Bob Currey – Chief Executive Officer

Steve Childers – Chief Financial Officer

Steve Jones – Vice President, Investor Relations

April 2008

1

Safe Harbor

2

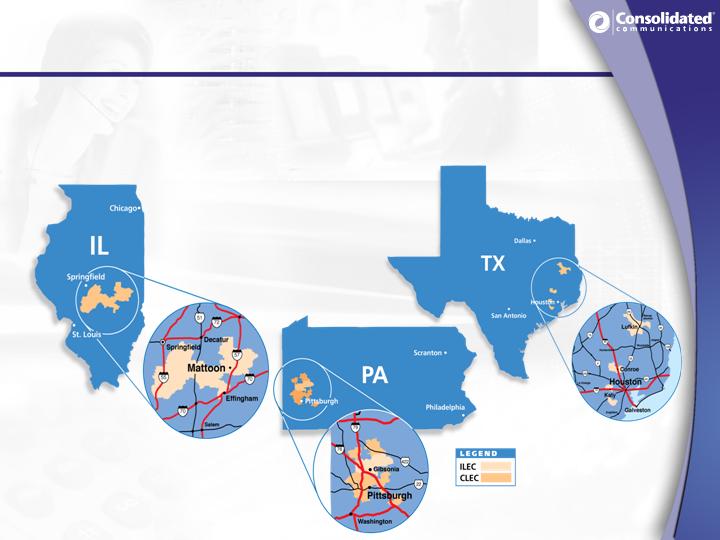

Company Overview

12th largest Independent Local Exchange Carrier in the U.S., with

operations in Illinois, Texas and Pennsylvania

Approximately 282,028 ILEC access lines, 68,874 CLEC access line equivalents,

83,521 DSL subscribers and 12,241 IPTV subscribers, representing 446,664 total

connections

Providing voice, video and data services

Triple play offerings in both Texas and Illinois, and coming soon in Pennsylvania

Full year 2007 CNSL financial overview:

Revenues of $329.2 million

Adjusted EBITDA of $143.8 million

$82.1 million in cash from operations

Dividend payout ratio of 75.9%

Full year 2007 NPSI financial overview:

Revenues of $95.7 million

Adjusted EBITDA of $43.2 million

$9.8 million in cash from operations

3

Operations in Illinois, Texas and

Pennsylvania

ILEC markets are a balance of both rural and

suburban markets

4

Marketing, customer service and technology initiatives have been

designed to minimize competitive traction

This approach will be leveraged in Pennsylvania

Cable operators - Mediacom and Nu Wave in Illinois, Comcast and

Suddenlink in Texas, and Armstrong and Comcast in Pennsylvania

Mediacom, Armstrong and Comcast in Pennsylvania have launched

voice products in CNSL’s markets

Managing Competition

CNSL’s strategy is to minimize competition from cable and

wireless companies by providing “sticky” bundled service

offerings and exemplary customer service

5

Regulatory Landscape

Rate of return regulated at the federal level in all states

Filed petition for price caps in Illinois and Texas

Will remain an average schedule company in Pennsylvania in 2008

Elected incentive regulation at the state level in Texas & Pennsylvania,

and rate of return in Illinois

Strong working relationships with the FCC and all state commissions

Actively involved in both USF and access charge reform

Favorable Regulatory Environment

6

Experienced & Operations-Focused

Management Team

Executive

Title

Telecom

Experience

Bob Currey

President & CEO

38 Years

Steve Childers

Senior Vice President &

Chief Financial Officer

20 Years

Joe Dively

Senior Vice President

21 Years

Steve Shirar

Senior Vice President

23 Years

Bob Udell

Senior Vice President

20 Years

Chris Young

Chief Information Officer

20 Years

Richard Lumpkin

Chairman

47 Years

CCI Date of

Initial Hire

1990

1986

1991

1996

1993

1985

1963

7

Executing on our Strategy

8

Sustain

and grow

cash flow

Increase

revenue

per customer

Improve

operating

efficiency

Pursue selective

acquisitions

Maintain

effective capital

deployment

8

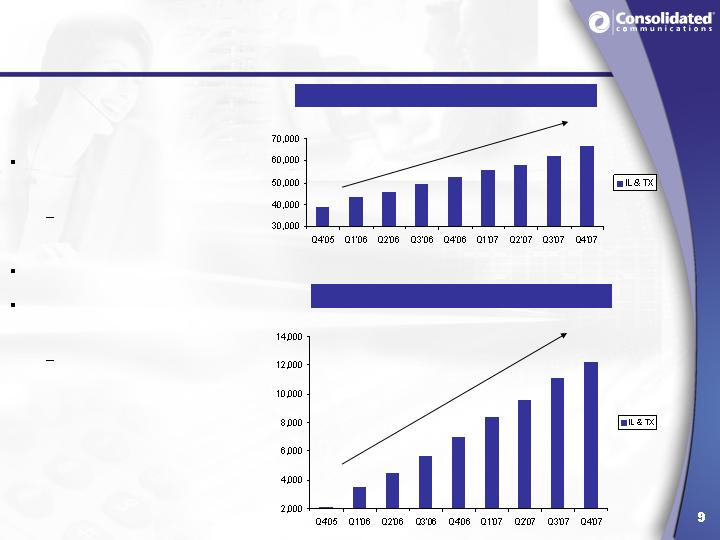

Increase Revenue per Customer

DSL Subscriber Growth

IPTV Subscriber Growth

Attractive, feature rich

broadband offerings

Multiple DSL speeds

and price points

Higher margin products

IPTV enables the Triple

Play offering

Enhances the value of

the bundle and

deepens customer

relationships

9

IPTV Service in Illinois & Texas

A robust offering with over 200 all-digital channels,

premium movie packages and over a 1000 hours of

movies on demand

10

Video Drives Incremental Revenue Per Customer

IPTV enables the Triple Play offering

Incremental Product Rollout

Leverages existing resources and network

IP Backbone/ADSL 2+

Future CapEx is success based

Enhances the value of the bundle and deepens customer

relationships

Currently available in Illinois and Texas

12,241 total video subscribers

HDTV rolled out in Q2 in Texas and Q3 in Illinois

Coming soon: In Q2 2008, IPTV service in PA and DVR in all states

11

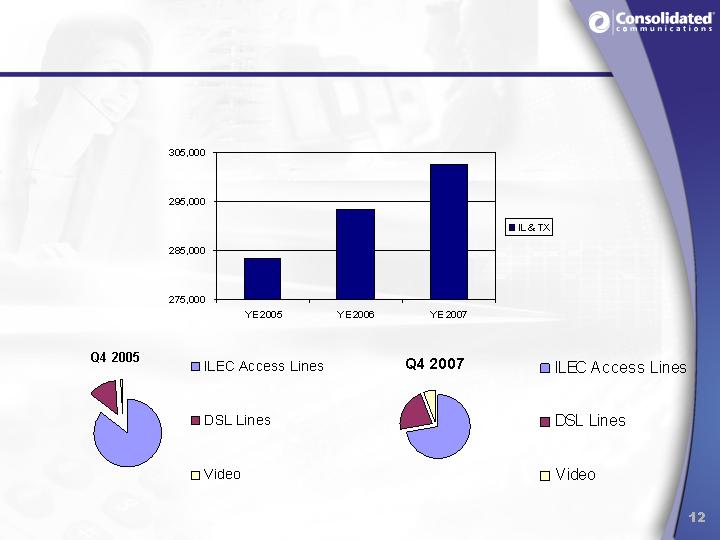

Stable Customer Base

CNSL’s total connections have grown by over 19,000 since

2005 and product mix has changed

12

CLEC Overview

True “edge-out” strategy, which leverages ILEC network, human capital skills

and reputation in the surrounding markets

Cash flow positive due to focus on success-based capital expenditures

Focus on small to mid-sized business customers (5 to 500 lines), educational

institutions and healthcare facilities

Operates an extensive SONET optical network with over 300 route miles of fiber

optic facilities in the Pittsburgh metropolitan market

Focus is on migrating to an on-net, ethernet and VoIP delivery system

13

Disciplined Capital Deployment

Installed television headends in Texas and Illinois and is currently

delivering an all digital video signal over its existing fiber/copper

network

Expect to launch IPTV service in Pennsylvania in Q2 2008, utilizing

Illinois headend

95% of total access lines are DSL-capable in Illinois and Texas, 100%

in Pennsylvania

The networks in all three states support speeds up to 10 megabits

per second, as required by consumer demand

Historically capital spending has run 10% -12% of revenue

CNSL’s advanced network enables it to offer advanced

products and services, which is a key part of its strategy to

retain customers and increase revenue

14

CNSL Acquisition Criteria

Attractiveness of the markets

North Pittsburgh:

High growth, affluent markets

Edge-out CLEC provides synergy with ILEC

Quality of the network

North Pittsburgh:

Well maintained plant

Short loops enable higher broadband speeds and efficient video

overlay

Ability to integrate efficiently

North Pittsburgh:

Leverage existing, proven systems and processes

Potential for operating synergies

North Pittsburgh:

$7-$11 million annually in estimated Op Ex savings

$3-$6 million annually in estimated Cap Ex savings

Cash flow accretive

North Pittsburgh:

Improves dividend payout ratio

15

CNSL Delivering Strong Financial Results…

16

($ in millions)

2005

2006

2007

CNSL

Revenue

321.4

$

320.8

$

329.2

$

Adjusted EBITDA

136.8

$

139.8

$

143.8

$

Cash Provided by Operating Activities

72.5

$

84.6

$

82.1

$

CapEx

31.1

$

33.4

$

33.5

$

Payout Ratio

(1)

68.9%

76.6%

75.9%

NPSI

Revenue

109.8

$

103.5

$

95.7

$

Cash Provided by Operating Activities

32.7

$

13.9

$

9.8

$

Adjusted EBITDA

55.6

$

46.2

$

43.2

$

CapEx

10.5

$

16.0

$

16.7

$

CNSL Balance Sheet

Total Cash and Marketable Securities

31.4

$

26.7

$

34.3

$

Total Debt

555.0

$

594.0

$

893.0

$

Leverage

3.8x

4.1x

4.6x

(1) 2005 reflects the three months ended December 31, 2005 only. 2006 excludes the impact of asset sales.

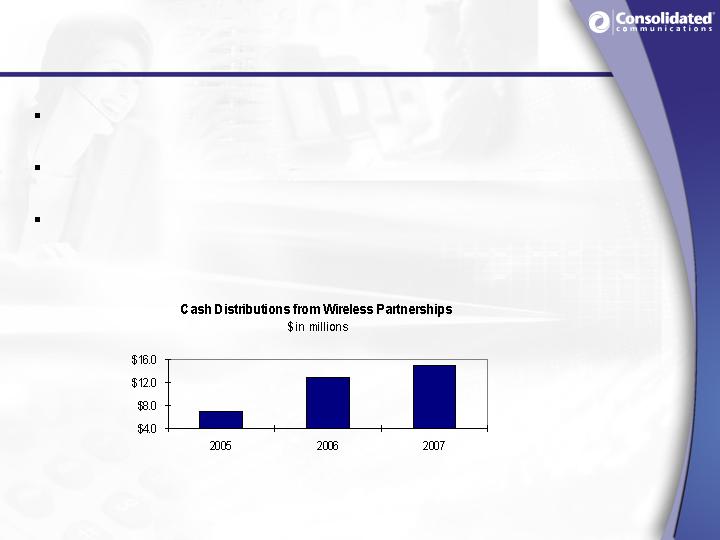

Wireless Partnerships

In addition to its core business, CNSL derives a portion of its cash

flow from five wireless partnerships.

All are managed by Verizon Wireless and overlap with our ILEC and

CLEC markets

All have experienced solid revenue, operating income, cash

distribution and subscriber growth over the past few years

17

Integration Update

Integration efforts well underway

Six major projects being worked

Most will be completed in 2008

Financial system consolidation complete and IPTV launch

scheduled for Q2 2008

Synergy estimates:

Op Ex: $7M in 2008 & $11M in 2009

Cap Ex: $3M in 2008 & $6M in 2009

18

Investment Highlights

Attractive Markets

Stable Local

Telephone Business

Bundled

Service Offerings

Favorable

Regulatory

Environment

Technologically

Advanced Network

Experienced

Management Team

19

Appendix

20

GAAP Reconciliation

21

GAAP Reconciliation (con’t)

22

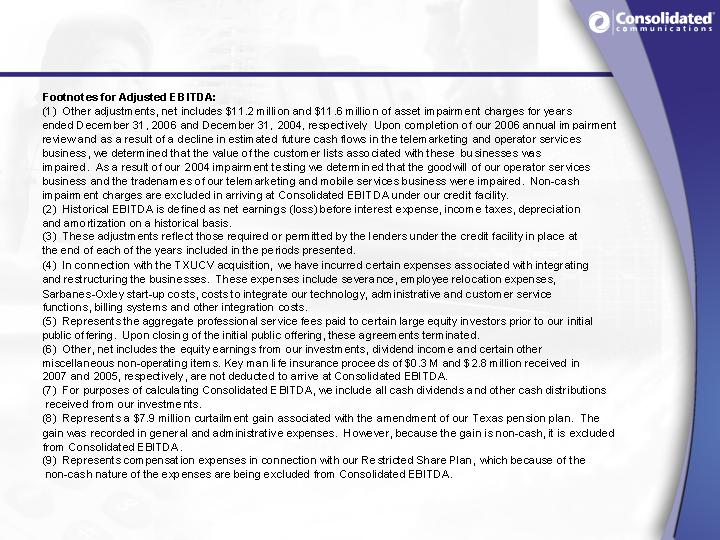

Adjusted EBITDA Reconciliation

See footnotes on next page

23

($ in millions)

CNSL

2005

2006

2007

Historical EBITDA:

Net cash provided by operating activities

72,475

$

84,593

$

82,069

$

Adjustments:

Pension curtailment gain

7,880

-

-

Compensation from restricted share plan

(8,590)

(2,482)

(4,034)

Other adjustments, net (1)

(19,068)

(8,083)

(3,781)

Changes in operating assets and liabilities

10,220

6,669

2,828

Interest expense, net

53,443

42,899

56,780

Income taxes

10,935

405

4,674

Historical EBITDA (2)

127,295

124,001

138,536

Adjustments to EBITDA (3)

Integration, restructuring and Sarbanes-Oxley (4)

7,400

3,684

1,187

Professional service fees (5)

2,867

-

-

Other, net (6)

(3,036)

(7,143)

(6,567)

Investment distributions (7)

1,590

5,516

6,586

Pension curtailment gain (8)

(7,880)

-

-

Intangible assets impairment (1)

-

11,240

-

Non-cash compensation (9)

8,590

2,482

4,034

Adjusted EBITDA

136,826

$

139,780

$

143,776

$

Year Ended

December 31,

Adjusted EBITDA Reconciliation

24

Adjusted EBITDA Reconciliation

See footnotes on next page

25

($ in millions)

NPSI

2005

2006

2007

Historical EBITDA:

Net cash provided by operating activities

32,723

$

13,863

$

9,771

$

Adjustments:

Curtailment and special termination benefits

-

-

(9,786)

Equity income of affiliated companies

6,001

8,623

9,944

Other adjustments, net

2,695

1,283

89

Changes in operating assets and liabilities

(423)

1,491

6,528

Interest expense, net

182

(1,144)

(1,146)

Income taxes

15,407

22,473

5,352

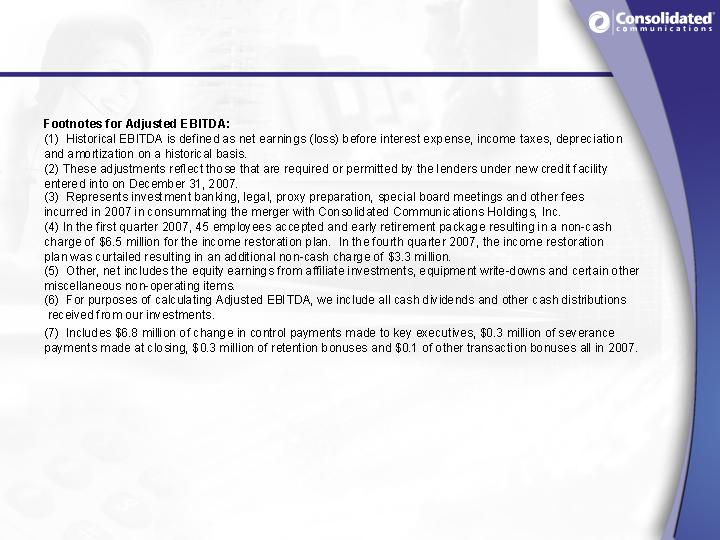

Historical EBITDA (1)

56,585

46,589

20,752

Adjustments to EBITDA (2)

Merger costs (3)

-

-

5,817

Curtailment expense (4)

-

-

9,786

Other, net (5)

(7,093)

(8,510)

(9,644)

Investment distributions (6)

6,177

8,087

8,972

Change of control, retention, severance and

-

-

-

other merger related payments (7)

-

-

7,482

Adjusted EBITDA

55,669

$

46,166

$

43,165

$

Year Ended

December 31,

Adjusted EBITDA Reconciliation

26

Cash Available to Pay Dividends

27

($ in millions)

2005

2006

2007

Adjusted EBITDA

35,626

$

139,780

$

143,776

$

- Cash interest expense

(9,384)

(40,613)

(44,222)

- Capital Expenditures

(9,498)

(33,388)

(33,495)

+ Proceeds from asset sales

(1)

-

6,594

-

- Cash income taxes

(172)

(8,237)

(13,976)

+ Cash interest income

174

745

893

��

- Repurchases of stock

(2)

-

(87)

-

Cash available to pay dividends

16,746

$

64,794

$

52,976

$

Quarterly Dividend

11,537

$

44,593

$

40,195

$

Payout Ratio

68.9%

68.8%

75.9%

Adjusted Payout Ratio

(3)

68.9%

76.6%

75.9%

(1) Represents $673 of proceeds from the sale of idle property and $5,921 of proceeds from the redemption of class C

shares of RTB stock.

(2) Represents the cancellation of stock by employees to pay withholding tax on shares vesting under the company's

Long Term Incentive Plan.

(3) Represents the payout ratio excluding the effect of asset sales.

Year Ended December 31,

Total Net Debt to Adjusted EBITDA Ratio

28

($ in millions)

2005

2006

2007

Summary of Outstanding Debt

Senior Notes

130,000

$

130,000

$

130,000

$

Term loan

425,000

464,000

760,000

Capital Leases

-

-

2,646

Total debt as of December 31, 2007

555,000

$

594,000

$

892,646

$

Less cash on hand

(31,409)

(26,672)

(37,297)

Total net debt

523,591

$

567,328

$

855,349

$

Adjusted EBITDA (1)

136,826

$

139,780

$

187,000

$

Total Net Debt to Adjusted EBITDA

3.8

4.1

4.6

(1) Per the new credit facility adjusted EBITDA has been agreed upon for the first three quarters of 2007 at

$138,700 and reflects a combined pro forma number for the fourth quarter 2007. Adjusted EBITDA for the

fourth quarter 2007 is the sum of $11,264 for the Pennsylvania operations and $37,036 for the Illinois and

Texas operations.

Year Ended December 31,