Revenues

| Sales Revenue by Product | |

| | Three Months Ended March 31 |

| | 2017 | 2016 | Change |

| Light to medium oil sales | 20.1 | 22.9 | (12%) |

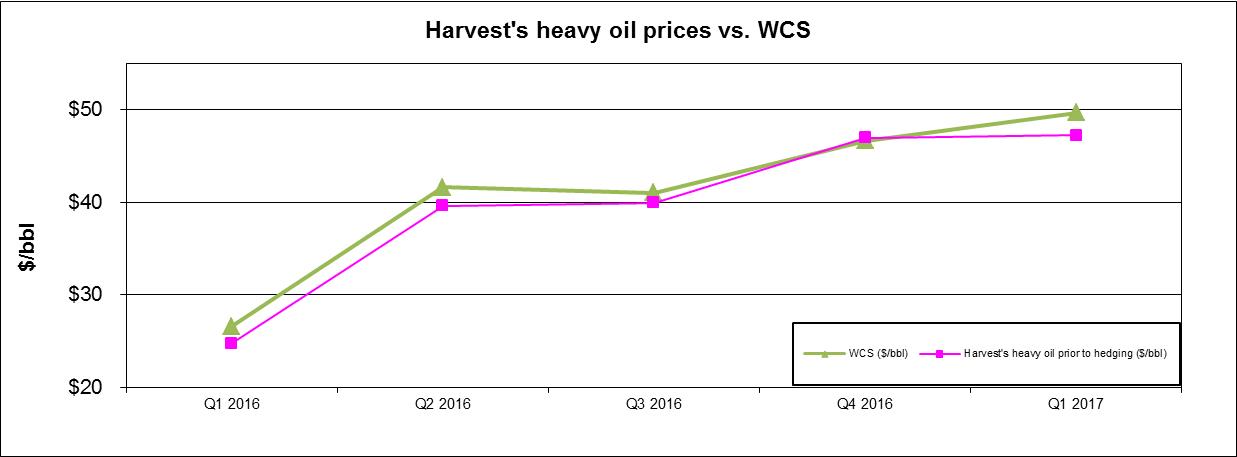

| Heavy oil sales | 33.0 | 22.8 | 45% |

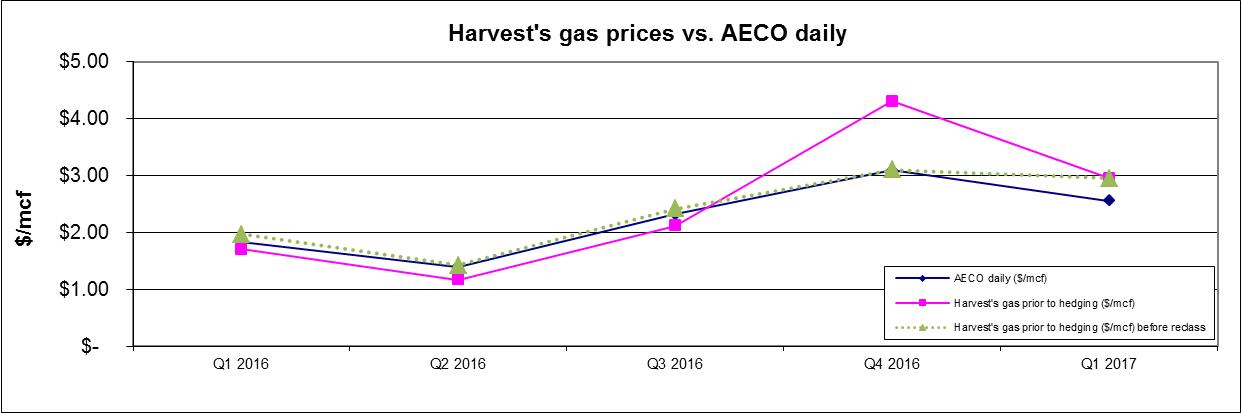

| Natural gas sales | 19.4 | 14.7 | 32% |

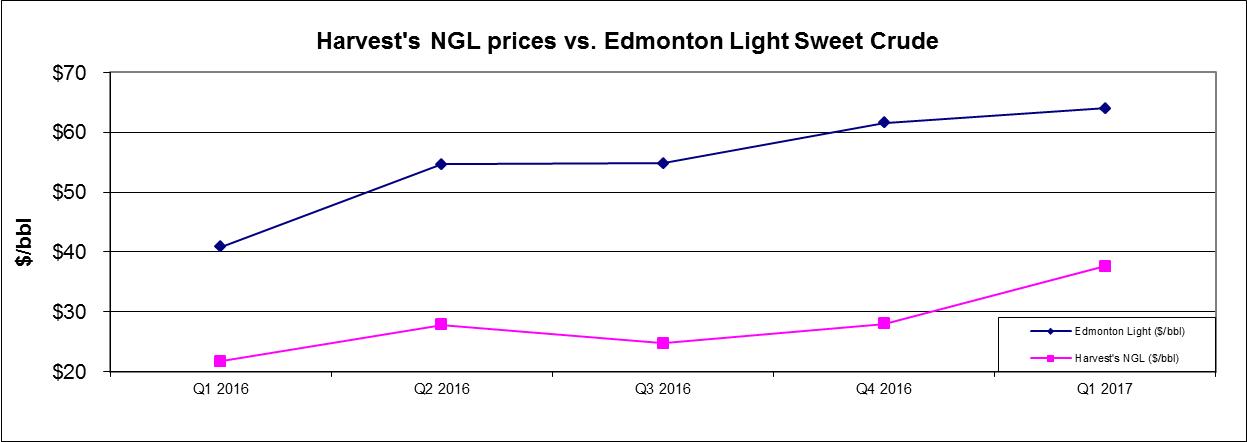

| Natural gas liquids sales | 11.7 | 7.7 | 52% |

Other(1) | 1.4 | 2.1 | (33%) |

| Petroleum and natural gas sales | 85.6 | 70.2 | 22% |

| Royalties | (8.3) | (5.8) | 43% |

| Revenues | 77.3 | 64.4 | 20% |

(1) Inclusive of sulphur revenue.

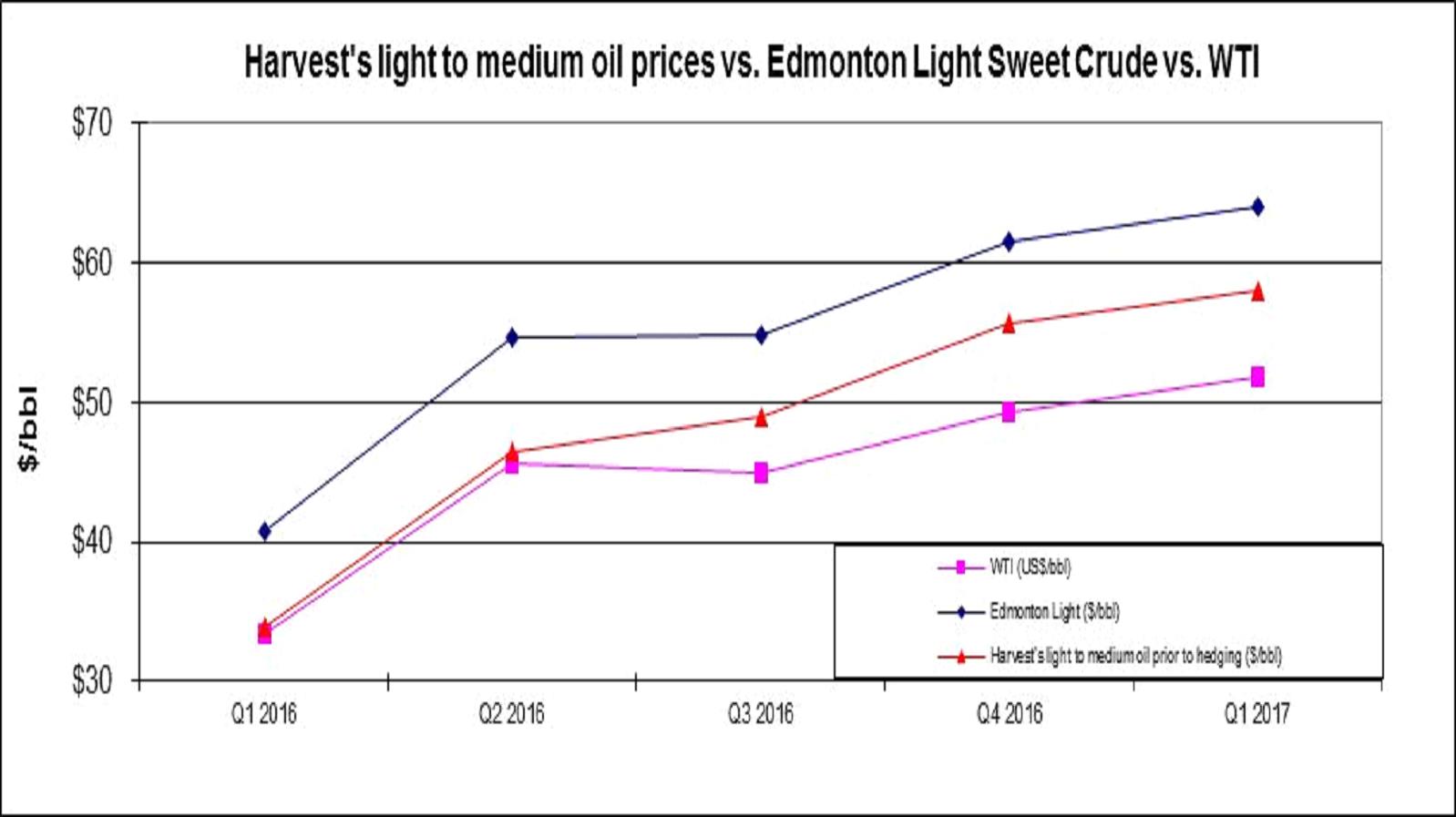

Harvest's revenue is subject to changes in sales volumes, commodity prices, currency exchange rates and hedging activities. Total petroleum and natural gas sales increased in the first quarter of 2017 as compared to 2016, mainly due to increased realized prices, partially offset by a decrease in production.

Sulphur revenue represented $1.4 million of the total in other revenues for the first quarter of 2017 (2016 - $2.1 million).

| Revenue by Product Type as % of Total Revenue |

| | Three Months Ended March 31 |

| | 2017 | 2016 |

| Light to medium oil sales | 23% | 33% |

| Heavy oil sales | 39% | 32% |

| Natural gas sales | 23% | 21% |

| Natural gas liquids sales | 14% | 11% |

| Other | 1% | 3% |

| Total Sales Revenue | 100% | 100% |

Although Harvest's product mix on a volumetric basis is slightly weighted heavier towards crude oil and natural gas liquids than natural gas, revenue contribution is more heavily weighted to crude oil and liquids as shown by the graphs above. Compared to the prior year period, revenue contributions by product has decreased in light oil sales, and increased in heavy oil sales, which is primarily the result of the disposition of light oil producing properties in Saskatchewan.

Royalties

Harvest pays Crown, freehold and overriding royalties to the owners of mineral rights from which production is generated. These royalties vary for each property and product and Crown royalties are based on various sliding scales dependent on incentives, production volumes and commodity prices.

For the first quarter ended March 31, 2017, royalties as a percentage of gross revenue averaged 9.7% (2016 – 8.3%). The increase in royalties as a percentage of gross revenue was mainly due to an increase in realized prices, and a reduction in Harvest's gas cost allowance related to prior periods.

Operating Expenses

| | | |

| | Three Months Ended March 31 |

| | 2017 | 2016 |

| | | |

| Operating expense | 38.4 | 46.7 |

| Operating expense ($/boe) | 15.67 | 13.89 |

Operating expenses for the first quarter of 2017 decreased by $8.3 million compared to the same period in 2016. The decrease was primarily due to the impact of asset dispositions which reduced overall operating expenditures.

Operating expenses on a per barrel basis increased by 13% to $15.67 per barrel for the first three months of 2017 when compared to the same period in 2016. This is primarily due to a reduction in volume base due to the effect of natural declines and dispositions since the first quarter of 2016.

For the first quarter of 2017 Power Pool Rates were $22.38 per megawatt hour (2016 - $18.09 per megawatt hour).

Transportation and Marketing Expense

| | | |

| | Three Months Ended March 31 |

| | 2017 | 2016 |

| | | |

| Transportation and marketing | 3.0 | 1.3 |

| Transportation and marketing ($/boe) | 1.23 | 0.39 |

Transportation and marketing expenses relate primarily to the cost of delivery of natural gas and natural gas liquids, and trucking crude oil to pipeline or rail receipt points. Transportation and marketing expenses in the first quarter of 2017 were $1.7 million higher in comparison to the same period in 2016. The increase was primarily due to gas transportation costs being presented on a gross basis, whereas in the first quarter of 2016, such costs were netted against gas revenues. If March 31, 2016 transportation costs had been presented on the same basis, then on a comparative perspective, transportation and marketing would have decreased $0.6 million in the first quarter of 2017 as compared to the same period in 2016.

Operating Netback(1)

| | Three Months Ended March 31 |

| ($/boe) | 2017 | 2016 | Change |

| Petroleum and natural gas | | | |

sales (2) | 34.91 | 20.86 | 14.05 |

| Royalties | (3.40) | (1.73) | (1.67) |

| Operating expenses | (15.67) | (13.89) | (1.78) |

| Transportation and marketing | (1.23) | (0.39) | (0.84) |

Operating netback prior to hedging(1) | 14.61 | 4.85 | 9.76 |

Hedging (loss) gain(3) | — | (0.14) | 0.14 |

Operating netback after hedging(1) | 14.61 | 4.71 | 9.90 |

| (1) | This is a non-GAAP measure; please refer to "Non-GAAP Measures" in this MD&A. |

| (2) | Excludes miscellaneous income not related to oil and gas production |

| (3) | Includes the settlement amounts for power contracts. |

For the quarter ended March 31, 2017 netback prior to hedging was $14.61 per boe representing an increase of 201 percent compared to the same period in 2016. The increase in period was mainly due to higher realized sales prices, partially offset by increased royalties, operating expenses, and transportation and marketing expenses on a per boe basis.

General and Administrative ("G&A") Expenses

| | Three Months Ended March 31 |

| | 2017 | 2016 | Change |

| Gross G&A expenses | 10.8 | 15.3 | (29%) |

| Capitalized G&A and recoveries | (1.1) | (0.5) | (120%) |

| Net G&A expenses | 9.7 | 14.8 | (34%) |

| Net G&A expenses ($/boe) | 3.93 | 4.40 | (11%) |

For the quarter ended March 31, 2017 G&A expenses net of capitalized G&A decreased $5.1 million, while gross G&A expenses decreased $4.5 million when compared to the same period in the prior year. During the first quarter of 2017, Harvest incurred an additional $2.6 million of G&A as the result of a change in estimate due to the settlement of an outstanding litigation. The decrease in the first quarter 2017 G&A expenses from the same period in the prior year was mainly due to decreases in salaries, employee benefits and severance charges related to staff reductions during 2016, which was partially offset by the litigation settlement revision. The increase in capitalized G&A is mainly related to increased capital spending in 2017.

On a per boe basis, G&A expenses decreased $0.47 in the first quarter of 2017 from the same period in the prior year mainly due to lower employee expenses as a result of lower staff levels, which was partially offset by the decline in sales volumes over the prior year.

Harvest does not have a stock option program, however there is a long-term incentive program which is a cash settled plan that has been included in the G&A expense.

Depletion, Depreciation and Amortization ("DD&A") Expenses

| | |

| | Three Months Ended March 31 |

| | 2017 | 2016 |

| DD&A | 38.3 | 74.7 |

| DD&A ($/boe) | 15.63 | 22.19 |

DD&A expense for the first quarter of 2017 decreased by $36.4 million as compared to the same period in 2016, mainly due to the change in estimate of decommissioning liabilities in the fourth quarter of 2016 which led to a reduction in the asset base for depletion in the first quarter of 2017.

Capital Asset Additions

| | Three Months Ended March 31 |

| | 2017 | 2016 |

| Drilling and completion | 9.1 | (0.2) |

| Well equipment, pipelines and facilities | 8.6 | 2.4 |

| Geological and geophysical | 0.7 | — |

| Corporate | 0.3 | (0.4) |

| Other | 0.9 | 0.3 |

| Total additions excluding acquisitions | 19.6 | 2.1 |

Total capital additions were higher for the first quarter of 2017 compared to 2016 mainly due to Harvest's winter drilling program initiated in the fourth quarter of 2016 which carried through the first quarter of 2017. Harvest's capital expenditures for the first three months of 2017 primarily related to the drilling and completion of new wells, and the addition of capital expenditures related to well equipment, pipelines and facilities.

During the first quarter of 2017 Harvest drilled a horizontal well in the Cecil area targeting light oil in the Charlie Lake formation, participated in two partner operated horizontal multi-stage fractured wells (1.0 net) in the Deep Basin area to develop the Falher gas formation, and one partner operated horizontal multi-stage fractured well (0.1 net) in the Rocky Mountain House area targeting light oil in the Cardium formation.

During the months ended March 31, 2017, Harvest's net undeveloped land additions were 9,095 acres (2016 – 5,566 acres), and net undeveloped land dispositions were nil (2016 – 7,586 acres).

Decommissioning Liabilities

Harvest's Conventional decommissioning liabilities at March 31, 2017 was $617.1 million (December 31, 2016 – $615.4 million) for future remediation, abandonment, and reclamation of Harvest's oil and gas properties. The total of the decommissioning liabilities are based on management's best estimate of costs to remediate, reclaim, and abandon wells and facilities. The increase in balance as at March 31, 2017 is mainly due to accretion and the addition of new wells rig released in the first quarter of 2017. The costs will be incurred over the operating lives of the assets with the majority being at or after the end of reserve life. Please refer to the "Contractual Obligations and Commitments" section of this MD&A for the payments expected for each of the next five years and thereafter in respect of the decommissioning liabilities.

Investments in Joint Ventures

Harvest has equity investments in Deep Basin Partnership ("DBP") and HK MS Partnership ("HKMS") joint ventures with KERR Canada Co. Ltd. ("KERR") which are accounted for as equity investments. Harvest derives its income or loss from its investments based upon Harvest's share in the change of the net assets of the joint venture. Harvest's share of the change in the net assets does not directly correspond to its ownership interest because of contractual preference rights to KERR and changes based on contributions made by either party during the year. For the three months ended March 31, 2017, Harvest recognized a loss of $3.8 million (2016 – $18.5 million) from its investment in the DBP and HKMS joint ventures.

Below is an overview of operational and financial highlights of the DBP and HKMS joint ventures for the three months ended March 31, 2017. Unless otherwise noted the following discussion relates to 100% of the joint venture results and not based on Harvest ownership share.

Deep Basin Partnership

DBP was established for the purposes of exploring, developing and producing certain oil and gas properties in the Deep Basin area in Northwest Alberta. During 2016 and in the three month ended March 31, 2017 Harvest made various contributions to the DBP that resulted in increase in its ownership percentage as reflected in the table below.

| | | | | | |

| | March 31, | December 31, | September 30, | June 30, | March 31, |

| | 2017 | 2016 | 2016 | 2016 | 2016 |

| Harvest's ownership interest | 82.50% | 82.32% | 82.03% | 82.00% | 81.98% |

| KERR's ownership interest | 17.50% | 17.68% | 17.97% | 18.00% | 18.02% |

| Total | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% |

As at March 31, 2017, the fair value of Harvest's top-up obligation to KERR, related to a minimum rate of return commitment was estimated as $7.4 million (December 31, 2016 - $6.7 million).

At March 31, 2017, Harvest received a total of $7.5 million (December 31, 2016 - $6.0 million) in distributions from the DBP from inception of the joint venture.

| | Three Months Ended March 31 |

| | 2017 | 2016 | Change |

| Natural gas liquids ($/bbl) | 55.13 | 29.33 | 88% |

| Natural gas ($/mcf) | 3.08 | 1.72 | 79% |

Average realized price ($/boe) (1) | 29.54 | 15.18 | 95% |

For the first quarter of 2017, average realized prices for natural gas liquids increased 88% over the same period in the prior year as a result of increases in benchmark prices.

In the fourth quarter of 2016, Harvest reclassified prior quarters' transportation charges previously netted against revenue that are now being presented on a gross basis. The increase in price for the first quarter of 2017 compared to the same period in 2016 for natural gas reflects both the strengthening of benchmark prices during the quarter plus the netting of transportation charges against revenue in the first quarter of 2016.

| | Three Months Ended March 31 |

| | 2017 | 2016 | Change |

| Natural gas (mcf/d) | 29,937 | 25,534 | 17% |

| Natural gas liquids (bbl/d) | 2,148 | 1,463 | 47% |

| Light to medium oil (bbl/d) | 3 | 1 | 200% |

| Total (boe/d) | 7,141 | 5,720 | 25% |

Harvest's share(1) | 5,892 | 4,689 | 26% |

(1) This is a non-GAAP measure; please refer to "Non-GAAP Measures" in this MD&A.

Sales volumes for the three months ended March 31, 2017 increased by 1,421 boe/d as compared to the same period in 2016. The increase was due to three new wells which were drilled in the fourth quarter of 2016 leading to new production in the first quarter of 2017.

| | | | |

| | Three Months Ended March 31 |

| | 2017 | 2016 | Change |

Revenues (2) | 17.4 | 7.6 | 129% |

| Operating expenses and Other | (10.1) | (7.1) | (41%) |

| Depletion, depreciation and amortization | (13.0) | (9.4) | (38%) |

| Finance costs | (0.7) | (0.7) | 0% |

| Impairment | — | (1.4) | 100% |

| Loss on disposition of assets | — | (9.8) | 100% |

Net loss(1) | (6.4) | (20.8) | 70% |

(1) Balances represent 100% share of the DBP.

(2) Revenue is presented net of royalties

The higher sales revenues in the first quarter of 2017 reflects higher commodity prices and higher volumes compared to the same period in the prior year.

Operating expenses and other expenses for the first quarter of 2017 were $15.74 per boe, an increase of $2.10 per boe from the same period in 2016. The increase was primarily due to gas transportation costs being presented on a gross basis, whereas in the first quarter of 2016, such costs were netted against gas revenues.

Depletion for the first quarter ended March 31, 2017 was $20.16 per boe (2016 – $18.06 per boe). The increase from prior year was primarily due to asset additions resulting from Deep Basin's winter drilling program.

| | | |

| | | |

| | Three Months Ended March 31 |

| | 2017 | 2016 |

| Drilling and completion | 5.9 | 6.3 |

| Well equipment, pipelines and facilities | 1.9 | 2.9 |

| Land and seismic | — | 0.1 |

Total (1) | 7.8 | 9.3 |

(1) Balances represent 100% share of the DBP.

Capital asset additions were $7.8 million in the three months ended March 31, 2017, mainly related to the completion and tie in activity of 3 wells rig released in 2016. During the first three months of 2017, Harvest rig released no new wells.

HKMS Partnership

The HKMS Partnership was formed for the purposes of constructing and operating a gas processing facility, which is primarily used to process the gas produced from the properties owned by the Deep Basin Partnership. A gas processing agreement was entered into by the two partnerships.

During 2016 and in the three months ended March 31, 2017 Harvest made various contributions to the HKMS Partnership that resulted in increases in its ownership percentage as reflected in the table below.

| | | | | | |

| | March 31, | December 31, | September 30, | June 30, | March 31, |

| | 2017 | 2016 | 2016 | 2016 | 2016 |

| Harvest's ownership interest | 70.25% | 70.23% | 70.21% | 70.19% | 70.15% |

| KERR's ownership interest | 29.75% | 29.77% | 29.79% | 29.81% | 29.85% |

| Total | 100.00% | 100.00% | 100.00% | 100.00% | 100.00% |

At March 31, 2017, Harvest received a total of $27.7 million (December 31, 2016 - $23.4 million) in distributions from HKMS from inception of the joint venture.

| | Three Months Ended March 31 |

| | 2017 | 2016 | Change |

| Revenues | 7.0 | 6.1 | 15% |

| Operating expenses and other | (1.0) | (0.5) | (100%) |

| Depreciation and amortization | (0.8) | (0.9) | 11% |

| Finance costs | (4.9) | (4.9) | 0% |

Net (loss) income (1) | 0.3 | (0.2) | 250% |

(1) Balances represent 100% share of HKMS.

The Gas Processing Agreement between HKMS and DBP ensures that HKMS receives an 18% internal rate of return on capital deployed over the term of the contract. In order to guarantee this return, DBP is required to provide HKMS with a minimum monthly capital fee that is currently $1.9 million a month. This capital fee is accounted for as revenue for HKMS and an operating expense for the DBP. In addition HKMS also generates revenue from charging an operating fee to recover operating expenses incurred. For the three months ended March 31, 2017 the partnership generated revenues of $7.0 million (2016 – $6.1 million).

Operating expenses of the facility are recovered through charging an operating fee to the producers. For the first quarter of 2017 the partnership's operating expenses and other were $1.0 million (2016 – $0.5 million).

Depreciation has been calculated on a straight-line basis over a 30 year useful life. Based on the capital expenditures incurred to date, the depreciation on a monthly basis is approximately $0.3 million per month. For the three months ended March 31, 2017 the partnership depreciation expense was $0.8 million (2016 –$0.9 million).

Finance costs mainly represent an accounting charge resulting from the Partner's contributions being classified as liabilities, as a result of the Gas Processing Agreement guaranteed returns. The finance costs represent the 18% rate of return on the partner's contributions. For the three months ended March 31, 2017 the partnership's financing costs were $4.9 million (2016 – $4.9 million).

See note 6 of the March 31, 2017 unaudited condensed interim consolidated financial statements for discussion of the accounting implications of these joint ventures.

OIL SANDS

Pre-operating Results

| | | |

| | Three Months Ended March 31 |

| | 2017 | 2016 |

| Expenses | | |

| Pre-operating | 3.0 | 3.8 |

| General and administrative | 0.4 | 0.5 |

| Depreciation and amortization | 0.1 | 0.2 |

Pre-Operating loss(1) | (3.5) | (4.5) |

(1) This is an non GAAP measure; please refer to "non-GAAP Measures" in this MD&A.

For the three months ended March 31, 2017, Harvest recognized a pre-operating loss of $3.5 million (2016 –$4.5 million) mainly relating to labour, power, maintenance and general and administrative expenses.

Capital Asset Additions

| | | |

| | Three Months Ended March 31 |

| | 2017 | 2016 |

| Well equipment, pipelines and facilities | 0.2 | — |

| Capitalized borrowing costs and other | — | 0.1 |

| Total Oil Sands additions | 0.2 | 0.1 |

The minimal capital spending during the first quarter of 2017 reflects a halt in Oil Sands activity since the first quarter of 2015. Over 2016, completion of sanctioning and commissioning activities was postponed due to the bitumen price environment. During 2017, Harvest plans to complete sanctioning and re-commence commissioning activities.

Decommissioning Liabilities

Harvest's Oil Sands decommissioning liabilities at March 31, 2017 was $48.9 million (December 31, 2016 - $48.6 million) relating to the future remediation, abandonment, and reclamation of the steam assisted gravity drainage ("SAGD") wells and CPF. The increase in this balance as at March 31, 2017 is due to accretion of the liability. Please see the "Contractual Obligations and Commitments" section of this MD&A for the payments expected for each of the next five years and thereafter in respect of the decommissioning liabilities.

Project Development

Harvest has been developing its Oil Sands CPF under the engineering, procurement and construction ("EPC") contract. Initial drilling of 30 SAGD wells (15 well pairs) was completed by the end of 2012 and the majority of the well completion activities were completed by the end of 2014. More SAGD wells will be drilled in the future to compensate for the natural decline in production of the initial well pairs and maintain the Phase 1 production capacity of 10,000 bbl/d. During the first quarter of 2015 construction had been substantially completed, including the building of the CPF plant site, well pads, and connecting pipelines. Several systems have since been commissioned and others will be progressed slowly within a limited budget. During 2017, Harvest plans to complete sanctioning and re-commence commissioning activities.

Harvest has recorded net $1,082.7 million of costs on the entire project since acquiring the Oil Sands assets in 2010. This $1,082.7 million includes certain Phase 2 pre-investment which is expected to improve the capital efficiency over the project lifecycle. Under the EPC contract, $94.9 million of the EPC costs will be paid in equal installments, without interest, over 10 years. Payments commenced during the second quarter of 2015 with two payments made on April 30, 2015. Harvest withheld the third deferred payment due April 30, 2016 as it is in process of conducting a comprehensive audit of costs and expenses incurred by the Contractor in connection with the work. The liability is considered a financial liability and is initially recorded at fair value, which is estimated as the present value of all future cash payments discounted using the prevailing market rate of interest for similar instruments. As at March 31, 2017, Harvest recognized a liability of $67.7 million (December 31, 2016 - $67.2 million) using a discount rate of 4.5% (December 31, 2016 - 4.5%).

As Harvest uses the unit of production method for depletion and the Oil Sands assets currently have no production, no depletion on the Oil Sands property, plant and equipment has been recorded. Minor depreciation has been recorded during the first quarter of 2017 on administrative assets.

RISK MANAGEMENT, FINANCING AND OTHER

Cash Flow Risk Management

The Company at times enters into natural gas, crude oil, electricity and foreign exchange contracts to reduce the volatility of cash flows from some of its forecast sales and purchases, and when allowable, will designate these contracts as cash flow hedges. The following is a summary of Harvest's derivative contracts outstanding at March 31, 2017:

| | | | | | |

| Contracts Not Designated as Hedges | |

| Contract Quantity | Type of Contract | Term/Expiry | Contract Price | Fair Value of asset | |

| US$290 million | Foreign exchange swap | April 2017 | $1.32 Cdn/US | | | 0.5 | |

| | | | | | $ | 0.5 | |

Harvest has entered into U.S. dollar currency swap transactions related to a LIBOR borrowings, which results in a reduction of interest expense paid on Harvest's borrowings related to its credit facility. As a result of these transactions, Harvest's effective interest rate for borrowings under the credit facility for the three months ended March 31, 2017 was 1.4% (2016 – 1.7%).

| | | | | | | | | | | | | | | | | | | | | | | | | |

| | | Three Months Ended March 31 | |

| | | 2017 | | | 2016 | |

| Realized (gains) losses | | | | | | | | Top-Up | | | | | | | | | | | | Top-Up | | | | |

| recognized in: | | Power | | | Currency | | | Obligation | | | Total | | | Power | | | Currency | | | Obligation | | | Total | |

| Derivative contract losses | | | — | | | | 1.1 | | | | — | | | | 1.1 | | | | 0.5 | | | | — | | | | — | | | | 0.5 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Unrealized (gains) losses | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| recognized in: | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | | |

| Derivative contract (gains) losses | | | — | | | | (0.6 | ) | | | 0.7 | | | | 0.1 | | | | 0.2 | | | | 0.8 | | | | (0.3 | ) | | | 0.7 | |

Finance Costs

| | | | |

| | Three Months Ended March 31 | |

| | 2017 | 2016 | |

Credit facility(1) | 4.2 | 5.0 | |

Term facility(1) | 3.1 | — | |

| 6⅞% senior notes | 6.8 | 12.6 | |

2⅛% senior notes(1) | 5.8 | 6.1 | |

2⅓% senior notes(1) | 1.8 | — | |

| Related party loans | — | 8.6 | |

| Amortization of deferred finance charges | | | |

| and other | 0.4 | 0.7 | |

| Interest and other financing charges | 20.1 | 33.0 | |

| Accretion of decommission and | | | |

| environmental remediation liabilities | 3.9 | 4.9 | |

| Accretion of long-term liability | 0.9 | 0.9 | |

| Total finance costs | 24.9 | 38.8 | |

| (1) | Includes guarantee fee to KNOC. |

Currency Exchange

| | | | |

| | Three Months Ended March 31 | |

| | 2017 | 2016 | |

| Realized gains on foreign exchange | (1.0) | (6.8) | |

| Unrealized gains on foreign exchange | (13.7) | (118.7) | |

| Total gains on foreign exchange | (14.7) | (125.5) | |

Currency exchange gains and losses are attributed to the changes in the value of the Canadian dollar relative to the U.S. dollar on the U.S. dollar denominated 6⅞%, 2⅛% and 2⅓% senior notes and on any U.S. dollar denominated monetary assets or liabilities. During the first quarter of 2016, Harvest also incurred foreign exchange gains and losses to the ANKOR and KNOC related party loans which were both settled by the end of that year. At March 31, 2017, the Canadian dollar had strengthened compared to the US dollar, resulting in an unrealized foreign exchange gain of $13.7 million for the first quarter of 2017 (2016 – $118.7 million). Harvest recognized a realized foreign exchange gain of $1.0 million for the first quarter of 2017 (2016 – $6.8 million) which was also a result of a stronger Canadian dollar.

Income Taxes

For the first quarter of 2017 Harvest recorded a deferred income tax recovery of $nil (2016 – $nil). Harvest's deferred income tax asset will fluctuate from time to time to reflect changes in the temporary differences between the book value and tax basis of assets and liabilities. The principal sources of temporary differences relate to the Company's property, plant and equipment, decommissioning liabilities and the unclaimed tax pools.

Related Party Transactions

The following provides a summary of the related party transactions between Harvest and KNOC for the quarter ended March 31, 2017:

Related party loans:

| | | | | | | | | |

| Related Party | | Principal | | | Interest Rate | | Three months ended March 31, 2016 | |

| KNOC | | US$171 | | | 5.91% | | $ | 2.5 | |

| KNOC | | $ | 200 | | | 5.30% | | | 3.4 | |

| ANKOR | | US$170 | | | 4.62% | | | 2.7 | |

| | | | | | | | | $ | 8.6 | |

As at March 31, 2017 and December 31, 2016 there were no related party loans outstanding

Other related party transactions and balances:

| | | | | | | | | | | | | |

| | | Transactions | | | Balance Outstanding | |

| | | Three months ended March 31 | | | Accounts payable as at | |

| | | 2017 | | | 2016 | | | March 31, 2017 | | | December 31, 2016 | |

| G&A Expenses | | | | | | | | | | | | |

KNOC(1) | | $ | 0.1 | | | $ | 0.1 | | | $ | 0.5 | | | $ | 0.4 | |

| | | | | | | | | | | | | | | | | |

| Finance costs | | | | | | | | | | | | | | | | |

KNOC(2) | | $ | 2.5 | | | $ | 2.3 | | | $ | 4.1 | | | $ | 1.7 | |

(1) | Amounts relate to the payments to (reimbursement from) KNOC for secondee salaries. |

(2) | Charges from KNOC for the irrevocable and unconditional guarantee they provided on Harvest's 2⅛% and 2⅓% senior notes, the credit facility and term loan. A guarantee fee of 52 basis points per annum is charged by KNOC on the 2⅛% senior notes and 37 basis points per annum on the 2⅓% senior notes. A guarantee fee of 37 basis points per annum is chanrged by KNOC on the credit facility and term loan. |

During the year ended December 31, 2016, Harvest entered into an agreement with KNOC to drill, complete and tie-in a well and provide technical data to KNOC. KNOC initially provided Harvest with $5.3 million as a cash advance to drill, complete and tie-in a well, and any additional amounts incurred relating to the well will be billed to KNOC for reimbursement up to a maximum of 9.4 billion Korean Won equivalent. During the three months ended March 31, 2017, an additional $5.3 million of expenditures were incurred on the well and earned for reimbursement from KNOC and recorded in contributed surplus (2016 - $nil). As at March 31, 2017, Harvest had a receivable of $5.4 million relating to this agreement from KNOC (December 31, 2016 - $0.1 million).

The Company identifies its related party transactions by making inquiries of management and the Board of Directors, reviewing KNOC's subsidiaries and associates, and performing a comprehensive search of transactions recorded in the accounting system. Material related party transactions require the Board of Directors' approval. Also see note 6, "Investment in Joint Ventures" in the March 31, 2017 unaudited consolidated interim financial statements for details of related party transactions with DBP and HKMS.

CAPITAL RESOURCES

The following table summarizes Harvest's capital structure and provides the key financial ratios defined in the credit facility agreement.

| | | |

| | March 31, 2017 | December 31, 2016 |

Credit facility(1) | 412.5 | 893.5 |

Term facility(1) | 500.0 | — |

6⅞% senior notes (US$282.5 million)(1)(2) | 375.6 | 379.3 |

2⅛% senior notes (US$630 million)(1)(2) | 837.8 | 845.9 |

2⅓% senior notes (US$195.8 million)(2) | 260.4 | 262.9 |

| | 2,386.3 | 2,381.6 |

| Shareholder's equity | | |

| 458,766,467 common shares issued | 78.6 | 104.0 |

| | 2,464.9 | 2,485.6 |

| (1) | Excludes capitalized financing fees |

| (2) | Face value converted at the period end exchange rate |

On February 17, 2017, Harvest entered an agreement with a Korean based bank that allowed Harvest to borrow $500 million through a three year fixed rate term loan. The proceeds from the term loan were used to repay credit facility borrowings. In addition, on February 24, 2017, Harvest entered into a new three year $500 million revolving credit facility with a syndicate of banks that replaced the Company's $1 billion revolving credit facility. Both the term loan and new syndicated revolving credit facility are guaranteed by KNOC. A guarantee fee of 37 basis points per annum payable semi-annually on the principal balance of each facility is payable to KNOC. The new syndicated revolving credit facility is secured by a first floating charge over all of the assets of Harvest and its material subsidiaries. Both facilities contain no financial covenants. Harvest continues to pay a floating interest rate based on a margin pricing grid based on the credit ratings of KNOC. The current rates are Canadian Dollar Offered Rate plus 90 basis point on Canadian dollar drawn balances and LIBOR plus 90 basis points on US dollar drawn balances.

LIQUIDITY

The Company's liquidity needs are met through the following sources: cash generated from operations, proceeds from asset dispositions, joint arrangements, borrowings under the credit facility, related party loans, long-term debt issuances and capital injections by KNOC. Harvest's primary uses of funds are operating expenses, capital expenditures, and interest and principal repayments on debt instruments.

Cash generated from operating activities for the three months ended March 31, 2017 was $9.9 million (2016 –$0.2 million). The increase in the first quarter of 2017 is mainly a result of increased revenues and reduced expenses partially offset by changes in working capital requirements.

Cash contributions from Harvest's Conventional operations for the first quarter and March 31, 2017 was $27.2 million (2016 – $0.8 million). The first quarter increase in cash contributions is primarily due to higher revenues, and lower operating costs, and general and administrative charges.

Harvest funded capital expenditures for the three months ended March 31, 2017 of $19.6 million (2016 – $2.2 million) with the proceeds of borrowings under the credit facility.

Harvest's net drawings from the credit facility and term loan was $17.2 million (2016 – $33.0 million net repayment) during the quarter ended March 31, 2017.

Harvest had a working capital deficiency of $476.5 million as at March 31, 2017, as compared to a $1,370.9 million deficiency at December 31, 2016. This change is primarily due to the replacement of the old credit facility with new three year term debt, and a new credit facility leading to a reclassification of debt from current to long term. Harvest is in consultation with KNOC about refinancing plans for the 6⅞% senior note due in October 2017. Harvest's working capital is expected to fluctuate from time to time, and will be funded from cash flows from operations and borrowings from the credit facility managing the collection and payment of accounts receivables and accounts payables respectively and using the proceeds from possible sale of assets, as required.

Harvest ensures its liquidity through the management of its capital structure, seeking to balance the amount of debt and equity used to fund investment in each of our operating segments. Harvest evaluates its capital structure using the same financial covenant ratios as the ones that were externally imposed under the Company's credit facility and the senior notes. The Company continually monitors its credit facility covenants and actively takes steps, such as reducing borrowings, increasing capitalization, amending or renegotiating covenants as and when required.

In response to improvements in the commodity price environment, Harvest has begun to reinvest in a conservatively budgeted drilling program, targeting specified core areas of development. In addition, Harvest is planning to complete sanctioning and re-commence commissioning activities on its Oil Sands project.

On February 17, 2017, Harvest entered an agreement with a Korean based bank that allowed Harvest to borrow $500 million through a three year fixed rate term loan. The proceeds from the term loan were used to repay credit facility borrowings. In addition, on February 24, 2017, Harvest entered into a new three year $500 million revolving credit facility with a syndicate of banks that replaced the Company's $1 billion revolving credit facility. Both the term loan and new syndicated revolving credit facility are guaranteed by KNOC. The new syndicated revolving credit facility is secured by a first floating charge over all of the assets of Harvest and its material subsidiaries and contains no financial covenants.

Harvest is a significant subsidiary for KNOC in terms of production and reserves. KNOC has directly or indirectly invested and provided financial support to Harvest since 2009 and, as at the date of preparation of this MD&A, it is the Company's expectation that such support will continue.

Contractual Obligations and Commitments

Harvest has recurring and ongoing contractual obligations and estimated commitments entered into in the normal course of operations. As at March 31, 2017, Harvest has the following significant contractual obligations and estimated commitments:

| | | | | | |

| | Payments Due by Period |

| | 1 year | 2-3 years | 4-5 years | After 5 years | Total |

Debt repayments(1) | 376.6 | 837.8 | 1,172.9 | — | 2,387.3 |

Debt interest payments(1) (2) | 62.0 | 71.6 | 24.6 | — | 158.2 |

Purchase commitments(3) | 20.5 | 19.0 | 19.0 | 34.2 | 92.7 |

| Operating leases | 6.7 | 16.2 | 16.9 | 26.8 | 66.6 |

| Firm processing commitments | 17.0 | 35.6 | 31.6 | 31.8 | 116.0 |

| Firm transportation agreements | 31.7 | 58.3 | 34.4 | 44.5 | 168.9 |

Employee benefits(4) | 0.5 | 0.3 | — | — | 0.8 |

| Decommissioning and environmental | | | | | |

liabilities(5) | 9.0 | 66.2 | 69.2 | 1,085.7 | 1,230.1 |

| Total | 524.0 | 1,105.0 | 1,368.6 | 1,223.0 | 4,220.6 |

(1) Assumes constant foreign exchange rate.

(2) Assumes interest rates as at March 31, 2017 will be applicable to future interest payments.

(3) Relates to the Oil Sands deferred payment under the EPC contract (see "Oil Sands" section of this MD&A for details), and revised estimated capital costs for the Bellshill area (see "Impairment of Property, Plant & Equipment" section of this MD&A for details).

(4) Relates to the long-term incentive plan payments.

(5) Represents the undiscounted obligation by period.

Off Balance Sheet Arrangements

See "Investments in Joint Ventures" section in this MD&A and note 6, "Investment in Joint Ventures" in the March 31, 2017 unaudited condensed interim consolidated financial statements.

SUMMARY OF QUARTERLY RESULTS

The following table and discussion highlights the first quarter of 2017 results relative to the preceding 8 quarters:

| | | | | | | | | |

| | | | | | | | | |

| | 2017 | 2016 | 2015 |

| | Q1 | Q4 | Q3 | Q2 | Q1 | Q4 | Q3 | Q2 |

| FINANCIAL | | | | | | | | |

| Revenue, Conventional | 77.3 | 84.4 | 65.8 | 72.7 | 64.4 | 97.1 | 120.4 | 130.8 |

| | | | | | | | | |

Net loss from continuing

operations | (30.7) | (162.5) | (106.9) | (65.7) | (13.1) | (894.2) | (588.7) | (87.0) |

Net loss from discontinued operations(1) | — | — | — | — | — | (15.5) | — | — |

| Net loss | (30.7) | (162.5) | (106.9) | (65.7) | (13.1) | (909.7) | (588.7) | (87.0) |

| | | | | | | | | |

| OPERATIONS | | | | | | | | |

| Continuing Operations | | | | | | | | |

Daily sales volumes (boe/d)(3) | 27,226 | 26,589 | 30,051 | 34,440 | 36,986 | 38,141 | 43,356 | 41,716 |

Realized price prior to hedging ($/boe)(2) | 34.91 | 37.06 | 28.03 | 26.50 | 20.86 | 27.89 | 31.47 | 37.85 |

(1) Relates to a purchase price adjustment from Downstream operations which has been classified as "Discontinued Operations" as a result of prior period disposition on November 13, 2014.

(2) Excludes volumes from the DBP

The quarterly revenues and cash from operating activities are mainly impacted by the Conventional sales volumes, realized prices and operating expenses. Significant items that impacted Harvest's quarterly revenues include:

| · | Total revenues were highest in the second quarter of 2015, as a result of high daily sales volumes and lowest in the first quarter of 2016 due to reduced commodity prices. |

| · | The declines in Conventional's sales volumes from the first quarter of 2015 to the fourth quarter of 2016 were mainly due to asset dispositions and a capital program that was insufficient to offset declines in production. Harvest began reinvesting in the drilling of new wells in the fourth quarter of 2016, resulting in an increase in volumes for the first quarter of 2017. |

Net loss reflects both cash and non-cash items. Changes in non-cash items include deferred income tax, DD&A expense, accretion of decommissioning and environmental remediation liabilities, accretion of onerous contracts, impairment of long-lived assets, unrealized foreign exchange gains and losses, and unrealized gains and losses on derivative contracts impact net loss from period to period. For these reasons, the net loss may not necessarily reflect the same trends as revenues or cash from operating activities, nor is it expected to. The net loss from continuing operations for the first quarter of 2017 is primarily the result of lower realized prices and sales volumes. The net loss from continuing operations in the fourth quarter of 2016 is mainly a result of a $17.4 million write off of exploration and evaluation assets, and $51.8 million of foreign exchange losses on the company's U.S. denominated debt. The net loss from continuing operations in the third quarter of 2016 is mainly a result of lower realized prices and sales volumes. The net loss from continuing operations in the second quarter of 2016 is mainly a result of lower realized prices and sales volumes, and a $10.6 million loss from joint ventures. The net loss from continuing operations in the first quarter of 2016 is mainly a result of lower realized prices and sales volumes, and an $18.5 million loss from joint ventures. The net loss from continuing operations in the fourth quarter of 2015 is mainly a result of lower realized prices and sales volumes, a $620.1 million impairment expense, and a $71.5 million loss from joint ventures. The net loss from continuing operations in the third quarter of 2015 is mainly a result of lower realized prices and sales volumes and a $542.0 million impairment expense. The net loss from continuing operations in the second quarter of 2015 is mainly a result of a result of lower realized prices and sales volumes and a $70.7 million impairment expense. The net loss from continuing operations in the first quarter of 2015 was mainly a result of lower realized prices and sales volumes, a $140.5 million foreign exchange loss and a $23.5 million impairment expense.

CRITICAL ACCOUNTING ESTIMATES

The preparation of financial statements in conformity with IFRS requires management to make judgments, estimates and assumptions that affect the application of accounting policies and the reported amounts of assets, liabilities, income and expenses. Actual results may differ from these estimates. Estimates and underlying assumptions are reviewed on an ongoing basis. Revisions to accounting estimates are recognized in the period in which the estimates are revised and in any future periods affected. Harvest has identified the following areas where significant estimates and judgments are required. Further information on the basis of preparation and significant accounting policies and estimates can be found in the notes to the audited consolidated financial statements for the year ended December 31, 2016. There have been no changes to the accounting policies and critical accounting estimates in the first quarter of 2017.

RECENT ACCOUNTING PRONOUNCEMENTS

Future Accounting Policy Changes

On May 28, 2014, the IASB issued IFRS 15 "Revenue from Contracts with Customers", which specifies how and when to recognize revenue as well as requiring entities to provide users of financial statements with more disclosure. In April 2016, the IASB issued its final amendments that provide new examples and clarification on how the principles should be applied. The standard supersedes IAS 18 "Revenue", IAS 11 "Construction Contracts", and related interpretations. IFRS 15 will be effective for annual periods beginning January 1, 2018. Application of the standard is mandatory and early adoption is permitted. IFRS 15 will be applied by Harvest on January 1, 2018. The Company has created a project plan and is currently in the process of reviewing its various revenue streams and underlying contracts with customers to determine the impact, if any, that the adoption of IFRS 15 will have on its financial statements, as well as the impact that adoption of the standard will have on disclosure.

On July 24, 2014, the IASB issued IFRS 9 "Financial Instruments" to replace IAS 39 "Financial Instruments: Recognition and Measurement". IFRS 9 includes revised guidance on the classification and measurement of financial instruments, including a new expected credit loss model for calculating impairment on financial assets, and the new general hedge accounting. No changes were introduced for the classification and measurement of financial liabilities, except for the recognition of changes in own credit risk in other comprehensive income for liabilities designated at fair value through profit or loss. IFRS 9 is effective for years beginning on or after January 1, 2018. Harvest has created a plan and is currently evaluating the impact of adopting IFRS 9 on its consolidated financial statements.

In January 2016, the IASB issued IFRS 16 "Leases" to replace IAS 17 "Leases". IFRS 16 requires lessees to recognize most leases on the statement of financial position using a single recognition and measurement model. IFRS 16 will be effective for annual periods beginning on or after January 1, 2019, with earlier adoption permitted if the entity is also applying IFRS 15. IFRS 16 will be applied by Harvest on January 1, 2019 and the Company is currently evaluating the impact on its consolidated financial statements.

OPERATIONAL AND OTHER BUSINESS RISKS FOR CONTINUING OPERATIONS

Harvest's operational and other business risks remain unchanged from those discussed in the annual MD&A and AIF for the year ended December 31, 2016 as filed on SEDAR at www.sedar.com.

CHANGES IN REGULATORY ENVIRONMENT

Harvest's regulatory environment remains unchanged from that discussed in the annual MD&A and AIF for the year ended December 31, 2016 as filed on SEDAR at www.sedar.com.

INTERNAL CONTROL OVER FINANCIAL REPORTING

Harvest is required to comply with National Instrument 52-109 "Certification of Disclosure in Issuers' Annual and Interim Filings". The certificate requires that Harvest disclosure in the interim MD&A any significant changes or material weaknesses in Harvest's internal control over financial reporting that occurred during the period that have materially affected, or are reasonably likely to materially affect Harvest's internal controls over financial reporting. Harvest confirms that no such significant changes or weaknesses were identified in Harvest's internal controls over financial reporting during the first quarter of 2017 described in the annual MD&A for the year ended December 31, 2016 as filed on SEDAR at www.sedar.com.

NON-GAAP MEASURES

Throughout this MD&A, Harvest uses certain terms or performance measure commonly used in the oil and natural gas industry that are not defined under IFRS (hereinafter also referred to as "GAAP"). These non-GAAP measures do not have any standardized meaning prescribed by IFRS and therefore may not be comparable with the calculation of similar measures of other companies. The data presented is intended to provide additional information and should not be considered in isolation or as a substitute for measures of performance prepared in accordance with IFRS. These non-IFRS measures should be read in conjunction with the Company's audited consolidated financial statements and the accompanying notes. The determination of the non-GAAP measures have been illustrated throughout this MD&A, with reconciliations to IFRS measures and/or account balances, except for cash contribution (deficiency) which is shown below.

BOE presentation

Boe means barrel of oil equivalent. All boe conversions in this MD&A are derived by converting gas to oil at the ratio of six thousand cubic feet ("Mcf") of natural gas to one barrel ("Bbl") of oil. Boe may be misleading, particularly if used in isolation. A Boe conversion rate of 1 Bbl : 6 Mcf is based on an energy equivalency conversion method primarily applicable at the burner tip and does not represent a value equivalency at the wellhead. Given that the value ratio of oil compared to natural gas based on currently prevailing prices is significantly different than the energy equivalency ratio of 1 Bbl : 6 Mcf, utilizing a conversion ratio of 1 Bbl : 6 Mcf may be misleading as an indication of value.

"Operating income (loss)" and "pre-operating loss" is a non-GAAP measure which Harvest uses as a performance measure to provide comparability of financial performance between periods excluding non-operating items. Harvest also uses this measure to assess and compare the performance of its operating segments. The amounts disclosed in the MD&A reconcile to segmented information in the financial statements.

"Operating netbacks" is calculated on a per boe basis and include revenues, operating expenses, transportation and marketing expenses, and realized gains or losses on derivative contracts. Operating netback is utilized by Harvest and other to analyze the operating performance of its oil and natural gas assets.

"Cash contribution (deficiency) from operations" is calculated as operating income (loss) adjusted for non-cash items. The measure demonstrates the ability of the each segment of Harvest to generate the cash from operations necessary to repay debt, make capital investments, and fund the settlement of decommissioning and environmental remediation liabilities. Cash contribution (deficiency) from operations represents operating income (loss) adjusted for non-cash expense items within: operating, general and administrative, exploration and evaluation, depletion, depreciation and amortization, gains on disposition of assets, derivative contracts gains or losses, impairment and other charges, and the inclusion of cash interest, realized foreign exchange gains or losses and other cash items not included in operating income (loss). The measure demonstrates the ability of Harvest's Conventional segment to generate cash from operations and is calculated before changes in non-cash working capital. The most directly comparable additional GAAP measure is operating income (loss). Operating income (loss) as presented in the notes to Harvest's consolidated financial statements is reconciled to cash contribution (deficiency) from operations below.

| | | | | | | |

| | | | | | | |

| | Three Months Ended March 31 |

| | Conventional | Oil Sands | Total |

| | 2017 | 2016 | 2017 | 2016 | 2017 | 2016 |

| Operating loss | (17.0) | (95.3) | (3.5) | (4.5) | (20.5) | (99.8) |

| Adjustments: | | | | | | |

| Loss from joint ventures | 3.8 | 18.5 | — | — | 3.8 | 18.5 |

| Operating, non-cash | — | 0.2 | — | — | — | 0.2 |

| General and administrative, non-cash | 2.1 | (0.5) | — | — | 2.1 | (0.5) |

| Exploration and evaluation, non-cash | — | 2.1 | — | — | — | 2.1 |

| Depletion, depreciation and amortization | 38.3 | 74.7 | 0.1 | 0.2 | 38.4 | 74.9 |

| Losses on disposition of assets | 0.3 | 0.4 | — | — | 0.3 | 0.4 |

| Unrealized losses on derivative contracts | 0.1 | 0.7 | — | — | 0.1 | 0.7 |

| Recovery on onerous contract | (0.4) | — | — | — | (0.4) | — |

| Cash contribution (deficiency) from operations | 27.2 | 0.8 | (3.4) | (4.3) | 23.8 | (3.5) |

| Inclusion of items not attributable to segments: | | | | | | |

| Net cash interest | | | | | (19.0) | (24.0) |

| Realized foreign exchange gains | | | | | 1.0 | 6.8 |

| Consolidated cash contribution from operations | | | 5.8 | (20.7) |

| Other non-cash items | | | | | (0.4) | (3.3) |

| Change in non-cash working capital | | | | | 4.5 | 24.2 |

| Cash used in operating activities | | | 9.9 | 0.2 |

FORWARD-LOOKING INFORMATION

This MD&A highlights significant business results and statistics from the consolidated financial statements for the three months ended March 31, 2017 and the accompanying notes thereto. In the interest of providing Harvest's lenders and potential lenders with information regarding Harvest, including the Company's assessment of future plans and operations, this MD&A contains forward-looking statements that involve risks and uncertainties.

Such risks and uncertainties include, but are not limited to: risks associated with conventional petroleum and natural gas operations; risks associated with the construction of the oil sands project; the volatility in commodity prices, interest rates and currency exchange rates; risks associated with realizing the value of acquisitions; general economic, market and business conditions; changes in environmental legislation and regulations; the availability of sufficient capital from internal and external sources; and, such other risks and uncertainties described from time to time in regulatory reports and filings made with securities regulators. The impact of any one risk, uncertainty or factor on a particular forward-looking statement is not determinable with certainty as these factors are interdependent, and management's future course of action would depend on the assessment of all information at that time. Please also refer to "Operational and Other Business Risks" in this MD&A and "Risk Factors" in the Annual Information Form for detailed discussion on these risks.

Forward-looking statements in this MD&A include, but are not limited to: commodity prices, price risk management activities, acquisitions and dispositions, capital spending and allocation of such to various projects, reserve estimates and ultimate recovery of reserves, potential timing and commerciality of Harvest's capital projects, the extent and success rate of Conventional and Oil Sands drilling programs, the ability to achieve the maximum capacity from the Oil Sands central processing facilities, availability of the credit facility, access and ability to raise capital, ability to maintain debt covenants, debt levels, recovery of long-lived assets, the timing and amount of decommission and environmental related costs, income taxes, cash from operating activities, regulatory approval of development projects and regulatory changes. For this purpose, any statements that are contained herein that are not statements of historical fact may be deemed to be forward-looking statements. Forward-looking statements often contain terms such as "may", "will", "should", "anticipate", "expect", "target", "plan", "potential", "intend", and similar expressions.

All of the forward-looking statements in this MD&A are qualified by the assumptions that are stated or inherent in such forward-looking statements. Although Harvest believes that these assumptions are reasonable based on the information available to us on the date such assumptions were made, this list is not exhaustive of the factors that may affect any of the forward-looking statements and the reader should not place an undue reliance on these assumptions and such forward-looking statements. The key assumptions that have been made in connection with the forward-looking statements include the following: that the Company will conduct its operations and achieve results of operations as anticipated; that its development plans and sustaining maintenance programs will achieve the expected results; the general continuance of current or, where applicable, assumed industry conditions; the continuation of assumed tax, royalty and regulatory regimes; the accuracy of the estimates of the Company's reserve volumes; commodity price, operation level, and cost assumptions; the continued availability of adequate cash flow and debt and/or equity financing to fund the Company's capital and operating requirements as needed; and the extent of Harvest's liabilities. Harvest believes the material factors, expectations and assumptions reflected in the forward-looking statements are reasonable, but no assurance can be given that these factors, expectations and assumptions will prove to be correct.

Although management believes that the forward-looking information is reasonable based on information available on the date such forward-looking statements were made, no assurances can be given as to future results, levels of activity and achievements. Therefore, readers are cautioned not to place undue reliance on forward-looking statements as the plans, intentions or expectations upon which the forward-looking information is based might not occur. Forward-looking statements contained in this MD&A are expressly qualified by this cautionary statement.

ADDITIONAL INFORMATION

Further information about us can be accessed under our public filings found on SEDAR at www.sedar.com or at www.harvestenergy.ca. Information can also be found by contacting our Investor Relations department at (403) 265-1178 or at 1-866-666-1178.