UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

ANNUAL REPORT

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934

For the fiscal year ended December 31, 2005

Commission File No. 333-120538

GTA-IB, LLC

State of Organization: FL |

| Federal Employer Identification No. 05-0546226 |

|

|

|

36750 US 19 N., Palm Harbor, FL 34684 | ||

| ||

Telephone Number: (727) 942-2000 | ||

SECURITIES REGISTERED PURSUANT TO SECTION 12(b) OF THE ACT:

None

SECURITIES REGISTERED PURSUANT TO SECTION 12(g) OF THE ACT:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act.

Yes o No ý

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act

Yes o No ý

Note — Checking the box above will not relieve any registrant required to file reports pursuant to Section 13 or 15(d) of the Exchange Act from obligations under those Sections.

Indicate by check mark whether the Registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days.

Yes ý No o

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K is not contained herein, and will not be contained, to the best of Registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendments to this Form 10-K. ý

Indicate by check mark if the Registrant is a large accelerated filer, an accelerated filer, or a non-accelerated filer. See definition of “accelerated filer and large accelerated filer” in Rule 12b-2 of the Act.

Large accelerated filer o Accelerated filer o Non-accelerated filer ý

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Act).

Yes o No ý

No established market exists for the Registrant’s membership interests, so there is no market value for such membership interests. There are no membership interests held by non-affiliates as of December 31, 2005.

Issuer has no common stock subject to this report.

Documents incorporated by reference: Certain exhibits to GTA-IB’s prior reports on Forms 10-K, 10-Q and 8-K are incorporated by reference in Part IV hereof.

The Exhibit Index begins on page 61.

GTA-IB, LLC

Annual Report on Form 10-K for the Year Ended December 31, 2005

TABLE OF CONTENTS

Cautionary Note Regarding Forward-Looking Statements

The following report contains forward-looking statements within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended. Forward-looking statements are statements that predict or describe future events or trends and that do not relate solely to historical matters. All of our projections in this annual report are forward-looking statements. You can generally identify forward-looking statements as statements containing the words “appears,” “believe,” “expect,” “hope,” “may,” “will,” “anticipate,” “intend,” “estimate,” “project,” “assume” or other similar expressions. Certain factors that might cause such a difference include the following: changes in general economic conditions; including changes that may influence group conference and guests’ vacation plans; changes in travel patterns; changes in consumer tastes in destinations or accommodations for group conferences and vacations; changes in Rental Pool participation by the current condominium owners; our ability to continue to operate the Westin Innisbrook Golf Resort under our management contracts; and the resale of condominiums to owners who elect neither to participate in the Rental Pool nor to become members of the Innisbrook Resort and Golf Club. You should not place undue reliance on our forward-looking statements because the matters they describe are subject to known (and unknown) risks, uncertainties and other unpredictable factors, many of which are beyond our control. Our forward-looking statements are based on the limited information currently available to us and speak only as of the date on which this report was filed with the Securities and Exchange Commission. Our continued internet posting or subsequent distribution of this dated report does not imply continued affirmation of the forward-looking statements included in it. We undertake no obligation, and we expressly disclaim any obligation, to issue any updates to our forward-looking statements, even if subsequent events cause our expectations to change regarding the matters discussed in those statements. Future events are inherently uncertain. Moreover, it is particularly difficult to predict business activity levels at the Resort with any certainty. Accordingly, our projections in this annual report are subject to particularly high uncertainty. Our projections should not be regarded as legal promises, representations or warranties of any kind whatsoever. Over time, our actual results, performance or achievements will likely differ from the anticipated results, performance or achievements that are expressed or implied by our forward-looking statements, and such differences might be significant and harmful to your interests.

Background

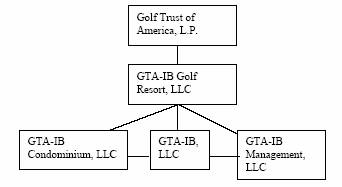

GTA-IB, LLC, also referenced in this report as the Company, us, we, or our, is a limited liability company that was formed in December 2002 and currently owns The Westin Innisbrook Golf Resort in Tarpon Springs, Florida. The Westin Innisbrook Golf Resort is referenced in this report as the Resort or Innisbrook. The Resort offers golf facilities, restaurant and conference facilities, and recreational activities including swimming, tennis and related resort activities. Westin Management Company South, or Westin, manages the Resort under a long-term management agreement expiring in 2017. Troon Golf, LLC, or Troon, manages the golf facilities at the Resort pursuant to its management agreement with Westin.

We are 100% owned by GTA-IB Golf Resort, LLC, which in turn is 100% owned by Golf Trust of America, L.P., or GTA, LP. Golf Trust of America, Inc., or GTA, owns 99.6% of GTA, LP. The remaining 0.4% of GTA, LP is owned by its one remaining limited partner. GTA is in the process of liquidating all of its assets pursuant to a plan of liquidation approved by its stockholders on May 22, 2001. GTA’s plan of liquidation contemplates the sale of the Resort.

Prior to July 16, 2004, the Resort was owned by Golf Host Resorts, Inc., or GHR, or our former borrower. As of July 16, 2004, GHR was an 80% owned subsidiary of Golf Hosts, Inc., or GHI. We entered into a Settlement Agreement and related transactions as of July 15, 2004 with GHR and certain other entities relating to the settlement of a number of issues between the parties, including GHR’s default under a $79 million loan, or the Loan, made by our affiliate GTA, LP to GHR in June 1997. This Settlement Agreement is referenced in this report as the Settlement Agreement. Pursuant to the Settlement Agreement, we settled claims relating to the Loan and took ownership of the Resort. We refer to our act of taking title to the Resort as the “Acquisition.”

In connection with the Settlement Agreement, we assumed control and operation of the Rental Pool Lease Operations at the Resort, or the Rental Pool. The Rental Pool was operated and controlled by GHR prior to the date of the Settlement Agreement. As a result of its administration of the Rental Pool, GHR was subject to the reporting requirements of Section 15(d) of the Exchange Act as an issuer. Upon our execution of the Settlement Agreement, we became the successor issuer to GHR and became subject to the information requirements of the Exchange Act and the rules and regulations promulgated thereunder.

We receive the majority of our operational revenue from the rental of hotel accommodations, food and beverage sales, golf operations (primarily greens and cart fees and merchandise sales) to both conference group and transient (individuals and families not participating in a conference) guests, and club membership initiation fees and dues. The Resort is different from many other hotels as a result of the use of condominium units as guest rooms pursuant to the Rental Pool lease agreements. When guests stay at the Resort, their hotel rooms are privately owned condominium units that are participating in the Resort’s Rental Pool. We lease these units from the participating condominium owners and then allow guests at the Resort to rent them from us during their stays. On a year-to-year basis, approximately 500 of the 938 condominium units participate in the Rental Pool pursuant to these lease arrangements. A percentage of room revenues that we receive are distributed to participating condominium owners pursuant to the terms of the Rental Pool lease agreements. In addition, we retain a percentage of the room revenues. While we do not bear the expense of certain operating and financing costs of the rental units, we do bear all other operating expenses of the Resort.

On November 23, 2005, CMI Financial Network, LLC terminated the Asset Purchase Agreement for the Resort that it entered with our parent, our parent’s operating partnership, and our parent’s operating partnership’s subsidiaries GTA-IB, LLC, GTA-IB Golf Resort, LLC, GTA-IB Condominium, LLC and GTA-IB Management, LLC.

Since November 23, 2005, GTA’s independent financial advisor Houlihan Lokey Howard and Zukin Capital, Inc., or Houlihan Lokey has continued to market the business and the Resort for sale on our behalf. As of the date that this annual report is filed, a definitive agreement for the purchase of the Resort has not been signed.

1

Rental Pool Condominiums

Condominium ownership is a realty subdivision in which the individual “lots” are deemed apartment units. Instead of owning a plot of ground, the condominium owners own the space where their condominium units are located. This leaves substantial properties in interest which are not individually owned, such as the underlying land, driveways, parking lots, building foundations, exterior walls and roofs, garden areas and utility lines. These areas are termed common property or common elements. Each condominium owner has an undivided fractional interest in the common property.

The condominium owners at the Resort have established an Association of Condominium Owners, or the Association, to administer and maintain this common property and to conduct the business of the condominium owners. In particular, the Association is responsible for maintaining insurance on the real property, upkeep of the structures, maintenance of the grounds, electricity for the common areas, water/sewer and security services. The Association assesses fees to defray these expenses and to establish necessary reserves. An assessment, if not timely paid, may result in a lien being placed upon the unit of a delinquent condominium owner. Each condominium owner must pay ad valorem property taxes, contents insurance, interior maintenance and to such other matters independent of the other unit owners. These expenses are incurred by each owner of condominium units whether or not the unit participates in the Rental Pool at the Resort. With respect to governing the affairs of the Association, the participating condominium owners are accorded one vote per condominium unit owned. State statutes also impact the way in which the Association’s affairs are administered.

General Resort Revenue Information

The following table sets forth the percentage of the Resort’s total revenues attributable to the four categories listed:

|

| 2005 |

| 2004 |

|

Revenues |

|

|

|

|

|

Resort facilities |

| 31.8 | % | 29.9 | % |

Food and beverage |

| 27.6 | % | 27.9 | % |

Golf |

| 31.9 | % | 31.4 | % |

Other |

| 8.7 | % | 10.8 | % |

Total |

| 100.0 | % | 100.0 | % |

The Resort hosted 586 conferences and related group meetings during 2005, and normally hosts more than 500 meetings per year, including social catering. The Resort hosts guests employed in a variety of industries, the majority of which are located in the central and eastern United States. Accordingly, we do not expect that the loss of a single conference or even a few conferences of average size would have a significant adverse impact on our business taken as a whole.

While conference-oriented resort business is quite competitive; we believe that the Resort has established itself in the industry and enjoys a solid reputation within its market. The Resort received the Pinnacle Award in January 2005 from Successful Meetings magazine. The Resort’s major competitors, also known as our competitive set, are other golf and conference-oriented resorts throughout the southeastern United States. We deem Preferred Amelia Plantation, Marriott Doral Golf Resort & Spa, PGA National Resort, the Renaissance World Golf Village Resort, the Belleview Biltmore Resort and the Marriott Sawgrass Resort & Spa to be the major competitors who comprise our competitive set.

Seasonality

The golf industry is seasonal in nature. Fewer tee times are available in the rainy season and the winter months. Revenues fall at the Resort during the summer months because the hot Florida weather makes the Resort less appealing for group golf outings and vacation destination golfers. Additionally, unusual weather patterns such as the hurricanes experienced in Florida in 2004 and in the southeastern United States in 2005 may reduce revenues for the Resort by negatively impacting reservations in comparable periods (July through September) of subsequent years. In each October since 2003, the Resort has hosted, and we expect will host again in 2006, a nationally televised PGA event, the Chrysler Championship, that brings some of the highest profile golfers, as well as high profile golf industry sponsors and vendors, to the Resort for several days to participate in the tournament. We do not expect to host another Chrysler Championship after 2006 due to the decision of Chrysler to reduce the number of golf tournaments it sponsors. Our management is attempting to successfully negotiate a contract with a replacement sponsor so that the Resort can host a PGA event during March of the years 2007 through 2012. We cannot guarantee the success of these negotiations. Historically, the Resort’s revenues increase in the fourth quarter but are generally the greatest during the first quarter as guests come from the northeast and other regions to enjoy the warm weather. The Resort uses seasonal pricing (peak, shoulder and off-peak) to maximize revenues.

Employees

As of December 31, 2005, the Resort had approximately 730 employees. Of these employees, approximately 87 are part-time and approximately 123 are casual laborers who are engaged as needed.

2

Environmental Matters

Operations at the golf courses at the Resort involve the use and storage of various hazardous materials such as herbicides, pesticides, fertilizers, motor oils and gasoline. Under various federal, state and local laws, ordinances and regulations, an owner or operator of real property may become liable for the costs of removal or remediation of certain hazardous substances released on or in its property. These laws often impose liability without regard to whether the owner or operator knew of, or was responsible for, the release of hazardous substances. The presence of these substances, or the failure to remediate these substances properly when released, may adversely affect the owner’s ability to sell the real estate or to borrow using the real estate as collateral.

The Florida Department of Environmental Protection, or the DEP, conducted a site inspection at the Resort on June 24, 2003. The Resort was found to have improperly disposed of waste paint and solvents and failed to properly store waste lamps and used oil and oil filters in properly labeled containers. The predecessor owner entered into a Consent Order wherein the DEP agreed to a reduced civil penalty to $22,000, and allowed the predecessor owner to offset 80% of this reduced civil penalty with credits obtained through the implementation of a pollution control project and a process of ongoing self-monitoring and reporting of environmental conditions to the DEP. The DEP determined that an above ground self-contained storage tank system at the Resort qualifies for this credit. The Resort installed the system and, on an ongoing basis, continues to monitor the environmental conditions at the Resort and to report these conditions to the DEP. As part of the ongoing self-monitoring and reporting process, the Resort engaged a third party, URS Corporation to develop a Site Assessment Report and monitor the environmental conditions noted in the DEP Consent Order. This report indicates that further remediation may be necessary and URS Corporation has estimated the remediation costs, if required by the DEP, to be approximately $35,000 to $40,000.

Except as discussed above, we have not been notified by any governmental authority of any material non-compliance, liability or other claim in connection with any of the golf courses at the Resort. At the time of GTA, LP’s loan to GHR in 1997 relating to the Resort, its golf courses were subjected to Phase I environmental audits (which do not involve invasive procedures, such as soil sampling or ground water analysis) by an independent environmental consultant. As a general rule, we do not update these Phase I environmental audits.

Based on the results of the Phase I environmental audits performed at or about the time of GTA, LP’s loan to GHR in 1997, at the time of that audit we were not aware of any existing environmental liabilities that we believe would harm our business, assets, results of operations or liquidity, nor were we aware of any condition that could create such a liability. We face the risk, however, that those Phase I environmental audits may have failed to reveal all potential environmental liabilities, that prior or adjacent owners may have created material environmental conditions not known to us or the independent environmental consultant, and that future uses or conditions (including, without limitation, changes in applicable environmental laws and regulations) may result in the imposition of environmental liability against us.

Government Regulation

The Resort, like most public businesses, is subject to the Americans with Disabilities Act of 1990. The ADA has separate compliance requirements for “public accommodations” and “commercial facilities,” but generally requires public facilities such as clubhouses and recreation areas to be accessible to people with disabilities. Compliance with the ADA requirements could require removal of access barriers and the construction of capital improvements at the Resort. Noncompliance could result in imposition of fines or an award of damages to private litigants. We are responsible for compliance costs incurred at the Resort.

Code of Ethics

See Part III, Item 10 for discussion of our Code of Ethics.

Web Site Access to Our Periodic SEC Reports

We make available free of charge our annual report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K and amendments to these reports filed or furnished pursuant to Section 13(a) or 15(d) of the Securities Exchange Act of 1934 as soon as reasonably practicable after we electronically file such material with, or furnish it to, the Securities and Exchange Commission. These reports can be obtained free of charge by contacting: GTA-IB, LLC, c/o Golf Trust of America, Inc., 10 North Adger’s Wharf, Charleston, South Carolina 29401. These reports are available on GTA’s website at www.golftrust.com. The public may read and copy any materials that we file with the SEC at the SEC’s Public Reference Room at 450 Fifth Street, NW, Washington, DC 20549. The public may obtain information on the operation of the Public Reference Room by calling the SEC at 1-800-SEC-0330. The SEC maintains an Internet Site that contains reports, proxy and information statements, and other issuers that file electronically with the SEC (www.sec.gov). Additional general information about the Resort may be obtained on the Resort’s website at www.golfinnisbrookresort.com.

3

In the event that the Resort does not provide sufficient cash flow to us, we may be forced to reduce capital expenditures and improvements at the Resort, diminishing the value of the Rental Pool units.

As the owner of the Resort, we will be responsible for any negative cash flow associated with the ownership and operation of the Resort. As a result of our assumption of these liabilities and our responsibility for any negative cash flow of the Resort, we may be exposed to liabilities and expenditures exceeding our expectations or ability to pay. In the event cash flow is insufficient to fund planned improvements, the ability of the participants in the Rental Pool to rent their units may decline. A decline in the rental rates that can be charged for the units or related vacancies resulting from our inability to make necessary capital expenditures may cause the value of the Rental Pool units, and the Resort, to decline.

We have been unsuccessful in our attempts to sell the Resort and the terms of a sale of the Resort, if any, remain uncertain.

We cannot guarantee that we will be able to sell the Resort on reasonable terms, if at all. Further, we cannot predict the amount of time that will be required to negotiate and close a sale of the Resort. In the event that GTA experiences liquidity constraints or other financial pressures due to the protracted negotiation of the sale of the Resort, GTA may be unwilling or unable to fund the Resort and the Rental Pool refurbishment. Even in the event that we successfully sell the Resort in the near term, we expect that the party who purchases the Resort will assume responsibility for the operational costs of the Resort and the Rental Pool. We cannot guarantee the level of funding and management attention that will be given to the Resort and the Rental Pool after we sell it. In the event that we, GTA and, if applicable, the Resort’s ultimate owner do not devote sufficient management resources and funding to the Resort and the Rental Pool, distributions to the Rental Pool participants could be adversely effected.

The Resort’s performance may not provide adequate resources to fund the refurbishment reimbursement to the Rental Pool participants.

Pursuant to the former borrower’s arrangement with many of the persons who own condominium units at the Resort, the condominiums owned by these participating persons are placed in a securitized pool and rented as hotel rooms to guests of the Resort. We refer to this securitized pool of participating condominiums as the Rental Pool. In addition to the current Rental Pool agreement, the former owner of the Resort agreed with the Association that the former owner of the Resort would reimburse 50% of the refurbishment costs, plus accrued interest at 5% per annum on the unpaid balance of that portion of the unpaid refurbishment costs which we are required to reimburse. This amount will be reimbursed to participating condominium owners (or transferees of their condominium unit(s)) over the five-year period beginning in 2005. The reimbursement is contingent on the units remaining in the Rental Pool from the time of their refurbishment through 2009. If the unit does not remain in the Rental Pool during the reimbursement period from 2005 through 2009, the owner or successor owner forfeits any unpaid installments at the time the unit is removed from the Rental Pool.

Accordingly, maintaining condominium owner participation in the Rental Pool is very important to the continued economic success of the Resort. We assumed certain existing or modified financial obligations of the former borrower, including its responsibilities regarding the administration of the condominium unit Rental Pool, when we took ownership of the Resort pursuant to the Settlement Agreement. Also as part of the Settlement Agreement, we assumed GHR’s obligation to reimburse the refurbishment expenses paid by the condominium owners.

As owner of the Resort, we are responsible for any negative cash flow associated with the ownership and operation of the Resort. As a result of the assumption of these liabilities and our responsibility for any negative cash flow, we face the risk that our ultimate liabilities and expenditures might be greater than we expected. In that case, we may not have sufficient cash available for the payment of the refurbishment expenses relating to the Rental Pool units, or we may otherwise decide not to use our funds in this manner. If this occurs, a disagreement involving the funding for the Rental Pool may arise, and this disagreement could both divert our management’s attention from the operation of the Resort and prove costly to the parties to any such dispute.

4

In the event that we sell the Resort , we expect that we will no longer be responsible for the Rental Pool obligations, and that the party who acquires the Resort will determine the funding for the Rental Pool based upon its willingness and ability to pay these obligations. We cannot guarantee that the party who acquires the Resort will provide adequate funding for the Resort in general or for refurbishment expenses in particular.

The number of Rental Pool units may decline if current owners find alternative uses of the units that are more attractive than participating in the Rental Pool, thereby reducing the number of available Rental Pool units and diminishing the value of the remaining units.

Participants in the Rental Pool may decide that alternative uses of their condominium units are more attractive than participating in the Rental Pool. In particular, condominium owners may determine that it is more financially advantageous to rent their units to longer term tenants, or to live in their units rather than paying to live elsewhere and allowing their units to participate in the Rental Pool. Any such reduction in the number of participants in the Rental Pool may result in increased pro-rata costs and reduced revenues for the remaining Rental Pool participants. In particular, a decrease in the number of participants in the Rental Pool will result in higher per capita costs relating to fixed costs that are incurred in connection with the administration of the Rental Pool. In the event that the number of units in the Rental Pool declines below 575, our obligation to reimburse refurbishment expenses for the units will be abated until the number of units in the Rental Pool is restored to 575 or higher.

Severe weather patterns experienced by Florida during 2004 and the southeastern portion of the United States during 2005 could result in depressed bookings, adversely affecting the Resort’s results of operations and reducing proceeds to the participants in the Rental Pool.

We expect that bookings at the Resort during the late summer and early fall of future years may be adversely affected as a result of a series of hurricanes that affected Florida during 2004 and the southeastern portion of the United States during 2005. In particular, the hurricanes that occurred during 2005 may have increased the awareness of potential guests, particularly those not residing in the southeastern portion of the United States, to the danger that hurricanes and tropical storms present. We expect that potential guests may be more reluctant to book rooms in regions subject to such weather patterns. In particular, it is possible that groups will choose alternative destinations for travel during the hurricane season. In the event that potential guests and groups choose alternative destinations as a result of these weather-related concerns, the Resort may experience lower bookings and reduced revenues, which in turn will result in reduced distributions to the Rental Pool participants.

Recent severe weather patterns could further intensify the seasonal nature of the results of the Resort.

The hotel industry is cyclical in nature. Our business has historically been weaker during the third quarter of each year. In the event that we suffer from reduced bookings during the third quarter as a result of hurricane-related concerns of potential guests, this effect could reduce the revenues to the Resort in the third quarter of each year, increasing the disparity between our results in the third quarter as compared to other quarters. This increased cyclicality could make it more difficult for us to project the results of the Resort, and may result in a lower than expected percentage of the Resort’s fixed costs being offset by revenue during the third quarter.

We are subject to all the operating risks common to the hotel industry which could adversely affect our results of operations.

Operating risks common to the Resort include:

• | changes in general economic conditions, including the timing and robustness of the apparent recovery in the United States from the recent economic downturn and the prospects for improved performance in other parts of the world; |

|

|

• | the impact of war and terrorist activity (including threatened terrorist activity) and heightened travel security measures instituted in response thereto; |

|

|

• | domestic and international political and geopolitical conditions; |

5

• | decreases in the demand for transient rooms and related lodging services, including a reduction in business travel as a result of general economic conditions; |

|

|

• | the impact of internet intermediaries on pricing and our increasing reliance on technology; |

|

|

• | cyclical over-building in the hotel industry which increases the supply of hotel rooms; |

|

|

• | changes in travel patterns; |

|

|

• | changes in operating costs, including, but not limited to, energy, labor costs (including the impact of unionization), workers’ compensation and health-care related costs, insurance and unanticipated costs such as acts of nature and their consequences; |

|

|

• | disputes with the managers of the Resort which may result in litigation; |

|

|

• | the availability of capital to allow us to fund renovations and investments at the Resort; and |

|

|

• | the financial condition of the airline industry and the impact on air travel. |

General economic downturns, or an increase in labor or insurance costs, may negatively impact our results.

Moderate or severe economic downturns or adverse conditions may negatively affect the operations of the Resort. These conditions may be widespread or isolated to one or more geographic regions. A tightening of the labor markets in Florida may result in fewer and/or less qualified applicants for job openings at the Resort. Higher wages, related labor costs and the increasing cost trends in the insurance markets may negatively impact our results as these costs increase. A general economic downturn, or increase in expenditures on insurance and labor costs, would adversely impact the operations of the Resort, potentially reducing funding that we provide to the Rental Pool and reducing the distributions to the Rental Pool participants.

If we are unable to successfully compete for customers, it may adversely affect our operating results and reduce the proceeds to participants in the Rental Pool.

The hotel industry is highly competitive. The Resort competes for customers with other hotel and resort properties. Some of our competitors may have substantially greater marketing and financial resources than we do, and they may improve their facilities, reduce their prices, or expand or improve their marketing programs in ways that adversely affect the Resort and our operating results, and reduce the proceeds to participants in the Rental Pool.

Internet reservation channels may negatively impact our bookings and results of operations.

Internet travel intermediaries such as Travelocity.com®, Expedia.com® and Priceline.com® are attempting to commoditize hotel rooms by increasing the importance of price and general indicators of quality at the expense of brand or property-specific identification. These travel intermediaries hope that consumers will eventually develop brand loyalties to their reservations system rather than to lodging brands. Although we expect to derive most of our business from traditional channels, if the amount of sales made through internet intermediaries increases significantly, our business and profitability may be significantly harmed, and proceeds to participants in the Rental Pool may be reduced.

The Resort places significant reliance on technology.

The hospitality industry continues to demand the use of sophisticated technology and systems including technology utilized for property management, procurement, reservation systems, operation of customer loyalty programs, distribution and guest amenities. These technologies can be expected to require refinements and there is the risk that advanced new technologies will be introduced. There can be no assurance that as various systems and technologies become outdated or new technology is required we will be able to replace or introduce them as quickly as our competition or within budgeted costs for such technology. Further, there can be no assurance that we will achieve the benefits that may have been anticipated from any new technology or system.

6

The Resort is capital intensive, and may become uncompetitive in the event that sufficient financing is not available.

For the Resort to remain attractive and competitive, we must spend money periodically to keep the properties well maintained, modernized and refurbished. These expenditures result in an ongoing need for cash. To the extent we cannot fund expenditures from cash generated by the Resort’s operations, we must seek to obtain funds by borrowing or otherwise. We may be unable to find such financing on favorable terms, if at all. To the extent that we are unsuccessful in obtaining such financing, it could adversely impact the Resort’s results from operations and proceeds to the Rental Pool participants.

Our investment in the Resort is subject to numerous risks, which could adversely affect our income.

As a result of our ownership of the Resort, we are subject to the risks that generally relate to investments in real property. The investment returns available from equity investments in real estate such as the Resort depends in large part on the amount of income earned and capital appreciation generated by the Resort, reduced by the expenses incurred to operate it. In addition, a variety of other factors affect both income from the Resort and the Resort’s real estate value, including governmental regulations, real estate, insurance, zoning, tax and eminent domain laws, interest rate levels and the availability of financing. When interest rates increase, the cost of developing, expanding or renovating real property increases and real property values may decrease as the number of potential buyers decreases. Any of these factors could have a material adverse impact on our results of operations or financial condition. If the Resort does not generate revenue sufficient to meet operating expenses, including debt service and capital expenditures, our income will be adversely affected.

Environmental regulations may increase the Resort’s costs, or limit our ability to develop, use or sell the Resort.

Environmental laws, ordinances and regulations of various federal, state, local and foreign governments impact our properties and could make us liable for the costs of removing or cleaning up hazardous or toxic substances on, under, or in property we currently own or operate. These laws could impose liability without regard to whether we knew of, or were responsible for, the presence of hazardous or toxic substances. The presence of hazardous or toxic substances, or the failure to properly clean up such substances when present, could jeopardize our ability to develop, use, sell or rent the real property or to borrow using the real property as collateral. If we arrange for the disposal or treatment of hazardous or toxic wastes, we could be liable for the costs of removing or cleaning up wastes at the disposal or treatment facility, even if we never owned or operated that facility. Other laws, ordinances and regulations could require us to manage, abate or remove lead or asbestos containing materials. Certain laws, ordinances and regulations, particularly those governing the management or preservation of wetlands, coastal zones and threatened or endangered species, could limit our ability to develop, use, or sell the Resort. Further, in the event that environmental obligations prevent us from developing, using or selling the Resort, distributions to the Rental Pool participants may be adversely affected either directly or as a result of reduced funding for the marketing and operation of the Rental Pool.

Although the courts have recently delivered favorable rulings in the Land Use Lawsuits to which we are a party, in the event that the ultimate rulings in these matters are unfavorable to us, the value of Parcel F and the Resort would be adversely effected.

As discussed in further detail under the heading “Legal Matters” in Part I, Item 3 of this report, on March 10, 2005 we filed a motion to intervene as a defendant in the lawsuit styled Innisbrook Condominium Association, Inc., C. Frank Wreath, Meredith P. Sauer, and Mark Banning (as plaintiffs) vs. Pinellas County, Florida, Golf Host Resorts, Inc. and Innisbrook F LLC (as defendants), Case No. 043388CI-15. This matter relates to a tract of land within the Resort known as Parcel F. In April 2005, a subsequent lawsuit relating to this matter was filed. We are also a defendant in this subsequent lawsuit. In this report, we refer to the March 2005 and the April 2005 lawsuits as the Land Use Lawsuits.

On January 6, 2006, the court ruled in favor of all defendants and against all plaintiffs as to each count in both cases. While the January 6, 2006 ruling is a very favorable result for us and for the other defendants, the plaintiffs in the Land Use Lawsuits have the right to appeal or otherwise challenge that ruling.

In the event that the plaintiffs convince a court to overturn the January 6, 2006 ruling, we could lose all or substantially all of our land use and development rights with respect to Parcel F. Such an unfavorable result could also cause us to experience reduced club memberships at the Resort and could adversely impact our ability to realize the benefits from the proposed development of Parcel F. In addition, if the defendants do not ultimately prevail in the Land Use Lawsuits and a court subsequently applies a similar interpretation of our rights with respect to the remaining developable units at the Resort, our land use and development rights in those remaining units could be jeopardized, adversely effecting both our ability to develop the Resort and the value of the Rental Pool units.

7

So-called acts of God, terrorist activity and war could adversely affect the Resort.

The Resort’s financial and operating performance may be adversely affected by so-called acts of God, such as natural disasters, in Florida and in areas of the world from which we draw a large number of guests. Similarly, wars (including the potential for war), terrorist activity (including threats of terrorist activity), political unrest and other forms of civil strife and geopolitical uncertainty have caused in the past, and may cause in the future, our results to differ materially from anticipated results. The returns to participants in the Rental Pool could be adversely impacted in the event that acts of God, war or terrorism impact the Resort’s ability to attract guests.

Some potential losses of the Resort are not covered by insurance.

We carry comprehensive insurance coverage for general liability, property, business interruption and other risks with respect to the Resort. Our policies offer coverage features and insured limits that we believe are customary for similar types of property. Generally, our “all-risk” property policies provide that coverage is available on a per occurrence basis and that, for each occurrence, there is a limit as well as various sub-limits on the amount of insurance proceeds we can receive. In addition, there may be overall limits under the policies. Sub-limits exist for certain types of claims such as service interruption, abatement, expediting costs or landscaping replacement, and the dollar amounts of these sub-limits are significantly lower than the dollar amounts of the overall coverage limit.

In addition, there are also other risks such as war, certain forms of terrorism such as nuclear, biological or chemical terrorism, acts of God such as hurricanes and earthquakes and some environmental hazards that may be deemed to fall completely outside the general coverage limits of our policies or may either be uninsurable or too expensive to justify insuring against.

Our operations at the Resort are dependent upon outside managers, and if those managers are less successful than expected, the Resort’s results of operations and the proceeds available for distribution to the Rental Pool participants will be adversely affected, potentially in a material way.

Westin manages the daily operations of the Resort pursuant to our management agreement with Westin, and Troon manages the golf facilities at the Resort pursuant to related contractual commitments with Westin. In the event that these third party managers fail to perform under their respective contracts as expected, or in the event that they default on their obligations, the Resort’s results of operations and proceeds available for distribution to the Rental Pool participants will be adversely affected, potentially in a material way.

A sustained increase in energy costs may negatively impact the Resort’s results by increasing its energy-related costs and by discouraging potential guests from traveling and taking part in recreational activities.

During the past year, energy costs in the United States have increased substantially. Energy costs represent an increasingly larger percentage of the costs of the Resort, and we expect energy costs to increase in both absolute and relative terms in future periods. In addition, we expect that higher energy costs will negatively affect the Resort by discouraging travel and recreational activities. In particular, potential guests of the Resort are less likely to travel as they bear the affects of higher energy costs as either higher airline fares or in an increased cost per gallon of gasoline. In addition, higher energy costs may reduce the disposable income of potential guests, making them less likely to spend money for travel and recreational activities. As a result of these factors, a sustained increase in energy costs may negatively impact the Resort’s results by increasing its energy-related costs and by discouraging traveling and taking part in recreational activities.

Risk factors relating to GTA and GTA’s operating partnership

Our parent is a subsidiary of GTA’s operating partnership. GTA is a public reporting company under the Exchange Act. Due to our relationship with GTA, including our dependence upon GTA, its operating partnership or its subsidiaries for funding that we may require, we believe that its risk factors are relevant to our sole member and to the participants in the Rental Pool. You should note that certain of the information contained in GTA’s risk factors from GTA’s Form 10-K for the year ended December 31, 2005, which are filed as Exhibit 99.1 hereto, particularly those specific to GTA’s liquidating distributions, are not relevant to you unless you are a holder of GTA’s common stock; however, such risk factors are informative in that they may indicate certain factors or events that may impact GTA and reduce GTA’s willingness or ability to provide funding to the Resort and the Rental Pool units.

8

ITEM 1B. UNRESOLVED STAFF COMMENTS

Not applicable.

The Resort is situated on approximately 1,000 acres of land located in the northern portion of Pinellas County, Florida, near the Gulf of Mexico. It is approximately 9 miles north of Clearwater and approximately 20 miles west of Tampa. There are 938 condominium units, 36 of which are strictly residential, with the balance eligible for Rental Pool participation. Of the 902 remaining eligible units, 500, on average, participate in the Rental Pool on a year-to-year basis. See additional discussion in Item 1 under the caption “Rental Pool Condominiums.” These condominium units are leased by us from the condominium owners and used as hotel accommodations for the Resort. GTA-IB Condominium, LLC, which, like us, is a subsidiary of GTA-IB Golf Resort, LLC, owns three condominium units that participate in the rental pool in the same fashion as all other Rental Pool participants. Approximately 25% of the units have internal lockout doors, which allow the rental of the condominium unit as two hotel rooms. We estimate that as a result of the potential use of internal lockout doors, the average of 500 units participating in the Rental Pool at any one time is equivalent to approximately 600 hotel rooms. The Resort complex includes 72 holes of golf; practice ranges; three clubhouses with retail, golf, and food and beverage outlets; three conference and exhibit buildings; six swimming pools including a themed water attraction; a recreation center; a tennis/fitness facility and numerous administrative and support structures. These amenities are owned by us. Substantially all of the assets of the Resort are encumbered by the mortgage held by GTA, LP.

In the normal course of our operations, we are subject to claims and lawsuits. We do not believe that the ultimate resolution of such matters will materially impair operations or have an adverse effect on our financial position and results of operations.

Land Use Lawsuit

On March 10, 2005 in the Circuit Court of the Sixth Judicial Circuit, in and for Pinellas County, Florida, Civil Division, the Company filed a Motion to Intervene in the suit titled Innisbrook Condominium Association, Inc., C. Frank Wreath, Meredith P. Sauer, and Mark Banning, Plaintiffs vs. Pinellas County, Florida, Golf Host Resorts, Inc. and Innisbrook F LLC, Defendants, Case No. 043388CI-15. In this report, we refer to this matter as the “Initial Land Use Lawsuit.” The plaintiffs in the Initial Land Use Lawsuit have filed a multi-count complaint seeking injunctive and declaratory relief with respect to the land use and development rights of a tract of land known as Parcel F. Parcel F is a parcel of land located within the Resort. The plaintiffs allege that there are no remaining development units (residential units) available to be developed within the Resort property. On March 29, 2005, we filed a Motion to Intervene as a defendant in the Initial Land Use Lawsuit in order to protect our property, and our land use and development rights with respect to Parcel F and our property. A hearing on the Motion to Intervene was held on April 4, 2005, after which the court granted our Motion to Intervene. On April 5, 2005, we joined in the filing of a Motion to Dismiss and Motion to Strike three of the seven counts of the plaintiffs’ complaint. The court granted the Motion to Dismiss on April 26, 2005. On that same date, four individuals (Joseph E. Colwell, Marcia G. Colwell, Kirk E. Covert, Deborah A. Covert) and Autumn Woods Homeowner’s Association, Inc. moved to intervene in the Initial Land Use Lawsuit. The court has not ruled on that motion. On April 8, 2005, a separate suit was filed by James M. and Mary H. Luckey and Andrew J. and Aphrodite B. McAdams against Pinellas County, a political subdivision of the State of Florida, Golf Host Resorts, Inc., a foreign corporation and Bayfair Innisbrook, LLC, a Florida limited liability corporation. In this report we refer to this matter as the “Subsequent Land Use Lawsuit.” The Subsequent Land Use Lawsuit seeks injunctive and declaratory relief in six separate counts, all relating to the land use and development rights of Parcel F. This suit was consolidated with the Initial Land Use Lawsuit on May 3, 2005. After May 6, 2005 we have filed our Motion to Dismiss the Subsequent Land Use Lawsuit. The motion was heard by the court on May 31, 2005. Since that hearing, we have filed an Answer and Affirmative Defenses to both complaints that have been filed in the consolidated action. On August 3, 2005, a case management conference was held before the judge who is now presiding over this case. At that hearing, the court scheduled a hearing on the defense motions for summary judgment for August 30, 2005, and a trial starting on December 12, 2005. On August 30, 2005, the judge heard extensive argument on the defense motions for summary judgment and entered a number of rulings in the defendants’ favor. In summary, the court dismissed those claims in the Initial Land Use Lawsuit and the Subsequent Land Use Lawsuit which are founded upon the theory that the proposed development is inconsistent with the Pinellas Countywide Plan and Rules adopted pursuant to Chapter 73-594, Laws of Florida. The court further dismissed for lack of jurisdiction those claims of the plaintiffs’ in the Subsequent Land Use Lawsuit that are based on the theory that the proposed development is inconsistent with the Pinellas Comprehensive Plan. The court entered a similar ruling on certain counts of the Third Amended Complaint as to some, but not all, of the Plaintiffs in the Initial Land Use Lawsuit.

9

The defendants in the Initial Land Use Lawsuit also filed a Motion to Strike the plaintiffs’ Demand for Jury Trial. In the face of that motion, the plaintiffs dropped their jury trial demand and the court confirmed by order dated September 21, 2005 that this case would not be tried by a jury. The court then entered an order scheduling the remaining claims for non-jury trial during December 2005.

In addition, the plaintiffs in the Initial Land Use Lawsuit have filed a motion for summary judgment. The court set the hearing date for the summary judgment review for December 7, 2005.

As an intervenor in the Initial Land Use Lawsuit, we will seek to obtain a ruling from the court which preserves and protects our property, and our land use and development rights with respect to Parcel F and our property, in order to maximize the value of those rights as they relate both to Parcel F and the Resort in general. We refer to these two matters as the “Land Use Lawsuits.” See further discussion of the Land Use Lawsuits under the heading “Risk Factors” in Part I, Item 1A of this report.

From December 19 through December 23, 2005, the court tried these consolidated cases in a non-jury trial. At the conclusion of the evidentiary portion of the trial, the court deferred final argument until Friday, January 6, 2006. On that date, the court heard final arguments and rendered its decision. The court ruled in favor of all defendants and against all plaintiffs as to each count in both Land Use Lawsuits. On March 8, 2006, the court formally entered its final judgment on the record ruling in favor of the defendants on all counts and denying all claims asserted by the plaintiffs in both Land Use Lawsuits. On March 31, 2006, the plaintiffs in the consolidated cases filed a notice of appeal.

Property Tax Lawsuit

We filed lawsuits against the property appraiser of Pinellas County Florida, or Pinellas County, to challenge the 2004 and 2005 real estate assessment on the Resort property. Pinellas County filed a motion to dismiss, which was denied by the court. No trial date has been set. If Pinellas County were to prevail, management believes that there would be no material adverse effect upon our financial statements, as the entire Pinellas County assessment is fully accrued and accounted for at December 31, 2005.

Complaints by a Former Employee of Golf Host Securities, Inc., or GHSI

Occupational Safety and Health Administration, or OSHA, Complaints

In July 2005, GHSI, a subsidiary of our parent, received from OSHA notice that a former employee of GHSI had filed a complaint with OSHA alleging that GHSI had violated Title VIII of the Sarbanes-Oxley Act of 2002 and Section 806 of the Corporate and Criminal Fraud Accountability Act. OSHA requested that GHSI respond to the allegation that GHSI violated these laws. On November 3, 2005, our counsel in this matter received a letter from OSHA notifying us that this matter had been deferred to the settlement agreement, described below, and, as such, the matter had been administratively closed.

Equal Employment Opportunity Commission, or EEOC, Complaints

In July 2005, we received from the EEOC, a notice of a charge of discrimination by the same former employee of GHSI. The EEOC has requested that we provide a statement of our position on the issues covered by the former employee’s charge and copies of supporting documentation. The former employee of GHSI alleged in his charge of discrimination that the termination of his employment with GHSI was the result of unlawful discrimination by us in violation of the Age Discrimination in Employment Act and the Florida Civil Rights Act. On November 21, 2005, we received an acknowledgment of settlement from the EEOC notifying us that the EEOC will take no further action on this matter.

10

National Association of Securities Dealers, or NASD, Complaints

In July 2005, GHSI received notice that the same former employee of GHSI had filed a complaint with the NASD alleging violations of NASD rules and violations of federal and state securities statutes. This former employee included in his claim an allegation that our parent had ignored his complaints that our parent’s actions were violations of law, and he asked the NASD to revisit its approval of our parent’s ownership of GHSI.

Florida Department of Real Estate, or FDRE, Complaints

In July 2005, GHSI received notice that the same former employee of GHSI had filed a complaint with the FDRE for GHSI’s alleged failure to deliver commissions of approximately $13,000 which this former employee claimed GHSI owed to him. GHSI’s former employee also alleged that (i) our parent’s officers (who are also our officers) violated Florida Statute 475, as well as other federal and state statutes and the regulations of various regulatory agencies, and that (ii) our parent’s actions violated, among other federal and state laws, the whistleblower protections under state and federal law, and the Age Discrimination in Employment Act and Florida Civil Rights Act prohibiting age discrimination.

Settlement Agreement

On November 4, 2005, this former employee of GHSI entered into a settlement agreement with us, GTA, LP, GHSI, GTA G.P., Inc., GTA L.P., Inc., GTA-IB Golf Resort, LLC, GTA-IB Operations, LLC and GTA-IB Management, LLC relating to the employee’s claims with OSHA, the EEOC, the NASD and the FDRE. Pursuant to the settlement agreement, among other things, neither party admits any liability or wrongdoing, we paid the former employee $50,000, the former employee dismissed its claims and filed appropriate papers to withdraw or dismiss the referenced claims with prejudice and the former employee notified the agencies involved that all disputes between GHSI and the former employee have been resolved with prejudice.

Class Action Lawsuit

The Resort, which we now own, served as collateral for a $79 million original balance non-recourse loan that GTA, LP made in 1997 to GHR. GHR entered into an arrangement with many of the parties who own condominium units at the Resort providing for the condominiums owned by these persons to be placed in a pool and rented as hotel rooms to guests of the Resort. Certain of the condominium owners (as plaintiffs) initiated a legal action against GHR, and its corporate parent, Golf Hosts, Inc. (as defendants), regarding various aspects of this arrangement. We are not a party to this lawsuit, nor are GTA, GTA-IB Golf Resort, LLC, Golf Trust of America, L.P. or our respective affiliates.

On July 29, 2004, the court entered an order granting the defendant’s motion for summary judgment. The plaintiffs filed an appeal of this ruling on October 26, 2004. Briefing has been completed in the appeal from the court’s final judgment granting the motion for summary judgment. Argument before the appellate court was held September 21, 2005. By Order dated September 30, 2005, the Florida appellate court (Second District Court of Appeals) affirmed the lower court’s final judgment granting the defendant’s motion for summary judgment. The plaintiffs subsequently filed a motion with the appellate court for a rehearing of their appeal, or in the alternative, to certify a question to the Florida Supreme Court. The appellate court denied that motion by Order dated November 3, 2005. The time available for the Plaintiffs to appeal has now expired.

In connection with the execution of the Settlement Agreement between us and GHR (and certain other affiliated parties), GHR provided a limited indemnity to defend and hold harmless GTA (and its affiliates, including us) from and against any and all costs, liabilities, claims, losses, judgments, or damages arising out of or in connection with the class action lawsuit described above, as well as liabilities accruing on or before the closing data relating to employee benefits and liabilities for contracts or agreements not disclosed by GHR to GTA. In return, we delivered a duly executed release.

ITEM 4. SUBMISSION OF MATTERS TO A VOTE OF SECURITY HOLDERS

Not applicable.

11

ITEM 5. MARKET FOR REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Market Information

We are a single member limited liability company and do not have any stock. Our membership interests are not publicly traded.

There are a total of 902 condominium units allowing Rental Pool participation by their owners, of which three are owned by our affiliate GTA-IB Condominium, LLC. Of the units not owned by GTA-IB Condominium, LLC, 878 were sold by GHR under Registration Statements filed by GHR that were declared effective by the Securities and Exchange Commission on or before March 1, 1983. The remaining 21 units were sold via private offerings exempt from registration with the Securities and Exchange Commission. As of December 31, 2005, approximately 850 different owners hold the condominium units not owned by us or by our affiliates.

Those condominium units sold by GHR, which allow Rental Pool participation, are deemed to be securities because of the Rental Pool feature. These units are referenced in this report as Rental Pool securities. While the Rental Pool securities are deemed securities pursuant to the Securities Act of 1933, as amended, there is no market for such securities other than the normal real estate market. As such, certain items referenced under the heading “Risk Factors” in Part I, Item 1A of this report may have a more significant effect due to this lack of liquidity and the fact that the lease agreements governing Rental Pool participation generally provide the participants in the Rental Pool with an annual right to terminate their participation in the pool.

Since the Rental Pool securities are real estate, no dividends have been paid or will be paid to their owners. However, the Rental Pool lease agreements provide that the Rental Pool participants are entitled to a contractual distribution paid quarterly in exchange for our right to use their condominium units in the Rental Pool.

Equity Compensation Plans

We do not have any equity compensation plans.

Recent Sales of Unregistered Securities

Not applicable.

ITEM 6. SELECTED FINANCIAL DATA

The following selected financial data should be read in conjunction with our consolidated financial statements and the related notes and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” included elsewhere in this report. Historical results are not necessarily indicative of the results to be expected in the future.

|

| Predecessor Basis(1) |

| |||||||||||||||||

|

|

|

|

|

|

|

| Year ended December 31, |

| |||||||||||

|

| Year ended December 31, 2005 |

| Period |

| Period |

| 2003 |

| 2002 |

| 2001 |

| |||||||

|

| (in thousands, except average daily Rental Pool distribution) |

| |||||||||||||||||

Revenue |

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Hotel |

| $ | 13,335 |

| $ | 4,356 |

| $ | 6,672 |

| $ | 11,786 |

| $ | 12,156 |

| $ | 16,287 |

| |

Food and beverage |

| 11,557 |

| 4,445 |

| 5,824 |

| 12,102 |

| 11,336 |

| 12,966 |

| |||||||

Golf |

| 13,352 |

| 4,248 |

| 7,334 |

| 11,269 |

| 11,852 |

| 13,637 |

| |||||||

Other |

| 3,637 |

| 1,174 |

| 2,793 |

| 3,778 |

| 5,252 |

| 4,829 |

| |||||||

Total revenue |

| $ | 41,881 |

| $ | 14,223 |

| $ | 22,623 |

| $ | 38,935 |

| $ | 40,596 |

| $ | 47,719 |

| |

Net loss |

| $ | (4,050 | ) | $ | (4,440 | ) | $ | (6,345 | ) | $ | (11,466 | ) | $ | (9,178 | ) | $ | (10,355 | ) | |

Cash dividends per common share/LLC Interest(2) |

| — |

| — |

| — |

| — |

| — |

| — |

| |||||||

Average daily Rental Pool |

| $ | 23.28 |

| $ | 14.71 |

| $ | 20.62 |

| $ | 18.32 |

| $ | 20.21 |

| $ | 25.73 |

| |

Total Rental Pool distribution, net(4) |

| $ | 4,996 |

| $ | 1,473 |

| $ | 2,383 |

| $ | 3,932 |

| $ | 4,415 |

| $ | 6,127 |

| |

Total assets |

| $ | 54,095 |

| $ | 55,694 |

| $ | 96,025 |

| $ | 60,933 |

| $ | 62,516 |

| $ | 59,870 |

| |

Long-term obligations |

|

|

|

|

|

|

|

|

|

|

|

|

| |||||||

Notes payable |

| $ | 39,240 |

| $ | 39,240 |

| $ | 78,975 |

| $ | 78,975 |

| $ | 79,004 |

| $ | 79,614 |

| |

Capital leases |

| $ | 625 |

| $ | 612 |

| $ | 761 |

| $ | — |

| $ | — |

| $ | — |

| |

Other obligations |

| $ | 13,478 |

| $ | 11,489 |

| $ | 21,932 |

| $ | 18,481 |

| $ | 17,069 |

| $ | 13,460 |

| |

(1) The predecessor basis financial statements for the period January 1, 2004 to July 15, 2004 and the years ended December 31, 2003, 2002 and 2001, represent the operating results of Golf Host Resorts, Inc. The predecessor’s financial statements for 2004 and 2003 are included in Item 15 herein. Those financial statements include assets and liabilities at carrying values that differ from ours; therefore, direct comparisons may not be made between periods.

(2) We have not made any distributions to our sole member and do not intend to make any distributions to our sole member in the near term.

(3) The average daily Rental Pool distribution is calculated by dividing the Rental Pool distribution by the total available room nights.

(4) The total Rental Pool distribution is reflected net of allowable deductions for Lessee Advisory Committee expenses pursuant to the Master Lease Agreement.

12

ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATION

We were formed on December 30, 2002. We are a wholly owned subsidiary of GTA-Golf Resort, LLC. GTA-Golf Resort, LLC is a wholly owned subsidiary of GTA, LP, the operating partnership of GTA. GHR, an entity affiliated with Starwood Capital Group LLC, is the former owner of the Resort and the former borrower under a $79 million participating mortgage loan funded by GTA, LP in June 1997. This participating mortgage loan was secured by the Resort, cash, certain shares of GTA’s common stock held by GHR and excess land at the Resort. The Resort is a 72-hole destination golf and conference facility, with a private club component, located near Tampa, Florida.

GHR became delinquent in its interest payments on the loan from GTA, LP in November 2001. On March 8, 2002, GTA, LP delivered a legal notice to GHR accelerating the entire amount of GHR’s indebtedness to GTA, LP as a result of GHR’s continuing default under the participating mortgage loan. GTA, LP also notified Westin, the manager of the Resort, that it deemed Westin to be in breach under its subordination agreement with GTA, LP as a result of Westin’s failure to remit payment of funds to GTA, LP on behalf of GHR. The participating mortgage loan was a non-recourse loan. Accordingly, following an event of default thereunder, GTA, LP and GTA could not bring a legal action directly against GHR to compel payment. Rather, GTA, LP’s only recourse was to proceed against the guarantors and/or to foreclose upon GHR and the Resort’s assets, three condominiums then owned by GHR, certain shares of GTA’s common stock held by GHR and any other property of GHR that had been pledged as collateral to secure GTA, LP’s loan.

We and GTA, LP entered into the Settlement Agreement dated July 15, 2004 with GHR, Golf Hosts, Inc., Golf Host Management, Inc. and Golf Host Condominium, Inc. The Settlement Agreement settled a number of issues between the parties, including GHR’s default under the $79 million loan made by GTA, LP to GHR in June 1997. As part of the Settlement Agreement, we took ownership of the Resort effective July 16, 2004. Also in connection with the Settlement Agreement, we entered into a management agreement with Westin providing for Westin’s management of the Resort, and Westin and Troon entered into a facility management agreement providing for Troon’s management of the golf facilities at the Resort.

GTA, LP had previously entered into an agreement with GHR and the prospective purchaser of a parcel of undeveloped land within the Resort known as Parcel F. This agreement, known as the Parcel F Development Agreement, was executed on March 29, 2004 and held in escrow pending execution of the Settlement Agreement and consummation of related transactions. The Parcel F Development Agreement, which we and our affiliates entered into as a means to avoid interference with the operations of the Resort, sets forth the terms and conditions under which Parcel F may be developed, including restrictions on the owner of Parcel F in favor of us as owner of the Resort.

13

Critical Accounting Policies

The following accounting policies are considered critical by our management. These and other accounting policies require that estimates be made based on assumptions and judgment, which affect revenues, expenses, assets, liabilities and disclosure of contingencies in our financial statements. These estimates and assumptions are based on historical experience and on various other factors that are believed to be reasonable under the circumstances. However, actual results may differ from these estimates due to different conditions.

Impairment of Long-Lived Assets

We periodically review our long-lived assets for impairment by comparing the carrying values of the assets with their estimated future undiscounted cash flows. If it is determined that an impairment loss has occurred, the loss is recognized during that period. The impairment loss is calculated as the difference between asset carrying values and fair value as determined by discounted cash flow analysis, giving consideration to recent operating performance and pricing trends.

The settlement was accounted for using methods consistent with purchase accounting in accordance with Statement of Financial Accounting Standards, or SFAS, No. 141 “Business Combinations.” The settlement amount was allocated to the net assets acquired, including the liabilities assumed as of July 15, 2004, based upon their estimated fair values as of that date. The settlement amount was allocated in the table below (in thousands):

Current assets |

| $ | 4,621 |

|

Property & Equipment |

| 28,850 |

| |

Intangible Assets |

| 20,170 |

| |

Other Assets |

| 2,454 |

| |

Total assets |

| $ | 56,095 |

|

Current liabilities |

| $ | 6,219 |

|

Long term liabilities |

| 10,636 |

| |

Loan payable to GTA, LP |

| 39,240 |

| |

Total liabilities |

| $ | 56,095 |

|

In reviewing for impairment of our long lived assets, we review the financial performance of the Resort in the aggregate for material variances from our expectations of the Resort’s revenues. The Resort’s performance has continued to improve since we took title to it on July 15, 2004 and, based upon bookings, this trend indicates this performance recovery it will continue through 2006. Therefore, there were no significant impairment losses related to long-lived assets for year ended December 31, 2005. In particular, our primary long-lived asset is Parcel F. Due to the fact that the assumptions that we applied to derive the $2,200,000 value of Parcel F and our other intangible assets have not materially changed, there is no significant impairment loss reported for the year ended December 31, 2005.

Intangible assets

We evaluate intangible assets for impairment annually or if a significant event occurs or circumstances change. Factors we consider important, and which could indicate impairment, include the following: (i) significant underperformance relative to historical or projected future operating results; (ii) significant changes in the manner of our use of the acquired assets or the strategy for our overall business; and (iii) significant negative industry or economic trends.

We place our intangible assets in the following categories: (i) the water contract; (ii) club memberships; (iii) the trademark and the trade name; (iv) the Rental Pool; and (v) guest bookings. The valuation of the water contract is based on the projected annual savings associated with having this contract. The water contract has an indefinite life. The value of the club membership is derived from our membership base. There have been no material changes in the number of members of our club. The valuation of the trademark and trade name is derived from the residual revenue stream from the Resort revenues that is attributed to the Innisbrook trade name. We attribute an indefinite life to the trademark and trade name. The valuation of the Rental Pool is based on estimates of revenue derived by us from our Rental Pool operations. The Rental Pool’s valuation is dependent on maintaining a specific number of units in the Rental Pool to accommodate the Resort operations. There has been no material change in the number of participating condominium units in the Rental Pool during the period.

14

During the fourth quarter of 2005, we completed our annual intangible asset impairment assessment, and based on the results, we determined that no impairment of intangible assets existed at December 31, 2005, and there have been no indicators of impairment since that date. A subsequent determination that the intangible assets are impaired, however, could have a significant adverse impact on our results of operations or financial condition.

Results of Operations

We took title to the Resort at 12:00 a.m. on July 16, 2004. As a result, the financial results of GHR, the predecessor owner, are included below for the periods prior to July 16, 2004. The predecessor owner’s results are included only for comparative purposes. While the operations of the Resort have remained substantially unchanged with respect to the manner of recording revenues and expenses, the financial statements of the predecessor owner include assets and liabilities at carrying values that differ from the carrying values presented in our financial statements. As a result, there can be no assurances that the comparative information provided below is not impacted to some degree by the change in the carrying values of the assets and liabilities between the predecessor owner’s financial statements and our financial statements.

Utilization of the Resort facilities during the past three years by facility type is illustrated in the table below:

|

| 2005 |

| 2004 |

| 2003 |

| |||

Available room nights |

| 214,580 |

| 215,716 |

| 214,557 |

| |||

Actual room nights |

|

|

|

|

|

|

| |||

Group |

| 59,138 |

| 51,606 |

| 65,167 |

| |||

Transient |

| 39,281 |

| 32,858 |

| 21,997 |

| |||

Total room nights |

| 98,419 |

| 84,464 |

| 87,164 |

| |||

Average room rate |

| $ | 135.49 |

| $ | 130.55 |

| $ | 135.21 |

|

Food and beverage covers |

| 406,175 |

| 379,059 |

| 437,174 |

| |||

Average food check |

| $ | 19.40 |

| $ | 18.47 |

| $ | 19.18 |

|

Golf Rounds |

|

|

|

|

|

|

| |||

Resort guests |

| 79,312 |

| 70,672 |

| 68,043 |

| |||

Member/guests |

| 39,694 |

| 37,577 |

| 34,172 |

| |||

Total golf rounds |

| 119,006 |

| 108,249 |

| 102,215 |

| |||

Total golf revenue per golf round |

| $ | 112.20 |

| $ | 106.99 |

| $ | 110.25 |

|

Golf course maintenance cost per golf round |

| $ | 32.53 |

| $ | 34.81 |

| $ | 35.00 |

|

The 2004 and 2003 Combined Statements of Loss are used as a reference for the comparative analysis of changes in operating results in the table below (in thousands):

|

| Year Ended December 31, |

| Year |

| Period |

| Period |

| Year Ended December 31, |

| |||||

Revenues |

|

|

|

|

|

|

|

|

|

|

| |||||

Hotel |

| $ | 13,335 |

| $ | 11,028 |

| $ | 4,356 |

| $ | 6,672 |

| $ | 11,786 |

|

Food and beverage |

| 11,557 |

| 10,269 |

| 4,445 |

| 5,824 |

| 12,102 |

| |||||

Golf |

| 13,352 |

| 11,582 |

| 4,248 |

| 7,334 |

| 11,269 |

| |||||

Other |

| 3,637 |

| 3,967 |

| 1,174 |

| 2,793 |

| 3,778 |

| |||||

Total revenues |

| 41,881 |

| 36,846 |

| 14,223 |

| 22,623 |

| 38,935 |

| |||||

Expenses |

|

|

|

|

|

|

|

|

|

|

| |||||

Hotel |

| 11,411 |

| 9,749 |

| 4,138 |

| 5,611 |

| 10,169 |

| |||||

Food and beverage |

| 8,140 |

| 7,886 |

| 3,238 |

| 4,648 |

| 8,037 |

| |||||

Golf |

| 7,620 |

| 7,423 |

| 3,173 |

| 4,250 |

| 7,157 |

| |||||

Other |

| 9,902 |

| 9,003 |

| 4,100 |

| 4,903 |

| 8,285 |

| |||||

General and administrative expenses |

| 4,744 |

| 4,899 |

| 2,096 |

| 2,803 |

| 4,639 |

| |||||

Depreciation and amortization |

| 2,479 |

| 2,875 |

| 1,249 |

| 1,626 |

| 2,998 |

| |||||

Total expenses |

| 44,296 |

| 41,835 |

| 17,994 |

| 23,841 |

| 41,285 |

| |||||

Operating loss |

| (2,415 | ) | (4,989 | ) | (3,771 | ) | (1,218 | ) | (2,350 | ) | |||||

Interest expense, net |

| (1,635 | ) | (5,796 | ) | (669 | ) | (5,127 | ) | (9,116 | ) | |||||

Net loss |

| $ | (4,050 | ) | $ | (10,785 | ) | $ | (4,440 | ) | $ | (6,345 | ) | $ | (11,466 | ) |

15

2005 Compared to 2004

During the year ended December 31, 2005, total room nights at the Resort increased to 98,419 from 84,464 in the same period of 2004. Total room nights are comprised of transient room nights and group room nights. During the year ended December 31, 2005, the Resort saw stronger transient business which exceeded historical averages. For the year ended December 31, 2005, total transient room nights were 39,281, an increase of 6,423 room nights, or 19.5%, from the same period in 2004. In addition, during 2005 the Resort also began to see a recovery in golf package business and corporate group booking patterns as against booking patterns for 2004. Total golf packages sold increased by 1,493 packages, or 35.8%, from 2004 to 2005. Group room nights for the year ended December 31, 2005 increased by 7,532, or 14.6%, as compared to the prior year. We hope that the recovery in golf package business and corporate group booking patterns which resulted in the increase in room nights in 2005 will continue into 2006. The last minute cancellations of two large corporate events in the first half of 2004, within the peak season, and the loss of approximately 3,148 golf rounds as a result of the unusual weather conditions in the state of Florida in August and September of 2004, caused the Resort to lose an aggregate of approximately $850,000 in revenue, net of cancellation fees, during that year. Cancellation fees of approximately $651,000 relating both to these two large events and to a number of smaller events have been included in total revenues during the year ended December 31, 2004. During 2005, due to improved weather conditions, the Resort did not experience as many cancellations as in 2004. As a result, cancellation fees we received in 2004 were $512,000 less than in 2004. Although the Resort experienced less cancellations, our management believes that the Resort’s bookings in 2005 were adversely effected as a result of the 2004 hurricane season.