Exhibit 99.1

| Investor Presentation April 2008 |

| 1 Safe Harbor Statement Statements made in this presentation that express the company's or management's intentions, plans, beliefs, expectations or predictions of future events, are forward-looking statements. Those statements are based on many assumptions and are subject to many known and unknown risks, uncertainties and other factors that could cause the company's actual activities, results or performance to differ materially from those anticipated or projected in such forward-looking statements. In light of significant risks and uncertainties inherent in forward-looking statements included herein, the inclusion of such statements should not be regarded as a representation by Nascent Foodservice that they will achieve such forward-looking statements. For further details and a discussion of these and other risks and uncertainties, please see our most recent reports on Form 10-KSB and Form 10-QSB, as filed with the Securities and Exchange Commission, as they may be amended from time to time. Nascent Foodservice undertakes no obligation to publicly update any forward-looking statement, whether as a result of new information, future events, or otherwise. |

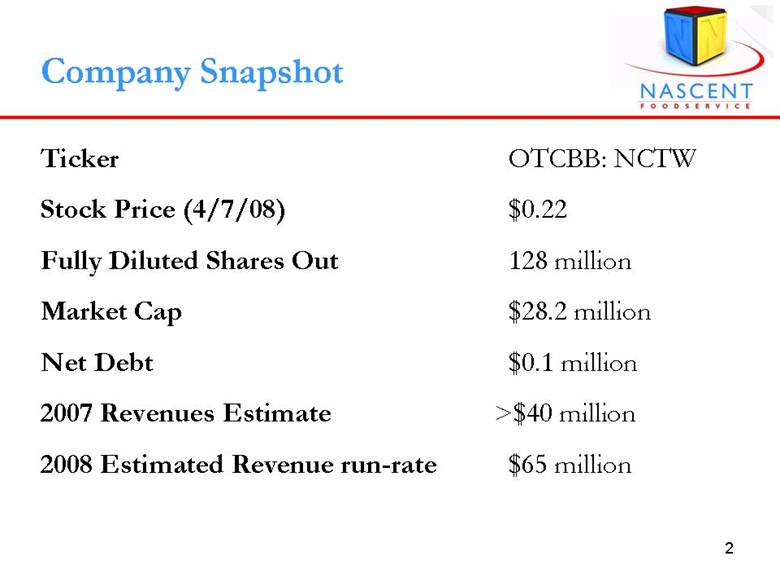

| 2 Company Snapshot Ticker OTCBB: NCTW Stock Price (4/7/08) $0.22 Fully Diluted Shares Out 128 million Market Cap $28.2 million Net Debt $0.1 million 2007 Revenues Estimate >$40 million 2008 Estimated Revenue run-rate $65 million |

| 3 Company Overview • First-mover advantage and fastest growing foodservice distributor of imported branded and private-label food & beverage products in Mexico – Over 2,000 products and 200 national and private-label brands – Seven exclusive distribution rights • National footprint • Services over 2,300 Foodservice and Retail Accounts through 240,000 sales points • Organic and acquisition-focused strategy |

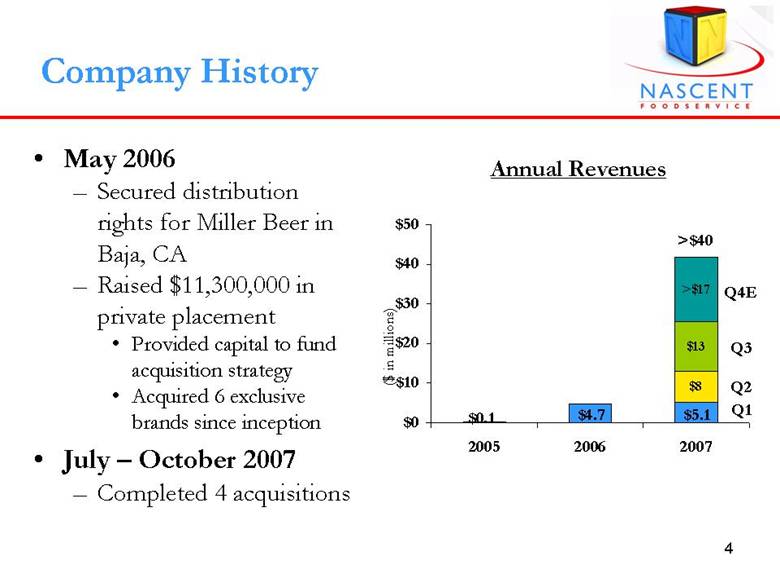

| 4 Company History • May 2006 – Secured distribution rights for Miller Beer in Baja, CA – Raised $11,300,000 in private placement • Provided capital to fund acquisition strategy • Acquired 6 exclusive brands since inception • July – October 2007 – Completed 4 acquisitions $8 $13 $5.1 $4.7 $0.1 >$17 $0 $10 $20 $30 $40 $50 2005 2006 2007 ($ in millions) Annual Revenues >$40 Q1 Q2 Q3 Q4E |

| 5 Strategic Acquisition History Date of Acquisition Company Name Brands/ Strategic Advantage April 2006 Miller Beer of Baja, CA October 2007 Piancone Group International November 2007 Palermo Italian Food May 2007 Pasani, SA July 2007 Grupo Sur Promociones October 2007 Comercial Targa |

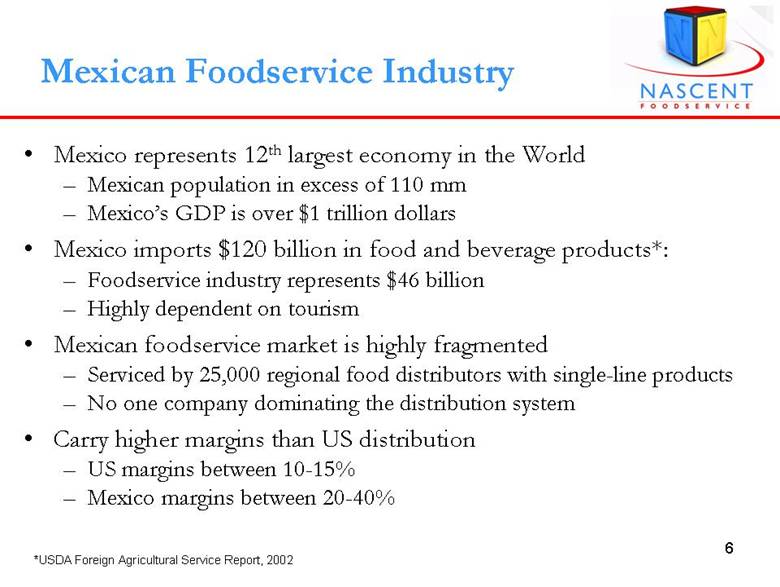

| 6 Mexican Foodservice Industry • Mexico represents 12th largest economy in the World – Mexican population in excess of 110 mm – Mexico’s GDP is over $1 trillion dollars • Mexico imports $120 billion in food and beverage products*: – Foodservice industry represents $46 billion – Highly dependent on tourism • Mexican foodservice market is highly fragmented – Serviced by 25,000 regional food distributors with single-line products – No one company dominating the distribution system • Carry higher margins than US distribution – US margins between 10-15% – Mexico margins between 20-40% *USDA Foreign Agricultural Service Report, 2002 |

| 7 Demographic Served |

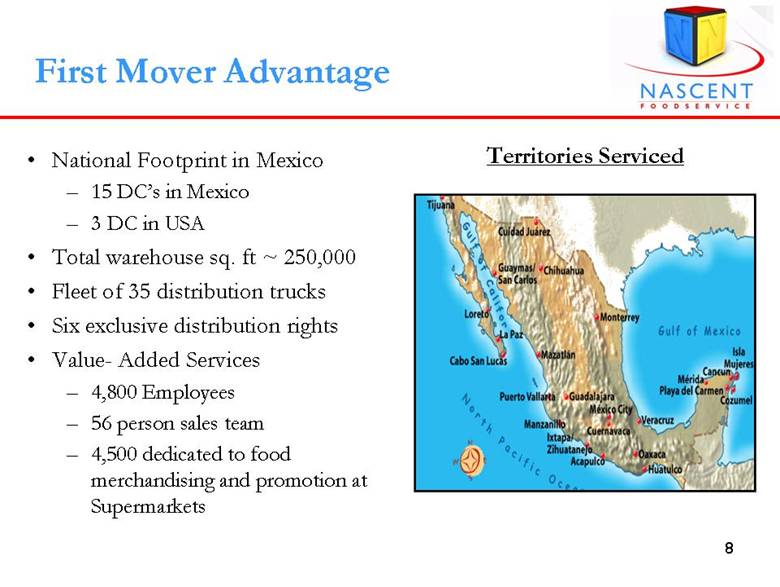

| 8 First Mover Advantage • National Footprint in Mexico – 15 DC’s in Mexico – 3 DC in USA • Total warehouse sq. ft ~ 250,000 • Fleet of 35 distribution trucks • Six exclusive distribution rights • Value- Added Services – 4,800 Employees – 56 person sales team – 4,500 dedicated to food merchandising and promotion at Supermarkets Territories Serviced |

| 9 Leading Branded & Private Label Portfolio Strong portfolio of private label & branded products • Over 2,000 branded and private label products – 250 private label products – 750 products under exclusive agreements – 1,000 products purchased in the open market |

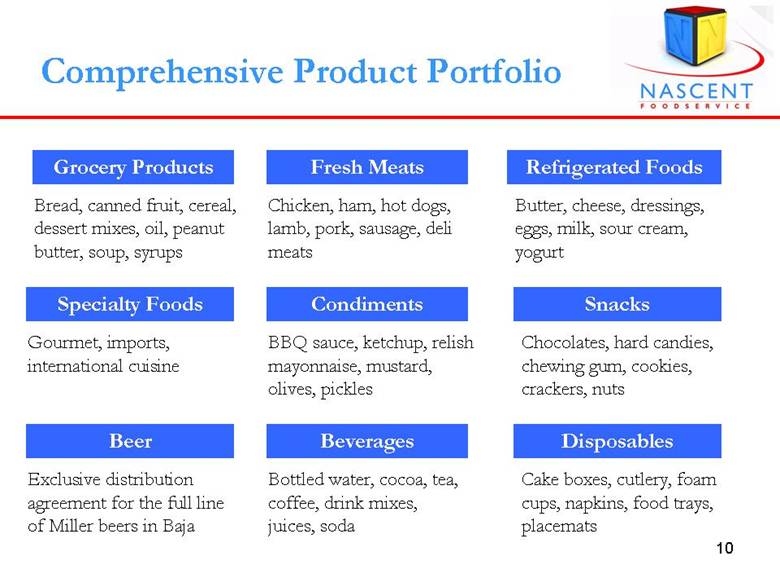

| 10 Comprehensive Product Portfolio Beverages Snacks Grocery Products Bottled water, cocoa, tea, coffee, drink mixes, juices, soda Chocolates, hard candies, chewing gum, cookies, crackers, nuts Disposables Fresh Meats Condiments Specialty Foods Refrigerated Foods Beer Bread, canned fruit, cereal, dessert mixes, oil, peanut butter, soup, syrups Cake boxes, cutlery, foam cups, napkins, food trays, placemats Chicken, ham, hot dogs, lamb, pork, sausage, delimeats BBQ sauce, ketchup, relish mayonnaise, mustard, olives, pickles Gourmet, imports, international cuisine Butter, cheese, dressings, eggs, milk, sour cream, yogurt Exclusive distribution agreement for the full line of Miller beers in Baja |

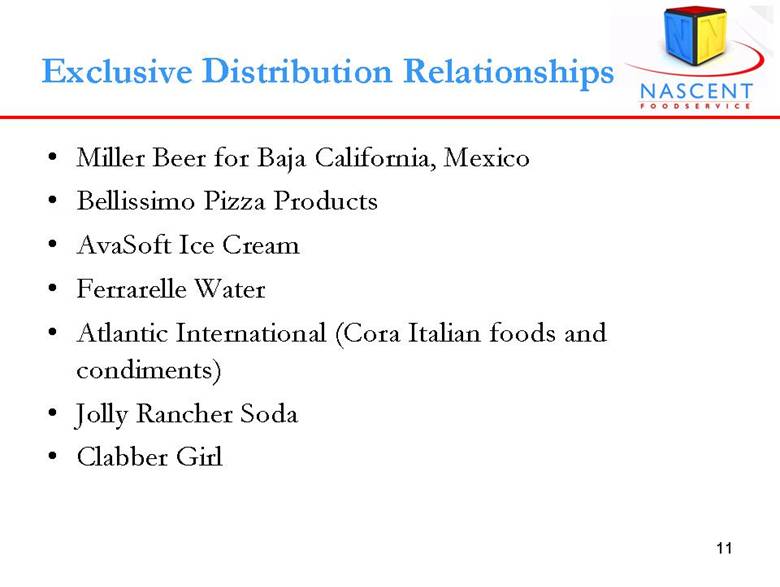

| 11 Exclusive Distribution Relationships • Miller Beer for Baja California, Mexico • Bellissimo Pizza Products • AvaSoft Ice Cream • Ferrarelle Water • Atlantic International (Cora Italian foods and condiments) • Jolly Rancher Soda • Clabber Girl |

| 12 Channels Accounts Supermarkets Club stores Convenience Stores BTL Marketing Foodservice Restaurants, hotels, bakeries Key Retail Partners |

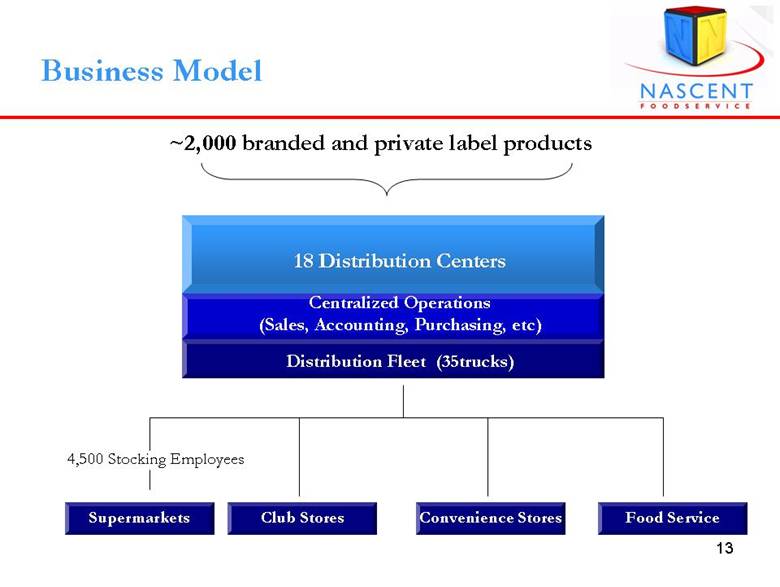

| 13 Business Model ~2,000 branded and private label products 18 Distribution Centers Centralized Operations (Sales, Accounting, Purchasing, etc) Distribution Fleet (35trucks) 4,500 Stocking Employees Supermarkets Club Stores Convenience Stores Food Service |

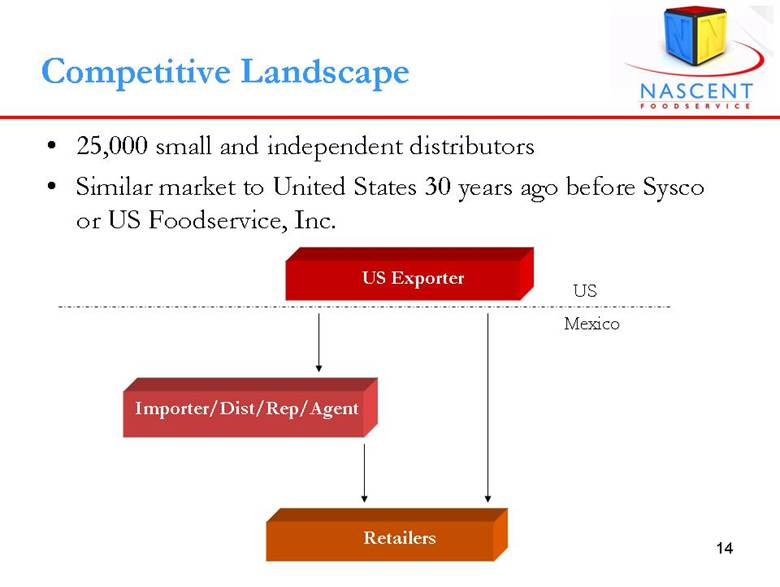

| 14 Competitive Landscape • 25,000 small and independent distributors • Similar market to United States 30 years ago before Sysco or US Foodservice, Inc. US Exporter Importer/Dist/Rep/Agent Retailers US Mexico |

| 15 Growth Opportunities • Organic growth expected to be over 30% in 2008 • Pursue Selective Acquisitions • Leverage Business Model – Majority of investment in distribution platform complete – Expand higher margin private label offering – Adding additional leading brands • Further Penetrate Existing Distribution Channels |

| 16 Pursue Selective Acquisitions • Fragmented industry (comparable to United States 30 years ago) • Estimated 10,000 acquisition opportunities • Average P/E multiple of acquired Company 2.0x -4.0x • Limited strategic buyer universe Opportunity • Leverage existing infrastructure • Expand branded and private label portfolio • Access additional distribution channels • Enter complementary product categories • Retain owners of acquired company to handle sales and collections Rationale |

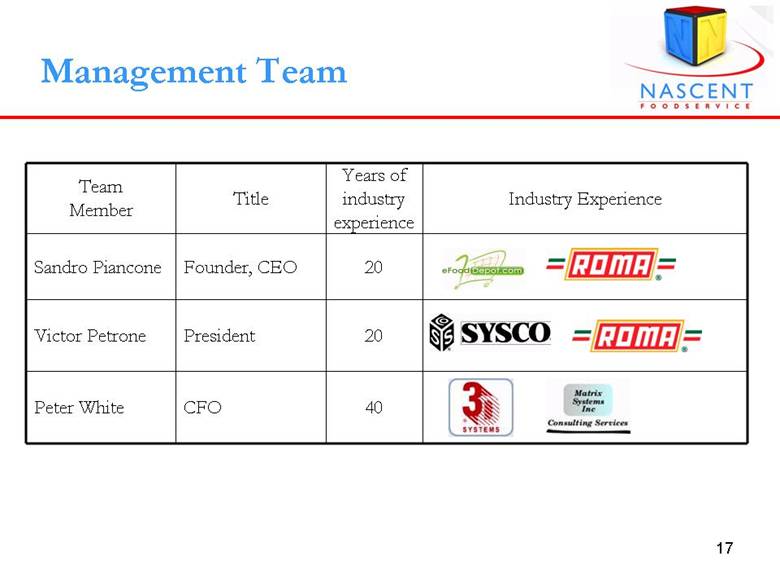

| 17 Management Team Team Member Title Years of industry experience Industry Experience Sandro Piancone Founder, CEO 20 Victor Petrone President 20 Peter White CFO 40 |

| Financial Overview |

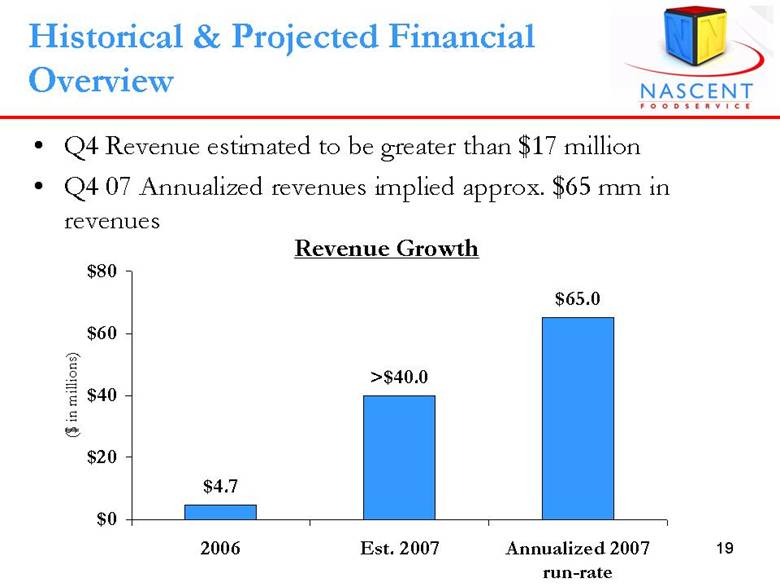

| 19 • Q4 Revenue estimated to be greater than $17 million • Q4 07 Annualized revenues implied approx. $65 mm in revenues Historical & Projected Financial Overview Revenue Growth $4.7 $65.0 >$40.0 $0 $20 $40 $60 $80 2006 Est. 2007 Annualized 2007 run-rate ($ in millions) |

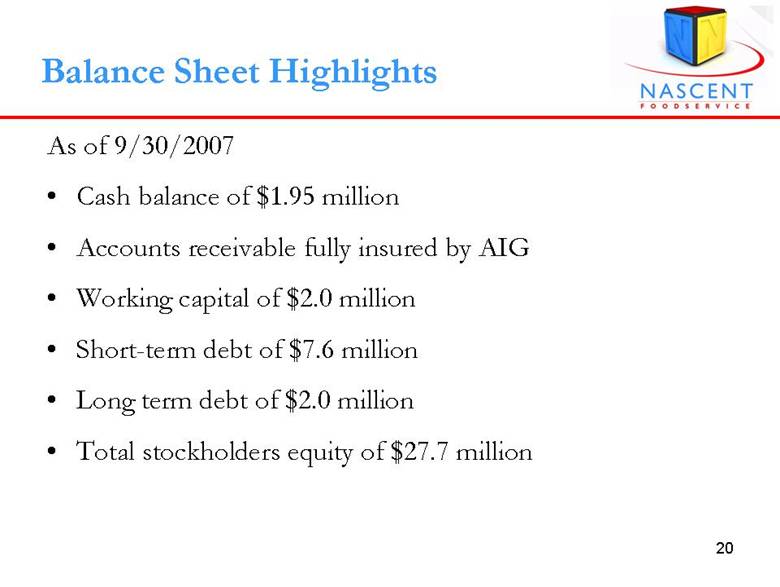

| 20 Balance Sheet Highlights As of 9/30/2007 • Cash balance of $1.95 million • Accounts receivable fully insured by AIG • Working capital of $2.0 million • Short-term debt of $7.6 million • Long term debt of $2.0 million • Total stockholders equity of $27.7 million |

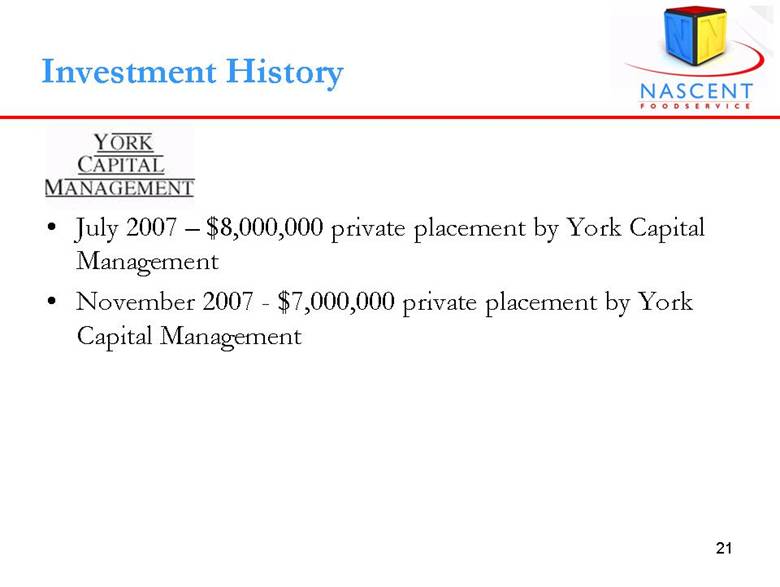

| 21 Investment History • July 2007 – $8,000,000 private placement by York Capital Management • November 2007 - $7,000,000 private placement by York Capital Management |

| 22 Investment Summary • Rapidly Expanding Sales Growth • First-Mover Advantage • Fragmented Industry • Leveraging Infrastructure • Improving Margins • Diversified Branded and Private Label Products • Compelling Customer Value Proposition |