| Ashland Inc. | |

J. Kevin Willis Senior Vice President and Chief Financial Officer | 50 E. RiverCenter Blvd., P. O. Box 391 Covington, KY 41012-0391 Tel: 859 815 3871, Fax: 859 815 5895 |

April 4, 2014

CONFIDENTIAL TREATMENT OF CERTAIN DESIGNATED PORTIONS OF APPENDIX A TO THIS LETTER HAS BEEN REQUESTED BY ASHLAND INC. PURSUANT TO RULE 83. SUCH CONFIDENTIAL PORTIONS HAVE BEEN OMITTED, AS INDICATED BY [***], AND SUPPLEMENTALLY SUBMITTED UNDER SEPARATE COVER TO THE COMMISSION.

Mr. Terence O’Brien

Accounting Branch Chief

United States Securities and Exchange Commission

Division of Corporation Finance

100 F Street, N.E.

Washington, DC 20549

Ashland Inc.

Form 10-K for the Year Ended September 30, 2013

Filed November 27, 2013

Form 10-Q for the Period Ended December 31, 2013

Filed January 30, 2014

File No. 1-32532

Dear Mr. O’Brien:

Set forth below are responses from Ashland Inc. (“Ashland” or “we”) to the comments (the “Comments”) of the staff (the “Staff”) of the United States Securities and Exchange Commission (the “SEC”), dated March 19, 2014, concerning Ashland’s Annual Report on Form 10-K for the fiscal year ended September 30, 2013 and Ashland’s Quarterly Report on Form 10-Q for the period ended December 31, 2013.

For your convenience, the responses set forth below have been put in the same order as the Comments were presented and repeat each Comment prior to the response. The Comments are highlighted in bold.

FORM 10-K FOR THE YEAR ENDED SEPTEMBER 30, 2013

General

Comment 1

Where a comment below requests additional disclosures or other revisions to be made, please show us in your supplemental response what the revisions will look like. These revisions should be included in your future filings, including your interim filings, if applicable.

Confidential Treatment

Requested by Ashland Inc.

ASH-001

U.S. Securities and Exchange Commission

April 4, 2014

Page 2

Response 1

Where a comment below requests that additional disclosures or other revisions be made, we have included a draft of the disclosures or revisions within our responses. We will also include such disclosures or revisions in our future filings, including interim filings, as applicable, consistent with the responses outlined below.

Management’s Discussion and Analysis (MD&A)

Out of Period Adjustments, page M-18

Comment 2

Fiscal year 2013 included inventory valuation charges related to the Elastomers line of business of approximately $20 million, of which $12 million related to 2012 and $8 million related to 2013. We also note you determined that you had a material weakness as a result of not maintaining effective internal controls over the valuation of inventory for the Elastomers line of business. Given that the $12 million related to 2012 represents approximately 86% of the loss from continuing operations before income taxes for 2012, please help us understand how you determined it was appropriate to record this adjustment amount in 2013. Please provide us with your materiality analysis pursuant to SAB Topics 1:M and 1:N.

Response 2

We have noted your request to assist you in understanding our determination that it was appropriate to record the $12 million inventory valuation charge relating to 2012 in our financial results for the year ended September 30, 2013. The following response is intended to provide an understanding of the quantitative and qualitative evaluation process Ashland performed for the years ended September 30, 2012 and 2013. Additionally, as requested, Appendix A includes a discussion of our quantitative and qualitative analysis of materiality for the years ended September 30, 2012 and 2013 related to the $12 million inventory valuation error pursuant to SAB Topics 1-M and 1-N.

When assessing the effect an error has on the financial statements Ashland’s process is to initially review the effect of the error on its significant financial statement captions for the period in which the transaction should have been reported. In this case, the analysis focused on the significant captions within the Statement of Consolidated Comprehensive Income (including income (loss) from continuing operations before income taxes, income from continuing operations and net income) and other financial metrics (EBITDA).

When analyzing the significance of an error, Ashland’s process is to evaluate the quantitative and qualitative materiality of an error to its financial results (1) as reported in accordance with accounting principles generally accepted in the United States of America (“U.S. GAAP”) and (2) as adjusted for what Ashland refers to as “key items”. Management believes that adjusting the reported U.S. GAAP results for these key items on a consolidated and business segment basis assists investors in understanding the ongoing operating performance by presenting comparable financial results between periods. The key items considered in the analysis of errors are the same adjustments referenced within Ashland’s disclosures in the “Use of Non-GAAP measures” section on page M-6 of the 2013 Form 10-K.

Confidential Treatment

Requested by Ashland Inc.

ASH-002

U.S. Securities and Exchange Commission

April 4, 2014

Page 3

The year ended September 30, 2012 included several key items that substantially affected the U.S. GAAP reported amounts. For example, after adjusting for these key items, in fiscal year 2012, Ashland’s adjusted income from continuing operations before income taxes was $714 million, compared to the U.S. GAAP reported loss from continuing operations before income taxes of $14 million. The most significant key item was the pre-tax actuarial loss of $493 million on the annual pension and other postretirement plan remeasurement recorded in the fourth quarter of 2012. Ashland disclosed its consideration of excluding the actuarial gains and losses as a result of remeasurement of pension and other postretirement liabilities in calculating its non-GAAP measures on page M-6 of the 2013 Form 10-K. Although the $12 million inventory valuation error represented 86% of Ashland’s reported loss from continuing operations before income taxes in 2012 Ashland determined that the effect of the inventory valuation error related to the year ended September 30, 2012 represented between 1% and 2% of the significant financial statement captions and metrics, after adjusting the U.S. GAAP reported results for key items.

The next step in Ashland’s assessment was to add this error into its existing materiality analysis for 2012 and assess in aggregate all errors that impacted the financial results for the year ended September 30, 2012 on a quantitative and qualitative basis, in accordance with the guidance within SAB Topics 1-M and 1-N. In completing this analysis, on a quantitative basis the inventory valuation error of $12 million, in aggregate with the other previously identified errors, was between 1% and 2% of the adjusted significant financial statement captions and metrics previously noted.

In addition, Ashland completed a qualitative evaluation of the errors on its financial results for the year ended September 30, 2012 considering the criteria outlined in SAB Topic 1-M. Some of the qualitative factors that Ashland considered during its assessment were as follows:

| · | Whether the error impacted a trend in earnings |

| · | Whether the error related to a business that is significant to Ashland’s current or future financial results |

| · | Whether disclosure of the quantitative error is likely to result in a significant positive or negative market reaction |

| · | Whether the misstatement was intentional |

| · | Whether the misstatement arises from an item capable of precise measurement or whether it arises from an estimate and, if so, the degree of imprecision inherent in the estimate |

| · | Whether the misstatement hides a failure to meet analysts’ consensus expectations for the enterprise |

| · | Whether the misstatement changes a loss into income or vice versa |

| · | Whether the misstatement affects the registrant’s compliance with regulatory, loan covenants or other contractual requirements |

| · | Whether the misstatement has the effect of increasing management’s compensation |

| · | Whether the misstatement involves concealment of an unlawful transaction |

Based on the quantitative and qualitative analysis of materiality, Ashland determined that the $12 million inventory valuation error, along with the adjustments that had previously been identified, were not material to the financial statements for the year ended September 30, 2012. As noted above, further information related to our evaluation is included in Appendix A.

Following the quantitative and qualitative evaluation of materiality for the year ended September 30, 2012, Ashland completed a similar quantitative and qualitative analysis for the year ended September 30, 2013 to determine whether recording the error as an “out of period” adjustment in the year ended September 30, 2013 would materially impact the period of correction. As the impact of the $12 million inventory valuation error constituted 2% or less of the significant financial statement captions and metrics (adjusted for key items) noted above, the error correction was recorded in the year ended September 30, 2013 and disclosed in the 2013 Form 10-K.

Confidential Treatment

Requested by Ashland Inc.

ASH-003

U.S. Securities and Exchange Commission

April 4, 2014

Page 4

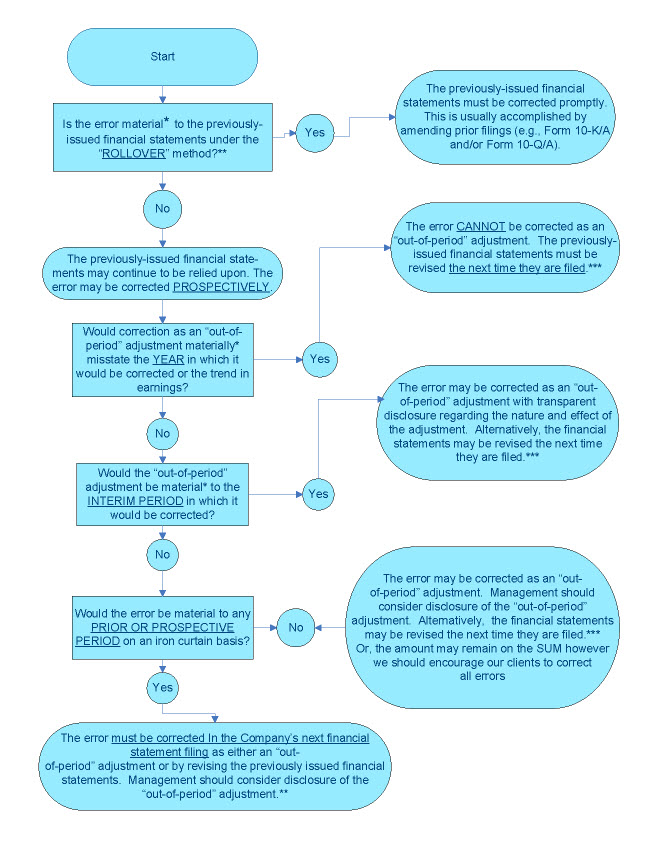

As an additional guide to assist and aid in your understanding of our decision making process concerning Ashland’s assessment of financial reporting errors identified after the financial statements have been issued, we have included as Appendix B the decision tree that graphically depicts the process that we follow on these types of issues.

Critical Accounting Policies

Employee Benefit Obligations, page M-31

Comment 3

As you note, operating income for each period has been significantly affected by the immediate recognition of the change in the fair value of plan assets and net actuarial gains and losses for defined benefit pension plans and other postretirement benefit plans. For 2013, you recorded a gain of $498 million compared to operating income of $1.2 billion. In this regard, please address the following:

| · | Please expand your disclosures to better explain the specific factors that resulted in the gain amount recorded during 2013. In this regard, your disclosures on page M-32 indicate that the gain was primarily attributable to the change in discount rate and other actuarial assumptions. We note that the discount rate used to determine your expense for 2013 decreased from 4.76% for 2012 to 3.70% in 2013. As you show in your table on page M-33, a decrease in the discount rate would typically result in an increase in pension costs rather than a decrease in pension costs. Please advise and correspondingly expand your disclosures; and |

| · | During 2013, you elected to use the above mean yield curve which resulted in higher discount rates than if you had used the prior yield curve. Please help us better understand the differences between the two yield curves used and your basis for changing the yield curve used. |

Response 3

We have noted your comment on our disclosure related to the specific factors that resulted in the actuarial gain for pension and other postretirement plans of $498 million recorded during the year ended September 30, 2013, particularly in light of the discount rates noted in your comment.

There are generally two significant components to the pension and other postretirement benefit costs recognized in Ashland’s Consolidated Statement of Comprehensive Income for a given year:

| ● | Pension and other postretirement costs recorded during the year – Ashland records the following elements of pension and other postretirement costs throughout the year based on actuarial assumptions which are established at the beginning of a given year: service cost, interest cost, amortization of prior service cost (credit) and expected return on plan assets (applicable only to pension cost, as other postretirement benefit plans are unfunded). |

Confidential Treatment

Requested by Ashland Inc.

ASH-004

U.S. Securities and Exchange Commission

April 4, 2014

Page 5

The weighted average discount rates of 4.76% for 2012 and 3.70% for 2013 were used to determine the pension costs recognized during the interim periods for the years ended September 30, 2012 and 2013, respectively. |

| ● | Actuarial gains and losses – Subsequent to the change in accounting policy during the year ended September 30, 2011 disclosed on pages M-31 and F-10 of the 2013 Form 10-K, Ashland immediately recognizes actuarial gains and losses in conjunction with the annual remeasurement or a qualifying remeasurement of pension and other postretirement benefits. |

The liabilities for pension and other postretirement benefits are remeasured in accordance with U.S. GAAP (ASC 715-30-35-62 through 68) using discount rates as of the measurement date with any actuarial gains or losses being immediately recognized in the Consolidated Statement of Comprehensive Income. As of September 30, 2013 and 2012, the pension obligation was remeasured using weighted-average discount rates of 4.68% and 3.70%, respectively. The 98 basis point increase in the discount rate between September 30, 2012 and 2013 was the primary driver of the $498 million gain recognized in the year ended September 30, 2013. The other components of the gain are disclosed in the table included at the top of page M-32 in the 2013 Form 10-K. |

In future filings, we will enhance the disclosure within the MD&A under the Critical Accounting Policies – Employee benefit obligations section as follows:

“Ashland’s expense, excluding actuarial gains and losses, for both U.S. and non-U.S. pension plans is determined using the weighted-average discount rate as of the beginning of the fiscal year, which were 3.70%, 4.76% and 5.01% measured at September 30, 2012, 2011 and 2010, respectively. The weighted-average discount rates used for the postretirement health and life plans were 3.23%, 4.39% and 4.68% measured at September 30, 2012, 2011 and 2010, respectively. The actuarial gains and losses recognized within the Statements of Consolidated Comprehensive Income are calculated using updated actuarial assumptions (including discount rates) as of the measurement date, which for Ashland is the end of the fiscal year, unless a plan qualifies for a remeasurement during the year. The weighted-average discount rate at the end of fiscal year 2013 was 4.68% for the pension plans and 4.28% for the postretirement health and life plans. These rates will also be used to determine the fiscal 2014 pension and other postretirement plans expense that is recognized quarterly during the fiscal year.”

We have also noted your request for additional insight on the differences between the above mean yield curve and prior yield curve used by Ashland and the basis for changing the yield curve used in valuing our U.S. pension and other postretirement obligations as of September 30, 2013. Ashland’s discount rate is based on an actuarially-developed yield curve using only high-quality corporate bonds as disclosed on page M-32 of our 2013 Form 10-K. The range of discount rates disclosed on page M-32 of our 2013 Form 10-K filing presents the range of plan-specific discount rates, based on the above mean yield curve and prior yield curve, applicable to each U.S. pension and other postretirement plan. The U.S. pension plans’ obligations, which at September 30, 2013 represented 82% of the projected benefit obligation, consist primarily of one U.S. qualified pension plan for which the discount rate as of September 30, 2013 was 4.86% using the above mean yield curve. The comparable discount rate as of September 30, 2013, had Ashland continued to use the prior yield curve, would have been 4.53%, resulting in a 33 basis point difference. An increase in the discount rate of 33 basis points for this plan resulted in income of approximately $135 million, which is approximately 27% of the actuarial gain Ashland recognized in fiscal year 2013.

Confidential Treatment

Requested by Ashland Inc.

ASH-005

U.S. Securities and Exchange Commission

April 4, 2014

Page 6

The prior yield curve was constructed using a population of AA quality bonds meeting certain size and maturity characteristics. The above mean yield curve is constructed in the same manner, however, it uses only bonds in the population that had above average yields for their maturity. Both the above mean yield curve and prior yield curve are prepared by Ashland’s external actuary and used by Ashland and other peer companies. The above mean yield curve was initially introduced by our external actuary in November 2012, making the September 30, 2013 measurement date the first date the above mean yield curve was available for Ashland to consider. As part of Ashland’s annual review of the pension and other postretirement plans assumptions, Ashland consulted with our external actuary to determine if the above mean yield curve produced a more refined estimate of the discount rate and ultimately resulted in a better estimate of Ashland’s benefit obligations. Based on these discussions, Ashland concluded that the use of the above mean yield curve resulted in a better estimate of the rate at which Ashland could effectively settle the pension and other postretirement plans obligations within the current interest rate environment. In addition, the above mean yield curve is an established benchmark rate that is used by other peer companies. As a result of these factors and discussions with our external actuary, Ashland determined it was appropriate to use the above mean yield curve for the September 30, 2013 measurement date.

Comment 4

Please also include the expected rate of return in your table showing the impact of a one percentage point change in assumptions related to pension and postretirement expense.

Response 4

We have noted your comment for additional disclosure on the impact of a one percentage point change in the expected rate of return assumptions related to pension and other postretirement expense. We will adjust our disclosures in future Form 10-K filings to include this information for pension expense only since Ashland’s other postretirement plans are unfunded and there are no assets associated with these plans. The following is an example of our suggested revised table for the three years ended September 30, 2013.

| (In millions) | 2013 | 2012 | 2011 | |||||||||

| Increase in pension costs from | ||||||||||||

| Decrease in the discount rate | $ | 557 | $ | 707 | $ | 498 | ||||||

| Increase in the salary adjustment rate | 44 | 54 | 50 | |||||||||

| Decrease in expected return on plan assets | 33 | 29 | 29 | |||||||||

| Increase in other postretirement costs from | ||||||||||||

| Decrease in the discount rate | 20 | 26 | 27 | |||||||||

Confidential Treatment

Requested by Ashland Inc.

ASH-006

U.S. Securities and Exchange Commission

April 4, 2014

Page 7

Goodwill, page M-29

Comment 5

Please help us better understand how you determined what your reporting units are pursuant to ASC 350-20-35-33 through 35-38, including if you are aggregating components of an operating segment to arrive at your reporting units. It appears that certain of your operating segments consist of multiple businesses. For example, we note the Elastomers business within the Performance Materials operating segment and the guar-based products business within the Specialty Ingredients operating segment. We also note that certain businesses within the Performance Materials operating segment represent separate reporting units. Please help us understand why all businesses within an operating segment do not in a similar manner reflect separate reporting units.

Response 5

We have noted your request to better understand our reporting units pursuant to ASC 350-20-35-33 through 35-38, including if components of an operating segment are aggregated in arriving at our reporting units. We have also noted that you have requested to understand why all businesses within an operating segment do not, in a similar manner, reflect separate reporting units.

Ashland’s process for identifying reporting units consists of first reviewing our determination of operating segments based on the guidance in ASC 280-10-50-1 through 50-10. Once this initial process is completed, Ashland then assesses its operating segments and the components one level below an operating segment to determine which may qualify for classification as reporting units based on the provisions within ASC 350-20-35-33 through 35-38. Once Ashland has determined its operating segments and reporting units, the conclusions from this assessment are monitored quarterly to ensure changes within the operations of segments have not resulted in changes to these previous determinations.

Ashland has not aggregated components of an operating segment in arriving at its reporting units. Within the Performance Materials operating segment, Ashland has determined that the following two components constitute reporting units: (1) Composites and Adhesives and (2) Elastomers. In assessing these provisions in U.S. GAAP, Ashland noted specifically that each component complied with the provisions of ASC 350-20-35-34, whereby each component constitutes a business (as defined in ASC 805-10-55-4 to 805-10-55-9), Ashland prepares discrete financial information for each component and that segment management (President, Ashland Performance Materials – who reports to the Chief Operating Decision Maker) reviews this financial information on a regular basis.

A key factor in determining that each of the components within Performance Materials meets the definition of a business and therefore, a reporting unit was the presence of key inputs including different intellectual property for each component and the presence of separate and dedicated manufacturing facilities. In addition, Ashland determined that the two reporting units within the Performance Materials operating segment did not qualify for aggregation pursuant to ASC 350-20-35-35 as they do not have similar economic characteristics.

Specifically, the Elastomers business was part of Ashland’s purchase of International Specialty Products Inc. (“ISP”) in August 2011. Ashland purchased ISP for its core specialty chemicals business and combined the core specialty chemicals business with Ashland’s Functional Ingredients business, so it could be managed together in order to take advantage of multiple synergy opportunities within the specialty chemical market. The remaining business from ISP was the Elastomers business, consisting of one plant that primarily produces emulsion styrene butadiene rubber (“eSBR”) for sale to replacement tire manufacturers. The commodity nature of Elastomers products and related margin volatility of this business does not fit Ashland’s overall strategic objectives for its core businesses. As such, the Elastomers business was thought to be a potential divestiture candidate at the right time for Ashland, after assessing the business for value creation opportunities. As a result, the Elastomers business has not been fully integrated into Ashland’s operating model and was included within the Performance Materials operating segment, where the management team had experience and expertise in managing more commoditized businesses.

Confidential Treatment

Requested by Ashland Inc.

ASH-007

U.S. Securities and Exchange Commission

April 4, 2014

Page 8

Within Ashland’s other operating segments, the level below the operating segment is focused on end-use markets, industries or distribution channels served by the operating segment. In contrast to the components within Performance Materials outlined above, the components one level below the other operating segments share significant raw materials, manufacturing facilities and intellectual property. Additionally, common products are sold across the components within each operating segment. In evaluating these components versus the requirements of ASC 350-20-35-34, Ashland concluded that these components do not qualify as reporting units, as they do not meet the definition of a business pursuant to ASC 805-10-55-4, given the significant inputs and processes shared across the various components.

In addition, your comment referenced Ashland’s guar-based products business within our Specialty Ingredients operating segment. Our use of the term “business” on page M-14 in the 2013 Form 10-K to describe Ashland’s guar-based products was not used in the context of ASC 805-10-55-4, but was a “plain English” use of the term. Guar-based products are sold across multiple end-use markets that form the basis for the level below the operating segment in Specialty Ingredients. Ashland generally does not disclose information at a product level, but felt that the impact of the change in prices on guar-based products was so significant that transparent, product-based disclosure was required in this instance for a better understanding of this reportable segment’s overall financial performance within the period and future trends in earnings.

FORM 10-Q FOR THE PERIOD ENDED DECEMBER 31, 2013

Management’s Discussion and Analysis

Key Developments

Divestitures, page 27

Comment 6

During the quarter ended December 31, 2013, you announced a formal sale process is currently undergoing for both Water Technologies and the Elastomers business. Please tell us what consideration you gave to ASC 205-20 and ASC 360-10-45-9 in determining whether these businesses should be reflected as assets held for sale and correspondingly discontinued operations.

Response 6

We have noted your request to outline the considerations Ashland gave to ASC 205-20 and ASC 360-10-45-9 in determining whether the Water Technologies and Elastomers businesses should be presented as assets held for sale and discontinued operations within Ashland’s consolidated financial statements as of December 31, 2013. Ashland’s process when going through a divestiture is to analyze the provisions of ASC 360-10-45-9 in a checklist format to verify if the held for sale treatment has been reached, and if so, classify the applicable assets and liabilities as “Held for Sale” within the Consolidated Balance Sheet and likewise classify the applicable revenue and expenses within the “Discontinued Operations” caption in the Statement of Consolidated Comprehensive Income should a component of Ashland qualify for this method of presentation consistent with the provisions within ASC 205-20.

Confidential Treatment

Requested by Ashland Inc.

ASH-008

U.S. Securities and Exchange Commission

April 4, 2014

Page 9

Specifically for our assessment during the quarter ended December 31, 2013 for the Water Technologies and Elastomers businesses, Ashland determined that the requirements of ASC 360-10-45-9(a),(d) and (f) were not met as of December 31, 2013. In addition, Ashland determined that the Elastomers business also did not meet ASC 360-10-45-9(e).

As of December 31, 2013, Ashland was not formally committed to a plan to sell either business as required under ASC 360-10-45-9(a) as the divestiture process for each had not yet advanced to the point where the Board of Directors had approved a formal plan to commit the assets to sale. In addition, consistent with historical treatment on the classification and presentation of divestitures, Ashland concluded that it was not “probable” as of December 31, 2013 that the transfer of assets for recognition as a completed sale would occur within one year. In its previous divestitures, Ashland’s practice in applying ASC 360-10-45-9(d) has been to wait until a formal sale agreement has been entered into in order to cross the “probable” threshold of when the assets will be disposed, thereby qualifying for presentation as “Held for Sale.” Likewise, in assessing the requirement of ASC 360-10-45-9(f), Ashland concluded that there was a possibility of significant changes being made to the divestiture process as of December 31, 2013 due to the fluid nature of negotiations with multiple potential buyers and other aspects within the ongoing divestiture process such as due diligence, financing and market dynamics. Additionally, ASC 360-10-45-9(e) was not met due to an unusual and unforeseen development within the Elastomers marketplace that caused Ashland to cease actively marketing the business for sale prior to December 31, 2013 until implications of a competitor’s potential exit from the market could be more fully understood.

Ashland entered into an agreement to sell the Water Technologies business in February 2014 following solicitation of a final round of bids from multiple potential buyers and negotiation of the purchase agreement during the month. Ashland has concluded that the criteria outlined in ASC 360-10-45-9 have been met in the quarter ended March 31, 2014. As such, Ashland will classify the qualifying Water Technologies assets and liabilities as “Held for Sale” within the Consolidated Balance Sheet as of March 31, 2014 and in the comparative balance sheet for September 30, 2013. Furthermore, Ashland has concluded that the Water Technologies business meets the definition of a component. As a result of the divestiture, the operations and cash flows of the Water Technologies business will be eliminated from Ashland’s continuing operations and Ashland will not have any significant continuing involvement in the Water Technologies business. Thus, pursuant to the guidance in ASC 205-20, the qualifying revenue and expenses will be classified within the “Discontinued Operations” caption in the Statement of Consolidated Comprehensive Income for the three and six month periods ended March 31, 2014 and all prior and future reporting periods.

Global Restructuring, page 27

Comment 7

Please help us better understand the impact the restructuring will have on your operating and reportable segments pursuant to ASC 280. In this regard, we note that you will have three commercial units, which will consist of Specialty Ingredients, Performance Materials, and Valvoline. Specialty Ingredients will be organized in two businesses while Performance Materials will comprise of three businesses. Please also revise your disclosures to better explain how you determine your reportable segments, including whether operating segments have been aggregated. Refer to ASC 280-10-50-21(a).

Confidential Treatment

Requested by Ashland Inc.

ASH-009

U.S. Securities and Exchange Commission

April 4, 2014

Page 10

Response 7

We have noted your request to more fully understand the effect Ashland’s ongoing restructuring will have regarding our operating and reportable segments. Implementation of Ashland’s restructuring process and activities are ongoing in many areas as of the date of this response, including activities such as finalizing the organizational design and defining roles and responsibilities within the commercial units and supporting functional administrative groups. In addition, Ashland is identifying and determining the financial information that these new organizations are anticipating they will require to monitor operational performance. We currently anticipate being able to externally report our financial results under the restructured reporting structure in the quarter ending June 30, 2014. Since this process is still ongoing and certain aspects and information needed to assess operating segments, reportable segments and reporting units, as required under U.S. GAAP, have not yet been fully created or identified, Ashland is not able to fully conclude at this time an exact determination of its operating segments, reportable segments and reporting units under this new structure. Once we have completed our ongoing restructuring process, we fully intend to disclose our determination of the new operating and reporting segment structure and the manner in which Ashland reached these conclusions.

Ashland anticipates that initially the new organization will most likely consist of three operating and reportable segments: Specialty Ingredients, Performance Materials and Valvoline. However, it currently is not possible for Ashland to further assess if discrete financial information will be available or if its chief operating decision maker will make decisions on resources for other components below these operating segments that will allow another component to qualify under ASC 280-10-50-1 as an operating segment. Ashland does anticipate more detailed financial information on various components of the newly restructured operating segments to continually be developed to the point that the related U.S. GAAP provisions will need to be evaluated to eventually determine if the three operating segments should or could be further divided and what additional operating segments or reporting units may be identified. However, Ashland does not expect the information to complete this assessment to be available during the year ending September 30, 2014 based on its current internal process surrounding operational management, utilization of resources and organizational structure, as well as the initial financial reporting metrics and information available.

We also noted your request that Ashland revise our disclosures regarding how reportable segments are determined, including whether operating segments have been aggregated in accordance with the provisions contained within ASC 280-10-50-21(a). In future filings we will expand our disclosures within Note Q “Segment Information” of the 2013 Form 10-K to include the explanation prescribed within ASC 280-10-50-21(a) as follows:

“Ashland determines its reportable segments based on how operations are managed internally for the products and services sold to customers and does not aggregate operating segments to arrive at these reportable segments.”

******

Ashland acknowledges that it is responsible for the adequacy and accuracy of the disclosure in the filing; that the Staff’s comments or changes to disclosure in response to the Staff’s comments do not foreclose the SEC from taking any action with respect to the filing; and that Ashland may not assert the Staff’s comments as a defense in any proceeding initiated by the SEC or any person under the federal securities laws of the United States.

Confidential Treatment

Requested by Ashland Inc.

ASH-010

U.S. Securities and Exchange Commission

April 4, 2014

Page 11

We believe that the information contained in this letter is responsive to the Comments in the Comment Letter.

Please acknowledge receipt of this response letter by electronic confirmation.

Please call Michael S. Roe, Assistant General Counsel, or Michael A. Meade, Assistant Controller, at (859) 815-3430 and (859) 815-3402, respectively, if you have any questions regarding this submission.

| Sincerely, | |||

| /s/ J. Kevin Willis | |||

J. Kevin Willis Senior Vice President and Chief Financial Officer | |||

cc: Nudrat Salik, Staff Accountant

Confidential Treatment

Requested by Ashland Inc.

ASH-011

Appendix A

Ashland Inc. (“Ashland,” the “Company” or “we”) considered the following quantitative and qualitative factors in evaluating the materiality of the $12 million inventory valuation charge related to the Elastomers business for the years ended September 30, 2012 (“FY 2012”) and 2013 (“FY 2013”).

During the FY 2013 Form 10-K reporting process, the conclusions in Ashland’s summarized SAB Topic 1-M / 1-N analysis for FY 2012 and FY 2013 below were reviewed with the Company’s external securities counsel, Cravath, Swaine & Moore LLP and with the Company’s Audit Committee and following that review, with our independent auditors, PricewaterhouseCoopers LLC.

The pre-tax amount of the errors included in the quantitative analysis of materiality includes all errors or out-of-period adjustments identified related to the years ended September 30, 2012 and 2013. The $12 million inventory valuation charge related to the Elastomers business constitutes the vast majority of the total pre-tax errors of $13.2 million related to the year-ended September 30, 2012 and $13.3 million for the year-ended September 30, 2013.

Quantitative Analysis

The tables in Exhibit I and Exhibit II, respectively, set forth the impact of the inventory valuation error for the Elastomers business, as well as the impact for all identified errors or out-of-period adjustments, for FY 2012 and FY 2013 on an “as reported basis” for Ashland’s consolidated pre-tax income, income from continuing operations, net income and EBITDA. In assessing the error’s total effect as set forth in Exhibit I and II, Ashland concluded that certain captions on an “as reported basis” were significantly impacted by the error on a percentage basis.

A quantitatively large number may nonetheless be immaterial. This may be particularly the case in the context of a break-even or near break-even year. In that context, small or non-existent income may artificially distort the percentage impact of the misstatement, which is the case in this situation where a $12 million inventory valuation error constitutes 86% of Ashland’s reported loss from continuing operations before income taxes of $14 million in FY 2012. The Company believes that certain items included in its financial statements do not reflect the Company’s operating performance and, as a result, distort the impact of the inventory valuation error on its financial results. Accordingly, it is appropriate to adjust the Company’s reported results to reflect these non-operating items when assessing the materiality of the accounting misstatement.

In addition to reporting its financial statements in accordance with U.S. GAAP, Ashland publicly discloses financial information on a non-GAAP, “as adjusted basis” which excludes the impact of unusual, non-operational or restructuring-related activities. Ashland’s management uses these adjusted results in its own evaluation of business performance and believes the use of as adjusted measures on a consolidated and business segment basis assists investors in understanding Ashland’s ongoing operating performance by presenting comparable financial results between periods. Management’s viewpoint concerning what information is material to investors, and in particular management’s discussions with investors, are important factors to be considered in assessing an item’s materiality. In the context of assessing the inventory valuation errors in the Elastomers business, Ashland’s management believes that it is more appropriate to consider their impact on the Company’s “as adjusted” results rather than on its “as reported” results, especially given the near break-even “as reported” results in FY 2012. In the experience of Ashland’s management, the financial information about Ashland that is most significant to investors is adjusted EBITDA and adjusted income from continuing operations (on a pre-tax and after-tax basis). For FY 2012, the adjustments to income from continuing operations (pre-tax) included: (i) a $493 million actuarial loss on pension and other postretirement plan remeasurement, (ii) an $85 million charge related to restructuring and other integration costs, (iii) a $28 million inventory fair value charge related to stepped-up inventory values from the acquisition of International Specialty Products Inc. (“ISP”), (iv) a $13 million charge related to the impairment of in-process research and development assets, (v) an $8 million charge for environmental reserve adjustments, and (vi) a $7 million charge for asset impairment and accelerated depreciation. These adjustments are consistent with the Company’s practices, and Ashland’s management believes assessing the significance of the accounting errors after giving effect to these adjustments better reflects the impact of the misstatements on the operating performance of the Company.

Confidential Treatment

Requested by Ashland Inc.

ASH-012

The tables in Exhibit III and Exhibit IV, respectively, set forth the impact of the inventory valuation error for the Elastomers business, as well as the impact of all other identified but unrecorded accounting errors, for FY 2012 and FY 2013 on an “as adjusted basis” for Ashland’s consolidated pre-tax income, income from continuing operations, net income, and adjusted EBITDA. For FY 2012 and FY 2013, the inventory valuation errors and all other identified adjustments did not exceed 1.1% of EBITDA or 1.7% of adjusted income from continuing operations (see Exhibits III and IV).

Qualitative Analysis

SAB 99 states that: “quantifying in percentage terms, the magnitude of a misstatement is only the beginning of an analysis of materiality; it cannot appropriately be used as a substitute for a full analysis of all relevant considerations. Materiality concerns the significance of an item to users of a registrant’s financial statement. A matter is ‘material’ if there is substantial likelihood that a reasonable person would consider it important” or, put another way, if there is “a substantial likelihood that the…fact would have been viewed by the reasonable investor as having significantly altered the ‘total mix’ of information made available.” Moreover, even a large quantitative error can be immaterial based on the total mix of factors. The question is whether there is a substantial likelihood that the size of the error would have been viewed by the reasonable investor as having significantly altered the “total mix” of information available. Furthermore, when assessing an accounting error and the need to restate financial statements, it is appropriate to consider the needs of current investors.

The Elastomers business is not a core business

As noted above, the majority of the errors noted between FY 2012 and FY 2013 related to the Elastomers business. Therefore, Ashland evaluated the importance of the Elastomers business to the Company as a whole, as SAB 99 states that materiality may turn on where the misstatement appears in the financial statements. For example, in assessing materiality of a misstatement involving a segment of the registrant’s operations to the financial statements taken as a whole, registrants should consider not only the size of the misstatement but also the significance of the segment information to the financial statements taken as a whole. SAB 99 provides the example that a misstatement in “a relatively small segment that has been represented by management as important to the future profitability of the entity is more likely to be material to investors than a misstatement in a segment that management has not identified as especially important.” Although not expressly addressed in SAB 99, the reverse also should be true. A misstatement in a relatively small business that is not important to the future profitability of the Company is likely not to be material.

Confidential Treatment

Requested by Ashland Inc.

ASH-013

A-2

Ashland’s core business is its high margin specialty chemicals business. Ashland has been engaged in a multi-year transformation from a diversified industrial business whose holdings included a refining and marketing business, a road construction business and a chemicals distribution business, all of which have been divested over the last decade, to a high margin specialty chemicals business that was created primarily through acquisitions over the same period, including the acquisitions of Hercules Inc. (”Hercules”) in 2008 in a transaction valued at $3.3 billion and the acquisition of ISP in the fourth quarter of 2011 in a transaction valued at $3.2 billion. As a result of this series of acquisitions and divestitures, Ashland is today a leading specialty chemicals business and its Ashland Specialty Ingredients (“ASI”) commercial unit is its largest segment. Analysts that follow Ashland often refer to ASI as the Company’s “crown jewel” and as its core high margin specialty chemical segment.

ISP was a global specialty chemical manufacturer. Included in the acquisition was ISP’s relatively small, commodity Elastomers business. The Elastomers business is a supplier of high quality emulsion styrene butadiene rubber (“eSBR”), a raw material used primarily in the tire market, to the North American market. The Elastomers business was not consistent with the Company’s strategy of building a high margin specialty chemicals company. Following the acquisition, Ashland structured all the ISP business lines, except the Elastomers business, within the Company’s newly-formed specialty chemicals commercial unit, ASI. Elastomers became part of the Ashland Performance Materials (“APM”) commercial unit primarily because it was not a specialty chemicals business and its operations aligned best with those of APM. Both ASI and APM are financial reporting segments of Ashland.

As demonstrated in the tables below, the Elastomers business is a very small part of Ashland and is not, and has not been at any time since the acquisition, a material part of Ashland’s business. [***]. As noted in Table 2, APM has been Ashland’s smallest business segment with respect to sales and adjusted EBITDA in each of FY 2011 (pro forma), FY 2012 and FY 2013 (with the exception of adjusted EBITDA in FY 2012).

[***]

Confidential Treatment

Requested by Ashland Inc.

ASH-014

A-3

Table 2: Sales and Adjusted EBITDA for each of Ashland’s Reporting Segments

| (Dollars in millions) | FY 2011 (Pro forma)* | FY 2012 | FY 2013 | |||||||||

| SALES | ||||||||||||

| Specialty Ingredients | $ | 2,540 | $ | 2,878 | $ | 2,616 | ||||||

| As a % of Total Ashland | 31% | 35% | 33% | |||||||||

| Water Technologies | $ | 1,902 | $ | 1,734 | $ | 1,722 | ||||||

| As a % of Total Ashland | 23% | 21% | 22% | |||||||||

| Performance Materials | $ | 1,735 | $ | 1,560 | $ | 1,479 | ||||||

| As a % of Total Ashland | 22% | 19% | 19% | |||||||||

| Consumer Markets | $ | 1,971 | $ | 2,034 | $ | 1,996 | ||||||

| As a % of Total Ashland | 24% | 25% | 26% | |||||||||

| Adjusted EBITDA | ||||||||||||

| Specialty Ingredients | $ | 608 | $ | 763 | $ | 550 | ||||||

| As a % of Total Ashland | 51% | 57% | 47% | |||||||||

| Water Technologies | $ | 194 | $ | 149 | $ | 164 | ||||||

| As a % of Total Ashland | 17% | 11% | 14% | |||||||||

| Performance Materials | $ | 133 | $ | 159 | $ | 122 | ||||||

| As a % of Total Ashland | 11% | 12% | 11% | |||||||||

| Consumer Markets | $ | 251 | $ | 272 | $ | 330 | ||||||

| As a % of Total Ashland | 21% | 20% | 28% | |||||||||

* During 2011 Ashland included the operational results of the former ISP business within its reported operating results on a pro-forma basis. Ashland did not attempt to adjust these pro-forma results for any ongoing operational changes and these results are based on certain assumptions and policies that are not consistent with Ashland’s. Therefore, there are inherent limitations in utilizing this information but Ashland has included in order to enhance the understanding of the acquisition and its overall effect on the applicable businesses.

Confidential Treatment

Requested by Ashland Inc.

ASH-015

A-4

As noted above, the acquisition of ISP was motivated by a desire to acquire its high margin specialty chemicals business, not by a desire to acquire the commodity Elastomers business. At the time of the FY 2013 Form 10-K reporting process, when the materiality of this error was assessed, the Company had recently announced processes to sell its Water Technologies business and the Elastomers business as part of the Company’s continuing focus on its core high margin specialty chemicals business. Subsequently, Ashland ceased actively marketing the Elastomers business for sale until the implications of a competitor’s potential exit from the market could be more fully understood. That analysis is ongoing; however, Ashland’s management currently expects the sale process for the Elastomers business will resume at some point in FY 2014. In February 2014, the Company announced that it had entered into an agreement to sell its Water Technologies business for approximately $1.8 billion.

Since the time of the ISP acquisition, Elastomers also has been viewed by the investor and analyst community as a non-core business and a potential candidate for divestiture, and analysts and investors have frequently inquired with management as to when Ashland plans to sell the business. Examples of analyst sentiment and expectations regarding the Elastomers business include the following:

[***]

In this context, Ashland management believes that the quantitative errors related to the valuation of the inventory of a non-core business would not be viewed by investors as important or as significantly altering the mix of information available to them.

The Company is engaged in a process to sell the Elastomers business, and the business is expected to be treated as a discontinued operation during fiscal 2014

Historical accounting errors in discontinued businesses are not typically viewed by investors as important to either the current or future value of the business. Management believes that this same principle applies to errors in a business that is in the process of being sold, particularly in the context of a non-core business in the process of being sold. The Company announced in July 2013 that it was engaged in a process to sell the Elastomers business and disclosed that it expected to announce an agreement for the sale in the second fiscal quarter of 2014. At the time of the FY 2013 Form 10-K reporting process, when the materiality of this error was assessed, Ashland’s management expected the sale as well as discontinued operations classification to occur in the second fiscal quarter of 2014. Ashland’s management now expects that the Elastomers business will be reported as a discontinued operation some time in FY 2014. In this context, management believed and continues to believe that the quantitative errors related to the valuation of the inventory of a business that is soon to be sold and accounted for as discontinued would not be viewed by investors as important or as significantly altering the information available to them.

Confidential Treatment

Requested by Ashland Inc.

ASH-016

A-5

Disclosure of the quantitative errors is not likely to result in a significant positive or negative market reaction

SAB 99 notes that, although potential market reaction to disclosure of a misstatement is not by itself a measure of materiality, the expectation that a misstatement may result in a significant positive or negative market reaction should be taken into account when considering materiality. Although not expressly addressed in SAB 99, the converse should also be true. Given the non-core nature of the business, and the fact that at the time of the FY 2013 Form 10-K reporting process, when the materiality of this error was assessed, the Elastomers business was being actively marketed for sale, Ashland’s management believed that it was very unlikely there would be a significant market reaction to disclosure of these errors. Ashland’s management believed that these errors were not likely to be viewed as important or as significantly altering the mix of information that is available to investors. Subsequent to the November 2013 Form 10-K filing, Ashland has monitored its interaction with investors and analysts, noting no inquiries or questions about the treatment of the error have been received despite numerous investor and analyst interactions and meetings with Ashland’s management team.

The misstatement was not intentional

SAB 99 states that whether a misstatement was intentional may also provide evidence of materiality particularly in the context of an intentional misstatement for the purpose of managing earnings. The Elastomers inventory valuation adjustments were clearly not intentional but rather resulted primarily from a material weakness in internal controls over financial reporting in the application of lower of cost or market (LCM) inventory valuation procedures during a period when there was significant volatility in the price of butadiene. The acquisition and integration of the Elastomers business at the time of the ISP acquisition also was a contributing factor, including the fact that the Elastomers business was accounted for on a different IT platform than the rest of Ashland’s business. Ashland included disclosure concerning the material weakness in internal controls in Item 9A of the 2013 Form 10-K.

In addition, management considered the qualitative factors specifically identified by the SEC in SAB 99:

| · | whether the misstatement arises from an item capable of precise measurement or whether it arises from an estimate and, if so, the degree of imprecision inherent in the estimate |

| o | Analysis: The misstatements primarily arose as a result of a material weakness in internal controls over financial reporting in the application of LCM inventory valuation procedures. The Elastomers inventory valuation errors also arose at a time when the applicable raw material pricing was highly volatile and the inventory had recently written-up in value due to purchase accounting. |

| · | whether the misstatement masks a change in earnings or other trends |

| o | Analysis: The misstatements did not mask a change in earnings or other trends. The errors also did not have a significant impact on earnings as the effect for FY 2012 and FY 2013 from the Elastomers inventory valuation errors and all other identified adjustments did not exceed 1.1% of EBITDA or 1.7% of adjusted income from continuing operations (see Exhibits III and IV). |

Confidential Treatment

Requested by Ashland Inc.

ASH-017

A-6

| · | whether the misstatement hides a failure to meet analysts’ consensus expectations for the enterprise |

| o | Analysis: The Elastomers inventory misstatements did not hide a failure to meet analysts’ expectations. |

| · | whether the misstatement changes a loss into income or vice versa |

| o | Analysis: The misstatements in FY 2012 and FY 2013 did not change a loss into income or vice versa. |

| · | whether the misstatement concerns a segment or other portion of the registrant’s business that has been identified as playing a significant role in the registrant’s operations or profitability |

| o | Analysis: The Elastomers business line has not been, and is not now, a material part of Ashland’s operations or profitability for, among other things, the following reasons: |

| ▪ | The Elastomers business manufactures and sells eSBR primarily to the replacement tire market. This type of business has not played, and does not play, any role in Ashland’s specialty chemical business. | |

| ▪ | Elastomers was acquired as part of the ISP acquisition in August 2011. All of the other businesses that Ashland acquired from ISP were added to the newly named “Specialty Ingredients” commercial unit, except for Elastomers which was added to the Performance Materials commercial unit. | |

| ▪ | As discussed above, at the time of the FY 2013 Form 10-K reporting process, when the materiality of this error was assessed, Ashland had announced that it has commenced a sale process for Elastomers. Although the process is currently on hold, Ashland’s management currently expects the process to resume and the Elastomers business to be classified within discontinued operations during FY 2014 once the requirements of ASC 205-20 and ASC 360-10-45-9 are met. |

| · | whether the misstatement affects the registrant’s compliance with regulatory requirements |

| o | Analysis: The misstatements do not in any way affect Ashland’s compliance with regulatory requirements. |

| · | whether the misstatement affects the registrant’s compliance with loan covenants or other contractual requirements |

| o | Analysis: The Elastomers inventory errors did not affect Ashland’s compliance with its loan covenants or other contractual requirements in FY 2012 and FY 2013. |

Confidential Treatment

Requested by Ashland Inc.

ASH-018

A-7

| · | whether the misstatement has the effect of increasing management’s compensation – for example, by satisfying requirements for the award of bonuses or other forms of incentive compensation |

| o | Analysis: Management’s incentive compensation is primarily based on Ashland Inc.’s and/or the applicable operating segment’s operating income during the full fiscal year. The net effect of the Elastomers inventory misstatement was to decrease income from continuing operations by $12 million and $8 million during FY 2012 and FY 2013, respectively. These amounts represented approximately 1% of the adjusted operating income (the key segment measure for Ashland’s incentive compensation programs) during these fiscal periods. |

| · | whether the misstatement involves concealment of an unlawful transaction. |

| o | Analysis: The misstatements did not involve any unlawful transactions, including any concealment of unlawful transactions. |

Based on the foregoing analysis of qualitative factors, Ashland concluded there was not a substantial likelihood that the size of the inventory valuation errors would have been viewed by the reasonable investor as important or as having significantly altered the “total mix” of information available whether at the time of the errors or currently, and accordingly, that the inventory valuation errors are immaterial from a qualitative perspective.

Conclusion

Based on the foregoing analysis, Ashland did not believe the impact of correcting the errors related to the misstatements of pre-tax income, income from continuing operations, net income and EBITDA (both on an as reported and an as adjusted basis) was material to Ashland’s consolidated financial statements for FY 2012 and FY 2013, from either a quantitative or qualitative perspective. Accordingly restatement was not required, and, as a result, restatement of the other accounting errors during the relevant period was also not required. Management reviewed its assessment with the Company’s Audit Committee of the Board of Directors.

Confidential Treatment

Requested by Ashland Inc.

ASH-019

A-8

Exhibit I

Ashland Inc.

Analysis of Out-of-Period Adjustments on FY 2012

(Understated) / Overstated Income

Understated / (Overstated) Expense

| Period / FS Line Item | As Reported Results | Impact as of September 30, 2012 | ||||||||||

| Fiscal Year 2012 | ||||||||||||

| Roll-Over | % Error | |||||||||||

| Pre-tax income | $ | (14 | ) | $ | 13.2 | -94.1 | % | |||||

| Income from continuing operations | 38 | 9.1 | 23.8 | % | ||||||||

| Net income | 26 | 8.2 | 31.3 | % | ||||||||

| EBITDA | 714 | 13.2 | 1.8 | % | ||||||||

Confidential Treatment

Requested by Ashland Inc.

ASH-020

A-9

Exhibit II

Ashland Inc.

Analysis of Out-of-Period Adjustments on FY 2013

(Understated) / Overstated Income

Understated / (Overstated) Expense

| Period / FS Line Item | As Reported Results | Impact at September 30, 2013 | ||||||||||

| Fiscal Year 2013 | ||||||||||||

| Roll-Over | % Error | |||||||||||

| Pre-tax income | $ | 951 | $ | (13.3 | ) | -1.4 | % | |||||

| Income from continuing operations | 677 | (6.9 | ) | -1.0 | % | |||||||

| Net income | 683 | (0.6 | ) | -0.1 | % | |||||||

| EBITDA | 1,662 | (13.3 | ) | -0.8 | % | |||||||

Confidential Treatment

Requested by Ashland Inc.

ASH-021

A-10

Exhibit III

Ashland Inc.

Analysis of Out-of-Period Adjustments on FY 2012

(Understated) / Overstated Income

Understated / (Overstated) Expense

| Period / FS Line Item | As Adjusted Results | Impact as of September 30, 2012 | ||||||||||

| Fiscal Year 2012 | ||||||||||||

| Roll-Over | % Error | |||||||||||

| Pre-tax income | $ | 714 | $ | 13.2 | 1.8 | % | ||||||

| Income from continuing operations | 529 | 9.1 | 1.7 | % | ||||||||

| Net income | 517 | 8.2 | 1.6 | % | ||||||||

| Adjusted EBITDA | 1,359 | 13.2 | 1.0 | % | ||||||||

Confidential Treatment

Requested by Ashland Inc.

ASH-022

A-11

Exhibit IV

Ashland Inc.

Analysis of Out-of-Period Adjustments on FY 2013

(Understated) / Overstated Income

Understated / (Overstated) Expense

| Period / FS Line Item | As Adjusted Results | Impact at September 30, 2013 | ||||||||||

| Fiscal Year 2013 | ||||||||||||

| Roll-Over | % Error | |||||||||||

| Pre-tax income | $ | 644 | $ | (13.3 | ) | -2.1 | % | |||||

| Income from continuing operations | 485 | (6.9 | ) | -1.4 | % | |||||||

| Net income | 491 | (0.6 | ) | -0.1 | % | |||||||

| Adjusted EBITDA | 1,242 | (13.3 | ) | -1.1 | % | |||||||

Confidential Treatment

Requested by Ashland Inc.

ASH-023

A-12

Appendix B

Confidential Treatment

Requested by Ashland Inc.

ASH-024