QuickLinks -- Click here to rapidly navigate through this documentAs filed with the Securities and Exchange Commission on December 3, 2004

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-4

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

FOUNDATION PA COAL COMPANY

(Exact name of registrant issuer as specified in its charter)

Delaware

(State or other jurisdiction of

incorporation or organization)

1221

(Primary Standard Industrial

Classification Code Number)

42-1638663

(I.R.S. Employer

Identification Number) | | FOUNDATION COAL CORPORATION

(Exact name of registrant parent guarantor as specified in its charter)

Delaware

(State or other jurisdiction of

incorporation or organization)

1221

(Primary Standard Industrial

Classification Code Number)

26-0085077

(I.R.S. Employer

Identification Number) |

| | | |

SEE TABLE OF ADDITIONAL GUARANTOR REGISTRANTS

999 Corporate Boulevard

Suite 300

Linthicum Heights, Maryland 21090-2227

(410) 689-7600

(Address, including zip code, and telephone number, including area code, of registrant's principal executive offices)

Greg A. Walker, Esq.

General Counsel

Foundation Coal Holdings, Inc.

999 Corporate Boulevard

Suite 300

Linthicum Heights, Maryland 21090-2227

(410) 689-7500

(Name and address, including zip code, of agent for service) |

With a copy to: |

Edward P. Tolley III, Esq.

Simpson Thacher & Bartlett LLP

425 Lexington Avenue

New York, New York 10017-3954

(212) 455-2000 |

Approximate date of commencement of proposed sale to the public:

As soon as practicable after this registration statement becomes effective.

If the securities being registered on this form are being offered in connection with the formation of a holding company and there is compliance with General Instruction G. please check the following box. o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective filed pursuant to Rule 462(d) under the Securities Act check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

CALCULATION OF REGISTRATION FEE

|

Title of Each Class of

Securities to be Registered

| | Amount to

be Registered

| | Proposed Maximum

Offering Price

Per Note

| | Proposed Maximum

Aggregate

Offering Price(1)

| | Amount of

Registration Fee

|

|---|

|

| 71/4% Senior Notes due 2014 | | $300,000,000 | | 100% | | $300,000,000 | | $38,010 |

|

| Guarantees of 71/4% Senior Notes Due 2014 | | N/A(2) | | (2) | | (2) | | (2) |

|

- (1)

- Estimated solely for the purpose of calculating the registration fee under Rule 457(f) of the Securities Act of 1933, as amended (the "Securities Act").

- (2)

- Pursuant to Rule 457(n) under the Securities Act, no separate filing fee is required for the guarantees.

The registrants hereby amend this Registration Statement on such date or dates as may be necessary to delay its effective date until the registrants shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933 or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

TABLE OF CO-REGISTRANTS

Name

| | State or other

jurisdiction of

incorporation

or organization

| | I.R.S.

Employer

Identification

Number

|

|---|

| Alliance Power Marketing, Inc. | | Delaware | | 93-1155825 |

| Barbara Holdings Inc. | | Delaware | | 25-1292326 |

| Castle Gate Holding Company | | Delaware | | 84-1456620 |

| Coal Gas Recovery, LP | | Delaware | | 30-0210759 |

| Cumberland Coal Resources, LP | | Delaware | | 84-1521723 |

| Delta Mine Holding Company | | Delaware | | 91-1897558 |

| Emerald Coal Resources, LP | | Delaware | | 84-1521724 |

| Foundation American Coal Company, LLC | | Delaware | | 54-1947356 |

| Foundation American Coal Holding, Inc. | | Delaware | | 13-2793319 |

| Foundation Coal Development Corporation | | Delaware | | 84-1341308 |

| Foundation Coal Resources Corporation | | Delaware | | 84-1341308 |

| Foundation Coal West, Inc. | | Delaware | | 35-1867616 |

| Foundation Energy Sales, Inc. | | Delaware | | 84-1130962 |

| Foundation Equipment Company | | Delaware | | 84-1152493 |

| Foundation Midwest Holding Company | | Delaware | | 84-1456626 |

| Foundation Royalty Company | | Delaware | | 84-1456627 |

| Foundation Wyoming Land Company | | Delaware | | 35-1661756 |

| Freeport Mining, LP | | Delaware | | 84-1521725 |

| Freeport Resources Corporation | | Delaware | | 84-1230391 |

| Laurel Creek Co., Inc. | | Delaware | | 31-1241957 |

| Maple Meadow Mining Company | | Delaware | | 55-0529664 |

| Pennsylvania Land Holdings Corporation | | Delaware | | 84-1452626 |

| Pennsylvania Services Corporation | | Delaware | | 93-1162601 |

| Plateau Mining Corporation | | Delaware | | 95-3761213 |

| River Processing Corporation | | Delaware | | 84-1199433 |

| Riverton Coal Production, Inc. | | Delaware | | 55-0739658 |

| Rockspring Development, Inc. | | Delaware | | 31-1241956 |

| Wabash Mine Holding Company | | Delaware | | 91-1897559 |

| Warrick Holding Company | | Delaware | | 91-1897557 |

| Energy Development Corporation | | West Virginia | | 25-1209977 |

| Kingston Mining, Inc. | | West Virginia | | 31-1562659 |

| Kingston Processing, Inc. | | West Virginia | | 55-0756214 |

| Kingston Resources, Inc. | | Kentucky | | 61-1093577 |

| Neweagle Coal Sales Corp. | | Virginia | | 54-1695745 |

| Neweagle Development Corp. | | Virginia | | 54-1695747 |

| Neweagle Industries, Inc. | | Virginia | | 54-1695751 |

| Neweagle Mining Corp. | | Virginia | | 54-1695750 |

| Odell Processing Inc. | | West Virginia | | 55-0708613 |

| Paynter Branch Mining, Inc. | | West Virginia | | 55-0746860 |

| Pioneer Fuel Corporation | | West Virginia | | 55-0545211 |

| Pioneer Mining, Inc. | | West Virginia | | 55-0746859 |

| Red Ash Sales Company, Inc. | | West Virginia | | 55-0515479 |

| Rivereagle Corp. | | Virginia | | 54-1695746 |

| Riverton Capital Ventures I, Limited Liability Company | | West Virginia | | 55-0746861 |

| Riverton Capital Ventures II, Limited Liability Company | | West Virginia | | 55-0746862 |

| Riverton Coal Sales, Inc. | | West Virginia | | 55-0748037 |

| Ruhrkohle Trading Corporation | | West Virginia | | 55-0266080 |

| Simmons Fork Mining, Inc. | | West Virginia | | 31-1537134 |

| Southern Resources, Inc. | | West Virginia | | 55-0548442 |

The information in this prospectus is not complete and may be changed. We may not sell the securities until the registration statement filed with the Securities and Exchange Commission is effective. This prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state where the offer or sale is not permitted.

Subject to Completion dated December 3, 2004

PRELIMINARY PROSPECTUS

Foundation PA Coal Company

Offers to Exchange

$300,000,000 principal amount of its 71/4% Senior Notes due 2014, which have been registered under the Securities Act of 1933, for any and all of its outstanding 71/4% Senior Notes due 2014.

The exchange notes will be fully and unconditionally guaranteed on an unsecured basis by Foundation Coal Corporation and each of its wholly owned direct and indirect subsidiaries, other than Foundation PA Coal Company (the "Issuer"), that guarantee the Issuer's obligations under the senior credit facilities.

The Issuer is conducting the exchange offer in order to provide you with an opportunity to exchange your unregistered notes for freely tradeable notes that have been registered under the Securities Act.

The Exchange Offer

- •

- The Issuer will exchange all outstanding notes that are validly tendered and not validly withdrawn for an equal principal amount of exchange notes that are freely tradeable.

- •

- You may withdraw tenders of outstanding notes at any time prior to the expiration date of the exchange offer.

- •

- The exchange offer expires at 12:00 a.m., midnight, New York City time on , 2005 unless extended.

- •

- The exchanges of outstanding notes for exchange notes in the exchange offer will not be a taxable event for U.S. federal income tax purposes.

- •

- The terms of the exchange notes to be issued in the exchange offer are substantially identical to the outstanding notes except that the exchange notes will be freely tradeable.

All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indenture. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer the Issuer does not currently anticipate that the Issuer will register the outstanding notes under the Securities Act.

See "Risk Factors" beginning on page 18 for a discussion of certain risks that you should consider before participating in the exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of the exchange notes to be distributed in the exchange offer or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is , 2004.

You should rely only on the information contained in this prospectus. We have not authorized anyone to provide you with different information. We are not making an offer of these securities in any state where the offer is not permitted.

TABLE OF CONTENTS

| | Page

|

|---|

| Prospectus Summary | | 1 |

| Risk Factors | | 18 |

| Special Note Regarding Forward-Looking Statements | | 36 |

| Use of Proceeds | | 37 |

| Market and Industry Data and Forecasts | | 37 |

| Capitalization | | 38 |

| Unaudited Consolidated Pro Forma Financial Information | | 39 |

| Selected Historical Consolidated Financial Data | | 45 |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | | 51 |

| The Coal Industry | | 80 |

| Business | | 86 |

| Environmental and Other Regulatory Matters | | 100 |

| Management | | 104 |

| Security Ownership of Certain Beneficial Owners | | 113 |

| Certain Relationships and Related Party Transactions | | 115 |

| Description of Other Indebtedness | | 118 |

| The Exchange Offer | | 121 |

| Description of Notes | | 132 |

| United States Federal Income Tax Consequences of the Exchange Offer | | 187 |

| ERISA Considerations | | 188 |

| Plan of Distribution | | 190 |

| Legal Matters | | 191 |

| Experts—Independent Registered Public Accounting Firm | | 191 |

| Experts—Coal Reserves | | 191 |

| Where You Can Find Additional Information | | 191 |

| Glossary of Selected Terms | | 192 |

| Index to Financial Statements | | F-1 |

i

PROSPECTUS SUMMARY

The following summarizes information contained elsewhere in this prospectus and does not contain all of the information you should consider in making your investment decision. You should read this summary together with the more detailed information, including our financial statements and the related notes, elsewhere in this prospectus. You should carefully consider, among other things, the matters discussed in "Risk Factors."

Unless the context otherwise indicates, as used in this prospectus, (i) the terms "we," "our," "us" and similar terms refer to Foundation Coal Corporation and its consolidated subsidiaries, (ii) the term "Issuer" refers to Foundation PA Coal Company and (iii) the term "Guarantors" refers to Foundation Coal Corporation and its direct and indirect wholly owned subsidiaries, other than the Issuer, each of which guarantee on a senior unsecured basis the obligations of the Issuer under the senior credit facilities. Foundation Coal Corporation, which is a wholly-owned subsidiary of Foundation Coal Holdings, Inc., was formed on April 23, 2004 to acquire the North American coal mining assets of RAG Coal International AG, which acquisition closed on July 30, 2004. All references to Foundation Coal Corporation, including the business description, operating data and financial data, exclude RAG Coal International AG's former Colorado operations, which were sold to a third party on April 15, 2004 and are accounted for herein as discontinued operations. References to pro forma financial and other pro forma information give effect to the repayment of a portion of our term loan with proceeds from our parent company's initial public offering of common stock as if such repayment had occurred on September 30, 2004 for balance sheet data and on January 1, 2003 for statement of operations and other data. Certain statements in this Prospectus Summary are forward-looking statements. All references herein to financial data for the nine months ended September 30, 2004 are presented on a pro forma basis for Foundation Coal Corporation by aggregating the financial data for the two months ended September 30, 2004 of Foundation Coal Corporation with the financial data for the seven months ended July 29, 2004 of RAG American Coal Holding, Inc.

The Company

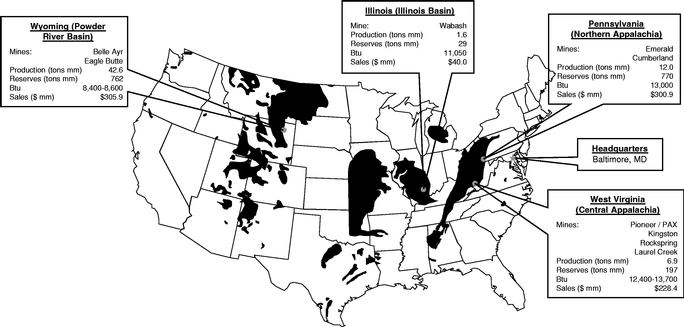

We are the fourth largest coal producer in the United States, with operations in the four major coal producing regions in the United States: the Powder River Basin, Northern Appalachia, Central Appalachia and the Illinois Basin. Our primary business is to produce, process and sell steam coal, which we sell to producers of electric power, the majority of whom are large U.S.-based utilities with an investment grade credit rating. We also produce and process metallurgical coal for use in the manufacture of steel.

For the year ended December 31, 2003 and the nine months ended September 30, 2004, we sold 67.2 million tons of coal and 47.4 million tons of coal, respectively, to approximately 85 customers. We generated total revenues of $994.3 million and $734.2 million, respectively, for such periods. As of December 31, 2003, we controlled approximately 1.8 billion tons of proven and probable coal reserves located in the Powder River Basin, Northern Appalachia, Central Appalachia and Illinois Basin. Based on these reserve estimates and our actual rate of production during the year ended December 31, 2003, we have a total reserve life of approximately 28 years. We are the only producer with significant operations and major reserve blocks in both the Powder River Basin and Northern Appalachia, the two U.S. coal production regions for which future demand is expected to have the largest increase, according to the EIA.

We employ a variety of different mining techniques at our nine underground mines and four surface mines. A number of these mines are among the most productive coal producers in the regions in which they operate, due to, among other things, our employment of advanced longwall technologies and truck-and-shovel systems. Our current management team has successfully managed our operations as a stand-alone subsidiary of RAG Coal International AG since 1999 and has continued to manage our operations since we became an independent company on July 30, 2004.

1

We have a large, geographically diverse reserve base which contains a broad range of coal qualities. Our reserves in Wyoming and West Virginia contain compliance coal, which does not require our customers to use sulfur dioxide reduction technologies (commonly referred to as scrubbers) to comply with the requirements of the Clean Air Act, and other low sulfur coal. Demand for clean burning, lower sulfur coal has grown significantly since the adoption of the Clean Air Act. Our reserves in Pennsylvania contain high Btu coal, which produces a greater amount of energy per ton when burned, but which results in higher sulfur emissions than compliance coal. A significant number of utilities have installed or recently initiated plans to install scrubbers and would thus be able to more efficiently burn higher sulfur coals. In addition, other utilities can utilize higher sulfur coal through their use of coal blending or purchased emissions allowances. As a result of the broad range of characteristics and qualities of our reserves, we are positioned to serve our customers in all the major segments of the market.

We operate our business through four segments: the Powder River Basin, Northern Appalachia, Central Appalachia and Other. The table below summarizes our revenues from coal sales, tons of coal sold and proven and probable coal reserves by segment as of December 31, 2003:

Revenues from Coal Sales, Tons Sold and Reserves by Segment

| | Year Ended December 31, 2003

| |

| |

|

|---|

Segment

| | Revenues

| | %

| | Tons Sold(1)

| | %

| | Reserves

| | %

| | Btu

| | Coal Quality

|

|---|

| | (Dollars and Tons in Millions)

| |

| |

|

|---|

| Powder River Basin | | $ | 303.5 | | 31 | % | 42.6 | | 63 | % | 761.6 | | 43 | % | Low | | Compliance |

| Northern Appalachia | | | 326.4 | | 33 | % | 13.2 | | 20 | % | 769.8 | | 44 | % | High | | Medium sulfur |

| Central Appalachia | | | 270.7 | | 28 | % | 8.2 | | 12 | % | 197.2 | | 11 | % | High | | Compliance, low sulfur

and metallurgical |

| Other | | | 75.4 | | 8 | % | 3.2 | | 5 | % | 29.0 | | 2 | % | Mid | | Medium sulfur |

| | |

| |

| |

| |

| |

| |

| | | | |

| Total | | $ | 976.0 | | 100 | % | 67.2 | | 100 | % | 1,757.6 | | 100 | % | | | |

| | |

| |

| |

| |

| |

| |

| | | | |

- (1)

- Central Appalachia tons include 1.5 million tons of produced metallurgical coal that accounted for $56.9 million of revenues and 0.7 million tons of metallurgical coal that was purchased and resold. Other tons include 1.6 million tons of Illinois Basin production and 1.6 million tons of coal that were purchased and resold.

Competitive Strengths

We believe that the following competitive strengths enhance our prominent market position in the United States:

We are the fourth largest coal producer in the United States and have a significant reserve base. Based on 2003 production of 64.0 million tons, we are the fourth largest coal producer in the United States. As of December 31, 2003, we controlled approximately 1.8 billion tons of proven and probable coal reserves. Based on these reserve estimates and our actual rate of production during the year ended December 31, 2003, we have a total reserve life of approximately 28 years.

We have a diverse portfolio of coal-mining operations and reserves. We operate a total of 13 mines in the Powder River Basin, Northern Appalachia, Central Appalachia and the Illinois Basin, selling coal to approximately 85 domestic and foreign electric utilities, steel producers and industrial users. We are the only producer with significant operations and major reserve blocks in both the Powder River Basin and Northern Appalachia, the two U.S. coal production regions for which future demand is expected to have the largest increase, according to the EIA. We believe that this geographic diversity provides us with a significant competitive advantage, allowing us to source coal from multiple regions to meet the needs of our customers and reduce their transportation costs.

2

We operate highly productive mines and have had strong EBITDA margins. We believe our focus on productivity has helped contribute to our strong EBITDA margins for fiscal years ended 2001, 2002 and 2003. Our strategic investment in equipment and technology has increased the efficiency of our operations, which we believe reduces our costs and provides us with a competitive advantage. Maintaining our low-cost position enables us to maximize our profitability in all coal pricing environments.

We are a recognized industry leader in safety and environmental performance. Our focus on safety and environmental performance results in a lower likelihood of disruption of production at our mines, which leads to higher productivity and improved financial performance. We operate some of the nation's safest mines, with 2003 injury incident rates, as tracked by the Mine Safety and Health Administration ("MSHA"), below industry averages.

We have long-standing relationships and long-term contracts with many of the largest coal-burning utilities in the United States. We supply coal to approximately 100 power plants operated by more than 70 electricity generators in 29 states across the country. We believe we have a reputation for reliability and superior customer service that has enabled us to solidify our customer relationships.

Our management team has a track record of success during our long operating history. Our management team has a proven record of generating free cash flow, increasing productivity, reducing costs, developing and maintaining long-standing customer relationships and effectively positioning us for future growth and profitability. We operated as a stand-alone subsidiary of privately held RAG Coal International AG from 1999 until becoming an independent company on July 30, 2004. Our senior executives have an average of approximately 26 years of experience in the coal industry, including an average of 13 years operating our assets when owned by us and our predecessors, and have the management and organizational capability to successfully operate an independent public company.

Business Strategy

Our objective is to increase shareholder value through sustained earnings and cash flow growth. Our key strategies to achieve this objective are described below:

Maintaining our commitment to operational excellence as a low-cost producer. We seek to maintain our productivity leadership with an emphasis on lowering costs by continuing to invest selectively in new equipment and advanced technologies, such as our previous investments in underground diesel, increased longwall face widths and a larger shield system. We will continue to focus on profitability and efficiency by leveraging our significant economies of scale, large fleet of mining equipment, information technology systems and coordinated purchasing and land management functions. In addition, we continue to focus on productivity through our culture of workforce involvement by leveraging our strong base of experienced, well-trained employees.

Capitalizing on favorable industry dynamics through an opportunistic approach to selling our coal. The fundamentals of the current U.S. coal market are among the strongest in the past decade resulting in a favorable coal pricing environment which, based on current coal forward prices, we believe will continue for the foreseeable future. We employ an opportunistic approach to selling our coal, including the use of long-term sales commitments for a portion of our future production while maintaining uncommitted planned production to capitalize on favorable future pricing environments.

Selectively expanding our production and reserve base. Given our broad scope of operations and expertise in mining in each of the major coal-producing regions in the United States, we believe that we are well-situated to capitalize on the expected continued growth in U.S. and international coal consumption by evaluating growth opportunities, including (i) expansion of production capacity at our existing mining operations, (ii) further development of existing significant reserve blocks in Northern Appalachia and Central Appalachia, and (iii) potential strategic acquisition opportunities that arise in

3

the United States or internationally. We will prudently act to manage our reserve base when appropriate. For example, we currently plan to seek to increase our reserve position by obtaining mining rights to federal coal reserves adjoining our current operations in Wyoming through the lease by application process.

Continuing to provide a mix of coal types and qualities to satisfy our customers' needs. By having operations and reserves in the four major coal producing regions, we are able to source coal from multiple mines to meet the needs of our domestic and international customers. Our broad geographic scope and mix of coal qualities provide us with the opportunity to work with many leading electricity generators, steel companies and other industrial customers across the country.

Continuing to focus on excellence in safety and environmental stewardship. We intend to maintain our recognized leadership in operating some of the safest mines in the United States and in achieving recognized standards of environmental excellence. Our ability to minimize lost-time injuries and environmental violations improves our operating efficiency, which directly improves our cost structure and financial performance.

Risks Related to our Business and Strategy

Our ability to execute our strategy is subject to certain risks that are generally associated with the coal industry. For example, our profitability could decline due to changes in coal prices or coal consumption patterns, as well as unanticipated mine operating conditions, loss of customers, changes in the ability to access our coal reserves and other factors that are not within our control. Furthermore, we operate in a heavily regulated industry, which imposes significant actual and potential costs on us, and future regulations could increase those costs or limit our ability to produce coal. For additional risks relating to our business or this offering, see "Risk Factors" beginning on page 19 of this prospectus.

Coal Market Outlook

According to coal indices and reference prices, U.S. and international coal fundamentals are currently strong, and coal pricing in 2004 has increased over 2003 in every significant U.S. and international market. We believe that the current strong fundamentals in the U.S. coal industry are supported primarily by:

- •

- stronger industrial demand following a recovery in the U.S. manufacturing sector, demonstrated by the most recent estimate of 3.7% real GDP growth in the third quarter of 2004, as reported by the Bureau of Economic Analysis;

- •

- low coal stockpiles, estimated by the EIA to be approximately 126 million tons in the second quarter of 2004, down 16% from the same period a year ago;

- •

- limited incremental capacity available from U.S. nuclear-powered electricity generators, with average utilization estimated by the EIA to be 88.4% in 2003, up from 70.5% in 1993;

- •

- high current and forward prices for natural gas and oil, the primary competing fuels for electricity generation, with spot prices at November 8, 2004 for natural gas and heating oil at $6.74 per million Btu and $1.35 per gallon, respectively, as reported by Bloomberg L.P.; and

- •

- increased international demand for U.S. coal for steelmaking, driven by global economic growth, high ocean freight rates from other countries and the weaker U.S. dollar.

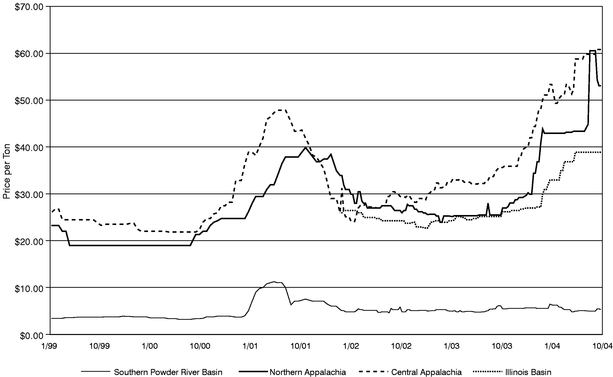

During 2003, U.S. spot steam coal prices began to strengthen and have steadily increased since mid-2003, particularly for coals sourced in the eastern United States. The table below describes year-to-date average reference prices for coal at November 1, 2004, compared to year-to-date average

4

reference prices in November 2003, according to Platts, and the percentage of our 2003 coal sales revenue by region:

| | Increase in Average

Reference Prices

| | Percentage of 2003 Coal Sales Revenue

| |

|---|

| Powder River Basin (Southern) | | 6 | % | 31 | % |

| Northern Appalachia | | 72 | % | 33 | % |

| Central Appalachia | | 61 | % | 28 | % |

| Illinois Basin | | 39 | % | 4 | % |

We expect near-term volume growth in U.S. coal consumption to be driven by a number of factors, including increased growth in electricity consumption and greater utilization at existing coal-fired plants, which operated at an estimated 71% of capacity in 2003, according to Platts. If the existing U.S. coal-fired plants operated at estimated potential utilization rates of 85%, we believe they would consume approximately 200 million additional tons of coal per year, which represents an increase of approximately 18% over current coal consumption.

We expect longer-term volume growth in U.S. coal consumption to be driven by the construction of new coal-fired plants. The NETL projects that 74,000 megawatts of new coal-fired electric generation capacity will be constructed in the United States by 2025, which would represent a 22% increase over current U.S. coal-fired electric generation capacity. The NETL has identified 94 coal-fired plants, representing 62,000 megawatts of electric generation capacity, which have been proposed and are currently in various stages of development. The DOE projects that 58 of these proposed coal-fired plants, representing 38,000 megawatts of electric generation capacity, will be completed and will begin consuming coal to produce electricity by the end of 2010.

The Transactions

On July 30, 2004, Foundation Coal Corporation completed the acquisition, which we refer to as the Acquisition, of all of the outstanding shares of capital stock of certain subsidiaries (the "Acquired Companies") of RAG Coal International AG (the "Seller"), consisting primarily of its then-North American coal operations, for a purchase price of approximately $975 million. We issued new 71/4% Senior Notes due 2014 (the "Notes") and entered into a new senior secured credit facility consisting of a term loan facility and revolving credit facility (the "Senior Credit Facilities"), the net proceeds of which were used to finance the Acquisition and to provide for an on-going working capital requirement. The term "Transactions" means, collectively, the Acquisition and the related financings, including the Notes and the Senior Credit Facilities. Affiliates of each of First Reserve Corporation ("First Reserve"), The Blackstone Group ("Blackstone") and American Metals and Coal International, Inc. ("AMCI") currently own approximately 42.0%, 42.0% and 14.8% of Foundation Coal Holdings, Inc., the ultimate parent of Foundation Coal Corporation, respectively and, after giving effect to our parent's initial public offering, will own 19.7%, 19.7% and 6.9%, respectively (assuming no exercise of the over-allotment option). First Reserve, Blackstone and AMCI are collectively referred to herein as the "Sponsors."

Recent Developments

New Commitments Negotiated at Higher Prices. Through October 31, 2004, we have been able to leverage our long-standing customer relationships and uncommitted planned production to enter into new sales commitments for long-term supply contracts at average sales prices above those realized in the past year. The table below illustrates our realized prices for produced tons sold in the period between September 30, 2003 and September 30, 2004 by region, as well as the average committed price per ton by region for the 2005 to 2008 period for both new commitments secured in the first ten months of 2004, as well as for all commitments obtained as of October 31, 2004. As of October 31,

5

2004, we had sales commitments in place for approximately 100% of our planned 2004 production, approximately 97% of our planned 2005 production and approximately 83% of our planned 2006 production. We have uncommitted planned production for 2005 and 2006 of 3% and 17%, respectively, most of which is in our eastern regions. We expect that due to the quality and expected market price of the uncommitted tonnage, this production will generate an even greater proportion of our revenues.

| | Average

Sale Price

Per Ton

(September 30, 2003-

September 30, 2004)

| | Year to Date New Commitments as of

October 31, 2004 for Years 2005-2008

| | Total Commitments as of

October 31, 2004 for Years 2005-2008

|

|---|

| | Price Per Ton

| | Tons

| | Price Per Ton

| | Tons

|

|---|

| | (Tons in Thousands)

|

|---|

| Powder River Basin | | $ | 7.44 | | $ | 6.51 | | 48,564 | | $ | 7.15 | | 151,281 |

| Northern Appalachia | | | 26.59 | | | 33.36 | | 20,750 | | | 31.69 | | 31,193 |

| Central Appalachia | | | | | | | | | | | | | |

| | Steam Coal | | | 31.28 | | | 45.03 | | 824 | | | 34.65 | | 13,428 |

| | Metallurgical/

Industrial Coal | | | 40.69 | | | 69.28 | | 2,528 | | | 64.76 | | 2,815 |

6

THE EXCHANGE OFFER

In this prospectus, the term "outstanding notes" refers to the 71/4% senior notes due 2014; the term "exchange notes" refers to the 71/4% senior notes due 2014 such as registered under the Securities Act of 1933, as amended (the "Securities Act"); the term "notes" refers to both the outstanding notes and exchange notes. On July 30, 2004, the Issuer issued an aggregate of $300,000,000 principal amount of 71/4% senior notes due 2014 in a private offering.

General |

|

In connection with the private offering, the Issuer and the Guarantors entered into a registration rights agreement with the initial purchasers in which they agreed, among other things, to deliver this prospectus to you and to complete the exchange offer within 270 days after the date of first issuance of the outstanding notes. You are entitled to exchange in the exchange offer your outstanding notes for exchange notes which are identical in all material respects to the outstanding notes except: |

|

|

• |

|

the exchange notes have been registered under the Securities Act; |

|

|

• |

|

the exchange notes are not entitled to any registration rights which are applicable to the outstanding notes under the registration rights agreement; and |

|

|

• |

|

the liquidated damages provisions of the registration rights agreement are no longer applicable. |

The Exchange Offer |

|

The Issuer is offering to exchange; |

|

|

• |

|

$300,000,000 principal amount of its 71/4% Senior Notes due 2014, which have been registered under the Securities Act for any and all of its outstanding 71/4% Senior Notes due 2014. |

|

|

You may exchange outstanding notes in integral multiples of $1,000. |

Resale |

|

Based on an interpretation by the staff of the Securities and Exchange Commission (the "SEC") set forth in no-action letters issued to third parties, the Issuer believes that the exchange notes issued pursuant to the exchange offer in exchange for outstanding notes may be offered for resale, resold and otherwise transferred by you (unless you are our "affiliate" within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that: |

|

|

• |

|

you are acquiring the exchange notes in the ordinary course of your business; and |

|

|

• |

|

you have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person to participate in, a distribution of the exchange notes. |

| | | | | |

7

|

|

If you are a broker-dealer and receive exchange notes for your own account in exchange for outstanding notes that you acquired as a result of market-making activities or other trading activities, you must acknowledge that you will deliver this prospectus in connection with any resale of the exchange notes. See "Plan of Distribution." |

|

|

Any holder of outstanding notes who; |

|

|

• |

|

is an affiliate of the Issuer or the Guarantors; |

|

|

• |

|

does not acquire exchange notes in the ordinary course of its business; or |

|

|

• |

|

tenders its outstanding notes in the exchange offer with the intention to participate, or for the purpose of participating, in a distribution of exchange notes |

|

|

cannot rely on the position of the staff of the SEC enunciated inMorgan Stanley & Co. Incorporated (available June 5, 1991) andExxon Capital Holdings Corporation (available May 13, 1988), as interpreted in the SEC's letter toShearman & Sterling, dated available July 2, 1993, or similar no-action letters and, in the absence of an exemption therefrom, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with any resale of the exchange notes. |

Expiration Date |

|

The exchange offer will expire at 12:00 a.m. midnight, New York City time on , 2005, unless extended by us. The Issuer and the Guarantors do not currently intend to extend the expiration date. |

Withdrawal |

|

You may withdraw the tender of your outstanding notes at any time prior to the expiration of the exchange offer. The Issuer and the Guarantors will return to you any of your outstanding notes that are not accepted for any reason for exchange without expense to you, promptly after the expiration or termination of the exchange offer. |

Conditions to the Exchange Offer |

|

The exchange offer is subject to customary conditions, which the Issuer and the Guarantors may waive. See "The Exchange Offer—Conditions to the Exchange Offer." |

Procedures for Tendering Outstanding Notes |

|

If you wish to participate in the exchange offer, you must complete, sign and date the applicable accompanying letter of transmittal, or a facsimile of such letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal. You must then mail or otherwise deliver the applicable letter of transmittal, or a facsimile of such letter of transmittal, together with the outstanding notes and any other required documents, to the exchange agent at the address set forth on the cover page of the letter of transmittal. |

| | | | | |

8

|

|

If you hold outstanding notes through The Depository Trust Company ("DTC") and wish to participate in the exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC, by which you will agree to be bound by the letter of transmittal. By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things: |

|

|

• |

|

you are not our "affiliate" within the meaning of Rule 405 under the Securities Act or, if you are our affiliate, that you will comply with any applicable registration and prospectus delivery requirements of the Securities Act; |

|

|

• |

|

you do not have an arrangement or understanding with any person or entity to participate in the distribution of the exchange notes; |

|

|

• |

|

you are acquiring the exchange notes in the ordinary course of your business; and |

|

|

• |

|

if you are a broker-dealer that will receive exchange notes for your own account in exchange for outstanding notes that were acquired as a result of market-making activities, that you will deliver a prospectus as required by law in connection with any resale of such exchange notes. |

Special Procedures for Beneficial Owners |

|

If you are a beneficial owner of outstanding notes that are registered in the name of a broker, dealer, commercial bank, trust company or other nominee, and you wish to tender those outstanding notes in the exchange offer, you should contact the registered holder promptly and instruct the registered holder to tender those outstanding notes on your behalf. If you wish to tender on your own behalf, you must, prior to completing and executing the applicable letter of transmittal and delivering your outstanding notes, either make appropriate arrangements to register ownership of the outstanding notes in your name or obtain a properly completed bond power from the registered holder. The transfer of registered ownership may take considerable time and may not be able to be completed prior to the expiration date. |

Guaranteed Delivery Procedures |

|

If you wish to tender your outstanding notes and your outstanding notes are not immediately available or you cannot deliver your outstanding notes, the applicable letter of transmittal or any other required documents, or you cannot comply with the applicable procedures under DTC's Automated Tender Offer Program for transfer of book-entry interests, prior to the expiration date, you must tender your outstanding notes according to the guaranteed delivery procedures set forth in this prospectus under "The Exchange Offer—Guaranteed Delivery Procedures." |

| | | | | |

9

Effect on Holders of Outstanding Notes |

|

As a result of the making of, and upon acceptance for exchange of all validly tendered outstanding notes pursuant to the terms of the exchange offer, the Issuer and the Guarantors will have fulfilled a covenant under the registration rights agreement. Accordingly, there will be no increase in the interest rate on the outstanding notes under the circumstances described in the registration rights agreements. If you do not tender your outstanding notes in the exchange offer, you will continue to be entitled to all the rights and limitations applicable to the outstanding notes as set forth in the indenture, except the Issuer and the Guarantors will not have any further obligation to you to provide for the exchange and registration of the outstanding notes under the applicable registration rights agreement. To the extent that outstanding notes are tendered and accepted in the exchange offer, the trading market for outstanding notes could be adversely affected. |

Consequences of Failure to Exchange |

|

All untendered outstanding notes will continue to be subject to the restrictions on transfer set forth in the outstanding notes and in the indenture. In general, the outstanding notes may not be offered or sold, unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, the Issuer and the Guarantors do not currently anticipate that they will register the outstanding notes under the Securities Act. |

U.S. Federal Income and Tax Consequences |

|

The exchange of outstanding notes in the exchange offer will not be a taxable event for United States federal income tax purposes. See "United States Federal Income Tax Consequences of the Exchange Offer." |

Use of Proceeds |

|

The Issuer will not receive any cash proceeds from the issuance of exchange notes in the exchange offer. See "Use of Proceeds." |

Exchange Agent |

|

The Bank of New York is the exchange agent for the exchange offer. The addresses and telephone numbers of the exchange agent are set forth in the section captioned "The Exchange Offer—Exchange Agent" of this prospectus. |

10

Exchange Notes

The summary below describes the principal terms of the exchange notes. Some of the terms and conditions described below are subject to important limitations and exceptions. You should carefully read the "Description of Notes" section of this prospectus for a more detailed description of the terms of the exchange notes.

Issuer |

|

Foundation PA Coal Company. |

Notes Offered |

|

$300,000,000 aggregate principal amount of 71/4% Senior Notes due 2014. |

Maturity Date |

|

August 1, 2014. |

Guarantees |

|

Foundation Coal Corporation and each of its wholly owned direct and indirect subsidiaries, other than the Issuer, that guarantee the Issuer's obligations under the senior credit facilities will guarantee the exchange notes on a senior unsecured basis. |

Interest Payment Dates |

|

Interest will be payable in cash on February 1 and August 1 of each year, beginning on February 1, 2005. |

Ranking |

|

The exchange notes will be unsecured senior obligations of the Issuer and will rank equally with all of its existing and future senior unsecured debt, and senior to any of its subordinated debt. The guarantees of the exchange notes will rank equally to all of such Guarantors' existing and future senior unsecured obligations. The exchange notes and the guarantees thereof will be effectively subordinated to all secured indebtedness of the Issuer and the Guarantors to the extent of the assets securing such indebtedness. As of September 30, 2004, on a pro forma basis after giving effect to the repayment of a portion of our term loan with a portion of the proceeds from our ultimate parent's initial public offering, the Issuer and the Guarantors would have had $425.6 million of secured debt. |

|

|

See "Summary Historical and Pro Forma Financial Data" and "Capitalization." |

Optional Redemption |

|

The Issuer may redeem some or all of the exchange notes at any time on or after August 1, 2009 at the redemption prices set forth under "Description of Notes—Optional Redemption." |

|

|

Additionally, the Issuer may redeem some or all of the exchange notes prior to August 1, 2009 at a price equal to 100% of the principal amount plus a "make-whole" premium as set forth under "Description of Notes—Optional Redemption." |

|

|

The Issuer may redeem up to 35% of the exchange notes on or prior to August 1, 2007 from the proceeds of certain equity offerings at 107.25% of the principal amount, plus accrued and unpaid interest, if any, to the date of redemption. The Issuer may make that redemption only if, after the redemption, at least 65% of the aggregate principal amount of the exchange notes originally issued remains outstanding and the redemption occurs within 180 days of the date of the equity offering closing. See "Description of Notes—Optional Redemption." |

| | | | | |

11

Change of Control Offer |

|

Upon the occurrence of a change of control, you will have the right, as holders of the exchange notes, to require the Issuer to repurchase some or all of your notes at 101% of their principal amount, plus accrued and unpaid interest, if any, to the repurchase date. See "Description of Notes—Repurchase at the Option of Holders—Change of Control." |

Certain Covenants |

|

The indenture governing the exchange notes contains covenants limiting, among other things, the ability of Foundation Coal Corporation and the ability of its restricted subsidiaries to: |

|

|

• |

|

incur additional debt; |

|

|

• |

|

pay dividends on its capital stock or repurchase its capital stock; |

|

|

• |

|

make certain investments; |

|

|

• |

|

enter into certain types of transactions with affiliates; |

|

|

• |

|

limit dividends or other payments by its restricted subsidiaries to it and its other restricted subsidiaries; |

|

|

• |

|

use assets as security in other transactions; and |

|

|

• |

|

sell certain assets or merge with or into other companies. |

|

|

These covenants are subject to important exceptions and qualifications. See "Description of Notes." |

No Public Market |

|

The exchange notes will be freely transferable but will be new securities for which there will not initially be a market. Accordingly, there is no assurance that a market for the exchange notes will develop or as to the liquidity of any market. The initial purchasers in the private offering of the outstanding notes have advised the Issuer that they currently intend to make a market in the exchange notes. The initial purchasers are not obligated, however, to make a market in the exchange notes, and any such market-making may be discontinued by the initial purchasers in their discretion at any time without notice. |

Additional Information

Our principal executive office is located at 999 Corporate Boulevard, Suite 300, Linthicum Heights, Maryland 21090 and our telephone number is (410) 689-7500.

Risk Factors

Investment in the exchange notes involves certain risks. You should carefully consider the information in the "Risk Factors" section and all other information included in this prospectus before investing in the exchange notes.

12

Summary Historical and Pro Forma Financial Data

The following summary historical financial data as of and for the years ended December 31, 2003, 2002 and 2001 have been derived from the audited consolidated financial statements of RAG American Coal Holding, Inc. (our predecessor), which have been audited by Ernst & Young LLP, an independent registered public accounting firm. The summary historical financial data of our predecessor as of and for the period from January 1, 2004 to July 29, 2004 and for the nine months ended September 30, 2003 have been derived from the unaudited consolidated financial statements of RAG American Coal Holding, Inc., which have been prepared on a basis consistent with the audited consolidated financial statements as of and for the year ended December 31, 2003. The summary historical financial data as of and for the period from April 23, 2004 (our date of inception) to September 30, 2004 have been derived from the unaudited consolidated financial statements of Foundation Coal Corporation. In the opinion of management, such unaudited financial data reflect all adjustments, consisting only of normal and recurring adjustments, necessary for a fair presentation of the results for those periods. The results of operations for the interim periods are not necessarily indicative of the results to be expected for the full year or any future period. The audited consolidated financial statements as of and for the years ended December 31, 2003, 2002 and 2001 and the unaudited consolidated financial statements as of and for the nine months ended September 30, 2003, the period from January 1, 2004 to July 29, 2004 and the period from April 23, 2004 to September 30, 2004 are included elsewhere in this prospectus.

The following summary unaudited pro forma consolidated financial data of Foundation Coal Corporation and its subsidiaries as of and for the year ended December 31, 2003 and the nine months ended September 30, 2004 have been prepared to give pro forma effect to the Transactions and the repayment of a portion of our term loan with proceeds from our ultimate parent company's initial public offering, as if they had occurred on January 1, 2003, in the case of unaudited pro forma statement of operations data, and to the repayment of a portion of our term loan with proceeds from our ultimate parent company's initial public offering, as if it had occurred on September 30, 2004, in the case of unaudited pro forma balance sheet data. The successor balance sheet data and pro forma adjustments used in preparing the pro forma financial data reflect our preliminary estimates of the purchase price allocation, which may change upon finalization of appraisals and other valuation studies that we have arranged to obtain. The pro forma financial data are for informational purposes only and should not be considered indicative of actual results that would have been achieved had the Transactions and the term loan repayment actually been consummated on the dates indicated and do not purport to indicate balance sheet data or results of operations as of any future date or for any future period. You should read the following data in conjunction with "Unaudited Consolidated Pro Forma Financial Information," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the consolidated financial statements and related notes thereto of RAG American Coal Holding, Inc. and Foundation Coal Corporation included elsewhere in this prospectus.

13

| | Predecessor

| | Successor

| |

| |

| |

|---|

| |

| | Pro Forma

Nine Months

Ended

September 30,

2004

| |

|---|

| | Year Ended December 31,

| | Nine Months

Ended

September 30,

2003

| | Period

January 1

to July 29,

2004

| | Period

April 23 to

September 30,

2004

| | Pro Forma

Year Ended

December 31,

2003

| |

|---|

| | 2001

| | 2002

| | 2003

| |

|---|

| |

| |

| |

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| | (unaudited)

| |

|---|

| | (in millions, except per share and per ton data)

| |

|---|

| Statement of Operations Data: | | | | | | | | | | | | | | | | | | | | | | | | | |

| Revenues: | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Coal sales | | $ | 746.4 | | $ | 891.8 | | $ | 976.0 | | $ | 732.0 | | $ | 544.9 | | $ | 180.4 | | $ | 976.0 | | $ | 725.3 | |

| | Other revenues | | | 32.8 | | | 12.9 | | | 18.3 | | | 12.9 | | | 6.1 | | | 2.8 | | | 18.3 | | | 8.9 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| | | Total revenues | | | 779.2 | | | 904.7 | | | 994.3 | | | 744.9 | | | 551.0 | | | 183.2 | | | 994.3 | | | 734.2 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| Costs and expenses: | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Cost of coal sales | | | 605.5 | | | 699.8 | | | 798.3 | | | 597.7 | | | 484.5 | | | 147.6 | | | 787.4 | | | 618.4 | |

| | Selling, general and administrative expenses | | | 36.9 | | | 45.1 | | | 45.3 | | | 32.6 | | | 27.4 | | | 6.8 | | | 44.8 | | | 33.0 | |

| | Accretion on asset retirement obligations | | | — | | | — | | | 7.0 | | | 5.2 | | | 4.0 | | | 1.3 | | | 8.2 | | | 6.2 | |

| | Depreciation, depletion and amortization | | | 83.8 | | | 91.6 | | | 99.8 | | | 74.5 | | | 61.2 | | | 26.2 | | | 145.5 | | | 127.4 | |

| | Amortization of coal supply agreements | | | 16.9 | | | 17.5 | | | 17.9 | | | 13.8 | | | 8.8 | | | (22.5 | ) | | (103.5 | ) | | (33.1 | ) |

| | Asset impairment charges | | | 16.6 | | | 7.0 | | | — | | | — | | | — | | | — | | | — | | | — | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| | | Total costs and expenses | | | 759.7 | | | 861.0 | | | 968.3 | | | 723.8 | | | 585.9 | | | 159.4 | | | 882.4 | | | 751.9 | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| Income (loss) from operations | | | 19.5 | | | 43.7 | | | 26.0 | | | 21.1 | | | (34.9 | ) | | 23.8 | | | 111.9 | | | (17.7 | ) |

| Other income (expense): | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Interest expense | | | (52.5 | ) | | (48.9 | ) | | (46.9 | ) | | (35.7 | ) | | (18.0 | ) | | (8.5 | ) | | (50.5 | ) | | (37.7 | ) |

| | Loss on termination of hedge accounting for interest rate swaps | | | — | | | — | | | — | | | — | | | (48.9 | ) | | — | | | — | | | (48.9 | ) |

| | Contract settlement | | | — | | | — | | | — | | | — | | | (26.0 | ) | | — | | | — | | | (26.0 | ) |

| | Loss on early debt extinguishment | | | — | | | — | | | — | | | — | | | (21.7 | ) | | — | | | — | | | (21.7 | ) |

| | Mark to market gain (loss) on interest rate swaps | | | — | | | — | | | — | | | — | | | 5.8 | | | (0.1 | ) | | — | | | 5.7 | |

| | Interest income | | | 6.8 | | | 12.3 | | | 3.2 | | | 2.5 | | | 1.3 | | | 0.2 | | | 3.2 | | | 1.5 | |

| | Minority interest | | | 15.0 | | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

| | Litigation settlements | | | — | | | — | | | 43.5 | | | 43.5 | | | — | | | — | | | 43.5 | | | — | |

| | Arbitration award | | | — | | | 31.1 | | | — | | | — | | | — | | | — | | | — | | | — | |

| | Insurance settlement | | | 31.2 | | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| Income (loss) before income tax expense (benefit) | | | 20.0 | | | 38.2 | | | 25.8 | | | 31.4 | | | (142.4 | ) | | 15.4 | | | 108.1 | | | (144.8 | ) |

| Income tax expense (benefit) | | | 3.9 | | | 13.1 | | | (0.2 | ) | | 1.9 | | | (51.8 | ) | | 5.1 | | | 31.1 | | | (53.5 | ) |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| Income (loss) from continuing operations (2)(3) | | | 16.1 | | | 25.1 | | | 26.0 | | | 29.5 | | | (90.6 | ) | $ | 10.3 | | $ | 77.0 | | $ | (91.3 | ) |

| | | | | | | | | | | | | | | | | | | | |

| |

| |

Income from discontinued operations net of income tax expense |

|

|

9.9 |

|

|

8.1 |

|

|

10.1 |

|

|

6.7 |

|

|

2.3 |

|

|

— |

|

|

|

|

|

|

|

| Gain on disposal of discontinued operations, net of income tax expense | | | — | | | — | | | — | | | — | | | 20.8 | | | — | | | | | | | |

| Cumulative effect of accounting changes, net of tax benefit | | | — | | | — | | | (3.6 | ) | | (3.6 | ) | | — | | | — | | | | | | | |

| | |

| |

| |

| |

| |

| |

| | | | | | | |

| Net income (loss) | | $ | 26.0 | | $ | 33.2 | | $ | 32.5 | | $ | 32.6 | | $ | (67.5 | ) | $ | 10.3 | | | | | | | |

| | |

| |

| |

| |

| |

| |

| | | | | | | |

Balance Sheet Data (at period end): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Cash and cash equivalents | | $ | 20.2 | | $ | 21.8 | | $ | 7.6 | | $ | 7.6 | | | | | $ | 39.1 | | | | | $ | 39.1 | |

| Cash on deposit with RAG Coal International AG | | | 137.7 | | | 66.5 | | | 233.0 | | | 173.4 | | | | | | — | | | | | | — | |

| Cash pledged | | | — | | | 75.0 | | | 20.0 | | | 20.0 | | | | | | — | | | | | | — | |

| Total assets | | | 1,849.1 | | | 1,861.8 | | | 1,864.8 | | | 1,847.6 | | | | | | 2,138.9 | | | | | | 2,137.8 | |

| Total debt | | | 697.0 | | | 656.8 | | | 616.5 | | | 616.5 | | | | | | 770.1 | | | | | | 725.7 | |

| Stockholders' equity | | | 489.0 | | | 487.9 | | | 523.2 | | | 523.5 | | | | | | 206.3 | | | | | | 250.8 | |

| | | | | | | | | | | | | | | | | | | | | | | | | | |

14

Statement of Cash Flows Data: |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Net cash provided by (used in) continuing operations: | | | | | | | | | | | | | | | | | | | | | | | | | |

| | Operating activities | | $ | 97.0 | | $ | 136.2 | | $ | 197.7 | | $ | 125.7 | | $ | (8.0 | ) | $ | 24.9 | | | | | | | |

| | Investing activities | | | (8.3 | ) | | (105.2 | ) | | (92.7 | ) | | (68.0 | ) | | (50.6 | ) | | (924.1 | ) | | | | | | |

| | Financing activities | | | (148.6 | ) | | (44.1 | ) | | (151.7 | ) | | (92.1 | ) | | (127.8 | ) | | 938.3 | | | | | | | |

| Capital expenditures | | | 100.0 | | | 118.9 | | | 97.1 | | | 71.3 | | | 52.7 | | | 12.7 | | | | | | | |

Other Financial Data

(unaudited): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| EBITDA (1)(2)(3) | | $ | 166.4 | | $ | 183.9 | | $ | 187.2 | | $ | 152.9 | | $ | (55.7 | ) | $ | 27.4 | | $ | 197.4 | | $ | (14.3 | ) |

| EBITDA margin (1) | | | 21.4 | % | | 20.3 | % | | 18.8 | % | | 20.5 | % | | (10.1 | )% | | 15.0 | % | | 19.8 | % | | (1.9 | )% |

Cumberland mine force majeure

(4) | | | — | | | — | | | — | | | — | | | 31.1 | | | — | | | — | | | 31.1 | |

| Ratio of earnings to fixed charges(5) | | | 1.1 | x | | 1.7 | x | | 1.5 | x | | 1.8 | x | | — | | | 2.7 | x | | 3.0 | x | | — | |

Operating Data (unaudited): |

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

|

| Tons sold | | | 58.6 | | | 64.4 | | | 67.2 | | | 50.0 | | | 35.9 | | | 11.5 | | | | | | | |

| Tons produced | | | 57.6 | | | 63.5 | | | 64.0 | | | 48.1 | | | 34.6 | | | 11.2 | | | | | | | |

| Coal sales price (per ton) | | $ | 12.73 | | $ | 13.85 | | $ | 14.52 | | $ | 14.65 | | $ | 15.17 | | $ | 15.70 | | | | | | | |

- (1)

- EBITDA, a measure expected to be used by management to measure performance is defined as income (loss) from continuing operations, plus interest expense, net of interest income, income tax expense (benefit), and depreciation, depletion and amortization. Our management believes EBITDA and EBITDA margin are useful to investors because they are frequently used by securities analysts, investors and other interested parties in the evaluation of companies in our industry. Because not all companies use identical calculations, this presentation of EBITDA and EBITDA margin may not be comparable to other similarly titled measures of other companies. EBITDA is not a recognized term under GAAP and does not purport to be an alternative to net income as a measure of operating performance or to cash flows from operating activities as a measure of liquidity.

Additionally, EBITDA is not intended to be a measure of free cash flow for management's discretionary use, as it does not reflect certain cash requirements such as interest payments, tax payments and debt service requirements. The amounts shown for EBITDA as presented herein differ from the amounts calculated under the definition of EBITDA used in our debt instruments. The definition of EBITDA used in our debt instruments is further adjusted for certain cash and non-cash charges and is used to determine compliance with financial covenants and our ability to engage in certain activities such as incurring additional debt and making certain payments. See "Management's Discussion and Analysis of Financial Condition and Results of Operations—Liquidity and Capital Resources—Covenant Compliance".

15

EBITDA is calculated and reconciled to income (loss) from continuing operations and EBITDA margin is calculated in the table below:

| | Predecessor

| | Successor

| |

| |

| |

|---|

| |

| | Pro Forma

Nine Months

Ended

September 30,

2004

| |

|---|

| | Year Ended December 31,

| | Nine Months

Ended

September 30,

2003

| | Period

January 1

to July 29,

2004

| | Period

April 23 to

September 30,

2004

| | Pro Forma

Year Ended

December 31,

2003

| |

|---|

| | 2001

| | 2002

| | 2003

| |

|---|

| | (in millions)

| |

|---|

| Income (loss) from continuing operations | | $ | 16.1 | | $ | 25.1 | | $ | 26.0 | | $ | 29.5 | | $ | (90.6 | ) | $ | 10.3 | | $ | 77.0 | | $ | (91.3 | ) |

| Interest expense | | | 52.5 | | | 48.9 | | | 46.9 | | | 35.7 | | | 18.0 | | | 8.5 | | | 50.5 | | | 37.7 | |

| Interest income | | | (6.8 | ) | | (12.3 | ) | | (3.2 | ) | | (2.5 | ) | | (1.3 | ) | | (0.2 | ) | | (3.2 | ) | | (1.5 | ) |

Income tax expense

(benefit) | | | 3.9 | | | 13.1 | | | (0.2 | ) | | 1.9 | | | (51.8 | ) | | 5.1 | | | 31.1 | | | (53.5 | ) |

| Depreciation, depletion and amortization | | | 83.8 | | | 91.6 | | | 99.8 | | | 74.5 | | | 61.2 | | | 26.2 | | | 145.5 | | | 127.4 | |

| Coal supply agreement amortization | | | 16.9 | | | 17.5 | | | 17.9 | | | 13.8 | | | 8.8 | | | (22.5 | ) | | (103.5 | ) | | (33.1 | ) |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| EBITDA | | $ | 166.4 | | $ | 183.9 | | $ | 187.2 | | $ | 152.9 | | $ | (55.7 | ) | $ | 27.4 | | $ | 197.4 | | $ | (14.3 | ) |

| | |

| |

| |

| |

| |

| |

| |

| |

| |

| Total revenues | | $ | 779.2 | | $ | 904.7 | | $ | 994.3 | | $ | 744.9 | | $ | 551.0 | | $ | 183.2 | | $ | 994.3 | | $ | 734.2 | |

| EBITDA margin | | | 21.4 | % | | 20.3 | % | | 18.8 | % | | 20.5 | % | | (10.1 | )% | | 15.0 | % | | 19.8 | % | | (1.9 | )% |

- (2)

- Income (loss) from continuing operations and EBITDA, as defined above, were impacted by the following non-cash charges (income):

| | Predecessor

| | Successor

| |

| |

|

|---|

| |

| | Pro Forma

Nine Months

Ended

September 30,

2004

|

|---|

| | Year Ended December 31,

| | Nine Months

Ended

September 30,

2003

| | Period

January 1

to July 29,

2004

| | Period

April 23 to

September 30,

2004

| | Pro Forma

Year Ended

December 31,

2003

|

|---|

| | 2001

| | 2002

| | 2003

|

|---|

| | (in millions)

|

|---|

| Interest rate swaps (a) | | $ | — | | $ | — | | $ | — | | $ | — | | $ | 43.1 | | $ | 0.1 | | $ | — | | $ | 43.2 |

| Early extinguishment of debt | | | — | | | — | | | — | | | — | | | 21.7 | | | — | | | — | | | 21.7 |

Accretion on asset

retirement obligations/

reclamation expense (b) | | | 5.1 | | | 5.5 | | | 7.0 | | | 5.2 | | | 4.0 | | | 1.3 | | | 8.2 | | | 6.2 |

| Asset impairment charges | | | 16.6 | | | 7.0 | | | — | | | — | | | — | | | | | | — | | | — |

Amortization included in

benefits expense (c) | | | 2.9 | | | 6.1 | | | 11.4 | | | 8.1 | | | 10.3 | | | — | | | — | | | — |

| Minority interests (d) | | | (15.0 | ) | | — | | | — | | | — | | | — | | | | | | — | | | — |

| Profit in inventory (e) | | | — | | | — | | | — | | | — | | | — | | | 3.8 | | | — | | | — |

- (a)

- For the Predecessor, this amount includes $48.9 million of expense resulting from loss on termination of hedge accounting for interest rate swaps less $5.8 million mark-to-market adjustment. Under the terms of the stock purchase agreement, we did not assume any existing interest rate swaps. For the Successor, this amount includes the mark-to-market loss on interest rate swaps not yet designated as cash flow hedges.

- (b)

- For 2001 and 2002, this amount represents reclamation expense recorded prior to the adoption of Statement of Financial Accounting Standards No. 143,Accounting for Asset Retirement Obligations ("SFAS No. 143").

- (c)

- Represents the portion of pension, other post-retirement and black lung expense resulting from the amortization of unrecognized actuarial losses, prior service costs and transition obligations.

- (d)

- Relates to the 15% interest in Plateau Mining Corporation that was held by an unaffiliated entity until we purchased this interest in December 2001.

- (e)

- Represents incremental cost of sales recorded in the period arising from the preliminary estimate of profit added to inventory in purchase accounting.

16

- (3)

- Income (loss) from continuing operations and EBITDA, as defined above, were also impacted by the following unusual (income) expense:

| | Predecessor

| | Successor

| |

| |

| |

|---|

| |

| | Pro Forma

Nine Months

Ended

September 30,

2004

| |

|---|

| | Year Ended December 31,

| | Nine Months

Ended

September 30,

2003

| | Period

January 1

to July 29,

2004

| | Period

April 23 to

September 30,

2004

| | Pro Forma

Year Ended

December 31,

2003

| |

|---|

| | 2001

| | 2002

| | 2003

| |

|---|

| | (in millions)

| |

|---|

Litigation/arbitration/contract

settlements, net (a) | | $ | 1.0 | | $ | (24.3 | ) | $ | (41.9 | ) | $ | (42.0 | ) | $ | 28.9 | | $ | — | | $ | (41.9 | ) | $ | 28.9 | |

| Transaction bonus (b) | | | — | | | — | | | — | | | — | | | 1.8 | | | — | | | — | | | 1.8 | |

Long-term incentive plan

expense (c) | | | 1.5 | | | 1.0 | | | 3.9 | | | 2.2 | | | 2.4 | | | — | | | 3.9 | | | 2.4 | |

| Insurance recoveries (d) | | | (31.2 | ) | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

Terminated royalty

agreement (e) | | | (11.5 | ) | | — | | | — | | | — | | | — | | | — | | | — | | | — | |

Gain on asset sales and

sale of affiliates | | | (3.8 | ) | | (3.4 | ) | | (4.8 | ) | | (4.6 | ) | | (1.0 | ) | | — | | | (4.8 | ) | | (1.0 | ) |

| Other (f) | | | (2.6 | ) | | — | | | — | | | — | | | — | | | 0.8 | | | — | | | — | |

- (a)

- Represents arbitration awards, litigation settlements and contract settlements net of related legal and tax fees.

- (b)

- Represents the cost of a one-time bonus awarded to certain employees in connection with the Transactions.

- (c)

- Represents the cost of a long-term incentive plan instituted by the Seller in 2001 that was terminated prior to closing as required by the change in control provisions in the plan agreement. We have implemented a management equity program that will not result in a cash cost to us.

- (d)

- Consists of insurance proceeds in excess of the book value of net assets and closure costs at the Willow Creek mine.

- (e)

- Consists of a gain recognized on termination of a royalty agreement in conjunction with the closure of Willow Creek.

- (f)

- Represents $2.6 million from management services provided to an affiliate of RAG Coal International AG by the Predecessor and $0.8 million from a sponsor monitoring fee incurred by the Successor which will be terminated in connection with our ultimate parent company's initial public offering.

- (4)

- Represents the estimated impact on EBITDA of the temporary idling of our Cumberland mine in the first half of 2004 as a result of a revised interpretation of mine ventilation laws by MSHA. See "Management's Discussion and Analysis of Financial Condition and Results of Operations" and note 25 to the consolidated financial statements for additional information.

- (5)

- For purposes of this computation, "earnings" consist of pre-tax income from continuing operations (excluding minority interest and equity in earnings of affiliates) plus fixed charges. "Fixed charges" consist of interest expense on all indebtedness plus amortization of deferred costs of financing and the interest component of lease rental expense. Earnings were insufficient to cover fixed charges by $142.4 million for the period January 1 to July 29, 2004 and $144.8 million on a pro forma basis for the nine months ended September 30, 2004.

17

RISK FACTORS

An investment in our exchange notes and notes involves risks. You should carefully consider the risks described below, together with the other information in this prospectus, before deciding to tender your outstanding notes in the exchange offer.

Risks Relating to Our Business

A substantial or extended decline in coal prices could reduce our revenues and the value of our coal reserves.

The prices we charge for coal depend upon factors beyond our control, including:

- •

- the supply of, and demand for, domestic and foreign coal;

- •

- the demand for electricity;

- •

- domestic and foreign demand for steel and the continued financial viability of the domestic and/or foreign steel industry;

- •

- the proximity to, capacity of, and cost of transportation facilities;

- •

- domestic and foreign governmental regulations and taxes;

- •

- air emission standards for coal-fired power plants;

- •

- regulatory, administrative and court decisions;

- •

- the price and availability of alternative fuels, including the effects of technological developments; and

- •

- the effect of worldwide energy conservation measures.

Our results of operations are dependent upon the prices we charge for our coal as well as our ability to improve productivity and control costs. Any decreased demand would cause spot prices to decline and require us to increase productivity and decrease costs in order to maintain our margins. If we are not able to maintain our margins, our operating results could be adversely affected. Therefore, price declines may adversely affect operating results for future periods and our ability to generate cash flows necessary to improve productivity and invest in operations.

Any adverse change in coal consumption patterns by North American electric power generators or steel producers could result in weaker demand and possibly lower prices for our production, which would reduce our revenues.

During 2003, sales of steam coal accounted for approximately 97% of our total coal sales volume and 91% of our coal sales revenue, and the vast majority of our sales of steam coal were to U.S. electric power generators. Domestic electric power generation accounted for approximately 92% of all U.S. coal consumption in 2003, according to the EIA. The amount of coal consumed for U.S. electric power generation is affected primarily by the overall demand for electricity, the location, availability, quality and price of competing fuels such as natural gas, nuclear, fuel oil and alternative energy sources such as hydroelectric power, technological developments and environmental and other governmental regulations. Many of the recently constructed electric power sources have been gas-fired, by virtue of lower construction costs and reduced environmental risks. Gas-based generation from existing and newly constructed gas-based facilities has the potential to displace coal-based generation, particularly from older, less efficient coal generators. In addition, the increasingly stringent requirements of the Clean Air Act may result in more electric power generators shifting from coal to natural gas-fired power plants. Any reduction in coal demand from the electric generation and steel sectors could create short-term market imbalances, leading to lower demand for, and price of, our products, thereby reducing our revenue.

18

Our profitability may decline due to unanticipated mine operating conditions and other factors that are not within our control.

Our mining operations are influenced by changing conditions that can affect production levels and costs at particular mines for varying lengths of time and as a result can diminish our profitability. Weather conditions, equipment availability, replacement or repair, prices for fuel, steel, explosives and other supplies, fires, variations in thickness of the layer, or seam, of coal, amounts of overburden, rock and other natural materials, accidental mine water discharges and other geological conditions have had, and can be expected in the future to have, a significant impact on our operating results. For example, in September 2004, our Emerald mine in Green County, Pennsylvania experienced adverse geological conditions, consisting of sandstone intrusions from the roof into the coal seam in the panel being mined, which slowed mining by forcing the machinery to cut harder material and causing less stable roof conditions. These conditions prevented normal longwall production and thus reduced the quantity of coal available for shipment pursuant to this mine's contractual obligations. Emerald personnel have completed production on the longwall panel that experienced the geological problems. The longwall is in the process of being moved to the next panel and normal production is currently expected to resume in early November. Prolonged disruption of production at any of our mines would result in a decrease in our revenues and profitability, which could be material.

Decreases in our profitability as a result of the factors described above could materially adversely impact our quarterly or annual results. These risks may not be fully covered by our insurance policies.

MSHA may order certain of our mines to be temporarily closed, which would adversely affect our ability to meet our customers' demands.