As filed with the Securities and Exchange Commission on January 6, 2011

Registration No. 333-157700

UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D. C. 20549

POST-EFFECTIVE

AMENDMENT NO. 5

TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

THE MONEY TREE INC.

(Exact name of registrant as specified in its charter)

| | | | |

| Georgia | | 6141 | | 58-2171386 |

(State or other jurisdiction of Incorporation of organization) | | (Primary Standard Industrial Classification Code Number) | | (I.R.S. Employer Identification Number) |

114 South Broad Street

Bainbridge, Georgia 39817

(229) 246-6536

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

Bradley D. Bellville

President

114 South Broad Street

Bainbridge, Georgia 39817

(229) 246-6536

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies to:

Michael K. Rafter, Esq.

Baker, Donelson, Bearman,

Caldwell & Berkowitz, PC

Monarch Plaza

Suite 1600

3414 Peachtree Road, NE

Atlanta, Georgia 30326

(404) 577-6000

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this Form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act, check the following box. x

If this Form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this Form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, or a smaller reporting company. See definitions of “large accelerated filer,” “accelerated filer,” and “smaller reporting company” in Rule 12b-2 of the exchange Act. (Check one):

| | |

| Large accelerated filer ¨ | | Accelerated filer ¨ |

| Non-accelerated filer ¨ | | Smaller reporting company x |

(Do not check if a smaller reporting company)

THE MONEY TREE INC.

$35,000,000 Subordinated Demand Notes

We are offering up to $35.0 million in aggregate principal amount of our Subordinated Demand Notes (“Demand Notes”) on a continuous basis. A minimum initial investment of $100 is required. As of December 25, 2010, we had raised a total of $5.8 million in gross offering proceeds from the sale of Demand Notes and had a total of $29.2 million remaining to be sold in this offering.

We will issue the Demand Notes in denominations of at least $1, subject to the initial minimum investment requirement of $100. The Demand Notes shall have no stated maturity and shall be payable or redeemable, in whole or in part, at any time at your option, subject to the subordination provisions. The Demand Notes shall bear interest at a variable rate (compounded daily based upon a 365-day year), which will vary depending upon the daily average balance held by you. When we set interest rates for each range of balances, such rates become effective for and applied to all Demand Notes with a daily average balance within that range, whether existing or newly issued. These interest rates may be the same or different for each range of balances and we may increase or decrease the rate for any range independently of the other ranges without advance notice to you after the date of purchase. We will only pay interest on a Demand Note when you make a demand for payment of principal of the Demand Note.

You may obtain the current interest rates payable on the Demand Notes by calling our executive offices in Bainbridge, Georgia at (877) 468-7878 (toll free) or (229) 248-0990 or by visiting our web site atwww.themoneytreeinc.com. We will file a Rule 424(b)(2) prospectus supplement setting forth the current interest rates with the Securities and Exchange Commission (SEC) upon any change in the interest rates.

We are offering the Demand Notes through our designated selling officer, Jennifer Ard, without an underwriter and on a continuous basis. We do not have to sell any minimum amount of Demand Notes to accept and use the proceeds of this offering. We cannot assure you that all or any portion of the Demand Notes we are offering will be sold. We have not made any arrangement to place any of the proceeds from this offering in an escrow, trust or similar account. Therefore, you will not be entitled to the return of your investment. The Demand Notes are not listed on any securities exchange, and there is no public trading market for the Demand Notes. We have the right to reject any subscription, in whole or in part, for any reason.

We may at our option redeem at any time the Demand Notes (1) upon at least 30 days’ written notice to you, or (2) if the principal balance falls below $100, for a redemption price equal to the principal amount plus any unpaid interest thereon to the date of redemption. Demand Notes shall be payable or redeemable, in whole or in part, at your option at any time, subject to subordination. All payments or redemptions must be made either in person or by mail at our executive offices in Bainbridge, Georgia.

You should read this prospectus and any applicable prospectus supplement carefully before you invest in the Demand Notes. These Demand Notes are our general unsecured obligations and are subordinated in right of payment to all of our present and future senior debt. We expect to incur additional debt in the future, including, without limitation, the Demand Notes offered pursuant to this prospectus.

The Demand Notes are not certificates of deposit or similar obligations guaranteed by any depository institution, and they are not insured by the Federal Deposit Insurance Corporation (FDIC) or any governmental or private insurance fund, or any other entity. We do not contribute funds to a separate account such as a sinking fund to use to repay the Demand Notes.

See “Risk Factors” beginning on page 9 for certain factors you should consider before buying the Demand Notes. These risks include the following:

| | • | | The Demand Notes are risky and speculative investments for suitable investors only. |

| | • | | The opinion of our independent registered accounting firm for the fiscal year ended September 25, 2010, includes an explanatory paragraph that states that we have incurred recurring losses from operations, negative cash flows from operating activities and have a net shareholders’ deficit that raise substantial doubt about our ability to continue as a going concern. Our net loss was $12.1 million and $12.9 million and we incurred negative cash flows from operating activities of $4.4 million and $1.6 million during fiscal years 2010 and 2009, respectively. As of September 25, 2010, we had a shareholders’ deficit of $45.9 million. |

| | • | | The collectability of our finance receivables has been severely and negatively affected by general economic conditions, and we have not been able to recover the full amount of delinquent accounts by resorting to the sale of collateral or receipt of non-filing insurance proceeds. As of September 25, 2010, our finance receivables, net of allowance for credit losses, were $35.4 million, and our total debt outstanding, including accrued interest, was $87.3 million. |

| | • | | If we continue to redeem more debentures and demand notes than we sell in any given period, our liquidity and capital resources will continue to be severely and negatively affected. During the fiscal year ended September 25, 2010, we (1) received gross proceeds of $12.0 million from the sale of debentures and $2.6 million from the sale of demand notes, and (2) paid $14.4 million for redemption of debentures and $2.6 million for redemption of demand notes. |

| | • | | We have restated our consolidated financial statements twice in the past three years, resulting in material financial misstatements and the temporary suspension of our offerings. Our inability to sell debentures and demand notes during these periods has negatively affected our consolidated financial condition, and any future misstatement could further weaken our liquidity and operating results. |

| | • | | If we or our operations suffer from severe negative publicity, we could be faced with significantly greater payment or redemption obligations from holders of the Series B Variable Rate Subordinated Debentures (“Debentures”) and Demand Notes than we have cash available for such payments or redemptions. |

| | • | | We may be unable to meet our debenture and demand note obligations, which could force us to sell off our loan receivables and other operating assets or we might be forced to cease our operations, and you could lose some or all of your investment. |

| | • | | Our decreased sales of Debentures and Demand Notes, along with the increased redemptions of these securities, has resulted in fewer loans being made to customers, which has significantly negatively affected our operations, financial position and liquidity. |

| | • | | If we default in our Debenture or Demand Note payment obligations, the indenture agreements relating to our Debentures and Demand Notes provide that the trustee could accelerate all payments due under the Debentures and Demand Notes, which would further negatively affect our financial position. |

These securities have not been approved or disapproved by the SEC or any state securities commission, and neither the SEC nor any state securities commission has passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this Prospectus is January , 2011.

TABLE OF CONTENTS

i

ii

You should rely only upon the information contained in this prospectus. We have not authorized anyone to provide you with information different from that contained in this prospectus. We are offering to sell the Demand Notes only in jurisdictions where offers and sales are permitted.

iii

QUESTIONS AND ANSWERS

Below we have provided some of the more frequently asked questions and answers relating to the offering of the Demand Notes. Please see the “Prospectus Summary” and the remainder of this prospectus for more information about the offering of the Demand Notes.

| Q: | Who is The Money Tree Inc. (the Company)? |

| A: | We are a consumer finance company operating since our inception in 1987 through our branch offices in 91 locations throughout Georgia, Alabama, Louisiana and Florida. |

| Q: | What are your primary business activities? |

| A: | We primarily make, purchase and service direct consumer loans, consumer sales finance contracts and motor vehicle installment sales contracts. Direct consumer loans are direct loans to customers for general use, which are collateralized by existing automobiles or consumer goods, or are unsecured. Consumer sales finance contracts consist of retail installment sales contracts for purchases of specific consumer goods by customers either from one of our branch locations or from a retail store and are collateralized by such consumer goods. Motor vehicle installment sales contracts are initiated by us or purchased from automobile dealers subject to our credit approval. We originate direct consumer loans and consumer sales finance contracts primarily in our branch office locations. As of September 25, 2010, direct consumer loans comprised 29.8%, motor vehicle installment sales contracts comprised 45.6%, and consumer sales finance contracts comprised 24.6% of the gross amount of our outstanding loans and contracts. Most of our customers have “subprime” credit ratings and are considered higher than average credit risks. We sell retail merchandise, principally furniture, appliances and electronics, at certain of our branch office locations and operate two used automobile dealerships in the State of Georgia. We also offer, among other products and services, credit and non-credit insurance products, prepaid phone services and automobile club memberships to our loan customers. Insurance products include credit life, credit accident and sickness, and collateral protection, which are issued by a non-affiliated insurance company. |

| Q: | What kind of offering is this? |

| A: | We are offering up to $35.0 million of Demand Notes to residents of the State of Georgia. As of December 25, 2010, we had raised a total of $5.8 million in gross offering proceeds from the sale of Demand Notes and had a total of $29.2 million remaining to be sold in this offering. |

| A: | A Demand Note is our promise to repay your principal investment on demand by you plus interest earned to that date. The Demand Notes are our general unsecured obligations and are subordinated in right of payment to all of our present and future senior debt. Subordinated means that if we are unable to pay our debts as they come due, all of the senior debt would be paid first, before any payment would be made on the Demand Notes. As of September 25, 2010, we had the following accrued interest payable and outstanding debt that ranks equal with or senior to the Demand Notes: |

| | | | |

Accrued interest payable | | $ | 12,733,503 | |

Senior debt | | | 164,625 | |

Debentures | | | 71,226,698 | |

Demand Notes | | | 3,174,913 | |

| | | | |

Total | | $ | 87,299,739 | |

| | | | |

We expect to incur additional debt in the future, including, without limitation, the Demand Notes offered pursuant to this prospectus.

| Q: | Is my investment in the Demand Notes insured? |

| A: | No.The Demand Notes are not certificates of deposit or similar obligations or guaranteed by any depository institution, and they are not insured by the FDIC or any governmental or private insurance fund, or any other entity. They are backed only by the faith and credit of our company and our operations. |

| Q: | How is the interest rate determined? |

| A: | The interest rate offered on the Demand Notes varies depending on the average daily balances in the following ranges: $1.00 to $9,999.99; $10,000.00 to $49,999.99; $50,000.00 to $99,999.99; and $100,000.00 and over. When we establish an interest rate for each range of balances, it becomes effective for and applied to all Demand Notes with a daily balance within that range, whether existing or newly issued. If your average daily balance changes at any time during which you hold Demand Notes, your interest rate will change accordingly. |

| Q: | How is interest calculated and paid to me? |

| A: | The interest rate is a variable rate, and interest is compounded daily (based on a 365-day year). The interest rate may be the same or different for each range of balances, and we may increase or decrease the rate for any range independently of the others without notice to you after the date of purchase. In other words, we can change the interest rate payable to you at any time in our discretion. Interest is only payable when you make a demand for payment of principal of the Demand Note. |

| Q: | Do the Demand Notes have a maturity date? |

| A: | No. A Demand Note is payable to you on your demand. |

| Q: | When may I redeem the Demand Note? |

| A: | Subject to the subordination provisions, you may redeem or demand payment on the Demand Note at any time. In such event, we will pay you the outstanding principal balance plus interest earned to the date of redemption. |

2

| Q: | Can you force me to redeem my Demand Note? |

| A: | Yes, we may call your Demand Note for redemption at any time upon 30 to 60 days’ notice. We may, in our sole discretion, redeem any Demand Note in full if the principal balance falls below $100 at any time. Any such redemptions by us will be for a price equal to the principal amount plus accrued interest to the date of redemption. |

| Q: | How are the Demand Notes sold? |

| A: | The Demand Notes are offered by our designated selling officer without an underwriter. We intend to market the offering primarily by placing advertisements in local newspapers, purchasing roadway sign advertisements and placing signs in our branch office locations in states in which we have properly registered the offering or qualified for an exemption from registration. |

| Q: | What will you do with the proceeds raised from this offering? |

| A: | If all the Demand Notes offered by this prospectus are sold, we expect to receive approximately $34,385,000 in net proceeds after deducting all costs and expenses associated with this offering. We intend to use substantially all of the net cash proceeds from this offering in the following order of priority: |

| | • | | to redeem (1) debentures and demand notes of our subsidiary, The Money Tree of Georgia Inc. and (2) the Series A Variable Rate Subordinated Debentures, Debentures and Demand Notes issued by us; |

| | • | | to make interest payments to holders of all of our debentures and demand notes; |

| | • | | to the extent we have remaining net proceeds and adequate cash on hand, to fund the following activities: |

| | ¡ | | for working capital and other general corporate purposes; |

| | ¡ | | to make additional consumer loans; |

| | ¡ | | to fund the purchase of inventory of used cars; |

| | ¡ | | to open new branch office locations; and |

| | ¡ | | to acquire loan receivables from competitors. |

| Q: | What are some of the significant risks of my investment in the Demand Notes? |

| A: | You should carefully read and consider all risk factors beginning on page 9 of this prospectus prior to investing. Below is a summary of some of the significant risks of an investment in the Demand Notes: |

3

| | • | | the Demand Notes are risky and speculative investments for suitable investors only; |

| | • | | the opinion of our independent registered accounting firm for the fiscal year ended September 25, 2010, includes an explanatory paragraph that states that we have incurred recurring losses from operations, negative cash flows from operating activities and have a net shareholders’ deficit that raise substantial doubt about our ability to continue as a going concern; |

| | • | | we suffered significant losses during fiscal years 2007 through 2010 and we anticipate such losses will likely continue in 2011; |

| | • | | we have suffered significant credit losses due to continued weakening economic conditions, and there is no guarantee such credit losses will not continue during this downturn in the economy or that our operations and profitability will not continue to be negatively affected; |

| | • | | if we continue to redeem more debentures and demand notes than we sell in any given period, our liquidity and capital needs will continue to be severely and negatively affected; |

| | • | | we may have insufficient cash to meet our debt obligations; |

| | • | | if we default in our Debenture or Demand Note payment obligations, the indenture agreements relating to our Debentures and Demand Notes provide that the trustee could accelerate all payments due under the Debentures and Demand Notes, which would further negatively affect our financial position; |

| | • | | if we are unable to meet our debenture and demand note redemption obligations, and we are unable to obtain additional financing or other sources of capital, we may be forced to sell off our loan receivables and other operating assets or we might be forced to cease our operations, and you could lose some or all of your investment; |

| | • | | our decreased sales of Debentures and Demand Notes, along with the increased redemptions of these securities, has resulted in fewer loans being made to customers, which has significantly negatively affected our operations, financial position and liquidity; |

| | • | | our internal controls over financial reporting have not been effective in preventing or detecting misstatements in our consolidated financial statements, and if we fail to detect material misstatements in our consolidated financial statements, our consolidated financial condition and operating results could be severely and negatively affected; |

| | • | | if we find further errors in our previously issued consolidated financial statements, we may again need to suspend our offerings of demand notes and debentures until such time as the financial misstatements can be corrected, and if correcting those errors requires an extended period of time, our ability to meet our financial obligations could be severely and negatively affected; |

4

| | • | | the collectability of our finance receivables has been severely and negatively affected by general economic conditions and we have not been able to recover the full amount of delinquent accounts by resorting to sale of collateral or receipt of non-filing insurance proceeds; |

| | • | | our typical customer base has “subprime” credit ratings and higher than average credit risks which may result in increased loan defaults; |

| | • | | if we or our operations suffer from severe negative publicity, we could be faced with significantly greater payment or redemption obligations from holders of the Debentures and Demand Notes than we have cash available for such payments or redemptions; |

| | • | | we can provide no assurance that any Demand Notes will be sold or that we will raise sufficient proceeds to carry out our business plans; |

| | • | | our Demand Notes are not insured or guaranteed by any third party, so you are dependent upon our ability to manage our business and generate adequate cash flows; |

| | • | | payment on the Demand Notes is subordinate to the payment of all outstanding present and future senior debt, and the indenture does not limit the amount of senior debt we may incur; |

| | • | | payment of interest and principal on the Demand Notes is effectively subordinate to the payment of the secured and unsecured creditors of our subsidiaries, including holders of debentures and demand notes issued by The Money Tree of Georgia Inc.; |

| | • | | our significant shareholders’ deficit balance (and balance sheet insolvency) may limit our ability to obtain future financing, which could have a negative effect on our operations and our liquidity; |

| | • | | our lack of a significant line of credit could affect our liquidity; and |

| | • | | we are controlled by Bradley D. Bellville and do not have any independent board members overseeing our operations. |

| Q: | Who may I contact for more information? |

| A: | While our branch office personnel would be happy to provide you with a prospectus and may accept your investment check and documentation, they are not allowed to answer any substantive questions about your investment. If you have questions about the offering of the Demand Notes or need additional information, please call our executive office at (877) 468-7878 (toll free) or (229) 248-0990 (in Georgia). |

5

PROSPECTUS SUMMARY

This summary highlights selected information, most of which was not otherwise addressed in the “Questions and Answers” section of this prospectus. For more information about us, you should carefully read the entire prospectus, including the section entitled “Risk Factors,” the consolidated financial statements and other consolidated financial data, any related prospectus supplement and the documents we have referred you to in “Where You Can Find More Information.”

Our Company

We were incorporated in Georgia in 1987, and our principal corporate office is located at 114 South Broad Street, Bainbridge, Georgia 39817. Our general telephone number is (229) 246-6536. Information about us can be found atwww.themoneytreeinc.com. The information contained on this website is not part of this prospectus.

The Offering

| | |

| Securities Offered | | We are offering up to $35.0 million in aggregate principal amount of our Demand Notes. As of December 25, 2010, we had raised a total of $5.8 million in gross offering proceeds from the sale of Demand Notes and had a total of $29.2 million remaining to be sold in this offering. The Demand Notes are governed by an indenture between us and U.S. Bank National Association, as trustee. The Demand Notes do not have the benefit of a sinking fund. See “Description of Demand Notes.” |

| |

| Denominations | | Increments of at least $1. |

| |

| Minimum Investment | | A minimum initial investment of $100 is required. |

| |

| Form of Investment | | Investments in Demand Notes may be made by check or by automatic debit of your bank account. |

| |

| Interest Rate | | Variable interest rate, compounded daily based on a 365-day year, which will vary depending upon the average daily balances in the following ranges: $1.00 to $9,999.99; $10,000.00 to $49,999.99; $50,000.00 to $99,999.99; and $100,000.00 and over. |

| |

| Payment of Interest | | Interest is payable only when you make a demand for payment of principal of the Demand Note. |

| |

| No Maturity | | Demand Notes shall have no stated maturity. |

| |

| Payment/Redemption | | Demand Notes shall be payable or redeemable, in whole or in part, at your option at any time, subject to subordination. All payments or redemptions must be made either in person or by mail at our executive offices in Bainbridge, Georgia. |

6

| | |

| Redemption by Us | | We may redeem the Demand Notes at any time upon 30 to 60 days’ written notice to you for a price equal to principal plus interest accrued to the date of redemption. |

| |

| Redemption if Balance Falls Below $100 | | We may, at our sole option, redeem any Demand Note in full, if the principal balance of such Demand Note falls below $100 at any time, for a price equal to principal plus interest accrued to the date of redemption. |

| |

| Subordination | | Demand Notes are subordinated, in all rights to payment and in all other respects, to all of our debt except for debt that by its terms expressly provides that such debt is not senior in right to payment of the Demand Notes. Senior debt includes, without limitation, all of our bank and finance company debt and any line of credit we may obtain in the future. This means that if we are unable to pay our debts when due, all of the senior debt would be paid first, before any payment would be made on the Demand Notes. |

| |

| Event of Default | | Under the indenture, an event of default is generally defined as (1) a default in the payment of principal and interest on the Demand Notes that is not cured for 30 days, (2) our becoming subject to certain events of bankruptcy or insolvency, or (3) our failure to comply with provisions of the Demand Notes or the indenture if such failure is not cured or waived within 60 days after receipt of a specific notice. |

| |

| Transfer Restrictions | | Transfer of a Demand Note is effective only upon the receipt of valid transfer instructions by the registrar from the Demand Note holder of record. |

| |

| Trustee | | U.S. Bank National Association, a national banking association. |

| |

| Risk Factors | | See “Risk Factors” beginning on page 9 and other information included in this prospectus and any prospectus supplement for a discussion of factors you should carefully consider before investing in the Demand Notes. |

Summary Consolidated Financial Data

The following table summarizes certain financial data of our business. You should read this summary together with “Selected Consolidated Financial Data,” “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited consolidated financial statements and related notes included elsewhere in this prospectus. The summary consolidated balance sheet data, as of September 25, 2010 and 2009, and the summary consolidated statement of operations data, for the fiscal years ended September 25, 2010 and 2009, have been derived from our audited consolidated financial statements and related notes included in this prospectus. The summary consolidated balance sheet data, as of September 25, 2008, 2007, and 2006, and the summary consolidated statement of operations data, for the fiscal year ended September 25, 2008, 2007 and 2006, have been derived from our audited financial statements that are not included in this prospectus.

7

| | | | | | | | | | | | | | | | | | | | |

| | | As of, and for, the Fiscal Year Ended September 25, | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Net interest and fee income (loss)(1) | | $ | (851 | ) | | $ | (2,784 | ) | | $ | (2,038 | ) | | $ | 3,515 | | | $ | 7,980 | |

Insurance commissions | | | 5,032 | | | | 8,354 | | | | 9,615 | | | | 10,120 | | | | 11,263 | |

Delinquency fees | | | 1,326 | | | | 1,561 | | | | 1,720 | | | | 1,776 | | | | 1,565 | |

Other income(2) | | | 1,772 | | | | 2,132 | | | | 2,491 | | | | 2,698 | | | | 2,729 | |

| | | | | | | | | | | | | | | | | | | | |

Net revenues before retail sales | | | 7,279 | | | | 9,263 | | | | 11,788 | | | | 18,109 | | | | 23,537 | |

| | | | | | | | | | | | | | | | | | | | |

Gross margin on retail sales | | | 3,579 | | | | 5,653 | | | | 6,033 | | | | 6,832 | | | | 6,361 | |

Net revenues | | | 10,858 | | | | 14,916 | | | | 17,821 | | | | 24,941 | | | | 29,898 | |

Operating expenses | | | (22,806 | ) | | | (28,278 | ) | | | (28,469 | ) | | | (27,604 | ) | | | (29,151 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net operating income (loss) | | | (11,948 | ) | | | (13,362 | ) | | | (10,468 | ) | | | (2,663 | ) | | | 747 | |

Other non-operating income | | | - | | | | - | | | | - | | | | - | | | | 151 | |

Loss on sale of property and equipment | | | (187 | ) | | | (11 | ) | | | (21 | ) | | | (19 | ) | | | (75 | ) |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) before income tax benefit (expense) | | | (12,135 | ) | | | (13,373 | ) | | | (10,669 | ) | | | (2,682 | ) | | | 823 | |

Income tax benefit (expense) | | | - | | | | 438 | | | | 682 | | | | (1,109 | ) | | | (274 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | $ | (12,135 | ) | | $ | (12,935 | ) | | $ | (9,987 | ) | | $ | (3,791 | ) | | $ | 549 | |

| | | | | | | | | | | | | | | | | | | | |

Ratio of earnings to fixed charges(3) | | | (4 | ) | | | (4 | ) | | | (4 | ) | | | (4 | ) | | | 1.10 | |

Cash and cash equivalents | | $ | 2,115 | | | $ | 2,922 | | | $ | 12,541 | | | $ | 17,854 | | | $ | 12,920 | |

Finance receivables, net(5) | | | 35,448 | | | | 47,356 | | | | 59,787 | | | | 67,126 | | | | 70,903 | |

Other receivables | | | 493 | | | | 717 | | | | 957 | | | | 861 | | | | 1,013 | |

Inventory | | | 1,202 | | | | 2,202 | | | | 3,167 | | | | 3,057 | | | | 2,195 | |

Property and equipment, net | | | 3,369 | | | | 4,227 | | | | 4,906 | | | | 4,220 | | | | 4,581 | |

Total assets | | | 43,226 | | | | 59,254 | | | | 83,857 | | | | 95,862 | | | | 95,732 | |

Senior debt | | | 165 | | | | 327 | | | | 695 | | | | 512 | | | | 669 | |

Subordinated debt | | | - | | | | - | | | | - | | | | - | | | | 970 | |

Debentures(6) | | | 71,227 | | | | 73,603 | | | | 82,209 | | | | 81,861 | | | | 77,910 | |

Demand notes(6) | | | 3,175 | | | | 3,147 | | | | 3,658 | | | | 5,991 | | | | 8,137 | |

Shareholders’ deficit | | $ | (45,909 | ) | | $ | (33,774 | ) | | $ | (20,839 | ) | | $ | (10,852 | ) | | $ | (7,060 | ) |

| (1) | Net of interest expense and provision for credit losses. |

| (2) | Includes commissions from motor club memberships received from Interstate Motor Club, Inc., an affiliated entity, and income from income tax return preparation services received from Cash Check Inc. of Ga., a previously affiliated entity that was dissolved in December 2007. |

| (3) | The ratio of earnings to fixed charges represents the number of times fixed charges are covered by earnings. For purposes of this ratio, “earnings” is determined by adding pre-tax income to “fixed charges,” which consists of interest on all indebtedness and an interest factor attributable to rent expense. |

| (4) | Calculation results in a deficiency in the ratio (i.e., less than one-to-one coverage). The deficiency in earnings to cover fixed charges was $12,134,947, $13,372,623; $10,669,231; and $2,682,314 for the years ended September 25, 2010, 2009, 2008, and 2007, respectively. |

| (5) | Net of unearned insurance commissions, unearned finance charges and unearned discounts. |

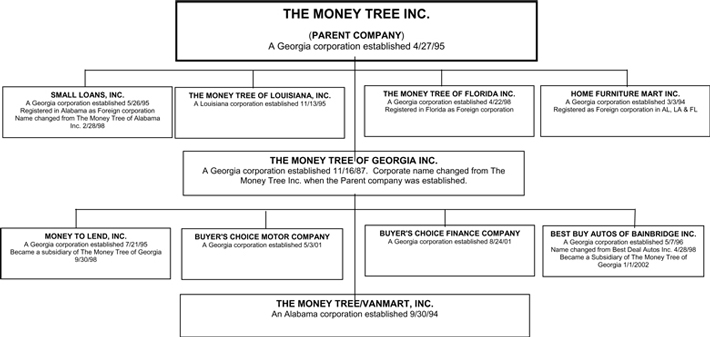

| (6) | Issued, in part, by our subsidiary, The Money Tree of Georgia Inc. See Note 7 to our consolidated audited financial statements for the year ended September 25, 2010. |

8

RISK FACTORS

Our operations and your investment in the Demand Notes are subject to a number of risks. You should carefully read and consider these risks, together with all other information in this prospectus, before you decide to buy the Demand Notes. If any of the following risks actually occur, our business, consolidated financial condition or operating results and our ability to repay the Demand Notes could be materially adversely affected.

Risks Related to Our Offering

The Demand Notes are risky and speculative investments for suitable investors only.

You should be aware that the Demand Notes are risky and speculative investments suitable only for investors of adequate financial means. If you cannot afford to lose your entire investment, you should not invest in the Demand Notes. Potential investors are required to complete a purchaser suitability questionnaire to assist our executive officers in determining whether an investment in the Demand Notes is a suitable investment, and such executive officers have the right to reject any potential investor. If we accept an investment, you should not assume that the Demand Notes are a suitable and appropriate investment for you.

If we continue to redeem more debentures and demand notes than we sell in any given period, our liquidity and capital needs will continue to be severely and negatively affected.

We are substantially reliant upon the net offering proceeds we receive from the sale of our debentures and demand notes to meet our liquidity needs. We use these net offering proceeds to fund redemption obligations, make interest payments and to fund other working capital. Since 2005, we or our subsidiary, The Money Tree of Georgia Inc., have sold approximately $69.0 million of debentures and $22.6 million of demand notes. For the fiscal year ended September 25, 2010, we redeemed $14.4 million in debentures and $2.6 million in demand notes, while only receiving $12.0 million and $2.6 million from the sale of new debentures and demand notes, respectively. If we continue to redeem more debentures and demand notes than we sell in any given period, our liquidity and capital needs will be severely and negatively affected.

We may have insufficient cash to meet our debt obligations.

Our cash and cash equivalents as of September 25, 2010 was $2.1 million. Furthermore, our ratio of earnings to fixed charges is less than one, and has been negative since fiscal year 2006, indicating that we have insufficient funds from operations to meet our fixed obligations. Our net loss before taxes, which equates to the deficiency in earnings to cover fixed charges, was $12.1 million for the fiscal year ended September 25, 2010. In addition to our fixed obligations and elective redemptions of our demand notes and debentures, based on the scheduled maturity dates (i.e., debentures which have reached their extended eight-year maturity dates) of the debentures issued by our subsidiary, The Money Tree of Georgia Inc., during calendar year 2011 redemptions of these debentures will total $8.5 million. If we are unable to raise sufficient funds through the sale of debentures and demand notes, and we are unable to obtain additional financing or other sources of capital, we may not have adequate cash on hand to meet all of our financial obligations.

If we default in our Debenture or Demand Note payment obligations, the indenture agreements relating to our Debentures and Demand Notes provide that the trustee could accelerate all payments due under the Debentures and Demand Notes, which would further negatively affect our financial position.

Our obligations with respect to the Debentures and Demand Notes are governed by the terms of indenture agreements with U.S. Bank National Association, as trustee. Under the indentures, in addition to other possible events of default, if we fail to make a payment of principal or interest under any Debenture or Demand Note and this failure is not cured within 30 days, we will be deemed in default. Upon such a default, the trustee or holders of 25% in principal of the outstanding Debentures or Demand Notes could declare all principal and accrued interest immediately due and payable. Since our total assets do not cover these debt payment obligations, we would most likely be unable to make all payments under the Debentures or Demand Notes when due, and we might be forced to cease our operations.

9

If we are unable to meet our debenture and demand note redemption obligations, and we are unable to obtain additional financing or other sources of capital, we may be forced to sell off our loan receivables and other operating assets or we might be forced to cease our operations, and you could lose some or all of your investment.

In addition to the Demand Notes we issue pursuant to this prospectus, we may issue demand notes, debentures, or similar debt instruments to investors in order to raise funds for our operations. As of September 25, 2010, we had a total of $71.2 million of debentures and $3.2 million of demand notes outstanding, which demand notes may be redeemed by our investors at any time. Of this amount, our subsidiary, The Money Tree of Georgia Inc., has $22.5 million of debentures and $0.3 million of demand notes outstanding. While the maturing debentures of our subsidiary are subject to substantially similar early redemption and automatic extension provisions as the debentures, we cannot predict with any accuracy the number of debenture holders who will elect to redeem such debentures at or prior to maturity. We intend to pay these and any other redemption obligations using our normal cash sources, such as collections on finance receivables and used car sales, as well as proceeds from the sale of the debentures and demand notes. We are substantially reliant upon the net offering proceeds we receive from the sale of the debentures and demand notes. However, during the fiscal year ended September 25, 2010, we redeemed $14.4 million in debentures, while only receiving $12.0 million from the sale of new debentures. Therefore, we have had to use funds from operations to fund these net redemptions. Our operations and other sources of funds may not provide sufficient available cash flow to meet our continued redemption obligations if the amount of redemptions continues at its current pace and we continue to suffer losses and use funds from operations to fund redemptions. If we are unable to repay or redeem the principal amount of debentures or demand notes when due, and we are unable to obtain additional financing or other sources of capital, we may be forced to sell off our loan receivables and other operating assets or we might be forced to cease our operations, and you could lose some or all of your investment.

Our decreased sales of Debentures and Demand Notes, along with the increased redemptions of these securities, has resulted in fewer loans being made to customers, which has significantly negatively affected our operations, financial position and liquidity.

For the fiscal years ended September 25, 2010 and 2009, we sold $12.0 million and $10.0 million of Debentures, respectively. Meanwhile, we had redemptions of Debentures of $14.4 million and $18.6 million during the same periods, respectively. For the fiscal years ended September 25, 2010 and 2009, we sold $2.6 million and $3.0 million of Demand Notes, respectively. Meanwhile, we had redemptions of Demand Notes of $2.6 million and $3.5 million during the same periods, respectively. These $11.5 million combined net redemptions during the past two years have required us to use significant funds from operations to pay these net redemptions and corresponding interest payments. Accordingly, we have made significantly less loans to our customers resulting in reduced net finance receivables balances and net interest and fee income. This decrease in sales of Debentures and Demand Notes, along with the increased redemptions of these securities, have significantly negatively affected our operations, financial position and liquidity.

Our internal controls over financial reporting have not been effective in preventing or detecting misstatements in our consolidated financial statements, and if we fail to detect material misstatements in our consolidated financial statements, our consolidated financial condition and operating results could be severely and negatively affected.

During our fiscal years ended September 25, 2010, 2009 and 2008, we concluded that our system of internal controls over financial reporting contained a material weakness and was not operating effectively. This resulted in errors in our consolidated financial statements. There can be no assurance that in the future our system of internal controls would detect misstatements in our consolidated financial statements. If we fail to detect material misstatements in our consolidated financial statements in the future, our consolidated financial condition and operating results could be severely and negatively affected.

If we find further errors in our previously issued consolidated financial statements, we may again need to suspend our offerings of demand notes and debentures until such time as the financial misstatements can be corrected, and if correcting those errors requires an extended period of time, our ability to meet our financial obligations could be severely and negatively affected.

On April 23, 2010, we concluded that the previously issued audited consolidated financial statements contained in our Annual Report on Form 10-K for the fiscal year ended September 25, 2009 and the unaudited consolidated financial statements contained in our Quarterly Report on Form 10-Q for the three months ended December 25, 2009, should no longer be relied upon because of an error in the statements. We decided to restate our audited consolidated financial results as of September 25,

10

2009 and 2008 and for the three years ended September 25, 2009, 2008 and 2007, and subsequently filed an amended Annual Report on Form 10-K and Quarterly Report on Form 10-Q to accurately reflect our restated consolidated financial position and results of operations. The error in the consolidated financial statements was, in part, caused by a material weakness in our internal control over financing reporting. In the future, if we conclude that our previously issued consolidated financial statements contain errors and cannot be relied upon, we may suspend the sale of debentures and demand notes under our current offerings until such time as the errors are corrected. If correcting these errors requires an extended period of time, our ability to meet our financial obligations could be severely and negatively affected.

We can provide no assurance that any Demand Notes will be sold or that we will raise sufficient proceeds to carry out our business plans.

We are offering the Demand Notes through our designated selling officer without a firm underwriting commitment. While we intend to sell up to $35 million in principal amount of Demand Notes, there is no minimum amount of proceeds that must be received from the sale of the Demand Notes in order to accept proceeds from the Demand Notes actually sold. Accordingly, we can provide no assurance about the total principal amount of Demand Notes that will be sold. Therefore, we cannot assure you that we will raise sufficient proceeds to carry out our business plans.

If we or our operations suffer from severe negative publicity, we could be faced with significantly greater payment or redemption obligations from holders of the Debentures and Demand Notes than we have cash available for such payments or redemptions.

Because our Debentures are redeemable by holders at the end of any interest adjustment period and our Demand Notes are payable or redeemable at any time by holders, we cannot control the amount or timing of such payments or redemptions. If we or our operations suffer from severe negative publicity, we may receive significantly greater payment or redemption requests in a short time period than we have cash available to fund such payments or redemptions. In such event, we could be declared in default on the Demand Notes and other debt instruments and you could lose your entire investment.

11

Our Demand Notes are not insured or guaranteed by any third party, so you are dependent upon our ability to manage our business and generate adequate cash flows.

Our Demand Notes are not insured or guaranteed by the FDIC, any governmental agency or any other public or private entity as are certificates of deposit or other accounts offered by banks, savings and loan associations or credit unions. You are dependent upon our ability to effectively manage our business to generate sufficient cash flow, including cash flow from our financing activities, for the repayment of principal and interest on the Demand Notes. During 2007 through 2010, we incurred significant losses and we have used substantial amounts of operating cash flows to fund redemptions of debentures and demand notes. If these trends continue, you could lose your entire investment.

Our operations are not subject to the stringent banking regulatory requirements designed to protect investors, so your investment is completely dependent upon our successful operation of our business.

Our operations are not subject to the stringent regulatory requirements imposed upon the operations of commercial banks, savings banks and thrift institutions and are not subject to periodic compliance examinations by federal banking regulators. Therefore, an investment in our Demand Notes does not have the regulatory protections that the holder of a demand account or a certificate of deposit at a bank does. The return on your investment is completely dependent upon our successful operation of our business. To the extent that we do not successfully operate our business, our ability to repay the principal and interest on the Demand Notes will be impaired.

There is no sinking fund to ensure repayment of the Demand Notes at maturity, so you are totally reliant upon our ability to generate adequate cash flows.

We do not contribute funds to a separate account, commonly known as a sinking fund, to repay the Demand Notes. Because funds are not set aside periodically for the repayment of the Demand Notes, you must rely on our cash flow from operations and other sources of financing for repayment, such as funds from the sale of demand notes and debentures and credit facilities, if any. To the extent cash flow from operations and other sources are not sufficient to repay the Demand Notes, you may lose all or a part of your investment.

An increase in market interest rates may result in a reduction in our liquidity and increased losses or delay in our return to profitability and impair our ability to pay interest and principal on our debentures and demand notes.

Interest rates are currently at or near historic lows. Sustained, significant increases in interest rates could unfavorably impact our liquidity and increase our losses or delay our return to profitability by reducing the interest rate spread between the rate of interest we receive on loans and interest rates we must pay under our demand notes and debentures and any bank debt we incur. Any reduction in our liquidity and increase in our losses or delay in our return to profitability would diminish our ability to pay interest and principal on the Demand Notes.

Payment on the Demand Notes is subordinate to the payment of all outstanding present and future senior debt, and the indenture does not limit the amount of senior debt we may incur.

The Demand Notes are subordinate and junior to any and all of our senior debt. There are no restrictions in the indenture regarding the amount of senior debt or other indebtedness that we or our subsidiaries may incur. Upon the maturity of our senior debt, by lapse of time, acceleration or

12

otherwise, the holders of our senior debt have first right to receive payment in full prior to any payments being made to you as a Debenture holder. Therefore, you would only be repaid if funds remain after the repayment of our senior debt. As of September 25, 2010, we had $164,625 of senior debt outstanding.

Payment of interest and principal on the Demand Notes is effectively subordinate to the payment of the secured and unsecured creditors of our subsidiaries, including holders of debentures and demand notes issued by The Money Tree of Georgia Inc.

Substantially all of our assets and operations are conducted through our subsidiaries. As a result, all the creditors of our subsidiaries, including the holders of the demand notes and debentures issued by The Money Tree of Georgia Inc., would be paid prior to our subsidiaries being allowed to distribute any amounts to us. As of September 25, 2010, $0.3 million of demand notes and $22.5 million of debentures issued by The Money Tree of Georgia Inc. were outstanding. If our subsidiaries did not have sufficient funds to pay their debts, our ability to pay interest and principal on the Demand Notes would be impaired.

The indenture does not contain covenants restricting us from taking certain actions, and therefore the indenture provides very little protection of your investment.

The Demand Notes do not have the benefit of extensive covenants. The covenants in the indenture are not designed to protect your investment if there is a material adverse change in our financial condition or results of operations. For example, the indenture does not contain any restrictions on our ability to create or incur senior debt or other debt or to pay dividends or any financial covenants (such as a fixed charge coverage or minimum net worth covenants) to help ensure our ability to repay the principal and interest on the Demand Notes. In addition, the indenture does not contain covenants specifically designed to protect you if we engage in a highly leveraged transaction. Therefore, the indenture provides very little protection of your investment.

If we redeem the Demand Notes, you may not be able to reinvest the proceeds at comparable rates.

We may redeem, at our option, at any time, the Demand Notes (1) upon at least 30 days written notice, or (2) if the principal balance falls below $100. In the event we redeem your Demand Note, you would have the risk of reinvesting the proceeds at the then-current market rates, which may be higher or lower.

Risks Related to Our Business

There is uncertainty as to our ability to continue as a going concern.

The opinion of our independent registered accounting firm for the fiscal year ended September 25, 2010, which is included with our audited consolidated financial statements and related notes included in this prospectus, includes an explanatory paragraph that states that we have incurred recurring losses from operations, negative cash flows from operating activities and have a net shareholders’ deficit that raise substantial doubt about our ability to continue as a going concern. If we cannot generate sufficient cash flow to meet our obligations on a timely basis through the sale of Debentures and Demand Notes and collections from our customers, originate new loans, and ultimately attain profitable operations, there can be no assurance that we will be able to continue as a going concern. See “Basis of Financial Statement Presentation” in Note 2 to our Consolidated Financial Statements.

13

We suffered significant losses during fiscal years 2007 through 2010 and we anticipate such losses will likely continue in 2011.

Our net losses were approximately $3.8 million, $10.0 million, $12.9 million and $12.1 million during fiscal years 2007, 2008, 2009 and 2010, respectively. We anticipate that such significant losses will likely continue in 2011.

We have suffered significant credit losses due to continued weakening economic conditions, and there is no guarantee such credit losses will not continue during this downturn in the economy or that our operations and profitability will not continue to be negatively affected.

Because our business consists mainly of making loans to individuals who depend on their earnings to make their repayments, our ability to operate on a profitable basis depends to a large extent on the continued employment of those individuals and their ability to meet their financial obligations as they become due. In the current recession and continued downturn in the U.S. and local economies in which we operate, our customers have been affected by the resulting unemployment and increases in the number of personal bankruptcies. Therefore, we continue to experience increased credit losses and our collection ratios and profitability could continue to be materially and adversely affected. This recession has negatively affected our customers’ disposable income, confidence and spending patterns and preferences, which in turn are negatively impacting our sales of consumer goods and vehicles and our customers’ ability to repay their obligations to us. As a result, we continue to experience significant credit losses through loan charge-offs. For the fiscal year ended September 25, 2010, our charge-offs, net of recoveries, for our entire loan portfolio were $7.7 million, or 15.5% of average net finance receivables, and charge-offs for the direct consumer loans and consumer sales finance contract segments were 19.7% of the related average receivables. Although the net charge-offs for this fiscal year are less than in the previous year, these high levels of charge-offs have had a negative impact on our operations and profitability. Should the current economic conditions continue or worsen, our operations and profitability will continue to be materially and adversely affected.

Our significant shareholders’ deficit balance (and balance sheet insolvency) may limit our ability to obtain future financing, which could have a negative effect on our operations and our liquidity.

As of September 25, 2010, we had a shareholders’ deficit of $45.9 million which means our total liabilities exceed our total assets. Bankruptcy law defines this as balance sheet insolvency. The existence of a significant shareholders’ deficit may limit our ability to obtain future debt or equity financing. If we are unable to obtain financing in the future, it will likely have a negative effect on our operations and our liquidity and our ability to continue as a going concern.

Our lack of a significant line of credit could affect our liquidity.

We have operated without a significant line of credit for the past several years. We have been seeking for several months to obtain a line of credit as an additional source of long-term financing. If we fail to obtain a line of credit, we will be more dependent on the proceeds from the debentures and demand notes for our continued liquidity. Since our sales of the debentures and demand notes have been significantly curtailed, our failure to obtain a line of credit would negatively affect our ability to meet our obligations.

14

The collectability of our finance receivables has been severely and negatively affected by general economic conditions and we have not been able to recover the full amount of delinquent accounts by resorting to sale of collateral or receipt of non-filing insurance proceeds.

Our liquidity is dependent on, among other things, the collection of our finance receivables. We continually monitor the delinquency status of our finance receivables and promptly institute collection efforts on delinquent accounts. Collections of our consumer finance receivables have been severely and negatively affected by general economic conditions. Since we do not ordinarily perfect our security interest in collateral for loans, we have not been able to recover the full amount of outstanding receivables by resorting to the sale of collateral or receipt of non-filing insurance proceeds.

Our typical customer base has “subprime” credit ratings and higher than average credit risks which may result in increased loan defaults.

We typically lend money to individuals who have difficulty receiving loans from banks and other financial institutions because of credit problems or other adverse financial circumstances. Therefore, we have a higher risk of loan default among our customers than other lending companies. If we continue to suffer increased loan defaults, our operations will be materially adversely affected, and we may have difficulty making our principal and interest payments on the Demand Notes.

Hurricanes or other adverse weather events could negatively affect local economies or cause disruption to our branch office locations, which could have an adverse effect on our business or results of operations.

Our operations are conducted in the States of Georgia, Florida, Alabama and Louisiana, including areas susceptible to hurricanes or tropical storms. Such weather events can disrupt our operations, result in damage to our branch office locations and negatively affect the local economies in which we operate. We cannot predict whether or to what extent future hurricanes will affect our operations or the economies in our market areas, but such weather events could result in a decline in loan originations and an increase in the risk of delinquencies, foreclosures or loan losses. Our business or results of operations may be adversely affected by these and other negative effects of future hurricanes.

Additional competition may decrease our liquidity and profitability, which would adversely affect our ability to repay the Demand Notes.

We compete for business with a number of large national companies and banks that have substantially greater resources, lower cost of funds, and a more established market presence than we have. If these companies increase their marketing efforts to include our market niche of borrowers, or if additional competitors enter our markets, we may be forced to reduce our interest rates and fees in order to maintain or expand our market share. Any reduction in our interest rates or fees could have an adverse impact on our liquidity and profitability and our ability to repay the Demand Notes.

We are subject to many laws and governmental regulations, and any changes in these laws or regulations may materially adversely affect our financial condition and business operations.

Our operations are subject to regulation by federal authorities and state banking, finance, consumer protection and insurance authorities and are subject to various laws and judicial and administrative decisions imposing various requirements and restrictions on our operations which, among other things, require that we obtain and maintain certain licenses and qualifications, and limit

15

the interest rates, fees and other charges we may impose in our consumer finance business. Although we believe we are in compliance in all material respects with applicable laws, rules and regulations, we cannot assure you that we are or that any change in such laws, or in the interpretations thereof, will not make our compliance with such laws more difficult or expensive or otherwise adversely affect our financial condition or business operations.

The impact on us of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (the “Dodd-Frank Act”) and its implementing regulations cannot be predicted at this time.

A wide range of regulatory initiatives directed at the financial services industry has been proposed in recent months. One of those initiatives, the Dodd-Frank Act, was signed into law by President Obama on July 21, 2010. The Dodd-Frank Act represents a comprehensive overhaul of the financial services industry within the United States, establishes the new federal Bureau of Consumer Financial Protection (the “BCFP”) and will require the BCFP, the FDIC, the SEC and other federal agencies to implement numerous new rules, many of which may not be implemented for several months or years. The Dodd-Frank Act and the resulting regulations will significantly impact the current regulatory structure and affect the lending, deposit, investment, trading and operating activities of financial institutions. At this time, it is difficult to predict the extent to which the Dodd-Frank Act or the resulting regulations will impact our business. However, compliance with these new laws and regulations may result in additional cost and expenses, which may impact our results of operations, financial condition or liquidity.

We are devoting resources to comply with various provisions of the Sarbanes-Oxley Act, including Section 404 relating to internal controls testing, and this may reduce the resources we have available to focus on our core business.

For fiscal year ended September 25, 2010, we are subject to the requirements of Section 404(A) of the Sarbanes-Oxley Act, and in order to ensure compliance with the various provisions of the Sarbanes-Oxley Act, we have evaluated our internal controls over financial reporting to allow management to report on our internal controls systems. Among other things, we may not be able to conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with Section 404. Any failure to comply with the various requirements of the Sarbanes-Oxley Act, may require significant management time and expenses, and divert attention or resources away from our core business.

We are controlled by Bradley D. Bellville and do not have any independent board members overseeing our operations.

Our board of directors consists of Bradley D. Bellville, our President, and Jefferey V. Martin. We do not have any independent directors on our board. In addition, Bradley D. Bellville owns a majority of the outstanding shares of our voting capital stock. Therefore, Mr. Bellville will be able to exercise significant control over our affairs, including the election of directors.

16

FORWARD-LOOKING STATEMENTS

This prospectus contains forward-looking statements within the meaning of federal securities law. Words such as “may,” “will,” “expect,” “anticipate,” “believe,” “estimate,” “continue,” “predict,” or other similar words identify forward-looking statements. Forward-looking statements appear in a number of places in this prospectus, including, without limitation, “Use of Proceeds” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations,” and they include statements regarding our intent, belief or current expectation about, among other things, trends affecting the markets in which we operate, our business, our financial condition and our growth strategies. Although we believe that the expectations reflected in these forward-looking statements are based on reasonable assumptions, forward-looking statements are not guarantees of future performance and involve risks and uncertainties. Actual results may differ materially from those predicted in the forward-looking statements as a result of various factors, including those set forth in the “Risk Factors” section of this prospectus. If any of the events described in “Risk Factors” occur, they could have an adverse effect on our business, financial condition and results of operations. When considering forward-looking statements, you should keep these risk factors, as well as the other cautionary statements in this prospectus, in mind. You should not place undue reliance on any forward-looking statement. We are not obligated to update forward-looking statements.

17

USE OF PROCEEDS

If we sell all of the Demand Notes offered by this prospectus, we estimate that the net proceeds will be approximately $34,385,000 after deduction of estimated offering expenses of $615,000. We will pay all of the expenses related to this offering.

We will receive cash proceeds in varying amounts from time to time as the Demand Notes are sold. Due to our inability to predict with any certainty whatsoever the amount of offering proceeds we will receive from the sale of the Demand Notes or when holders of the Demand Notes will redeem or which holders of other demand notes or debentures will redeem at or prior to maturity, we cannot provide any specific allocation of proceeds we will use for any particular purpose. However, we intend to use substantially all of the net offering proceeds in the following order of priority:

| | • | | to redeem (1) debentures listed in the maturity date table below and any other debentures and demand notes of our subsidiary, The Money Tree of Georgia Inc., and (2) the Series A Variable Rate Subordinated Debentures, the Demand Notes offered in this offering and Debentures issued by us; |

| | • | | to make interest payments to holders of all of our debentures and demand notes; |

| | • | | to the extent that net proceeds remain and we have adequate cash on hand, to fund the following company activities: |

| | ¡ | | for working capital and other general corporate purposes; |

| | ¡ | | to make additional consumer loans; |

| | ¡ | | to fund the purchase of inventory of used cars; |

| | ¡ | | to open new branch office locations; and |

| | ¡ | | to acquire loan receivables from competitors. |

Although we are unable to predict with any certainty when holders of the Demand Notes will redeem or which holders of other demand notes or debentures will redeem, below is a schedule showing the scheduled maturity dates (i.e., debentures which have reached their extended eight-year maturity dates) of the debentures issued by our subsidiary, The Money Tree of Georgia Inc. over the next three years. We anticipate primarily using net proceeds from this offering of the Demand Notes to fund the below scheduled redemptions of the debentures of our subsidiary, The Money Tree of Georgia Inc., and any other redemptions that occur prior to the scheduled maturity dates.

The Money Tree of Georgia Inc.

| | | | |

Debentures Maturity Schedule | | 8-Year Maturities | |

1/2011 thru 12/2011 | | $ | 8,749,004 | |

1/2012 thru 12/2012 | | | 8,910,762 | |

1/2013 thru 12/2013 | | | 9,589,266 | |

| | | | |

Total | | $ | 27,249,032 | |

There is no minimum number or amount of Demand Notes that we must sell to receive and use the proceeds from the sale of the Demand Notes, and we cannot assure you that all or any portion of the Demand Notes will be sold. In the event that we do not raise sufficient proceeds from our offerings

18

of the Demand Notes and Debentures to adequately fund our operations, we could curtail the amount of funds we loan to our customers and focus on cash collections to increase cash flow. Please see “Risk Factors – Risks Related to Our Offering – If we continue to redeem more debentures and demand notes than we sell in any given period, our liquidity and capital needs will continue to be severely and negatively affected,” “Risk Factors – Risks Related to Our Offering – We can provide no assurance that any Demand Notes will be sold or that we will raise sufficient proceeds to carry out our business plans,” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources.”

SELECTED CONSOLIDATED FINANCIAL DATA

The following selected consolidated financial data should be read in conjunction with “Management’s Discussion and Analysis of Financial Condition and Results of Operations” and our audited consolidated financial statements and related notes included elsewhere in this prospectus. The selected consolidated balance sheet data, as of September 25, 2010 and 2009, and the selected consolidated statement of operations data, for the fiscal years ended September 25, 2010 and 2009, have been derived from our audited consolidated financial statements and related notes included in this prospectus. The selected consolidated balance sheet data, as of September 25, 2008, 2007, and 2006, and the selected consolidated statement of operations data, for the fiscal year ended September 25, 2008, 2007 and 2006, have been derived from our audited financial statements that are not included in this prospectus.

[Remainder of page intentionally left blank]

19

| | | | | | | | | | | | | | | | | | | | |

| | | As of, and for, the Fiscal Year Ended September 25, | |

| | | 2010 | | | 2009 | | | 2008 | | | 2007 | | | 2006 | |

Interest and fee income | | $ | 11,807 | | | $ | 15,589 | | | $ | 19,280 | | | $ | 19,481 | | | $ | 20,048 | |

Interest expense | | | (6,976 | ) | | | (7,611 | ) | | | (8,275 | ) | | | (8,026 | ) | | | (7,350 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net interest and fee income before provision for credit losses | | | 4,831 | | | | 7,978 | | | | 11,005 | | | | 11,455 | | | | 12,698 | |

Provision for credit losses | | | (5,682 | ) | | | (10,762 | ) | | | (13,043 | ) | | | (7,940 | ) | | | (4,718 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net revenue (loss) from interest and fees after provision for credit losses | | | (851 | ) | | | (2,784 | ) | | | (2,038 | ) | | | 3,515 | | | | 7,980 | |

Insurance commissions | | | 5,032 | | | | 8,354 | | | | 9,615 | | | | 10,120 | | | | 11,263 | |

Commissions from motor club memberships(1) | | | 1,371 | | | | 1,602 | | | | 1,844 | | | | 1,947 | | | | 1,957 | |

Delinquency fees | | | 1,326 | | | | 1,561 | | | | 1,720 | | | | 1,776 | | | | 1,565 | |

Income tax service income(2) | | | - | | | | - | | | | - | | | | 3 | | | | 83 | |

Other income | | | 401 | | | | 530 | | | | 647 | | | | 748 | | | | 689 | |

| | | | | | | | | | | | | | | | | | | | |

Net revenues before retail sales | | | 7,279 | | | | 9,263 | | | | 11,788 | | | | 18,109 | | | | 23,537 | |

Retail sales | | | 9,419 | | | | 16,019 | | | | 17,164 | | | | 19,002 | | | | 17,972 | |

Cost of sales | | | (5,840 | ) | | | (10,366 | ) | | | (11,131 | ) | | | (12,170 | ) | | | (11,611 | ) |

| | | | | | | | | | | | | | | | | | | | |

Gross margin on retail sales | | | 3,579 | | | | 5,653 | | | | 6,033 | | | | 6,832 | | | | 6,361 | |

Net revenues | | | 10,858 | | | | 14,916 | | | | 17,821 | | | | 24,941 | | | | 29,898 | |

Operating expenses | | | (22,806 | ) | | | (28,278 | ) | | | (28,469 | ) | | | (27,604 | ) | | | (29,151 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net operating income (loss) | | | (11,948 | ) | | | (13,362 | ) | | | (10,468 | ) | | | (2,663 | ) | | | 747 | |

Other non-operating income | | | - | | | | - | | | | - | | | | - | | | | 151 | |

Loss on sale of property and equipment | | | (187 | ) | | | (11 | ) | | | (21 | ) | | | (19 | ) | | | (75 | ) |

| | | | | | | | | | | | | | | | | | | | |

Income (loss) before income tax benefit (expense) | | | (12,135 | ) | | | (13,373 | ) | | | (10,669 | ) | | | (2,682 | ) | | | 823 | |

Income tax benefit (expense) | | | - | | | | 438 | | | | 682 | | | | (1,109 | ) | | | (274 | ) |

| | | | | | | | | | | | | | | | | | | | |

Net income (loss) | | $ | (12,135 | ) | | $ | (12,935 | ) | | $ | (9,987 | ) | | $ | (3,791 | ) | | $ | 549 | |

| | | | | | | | | | | | | | | | | | | | |

Ratio of earnings to fixed charges(3) | | | (4 | ) | | | (4 | ) | | | (4 | ) | | | (4 | ) | | | 1.10 | |

| | | | | |

Cash and cash equivalents | | $ | 2,115 | | | $ | 2,922 | | | $ | 12,541 | | | $ | 17,854 | | | $ | 12,920 | |

Finance receivables(5) | | | 42,319 | | | | 56,281 | | | | 68,601 | | | | 72,276 | | | | 73,178 | |

Allowance for credit losses | | | (6,871 | ) | | | (8,925 | ) | | | (8,814 | ) | | | (5,150 | ) | | | (2,275 | ) |

| | | | | | | | | | | | | | | | | | | | |

Finance receivables, net | | | 35,448 | | | | 47,356 | | | | 59,787 | | | | 67,126 | | | | 70,903 | |

Other receivables | | | 493 | | | | 717 | | | | 957 | | | | 861 | | | | 1,013 | |

Inventory | | | 1,202 | | | | 2,202 | | | | 3,167 | | | | 3,057 | | | | 2,195 | |

Property and equipment, net | | | 3,369 | | | | 4,227 | | | | 4,906 | | | | 4,220 | | | | 4,581 | |

Total assets | | | 43,226 | | | | 59,254 | | | | 83,857 | | | | 95,862 | | | | 95,732 | |

Senior debt | | | 165 | | | | 327 | | | | 695 | | | | 512 | | | | 669 | |

Senior subordinated debt | | | - | | | | - | | | | - | | | | - | | | | 600 | |

Subordinated debt, related parties | | | - | | | | - | | | | - | | | | - | | | | 370 | |

Debentures(6) | | | 71,227 | | | | 73,603 | | | | 82,209 | | | | 81,861 | | | | 77,910 | |

Demand notes(6) | | | 3,175 | | | | 3,147 | | | | 3,658 | | | | 5,991 | | | | 8,137 | |

Shareholders’ deficit | | $ | (45,909 | ) | | $ | (33,774 | ) | | $ | (20,839 | ) | | $ | (10,852 | ) | | $ | (7,060 | ) |

| (1) | Received from Interstate Motor Club, Inc., an affiliated entity. |

| (2) | Received from Cash Check Inc. of Ga., an affiliated entity. |

| (3) | The ratio of earnings to fixed charges represents the number of times fixed charges are covered by earnings. For purposes of this ratio, “earnings” is determined by adding pre-tax income to “fixed charges,” which consists of interest on all indebtedness and an interest factor attributable to rent expense. |

| (4) | Calculation results in a deficiency in the ratio (i.e., less than one-to-one coverage). The deficiency in earnings to cover fixed charges was $12,134,947, $13,372,623; $10,669,231; and $2,682,314 for the years ended September 25, 2010, 2009, 2008, and 2007, respectively. |

| (5) | Net of unearned insurance commissions, unearned finance charges and unearned discounts. |

| (6) | Issued, in part, by our subsidiary, The Money Tree of Georgia Inc. See Note 7 to our consolidated audited financial statements for the year ended September 25, 2010. |

20

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND

RESULTS OF OPERATIONS

The following discussion should be read in conjunction with the information under “Selected Consolidated Financial Data” and our audited consolidated financial statements and related notes and other financial data included elsewhere in this prospectus.

Overview

We make consumer finance loans and provide other financial products and services through our branch offices in Georgia, Alabama, Louisiana and Florida. We sell retail merchandise, principally furniture, appliances and electronics, at certain of our branch office locations and operate two used automobile dealerships in the State of Georgia. We also offer insurance products, prepaid phone services and automobile club memberships to our loan customers.

We fund our consumer loan demand through a combination of cash collections from our consumer loans, proceeds raised from the sale of debentures and demand notes and loans from various banks and other financial institutions. Our consumer loan business consists of making, purchasing and servicing direct consumer loans, consumer sales finance contracts and motor vehicle installment sales contracts. Direct consumer loans generally serve individuals with limited access to other sources of consumer credit, such as banks, savings and loans, other consumer finance businesses and credit cards. Direct consumer loans are general loans made typically to people who need money for some unusual or unforeseen expense, for the purpose of paying off an accumulation of small debts or for the purchase of furniture and appliances. Consumer sales finance contracts consist of retail installment sales contracts for purchases of specific consumer goods by customers either from our branch locations or from a retail store and are collateralized by such consumer goods. Motor vehicle installment sales contracts are initiated by us or purchased from automobile dealers subject to our credit approval and are collateralized by such automobiles. The following table sets forth certain information about the components of our finance receivables:

Description of Loans and Contracts

| | | | | | | | |

| | | As of, or for, the Year Ended September 25, | |

| | | 2010 | | | 2009 | |

Direct Consumer Loans: | |

Number of Loans Made to New Borrowers | | | 23,075 | | | | 33,045 | |

Number of Loans Made to Former Borrowers | | | 57,651 | | | | 64,774 | |

Number of Loans Made to Existing Borrowers | | | 45,653 | | | | 50,504 | |

Total Number of Loans Made | | | 126,379 | | | | 148,323 | |

Total Volume of Loans Made | | $ | 36,677,415 | | | $ | 48,940,971 | |

Average Size of Loans Made | | $ | 290 | | | $ | 330 | |

Number of Loans Outstanding | | | 36,715 | | | | 47,619 | |

Total of Loans Outstanding | | $ | 14,790,670 | | | $ | 20,098,661 | |

Percent of Loans Outstanding | | | 29.8 | % | | | 30.0 | % |

Average Balance on Outstanding Loans | | $ | 403 | | | $ | 422 | |

21

Description of Loans and Contracts

| | | | | | | | |

| | | As of, or for, the Year Ended September 25, | |

| | | 2010 | | | 2009 | |

Motor Vehicle Installment Sales Contracts: | | | | | | | | |