Exhibit 99.1(a)

Third Quarter 2022 Earnings Prepared Comments

Brandon Ayache, Celanese Corporation, Vice President, Investor Relations

This is the Celanese Corporation third quarter 2022 earnings prepared comments. The Celanese Corporation third quarter 2022 earnings release was distributed via Business Wire this afternoon and posted on our investor relations website, investors.celanese.com. As a reminder, some of the matters discussed below may include forward-looking statements concerning, for example, our future objectives and plans. Please note the cautionary language contained at the end of these comments. Also, some of the matters discussed include references to non-GAAP financial measures. Explanations of these measures and reconciliations to the comparable GAAP measures are included on our investor relations website under Financial Information/Non-GAAP Financial Measures. The earnings release and non-GAAP information and the reconciliations are being furnished to the SEC in a Current Report on Form 8-K. These prepared comments are also being furnished to the SEC in a separate Current Report on Form 8-K.

On the earnings conference call tomorrow morning, management will be available to answer questions.

Lori Ryerkerk, Celanese Corporation, Chairman of the Board and Chief Executive Officer

I am pleased to share that earlier this week we successfully closed our acquisition of the Mobility & Materials (M&M) business. The executive leadership team and I were pleased to join our newest colleagues across six M&M sites on day one to personally welcome them to Celanese. The energy this week has been high across the organization and we are thrilled to enter the next chapter of Celanese growth together by integrating and elevating M&M as part of Engineered Materials (EM).

We have a significant amount of work in front of us to execute against our objectives. I have full confidence in our ability to get the work done, even amid external challenges. My confidence is supported by our third quarter performance of adjusted earnings of $3.94 per share and free cash flow generation of $325 million. Given the long list of unanticipated headwinds in the quarter, I am proud of the entire team

1

for delivering adjusted earnings per share less than 2 percent off of our quarterly guidance. They once again demonstrated their resolve to achieve our targeted results. In the third quarter, we navigated:

•a sharp pullback in demand for acetyls in paints, coatings, and construction applications that progressed across the quarter due to lower renovation and construction activity as well as customer destocking;

•foreign currency headwinds including a significant euro headwind beyond the forecast we provided in July;

•a multi-week outage of Clear Lake acetic acid production in September to perform maintenance due to an unanticipated mechanical issue;

•a $40 million sequential increase in EM energy costs, which translated to an approximately $15 million headwind in the third quarter due to the one-month lag in our natural gas surcharge;

•China acetic acid pricing that fell from approximately $450 per ton in July to below $400 per ton in the third quarter and cut into the industry cost curve;

•and incremental costs and logistics disruptions due to unprecedented low water levels on the Rhine.

Demand conditions across certain regions deteriorated through the quarter beyond our expectations and beyond the moderation reflected in the lower end of our quarterly guidance. Our heaviest concern today is in Europe, where the demand deterioration has been most pronounced and widespread, impacting primarily paints and coatings, construction, consumer electronics, and industrial end-markets. While August demand was only slightly below the typical summer travel season, we saw further deterioration during September and October. Uncertainty as a result of the conflict in Ukraine and high energy costs in the region are impacting consumer activity and also driving customer destocking in select end-markets.

In Asia, there was an expectation that demand would recover modestly on the easing of COVID restrictions in China. Unfortunately, lockdowns were initiated or reinstated in certain provinces and where lockdowns did ease, our demand did not materially recover. Unlike Europe, the demand softness we are seeing in Asia is concentrated in paints, coatings, and construction applications.

Finally, in the U.S., demand held up quite resiliently across most end-markets and remains stable in our fourth quarter order book for the Acetyl Chain (AC). In EM, our order book is slightly weaker due to softer end-market demand and some destocking activity.

2

Amid this backdrop, our focus remains on that which we can control. As I cover our overarching objectives as an organization, I will also provide clarity on the actions we are taking to align with current demand dynamics, adapt to a full range of potential near-term scenarios, and prepare for recovery.

Let me start with our first objective of differentiated performance in our existing businesses. Engineered Materials (EM) delivered third quarter adjusted EBIT of $206 million and operating EBITDA of $246 million at margins of 22 percent and 26 percent, respectively. Across 2022, EM has delivered the three strongest quarterly adjusted EBIT performances in its history, even when excluding contributions from the Santoprene acquisition. Net sales of $929 million were supported by a 2 percent sequential lift in pricing, representing the seventh consecutive quarter of pricing expansion. Third quarter volume was consistent with last quarter as moderation in the legacy non-auto end markets was offset by strength in our auto volume and contributions from the restructuring of the KEPCO joint venture. I want to congratulate our EM team for delivering results near the upper end of our guidance range despite a series of unanticipated challenges across the third quarter. They successfully navigated a headwind due to the one-month lag on our energy surcharge of approximately $15 million, unfavorable currency impacts, continued cost inflation, and softening demand. They have demonstrated the resiliency of our project pipeline model and commercial agility.

Let me start with our first objective of differentiated performance in our existing businesses. Engineered Materials (EM) delivered third quarter adjusted EBIT of $206 million and operating EBITDA of $246 million at margins of 22 percent and 26 percent, respectively. Across 2022, EM has delivered the three strongest quarterly adjusted EBIT performances in its history, even when excluding contributions from the Santoprene acquisition. Net sales of $929 million were supported by a 2 percent sequential lift in pricing, representing the seventh consecutive quarter of pricing expansion. Third quarter volume was consistent with last quarter as moderation in the legacy non-auto end markets was offset by strength in our auto volume and contributions from the restructuring of the KEPCO joint venture. I want to congratulate our EM team for delivering results near the upper end of our guidance range despite a series of unanticipated challenges across the third quarter. They successfully navigated a headwind due to the one-month lag on our energy surcharge of approximately $15 million, unfavorable currency impacts, continued cost inflation, and softening demand. They have demonstrated the resiliency of our project pipeline model and commercial agility.Whether looking at demand conditions, cost inflation, or currency, Europe remains the primary region of concern for EM. The common theme behind each of these challenges, from our perspective, is the energy uncertainty across the region. As we discuss it internally, we look at the energy uncertainty from three perspectives - (1) our ability to source natural gas to manufacture, (2) our ability to pass along record energy costs, and (3) the indirect impacts of energy uncertainty including customer demand. Let me provide an update on each.

Our production facility in Frankfurt, Germany represents 70 percent of our natural gas exposure in Europe. I am pleased to share that we are nearing completion of the previously mentioned capital project

3

to enable us to operate Frankfurt on fuel oil, as a contingency, in the event natural gas is unavailable. Our teams have also secured the necessary permits to make that energy transition, if necessary.

Our natural gas surcharge continues to be a very effective mechanism to pass along elevated energy costs. During the quarter, we did see some initial demand destruction due to the magnitude and affordability of the surcharge in a challenging demand environment. However, this lost volume represented less than 5 percent of our global demand for POM. Of the EM global portfolio, POM comprises about a third of our volume prior to the M&M acquisition.

Finally, we are closely monitoring the impacts of energy uncertainty on our customers' ability to operate and demand for their products. Our focus here is on that which we can control - aligning our production and cost structure to the realities of European demand. Our Frankfurt, Germany facility is currently the highest-cost POM production in our global network, which consists of 4 wholly-owned or JV POM units. As a result, we reduced operating rates of Frankfurt POM in the third quarter to align with our customers' needs and to avoid building higher-cost inventory. We are also pulling forward a scheduled Frankfurt POM turnaround from 2023 into the fourth quarter of 2022 to be positioned to capture incremental value when demand recovers.

The value of EM's broad and diversified portfolio was reflected in strong sequential growth in medical and automotive. Our medical team captured double-digit sequential volume growth in our medical implants business, which is tied to elective procedures. I am pleased to share that our volumes into medical implants now exceed our pre-COVID run-rate and we anticipate these volumes will be sustained going into 2023.

Our legacy global auto business also showed strong volume growth, driven by sequential performance in each of the three regions that was consistent with or exceeded the growth in auto build rates. Our sequential auto growth in North America and Europe each outpaced the change in industry build rates. We continued to deliver our strongest regional growth in Asia, with sequential volume growth of over 20 percent, excluding any additional KEPCO volume sold there. Our growth in Asia was consistent with sequential increases in industry build rates despite meaningful pre-buying that occurred in the second quarter. We continue to drive meaningful penetration in the electric vehicle market as a result of our project pipeline model as well as the investments we made in 2021 to expand our GUR facility in Bishop, Texas and further localize EM capabilities in Asia.

Looking to the fourth quarter, we expect to see high-single digit volume declines in the legacy EM business off of the previous quarter due primarily to seasonality which traditionally amounts to about 5

4

percent of total volume. Beyond seasonality, we anticipate that any further modest sequential deterioration in demand across non-auto end-markets will be largely offset by the final tranche of KEPCO business that will transition to EM in the fourth quarter. With these demand conditions and sequentially lower affiliate earnings of $25 to $30 million, largely driven by Ibn Sina, we anticipate EM fourth quarter adjusted EBIT of $150 to $170 million. This estimate is also inclusive of the currently expected impact of the M&M acquisition in November and December.

The Acetyl Chain (AC) generated third quarter adjusted EBIT of $322 million and operating EBITDA of $365 million, the second-highest third quarter performance in our history. The business continued to show differentiated margin performance by delivering third quarter operating EBITDA margin of 29 percent, consistent with our previous 5-year average. These results were delivered despite a sequential volume decline of 4 percent, challenging pricing conditions in Asia due to supply and demand dynamics, and a major unanticipated outage at Clear Lake. I want to commend our AC team for the remarkable results in a difficult macro environment. Though some of our products might be considered commodity in application, our operating model and corresponding results continue to be differentiated.

In September, our teams executed a multi-week, unplanned shutdown of our Clear Lake acetic acid plant to perform maintenance on a mechanical issue. The timing of the outage was unfortunate as it limited our ability to leverage our low-cost U.S. natural gas feedstock across the Western Hemisphere for acetic acid to downstream derivatives. Across the third and fourth quarters, we estimate the outage will ultimately increase our total cost to supply customers by $15 million due to suboptimal production, sourcing, and logistics costs. Due to a significant reduction in demand as we progressed through the quarter, the Clear Lake outage did not result in any material loss of sales volume.

Europe and China demand deteriorated significantly for AC as we progressed through the third quarter. In China, demand into paints, coatings, and construction applications was very poor due, in part, to the impact of continued COVID lockdowns. Other AC applications including adhesives, paper, packaging, and food and beverage showed far more stability in China. In Europe, the demand deterioration was most acute in paints, coatings, and construction, but also spread to other application areas due to declining consumer activity as the quarter progressed. Additionally, for the first time since the initial wave of COVID, we saw intentional customer destocking due to weaker demand, continued moderation in acetyls pricing, and greater supply availability globally. These third quarter demand dynamics resulted in sequential volume and pricing headwinds of 4 percent and 7 percent, respectively.

Approximately one-third of our AC volume goes into paints, coatings and construction applications, with increased exposure as we move downstream in the product chain. In emulsions, where we had been

5

maximizing volume to drive second quarter profitability, we sold approximately 15 percent fewer tons globally in the third quarter. In China, that sequential decline in emulsions volume soared to approximately 45 percent and was reflective of a construction industry that was effectively at a standstill. We believe this pause in construction activity is both temporary and unsustainable and we are closely monitoring the governmental response in China in terms of future lockdown policy as well as potential stimulus.

Softer demand and stable industry supply, particularly in China, led to a deterioration in average quarterly pricing for acetic acid and VAM in China that sequentially fell by approximately 30 percent. For the first time since 2020, China acetic acid pricing fell below $400 per ton within the third quarter, despite a China cost curve that is meaningfully higher than it was in 2020.

Our teams responded to these third quarter challenges with decisive actions to keep our global production network aligned with the needs of the market in real time. We immediately reduced our operating rates across China and Singapore to 50 to 70 percent rates across most production units. Some units manufacturing downstream products were curtailed more aggressively to as low as 30 percent operating rates. In Frankfurt, Germany, the team completed a scheduled VAM turnaround in the third quarter and made the decision to keep that production unit down following the outage. Though profitable, the Frankfurt VAM unit is currently the highest-cost of our five VAM plants across the globe. With softer demand, we are able to fully meet the current European demand outlook more cost effectively by relying on our global supply chain. At this time Frankfurt VAM remains idle and we will remain agile in monitoring and aligning our production with European demand conditions. The differentiated earnings and margin performance AC delivered this quarter is a testament to the teams' unique ability to respond nimbly to rapidly changing demand and industry dynamics.

Based on the current order book and dynamics in certain regions and segments that have not improved from September, we anticipate sub-foundational conditions across the entirety of the fourth quarter. Both demand softness in Asia and Europe as well as customer destocking are expected to persist to at least year-end. While Asia acetic acid pricing at the end of the third quarter was at a level that we believe is unsustainably low, in the fourth quarter we anticipate it may approach levels more representative of the cost curve. However, we do anticipate moderation in VAM and downstream products particularly in the Western Hemisphere. Based on continued pricing declines and fourth quarter volume that will be sequentially lower by another few percent, we anticipate AC adjusted EBIT of $200 to $225 million for the fourth quarter.

6

Acetate Tow (AT) delivered third quarter adjusted EBIT of $27 million and operating EBITDA of $37 million with the sequential drop largely driven by reduced affiliate dividends. The business lifted sequential volume and pricing to help offset continued cost inflation. In the fourth quarter, we anticipate AT adjusted EBIT approximately in line with the third quarter.

I am pleased to share that we are progressing well with the previously announced and ongoing AT strategic overhaul to manage acetate flake and tow as derivatives of acetic acid. We will continue to implement greater flexibility to create value across our sourcing, production, and commercial operations that will enhance our profitability and better protect our margins amid future variability in costs. While the planning for next year is not complete, we anticipate that these actions will improve the profitability of our acetate flake and tow products in 2023. As we continue to progress in integrating the acetate flake and tow products into the broader acetyl chain, we expect that the financial contribution from these products will be reported as part of the AC reporting segment beginning with our fourth quarter 2022 results.

Finally, we expect that net expenses in Other Activities will increase sequentially in the fourth quarter, driven primarily by the timing of expenses, and will total close to $200 million of net expense for 2022.

To summarize our business outlooks for the fourth quarter, we will continue to take decisive action to maximize our earnings generation amid continued soft demand in Europe and Asia, continued destocking, and winter seasonality. We expect to deliver fourth quarter adjusted earnings of $1.50 to $2.00 per share, inclusive of the currently expected impact of the M&M acquisition in November and December.

Let me transition to our second objective of integrating and synergizing our acquisitions. We remain excited about the value creation opportunities represented by the M&M acquisition that we have been discussing with you since we announced it in February. Now that the M&M acquisition has closed, we are eager to transition to the next phase of long-term value creation. I thank and congratulate the many teams who worked so diligently to make a November 1 close possible.

Let me transition to our second objective of integrating and synergizing our acquisitions. We remain excited about the value creation opportunities represented by the M&M acquisition that we have been discussing with you since we announced it in February. Now that the M&M acquisition has closed, we are eager to transition to the next phase of long-term value creation. I thank and congratulate the many teams who worked so diligently to make a November 1 close possible.•Pre-Integration: The pre-integration planning done by our team has been significant. While the work to complete the integration into Celanese's business is ongoing, I am pleased by the early signs of success we are seeing throughout our first week.

•Regulatory Approval: As we anticipated at signing, we took preemptive actions to support the regulatory approval process by offering and executing a divestiture remedy. In August we signed an agreement to divest our production facility at Ferrara Donegani, Italy along with our global TPC

7

and polyester hot-melt businesses. That divestiture represented an immaterial portion of EM adjusted EBIT of a few million dollars in 2021.

•Financing: Our finance teams successfully secured over $11 billion in financing via a series of transactions in a very challenging debt market. We have taken purposeful actions to optimize the debt structure and costs and we will continue to take appropriate action to further hone them going forward.

The focus of our work immediately transitions from preparing for and completing the closing to delivering value by integrating and synergizing M&M. We have teams of functional experts, both Celanese employees and external advisors, who are wholly dedicated to this work.

We are starting from a more challenging place than we anticipated at signing, driven by unexpected underperformance of M&M, higher than anticipated borrowing costs, and a challenging demand backdrop in Europe and Asia.

Between closing and the end of 2022, we anticipate that the acquired business will contribute $50 to $60 million in EBITDA to EM, which we included in our fourth quarter guidance. Even when accounting for the impact of normal year-end seasonality, this contribution, on an annualized run-rate, is well below the M&M 2022 forecast at the time of the transaction announcement and our own expectations.

Having closed the acquisition, we are now quickly assessing the challenges to M&M's performance with the help of our new colleagues. We are rapidly prioritizing our actions to address those challenges. While we have only owned the business for three days, let me share some of our very early observations from our post-closing review to date:

•On an EBITDA basis, the M&M business is forecasting a year over year foreign currency headwind of over $20 million across November and December. We will work to optimize our commercial practices to seek to better address our sales currency exposures in future periods. As a result of the higher than anticipated M&M currency exposure, we will assess converting more of our U.S. dollar debt into lower rate currencies, such as the euro, yen, and yuan to lower our blended borrowing rate and align our underlying business currency exposure to our debt mix.

•We are immediately cross-selling the combined product portfolio, particularly to customers where there has been little overlap. In particulare, we are deploying legacy EM commercial teams to cross-sell nylon to help mitigate volume softness in the M&M portfolio.

8

•Amid a soft demand backdrop, M&M has been challenged by purchasing requirements for certain raw materials to polymerize nylon. As EM is a large buyer of nylon polymer, we plan to immediately exercise our sourcing flexibility and utilize excess nylon polymerization capacity of M&M to help alleviate this pressure. Additionally, raw material sourcing agreements for M&M have and will be renegotiated for 2023 with incremental flexibility.

•For certain products, the M&M business has not fully offset cost inflation since 2021. It is clear that pricing needs to be adjusted to offset higher costs. We are quickly quantifying the appropriate price increases by region and product and expect to begin implementing those during the fourth quarter.

•The M&M business has built excess finished goods inventory over the course of 2022, due in part to sourcing commitments, lower demand, and production levels that remain too high. As a result, we expect that the November and December EBITDA contributions will be burdened by inventory that reflects higher cost dynamics from earlier in the year. Much like our recent actions in legacy EM, we intend to closely manage inventory and production levels so that pricing and cost dynamics hitting the income statement are both more contemporary.

We expect that it will take time for us to realize these improvements in the underlying M&M business performance and we will give detail on the specific actions we are taking in the coming months. As I said earlier, we remain confident in the long-term value creation opportunity that the M&M acquisition brings to Celanese and that the talented women and men of M&M will embrace the collaboration, empowerment, and accountability that we strive to foster at Celanese.

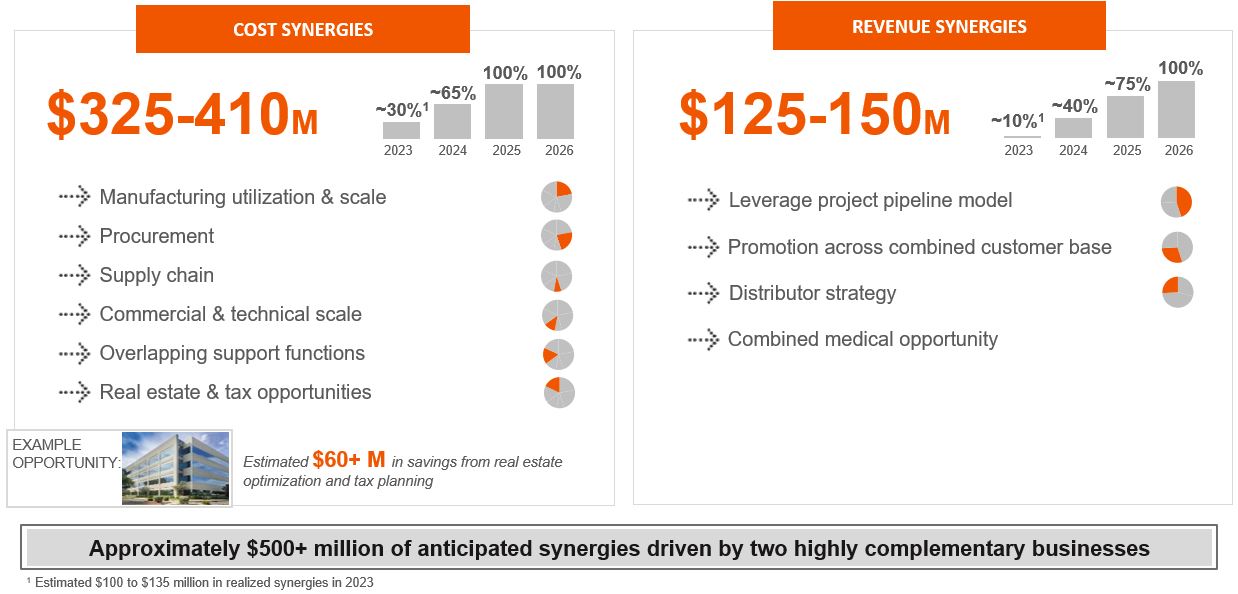

Our synergy efforts will be additive to improvement in underlying M&M performance in 2023. Over the last several months, we have had teams working to further refine and detail our M&M synergy plan. We now expect over $500 million of run-rate cost and revenue synergies, an increase of approximately $50 million versus the estimate we provided when we announced the acquisition in February. Our teams have identified entirely new synergy opportunities, including tax synergies. Our teams have also worked to accelerate the timing of synergies and now anticipate between $100 and $135 million in synergies across 2023, an increase of up to approximately $50 million versus prior year one estimates.

9

Figure 1: Substantial Synergy Opportunity

I am pushing our teams to achieve a neutral adjusted earnings per share impact from the M&M transaction in 2023. In order to achieve this, the base M&M business will need to deliver approximately $800 million in 2023 EBITDA as well as expected year one synergies. Let me remind you that the M&M EBITDA contribution to adjusted earnings per share will be burdened by $550 to $600 million of 2023 interest on deal-related debt and a preliminary estimate of approximately $350 million of forecasted depreciation and amortization (inclusive of transaction amortization).

In any scenario, the free cash flow (levered) contribution from the M&M acquisition will exceed its earnings contribution. Our work over recent months to enhance the M&M synergy opportunity and refine cash needs for M&M working capital and capital expenditures has supported this objective.

Over the next few years, we will be focused on driving recovery in the base EBITDA performance of M&M, delivering synergies higher than originally estimated, and paying down higher cost debt. As a result of these actions, we expect that the M&M earnings and free cash flow contribution shortfall in 2023 will continue to close as we capture full run-rate synergies.

To summarize my comments today, we are aligned and energized as an organization on those actions which will drive the most shareholder value. Though the current demand uncertainty makes it particularly challenging to offer explicit guidance for next year, let me offer some context on how we are thinking about 2023.

10

While it often appears the market is pricing in a global recession for 2023, we do not yet see broad regional or end-market demand conditions in our order books that warrant such a forecast in our outlook. Though we would describe European demand as recession-like, softness in Asia demand is still fairly concentrated to certain end-markets and Chinese provinces, and the U.S. is holding up well. At this stage, we expect that the first quarter will be the weakest of 2023 due to the combined effect of the underlying demand conditions just described, winter seasonality, and potentially lingering impacts of destocking. As the year progresses, we anticipate modest improvement in demand with warmer weather (construction seasonality and, potentially, post-winter clarity in Europe), completion of the destocking cycle, and anticipated improvement in underlying automotive build rates. The fact that automotive build rates have not materially recovered off of historic lows in 2020 and 2021 presents a significant opportunity for our commercial teams to drive to offset softness in other end-markets going into 2023.

At Investor Day in March of 2021, we provided financial guidance through 2023. Even with the particularly challenging start we expect in 2023, we have line of sight to meeting or exceeding the adjusted earnings per share guidance we provided at that time.

Across Celanese, our employees are hard at work to deliver against our objectives. I sincerely thank them for the ownership and individual dedication they demonstrate to generate value for our customers, communities, and shareholders.

Scott Richardson, Celanese Corporation, Chief Financial Officer

I would like to also thank the many teams who have worked so hard to successfully close the M&M acquisition, deliver differentiated business performance amid a challenging backdrop, and prepare us to execute against our deleveraging plan.

Let me start by highlighting the $11.25 billion in debt issuances we completed leading up to the close of the M&M acquisition, $9.0 billion of which is fixed rate and locked at meaningfully lower rates than we see in the debt markets today:

Let me start by highlighting the $11.25 billion in debt issuances we completed leading up to the close of the M&M acquisition, $9.0 billion of which is fixed rate and locked at meaningfully lower rates than we see in the debt markets today:•the $1.5 billion of delayed draw term loans under the Term Loan Credit Agreement dated March 18, 2022 and which we entirely drew at the time of close;

•the registered offering of $7.5 billion principal amount of U.S. dollar notes priced on July 7, 2022;

11

•the euro cross-currency swap entered on July 7, 2022 to effectively convert $2.5 billion of the U.S. dollar denominated debt into euro-denominated borrowing at prevailing euro interest rates;

•the registered offering of €1.5 billion principal amount of euro notes priced on July 12, 2022;

•an additional $750 million of delayed draw term loans dated September 16, 2022 which we entirely drew at the time of close;

Our teams secured slightly more than $11.0 billion in debt to prepare for possible closing adjustments. The M&M closing cash cost to Celanese was ultimately $11.0 billion and the incremental net debt on the Celanese balance sheet from the acquisition is consistent with our original expectations.

As we transition to executing on our deleveraging plan, our focus is squarely on generating cash, further optimizing our borrowing costs, and strategically retiring our debt balances. Our first action will come in less than two weeks with $500 million in U.S. dollar notes maturing on November 15, 2022. You will see us flex our sources of liquidity between cash and temporary draws on our revolver in the near term, as we centralize excess cash balances into the U.S. for deleveraging as part of normal global cash management.

At the time of closing the M&M acquisition, total debt on the Celanese balance sheet is approximately $15.0 billion. Cash balances at the same time are approximately $1.7 billion. As a result, net debt is approximately $13.3 billion for an estimated level of leverage at closing that is consistent with expectations set with credit agencies at the time we announced the acquisition. Our legacy businesses have delivered incremental EBITDA across 2022 to offset underperformance in the acquired business over the same period.

Looking ahead to 2023, as we work to deliver on the guidance we gave at Investor Day, we would anticipate a corresponding $1.5 billion or more in free cash flow generation, inclusive of contributions from the M&M acquisition. Factored into this estimate are 2023 capital expenditures of approximately $600 million across Celanese (inclusive of M&M) and one-time costs to achieve synergies of $75 million.

With a committed dividend outlay of approximately $300 million in 2023, we expect to have over $1 billion in discretionary cash flow next year, which will be devoted to paying down debt. This level of net debt reduction across 2023 would be consistent with the original deleveraging plan we shared when we announced the acquisition. Any potential divestitures of certain product lines or joint ventures would present incremental opportunity to accelerate our deleveraging plan.

Finally, let me reiterate that we are confident in our ability to pay down debt across 2023 consistent with our deleveraging plan in a wide range of potential macro scenarios. For the most challenging of potential

12

demand backdrops, we have a detailed playbook consisting of discrete actions which are available to us to ensure the resiliency of our debt pay down. We remain fully committed to this objective.

We look forward over the coming quarters to providing updates on the progress of our continued business enhancement, integration of the M&M acquisition, and execution of our deleveraging plan. This concludes our prepared remarks. We look forward to discussing our third quarter results and addressing your questions.

13

Forward-Looking Statements

These prepared comments may contain "forward-looking statements," which include information concerning the Company's plans, objectives, goals, strategies, future revenues or performance, capital expenditures, financing needs and other information that is not historical information. All forward-looking statements are based upon current expectations and beliefs and various assumptions. There can be no assurance that the Company will realize these expectations or that these beliefs will prove correct. There are a number of risks and uncertainties that could cause actual results to differ materially from the results expressed or implied in the forward-looking statements contained in these comments. These risks and uncertainties include, among other things: changes in general economic, business, political and regulatory conditions in the countries or regions in which we operate; volatility or changes in the price and availability of raw materials and energy, particularly changes in the demand for, supply of, and market prices of ethylene, methanol, natural gas, wood pulp and fuel oil and the prices for electricity and other energy sources; the length and depth of product and industry business cycles, particularly in the automotive, electrical, mobility, textiles, medical, electronics and construction industries; the ability to pass increases in raw material prices, logistics costs and other costs on to customers or otherwise improve margins through price increases; the accuracy or inaccuracy of our beliefs and assumptions regarding anticipated benefits of the acquisition (the "M&M Acquisition") by us of the majority of DuPont's Mobility & Materials business (the "M&M Business"), including as a result of the performance of the M&M Business between signing and closing of the M&M Acquisition; the possibility that we will not be able to realize anticipated improvements in the M&M Business's financial performance — including optimizing pricing, currency mix and inventory — or realize the anticipated benefits of the M&M Acquisition, including synergies and growth opportunities, within the anticipated timeframe, or at all, whether as a result of difficulties arising from the operation or integration of the M&M Business or other unanticipated delays, costs, inefficiencies or liabilities; increased commercial, legal or regulatory complexity of entering into, or expanding our exposure to, certain end markets and geographies; risks in the global economy and equity and credit markets and their potential impact on our ability to pay down debt in the future and/or refinance at suitable rates, in a timely manner, or at all; diversion of management's attention from ongoing business operations and opportunities and other disruption caused by the M&M Acquisition and the integration processes and their impact on our existing business and relationships; risks and costs associated with increased leverage from the M&M Acquisition, including increased interest expense and potential reduction of business and strategic flexibility; the ability to maintain plant utilization rates and to implement planned capacity additions and expansions as well as facility turnarounds; the ability to reduce or maintain their current levels of production costs and to improve productivity by implementing technological improvements to existing plants; the ability to identify desirable potential acquisition targets and to complete and integrate acquisition or investment transactions, including regulatory approvals, consistent with the Company's strategy; increased price competition and the introduction of competing products by other companies; market acceptance of our products and technology; compliance and other costs and potential disruption or interruption of production or operations due to accidents, interruptions in sources of raw materials, transportation logistics or supply chain disruptions, cyber security incidents, terrorism or political unrest, public health crises (including, but not limited to, the COVID-19 pandemic); other unforeseen events or delays in construction or operation of facilities, including as a result of geopolitical conditions, the occurrence of acts of war (such as the Russia-Ukraine conflict) or terrorist incidents or as a result of weather or natural disasters or other crises including public health crises; the ability to obtain governmental approvals and to construct facilities on terms and schedules acceptable to the Company; changes in applicable tariffs, duties and trade agreements, tax rates or legislation throughout the world including, but not limited to, adjustments, changes in estimates or interpretations or the resolution of tax examinations or audits that may impact recorded or future tax impacts and potential regulatory and legislative tax developments in the United States and other jurisdictions; changes in the degree of intellectual property and other legal protection afforded to our products or technologies, or the theft of such intellectual property; potential liability for remedial actions and increased costs under existing or future environmental, health and safety regulations, including those relating to climate change; the extent to which resurgences or variants of COVID-19 may adversely impact the economic environment, market demand, our operations, availability and cost of transportation and materials, the labor supply, and pace of economic recovery; potential liability resulting from pending or future claims or litigation, including investigations or enforcement actions, or from changes in the laws, regulations or policies of governments or other governmental activities in the countries in which we operate; changes in currency exchange rates and interest rates; our level of indebtedness, which could diminish our ability to raise additional capital to fund operations or limit our ability to react to changes in the economy or the chemicals industry; tax rates and changes thereto; our ability to obtain regulatory approval for, and satisfy closing conditions to, any transactions described herein that have not closed; and various other factors discussed from time to time in the Company's filings with the Securities and Exchange Commission.

Any forward-looking statement speaks only as of the date on which it is made, and the Company undertakes no obligation to update any forward-looking statements to reflect events or circumstances after the date on which it is made or to reflect the occurrence of anticipated or unanticipated events or circumstances.

Results Unaudited

The results in this document, together with the adjustments made to present the results on a comparable basis, have not been audited and are based on internal financial data furnished to management. Quarterly results should not be taken as an indication of the results of operations to be reported for any subsequent period or for the full fiscal year.

Non-GAAP Financial Measures

These prepared comments, and statements made in connection with these prepared comments, refer to non-GAAP financial measures. For more information on the non-GAAP financial measures used by the Company, including the most directly comparable GAAP financial measure for each non-GAAP financial measure used, including definitions and reconciliations of the differences between such non-GAAP financial measures and the comparable GAAP financial measures, please refer to the Non-US GAAP Financial Measures and Supplemental Information document available on our website, investors.celanese.com, under Financial Information/Financial Document Library.

14