UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act File Number 811-21653

DOMINI ADVISOR TRUST

(Exact Name of Registrant as Specified in Charter)

536 Broadway, 7th Floor, New York, New York 10012

(Address of Principal Executive Offices)

Amy Domini Thornton

Domini Social Investments LLC

536 Broadway, 7th Floor

New York, New York 10012

(Name and Address of Agent for Service)

Registrant’s Telephone Number, including Area Code: 212-217-1100

Date of Fiscal Year End: July 31

Date of Reporting Period: January 31, 2008

Item 1. | Reports to Stockholders. |

A copy of the report transmitted to stockholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 follows.

TABLE OF CONTENTS

2 |

| Letter from the President |

4 |

| Domini News |

5 |

| The Way You Invest Matters: Human Rights |

11 |

| The Way You Invest Matters: Activism |

|

| Fund Performance and Holdings |

12 |

| Economic and Market Background |

15 |

| Domini Social Equity Portfolio |

21 |

| Domini European Social Equity Portfolio |

27 |

| Domini PacAsia Social Equity Portfolio |

35 |

| Domini European PacAsia Social Equity Portfolio |

44 |

| Expense Example |

47 |

| Financial Statements |

| Domini Social Equity Trust | |

| Domini European Social Equity Trust | |

| Domini PacAsia Social Equity Trust | |

| Domini European PacAsia Social Equity Trust | |

62 |

| Financial Statements |

| Domini Social Equity Portfolio | |

| Domini European Social Equity Portfolio | |

| Domini PacAsia Social Equity Portfolio | |

| Domini European PacAsia Social Equity Portfolio | |

76 |

| Proxy Voting Information |

76 |

| Quarterly Portfolio Schedule Information |

THE WAY YOU INVEST MATTERS ® |

|

LETTER FROM THE PRESIDENT

Dear Fellow Shareholders:

In this year of tough economic news and a hard-fought presidential campaign, calls for change are in the air.

This represents, I think, more than dissatisfaction with American progress. It reflects also a determination that government should once again take up its historic role of promoting the common good and its obligation to regulate corporate conduct.

That would certainly be a welcome development.

In the meanwhile it has been up to social investors like you to make change happen.

Many of the issues being aired during this interesting campaign season are ones we social investors have been talking about for years. We look closely at how companies use lobbyists and campaign contributions to maximize their political influence, at the social costs of for-profit healthcare that leaves so many behind, at companies’ responses to climate change, and at the profound impact of government contracts and tax incentives on crucial matters of war and peace, energy development and human capital.

In this year’s Semi-Annual Report, we report on issues of basic human dignity. On behalf of our shareholders, we encourage companies to use their influence to help end the genocide in Darfur, to protect freedom of expression, and to provide safe conditions and fair pay to workers in the far-flung factories that make the products we use every day.

Your commitment to social investing makes all the difference on these and many other important issues. The progress we make is slow, and requires long-term commitment. As Martin Luther King said, “the arc of the moral universe is long, but it bends toward justice.”

This has been a difficult period for investors. Over the past six months, stock markets are down across the U.S., Europe, and Asia, a decline precipitated in part by the U.S. housing slump and the credit crisis that came in its wake. A primary reason for the collapse of the subprime lending market is that unscrupulous mortgage lenders made loans — often with deceptive terms — that people could not afford to repay. Then they bundled those unsustainable mortgages into securities with unrealistically high credit ratings.

Domini research has long focused on predatory lending, and we do our best to avoid companies that practice it. We sounded the alarm a decade ago. Our commitment to community development investments demonstrates and supports a better way to serve low-income people. This, in a nutshell, is why what we social investors do is so important, for people and the planet. A groundswell of change is building, and your investments are a part of it.

2

THE WAY YOU INVEST MATTERS ® |

|

We are honored that our shareholders share this vision, and continue to place their trust in us. Thank you, as always, for your decision to invest with Domini.

Very truly yours,

Amy Domini

amy@domini.com

KEEP IN TOUCH WITH DOMINI |

A report like this comes twice a year, but your dollars work for change all year long. Now there’s a great way to stay in touch. Sign up for Domini Updates at www.domini.com to receive:

• | Our e-newsletter Investing Matters, with news on how your funds are making a difference |

• | Domini Action Alerts that help you speak out on issues from child labor to global warming. |

We will not “spam” you, and we will never sell or rent your email address to anyone, for any reason. (Please visit our website for more information about our Privacy Policy.) And you can, of course, unsubscribe at any time.

If you invest through a financial advisor, brokerage firm, or employer-sponsored retirement plan, you may be able to sign up for paperless E-Delivery of your statements and reports. Just ask your advisor or plan sponsor how to receive your documents electronically. It can reduce your carbon footprint, save trees, and unclutter your life, all with just a few strokes of your keyboard!

3

THE WAY YOU INVEST MATTERS ® |

DOMINI NEWS

Domini Wins “Social Capitalist” Award From Fast Company: Domini Social Investments was among the winners of Fast Company magazine’s fifth annual Social Capitalist Award, in the first year that for-profit companies were eligible for selection. These awards recognize organizations and companies that use the tools of business to solve the world’s most pressing social problems. (Winners were featured in the December/January 2008 issue of Fast Company, with expanded online coverage at www.fastcompany.com.)

Responding to this honor, Amy Domini said, “This award is a tribute to the Domini Funds’ thousands of investors, who put their investments to work not only for their families’ future but to build a better future for all of us. Our firm is built on the idea that the way you invest matters — that investors, if we harness our power and think beyond next quarter’s profits, can change companies, change Wall Street, and ultimately change the world. In choosing to invest sustainably and responsibly, our shareholders make change happen every day.”

Amy Domini Honored by Yale: In October 2007, Yale University’s Berkeley Divinity School presented Amy Domini with an honorary doctorate. In its citation, Yale said the degree was awarded in recognition of her “ability to turn compassion into action” and an influence that has “spurred hundreds of companies to evaluate their impact on the environment and human rights.”

Accepting the degree, Amy spoke of the role of faith in the development of her ideas. In the end, she said, finance and capitalism are still subject to basic conceptions of right and wrong. By shaping a career in line with one’s faith and values, she discovered, one could become “a powerful force for good.”

Conventional Funds Still Voting No: The latest data from FundVotes.com has confirmed that U.S. mutual fund companies overwhelmingly side with management when voting their proxies. The 54 fund groups surveyed supported approximately 90.7% of management proposals during the year ended June 30, 2007, but only 35.2% of shareholder proposals. By contrast, Domini supported 67% of management proposals and 63% of shareholder proposals for the same period, making it one of the most activist fund groups surveyed.

New Fund Name: The Domini EuroPacific Social Equity Portfolio has a new name: Domini European PacAsia Social Equity Portfolio.

4

THE WAY YOU INVEST MATTERS ® |

THE WAY YOU INVEST MATTERS: HUMAN RIGHTS

At the core of socially responsible investing lies a commitment to universal human dignity and the idea that profits should not come at the cost of anyone’s fundamental rights.

As the world economy becomes ever more globalized, this simple ideal has become more difficult to attain. While some companies have been directly implicated in severe abuses, more often corporations are confronted with the human rights challenges that come with doing business — sourcing raw materials, contracting with local manufacturers, seeking to offer products and services — in countries where abuses are common or even endemic.

Human rights is a complex and difficult subject for investors. It touches many different aspects of a company’s activities, including relationships with suppliers, employees, communities, customers, and governments. Social investors have been playing a critical role by alerting corporations to their human rights obligations, encouraging respect for international norms, and building the demand for consistent, reliable data so that corporate behavior can be more accurately assessed, and abuses brought to light and addressed. We look at the codes of conduct companies have adopted and the countries where they operate to assess the risk of human rights abuses. Conversations with company management and human rights organizations are also often helpful in understanding the role a company is playing. Comparable, reliable data, however, is generally unavailable.

In our discussion below, we focus mainly on companies held by the Domini Funds as of January 31, 2008. Some of the companies noted here are leaders in their industries. Others are just beginning to grapple with these difficult issues. Just as there are few perfect people, there are few perfect companies. We expect companies to responsibly address the real challenges they face, and we expect them to do their part to uphold universal human dignity wherever they do business. In this brief report we are able to touch on only a few areas of human rights. There are many other stories to tell, and we look forward to telling them in future reports.

Though protecting and promoting human rights is often considered purely the role of government, we believe that corporations, investors, and consumers also bear responsibility. Human rights is everyone’s business. Through this report, we hope to convey some of the work that corporations in your portfolio are doing, and the role that Domini is playing on your behalf to protect and promote universal human dignity.

Domini’s Response

Domini’s Global Investment Standards address the relationship of companies to the communities — global, national, and local — in which they operate. These standards encompass various aspects of human rights,

5

THE WAY YOU INVEST MATTERS ® |

including freedom of speech; protection of minority and indigenous peoples and their cultures; rights of workers to a safe, healthy workplace and fair compensation; and endorsement of international standards in areas like labor, health, product quality, and children’s rights.

Guided by these standards, we seek to promote universal human dignity through our research, shareholder activism, and commitment to community development.

Domini’s team of in-house research analysts evaluates companies on a range of human rights issues. Our goal is to identify companies that are responsibly addressing the key sustainability challenges of their industry. By including human rights considerations in our process, we are helping to raise expectations for corporate behavior among investors, the public, and the corporations we are evaluating.

This issue must also be considered in the context of a larger question: Just what are a corporation’s obligations regarding human rights in the countries and communities where it does business? And how can companies be held accountable for consistently and constructively exercising that responsibility?

Some companies have volunteered to take on these difficult questions and to work together to provide guidance to the corporate community. The Business Leaders Initiative on Human Rights has produced A Guide for Integrating Human Rights into Business Management, produced in cooperation with the UN Global Compact, a framework for businesses that wish to align themselves with ten principles regarding human rights, labor, the environment, and anticorruption. Of the 13 corporate members of the Business Leaders Initiative, six — Barclays, Coca-Cola, Gap Inc., Hewlett-Packard, Novartis, and StatoilHydro — were held in the portfolios of the Domini Funds as of January 31.

The United Nations is also actively struggling with these questions. In 2007, Domini participated in a session convened by the UN High Commissioner on Human Rights, focusing on human rights and the financial sector, and a later brainstorming session to help plan the work of the special representative appointed by the UN Secretary General to help clarify standards of corporate responsibility regarding human rights. Domini continues to provide our input on this important process.

For many years, Domini has worked with a range of concerned investors and human rights organizations in the wider effort to clarify — and inculcate — human rights standards for corporate behavior. One of the most effective of these has been the Interfaith Center on Corporate Responsibility (ICCR), with which we have partnered on many shareholder campaigns for more than ten years. For the past two years, we have helped lead ICCR’s efforts to address working conditions in corporate supply chains.

6 The Way You Invest Matters: Human Rights

THE WAY YOU INVEST MATTERS ® |

Here are more examples of ways that your investment in the Domini Funds is making a difference for human rights:

Fighting Genocide in Sudan

With the steady increase in economic globalization, global banks and other major financial institutions provide the credit, financing, and liquidity that make it possible for companies and governments to do business around the world. As a result, those institutions have the potential to be an important influence on human rights.

Five years into a campaign of genocide by government-backed militias in the Sudanese province of Darfur, atrocities continue to take place on a massive scale. Working with Amnesty International, the Genocide Intervention Network, and other concerned investors, Domini met in recent months with large U.S. banks including Citigroup and JPMorgan Chase. We are encouraging them to use their influence with the companies they invest in — as well as the investors, companies, and governments they serve — to help end the ongoing genocide in Darfur.

In our Funds, Domini seeks to avoid investing in companies whose activities provide direct benefits to the Sudanese government, or that are otherwise complicit in human rights abuses in Sudan. Domini shares information about corporate activities in Sudan that we have acquired through our independent research with other investors and organizations working against the Darfur genocide.

Encouraging Internet Freedom

The Internet and telecommunications technologies are powerful tools for facilitating free speech and disseminating information, organizing political activity, promoting democracy, and exposing human rights violations. Protecting them from pressure by repressive governments is an important challenge. Domini is working as part of a multi-stakeholder group — including France Telecom, Google, Microsoft, TeliaSonera, Vodafone, and Yahoo,* and a range of human rights groups and academics — to develop principles to protect freedom of expression and privacy on the Internet and other communication technologies. Recently, Domini filed a shareholder resolution calling on Cisco Systems, which has not joined this group, to report on its involvement with repressive regimes that seek to censor Internet content or restrict citizens’ access to the Internet . The resolution achieved a significant 36% vote of support.

Focus on: Improving Global Working Conditions

Over the past few decades, much of U.S. manufacturing has shifted to the developing world, where labor costs are lower. In making this transition, companies have increasingly outsourced production to separately owned, locally based contract manufacturers. These facilities vary tremendously, but some have been marked by harsh working conditions, low pay, and the exploitation of children and even slave laborers. The risks to both workers

The Way You Invest Matters: Human Rights 7

THE WAY YOU INVEST MATTERS ® |

and companies are amplified by the fact that many companies cannot identify the full breadth and scope of their supply chain, which may reach all the way from a modern production facility in China to a cotton field in Central Asia.

Ensuring decent working conditions in corporate supply chains is an unusually complex problem, and progress has been slow. Companies in the clothing industry were among the first to face public controversy and to take action, followed by toy companies and electronics companies. Domini and other concerned investors have encouraged companies to publish the data on their supply chains that can help to evaluate their performance. In addition to providing public accountability, that data has enabled companies to better understand the challenges they face, and to work to solve problems that previously remained hidden.

By working with industry leaders, we hope to create momentum — and pressure — for their competitors to make similar improvements. One sign of progress is the increasing number of companies that have developed codes of conduct for their suppliers, and that monitor factories with the use of their own or third-party auditors. The Electronic Industry Citizenship Coalition, created in 2004, is an example of an industrywide effort to set basic labor and environmental standards for suppliers in an industry with an unusually complex supply chain. The 32 corporate members of the EICC Group, including Apple, Dell, Hewlett-Packard, and IBM, have agreed to work together to improve conditions in the global electronic supply chain. Domini has provided input over the past few years through periodic stakeholder consultations as the group worked to develop audit protocols, questionnaires, and other monitoring tools.

Promoting International Standards

Domini encourages companies to adopt comprehensive labor standards for their operations and their suppliers that incorporate the core conventions of the International Labor Organization (ILO). These conventions address the right to organize and bargain collectively, child labor, forced labor, discrimination, and equal pay for equal work. Although the ILO’s conventions apply to governments, we have worked with a number of companies to incorporate the ILO’s “core conventions” into their formal policies. In 2005, for example, we convinced Apple to adopt its first code of conduct, setting labor and environmental standards for its supply chain.

According to the ILO, the right to freely associate, including the right to form or join a union of one’s choice, and to bargain collectively for the terms of one’s employment, are fundamental labor rights. Human Rights Watch has reported, however, that U.S. labor law falls short in protecting these fundamental rights. In the fall of 2007, Domini filed a shareholder resolution urging Cummins to adhere to international standards in its relationships with labor unions. We are currently in dialogue with Cummins management to work through these complicated issues. Domini also co-filed its first shareholder resolution in Europe last year, addressing

8 The Way You Invest Matters: Human Rights

THE WAY YOU INVEST MATTERS ® |

allegations of anti-union activity in the U.S. by a subsidiary of the British transportation company FirstGroup.*

Domini has been in dialogue with Disney since 1996, when the company created its Code of Conduct for Manufacturers and International Labor Standards program. The program reportedly includes factory monitoring and remediation as well as education and communication with internal business units, licensees, and vendors. Disney also works with others committed to improving labor conditions, including socially responsible investors and multilateral institutions. The company has reportedly carried out tens of thousands of factory audits in more than 50 countries. As an outgrowth of that work, Domini has been working with McDonald’s and Disney on a multi-year project seeking to sustain factory compliance with acceptable labor standards.

Encouraging Transparency

For years, two of America’s biggest and most successful clothing retailers, Nike and Gap, were the target of criticism by activists on sweatshop labor issues. In recent years, in addition to extensive efforts to monitor their supply chains and address poor working conditions, both companies responded by taking steps to increase transparency. Gap’s first Social Responsibility Report, released in 2004, was developed in cooperation with Domini and a small group of social investors, in response to a shareholder resolution we filed. The report marked the first time that a clothing retailer had publicly rated the way the factorie s in its global supply chain treated their workers. Gap’s third and most recent report, for 2005-2006, noted that the company conducted 4,316 inspections in 2,053 garment factories around the world during 2006 — more than 99% of its garment factory base. Domini has provided feedback to Gap during the drafting of each of its reports.

In its 2004 Corporate Responsibility report, Nike announced that it was publishing on its website the names and addresses of each of its factories. In addition, Nike and Hewlett-Packard, in their reports that year, reported on noncompliant factories using charts similar to those in Gap’s first report — bringing us one step closer to standardized reporting in this area. Unfortunately, most companies have resisted a commitment to greater accountability through annual public reporting, and this type of reporting remains voluntary. Nevertheless, the expectations of corporations have changed dramatically.

Correcting Abuses

Gap faced renewed controversy in 2007, when the British newspaper The Observer reported that children as young as ten years old were doing hand embroidery for up to 16 hours a day in a workshop in Delhi.

These revelations showed the persistence of labor rights violations, including child labor, in certain emerging markets, and Gap’s response illustrates that leading companies now recognize the importance of

The Way You Invest Matters: Human Rights 9

THE WAY YOU INVEST MATTERS ® |

addressing abuses quickly and comprehensively. The company, which said it learned of the abuses on October 22, announced on November 14 that it had “launched a thorough investigation, cancelled the product order in question and made sure the garment would never be sold.” By November 2, the company had convened all of its Indian suppliers to stress its “zero tolerance” policy on child labor. The exploited children were placed under the care of a nonprofit group affiliated with Global March Against Child Labour, an organization founded and led by one of the world’s leading defenders of children’s rights. Gap is partnering with the Global March to develop an independent oversight and monitoring program to address hand embroidery and beadwork for Gap products — work that is generally not done in factories, but in the “informal sector” of India’s economy. Gap also committed itself to ensure the children receive “access to schooling, financial support until they reach the legal working age, and job opportunities thereafter.”

All of us share a responsibility to end child labor, as well as other abuses of human rights. We hope that this recent controversy will underline the importance of shedding light on the practices of the many companies that are less well known, and less transparent.

______________* | As of January 31, 2008, Yahoo and FirstGroup were not held in any of the Domini Funds’ portfolios. |

The holdings discussed above can be found in the portfolios of the Domini Funds, included herein. The composition of the Funds’ portfolios is subject to change.

As of January 31, 2008, the companies discussed above were held in the portfolios of the following Domini Funds: Apple, Cisco Systems, Citigroup, Coca-Cola, Cummins, Dell, Gap Inc., Google, Hewlett-Packard, IBM, JPMorgan Chase, McDonald’s, Microsoft, Nike, and Walt Disney were held by the Domini Social Equity Portfolio. Barclays, France Telecom, Novartis, StatoilHydro, and Vodafone were held by the Domini European Social Equity Portfolio and by the Domini European PacAsia Social Equity Portfolio. TeliaSonera was held by the Domini European PacAsia Social Equity Portfolio. The composition of the Funds’ portfolios is subject to change.

Unlike other mutual funds, the Domini Social Equity Portfolio, Domini European Social Equity Portfolio, Domini PacAsia Social Equity Portfolio, and Domini European PacAsia Social Equity Portfolio seek to achieve their investment objectives by investing all of their investable assets, respectively, in separate portfolios with identical investment objectives called the Domini Social Equity Trust (DSET), Domini European Social Equity Trust (DESET), Domini PacAsia Social Equity Trust (DASET), and Domini European PacAsia Social Equity Trust (DUSET). References to each Domini Fund include the applicable Domini Trust, unless the context otherwise requires.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The preceding profiles should not be deemed an offer to sell or a solicitation of an offer to buy the stock of any of the companies noted, or a recommendation concerning the merits of any of these companies as an investment.

10 The Way You Invest Matters: Human Rights

THE WAY YOU INVEST MATTERS ® |

|

THE WAY YOU INVEST MATTERS: ACTIVISM

Below are a few recent highlights of Domini’s shareholder activism, which each year includes meetings with dozens of companies on a wide range of important issues. (For more information, visit www.domini.com.)

Shareholder Resolutions: For the 2008 proxy season, Domini filed 20 shareholder resolutions, and was the lead filer for 12, on issues including political contributions, the climate crisis, and product safety.

Toxic Substances: Domini gained a strong vote of 36.1% for a resolution asking the medical products company Becton Dickinson to evaluate its policy on brominated flame retardants, which may pose a risk to human health.

As part of a dialogue led by the As You Sow Foundation, Domini helped convince Target to reduce its use of toxic PVC plastic in infant products, children’s toys, shower curtains, packaging, and accessories.

Climate Change: The Carbon Disclosure Project, which now represents investors with over $57 trillion of assets, is a catalyst for productive dialogue on climate change between corporations and their shareholders. More than 1,300 companies have reported on their carbon emissions through the CDP. To help increase this total, Domini recently wrote to 194 companies in 23 countries that had not responded to its most recent annual survey.

Facing Domini’s shareholder resolution (later withdrawn), Lowe’s committed to improve its sustainability reporting, most notably on its policies for purchasing the wood products sold in its stores. Domini recently joined the Boreal Leadership Council, an organization committed to protecting one of the world’s largest forest ecosystems.

Political Contributions: Following earlier successes with Verizon and Hewlett-Packard, Domini filed shareholder resolutions calling on American Express and AT&T to disclose their political contributions. We were pleased to withdraw the resolution with American Express when the company agreed to disclose its contributions. Do mini is also asking companies to disclose contributions to trade associations — an increasingly important avenue for political influence.

Shareholder Rights: In July 2007, the SEC raised ideas challenging the right to file nonbinding resolutions. Domini’s Action Alerts on the subject generated more than 2,000 responses, and Domini submitted three comment letters, including one on behalf of 47 institutional investors and service providers from ten countries representing $1.4 trillion in assets. The SEC decided to take no action on this issue, at least for now.

11

FUND PERFORMANCE AND HOLDINGS

ECONOMIC AND MARKET BACKGROUND

U.S. Markets Financial markets experienced significant volatility during the six-month period ending January 31, 2008. The S&P 500 Index declined –4.32% and the bond market (measured by the Lehman Brothers Intermediate Aggregate Index, or LBIA) returned 6.75%. A variety of factors led many analysts to note an increasing risk of recession in 2008:

• | The employment picture weakened — unemployment reached 5% in December, when the economy added only 18,000 new jobs, the smallest monthly increase in four years. |

• | The housing market in the U.S. continued to deteriorate, and sales of new homes dropped 34% during 2007, the biggest decline since 1991. Mortgage foreclosures began to rise dramatically. The meltdown of the subprime mortgage market sparked broad concerns throughout the credit markets, and many large financial companies took hits to their profits, reputations, and share prices as their bets on complex subprime mortgage securities went sour. |

• | Oil prices increased significantly, reaching a record price of $100 per barrel in January 2008. This was exacerbated by the weakness of the U.S. dollar, since oil prices are denominated in dollars. |

Bond markets turned in a relatively strong performance during the six months, and saw increased demand for higher-quality bonds as cautious investors sought out more conservative investments.

Ending a long series of rate increases, the Federal Reserve responded to deteriorating economic conditions and shaky markets by reducing short-term interest rates five times, by a total of 2.25%. This included two cuts during a period of eight days in January, the first a dramatic 0.75% cut implemented between the Fed’s regularly scheduled meetings, during a week in which global stock markets were falling sharply. Bond yields declined and prices increased for both long-term and short-term bonds. Long-term bonds continued to pay higher yields than short-term bonds, reversing the inverted yield curve seen in 2006 and earlier in 2007.

European Markets European stock markets declined sharply during the six months ending January 31, 2008, with the MSCI Europe Index declining by –11.59% in local currency terms. However, the strength of European currencies compared to the dollar counterbalanced at least a portion of this decline for U.S.-based investors, resulting in a total return of –7.31% in dollar terms.

12

Economic and business signals were decidedly mixed:

• | Unemployment in the European Union, while still high by U.S. standards, continued to decline, to 7.2% at the end of 2007. Labor productivity lagged, however, with the estimated growth for 2007 at only 1.4%. |

• | The strong euro helped drive a significant decline in business confidence, as European exports become more expensive, hurting export-driven economies like Germany’s. |

• | Inflation has become a concern, as December’s 3.1% EU inflation rate was the highest since May 2001. |

• | The financial sector also caused concern, because several European banks held large quantities of troubled U.S. subprime mortgage assets and were slow to make the necessary write-offs. |

In confronting the climate crisis, the EU moved towards imposing the world’s strictest standards for CO2 emissions from vehicles, building on Europe’s previous leadership in regulation of industrial emissions.

Asian Markets As in Europe, Asian stock markets declined sharply during the six months ended January 31, 2008, with the MSCI All Country Asia Pacific Index down by –12.73% in local currency terms. However, the appreciation of Asian currencies against the dollar resulted in a total return of –7.11% in dollar terms.

India and certain other emerging Asian markets saw positive returns during the period, though China was down about 3% in local currency terms. Japan, representing about half of the index, was down by over 21% in local currency terms. This was a case in which the stock market reflected its underlying economy: The Japanese economy continued to struggle during this period.

In Japan, the third quarter’s Tankan survey of business trends showed that business confidence was relatively unaffected by the U.S. subprime crisis. However, the later months of 2007 saw a sell-off in the Japanese stock market and a number of negative factors were evident:

• | Consumer spending was weak toward year-end, and the country had not yet emerged from deflation — a problem since the latter half of the 1990s. |

• | Japan accounted for approximately 9% of the global economy in 2006, the lowest figure in more than 25 years. |

Economic and Market Background 13

• | The reliance of Japanese companies on the use of temporary workers was among the highest in developed countries. These workers earn one third less than full-timers, receive few benefits, and contribute relatively little to consumer spending and economic growth. |

An important environmental milestone for the region came in the fourth quarter of 2007, as Australia — following the election of Kevin Rudd as prime minister — joined in efforts at a conference in Bali to develop a successor to the Kyoto Protocol on climate change.

14 Economic and Market Background

DOMINI SOCIAL EQUITY PORTFOLIO

PERFORMANCE COMMENTARY

For the six months ended January 31, 2008, the Domini Social Equity Portfolio (the “Fund”) declined –12.69%, excluding sales charges, underperforming the S&P 500 Index return of –4.32%.

The Fund’s subadvisor, in selecting stocks for the Fund’s portfolio, utilizes an approach that focuses on indicators of both valuation (how reasonably priced a company’s stock is relative to the value of its businesses) and momentum (the rate at which the company’s profits and/or share price have been increasing). During this period, companies that appeared to have attractive valuations performed more poorly than expected.

In particular, the Fund’s performance relative to the index was hurt by stock selection within the industrial, consumer staples, and information technology sectors, and by positions in the following stocks:

• | The stock of YRC Worldwide declined when analysts turned negative on the freight industry due to increases in fuel and equipment costs. |

• | The Fund’s performance was hurt by its overweight position in the electronics companies Electronic Data Systems and LAM Research, which performed poorly, and by its underweight position in Apple, which had a positive return for the period. |

An overweight position in the financial sector, which was hurt by the collapse of the subprime mortgage market, was also negative for performance. However, stock selection within that sector, including positions in JPMorgan Chase and Goldman Sachs, resulted in a positive contribution to returns. The Fund was also helped by its positions in Energen and Express Scripts, each of which announced profit outlooks that beat the expectations of analysts.

15

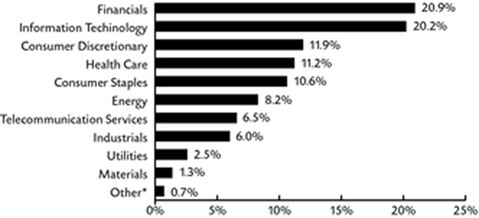

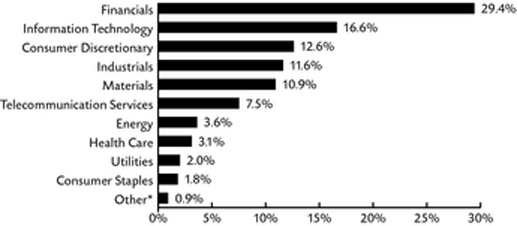

The Domini Social Equity Portfolio invests in the Domini Social Equity Trust. The table and bar chart below provide information as of January 31, 2008, about the ten largest holdings of the Domini Social Equity Trust and its portfolio holdings by industry sector:

TEN LARGEST HOLDINGS

SECURITY DESCRIPTION |

| % NET |

|

JP Morgan Chase & Co. |

| 4.2% |

|

Johnson & Johnson |

| 3.5% |

|

Verizon Communications |

| 3.4% |

|

Microsoft |

| 3.3% |

|

Intl Business Machines Corp |

| 3.2% |

|

Hewlett-Packard Co |

| 3.1% | |

Bank of America Corporation |

| 2.7% | |

Goldman Sachs Group Inc |

| 2.7% | |

AT&T Inc |

| 2.6% | |

Travelers Cos Inc/The |

| 2.1% |

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS)

———————

* | Other reflects Repurchase Agreements and Other Assets, less liabilities. |

The holdings mentioned above are described in the Domini Social Equity Trust’s Portfolio of Investments at January 31, 2008, included herein. The composition of the Trust’s portfolio is subject to change.

16 Domini Social Equity Portfolio — Performance Commentary

AVERAGE ANNUAL TOTAL RETURNS

|

|

|

| Domini Social Equity Portfolio |

| Domini Social Equity Portfolio |

| S&P 500 | |||

As of |

| 1 Year |

| –7.95 | % |

| –3.36 | % |

| 5.50 | % |

| 5 Year |

| 7.87 | % |

| 8.93 | %(2) |

| 12.83 | % | |

| 10 Year |

| 3.42 | % |

| 3.92 | %(2) |

| 5.91 | % | |

| Since Inception |

| 8.75 | %(1) |

| 9.07 | %(1),(2) |

| 10.49 | %(1) | |

As of |

| 1 Year |

| –17.07 | % |

| –12.93 | % |

| –2.31 | % |

| 5 Year |

| 6.72 | % |

| 7.76 | %(2) |

| 12.02 | % | |

| 10 Year |

| 2.38 | % |

| 2.87 | %(2) |

| 5.14 | % | |

| Since Inception |

| 8.17 | %(1) |

| 8.48 | %(1),(2) |

| 10.03 | %(1) | |

COMPARISON OF $10,000 INVESTMENT IN THE

DOMINI SOCIAL EQUITY PORTFOLIO (WITH 4.75% MAXIMUM SALES CHARGE) AND THE S&P 500

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Economic and market conditions change, and both will cause investment return, principal value, and yield to fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month-end, call 1-800-582-6757 or visit www.domini.com. A 2.00% redemption fee is charged on sales or exchanges of shares made less than 30 days after the settlement of purchase or acquisition through exchange, with certain exceptions. Performance data quote d above does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

For the period reported in its current prospectus, the Fund’s gross annual operating expenses totaled 9.51% of net assets. Until November 30, 2008, Domini has contractually agreed to waive fees and reimburse expenses to limit the Fund’s expenses, on a per annum basis, to 1.13% of net assets.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini Social Equity Portfolio is based on the Fund’s net asset values and assumes all dividends and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money. Certain fees payable by the Fund were waived during the period, and the Fund’s average annual total returns would have been lower had these not been waived.

The Standard & Poor’s 500 Index (S&P 500) is an unmanaged index of common stocks. Investors cannot invest directly in the S&P 500.

______________(1) | Since June 3, 1991. |

(2) | The Domini Social Equity Portfolio, which commenced operations on May 1, 2005, invests all of its assets in the Domini Social Equity Trust (DSET), which has the same investment objectives as the Fund. The DSET commenced operations on June 3, 1991. Performance prior to the Fund’s commencement of operations is the performance of the DSET adjusted for expenses of the Fund. |

This material must be preceded or accompanied by the Fund’s current prospectus. DSIL Investment Services LLC, Distributor. 03/08

Domini Social Equity Portfolio — Performance Commentary 17

DOMINI SOCIAL EQUITY TRUST

PORTFOLIO OF INVESTMENTS

JANUARY 31, 2008 (UNAUDITED)

SECURITY |

| SHARES |

| VALUE |

| |

Common Stocks – 99.3% |

|

|

|

|

|

|

Consumer Discretionary – 11.9% |

|

|

|

|

|

|

Amazon.com Inc. (a) |

| 119,650 |

| $ | 9,296,805 |

|

American Eagle Outfitters |

| 700 |

|

| 16,121 |

|

Autoliv Inc. |

| 133,700 |

|

| 6,678,315 |

|

AutoZone Inc. (a) |

| 54,047 |

|

| 6,533,201 |

|

Best Buy Co Inc. |

| 120,758 |

|

| 5,894,198 |

|

Big Lots Inc. (a) |

| 338,000 |

|

| 5,867,680 |

|

Black & Decker Corporation |

| 600 |

|

| 43,524 |

|

CBS Corp, Class B |

| 584,300 |

|

| 14,718,517 |

|

Comcast Corp, Class A (a) |

| 5,550 |

|

| 100,788 |

|

Darden Restaurants Inc. |

| 255,700 |

|

| 7,241,424 |

|

DR Horton Inc. |

| 1,975 |

|

| 34,069 |

|

Gap Inc./The |

| 1,887 |

|

| 36,079 |

|

Home Depot Inc. |

| 3,244 |

|

| 99,493 |

|

J.C. Penney Co Inc. |

| 758 |

|

| 35,937 |

|

Johnson Controls Inc. |

| 1,954 |

|

| 69,113 |

|

Limited Brands |

| 1,668 |

|

| 31,842 |

|

Liz Claiborne Inc. |

| 600 |

|

| 13,134 |

|

Lowe’s Cos Inc. |

| 2,986 |

|

| 78,950 |

|

McDonald’s Corporation |

| 412,574 |

|

| 22,093,338 |

|

McGraw-Hill Companies Inc. |

| 1,212 |

|

| 51,825 |

|

Meredith Corp. |

| 823 |

|

| 38,673 |

|

Nike Inc., Class B. |

| 362,988 |

|

| 22,418,139 |

|

Nordstrom Inc. |

| 895 |

|

| 34,816 |

|

Pulte Homes Inc. |

| 2,094 |

|

| 34,216 |

|

Scholastic Corp (a) |

| 722 |

|

| 24,743 |

|

Staples Inc. |

| 2,258 |

|

| 54,057 |

|

Starbucks Corporation (a) |

| 2,578 |

|

| 48,750 |

|

Target Corp. |

| 1,636 |

|

| 90,929 |

|

Time Warner Inc. |

| 7,876 |

|

| 123,968 |

|

VF Corp. |

| 800 |

|

| 61,896 |

|

Viacom Inc. – Class B (a) |

| 2,100 |

|

| 81,396 |

|

Walt Disney Co./The |

| 285,137 |

|

| 8,534,150 |

|

Washington Post Co/The, Class B |

| 95 |

|

| 70,680 |

|

Whirlpool Corporation |

| 222,363 |

|

| 18,925,315 |

|

|

|

|

|

| 129,476,081 |

|

Consumer Staples – 10.6% |

|

|

|

|

|

|

Avon Products Inc. |

| 2,406 |

|

| 84,258 |

|

Church & Dwight Co Inc. |

| 124,180 |

|

| 6,608,860 |

|

Coca Cola Co/The |

| 299,384 |

|

| 17,714,551 |

|

Coca-Cola Enterprises Inc. |

| 752,400 |

|

| 17,357,868 |

|

Colgate-Palmolive Co. |

| 2,296 |

|

| 176,792 |

|

Costco Wholesale Corp. |

| 53,400 |

|

| 3,627,996 |

|

Hershey Co/The |

| 1,936 |

|

| 70,083 |

|

JM Smucker Co/The – New Common |

| 108,530 |

|

| 5,071,607 |

|

Kimberly-Clark Corp. |

| 125,056 |

|

| 8,209,926 |

|

Kraft Foods Inc., Class A |

| 5,000 |

|

| 146,300 |

|

Kroger Co. |

| 697,377 |

|

| 17,748,245 |

|

Pepsi Bottling Group Inc. |

| 142,000 |

|

| 4,948,700 |

|

PepsiAmericas Inc. |

| 608,600 |

|

| 14,995,904 |

|

PepsiCo Inc. |

| 3,653 |

|

| 249,098 |

|

Procter & Gamble Co. |

| 135,461 |

|

| 8,933,653 |

|

SUPERVALU Inc. |

| 326,300 |

|

| 9,808,578 |

|

Walgreen Co. |

| 3,064 |

|

| 107,577 |

|

|

|

|

|

| 115,859,996 |

|

Energy – 8.2% |

|

|

|

|

|

|

Anadarko Petroleum Corporation |

| 5,418 |

|

| 317,441 |

|

Apache Corporation |

| 162,862 |

|

| 15,543,549 |

|

Chesapeake Energy Corporation |

| 109,500 |

|

| 4,076,685 |

|

Devon Energy Corporation |

| 42,570 |

|

| 3,617,599 |

|

ENSCO International, Inc. |

| 131,300 |

|

| 6,712,056 |

|

EOG Resources Inc. |

| 3,908 |

|

| 341,950 |

|

National Oilwell Varco Inc. (a) |

| 67,600 |

|

| 4,071,548 |

|

Noble Corp. |

| 94,200 |

|

| 4,123,134 |

|

Noble Energy Inc. |

| 90,200 |

|

| 6,546,716 |

|

Technip SA |

| 135,390 |

|

| 8,664,960 |

|

Tidewater Inc. |

| 157,400 |

|

| 8,335,904 |

|

Unit Corp (a) |

| 370,750 |

|

| 18,581,989 |

|

XTO Energy Inc. |

| 167,770 |

|

| 8,713,974 |

|

|

|

|

|

| 89,647,505 |

|

Financials – 20.9% |

|

|

|

|

|

|

American Express Co. |

| 3,576 |

|

| 176,368 |

|

American International Group |

| 222,300 |

|

| 12,262,068 |

|

Bank of America Corporation |

| 677,000 |

|

| 30,024,950 |

|

Bank of Ireland ADR |

| 112,890 |

|

| 6,626,643 |

|

Barclays Plc – Spons ADR |

| 274,200 |

|

| 10,345,566 |

|

18

DOMINI SOCIAL EQUITY TRUST / PORTFOLIO OF INVESTMENTS (CONTINUED)

JANUARY 31, 2008 (UNAUDITED)

SECURITY |

| SHARES |

| VALUE |

| |

Financials (Continued) |

|

|

|

|

|

|

Charles Schwab Corp/The |

| 515,500 |

| $ | 11,495,650 |

|

Citigroup Inc. |

| 10,300 |

|

| 290,666 |

|

Federal National Mortgage Association |

| 2,476 |

|

| 83,837 |

|

Freddie Mac |

| 2,322 |

|

| 70,566 |

|

Goldman Sachs Group Inc. |

| 146,400 |

|

| 29,392,728 |

|

HDFC Bank Ltd – ADR |

| 41,240 |

|

| 4,921,582 |

|

Janus Capital Group Inc. |

| 240,910 |

|

| 6,506,979 |

|

JP Morgan Chase & Co. |

| 974,730 |

|

| 46,348,412 |

|

Lehman Brothers Holdings Inc. |

| 1,400 |

|

| 89,838 |

|

Nationwide Financial Serv, Class A |

| 204,000 |

|

| 9,010,680 |

|

Royal Bank of Scotland Group plc – Spon ADR (a) |

| 1,082,500 |

|

| 8,432,675 |

|

TD Ameritrade Holding Corp (a) |

| 271,200 |

|

| 5,087,712 |

|

Travelers Cos Inc./The |

| 482,852 |

|

| 23,225,181 |

|

US Bancorp. |

| 6,463 |

|

| 219,419 |

|

Wachovia Corp. |

| 5,583 |

|

| 217,346 |

|

Washington Mutual Inc. |

| 4,631 |

|

| 92,250 |

|

Wells Fargo & Co. |

| 566,506 |

|

| 19,266,869 |

|

Westpac Banking Corp – SP ADR |

| 42,160 |

|

| 4,901,943 |

|

|

|

|

|

| 229,089,928 |

|

Health Care –11.2% |

|

|

|

|

|

|

Amgen Inc. (a) |

| 150,466 |

|

| 7,010,211 |

|

Baxter International Inc. |

| 205,122 |

|

| 12,459,110 |

|

Becton Dickinson & Company |

| 2,302 |

|

| 199,192 |

|

Express Scripts Inc. – Common (a) |

| 203,800 |

|

| 13,754,462 |

|

Forest Laboratories Inc. (a) |

| 199,700 |

|

| 7,942,069 |

|

Genentech Inc. (a) |

| 1,600 |

|

| 112,304 |

|

Gilead Sciences Inc. (a) |

| 155,210 |

|

| 7,091,545 |

|

Invitrogen Corp (a) |

| 39,500 |

|

| 3,383,965 |

|

Johnson & Johnson |

| 609,324 |

|

| 38,545,836 |

|

Kinetic Concepts Inc. (a) |

| 144,500 |

|

| 7,193,210 |

|

Medtronic Inc. |

| 3,655 |

|

| 170,213 |

|

Merck & Co. Inc. |

| 320,202 |

|

| 14,818,949 |

|

Watson Pharmaceuticals Inc. (a) |

| 384,300 |

|

| 10,034,073 |

|

|

|

|

|

| 122,715,139 |

|

Industrials – 6.0% |

|

|

|

|

|

|

3M Co. |

| 2,864 |

| 228,118 |

| |

Air France-KLM –ADR |

| 121,100 |

|

| 3,375,057 |

|

AMR Corp (a) |

| 1,100 |

|

| 15,334 |

|

Cooper Industries Ltd, Class A |

| 2,286 |

|

| 101,818 |

|

Cummins Inc. |

| 286,464 |

|

| 13,830,481 |

|

Deere & Co. |

| 140,200 |

|

| 12,303,952 |

|

Deluxe Corporation |

| 265,200 |

|

| 6,449,664 |

|

Emerson Electric Company |

| 3,308 |

|

| 168,179 |

|

Illinois Tool Works |

| 3,600 |

|

| 181,440 |

|

Jetblue Airways (a) |

| 5,793 |

|

| 40,030 |

|

PACCAR Inc. |

| 106,350 |

|

| 4,989,942 |

|

RR Donnelley & Sons Co. |

| 128,918 |

|

| 4,497,949 |

|

Southwest Airlines |

| 6,578 |

|

| 77,160 |

|

Teleflex Inc. |

| 107,600 |

|

| 6,361,312 |

|

TNT NV – ADR |

| 172,600 |

|

| 6,394,830 |

|

Tomkins plc – Sponsored ADR |

| 292,800 |

|

| 4,023,072 |

|

Toppan Printing Co Ltd – Unspons ADR |

| 60,650 |

|

| 2,971,850 |

|

United Parcel Service, Class B |

| 3,373 |

|

| 246,769 |

|

|

|

|

|

| 66,256,957 |

|

Information Technology – 20.2% |

|

|

|

|

|

|

Apple Inc. (a) |

| 124,282 |

|

| 16,822,812 |

|

Arrow Electronics, Inc. (a) |

| 146,900 |

|

| 5,026,918 |

|

Cisco Systems Inc. (a) |

| 580,636 |

|

| 14,225,582 |

|

Dell Inc. (a) |

| 5,484 |

|

| 109,899 |

|

eBay Inc. (a) |

| 2,376 |

|

| 63,891 |

|

EMC Corp/ Massachusetts (a) |

| 4,400 |

|

| 69,828 |

|

Google Inc., Class A (a) |

| 4,580 |

|

| 2,584,494 |

|

Hewlett-Packard Co |

| 764,347 |

|

| 33,440,181 |

|

Intel Corp. |

| 869,909 |

|

| 18,442,071 |

|

Intl Business Machines Corp |

| 329,000 |

|

| 35,314,860 |

|

Jabil Circuit Inc. |

| 3,100 |

|

| 41,075 |

|

Juniper Networks Inc. (a) |

| 128,700 |

|

| 3,494,205 |

|

LAM Research Corp (a) |

| 338,900 |

|

| 13,010,371 |

|

Microsoft Corp |

| 1,107,352 |

|

| 36,099,675 |

|

Motorola Inc. |

| 7,500 |

|

| 86,475 |

|

Nvidia Corp (a) |

| 156,990 |

|

| 3,860,384 |

|

Oracle Corp (a) |

| 738,200 |

|

| 15,170,010 |

|

QUALCOMM Inc. |

| 4,234 |

|

| 179,606 |

|

19

DOMINI SOCIAL EQUITY TRUST / PORTFOLIO OF INVESTMENTS (CONTINUED)

JANUARY 31, 2008 (UNAUDITED)

SECURITY |

| SHARES |

| VALUE |

| |

Information Technology (Continued) |

|

|

|

|

|

|

STMicroelectronics NV – NY Shs |

| 458,100 |

| $ | 5,675,859 |

|

Symantec Corp (a) |

| 425,846 |

|

| 7,635,419 |

|

Texas Instruments Inc. |

| 3,928 |

|

| 121,493 |

|

Western Digital Corp (a) |

| 345,080 |

|

| 9,127,366 |

|

Xerox Corporation |

| 5,598 |

|

| 86,209 |

|

|

|

|

|

| 220,688,683 |

|

Materials – 1.3% |

|

|

|

|

|

|

International Paper Co. |

| 4,600 |

|

| 148,350 |

|

Lubrizol Corp. |

| 88,200 |

|

| 4,640,202 |

|

MeadWestvaco Corp. |

| 3,466 |

|

| 97,048 |

|

Nucor Corp. |

| 81,916 |

|

| 4,734,745 |

|

Rohm and Haas Co. |

| 2,210 |

|

| 117,904 |

|

United States Steel Corp. |

| 46,200 |

|

| 4,717,482 |

|

|

|

|

|

| 14,455,731 |

|

Telecommunication Services – 6.5% |

|

|

|

|

|

|

AT&T Inc. |

| 748,604 |

|

| 28,813,768 |

|

France Telecom SA – Spons ADR |

| 144,530 |

|

| 5,110,581 |

|

Sprint Nextel Corp. |

| 7,259 |

|

| 76,437 |

|

Verizon Communications Inc. |

| 946,438 |

|

| 36,759,652 |

|

|

|

|

|

| 70,760,438 |

|

Utilities – 2.5% |

|

|

|

|

|

|

Energen Corp. |

| 352,677 |

| 22,183,383 |

| |

Pepco Holdings Inc. |

| 182,600 |

|

| 4,648,996 |

|

|

|

|

|

| 26,832,379 |

|

Total Common Stocks |

|

|

|

| 1,085,782,837 |

|

Repurchase Agreements – 0.6% |

|

|

|

|

|

|

State Street Bank & Trust, dated 1/31/2008, 1.60% due 2/1/2008, maturity amount $6,221,058 (collateralized by U.S. Government Agency Obligations, Freddie Mac, 3.25%, 3/14/2008, market value $6,348,375) |

| 6,220,781 |

|

| 6,220,781 |

|

Total Repurchase Agreements |

|

|

|

| 6,220,781 |

|

Total Investments — 99.9% |

|

|

|

|

|

|

(Cost $1,039,758,128) (b) |

|

|

|

| 1,092,003,618 |

|

Other Assets, less liabilities — 0.1% |

|

|

|

| 967,093 |

|

Net Assets — 100.0% |

|

|

| $ | 1,092,970,711 |

|

(a) | Non-income producing security. |

(b) | The aggregate cost for federal income tax purposes is $1,080,406,528. The aggregate gross unrealized appreciation is $83,814,064 and the aggregate gross unrealized depreciation is $72,216,974, resulting in net unrealized appreciation of $11,597,090. |

ADR – American Depository Receipt

SEE NOTES TO FINANCIAL STATEMENTS

20

DOMINI EUROPEAN SOCIAL EQUITY PORTFOLIO

PERFORMANCE COMMENTARY

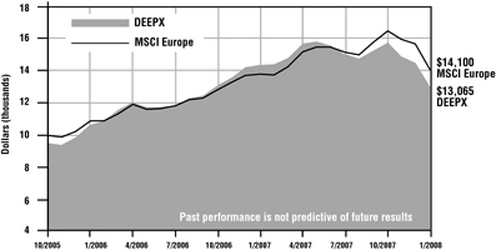

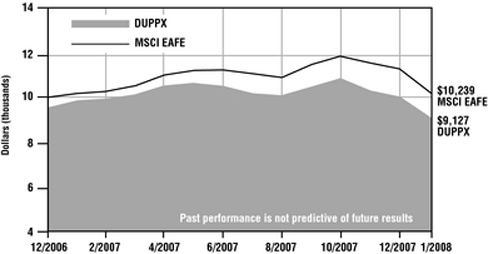

For the six months ended January 31, 2008, the Domini European Social Equity Portfolio (the “Fund”) declined –13.30%, excluding sales charges, underperforming the MSCI Europe Index, which declined by –7.31%.

During this period, stock selection — particularly in the financial, materials, and consumer discretionary sectors — was the primary driver of underperformance:

• | Royal Bank of Scotland was affected by the impact of problems in the U.S. subprime mortgage market on mortgage-related securities that it held. |

• | Trinity Mirror, the U.K.’s largest newspaper publisher, saw its shares drop sharply after it sold its Midlands newspapers for less than expected. |

• | The stock of Rautaruukki, a Finnish manufacturer of galvanized steel products, declined after the company issued a lower-than-expected earnings forecast. |

The Fund’s subadvisor, in selecting stocks for the Fund’s portfolio, uses an approach that considers measures of a company’s valuation (the price of its stock relative to the value of its businesses) and its momentum (the rate at which the company’s profits and/or share price have been increasing). During this period, valuation measures were less effective than momentum measures.

21

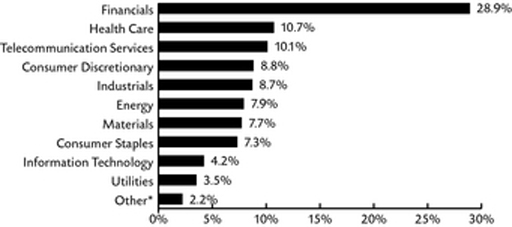

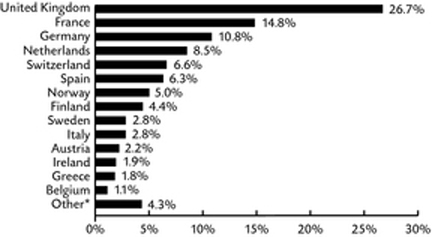

The Domini European Social Equity Portfolio invests in the Domini European Social Equity Trust. The table and bar chart below provide information as of January 31, 2008, about the ten largest holdings of the Domini European Social Equity Trust and its portfolio holdings by industry sector and by country:

TEN LARGEST HOLDINGS

SECURITY DESCRIPTION |

| % NET |

|

StatoilHydro ASA |

| 3.9% |

|

Vodafone Group PLC |

| 3.7% |

|

Sanofi-Aventis |

| 3.7% |

|

Vivendi SA |

| 3.4% |

|

Nokia OYJ |

| 3.2% |

|

France Telecom SA |

| 3.0% |

|

Swiss Re-Reg |

| 2.9% |

|

Royal Bank of Scotland Group |

| 2.8% |

|

Telefonica SA |

| 2.5% |

|

Unilever PLC |

| 2.5% |

|

PORTFOLIO HOLDINGS BY INDUSTRY SECTOR (% OF NET ASSETS)

* | Other reflects Repurchase Agreements and Other Assets, less liabilities. |

PORTFOLIO HOLDINGS BY COUNTRY (% OF NET ASSETS)

* | Other reflects Portugal, Turkey, Denmark, Poland, Russia, Repurchase Agreements, and Other Assets, less liabilities. |

The holdings mentioned above are described in the Domini European Social Equity Trust’s Portfolio of Investments at January 31, 2008, included herein. The composition of the Trust’s portfolio is subject to change.

22 | Domini European Social Equity Portfolio — Performance Commentary |

AVERAGE ANNUAL TOTAL RETURNS

|

|

|

| Domini European Social |

| Domini European |

| MSCI Europe |

| ||

As of 12-31-07 |

| 1 Year |

| –2.84% |

|

| 2.00% |

|

| 14.38% |

|

| Since Inception(1) |

| 18.27% |

|

| 20.86% |

|

| 22.40% |

| |

As of 1-31-08 |

| 1 Year |

| –13.59% |

|

| –9.29% |

|

| 1.86% |

|

| Since Inception(1) |

| 12.17% |

|

| 14.53% |

|

| 15.90% |

| |

COMPARISON OF $10,000 INVESTMENT IN THE

DOMINI EUROPEAN SOCIAL EQUITY PORTFOLIO (WITH 4.75% MAXIMUM SALES CHARGE) AND THE MSCI EUROPE

Past performance is no guarantee of future results. The Fund’s returns quoted above represent past performance after all expenses. Economic and market conditions change, and both will cause investment return, principal value, and yield to fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance data quoted. For performance information current to the most recent month-end, call 1-800-582-6757 or visit www.domini.com. A 2.00% redemption fee is charged on sales or exchanges of shares made less than 30 days after the settlement of purchase or acquisition through exchange, with certain exceptions. Performance data quote d above does not reflect the deduction of this fee, which would reduce the performance quoted. See the Fund’s prospectus for further information.

For the period reported in its current prospectus, the Fund’s gross annual operating expenses totaled 3.37% of net assets. Until November 30, 2008, Domini has contractually agreed to waive fees and reimburse expenses to limit the Fund’s expenses, on a per annum basis, to 1.57% of net assets.

Investing internationally involves special risks, such as currency fluctuations, social and economic instability, differing securities regulations and accounting standards, limited public information, possible changes in taxation, and periods of illiquidity.

The table and the graph do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of Fund shares. Total return for the Domini European Social Equity Portfolio is based on the Fund’s net asset values and assumes all dividends and capital gains were reinvested. An investment in the Fund is not a bank deposit and is not insured. You may lose money. Certain fees payable by the Fund were waived during the period, and the Fund’s average annual total returns would have been lower had these not been waived.

The Morgan Stanley Capital International Europe (MSCI Europe) is an unmanaged index of common stocks. Investors cannot invest directly in the MSCI Europe.

______________(1) Since October 3, 2005.

This material must be preceded or accompanied by the Fund’s current prospectus. DSIL Investment Services LLC, Distributor. 03/08

| Domini European Social Equity Portfolio — Performance Commentary | 23 |

DOMINI EUROPEAN SOCIAL EQUITY TRUST

PORTFOLIO OF INVESTMENTS

JANUARY 31, 2008 (UNAUDITED)

COUNTRY/SECURITY |

| INDUSTRY |

| SHARES |

| VALUE | |

Common Stocks – 97.8% |

|

|

|

|

|

|

|

Austria – 2.2% |

|

|

|

|

|

|

|

Immofinanz AG |

| Real Estate |

| 107,410 |

| $ | 1,018,008 |

OMV AG |

| Energy |

| 2,399 |

|

| 172,329 |

Voestalpine AG |

| Materials |

| 19,568 |

|

| 1,201,716 |

|

|

|

|

|

|

| 2,392,053 |

Belgium – 1.1% |

|

|

|

|

|

|

|

Delhaize Group |

| Food & Staples Retailing |

| 9,050 |

|

| 690,105 |

KBC Groep NV |

| Banks |

| 3,926 |

|

| 499,168 |

|

|

|

|

|

|

| 1,189,273 |

Denmark – 0.4% |

|

|

|

|

|

|

|

Dampskibsselskabet (d/s) Torm |

| Energy |

| 10,152 |

|

| 325,516 |

H. Lundbeck A/S |

| Pharma, Biotech & Life Sciences |

| 5,300 |

|

| 128,463 |

|

|

|

|

|

|

| 453,979 |

Finland – 4.4% |

|

|

|

|

|

|

|

Nokia OYJ |

| Technology Hardware & Equipment |

| 96,971 |

|

| 3,556,053 |

Orion OYJ/New |

| Pharma, Biotech & Life Sciences |

| 58,484 |

|

| 1,314,449 |

|

|

|

|

|

|

| 4,870,502 |

France – 14.8% |

|

|

|

|

|

|

|

Air France-KLM |

| Transportation |

| 33,873 |

|

| 941,108 |

BNP Paribas |

| Banks |

| 23,573 |

|

| 2,328,712 |

Credit Agricole SA |

| Banks |

| 18,360 |

|

| 562,680 |

France Telecom SA |

| Telecommunication Services |

| 94,621 |

|

| 3,323,389 |

Lafarge SA |

| Materials |

| 1,395 |

|

| 219,562 |

Sanofi-Aventis |

| Pharma, Biotech & Life Sciences |

| 49,881 |

|

| 4,051,006 |

Schneider Electric SA |

| Capital Goods |

| 4,100 |

|

| 472,311 |

Ste Des Ciments Francais – a |

| Materials |

| 3,576 |

|

| 540,566 |

Vallourec |

| Capital Goods |

| 1,525 |

|

| 305,254 |

Vivendi SA |

| Media |

| 94,767 |

|

| 3,803,022 |

|

|

|

|

|

|

| 16,547,610 |

Germany – 10.8% |

|

|

|

|

|

|

|

Allianz SE – Reg |

| Insurance |

| 13,278 |

|

| 2,356,863 |

Altana AG |

| Materials |

| 67,383 |

|

| 1,508,210 |

Deutsche Boerse AG |

| Diversified Financials |

| 1,774 |

|

| 309,136 |

Deutsche Lufthansa AG – Reg |

| Transportation |

| 63,951 |

|

| 1,526,926 |

Deutsche Telekom AG – Reg |

| Telecommunication Services |

| 34,069 |

|

| 694,997 |

Epcos AG |

| Technology Hardware & Equipment |

| 55,076 |

|

| 749,366 |

Fresenius SE |

| Health Care Equipment & Services |

| 28,437 |

|

| 2,260,529 |

Muenchener Rueckver AG – Reg |

| Insurance |

| 11,527 |

|

| 2,062,496 |

Salzgitter AG |

| Materials |

| 3,768 |

|

| 588,514 |

|

|

|

|

|

|

| 12,057,037 |

Greece – 1.8% |

|

|

|

|

|

|

|

National Bank of Greece |

| Banks |

| 18,922 |

|

| 1,151,765 |

Public Power Corp |

| Utilities |

| 18,837 |

|

| 879,720 |

|

|

|

|

|

|

| 2,031,485 |

Ireland – 1.9% |

|

|

|

|

|

|

|

Anglo Irish Bank PLC |

| Banks |

| 27,866 |

|

| 392,428 |

Elan Corporation PLC (a) |

| Pharma, Biotech & Life Sciences |

| 15,167 |

|

| 384,267 |

Kerry Group PLC – A |

| Food & Beverage |

| 47,593 |

|

| 1,275,645 |

|

|

|

|

|

|

| 2,052,340 |

24

DOMINI EUROPEAN SOCIAL EQUITY TRUST / PORTFOLIO OF INVESTMENTS (CONTINUED)

JANUARY 31, 2008 (UNAUDITED)

COUNTRY/SECURITY |

| INDUSTRY |

| SHARES |

| VALUE | |

Italy – 2.8% |

|

|

|

|

|

|

|

Banca Popolare dell’Emilia |

|

|

|

|

|

|

|

Romagna Scrl |

| Banks |

| 20,412 |

| $ | 453,368 |

Fiat SPA |

| Automobiles & Components |

| 111,050 |

|

| 2,597,176 |

|

|

|

|

|

|

| 3,050,544 |

Netherlands – 8.5% |

|

|

|

|

|

|

|

Fugro NV – CVA |

| Energy |

| 26,164 |

|

| 1,785,971 |

ING Groep NV – CVA |

| Diversified Financials |

| 50,956 |

|

| 1,653,434 |

Koninklijke Ahold NV (a) |

| Food & Staples Retailing |

| 36,992 |

|

| 482,782 |

Koninklijke DSM NV |

| Materials |

| 45,131 |

|

| 1,897,353 |

OCE NV |

| Technology Hardware & Equipment |

| 7,527 |

|

| 150,749 |

SNS Reaal |

| Diversified Financials |

| 49,704 |

|

| 937,739 |

TNT NV |

| Transportation |

| 44,686 |

|

| 1,649,991 |

Unilever NV – CVA |

| Food & Beverage |

| 25,987 |

|

| 843,959 |

|

|

|

|

|

|

| 9,401,978 |

Norway – 5.0% |

|

|

|

|

|

|

|

Norsk Hydro ASA |

| Materials |

| 70,578 |

|

| 840,871 |

Petroleum Geo-Services |

| Energy |

| 16,167 |

|

| 347,625 |

StatoilHydro ASA |

| Energy |

| 166,024 |

|

| 4,346,820 |

|

|

|

|

|

|

| 5,535,316 |

Poland – 0.3% |

|

|

|

|

|

|

|

Polish Oil & Gas |

| Energy |

| 166,817 |

|

| 303,750 |

|

|

|

|

|

|

| 303,750 |

Portugal – 0.7% |

|

|

|

|

|

|

|

Banco Espirito Santo SA – Reg |

| Banks |

| 41,320 |

|

| 724,507 |

|

|

|

|

|

|

| 724,507 |

Russia – 0.3% |

|

|

|

|

|

|

|

Vimpel-Communications – SP ADR |

| Telecommunication Services |

| 8,500 |

|

| 292,740 |

|

|

|

|

|

|

| 292,740 |

Spain – 6.3% |

|

|

|

|

|

|

|

Banco Santander SA |

| Banks |

| 119,389 |

|

| 2,091,158 |

Corporacion Financiera Alba |

| Diversified Financials |

| 2,343 |

|

| 136,987 |

Gas Natural SDG SA |

| Utilities |

| 35,787 |

|

| 1,967,382 |

Telefonica SA |

| Telecommunication Services |

| 95,438 |

|

| 2,778,547 |

|

|

|

|

|

|

| 6,974,074 |

Sweden – 2.8% |

|

|

|

|

|

|

|

Nordea Bank AB |

| Banks |

| 61,223 |

|

| 830,904 |

Scania AB – B Shs |

| Capital Goods |

| 76,600 |

|

| 1,580,128 |

SSAB Svenskt Stal AB – Ser A |

| Materials |

| 25,450 |

|

| 670,698 |

|

|

|

|

|

|

| 3,081,730 |

Switzerland – 6.6% |

|

|

|

|

|

|

|

Holcim Ltd – Reg |

| Materials |

| 11,206 |

|

| 1,090,620 |

Lonza Group AG – Reg |

| Pharma, Biotech & Life Sciences |

| 6,595 |

|

| 843,434 |

Novartis AG – Reg Shs |

| Pharma, Biotech & Life Sciences |

| 17,797 |

|

| 898,496 |

Rieter Holding AG |

| Automobiles & Components |

| 993 |

|

| 358,590 |

Roche Holding AG |

| Pharma, Biotech & Life Sciences |

| 1,461 |

|

| 264,346 |

Sonova Holding AG |

| Health Care Equipment & Services |

| 1,073 |

|

| 95,584 |

Swiss Reinsurance – Reg |

| Insurance |

| 43,673 |

|

| 3,269,886 |

The Swatch Group AG – Reg |

| Consumer Durables & Apparel |

| 9,901 |

|

| 517,484 |

|

|

|

|

|

|

| 7,338,440 |

25

DOMINI EUROPEAN SOCIAL EQUITY TRUST / PORTFOLIO OF INVESTMENTS (CONTINUED)

JANUARY 31, 2008 (UNAUDITED)

COUNTRY/SECURITY |

| INDUSTRY |

| SHARES |

| VALUE | |

Turkey – 0.4% |

|

|

|

|

|

|

|

Trakya Cam Sanayii AS |

| Capital Goods |

| 148,026 |

| $ | 287,914 |

Turk Sise Ve Cam Fabrikalari |

| Consumer Durables & Apparel |

| 145,580 |

|

| 209,592 |

|

|

|

|

|

|

| 497,506 |

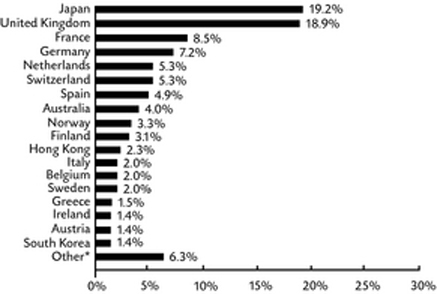

United Kingdom – 26.7% |

|

|

|

|

|

|

|

3i Group PLC |

| Diversified Financials |

| 101,733 |

|

| 1,904,873 |

Aviva PLC |

| Insurance |

| 63,993 |

|

| 802,600 |

Barclays PLC |

| Banks |

| 177,780 |

| �� | 1,677,718 |

BG Group PLC |

| Energy |

| 66,028 |

|

| 1,456,320 |

Carphone Warehouse Group PLC |

| Retailing |

| 18,733 |

|

| 123,315 |

Cookson Group New PLC |

| Capital Goods |

| 51,090 |

|

| 567,126 |

CSR PLC (a) |

| Semiconductors & |

|

|

|

|

|

|

| Semiconductor Equipment |

| 20,624 |

|

| 218,814 |

Drax Group PLC |

| Utilities |

| 97,495 |

|

| 982,755 |

Emap PLC |

| Media |

| 53,548 |

|

| 986,567 |

GlaxoSmithKline PLC |

| Pharma, Biotech & Life Sciences |

| 68,834 |

|

| 1,630,949 |

HBOS PLC |

| Banks |

| 93,511 |

|

| 1,302,629 |

Home Retail Group PLC |

| Retailing |

| 198,701 |

|

| 1,125,895 |

HSBC Holdings PLC |

| Banks |

| 65,643 |

|

| 984,604 |

Man Group PLC |

| Diversified Financials |

| 14,754 |

|

| 162,397 |

Old Mutual PLC |

| Insurance |

| 454,546 |

|

| 1,133,676 |

Royal Bank of Scotland Group PLC |

| Banks |

| 403,531 |

|

| 3,110,160 |

Stagecoach Group Ordinary PLC |

| Transportation |

| 470,752 |

|

| 2,269,688 |

Standard Life PLC |

| Insurance |

| 61,536 |

|

| 265,531 |

Unilever PLC |

| Food & Beverage |

| 83,812 |

|

| 2,762,005 |

Vodafone Group PLC |

| Telecommunication Services |

| 1,183,877 |

|

| 4,140,369 |

WM Morrison Supermarkets PLC |

| Food & Staples Retailing |

| 345,419 |

|

| 2,077,731 |

|

|

|

|

|

|

| 29,685,722 |

Total Common Stocks (Cost $118,634,552) |

|

|

|

|

|

| 108,480,586 |

Repurchase Agreements – 0.1% |

|

|

|

|

|

|

|

State Street Bank & Trust, dated 1/31/2008, 1.60% due 2/1/2008, maturity amount $79,687 (collateralized by U.S. Government Agency Obligations, Freddie Mac, 3.25%, 3/14/2008, market value $86,063) |

| Repurchase Agreements |

| 79,683 |

|

| 79,683 |

Total Repurchase Agreements (Cost $79,683) |

|

|

|

|

|

| 79,683 |

Total Investments — 97.9% (Cost $118,714,235) (b) |

|

|

|

|

|

| 108,560,269 |

Other Assets, less liabilities — 2.1% |

|

|

|

|

|

| 2,346,496 |

Net Assets — 100.0% |

|

|

|

|

| $ | 110,906,765 |

(a) | Non-income producing security. |

(b) | The aggregate cost for federal income tax purposes is $118,707,448. The aggregate gross unrealized appreciation is $5,566,078 and the aggregate gross unrealized depreciation is $15,713,257, resulting in net unrealized depreciation of $10,147,179. |

ADR – American Depository Receipt

As of the date of this report, certain foreign securities were fair valued by an independent pricing service under the direction of the Board of Trustees or its delegates in accordance with the Trust’s Valuation and Pricing Policies and Procedures.

SEE NOTES TO FINANCIAL STATEMENTS

26

DOMINI PACASIA SOCIAL EQUITY PORTFOLIO

PERFORMANCE COMMENTARY

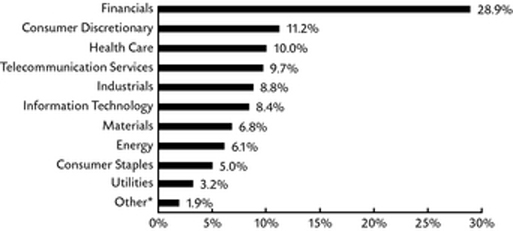

For the six months ended January 31, 2008, the Domini PacAsia Social Equity Portfolio (the “Fund”) declined –8.54%, excluding sales charges, underperforming the MSCI All Country Asia Pacific Index, which declined by –7.11%.

The Fund’s performance relative to the index was hurt primarily by sector allocation in the consumer staples and information technology sectors, and by stock selection in the energy and materials sectors. In particular, negative contributions to performance came from positions in companies including the following:

• | Tokyo Steel Manufacturing, which was expected to be affected by higher scrap steel costs and weaker construction demand. |

• | The bank Chuo Mitsui Trust, which experienced significant costs due to nonperforming loans in Japan. |

• | Korea Zinc, whose stock declined dramatically during the period. |

The Fund’s relative performance was helped by stock selection in the consumer discretionary and healthcare sectors, and by positions in the Singaporean motor vehicle company Jardine Cycle and in two Hong Kong real estate companies: Swire Pacific, whose real estate holdings were viewed favorably by analysts, and Wharf Holdings, whose expansion into China was seen as a positive.

27

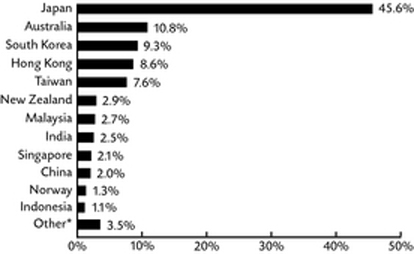

The Domini PacAsia Social Equity Portfolio invests in the Domini PacAsia Social Equity Trust. The table and bar chart below provide information as of January 31, 2008, about the ten largest holdings of the Domini PacAsia Social Equity Trust and its portfolio holdings by industry sector and by country:

TEN LARGEST HOLDINGS

SECURITY DESCRIPTION |

| % NET |

|

Honda Motor Co Ltd |