Filed pursuant to Rule 253(g)(2)

File No. 024-10918

OFFERING CIRCULAR DATED FEBRUARY 11, 2019

Coherix, Inc.

3980 Ranchero Dr.

Ann Arbor, MI 48108

(734) 922-4073

Up to 2,500,000 shares of Common Stock, par value $0.001

SEE “DESCRIPTION OF CAPITAL STOCK” AT PAGE 46

MINIMUM INDIVIDUAL INVESTMENT: 200 Shares $1,200

| | Price to Public | Underwriting discount and

commissions (2) | Proceeds to issuer |

| Per share/unit | $ 6.00 | $ 0.00 | $ 6.00 |

| Total Maximum | $ 15,000,000 | $ 0.00 | $ 15,000,000(1) |

(1)Before deducting expenses, estimated to be approximately $500,000 including legal fees, accounting fees, and printer costs. For more details, please see the section of this offering circular captioned “Plan of Distribution.” This is a “best efforts” offering. There is no minimum number of shares that must be distributed in this offering.

(2)The company does not currently intend to use commissioned sales agents or underwriters. In the event it uses commissioned sales agents or underwriters, it will file an amendment to the Offering Statement of which this Offering Circular forms a part.

The offering will commence within two calendar days after the offering statement in which this offering circular is included has been qualified by the US Securities and Exchange Commission (the “Commission” or the “SEC”) and includes an amount of shares that we reasonably expect to be offered and sold within two years from the date of initial qualification, unless subsequently amended. The offering will terminate at the earlier of: (1) the date at which the maximum offering amount has been sold, (2) the date which is one year from this offering being qualified by the Commission, or (3) the date at which the offering is earlier terminated by us in our sole discretion.

There is no minimum number of shares that we must sell in order to conduct a closing in this offering. We have made no arrangements to place subscription funds in an escrow, trust or similar account. Shares issued under this offering will be issued on a continuous basis under Rule 251(d)(3) under the Securities Act, and the company will have access to such funds from the first dollar invested, even if those proceeds do not cover the costs of this offering. For further details please see the section of this offering circular captioned “Plan of Distribution.”

THE UNITED STATES SECURITIES AND EXCHANGE COMMISSION DOES NOT PASS UPON THE MERITS OF OR GIVE ITS APPROVAL TO ANY SECURITIES OFFERED OR THE TERMS OF THE OFFERING, NOR DOES IT PASS UPON THE ACCURACY OR COMPLETENESS OF ANY OFFERING CIRCULAR OR OTHER SELLING LITERATURE. ANY REPRESENTATION TO THE CONTRARY IS UNLAWFUL.

THE SECURITIES HAVE NOT BEEN REGISTERED UNDER THE SECURITIES ACT OF 1933, AS AMENDED (THE “SECURITIES ACT”) OR APPLICABLE STATE SECURITIES LAWS, AND THESE SECURITIES ARE OFFERED PURSUANT TO AN EXEMPTION FROM REGISTRATION WITH THE COMMISSION. HOWEVER, THE COMMISSION HAS NOT MADE AN INDEPENDENT DETERMINATION THAT THE SECURITIES OFFERED HEREUNDER ARE EXEMPT FROM REGISTRATION.

THIS OFFERING CIRCULAR CONTAINS ALL OF THE REPRESENTATIONS BY THE COMPANY CONCERNING THIS OFFERING, AND NO PERSON SHALL MAKE DIFFERENT OR BROADER STATEMENTS THAN THOSE CONTAINED HEREIN. INVESTORS ARE CAUTIONED NOT TO RELY UPON ANY INFORMATION NOT EXPRESSLY SET FORTH IN THIS OFFERING CIRCULAR.

GENERALLY NO SALE MAY BE MADE TO YOU IN THIS OFFERING IF THE AGGREGATE PURCHASE PRICE YOU PAY IS MORE THAN 10% OF THE GREATER OF YOUR ANNUAL INCOME OR NET WORTH. DIFFERENT RULES APPLY TO ACCREDITED INVESTORS AND NON-NATURAL PERSONS. BEFORE MAKING ANY REPRESENTATION THAT YOUR INVESTMENT DOES NOT EXCEED APPLICABLE THRESHOLDS, WE ENCOURAGE YOU TO REVIEW RULE 251(d)(2)(i)(C) OF REGULATION A. FOR GENERAL INFORMATION ON INVESTING, WE ENCOURAGE YOU TO REFER TOwww.investor.gov.

This offering is inherently risky. See “Risk Factors” on page 8.

Sales of these securities will commence on approximately February 11, 2019.

The company is following the Form S-1 format of disclosure under Regulation A.

Table of Contents

In this Offering Circular, the terms “Coherix” or “the company,” “us” or “we” refer to Coherix, Inc. and its consolidated subsidiaries.

Statement Regarding Forward-Looking Statements

THIS OFFERING CIRCULAR MAY CONTAIN FORWARD-LOOKING STATEMENTS AND INFORMATION RELATING TO, AMONG OTHER THINGS, THE COMPANY, ITS BUSINESS PLAN AND STRATEGY, AND ITS INDUSTRY. THESE FORWARD-LOOKING STATEMENTS ARE BASED ON THE BELIEFS OF, ASSUMPTIONS MADE BY, AND INFORMATION CURRENTLY AVAILABLE TO THE COMPANY’S MANAGEMENT. WHEN USED IN THE OFFERING MATERIALS, THE WORDS “ESTIMATE,” “PROJECT,” “BELIEVE,” “ANTICIPATE,” “INTEND,” “EXPECT” AND SIMILAR EXPRESSIONS ARE INTENDED TO IDENTIFY FORWARD-LOOKING STATEMENTS, WHICH CONSTITUTE FORWARD LOOKING STATEMENTS. THESE STATEMENTS REFLECT MANAGEMENT’S CURRENT VIEWS WITH RESPECT TO FUTURE EVENTS AND ARE SUBJECT TO RISKS AND UNCERTAINTIES THAT COULD CAUSE THE COMPANY’S ACTUAL RESULTS TO DIFFER MATERIALLY FROM THOSE CONTAINED IN THE FORWARD-LOOKING STATEMENTS. INVESTORS ARE CAUTIONED NOT TO PLACE UNDUE RELIANCE ON THESE FORWARD-LOOKING STATEMENTS, WHICH SPEAK ONLY AS OF THE DATE ON WHICH THEY ARE MADE. THE COMPANY DOES NOT UNDERTAKE ANY OBLIGATION TO REVISE OR UPDATE THESE FORWARD-LOOKING STATEMENTS TO REFLECT EVENTS OR CIRCUMSTANCES AFTER SUCH DATE OR TO REFLECT THE OCCURRENCE OF UNANTICIPATED EVENTS.

Industry and Market Data

Although we are responsible for all disclosure contained in this Offering Circular, in some cases we have relied on certain market and industry data obtained from third-party sources that we believe to be reliable. Market estimates are calculated by using independent industry publications in conjunction with our assumptions regarding the machine vision for manufacturing industry and market. While we are not aware of any misstatements regarding any market, industry or similar data presented herein, such data involves risks and uncertainties and is subject to change based on various factors, including those discussed under the headings “Statement Regarding Forward-Looking Statements” and “Risk Factors” in this Offering Circular.

OFFERING CIRCULAR SUMMARY

This summary highlights selected information contained elsewhere in this Offering Circular. This summary is not complete and does not contain all the information that you should consider before deciding whether to invest in our Common Stock. You should carefully read the entire Offering Circular, including the risks associated with an investment in the company discussed in the "Risk Factors" section of this Offering Circular, before making an investment decision. Some of the statements in this Offering Circular are forward-looking statements. See the section entitled "Statement Regarding Forward-Looking Statements."

Company Information

The company was organized on October 30, 2003, under the laws of the State of Delaware. Our principal executive office is located at 3980 Ranchero Drive, Ann Arbor, MI 48108, and our telephone number is 734-922-4073. We have a wholly owned subsidiary in Singapore, Coherix Asia PTE Ltd., to market Coherix semiconductor products in the Asia Pacific region and a wholly owned subsidiary in Germany, Coherix GMBH, to market Coherix products in Europe. We have a distribution agreement with Marubeni to market Coherix products in Japan. In March 2018, we began to operate a Chinese Wholly Foreign Owned Enterprise (“WFOE”) in Shanghai, China to market and distribute Coherix, Inc. products in China.

Our website address is www.coherix.com. We do not incorporate the information on or accessible through our website into this Offering Circular, and you should not consider any information on, or that can be accessed through, our website as part of this Offering Circular.

Our Business

Coherix is a leading three-dimensional (“3D”) machine vision provider engaged in the development and application of high-speed error-proofing solutions for the automotive, semiconductor, electronics and general manufacturing sectors. Such solutions support the increasing demand to further automate various manufacturing processes. Coherix’s 3D machine vision products include software and hardware that serve as the “Eyes of Automation” and function like eyes for automation equipment such as robots and other complex machines. Coherix 3D machine vision products can perform many functions human eyes cannot, such as high precision, high speed, in-line error-proofing. To capture 3D information, Coherix uses its proprietary “SHARK™” electronic modules providing advanced sensor technology (the eyes). In addition, our proprietary “i-Cite™” software serves as the brains behind the eyes, and performs high speed processing of the 3D information coming from the sensors. Over 200 field tested powerful i-Cite software modules are adaptable, efficient, and easy-to use, acting as the “brains” of our entire suite of the company’s 3D machine vision products.

Machine vision is used in manufacturing when the requirements of the manufacturing process have surpassed the limits of human eyesight. Our products deliver substantial cost savings which are obtained through improved product quality and higher throughput. Manufactured parts often are produced with tolerances too small to be analyzed by the human eye. Machine vision technology provided by Coherix provides manufacturing solutions with sight, which meet the increasing demands for speed and accuracy in manufacturing processes, as well as smaller tolerances on parts being manufactured. Machine vision technologies have traditionally been two-dimensional (“2D”). It is well known that 2D vision cameras operate based on contrast of light in the scene, therefore, if the ambient light or the color of the part changes, the functions of the 2D vision camera are negatively impacted. Coherix 3D vision systems are not susceptible to ambient light or if the color of the part changes, which we believe is a significant change in inspection (error-proofing) in manufacturing. Industry analysts estimate that the 3D machine vision business could grow at a rate of 30% annually in terms of revenues.

Software and Hardware Platforms for our Products

Our core strategy is to displace temperamental 2D technology by offering manufacturers what we believe to be a more capable, cost-effective, and more reliable 3D solution. Coherix’s high-speed 3D solutions are based on our two proprietary software and hardware platforms: i-Cite modular software platform, and our proprietary modular SHARK hardware platform. The combination of the i-Cite software and SHARK hardware platforms significantly reduce time and effort to develop 3D vision solutions, thereby delivering greater performance at lower cost.

Our Error-Proofing Products

Error-proofing solutions are critical to the manufacturing of high volume and high value parts. Error-proofing is necessary given manufacturers’ stringent focus on quality and safety while delivering higher efficiencies and throughput. Coherix’s 3D error-proofing products are used in the electronics, semiconductor, automotive, and general manufacturing market segments. Our customers implement our high speed Robust3D® error-proofing solutions directly into their manufacturing processes in order to avoid defects in their manufacturing process.

Coherix solves difficult problems in manufacturing with its 3D vision solutions that cannot be performed by humans. Most of the manufacturing problems our products are solving have existed over several decades. Previously they could not be solved with human inspectors, mechanical probes, or 2D machine vision technologies. Solving these difficult manufacturing problems requires robust 3D (capable of performing without failure under a wide range of conditions) machine vision technology.

Coherix’s Robust3D machine vision technology has only been available since 2015 when Coherix introduced three new product lines.

Predator3D™

Our Predator3D™ product line performs error-proofing of the dispensing of sealants and structural adhesives. It is primarily used for structural adhesive bead volume and location in body assembly and room temperature vulcanization, used for sealing in engine and transmission assemblies.

Robust3D®

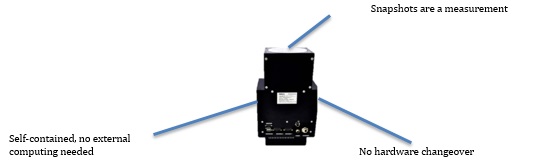

The second product line Coherix introduced in 2015 is called Robust3D, which is the new standard for assembly error-proofing in manufacturing processes. With its self-contained processor, the Tru3D™ sensor, it can be used for several applications.

Currently Tru3D (one sensor in the Robust3D error-proofing product line) is primarily used in the assembly of auto engines. However, any industry that assembles high value products will benefit from using our Robust3D error-proofing products.

Saber3D™

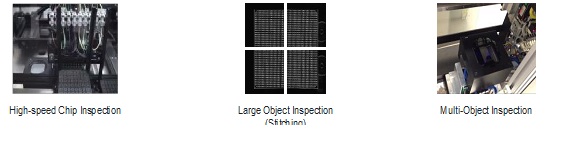

The third product line is called Saber3D, which is a high-speed, in-line inspection product line that eliminates the need for production machines to stop the assembly to perform inspection. Saber3D is the second generation of the 3DX product line, now featuring enhanced “Field of View” resolution and speed characteristics. It is used for very high speed error-proofing of small parts (maximum size 35 millimeters by 35 millimeters) primarily in the semiconductor and electronics manufacturing processes. However, in the future the company intends to introduce Saber3D products with larger Fields of View into other industries which have a need to perform high speed inspection of small objects.

Diverse End-User Markets

Our products can be used in a number of different markets.

Structural Adhesives

The global structural adhesives market grew to approximately $18.3 billion in 2016 with the compound annual growth rate (“CAGR”) anticipated to be approximately 7.9% from 2016 to 2022. High demand for lightweight metals and composites in applications such as automotive, transportation, building and construction and furniture are expected to fuel the overall demand of structural adhesives in future.

Automotive

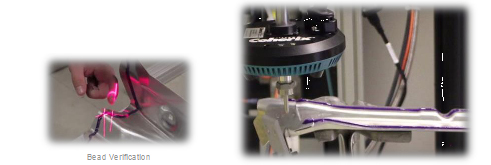

The International Organization of Motor Vehicle Manufacturers reported global production of 97.3 million motor vehicles in 2017, up 2.4% over 2016. Automobiles and commercial vehicles require precision and consistency in manufacturing. Our error-proofing solutions enable our customers to reduce variation, resulting in consistent high quality. The automotive industry’s need to reduce vehicle weight promotes the joining of light weight dissimilar materials such as magnesium, aluminum, special light weight steel, and composites. The joining of these dissimilar materials cannot be done by traditional joining methods such as welding. Therefore, sophisticated adhesives and sealers have been developed and their use is accelerating in the aircraft, automotive, truck, and other industries. The requirement to know how much adhesive is applied and where it is applied to join dissimilar materials drives the demand for our Predator3D Bead Verification products. Our Predator3D™ products are used in automotive vehicle assembly plants where the auto bodies are constructed. Some classes of body joints are also subject to federal government safety standards requiring 100% error-proofing inspection. Also, in what is called the general vehicle assembly area, Predator3Ds are used to control the glass bonding of windshield and other glass components into the auto body. We call this Predator3D the GlassMaster™. Coherix continually focuses on adding value to improve the end user’s process control. As an example, the distance between the dispensing nozzle tip and the surface of the part is critical to the quality of the bead. Fortunately, Predator3D is designed with lasers all around the dispensing nozzle. Therefore, there are lasers behind the nozzle to inspect the dispensed bead, and there are also lasers ahead of the bead to control a predetermined distance between the nozzle tip and the surface (the distance in the “Z” dimension). To maintain this distance, Predator3D measures the distance continuously and sends Z height dimension offsets to adjust the robot path.

Predator3Ds are also used for error-proofing to control inspection in the manufacturing of doors, hoods, and trunks. To gain additional competitive advantage, the company has developed a special solution product for verifying the correct shape and volume of mastic dots, which are used to prevent the outer skin of a vehicle from fluttering when being driven. We call this special sensor DotMaster™.

Structural adhesives used in automotive are known for providing better adhesion between distinct substrates such as steel and plastics. Thus, these composites are used in doors, window glass attachments, brakes and clutch plates and others. On account of high demand for passenger cars in countries like China and India, the automotive industry requires adhesives with structural integrity and strong bonding properties that is expected to impact the global structural adhesive market growth.

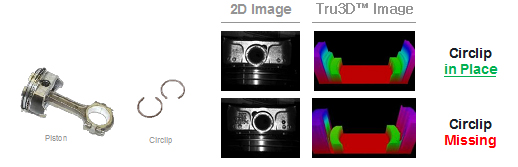

Other auto manufacturing plants build engines and transmissions. These plants are called powertrain plants. Coherix Robust3D solutions are used for error-proofing the engine assembly process. There are several different applications in a powertrain plant. One application uses Predator3Ds to error proof “form in place gaskets.” This dispensed material eliminates the need to design, build, and stock hard gaskets. The company also has Robust3D error-proofing solutions for piston-pin circlips, rolling finger followers, and valve assembly. Additional applications are in development.

Coherix provides accurate and reliable error-proofing powertrain solutions globally to top automotive industry names. A sample list of these customers is Fiat Chrysler Automotive, Ford Motor Company, General Motors, Toyota, Honda, Nissan, Mazda, and SAIC-GM-Wuling Automobile.

The International Organization of Motor Vehicle Manufacturers reports 5 regions of the world accounted for nearly 70% of global motor vehicle production last year.

Management presentation of data derived from International Organization of Motor Vehicle Manufacturers Global Production Statistics.

Semiconductors

According to industry analysts, the global semiconductor market in 2017 was estimated to grow to approximately $377 billion in annual sales. According to World Semiconductor Trade Statistics, the worldwide semiconductor market is expected to increase by 15.7 percent in 2018 after 21.6 percent growth in 2017.

The semiconductor industry produces billions of components/packages per year. Most high value packages need to be inspected in 3D for several types of defects. Since its founding, Coherix has developed in-depth knowledge of the semiconductor industry through close relationships with several customers serving the “back end assembly and test” part of the semiconductor manufacturing process. We believe as the semiconductor industry moves to wafer level packaging (back end), 3D machine vision error-proofing solutions will need to adapt, and Coherix technology will be used to rapidly develop new applications via SHARK and i-Cite because of its high performance and low cost.

The company serves a significant number of industry leaders through its error-proofing solutions. Coherix views the Chinese market as a focused area of expansion in semiconductors due to the Chinese government’s intended investment of up to $161 billion over the next decade to promote domestic chip manufacturers.

In early 2018, Coherix incorporated Coherix China, Inc., a Chinese Wholly Foreign Owned Enterprise, to capitalize on the opportunities that the company believes exist in the automotive and semiconductor business in China. Coherix’s ability to take advantage of the large market in semiconductor has been limited due to lack of growth capital.

Electronics

The company’s understanding of the electronics industry was increased through a joint development project with Panasonic Factory Solutions Co, Ltd. (“Panasonic”), a large electronics manufacturer. Coherix owns the intellectual property (“IP”) developed during this project, and has licensed its IP portfolio to be used solely on one application. The company’s modular SHARK technology platform was developed during this project.

Other Opportunities

Coherix solutions can be applied across a variety of end markets where precision, speed, and automation are paramount. Examples include aircraft manufacturing, solar panels, biotechnology/medical, robot guidance for packaging, etc. Coherix’s strategy has been to first gain critical mass and exposure in the automotive, semiconductor, electronics, and general manufacturing markets with future plans to capitalize on additional end markets. Many of our large system integrators and dispensing customers not only use our products in their primary industries, but they are also beginning to utilize our products in their other industry segments.

Due to continued miniaturization of electronic systems, the error-proofing challenges are becoming more demanding, and therefore, we believe, increasing the need for Coherix’s products. With the increase in growth capital from this offering, the company plans to expand marketing into the electronics industry.

The Offering

| Securities offered: | 2,500,000 shares of Common Stock |

| Number of outstanding shares of Common Stock before the offering: | 13,091,200 |

| Number of shares of Common Stock to be outstanding after the offering: | 15,591,200 |

| Price per share:

| $6.00 |

| Maximum offering amount: | $15,000,000 |

| Use of proceeds: | Growth capital and certain debt repayment |

Risk Factors

Our business is subject to a number of risks and uncertainties, including those highlighted in the section titled “Risk Factors” immediately following this summary. These risks include, but are not limited to, the following:

Risks Related to the Company

| · | We have an evolving business model. |

| · | Our auditors have included a “going concern” explanatory paragraph in their audit opinion indicating substantial doubt about the company’s ability to continue as a going concern. |

| · | We are in default with respect to certain of our liabilities. |

| · | Our failure to introduce new products in a successful and timely manner could result in the loss of our market share and a decrease in our revenues and profits. |

| · | Future disruptive new technologies could have a negative effect on our business. |

| · | The loss of a large customer could have an adverse effect on our business. |

| · | A downturn in the semiconductor, electronics, or automotive industries may adversely affect our business. |

| · | Our inability to penetrate new markets may impede our revenue growth. |

| · | Information security breaches or business system disruptions may adversely affect our business. |

| · | The failure of a key supplier to deliver quality product in a timely manner or our inability to obtain components for our products could adversely affect our operating results. |

| · | We do not have agreements with our suppliers and rely on purchase order requests to obtain components for our products; the inability to obtain components for our products could adversely affect our operating results. |

| · | Our products may contain design or manufacturing defects, which could result in reduced demand, significant delays, or substantial costs. |

| · | Our failure to properly manage the distribution of our products and services could result in the loss of revenues and profits. |

| · | If we fail to successfully protect our intellectual property, our competitive position and operating results could suffer. |

| · | Our company may be subject to time-consuming and costly litigation. |

| · | Increased competition may result in decreased demand or prices for our products and services. |

| · | Our business could suffer if we lose the services of, or fail to attract, key personnel and additional personnel. |

| · | Implementation of our joint venture strategy may not be successful, which could affect our ability to increase our revenue or profitability and result in the impairment of acquired intangible assets. |

| · | Global economic conditions may negatively impact our operating results. |

| · | Financial, political, and other risks associated with international sales and operations could adversely affect our business and operating results. |

| · | The status of our joint venture in China is uncertain. |

| · | The trade war between the United States and China may have a negative impact on our business. |

| · | Fluctuations in foreign currency exchange rates could adversely affect our reported results, liquidity, and competitive position. |

| · | Investment in technologies, products, and regions that are unprofitable could have a negative impact on our company. |

| · | Our bylaws designate the Court of Chancery of the State of Delaware as the sole and exclusive forum for certain types of actions and proceedings that may be initiated by our stockholders, which could limit our stockholders’ ability to obtain a favorable judicial forum for disputes with us or our directors, officers or employees. |

Risks Related to the Offering and Investment

| · | Our stock price may be volatile. |

| · | We have not paid cash dividends on Common Stock in the past and do not expect to pay dividends in the future. Any return on investment may be limited to the value of our Common Stock. |

| · | There is currently no trading market for our Common Stock and we cannot ensure that one will ever develop or be sustained. |

| · | Sales by our significant stockholders could have an adverse effect on the market price of our stock. |

| · | We may need to implement additional finance and accounting systems, procedures and controls as we grow our business and organization and to satisfy new reporting requirements. |

| · | We have not conducted an evaluation of the effectiveness of our internal control over financial reporting and will not be required to do so until we are a public company. If we are unable to implement and maintain effective internal control over financial reporting investors may lose confidence in the accuracy and completeness of our financial reports and the market price of our Common Stock may be negatively affected. |

| · | There may be implications of being an Emerging Growth Company. |

| · | We may not satisfy NASDAQ’s initial quotation standards and, even if we do, we may be removed from quotation in the future. |

| · | Investors in this offering are bound by the governing law and jurisdiction provision contained in the subscription agreement, which limits an investor’s ability to bring lawsuits in connection with this offering. |

| · | You will experience future dilution as a result of future equity offerings. |

RISK FACTORS

The SEC requires the company to identify risks that are specific to its business and its financial condition. The company is still subject to all the same risks that all companies in its business, and all companies in the economy, are exposed to. These include risks relating to economic downturns, political and economic events and technological developments (such as hacking and the ability to prevent hacking). Additionally, early-stage companies are inherently more risky than more developed companies. You should consider general risks as well as specific risks when deciding whether to invest.

We have an evolving business model.

As machine vision technologies evolve, so will our business model. We may continue to try to offer additional types of products and services, and we cannot offer any assurance that any of them will be successful. From time to time we may also modify aspects of our business model relating to our product mix and service offerings. We cannot offer any assurance that these or any other modifications will be successful or will not result in harm to the business. Among the risks associated with the introduction of new products are research and development costs involved in new products, costs associated with launching new products, difficulty predicting customer demand and effectively managing inventory levels to ensure adequate supply of the new product and avoid excess supply of the legacy product. We may not be able to manage growth effectively, which could damage our reputation, limit our growth, and negatively affect our operating results.

We may strategically enter into non-cancelable commitments with vendors to purchase materials for our products in advance of demand to take advantage of favorable pricing or address concerns about the availability of future supplies or long lead times. This practice may expose us to an increased risk of excess or obsolete inventory and resulting charges if actual demand is lower than anticipated. Our failure to effectively manage product transitions or accurately forecast customer demand, in terms of both volume and configuration, has led to, and may again in the future lead to, an increased risk of excess or obsolete inventory and resulting charges.

Our auditors have included a “going concern” explanatory paragraph in their audit opinion indicating substantial doubt about the company’s ability to continue as a going concern.

As indicated in our December 31, 2017 financial statements and our independent auditor’s report, the financial statements have been prepared assuming that the company will continue as a going concern. The company’s ability to continue as a going concern is dependent on our ability to continue with our increased operating cash flow, debt management, and capital raising. The December 31, 2017 financial statements do not include any adjustments to reflect the possible future effects on the recoverability and classification of assets, or the amounts and classification of liabilities that may result if we do not continue as a going concern. Therefore, you should not rely on our balance sheet as an indication of the amount of proceeds that would be available to satisfy claims of creditors, and potentially be available for distribution to stockholders, in the event of liquidation.

We are in default with respect to certain of our liabilities.

We are currently in default with respect to certain of our liabilities. These liabilities consist of:

| · | $1,497,087 in principal amount of convertible debentures owed to investors and service providers who accepted notes in lieu of cash payments. Accrued and unpaid interest on these debentures is a current liability. |

| · | $1,973,627 in principal owed to Volvo Group Venture Capital AB (“Volvo”) under a promissory note. Accrued and unpaid interest on the promissory note is a current liability. |

| · | $2,027,139 owed to employees and consultants who agreed to defer all or a portion of their compensation in 2005-2011 under a plan that we refer to as the “Top Hat Deferred Compensation Plan.” Accrued and unpaid interest on this deferred compensation is a current liability. |

| · | $849,963, which represents accrued and unpaid cumulative dividends declared by the Board on previously outstanding shares of the company’s preferred stock that were converted into shares of Common Stock in November 2017. |

If we raise all the funds we are seeking under this offering, we intend to use $5 million of the net proceeds to repay all of the above amounts owed under the convertible debentures ($1,497,087), 50% of the principal and accrued interest amount owed to Volvo ($1,036,657), $1,616,293 of the amount owed under the Top Hat Deferred Compensation Plan, which includes a portion of the accrued interest under that program, and all of the accrued and unpaid dividends ($849,963). These proceeds will not therefore be available to grow our business. See “Use of Proceeds.”

Our failure to introduce new products in a successful and timely manner could result in the loss of our market share and a decrease in our revenues and profits.

The market for our products is characterized by rapidly changing technology. Accordingly, we believe that our future success will depend upon our ability to accelerate time-to-market for new products with improved functionality, ease-of-use, performance, or price. There can be no assurance that we will be able to introduce new products in accordance with scheduled release dates or that new products will achieve market acceptance. Our ability to keep pace with the rapid rate of technological change in the high-technology marketplace could have a material adverse effect on our operating results.

Product development is often a complex, time-consuming, and costly process involving significant investment in research and development with no assurance of return on investment. Research is by its nature speculative and the ultimate commercial success of a product depends upon various factors, many of which are not under our control. We may not achieve significant revenue from new product investments for a number of years, if at all. Moreover, new products may not generate the operating margins that we have experienced historically.

Future disruptive new technologies could have a negative effect on our business.

We are subject to the risk of future disruptive technologies. If new vision technologies develop that are superior to ours, or are perceived to be superior by consumers, it could have a material adverse effect on the company.

The loss of a large customer could have an adverse effect on our business.

Revenue from a single customer, Panasonic, accounted for 38% and 42% of total revenue in 2017 and 2016, respectively, representing the sixth and fifth years of a ten-year licensing fee arrangement. Customers of this size may divert management’s attention from other operational matters and pull resources from other areas of the business, resulting in potential loss of revenue from other customers. In addition, the loss of a large customer could be difficult to replace with another large customer or numerous smaller customers, and the company may initially experience a sharp drop in revenue. The market leaders in these industries are able to exert purchasing power over their vendors' supply chains, and our large customers in these industries may decide to purchase fewer products from Coherix or stop purchasing from Coherix altogether.

As a large portion of our sales are through resellers, there may be end customers of our resellers that are large consumers of our products. Furthermore, there may be industry leaders that are able to exert purchasing power over their vendors' supply chains, particularly in the automotive and consumer electronics industries. Our expansion within the factory automation marketplace has reduced our reliance on the revenue from any one customer. Nevertheless, the loss of, or significant curtailment of purchases by, any one or more of our larger customers could have a material adverse effect on our operating results.

A downturn in the semiconductor, electronics, or automotive industries may adversely affect our business.

The industries we currently serve in the factory automation market are the semiconductor, electronics, and automotive industries. We are reliant on sales from these industries and therefore our business is impacted by their economic and cyclical trends, including, the level of capital spending and product design cycles. Factors that negatively impact these industries (including those that reduce levels of capital spending or prolong design cycles), could materially and adversely affect our business.

Our inability to penetrate new markets may impede our revenue growth.

We are pursuing applications in machine vision beyond the automotive, semiconductor, and electronics sectors, including expanding to the aircraft manufacturing, packaging, and other general manufacturing sectors. Our growth plan includes successful penetration of these other manufacturing markets. Therefore, our failure to generate revenue in these new markets in the amounts or within the time periods anticipated may have a material adverse impact on our revenue growth and operating results.

Information security breaches or business system disruptions may adversely affect our business.

We rely on our information technology infrastructure and management information systems to effectively run our business. We may be subject to information security breaches caused by hacking, malicious software, or acts of vandalism or terrorism. Our security measures or those of our third-party service providers may not detect or prevent such breaches. Any such compromise to our information security could result in theft of our intellectual property, a misappropriation of our cash or other assets, an interruption in our operations, the unauthorized publication of our confidential business or proprietary information, the unauthorized release of customer, vendor, or employee data, the violation of privacy or other laws, and the exposure to litigation, any of which could harm our business and operating results.

The failure of a key supplier to deliver quality product in a timely manner or our inability to obtain components for our products could adversely affect our operating results.

A significant portion of our product is manufactured by a third-party contractor located in Livonia, Michigan. We do not have a contract with this contractor. We rely on this contractor to provide quality parts and meet delivery schedules. We engage in extensive product quality programs and processes, including actively monitoring the performance of our third-party manufacturers; however, we may not detect all product quality issues through these programs and processes.

Certain components are presently sourced from a single vendor that is selected based on price and performance considerations. We do not have a contract with this vendor. In the event of a supply disruption from a single-source vendor, these components may be purchased from an alternative vendor, which may result in manufacturing delays. Certain key electronic and mechanical components that are purchased from strategic suppliers, such as processors or imagers, are fundamental to the design of Coherix products. A disruption in the supply of these key components, such as a last-time-buy announcement, natural disaster, financial bankruptcy, or other event, may require us to purchase a significant amount of inventory at unfavorable prices resulting in lower gross margins and higher risk of carrying excess inventory. An interruption in, termination of, or material change in the purchase terms of any key components could have a material adverse effect on our operating results.

We do not have agreements with our suppliers and rely on purchase order requests to obtain components for our products; the inability to obtain components for our products could adversely affect our operating results.

We rely on all of our suppliers to provide us with components through the use of purchase order requests and do not have any agreements with the suppliers of our components. If our suppliers do not continue to satisfy our purchase order requests, we may experience a disruption in the supply of components, which could have a material adverse effect on our operating results.

Our products may contain design or manufacturing defects, which could result in reduced demand, significant delays, or substantial costs.

If flaws in either the design or manufacture of our products were to occur, we could experience a rate of failure in our products that could result in significant delays in shipment and material repair or replacement costs. Our release-to-market process may not be robust enough to detect significant design flaws or software bugs. Our product quality programs and processes, including actively monitoring and evaluating the quality of our component suppliers and contract manufacturers, may not be sufficient to avoid a product failure rate that results in:

| | · | Substantial delays in shipment, |

| | · | Significant repair or replacement costs, |

| | · | Product liability claims or lawsuits, or |

| | · | Potential damage to our reputation. |

Any of these results could have a material adverse effect on our operating results.

Our failure to properly manage the distribution of our products and services could result in the loss of revenues and profits.

We utilize a direct sales force and several integration and distribution channel partners to sell our products and services. For example, we use a network of machine vision system integratorsto serve a wide customer base in automotive, aerospace, electronics and other industries. System integrators provide turnkey inspection solutions, consulting, onsite support, and customer training services to deliver innovative machine vision solutions integrating Coherix Robust3D error-proofing solutions, includingPredator3Dadhesive and sealant bead inspection.

Successfully managing the interaction of our direct and indirect sales channels to reach various potential customers for our products and services is a complex process. In addition, our reliance upon indirect selling methods may reduce visibility to demand and pricing issues. Each sales channel has distinct risks and costs, and therefore, our failure to implement the most advantageous balance in the sales model for our products and services could adversely affect our revenue and profitability.

If we fail to successfully protect our intellectual property, our competitive position and operating results could suffer.

We rely on our proprietary software technology and hardware designs, as well as the technical expertise, creativity, and knowledge of our personnel to maintain our position as a leading provider of machine vision products. Software piracy and reverse engineering, specifically from companies in Russia and Asia, may result in counterfeit products that are misrepresented in the market as Coherix products. To protect our intellectual property, we never embed the core source code in our products and we do not give out the source code, except for customer specific portions associated with joint developments, which makes copying our software difficult. We also rely on patent, trademark, copyright, and trade secret protection, as well as non-disclosure agreements with customers, suppliers, employees, and consultants as well as restricting access to our proprietary information by a combination of technical and internal security measures. These measures, however, may not be adequate to:

| | · | Protect our proprietary technology, |

| | · | Protect our patents from challenge, invalidation, or circumvention, or |

| | · | Ensure that our intellectual property will provide us with competitive advantages. |

Any of these adverse circumstances could have a material adverse effect on our operating results.

Our company may be subject to time-consuming and costly litigation.

From time to time, we may be subject to various claims and lawsuits by competitors, customers, or other parties arising in the ordinary course of business, including lawsuits charging patent infringement, or claims and lawsuits instituted by us to protect our intellectual property or for other reasons. These matters can be time-consuming, divert management’s attention and resources, and cause us to incur significant expenses, regardless of the merit of a particular lawsuit or the eventual outcome. Furthermore, the results of any of these actions may have a material adverse effect on our operating results.

Increased competition may result in decreased demand or prices for our products and services.

The machine vision market is fragmented and Coherix’s competitors are typically other vendors of machine vision systems, controllers, and components; manufacturers of image processing systems, sensors, and components; and system integrators. Any of these competitors may have greater financial and other resources than we do. Ease-of-use and product price are significant competitive factors in the factory automation marketplace. We may not be able to compete successfully in the future and our investments in research and development, sales and marketing, and support activities may be insufficient to enable us to maintain our competitive advantage. In addition, competitive pressures could lead to price erosion that could have a material adverse effect on our gross margins and operating results.

Our business could suffer if we lose the services of, or fail to attract, key personnel and additional personnel.

We are highly dependent on the management and leadership of Dwight Carson, our Chief Executive Officer and Chairman of our Board of Directors, and Doug Davison, Chief Technology Officer, as well as other members of our senior management team. Although we have many experienced and qualified senior managers, the loss of key personnel could have a material adverse effect on our company. Our continued growth and success also depends upon our ability to attract and retain skilled employees and on the ability of our officers and key employees to effectively manage the growth of our business through the implementation of appropriate management information systems and internal controls. If we have difficulty attracting and retaining good employees, any such difficulties could materially adversely affect our business.

Implementation of our joint venture strategy may not be successful, which could affect our ability to increase our revenue or profitability and result in the impairment of acquired intangible assets.

We have in the past partnered, and will in the future consider joint ventures with or acquisition of, businesses and technologies in the machine vision industry. Our business may be negatively impacted by risks related to those acquisitions. These risks include, among others:

| | · | The inability to find or close attractive acquisition opportunities, |

| | · | The diversion of management’s attention from other operational matters, |

| | · | The inability to realize expected benefits resulting from the acquisition, |

| | · | Difficulties or delays in integrating the personnel, operations, technologies, products and systems of acquired businesses, |

| | · | Disagreements with joint venture partners, |

| | · | The failure to retain key customers or employees, and |

| | · | The impairment of acquired intangible assets resulting from lower-than-expected cash flows from the acquired assets. |

Joint ventures and acquisitions are inherently risky and the inability to effectively manage these risks could have a material adverse effect on our operating results.

Global economic conditions may negatively impact our operating results.

As we have a significant business presence in other countries throughout the world, our revenue levels are impacted by global economic conditions. If global economic conditions were to deteriorate, our revenue and our ability to generate operating profits could be materially adversely affected.

Unfavorable economic condition could negatively impact our business, including the following risks:

| · | Our customers may not have sufficient cash flow or access to financing to purchase our products, |

| · | Our customers may not pay us within agreed upon terms or may default on their payments altogether, |

| · | Our vendors may be unable to fulfill their delivery obligations to us in a timely manner, |

| · | Lower demand for our products may result in charges for excess and obsolete inventory, |

| · | Lower cash flows may result in impairment charges for acquired intangible assets or goodwill, and |

| · | A decline in our stock price may make stock options a less attractive form of compensation and therefore more difficult or expensive for us to retain our employees. |

Our operating results have been materially adversely affected in the past, and could be materially adversely affected in the future, as a result of unfavorable economic conditions and reduced capital spending by manufacturers worldwide.

Financial, political, and other risks associated with international sales and operations could adversely affect our business and operating results.

In 2016, approximately 62% of our revenue was derived from customers located outside of the United States. During 2017, approximately 65% of our revenue was derived from customers located outside of the United States. We intend to continue to expand our sales and operations outside the United States and expand our presence in international markets. As a result, our business is subject to the risks inherent in international sales and operations, including, among other things:

| · | Global political developments, |

| | · | Various regulatory and statutory requirements, |

| | · | Difficulties in injecting and repatriating cash, |

| | · | Export and import restrictions, |

| | · | Transportation delays, |

| | · | Employment regulations and local labor conditions, |

| | · | Difficulties in staffing and managing foreign sales operations, |

| | · | Instability in economic or political conditions, |

| | · | Difficulties protecting intellectual property, |

| | · | Business systems connectivity issues, and |

| | · | Potentially adverse tax consequences. |

Any of these factors could have a material adverse effect on our operating results.

The status of our joint venture in China is uncertain.

In 2015, we formed a joint venture (“JV”) with Dandong Xintai Electric Company Ltd. (“Dandong Xintai”). In connection with the formation of the JV, Dandong Xintai became an investor in Coherix, Inc. and was granted a board seat pursuant to an investors’ rights agreement. When we formed the JV with Dandong Xintai, Dandong Xintai was a listed public company in China; in June 2017, Dandong Xintai was delisted by the relevant Chinese securities authority. In September 2017, the company was told by a Dandong Xintai representative that Dandong Xintai was in bankruptcy proceedings in China. Recently, the company was informed that Dandong Xintai is now in reorganization proceedings in China. The company has not been able to verify whether Dandong Xintai was in bankruptcy or is now in reorganization proceedings under applicable Chinese law.

On September 27, 2017, we delivered a certified letter to Dandong Xintai, terminating the joint venture contract, based on Dandong Xintai’s defaults under the joint venture contract. Dandong Xintai responded to the letter via e-mail on October 10, 2017 and in a formal letter that was delivered to the company on October 17, 2017, objecting to our unilateral termination of the joint venture contract. Shortly after we sent the letter terminating the JV contract, our Board approved the formation of a WFOE in Shanghai. Dandong Xintai, which has a representative on our Board, objected to this decision. Early in 2018, the Board, including the director appointed by Dandong Xintai, provided written authorization to purchase a Shanghai company and we formed a WFOE to sell our products in China. We have a limited number of employees still on the payroll of the JV while we complete the JV’s existing purchase orders. As of June 30, 2018, we also had approximately $455,619 in past due receivables to collect from the JV. Dandong Xintai believes that the establishment of the WFOE may violate the joint venture contract the company has with Dandong Xintai in China. It has indicated it believes it may have rights under the terminated contract. However, as of the date of this Offering Circular, Dandong Xintai has not taken any legal action against the company with respect to this dispute. We cannot predict whether Dandong Xintai’s reorganization, or its objections to our formation of the WFOE and our sales of the company’s products through the WFOE, will affect the company and/or our operations in China.

The trade war between the United States and China may have a negative impact on our business.

Changes in international trade duties and other aspects of international trade policy, both in the United States and abroad, could materially impact our business. For example, China announced 20% tariffs on optical instruments covering our products. With the establishment of our China WFOE in 2018, we have been shipping sensor products to fulfill customer orders in the Chinese market during 2018 tariff free. However, future shipments will be subject to tariffs of up to 20%. For example, should the tariffs remain in place, our next shipment, estimated at $500,000, would incur an additional cost of $100,000 in tariffs. Accordingly, any additional tariffs or government actions related to international trade agreements or policies has the potential to further adversely impact demand for our products, our costs, customers, suppliers and/or the US economy or certain sectors thereof and, thus, to adversely impact our businesses.

Fluctuations in foreign currency exchange rates could adversely affect our reported results, liquidity, and competitive position.

Although, the majority of our business is done in US currency, we may face exposure to foreign currency exchange rate fluctuations in the future. We estimate that approximately 3% of our sales in 2016 and 11% in 2017 were invoiced in currencies other than the US Dollar. Changes in the relative strength of the US Dollar (for example, strengthening of the value of the dollar, making our products more expensive) may have a material impact on our operating results.

Investment in technologies, products, and regions that are unprofitable could have a negative impact on our company.

For several years the company has invested heavily in the development of certain technologies and products, as well as in establishing its presence in several global regions to support the global footprints of its large customers (such as General Motors, Ford, and Fiat Chrysler Automotive). This has resulted in several consecutive years of unprofitable operations, although in 2017 the company achieved a net profit. Although the company’s overall financial performance has reached a state of profitable operations, there are no assurances that this trend will continue. Furthermore, to rapidly accelerate global sales of the company’s product lines, the company intends that some of the proceeds from this offering will be used to increase sales and marketing personnel globally, which would increase the operating expenses, and may cause the company to experience net losses.

Risks Related to the Offering and Investment

We have not paid cash dividends on Common Stock in the past and do not expect to pay dividends in the future. Any return on investment may be limited to the value of our Common Stock.

We have never paid cash dividends on our Common Stock and do not anticipate doing so in the foreseeable future. The payment of dividends on our Common Stock will depend on earnings, financial condition and other business and economic factors affecting us at such time as our board of directors may consider relevant. If we do not pay dividends, our Common Stock may be less valuable because a return on your investment will only occur if our stock price appreciates.

There is currently no trading market for our Common Stock and we cannot ensure that one will ever develop or be sustained.

There is no current market for any of our shares of stock and a market may not develop. We hope to eventually apply to list our Common Stock on the Nasdaq Capital Market (“NASDAQ”) if we raise enough money in this offering, but there is no guarantee that we will be able to do so (see “--We may not satisfy NASDAQ’s initial quotation standards and, even if we do, we may be removed from quotation in the future.”). If not quoted on NASDAQ, shares of Common Stock, when issued, may be traded on the over-the-counter market to the extent any demand exists. Even if quoted on NASDAQ, a liquid trading market may not develop. Investors should assume that they may not be able to liquidate their investment for some time, or be able to pledge their shares as collateral.

We may need to implement additional finance and accounting systems, procedures and controls as we grow our business and organization and to satisfy new reporting requirements.

We are required to comply with a variety of reporting, accounting, and other rules and regulations and those rules and requirements will become more extensive if we become a public company. Compliance with existing requirements is expensive. Further requirements may increase our costs and require additional management time and resources. We may need to implement additional finance and accounting systems, procedures and controls to satisfy our reporting requirements. If our internal controls over financial reporting are determined to be ineffective, such failure could cause investors to lose confidence in our reported financial information, negatively affect the market price of our Common Stock, subject us to regulatory investigations and penalties, and adversely impact our business and financial condition.

We have not conducted an evaluation of the effectiveness of our internal control over financial reporting and will not be required to do so until we are a public company. If we are unable to implement and maintain effective internal control over financial reporting investors may lose confidence in the accuracy and completeness of our financial reports and the market price of our Common Stock may be negatively affected.

We hope to list as a public company eventually, and at that time various accounting rules applicable to public companies will apply to us. We can make no assurances that we have the procedures in place to make sure we meet those requirements, and compliance will be a burden. If and when required, our independent registered public accounting firm is unable to express an opinion as to the effectiveness of our internal control over financial reporting, at that time, investors may lose confidence in the accuracy and completeness of our financial reports and the market price of our Common Stock could be negatively affected, and we could become subject to investigations by the stock exchange on which our securities are listed, the SEC, or other regulatory authorities, which could require additional financial and management resources.

There may be implications of being an Emerging Growth Company.

As an issuer with less than $1 billion in total annual gross revenues during our last fiscal year, we will qualify as an “emerging growth company” under the Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”). An emerging growth company may take advantage of certain reduced reporting requirements and is relieved of certain other significant requirements that are otherwise generally applicable to public companies. In particular, as an emerging growth company, even if and when we become registered with the SEC, we:

| · | Would not be required to obtain an auditor attestation on our internal control over financial reporting pursuant to the Sarbanes-Oxley Act of 2002; |

| · | Would not be required to provide a detailed narrative disclosure discussing our compensation principles, objectives and elements and analyzing how those elements fit with our principles and objectives (commonly referred to as “compensation discussion and analysis”); |

| · | Would not be required to obtain a non-binding advisory vote from our stockholders on executive compensation or golden parachute arrangements (commonly referred to as the “say-on-pay,” “say-on-frequency” and “say-on-golden-parachute” votes); |

| · | Would be exempt from certain executive compensation disclosure provisions requiring a pay-for-performance graph and CEO pay ratio disclosure; |

| · | Could present only two years of audited financial statements and only two years of related Management’s Discussion and Analysis of Financial Condition and Results of Operations; and |

| · | Would be eligible to claim longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act. |

We intend to take advantage of all of these reduced reporting requirements and exemptions, including the longer phase-in periods for the adoption of new or revised financial accounting standards under §107 of the JOBS Act. Our election to use the phase-in periods may make it difficult to compare our financial statements to those of non-emerging growth companies and other emerging growth companies that have opted out of the phase-in periods under §107 of the JOBS Act.

Under the JOBS Act, we may take advantage of the above-described reduced reporting requirements and exemptions for up to five years after our initial sale of common equity pursuant to a registration statement declared effective under the Securities Act, or such earlier time that we no longer meet the definition of an emerging growth company. Note that this offering, while a public offering, is not a sale of common equity pursuant to a registration statement, since the offering is conducted pursuant to an exemption from the registration requirements. In this regard, the JOBS Act provides that we would cease to be an “emerging growth company” if we have more than $1 billion in annual revenues, have more than $700 million in market value of our Common Stock held by non-affiliates, or issue more than $1 billion in principal amount of non-convertible debt over a three-year period.

We may not satisfy NASDAQ’s initial quotation standards and, even if we do, we may be removed from quotation in the future.

We hope to eventually apply to quote our Common Stock on NASDAQ. Our Common Stock will not commence trading on NASDAQ until a number of conditions are met, including that we have raised the minimum amount of offering proceeds necessary for us to meet the initial quotation requirements of NASDAQ. There is no guarantee that we will be able to sell a sufficient number of shares to raise the proceeds required. In addition, in order to be quoted on NASDAQ, we will be required to, among other things, file with the SEC a post qualification amendment to the Offering Statement of which this Offering Circular forms a part, and then file an SEC Form 8-A in order to register our shares under the Securities Exchange Act of 1934, as amended (the “Exchange Act”). The post qualification amendment of the Offering Statement is subject to review by the SEC, and there is no guarantee that such amendment will be qualified quickly after filing. Any delay in the qualification of the post qualification amendment may cause a delay in the initial trading of our Common Stock on NASDAQ. For all of the foregoing reasons, you may experience a delay between the closing of your purchase of our Common Stock and the commencement of exchange trading of our Common Stock, if such trading were ever to be initiated.

In the event we are able to quote our Common Stock on NASDAQ, we will be required to meet certain financial, public float, bid price and liquidity standards on an ongoing basis in order to continue the quotation of our Common Stock. If we fail to meet these continued listing requirements, our Common Stock may be subject to removal from quotation. If our Common Stock were to no longer be quoted on NASDAQ and we could not list or quote our Common Stock on another national securities exchange, we expect our securities would be quoted on an over-the-counter market. If this were to occur, our stockholders could face significant material adverse consequences, including limited availability of market quotations for our Common Stock and reduced liquidity for the trading of our securities. In addition, we could experience a decreased ability to issue additional securities and obtain additional financing in the future.

Investors in this offering are bound by the governing law and jurisdiction provision contained in the subscription agreement, which limits an investor’s ability to bring lawsuits in connection with this offering.

Investors agree to be bound by the governing law and jurisdiction provisions contained in the subscription agreement. These provisions apply to claims that may be made regarding this offering and, among other things, limit the ability of investors to seek remedies outside of the State of Michigan. As such, these provisions may limit an investor’s ability to bring a claim in a judicial forum that the investor believes is favorable for such disputes and may discourage lawsuits with respect to such claims, or investors located outside the State of Michigan may have difficulty bringing a legal claim against the company due to geographic limitations. This limitation is likely to result in increased costs, both in terms of time and money, to individual investors who wish to pursue claims against us.

You will experience future dilution as a result of future equity offerings.

We may in the future offer additional shares of our Common Stock or other securities convertible into or exchangeable for our Common Stock. Although no assurances can be given that we will consummate a financing, in the event we do, or in the event we sell shares of Common Stock or other securities convertible into shares of our Common Stock in the future, additional and substantial dilution will occur. In addition, investors purchasing shares or other securities in the future could have rights superior to investors in this offering. Subsequent offerings at a lower price (a “down round”) could result in additional dilution.

USE OF PROCEEDS

The company estimates that, at a per share price of $6.00, the net proceeds from the sale of 2,500,000 shares in this offering will be approximately $14,500,000, after deducting the estimated offering expenses of approximately $500,000 (including marketing, other legal and accounting professional fees, technology fees associated with hosting our offering online and other expenses).

The following table sets forth a breakdown of our estimated use of our net proceeds as we currently expect to use them, assuming the sale of, respectively, 25%, 50%, 75% and 100% of the maximum number of shares offered for sale in this offering.

| | | 100% Shares | | | % | | | 75% Shares | | | % | | | 50% Shares | | | % | | | 25% Shares | | | % | |

| Assumed percentage of shares sold | | Sold | | | Total | | | Sold | | | Total | | | Sold | | | Total | | | Sold | | | Total | |

| Gross Proceeds | | $ | 15,000,000 | | | | | | | $ | 11,250,000 | | | | | | | $ | 7,500,000 | | | | | | | $ | 3,750,000 | | | | | |

| Offering Expenses | | $ | 500,000 | | | | 3% | | | $ | 375,000 | | | | 3% | | | $ | 315,000 | | | | 4% | | | $ | 315,000 | | | | 8% | |

| Global Sales and Marketing | | $ | 5,000,000 | | | | 33% | | | $ | 5,000,000 | | | | 44% | | | $ | 2,500,000 | | | | 33% | | | $ | 1,000,000 | | | | 27% | |

| Debt Reduction | | $ | 5,000,000 | | | | 33% | | | $ | 3,750,000 | | | | 33% | | | $ | 2,500,000 | | | | 33% | | | $ | 2,400,000 | | | | 64% | |

| Product Development | | $ | 2,000,000 | | | | 13% | | | $ | 1,000,000 | | | | 9% | | | $ | 500,000 | | | | 7% | | | $ | 0 | | | | 0% | |

| General Administration | | $ | 1,000,000 | | | | 7% | | | $ | 750,000 | | | | 7% | | | $ | 375,000 | | | | 5% | | | $ | 0 | | | | 0% | |

| Working Capital & All Other General Corporate Purposes | | $ | 1,500,000 | | | | 10% | | | $ | 375,000 | | | | 3% | | | $ | 1,310,000 | | | | 17% | | | $ | 35,000 | | | | 1% | |

| Total Use of Proceeds | | $ | 15,000,000 | | | | 100% | | | $ | 11,250,000 | | | | 100% | | | $ | 7,500,000 | | | | 100% | | | $ | 3,750,000 | | | | 100% | |

The expected use of net proceeds from this offering represents our intentions based on our current plans and business conditions, which could change in the future as our plans and business conditions evolve and change. The amounts and timing of our actual expenditures, specifically with respect to working capital, may vary significantly depending on numerous factors.As a result, the company reserves the right to change the above use of proceeds if management believes it is in the best interests of the company.

In the event we do not sell all of the shares being offered, we may seek additional financing from other sources to support the intended use of proceeds indicated above. If we secure additional equity funding, investors in this offering would be diluted.

Restructuring and repayment of debt

The company is currently seeking a $15 million credit facility for working capital, general corporate purposes, and debt restructuring. We are in the due diligence stage of this negotiation and there is no guarantee the company will be successful in securing the credit facility, and in all events, there can be no assurance that additional financing would be available to use when wanted or needed and, if available, on terms acceptable to us. See “Management’s Discussion and Analysis of Financial Condition and Results of Operations – Liquidity and Capital Resources – Line of Credit.”

We plan to use certain of the net proceeds of this offering to repay the following debt:

| · | $1,497,087 in principal amount of convertible debentures owed to investors and service providers who accepted notes in lieu of cash payments. |

| · | $1,036,657, representing 50% of the principal and interest owed to Volvo Group under a promissory note. |

| · | $1,616,293 owed to employees and consultants under the Top Hat Deferred Compensation Plan. |

| · | $849,963 in accrued and unpaid dividends to the former holders of shares of our preferred stock. |

Dilution

Dilution means a reduction in value, control or earnings of the shares the investor owns.

Immediate Dilution

An early-stage company typically sells its shares (or grants options over its shares) to its founders and early employees at a very low cash cost, because they are, in effect, putting their “sweat equity” into the company. Coherix has a long standing and broadly based option grant program with all full time team members participating.

When the company seeks cash investments from outside investors, like you, the new investors typically pay a much larger sum for their shares than the founders or earlier investors, which means that the cash value of your stake is diluted because all the shares are worth the same amount, and you paid more than earlier investors for your shares.

The following table demonstrates the dilution new investors will experience upon investment in the company. The table uses the company’s net tangible book value deficit as of June 30, 2018 of ($18,988,215), which is derived from the net equity of the company per the unaudited interim financial statements reduced by the value of intangible assets as presented in this Offering Circular.

The table presents four scenarios: the sale in this offering of 625,000 shares (representing proceeds of $3,750,000); 1,250,000 shares (representing proceeds of $7,500,000), 1,875,000 shares (representing proceeds of $11,250,000) and 2,500,000 shares (representing proceeds of $15,000,000).

| | | Assuming the sale of offered shares | |

| | | 25% sold | | | 50% sold | | | 75% sold | | | maximum | |

| SHARES OFFERED | | 625,000 | | | 1,250,000 | | | 1,875,000 | | | 2,500,000 | |

| Offering price per share | | $ | 6.00 | | | $ | 6.00 | | | $ | 6.00 | | | $ | 6.00 | |

| | | | | | | | | | | | | | | | | |

| Offering proceeds before transaction expenses | | $ | 3,750,000 | | | $ | 7,500,000 | | | $ | 11,250,000 | | | $ | 15,000,000 | |

| Offering expenses | | $ | 315,000 | | | $ | 315,000 | | | $ | 375,000 | | | $ | 500,000 | |

| Net proceeds from offering | | $ | 3,435,000 | | | $ | 7,185,000 | | | $ | 10,875,000 | | | $ | 14,500,000 | |

| | | | | | | | | | | | | | | | | |

| Net tangible book value per share before offering | | $ | (1.45 | ) | | $ | (1.45 | ) | | $ | (1.45 | ) | | $ | (1.45 | ) |

| | | | | | | | | | | | | | | | | |

| Shares issued before the offering | | | 13,091,200 | | | | 13,091,200 | | | | 13,091,200 | | | | 13,091,200 | |

| Shares outstanding after the offering | | | 13,716,200 | | | | 14,341,200 | | | | 14,966,200 | | | | 15,591,200 | |

| | | | | | | | | | | | | | | | | |

| Net tangible book value per share after offering | | $ | (1.13 | ) | | $ | (0.82 | ) | | $ | (0.54 | ) | | $ | (0.29 | ) |

| | | | | | | | | | | | | | | | | |

| Net increase in net tangible book value per share to original stockholders | | $ | 0.32 | | | $ | 0.63 | | | $ | 0.91 | | | $ | 1.16 | |

| Decrease in investment to new stockholders | | $ | 7.13 | | | $ | 6.82 | | | $ | 6.54 | | | $ | 6.29 | |

| Dilution to new stockholders (%) | | | 119% | | | | 114% | | | | 109% | | | | 105% | |

The tangible net book value in the above table does not reflect the possible exercise of all options (1,314,140) and warrants (1,171,046) outstanding as of June 30, 2018. The options and warrants have exercise prices that range from $0.25 to $5.00 and include a cashless exercise feature. If all of the outstanding options and warrants were to be exercised, such exercise would provide $3,221,019 of proceeds and result in the issuance of 2,485,186 additional shares of Common Stock. The table above also excludes 1,767,088 shares related to options available for future grants under our existing stock option plan.

Future Dilution

Another important way of looking at dilution is the dilution that happens due to future actions by the company. The investor’s stake in a company could be diluted due to the company issuing additional shares. In other words, when the company issues more shares, the percentage of the company that you own will go down, even though the value of the company may go up. You will own a smaller piece of a larger company. This increase in number of shares outstanding could result from a stock offering (such as an initial public offering, a venture capital round, angel investment), employees exercising stock options, or by conversion of certain instruments (e.g. convertible bonds, preferred shares or warrants) into stock.

If the company decides to issue more shares, an investor could experience value dilution, with each share being worth less than before, and control dilution, with the total percentage an investor owns being less than before. There may also be earnings dilution, with a reduction in the amount earned per share (though this typically occurs only if the company offers dividends, and most early stage companies are unlikely to offer dividends, preferring to invest any earnings into the company).

The type of dilution that hurts early-stage investors most occurs when the company sells more shares in a “down round,” meaning at a lower valuation than in earlier offerings.

An example of how this might occur is as follows (numbers are for illustrative purposes only):

| · | In June 2017 Jane invests $20,000 for shares that represent 2% of a company valued at $1 million. |

| | · | In December the company is doing very well and sells $5 million in shares to venture capitalists on a valuation (before the new investment) of $10 million. Jane now owns only 1.3% of the company but her stake is worth $200,000. |

| | · | June 2018 the company has run into serious problems and in order to stay afloat it raises $1 million at a valuation of only $2 million (the “down round”). Jane now owns only 0.89% of the company and her stake is worth only $26,660. |

This type of dilution might also happen upon conversion of convertible notes into shares. Typically, the terms of convertible notes issued by early-stage companies provide that in the event of another round of financing, the holders of the convertible notes get to convert their notes into equity at a “discount” to the price paid by the new investors, i.e., they get more shares than the new investors would for the same price. Additionally, convertible notes may have a “price cap” on the conversion price, which effectively acts as a share price ceiling. Either way, the holders of the convertible notes get more shares for their money than new investors. In the event that the financing is a “down round”, the holders of the convertible notes will dilute existing equity holders, and even more than the new investors do, because they get more shares for their money. Investors should pay careful attention to the amount of convertible notes that the company has issued (and may issue in the future, and the terms of those notes.

If you are making an investment expecting to own a certain percentage of the company or expecting each share to hold a certain amount of value, it’s important to realize how the value of those shares can decrease by actions taken by the company. Dilution can make drastic changes to the value of each share, ownership percentage, voting control, and earnings per share.

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS

Financial Results

You should read the following discussion and analysis of our financial condition and results of our operations together with our consolidated financial statements and the notes thereto appearing elsewhere in this Offering Circular. This discussion contains forward-looking statements reflecting our current expectations, whose actual outcomes involve risks and uncertainties. Actual results and the timing of events may differ materially from those stated in or implied by these forward-looking statements due to a number of factors, including those discussed in the sections entitled “Risk Factors,” “Statement Regarding Forward-Looking Statements,” and elsewhere in this Offering Circular.

Overview

Since our incorporation in 2003, we have been engaged primarily in the design and manufacturing of 3D vision products for the automotive and semiconductor industries. Among the products offered, the company produces digital holographic imaging and 3D imaging technologies and related equipment that provide “on-the-fly” measurements within very tight tolerances. Our prospects must be considered in light of the uncertainties, risks, expenses, and difficulties frequently encountered by companies in their early stages of operations. We expect to incur additional net expenses over the next several years as we continue to maintain and expand our existing operations. The amount of future losses and when, if ever, we will achieve sustained profitability are uncertain.

Results of Operations