James J. O'Brien, Chairman and Chief Executive Officer

Lamar M. Chambers, Senior Vice President and Chief Financial Officer

John E. Panichella, President, Ashland Aqualon Functional Ingredients

Paul C. Raymond III, President, Ashland Hercules Water Technologies

Eric N. Boni, Director, Investor Relations

KeyBanc Analyst Day

August 14, 2009

August 14, 2009

Formula for growth.

2

Forward-Looking Statements

This presentation contains forward-looking statements within the meaning of Section 27A of the Securities Act

of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based

upon a number of assumptions, including those mentioned within this presentation. Performance estimates are

also based upon internal forecasts and analyses of current and future market conditions and trends;

management plans and strategies; operating efficiencies and economic conditions, such as prices, supply and

demand, and cost of raw materials; legal proceedings and claims (including environmental and asbestos

matters); and weather. These risks and uncertainties may cause actual operating results to differ materially

from those stated, projected or implied. Other risks and uncertainties include the possibility that the benefits

anticipated from Ashland's acquisition of Hercules will not be fully realized; Ashland's substantial

indebtedness may impair its financial condition; the restrictive covenants under the debt instruments may

hinder the successful operation of Ashland’s business; future cash flow may be insufficient to repay the debt;

and other risks that are described in filings made by Ashland with the Securities and Exchange Commission

(the “SEC”). Although Ashland believes its expectations are based on reasonable assumptions, it cannot

assure the expectations reflected herein will be achieved. This forward-looking information may prove to be

inaccurate and actual results may differ significantly from those anticipated if one or more of the underlying

assumptions or expectations proves to be inaccurate or is unrealized or if other unexpected conditions or

events occur. Other factors, uncertainties and risks affecting Ashland are contained in Ashland's periodic

filings made with the SEC, including its Form 10-K for the fiscal year ended Sept. 30, 2008, and Form 10-Q for

the quarters ended Dec. 31, 2008, and March 31 and June 30, 2009, which are available on Ashland’s Investor

Relations website at http://investor.ashland.com or the SEC’s website at www.sec.gov. Ashland undertakes no

obligation to subsequently update or revise the forward-looking statements made in this presentation to reflect

events or circumstances after the date of this presentation.

of 1933 and Section 21E of the Securities Exchange Act of 1934. These forward-looking statements are based

upon a number of assumptions, including those mentioned within this presentation. Performance estimates are

also based upon internal forecasts and analyses of current and future market conditions and trends;

management plans and strategies; operating efficiencies and economic conditions, such as prices, supply and

demand, and cost of raw materials; legal proceedings and claims (including environmental and asbestos

matters); and weather. These risks and uncertainties may cause actual operating results to differ materially

from those stated, projected or implied. Other risks and uncertainties include the possibility that the benefits

anticipated from Ashland's acquisition of Hercules will not be fully realized; Ashland's substantial

indebtedness may impair its financial condition; the restrictive covenants under the debt instruments may

hinder the successful operation of Ashland’s business; future cash flow may be insufficient to repay the debt;

and other risks that are described in filings made by Ashland with the Securities and Exchange Commission

(the “SEC”). Although Ashland believes its expectations are based on reasonable assumptions, it cannot

assure the expectations reflected herein will be achieved. This forward-looking information may prove to be

inaccurate and actual results may differ significantly from those anticipated if one or more of the underlying

assumptions or expectations proves to be inaccurate or is unrealized or if other unexpected conditions or

events occur. Other factors, uncertainties and risks affecting Ashland are contained in Ashland's periodic

filings made with the SEC, including its Form 10-K for the fiscal year ended Sept. 30, 2008, and Form 10-Q for

the quarters ended Dec. 31, 2008, and March 31 and June 30, 2009, which are available on Ashland’s Investor

Relations website at http://investor.ashland.com or the SEC’s website at www.sec.gov. Ashland undertakes no

obligation to subsequently update or revise the forward-looking statements made in this presentation to reflect

events or circumstances after the date of this presentation.

3

3

Agenda

• Ashland Overview and Strategy

• Ashland Hercules Water Technologies

• Ashland Aqualon Functional Ingredients

List of Abbreviations Used in This Presentation

4

To be a leading, global specialty chemicals company

that is a market leader in all major businesses

that is a market leader in all major businesses

Ashland Vision for the Future

• Built on three growth platforms

– Ashland Aqualon Functional

Ingredients

Ingredients

– Ashland Hercules Water

Technologies

Technologies

– Ashland Performance Materials

• Investing in two primary

chemistries

chemistries

– Water-soluble polymers

– Thermoset resins

• Sharing three common capabilities

– Application expertise

– Formulation expertise

– Polymerization expertise

• Focused on five key markets

– Paper and packaging

– Personal care

– Pharmaceutical

– Construction

– Transportation

5

Ashland

Consumer

Markets

Consumer

Markets

(Valvoline)

Ashland

Performance

Materials

Materials

Ashland

Hercules

Water

Technologies

Water

Technologies

Ashland

Distribution

Ashland

Aqualon

Functional

Ingredients

Functional

Ingredients

#1 global leader

in unsaturated

polyester resins

and vinyl ester

resins

in unsaturated

polyester resins

and vinyl ester

resins

#3 passenger-

car motor oil

and

#2 quick-lube

chain in the

United States

car motor oil

and

#2 quick-lube

chain in the

United States

#2 plastics

and #3

chemicals

distributor

in North

America

and #3

chemicals

distributor

in North

America

#1 global

producer

of

papermaking

chemicals

producer

of

papermaking

chemicals

#2 global

producer

of cellulose

ethers

producer

of cellulose

ethers

Ashland

Strong Leadership Positions

in the Markets We Serve

in the Markets We Serve

6

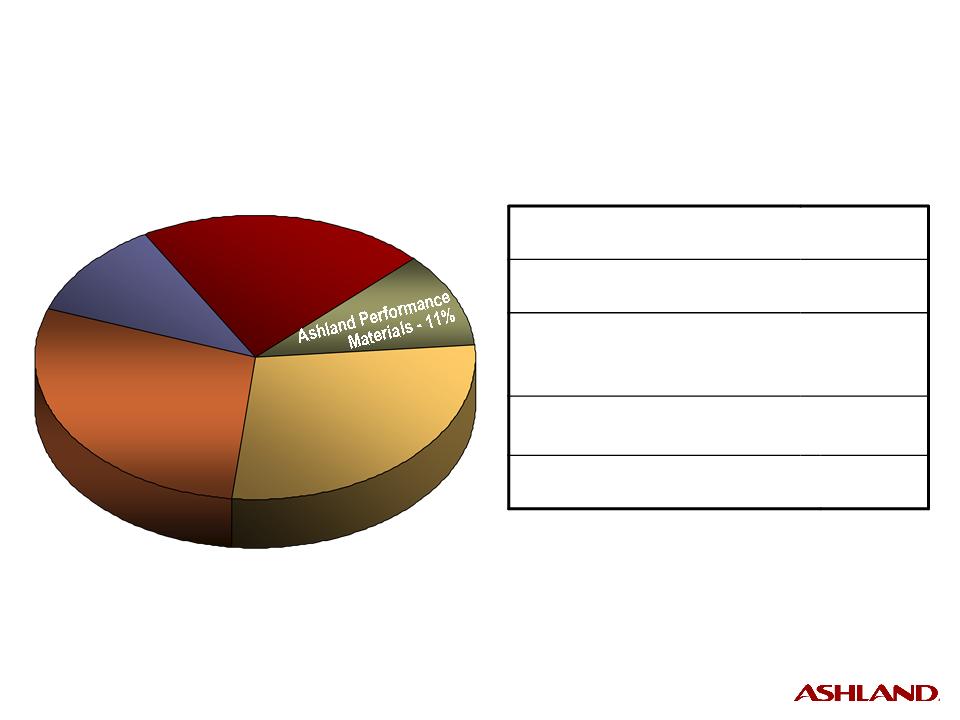

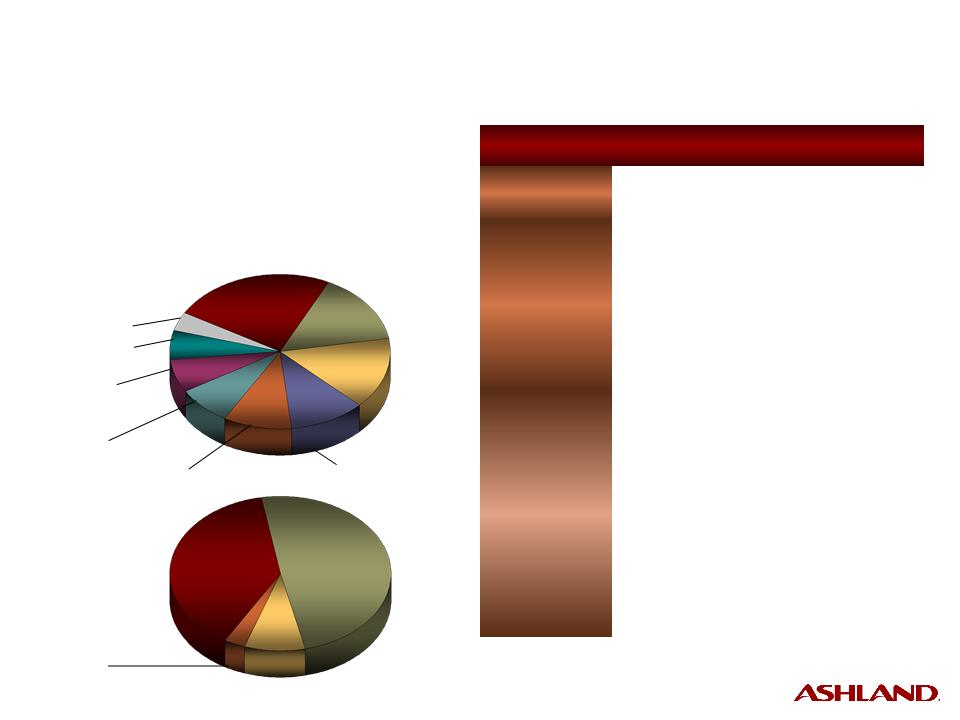

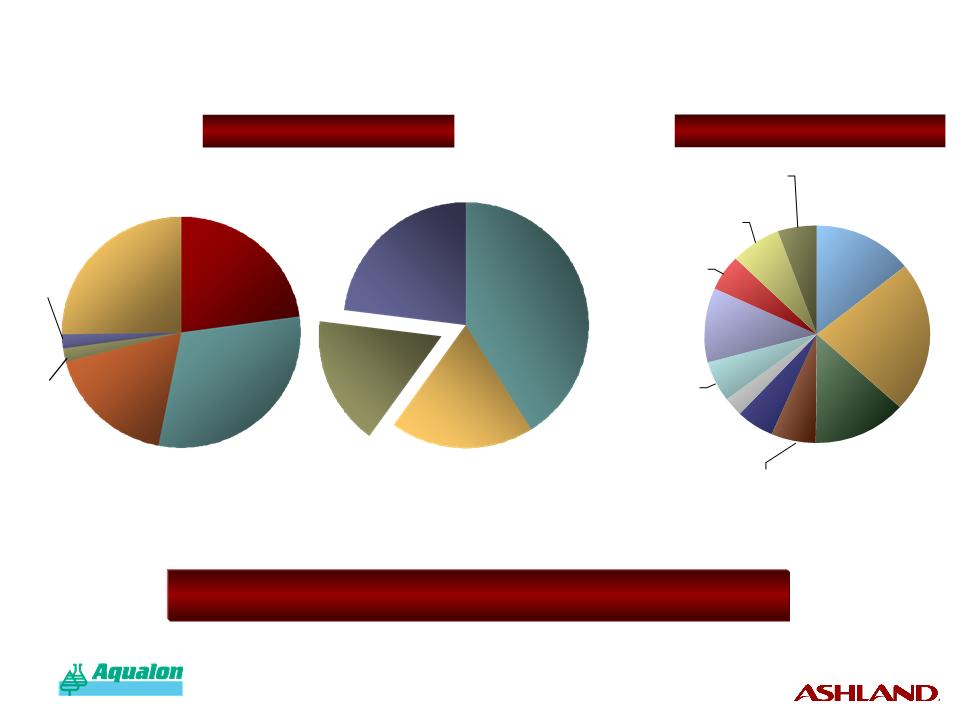

1 For the 12 months ended June 30, 2009.

Ashland

Ashland

Distribution

Distribution

11%

11%

Ashland Consumer

Markets

29%

Markets

29%

Ashland Hercules

Water Technologies

Water Technologies

Ashland Hercules

Water Technologies

Water Technologies

21%

21%

Ashland

Ashland

Aqualon Functional

Aqualon Functional

Ingredients

Ingredients

28%

28%

• 60 percent of EBITDA comes from specialty chemicals

• More than 25 percent from renewable materials

Pro Forma Ongoing EBITDA1

by Commercial Unit

by Commercial Unit

ASH

NYSE Ticker Symbol:

~2,600

Active patents worldwide:

~650

Active patents in U.S.:

More than

100

100

Number of countries

in which Ashland

has sales:

in which Ashland

has sales:

~15,000

Employees:

Corporate Profile

7

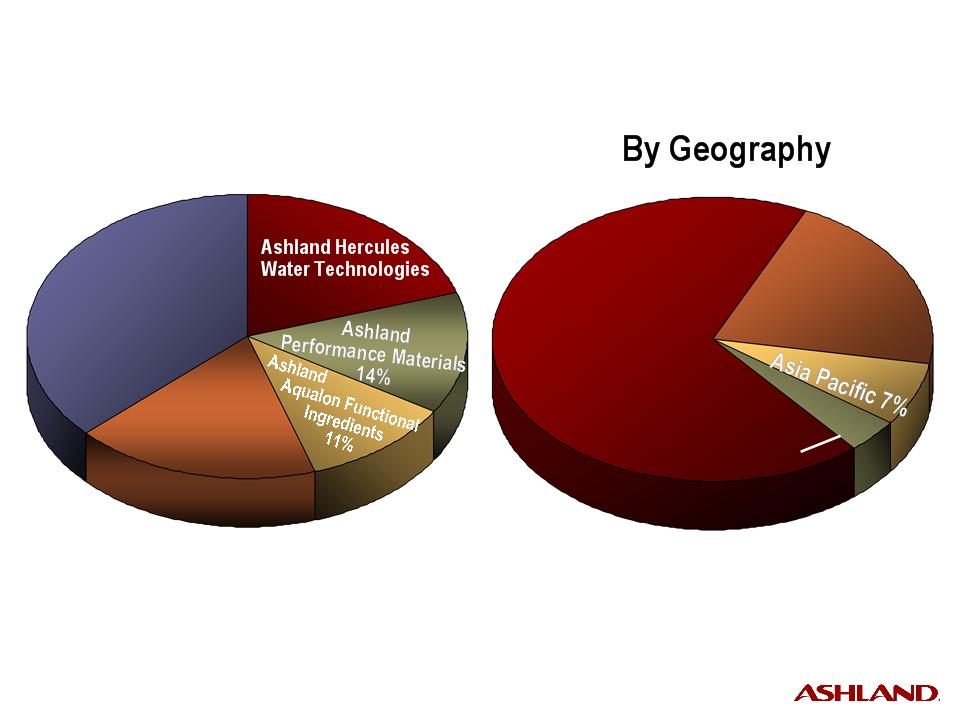

Ashland

Distribution

37%

Distribution

37%

Ashland

Distribution

37%

Distribution

37%

Ashland

Consumer

Markets

18%

Consumer

Markets

18%

By Commercial Unit

20%

20%

1 For the 12 months ended June 30, 2009, including intersegment sales.

North

America

68%

America

68%

North

America

68%

America

68%

Latin America/

Other - 4%

Other - 4%

Europe

Europe

21%

21%

• 32 percent of total revenue comes

from outside North America

from outside North America

Trailing 12 Months' Pro Forma1

Sales and Operating Revenue

Sales and Operating Revenue

8

North

America

America

North

America

America

42%

42%

Asia

Pacific

Pacific

Asia

Pacific

Pacific

17%

17%

Europe

37%

Latin America/

Other - 4%

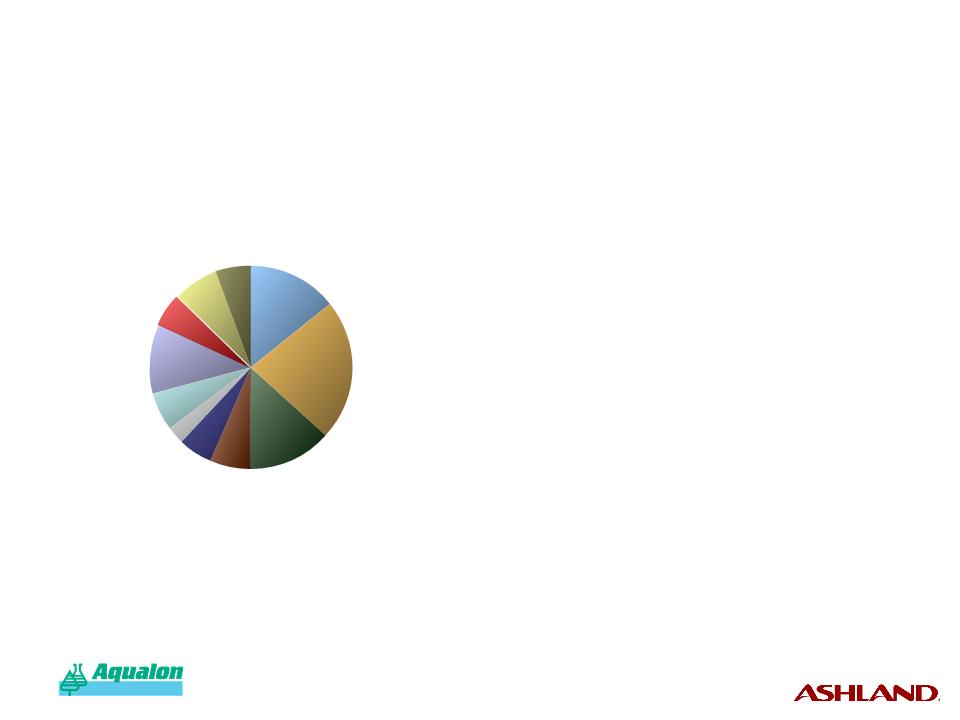

Coatings

26%

26%

Coatings

26%

26%

Energy & Spec.

Solutions

25%

Solutions

25%

Regulated

Industries

28%

Industries

28%

Regulated

Industries

28%

Industries

28%

Revenue

by Geography

by Geography

Revenue

by Market

by Market

For the 12 Months Ended June 30, 2009

Pro Forma Revenue: $1.0 billion

Pro Forma Ongoing EBITDA: $216 million

Pro Forma Ongoing EBITDA Margin: 21.6%

Business Overview | |

Customers | • Diversified, global customer base |

Products | • Broad product line based on renewable resources - Water-soluble polymers (cellulose ethers and guar derivatives) - Refined wood rosin and natural wood terpenes |

Markets | • Water-based paints • Regulated markets - Personal care - Food - Pharmaceuticals • Construction • Paper coatings • Oilfield (chemicals and drilling muds) |

Revenue

by Product

by Product

CMC

17%

17%

CMC

17%

17%

HEC

28%

28%

HEC

28%

28%

MC

22%

22%

MC

22%

22%

Other

17%

17%

Other

17%

17%

Stumpwood

Derivatives

Derivatives

6%

6%

Construction

21%

21%

Construction

21%

21%

9

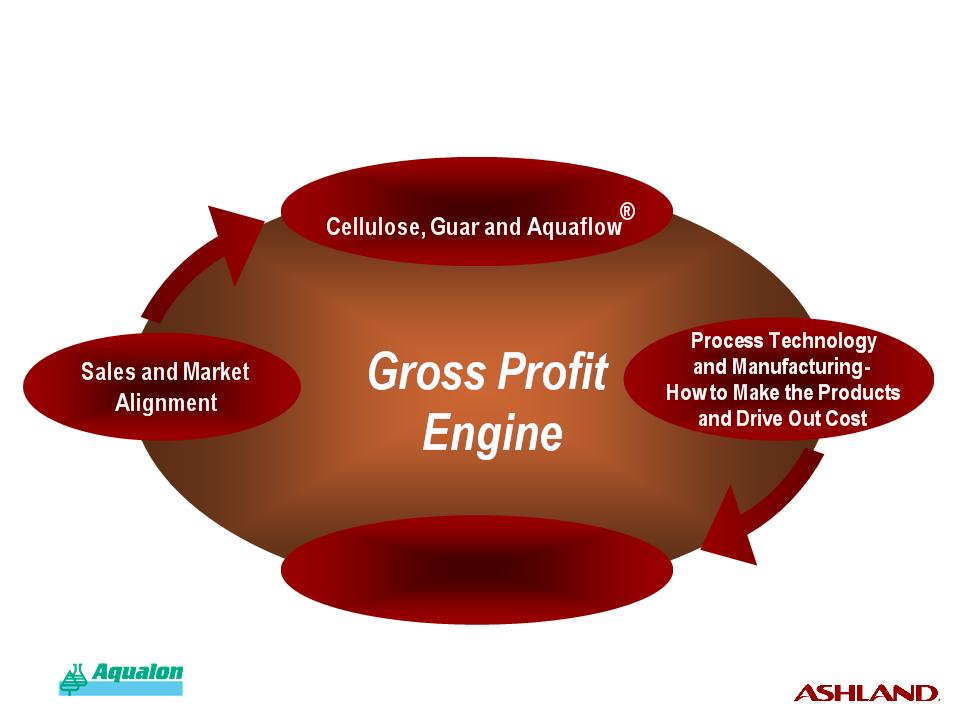

• Use leadership position in cellulose ethers

to drive growth through product innovation

and geographic expansion

to drive growth through product innovation

and geographic expansion

• Invest in additional water-soluble polymers that can be

leveraged across multiple growth platforms and markets

leveraged across multiple growth platforms and markets

• Leverage deep customer relationships

in core markets (coatings, construction,

personal care and pharmaceutical) to introduce

high-value complementary products

in core markets (coatings, construction,

personal care and pharmaceutical) to introduce

high-value complementary products

Ashland Aqualon Functional Ingredients

Strategy

Strategy

10

North

America

America

48%

Latin America/

Other - 6%

Other - 6%

E&PS

16%

16%

E&PS

16%

16%

Pulp/Paper

59%

Business Overview | |

Customers/ Markets | • Pulp and paper processing • Industrial and institutional • Mining • Municipal wastewater treatment |

Products/ Services | • Process chemicals for microbial and contaminant control, pulping aids and retention aids • Functional chemicals for sizing and wet strength • Utility water treatments • Process water treatments |

Revenue

by Geography

by Geography

Revenue

by Market

by Market

Asia

Pacific

11%

Pacific

11%

Europe

35%

35%

For the 12 Months Ended June 30, 2009

Pro Forma Revenue: $1.9 billion

Pro Forma Ongoing EBITDA: $165 million

Pro Forma Ongoing EBITDA Margin: 8.7%

Ashland Hercules Water Technologies

A major global supplier of process and functional chemicals

A major global supplier of process and functional chemicals

11

• Build on leadership position

in specialty papermaking chemicals

through product-line extension and

geographic expansion

in specialty papermaking chemicals

through product-line extension and

geographic expansion

• Extend best-in-class, market-focused business model

to additional water-intensive verticals, leveraging

core process chemical technologies

to additional water-intensive verticals, leveraging

core process chemical technologies

• Continue to optimize operational efficiency

of high-volume functional chemical assets

of high-volume functional chemical assets

Ashland Hercules Water Technologies

Strategy

Strategy

12

North

America

America

North

America

America

56%

56%

Europe

27%

Latin

America/

Other - 8%

America/

Other - 8%

Trans-

portation

portation

Trans-

portation

portation

18%

18%

Ind.

Constr.

Constr.

30%

Business Overview | |

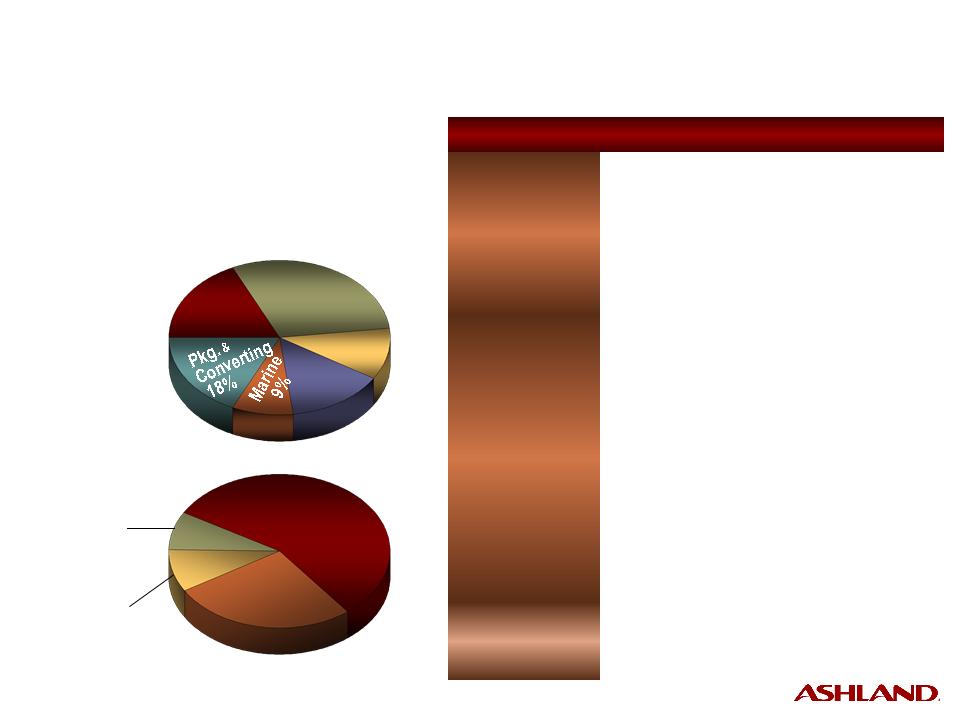

Customers | • Auto manufacturers; foundries; pipe and tank fabricators; packaging and converting; bathware, countertop and window lineal manufacturers; pipe relining contractors; boat builders; wide and narrow web printers |

Products/ Services | • Adhesives and Composites - Unsaturated polyester resins - Vinyl ester resins - Gelcoats - Pressure-sensitive adhesives - Structural adhesives - Specialty resins • Casting Solutions - Foundry binder resins - Chemicals - Sleeves and filters - Design services |

Markets | • Construction, packaging and con- verting, transportation, and marine |

Revenue

by Geography

by Geography

Revenue

by Market

by Market

For the 12 Months Ended June 30, 2009

Pro Forma Revenue: $1.3 billion

Pro Forma Ongoing EBITDA: $81 million

Pro Forma Ongoing EBITDA Margin: 6.3%

Res. Constr.

11%

Infra-

structure

structure

14%

Asia

Pacific - 9%

Pacific - 9%

Ashland Performance Materials

A global leader in specialty chemicals

A global leader in specialty chemicals

13

• Use market insight and thermoset chemistry expertise

to create innovative substitutes that are stronger,

lighter and more resistant than traditional materials

for core transportation, construction and

infrastructure markets

to create innovative substitutes that are stronger,

lighter and more resistant than traditional materials

for core transportation, construction and

infrastructure markets

• Use leadership position in unsaturated polyester resins

and vinyl ester resins to catalyze growth

in Brazil, Russia, India and China

and vinyl ester resins to catalyze growth

in Brazil, Russia, India and China

• Further build position in packaging and converting market,

capitalizing on strength in high-end, solvent-based systems

to drive innovation from our new water-based and

radiation-cured technologies

capitalizing on strength in high-end, solvent-based systems

to drive innovation from our new water-based and

radiation-cured technologies

Ashland Performance Materials

Strategy

Strategy

14

Lubricants

84%

Filters - 2%

Valvoline

Int'l

20%

Int'l

20%

Valvoline

Int'l

20%

Int'l

20%

Do-It-

Yourself

Yourself

38%

Business Overview | |

Customers | • Retail auto parts stores and mass merchandisers who sell to consumers; installers, such as car dealers and quick lubes; distributors |

Products/ Services | • Valvoline® lubricants and automotive chemicals • MaxLife® lubricants for high-mileage vehicles • SynPower® synthetic motor oil • Eagle One® and Car Brite® appearance products • Zerex® antifreeze • Valvoline Instant Oil Change® service |

Market Channels | • Do-It-Yourself (DIY) • Do-It-For-Me (DIFM) • Valvoline International |

Revenue

by Product Line

by Product Line

Revenue

by Market Channel

by Market Channel

Do-It-

For-Me

40%

For-Me

40%

DIFM:

Installer channel

29%

Installer channel

29%

Specialty/

Other - 2%

Other - 2%

DIFM:

Valvoline Instant

Oil Change - 11%

Valvoline Instant

Oil Change - 11%

Antifreeze - 5%

Appearance

products - 3%

products - 3%

Chemicals - 6%

For the 12 Months Ended June 30, 2009

Pro Forma Revenue: $1.7 billion

Pro Forma Ongoing EBITDA: $227 million

Pro Forma Ongoing EBITDA Margin: 13.4%

Ashland Consumer Markets: A leading worldwide

marketer of premium-branded automotive lubricants and chemicals

marketer of premium-branded automotive lubricants and chemicals

15

• Use superior consumer insight to create channel-focused

solutions that leverage the Valvoline brand

solutions that leverage the Valvoline brand

• Build brand loyalty in key Do-It-Yourself (DIY) growth

segments, such as youth and Hispanics, through

highly targeted advertising, promotions and programs

segments, such as youth and Hispanics, through

highly targeted advertising, promotions and programs

• Continue to deliver preferred customer experience

in oil-change business through superior employee training,

store traffic optimization, point-of-sale enhancements

and highly targeted service offerings

in oil-change business through superior employee training,

store traffic optimization, point-of-sale enhancements

and highly targeted service offerings

Ashland Consumer Markets

Strategy

Strategy

16

Chemicals

Chemicals

49%

49%

Plastics

39%

Environmental

Services/Other

- 3%

Services/Other

- 3%

Construction

Construction

24%

24%

Other

15%

Business Overview | |

Customers | • Diversified customer base in North America and Europe |

Products/ Services | • More than 28,000 packaged and bulk chemicals, solvents, plastics and additives • Comprehensive, hazardous and nonhazardous waste- management solutions in North America |

Markets | • Construction • Transportation • Chemical manufacturing • Paint and coatings • Retail consumer • Personal care • Medical • Marine |

Revenue

by Product

Line

by Product

Line

Revenue

by Market

by Market

Trans-

portation

portation

15%

Paint & Coatings - 10%

Medical - 6%

Marine - 4%

Com-

posites

posites

9%

Chemical Mfg.

- 11%

- 11%

Retail

Consumer - 8%

Consumer - 8%

Personal

Care - 7%

Care - 7%

For the 12 Months Ended June 30, 2009

Pro Forma Revenue: $3.4 billion

Pro Forma Ongoing EBITDA: $88 million

Pro Forma Ongoing EBITDA Margin: 2.6%

Ashland Distribution

A leading North American chemicals and plastics distributor

A leading North American chemicals and plastics distributor

17

• Continue focus on efficiency to create

highest-value channel for customers and suppliers

highest-value channel for customers and suppliers

• Build best-in-class product offering by aligning

with globally leading suppliers that:

with globally leading suppliers that:

– have low-cost production

– can ensure continuity of supply

– are investing in their business

– are industry leaders in quality and reliability

• Leverage Ashland's technical resources and asset network

to provide mass market penetration for specialty products

to provide mass market penetration for specialty products

Ashland Distribution

Strategy

Strategy

18

Ashland Recent Performance and

Near-Term Outlook

Near-Term Outlook

• Repayment of debt through cash flow is a priority

to achieve investment-grade credit statistics

to achieve investment-grade credit statistics

– Reduced gross debt to under $2 billion at June 30

• Focus on generating and growing cash flow

– Generated cash flows from operating activities of $649 million

for fiscal year-to-date at June 30

for fiscal year-to-date at June 30

– Can be supplemented with noncore assets sales

• Exceeded $265 million cost-reduction target by $22 million,

three months ahead of plan

three months ahead of plan

• Margin and price management mitigating significant volume declines

• Resizing business and cost structure to reflect

20-percent volume-reduction environment

20-percent volume-reduction environment

• Ashland is well-positioned to outperform as the economy improves

19

Ashland's Strategy

• Focus on specialty chemicals supported by Hercules acquisition

• Generate cash flow for paying down debt

• Manage cost structure and leverage new scale

• Reduce volatility of earnings and cash flow

and retain conservative financial position

and retain conservative financial position

• Invest in sustainable technologies to decrease reliance

on petroleum-based raw materials

on petroleum-based raw materials

• Continue to grow in water-intensive industries

to capitalize on increasing demand for clean, usable water

to capitalize on increasing demand for clean, usable water

• Leverage formulation and application expertise

into adjacent markets that value our customized-service model

into adjacent markets that value our customized-service model

• Accelerate investment in long-term high-growth nations

such as Brazil, Russia, India and China

such as Brazil, Russia, India and China

• Improve position in core specialty chemical businesses,

while reducing investment in noncore businesses

while reducing investment in noncore businesses

Paul C. Raymond III, President

20

Ashland Hercules Water Technologies

Formula for growth.

21

Microbial Control

Contaminant Control

Foam Control

Retention Aids

Softness

Strength

Printability

Sizing

Cooling Water

Wastewater

Influent Water

Boiler Water

Process

Additives

Additives

Water

Treatment

Chemicals

Treatment

Chemicals

Functional

Additives

Additives

How Our Products Are Used

22

Application Expertise -

Understanding Customers’

Unique Applications

Customer Intimacy -

Sales and Market

Alignment

Technology Expertise -

Process, Water Treatment, Functional

Core of the Business … How We Make Money

23

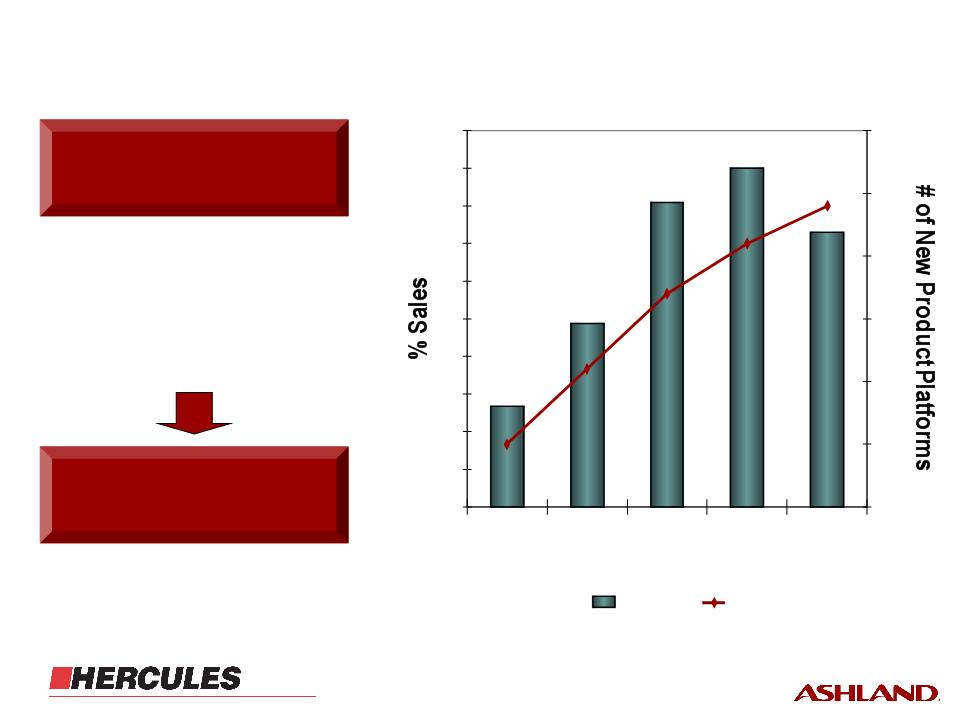

0

2

4

6

8

10

12

14

16

18

20

2004

2005

2006

2007

2008

0

5

10

15

20

25

30

% Sales

# Platforms

AHWT Platform Launch

• Reflects strategic priorities

• Emphasizes high-margin

products

products

• Showcases platforms that

build competitive advantage

build competitive advantage

Organizational

Alignment

Alignment

• Dedicated team in each region

• Specific accountabilities

Platform Launch

24

Time

(years)

Traditional Cooling

Water Chemistries

Water Chemistries

Corrosion Inhibitors

Scale Control

Biocides

Incubator Market

Identification

Bus Plan

Dev.

Incubator

Commercialization

Value

Capture

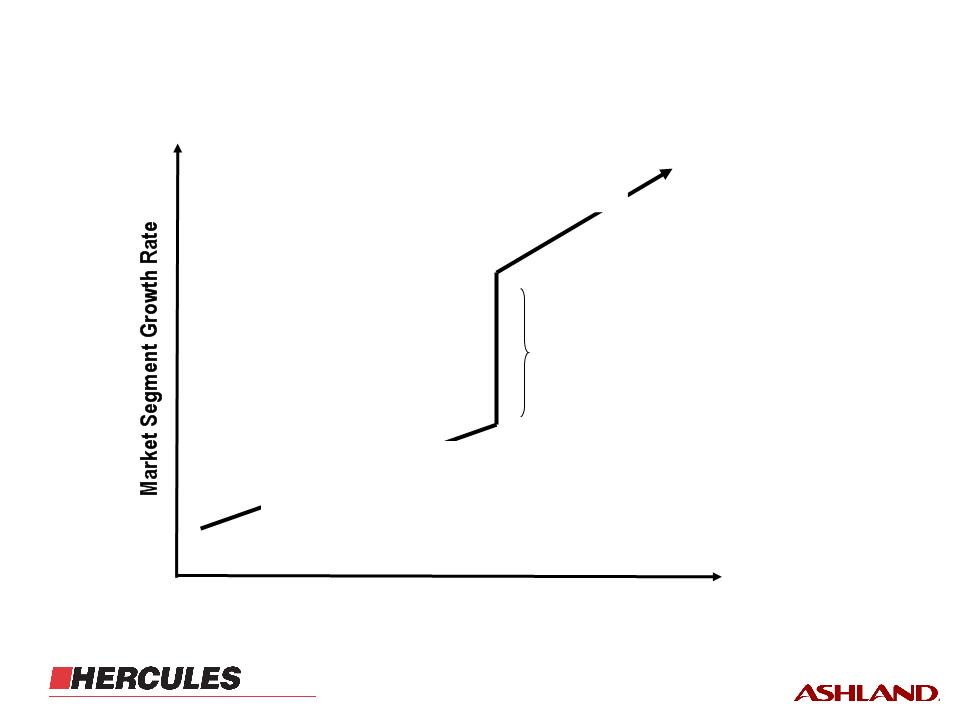

New Growth Curve

Growth Step Change

Hybrid Technology

SONOXIDE + chemical treatment

SONOXIDE®

ultrasonic

water

treatment

system

ultrasonic

water

treatment

system

Incubator Businesses

25

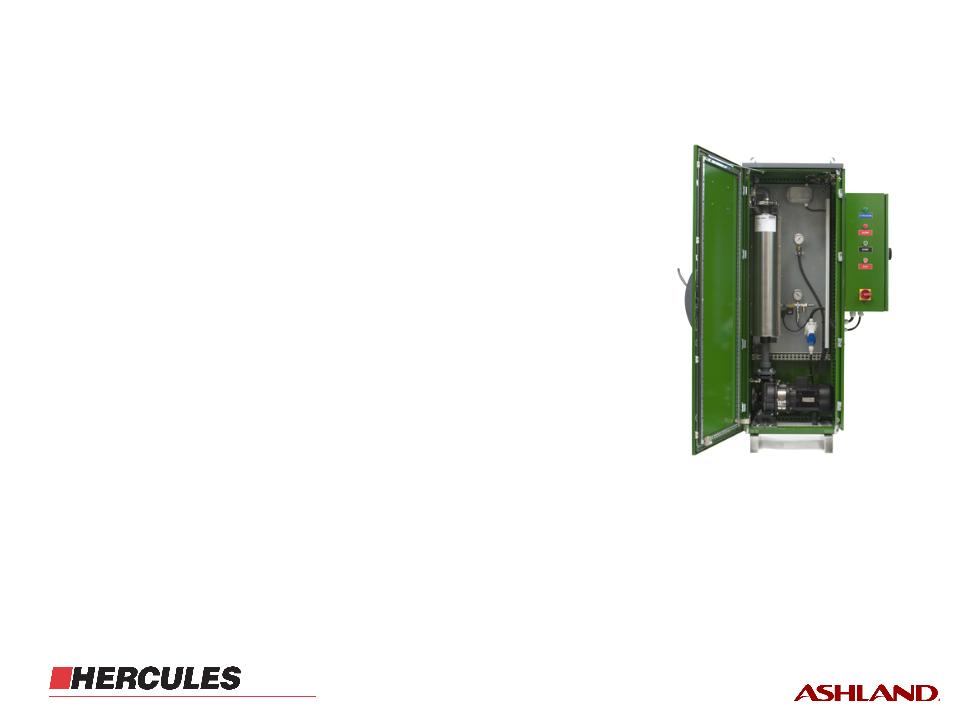

Sonoxide Ultrasonic Water Treatment System

• Nonchemical, microbiological control

for cooling water systems

for cooling water systems

• Market: $800 million in cooling water

• Improved environmental profile

• Energy optimization

• Reduced chemical use

• Improved worker safety

26

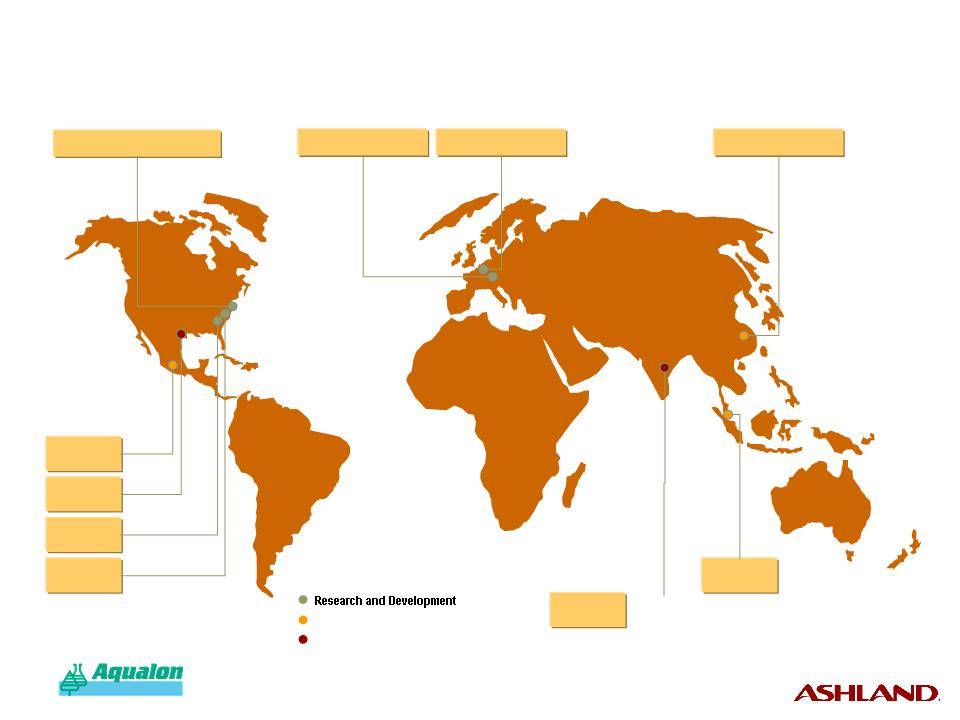

Global Technology Footprint

• Research & Development

– Wilmington, Delaware, U.S.A.

– Krefeld, Germany

• Customer Applications Laboratories

– Wilmington, Delaware, U.S.A.

– Krefeld, Germany

– Shanghai, P.R. China

– Paulinia, Brazil (2010)

27

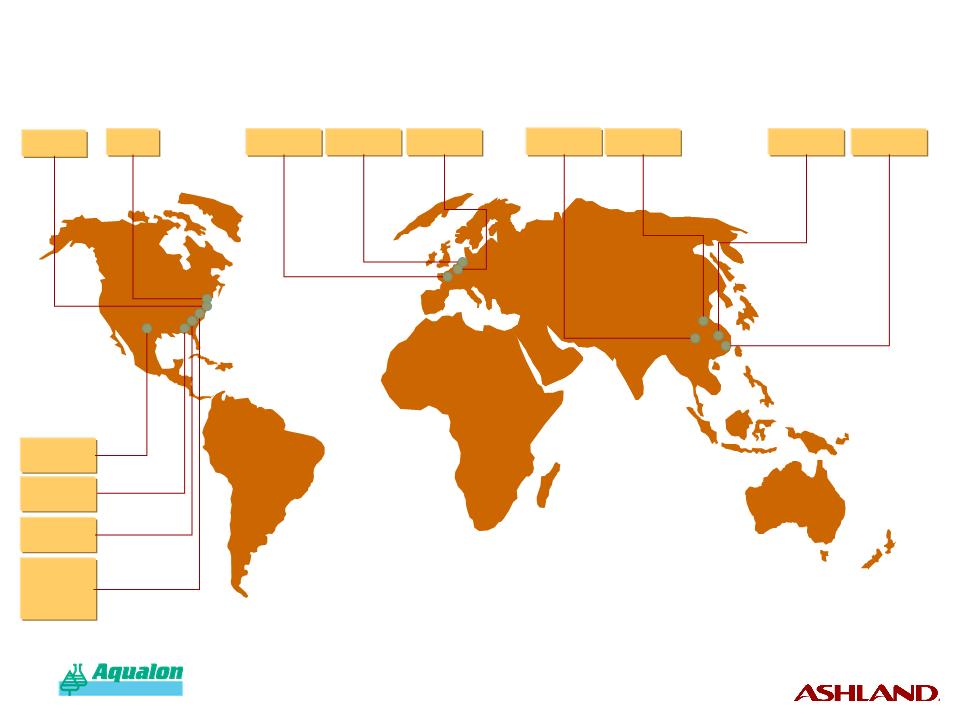

17. Beringen, Belgium

18. Busnago, Italy

19. Helsingborg, Sweden

20. Krefeld, Germany

21. Perm, Russia

22. Sobernheim, Germany

23. Somercotes, United Kingdom

24. Tampere, Finland

25. Tarragona, Spain

26. Voreppe, France*

27. Zwijndrecht, Netherlands

14. Americana, Brazil

15. Leme, São Paulo, Brazil

16. Paulinia, Brazil

1. Burlington, Ontario, Canada

2. Chicopee, Massachusetts

3. Franklin, Virginia

4. Greensboro, North Carolina

5. Hattiesburg, Mississippi*

6. Houston, Texas

7. Kearny, New Jersey*

8. Louisiana, Missouri

9. Macon, Georgia

10. Mexico City, Mexico

11. Milwaukee, Wisconsin

12. Portland, Oregon

13. Savannah, Georgia

28. Beijing, P.R. China

29. Kim Cheon, Korea

30. Nanjing, P.R. China*

31. Nantou, Taiwan

32. Perawang, Indonesia

33. Shanghai, P.R. China

34. Singapore

35. Chester Hill, Australia

* Facility closure announced.

Global Manufacturing Footprint

28

Business Strategy

• Follow Responsible Care* principles to ensure that safety

and environmental excellence are core values

and environmental excellence are core values

• Achieve leadership positions in all of our growth

and base markets

and base markets

• Improve sales mix through new product introduction

• Grow top line in adjacent markets and emerging geographies

• Leverage external technology to augment internal efforts

• Balance service delivery investment to maximize

profitable growth

profitable growth

• Maintain reliable and efficient global supply chain

29

Water

Test

$4 B

Test

$4 B

Municipal Water &

Wastewater

Treatment

Wastewater

Treatment

Municipal Water &

Wastewater

Treatment

Wastewater

Treatment

$138 B

$138 B

Infrastructure $40 B

Valves

$40 B

$40 B

Valves

$40 B

$40 B

Pumps $25 B

Other Water-Related $20 B

Residential $18 B

Water Market

~$365 B

~$365 B

Industrial Water

Treatment

Treatment

Industrial Water

Treatment

Treatment

$80 B

$80 B

Functional

Chemicals

Chemicals

Functional

Chemicals

Chemicals

$10 B

$10 B

Pigments & Fillers

Pigments & Fillers

$7.4 B

$7.4 B

Coatings

$5.5 B

Bleaching

Bleaching

$4.7 B

$4.7 B

Pulping

$4.3 B

Process Chem $2 B

Deinking $1 B

Global Water/Pulp & Paper Market $400 Billon

AHWT Target

Markets

Markets

$28.5 B

Water

Treatment

Treatment

Water

Treatment

Treatment

$17.5 B

$17.5 B

Pulp & Paper

Pulp & Paper

$11.0 B

$11.0 B

Non-Focus

Water Segments

· Equipment and

hardware

hardware

· Infrastructure

· Residential

· Water test

Non-Focus

Paper Segments

· Pigments and fillers

· Coatings

· Deinking

· Bleaching

Sources: Poyry Global Pulp & Paper Market Review, 2008: Goldman Sachs Water Sector Primer,

June 2005; Global Water Intelligence (GWI) Global Water Market Survey, 2008; The Future

of Global Water Treatment Chemicals Market, Pira International; Citi Investment Research,

“A Rising Tide of Growth” (March 2008), internal estimates.

June 2005; Global Water Intelligence (GWI) Global Water Market Survey, 2008; The Future

of Global Water Treatment Chemicals Market, Pira International; Citi Investment Research,

“A Rising Tide of Growth” (March 2008), internal estimates.

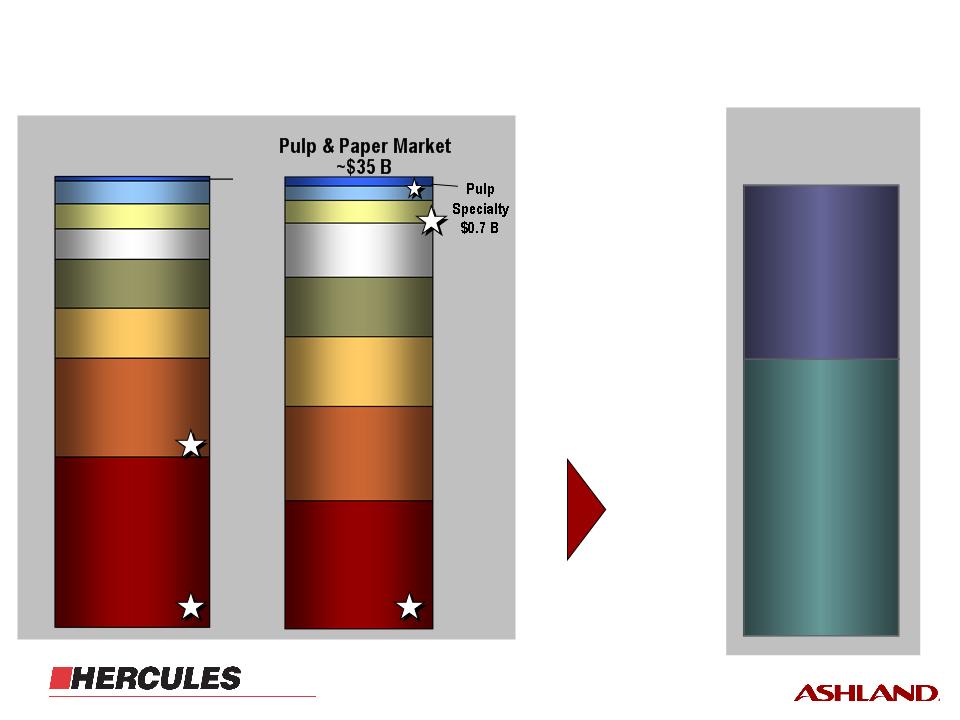

Defining AHWT’s Markets

30

• Pulp

• Other

$2.0 B

• Size

• Strength

• Retention aids

• Boiler water

• Cooling water

• Waste water

• Recovery boilers

AHWT Position

• Leading position in boiler &

cooling water treatment

for paper, commercial &

institutional, food & bever-

age, general manufacturing

and marine

cooling water treatment

for paper, commercial &

institutional, food & bever-

age, general manufacturing

and marine

• Significant player in highly

fragmented market

fragmented market

$0.9 B

$1.1 B

• Leading position in size,

strength, retention aids,

MB

strength, retention aids,

MB

• Complementary ultrasonic

technology to current MB

control offering

technology to current MB

control offering

• Sizeable, but underperforming,

position in polyacrylamides

(municipal)

position in polyacrylamides

(municipal)

Water

Treatment

Treatment

Water

Treatment

Treatment

~$900 MM

~$900 MM

Process

Chemicals

~$450 MM

Chemicals

~$450 MM

Process

Chemicals

~$450 MM

Chemicals

~$450 MM

Functional

Chemicals

Chemicals

Functional

Chemicals

Chemicals

~$650 MM

~$650 MM

Water

Treatment

Treatment

Water

Treatment

Treatment

$17.5 B

$17.5 B

Pulp & Paper

Pulp & Paper

$11.0 B

$11.0 B

$28.5 B

• Defoamers

• Microbiocides (MB)

• Contaminant control

Target Market

AHWT

AHWT Business Overview

31

Process

Chemicals

~$450 MM

Chemicals

~$450 MM

Process

Chemicals

~$450 MM

Chemicals

~$450 MM

AHWT

$2.0 B

$2.0 B

Water

Treatment

Treatment

Water

Treatment

Treatment

~$900 MM

~$900 MM

Functional

Chemicals

Chemicals

Functional

Chemicals

Chemicals

~$650 MM

~$650 MM

Vertical Markets

Growth

• Pulp and paper segments

with high growth rates

with high growth rates

• High-margin water segments

with process expansion

potential

with process expansion

potential

Segmentation

Base

• Paper segments with

moderate growth rates

moderate growth rates

• Water segments with

reasonable growth

in water treatment

reasonable growth

in water treatment

Municipal

Oil Refining

Power

Metals

Printing &

Writing

Writing

Mining

Chemicals

Gen’l Mfgr.

Packaging

Tissue/Towel

Pulp

C&I

Food & Bev

Opportunistic

• Low service, underperforming

• Water segments with limited/

no expansion into process

applications

no expansion into process

applications

Stand-alone

• Lubes

Commercial &

Institutional (C&I)

Institutional (C&I)

Chemicals

Food & Beverage

General

Manufacturing

Manufacturing

Lubes

Metals

Mining

Municipal

Oil Refining

Printing & Writing

Packaging

Power Generation

Pulp

Tissue/Towel

AHWT Strategic Market Segmentation

32

Focus on markets with inherently higher growth

Demand | Customer Profitability | Key Drivers | |

Tissue | • Fiber types/recycle - Biocides/contaminant control • Emerging markets growing • Absorbency and strength | ||

Packaging | • Machine productivity - Dry strength • China expansion | ||

Commercial & Institutional (C&I) | • Urbanization driving market growth • Purchasing consolidation driving demand for global suppliers • Geographic expansion in industrialized markets • Energy-reduction requirements driving treatment demand | ||

Food & Beverage | • Industrialization driving demand for processed foods • Increased water and food regulation driving chemical demand • Emerging markets growing rapidly | ||

Pulp | • Changing paper, board, tissue grade needs and fiber source • Emerging market growth (Brazil, Chile, Russia, Indonesia, China and India) • New technologies for new fiber sources |

Growth Market Segments

33

• Paper: MB, retention, contaminant control, dry strength

• Water: Scale inhibitors, defoamers, cooling/boiler water

treatment applications

treatment applications

• Rapid deployment in growing geographies

(Latin America and Asia Pacific)

(Latin America and Asia Pacific)

Seed Key

Industry Verticals

Industry Verticals

Expand via

Core Technologies

Core Technologies

Seek Sustainable

Critical Mass

Critical Mass

Align Resources

Actions

• Dedicated marketing leader for each growth vertical

• Develop and staff R&D pipeline

• Align platform-launch teams and programs

on high-margin, high-growth applications

on high-margin, high-growth applications

• Build knowledge and credibility in key verticals

for future expansion

for future expansion

• Use “incubator” model across high-potential segments

• Carve off verticals that have achieved critical mass

into market-focused virtual teams

into market-focused virtual teams

• Established market-specific product lines and

service offerings

service offerings

2009 Strategy for Growth Verticals

34

Protect and maintain the business base

Demand | Customer Profitability | Key Drivers | |

Printing & Writing | • Reduce costs - Increase filler loading, reduce overall chemical costs • Resume significant expansion in Asia, mainly China • Building larger machines and shutting the smaller ones | ||

Mining | • Global slowdown has led to high reserves of aluminum, copper, nickel, zinc; prices flat in 2009, down from 2008 • Precious metals and coal demand increasing • Increased need for process chemicals to improve metals yield and water removal | ||

Chemicals | • Process-focused, performance-driven and seeking more sophisticated programs and service expertise • Accommodate volatility in supply and demand • Typically engage in long-term corporate and/or global agreements • Energy conservation | ||

General Manufacturing | • Optimize efficiencies and reduce total cost of operation • Cost - Economic slowdown has significantly reduced production in most sectors • Need for restructuring will open door for innovation in water treatment |

Base Market Segments

35

• Cross-train field sales team to cover multiple markets

• Improve sales and applications expertise in Latin America and

Asia Pacific

Asia Pacific

• Develop R&D relationships with early-adopter customers

to develop game-changing products

to develop game-changing products

Protect Profit Engine

Standardization

Actions

• Maintain product differentiation in base printing & writing and

chemicals via healthy R&D pipeline

chemicals via healthy R&D pipeline

• Rationalize manufacturing assets to lower unit costs

• Commercialize new technologies in emerging geographies

Grow Water

Treatment

Treatment

Channel to Market

• Expand geographical coverage in underdeveloped markets

• Develop products to fill gaps (e.g., equipment for dosing and

monitoring)

monitoring)

• Identify supply chain synergies to remove costs

• Rationalize water treatment product lines across geographies

• All regions reporting via SAP* platform

Strategy for Base Verticals

36

• Municipal market

• PAM distributors/contract service companies

• Paper sizing

• Paper wet strength

Implement Alternate Business Model

• Low/declining margins in sizing/wet strength

• Lack of vertical integration in polyacrylamides (PAM)

drives uncompetitive cost position in municipal segment

drives uncompetitive cost position in municipal segment

• Overall trend toward product commoditization

• Inability to monetize service offering

• Low value of innovation to customers

• Some competitors have moved to low-cost model

Business

Trends

Product Lines and

Verticals Impacted

Consolidate

FTEs

Lower Raw Material

and Freight Costs

and Freight Costs

SG&A Savings

Cost Leverage via

Lower Complexity

Targeted Outcomes

Alternate Business Model

37

Summary

• AHWT Business Overview

– $2.0 billion business

– Provides process, water treatment and functional chemistries to paper, pulp,

commercial and institutional, food and beverage, chemical, marine and

municipal industries

commercial and institutional, food and beverage, chemical, marine and

municipal industries

– Products are used to improve operational efficiencies, enhance product quality,

protect plant assets and ensure environmental compliance

protect plant assets and ensure environmental compliance

• Business Strategy

– Leverage platform-launch and incubator processes to accelerate growth

through delivery of innovative, low-cost products to current and adjacent

markets

through delivery of innovative, low-cost products to current and adjacent

markets

• Use segmented approach to AHWT vertical markets

– Resource growth verticals with dedicated sales, marketing and R&D teams

– Manage base verticals primarily by sales to maximize profitable growth

– Alternate business model enables cost-effective approach to volume growth

with enhanced profitability in segments that do not require high service levels

with enhanced profitability in segments that do not require high service levels

John E. Panichella, President

38

Ashland Aqualon Functional Ingredients

Formula for growth.

39

Flow and Leveling

Conditioning

Stabilizing

Drilling & Fracturing

Extrusion

Protective Coating

Flow Properties

Suspending

Binding

Thickening

Gel Formation

Water Retention

How Customers Use Our Products

40

Technology Expertise -

Application Expertise -

Understanding Customers’

Unique Applications

Core of the Business … How We Make Money

41

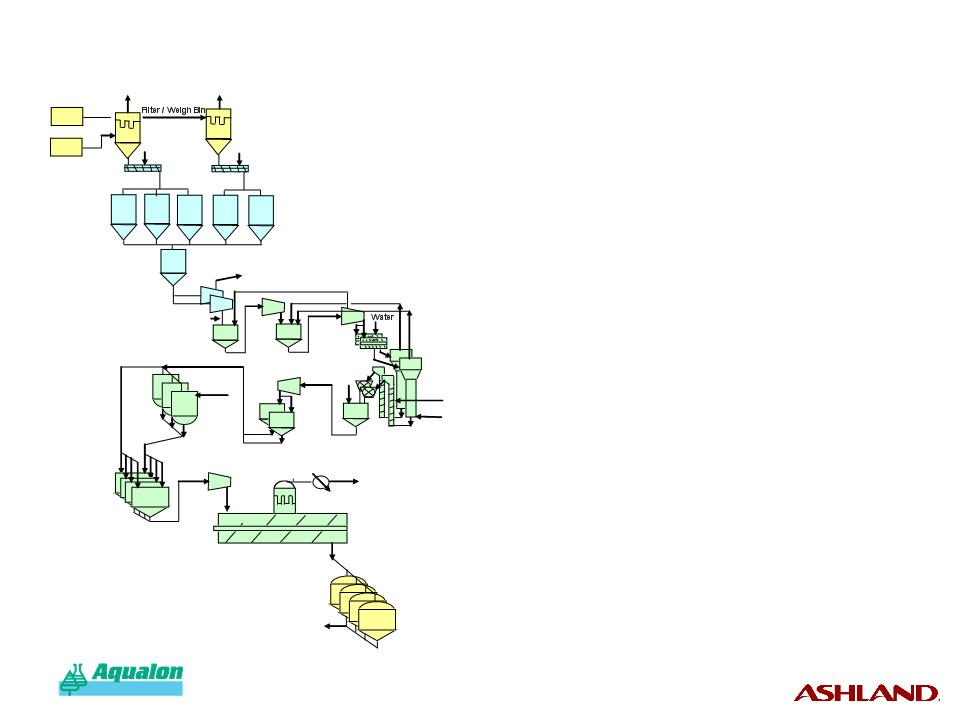

• Cellulose is cut from sheets/rolls

into fine particles

into fine particles

• Cellulose is air-conveyed to reactor

and swollen with caustic

and swollen with caustic

• Ethylene oxide, propylene oxide

or other reactants impart

water-solubility

or other reactants impart

water-solubility

• Solvent recycled via distillation

• Viscosity reduction and purification

• Hot-air drying

• Grinding to control dissolution rate,

dry blending, packing into bags/

sacks

dry blending, packing into bags/

sacks

Caustic

Caustic

H2O2

Cellulose

Cellulose

Distillation

Solvent

Washing

Grinding/Sifting/

Blending/Packaging

Viscosity

Reduction

Reactor

Drying

Cutting

How We Make Our Products

42

CMC

MC

HEC

HEC

HEC

HEC

CMC

HPC

CMC

HPC

EC

Rosins and

Phosphate Esters

Guar

Aquaflow

Aquaflow

MC

MC

Parlin, New Jersey

Hopewell, Virginia

Kenedy, Texas

Dalton, Georgia

Alizay,

France

Doel,

Belgium

Zwijndrecht,

Netherlands

Luzhou,

P.R. China

Suzhou,

P.R. China

Jiangmen,

P.R. China

Guar

Brunswick,

Georgia

CMC

Nanjing,

P.R. China

(Under

construction.)

construction.)

Aquarius®

Wilmington,

Delaware

Global Manufacturing Footprint

43

Zwinjdrecht, Netherlands

Facilities and Processes

• Eleven world-class

manufacturing facilities

including one joint

venture

manufacturing facilities

including one joint

venture

• New 10,000MT HEC

facility under

construction

facility under

construction

• Low-cost facilities

• Combination of batch and

continuous processes -

24/7 operations

continuous processes -

24/7 operations

• All facilities ISO-certified,

well-maintained and in

compliance with stringent

EH&S guidelines

well-maintained and in

compliance with stringent

EH&S guidelines

• Capital intensive

44

Regional Technical Service

External Technology Partner

Construction

Technical Service

Technical Service

Coatings Additives,

Personal Care

Technical Service

China

Engineering and

Pilot Plant

Specialty Resins

and Adhesives

Technical Service

Latin America

Hopewell, Virginia

Mexico City,

Mexico

Houston, Texas

Düsseldorf,

Germany

Zwijndrecht,

Netherlands

Oil and Gas

Technologies

Brunswick, Georgia

Nanjing,

P.R. China

Central R&D

Technical Service North America

Wilmington,

Delaware

Natural

Hydrocolloids

Delhi, India

Technical Service

Asia Pacific

Singapore

Global Technology Footprint

45

• Follow Responsible Care* principles to ensure that safety

and environmental excellence are core values

and environmental excellence are core values

• Expand Ashland Aqualon Functional Ingredients' portfolio

of water-soluble polymers while adding

complementary adjacent technologies

that enable us to provide broader solutions

to meet our customers’ formulation needs globally

of water-soluble polymers while adding

complementary adjacent technologies

that enable us to provide broader solutions

to meet our customers’ formulation needs globally

Growth Strategy

46

Core Organic

Adjacent Organic

Acquisition

„ Geographic expansion

• China, Russia, India, Japan

and South America

and South America

„ Accelerate new product

introductions

introductions

„ Productivity … cost/unit

reduction

reduction

„ Pricing leadership

„ Capital investment consistent

with growth

with growth

„ Commercialize existing

programs … film coatings,

phosphate esters and

redispersible powders

programs … film coatings,

phosphate esters and

redispersible powders

„ Launch adjacent

technologies consistent

with strategic direction

technologies consistent

with strategic direction

„ Align resources (capital

and work force) to deliver

this growth

and work force) to deliver

this growth

„ Accelerate growth via bolt-on

acquisitions … good

opportunities and consistent

with the strategy

acquisitions … good

opportunities and consistent

with the strategy

Ashland Aqualon Functional Ingredients

Strategies

Strategies

47

Voice of Customer

Solutions Mode

Broad portfolio of

functional ingredients

Specialty Blends

A product customized to

individual customer needs

Innovation

New products to

solve clients' needs

Regulatory

Products that help

customers solve their

regulatory issues

Total Costs

Products and solutions

to drive down the total

cost of ownership

Current

State

Core products

in a narrow

technology

technology

area …

rheology

control,

water

retention,

etc.

Future State … Solutions Platform

Core products, plus additional functionality

• Broaden the rheology portfolio

• Adjacent functionality … redispersible

powders, antifoam, color, etc.

powders, antifoam, color, etc.

• Specialty blends

• Synthetic functionality

• Expand hydrocolloid functionality

Solutions Offering … How We Win!

48

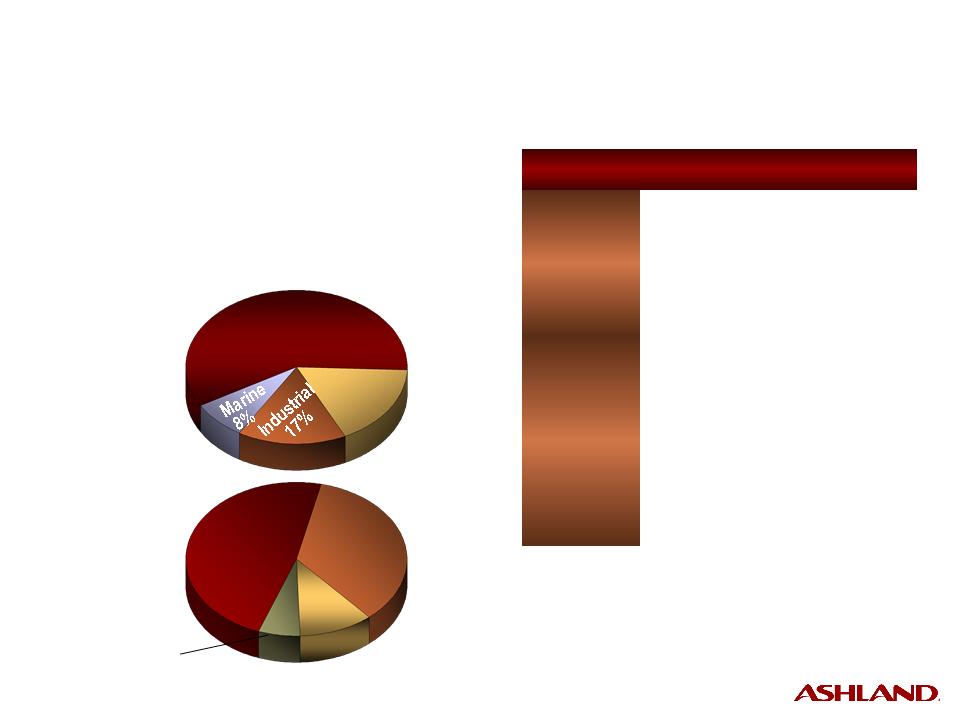

Segmenting Our Markets to Develop Our Growth Strategy

Redefined Markets

(estimated market size)

(estimated market size)

Industry

Targeted Markets

(estimated market size)

(estimated market size)

Construction

$6.2 billion

$2.1 billion

Food

$5.8 billion

$2.2 billion

Personal Care

$3.5 billion

$1.4 billion

Pharmaceutical

$2.0 billion

$1.0 billion

$2.3 billion

$1.7 billion

Coatings Additives

Energy

$1.0 billion

$0.5 billion

Specialties Solutions

$3.0 billion

$1.9 billion

Regulated Industries

Source: Internal estimates.

Market Segmentation

49

Industry

Construction

Food

Personal Care

Pharmaceutical

Coatings Additives

Energy

Specialties Solutions

Regulated Industries

Targeted Markets

(estimated market size)

$1.7 billion

Targeted Segment

Water-Based Architectural

Cementing and

Stimulation

Stimulation

Dry Mortar and Gypsum

Hair Care

Rheology and Conditioning

Oral Dosage

Binders and Coatings

Binders and Coatings

Civil Engineering

and Ceramics

and Ceramics

Bakery, Process Foods

and Beverage

and Beverage

$2.1 billion

$0.5 billion

$1.9 billion

$1.0 billion

$1.4 billion

$2.2 billion

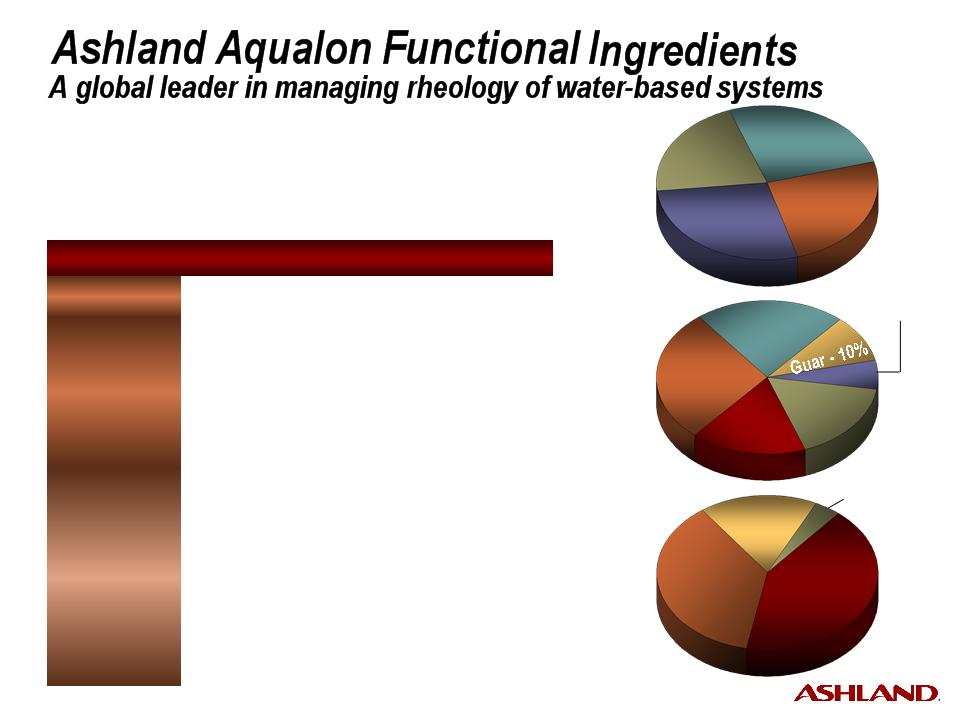

Targeting Segments to Focus and Align Resources

Source: Internal estimates.

Ashland Aqualon Functional Ingredients

Targeted Segments

Targeted Segments

50

Industry

Construction

Food

Personal Care

Pharmaceutical

Coatings Additives

Energy

Specialties Solutions

Regulated Industries

Primary Target

Future Target

Water-Based

(rheology, surfactants)

Cementing and

Stimulation

Stimulation

Dry Mortar and Gypsum

Hair Care

(rheology, conditioning)

Oral Dosage

(binders, coatings)

Civil Engineering

and Ceramics

and Ceramics

Bakery, Process Foods

and Beverage

Targeting Segments to Focus and Align Resources

Industrial Coatings

Emulsion Polymerization

Concrete

Skin Care

Oral Dosage

(disintegrants)

Targeted Segments

51

• Products have a long history of effective

performance

performance

• Strong brand recognition with Klucel HPC

• Vertical integration strategy with Aquarius

coating systems

coating systems

• Strong position in the nutritional supplement

industry

industry

Pharmaceutical

The $2.0 billion business of producing and marketing excipients (i.e., inactive ingredients)

for pharmaceuticals and nutritional supplements.

• Long approval cycles

for new formulations

for new formulations

• Pending patent

expirations for key

drugs

expirations for key

drugs

• Fragmented market

Key Challenges

• AAFI’s highest-margin

segment and relatively

recession-resistant

segment and relatively

recession-resistant

• The growth of generics

offers opportunity and

threat

offers opportunity and

threat

Health of Industry

• The formulator is

traditionally the

decision maker

traditionally the

decision maker

• Highly risk averse -

compelling value

proposition required

to dislodge incumbents

compelling value

proposition required

to dislodge incumbents

Buying Behavior

Sources of Differentiation

Economic Model and Path to Win

Target

Excipient

Market

$1.0 B

Major Competitors

Binders

$400 MM

$400 MM

Coatings

$500 MM

Immediate-release and controlled-release binders - AAFI’s

traditional focus with Klucel® HPC and Benecel® HPMC.

traditional focus with Klucel® HPC and Benecel® HPMC.

Polymers and formulated systems that deliver aesthetic (color)

and functional (controlled release, moisture barrier) properties.

AAFI introduced Aquarius coating systems in 2007.

and functional (controlled release, moisture barrier) properties.

AAFI introduced Aquarius coating systems in 2007.

Dow/Colorcon

FMC

ISP

ISP

Colorcon

Evonik

• Large industrial base needed for cost-effective

excipient manufacturing

excipient manufacturing

• Excipients are low-volume, high-value

• Continue to optimize the customer mix:

branded, generic, OTC and nutritional

branded, generic, OTC and nutritional

• Continue to build mind-share with application

studies, publications and frequent customer

seminars

studies, publications and frequent customer

seminars

• Need to improve positioning in the emerging

markets

markets

Disintegrants

$100 MM

Additives that enhance tablet disintegration. AAFI does not

participate in this space.

participate in this space.

FMC

ISP

DMV International

BASF

Source: Internal estimates.

Key Chemistries

• EC

• HEC

• HPC

• MC

• Film coatings

51

52

• Technical leadership and product performance

• Brand recognition

• Technical support and collaboration, including

regional labs

regional labs

• Global channel to market and depth of

relationships with key commercial and

technical decision makers

relationships with key commercial and

technical decision makers

Coatings

The $2.3 billion business of producing and marketing specialty additives for water-based

architectural coatings.

• Weak global economy

and paint demand

and paint demand

• Mature product lines

contribute a lot of profit

today

contribute a lot of profit

today

• Rate of growth of new

product sales

product sales

Key Challenges

• Although current crisis

hurts industry profit-

ability, long-term pros-

pects for growth are

solid, especially as

housing standards

improve in developing

world

hurts industry profit-

ability, long-term pros-

pects for growth are

solid, especially as

housing standards

improve in developing

world

Health of Industry

• Most customers value

technical excellence

in products and

technical service

technical excellence

in products and

technical service

• Customers prefer to

align with strategic

suppliers that are

innovators and have

broad portfolios

align with strategic

suppliers that are

innovators and have

broad portfolios

Buying Behavior

Sources of Differentiation

Economic Model and Path to Win

Target

Additives

Market

$1.7 B

Major Competitors

Rheology

$700 MM

$700 MM

Surfactants

$300 MM

Chemicals used to improve flow, leveling, water retention

and anti-spatter.

and anti-spatter.

Chemicals used for surface wetting, dispersion of

pigments, improved gloss and color stability.

pigments, improved gloss and color stability.

Dow/Rohm & Haas

Akzo Nobel

SE Tylose

Dow/Rohm & Haas

Rhodia

Air Products

• Requires new products and strong regional

technical service

technical service

• Must maintain premium/price leader status in

key products, e.g., HEC

key products, e.g., HEC

• Grow emerging markets via continued

investment in people

investment in people

• Grow via adjacencies that allow us to leverage

our strong channel and bring more value with

the “total solutions” approach

our strong channel and bring more value with

the “total solutions” approach

• Maintain HEC market leadership with

technology and manufacturing capacity

technology and manufacturing capacity

Foam & pH

Control

Control

$400 MM

Chemicals used to neutralize and stabilize paint.

Cognis

BYK

Rhodia

Preservatives

$300 MM

Chemicals used to ensure long-term stability.

Dow/Rohm & Haas

Arch

Key Chemistries

• HEC

• Synthetic (Aquaflow)

• Phosphate esters

• Antifoams

Source: Internal estimates.

52

53

• Technical depth in focus areas

• Global account management

• Chemistry based on naturally occurring raw

materials

materials

Personal Care

The $3.5 billion business of producing and marketing specialty additives for the

personal-care and cosmetics consumer markets.

• 3- to 5-year

development timeline

development timeline

• Replacement of cationic

chemistry with less eco-

toxic molecules

chemistry with less eco-

toxic molecules

• Competition from small,

lower-priced suppliers

in China and India

lower-priced suppliers

in China and India

Key Challenges

• Recession is hitting

even P&G and Unilever

hard as retailers manage

to lower inventories and

consumers switch to

generics

even P&G and Unilever

hard as retailers manage

to lower inventories and

consumers switch to

generics

Health of Industry

• Customers value

technical excellence

in products and product

support

technical excellence

in products and product

support

• Customers value

interaction and input

to their R&D processes

interaction and input

to their R&D processes

Buying Behavior

Sources of Differentiation

Economic Model and Path to Win

Target

Specialty

Chemicals

Market

$1.4 B

Major Competitors

Conditioning

$300 MM

Rheology

Control

Control

$300 MM

Chemicals that are substantive to hair and skin and provide

conditioning performance such as softness, smoothness

and de-tangling.

conditioning performance such as softness, smoothness

and de-tangling.

Chemicals used to provide flow control, formulation

stabilization, syneresis-control and suspension of active

ingredients in a wide variety of personal care compositions,

including toothpaste, shampoos, shower gels, shaving gels

and conditioners

stabilization, syneresis-control and suspension of active

ingredients in a wide variety of personal care compositions,

including toothpaste, shampoos, shower gels, shaving gels

and conditioners

Rhodia

BASF

ISP

• Must maintain premium/price leader status

in key products, e.g., Natrosol HEC and Klucel

HPC

in key products, e.g., Natrosol HEC and Klucel

HPC

• Follow multinational corporations into

emerging regions and source the demand

from local plants at price points required

to win in these geographies

emerging regions and source the demand

from local plants at price points required

to win in these geographies

• Engage with multinational corporations

at R&D level and focus R&D programs

on a key few opportunities where AAFI

is competitively positioned to win

at R&D level and focus R&D programs

on a key few opportunities where AAFI

is competitively positioned to win

Dow

Noveon

Other

Specialty

Polymers

Specialty

Polymers

$800 MM

Silicones, proteins and fixative polymers. AAFI does not

participate in this space today.

participate in this space today.

Momentive

Dow Corning

BASF

ISP

Akzo

Key Chemistries

• CMC

• HEC

• Guar

Source: Internal estimates.

53

54

• Technical leadership and product performance

• Product portfolio scope

• Brand recognition

• Large-scale Chinese operations

with high quality … Tianpu joint venture

with high quality … Tianpu joint venture

• First-mover abilities in establishing JDAs

with key clients

with key clients

• Global channel

• Sustainability

Construction

The $6.2 billion business of producing and marketing additives for the tile cement,

gypsum and exterior insulation markets.

• Cellulose supply and

costs

costs

• Commoditization

• Mature vs. emerging

markets

markets

• Changing construction

practice

practice

• Cost vs. performance

• Regional needs

Key Challenges

• MC global demand has

grown steadily over the

past 10 years. Continued

growth expected, but

economic crisis has

impacted this market

grown steadily over the

past 10 years. Continued

growth expected, but

economic crisis has

impacted this market

• Redispersible powders

will continue to grow

as more formulated

products are developed

and job-site mixing is

reduced in emerging

regions

will continue to grow

as more formulated

products are developed

and job-site mixing is

reduced in emerging

regions

Health of Industry

• Customers value

technical excellence

in products and product

support

technical excellence

in products and product

support

• Customers expect just-

in-time supply and

formulation support

in-time supply and

formulation support

Buying Behavior

Sources of Differentiation

Economic Model and Path to Win

Target

Additives

Market

Market

$2.1 B

Major Competitors

Cellulose

Ethers

Ethers

$1.1 B

Functional

Additives

$100 MM

MC, HEC and EHEC used for water retention and rheology

control to achieve workability, adhesion and strength.

control to achieve workability, adhesion and strength.

Starch ethers, air-entrainers, polyacrylamides, set-time

additives and defoamers used to enhance workability and

durability.

additives and defoamers used to enhance workability and

durability.

Dow Wolff

SE Tylose

Samsung

Akzo

Chinese suppliers

• Tianpu joint venture to serve low-end and

price-sensitive markets

price-sensitive markets

• Must maintain premium/price leader status

• Grow in emerging markets via investment

in plants/people to seed the market as

technology advances

in plants/people to seed the market as

technology advances

• Technology differentiation via formulation

expertise

expertise

• Grow mature markets via adjacencies; however,

need continuous product evolution

to offer alternatives to lower-priced products

need continuous product evolution

to offer alternatives to lower-priced products

Redispersible

Powders

$900 MM

Redispersible latex polymers added to improve adhesion,

flexibility and water repellency.

flexibility and water repellency.

Wacker

Akzo (Elotex)

Dairen

Dow

Hexion

BASF

Avebe

Agrana

Emsland

Sichel (Henkel)

Cognis

Key Chemistries

• MC

• Redispersible powders

Source: Internal estimates.

54

55

Guar and guar derivatives used for rheology control and

proppant carrier for high-pressure fracturing of gas wells.

proppant carrier for high-pressure fracturing of gas wells.

• Innovative manufacturer of novel products

• Industry application expertise

• Broad portfolio of additives for drilling,

stimulation and cementing

stimulation and cementing

• Global manufacturing footprint

Energy

The $1.0 billion business of producing and marketing drilling, well-stimulation

and cementing additives for the production of oil and natural gas.

• Current downturn in

global oilfield market

global oilfield market

• Global applications

expertise

expertise

• Geographical expansion

• Emerging market

competitors

competitors

Key Challenges

• Current downturn in mar-

ket due to lower global

price/demand for oil and

natural gas. N. A. rig

count down to levels last

seen in 2004

ket due to lower global

price/demand for oil and

natural gas. N. A. rig

count down to levels last

seen in 2004

• Industry turnaround

expected 2010

expected 2010

Health of Industry

• Customers value techni-

cal excellence in prod-

ucts and product support

cal excellence in prod-

ucts and product support

• Customers expect to buy

a full range of products

from a single supplier

a full range of products

from a single supplier

• Customers value

suppliers with global

reach both commercial

and technical

suppliers with global

reach both commercial

and technical

Buying Behavior

Sources of Differentiation

Economic Model and Path to Win

Target

Energy

Market

Market

$500 MM

Major Competitors

Drilling

Additives

$200 MM

Additives

$200 MM

Well

Stimulation

Stimulation

$200 MM

Cellulosic ethers (CMC) used for rheology and filtration

control as additives with drilling muds.

control as additives with drilling muds.

CP Kelco

Lamberti

Lamberti

Dow Wolff

Benchmark

Rhodia

Economy Polymer

Other

• Requires supply chain efficiency and ability

to maintain local inventory near well sites

to maintain local inventory near well sites

• Must maintain premium/price leader status

in key products, e.g., cementing, synthetics

in key products, e.g., cementing, synthetics

• Grow emerging markets via investment

in plants/people

in plants/people

• Expand global applications expertise

to support regional requirements

by service companies

to support regional requirements

by service companies

Cementing

Additives

Additives

$100 MM

Cellulosic ethers (HEC) used for rheology and fluid loss and

gas migration control as additives into high-density cement.

gas migration control as additives into high-density cement.

Dow Wolff

SE Tylose

Clariant

Key Chemistries

• CMC

• Guar

Source: Internal estimates.

55

56

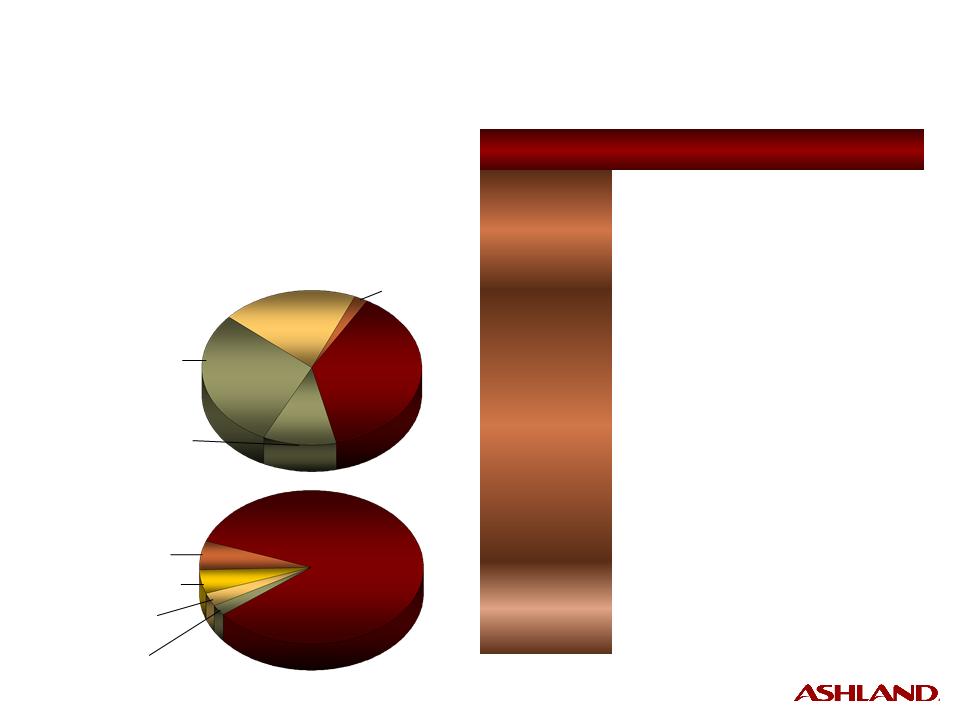

Significant Potential for Growth

One-Step Adjacencies

Superplasticizer

3%

Enzymes

6%

Silicones

5%

Diluents

7%

Film Coatings

6%

Emulsifiers

11%

Antifoams

6%

Redispersible

Powders

6%

Dispersants

13%

Biocides

15%

Surfactants

and Other

22%

Total = $9 Billion

Core

Total = $4 Billion

Total = $23 Billion

Cellulose

Ethers and

Resins

Resins

17%

One-Step

Adjacencies

41%

Natural

Hydrocolloids

19%

Synthetics

23%

CMC

$800 MM

Resins

$1,100 MM

MC

$1,200 MM

HEC

$700 MM

HPC

$80 MM

(Water-Soluble Polymers)

EC

$80 MM

Grow the Core First ... Then Adjacencies

57

AAFI 2008 (MT) | Food | Pharma | Personal Care | Energy | Construction | Specialties Solutions | Coatings Additives | |

HEC | 42,000 | L | L | M | L | L | H | |

CMC | 55,000 | H | M | H | M | L | ||

MC | 39,000 | M | L | H | M | |||

EC | 900 | L | H | |||||

HPC | 1,900 | H | L | |||||

Guar | 53,900 | M | M | H | L | |||

Polyterpene Resin | 31,500 | L | H | |||||

Film Coatings | 100 | H | ||||||

Redispersible Powders | 300 | H | ||||||

Synthetic (Aquaflow) | 600 | L | H | |||||

Phosphate Esters | 1,000 | H | ||||||

Antifoams | 200 | L | M | H |

Relative Consumption: H = High, M = Medium, L= Low

Products by Industry Segment

58

ü Market size and growth rate

ü Channel strategy

ü Target existing customer base

ü Competitive landscape

ü Intellectual-property landscape

ü Technical capability requirements

ü Relative cost position vs. market leader

ü Value chain analysis

ü Regulatory environment and trends

ü Formulation expertise

ü Voice-of-customer interviews

One-Step

Adjacencies

Adjacencies

Total = $9 Billion

Superplasticizer

3%

Enzymes 6%

Silicones 5%

Diluents 7%

Film Coatings

6%

Emulsifiers

11%

Antifoams 6%

Redispersible

Powders

6%

Dispersants

13%

Biocides

15%

Surfactants

and Other

22%

Adjacent Products Selection Criteria

59

Core Organic

Adjacent Organic

Acquisition

„ Geographic expansion

• China, Russia, India, Japan

and South America

and South America

„ Accelerate new product

introductions

introductions

„ Productivity … cost/unit

reduction

reduction

„ Pricing leadership

„ Capital investment consistent

with growth

with growth

„ Commercialize existing

programs … film coatings,

phosphate esters and

redispersible powders

programs … film coatings,

phosphate esters and

redispersible powders

„ Launch adjacent

technologies consistent

with strategic direction

technologies consistent

with strategic direction

„ Align resources (capital

and work force) to deliver

this growth

and work force) to deliver

this growth

„ Accelerate growth via bolt-on

acquisitions … good

opportunities and consistent

with the strategy

acquisitions … good

opportunities and consistent

with the strategy

Ashland Aqualon Functional Ingredients

Strategies

Strategies

60

KeyBanc Analyst Day

August 14, 2009

August 14, 2009

Formula for growth.

61

Investment Highlights

• Among top 10 specialty chemicals companies worldwide

– Diversified business portfolio serving wide range of end markets

– Leading market positions across platform

• Strong emphasis on cash flow generation and debt pay-down

– Reduced debt by $616 million in eight months since Hercules acquisition

• Over-delivering on cost-reduction program

– Achieved $287 million in total Ashland run-rate savings at June 30,

three months ahead of plan

three months ahead of plan

– Total Hercules run-rate synergies of $130 million by fiscal year-end 2010

• Additional sources of cash available

– Working capital, auction rate securities, divestitures

• Management committed to conservative financing structure

– Total leverage of 2.4x

– Aim to achieve investment-grade credit statistics within 12 months

• Equity market capitalization of approximately $2.0 billion

• Experienced management team

AAFI = Ashland Aqualon Functional Ingredients

AHWT = Ashland Hercules Water Technologies

BWT = Boiler Water Treatment(s)

C&I = Commercial & Institutional

CMC = Carboxymethylcellulose

CWT = Cooling Water Treatment(s)

EC = Ethylcellulose

EH&S = Environmental, Health & Safety

EMEA = Europe, Middle East, Africa

FTEs = Full-time employees

HEC = Hydroxyethylcellulose

HPC = Hydroxypropylcellulose

MB = Microbiocide(s)

MC = Methylcellulose

PAM = Polyacrylamide(s)

RDP = Redispersible powders

® Registered trademark, Ashland or its subsidiaries

* Trademark owned by third party

62

Abbreviations