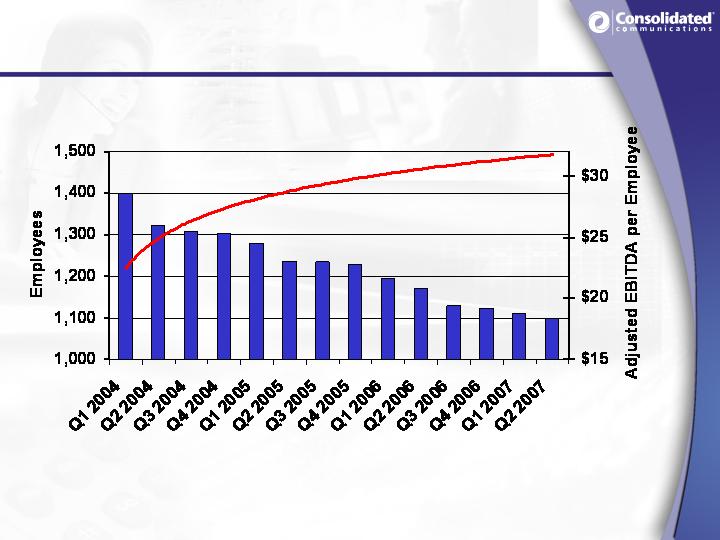

Increasing Efficiencies & Adjusted EBITDA per

Employee

Adjusted EBITDA per employee is represented by a trend line. See appendix for detail.

15

Effective Capital Deployment

Since the beginning of 2003, CNSL has invested over $125 million in

its network, including its core IP backbone and softswitch technology

Installed television headends in Texas and Illinois and is currently

delivering an all digital video signal over its existing fiber/copper

network

92% of total access lines are DSL-capable

Network supports speeds up to 10 megabits per second, as

required by consumer demand

CNSL’s advanced network enables it to offer advanced

products and services, which is a key part of its strategy to

retain customers and increase revenue

16

Acquisition Criteria

It will continue to monitor and potentially pursue select acquisition

opportunities based on the following criteria:

Attractiveness of the markets

Quality of the network

The company’s ability to integrate the acquired company efficiently

Potential operating synergies

Cash flow accretive from day one

CNSL has a proven track record of successful business

integrations

17

North Pittsburgh Current Operations

North Pittsburgh Systems, Inc.

LTM Revenue ………………………….. $99.8M

ILEC access lines ………… ……………60,663

CLEC access line equivalents ………... 66,699

DSL subscribers ………………...………16,572

Employees ……………………………… 300

18

NPSI Transaction Highlights

Expands Consolidated’s footprint

North Pittsburgh provides:

An integrated telecommunications business providing ILEC, edge-out CLEC and

Internet services

An extensive fiber network that extends into Pittsburgh and surrounding

communities

As of June 30, 2007, it served 60,700 ILEC access lines, 66,700 CLEC access

line equivalents and 16,600 DSL subscribers

After completion of this transaction Consolidated will be the 12th largest telephone

company in the United States

Provides an advanced network

99% DSL capable

Enables rollout IPTV in 2008

Opportunity to grow the product suite, increase penetration and improve

customer retention

Improves the dividend payout ratio

Increases operating efficiencies and drives annual cash synergies

Delivers strong cash flow from wireless partnerships

Projected to be cash flow accretive in first full year of operations (post synergies)

19

Consolidated’s Strategy for North Pittsburgh Market

Grow Revenue

Launch IPTV in 2008

Aggressively market broadband products and the triple-play bundle

Retain customers

Leverage North Pittsburgh’s new pricing/bundling strategy

Create “stickiness” with existing products and leverage the triple-play offer

Build on North Pittsburgh’s initiatives by implementing the best customer

care and community involvement practices from both companies

Improve operating efficiency

Move to functional organization structure

Integrate the properties utilizing Consolidated’s proven processes

Achieve synergies

Leverage economies of scale

20

Synergies

Consolidation

One functional organization across three markets

Leverage Consolidated’s operating capabilities

Leveraging Scale

Software licenses

Maintenance contracts

Purchasing contracts

Reduce third party costs

Legal fees

Audit and SOX fees

Outsourced billing and financial system costs

Public company fees

21

CNSL Acquisition Criteria

Attractiveness of the markets

High growth, affluent markets

Edge-out CLEC provides synergy with ILEC

Quality of the network

Well maintained plant

Short loops enable higher broadband speeds and efficient video

overlay

Ability to integrate efficiently

Leverage existing, proven systems and processes

Potential for operating synergies

$7-11 million annually in estimated Op Ex savings

$3-6 million annually in estimated Cap Ex savings

Cash flow accretive

Improves dividend payout ratio

22

CNSL Delivering Strong Financial Results…

23

Investment Highlights

Attractive Markets

Stable Local

Telephone Business

Bundled

Service Offerings

Favorable

Regulatory

Environment

Technologically

Advanced Network

Experienced

Management Team

24

Appendix

25

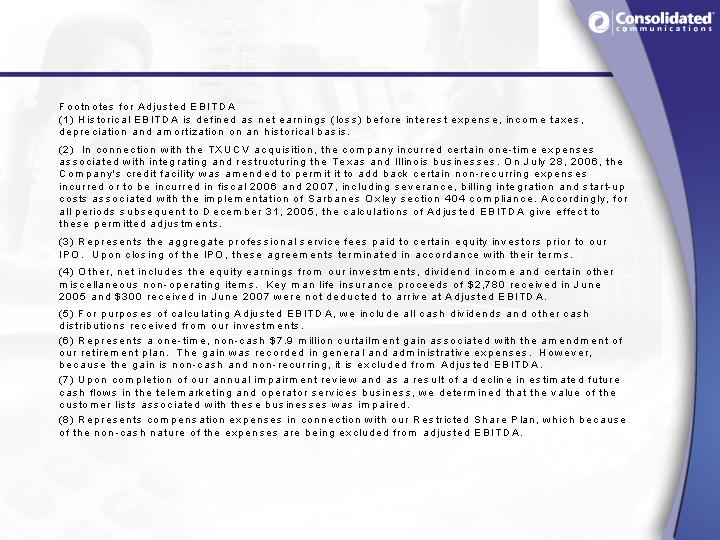

GAAP Reconciliation

This presentation includes disclosures regarding “Adjusted EBITDA”, “cash available to pay dividends” and “total net debt to last 12-

month Adjusted EBITDA ratio” (which we refer to as leverage), all of which are non-GAAP financial measures. Accordingly, they

should not be construed as alternatives to net cash from operating or investing activities, cash flows from operations or net income

(loss) as defined by GAAP and are not, on their own, necessarily indicative of cash available to fund our cash needs as determined in

accordance with GAAP. In addition, not all companies use identical calculations, and these non-GAAP financial measures may not be

comparable to other similarly titled measures of other companies. A reconciliation of the differences between these non-GAAP

financial measures and the most directly comparable financial measures presented in accordance with GAAP is included in the tables

that follow.

Adjusted EBITDA, which corresponds to pro forma Bank EBITDA as used and defined in the prospectus dated July 21, 2005 filed in

connection with the IPO, is comprised of historical EBITDA, as adjusted to give effect to the Texas Communications Ventures

Company (TXUCV) acquisition and certain other adjustments permitted and contemplated by our amended and restated credit

facilities.

EBITDA is defined as net earnings (loss) before interest expenses, income taxes, depreciation and amortization on an historical basis.

We believe net cash provided by operating activities is the most directly comparable financial measure to EBITDA under GAAP.

To give pro forma effect to the TXUCV acquisition as if it had occurred on the first day of the periods presented, we have made two

sets of adjustments. First, because the operating results of TXUCV are not reflected in our historical EBITDA and financial results for

the period prior to the date of its acquisition, TXUCV’s historical EBITDA for 2003 and 2004 has been added to our historical EBITDA.

Second, we made pro forma adjustments to the selling, general and administrative expenses to reflect (1) a reduction in costs due to

the termination of certain TXUCV employees upon the closing of the acquisition and (2) incremental professional service fees paid to

certain equity investors pursuant to a new professional services agreement entered into in connection with the TXUCV acquisition.

Finally, when calculating EBITDA in accordance with our credit agreement, the credit agreement permits us to exclude the effect of

certain items. Each of these adjustments is described in the footnotes to the attached reconciliations.

Cash available to pay dividends represents Adjusted EBITDA plus cash interest income, less (1) cash interest expense (after giving

pro forma effect to the IPO as if it had been completed on July 1, 2005), (2) capital expenditures and (3) cash taxes.

26

GAAP Reconciliation

We present Adjusted EBITDA and cash available to pay dividends for several reasons. Management believes Adjusted EBITDA and

cash available to pay dividends are useful as a means to evaluate our ability to fund our estimated uses of cash (including interest on

our debt) and pay dividends. In addition, we have presented Adjusted EBITDA and cash available to pay dividends to investors in the

past because they are frequently used by investors, securities analysts and other interested parties in the evaluation of companies in

our industry, and management believes presenting them here provides a measure of consistency and comparability in our financial

reporting. Adjusted EBITDA and cash available to pay dividends, referred to as Available Cash in our credit agreement, are also

components of the restrictive covenants and financial ratios contained in the agreements governing our debt that require us to maintain

compliance with these covenants and limit certain activities, such as our ability to incur debt and to pay dividends. The definitions in

these covenants and ratios are based on Adjusted EBITDA and cash available to pay dividends after giving effect to specified charges.

As a result, management believes the presentation of Adjusted EBITDA and cash available to pay dividends as supplemented by these

other items provides important additional information to investors. In addition, Adjusted EBITDA and cash available to pay dividends

provide our board of directors with meaningful information to determine, with other data, assumptions and considerations, our dividend

policy and our ability to pay dividends under the restrictive covenants in the agreements governing our debt and to measure our ability

to service and repay debt.

While we use Adjusted EBITDA and cash available to pay dividends in managing and analyzing our business and financial condition

and believe they are useful to our management and investors for the reasons described above, these non-GAAP financial measures

have certain shortcomings. In particular, Adjusted EBITDA does not represent the residual cash flows available for discretionary

expenditures, since items such as debt repayment and interest payments are not deducted from such measure. Similarly, while we

may generate cash available to pay dividends, we are not required to use any such cash to pay dividends, and the payment of any

dividends is subject to declaration by our board of directors, compliance with applicable law and the terms of our credit agreement and

the indenture governing our senior notes.

Because Adjusted EBITDA is a component of the ratio of total net debt to last 12-month Adjusted EBITDA, it is subject to the material

limitations discussed above, and the risk that we may not be able to use the cash on the balance sheet to reduce our debt on a dollar-

for-dollar basis. Management believes that this ratio is useful as a means to evaluate our ability to incur additional indebtedness in the

future and to assist investors, securities analysts and other interested parties in evaluating the companies in our industry.

27

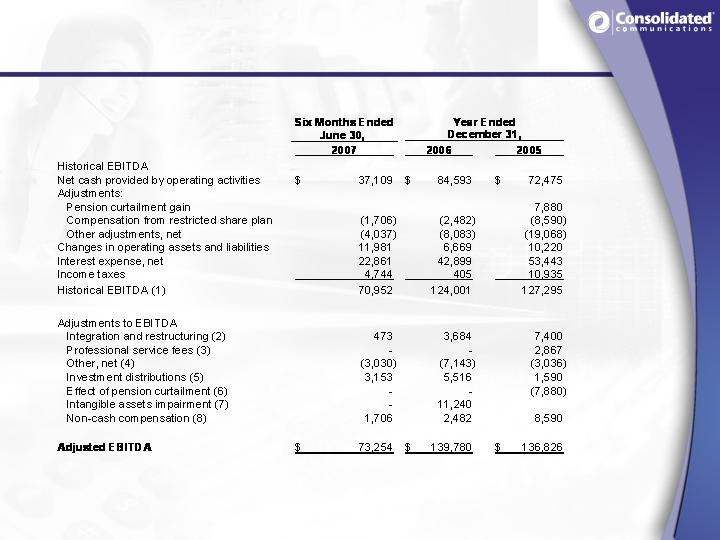

Adjusted EBITDA Reconciliation

See footnotes on next page

28

Adjusted EBITDA Reconciliation

29

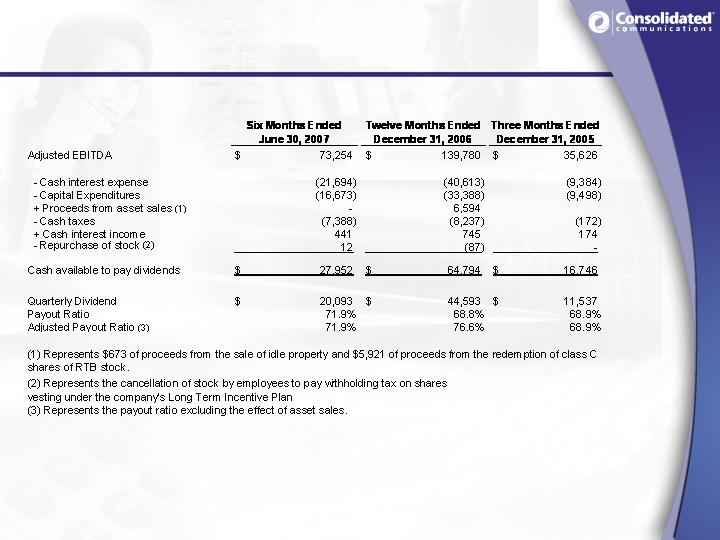

Cash Available to Pay Dividends

30

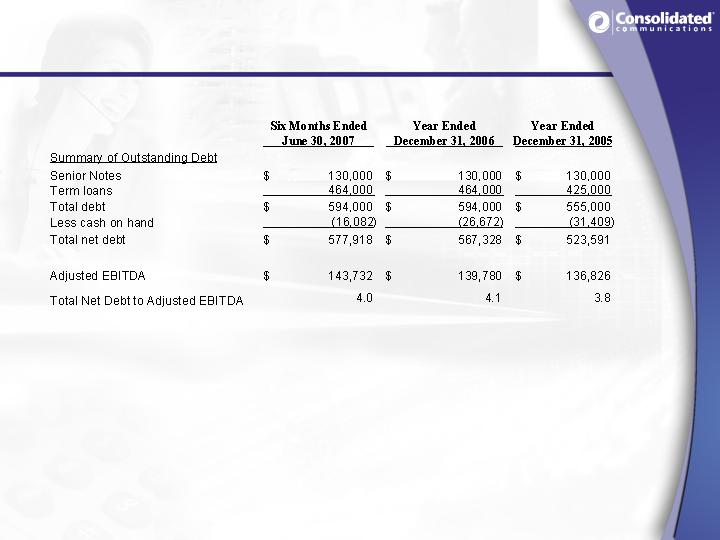

Total Net Debt to Adjusted EBITDA Ratio

31

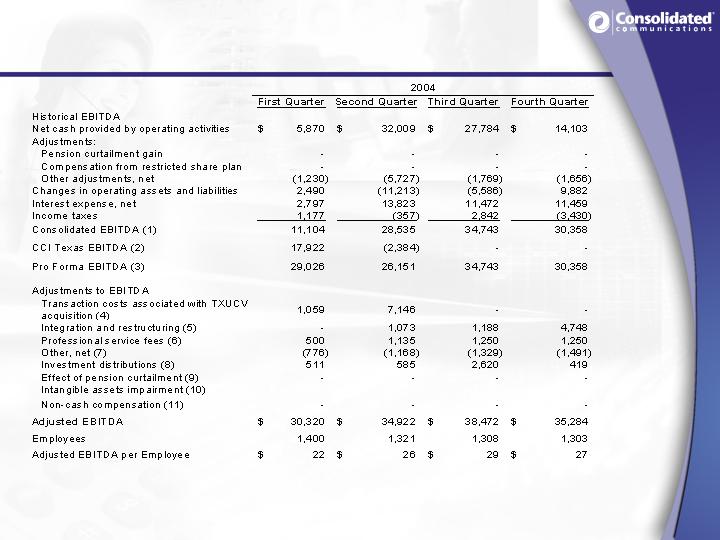

Adjusted EBITDA per Employee - 2004

See footnotes on page 36

32

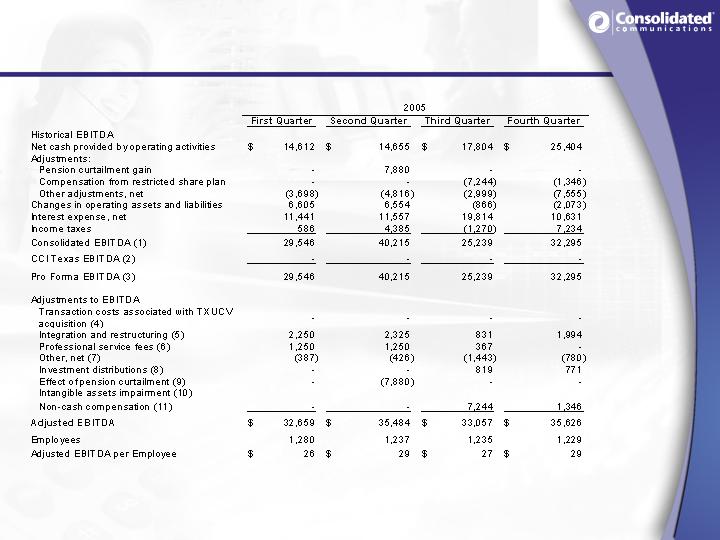

Adjusted EBITDA per Employee - 2005

See footnotes on page 36

33

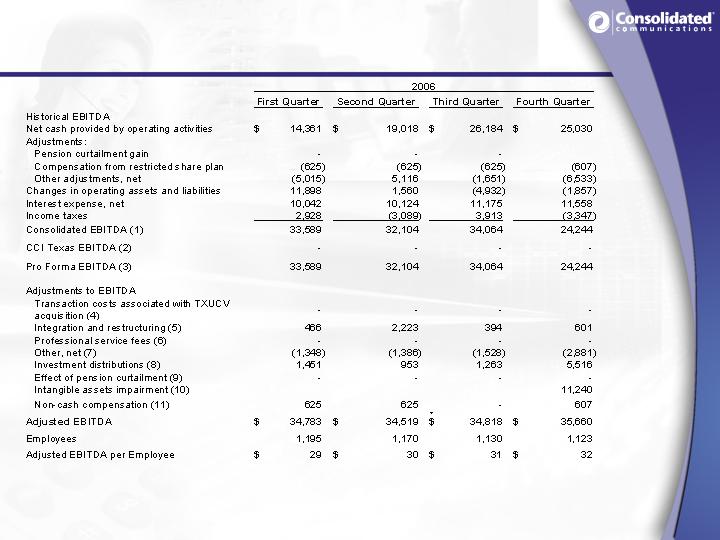

Adjusted EBITDA per Employee - 2006

See footnotes on page 36

34

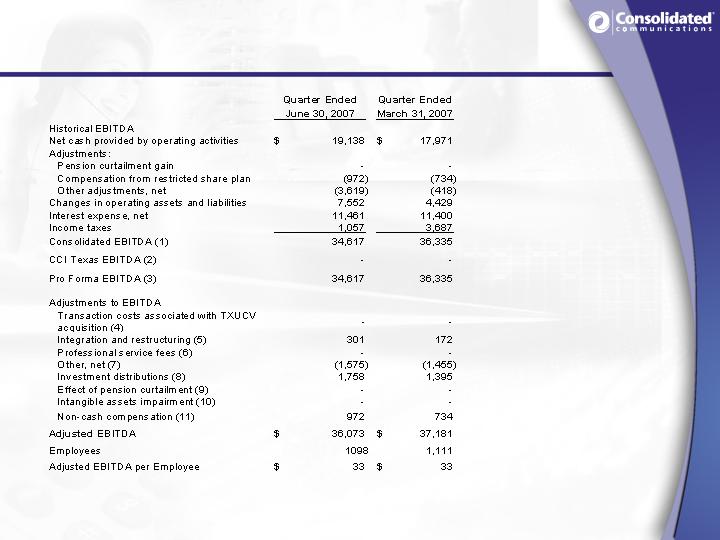

Adjusted EBITDA per Employee - 2007

See footnotes on page 36

35

Adjusted EBITDA per Employee

36

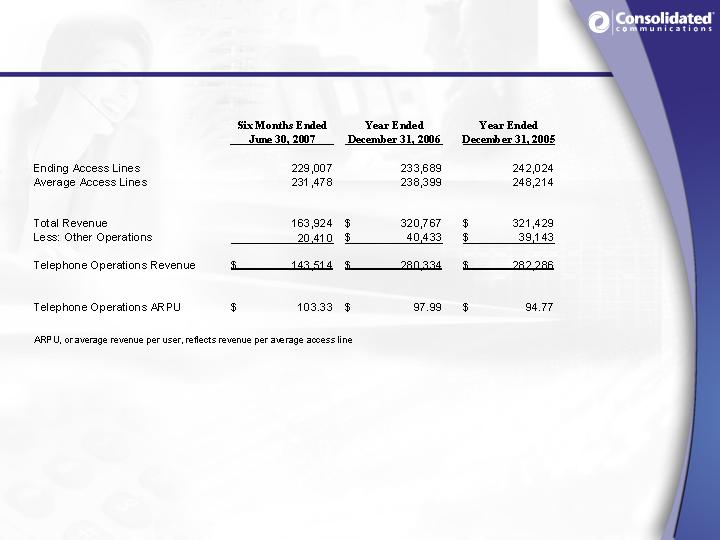

Telephone Operations ARPU

37