| PROSPECTUS | Filed Pursuant to Rule 424(b)(3) Registration No. 333-121121 |

(Proposed Holding Company for North Penn Bank)

Up to 861,638 Shares of Common Stock

North Penn Bancorp, Inc., a Pennsylvania state-chartered stock corporation, is offering common stock for sale in connection with the reorganization of North Penn Bank into the mutual holding company form of organization. The shares we are offering will represent 44.1% of the outstanding common stock of North Penn Bancorp. North Penn Bank (in mutual form) has formed North Penn Bancorp to own North Penn Bank (in stock form) as part of the reorganization and will also form North Penn Mutual Holding Company, a Pennsylvania state-chartered mutual holding company, which will own 53.9% of the outstanding common stock of North Penn Bancorp. We also intend to contribute 2% of the common stock issued in the reorganization and $100,000 in cash to the North Penn Charitable Foundation, a charitable foundation which we intend to form in connection with the reorganization. We expect that our common stock will be quoted on the OTC Bulletin Board.

If you are or were a depositor of North Penn Bank:

| • | You may have priority rights to purchase shares of common stock. |

If you are a participant in the North Penn Bank 401(k) Plan:

| • | You may direct that all or part of your current account balances in this plan be invested in shares of common stock. |

| • | You will be receiving separately a supplement to this prospectus that describes your rights under this plan. |

If you fit none of the categories above, but are interested in purchasing shares of our common stock:

| • | You may have an opportunity to purchase shares of common stock after priority orders are filled. |

We are offering up to 861,638 shares of common stock for sale on a best efforts basis, subject to certain conditions. We must sell a minimum of 636,863 shares to complete the offering. We may sell up to 990,883 shares without resoliciting subscribers because of regulatory considerations, demand for the shares or changes in market conditions. The offering is expected to terminate at 10:00 a.m., Eastern Time, on April 27, 2005. We may extend this expiration date without notice to you until June 10, 2005, unless the Pennsylvania Department of Banking or Federal Deposit Insurance Corporation approves a later date, which will not be beyond May 4, 2007. If the offering is terminated or if the minimum number of shares are not sold by May 4, 2007, subscribers will have their funds returned promptly with interest.

Ryan Beck & Co., Inc. will use its best efforts to assist us in our selling efforts, but is not required to purchase any of the common stock being offered for sale. Purchasers will not pay a commission to purchase shares of common stock in the offering. All shares are offered for sale at a price of $10.00 per share.

The minimum purchase is 25 shares. Once submitted, orders are irrevocable unless the offering is terminated or extended beyond June 10, 2005. If the offering is extended beyond June 10, 2005 or the number of shares of common stock to be sold is increased to more than 990,883 shares or decreased to less than 636,863 shares, subscribers will have a designated period to modify or rescind their purchase orders. Those who do not respond will have their funds returned promptly with interest. Funds received before completion of the offering will be held in an escrow account at North Penn Bank and will earn interest at our passbook rate.

We expect our trustees and executive officers, together with their associates, to subscribe for 56,400 shares, which equals 7.21% of the shares that will be sold in the offering at the midpoint of the offering range.

OFFERING SUMMARY

Price Per Share: $10.00

| Minimum | Maximum | Maximum As Adjusted | |||||||

Number of shares | 636,863 | 861,638 | 990,883 | ||||||

Gross offering proceeds | $ | 6,368,630 | $ | 8,616,380 | $ | 9,908,830 | |||

Estimated offering expenses | $ | 510,000 | $ | 510,000 | $ | 510,000 | |||

Estimated net proceeds | $ | 5,858,630 | $ | 8,106,380 | $ | 9,398,830 | |||

Estimated net proceeds per share | $ | 9.20 | $ | 9.41 | $ | 9.49 | |||

This investment involves a degree of risk, including the possible loss of principal.

Please read “Risk Factors” beginning on page 16.

These securities are not deposits or savings accounts and are not insured or guaranteed by the Federal Deposit Insurance Corporation or any other government agency.

Neither the Securities and Exchange Commission, the Pennsylvania Department of Banking, the Federal Deposit Insurance Corporation nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

For assistance, please contact the Stock Information Center at (570) 983-0240.

The date of this prospectus is March 28, 2005.

This summary highlights selected information from this document and may not contain all the information that is important to you. To understand the stock offering fully, you should read this entire document carefully. In certain instances where appropriate, the terms “we,” “us” and “our” refer collectively to North Penn Mutual Holding Company, North Penn Bancorp,North Penn Bank (in stock form) and North Penn Bank (in mutual form) or any of these entities, depending on the context.

The Companies

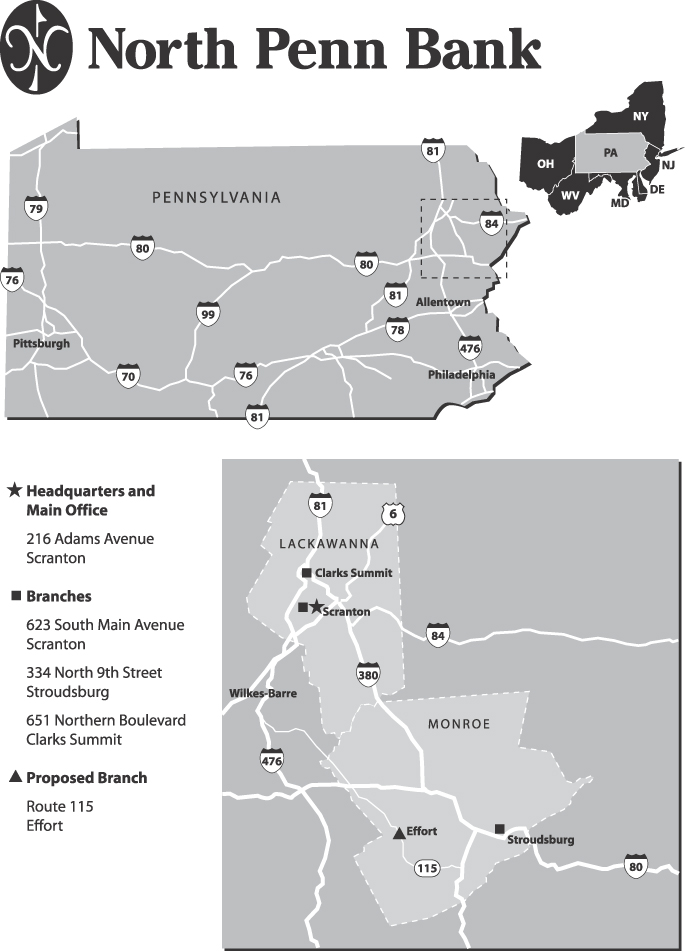

North Penn Bank 216 Adams Avenue Scranton, Pennsylvania 18503-1692 (570) 344-6113 | North Penn Bank is a community-oriented financial institution dedicated to serving the financial service needs of consumers and businesses within our market area. We engage primarily in the business of attracting deposits from the general public and using such funds to originate loans. We emphasize the origination of loans secured by first mortgages on owner-occupied, residential real estate. In recent years, our emphasis has also included automobile and commercial loans. To a lesser extent, we originate other types of real estate loans and consumer loans. We currently operate from our main office in Scranton, Pennsylvania and three branch offices in Lackawanna and Monroe Counties. At September 30, 2004, we had total assets of $93.4 million, deposits of $77.9 million and total capital of $7.7 million. We have also been granted approval to open an additional branch office in Effort, Pennsylvania. We anticipate that the Effort branch office will be open in late 2005. Upon completion of the proposed transaction, we will continue to operate under the name North Penn Bank. | |

North Penn Bancorp, Inc. 216 Adams Avenue Scranton, Pennsylvania 18503-1692 (570) 344-6113 | This offering is made by North Penn Bancorp, Inc., a Pennsylvania state-chartered stock corporation. North Penn Bancorp has been formed in connection with the reorganization and will become our Pennsylvania state-chartered mid-tier stock holding company. North Penn Bancorp is not currently an operating company. After the reorganization, North Penn Bancorp will own 100% of North Penn Bank’s capital stock and will direct, plan and coordinate North Penn Bank’s business activities. In the future, North Penn Bancorp might also acquire or organize other operating subsidiaries, including other financial institutions or financial services companies, although it currently has no specific plans or agreements to do so. | |

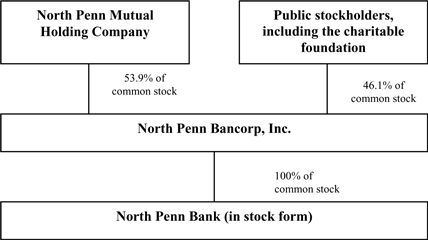

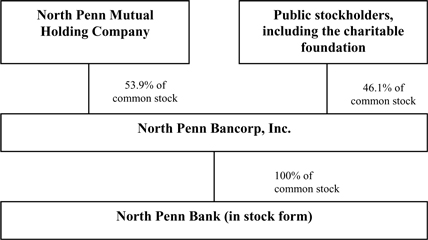

North Penn Mutual Holding Company 216 Adams Avenue Scranton, Pennsylvania 18503-1692 (570) 344-6113 | North Penn Mutual Holding Company will be formed upon completion of the reorganization and will become our Pennsylvania state-chartered mutual holding company parent and will own 53.9% of North Penn Bancorp’s common stock. So long as North Penn Mutual Holding Company exists, it will own a majority of the voting stock of North Penn Bancorp. North Penn Mutual Holding Company is not currently an operating company. North Penn Mutual Holding Company will have no stockholders. Depositors of North Penn Bank will have liquidation rights in North Penn Mutual Holding Company. We do not expect that North Penn Mutual Holding Company will engage in any business activity other than owning a majority of the common stock of North Penn Bancorp. | |

1

| North Penn Charitable Foundation (page 113) | To continue our long-standing commitment to our local communities, we intend to establish a charitable foundation, the North Penn Charitable Foundation, as a non-stock Pennsylvania corporation in connection with the reorganization. We will fund the foundation with 2% of the shares of our common stock issued in the reorganization and $100,000 in cash. Based on the purchase price of $10.00 per share, we would fund the foundation with $332,670 worth of common stock at the midpoint of the offering range. Our contribution to the foundation would reduce net earnings by approximately $255,000, after tax, in the year in which the foundation is established, which is expected to be fiscal 2005. The North Penn Charitable Foundation will make grants and donations to non-profit and community groups and projects located within our market area. The amount of common stock that we would offer for sale would be greater if the stock offering were to be completed without the formation of the North Penn Charitable Foundation. The establishment of the foundation requires the affirmative vote of a majority of the votes eligible to be cast by our depositors. For a further discussion of the financial impact of the foundation, including its effect on those who purchase shares in the offering, see “Comparison of Independent Valuation and Pro Forma Financial Information With and Without the Foundation” on page 51. | |

Our Operating Strategy (page 60) | North Penn Bank has never been affiliated with another bank and will remain independent after the reorganization which is an internal corporate restructuring meant to give us added operating flexibility. Our mission will continue to be to operate and grow a profitable community-oriented financial institution serving primarily retail customers and small businesses in our market area. After the reorganization, our operating strategy will be:

• operating as an independent community-oriented financial institution;

• increasing core deposits;

• expanding our branch network and upgrading our existing branches;

• pursuing opportunities to increase and diversify lending in our market area;

• applying conservative underwriting practices to maintain the high asset quality of our loan portfolio; and

• managing our net interest margin and interest rate risk. | |

2

| The Reorganization | ||

| Description of the Reorganization (page 98) | Currently, North Penn Bank is a Pennsylvania state-chartered savings bank organized in the mutual form (meaning no stockholders). Our depositors currently do not have any voting rights on any matters including the election of trustees.

The mutual holding company reorganization process that we are now undertaking involves a series of transactions by which we will convert from a state-chartered mutual form of organization to a state-chartered mutual holding company form of organization. In the mutual holding company structure, North Penn Bank will be a state-chartered stock savings bank and all of its stock will be owned by North Penn Bancorp, a new state-chartered stock holding company that we formed. In addition, 46.1% of North Penn Bancorp’s stock will be owned by the public, our employee stock ownership plan and our charitable foundation and 53.9% of North Penn Bancorp’s common stock will be owned by North Penn Mutual Holding Company, a mutual holding company that we are forming. Our depositors on the closing date of the reorganization will have liquidation rights in North Penn Mutual Holding Company and will not have voting rights. | |

| After the reorganization, our ownership structure will be as follows: | ||

| ||

| Our normal business operations will continue without interruption during the reorganization and the same officers and trustees who currently serve us will continue to serve us as officers and directors after the reorganization. The reorganization will not affect the balance or terms of deposit or loan accounts and deposits will continue to be federally insured by the Federal Deposit Insurance Corporation up to the maximum legal limits. Deposit accounts are not being converted to stock. | ||

3

| Reasons for the Reorganization (page 97) | Our primary reasons for the reorganization are to:

• structure our business in a form that will enable us to access capital markets;

• permit us to control the amount of capital being raised to enable us to prudently deploy the proceeds of the offering;

• support future lending and growth;

• enhance our ability to attract and retain qualified directors, management and other employees through stock-based compensation plans; and

• support future branching activities and/or the acquisition of other financial institutions or financial services companies or their assets.

Although we are interested in finding new possible branch locations, we do not have any specific plans or arrangements for further branch expansion, other than the branch expansion plans discussed in “Our Business – Properties” that are already underway. | |

| The Purchase Price is $10.00 | The purchase price is $10.00 per share. We determined this per share price in order to achieve a wide distribution of stock. You will not pay a commission to buy any shares in the offering. | |

| Number of Shares to be Sold | We are offering for sale between 636,863 and 861,638 shares of common stock in this offering. With regulatory approval, we may increase the number of shares to be sold to 990,883 shares without giving you further notice or the opportunity to change or cancel your order. The Pennsylvania Department of Banking and Federal Deposit Insurance Corporation will consider the level of subscriptions, our financial condition and results of operations and changes in market conditions in connection with a request to increase the offering size. | |

The Offering | ||

Persons Who Can Order Stock in the Offering (page 100) | We have granted rights to subscribe for our shares of common stock in a “subscription offering” to the following persons in the following order of priority:

1. Persons with balances aggregating $50 or more on deposit at North Penn Bank as of September 30, 2003.

2. Our employee stock ownership plan, which provides retirement benefits to our employees.

3. Persons with balances aggregating $50 or more on deposit at North Penn Bank as of December 31, 2004.

4. North Penn Bank’s depositors as of March 22, 2005. | |

| We may offer shares not sold in the subscription offering to the general public in a community offering and/or syndicated community offering. People who are residents of Lackawanna and Monroe Counties, Pennsylvania, will have first preference to purchase shares in a community offering. The community offering and/or syndicated community offering, if held, may begin concurrently, during or immediately after the end of the subscription offering. | ||

4

| If we receive subscriptions for more shares than are to be sold in this offering, we may be unable to fill or partially fill your order. Shares will be allocated first to categories in the subscription offering, under a formula outlined in the plan of reorganization and as described in “The Reorganization and Stock Offering.” If we are unable to fill your order, or can only fill your order in part, you will receive an appropriate refund, with interest. If you paid by check or money order, we will issue you a refund/interest check. If you paid by authorizing withdrawal from your North Penn Bank deposit account(s), we will only withdraw the funds necessary to pay for the shares you receive. Unused funds, along with accrued interest, will remain in your account(s). | ||

| Subscription Rights Are Not Transferable | You are not allowed to transfer or sell your subscription rights and we will act to ensure that you do not do so. You will be required to certify that you are purchasing shares solely for your own account. We will not accept any stock orders that we believe involve the transfer of subscription rights. | |

| The Deadline for Ordering Stock is April 27, 2005 (page 102) | The offering will end at 10:00 a.m., Eastern Time, on April 27, 2005 unless otherwise terminated or extended. A properly signed and completed order form with the required payment must be received (not postmarked) by us no later than 10:00 a.m., Eastern Time, on April 27, 2005. You may submit your order form using the enclosed order reply envelope, by bringing your order form to the Stock Information Center or by overnight delivery to the address noted on the order form.Order forms may not be delivered to our branch offices. We reserve the right to terminate the offering at any time, in which case subscribers’ funds will be promptly returned with interest. | |

| Minimum and Maximum Purchase Limitations (page 109) | Our plan of reorganization establishes limitations on the purchase of the common stock in the offering. These limitations include the following:

The minimum purchase is 25 shares.

No individual may purchase more than $100,000 of common stock (which equals 10,000 shares). If any of the following persons purchase stock, their purchases when combined with your purchases cannot exceed $200,000 of common stock (which equals 20,000 shares):

• Your spouse or relatives of you or your spouse living in your house;

• Companies, trusts or other entities in which you are a director, officer or partner, or have a controlling interest or hold a position;

• Trusts or other estates in which you have a substantial beneficial interest or as to which you serve as trustee or in another fiduciary capacity; or

• Other persons who may be associates or acting in concert with you.

All persons exercising subscription rights through a single qualifying deposit account held jointly will be counted as a single depositor for purposes of determining the maximum amount that may be subscribed for by an individual, and persons sharing the same address or exercising subscription rights through qualifying accounts registered to the same address will be subject to the overall purchase limitation. | |

5

| Subject to Pennsylvania Department of Banking and Federal Deposit Insurance Corporation’s approval, we may increase or decrease the purchase limitations at any time. | ||

How to Purchase Common Stock (page 105) | If you want to place an order for shares in the offering, you must complete an original stock order form and send it to us together with full payment. Once we receive your order, you cannot cancel or change it without our consent.

We may, in our sole discretion, reject orders received in the community offering and/or syndicated community offering, either in whole or in part.

You may pay for shares in the subscription offering, or the community offering in the following ways:

• By personal or bank check or money order made payable directly to North Penn Bancorp, Inc. (do not endorse third party checks); or

• By authorizing withdrawal from the types of North Penn Bank deposit account(s), on the order form. To use funds in an Individual Retirement Account at North Penn Bank, you may not authorize direct withdrawal on the order form. You must first transfer your funds to an unaffiliated institution able to hold self-directed IRAs. Purchasing stock through an IRA requires additional processing time. Please contact the Stock Information Center promptly, preferably at least two weeks before the April 27, 2005 offering deadline, for assistance using IRA funds that you have at North Penn Bank or elsewhere. Your ability to use retirement funds may depend on timing constraints and any limitations imposed by the IRA trustee. | |

| Checks and money orders will be deposited upon receipt. We will pay interest on your funds submitted by check or money order at the rate that we pay on passbook accounts from the date that we receive your funds until the offering is completed or terminated. All funds authorized for withdrawal from deposit accounts with us will remain in the accounts and continue to earn interest at the applicable contractual account rate and will be withdrawn upon completion of the offering. A hold will be placed on those funds when your stock order is received, making the designated funds otherwise unavailable to you. If, as a result of a withdrawal from a certificate account, the balance falls below the minimum balance requirement, the remaining funds will earn interest at our passbook rate. There will be no early withdrawal penalty for withdrawals from certificate accounts used to pay for stock.Federal law prohibits us from knowingly loaning funds to purchase stock in the offering. In addition, you may not submit a check drawn on a North Penn Bank line of credit. | ||

| Delivery of Stock Certificates | Certificates representing shares of common stock sold in the offering will be mailed to the persons entitled to the certificates at the certificate registration address noted on the order form as soon as practicable following consummation of the offering.It is possible that, until certificates for the common stock are delivered to purchasers, purchasers might not be able to sell the shares of common stock which they ordered, even though the common stock will have begun trading. | |

6

| How We Will Use the Proceeds of this Offering (page 37) | The following table summarizes how we will use the proceeds of this offering, based on the sale of shares at the minimum and maximum of the offering range. |

| 636,863 Shares at $10.00 Per Share | 861,638 Shares at $10.00 Per Share | |||||

| (In Thousands) | ||||||

Offering proceeds | $ | 6,369 | $ | 8,616 | ||

Less: offering expenses | 510 | 510 | ||||

Net offering proceeds | $ | 5,859 | $ | 8,106 | ||

Less: | ||||||

Proceeds contributed to North Penn Bank | 2,930 | 4,053 | ||||

Proceeds used for loan to employee stock ownership plan | 532 | 720 | ||||

Proceeds contributed to North Penn Charitable Foundation | 100 | 100 | ||||

Proceeds to North Penn Mutual Holding Company | 100 | 100 | ||||

Proceeds remaining for North Penn Bancorp, Inc. | $ | 2,197 | $ | 3,133 | ||

| We may use the portion of the proceeds that we do not contribute to North Penn Bank to, among other things, invest in securities, pay cash dividends or buy back shares of common stock, subject to regulatory restrictions. North Penn Bank may use the portion of the proceeds that it receives to fund new loans, establish or acquire new branches, invest in securities and expand its business activities. We intend to open a new branch in late 2005. We estimate that the total turn-key cost of the branch will be $1.0 million, which does not include the land acquisition cost of $563,000. We may also use the proceeds of the offering to diversify our business and acquire other companies, although we have no specific plans to do so at this time. | ||

| Trustees and Executive Officers Intend to Subscribe for Insider Shares (page 95) | We expect that our trustees and executive officers, together with their associates, will subscribe for 56,400 shares, which equals 7.21% of the shares that would be sold in the offering at the midpoint of the offering range and issued to our charitable foundation. Trustees and executive officers will pay the same $10.00 per share price as everyone else who purchases shares in the offering. Purchases by trustees and executive officers, together with their associates, will count toward the 636,863 offering minimum and will be purchased for investment purposes only. | |

7

| Market for North Penn Bancorp Common Stock (page 39) | After the shares begin trading, you may contact a firm offering investment services in order to buy or sell shares. We anticipate that our common stock will be quoted on the OTC Bulletin Board. The OTC Bulletin Board is a market with generally less liquidity and fewer buyers and sellers than the Nasdaq Stock Market. | |

| This may affect your ability to sell your shares on short notice, and the sale of a large number of shares at one time could temporarily depress the market price. For these reasons, among others, our stock should not be viewed as a short term investment. | ||

| Additionally, the aggregate purchase price of stock sold in the offering is based on an independent appraisal. After our shares begin trading, the marketplace will determine the price per share, which may be influenced by factors, such as prevailing interest rates, investor perceptions of North Penn Bancorp, economic conditions and the outlook for financial institutions. Price fluctuations may be unrelated to the operating performance of particular companies. In several cases, due to market volatility, shares of common stock of newly converted savings banks traded below the price at which the shares were sold in their initial public offering. We cannot assure you that, after the reorganization, the trading price of our common stock will be at or above $10.00. | ||

| North Penn Bancorp’s Dividend Policy (page 38) | After the reorganization, we intend to adopt a policy of paying regular cash dividends, but have not yet decided on the amount or frequency of payments or when payments may begin. Based upon our estimate of offering expenses and other assumptions described in “Pro Forma Data,” we expect to have between $5.9 million and $8.1 million in net proceeds, at the minimum and the maximum of the offering range, respectively, that, subject to annual earnings and expenses, we could potentially use to pay dividends. We cannot assure you that dividends will be paid. | |

| Possible Conversion of North Penn Mutual Holding Company to Stock Form (page 120) | In the future, North Penn Mutual Holding Company may convert from the mutual (meaning no stockholders) to capital stock form of organization, in a transaction commonly known as a “second-step conversion.” In a second-step conversion, depositors of North Penn Bank would have subscription rights to purchase common stock of North Penn Bancorp or its successor, and the public stockholders of North Penn Bancorp would be entitled to exchange their shares of common stock for an equal percentage of shares of the converted North Penn Mutual Holding Company, adjusted to reflect any assets owned by North Penn Mutual Holding Company. As a result of a second-step transaction, our stock’s liquidity would increase and we would have additional capital that could be used to facilitate business growth. In addition, as a fully converted stock holding company, we would have greater flexibility in structuring mergers and acquisitions. A second-step conversion would also eliminate the anti-takeover effect inherent in the mutual holding company structure because North Penn Mutual Holding Company would no longer have voting control because it would no longer exist. We have no current plan to undertake a second-step conversion transaction. | |

| Delivery of Prospectus | To ensure that investors receive a prospectus at least 48 hours before the offering deadline, we will not mail prospectuses any later than five days before such date or hand-deliver any prospectuses later than two days before that date. Stock order forms may only be distributed with or preceded by a prospectus. Subscription rights expire at 10:00 a.m., Eastern Time, on April 27, 2005, whether or not we have located each person entitled to such rights. | |

8

| Stock Information Center | If you have any questions regarding the offering or our reorganization, please call the Stock Information Center at (570) 983-0240, where registered representatives of Ryan Beck & Co., Inc. will be available to answer questions. You may also visit our Stock Information Center, which is located at our main office in Scranton, Pennsylvania, 216 Adams Avenue, Scranton, Pennsylvania. The Stock Information Center is open Monday through Friday, except for bank holidays, from 9:30 a.m. to 4:00 p.m., Eastern Time. Our branches willnot have offering materials and cannot accept completed order forms or proxy cards. | |

| How We Determined the Offering Range (page 107) | The offering range is based on an independent appraisal of North Penn Bank by FinPro, Inc., an appraisal firm experienced in appraising savings institutions. FinPro, Inc.’s estimate of our market value was based in part upon our financial condition and results of operations and the effect of the capital raised in this offering. FinPro, Inc.’s appraisal, dated as of November 29, 2004, estimated our pro forma market value on a fully converted basis with a foundation to be between $14,435,550 and $19,530,450, with a midpoint of $16,983,000. Subject to regulatory approval, our pro forma market value on a fully converted basis may increase to $22,460,020 without notice to you. Based on the sale of 44.1% of our common stock in the offering, FinPro, Inc. estimated the pro forma market value of our common stock being offered to be between $6,368,630 and $8,616,380, with a midpoint of $7,492,500. Subject to regulatory approval, the pro forma market value of our common stock being offered may increase to $9,908,830 without notice to you.

We cannot guarantee that anyone who purchases shares in the offering will be able to sell their shares at or above the $10.00 purchase price.

The Pennsylvania Department of Banking and the Federal Deposit Insurance Corporation will consider the appraisal and may require adjustments to the ratio and/or appraisal value.

The following table summarizes the fully converted pricing ratios as of November 29, 2004 and price to pro forma per share data for us. Fully converted equivalent ratios and data assume the sale of 100% of the North Penn Bancorp’s common stock to the public. See “Pro Forma Data” for a description of the assumptions that we used in making these calculations. | |

| Fully Converted Equivalent Pro Forma | |||||

Price To Core Earnings Per Share | Price To Tangible Book Value Per Share | ||||

Peer group company trading multiples | |||||

Average | 43.94x | 103.35 | % | ||

Median | 38.99x | 105.47 | % | ||

North Penn Bancorp upon issuance of 100% of its stock for the twelve months ended September 30, 2004 | |||||

Minimum | 40.00x | 73.42 | % | ||

Maximum | 52.63x | 81.10 | % | ||

9

| For a presentation of the mutual holding company pricing ratios (not on a fully converted basis), see “–Mutual Holding Company Pricing Ratios.” | ||

| Mutual Holding Company Pricing Ratios | Two measures that some investors use to analyze whether a stock might be a good investment are the ratio of the offering price to the issuer’s “book value” and the ratio of the offering price to the issuer’s annual core net income. FinPro, Inc., in preparing its appraisal, and our Board of Trustees, in approving the appraisal, considered these ratios, among other factors. Book value is the same as total equity and represents the difference between the issuer’s assets and liabilities. FinPro, Inc.’s appraisal also incorporates an analysis of a peer group of publicly traded mutual holding companies that FinPro, Inc. considered comparable to us.

The following table summarizes mutual holding company pricing ratios as of November 29, 2004, and price to pro forma per share data for us. See “Pro Forma Data” for a description of the assumptions that we used in making these calculations. | |

Price To Core Earnings Per Share | Price To Tangible Book Value Per Share | ||||

National mutual holding company trading multiples listed on the NYSE, NASDAQ, and AMEX | |||||

Average (1) | 54.38x | 255.52 | % | ||

Median (1) | 46.40x | 238.40 | % | ||

North Penn Bancorp upon sale of 44.1% of its stock for the nine months ended September 30, 2004 | |||||

Minimum | 39.47x | 113.51 | % | ||

Maximum | 50.00x | 132.63 | % | ||

North Penn Bancorp upon sale of 44.1% of its stock for the year ended December 31, 2003 | |||||

Minimum | 33.33x | 113.64 | % | ||

Maximum | 45.45x | 132.80 | % | ||

(1) The information for national mutual holding companies may not be meaningful for investors because it presents average and median information for mutual holding companies that may have issued a different percentage of their stock in their offerings than the 44.1% that we are offering. In addition, stock repurchases also affect the ratios to a greater or lesser degree depending upon repurchase activity. Additionally, many factors that historically have affected pricing for mutual holding companies may not impact our trading price. See “–After-Market Performance Information Provided By Independent Appraiser” and “Risk Factors – Risks Related to the Reorganization – As a result of the amount of capital we are raising, we expect our return on equity and our stock price performance to be negatively affected.” |

10

| After-Market Performance Information Provided by Independent Appraiser | As part of its appraisal of our pro forma market value, FinPro considered the after-market performance of “first step” mutual holding company offerings since January 1, 2001 through June 29, 2004. |

| Appreciation From Initial Offering Price | |||||||||||||||||

Issuer | Date of IPO | After 1 Day | After 1 Week | After 1 Month | After 3 Months | To November | |||||||||||

First Federal Financial Services, Inc. (1) | 06/29/04 | 15.0 | % | 22.5 | % | 35.0 | % | 35.0 | % | 50.0 | % | ||||||

Monadnock Community Bancorp, Inc. (2) | 06/29/04 | 3.8 | 2.5 | (3.1 | ) | (0.13 | ) | 25.0 | |||||||||

Wawel Savings Bank (2) | 04/01/04 | 29.5 | 25.0 | 12.5 | 25.0 | 15.0 | |||||||||||

Osage Federal Financial, Inc. (2) | 04/01/04 | 20.0 | 22.5 | 9.5 | 9.5 | 21.5 | |||||||||||

K-Fed Bancorp (3) | 03/31/04 | 34.9 | 30.0 | 15.1 | 29.0 | 52.2 | |||||||||||

Citizens Community Bancorp (2) | 03/30/04 | 23.7 | 32.5 | 17.5 | 18.5 | 50.0 | |||||||||||

Clifton Savings Bancorp, Inc. (3) | 03/04/04 | 22.5 | 37.5 | 32.9 | 24.0 | 25.8 | |||||||||||

Cheviot Financial Corp. (1) | 01/06/04 | 33.2 | 34.7 | 33.0 | 31.0 | 14.3 | |||||||||||

Flatbush Federal Bancorp, Inc. (2) | 10/21/03 | 63.8 | 54.4 | 60.6 | 60.0 | 45.6 | |||||||||||

ASB Holding Company (2) | 10/03/03 | 62.0 | 71.0 | 68.5 | 79.5 | 75.0 | |||||||||||

Minden Bancorp, Inc. (2) | 07/02/02 | 19.5 | 20.0 | 18.5 | 13.0 | 99.0 | |||||||||||

New England Bancshares, Inc. (2) | 06/04/02 | 23.0 | 24.0 | 24.0 | 23.0 | 98.0 | |||||||||||

Westfield Financial, Inc. (4) | 12/28/01 | 33.4 | 32.4 | 36.0 | 47.0 | 157.4 | |||||||||||

AJS Bancorp, Inc. (2) | 12/27/01 | 32.0 | 29.1 | 32.5 | 40.0 | 147.5 | |||||||||||

Charter Financial Corp. (GA)(3) | 10/17/01 | 42.5 | 52.5 | 74.1 | 121.0 | 308.2 | |||||||||||

Average | 27.2 | % | 28.4 | % | 27.1 | % | 37.0 | % | 67.3 | % | |||||||

| (1) | Quoted on the Nasdaq SmallCap Market. |

| (2) | Quoted on the OTC Electronic Bulletin Board. |

| (3) | Quoted on the Nasdaq National Market. |

| (4) | Listed on the American Stock Exchange |

This table is not intended to be indicative of how our stock may perform. Furthermore, this table presents only recent historic price performance and may not be indicative of future stock price performance of these companies. During the time period for which the data is provided, the thrift industry experienced strong returns which are, at least partially, attributable to the historically low interest rate environment, strong housing market and strong mortgage refinance market.Stock price performance is affected by many factors, including, but not limited to: general market and economic conditions; the interest rate environment; an active and liquid trading market for the stock; the amount of proceeds a company raises in its offering; and numerous factors relating to the specific company, including the experience and ability of management, historical and anticipated operating results, the nature and quality of the company’s assets, and the company’s market area. Before you make an investment decision, we urge you to carefully read this prospectus, including, but not limited to, the Risk Factors beginning on page 16.

You should be aware that, in certain market conditions, stock prices of thrift IPOs have decreased. For example, as the above table illustrates, after one month, the shares of one company traded below its initial offering price. We can give you no assurance that our stock will not trade below the $10.00 purchase price.

Possible Change in Offering Range (page 107) | FinPro, Inc.’s independent appraisal will be updated before the reorganization is completed. If the pro forma market value of the common stock being offered at that time is either below $6,368,630 or above $9,908,830, we will notify subscribers, who will each have the opportunity to confirm, modify or cancel their order, within a specified resolicitation period or else the order would be cancelled and funds returned promptly, with interest. If we are unable to sell at least the number of shares at the minimum of the offering range, as the range may be amended, the reorganization would be terminated and all orders would be cancelled and funds returned promptly with interest. |

11

Conditions to Completing the Reorganization | We are conducting the reorganization under the terms of our plan of reorganization. We cannot complete the reorganization and related offering unless:

• the plan of reorganization is approved by at least a majority of votes eligible to be cast by depositors of North Penn Bank;

• we sell at least the minimum number of shares offered; and

• we receive the final approval of the Pennsylvania Department of Banking, the Federal Deposit Insurance Corporation and the Federal Reserve Board to complete the reorganization and offering. | |

Benefits of the Reorganization to Management (page 90) | We intend to adopt the following benefit plans and employment agreements:

• Employee Stock Ownership Plan. We intend to establish an employee stock ownership plan that will purchase 8.0% of the sum of the shares sold in the offering plus shares issued to our charitable foundation. We will allocate these shares to our employees over a period of 10 years in proportion to their compensation. Non-employee directors are not eligible to participate in the employee stock ownership plan. We will incur additional compensation expense as a result of this plan. See “Pro Forma Data” for an illustration of the effects of this plan.

• Future Omnibus Stock Option Plan. We intend to implement an omnibus stock option plan no earlier than six months after the completion of the reorganization. Approval of this plan by a majority of the total votes eligible to be cast by our stockholders, other than by North Penn Mutual Holding Company, will be required if we present the plan to stockholders within one year of the reorganization subject to applicable regulations. Approval of this plan by a majority of the votes cast by our stockholders, including North Penn Mutual Holding Company, will be required if we present the plan to our stockholders more than a year from the date of the reorganization. Under this plan, we may award stock options and shares of restricted stock to key employees and directors. Shares of restricted stock, in an amount up to 4.0% of the sum of the shares sold in the offering plus shares issued to our charitable foundation, may be awarded at no cost to the recipient. Stock options, in an amount up to 10.0% of the sum of the shares sold in the offering plus shares issued to our charitable foundation, may be granted at an exercise price equal to 100% of the fair market value of our common stock on the option grant date. We will incur additional compensation expense as a result of this plan. See “Pro Forma Data” for an illustration of the effects of this plan. In addition, the Financial Accounting Standards Board, or FASB, recently issued a statement requiring companies to expense the cost of stock options granted to officers, directors and employees, effective for reports filed with the Securities and Exchange Commission after June 15, 2005. As a result, we will expense the cost of stock options granted under the stock-based incentive plan, and this will further increase our compensation costs and reduce our earnings. | |

12

• Employment Agreements. We intend to enter into an amended and restated three-year employment agreement with Frederick L. Hickman, our President and Chief Executive Officer and Thomas J. Dziak, our Executive Vice President and Senior Lending Officer. We also intend to enter into a two-year employment agreement with Thomas A. Byrne, our Senior Vice President for Commercial Lending and a one year employment agreement with Theresa Yocum, our Vice President and Stroudsburg Branch Manager. These agreements will provide for severance benefits if the executives are terminated following a change in control involving us, such as an acquisition of North Penn Bancorp. Based solely on current cash compensation and excluding any benefits that would be payable under any employee benefit plan, if a change in control occurred, and we terminated all officers covered by the employment agreements, the total payments due under the employment agreements would equal approximately $ 468,302, $224,357, $165,000 and $51,864, respectively.

The following table summarizes at the maximum of the offering range the total number and value of the shares of common stock that the employee stock ownership plan expects to acquire and the total value of all restricted stock awards and stock options that are expected to be available under the omnibus stock option plan. |

| Number of Shares to be Granted or Purchased | ||||||||

| At Maximum of Offering Range | As % of Shares Sold plus Shares issued to Foundation | Total Estimated Value of Grants (1)(2) | ||||||

Employee stock ownership plan | 71,991 | 8.0 | % | $ | 719,910 | |||

Restricted stock Awards | 35,995 | 4.0 | % | 359,950 | ||||

Stock options | 89,989 | 10.0 | % | 351,859 | ||||

Total | 197,975 | 22.0 | % | $ | 1,431,719 | |||

(1) Assumes the value of our common stock is $10.00 per share. Ultimately, the value of the grants will depend on the actual trading price of our common stock, which depends on numerous factors. There can be no assurance that our stock price will appreciate in the same manner as other mutual holding companies, if at all. See “Summary – After-Market Performance Information Provided by Independent Appraiser” and “Risk Factors – Risks Related to the Reorganization – As a result of the amount of capital we are raising, we expect our return on equity and our stock price performance to be negatively affected” for more information regarding factors that could negatively affect our stock appreciation. (2) The pro forma net income assumes that the options granted under the omnibus stock option plan will be expensed in accordance with SFAS No. 123R. The number of shares to be granted is 66,514 shares, 78,252 shares, 89,989 shares and 103,488 shares at the minimum, midpoint, maximum and maximum, as adjusted, respectively, of the offering range. The options are assumed to have a value of $3.91 per option, which was calculated using the Black-Scholes option pricing model. |

13

The assumptions used in the Black-Scholes option pricing model using the following assumptions: (i) the trading price on date of grant was $10.00 per share; (ii) exercise price is equal to the trading price on the date of grant; (iii) dividend yield of 0%; (iv) expected life of 10 years; (v) expected volatility of 16.72%; and (vi) risk-free interest rate of 4.13%. There is no market for the common stock of North Penn Bancorp, Inc. As such, the expected volatility was calculated based upon the historical performance of the SNL MHC Index. The foregoing assumptions are used for illustrating purposes and should not be considered indicative of expected performance of the stock. Changes in the assumptions used in the Black-Scholes option pricing model can materially impact the results. The assumptions were prepared based upon data available as of September 30, 2004. However, future market conditions could materially impact these assumptions going forward. There can be no assurance that the actual fair market value per share on the date of grant, and correspondingly the exercise price of the options, will be $10.00 per share. | ||

| Ultimately, the value of the grants will depend on the actual trading price of our common stock, which depends on numerous factors. The following table presents the total value of all shares to be available for restricted stock awards under the omnibus stock option plan, based on a range of market prices from $8.00 per share to $14.00 per share. The shares of restricted stock will not be awarded until at least six months after the completion of the reorganization. | ||

| Share Price | 26,605 Shares Awarded at Minimum of Offering Range | 31,300 Shares Awarded at Midpoint of Offering Range | 35,995 Shares Awarded at Maximum of Offering Range | 41,395 Shares Awarded at 15% above Maximum of Offering Range | |||||||||

| $ | 8.00 | $ | 212,840 | $ | 250,400 | $ | 287,960 | $ | 331,160 | ||||

| 10.00 | 266,050 | 313,000 | 359,950 | 413,950 | |||||||||

| 12.00 | 319,260 | 375,600 | 431,940 | 496,740 | |||||||||

| 14.00 | 372,470 | 438,200 | 503,930 | 579,530 | |||||||||

The Offering Will Not Be Taxable to Us or to Persons Receiving Subscription Rights (page 112) | As a general matter, the reorganization will not be a taxable transaction for purposes of federal or state income taxes to us or to persons who receive or exercise subscription rights, except to the extent, if any, that subscription rights are deemed to have fair market value on the date such rights are distributed or exercised. Our special counsel, Stevens & Lee, P.C., has issued an opinion to us that, among other items, for federal income tax purposes:

• no gain or loss will be recognized by us as a result of the reorganization;

• no gain or loss will be recognized by North Penn Bank depositors upon the issuance to them of deposit accounts in North Penn Bank immediately after the reorganization;

• assuming that subscription rights do not have any value, the tax basis to our depositors, who exercise subscription rights to purchase our common stock in the offering, will be the amount paid for our common stock, and the holding period for shares of common stock will begin on the date of completion of the offering.

• the holding period for shares of common stock purchased in the community offering or syndicated community offering will begin on the day after the date of the purchase. |

14

We have received an opinion from FinPro, Inc. stating that, pursuant to its valuation, FinPro, Inc., is of the opinion that subscription rights do not have any value. See “The Reorganization and Stock Offering – Material Income Tax Consequences.”

We have also received an opinion from our independent auditors, McGrail Merkel Quinn & Associates, stating that, assuming the reorganization does not result in any federal income tax liability to us, or our account holders, implementation of the plan of reorganization will not result in any Pennsylvania income tax liability to those entities or persons. See “The Reorganization and Stock Offering – Material Income Tax Consequences.” |

15

In addition to the other information in this document, you should consider carefully the following risk factors before purchasing North Penn Bancorp common stock.

Risks Related to Our Business

Our increased emphasis on commercial lending and the unseasoned nature of these loans may expose us to increased lending risks and could impact the level of our allowance for loan losses.

Since December 31, 2002, our commercial loan portfolio has increased $11.7 million, or 224% at September 30, 2004. These types of loans generally expose a lender to greater risk of non-payment and loss than one- to four- family residential mortgage loans because repayment of the loans often depends on the income stream of the borrower. These factors can be impacted by many variables including economic events beyond the borrowers control. Such loans typically involve larger loan balances to single borrowers or groups of related borrowers compared to one- to four- family residential mortgage loans. Also many of our commercial borrowers have more than one loan outstanding with us. Consequently, an adverse development with respect to one loan or one credit relationship can expose us to a significantly greater risk of loss compared to an adverse development with respect to a one- to four- family residential mortgage loan.

Because of our planned continued emphasis on commercial lending and the unseasoned nature of many of these loans, we may determine it necessary to increase the level of our allowance for loan losses. We make various judgments about the collectibility of our loans, including the creditworthiness of our borrowers and the value of the real estate and other assets serving as collateral for our loans. In determining the amount of the allowance for loan losses, we review our loans and our loan loss and delinquency experience, and we evaluate economic conditions. However, as a result of our recent expansion, a significant portion of our commercial loans are unseasoned, with the risk that these loans may not have had sufficient time to perform to properly indicate the potential magnitude of intrinsic losses. If our judgments are incorrect, our allowance for loan losses may not be sufficient to cover future losses, which will result in additions to our allowance through increased provisions for loan losses. In addition, bank regulators periodically review our allowance for loan losses and may require us to increase our provision for loan losses or recognize further loan charge-offs. Increased provisions for loan losses would increase our expenses and reduce our profits. Finally, during our recent expansion, we have also experienced a historically low interest rate environment. Our unseasoned adjustable rate loans have not, therefore, been subject to a rising interest rate environment which could cause them to adjust to their maximum interest rate level. Such an increase could increase collection risks resulting from potentially higher payment obligations by the borrowers.

Our emphasis on indirect automobile loans may expose us to increased lending risks and could impact the level of our allowance for loan losses.

Since 2002, North Penn Bank has actively originated indirect automobile loans. At September 30, 2004, such loans approximated $7.0 million, or 12%, of the total loan portfolio. Though we have not recently experienced a greater degree of default or an inability to resell the collateral of these loans, indirect automobile loans are generally considered to have a greater degree of lending risk than traditional one- to four- family residential lending. Indirect automobile loans are secured by new or used automobiles, which depreciate rapidly. Additionally, there is generally no recourse against the automobile dealer in the event of a default by the borrower. We also rely on the dealers to provide accurate information to us and accurate disclosures to borrowers. We seek to mitigate these risks by dealing only with automobile dealers with whom our senior lending officer has had a long-standing relationship. Although we do not anticipate a significant increase in the size of this portfolio, we anticipate that this portfolio will continue to be a significant percentage of our total loan portfolio. Because of these risks, we could experience an increase in non-performing loans and provisions for loan losses. See“Our Business – Lending Activities – Consumer Loans.”

16

Increases in market rates of interest could adversely affect our profits and stockholders’ equity.

At September 30, 2004, North Penn Bank owned approximately $26.5 million of marketable securities available for sale, which consisted of $14.3 million of investment securities and $12.2 million of mortgage-backed securities. Generally accepted accounting principles require that these securities be carried at fair value on the consolidated balance sheet. Unrealized gains or losses on these securities, that is, the difference between the fair value and the amortized cost of these securities, is reflected in stockholders’ equity, net of deferred taxes. As of September 30, 2004, North Penn Bank’s available for sale marketable securities portfolio had a net unrealized gain, net of taxes, of $50 thousand, which resulted in an increase in stockholders’ equity. However, if interest rates increase, the fair value of North Penn Bank’s available for sale marketable securities is likely to decrease, which would not affect recorded earnings but would reduce stockholders’ equity.

Interest rates are at historically low levels, but short-term rates have risen recently. If interest rates continue to rise, our net interest income likely would be reduced since, due to the generally shorter terms of interest-bearing liabilities, interest expense paid on interest-bearing liabilities, such as deposits and borrowings, increase more quickly than interest income earned on interest-earning assets, such as loans and investments. In addition, rising interest rates may hurt our income because they may reduce the demand for new loans, and refinance loans. Also, the interest rate spread and net interest margin could be compressed, which would have a negative effect on our profitability until our loan portfolio reprices with higher rates. Rising rates will also result in increased rates on existing adjustable rate loans, which could increase collection risks as a result of higher payment obligations by our borrowers.

If we do not achieve profitability on new branches, the new branches may negatively impact our earnings.

We have not expanded our branch network for a number of years. However, we intend to pursue opportunities to pursue such expansion, as well as to upgrade our current branch facilities. Currently, we have plans to open a new branch in late 2005. We cannot assure you that our this branch expansion strategy and our branch upgrading will be accretive to our earnings, or that it will be accretive to earnings within a reasonable period of time. Numerous factors contribute to the performance of a new branch, such as a suitable location, qualified personnel and an effective marketing strategy. Additionally, it takes time for a new branch to generate significant deposits and make sufficient loans to produce enough income to offset expenses, some of which, like salaries and occupancy expense, are relatively fixed costs. In addition to branch employees, we will hire lending and other employees to support our expanded infrastructure.

Strong competition within our market area could hurt our profits and slow growth.

Although we consider ourselves competitive in Northeastern Pennsylvania, which we consider our market area, we face intense competition both in making loans and attracting deposits. Price competition for loans and deposits might result in us earning less on our loans and paying more on our deposits, which reduces net interest income. Some of the institutions with which we compete have substantially greater resources and lending limits than we have and may offer services that we do not provide. We expect competition to increase in the future as a result of legislative, regulatory and technological changes and the continuing trend of consolidation in the financial services industry. Our profitability depends upon our continued ability to compete successfully in our market area.Our market area has traditionally consisted of the Scranton area. Scranton has been a low-growth area with an aging population. In 1989, we opened a branch office in Stroudsburg which has experienced strong population growth in recent years and we plan to open an additional branch office in Effort, Pennsylvania. Our ability to successfully penetrate this fast-growing market will impact our growth and profitability plans. For more information about our market area and the competition we face, see“Our Business – Market Area”and“Our Business – Competition.”

We have broad discretion in allocating the proceeds of the offering. Our failure to effectively utilize such proceeds would reduce our profitability.

We intend to contribute approximately 50% of the net proceeds of the offering to North Penn Bank. We expect to use a portion of the net proceeds to fund the employee stock ownership plan’s purchases of shares in the offering and to capitalize North Penn Mutual Holding Company. North Penn Bancorp may use the remaining net

17

proceeds to pay dividends to shareholders, repurchase common stock, purchase investment securities, finance the acquisition of other financial institutions or other businesses that are related to banking, or for other general corporate purposes. North Penn Bank may use the proceeds it receives to fund new loans, purchase investment securities, establish or acquire new branches, acquire financial institutions or other businesses that are related to banking or for general corporate purposes. We have not allocated specific amounts of proceeds for any of these purposes, and we will have significant flexibility in determining how much of the net proceeds we apply to different uses and the timing of such applications. Our failure to utilize these funds effectively would reduce our profitability.

We operate in a highly regulated environment and we may be adversely affected by changes in laws and regulations.

We are subject to extensive government regulation, supervision and examination. Such regulation, supervision and examination govern the activities in which we may engage, and is intended primarily for the protection of the deposit insurance fund and our depositors. Regulatory authorities have extensive discretion in their supervisory and enforcement activities, including the imposition of restrictions on our operations, the classification of our assets and determination of the level of our allowance for loan losses. Any change in such regulation and oversight, whether in the form of regulatory policy, regulations, legislation or supervisory action, may have a material impact on our operations.

Risks Related to the Reorganization

As a result of the amount of capital we are raising, we expect our return on equity and our stock price performance to be negatively affected.

We are raising net proceeds of up to $8.1 million at the maximum of the offering range. The amount of capital that we are raising may have several consequences, including the following:

| • | Return on equity will decline. Return on equity, which equals net income divided by average equity, is a ratio that many investors use to compare the performance of a particular company with other companies. For the nine months ended September 30, 2004, our annualized return on average equity was 4.95%. For the year ended December 31, 2003, our return on average equity was 5.00%. The net proceeds from the reorganization will significantly increase our equity capital, which will further decrease our return on equity, which on a pro forma basis at the midpoint of the offering is 2.81% for the nine months ended September 30, 2004 (annualized) and 2.97% for the year ended December 31, 2003 compared to a 5.12% median for our peer group. It will take time for us to fully use the new capital in our business operations to increase net income and improve our return on equity. Consequently, you should not expect a competitive return on equity in the near future. |

| • | Stock price may decline.Failure to achieve a competitive return on equity might make an investment in our common stock unattractive to some investors and might cause our common stock to trade at lower prices than comparable companies with higher returns on equity. See “Pro Forma Data” for an illustration of the financial impact of this offering. |

Additional public company and annual stock employee compensation and benefit expenses following the reorganization will reduce our profitability and stockholders’ equity.

Following the reorganization, our noninterest expense will increase as a result of the financial accounting, legal and various other additional expenses usually associated with operating as a public company, which will adversely affect our profitability and stockholders’ equity. Costs of preparing reports for shareholders and the Securities and Exchange Commission will cause our expenses to be higher than they would be if we did not conduct the stock offering and become a public company. In addition, we will recognize additional annual material employee compensation and benefit expenses stemming from the shares granted to employees and executives under new benefit plans, which we will establish, subject to our stockholders’ approval. We cannot predict the actual amount of these new expenses because applicable accounting practices require that they be based on the fair market value of the shares of common stock at specific points in the future. We would recognize expenses for our

18

employee stock ownership plan when shares are committed to be released to participants’ accounts and would recognize expenses for restricted stock awards over the vesting period of the awards. These compensation and benefit expenses in the first year following the reorganization have been estimated to be approximately $510,000 at the maximum of the offering range as set forth in the pro forma financial information under “Pro Forma Data” assuming the $10.00 per share offering price as fair market value. Actual expenses, however, may be higher or lower, depending on the then-prevailing price of our common stock. In addition, changes in accounting guidelines have required us to recognize expenses relating to stock option grants. See“Pro Forma Data” and“Our Management – Benefit Plans.”

Issuance of shares for benefit programs may dilute your ownership interest.

We intend to adopt an omnibus stock option plan following the reorganization. If our stockholders approve the new omnibus stock option plan, we intend to issue restricted stock awards and stock options to our officers and directors through this plan. If the restricted stock awards under the omnibus stock option plan are funded from authorized but unissued stock, your ownership interest in shares held by persons other than North Penn Mutual Holding Company could be diluted by up to approximately 1.8%, assuming awards of common stock equal to 4.0% of the sum of the shares to be sold in the reorganization, plus shares issued to our charitable foundation, are awarded under the plan. If the shares issued upon the exercise of stock options under the omnibus stock option plan are issued from authorized but unissued stock, your ownership interest in shares held by persons other than North Penn Mutual Holding Company could be diluted by up to approximately 4.4% assuming stock option grants equal to 10.0% of the sum of the shares sold in the offering plus shares issued to our charitable foundation, are granted under the plan. See “Pro Forma Data”and“Our Management – Benefit Plans.”

North Penn Mutual Holding Company will own a majority of our common stock and will be able to exercise voting control over most matters put to a vote of stockholders, including preventing sale or merger transactions you may like or a second-step conversion by North Penn Mutual Holding Company.

Public stockholders collectively will own a minority of the outstanding shares of North Penn Bancorp’s common stock. North Penn Mutual Holding Company will own a majority of our common stock and, through its Board of Directors, will be able to exercise voting control over most matters put to a vote of stockholders. The same directors and officers will manage North Penn Bancorp, North Penn Bank (in stock form) and North Penn Mutual Holding Company. As a Pennsylvania state-chartered mutual holding company, the Board of Directors of North Penn Mutual Holding Company must ensure that the interests of depositors of North Penn Bank are represented and considered in matters put to a vote of stockholders of North Penn Bancorp. Therefore, the votes cast by North Penn Mutual Holding Company may not be in your personal best interests as a stockholder. For example, North Penn Mutual Holding Company may exercise its voting control to prevent a sale or merger transaction in which stockholders could receive a premium for their shares, prevent a second-step conversion transaction by North Penn Mutual Holding Company or defeat a stockholder nominee for election to the Board of Directors of North Penn Bancorp. The matters as to which stockholders other than North Penn Mutual Holding Company will be able to exercise voting control are limited and include any proposal to implement an omnibus stock option plan.

In addition, North Penn Bancorp’s directors, executive officers and their associates are expected to purchase approximately 56,400 shares in the offering, which represents 8.48%, 7.21%, 6.27% and 5.45% at the minimum, midpoint, maximum and maximum, as adjusted of the offering range, respectively, including shares issued to North Penn Mutual Holding Company. Furthermore, if stockholders of North Penn Bancorp approve the omnibus stock option plan, and if all restricted stock awards are awarded and all options reserved under the stock option plan are awarded and exercised, insider ownership would increase. See “Our Management – Executive Compensation,” and “Management – Benefit Plans.”

Our stock price may suffer from anti-takeover provisions and our mutual holding company structure that may impede potential takeovers.

Anti-Takeover Provisions in our Articles of Incorporation and Bylaws. Provisions in our corporate documents, as well as regulations restricting takeovers after the reorganization, may make it difficult and expensive to pursue a tender offer, change in control or takeover attempt that our board of directors opposes. As a result, you may not have an opportunity to participate in such a transaction, and the trading price of our stock may not rise to

19

the level of other institutions that are more vulnerable to hostile takeovers. Anti-takeover provisions contained in our corporate documents include:

| • | Restrictions on acquiring more than 10% of our common stock by any person other than North Penn Mutual Holding Company limitations on the voting rights of shares held in excess of that amount; |

| • | The election of members of the board of directors to staggered three-year terms; |

| • | The absence of cumulative voting by stockholders in elections of directors; |

| • | Provisions restricting the calling of special meetings of stockholders; and |

| • | Our ability to issue up to 20,000,000 shares of preferred stock and up to 80,000,000 shares of common stock without stockholder approval. |

See “Restrictions on Acquisition of North Penn Bancorp” for a description of anti-takeover provisions in our corporate documents and applicable regulations.

Our stock price may decline when trading commences.

We cannot guarantee that if you purchase shares in the offering that you will be able to sell them at or above the $10.00 offering price. After the shares of our common stock begin trading, the trading price of the common stock will be determined by the marketplace, and will be influenced by investor perceptions of North Penn Bancorp and other factors outside of our control, including prevailing interest rates, and general industry, geopolitical and economic conditions. Publicly traded stocks, including stocks of financial institutions, have recently experienced substantial market price volatility. These market fluctuations might not be related to the operating performance of particular companies whose shares are traded.

There may be a limited market for our common stock, which may lower our stock price.

We expect our shares of common stock will be quoted on the OTC Bulletin Board. We cannot guarantee that the shares will be regularly traded. If an active trading market for our common stock does not develop, you may not be able to sell all of your shares of common stock on short notice and the sale of a large number of shares at one time could temporarily depress the market price.

Risks Related to the Formation of Our Foundation

The contribution to the North Penn Charitable Foundation will hurt our profits for fiscal year 2005 and means that a stockholder’s ownership interest will be up to 2% less after the contribution.

We intend to contribute 2% of the shares of our common stock issued in the reorganization to the North Penn Charitable Foundation. This contribution will be an additional operating expense and will reduce net income during the fiscal year in which the North Penn Charitable Foundation is established, which is expected to be the year ending December 31, 2005.Based on the pro forma assumptions, the contribution to the North Penn Charitable Foundation would reduce net earnings by approximately $255,000 at the midpoint of the offering range, after tax, in fiscal year 2005. In addition, purchasers of shares in the offering will have their ownership and voting interests diluted by up to 2% at the close of the offering when we contribute the shares of our common stock to the North Penn Charitable Foundation. For a further discussion regarding the effect of the contribution to the charitable foundation, see“Pro Forma Data”and“Comparison of Independent Valuation and Pro Forma Financial Information With and Without the Foundation.”

Our contribution to the North Penn Charitable Foundation may not be tax deductible, which could hurt our profits.

We believe that our contribution to the North Penn Charitable Foundation, valued at $432,670 at the midpoint of the offering range, pre-tax, will be deductible for federal income tax purposes. However, we do not have any assurance that the Internal Revenue Service will grant tax-exempt status to the foundation and, accordingly, that the after tax expense would be approximately $255,000. If the contribution is not deductible, we would not receive any tax benefit from the contribution. In addition, even if the contribution is tax deductible, we may not have sufficient profits to be able to use the deduction fully.

20

Failure to approve the North Penn Charitable Foundation may materially affect our pro forma market value, which may delay the completion of the reorganization.

The establishment and funding of the foundation as part of the reorganization is subject to the approval of our depositors. If our depositors approve the reorganization, but not the foundation, we may determine to complete the reorganization without the establishment of the foundation and may do so without amending the plan of reorganization or obtaining any further vote of our depositors. FinPro, Inc., which performed the appraisal of us on which this offering is based, has informed us that our value would be greater if we did not form the charitable foundation and fund it with shares of our common stock. Therefore, if our depositors do not approve the foundation, our pro forma market value will increase. If our pro forma market value increases above $22,460,020 for any reason, all subscribers will be resolicited and given the chance to change or cancel their orders. A resolicitation would delay the completion of the stock offering.

21

A Warning About Forward-Looking Statements

This prospectus contains forward-looking statements, which can be identified by the use of words such as “believes,” “expects,” “anticipates,” “estimates” or similar expressions. Forward-looking statements include:

| • | statements of our goals, intentions and expectations; |

| • | statements regarding our business plans, prospects, growth and operating strategies; |

| • | statements regarding the quality of our loan and investment portfolios; and |

| • | estimates of our risks and future costs and benefits. |

These forward-looking statements are subject to significant risks and uncertainties. Actual results may differ materially from those contemplated by the forward-looking statements due to, among others, the following factors:

| • | general economic conditions, either nationally or in our market area, that are worse than expected; |

| • | changes in the interest rate environment that reduce our interest margins or reduce the fair value of financial instruments |

| • | increased competitive pressures among financial services companies; |

| • | changes in consumer spending, borrowing and savings habits; |

| • | legislative or regulatory changes that adversely affect our business; |

| • | adverse changes in the securities markets; and |

| • | changes in accounting policies and practices, as may be adopted by the bank regulatory agencies or the Financial Accounting Standards Board or the Public Company Accounting Oversight Board. |

Forward-looking statements that we make in this prospectus and in other public statements we make may turn out to be wrong because of inaccurate assumptions we might make, because of the factors illustrated above or because of other factors that we cannot foresee. Consequently, no forward-looking statement can be guaranteed.

22

Selected Financial and Other Data

The summary financial information presented below is derived in part from the financial statements of North Penn Bank. The following is only a summary and you should read it in conjunction with the financial statements and notes beginning on page F-1. The information at December 31, 2003 and for the years ended December 31, 2003 and 2002 is derived in part from the audited consolidated financial statements of North Penn Bank that appear in this prospectus. The information at September 30, 2004 and 2003 and for the nine months ended September 30, 2004 and 2003 was not audited, but, in the opinion of management, reflects all adjustments necessary for a fair presentation. No adjustments were made other than normal recurring entries. The results of operations for the nine months ended September 30, 2004 are not necessarily indicative of the results of operations that may be expected for the entire year.

At September 30, 2004 | At December 31, | ||||||||

| 2003 | 2002 | ||||||||

| (In thousands) | |||||||||

Financial Condition Data: | |||||||||

Total assets | $ | 93,444 | $ | 92,199 | $ | 91,265 | |||

Cash and cash equivalents | 659 | 3,068 | 7,312 | ||||||

Securities held-to-maturity | 1,097 | 2,437 | 4,423 | ||||||

Securities available-for-sale | 26,506 | 31,530 | 16,318 | ||||||

Loans receivable, net | 58,991 | 49,021 | 58,248 | ||||||

Deposits | 77,910 | 79,180 | 76,256 | ||||||

FHLB advances | 7,240 | 5,000 | 7,000 | ||||||

Total equity | 7,699 | 7,683 | 7,607 | ||||||

23

For the Nine Months Ended | For the Year Ended December 31, | |||||||||||

| 2004 | 2003 | 2003 | 2002(1) | |||||||||

Operating Data: | ||||||||||||

Interest and dividend income | $ | 3,590 | $ | 3,880 | $ | 5,042 | $ | 5,834 | ||||

Interest expense | 1,488 | 1,800 | 2,336 | 2,847 | ||||||||

Net interest income | 2,102 | 2,080 | 2,706 | 2,987 | ||||||||

Provision for loan losses | — | 15 | 15 | 40 | ||||||||

Net interest income after Provision for loan losses | 2,102 | 2,065 | 2,691 | 2,947 | ||||||||

Noninterest income | 328 | 321 | 469 | 286 | ||||||||

Noninterest expense | 2,042 | 1,831 | 2,554 | 2,581 | ||||||||

Income before provision for income taxes | 388 | 555 | 606 | 652 | ||||||||

Provision for income taxes | 103 | 182 | 206 | 259 | ||||||||

Net income | $ | 285 | $ | 373 | $ | 400 | $ | 393 | ||||

| (1) | Noninterest expense includes a $160 thousand penalty for prepayment of $4.1 million in FHLB borrowings. |

24

At or For the Nine Months Ended | At or For the Year Ended December 31, | |||||||||||

| 2004 | 2003 | 2003 | 2002(1) | |||||||||

Performance Ratios (2): | ||||||||||||

Return on average assets (net income divided by average total assets) | 0.41 | % | 0.54 | % | 0.43 | % | 0.43 | % | ||||

Return on average equity (net income divided by average equity) | 4.95 | 6.25 | 5.00 | 5.30 | ||||||||

Interest rate spread (3) | 3.06 | 3.00 | 2.92 | 3.17 | ||||||||

Net interest margin (4) | 3.21 | 3.20 | 3.12 | 3.40 | ||||||||

Noninterest expense to average assets | 2.93 | 2.65 | 2.77 | 2.80 | ||||||||

Efficiency ratio (5) | 84.17 | 75.49 | 79.86 | 78.86 | ||||||||

Average interest-earning assets to average interest-bearing liabilities | 106.74 | 107.25 | 107.21 | 106.87 | ||||||||

Capital Ratios: | ||||||||||||

Average equity to average assets | 8.27 | % | 8.64 | % | 8.62 | % | 8.08 | % | ||||

Equity to assets at period end | 8.24 | 8.78 | 8.33 | 8.34 | ||||||||

Asset Quality Ratios: | ||||||||||||

Allowance for loan losses as a percent of total loans | 1.61 | % | 1.98 | % | 1.97 | % | 1.72 | % | ||||

Allowance for loan losses as a percent of nonperforming loans | 90.30 | 112.67 | 99.39 | 116.31 | ||||||||

Net charge-offs to average outstanding loans during the period | 0.03 | .06 | .09 | .02 | ||||||||

Nonperforming loans as a percent of total loans | 1.79 | 1.76 | 1.98 | 1.48 | ||||||||

Nonperforming assets and troubled debt restructurings as a percent of total assets | 1.19 | 1.01 | 1.17 | 1.30 | ||||||||

Other Data: | ||||||||||||

Number of: | ||||||||||||

Full service customer service facilities | 4 | 4 | 4 | 4 | ||||||||

| (1) | Noninterest expense for 2004 includes a $160 thousand penalty for prepayment of $4.1 million in FHLB borrowings. |

| (2) | Performance ratios for the nine months ended September 30, 2004 and 2003 are annualized. |

| (3) | Represents the difference between the weighted average yield on average interest-earning assets and the weighted average cost of interest-bearing liabilities. |

| (4) | Represents net interest income as a percent of average interest-earning assets. |