Table of Contents

As filed with the Securities and Exchange Commission on January 11, 2005

Registration No. 333-

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

FreightCar America, Inc.

(Exact name of Registrant as specified in its charter)

| Delaware | 3743 | 25-1837219 | ||

(State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. employer identification number) |

Two North Riverside Plaza

Suite 1250

Chicago, Illinois 60606

(800) 458-2235

(Address, including zip code, and telephone number, including area code, of registrant’s principal executive offices)

John E. Carroll, Jr.

President and Chief Executive Officer

FreightCar America, Inc.

Two North Riverside Plaza

Suite 1250

Chicago, Illinois 60606

(800) 458-2235

(Name, address, including zip code, and telephone number, including area code, of agent for service)

Copies To:

Robert F. Wall, Esq. David A. Sakowitz, Esq. Winston & Strawn LLP 35 W. Wacker Drive Chicago, Illinois 60601-9703 (312) 558-5600 | Stephen T. Giove, Esq. Lisa L. Jacobs, Esq. Shearman & Sterling LLP 599 Lexington Avenue New York, New York 10022-6069 (212) 848-4000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after the effectiveness of this registration statement.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, please check the following box. ¨

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, please check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. ¨

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. ¨

CALCULATION OF REGISTRATION FEE

| Title of each class of securities to be registered | Proposed maximum aggregate offering | Amount of registration fee | ||

Common Stock, par value $0.01 per share | $115,000,000 | $13,536 |

| (a) | Includes shares of Common Stock which may be purchased by the underwriters from selling stockholders to cover over-allotments, if any. |

| (b) | Estimated solely for the purpose of calculating the registration fee in accordance with Rule 457(o) promulgated under the Securities Act. |

The registrant hereby amends this registration statement on such date or dates as may be necessary to delay its effective date until the registrant shall file a further amendment which specifically states that this registration statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act, or until the registration statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Table of Contents

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and we are not soliciting offers to buy these securities in any jurisdiction where the offer or sale is not permitted.

| PRELIMINARY PROSPECTUS | Subject to Completion | , 2005 |

Shares

FreightCar America, Inc.

Common Stock

This is our initial public offering of our common stock. No public market currently exists for our common stock. We are offering shares of common stock by this prospectus. We expect the public offering price to be between $ and $ per share.

We expect to apply to have our common stock approved for quotation on the Nasdaq National Market under the trading symbol “RAIL.”

Investing in our common stock involves a high degree of risk. Before buying any shares, you should carefully read the discussion of material risks of investing in our common stock in “Risk factors” beginning on page 12 of this prospectus.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or determined if this prospectus is truthful or complete. Any representation to the contrary is a criminal offense.

| Per Share | Total | |||

| Public offering price | $ | $ | ||

| Underwriting discounts and commissions | $ | $ | ||

| Proceeds, before expenses, to us | $ | $ |

The underwriters may also purchase from the selling stockholders up to an additional shares of our common stock at the public offering price, less the underwriting discounts and commissions payable by us, to cover over-allotments, if any, within 30 days from the date of this prospectus. We will not receive any proceeds from the sale of shares by the selling stockholders.

The underwriters are offering the common stock as set forth under “Underwriting.” Delivery of the shares will be made on or about , 2005.

Sole Book-Running Manager

UBS Investment Bank

Co-Lead Manager

Jefferies & Company, Inc. CIBC World Markets |

The date of this prospectus is , 2005.

Table of Contents

Table of Contents

You should rely only on the information contained in this prospectus. We have not, and the underwriters have not, authorized anyone to provide you with additional information or information different from that contained in this prospectus. We are offering to sell, and seeking offers to buy, shares of our common stock only in jurisdictions where offers and sales are permitted. The information contained in this prospectus is accurate only as of the date of this prospectus, regardless of the time of delivery of this prospectus or of any sale of shares of our common stock.

| 1 | ||

| 12 | ||

| 28 | ||

| 29 | ||

| 31 | ||

| 32 | ||

| 34 | ||

| 36 | ||

Management’s discussion and analysis of financial condition and results of operations | 39 | |

| 62 | ||

| 67 |

| 85 | ||

| 99 | ||

| 103 | ||

| 106 | ||

| 110 | ||

| 116 | ||

Material U.S. income tax considerations for non-U.S. holders | 118 | |

| 121 | ||

| 125 | ||

| 125 | ||

| 125 | ||

| F-1 |

In this prospectus, references to “our company,” “we,” “us” and “our” refer to FreightCar America, Inc. and its consolidated subsidiaries and its predecessors, except where the context otherwise indicates.

The prospectus contains some of our trademarks, trade names and service marks. Each trademark, trade name or service mark of any other company appearing in this prospectus belongs to its respective holder.

The market and industry data and forecasts included in this prospectus are based upon independent industry sources, including the Association of American Railroads, the Railway Supply Institute, Economic Planning Associates, Inc., the Energy Information Administration of the U.S. Department of Energy and Resource Data International. Although we believe that these independent sources are reliable, we have not independently verified the accuracy and completeness of this information, nor have we independently verified the underlying economic assumptions relied upon in preparing any forecasts. See “Risk factors—Risks related to our business—The market and industry data included in this prospectus cannot be verified with certainty and may prove to be inaccurate.” In addition, we recognize sales of our railcars, which we sometimes refer to as deliveries of our railcars, when we have completed production, the railcars are accepted by the customer following inspection, the risk for any damage or other loss with respect to the railcars passes to the customer and title to the railcars transfers to the customer. Information related to our railcar deliveries is based on our recognized sales. Sales recognition policies of other manufacturers may not necessarily be the same as our policy. Therefore, industry information related to railcar deliveries by all manufacturers, which includes railcars we have delivered, may be based on different sales recognition policies than we use. Furthermore, the industry-wide railcar delivery information included in this prospectus is based, in part, on railcar delivery information that we provided to independent industry sources that recognized deliveries in a given period before title to the railcar transferred to the customer. Therefore, industry-wide railcar delivery information may not be directly comparable to our actual railcar delivery information.

Table of Contents

This summary highlights information contained elsewhere in this prospectus. It is not complete and may not contain all the information that may be important to you. You should read the entire prospectus carefully before making an investment decision, especially the information presented under the heading “Risk factors” and our consolidated financial statements and the related notes included elsewhere in this prospectus.

OUR COMPANY

We are one of the leading designers and manufacturers of aluminum-bodied and steel-bodied railroad freight cars, which we also refer to as railcars, in North America. We specialize in the production of coal-carrying railcars, which represented 76% of our deliveries of railcars in 2003, while the balance of our production consisted of a broad spectrum of railcar types. We also refurbish and rebuild railcars and sell forged, cast and fabricated parts for all of the railcars that we produce, as well as those manufactured by others. We have chosen not to offer significant railcar leasing services, as we have made a strategic decision not to compete with our leasing customers, which represent a significant portion of our revenue.

We believe that we are the leading North American manufacturer of coal-carrying railcars. We estimate that we have produced 87% of the coal-carrying railcars delivered over the last three years in the North American market. Our aluminum BethGon railcar has been the leading aluminum-bodied coal-carrying railcar sold in North America for nearly 20 years. We believe that over the last 25 years we have built and introduced more types of coal-carrying railcars than all other manufacturers in North America combined.

Our main manufacturing facilities are located in Danville, Illinois and Johnstown, Pennsylvania. Our Danville facility produced approximately 81% of our railcars manufactured during the nine months ended September 30, 2004, and all of our aluminum-bodied coal-carrying railcars. We believe that our Danville facility has become the industry leader in operational efficiency in the manufacture of coal-carrying railcars, which has enabled us to reduce our manufacturing costs and increase our capacity significantly. Our Johnstown facility manufactures all of our other railcar types, such as small covered hopper railcars, coiled steel railcars and aluminum vehicle carrier railcars, and it also has the capability to manufacture coal-carrying railcars.

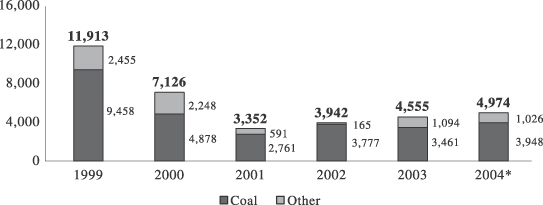

Our primary customers are leasing companies, utilities, railroads and industrial companies, which represented 47%, 34%, 16% and 3%, respectively, of our total net sales attributable to each type of customer for the nine months ended September 30, 2004. In 2003, we delivered 4,555 new railcars, including 3,461 aluminum-bodied coal-carrying railcars. Our total backlog of firm orders for new railcars increased from 4,438 railcars as of September 30, 2003 to 11,491 railcars as of September 30, 2004, representing estimated net sales of $248.8 million and $750.3 million, respectively, attributable to such backlog.

We and our predecessors have been manufacturing railcars since 1901. From 1923 to 1991, our business was owned and operated by Bethlehem Steel Corporation. In 1991, Transportation Technologies Industries, Inc., or TTII (then known as Johnstown America Industries, Inc.), purchased our business from Bethlehem Steel. In June 1999, TTII sold our railcar business to an investor group led by certain members of TTII’s management who became our management. In December 2004, we changed our name from JAC Holdings International, Inc. to FreightCar America, Inc. to better reflect our business of manufacturing railcars.

1

Table of Contents

OUR INDUSTRY

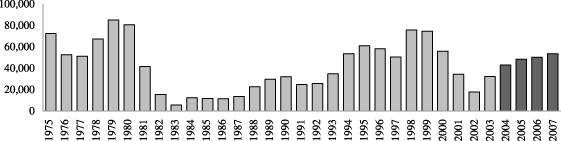

The North American railcar market is the primary market in which we compete. The North American railcar manufacturing industry has been consolidating over the last 20 years with the number of manufacturers falling from 24 companies in 1980 to six companies today. Of these six companies, four manufacture railcars primarily for third-party customers, while the other two manufacture railcars primarily for their own railcar leasing operations. According to the Association of American Railroads, there were approximately 1.3 million railcars in circulation in 2003, and the number of railcars delivered in the North American market increased from 17,736 railcars in 2002 to 32,183 railcars in 2003. According to Economic Planning Associates, the compound annual growth rate for railcar deliveries over the next four years is expected to be approximately 14.2%, resulting in an estimated 53,550 railcar deliveries per year by 2007.

Rail transport is important to the North American economy. In 2001, railroads transported approximately 42% of the freight hauled in the United States, an increase from approximately 38% in 1990. A number of industries in North America rely heavily on rail for the transport of the various inputs and outputs associated with their operations.

We believe the main characteristics and trends affecting the railcar industry are:

| Ø | the cyclical nature of the railcar market; |

| Ø | the replacement demand for the aging North American railcar fleet; |

| Ø | the shift from steel-bodied to aluminum-bodied railcars; |

| Ø | the shift in the customer base from railroads to leasing companies, utilities and industrial companies; and |

| Ø | the consolidation of railcar manufacturers. |

We believe the main trends affecting the coal-carrying railcar business are:

| Ø | the increase in demand for electricity; |

| Ø | the increase in demand for coal as a fuel source; and |

| Ø | the increase in demand for coal from the western United States. |

These trends affecting the railcar industry and the coal-carrying railcar business are summarized in the section entitled “Industry.”

OUR BUSINESS STRENGTHS AND COMPETITIVE ADVANTAGES

We believe that the following key business strengths and competitive advantages will contribute to our growth:

| Ø | Leader in coal-carrying railcar market. We believe we are the leading manufacturer of coal-carrying railcars in North America, producing an estimated 87% of the coal-carrying railcars delivered in the North American market over the last three years. Through our leading position in the coal-carrying railcar market, we expect to benefit from the increasing use of coal as an energy source. |

2

Table of Contents

| Ø | Leading manufacturer of aluminum-bodied railcars. Since pioneering the modern aluminum-bodied coal-carrying railcar design in 1986, we believe that we have introduced more aluminum-bodied railcar types and have manufactured more aluminum-bodied railcars than any other company. We plan to leverage our expertise in aluminum-bodied coal-carrying railcar production as railroads and utilities continue to upgrade their fleets from aging steel-bodied coal-carrying railcars to lighter and more durable aluminum-bodied railcars. |

| Ø | Strong relationships with long-term customer base. We have established long-term relationships with a customer base that includes some of the largest utilities, railroads, leasing companies and industrial companies in North America. We believe that our ability to meet our customers’ preference for reliable, high-quality products, the relatively high cost for customers to switch manufacturers, our technological leadership in developing innovative products and the competitive pricing of our railcars have helped us maintain our long-standing relationships with our customers. |

| Ø | Low-cost structure. We believe that our Danville railcar production facility can produce railcars at a lower cost than our competitors’ facilities. Over the past several years, we have reduced our fixed costs and have increased our production efficiency through a series of operational changes and the introduction of proprietary production systems. We also have contractual arrangements with certain of our suppliers and customers that help limit our exposure to fluctuations in material prices. As a result of our low-cost structure, we were able to generate positive cash flow from operations during the most recent cyclical downturn in the railcar industry despite the decline in our sales. |

| Ø | Innovative product development. We continuously seek to create new railcar designs and develop improvements to our existing designs. We have added nine new or redesigned products to our portfolio in the last five years, and railcar designs introduced in the last three years represented 94% of the railcars that we produced in fiscal year 2003. |

| Ø | Stable labor relations. We have a collective bargaining agreement with the union representing the employees at our Danville facility, which expires on November 1, 2008. In November 2004, we entered into a settlement agreement with the union representing our existing and former unionized employees at our Johnstown facility setting forth the terms of a new collective bargaining agreement, which expires on May 15, 2008. We expect the settlement to allow our Johnstown facility to become more cost-competitive. The settlement, among other things, limits our future contributions for health care coverage and pension costs for retired unionized employees at our Johnstown facility. The settlement is conditioned on, among other things, approval by the National Labor Relations Board (NLRB) and the United States District Court for the Western District of Pennsylvania of the settlement and the withdrawal of the NLRB charges, the class-action lawsuits and certain workplace grievance matters against us related to the Johnstown facility. See “—Recent Developments” below. |

| Ø | Strong and experienced management team. We have an experienced senior management team that has an average of over 28 years of experience in the railcar or other manufacturing industries. We believe that our management team has successfully managed our business during the most recent cyclical downturn in the railcar industry, and the continued contributions of our management team will be important for our future success. |

OUR STRATEGY

The key elements of our business strategy are as follows:

| Ø | Maintain leadership in the coal-carrying railcar segment. Since we introduced our aluminum-bodied coal-carrying railcar design in 1986, we have been the leading manufacturer of coal-carrying railcars in North America with an estimated 87% share of the coal-carrying railcars delivered over the last three years in the North American market. We intend to continue to develop new and innovative railcar designs that respond to the needs of our customers, thereby capitalizing on the forecasted growth in coal usage in the United States. |

3

Table of Contents

| Ø | Leverage aluminum expertise into new applications and railcar types. We are applying our expertise in aluminum-bodied coal-carrying railcar production to develop new types of railcars and related applications. For example, our aluminum vehicle carrier is a competitively priced alternative to a steel vehicle carrier for the efficient transport of new passenger vehicles. |

| Ø | Continue to improve operating efficiencies. We intend to build on the success of our cost improvement initiatives at our Danville facility, and we will continue to identify opportunities to enhance operating efficiencies across our manufacturing facilities, thereby allowing us to reduce our costs and maintain competitive prices. |

| Ø | Continue to expand our product portfolio. We intend to continue to introduce new and improved railcar designs that respond to the needs of our customers. In addition to developing new aluminum-bodied railcar types, we may seek to expand our product portfolio to selected steel-bodied railcars. |

| Ø | Continue to pursue incremental internal growth and additional external opportunities. By significantly reducing our debt through this offering, we will have the financial flexibility to supplement internal growth with select acquisitions. We also intend to expand into underserved international markets through licensing arrangements or through joint ventures with established railcar manufacturers. In response to the current demand for our railcars, we are exploring opportunities to increase our production capacity, including by adding another manufacturing facility. |

THE TRANSACTIONS

We intend to use the proceeds of this offering, borrowings under a proposed $ million revolving credit facility, which we expect to enter into upon completion of this offering and which we refer to as the new revolving credit facility, and available cash to repay substantially all of our long-term debt, to redeem all of our outstanding redeemable preferred stock, to pay the additional consideration related to the acquisition of our business in 1999 that will become due upon the completion of this offering pursuant to certain rights under the acquisition agreement, which we refer to as the rights to additional acquisition consideration, and to pay fees and expenses related to this offering and the related transactions. For more information, see “Use of proceeds.”

We refer to this offering, the entering into of the new revolving credit facility and the application of the net proceeds of this offering, borrowings under the new revolving credit facility and available cash in the manner described in “Use of proceeds” as the Transactions.

RECENT DEVELOPMENTS

Johnstown settlement. On November 15, 2004, our subsidiary, Johnstown America Corporation, or JAC, entered into a settlement agreement with The United Steelworkers of America, or the USWA, which represents our unionized employees in our Johnstown, Pennsylvania manufacturing facility. Our unionized employees at our Johnstown facility, who comprise approximately 46% of our total workforce, had been without a collective bargaining agreement since October 2001. The settlement agreement sets forth the terms of a new 42-month collective bargaining agreement with our unionized employees at our Johnstown facility. The settlement agreement also provides for the resolution of charges made by the USWA against us with the NLRB, certain related class-action lawsuits, which we refer to as the Deemer and Britt lawsuits, and certain workplace grievance matters. Under the terms of the settlement agreement, the plaintiffs in the Deemer and Britt lawsuits are to withdraw their lawsuits with prejudice and the USWA agreed to request that the NLRB prosecutor withdraw the NLRB charges against us. In addition, the settlement agreement limits our future contributions for health care coverage and pension costs for retired unionized employees at our Johnstown facility. The settlement is conditioned on, among other things, approval by the NLRB and the United States District Court for the Western District of Pennsylvania of the settlement, the withdrawal of the NLRB charges, the Deemer and

4

Table of Contents

Britt lawsuits and the workplace grievance matters. We refer to the settlement agreement and the related matters discussed above as the Johnstown settlement. See “Business—Legal proceedings—Labor dispute settlement.”

New executive officer. In November 2004, Kevin P. Bagby joined us as our Vice President, Finance, Chief Financial Officer, Treasurer and Secretary. Mr. Bagby served most recently as Vice President and Chief Financial Officer of Stoneridge, Inc., a company that designs and manufactures highly engineered electrical and electronic components, modules and systems for certain agricultural and vehicle markets.

CORPORATE INFORMATION

We are incorporated in Delaware, and the address of our principal executive offices is Two North Riverside Plaza, Suite 1250, Chicago, Illinois 60606. Our telephone number is (800) 458-2235. Our web site address is www.freightcaramerica.com. Information contained in or connected to our web site is not a part of this prospectus.

5

Table of Contents

The offering

Unless otherwise indicated, all of the information in this prospectus assumes the underwriters do not exercise their over-allotment option. Please see “Description of capital stock” for a summary of the terms of our common stock.

Common stock offered by us | shares |

Common stock subject to the over-allotment option granted by the selling stockholders | shares |

Common stock outstanding after this offering | shares |

Use of proceeds | We expect to receive net proceeds from the offering of approximately $ million, after deducting underwriting discounts and commissions and estimated expenses of this offering payable by us. |

We intend to use all of the proceeds of this offering, borrowings under the new revolving credit facility and available cash to repay substantially all of our outstanding indebtedness, to redeem all of our outstanding redeemable preferred stock, to pay amounts that will become due under the rights to additional acquisition consideration and to pay related fees and expenses. See “Use of proceeds.” |

We will receive no proceeds from the sale of common stock by the selling stockholders. |

Dividend policy | Following this offering, we intend to pay regular cash dividends on our common stock. |

Future dividends will be subject to certain considerations discussed under “Risk factors—Risks related to the purchase of our common stock in this offering—We intend to pay regular cash dividends on our common stock but may change our dividend policy, and the agreements governing our new revolving credit facility will likely contain various covenants that limit our ability to pay dividends” and “Dividend policy.” |

Proposed Nasdaq symbol | RAIL |

Risk factors | You should carefully read and consider the information set forth under the caption “Risk factors” and all other information set forth in this prospectus before investing in our common stock. |

6

Table of Contents

Unless otherwise indicated, all of the information in this prospectus relating to the number of shares of common stock to be outstanding after this offering:

| Ø | gives effect to the reclassification of our existing Class A voting common stock and our Class B non-voting common stock into a single class of our common stock on a one-for-one basis immediately prior to the completion of this offering, which we refer to as the reclassification; |

| Ø | gives effect to a -for-one stock split of all outstanding shares of our common stock following the reclassification, which we refer to as the stock split, effective immediately before the completion of this offering; and |

| Ø | excludes shares of our common stock issuable upon the exercise of stock options currently outstanding following the reclassification and the stock split, referred to in this prospectus as the 2004 Options, and shares of our common stock that will be available for future issuance under our 2005 Long-Term Incentive Plan, of which will be exercisable upon the completion of this offering with a weighted average exercise price of $ per share. |

7

Table of Contents

Summary consolidated financial data

The following table sets forth our summary consolidated financial data. The consolidated statements of operations and cash flow data for the years ended December 31, 2001, 2002 and 2003 and the consolidated balance sheet data as of December 31, 2002 and 2003 are derived from our audited consolidated financial statements and related notes included elsewhere in this prospectus. The consolidated statements of operations and cash flow data for the period from June 4, 1999 through December 31, 1999 and the year ended December 31, 2000 and the consolidated balance sheet data as of December 31, 1999, 2000 and 2001 are derived from our audited consolidated financial statements not included in this prospectus. The summary consolidated financial data for the period from January 1, 1999 through June 3, 1999 presented below includes financial data of our predecessor, consisting of certain direct and indirect wholly owned subsidiaries of TTII. On June 4, 1999, we were acquired from TTII by an investor group led by certain members of management of TTII who became our management. The financial data of our predecessor does not reflect any adjustments associated with our acquisition from TTII in 1999, and our consolidated financial data after our acquisition in 1999 is not directly comparable to our predecessor’s financial data.

The consolidated statements of operations and cash flow data for the nine months ended September 30, 2003 and 2004 and the consolidated balance sheet data as of September 30, 2004 are derived from our unaudited consolidated interim financial statements included in this prospectus. The consolidated balance sheet data as of September 30, 2003 is derived from our unaudited consolidated interim financial statements that are not included in this prospectus. The unaudited consolidated financial statements as of and for the nine months ended September 30, 2003 and 2004 reflect all adjustments which are, in the opinion of our management, necessary for a fair presentation of our financial position, results of operations and cash flows as of and for the periods presented.

The summary consolidated financial data set forth below for the twelve months ended September 30, 2004 has been derived from our unaudited consolidated financial statements and should be read together with our consolidated financial statements and the accompanying notes, included elsewhere in this prospectus.

The results included below and elsewhere in this document are not necessarily indicative of our future performance and our results for the nine months ended September 30, 2004 are not necessarily indicative of our results of operations for the full year. You should read this information together with “Capitalization,” “Management’s discussion and analysis of financial condition and results of operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus.

8

Table of Contents

Summary Consolidated Financial Data

| Predecessor | FreightCar America, Inc. | |||||||||||||||||||||||||||||||||||

Period from | Period from 1999 | Year ended December 31, | Nine months ended September 30, | Twelve 2004 | ||||||||||||||||||||||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2003 | 2004 | |||||||||||||||||||||||||||||||

| (in thousands, except share and per share data and railcar amounts) | ||||||||||||||||||||||||||||||||||||

Statements of operations data: | ||||||||||||||||||||||||||||||||||||

Net sales | $ | 316,931 | $ | 367,742 | $ | 397,577 | $ | 210,314 | $ | 225,497 | $ | 244,349 | $ | 165,955 | $ | 302,443 | $ | 380,837 | ||||||||||||||||||

Cost of sales | 271,714 | 325,640 | 358,267 | 187,646 | 212,589 | 225,216 | 153,171 | 294,883 | 366,928 | |||||||||||||||||||||||||||

Gross profit | 45,217 | 42,102 | 39,310 | 22,668 | 12,908 | 19,133 | 12,784 | 7,560 | 13,909 | |||||||||||||||||||||||||||

Selling, general and administrative expense | 8,215 | 11,397 | 18,580 | 13,370 | 12,778 | 14,318 | 9,029 | 10,700 | 15,989 | |||||||||||||||||||||||||||

Provision for settlement of labor disputes(1) | — | — | — | — | — | — | — | 9,159 | 9,159 | |||||||||||||||||||||||||||

Goodwill amortization expense | — | 1,074 | 1,812 | 1,744 | — | — | — | — | — | |||||||||||||||||||||||||||

Operating income (loss) | 37,002 | 29,631 | 18,918 | 7,554 | 130 | 4,815 | 3,755 | (12,299 | ) | (11,239 | ) | |||||||||||||||||||||||||

Interest income | (663 | ) | (354 | ) | (1,391 | ) | (887 | ) | (162 | ) | (128 | ) | (94 | ) | (87 | ) | (121 | ) | ||||||||||||||||||

Related-party interest expense | — | 2,535 | 5,165 | 5,723 | 6,517 | 6,764 | 5,485 | 5,184 | 6,463 | |||||||||||||||||||||||||||

Third-party interest expense | 451 | 3,623 | 3,999 | 2,398 | 1,595 | 1,367 | 788 | 819 | 1,398 | |||||||||||||||||||||||||||

Interest expense on rights to additional acquisition consideration | — | 1,192 | 2,341 | 2,927 | 3,659 | 4,573 | 3,326 | 4,157 | 5,404 | |||||||||||||||||||||||||||

Write-off of deferred financing costs | — | — | — | — | — | 348 | 348 | — | — | |||||||||||||||||||||||||||

Loss on disposal of railcar lease fleet | — | 689 | 187 | — | — | — | — | — | — | |||||||||||||||||||||||||||

Amortization of deferred financing costs | — | 410 | 702 | 702 | 702 | 629 | 528 | 364 | 465 | |||||||||||||||||||||||||||

Income (loss) before income taxes | 37,214 | 21,536 | 7,915 | (3,309 | ) | (12,181 | ) | (8,738 | ) | (6,626 | ) | (22,736 | ) | (24,848 | ) | |||||||||||||||||||||

Income tax provision (benefit) | 14,398 | 9,236 | 6,089 | 167 | (3,554 | ) | (1,318 | ) | (710 | ) | (7,250 | ) | (7,858 | ) | ||||||||||||||||||||||

Net income (loss) | 22,816 | 12,300 | 1,826 | (3,476 | ) | (8,627 | ) | (7,420 | ) | (5,916 | ) | (15,486 | ) | (16,990 | ) | |||||||||||||||||||||

Redeemable preferred stock dividends accumulated, but undeclared | — | 620 | 1,062 | 1,063 | 1,062 | 1,063 | 797 | 797 | 1,063 | |||||||||||||||||||||||||||

Net income (loss) attributable to common shareholders | $ | 22,816 | $ | 11,680 | $ | 764 | $ | (4,539 | ) | $ | (9,689 | ) | $ | (8,483 | ) | $ | (6,713 | ) | $ | (16,283 | ) | $ | (18,053 | ) | ||||||||||||

Weighted average common shares outstanding | 12,500 | 12,500 | 12,500 | 12,500 | 12,500 | 12,500 | 12,500 | 12,500 | ||||||||||||||||||||||||||||

Per share data: | ||||||||||||||||||||||||||||||||||||

Net income (loss) per share attributable to common shareholders (basic and diluted) | $ | 934.40 | $ | 61.12 | $ | (363.12 | ) | $ | (775.12 | ) | $ | (678.64 | ) | $ | (537.04 | ) | $ | (1,302.64 | ) | $ | (1,444.24 | ) | ||||||||||||||

9

Table of Contents

| Predecessor | FreightCar America, Inc. | |||||||||||||||||||||||||||||||

Period from | Period from 1999 | Year ended December 31, | Nine months ended September 30, | Twelve 2004 | ||||||||||||||||||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2003 | 2004 | |||||||||||||||||||||||||||

| (in thousands, except share and per share data and railcar amounts) | ||||||||||||||||||||||||||||||||

Other financial and operating data: | ||||||||||||||||||||||||||||||||

EBITDA(2) | $ | 39,492 | $ | 36,985 | $ | 27,407 | $ | 16,479 | $ | 7,747 | $ | 12,185 | $ | 9,260 | $ | (6,779 | ) | $ | (3,854 | ) | ||||||||||||

Adjusted EBITDA(2) | $ | 39,492 | $ | 36,985 | $ | 27,407 | $ | 16,479 | $ | 7,747 | $ | 12,185 | $ | 9,260 | $ | 2,380 | $ | 5,305 | ||||||||||||||

Other items (increasing) decreasing Adjusted EBITDA(3) | — | — | — | $ | (3,056 | ) | $ | (1,238 | ) | $ | 1,750 | $ | 1,750 | $ | 15,510 | $ | 15,510 | |||||||||||||||

Capital expenditures | $ | 1,260 | $ | 1,998 | $ | 3,441 | $ | 2,169 | $ | 553 | $ | 369 | $ | 279 | $ | 1,122 | $ | 1,212 | ||||||||||||||

New railcars delivered | 5,371 | 6,542 | 7,126 | 3,352 | 3,942 | 4,555 | 3,108 | 4,974 | 6,421 | |||||||||||||||||||||||

New railcar orders | 3,599 | 4,046 | 3,059 | 4,403 | 2,831 | 9,932 | 6,479 | 10,021 | 13,474 | |||||||||||||||||||||||

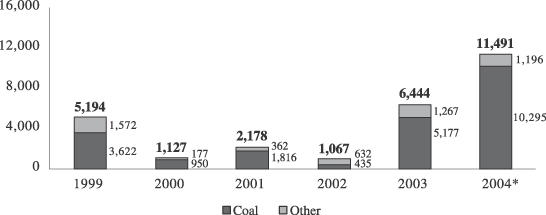

New railcar backlog | 7,690 | 5,194 | 1,127 | 2,178 | 1,067 | 6,444 | 4,438 | 11,491 | 11,491 | |||||||||||||||||||||||

Estimated backlog(4) | $ | 435,765 | $ | 295,188 | $ | 56,739 | $ | 108,217 | $ | 55,887 | $ | 365,876 | $ | 248,759 | $ | 750,293 | $ | 750,293 | ||||||||||||||

Balance sheet data (at period end): | ||||||||||||||||||||||||||||||||

Cash and cash equivalents | $ | 7,840 | $ | 30,487 | $ | 25,033 | $ | 19,725 | $ | 20,008 | $ | 4,702 | $ | 4,702 | ||||||||||||||||||

Restricted cash(5) | 82 | 3,882 | 4,061 | 4,116 | 11,698 | 12,936 | 12,936 | |||||||||||||||||||||||||

Total assets | 186,701 | 166,972 | 148,702 | 141,531 | 140,052 | 174,209 | 174,209 | |||||||||||||||||||||||||

Total debt(6) | 65,479 | 62,476 | 55,423 | 53,424 | 51,778 | 54,712 | 54,712 | |||||||||||||||||||||||||

Rights to additional acquisition consideration, including accumulated accretion(7) | 9,365 | 11,707 | 14,634 | 18,292 | 22,865 | 27,022 | 27,022 | |||||||||||||||||||||||||

Total redeemable preferred stock | 6,870 | 7,932 | 8,995 | 10,057 | 11,120 | 11,917 | 11,917 | |||||||||||||||||||||||||

Total stockholders’ equity (deficit) | 6,935 | 7,699 | 3,160 | (9,542 | ) | (19,710 | ) | (35,993 | ) | (35,993 | ) | |||||||||||||||||||||

| (1) | On November 15, 2004, we entered into the Johnstown settlement and recorded a $9.2 million charge with respect to the nine months ended September 30, 2004. As part of the Johnstown settlement, we agreed to pay back wages equal to $1.4 million to the covered employees and recorded a $0.8 million cash charge for expenses related to the Johnstown settlement in the nine months ended September 30, 2004. We also recorded $7.0 million of non-cash expense in the nine months ended September 30, 2004 related to pension and postretirement termination benefits accrued with respect to retired unionized employees at our Johnstown facility. See “Business—Legal proceedings—Labor dispute settlement.” |

| (2) | EBITDA represents net income (loss) before income tax expense, interest expense, net, amortization and depreciation of property and equipment. We believe EBITDA is useful to investors in evaluating our operating performance compared to that of other companies in our industry. In addition, our management uses EBITDA to evaluate our operating performance and our compliance with financial covenants contained in agreements governing our indebtedness. The calculation of EBITDA eliminates the effects of financing, income taxes and the accounting effects of capital spending. These items may vary for different companies for reasons unrelated to the overall operating performance of a company’s business. EBITDA is not a financial measure presented in accordance with U.S. generally accepted accounting principles, or U.S. GAAP. Accordingly, when analyzing our operating performance, investors should not consider EBITDA in isolation or as a substitute for net income, cash flows from operating activities or other income statement or cash flow statement data prepared in accordance with U.S. GAAP. Our calculation of EBITDA is not necessarily comparable to that of other similarly titled measures reported by other companies. |

| Adjusted EBITDA reflects EBITDA before the charge of $9.2 million that we recorded in the nine months ended September 30, 2004 in connection with the Johnstown settlement. See note (1) for more information. We believe Adjusted EBITDA is useful to investors in evaluating our operating performance compared to that of other companies in our industry by eliminating the effect of the Johnstown settlement, which is an unusual charge. Adjusted EBITDA is not a financial measure presented in accordance with U.S. GAAP. Accordingly, when analyzing our operating performance, investors should not consider Adjusted EBITDA in isolation or as a substitute for net income, cash flows from operating activities or other income statement or cash flow statement data prepared in accordance with U.S. GAAP. Our calculation of Adjusted EBITDA is not necessarily comparable to that of other similarly titled measures reported by other companies. |

10

Table of Contents

The following is a reconciliation of net income (loss) to EBITDA and Adjusted EBITDA:

| Predecessor | FreightCar America, Inc. | |||||||||||||||||||||||||||||||||||

Period from 1999 to | Period from 1999 | Year ended December 31, | Nine months ended September 30, | Twelve 2004 | ||||||||||||||||||||||||||||||||

| 2000 | 2001 | 2002 | 2003 | 2003 | 2004 | |||||||||||||||||||||||||||||||

| (in thousands) | ||||||||||||||||||||||||||||||||||||

Net income (loss) | $ | 22,816 | $ | 12,300 | $ | 1,826 | $ | (3,476 | ) | $ | (8,627 | ) | $ | (7,420 | ) | $ | (5,916 | ) | $ | (15,486 | ) | $ | (16,990 | ) | ||||||||||||

Income tax provision (benefit) | 14,398 | 9,236 | 6,089 | 167 | (3,554 | ) | (1,318 | ) | (710 | ) | (7,250 | ) | (7,858 | ) | ||||||||||||||||||||||

Related-party interest expense | — | 2,535 | 5,165 | 5,723 | 6,517 | 6,764 | 5,485 | 5,184 | 6,463 | |||||||||||||||||||||||||||

Third-party interest expense | 451 | 3,623 | 3,999 | 2,398 | 1,595 | 1,367 | 788 | 819 | 1,398 | |||||||||||||||||||||||||||

Interest expense on rights to additional acquisition | — | 1,192 | 2,341 | 2,927 | 3,659 | 4,573 | 3,326 | 4,157 | 5,404 | |||||||||||||||||||||||||||

Interest income | (663 | ) | (354 | ) | (1,391 | ) | (887 | ) | (162 | ) | (128 | ) | (94 | ) | (87 | ) | (121 | ) | ||||||||||||||||||

Amortization of deferred financing costs | — | 410 | 702 | 702 | 702 | 629 | 528 | 364 | 465 | |||||||||||||||||||||||||||

Write-off of deferred financing costs | — | — | — | — | — | 348 | 348 | — | — | |||||||||||||||||||||||||||

Amortization of goodwill | — | 1,074 | 1,812 | 1,744 | — | — | — | — | — | |||||||||||||||||||||||||||

Amortization of intangible assets | 677 | 3,196 | 632 | 711 | 853 | 590 | 443 | 442 | 589 | |||||||||||||||||||||||||||

Depreciation | 1,813 | 3,773 | 6,232 | 6,470 | 6,764 | 6,780 | 5,062 | 5,078 | 6,796 | |||||||||||||||||||||||||||

EBITDA | 39,492 | 36,985 | 27,407 | 16,479 | 7,747 | 12,185 | 9,260 | (6,779 | ) | (3,854 | ) | |||||||||||||||||||||||||

Provision for settlement of labor disputes | — | — | — | — | — | — | — | 9,159 | 9,159 | |||||||||||||||||||||||||||

Adjusted EBITDA | $ | 39,492 | $ | 36,985 | $ | 27,407 | $ | 16,479 | $ | 7,747 | $ | 12,185 | $ | 9,260 | $ | 2,380 | $ | 5,305 | ||||||||||||||||||

| (3) | Our net income (loss), EBITDA and Adjusted EBITDA were affected in the specified periods by the following items: |

| (a) | In the nine months ended September 30, 2004, an estimated $7.8 million in increased cost of raw materials, consisting primarily of aluminum and steel, which we were unable to pass on to our customers under our fixed-price customer contracts. As a result of the increased costs, we renegotiated our contracts with a majority of our customers to increase the purchase prices of our railcars to reflect the increased cost of raw materials, and as a result, we were able to pass on to our customers approximately 40% of the increased raw material costs with respect to the railcars that we produced and delivered in 2004. We had eight remaining fixed-price contracts reflecting a backlog of 2,828 railcars out of a total backlog of 11,491 railcars as of September 30, 2004, and we expect to deliver all of the railcars under the remaining fixed-price contracts by June 30, 2005. Other than the remaining fixed-price contracts, we have entered into contracts with all of our customers that allow for variable pricing to protect us against future changes in the cost of raw materials; |

| (b) | In the nine months ended September 30, 2004, a loss of $7.7 million on a customer contract for box railcars, which reflects increased raw material, labor and other costs that exceeded the fixed purchase price under this contract. This customer contract was our first contract for the manufacture of box railcars, and, following our delivery of the box railcars under this contract, we do not plan to produce any box railcars in the future; |

| (c) | For the year ended December 31, 2003, a finder’s fee of $1.8 million that we paid to a third party for securing a major railcar purchase order for us in early 2003, which is included in our selling, general and administrative expense. Our in-house sales personnel generally procure railcar purchase orders, and we do not ordinarily pay finder’s fees to obtain railcar purchase orders; and |

| (d) | In the years ended December 31, 2002 and 2001, curtailment gains of $1.2 million and $3.1 million, respectively, related to our postretirement benefit program resulting from our layoff of a significant number of unionized employees at our Johnstown facility. |

| See “Management’s discussion and analysis of financial condition and results of operations” and our consolidated financial statements and the related notes included elsewhere in this prospectus. |

| (4) | Estimated backlog reflects the total net sales attributable to the backlog reported at the end of the particular period as if such backlog were converted to actual sales. Estimated backlog does not reflect potential price increases or decreases under most of our customer contracts that provide for variable pricing based on changes in the cost of raw materials. See “Management’s discussion and analysis of financial condition and results of operations—Backlog.” |

| (5) | Our restricted cash for the year ended December 31, 2000 and the periods thereafter includes cash collateral of $3.8 million plus interest held in escrow for our participation in a residual support guarantee agreement with respect to railcars that we sold to a customer that are presently leased by the customer to a third party. Our restricted cash for the year ended December 31, 2003 and the periods thereafter also includes $7.5 million held in a restricted cash account as additional collateral for our existing revolving credit facility, which we expect to be released to us after we enter into the new revolving credit facility upon completion of this offering, and $1.2 million in escrow, representing security for workers’ compensation insurance, which will be replaced by a letter of credit under the new revolving credit facility upon completion of this offering. We do not expect the new revolving credit facility to require amounts to be held as cash collateral for borrowings. |

| (6) | Our total debt includes current maturities of long-term debt. |

| (7) | Our recorded liability under the rights to additional acquisition consideration is based on the fair value of the rights to additional acquisition consideration at the time that we acquired our business from TTII in 1999, using a discount rate of 25% and an expected redemption period of seven years. Upon a triggering event, including this offering, the amount payable as additional acquisition consideration will be $20.0 million in cash plus an accreted value that compounds at a rate of 10% annually. At September 30, 2004, assuming a triggering event had occurred, the amount payable as additional acquisition consideration was $33.3 million. |

11

Table of Contents

Investing in our common stock involves a high degree of risk. Before you invest in our common stock, you should understand and carefully consider the risks below, as well as all of the other information contained in this prospectus and our financial statements and the related notes included elsewhere in this prospectus. Any of these risks could materially adversely affect our business, financial condition, results of operations and the trading price of our common stock, and you may lose all or part of your investment.

RISKS RELATED TO THE RAILCAR INDUSTRY

We operate in a highly cyclical industry. Our sales are lower during economic downturns and unfavorable economic and market conditions adversely affect our business.

Historically, the North American railcar market has been highly cyclical, and we expect it to continue to be highly cyclical in the future. Our industry and the markets for which we supply railcars fluctuate in response to factors that are beyond our control. These factors include general North American and international economic conditions, changes in interest rates, federal and state regulatory activity and the purchasing habits of railcar buyers. Additionally, the demand for coal-carrying railcars fluctuates in response to changes in the rates of electricity usage. During downturns in overall economic conditions, electricity usage rates fall. Declines in rates of overall electricity usage will result in declines in the consumption of coal and, as a result, purchases of coal-carrying railcars. Coal-carrying railcars represented 76% of the railcars we delivered in 2003. Downturns in economic conditions could result in lower sales volumes, lower prices for railcars and a loss of profits. Any resulting decline in electricity usage will intensify these effects. See “Industry—Characteristics and trends affecting the railcar industry—Cyclical nature of the railcar market.”

During the most recent industry cycle, industry-wide railcar deliveries declined from a peak of 75,704 in 1998 to a low of 17,736 railcars in 2002. During this period, our railcar production declined from approximately 9,000 railcars in 1998 to 4,067 railcars in 2002. In 2003, industry-wide railcar deliveries grew to 32,183, and our railcar production increased to 4,376 railcars. The U.S. economy appears to be improving, as indicated by the increase in the U.S. real gross domestic product of 3.9% in the third quarter of 2004 following an increase of 3.3% in the second quarter of 2004, according to the U.S. Bureau of Economic Analysis. However, U.S. economic conditions may not continue to improve in the future or result in a sustained economic recovery. In addition, even if a sustained economic recovery occurs in the U.S., demand for our railcar offerings may not match or exceed past or expected levels.

Economic conditions may also result in shortages of raw materials or railcar component parts, longer sales cycles, deferral or delay of customer orders or our inability to market our products effectively. As a result, our business and results of operations could be materially adversely affected. In addition, any terrorist attacks in the United States, or elsewhere in the world, and any military action by the United States or other countries could intensify these conditions.

In addition, a substantial number of the end users of our railcars acquire railcars through leasing arrangements with our leasing company customers. Economic conditions that result in higher interest rates would increase the cost of new leasing arrangements, which could cause our leasing company customers to purchase fewer of our railcars.

12

Table of Contents

Risk factors

Increased cost and delivery delays of materials, especially aluminum and steel, may adversely affect our financial performance.

The production of railcars and our operations require substantial amounts of aluminum and steel. The cost of aluminum, steel and all other materials (including scrap metal) used in the production of our railcars represents approximately 70% of our direct manufacturing costs. Our business is subject to the risk of price increases and periodic delays in the delivery of aluminum, steel and other materials, all of which are beyond our control. The prices for steel and aluminum, the primary raw material components of our railcars, increased sharply in 2004 as a result of strong demand, limited availability of production inputs for steel and aluminum, including scrap metal, industry consolidation and import trade barriers. Our costs of raw steel and aluminum have increased by 140% and 35%, respectively, during the period from October 2003 through September 2004. The availability of scrap metal has been limited by exports of scrap metal to China, and as a result, steel producers have added surcharges on scrap metal in excess of agreed-upon prices. In addition, the price and availability of other railcar components that are made of steel have been adversely affected by the increased cost and limited availability of steel. Any fluctuations in the price or availability of aluminum or steel, or any other material used in the production of our railcars, may have a material adverse effect on our business, results of operations or financial condition.

In addition, if any of our suppliers were unable to continue its business or were to seek bankruptcy relief, the availability or price of the materials we use could be adversely affected. Deliveries of our materials may also fluctuate depending on supply and demand for the material or governmental regulation relating to the material, including regulation relating to the importation of the material.

We have renegotiated our contracts with a majority of our customers to increase the purchase prices of our railcars to reflect the increased cost of raw materials, and as a result, we were able to pass on to our customers approximately 40% of the increased raw material costs with respect to the railcars that we expect to produce and deliver by the end of 2004. In addition, we have entered into contracts with a majority of our customers that allow for variable pricing to protect us against future changes in the cost of raw materials. However, in the nine months ended September 30, 2004, we were unable to pass on an estimated $7.8 million in increased raw material costs to our customers under the existing fixed-price customer contracts, and we may not be able to pass on increases in the price of aluminum and/or steel to our customers in the future. In particular, when material prices increase rapidly or to levels significantly higher than normal, we may not be able to pass price increases through to our customers, which could adversely affect our operating margins and cash flows. Even if we are able to increase prices, any such price increases may reduce demand for our railcars.

We depend upon a small number of customers that represent a large percentage of our sales.

Since railcars are typically sold pursuant to large, periodic orders, a limited number of customers typically represent a significant percentage of our railcar sales in any given year. Over the last five years, our top five railcar customers in each year based on sales represented, in the aggregate, approximately 56% of our total net sales for the five-year period. In 2003, net sales to our top three customers accounted for approximately 22%, 16% and 13%, respectively, of our total net sales. Although we have long standing relationships with many of our major customers, the loss of any significant portion of our net sales to any major customer, the loss of a single major customer or a material adverse change in the financial condition of any one of our major customers could have a material adverse effect on our business and financial results.

13

Table of Contents

Risk factors

The variable purchase patterns of our customers and the timing of completion, delivery and acceptance of customer orders may cause our net sales and income from operations to vary substantially each quarter, which will result in significant fluctuations in our quarterly results.

Most of our individual customers do not make purchases every year, since they do not need to replace or replenish their railcar fleets on a yearly basis. Many of our customers place orders for products on an as-needed basis, sometimes only once every few years. As a result, the order levels for railcars, the mix of railcar types ordered and the railcars ordered by any particular customer have varied significantly from quarterly period to quarterly period in the past and may continue to vary significantly in the future. Therefore, our results of operations in any particular quarterly period may be significantly affected by the number of railcars ordered and delivered and product mix of railcars ordered in any given quarterly period. Additionally, because we record the sale of a railcar at the time we complete production, the railcar is accepted by the customer following inspection, the risk for any damage or loss with respect to the railcar passes to the customer and title to the railcar transfers to the customer, and not when the order is taken, the timing of completion, delivery and acceptance of significant customer orders will have a considerable effect on fluctuations in our quarterly results. As a result of these quarterly fluctuations, we believe that comparisons of our net sales and operating results between quarterly periods within the same fiscal year and between quarterly periods within different fiscal years may not be meaningful and, as such, these comparisons should not be relied upon as indicators of our future performance.

Limitations on the supply of heavy castings, wheels and other railcar components could adversely affect our business.

We rely upon third-party suppliers for railcar heavy castings, wheels and other components for our railcars. In particular, we purchase, and we believe most of our competitors purchase, a substantial percentage of our railcar heavy castings and wheels from subsidiaries of AMSTED Industries Inc. Due to manufacturing limitations at AMSTED Industries, we have only been supplied with a limited number of heavy castings, which has constrained, and which we expect will continue in the future to constrain, our production of railcars. For example, for the nine months ended September 30, 2004, due to a shortage of heavy castings, our deliveries were limited to 4,974 railcars, even though we had orders and production capacity to manufacture more railcars. AMSTED Industries and other suppliers of railcar components may be unable to meet the short-term or longer-term heavy castings and wheel supply demand of our industry. In the event that AMSTED Industries or our other suppliers of railcar components were to stop or reduce the production of heavy castings, wheels or the other railcar components that we use, go out of business, refuse to continue their business relationships with us or become subject to work stoppages, our business would be disrupted. Furthermore, our ability to increase our railcar production to expand our business and/or meet any increase in demand depends on our ability to obtain an adequate supply of these railcar components.

While we believe that we could secure alternative sources, we may incur substantial delays and significant expense in doing so, the quality and reliability of these alternative sources for these components may not be the same and our operating results may be significantly affected. In addition, if one of our competitors entered into a preferred supply arrangement with, or was otherwise favored by, AMSTED Industries, we would be at a competitive disadvantage, which could negatively affect our operating results. Furthermore, alternative suppliers might charge significantly higher prices for heavy castings or other railcar components than we currently pay. Under such circumstances, the disruption to our business could have a material adverse impact on our customer relationships, financial condition and operating results.

14

Table of Contents

Risk factors

We operate in a highly competitive industry.

We operate in a competitive marketplace and face substantial competition from established competitors in the railcar industry in North America. We have three principal competitors that primarily manufacture railcars for third-party customers. In addition, there are two other manufacturers of railcars whose production is used primarily for their own railcar leasing operations, competing directly with railcar leasing companies, some of which are among our largest customers. Some of these manufacturers have greater financial and technological resources than us, and they may increase their participation in the railcar segments in which we compete. Railcar purchasers’ sensitivity to price and strong price competition within the industry have historically limited our ability to increase prices. In addition to price, competition is based on product performance and technological innovation, quality, reliability of delivery, customer service and other factors. In particular, technological innovation by any of our existing competitors, or new competitors entering any of the markets in which we do business, could put us at a competitive disadvantage. We may be unable to compete successfully against other railcar manufacturers or retain our market share in our established markets. Increased competition for the sales of our railcar products, particularly our coal-carrying railcars, could result in price reductions, reduced margins and loss of market share, which could negatively affect our business, prospects and results of operations.

Further consolidation of the railroad industry may adversely affect our business.

Over the past ten years there has been a consolidation of railroad carriers operating in North America. Railroad carriers are large purchasers of railcars and represent a significant portion of our historical customer base. Future consolidation of railroad carriers may adversely affect our sales and reduce our income from operations because with fewer railroad carriers, each railroad carrier will have proportionately greater buying power and operating efficiency, which may intensify competition among railcar manufacturers to retain customer relationships with the consolidated railroad carriers and cause our prices to decline.

RISKS RELATED TO OUR BUSINESS

We rely significantly on the sales of our aluminum-bodied coal-carrying railcars. A decrease in the demand for coal relative to other energy sources could adversely affect us.

Our aluminum-bodied coal-carrying railcars are our primary railcar line, representing 71% of our net sales in 2003 and 76% of the total railcars that we delivered in 2003. Fluctuations in the price of coal relative to other energy sources may cause utility companies, which are significant customers of our coal-carrying railcar lines, to select an alternative energy source to coal, thereby reducing the strength of the market for coal-carrying railcars. For example, if utility companies were to begin preferring oil instead of coal as an energy source, demand for our coal-carrying railcar lines would decrease. The market for aluminum-bodied coal-carrying railcars may not remain favorable, and coal may not continue to be a preferred source of energy relative to other energy sources. In addition, our market share in the coal-carrying railcar segment depends on the continued market preference for coal-carrying railcars constructed with aluminum. If purchasers of coal-carrying railcars no longer purchase railcars constructed with aluminum, our market share in this segment may decline and our operating results may be negatively affected.

The U.S. federal and state governments may adopt new legislation and/or regulations, or judicial or administrative interpretations of existing laws and regulations, that materially adversely affect the coal

15

Table of Contents

Risk factors

industry and/or our customers’ ability to use coal or to continue to use coal at present rates. Such legislation or proposed legislation and/or regulations may include proposals for more stringent protections of the environment that would further regulate and tax the coal industry. This legislation could significantly reduce demand for coal, adversely affect the demand for our aluminum-bodied coal-carrying railcars and have a material adverse effect on our financial condition and results of operations.

In addition, the United States and over 160 other nations are signatories to the 1992 Framework Convention on Climate Change, which is intended to limit emissions of greenhouse gases, such as carbon dioxide. In December 1997, in Kyoto, Japan, the signatories to the convention, including the United States, established a binding set of emission targets for developed nations. Although the United States has not ratified the emission targets contained in the convention, the emission targets could serve as a guideline for efforts to stabilize or reduce greenhouse gas emissions in the United States, which could adversely impact the price of and demand for coal and the demand for our railcars. According to the Energy Information Administration’s Emissions of Greenhouse Gases in the United States 2003, coal accounts for approximately 36% of carbon dioxide emissions from both energy generating and industrial uses. Carbon dioxide represented 83% of greenhouse gas emissions in the United States in 2003. Efforts to control greenhouse gas emissions could result in reduced use of coal if electricity generators switch to sources of fuel with lower carbon dioxide emissions. If the United States were to adopt comprehensive regulations for its greenhouse gas emissions and/or ratify emissions targets for reduced greenhouse gas emissions (whether under the 1997 Kyoto convention or otherwise), these restrictions could adversely impact the price of and demand for coal, which could have a material adverse effect on our financial condition or results of operations.

We rely upon a single supplier to supply us with all of our cold-rolled center sills for our railcars, and any disruption of our relationship with this supplier could adversely affect our business.

We rely upon a single supplier to manufacture all of our cold-rolled center sills for our railcars, which are based upon our proprietary and patented process. In 2003, approximately 95% of the railcars we produced were manufactured using this cold-rolled center sill. Although we have a good relationship with our supplier and have not experienced any significant delays, manufacturing shortages or failures to meet our quality requirements and production specifications in the past, our supplier could stop production of our cold-rolled center sills, go out of business, refuse to continue its business relationship with us or become subject to work stoppages. While we believe that we could secure alternative manufacturing sources, our present supplier is currently the only manufacturer of our cold-rolled center sills for our railcars. We may incur substantial delays and significant expense in finding an alternative source, our results of operations may be significantly affected, and the quality and reliability of these alternative sources may not be the same. Moreover, alternative suppliers might charge significantly higher prices for our cold-rolled center sills than we currently pay. The prices for our cold-rolled center sills may also be impacted by the rising cost of steel and all other materials used in the production of our cold-rolled center sills. Under such circumstances, the disruption to our business may have a material adverse impact on our financial condition and results of operations.

Equipment failures, delays in deliveries or extensive damage to our facilities, particularly our facility in Danville, could lead to production or service curtailments or shutdowns.

We manufacture our railcars at production facilities in Danville, Illinois and Johnstown, Pennsylvania. An interruption in production capabilities at these facilities, as a result of equipment failure or other

16

Table of Contents

Risk factors

reasons, could reduce or prevent the production of our railcars. A halt of production at our facilities, particularly at our facility in Danville, which manufactured approximately 81% of our railcars manufactured during the nine months ended September 30, 2004 and produces all of our aluminum-bodied coal-carrying railcars, could severely affect delivery times to our customers. Any significant delay in deliveries to our customers could result in the termination of contracts, cause us to lose future sales and negatively affect our reputation among our customers and in the railcar industry and our results of operations. Our facilities are also subject to the risk of catastrophic loss due to unanticipated events, such as fires, explosions, floods or weather conditions. We may experience plant shutdowns or periods of reduced production as a result of equipment failures, delays in deliveries or extensive damage to any of our facilities, which could have a material adverse effect on our business, results of operations or financial condition.

An increase in health care and pension costs could adversely affect our results of operations.

The cost of health care benefits in the United States has increased significantly, leading to higher costs for us to provide health care benefits to our active and retired employees. If these costs continue to rise, our results of operations will be adversely affected. We are unable to limit our costs by changing or eliminating coverage under our employee benefit plans because a significant majority of our employee benefits are governed by union agreements. For example, as a result of the Johnstown settlement, we expect to make payments of approximately $2.7 million in 2005 and $2.9 million in 2006 for health care coverage costs of our retired employees at the Johnstown facility. As of September 30, 2004, our accumulated postretirement benefit obligation was $21.0 million and, as of December 31, 2004, we expect this amount to increase to approximately $53.7 million. Although the Johnstown settlement will limit our future contributions for health care coverage costs for our retired unionized Johnstown employees, we will continue to fund 100% of the health care coverage costs of our active unionized and non-unionized employees at our Johnstown facility and all of our active employees at our Danville facility. If our costs under our employee benefit plans for active employees at our Danville facility exceed our projections, our business and financial results could be materially adversely affected. See “Business—Legal proceedings—Labor dispute settlement.”

In addition, recent fluctuations in the financial markets have caused the valuation of the assets in our defined benefit pension plans to decrease, which has resulted in underfunding of our defined benefit pension plans and the recognition of a minimum pension liability on our balance sheet. As of September 30, 2004, our pension benefit obligations were underfunded by approximately $12.9 million and, as a result of the Johnstown settlement and the addition of existing retirees to our pension plans on January 1, 2005, we expect the underfunding to increase to approximately $24.6 million on January 1, 2005.Future fluctuations in the financial markets may result in additional underfunding of our defined benefit pension plans and may require contributions by us that could adversely affect our results of operations and financial position.

The level of our reported backlog may not necessarily indicate what our future sales will be.

We define backlog as the sales value of products or services to which our customers have committed in writing to purchase from us which have not been recognized as sales. In this prospectus, we have disclosed our backlog, or the number of railcars for which we have purchase orders, in various periods and the estimated sales value (in dollars) that would be attributable to this backlog once the backlog is converted to actual sales. We consider backlog to be an indicator of future sales of railcars. However, our reported backlog may not be converted into sales in any particular period, if at all, and the actual sales (including any compensation for lost profits and reimbursement for costs) from such contracts may not equal our reported estimates of backlog value. For example, we rely on third-party suppliers for heavy castings, wheels and components for our railcars and if these third parties were to stop or reduce

17

Table of Contents

Risk factors

their supply of heavy castings, wheels and other components, our actual sales would fall short of the estimated sales value attributed to our backlog. Furthermore, any contract included in our reported backlog that actually generates sales may not be profitable. Therefore, our current level of reported backlog may not necessarily represent the level of sales that we may generate in any future period.

Once we become a public company, we will need to comply with Section 404 of the Sarbanes-Oxley Act of 2002. If we fail to comply with Section 404 of the Sarbanes-Oxley Act or if we or our independent auditors report a material weakness in the effectiveness of our internal controls over financial reporting, our business, results of operations and financial condition could be materially adversely affected.

We are required under applicable law and regulations to integrate our systems of internal controls over financial reporting, and we are presently evaluating our existing internal controls with respect to the standards adopted by the Public Company Accounting Oversight Board. During the course of our evaluation, we may identify areas requiring improvement and may be required to design enhanced processes and controls to address issues identified through this review. This could result in significant delays and cost to us and require us to divert substantial resources, including management time, from other activities. We have recently commenced our review of our existing internal controls, and we cannot be certain at this time that we will be able to successfully complete the procedures, certification and attestation requirements of Section 404 of the Sarbanes-Oxley Act of 2002 by the time that we are required to file our Annual Report on Form 10-K for the year ended December 31, 2005, or that we or our independent auditors will not have to report a material weakness in connection with the presentation of our 2005 financial statements. If we fail to achieve and maintain the adequacy of our internal controls, we may not be able to ensure that we can conclude on an ongoing basis that we have effective internal controls over financial reporting in accordance with the Sarbanes-Oxley Act. Moreover, effective internal controls are necessary for us to produce reliable financial reports and are important to help prevent fraud. As a result, our failure to satisfy the requirements of Section 404 on a timely basis could result in the loss of investor confidence in the reliability of our financial statements, which in turn could harm our business and negatively impact the trading price of our common stock.

If we lose key personnel, our operations and ability to manage the day-to-day aspects of our business will be adversely affected.

We believe our success depends to a significant degree upon the continued contributions of our executive officers and key employees, both individually and as a group. Our future performance will substantially depend on our ability to retain and motivate them. If we lose key personnel or are unable to recruit qualified personnel, our ability to manage the day-to-day aspects of our business will be adversely affected.

The loss of the services of one or more members of our senior management team could have a material adverse effect on our business, financial condition and results of operations. Because our senior management team has many years of experience with our company and within the railcar industry and other manufacturing industries, it would be difficult to replace any of them without adversely affecting our business operations. Our future success will also depend in part upon our continuing ability to attract and retain highly qualified personnel. We do not currently maintain “key person” life insurance.

Labor disputes may have a material adverse effect on our operations and profitability.

Approximately 85% of our employees, as of September 30, 2004, are members of unions. We have a collective bargaining agreement with the United Automobile, Aerospace and Agricultural Workers of

18

Table of Contents

Risk factors

America, or the UAW, representing approximately 91% of our employees at the Danville facility. Our employees at our Johnstown facility represented by the USWA had been without a collective bargaining agreement since October 2001. The USWA, which represents approximately 81% of our employees at the Johnstown facility and approximately 46% of our total active labor force as of September 30, 2004, filed charges in January 2002 against our subsidiary alleging unfair labor practices in violation of the National Labor Relations Act, or the NLRA, in connection with our practices during our negotiation of a new collective bargaining agreement. In addition, our subsidiary was a defendant in the Deemer and Britt lawsuits, two class action lawsuits filed by the USWA on behalf of individual plaintiffs alleging violations of the NLRA and ERISA in connection with certain medical and life insurance benefits and pension supplements that were discontinued with respect to certain retirees. On November 15, 2004, our subsidiary entered into a settlement agreement setting forth the terms of a new collective bargaining agreement with the USWA which expires on May 15, 2008. The Johnstown settlement also resolved the NLRB charges filed against our subsidiary relating to the collective bargaining agreement, the Deemer and Britt lawsuits and certain other outstanding workplace grievances matters. See “Business—Legal proceedings—Labor dispute settlement.” Although the disputes involving the USWA did not result in strikes or other labor protests, any future labor disputes with the USWA or the UAW could result in strikes or other labor protests which could disrupt our operations. If we were to experience a strike or work stoppage, it would be difficult for us to find a sufficient number of employees with the necessary skills to replace these employees. Any such labor disputes could have a material adverse effect on our business, financial condition or results of operations.

Lack of acceptance of our new railcar offerings by our customers could adversely affect our business.