UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED

MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21681

Old Mutual/Claymore Long-Short Fund

(Exact name of registrant as specified in charter)

| 2455 Corporate West Drive, Lisle, IL | 60532 | |

| (Address of principal executive offices) | (Zip code) |

Nicholas Dalmaso, Chief Legal and Executive Officer

Old Mutual/Claymore Long-Short Fund

2455 Corporate West Drive, Lisle, IL 60532

(Name and address of agent for service)

Registrant’s telephone number, including area code: (630) 505-3700

Date of fiscal year end: December 31

Date of reporting period: December 31, 2005

Form N-CSR is to be used by management investment companies to file reports with the Commission not later than 10 days after the transmission to stockholders of any report that is required to be transmitted to stockholders under Rule 30e-1 under the Investment Company Act of 1940 (17 CFR 270.30e-1). The Commission may use the information provided on Form N-CSR in its regulatory, disclosure review, inspection, and policymaking roles.

A registrant is required to disclose the information specified by Form N-CSR, and the Commission will make this information public. A registrant is not required to respond to the collection of information contained in Form N-CSR unless the Form displays a currently valid Office of Management and Budget (“OMB”) control number. Please direct comments concerning the accuracy of the information collection burden estimate and any suggestions for reducing the burden to Secretary, Securities and Exchange Commission, 450 Fifth Street, NW, Washington, DC 20549-0609. The OMB has reviewed this collection of information under the clearance requirements of 44 U.S.C. Section 3507.

| Item 1. | Reports to Stockholders. |

The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940 is as follows:

www.oldmutualclaymore.com

| ...your course to the LATEST, | ||

| most up-to-date INFORMATION about the | ||

| Old Mutual/Claymore Long-Short Fund | ||

The shareholder report you are reading right now is just the beginning of the story. Online at oldmutualclaymore.com, you will find:

| • | Daily, weekly and monthly data on share prices, distributions and more |

| • | Monthly portfolio overviews and performance analyses |

| • | Announcements, press releases, special notices and tax characteristics |

Analytic Investors, Inc. and Claymore are continually updating and expanding shareholder information services on the Fund’s website, in an ongoing effort to provide you with the most current information about how your Fund’s assets are managed, and the results of our efforts. It is just one more way we are working to keep you better informed about your investment in the Fund.

2 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund

Dear Shareholder |

We are delighted to submit the first annual shareholder report for the Old Mutual/Claymore Long-Short Fund (“OLA”). This report covers performance from the Fund’s inception on August 25, 2005, through December 31, 2005. As you may know, the Fund’s investment objective is to seek a high level of current income and gains with a secondary objective of long-term capital appreciation. The Fund seeks to achieve that objective by investing in a diversified portfolio of common stocks and other equity securities utilizing a 120% long / 20% short strategy and opportunistically employing a strategy of writing (selling) calls on equity indexes.

Analytic Investors, Inc. (“Analytic”) is the Fund’s Sub-Adviser. The firm was founded in 1970 and is a wholly-owned subsidiary of Old Mutual (US) Holdings Inc., more commonly known as Old Mutual Asset Management. With approximately $10 billion in assets under management as of December 31, 2005, Analytic specializes in the creation and continuous management of optioned-equity and optioned-debt portfolios for mutual funds, foundations, insurance companies, endowments, profit-sharing plans, funds-of-hedge-funds and individual investors.

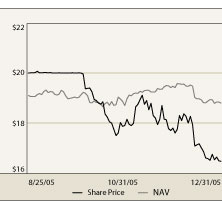

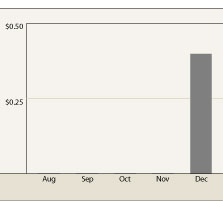

Since its inception on August 25, 2005, the Fund generated a total return of 0.52% at net asset value (“NAV”). This represents a change in NAV from $19.10 at inception to $18.80 on December 31, 2005, plus the reinvestment of the Fund’s quarterly distribution. During this same period, the Fund’s total return based on market price was -15.76%. This reflects a change in market price from $20.00 at inception to $16.47 on December 31, 2005, plus the reinvestment of dividends. The Fund paid its initial quarterly dividend of $0.40 per share on December 31, 2005. This dividend represents an annualized distribution yield of 8% based on the Fund’s initial offering price of $20.

The Fund’s market price is trading at a discount to its NAV. This discount from NAV highlights the fact that most closed-end funds have fallen out of favor with investors recently. However, we feel that this discount represents an opportunity as common shares of the Fund are now available in the market at prices below the value of the securities in the underlying portfolio.

Shareholders have the opportunity to reinvest their dividends from the Fund through the Dividend Reinvestment Plan (DRIP) that is described in detail on page 26 of this report. If shares trade at a discount to NAV, the DRIP takes advantage of the discount by reinvesting the quarterly dividend distribution in common shares of the Fund purchased in the market at a price less than NAV. Conversely, when the market price of the Fund’s common shares is at a premium above NAV, the DRIP reinvests participants’ dividends in newly-issued common shares at NAV, subject to an IRS limitation that the purchase price cannot be more than 5% below the market price per share. The DRIP provides a cost effective means to accumulate additional shares and enjoy the benefits of compounding returns over time.

To learn more about the Fund’s performance over this fiscal period, we encourage you to read the Questions & Answers section of the report on page 4. You will find information on Analytic’s investment philosophy and discipline and their views on the overall market environment and how they structured the portfolio based on their views.

We appreciate your investment and look forward to serving your investment needs in the future. For the most up-to-date information on your investment, please visit the Fund’s website at www.oldmutualclaymore.com.

Sincerely,

|

Nicholas Dalmaso |

| Old Mutual/Claymore Long-Short Fund |

February 3, 2006

| Annual Report | December 31, 2005 | 3 |

OLA | Old Mutual/Claymore Long-Short Fund

Questions & Answers |

Dennis M. Bein, CFA

Chief Investment Officer, Portfolio Manager

Analytic Investors, Inc.

As Chief Investment Officer, Dennis Bein oversees the implementation of Analytic’s investment strategies. He is a major contributor to the firm’s ongoing research efforts as well as to the new product development efforts and strategy applications. As Portfolio Manager, Bein directs the Fund’s management team on day-to-day portfolio management and research related to the Fund’s equity-based investment strategies. Bein joined Analytic in 1995, and has more than 15 years of investment experience. He is a CFA charterholder and earned an M.B.A. from the Anderson Graduate School of Management, University of California, Riverside.

The Old Mutual/Claymore Long-Short Fund is managed by Analytic Investors, Inc. In the following interview, Chief Investment Officer and Portfolio Manager Dennis Bein, CFA, explains how he and his team of investment professionals structured the portfolio. He also discusses the Fund’s performance from its inception on August 25, 2005 through December 31, 2005, the end of its annual fiscal period.

Before we discuss performance, will you first remind us of the Fund’s investment objectives and explain how your investment process seeks to achieve those objectives?

The Fund’s investment objective is to seek a high level of current income and gains with a secondary objective of long-term capital appreciation. The Fund seeks to achieve that objective by investing in a diversified portfolio of common stocks and other equity securities utilizing a 120% long/20% short strategy (“120/20”) and opportunistically employing a strategy of writing (selling) calls on equity indexes. This 120/20 strategy provides the Fund with full market exposure and participation relative to the S&P 500 Index. The S&P 500 Index is generally considered representative of the U.S. stock market. The Fund’s short position allows us to take advantage of securities that we believe are likely to experience declines.

Our investment process begins by utilizing quantitative models to develop an equity portfolio that offers the potential for capital appreciation. The portfolio is constructed with a level of diversification and risk similar to that of the S&P 500 Index, but is designed to outperform the index over a full market cycle by having its long positions invested in what we believe are the stocks that will outperform, while selling short the stocks that we believe will be the underperformers. To generate income and help reduce volatility, we then apply a call options overlay.

We believe our investment strategy is unique in the following ways.

Our Stock Selection Process Our process begins by analyzing stock characteristics, rather than focusing on individual stocks like many investment managers do. Our quantitative review is based on sophisticated mathematical models focused on variables that cover multiple dimensions of a stock’s true value, such as its valuation, growth potential, historical return patterns, liquidity and risk. The system identifies characteristics that are currently being rewarded or punished by investors through examining a universe of approximately 3,000

4 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund | Questions & Answers continued

stocks to determine which financial characteristics are shared by the market’s largest gaining or losing stocks. Stocks possessing favorable characteristics are ranked highly and become good candidates for the long portfolio. Stocks that possess unfavorable characteristics rank poorly and are good candidates for the short portfolio. Ultimately a portfolio of at least 75 highly-ranked stocks is combined with short positions in 20 to 30 low-ranked stocks. We monitor the portfolio on a real-time basis using our proprietary management system that identifies media events or changes in fundamental factors that are potentially significant for the portfolio holdings. However, we only trade securities when we believe the incremental return potential will exceed the associated transaction costs.

What is a short sale?

A short sale is a three-step trading strategy that seeks to capitalize on an anticipated decline in the price of a security. First, arrangements are made to borrow shares of the security, typically from a broker. Next, the investor will sell the shares immediately in the open market with the intention of buying them back at some point in the future. Finally, to complete the cycle, at a later date he/she will repurchase the shares (hopefully at a lower price) and will return them to the lender. In the end, the investor will pocket the difference if the share price falls, but will of course incur a loss if it rises.

Options Overlay This Fund is unique because we typically won’t write (sell) call options on individual securities like a traditional covered call fund might. We prefer to sell options on index options, since we have strong convictions about the stocks we own. This strategy helps preserve the upside potential on our individual equity holdings, which is more important to us than giving away the upside potential of the market sectors on which we’ve written the calls. We believe giving away market or sector upside potential in exchange for lower overall volatility and a higher yield provided by the call options premiums benefits the Fund.

What is an index option?

An index option is a contract which gives the buyer the right to participate in market gains over and above (in the case of a call) or below (in the case of a put) at a specified price (the strike price) on or before a pre-determined date (the expiration date). After this pre-determined date, the option and its corresponding rights expire. For example, the seller of an index call option is obligated, until the expiration date, to pay the holder of the option the difference between the index price and the option’s strike price, upon the holder’s request. The price of the option is determined from trading activity in the options market, and generally reflects the relationship between the current price for the index and the strike price, as well as the time remaining until the expiration date.

Will you provide a market overview for the fiscal period and discuss the Fund’s performance?

There was considerable volatility within the market from the Fund’s inception on August 25, 2005 through December 31, 2005. Days after the Fund’s inception, Hurricanes Katrina and Rita waged destruction on the Gulf Coast and crude oil prices reached historically high levels. Ongoing geopolitical events supported the

| Annual Report | December 31, 2005 | 5 |

OLA | Old Mutual/Claymore Long-Short Fund | Questions & Answers continued

volatility as did conjecture about whether the Federal Reserve Board was nearing an end to its interest rate tightening cycle. In the end, however, stocks posted strong gains, and the Standard & Poor’s 500 Index returned 3.65% during the fiscal period. Index returns include the reinvestment of all distributions. It is not possible to invest directly in an index.

The Fund generated a total return of 0.52% at net asset value (“NAV”). This represents a change in NAV from $19.10 at inception to $18.80 on December 31, 2005, plus the reinvestment of the Fund’s quarterly distribution. While the Fund underperformed the S&P 500 during this period, it outperformed the negative - -0.04% return of the CBOE BuyWrite Index (“BXM”). The BXM is an index that simulates an ongoing covered call strategy on the S&P 500 and consists of an unmanaged portfolio of stocks upon which a one-month call option on the S&P 500 is continuously written.

The Fund’s NAV underperformance relative to the S&P 500 was due in part to our stock selection, but to a greater degree it was due to the Fund’s options overlay. The Fund’s covered call program is designed to limit the Fund’s downside risk when the market declines. Conversely, it impedes performance when the market rises, as it did in this period. We believe, however, that the BXM is an index more reflective of the Fund’s structure than the S&P 500. With that said, we’re pleased with the Fund’s performance relative to the BXM.

During this same period, the Fund’s total return based on market price was a negative return of -15.76%. This reflects a change in market price from $20.00 at inception to $16.47 on December 31, 2005, plus the reinvestment of the Fund’s quarterly distributions. The decline in the Fund’s market price and its deep discount to the Fund’s NAV was disappointing. As the Fund’s investment manager we have a clear objective of providing a high level of current income and gains for shareholders. We are pleased that the Fund earned and paid its initial quarterly dividend of $0.40 per share on December 31, 2005. This dividend represents an annualized distribution yield of 8% based on the Fund’s initial offering price of $20. We believe that if we can continue to deliver a favorable distribution rate and improve the Fund’s net asset value, its discount to market price will improve. Market price may also be helped by positive analyst ratings and media coverage – both of which the Fund received during this period.

Will you provide examples of characteristics favored by your quantitative model during the period and explain how this information impacted Fund performance?

The model pointed us to companies with positive earnings estimate revisions, strong projected earnings growth rates, above average sales and revenues relative to price, and those with above average return on assets.

The model deemphasized companies with above-average dividend yield, above-average trading volume, and those with strong asset utilization/turnover.

6 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund | Questions & Answers continued

We structured the long equity portfolio and sold short positions based on the model’s assumptions and our fundamental review. In some cases, these assumptions translated into gains for the Fund. In other cases, they directed us to investments that detracted from performance.

Examples of stocks that helped performance Based on the model’s assumptions, we established an overweight position in Darden Restaurants (1.8% of long-term investments and securities sold short) because of the company’s strong estimate revisions scores. Darden Restaurants is the parent company of the Olive Garden and Red Lobster restaurant chains. Darden rallied strongly in the period after it posted a better-than-expected rise in quarterly earnings and boosted its profit outlook for the year. We established an equity position in Yahoo! Inc. (0.2% of long-term investments and securities sold short) because of its strong projected earnings growth rate. Yahoo! provides Internet services and a range of tools and marketing solutions for businesses. The stock rallied strongly after a surge in third quarter revenue was announced. The Fund also benefited from its short position in OfficeMax, Inc. (0.4% of long-term investments and securities sold short) We shorted the office supply retailer because of its above-average trading volume and below-average earnings estimate revisions. The stock moved lower in the period after the company reported a deeper-than-expected loss for the third quarter as a result of sluggish retail sales. The Fund profited from the stock’s decline as a result of using the short sale strategy.

Examples of stocks that hurt performance Strong sales relative to stock price led us to invest in CenterPoint Energy, Inc. (1.0% of long-term investments and securities sold short) The company, which distributes natural gas and electric energy, declined with the energy sector in the fourth quarter and on news that it would restate its finances to correct accounting errors that overstated the company’s revenue and natural gas expenses. The Fund’s overweight position in Johnson & Johnson (“J&J”) (3.1% of long-term investments and securities sold short) relative to the S&P 500 was also disappointing. J&J is a pharmaceutical, medical device and consumer products company. We liked J&J because of the strong return on assets it had been providing. Pharmaceutical companies struggled in the period and so did J&J. The company’s stock also declined when a company it had been pursuing to acquire announced failures in some of its medical device products. Janus Capital Group, Inc. (0.5% of long-term investments and securities sold short) is an example of a short position we took on a stock that gained ground in the period. We shorted this issuer, an investment products firm, because of its poor sales relative to its price per share, which suggested to us that its stock price was overvalued.

| Annual Report | December 31, 2005 | 7 |

OLA | Old Mutual/Claymore Long-Short Fund | Questions & Answers continued

The stock rallied, however, after Janus named a new chief executive officer and reported better-than- expected earnings and strong investor cash flows.

The Fund’s stock holdings provided mixed performance during this short period. While we were disappointed, we are not surprised at the results. The fiscal period was one of transition within the market and one in which investor attitudes vacillated rapidly. During such scenarios, it is likely that the Fund’s quantitative model will be less effective in its selection process and the stock portfolio may not provide its best returns. We would expect better equity performance within the portfolio during periods in which there are more consistent trends in place.

How quickly do you adjust portfolio holdings based on changing opinions toward characteristics?

We closely monitor the Fund’s portfolio and the dynamics of characteristics within the market. As soon as we see a characteristic begin to fall out of investors’ favor we react immediately, but not dramatically, by lessening the Fund’s exposure to stocks with that characteristic. We move the portfolio gradually to guard against being “whipsawed” based on what could simply be a temporary change in investor preferences. If investor preferences continue to shift, we continue to shift the portfolio away from the characteristic that is falling out of favor. We liken our approach to navigating a sailboat. We follow the direction of the wind slowly and steadily, not dramatically. If things reverse course, we adjust our direction.

Are you able to preserve potential upside in a strong equity market given the Fund’s options overlay strategy?

As with our equity portfolio, we actively manage the Fund’s options strategy. If market shifts cause our options to move “into the money,” meaning we’re sacrificing premiums and giving away upside potential, we’ll actively move (or roll) the options to higher strike prices in order to capture some of the appreciation in price as the underlying basket of securities moves higher. Conversely, if the market is declining and the options are not providing enough protection, we’ll trade out of those positions and establish other more favorable and defensive options positions. We work hard to add value at both and equity and options level at all times.

What is your outlook for the market and the Fund in 2006?

The valuation of the U.S. equity market remains attractive versus relatively low bond yields as the forecasted earnings for the S&P 500 improved in the fourth quarter of 2005. On a global basis, however, U.S. valuations still appear slightly more expensive than average. In this type of environment, we expect slightly higher-than-average returns for the U.S. equity market, which should produce strong positive returns for the Fund, though likely limited value added relative to the S&P 500.

8 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund | Questions & Answers continued

OLA Risks and Other Considerations

The Fund is a newly organized, diversified, closed-end management investment company with no history of operations. As with any stock, the price of the Fund’s Common Shares will fluctuate with market conditions and other factors. Shares of closed-end management investment companies frequently trade at a discount from their net asset value. If you sell your common shares, you may receive more or less than your original investment. Net asset value will be reduced immediately following the initial offering by the sales load and by offering expenses paid or reimbursed by the Fund. The Fund’s Common Shares may trade at a price that is less than their initial offering price. This risk may be greater for investors who sell their shares relatively shortly after completion of the initial public offering. The common shares are designed for long-term investors and should not be treated as a vehicle for trading.

The Fund will ordinarily have substantial exposure (both long and short) to common stocks and other equity securities in pursuing its investment objectives and policies. The market price of common stocks and other equity securities in which the Fund invests may go up or down, sometimes rapidly or unpredictably. Equity securities may decline in value due to factors affecting equity securities markets generally, particular industries represented in those markets or the issuer itself.

The Fund is expected to make substantial use of short sales for investment and risk management purposes, including when Analytic anticipates that the market price of securities will decline or will underperform relative to other securities held in the Fund’s portfolio. The Fund initially intends to take short equity positions in an amount equal to approximately 20% of the Fund’s net assets at the time of sale, but reserves the flexibility to hold short positions of up 70% of net assets. Short sales are transactions in which the Fund sells a security or other instrument (such as an option, forward, futures or other derivative contract) that it does not own. When the Fund engages in a short sale on a security, it must borrow the security sold short and deliver it to the counterparty. The Fund will ordinarily have to pay a fee or premium to borrow particular securities and be obligated to repay the lender of the security any dividends or interest that accrue on the security during the period of the loan. The amount of any gain from a short sale will be decreased, and the amount of any loss increased, by the amount of the premium, dividends, interest or expenses the Fund pays in connection with the short sale. Short sales expose the Fund to the risk that it will be required to cover its short position at a time when the securities have appreciated in value, thus resulting in a potentially unlimited loss to the Fund.

The distributions shareholders receive from the Fund are based primarily on the dividends it earns from its equity investments as well as the gains the Fund receives from writing options and using other derivative instruments, closing out short sales and selling portfolio securities, each of which can vary widely over the short and long term. The dividend income from the Fund’s investments in equity securities will be influenced by both general economic activity and issuer-specific factors. In the event of a recession or adverse events affecting a specific industry or issuer, an issuer of equity securities held by the Fund may reduce the dividends paid on such securities. If prevailing market interest rates decline, interest rates on any debt instruments held by the Fund, and shareholders’ income from the Fund, would likely decline as well. Please see “Distributions” for a description of other risks associated with the level, timing and character of the Fund’s distributions.

There are various risks associated with the Option Strategy. The purchaser of an index option written by the Fund has the right to any appreciation in the cash value of the index over the strike price on the expiration date. Therefore, as the writer of an index call option, the Fund forgoes the opportunity to profit from increases in the index over the strike price of the option. However, the Fund has retained the risk of loss (net of premiums received) should the price of the Fund’s portfolio securities decline. Similarly, as the writer of a call option on an individual security held in the Fund’s portfolio, the Fund forgoes, during the option’s life, the opportunity to profit from increases in the market value of the security covering the call option above the sum of the premium and the strike price of the call but has retained the risk of loss (net of premiums received) should the price of the underlying security decline. The value of options written by the Fund, which will be priced daily, will be affected by, among other factors, changes in the value of underlying securities (including those comprising an index), changes in the dividend rates of underlying securities, changes in interest rates, changes in the actual or perceived volatility of the stock market and underlying securities and the remaining time to an option’s expiration. The value of an option also may be adversely affected if the market for the option is reduced or becomes less liquid.

An investment in the Fund is subject to certain risks and other considerations, including, but not limited to: Equity Risk; Short Sale Risk; Options Risk, Management Risk; Tax Treatment of Distributions; Derivatives Risk; Counterparty Risk; Credit Risk; Income Risk; Medium- and Smaller-Company Risk; Focused Investment Risk; Interest Rate Risk; Liquidity Risk; Market Disruption and Geopolitical Risk; Leverage Risk; Foreign Investment Risk; Other Investment Companies Risk; and Inflation/Deflation Risk.

Investors should consider the investment objectives and policies, risk considerations, charges and expenses of the Fund carefully before investing.

| Annual Report | December 31, 2005 | 9 |

OLA | Old Mutual/Claymore Long-Short Fund

Fund Summary | As of December 31, 2005 (unaudited)

Fund Statistics | ||||

Share Price | $ | 16.47 | ||

Common Share Net Asset Value | $ | 18.80 | ||

Premium/(Discount) to NAV | -12.39 | % | ||

Net Assets ($000) | $ | 357,292 | ||

Total Returns | Market | NAV | ||||

Since Inception – cumulative | - 15.76 | % | 0.52 | % |

Sector Breakdown | % of Long-Term Investments and Securities Sold Short | ||

Financials | 23.8 | % | |

Energy | 14.5 | % | |

Technology | 14.1 | % | |

Consumer Discretionary | 13.2 | % | |

Health Care | 9.5 | % | |

Industrials | 6.9 | % | |

Consumer Staples | 6.9 | % | |

Telecommunications | 5.5 | % | |

Materials | 4.8 | % | |

Utilities | 0.8 | % |

Securities are classified by sectors that represent broad groupings of related industries.

Top Ten Long-Term Holdings | % of Net Assets | ||

Exxon Mobil Corp. | 4.3 | % | |

Johnson & Johnson | 4.1 | % | |

Allstate Corp. | 3.1 | % | |

International Business Machines Corp. | 3.1 | % | |

Intel Corp. | 3.0 | % | |

Chevron Corp. | 2.9 | % | |

St. Paul Travelers Cos., Inc. | 2.9 | % | |

MetLife, Inc. | 2.8 | % | |

Fortune Brands, Inc. | 2.7 | % | |

Home Depot, Inc. | 2.7 | % |

Sectors and holdings are subject to change daily. For more current information, please visit www.claymore.com The above summaries are provided for informational purposes only and should not be viewed as recommendations. Past performance does not guarantee future results.

Share Price & NAV Performance

Distributions to Shareholders

Top Five Securities Sold Short | % of Net Assets | ||

XL Capital, Ltd. | 2.3 | % | |

Kinder Morgan, Inc. | 2.2 | % | |

CenturyTel, Inc. | 1.8 | % | |

Vulcan Materials Co. | 1.0 | % | |

Temple-Inland, Inc. | 0.9 | % |

10 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund

Portfolio of Investments | December 31, 2005

| Number of Shares | Value | ||||

| Long-Term Investments - 113.8% | |||||

| Common Stocks - 113.8% | |||||

| Consumer Discretionary - 14.8% | |||||

| 15,925 | AutoNation, Inc. (a)(b) | $ | 346,050 | ||

| 24,741 | Black & Decker Corp. (b) | 2,151,477 | |||

| 217,726 | Brunswick Corp. (b) | 8,852,739 | |||

| 11,917 | Carnival Corp. (b) | 637,202 | |||

| 170,129 | Cendant Corp. (b) | 2,934,725 | |||

| 223,986 | Darden Restaurants, Inc. (b) | 8,708,576 | |||

| 238,726 | Home Depot, Inc. (b) | 9,663,628 | |||

| 6,315 | J.C. Penny Co., Inc. (b) | 351,114 | |||

| 21,000 | Lennar Corp.- Class A | 1,281,420 | |||

| 28,140 | News Corp.- Class A (b) | 437,577 | |||

| 139,898 | VF Corp. | 7,741,955 | |||

| 43,965 | Wal-Mart Stores, Inc. | 2,057,562 | |||

| 319,114 | Walt Disney Co. (b) | 7,649,163 | |||

| 52,813,188 | |||||

| Consumer Staples - 8.6% | |||||

| 24,521 | Altria Group, Inc. | 1,832,209 | |||

| 106,197 | Archer-Daniels - Midland Co. (b) | 2,618,818 | |||

| 14,394 | Clorox Co. (b) | 818,875 | |||

| 285,589 | Coca-Cola Enterprises, Inc. (b) | 5,474,741 | |||

| 47,246 | Constellation Brands, Inc.- Class A (a)(b) | 1,239,263 | |||

| 125,420 | Fortune Brands, Inc. (b) | 9,785,268 | |||

| 8,057 | Reynolds American, Inc. | 768,074 | |||

| 11,842 | SUPERVALU, Inc. (b) | 384,628 | |||

| 455,347 | Tyson Foods, Inc.- Class A (b) | 7,786,434 | |||

| 30,708,310 | |||||

| Energy - 16.1% | |||||

| 15,137 | Amerada Hess Corp. (b) | 1,919,674 | |||

| 10,776 | Burlington Resources, Inc. (b) | 928,891 | |||

| 356,955 | CenterPoint Energy, Inc. (b) | 4,586,872 | |||

| 184,266 | Chevron Corp. (b) | 10,460,781 | |||

| 42,346 | ConocoPhillips (b) | 2,463,690 | |||

| 123,432 | Devon Energy Corp. (b) | 7,719,437 | |||

| 70,350 | Edison International (b) | 3,067,963 | |||

| 274,311 | Exxon Mobil Corp. | 15,408,049 | |||

| 29,139 | Marathon Oil Corp. | 1,776,605 | |||

| 6,204 | Murphy Oil Corp. | 334,954 | |||

| 4,385 | Nabors Industries, Ltd. (Bermuda) (a)(b) | 332,164 | |||

| 10,041 | Occidental Petroleum Corp. (b) | 802,075 | |||

| 149,816 | TXU Corp. (b) | 7,519,265 | |||

| 57,320,420 | |||||

| Financials - 27.8% | |||||

| 204,186 | Allstate Corp. (b) | 11,040,337 | |||

| 55,692 | American Express Co. (b) | 2,865,910 | |||

| 45,089 | American International Group, Inc. (b) | 3,076,422 | |||

| 121,835 | Bank of America Corp. (b) | 5,622,685 | |||

| 3,041 | Bear Stearns Cos., Inc. (b) | 351,327 | |||

| 10,074 | Capital One Financial Corp. (b) | 870,394 | |||

| 13,771 | CIGNA Corp. (b) | 1,538,221 | |||

| 6,681 | CIT Group, Inc. (b) | 345,942 | |||

| 14,405 | Citigroup, Inc. (b) | 699,075 | |||

| 93,465 | Countrywide Financial Corp. (b) | 3,195,568 | |||

| 11,154 | Goldman Sachs Group, Inc. (b) | 1,424,477 | |||

| 341,072 | H&R Block, Inc. (b) | 8,373,318 | |||

| 31,104 | Hartford Financial Services Group, Inc. (b) | 2,671,523 | |||

| 111,432 | JPMorgan Chase & Co. (b) | 4,422,736 | |||

| 29,377 | Lehman Brothers Holdings, Inc. | 3,765,250 | |||

| 62,737 | Loews Corp. (b) | 5,950,604 | |||

| 35,171 | MBNA Corp. (b) | 954,893 | |||

| 203,448 | MetLife, Inc. (b) | 9,968,952 | |||

| 59,697 | PNC Financial Services Group, Inc. | 3,691,066 | |||

| 90,850 | Simon Property Group, Inc. (b) | 6,961,836 | |||

| 231,518 | St. Paul Travelers Cos., Inc. (b) | 10,341,909 | |||

| 63,182 | Wachovia Corp. | 3,339,801 | |||

| 42,302 | Washington Mutual, Inc. (b) | 1,840,137 | |||

| 96,179 | Wells Fargo & Co. | 6,042,927 | |||

| 99,355,310 | |||||

| Health Care - 12.4% | |||||

| 86,457 | Abbott Laboratories (b) | 3,409,000 | |||

| 220,662 | AmerisourceBergen Corp. (b) | 9,135,407 | |||

| 14,466 | Amgen, Inc. (a)(b) | 1,140,789 | |||

| 20,986 | Becton, Dickinson & Co. (b) | 1,260,839 | |||

| 18,708 | Boston Scientific Corp. (a)(b) | 458,159 | |||

| 8,719 | C.R. Bard, Inc. (b) | 574,756 | |||

| 5,098 | Cardinal Health, Inc. (b) | 350,488 | |||

| 32,767 | Fisher Scientific International, Inc. (a)(b) | 2,026,967 | |||

| 55,728 | Forest Laboratories, Inc. (a)(b) | 2,267,015 | |||

| 8,792 | Guidant Corp. (b) | 569,282 | |||

| 23,549 | Humana, Inc. (a)(b) | 1,279,417 | |||

| 243,648 | Johnson & Johnson (b) | 14,643,245 | |||

| 63,394 | McKesson Corp. (b) | 3,270,496 | |||

| 104,527 | Pfizer, Inc. (b) | 2,437,570 | |||

| 29,870 | Quest Diagnostics, Inc. (b) | 1,537,708 | |||

| 44,361,138 | |||||

See notes to financial statements.

| Annual Report | December 31, 2005 | 11 |

OLA | Old Mutual/Claymore Long-Short Fund | Portfolio of Investments continued

| Number of Shares | Value | ||||||

| Industrials - 7.8% | |||||||

| 6,975 | CSX Corp. (b) | $ | 354,121 | ||||

| 21,254 | Cummins, Inc. (b) | 1,907,121 | |||||

| 25,923 | D.R. Horton, Inc. (b) | 926,229 | |||||

| 35,188 | Eaton Corp. (b) | 2,360,763 | |||||

| 8,244 | General Dynamics Corp. (b) | 940,228 | |||||

| 32,425 | General Electric Co. (b) | 1,136,496 | |||||

| 13,324 | Goodrich Corp. (b) | 547,616 | |||||

| 77,319 | KB HOME (b) | 5,617,999 | |||||

| 8,085 | L-3 Communications Holdings, Inc. (b) | 601,120 | |||||

| 34,026 | Lockheed Martin Corp. (b) | 2,165,074 | |||||

| 27,347 | Navistar International Corp. (a)(b) | 782,671 | |||||

| 30,701 | Pulte Homes, Inc. (b) | 1,208,391 | |||||

| 8,221 | Ryder System, Inc. (b) | 337,225 | |||||

| 87,897 | Union Pacific Corp. | 7,076,587 | |||||

| 26,926 | United Parcel Service, Inc.- Class B | 2,023,489 | |||||

| 27,985,130 | |||||||

| Materials - 4.1% | |||||||

| 120,090 | Ball Corp. (b) | 4,769,975 | |||||

| 130,353 | Dow Chemical Co. (b) | 5,712,068 | |||||

| 200,311 | Hercules Inc. (a)(b) | 2,263,514 | |||||

| 19,959 | Newmont Mining Corp. (b) | 1,065,811 | |||||

| 16,701 | Sherwin-Williams Co. (b) | 758,559 | |||||

| 14,569,927 | |||||||

| Technology - 17.0% | |||||||

| 106,180 | Affiliated Computer Services, Inc.- Class A (a)(b) | 6,283,732 | |||||

| 101,818 | Amazon.com, Inc. (a)(b) | 4,800,719 | |||||

| 26,245 | Autodesk, Inc. (a)(b) | 1,127,223 | |||||

| 294,515 | Cisco Systems, Inc. (a)(b) | 5,042,097 | |||||

| 46,739 | Dell, Inc. (a)(b) | 1,401,703 | |||||

| 135,792 | Freescale Semiconductor, Inc.- Class B (a)(b) | 3,417,885 | |||||

| 228,585 | Hewlett-Packard Co. (b) | 6,544,389 | |||||

| 436,263 | Intel Corp. (b) | 10,889,124 | |||||

| 133,022 | International Business Machines Corp. (b) | 10,934,408 | |||||

| 18,216 | Intuit, Inc. (a) | 970,913 | |||||

| 17,402 | Microsoft Corp. (b) | 455,062 | |||||

| 29,431 | NCR Corp. (a)(b) | 998,888 | |||||

| 9,400 | NVIDIA Corp. (a)(b) | 343,664 | |||||

| 27,878 | Oracle Corp. (a)(b) | 340,390 | |||||

| 21,951 | Symantec Corp. (a)(b) | 384,143 | |||||

| 190,684 | Texas Instruments, Inc. (b) | 6,115,236 | |||||

| 19,041 | Yahoo!, Inc. (a) | 746,026 | |||||

| 60,795,602 | |||||||

| Telecommunications - 5.0% | |||||||

| 16,986 | AT&T, Inc. (b) | 415,987 | |||||

| 19,870 | Comcast Corp.- Class A (a)(b) | 515,825 | |||||

| 106,351 | Motorola, Inc. (b) | 2,402,469 | |||||

| 60,084 | Qwest Communications International, Inc. (a)(b) | 339,475 | |||||

| 218,033 | Sprint Nextel Corp. (b) | 5,093,251 | |||||

| 302,225 | Verizon Communications, Inc. | 9,103,017 | |||||

| 17,870,024 | |||||||

| Utilities - 0.2% | |||||||

| 21,461 | AES Corp. (a)(b) | 339,728 | |||||

| 6,420 | Public Service Enterprise Group, Inc. (b) | 417,107 | |||||

| 756,835 | |||||||

Total Long-Term Investments (Cost $413,094,976) | $ | 406,535,884 | |||||

| Principal Amount | Value | ||||||

| Short-Term Investments - 4.6% | |||||||

| U.S Government and Agency Securities - 4.6% | |||||||

| $ | 3,000,000 | Federal Home Loan Discount Notes, yielding | |||||

| 3.50%, 1/6/06 (c) | $ | 2,998,968 | |||||

| 13,600,000 | U.S. Treasury Bills, yielding | ||||||

| 3.60% - 3.86%, 2/23/06 (b)(c) | 13,526,560 | ||||||

Total Short-Term Investments (Cost $16,525,467) | 16,525,528 | ||||||

Total Investments - 118.4% (Cost $429,620,443) | 423,061,412 | ||||||

Securities Sold Short - (18.9%) (Proceeds $66,419,335) | (67,443,291 | ) | |||||

| Other Assets less Liabilities - 0.8% | 2,933,297 | ||||||

| Total Value of Options Written - (0.3%) | (1,259,800 | ) | |||||

| Net Assets - 100.0% | $ | 357,291,618 | |||||

See notes to financial statements.

12 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund | Portfolio of Investments continued

| Number of Shares | Value | ||||

| Securities Sold Short - 18.9% | |||||

| Common Stocks - 18.9% | |||||

| Consumer Discretionary - 2.7% | |||||

| 168,164 | Cooper Tire & Rubber Co. | $ | 2,576,272 | ||

| 12,514 | Dow Jones & Co., Inc. | 444,122 | |||

| 27,952 | New York Times Co.- Class A | 739,330 | |||

| 56,117 | Tiffany & Co. | 2,148,720 | |||

| 13,965 | Univision Communications, Inc.- Class A (a) | 410,431 | |||

| 117,115 | Visteon Corp. (a) | 733,140 | |||

| 48,614 | Wendy’s International, Inc. | 2,686,410 | |||

| 9,738,425 | |||||

| Consumer Staples - 0.5% | |||||

| 48,310 | Avon Products, Inc. | 1,379,251 | |||

| 6,317 | BrownForman Corp.- Class B | 437,894 | |||

| 1,817,145 | |||||

| Energy - 3.1% | |||||

| 27,498 | EOG Resources, Inc. | 2,017,528 | |||

| 85,091 | Kinder Morgan, Inc. | 7,824,117 | |||

| 59,765 | Williams Cos., Inc. | 1,384,755 | |||

| 11,226,400 | |||||

| Financials - 3.8% | |||||

| 23,325 | Ambac Financial Group, Inc. | 1,797,425 | |||

| 131,339 | Janus Capital Group, Inc. | 2,446,846 | |||

| 9,525 | MBIA, Inc. | 573,024 | |||

| 7,416 | Northern Trust Corp. | 384,297 | |||

| 121,421 | XL Capital, Ltd.- Class A (Cayman Islands) | 8,181,347 | |||

| 13,382,939 | |||||

| Health Care - 0.2% | |||||

| 22,272 | MedImmune, Inc. (a) | 779,965 | |||

Industrials - 1.4% | |||||

| 57,293 | Avery Dennison Corp. | 3,166,584 | |||

| 68,597 | OfficeMax, Inc. | 1,739,620 | |||

| 4,906,204 | |||||

| Materials - 2.3% | |||||

| 14,691 | Ashland, Inc. | 850,609 | |||

| 74,136 | Temple-Inland, Inc. | 3,325,000 | |||

| 54,817 | Vulcan Materials Co. | 3,713,852 | |||

| 5,768 | Weyerhaeuser Co. | 382,649 | |||

| 8,272,110 | |||||

| Technology - 1.7% | |||||

| 103,424 | International Game Technology | 3,183,391 | |||

| 46,550 | KLA-Tencor Corp. | 2,296,311 | |||

| 63,858 | PMC-Sierra, Inc. (a) | 492,345 | |||

| 5,972,047 | |||||

| Telcommunications - 2.4% | |||||

| 188,779 | CenturyTel, Inc. | 6,259,912 | |||

| 199,685 | Tellabs, Inc. (a) | 2,176,566 | |||

| 8,436,478 | |||||

| Utilities - 0.8% | |||||

| 70,413 | Pinnacle West Capital Corp. | 2,911,578 | |||

Total Securities Sold Short (Proceeds $66,419,335) | $ | 67,443,291 | |||

Contracts (100 shares per contract) | Call Options Written(a) | Expiration Date | Exercise Price | Value | ||||||

| 103 | Dow Jones Utilities | January 2006 | $ | 420.00 | $ | 10,300 | ||||

| 200 | Morgan Stanley Cyclical IX | January 2006 | 810.00 | 35,000 | ||||||

| 1,450 | Philadelphia KBW Bank Index | January 2006 | 102.50 | 304,500 | ||||||

| 350 | Philadelphia Utility Index | January 2006 | 452.50 | 17,500 | ||||||

| 500 | S&P 500 Index | January 2006 | 1,250.00 | 565,000 | ||||||

| 500 | S&P 500 Index | January 2006 | 1,265.00 | 280,000 | ||||||

| 950 | S&P 500 Index | January 2006 | 1,300.00 | 47,500 | ||||||

Total Call Options Written (Premiums received $2,306,421) | $ | 1,259,800 | ||||||||

| (a) | Non-income producing security. |

| (b) | All or a portion of these securities are held as collateral for Securities Sold Short, options, forwards and futures. |

| (c) | Interest rate shown represents discount rate at time of purchase. |

See notes to financial statements.

| Annual Report | December 31, 2005 | 13 |

OLA | Old Mutual/Claymore Long-Short Fund

Statement of Assets and Liabilities | December 31, 2005

Assets | ||||

Investments, at value (cost $429,620,443) | $ | 423,061,412 | ||

Cash | 1,773,442 | |||

Receivable for securities sold | 33,697,425 | |||

Unrealized appreciation on forward currency contracts | 658,351 | |||

Dividends and interest receivable | 377,058 | |||

Variation margin on futures | 371,251 | |||

Other assets | 4,495 | |||

Total assets | 459,943,434 | |||

Liabilities | ||||

Securities sold short, at value (proceeds $66,419,335) | 67,443,291 | |||

Options written, at value (premiums received of $2,306,421) | 1,259,800 | |||

Payable for securities purchased | 33,094,192 | |||

Offering costs payable | 333,648 | |||

Advisory fee payable | 309,318 | |||

Accrued expenses | 211,567 | |||

Total liabilities | 102,651,816 | |||

Net Assets | $ | 357,291,618 | ||

Composition of Net Assets | ||||

Common stock, $.01 par value per share; | $ | 190,052 | ||

Additional paid-in capital | 362,050,032 | |||

Net realized gain on investments, futures, options, securities sold short, forwards and currency transactions | 3,675,387 | |||

Net unrealized depreciation on investments, futures, options, securities sold short, forwards and currency translation | (5,747,753 | ) | ||

Distributions in excess of net investment income | (2,876,100 | ) | ||

Net Assets | $ | 357,291,618 | ||

Net Asset Value (based on 19,005,240 common shares outstanding) | $ | 18.80 | ||

See notes to financial statements.

14 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund

Statement of Operations | For the Period August 25, 2005* through December 31, 2005

Investment Income | |||||||

Dividends | $ | 2,356,140 | |||||

Interest | 493,445 | ||||||

Total income | $ | 2,849,585 | |||||

Expenses | |||||||

Advisory fee | 1,226,289 | ||||||

Dividends on securities sold short | 383,861 | ||||||

Custodian fee | 168,273 | ||||||

Professional fees | 71,010 | ||||||

Trustees’ fees and expenses | 63,815 | ||||||

Administration fee | 34,718 | ||||||

Fund accounting | 31,256 | ||||||

Printing expense | 22,903 | ||||||

Transfer agent fee | 17,027 | ||||||

NYSE listing fee | 11,801 | ||||||

Insurance | 5,600 | ||||||

Miscellaneous | 7,455 | ||||||

Total expenses | 2,044,008 | ||||||

Net investment income | 805,577 | ||||||

Realized and Unrealized Gain (Loss): | |||||||

Net realized gain (loss) on: | |||||||

Investments | 12,953,722 | ||||||

Futures | (647,783 | ) | |||||

Options | (4,579,570 | ) | |||||

Securities sold short | 1,149,267 | ||||||

Foreign currency forwards and currency transactions | (1,279,830 | ) | |||||

Net unrealized appreciation (depreciation) on: | |||||||

Investments | (6,559,031 | ) | |||||

Futures | 133,618 | ||||||

Options | 1,046,621 | ||||||

Securities sold short | (1,023,956 | ) | |||||

Foreign currency forwards and currency translation | 654,995 | ||||||

Net realized and unrealized gain | 1,848,053 | ||||||

Net Increase in Net Assets Resulting from Operations | $ | 2,653,630 | |||||

| * | Commencement of investment operations. |

See notes to financial statements.

| Annual Report | December 31, 2005 | 15 |

OLA | Old Mutual/Claymore Long-Short Fund

Statement of Changes in Net Assets |

For the Period August 25, 2005* through December 31, 2005 | ||||

Increase (Decrease) in Net Assets from Operations | ||||

Net investment income | $ | 805,577 | ||

Net realized gain on investments, futures, options, securities sold short, forwards and currency transactions | 7,595,806 | |||

Net unrealized depreciation on investments, futures, options, securities sold short, forwards and currency translation | (5,747,753 | ) | ||

Net increase in net assets resulting from operations | 2,653,630 | |||

Distributions to Common Shareholders | ||||

From and in excess of net investment income | (7,602,096 | ) | ||

Capital Share Transactions | ||||

Proceeds from the issuance of common shares | 362,900,000 | |||

Common share offering costs charged to paid-in capital | (760,000 | ) | ||

Net increase from capital share transactions | 362,140,000 | |||

Total increase in net assets | 357,191,534 | |||

Net Assets | ||||

Beginning of period | 100,084 | |||

End of period (including distributions in excess of net investment income of $2,876,100) | $ | 357,291,618 | ||

| * | Commencement of investment operations. |

See notes to financial statements.

16 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund

Financial Highlights |

Per share operating performance for a common share outstanding throughout the period | For the Period August 25, 2005* through December 31, 2005 | |||

Net asset value, beginning of period | $ | 19.10 | (a) | |

Income from investment operations | ||||

Net investment income (b) | 0.04 | |||

Net realized and unrealized gain on investments, futures, options, securities sold short, forwards and currency transactions and translation | 0.10 | |||

Total from investment operations | 0.14 | |||

Common shares’ offering expenses charged to paid-in capital | (0.04 | ) | ||

Distributions to Common Shareholders | ||||

From and in excess of net investment income | (0.40 | ) | ||

Net asset value, end of period | $ | 18.80 | ||

Market value, end of period | $ | 16.47 | ||

Total investment return (c) | ||||

Net asset value | 0.52 | % | ||

Market value | -15.76 | % | ||

Ratios and supplemental data | ||||

Net assets, end of period (thousands) | $ | 357,292 | ||

Ratios to average net assets, including dividend expense on securities sold short: | ||||

Expense ratio | 1.58 | %(d)(e) | ||

Net investment income ratio | 0.75 | %(d)(e) | ||

Portfolio turnover | 60 | % | ||

| * | Commencement of investment operations. |

| (a) | Before deduction of offering expenses charged to capital. |

| (b) | Based on average shares outstanding during the period. |

| (c) | Total investment return is calculated assuming a purchase of a common share at the beginning of the period and a sale on the last day of the period reported either at net asset value (“NAV”) or market price per share. Dividends and distributions are assumed to be reinvested at NAV for NAV returns or the prices obtained under the Fund’s Dividend Reinvestment Plan for market value returns. Total investment return does not reflect brokerage commissions. A return calculated for a period of less than one year is not annualized. |

| (d) | Annualized. |

| (e) | The expense ratio includes dividend payments made on securities sold short. During the approximate four month period from August 25, 2005 through December 31, 2005, nine securities sold short made two quarterly distribution payments. The annualized ratios noted above have been adjusted such that these securities would only reflect the equivalent of four quarterly dividends per security. Had this adjustment not been made, the expense ratio would have been 1.65% and the net investment income ratio would have been 0.68%. |

See notes to financial statements.

| Annual Report | December 31, 2005 | 17 |

OLA | Old Mutual/Claymore Long-Short Fund

Notes to Financial Statements |

Note 1 – Organization:

Old Mutual/Claymore Long-Short Fund (the “Fund”) was organized as a Massachusetts business trust on December 3, 2004. The Fund is registered as a diversified, closed-end management investment company under the Investment Company Act of 1940, as amended.

The Fund’s primary investment objective is to provide a high level of current income and current gains. The Fund’s secondary investment objective is to provide long-term capital appreciation. The Fund seeks to achieve its investment objective by investing in a diversified portfolio of equity securities and by selling securities short in the S&P 500 Index that it believes will underperform relative to the average stock in the S&P 500. The Fund will also write (sell) call options on equity indexes and, to a lesser extent on individual securities held in the Fund’s portfolio. The Fund may also employ a variety of other strategies involving futures and forward contracts and other derivative instruments in an attempt to enhance the Fund’s investment returns. There can be no assurance that the Fund’s investment objective will be achieved.

Note 2 – Accounting Policies:

The preparation of the financial statements in accordance with U.S. generally accepted accounting principles requires management to make estimates and assumptions that affect the reported amounts and disclosures in the financial statements. Actual results could differ from these estimates.

The following is a summary of significant accounting policies followed by the Fund.

(a) Valuation of Investments

Equity securities listed on an exchange are valued at the last reported sale price on the primary exchange on which they are traded. Equity securities for which there are no transactions on a given day are valued at the mean of the closing bid and asked prices. Securities traded on NASDAQ are valued at the NASDAQ Official Closing Price. Equity securities not listed on a securities exchange or NASDAQ are valued at the mean of the closing bid and asked prices. Debt securities are valued by independent pricing services or dealers using the mean of the closing bid and asked prices for such securities or, if such prices are not available, at prices for securities of comparable maturity, quality and type. Exchange-traded options are valued at the mean between the bid and asked price on the primary exchange on which they are traded. Futures and options on futures contracts are valued at the settlement price determined by the exchange on which they are traded. All other types of securities, including restricted securities, and securities for which market quotations are not readily available, are valued as determined in accordance with procedures established in good faith by the Board of Trustees. Short-term securities having a remaining maturity of sixty days or less at the time of purchase are valued at amortized cost, which approximates market value.

(b) Investment Transactions and Investment Income

Investment transactions are accounted for on the trade date. Realized gains and losses on investments are determined on the identified cost basis. Dividend income is recorded net of applicable withholding taxes on the ex-dividend date and interest income is recorded on an accrual basis. Discounts or premiums on debt securities purchased are accreted or amortized to interest income over the lives of the respective securities using the effective interest method.

(c) Futures

The Fund may engage in asset allocation strategies by purchasing or selling futures contracts on U.S. and foreign securities indexes and other assets. A futures contract provides for the future sale by one party and purchase by another party of a specified quantity of the security or other financial instrument at a specified price and time. A futures contract on an index is an agreement in which two parties agree to take or make delivery of an amount of cash equal to the difference between the value of the index at the close of the last trading day of the contract and the price at which the index contract was originally written. The Fund may use futures contracts in an attempt to enhance the Fund’s investment returns, as an efficient way to gain broad market exposure with reduced transaction costs and/or to to hedge against market and other risks in the Fund’s portfolio. There are a number of risks associated with the use of futures contracts. A purchase or sale of a futures contract may result in losses in excess of the amount invested in the futures contract. If futures are used for hedging, there can be no guarantee that there will be a correlation between price movements in the hedging vehicle and in the Fund’s portfolio securities being hedged.

(d) Options

The Fund will opportunistically employ an option strategy in an attempt to generate gains from option premiums, enhance distributions payable to the Fund’s shareholders and reduce overall portfolio risk. The Fund intends to pursue its options strategy primarily by writing call options on equity indexes. As the writer (seller) of an equity index call option, the Fund would receive cash (the premium) from the purchaser of the option, and the purchaser would have the right to receive from the Fund any appreciation in the cash value of the index over the strike price upon exercise. If the purchaser exercises the index option sold by the Fund, the Fund would pay the purchaser the difference between the cash value of the index and the strike price. In effect, the Fund sells the potential appreciation in the value of the index above the strike price in exchange for the premium.

(e) Securities Sold Short

The Fund may sell securities short. A short sale is a transaction in which the Fund sells securities it does not own, but rather has borrowed, in anticipation of a decline in the market price of the securities. The Fund is obligated to replace the borrowed securities at their market price at the time of replacement. The Fund’s obligation to replace the securities borrowed in connection with a short sale will be fully secured by collateral held in a segregated account at the custodian.

18 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund | Notes to Financial Statements continued

Short sales by the Fund involve certain risks and special considerations. Possible losses from short sales differ from losses that could be incurred from a purchase of a security because losses from a short sale may be unlimited, whereas losses from purchases cannot exceed the total amount invested.

(f) Currency Translation

Assets and liabilities denominated in foreign currencies are translated into U.S. dollars at the mean of the bid and asked price of respective exchange rates on the last day of the period. Purchases and sales of investments denominated in foreign currencies are translated at the exchange rate on the date of the transaction.

Foreign exchange gain or loss resulting from holding of a foreign currency, expiration of a currency exchange contract, difference in exchange rates between the trade date and settlement date of an investment purchased or sold, and the difference between dividends actually received compared to the amount shown in the Fund’s accounting records on the date of receipt are shown as net realized gains or losses on foreign currency forwards and currency transactions in the Fund’s Statement of Operations.

Foreign exchange gain or loss on assets and liabilities, other than investments, are shown as unrealized appreciation (depreciation) on foreign currency translations.

(g) Forward Exchange Currency Contracts

The Fund may enter into forward exchange currency contracts in order to hedge its exposure to changes in foreign currency exchange rates on its foreign portfolio holdings, to hedge certain firm purchases and sales commitments denominated in foreign currencies and for investment purposes. A forward exchange currency contract is a commitment to purchase or sell a foreign currency on a future date at a negotiated forward rate. The gain or loss arising from the difference between the original contracts and the closing of such contracts are included in net realized gain or loss on foreign currency transactions.

Fluctuations in the value of open forward exchange currency contracts are recorded for financial reporting purposes as unrealized appreciation and depreciation by the Fund.

The Fund’s custodian will place and maintain cash not available for investment or other liquid assets in a separate account of the Fund having a value at least equal to the aggregate amount of the Fund’s commitments under forward exchange currency contracts entered into with respect to position hedges.

Risks may arise from the potential inability of a counterparty to meet the terms of a contract and from unanticipated movements in the value of a foreign currency relative to the U.S. dollar. The face or contract amount, in U.S. dollars, reflects the total exposure the Fund has in that particular currency contract.

(h) Distributions to Shareholders

The Fund declares and pays quarterly dividends to common shareholders. These dividends consist of investment company taxable income, which generally includes qualified dividend income, ordinary income, short-term capital gains and premiums received on certain written options. Realized short-term capital gains and premiums received on certain options are considered ordinary income for tax purposes and will be reclassified at the Fund’s fiscal year end on the Fund’s Statement of Assets and Liabilities from accumulated net realized gains to distributions in excess of net investment income. Any net realized long-term capital gains are distributed annually to common shareholders.

Distributions to shareholders are recorded on the ex-dividend date. The amount and timing of distributions are determined in accordance with federal income tax regulations, which may differ from U.S. generally accepted accounting principles.

Note 3 – Investment Advisory Agreement, Sub-Advisory Agreement and Other Agreements:

Pursuant to an Investment Advisory Agreement (the “Agreement”) between the Fund and Claymore Advisors, LLC (the “Adviser”), the Adviser will furnish offices, necessary facilities and equipment, provide administrative services, oversee the activities of Analytic Investors, Inc. (“Analytic” or the “Sub-Adviser”), provide personnel including certain officers required for its administrative management and pay the compensation of all officers and trustees of the Fund who are its affiliates. As compensation for these services, the Fund will pay the Adviser an annual fee, payable monthly, in an amount equal to 1.00% of the Fund’s average daily total net assets.

Pursuant to a Sub-Advisory Agreement (the “Sub-Advisory Agreement”) between the Fund, the Adviser and the Sub-Adviser, the Sub-Adviser under the supervision of the Fund’s Board of Trustees and the Adviser, provides a continuous investment program for the Fund’s portfolio; provides investment research, makes and executes recommendations for the purchase and sale of securities; and provides certain facilities and personnel, including certain officers required for its administrative management and pays the compensation of all officers and trustees of the Fund who are its affiliates. As compensation for its services, the Adviser pays the Sub-Adviser a fee, payable monthly, in an annual amount equal to 0.50% of the Fund’s average daily total net assets. Analytic is wholly owned by Old Mutual (US) Holdings, Inc.

The Bank of New York (“BNY”) acts as the Fund’s custodian, accounting agent, administrator and transfer agent. As custodian, BNY is responsible for the custody of the Fund’s assets. As accounting agent and administrator, BNY is responsible for maintaining the books and records of the Fund’s securities and cash. As transfer agent, BNY is responsible for performing transfer agency services for the Fund.

| Annual Report | December 31, 2005 | 19 |

OLA | Old Mutual/Claymore Long-Short Fund | Notes to Financial Statements continued

Certain officers and trustees of the Fund are also officers and directors of the Adviser or the Sub-Adviser. The Fund does not compensate its officers or trustees who are officers of the aforementioned firms.

Note 4 – Federal Income Taxes:

The Fund intends to comply with the requirements of Subchapter M of the Internal Revenue Code of 1986, as amended, applicable to regulated investment companies. Accordingly, no provision for U.S. federal income taxes is required. In addition, by distributing substantially all of its ordinary income and long-term capital gains, if any, during each calendar year, the Fund intends not to be subject to U.S. federal excise tax.

Due to inherent differences in the recognition of income, expenses, and realized gains/losses under U.S. generally accepted accounting principles and federal income tax purposes, permanent differences between book and tax basis reporting have been identified and appropriately reclassified on the Statement of Assets and Liabilities. A permanent book and tax difference relating to a distribution reclass in the amount of $6,148,635 was reclassified from net investment income to net realized gain. Also permanent book and tax differences relating to losses on foreign currency transactions in the amount of $2,228,216 were reclassified from net realized gain to net investment income.

Capital losses and foreign currency transactions incurred after October 31 (“post-October” losses) within the taxable year are deemed to arise on the first business day of the Fund’s next taxable year. The Fund incurred and will elect to defer net capital losses during 2005 in the amount of $4,829,695 and foreign currency related loss of $2,217,749.

Information on the tax components of investments, excluding short sales transactions and excluding written options as of December 31, 2005 is as follows:

Cost of Investments for Tax Purposes | Gross Tax Unrealized Appreciation | Gross Tax Unrealized Depreciation | Net Tax Unrealized Depreciation on Investments | Net Tax Unrealized Appreciation on Derivatives and Foreign Currency | ||||||||||

$429,620,443 | $ | 5,766,460 | $ | (12,325,491 | ) | $ | (6,559,031 | ) | $ | 502,950 | ||||

Information on the tax components of securities sold short as of December 31, 2005 is as follows:

Cost of Securities Sold Short for Tax Purposes | Gross Tax Unrealized Appreciation | Gross Tax Unrealized Depreciation | Net Tax Unrealized Depreciation on Securities Sold Short | ||||||||

$(66,419,335) | $ | 1,973,065 | $ | (2,997,021 | ) | $ | (1,023,956 | ) | |||

Tax components of the following balances as of December 31, 2005 are as follows:

Undistributed ordinary income | $ | 9,179,015 | ||

Accumulated capital and other losses | $ | (7,047,444 | ) |

For the period ended December 31, 2005, the tax character of distributions paid, as reflected in the Statement of Changes in Net Assets, was $4,935,421 of ordinary income and $2,666,675 of long-term capital gains.

Note 5 – Investment Transactions and Options Written:

For the period ended December 31, 2005, purchases and sales of investments, excluding written options and short-term securities, were $563,176,821 and $247,428,327, respectively.

The Fund entered into written option contracts during the period ended December 31, 2005. Details of the transactions were as follows:

| Number of Contracts | Premiums Received | ||||||

Options written, during the period | 21,603 | $ | 16,631,029 | ||||

Options expired, during the period | (2,500 | ) | (2,084,562 | ) | |||

Options closed, during the period | (15,050 | ) | (12,240,046 | ) | |||

Options assigned, during the period | — | — | |||||

Options outstanding, end of period | 4,053 | $ | 2,306,421 | ||||

Note 6 – Derivatives:

At December 31, 2005, the following futures contracts were outstanding:

Long Contracts | Number of Contracts | Unrealized Appreciation (Depreciation) | |||

Amsterdam Exchanges Index - January 2006 (Current notional value of 87,410 Euro per contract) | 157 | $ | 113,524 | ||

CAC 40 10 Year Euro Index - January 2006 (Current notional value of 47,185 Euro per contract) | 276 | 55,805 | |||

Canada 10 Year Bond - March 2006 (Current notional value of 114,380 Canadian dollars per contract) | 400 | 78,575 | |||

Dow Jones Euro STOXX 50 - March 2006 (Current notional value of 35,880 Euro per contract) | 59 | 42,511 | |||

FTSE 100 Index - March 2006 (Current notional value of 56,160 Pound Sterling per contract) | 159 | 208,953 | |||

IBEX 35 Index - January 2006 (Current notional value of 106,970 Euro per contract) | 112 | 235,958 | |||

Japan 10 Year Bond (TSE) - March 2006 (Current notional value of 137,350,000 Japanese Yen per contract) | 25 | 140,123 | |||

OMXS 30 Index - January 2006 (Current notional value of 96,200 Swedish Krona per contract) | 108 | 28,866 | |||

RUIX Index - Euro Bond - March 2006 (Current notional value of 121,840 Euro per contract) | 180 | 218,322 | |||

TOPIX Index - March 2006 (Current notional value of 16,435,000 Japanese Yen per contract) | 98 | 435,179 | |||

| 1,574 | $ | 1,557,816 | |||

20 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund | Notes to Financial Statements continued

Short Contracts | Number of Contracts | Unrealized Appreciation | ||||

Australia 10 Year Bond - March 2006 (Current notional value of 106,097 Australian dollars per contract) | 115 | $ | (164,678 | ) | ||

DAX Index - March 2006 (Current notional value of 135,950 Euro per contract) | 96 | (330,496 | ) | |||

Hang Seng Stock Index - January 2006 (Current notional value of 741,900 Hong Kong dollar per contract) 105 | 314,820 | |||||

Long Gilt - March 2006 (Current notional value of 114,450 Pound Sterling per contract) | 215 | (401,059 | ) | |||

S&P 500 E-Mini - March 2006 (Current notional value of $62,740 per contract) | 150 | 141,750 | ||||

S&P/MIB Index - March 2006 (Current notional value of 179,100 Euro per contract) | 22 | (106,166 | ) | |||

S&P/TSE 60 Index - March 2006 (Current notional value of 127,420 Canadian dollars per contract) | 76 | (64,556 | ) | |||

SPI 200 Index - March 2006 (Current notional value of 118,175 Australian dollars per contract) | 167 | (441,125 | ) | |||

U.S. 10 Year Treasury Notes - March 2006 (Current notional value of $109,406 per contract) | 459 | (372,688 | ) | |||

| 1,405 | (1,424,198 | ) | ||||

| 2,979 | $ | 133,618 | ||||

All notional values are denominated in local currencies.

At December 31, 2005, the following forward exchange currency contracts were outstanding:

Long Contracts | Local Currency Value | Unrealized Appreciation (Depreciation) | ||||

Australian Dollar, 40,000,000 expiring 3/15/06 | 29,280,138 | $ | (375,983 | ) | ||

New Zealand Dollar, 13,000,000 expiring 3/15/06 | 8,801,436 | (91,084 | ) | |||

Norwegian Krone, 200,000,000 expiring 3/15/06 | 29,651,922 | (572,001 | ) | |||

Swedish Krona, 240,000,000 expiring 3/15/06 | 30,258,592 | 65,382 | ||||

| $ | (973,686 | ) | ||||

Short Contracts | ||||||

Canadian Dollar, 33,000,000 expiring 3/15/06 | 28,306,990 | 264,009 | ||||

Euro, 26,000,000 expiring 3/15/06 | 30,787,931 | 572,319 | ||||

Japanese Yen, 2,700,000,000 expiring 3/15/06 | 23,074,073 | 364,567 | ||||

Pound Sterling, 6,000,000 expiring 3/15/06 | 10,299,734 | 132,106 | ||||

Swiss Franc, 39,000,000 expiring 3/15/06 | 29,794,547 | 299,036 | ||||

| 1,632,037 | ||||||

| $ | 658,351 | |||||

Note 7 – Capital:

Common Shares

In connection with its organization process, the Fund sold 5,240 shares of beneficial interest to Claymore Securities, Inc., an affiliate of the Adviser, for consideration of $100,084 at a price of $19.10 per share. The Fund has an unlimited amount of common shares, $0.01 par value, authorized and 19,005,240 issued and outstanding. Of this amount, the Fund issued 18,000,000 shares of common stock in its initial public offering and issued pursuant to an over allotment option to the underwriters, an additional 1,000,000 shares on September 13, 2005. These shares were issued at $19.10 per share after deducting the sales load but before underwriters’ expense reimbursement. In addition, the Fund’s Adviser and Sub-Adviser have agreed to pay all of the Fund’s organizational costs, estimated at $25,000.

Offering costs, estimated at $760,000 or $0.04 per share, in connection with the issuance of common shares have been borne by the Fund and were charged to paid-in capital. The Adviser and Sub-Adviser have agreed to pay offering expenses (other than sales load, but including reimbursement of expenses to the underwriters) in excess of $0.04 per common share.

Note 8 – Indemnifications:

In the normal course of business, the Fund enters into contracts that contain a variety of representations, which provide general indemnifications. The Fund’s maximum exposure under these arrangements is unknown, as this would require future claims that may be made against the Fund that have not yet occurred. However, the Fund expects the risk of loss to be remote.

Note 9 – Subsequent event:

In November 2005, the Board of Trustees approved Claymore Advisors, LLC to replace BNY as the Fund Administration Agent, effective March 1, 2006.

| Annual Report | December 31, 2005 | 21 |

OLA | Old Mutual/Claymore Long-Short Fund

Report of Independent Registered Public Accounting Firm |

To the Shareholders and Board of Trustees of Old Mutual/Claymore Long-Short Fund

We have audited the accompanying statement of assets and liabilities of Old Mutual/Claymore Long-Short Fund (the “Fund”), including the portfolio of investments, as of December 31, 2005, and the related statement of operations, statement of changes in net assets, and financial highlights for the period from August 25, 2005 (commencement of investment operations) through December 31, 2005. These financial statements and financial highlights are the responsibility of the Fund’s management. Our responsibility is to express an opinion on these financial statements and financial highlights based on our audit.

We conducted our audit in accordance with the standards of the Public Company Accounting Oversight Board (United States). Those standards require that we plan and perform the audit to obtain reasonable assurance about whether the financial statements and financial highlights are free of material misstatement. We were not engaged to perform an audit of the Fund’s internal control over financial reporting. Our audit included consideration of internal control over financial reporting as a basis for designing audit procedures that are appropriate in the circumstances, but not for the purpose of expressing an opinion on the effectiveness of the Fund’s internal control over financial reporting. Accordingly, we express no such opinion. An audit also includes examining, on a test basis, evidence supporting the amounts and disclosures in the financial statements and financial highlights, assessing the accounting principles used and significant estimates made by management, and evaluating the overall financial statement presentation. Our procedures included confirmation of securities owned as of December 31, 2005, by correspondence with the custodian and brokers or by other appropriate auditing procedures where replies from brokers were not received. We believe that our audit provides a reasonable basis for our opinion.

In our opinion, the financial statements and financial highlights referred to above present fairly, in all material respects, the financial position of Old Mutual/Claymore Long-Short Fund at December 31, 2005, and the results of its operations, changes in its net assets and its financial highlights for the period from August 25, 2005 (commencement of investment operations) through December 31, 2005, in conformity with U.S. generally accepted accounting principles.

Chicago, Illinois

February 17, 2006

22 | Annual Report | December 31, 2005 |

OLA | Old Mutual/Claymore Long-Short Fund

Supplemental Information | (unaudited)

Federal Income Tax Information

Qualified dividend income of as much as $1,908,590 was taxable to the Fund through December 31, 2005. The Fund intends to designate the maximum amount of dividends that qualify for the reduced tax rate pursuant to the Jobs and Growth Tax Relief Reconciliation Act of 2003.

For corporate shareholders, $1,902,795 of investment income (dividend income plus short-term gains, if any) qualifies for the dividends-received deduction.

In January 2006, you were advised on IRS Form 1099 DIV or substitute 1099 DIV as to the federal tax status of the distributions received by you in the calendar year 2005.

Trustees

The Trustees of the Old Mutual/Claymore Long-Short Fund and their principal occupations during the past five years:

Name, Address*, Age and Position(s) held with Registrant | Term of Office** and Length of Time Served | Principal Occupation During the Past Five Years and Other Affiliations | Number of Portfolios in the | Other Directorships Held by Trustee | ||||

| Independent Trustees: | ||||||||

Randall C. Barnes Year of Birth: 1951 Trustee | Since 2005 | Formerly, Senior Vice President & Treasurer (1993-1997), President, Pizza Hut International (1991-1993) and Senior Vice President, Strategic Planning and New Business Development (1987-1990) of PepsiCo, Inc. (1987-1997). | 12 | None. | ||||

Steven D. Cosler Year of Birth: 1955 Trustee | Since 2005 | Formerly, President, Chief Executive Officer and Director of Priority Healthcare Corp. (2002-2005). Formerly, President and Chief Operating Officer of Priority Healthcare Corp. (2001-2002). Formerly, Executive Vice President and Chief Operating Officer of Priority Healthcare Corp. (2000-2001). | 2 | None. | ||||

Robert M. Hamje Year of Birth: 1942 Trustee | Since 2005 | Advisor to the Cleveland Foundation Investment Committee. Formerly, President and Chief Investment Officer of TRW Investment Management Co. (1990-2003). | 2 | Trustee, Old Mutual Advisor Mutual Funds. | ||||

L. Kent Moore Year of Birth: 1955 Trustee | Since 2005 | Partner at WilSource Enterprise (October 2005-present). Previously, Managing Director High Sierra Energy L.P., (2004-2005). Formerly, Portfolio Manager and Vice President of Janus Capital Corp. (2000-2002) and Senior Analyst/Portfolio Manager of Marsico Capital Management (1997-1999). | 2 | Trustee, Old Mutual Advisor Mutual Funds. | ||||

Ronald A. Nyberg Year of Birth: 1953 Trustee | Since 2005 | Principal of Ronald A. Nyberg, Ltd., a law firm specializing in corporate law, estate planning and business transactions (2000-present). Formerly, Executive Vice President, General Counsel and Corporate Secretary of Van Kampen Investments (1982-1999). | 16 | Director, Edward Hospital Foundation, Naperville, IL; Trustee, North Park University, Chicago. | ||||