| Michael Murphy | |

| 1 312 265 9605 | |

| mmurphy@thediscoverygroup.com |

April 8, 2013

The Board of Directors

Anaren, Inc.

6635 Kirkville Road

East Syracuse, NY 13057

Dear Directors:

As you know, Discovery Group is a long-term investor in Anaren. We manage a fund that owns approximately 6% of the Company. Discovery has been an investor since mid-2011 and we have met on several occasions with management. However, the Board has refused our request to meet with non-executive Directors to discuss important topics related to shareholder value, and so we hereby present our current recommendations in writing.

After conducting significant industry research, we have come to believe that there are multiple parties that have a keen interest in acquiring Anaren. Unfortunately, we also believe that the Anaren directors have failed to fulfill their duty to shareholders by translating that high degree of strategic interest into an improvement in shareholder value through the vigorous pursuit of a sale of the Company at a substantial premium.

Therefore, as a large, long-term shareholder with an interest in preserving and maximizing the value of capital invested by all Anaren shareholders, Discovery respectfully requests that the Board immediately engage an investment bank to solicit offers from the multiple parties interested in acquiring the Company.

Public Market Undervaluation

Discovery has a long history of research and investment in the defense, electronics, and communications industries. We invested in Anaren because of the Company’s excellent products, strong competitive position, and talented management team. Discovery believes that Anaren is a valuable business, but one that the public market prices at a discount to its inherent value. This is common among micro-cap companies for which small float, limited trading volume, and the resulting lack of research lead to low institutional interest and a persistent under-appreciation in the market.

Yet in Anaren’s case, the discount to true inherent value is likely magnified due to what we believe is a perception in the market that you, the Anaren Board, are inclined to keep Anaren independent and that you have therefore adopted corporate governance provisions which entrench the status quo.

191 N. Wacker Drive, Suite 1685, Chicago, IL 60606

Board of Directors

April 8, 2013

Page 2

Interested Acquirers

We believe that multiple parties are interested in acquiring Anaren at a significant premium to the current stock price. Over time, Discovery has contacted enterprises that, based on our knowledge and research, have the strategic interest and financial wherewithal to acquire Anaren. We found that many parties believe that consolidation in the industry will continue and that Anaren is a unique asset and a valuable target. However, we believe that firms contacting Anaren over the past 18 months have come away with an understanding that the Company is not interested in serious discussions about a business combination. It appears that Anaren has dismissed the opportunity to genuinely engage with various qualified acquirers, thereby failing to translate this high level of strategic interest into a significant improvement in shareholder value.

High Potential Value

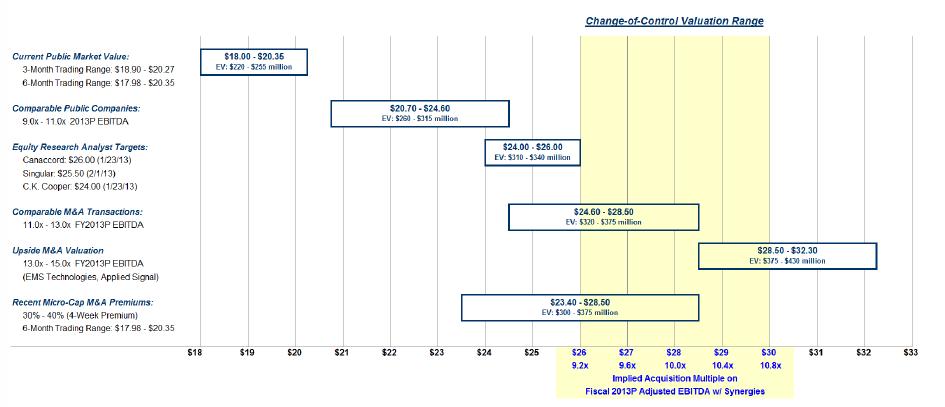

The opportunity cost of the Board’s decision not to pursue a transaction is in our view significant. To quantify this foregone value, consider the detailed valuation analysis Discovery has performed on Anaren.

As shown in the table above, we believe Anaren would likely be valued by a strategic buyer at roughly 12x to 14x 2013 projected EBITDA based on comparable M&A transactions in the defense, electronics, and communications industries. Furthermore, this change-of-control valuation range translates to an acquisition cost of only 9x to 11x adjusted EBITDA after including a conservative assumption for synergies.

Board of Directors

April 8, 2013

Page 3

In summary, we believe that Anaren will continue to be underappreciated in the market at a value near the current stock price, while a sale to a strategic buyer could reasonably achieve a value in the $26 to $30 range, or a 40%+ premium to the current stock price.

Entrenched Board

Compounding the Board’s failure to pursue this increased value are various defensive mechanisms adopted by it that largely preclude an aggressive acquirer from making an offer directly to shareholders. The Company instituted a poison pill in 2011, effectively preventing any party from circumventing the Board through a premium tender offer made directly to shareholders. Furthermore, Anaren’s Directors are elected to staggered three-year terms, making the coupling of such a tender offer with the replacement of existing Board members with new directors amenable to the offer at least a two-year process, and feasible only in theory.

Perhaps this entrenchment is what makes the Board complacent, and has led to the Directors’ conclusion that it is better to remain independent rather than pursue a sale in a competitive auction to capture a premium for shareholders.

Unlock Value Now

Discovery believes that the time has arrived for the Anaren Board to capture the potential increase in value that exists for all shareholders through a sale process.

As you know, we discussed the merits of a sale in prior years. We were told by CEO Larry Sala that the timing was inappropriate due to weak revenue performance in the Company’s wireless business and that therefore the pursuit of a sale would not elicit strong value for shareholders. Over the past year, the wireless segment has grown, profits have improved, and prospects for the business are very strong. The status of the wireless business can no longer be used as an excuse not to pursue a sale.

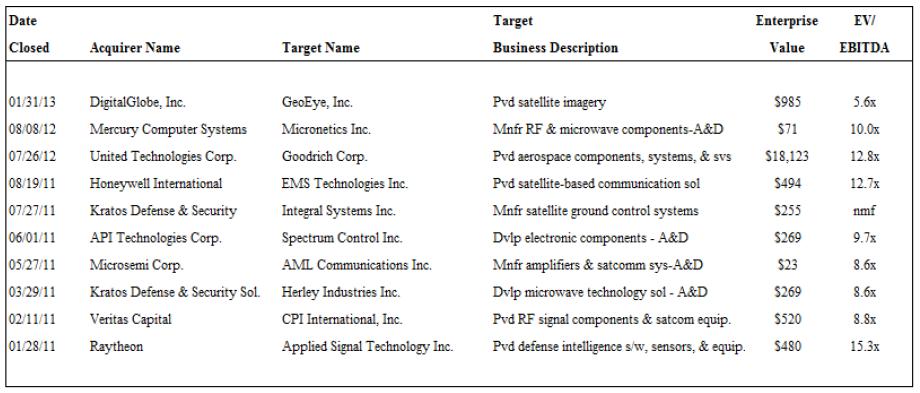

Meanwhile, the M&A market for high quality companies like Anaren is very strong. Consider the table of acquisitions of publicly traded defense, electronics, and communications companies since the beginning of 2011 that is set forth below. Consolidation continues at a steady pace, and Anaren stands out as a high quality target.

Board of Directors

April 8, 2013

Page 4

While there are macro concerns regarding potential weakness in the overall defense industry, acquirers are still seeking solid, profitable businesses to fuel growth. Over just the last 12 months, Raytheon acquired three companies (including Poseidon), General Dynamics bought six companies (including IP Wireless), Boeing bought three companies, and Honeywell acquired four.

Anaren’s solid defense business and impressive commercial wireless segment are attractive to many large consolidators facing softness in their existing business.

Alternatives to a Sale

Regarding other alternatives, we applaud the Board’s repurchase of shares as a prudent use of capital given the market’s undervaluation of the Company. Alone, however, repurchases only support the current undervalued public stock price. Any significant acquisition by Anaren would clearly not be prudent to pursue given the high valuation for quality companies in the industry. Any attractive business would most likely be priced at a multiple higher than Anaren’s, be destructive to shareholder value, and present unnecessary risk. And finally - as mentioned earlier - the status quo will likely result in continued improper pricing and undervaluation of Anaren in the public market.

Board of Directors

April 8, 2013

Page 5

Conclusion

Discovery believes that Anaren is a well run company that is undervalued in the public market. It is our strong opinion that the Company will remain mispriced given its current size and the Board’s apparent belief that it should not be “for sale” at this time. Meanwhile, our industry research suggests that there are multiple interested acquirers that would pay a significant premium to Anaren’s shareholders if they had a chance to participate in an organized sale process. To remedy the situation, Discovery strongly recommends that Anaren engage an industry-experienced investment bank to orchestrate a competitive sale process and solicit bids for the Company.

The outcome of a competitive sale process could produce a price higher or lower than the value range suggested by our experience and analysis. Regardless, we feel strongly that it will provide an outcome that is superior to any other alternative, especially if each alternative is objectively risk-adjusted.

Absent the commencement of a proactive sale process, Discovery will continue to withhold support from current Directors. Furthermore, we intend to continue the pursuit of improvement in shareholder value for all stockholders using all of the tools at our disposal.

Sincerely,

Michael R. Murphy

Managing Partner