Exhibit 99.2

The document following this cover page consists of extracts from a preliminary offering circular dated 9 November 2009. No part of this document constitutes an offer to sell, or a solicitation of an offer to purchase, any securities referenced therein. The definitive terms of the transaction referenced therein will be described in a final version of the offering circular.

PRESENTATION OF FINANCIAL AND OTHER INFORMATION

Financial Data

The audited consolidated financial information as of and for the years ended 31 December 2006, 2007 and 2008 included or incorporated by reference herein has been prepared in accordance with International Financial Reporting Standards ("IFRS"), as adopted for use in the European Union and IFRS as issued by the International Accounting Standards Board (the "IASB"). The unaudited condensed consolidated financial information as of and for the nine-month periods ended 30 September 2008 and 2009 included or incorporated by reference herein has been prepared on a basis consistent with IFRS and in accordance with International Accounting Standards ("IAS") 34, "Interim Financial Reporting". Our consolidated financial statements are presented in US dollars.

In addition, this offering circular includes unaudited consolidated financial information as of and for the twelve-month period ended 30 September 2009. This information has been calculated by taking the results of operations for the nine-month period ended 30 September 2009 and adding it to the difference between the results of operations for the year ended 31 December 2008 and the nine-month period ended 30 September 2008.

This offering circular also includes unaudited pro forma consolidated financial information which has been adjusted to reflect the impact of certain Transactions (as defined in "Summary—The Transactions") on our results of operations and financial position as of and for the twelve-month period ended 30 September 2009. This unaudited pro forma consolidated financial information has been prepared for illustrative purposes only, and does not purport to represent what our actual results of operations or financial position would have been had the Transactions occurred on the dates specified nor does it purport to project our results of operations or financial position at any future date. The unaudited pro forma consolidated financial information set forth in this offering circular is based upon available information and certain assumptions and estimates that we believe are reasonable.

Some of the financial information appearing or incorporated by reference in this offering circular has been rounded and, as a result, the totals of the information presented, or incorporated by reference, in this offering circular may vary slightly from the actual arithmetic totals of such information.

Currency

In this offering circular, the following currency terms are used:

| • | "GBP", "pounds sterling", "sterling" or "£" refers to the lawful currency of Great Britain; |

| • | "US dollar" "USD" or "US$" refers to the lawful currency of the United States; |

| • | "EUR", "Euro" or "€" refers to the single currency of the participating member states in the Third Stage of the European Economic and Monetary Union of the Treaty Establishing the European Union, as amended from time to time; and |

| • | "C$" refers to the lawful currency of Canada. |

Non-IFRS Financial Measures

EBITDA

EBITDA (defined as profit for the period before net interest payable, taxation, depreciation and amortisation) and the related ratios presented, or incorporated by reference, in this offering circular are supplemental measures of our performance and liquidity that are not required by, or presented in accordance with IFRS. Furthermore, EBITDA is not a measurement of our financial performance under IFRS and should not be considered as an alternative to net income, operating income or any other performance measures derived in accordance with IFRS.

We believe EBITDA, among other measures, facilitates operating performance comparisons from period to period and management decision making. It also facilitates operating performance comparisons from company to company. EBITDA as a performance measure eliminates potential differences caused by variations in capital structures (affecting interest expense), tax positions (such as the impact on periods or companies of changes in effective tax rates or net operating losses) and the age and book depreciation of tangible assets (affecting relative depreciation expense). We also present EBITDA because we believe it is frequently used by securities analysts, investors and other interested parties in evaluating similar companies, the vast majority of which present EBITDA when reporting their results.

vii

Nevertheless, EBITDA has limitations as an analytical tool, and you should not consider it in isolation from, or as a substitute for analysis of, our results of operations, as reported under IFRS. Some of these limitations are:

| • | it does not reflect our cash expenditures or future requirements for capital expenditures or contractual commitments; |

| • | it does not reflect changes in, or cash requirements for, our working capital needs; |

| • | it does not reflect the significant interest expense, or the cash requirements necessary to service interest or principal payments, on our debt; |

| • | although depreciation and amortisation are non-cash charges, the assets being depreciated and amortised will often have to be replaced in the future, and EBITDA does not reflect any cash requirements for such replacements; |

| • | it is not adjusted for all non-cash income or expense items that are reflected in our statements of cash flows; and |

| • | other companies in our industry may calculate these measures differently than we do, limiting their usefulness as a comparative measure. |

As a result of these limitations, EBITDA should not be considered as a measure of discretionary cash available to us to invest in the growth of our business. We compensate for these limitations by relying primarily on our IFRS results and using EBITDA measures only supplementally. See "Operating and Financial Review" and the consolidated financial statements incorporated by reference in this offering circular.

Free Cash Flow

We define free cash flow ("FCF") as cash generated from operations less capital expenditure, capitalised operating costs, net interest and cash tax payments. Other companies may define FCF differently and, as a result, our measure of FCF may not be directly comparable to the FCF of other companies.

FCF is a supplemental measure of our performance and liquidity under IFRS that is not required by, or presented in accordance with IFRS. Furthermore, FCF is not a measurement of our performance or liquidity under IFRS and should not be considered as an alternative to net income and operating income as a measure of our performance and net cash generated from operating activities as a measure of our liquidity, or any other performance measures derived in accordance with IFRS.

We believe FCF is an important financial measure for use in evaluating our financial performance and liquidity, which measures our ability to generate additional cash from our business operations. We believe it is important to view FCF as a measure that provides supplemental information to our entire statement of cash flows. See "Operating and Financial Review" and the consolidated financial statements incorporated by reference in this offering circular.

Net Borrowings

We define net borrowings ("Net Borrowings") as total borrowings less cash and cash equivalents. We use Net Borrowings as a part of our internal debt analysis. We believe that Net Borrowings is a useful measure as it indicates the level of borrowings after taking account of the financial assets within our business that could be utilised to pay down the outstanding borrowings. See "Operating and Financial Review" and the consolidated financial statements incorporated by reference in this offering circular.

Net External Debt

We define net external debt ("Net External Debt") as Net Borrowings less outstanding borrowings under the Subordinated Intercompany Shareholder Funding Loan (as defined herein) and any other intercompany loans. The Subordinated Intercompany Shareholder Funding Loan is subordinated to all other creditors of Inmarsat Group Limited, has no fixed maturity and has interest payable only upon repayment of the principal amount of the Subordinated Intercompany Shareholder Funding Loan. For more information, see "Description of Certain Financing Arrangements—Subordinated Intercompany Shareholder Funding Loan".

viii

This summary highlights selected information about this offering and us. This summary is not complete and does not contain all the information that may be important to you. You should read the entire offering circular carefully, including the financial information and the related notes thereto incorporated by reference herein, and the risks of investing in the Notes in the section entitled "Risk Factors" before making an investment decision.

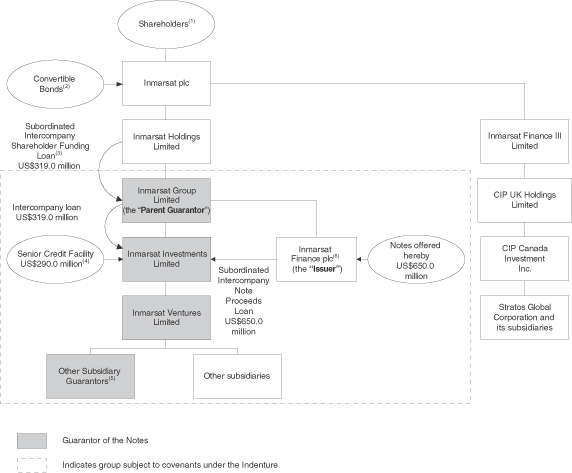

In this offering circular, references to "we," "us" and "our" are to Inmarsat Group Limited and its subsidiaries (including Inmarsat Finance plc). References to the "Issuer" are to Inmarsat Finance plc, the issuer of the Notes. References to the "Parent Guarantor" are to Inmarsat Group Limited. References to Inmarsat plc are to our ultimate parent company. Please refer to the Summary Corporate and Financial Structure chart on page 9 for more information on our corporate structure.

Please refer to the section entitled "Glossary of Terms" for a glossary of certain defined and technical terms relating to our business and used in this offering circular.

Business Overview

We believe that we are the leading provider of global mobile satellite communications services ("MSS"), providing data and voice connectivity to end-users worldwide. We have over 30 years of experience in designing, launching and operating our satellite-based network. With a fleet of 11 owned and operated geostationary satellites, we provide a comprehensive portfolio of global MSS for use at sea, on land and in the air. We estimate based on market share, that we have the leading MSS position in both the maritime and aeronautical sectors. Our services include voice and broadband data, which support safety communications as well as standard office applications, such as e-mail, internet, secure virtual private network ("VPN") access and videoconferencing. Our revenues, operating profit and EBITDA for the twelve-month period ended 30 September 2009 were US$673.9 million, US$301.2 million and US$477.1 million, respectively.

We have a successful launch and operating record. We have launched three generations of satellites and have never experienced a satellite failure either upon launch or in orbit. Our current fleet of satellites includes three Inmarsat-2 satellites, launched in the early 1990s, five Inmarsat-3 satellites, launched between 1996 and 1998, and three Inmarsat-4 satellites, launched in March and November 2005 and August 2008. Our Inmarsat-2 satellites have remained in commercial operation beyond their original design lives and we expect a similar experience with our Inmarsat-3 satellites. We currently expect that the last of our Inmarsat-2 satellites will be in commercial operation until 2014, and expect that the last of our Inmarsat-3 satellites will be in commercial operation until 2018. Each of our Inmarsat-4 satellites is up to 60 times more powerful, and has up to 16 times more communications capacity than an Inmarsat-3 satellite and the Inmarsat-4 satellites extend the commercial life of our satellite fleet to beyond 2020.

Our Inmarsat-2 and Inmarsat-3 satellites are used to offer our existing and evolved services ("Existing and Evolved Services"), which include all of our services other than broadband services and handheld satellite phone services ("SPS"). Our Inmarsat-4 satellites serve as the platform for our broadband services and our SPS and planned handheld global satellite phone service ("GSPS"), which we currently expect to launch in the second quarter of 2010, as well as provide continuity for our Existing and Evolved Services.

Data rates for our services have increased with each satellite generation. Our Existing and Evolved Services are available at transmission rates of up to 128 kbps, although higher rates are possible where multiple terminals are used in conjunction with channel bonding equipment. Our broadband services include our broadband global area network ("BGAN") service to the land mobile sector, our FleetBroadband service to the maritime sector and our SwiftBroadband service to the aeronautical sector. Our Inmarsat-4 satellites provide BGAN service at transmission rates of up to 492 kbps, FleetBroadband service at transmission rates of up to 432 kbps and SwiftBroadband service at transmission rates of up to 432 kbps. Our broadband services support higher-bandwidth applications, including, videoconferencing, live videostreaming and large file transfer, together with standard office applications such as e-mail, internet, secure local area network ("LAN") services access and voice telephony. These services have the same characteristics that our end-users have historically enjoyed, including reliability, ease of use and security, and are supported by terminals that are smaller, more portable and less expensive than the terminals used to access our Existing and Evolved Services.

1

We sell the majority of our services on a wholesale on-demand basis via a well-established, global network of distribution partners, which provide our services to end-users, either directly or indirectly through service providers. Our global network of 32 distribution partners and approximately 400 service providers who are present in over 100 countries on six continents provide our services to end-users worldwide. Our distribution partners are affiliated with some of the largest communications companies in the world, including KDDI and Singtel, and also include other significant distribution partners, such as Stratos Global Corporation ("Stratos") (which is indirectly wholly-owned by Inmarsat plc) and Vizada Satellite Communications ("Vizada") (formed by a merger of France Telecom Mobile Satellite Communications and Telenor Satellite Services). We continue to target and evaluate new distribution opportunities as they arise. Pursuant to our new distribution agreements which we entered into in April 2009 (the "Distribution Agreements"), we charge our distribution partners wholesale rates, based on duration or volume of data transmitted or length of voice call according to the types of services they distribute to end-users. In addition, a number of large end-users, such as the U.S. Navy, lease MSS capacity from us through our distribution partners.

Key Strengths

We believe that we are the leader in the global mobile satellite communications industry, with leading positions in the maritime, land mobile and aeronautical sectors. The following key strengths enhance our position:

| • | Unique Global Communications Network. We own and operate a fleet of 11 geostationary satellites, including three recently launched Inmarsat-4 satellites, all of which use the L-band spectrum, which is suited to mobile communications, to provide a comprehensive portfolio of on-demand and leased data and voice services on a global basis. We have global spectrum rights which we believe would be difficult for any new market entrant to replicate. Each of our Inmarsat-4 satellites is up to 60 times more powerful and has up to 16 times more communications capacity than an Inmarsat-3 satellite and the Inmarsat-4 satellites extend the commercial life of our satellite fleet to beyond 2020. The quality and coverage of our network is further underpinned by the fact that we are currently the only provider of satellite services for the operation of the global maritime distress and safety system ("GMDSS"), which maritime sector regulations require for all cargo vessels over 300 gross tons and for all passenger vessels that travel in international waters. In addition, we also comply with the International Civil Aviation Organisation ("ICAO") standards for the provision of aeronautical safety systems, such as air traffic management and aircraft operational control. |

| • | Established, Large End-User Base of Government and Military Entities, Corporations and International Aid Organisations. As of 30 September 2009, we had over 253,000 active terminals accessing our data, voice and broadband services, which in many instances are accessed by multiple end-users, such as those on board ships and aircraft. We believe that this large installed base of active terminals contributes to our stable revenues, due to the significant cost and effort required by end-users to switch to an alternative communications system. Government and military end-users, in particular the U.S. Department of Defense and the UK Ministry of Defence, are large users of our communications network. We believe that government and military end-users account for between 35% and 40% of our revenues. We believe that their rapidly growing mobile high-speed data and voice communications needs, together with an increasing willingness to procure from commercial service providers, position us favourably to increase both traditional sales of our on-demand services and leasing of our satellite capacity through distribution partners to government and military end-users. Our corporate end-users tend to have a high degree of day-to-day reliance on our services to support mission critical operations which contributes to our revenue stability. International aid organisations rely on our services when responding to global events, including aid relief missions in response to natural disasters. During the recent economic downturn, we have continued to report revenue growth in all of our business sectors. For the nine-month period ended 30 September 2009 as compared with the nine-month period ended 30 September 2008, we reported growth in our total MSS revenues of 9.7%. In particular, revenue growth in our maritime sector has been sustained despite otherwise difficult trading conditions for the shipping industry. For the nine-month period ended 30 September 2009, revenues from the maritime sector grew by 6.5% as compared with the nine-month period ended 30 September 2008. We believe the performance of our maritime business during the economic downturn underlines both the basic reliance on our services and the increasing demand for data communications services at sea. |

2

| • | Established, Global Distribution Network. We currently have 32 distribution partners who sell our services to end-users, either directly or through a network of approximately 400 service providers. In addition, our parent company, Inmarsat plc, owns our largest distributor, Stratos, which for the nine-month period ended 30 September 2009, accounted for a 43% share of our MSS revenues. Some of our distribution partners and service providers specialise in the delivery of services to key end-user market sectors and offer specialist applications and value-added services in addition to our airtime. Our well-established, global network of distribution partners enables the targeting and support of end-user market sectors across the globe. In April 2009, our previous five-year distribution agreements expired and were replaced with new evergreen Distribution Agreements with a minimum term of five years, that have significant operational and economic benefits compared to the previous distribution agreements, including the ability for us to contract directly with end-users and for us to own and operate land earth stations ("LESs") for our Existing and Evolved Services. We believe the terms of the new Distribution Agreements increase our ability to influence the price and positioning of our services to end-users and will result in the improved performance of our business over time. See "Operating and Financial Review—Significant Factors Affecting Our Results of Operations—Effect of Distribution Agreements" and "Material Contracts—Distribution Agreements". |

| • | High Margins and Attractive Cash Conversion Profile. For the past nine years, our EBITDA margin (EBITDA as a percentage of revenues) has exceeded 63% and our EBITDA has grown from US$289.7 million in 2000 to US$477.1 million for the twelve-month period ended 30 September 2009 (an EBITDA margin of 71%). Our wholesale business model results in our distribution partners and service providers incurring most of the marketing and associated subscriber, or end-user, acquisition costs, and consequently our EBITDA margins compare favourably to those of other communications service providers. As a result of completing our network of three Inmarsat-4 satellites, including related ground infrastructure development, our capital expenditures have reduced materially. For the twelve-month period ended 30 September 2009, our FCF more than doubled to US$316.2 million from US$119.1 million for the twelve-month period ended 30 September 2008. We expect our strong EBITDA margin and current lower capital expenditure profile to continue to generate strong FCF for the foreseeable future. |

| • | Proven Track Record of Deleveraging. Through a combination of increasing our revenues and controlling our operating costs and capital expenditures, we have increased our FCF and reduced our leverage. We have decreased the ratio of Net External Debt to EBITDA from 1.8x as of the year ended 31 December 2005 to 0.9x as of the twelve-month period ended 30 September 2009. |

| • | Global Broadband Services Portfolio in Place to Capitalise on Growth Opportunities. With the deployment of our Inmarsat-4 satellite fleet, we have introduced new broadband services into each of our market sectors. We launched our BGAN service for the land mobile sector in December 2005, our SwiftBroadband service for the aeronautical sector in October 2007 and our FleetBroadband service for the maritime sector in November 2007. We believe our broadband services enable us to capitalise on the growth opportunities presented by existing and new end-users' increasing demand for high-bandwidth mobile communication services, as evidenced by the strong growth in data services we have experienced in recent years. The incremental capacity of our Inmarsat-4 network has also allowed us to expand our leasing business, which has experienced substantial growth in recent years. |

| • | 30-Year History of Innovation, Technical Excellence and Reliability. We have over 30 years of experience in designing, implementing and operating global mobile satellite communications networks, and have a track record of high-quality services and reliability. We have never experienced a satellite failure in our operating history and, throughout our operating history, we have pioneered innovations in satellite communication services to make higher data speeds available to smaller and lighter mobile terminals. Our broadband services are the latest of these innovations and are designed to offer the same service characteristics our end-users have historically enjoyed through our Existing and Evolved Services including reliability, ease of use and security. In addition, over the three years ended 31 December 2008, our average satellite communications network availability exceeded 99.99%. We believe our reliability is particularly attractive to government, military and enterprise-level users whose operations typically require mission and business critical communications support. |

3

| • | Experienced Management Team. We have a highly experienced management team with a proven record of managing growth-oriented companies. Our Chief Executive Officer and Chief Financial Officer joined us in 2003 and 2004, respectively, and have managed our business through a period of sustained growth and de-leveraging. Members of our senior management team have held senior positions at a number of public companies, including Sprint PCS, NDS Group plc and Lockheed Martin. Our Chief Technology Officer, Senior Vice President of Global Networks and Engineering and Vice President of Satellite and Network Operations have over 100 years of combined experience in the satellite industry and have been involved in the successful launch and deployment of more than 100 satellites. We believe this base of experience was a significant factor in the successful development and deployment of the Inmarsat-4 network and better enables us to execute our strategy in the future. |

Strategies

Our goal is to increase our penetration in our core data and voice services sectors and enter new end-user sectors. We plan to:

| • | Maintain Strong Growth and Cash Flow Generation by Increasing Sales of Our Existing Services and Realise Economies of Scale as We Roll Out New Services. We believe that our disciplined investment approach, our relatively high EBITDA margins and our current low capital expenditure profile will result in attractive cash conversion in our business going forward. We intend to improve our margins and cash generation by leveraging our new broadband portfolio of services and leading position in the maritime, land mobile and aeronautical sectors to increase sales of our existing services, while maintaining our rigorous cost control. |

| • | Develop and Market New Handheld Global Satellite Phone Services. We estimate that we are the leader in land data MSS and believe our share in land voice MSS represents a significant growth opportunity. We are developing GSPS, as well as fixed land and maritime variants, to compete in the low-cost satellite voice sector. With the launch of our Inmarsat-4 satellites we introduced our first handheld SPS on a regional basis and began to access this opportunity within the MSS sector for the first time. We currently expect to launch GSPS in the second quarter of 2010. We expect that GSPS will feature competitively-priced hardware and usage charges and be attractive to end-users. In addition, we expect that our distributors and service providers may bundle GSPS with our data services to create single handheld voice and data packages that will be attractive to end-users, many of whom buy both handheld voice and data services to meet their needs. |

| • | Pursue New Business and Market Opportunities. Our Inmarsat-4 satellite fleet provides us with the capacity and functionality necessary to support a broad range of new business opportunities, which we expect will be consistent with our goal of continued strong growth and cash flow generation. We believe that the flexibility of our Inmarsat-4 satellite fleet will enable us to capitalise upon both event-driven and long-term revenue opportunities across the maritime, land mobile and aeronautical sectors. For example, we are working with certain distributors on the development of in-flight cellular-based services for use by commercial airline passengers. A number of airlines have already begun, or committed to, the commercial launch of these services, and a larger number of airlines have either trialled or are planning to trial these services in the future. |

| We also intend to seek to increase the amount of satellite capacity we lease to our distribution partners. We believe that there exists a significant opportunity for growth to provide additional services to the U.S. Government, including the Department of Defense and the Department of Homeland Security, as well as other governments around the world. The emergence of networked warfare techniques and the increased willingness of the U.S. Department of Defense to procure satellite communications from commercial suppliers creates an opportunity for us to benefit from the increased bandwidth demands and to play a significant role in the development of new communications platforms for military use. International homeland security issues are creating opportunities for us relating to emergency communications back-up and support to remote locations. In addition, we remain well-positioned to benefit from any upsurge in demand for our services that would follow a global security event, conflict or natural disaster. |

In 2009, we made a strategic decision to increase our focus on growing our revenues from satellite low data rate ("SLDR") services, sometimes referred to as telemetry services, which typically support asset |

4

tracking and monitoring applications. We believe the demand for low data rate services terminals is growing and that average satellite airtime revenue opportunity per terminal is also growing. In July 2009, we entered into a long-term direct distribution agreement with SkyWave Mobile Communications ("SkyWave"), a leading provider of SLDR services, based in Canada. In connection with the agreement, SkyWave recently completed the migration of approximately 50,000 terminals to our Inmarsat-4 network, from a competing network. We expect to continue a range of development activities to improve and grow our share in the SLDR sector. |

| In addition, we believe new services may be licensed and deployed in the future using a combination of elements from both terrestrial and satellite communications networks. Some of these services could be deployed using the radio spectrum we have either been allocated or are authorised to develop in the future. Such new service opportunities are likely to require us to form partnerships with strategic or financial partners, but could provide significant new sources of revenue. In December 2007, we signed a cooperation agreement (the "Cooperation Agreement") with SkyTerra Communications Inc. ("SkyTerra"), a satellite communications company located in the United States, to enable the efficient use and development of our spectrum across the Americas and to support the commercial deployment of hybrid satellite/terrestrial services by SkyTerra. In May 2009, we were awarded rights over 30 MHz of S-band spectrum to develop hybrid satellite/terrestrial services for deployment across the 27 member states of the European Union. Although such developments are at an early stage, we expect opportunities to be driven by spectrum scarcity and/or new service innovation in the future. |

| • | Develop and Deploy our Alphasat Satellite to Enhance our Service Offerings and Satellite Network Resilience. In 2007, we announced that we had been selected by the European Space Agency ("ESA") to be the commercial partner for the joint development of a new satellite platform called Alphabus. As a result of our selection, Inmarsat will build, deploy and fully own a new satellite, called Alphasat, and will benefit from an effective public subsidy of approximately €150 million against the cost of building and launching the satellite. We expect that, when launched, Alphasat will allow us to deploy enhanced end-user service offerings in the key Europe, Middle East and Africa ("EMEA") markets and add continuity resilience to our Inmarsat-4 satellite network. In addition, we believe that the successful launch of Alphasat will postpone the need to deploy our next generation of replacement satellites and will result in a material deferral of the capital expenditure costs associated with developing and launching these satellites. The Alphasat satellite began construction in 2008 under a contract with Astrium Satellites ("Astrium") and is expected to be delivered in 2012. The Alphasat satellite will be capable of providing our services across the complete 41 MHz of L-band mobile satellite spectrum available over the EMEA region. This capability provides greater flexibility in spectrum utilisation compared to the current Inmarsat-4 satellite for the EMEA region, which is limited to providing service across 27 MHz of the L-band. In addition, Alphasat's advanced digital processor capability and optimised antenna coverage will allow up to 50% more capacity for our services as compared with an Inmarsat-4 satellite, while remaining compatible with established launch vehicles. |

Recent Developments

Recent Developments relating to Inmarsat Group Limited and its subsidiaries

European S-band spectrum award

On 6 October 2008, our wholly-owned subsidiary, Inmarsat Ventures Limited, made an application under the European S-band Application Process ("ESAP") for an award of S-band spectrum for deployment of services across the 27 member states of the European Union. This followed our announcement in August 2008 that Thales Alenia Space ("Thales") and International Launch Services ("ILS") had been selected to support our ESAP application. On 13 May 2009, the European Commission selected two operators, Inmarsat Ventures Limited and Solaris Mobile Limited, as the successful applicants. Inmarsat Ventures Limited was awarded rights over 30 MHz of contiguous 2 GHz frequencies for use in a pan-European satellite and complementary terrestrial deployment.

Our S-band satellite programme, known as EuropaSat, aims to deliver next-generation telecommunications services across the European Union. These new services may include mobile multimedia broadcast, mobile broadband and next-generation MSS services for consumers, enterprise and institutional users throughout Europe, including those in remote and rural areas.

5

The further development of the EuropaSat satellite depends on our ability to significantly de-risk financial and/or market risk by means of an investment by, or partnership or collaboration with, substantial financial and/or strategic partners, as well as the favourable resolution of certain disputes between the European Commission and unsuccessful ESAP applicants who are seeking to contest the validity of the ESAP and the awards.

Possible strategic acquisition

We are currently in discussions with a third party regarding a potential acquisition of an established integrated satellite communications provider. We currently anticipate that the initial consideration for the acquisition would be less than US$150.0 million, excluding any contingent deferred consideration, and that the entity we may acquire will have no material indebtedness at closing. The entity we may potentially acquire has an established operating history, and in 2008 recorded revenues in excess of US$50.0 million together with positive operating profit and positive net income. We cannot guarantee that any agreement regarding this acquisition will be reached or, if an agreement is reached, the acquisition will be completed successfully.

Extension of Andrew Sukawaty's term of office

On 1 October 2009, we announced that Andrew Sukawaty had agreed to extend his role as Chairman and Chief Executive Officer until 30 September 2011, and then retain the role of Chairman until at least 30 September 2012.

Dividend to Inmarsat Holdings Limited

On 28 October 2009, we paid a dividend of US$58.4 million to Inmarsat Holdings Limited in connection with Inmarsat plc’s interim dividend (the "October Dividend").

Recent Developments Relating to Inmarsat plc

Inmarsat Group Limited and Inmarsat Finance plc are indirect wholly-owned subsidiaries of Inmarsat plc. Inmarsat plc and certain of its direct or indirect subsidiaries which are not subsidiaries of the Parent Guarantor, including Stratos, will not be party to the Indenture and will not be bound by the restrictive covenants contained therein. For a further description of our corporate structure, see "Summary Corporate and Financial Structure".

Harbinger Capital Partners

On 25 July 2008, Harbinger Capital Partners ("Harbinger") and SkyTerra announced their intention for SkyTerra to make an offer to acquire Inmarsat plc and its subsidiaries on terms to be announced following a satisfactory outcome of a regulatory approvals process. At the time of the announcement Harbinger held approximately 28.2% of the ordinary shares of Inmarsat plc. As of the date of this offering circular, we have not received an offer from Harbinger or SkyTerra. On 22 August 2008 and 26 March 2009, Harbinger submitted applications to the U.S. Federal Communications Commission (the "FCC") seeking review and pre-clearance of the transfer of control of the Inmarsat group to SkyTerra. As at the date of this offering circular, we are not aware of any decision by the FCC regarding the Harbinger applications. Harbinger has a substantial shareholding in SkyTerra and TerreStar Networks Inc. ("TerreStar"), both of which are our competitors in regional MSS in North America. See "Business—Competition—Regional MSS Competitors". On 23 September 2009, Harbinger announced a public offer to acquire the remaining shares of SkyTerra which it does not already own.

The board of directors of Inmarsat plc (the "Board") has announced its intention to maintain a constructive relationship with Harbinger (currently the largest shareholder in Inmarsat plc), and to consider carefully any future offer that may maximise value for Inmarsat plc's shareholders as a whole. The Board continues to remain highly confident in the standalone business prospects of Inmarsat plc and management's future plans for the continued independent development of the business.

Acquisition of Stratos Global Corporation

On 15 April 2009, Inmarsat plc announced that a direct wholly-owned subsidiary, Inmarsat Finance III Limited, completed the indirect acquisition of Stratos by exercising an option to acquire the entire share capital of CIP UK Holdings Limited ("CIP UK"), an indirect parent company of Stratos. The acquisition was previously funded in December 2007 and no additional financing was required to complete the transaction.

6

As a result of the acquisition, Stratos became an indirect wholly-owned subsidiary of Inmarsat plc. Stratos' operations will continue to be managed by the existing Stratos management team, reporting directly to Inmarsat plc at a corporate level.

Although Inmarsat plc completed the acquisition of CIP UK and therefore Stratos on 15 April 2009, Inmarsat plc has been consolidating the results of Stratos since 11 December 2007, the date on which it acquired the option over the entire share capital of CIP UK. During the period between 11 December 2007 and 15 April 2009, Inmarsat plc did not hold an equity interest in, nor have any control over the financial and operating policies of, nor any entitlement to receive dividends from, CIP UK or Stratos.

As a result of the acquisition of Stratos on 15 April 2009, Inmarsat plc indirectly assumed all the assets and liabilities of Stratos, including its existing indebtedness as at 31 December 2008. As the acquisition of Stratos occurred at the level of Inmarsat plc, none of CIP UK, CIP Canada Investment Inc. (which acquired the entire issued share capital of Stratos), Stratos, nor any of its subsidiaries is a Restricted Subsidiary (as defined in "Description of Notes—Certain Definitions") of the Parent Guarantor, and accordingly will not be bound by the restrictive covenants of the Indenture. None of the guarantors of the Notes will have any obligation with respect to the liabilities and indebtedness of Stratos. Equally, we will not benefit from any distributions by Stratos to Inmarsat plc.

We may agree with Inmarsat plc to a reorganisation in the future, such that Stratos would become an indirect wholly-owned subsidiary of Inmarsat Group Limited. However, no decision regarding such a reorganisation has been made and accordingly we cannot assure you that such a reorganisation will occur.

Under the terms of the Distribution Agreements between us and our distributors, including Stratos, Stratos will continue to purchase satellite capacity from us and provide certain related services. Payment and credit terms with Stratos will remain consistent with those offered to our other distributors.

SkyWave Mobile Communications

On 1 July 2009, Inmarsat plc acquired a 19% stake in the privately held SkyWave for cash consideration of US$10.0 million and non-cash consideration of US$11.5 million consisting of deferred airtime credits. Concurrent with this investment, SkyWave acquired assets relating to a competitor's SLDR business from its parent company, TransCore, a U.S.-based logistics operator for the transportation industry. SkyWave also entered into a sales distribution relationship with TransCore focusing on the North American trucking and rail segments of the SLDR sector.

In connection with this transaction, we simultaneously entered into a distribution agreement with SkyWave for the global supply of satellite capacity to SkyWave, which also provides for a fully-funded development programme by SkyWave for new products and services designed to work over the Inmarsat network.

The Transactions

During October 2009, we repaid US$50.0 million (the "October Debt Repayment") under our US$550.0 million senior credit agreement, dated 24 May 2005 (the "Previous Credit Facility").

On 6 November 2009, we made an initial drawdown of US$290.0 million under our US$500.0 million Senior Credit Facility (as defined herein), and used such borrowings, together with US$25.0 million of cash on hand, to simultaneously repay and effect the cancellation of the Previous Credit Facility. Such borrowing under the Senior Credit Facility and repayment and cancellation of the Previous Credit Facility, together with the October Debt Repayment, are collectively referred to herein as the "Senior Facility Refinancing". See "Description of Certain Financing Arrangements—Senior Credit Facility" for more information on the Senior Credit Facility.

On the date of the final offering circular, we intend to issue a notice of redemption for all of our outstanding 7 5/8% Senior Notes due 2012 issued under an indenture dated as of 3 February 2004 (the "Existing Senior Notes"), and Inmarsat Finance II plc intends to issue a notice of redemption for all of its outstanding 10 3/8% Senior Discount Notes due 2012 issued under an indenture dated as of 24 November 2004 (the "Existing DiscountNotes"). We intend to use the proceeds from this offering to fund these redemptions. See "Use

7

of Proceeds" for a description of the series of transactions relating to the redemption of the Existing Senior Notes and the Existing Discount Notes. The series of transactions resulting in the redemption of the Existing Senior Notes and the Existing Discount Notes, as well as the payments of any related fees and expenses, are collectively referred to herein as the "Existing Notes Refinancing".

The Senior Facility Refinancing and the Existing Notes Refinancing are collectively referred to herein as the "Refinancing". The October Dividend and the Refinancing are collectively referred to herein as the "Transactions".

Our Address

Our principal executive office is located at 99 City Road, London EC1Y 1AX, United Kingdom, and our telephone number is +44 (0)20 7728 1000. The website of Inmarsat Group Limited iswww.inmarsat.com. The information provided on our website, other than the information expressly incorporated by reference herein, is not part of this offering circular and is therefore not incorporated by reference herein.

8

SUMMARY CORPORATE AND FINANCIAL STRUCTURE

The following chart sets forth a summary of our corporate and financing structure as of 30 September 2009, as adjusted to give pro forma effect to the Transactions. Please refer to "Use of Proceeds", "Capitalisation", "Description of Certain Financing Arrangements" and "Description of Notes" for more information.

| (1) | For more information regarding Inmarsat plc’s shareholders, see "PrincipalShareholders". |

| (2) | On 16 November 2007, Inmarsat plc issued US$287.7 million in principal amount of 1.75% convertible bonds due 2017 (the"Convertible Bonds"). The Convertible Bonds are convertible into ordinary shares of Inmarsat plc and have a 1.75% per annum coupon payable semi-annually and a yield to maturity of 4.50%. The Convertible Bonds have an initial conversion premium of 32.5% over the reference share price of £4.6193 representing approximately 5% of Inmarsat plc's then current issued share capital. The initial conversion price is US$12.694 and the total number of common shares to be issued if all Convertible Bonds are converted is 22.7 million shares. Inmarsat plc has an option to call the Convertible Bonds after seven years at their accreted principal amount under certain circumstances. In addition, holders of the Convertible Bonds have the right to require Inmarsat plc to redeem their Convertible Bonds at their accreted principal amount on 16 November 2012 and 16 November 2014 or following the occurrence of certain change of control events. |

| (3) | Represents the US$784.6 million Subordinated Intercompany Shareholder Funding Loan, net of an estimated US$465.6 million repayment with the proceeds of the offering of the Notes hereby, which will be used by Inmarsat Holdings Limited to redeem the Existing Discount Notes. See "Use of Proceeds" and "Description of Certain Financing Arrangements—Subordinated Intercompany Shareholder Funding Loan". |

| (4) | Each of the Subsidiary Guarantors and certain of our other subsidiaries are borrowers and/or guarantors under the Senior Credit Facility. See "Description of Certain Financing Agreements—Senior Credit Facility". The shares of Inmarsat Ventures Limited are charged, on a first priority basis, to secure the obligations of Inmarsat Investments Limited under the Senior Credit Facility. On a pro forma basis, at 30 September 2009, we had an additional US$210.0 million of borrowings available under the Senior Credit Facility. |

| (5) | On the issue date of the Notes, the Subsidiary Guarantors will be Inmarsat Investments Limited, Inmarsat Ventures Limited, Inmarsat Global Limited, Inmarsat Leasing (Two) Limited and Inmarsat Launch Company Limited. During the year ended 31 December 2008, the Subsidiary Guarantors collectively (before intercompany eliminations) accounted for 122% of our consolidated revenue and 100% of our consolidated EBITDA. As at 31 December 2008, our Subsidiary Guarantors, accounted for 93% of our consolidated total assets, after deducting amounts due from, and investments in, fellow Subsidiary Guarantors. |

| (6) | Inmarsat Finance plc is a finance subsidiary whose only significant asset following the Refinancing, will be the Subordinated Intercompany Note Proceeds Loan. |

9

THE OFFERING

The summary below describes the principal terms of the Notes and the guarantees relating to the Notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The "Description of Notes" section of this offering circular contains a more detailed description of the terms and conditions of the Notes, including the definitions of certain terms used in this summary.

Issuer | Inmarsat Finance plc. |

Parent Guarantor | Inmarsat Group Limited. |

Subsidiary Guarantors | Inmarsat Investments Limited, Inmarsat Ventures Limited, Inmarsat Global Limited, Inmarsat Leasing (Two) Limited, Inmarsat Launch Company Limited and certain future subsidiaries of the Parent Guarantor. |

Notes Offered | US$650.0 million aggregate principal amount of % Senior Notes due 2017. |

Issue Price | % plus accrued interest, if any, from the issue date. |

Issue Date | On or about 2009. |

Maturity Date | 2017. |

Interest Payment Dates | Interest on the Notes will be payable semi-annually in arrears on and of each year, commencing on 2010. |

Ranking of the Notes | The Notes are general obligations of the Issuer and, following completion of the Existing Notes Refinancing, will be the only indebtedness of the Issuer. The Notes will be effectively subordinated to all obligations of the subsidiaries of the Parent Guarantor that do not guarantee the Notes. |

The Issuer is a finance subsidiary of the Parent Guarantor which does not conduct any operations and its only significant asset following the Refinancing will be the Subordinated Intercompany Note Proceeds Loan.

Ranking of the Guarantees | The Parent Guarantee |

| The Parent Guarantor's guarantee of the Notes: |

| • | will be a general unsecured obligation of the Parent Guarantor; |

| • | will rankpari passu in right of payment to all indebtedness and other obligations of the Parent Guarantor; and |

| • | will rank senior in right of payment to any indebtedness of the Parent Guarantor that is expressly subordinated to the parent guarantee. |

The Parent Guarantor is a holding company which does not conduct any operations, and its only assets are the shares of Inmarsat Finance plc and of Inmarsat Investments Limited (whose only significant asset is the shares of Inmarsat Ventures Limited and certain intercompany receivables).

The parent guarantee will be effectively subordinated to all obligations of the subsidiaries of the Parent Guarantor that do not guarantee the Notes.

10

The Subsidiary Guarantees

The guarantees of the Notes by each Subsidiary Guarantor:

| • | will be a general unsecured obligation of such Subsidiary Guarantor; |

| • | will be subordinated in right of payment to all existing and future senior debt of such Subsidiary Guarantor; |

| • | will rankpari passu in right of payment with any future senior subordinated indebtedness of such Subsidiary Guarantor; and |

| • | will rank senior in right of payment to any indebtedness of such Subsidiary Guarantor that is expressly subordinated to the relevant subsidiary guarantee. |

The guarantee of each Subsidiary Guarantor will provide that it will not mature (and no amount will become due or payable thereunder) until a payment event of default under the Notes has occurred and either (i) 179 days have elapsed since the date of the event of default or (ii) if earlier, certain other events, including certain insolvency events related to the relevant Subsidiary Guarantor, have occured and are continuing; a secured party has taken enforcement action in respect of senior debt; or the Notes have matured. In addition, the guarantee of each Subsidiary Guarantor, other than Inmarsat Investments Limited, may be released in certain circumstances.

The subsidiary guarantees will be contractually subordinated in right of payment to all senior debt of the Subsidiary Guarantors and effectively subordinated to all obligations of the subsidiaries of the Parent Guarantor that do not guarantee the Notes.

For more information regarding the guarantees, see "Description of Notes—Guarantees".

Optional Redemption | The Issuer may redeem some or all of the Notes at any time prior to 2013 at a redemption price equal to 100% of the principal amount thereof plus a make-whole premium as of, and accrued and unpaid interest up to, the redemption date. For a description of how to calculate the make-whole premium, see "Description of Notes—Optional Redemption". |

The Issuer may redeem up to 35% of the aggregate principal amount of the Notes outstanding at any time prior to 2012 at a redemption price of (expressed as a percentage of the principal amount) %, plus accrued and unpaid interest, with the proceeds of certain public equity offerings. The Issuer may make that redemption only if, after the redemption, at least 65% of the aggregate principal amount of the Notes remains outstanding and the redemption occurs within 90 days of the closing date of such public equity offering.

In addition, the Issuer may redeem some or all of the Notes on or after 2013 at the applicable redemption price described in the section entitled "Description of Notes—Optional Redemption".

Optional Redemption for Tax Reasons | The Issuer may redeem the Notes in whole, but not in part, at any time, if as a result of any changes in tax laws or their interpretation, the Issuer becomes obliged to pay any additional amounts. If the Issuer decides to redeem the Notes following such change, the Issuer must redeem the Notes at a price equal to the principal amount |

11

of the Notes plus accrued and unpaid interest to the date of redemption. See "Description of Notes—Optional Redemption for Tax Reasons". |

Change of Control | Upon the occurrence of certain change of control events, combined with a confirmation of a rating of the Notes below the ratings on the issue date, the Issuer may be required to offer to repurchase all or a portion of a holder's Notes at a price equal to 101% of the principal amount thereof, plus accrued and unpaid interest to the date of repurchase. See "Description of Notes—Repurchase at the Option of Holders—Change of Control". |

Covenants | The Issuer, the guarantors and The Bank of New York Mellon, as trustee, will be parties to the Indenture. The Indenture, among other things, will restrict the ability of the Issuer, the Parent Guarantor and its subsidiaries to: |

| • | make certain payments, including dividends or other distributions, with respect to the shares of the Parent Guarantor or its restricted subsidiaries; |

| • | incur or guarantee additional indebtedness and issue certain preference shares; |

| • | layer debt; |

| • | create or incur certain liens; |

| • | prepay or redeem subordinated debt or equity; |

| • | make certain investments; |

| • | create encumbrances on the payment of dividends or other distributions, loans or advances to and on the transfer of assets to the Parent Guarantor or any of its restricted subsidiaries; |

| • | sell, lease or transfer certain assets including shares of restricted subsidiaries; |

| • | engage in certain transactions with affiliates; |

| • | engage in any business other than a permitted business; |

| • | enter into sale and leaseback transactions; |

| • | merge, consolidate, amalgamate or combine with other entities; and |

| • | amend certain documents, including the Subordinated Intercompany Note Proceeds Loan. |

If at any time the Notes receive a rating of Baa3 or better by Moody's Investors Service, Inc. ("Moody's") or a rating of BBB- or better from Standard & Poor's Ratings Services, a division of The McGraw-Hill Companies Inc. ("S&P"), and no default or event of default has occurred and is continuing, certain covenants will cease to be applicable to the Notes, regardless of any subsequent changes in the rating of the Notes.

Each of the covenants is subject to a number of important exceptions and qualifications. See "Description of Notes—Certain Covenants".

12

Use of Proceeds | The proceeds from the offering of the Notes hereby will be used to redeem the Existing Senior Notes and the Existing Discount Notes, to pay the fees and expenses in relation to the offering of the Notes and for general corporate purposes. See "Use of Proceeds". |

Form of Notes | The Notes will initially be issued in the form of one or more Global Notes, registered in the name of a nominee of, and deposited with a custodian for, DTC. |

Ownership of interests in the Global Notes, and the book-entry interests therein, will be available only to persons who have accounts with DTC or persons that may hold interests through either of them. Book-entry interests will be shown on, and transfers thereof will be effected only through, records maintained in book-entry form by DTC and its respective participants. Except as set out under the section "Book Entry, Delivery and Form—Definitive Registered Notes", participants in DTC will not be entitled to receive physical delivery of Notes in definitive form or to have Notes issued and registered in their names and, while the Notes are in global form, will not be considered the owners or holders thereof under the Indenture. See "Book Entry, Delivery and Form".

No Prior Market | Although the Initial Purchasers have informed us that they intend to make a market in the Notes, they are not obligated to do so and may discontinue market-making at any time without notice. Accordingly, we cannot assure you that a liquid market for the Notes will develop or be maintained. |

Transfer Restrictions | The Notes have not been and will not be registered under the Securities Act or the securities laws of any other jurisdiction and are subject to restrictions on transferability and resale. See "Notice to Investors". We have not agreed to, or otherwise undertaken to, register the Notes (including by way of an exchange offer) and do not intend to so. |

Listing | Application has been made to have the Notes admitted for trading on the Euro MTF market. We have also applied, through The Bank of New York Mellon (Luxembourg) S.A., our listing agent in Luxembourg, to list the Notes on the Official List of the Luxembourg Stock Exchange. |

Ratings | The Notes are expected to be rated Ba3 by Moody's and BB+ by S&P. A rating is not a recommendation to buy, sell or hold securities and may be subject to a suspension, reduction or withdrawal at any time by the assigning rating agency. |

Trustee, Transfer Agent, Registrar, Principal Paying Agentand Paying Agent | The Bank of New York Mellon. |

Luxembourg Listing Agent, Transfer Agent, Registrar and Paying Agent | The Bank of New York Mellon (Luxembourg) S.A. |

Governing Law of the Notes, the guarantees and the Indenture | New York law. |

Risk Factors

Investing in the Notes involves substantial risks. Please see the section entitled "Risk Factors" for a description of some of the risks you should carefully consider before investing in the Notes.

13

SUMMARY HISTORICAL CONSOLIDATED FINANCIAL INFORMATION

The table below sets forth summary historical consolidated financial information as of and for the years ended 31 December 2006, 2007 and 2008 and summary historical condensed consolidated financial information as of and for the nine-month periods ended 30 September 2008 and 2009. The summary financial information as of and for the years ended 31 December 2006, 2007 and 2008 has been extracted from the audited consolidated financial statements prepared in accordance with IFRS, as adopted for use in the European Union and IFRS as issued by the IASB, and incorporated by reference in this offering circular. The summary financial information as of and for the nine-month periods ended 30 September 2008 and 2009 has been extracted from the unaudited condensed consolidated financial statements prepared on a basis consistent with IFRS and in accordance with IAS 34, "Interim Financial Reporting", and incorporated by reference in this offering circular. See "Documents Incorporated by Reference".

The table below also sets out unaudited consolidated financial information as of and for the twelve-month period ended 30 September 2009. This information has been derived from our financial statements incorporated by reference in this offering circular and is provided for illustrative purposes only.

The unaudited pro forma consolidated financial information set forth below reflects adjustments to give effect to the Transactions and is based upon available information and certain assumptions and estimates that we believe are reasonable. The unaudited pro forma consolidated financial information does not purport to present what our actual results of operations or financial position would have been had the Transactions occurred on the dates specified nor does it purport to project our results of operations or financial position at any future date. See "Presentation of Financial and Other Information – Financial Data".

You should read the table below in conjunction with "Capitalisation", "Selected Historical Consolidated Financial Information" and "Operating and Financial Review", as well as the consolidated financial statements and related notes thereto incorporated by reference into this offering circular.

| Year ended 31 December | Nine-month period ended 30 September | Twelve-month period ended 30 September | ||||||||||||||||

| 2006 | 2007 | 2008 | 2008 unaudited | 2009 unaudited | 2009 unaudited | |||||||||||||

| (US$ in millions) | ||||||||||||||||||

Consolidated Income Statement: | ||||||||||||||||||

Revenue | 500.1 | 557.2 | 634.7 | 474.1 | 513.3 | 673.9 | ||||||||||||

Net operating costs | (168.4 | ) | (173.7 | ) | (203.4 | ) | (144.2 | ) | (137.6 | ) | (196.8 | ) | ||||||

Depreciation and amortisation | (156.8 | ) | (174.2 | ) | (167.0 | ) | (126.6 | ) | (135.5 | ) | (175.9 | ) | ||||||

Operating profit | 174.9 | 209.3 | 264.3 | 203.3 | 240.2 | 301.2 | ||||||||||||

Net interest payable | (84.7 | ) | (81.4 | ) | (72.1 | ) | (57.3 | ) | (64.0 | ) | (78.8 | ) | ||||||

Profit before income tax | 90.2 | 127.9 | 192.2 | 146.0 | 176.2 | 222.4 | ||||||||||||

Income tax credit/(expense) | 37.8 | (29.0 | ) | 164.2 | (42.8 | ) | (46.4 | ) | 160.6 | |||||||||

Profit for the period | 128.0 | 98.9 | 356.4 | 103.2 | 129.8 | 383.0 | ||||||||||||

Consolidated Cash Flow Data: | ||||||||||||||||||

Cash inflow from operating activities | 330.7 | 377.0 | 425.0 | 308.0 | 393.7 | 510.7 | ||||||||||||

Cash flow for capital expenditure | (114.4 | ) | (209.9 | ) | (187.7 | ) | (146.4 | ) | (100.7 | ) | (142.0 | ) | ||||||

Cash flow used in investing activities | (132.4 | ) | (230.4 | ) | (213.6 | ) | (167.3 | ) | (118.2 | ) | (164.5 | ) | ||||||

Dividends paid | (101.4 | ) | (135.3 | ) | (159.6 | ) | (104.1 | ) | (86.5 | ) | (142.0 | ) | ||||||

Cash flow used in financing activities | (193.0 | ) | (154.4 | ) | (197.5 | ) | (129.9 | ) | (172.9 | ) | (240.5 | ) | ||||||

Consolidated Balance Sheet Data (at period end): | ||||||||||||||||||

Cash and cash equivalents | 39.5 | 31.3 | 51.2 | 42.7 | 148.2 | 148.2 | ||||||||||||

Current assets | 209.7 | 212.2 | 272.8 | 257.4 | 340.6 | 340.6 | ||||||||||||

Current liabilities | 174.9 | 228.2 | 369.8 | 404.2 | 577.3 | 577.3 | ||||||||||||

Total assets | 1,979.2 | 1,998.1 | 2,131.5 | 2,074.0 | 2,181.7 | 2,181.7 | ||||||||||||

Total liabilities | 1,589.4 | 1,648.0 | 1,611.2 | 1,789.7 | 1,650.8 | 1,650.8 | ||||||||||||

Shareholders' equity | 389.8 | 350.1 | 520.3 | 284.3 | 530.9 | 530.9 | ||||||||||||

Other Financial Data: | ||||||||||||||||||

EBITDA (1) | 331.7 | 383.5 | 431.3 | 329.9 | 375.7 | 477.1 | ||||||||||||

EBITDA margin (2) | 66 | % | 69 | % | 68 | % | 70 | % | 73 | % | 71 | % | ||||||

Free cash flow (3) | 165.9 | 110.0 | 180.7 | 115.0 | 250.5 | 316.2 | ||||||||||||

Pro forma cash and cash equivalents(4) | 20.2 | |||||||||||||||||

Pro forma net senior debt (5) | 319.4 | |||||||||||||||||

Pro forma Net External Debt (5) | 969.4 | |||||||||||||||||

Ratio of pro forma net senior debt to EBITDA | 0.7 | x | ||||||||||||||||

Ratio of pro forma Net External Debt to EBITDA | 2.0 | x | ||||||||||||||||

Ratio of EBITDA to pro forma cash interest expense (6) | 6.9 | x | ||||||||||||||||

Pro forma Fixed Charge Coverage Ratio(7) | 5.9 | x | ||||||||||||||||

14

| (1) | EBITDA is a non-IFRS performance measure and is defined as profit for the period before net interest payable, taxation, depreciation and amortisation. For a discussion of EBITDA, see "Presentation of Financial and Other Information—Non-IFRS Financial Measures—EBITDA". A reconciliation of EBITDA to profit for the periods indicated is as follows: |

| Year ended 31 December | Nine-month period ended 30 September | Twelve-month period ended 30 September | |||||||||||||

| 2006 | 2007 | 2008 | 2008 unaudited | 2009 unaudited | 2009 unaudited | ||||||||||

| (US$ in millions) | |||||||||||||||

Profit for the period | 128.0 | 98.9 | 356.4 | 103.2 | 129.8 | 383.0 | |||||||||

Add back: | |||||||||||||||

Income tax (credit)/expense | (37.8 | ) | 29.0 | (164.2 | ) | 42.8 | 46.4 | (160.6 | ) | ||||||

Net interest payable | 84.7 | 81.4 | 72.1 | 57.3 | 64.0 | 78.8 | |||||||||

Depreciation and amortisation | 156.8 | 174.2 | 167.0 | 126.6 | 135.5 | 175.9 | |||||||||

EBITDA | 331.7 | 383.5 | 431.3 | 329.9 | 375.7 | 477.1 | |||||||||

| (2) | EBITDA margin is defined as EBITDA divided by revenue. |

| (3) | FCF is a non-IFRS performance measure and is defined as cash generated from operations less capital expenditure, capitalised operating costs, net interest and cash tax payments. See "Presentation of Financial and Other Information—Non-IFRS Financial Measures—Free Cash Flow". A reconciliation of FCF to cash from operations for the periods indicated is as follows: |

| Year ended 31 December | Nine-month period ended 30 September | Twelve-month period ended 30 September | ||||||||||||||||

| 2006 | 2007 | 2008 | 2008 unaudited | 2009 unaudited | 2009 unaudited | |||||||||||||

| (US$ in millions) | ||||||||||||||||||

Cash generated from operations | 328.7 | 371.7 | 425.2 | 307.3 | 398.8 | 516.7 | ||||||||||||

Capital expenditure | (114.4 | ) | (209.9 | ) | (187.7 | ) | (146.4 | ) | (100.7 | ) | (142.0 | ) | ||||||

Capitalised operating costs | (14.0 | ) | (17.5 | ) | (23.4 | ) | (18.4 | ) | (15.0 | ) | (20.0 | ) | ||||||

Net cash interest paid | (33.9 | ) | (34.4 | ) | (32.1 | ) | (27.2 | ) | (27.2 | ) | (32.1 | ) | ||||||

Cash tax paid | (0.5 | ) | 0.1 | (1.3 | ) | (0.3 | ) | (5.4 | ) | (6.4 | ) | |||||||

Free cash flow | 165.9 | 110.0 | 180.7 | 115.0 | 250.5 | 316.2 | ||||||||||||

| (4) | Pro forma cash and cash equivalents reflects the pro forma adjustments to cash and cash equivalents to give effect to the Transactions. See "Capitalisation" for more information regarding the pro forma adjustments to cash and cash equivalents. |

| (5) | Senior debt is defined as indebtedness which is contractually and/or structurally senior to the subsidiary guarantees of the Notes, including indebtedness under the Senior Credit Facility. Pro forma net senior debt represents total senior debt after giving pro forma effect to the Transactions, net of pro forma cash and cash equivalents. Pro forma Net External Debt represents Net External Debt after giving pro forma effect to the Transactions. See "Capitalisation" for more information regarding the pro forma adjustments to our indebtedness and cash and cash equivalents. |

| (6) | Pro forma cash interest expense is adjusted to give effect to the Transactions as if they had occurred on 1 October 2008 and is calculated (i) using the assumption that drawings under the Senior Credit Facility of US$290.0 million remained constant over the twelve-month period (with interest on the Senior Credit Facility calculated using current three-month LIBOR plus the applicable margin) and (ii) using an assumed interest rate on the Notes. |

| (7) | Pro forma Fixed Charge Coverage Ratio is calculated based on the definition thereof set forth under "Description of Notes—Certain Definitions", and is adjusted to give effect to the Transactions as if they had occurred on 1 October 2008. |

15

In addition to the other information in this offering circular, you should carefully consider the risks described below before deciding whether to invest in the Notes. The risks and uncertainties we describe below are not the only ones we face. Additional risks and uncertainties of which we are not aware or that we currently believe are immaterial may also adversely affect our business, financial condition and results of operations. If any of the possible events described below were to occur, our business, financial condition and results of operations may be materially and adversely affected. If that happens, we and the Issuer may not be able to pay interest or principal on the Notes when due and you could lose all or part of your investment.

This offering circular contains forward-looking statements that involve risks and uncertainties. Our actual results may differ materially from those anticipated in these forward-looking statements as a result of various factors, including the risks described below and elsewhere in this offering circular. See "Forward-Looking Statements".

Risks Relating to Our Business

Sales to our key distribution partners represent a significant portion of our revenues and the loss of any of these distribution partners could adversely affect our revenues, profitability and liquidity.

For the nine-month period ended 30 September 2009, two of our distribution partners, Stratos and Vizada, accounted for 43% and 36%, respectively, of our MSS revenues (as compared with 44% and 37%, respectively, for the year ended 31 December 2008). Mergers among distribution partners could also increase our reliance on a few key distributors of our services. If our distribution partners were to fail to market or distribute our services effectively, or if they offered our services at prices which were not competitive, our revenues, profitability, liquidity and brand image could be adversely affected. The loss of any key distribution partners could materially affect our routes to market, reduce customer choice or represent a significant bad debt risk. On 15 April 2009, our parent company, Inmarsat plc, indirectly acquired Stratos.

The global communications industry is highly competitive. It is likely that we will face significant competition in the future from other network operators, which may adversely affect end-user take-up of our services and our revenues.

The global communications industry is highly competitive. We face competition today from a number of communications technologies in the various target sectors for our services. It is likely that we will continue to face increasing competition from other network operators in some or all of our target sectors in the future, particularly from satellite network operators. Competition from Iridium Communications Inc. ("Iridium") a global MSS operator, has been increasing. Iridium recently launched a maritime service that offers a 128 kbps capability and competes with the low end of our FleetBroadband capability. In addition, we also face regional competition for data and voice services from regional MSS operators such as Thuraya and SkyTerra, and to a lesser extent other regional MSS operators, which has influenced the price at which our distribution partners and service providers offer our services. Thuraya, a leader in the provision of handheld SPS, offers a 444 kbps mobile data communications service on a regional basis and recently launched a regional maritime 60 kbps data service. Two other companies, DBSD North America Inc. ("ICO") in the United States and TerreStar, in the United States and Canada, plan to deploy MSS in North America in the near future. Both companies have launched satellites, but, as yet, do not have services available commercially. Both companies also use the S-band, which has more contiguous bandwidth than the L-band in which we operate and may accommodate higher-speed multimedia services.

Communications providers who operate private networks using very small aperture terminals ("VSAT") or hybrid systems also continue to target users of mobile satellite services. Technological innovation in VSAT, together with increased C-band, Ku-band and Ka-band coverage and commoditisation, have increased, and we believe will continue to increase, the competitiveness of VSAT and hybrid systems in some traditional MSS sectors, including the maritime and aeronautical sectors. Businesses such as ARINC, CapRock, KVH, Row 44 Inc., MTN, Ship Equip and Vizada deploy mobile VSAT systems in direct competition with our maritime and aeronautical products. Furthermore, the gradual extension of terrestrial wireline and wireless communications networks to areas not currently served by them may reduce demand for some of our services in those areas.

16

The development of combined satellite and terrestrial networks could interfere with our services.

On 29 January 2003, the FCC promulgated a general ruling (the "ATC Ruling") that MSS spectrum, including the L-band spectrum we use to operate our services, could be used by MSS operators to integrate ancillary terrestrial component ("ATC") services into their satellite networks in order to provide combined terrestrial and satellite communications services to mobile terminals in the United States.

The implementation of ATC services by MSS operators in the United States or other countries may result in increased competition for the right to use L-band spectrum, and such competition may make it difficult for us to obtain or retain the spectrum resources we require for our existing and future services. In addition, the FCC's decision to permit integrated MSS/ATC services was based on certain assumptions, particularly relating to the level of interference that the provision of integrated MSS/ATC services would likely cause to other MSS operators, such as us, who use the L-band spectrum. If the FCC's assumptions with respect to the use of L-band spectrum for integrated MSS/ATC services prove inaccurate, or a significant level of integrated MSS/ATC services is provided in the United States, the provision of integrated MSS/ATC services could interfere with our satellites and user terminals, which may adversely impact our services. For example, the use of certain L-band spectrum to provide integrated MSS/ATC services in the United States could interfere with our satellites providing communications services outside the United States where the satellites' 'footprint' overlaps the United States. Such interference could limit our ability to provide services that are transmitted through any satellite visible to the United States. Two of our three Inmarsat-4 satellites, three of our Inmarsat-3 satellites and two of our Inmarsat-2 satellites are currently visible to the United States. In addition, users of our terminals in the United States could suffer interruptions to our services if they tried to use their terminals near ATC terrestrial base stations used to provide integrated MSS/ATC services. In the event that we anticipate significant usage of mobile user terminals near ATC terrestrial base stations, it may be necessary for the manufacturers of the mobile terminals to modify their products to make them less susceptible to interference and for us to replace or upgrade existing user terminals to avoid harmful interference.

Jurisdictions other than the United States are considering, and could implement, similar regulatory regimes in the future. In May 2004, Industry Canada, the Canadian regulator, decided in principle to allow ATC services in Canada. Pursuant to the ESAP, the European Commission has selected two operators, Inmarsat Ventures Limited and Solaris Mobile Limited, as the successful applicants for an award of 30 MHz each of contiguous S-band frequencies for use in the development and operation of a pan-European satellite and complementary terrestrial deployment.

We cannot assure you that the development of hybrid networks in the United States, Canada, Europe or in other countries will not result in harmful interference to our operations. If we are unable to prevent such interference it could have an effect on our revenues, profitability and liquidity.

We may not retain sufficient rights to the spectrum required to operate our satellite system to its expected capacity or to take full advantage of future business opportunities.

We must retain rights to use sufficient L-band and C-band spectrum necessary for the transmission of signals between our satellites and end-user terminals and between our satellites and our control stations. Our access to L-band spectrum and C-band spectrum is obtained through frequency coordination under International Telecommunication Union ("ITU") procedures. The L-band coordination is governed, in part, by sharing arrangements with other satellite operators that are re-evaluated and re-established through two annual, regional multilateral meetings of those satellite operators - one for operators whose satellites cover the Americas, and a second for those whose satellites cover Europe, Africa, Asia and the Pacific.

We agreed spectrum allocations for 2009 in the Europe, Africa, Asia and Pacific operators' review meeting. We, together with SkyTerra, also collectively have the rights to the majority of the L-band spectrum allocation in the Americas. As a result of the Cooperation Agreement we signed with SkyTerra in December 2007 for spectrum re-use and reorganisation of our respective L-band spectrum across the Americas, we have effectively agreed allocations for the Americas until at least 2013. See "Regulation—International Telecommunication Union Filings and Co-ordination Procedures". We believe those agreements provide sufficient spectrum to support our existing services for the duration of the agreements. As part of our business planning we may need to apply for additional spectrum to support our future services and existing services growth.

Competition for L-band and C-band spectrum from new operators or for new services or business opportunities could make it more difficult for us to retain rights to L-band and C-band spectrum or to take full

17

advantage of future business opportunities by acquiring further L-band and C-band spectrum. If we were unable to retain sufficient rights to L-band and C-band spectrum, our ability to provide our services in the future could be prejudiced, which could have an adverse effect on our revenue, profitability and liquidity.

We rely on third-party distribution partners to provide ground infrastructure for our Existing and Evolved Services.

We sell our Existing and Evolved Services, which currently constitute the majority of our revenues, to third-party distribution partners, many of whom operate the LESs that transmit and receive those services to and from our satellites. If any of these distribution partners fail to provide or maintain these facilities, our Existing and Evolved Services may be interrupted. Such service interruption may be beyond our control and could adversely affect our revenue, as well as our reputation and our brand image.

We rely on third parties to manufacture and supply terminals for end-users to access our services and, as a result, we cannot control the availability of such terminals.

Terminals used to access our services are built by a limited number of independent manufacturers. Although we provide manufacturers with key performance specifications for the terminals, these manufacturers could:

| • | reduce production of, or cease to manufacture, some of the terminals that access our services; |

| • | manufacture defective terminals that fail to perform to our specifications; |

| • | fail to build or upgrade terminals that meet end-users' requirements within our target sectors; |