QuickLinks -- Click here to rapidly navigate through this document

As filed with the Securities and Exchange Commission on March 25, 2005

Registration No. 333-122322

SECURITIES AND EXCHANGE COMMISSION

WASHINGTON, D.C. 20549

AMENDMENT NO. 2 TO

FORM S-1

REGISTRATION STATEMENT

UNDER

THE SECURITIES ACT OF 1933

NEW SKIES SATELLITES HOLDINGS LTD.

(Exact name of Registrant as specified in its charter)

| Bermuda | 4899 | 98-0439657 | ||

| (State or other jurisdiction of incorporation or organization) | (Primary Standard Industrial Classification Code Number) | (I.R.S. Employer Identification Number) |

Canon's Court

22 Victoria Street

Hamilton HM12

Bermuda

(441) 295-1433

(Address, including zip code, and telephone number, including area code,

of registrant's principal executive offices)

CT Corporation System

111 Eighth Avenue

New York, NY 10011

(212) 894-8400

(Name, address, including zip code, and telephone number, including area code, of agent for service)

With copies to:

| Risë B. Norman, Esq. Simpson Thacher & Bartlett LLP 425 Lexington Avenue New York, New York 10017 (212) 455-2000 | John A. Tripodoro, Esq. Cahill Gordon & ReindelLLP 80 Pine Street New York, New York 10005 (212) 701-3000 |

Approximate date of commencement of proposed sale to the public: As soon as practicable after this Registration Statement becomes effective.

If any of the securities being registered on this form are to be offered on a delayed or continuous basis pursuant to Rule 415 under the Securities Act of 1933, check the following box: o

If this form is filed to register additional securities for an offering pursuant to Rule 462(b) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If this form is a post-effective amendment filed pursuant to Rule 462(c) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering. o

If this form is a post-effective amendment filed pursuant to Rule 462(d) under the Securities Act, check the following box and list the Securities Act registration statement number of the earlier effective registration statement for the same offering: o

If delivery of the prospectus is expected to be made pursuant to Rule 434, please check the following box. o

CALCULATION OF REGISTRATION FEE

| TITLE OF EACH CLASS OF SECURITIES TO BE REGISTERED | PROPOSED MAXIMUM AGGREGATE OFFERING PRICE(1) | AMOUNT OF REGISTRATION FEE(2) | ||||

|---|---|---|---|---|---|---|

| Common Stock, par value $0.01 per share | $ | 350,000,000 | $ | 41,195 | ||

- (1)

- Estimated solely for the purpose of calculating the registration fee under Rule 457(o) of the Securities Act.

- (2)

- Previously paid.

The Registrant hereby amends this Registration Statement on such date or dates as may be necessary to delay its effective date until the Registrant shall file a further amendment which specifically states that this Registration Statement shall thereafter become effective in accordance with Section 8(a) of the Securities Act of 1933, as amended, or until this Registration Statement shall become effective on such date as the Commission, acting pursuant to said Section 8(a), may determine.

Subject to Completion. Dated March 25, 2005.

The information in this preliminary prospectus is not complete and may be changed. We may not sell these securities until the registration statement filed with the Securities and Exchange Commission is effective. This preliminary prospectus is not an offer to sell these securities and it is not soliciting an offer to buy these securities in any state or jurisdiction where the offer or sale is not permitted.

PROSPECTUS

Shares

Common Stock

This is an initial public offering of shares of common stock of New Skies Satellites Holdings Ltd. All of the shares of common stock are being sold by us. We intend to use approximately $130.8 million of our net proceeds from the sale of the shares being sold in this offering to repay outstanding indebtedness under our subsidiary's senior secured credit facilities and approximately $99.5 million to pay a dividend to existing shareholders.

Prior to this offering, there has been no public market for the common stock. It is currently estimated that the initial public offering price per share will be between $ and $ . We intend to apply for listing of the common stock on the New York Stock Exchange under the symbol " ".

See "Risk Factors" on page 17 to read about factors you should consider before buying shares of our common stock.

Neither the Securities and Exchange Commission nor any other regulatory body has approved or disapproved of these securities or passed upon the accuracy or adequacy of this prospectus. Any representation to the contrary is a criminal offense.

| | Per Share | Total | ||||

|---|---|---|---|---|---|---|

| Initial public offering price | $ | $ | ||||

| Underwriting discount | $ | $ | ||||

| Proceeds, before expenses, to us | $ | $ | ||||

To the extent that the underwriters sell more than shares of common stock, the underwriters have the option to purchase up to an additional shares from us at the initial public offering price less the underwriting discount. We intend to use the net proceeds from any shares sold pursuant to the underwriters' option to pay an additional dividend to existing shareholders.

The underwriters expect to deliver the shares against payment on , 2005.

| Goldman, Sachs & Co. | Lehman Brothers | |

| UBS Investment Bank |

Deutsche Bank Securities |

Banc of America Securities LLC |

Wachovia Securities |

Prospectus dated , 2005.

| | Page | |

|---|---|---|

| Summary | 1 | |

| Risk Factors | 17 | |

| Special Note Regarding Forward-Looking Statements | 37 | |

| Use of Proceeds | 38 | |

| Dividend Policy and Restrictions | 39 | |

| Capitalization | 53 | |

| Dilution | 54 | |

| Unaudited Pro Forma Condensed Consolidated Financial Information | 55 | |

| Selected Consolidated Historical Financial Data | 60 | |

| Management's Discussion and Analysis of Financial Condition and Results of Operations | 62 | |

| Industry | 87 | |

| Business | 90 | |

| Management | 114 | |

| Principal Shareholders | 121 | |

| The Transactions | 122 | |

| Certain Relationships and Related Party Transactions | 124 | |

| Description of Indebtedness | 126 | |

| Description of Capital Stock | 133 | |

| Shares Eligible for Future Sale | 140 | |

| Material United States Federal Income Tax Consequences | 142 | |

| Underwriting | 145 | |

| Industry and Market Data | 149 | |

| Legal Matters | 149 | |

| Independent Registered Public Accounting Firm | 149 | |

| Where You Can Find Additional Information | 149 | |

| Index to Consolidated Financial Statements | F-1 |

This prospectus does not constitute an offer to sell, or a solicitation of an offer to buy, any securities offered hereby in any jurisdiction where, or to any person to whom, it is unlawful to make such offer or solicitation. The information contained in this prospectus speaks only as of the date of this prospectus unless the information specifically indicates that another date applies. No dealer, salesperson or other person has been authorized to give any information or to make any representations other than those contained in this prospectus in connection with the offer contained herein and, if given or made, such information or representations must not be relied upon as having been authorized by us. Neither the delivery of this prospectus nor any sales made hereunder shall under any circumstances create an implication that there has been no change in our affairs or that of our subsidiaries since the date hereof.

We have been designated by the Bermuda Monetary Authority as a non-resident for Bermuda exchange control purposes. This designation allows us to engage in transactions in currencies other than the Bermuda dollar, and there are no restrictions on our ability to transfer funds, other than funds denominated in Bermuda dollars, in and out of Bermuda or to pay dividends to United States residents who are holders of our common shares.

i

We expect the Bermuda Monetary Authority to give its consent for the issue and free transferability of all of the shares of common stock that are the subject of this offering to and between non-residents of Bermuda for exchange control purposes. Approvals or permissions given by the Bermuda Monetary Authority do not constitute a guarantee by the Bermuda Monetary Authority as to our performance or our creditworthiness. Accordingly, in giving such consent or permissions, the Bermuda Monetary Authority shall not be liable for the financial soundness, performance or default of our business or for the correctness of any opinions or statements expressed in this prospectus. In some cases, issuances and transfers of shares of common stock involving persons deemed resident in Bermuda for exchange control purposes require the specific consent of the Bermuda Monetary Authority.

This prospectus will be filed with the Registrar of Companies in Bermuda pursuant to Part III of the Companies Act. In accepting this prospectus for filing, the Registrar of Companies in Bermuda shall not be liable for the financial soundness, performance or default of our business or for the correctness of any opinions or statements expressed in this prospectus.

In accordance with Bermuda law, share certificates are generally issued only in the names of companies, partnerships or individuals. In the case of a shareholder acting in a special capacity, such as a trustee, certificates may, at the request of the shareholder, record the capacity in which the shareholder is acting. Notwithstanding the recording of any special capacity, we are not bound to investigate or see to the execution of any such trust. We will take no notice of any trust applicable to any of our shares, whether or not we have been notified of such trust.

The shares may not be offered in The Netherlands, directly or indirectly, whether as part of their initial distribution or as part of any re-offering at any time thereafter, other than to individuals or legal entities who or which trade or invest in securities in the conduct of their profession or business within the meaning of section 2 of the exemption regulation pursuant to the Securities Market Supervision Act of The Netherlands 1995 (Vrijstellingsregeling Wet toezicht effectenverkeer 1995), which includes banks, securities firms, insurance companies, pension funds, investment institutions, other institutional investors, finance companies and treasury departments of large commercial enterprises, which are regularly active in the financial markets in a professional manner.

The NEW SKIES SATELLITES & DESIGN®, NEWSKIES® and IPSYS® registered trademarks and other trade names and service marks of New Skies mentioned in this prospectus are the property of, and are used with the permission of, New Skies and its subsidiaries.

ii

The following summary contains basic information about us and our common stock and highlights information appearing elsewhere in this prospectus. This summary is not complete and does not contain all of the information that you should consider before deciding to invest in our common stock. For a more complete understanding of us and our common stock, we encourage you to read this entire document and the documents to which we have referred you. This prospectus contains forward-looking statements, which involve risks and uncertainties. Our actual results could differ materially from those anticipated in these forward-looking statements as a result of certain factors, including those set forth in "Risk Factors" and elsewhere in this prospectus.

The Issuer is a recently-formed Bermuda holding company which does not have any independent external operations other than through the indirect ownership of the New Skies Satellites businesses. In this prospectus, the term "the Issuer" refers to New Skies Satellites Holdings Ltd., a Bermuda company, and not its subsidiaries, and the terms "we," "our" and "us" refer to the Issuer and its subsidiaries on a consolidated basis. Our subsidiaries include New Skies Satellites B.V. (formerly known as Munaro Holding B.V.) and its subsidiaries.

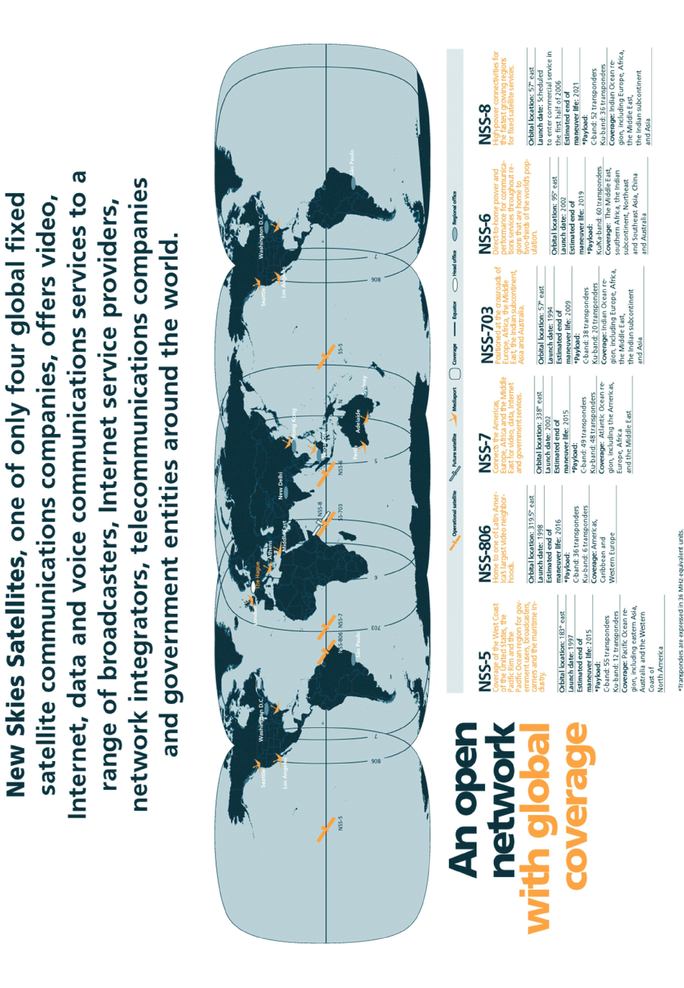

We are a satellite communications company with global operations and service coverage. We operate a network of five fixed satellite services ("FSS") satellites located at different orbital positions above the earth. Our customers can access one or more of our satellites from almost any point around the world using either our global network of ground-based facilities or their own ground-based facilities. At December 31, 2004, we had the youngest of the four global fleets in the FSS industry, based on the average number of years the satellites in each of the global fleets had been in service. We have consistently maintained one of the highest transponder availability rates in the FSS industry. For the year ended December 31, 2004, our availability rate was 99.9999%, based on the total number of hours the transponders in our fleet were available to provide service as compared to the total number of transponder-hours during the year.

Our technically advanced satellite fleet has substantial capacity focused on high growth markets, including India, Africa, the Middle East and Asia. NSS-6 and NSS-7 are among the most powerful and flexible satellites in the FSS industry and enable us to provide highly reliable, high quality services to our customers.

With the launches of NSS-6 and NSS-7 in 2002, we expanded our total transponder capacity available for sale by approximately 67%. Upon the entry into commercial service of NSS-8, which we anticipate will occur in the first half of 2006, we will further expand our available capacity by 28%. We believe that this incremental transponder capacity will enable us to generate additional revenues without significantly increasing our fixed costs, thereby improving our operating margins. The launches of the two satellites, NSS-6 and NSS-7, and the anticipated launch of NSS-8, represent the completion of our committed satellite procurement program initiated in 1999 and, consequently, we anticipate that our future revenues will generate significant cash flow to pay dividends in accordance with our dividend policy and to finance payments on our subsidiary's debt.

On November 2, 2004, investment funds affiliated with The Blackstone Group (the "investment funds") indirectly acquired substantially all of the assets, and assumed substantially all of the liabilities, of New Skies Satellites N.V. for an aggregate purchase price of approximately $982.8 million, including direct acquisition costs. See "—The Transactions."

Throughout our six-year history, we have consistently demonstrated our ability to achieve strong financial performance, increasing our revenues through organic growth. For the year ended December 31, 2004, we generated revenues of $210.7 million.

1

We primarily earn our revenues by providing capacity for satellite communications and ground-based services to our customers for contracted periods varying from less than one year to 15 years. Our base of over 200 customers includes established telecommunications carriers, leading broadcasting and video companies, governmental entities and fast-growing smaller companies from around the globe.

Our customers use the services we provide for a variety of applications, including data services, such as corporate and governmental data networks; video services, including cable and broadcast television distribution and contribution services and direct-to-home video ("DTH") services; Internet-related services; and voice services.

Data services Our satellites are used to create high-bandwidth private data networks for governments and businesses around the world. Many of these networks use relatively small antennas known as VSATs (very small aperture terminals) to connect geographically dispersed sites into a dedicated, interconnected communications network.

Video services We currently broadcast more than 400 channels of entertainment and news programming to cable networks, broadcast affiliates and consumers' homes around the world. Our video services can be grouped into two types:

- •

- Video distribution—We are a leading provider of satellite capacity for the distribution of international, regional and national television and cable programming to markets around the world, such as Latin America, India and Africa, both to ground-based cable and broadcasting systems and direct to the homes of multi-channel video subscribers; and

- •

- Video contribution—Broadcasters and news programmers who require a reliable transmission link use our satellites to transmit regular television contribution feeds as well as special events, such as the Olympics and fast-breaking news stories, back to their video production facilities. Depending upon their needs, broadcasters and news programmers can obtain our services on a full-time or an occasional use basis.

Internet-related services We offer telecommunications companies, service providers, network integrators, Internet service providers and other resellers high-speed connections directly to the Internet backbone. Our Internet-related service offerings, which we have branded IPsys, include one-way and two-way satellite-based links between an Internet service provider's points of presence or a customer's premises and the global Internet backbone.

Voice services We also provide satellite capacity for voice applications. Historically, we provided most of our voice services to major post, telephone and telegraph administrations, or PTTs. More recently, we have begun to market voice services to governmental users and to newly-authorized mobile telephone, local and long distance service providers in countries undergoing telephony deregulation or where there is a lack of ground-based infrastructure to support voice services.

Our business is characterized by the following key strengths:

Stable and predictable cash flow

We have a history of strong cash flow generation. Because we have nearly completed our committed capital investment program, anticipate only limited working capital requirements going forward and have a relatively fixed cost structure, we believe we are well positioned to generate strong cash flow to pay dividends to our shareholders and to finance payments on our debt.

2

Young satellite fleet

At December 31, 2004, we had the youngest global fleet in the FSS industry, based on the average number of years the satellites in each of the four global fleets had been in service. We believe the technical characteristics of the satellites we have built and launched to date make our capacity attractive to our customers. These satellites' high-powered transponders enable customers to improve the reliability of their service and transmit larger amounts of information within a given amount of satellite transponder capacity and make it possible for them to use smaller and less expensive ground station antennas. Due to the youth of our fleet, other than NSS-8 (which is currently under construction), we do not anticipate that we will need to begin procuring any replacement satellites until approximately 2010.

Strong revenue visibility and diversity

At December 31, 2004, we had a contractual backlog for future services of $517.0 million, which we will recognize as revenue when we actually perform the services. We believe that the size and average duration of our contractual backlog will help ensure that our revenues will remain strong and predictable going forward. $166.9 million of our backlog is contracted for receipt in the 12-month period ending December 31, 2005. This allows us to enter 2005, like each of the years since our inception, with a substantial portion of our anticipated revenues already secured.

High-quality customer base

Since our inception, we have continued to provide services to major telecommunications and broadcasting companies, such as British Telecommunications plc, Embratel and France Telecom. We have also expanded our customer base to include newer entrants to the telecommunications marketplace, particularly in markets undergoing deregulation, and in regions where strong GDP growth is driving demand for new services or where ground-based infrastructure is underdeveloped. Our satellites are used by major broadcasters, Fortune 100 business users and by governments and governmental agencies.

Substantial capacity focused on high growth markets

Communications satellites can be used to provide services anywhere within the geographic areas they cover with their signals. We have created a satellite system with substantial capacity focused on the relatively higher-growth regions of India, Africa, the Middle East and Asia. According to Euroconsult 2004, worldwide unit demand for satellite transponders is projected to grow at an estimated compounded annual growth rate of 4% from 2004 to 2009, while over the same period unit demand for satellite transponders is projected to grow at a compounded annual growth rate of 10% in the Indian subcontinent, 7% in the Middle East and Africa and 4% in Asia-Pacific.

Well positioned for industry consolidation

We believe our entrepreneurial management team, rights to expansion orbital locations, scale and scope place us in a strong position from which to capitalize upon strategic developments in the FSS industry.

Experienced, entrepreneurial management team

Our senior management team collectively has more than 70 years of experience in the FSS industry. In the years since our creation, they have demonstrated their entrepreneurial orientation, ability to build a global business and deliver strong operational and financial performance, even in the face of difficult market conditions.

3

Our goal is to be a commercially agile, technically excellent and profitable provider of global satellite services that meet our customers' requirements for the transmission of their data, video, Internet-related and voice services. Our strategy includes the following initiatives:

Maximizing cash flow

We are focused on disciplined capital expenditures, revenue growth and improving our operating margins in order to maximize cash flow available for dividend payments and to finance payments on our debt.

Emphasizing sales of "space-segment only" services

We focus our sales and marketing efforts principally on selling services that involve solely the provision of satellite transponder capacity. Such "space-segment only" services are our core business, representing approximately 80% of our revenues for the year ended December 31, 2004. Space-segment only services require no meaningful increase in operating expenses, as they require minimal incremental operational support and facilities. Customers of our space-segment only services are more likely to enter into long-term contracts, often for large amounts of satellite capacity, and generally are well-established.

Expanding our presence in core markets

The target markets for the sale of space-segment only services are video distribution service providers, government users and telecommunications services providers. We intend to further develop our position in the video services market by continuing to expand our presence in India and capitalizing on new opportunities in Asian markets. We intend to further develop our government services business by capitalizing on the technical strengths of our satellites, which we believe are particularly well-suited to serving the needs of government users, and by employing a strategy of working with resellers and system integrators, who combine our space-segment services with ground-based services, to provide government users with an end-to-end service.

Providing bundled services

We also provide bundled services in order to derive incremental revenues, optimize fleet utilization and optimize our potential customer base. When we sell our bundled services, we combine our space-segment only services with ground-based services, allowing us to reach customers who lack the scale or technical expertise to operate their own networks and to use satellite capacity that we cannot sell at reasonable rates in a space-segment only configuration.

Disciplined satellite expansion strategy

We have deployed a significant amount of our capacity in regions with high growth rates, including India, Africa, the Middle East and Asia. Satellite industry analysts project that, together, these regions will achieve above-average growth rates in the future. We have one additional satellite under construction, NSS-8, and we do not plan to procure any other satellites until such time as we have a demonstrated need for the additional capacity and a sound business case for a particular satellite, or require a replacement satellite.

Entering into strategic transactions

We intend to monitor developments as consolidation within the FSS industry continues to unfold, and may pursue acquisitions, joint ventures or other strategic transactions on an opportunistic basis to enhance our competitive profile, our financial performance and the value of our business.

4

Risks Relating to Our Business

Our ability to execute our strategy is subject to certain risks, including those that are generally associated with operating in the FSS industry. For example, unforeseen competing technologies may emerge, our satellites may be affected by launch and construction delays, failures or anomalies, demand for our services might not develop as expected, and regulation of the FSS industry may change in a way that is detrimental to our business. In addition, we have a substantial amount of indebtedness (approximately $526.2 million as of December 31, 2004, on a pro forma basis after giving effect to the Transactions (as defined below), the Reorganization (as defined below), the amended agreement for NSS-8, this offering and the application of the estimated net proceeds therefrom), which may adversely affect our ability to generate cash flow, pay dividends on our common stock, remain in compliance with debt covenants, make payments on our subsidiary's indebtedness and operate our business. Furthermore, four of our five satellites accounted for 10% or more of our total services and backlog as of December 31, 2004. Any of these factors or other factors described in this prospectus under "Risk Factors" may limit our ability to successfully execute our business strategy.

In January 2005, we entered into an amended agreement with Boeing Satellite Systems International, Inc. for our NSS-8 satellite, which (among other things) amended the satellite's contractual delivery deadline and the payment terms. Under the terms of the amended agreement, in February 2005 we received a refund of $168.0 million of milestone construction payments made to date. We will pay the entire purchase price of the satellite during the anticipated operational lifetime of NSS-8, subject to satisfactory performance of the satellite during its contractual design life, and we will provide commercially reasonable security to Boeing with respect to the unpaid portion of the purchase price. We currently expect that NSS-8 will be available to enter commercial service during the first half of 2006. We used the $168.0 million refund, along with cash on hand, to pay down approximately $88.8 million under the term loan facility and to pay a dividend of approximately $88.0 million to existing shareholders.

On February 17, 2005, we entered into a capacity restoration framework agreement that will result in the generation of additional revenues for us in 2005 and beyond. Under this agreement, we will provide to certain of Intelsat, Ltd.'s customers telecommunication services on one of our satellites and, in so doing, will provide a restoration service for these customers' transmissions. The agreement also creates a framework under which Intelsat, Ltd. may be requested to restore our services in the event of a significant failure or failures to one of our satellites.

On March 2, 2005, we reached an agreement with SES Global affiliates relating to certain orbital slot coordination matters. Under the terms of the agreement, we agreed not to bring a satellite into use at our 105o west longitude orbital location in order to ensure that SES Global will be able to operate its satellite without interference. In return, SES Global will make a one-time payment to us of $10.0 million. Both parties also committed to negotiate resolution of long-standing issues regarding satellite operations in the Atlantic Ocean region.

5

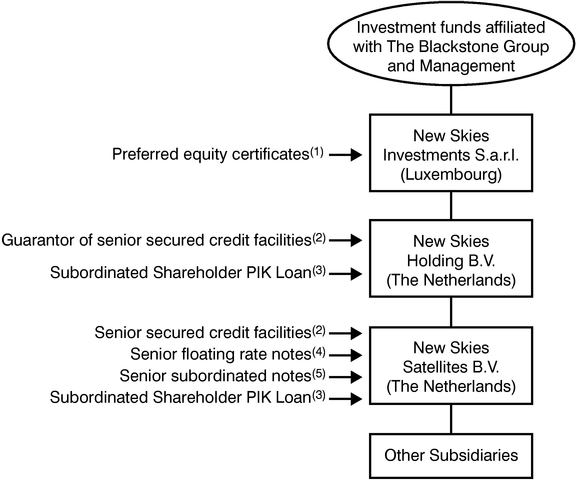

On June 5, 2004, Neptune One Holdings Ltd. and New Skies Satellites B.V., which are owned by the investment funds, entered into a definitive transaction agreement with New Skies Satellites N.V. ("Seller"), providing for New Skies Satellites B.V.'s acquisition of substantially all of Seller's assets (including the shares of all of Seller's subsidiaries), and the assumption of substantially all of Seller's liabilities, for an aggregate purchase price of $982.8 million, including direct acquisition costs (the "Acquisition"). New Skies Satellites N.V. is in liquidation as of November 3, 2004.

In connection with the Acquisition, the investment funds contributed $153.0 million in the form of preferred equity certificates, $8.5 million in the form of convertible preferred equity certificates and $1.5 million of equity to New Skies Investments S.a.r.l. New Skies Investments S.a.r.l. subsequently loaned $153.0 million (the "Holding PIK Loan") and contributed $10.0 million of equity to New Skies Holding B.V. New Skies Holding B.V. then loaned $153.0 million (the "Satellites PIK Loan" and, together with the Holding PIK Loan, the "Subordinated Shareholder PIK Loans") and contributed $10.0 million of equity to New Skies Satellites B.V. In addition, in November 2004, New Skies Satellites B.V.:

- •

- entered into senior secured credit facilities, consisting of a $460.0 million term loan facility and a $75.0 million revolving credit facility;

- •

- issued $160.0 million aggregate principal amount of Floating Rate Notes due 2011 (the "senior floating rate notes"); and

- •

- issued $125.0 million aggregate principal amount of 91/8% Senior Subordinated Notes due 2012 (the "senior subordinated notes" and, together with the senior floating rate notes, the "notes").

The Acquisition and the related financing transactions, together with Seller's liquidation and the related distributions, are referred to collectively in this prospectus as the "Transactions." For a more detailed description of the Transactions, see "The Transactions."

Concurrent with this offering, we intend to amend the senior secured credit facilities. The amendment of the senior secured credit facilities and this offering are conditioned on each other. See "Description of Indebtedness."

In connection with the Transactions, we paid the investment funds a $9.0 million transaction fee to compensate them for debt issuance and acquisition costs and $4.8 million to reimburse them for out-of-pocket expenses. We have also made monitoring fee payments of approximately $0.6 million to Blackstone Management Partners IV L.L.C. pursuant to the transaction and monitoring fee agreement. In February 2005, we paid our existing shareholders a dividend of $88.0 million. In addition, we expect to pay a dividend of $99.5 million to existing shareholders from the net proceeds of this offering (excluding any dividend that may be paid to them if and when the underwriters exercise their over-allotment option) and $6.5 million from the net proceeds of this offering to Blackstone Management Partners IV L.L.C. in connection with the anticipated termination of the transaction and monitoring fee agreement. In addition, management became the beneficial owner of approximately 2.8% of our common stock and received, together with other employees, approximately $3.7 million as bonuses and pursuant to the termination of the company's former stock incentive plan. We also plan to grant management options to purchase shares of our common stock.

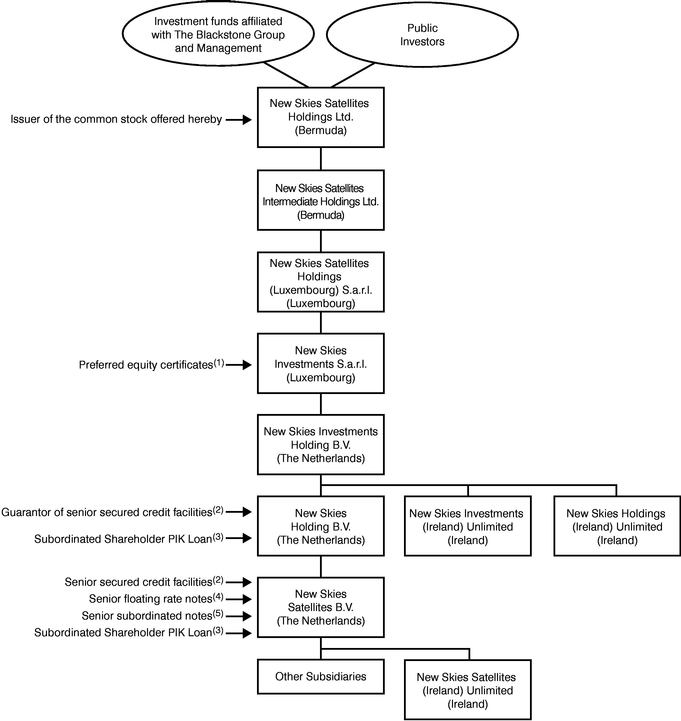

Prior to the consummation of this offering, we will complete an internal restructuring pursuant to which existing shareholders will contribute 100% of the equity and preferred equity certificates of New Skies Investments S.a.r.l. to the Issuer, after which existing shareholders will own 100% of the equity of the Issuer (the "Reorganization"). As a result, New Skies Investments S.a.r.l., New Skies Holding B.V. and New Skies Satellites B.V. will become indirect wholly-owned subsidiaries of the Issuer.

Although the Reorganization will not be completed until immediately prior to the consummation of this offering, unless we specifically state otherwise, all information in this prospectus assumes that the Reorganization has occurred as of the date hereof.

6

The charts below summarize our ownership structure before and after giving effect to the Reorganization.

Pre-Reorganization Structure

7

Post-Reorganization Structure

- (1)

- On November 2, 2004, the investment funds contributed to New Skies Investments S.a.r.l. aggregate proceeds of approximately $163.0 million in the form of preferred equity certificates, convertible preferred equity certificates and equity. In connection with the internal restructuring, the convertible preferred equity certificates and preferred equity certificates will be exchanged for newly issued convertible preferred equity certificates and preferred equity certificates, and New Skies Satellites Holdings Ltd. will directly and indirectly own 100% of the equity, convertible preferred equity certificates and preferred equity certificates in New Skies Investments S.a.r.l.

- (2)

- The senior secured credit facilities (as amended concurrently with this offering) consist of a $460.0 million senior secured term loan facility that matures in May 2011 and a $75.0 million senior secured revolving credit facility that matures in November 2010. As of December 31, 2004, there was $460.0 million outstanding under the term loan facility and no

8

outstanding borrowings under the revolving credit facility. As of December 31, 2004, $2.3 million of standby letters of credit were outstanding under the revolving credit facility. We expect to use approximately $130.8 million of the net proceeds from this offering to repay borrowings under the term loan facility. See "Description of Indebtedness—Senior Secured Credit Facilities."

- (3)

- In November 2004, New Skies Holding B.V. entered into a Subordinated Shareholder PIK Loan with New Skies Investments S.a.r.l. in an aggregate principal amount of $153.0 million, with interest accruing on such loan at a rate of 11.375% annually. Also in November 2004, New Skies Satellites B.V. entered into a Subordinated Shareholder PIK Loan with New Skies Holding B.V. in an aggregate amount of $153.0 million, with interest accruing on such loan at a rate of 11.5% annually. The maturity date of each of the Subordinated Shareholder PIK Loans is April 2014. The Subordinated Shareholder PIK Loans rank subordinate to any of our third-party indebtedness so long as the senior secured credit facilities or the notes remain outstanding and cannot be accelerated while the senior secured credit facilities or the notes remain outstanding. In connection with this offering, we intend to amend the terms of the Subordinated Shareholder PIK Loans to provide for the option to make payments of principal and interest in cash or in-kind.

- (4)

- In November 2004, New Skies Satellites B.V. issued $160.0 million aggregate principal amount of Senior Floating Rate Notes due 2011. The senior floating rate notes bear interest at a rate per annum, reset semi-annually, equal to LIBOR plus 51/8%. As of December 31, 2004, the senior floating rate notes accrued interest at the rate of approximately 7.4%. The Issuer may become a guarantor of the senior floating rate notes prior to the consummation of this offering. See "Description of Indebtedness—Senior Floating Rate Notes due 2011."

- (5)

- In November 2004, New Skies Satellites B.V. issued $125.0 million aggregate principal amount of 91/8% Senior Subordinated Notes due 2012. The Issuer may become a guarantor of the senior subordinated notes prior to the consummation of this offering. See "Description of Indebtedness—91/8% Senior Subordinated Notes due 2012."

The principal offices of the Issuer are located at Canon's Court, 22 Victoria Street, Hamilton HM12 Bermuda, and its telephone number is (441) 295-1433. The principal offices of our main operating company, New Skies Satellites B.V., are located at Rooseveltplantsoen 4, 2517 KR The Hague, The Netherlands, and its telephone number at that address is +31-70-306-4100. We maintain a website at www.newskies.com.Information contained on our website does not constitute a part of this prospectus and is not being incorporated by reference herein.

9

Shares of common stock offered by New Skies Satellites Holdings Ltd. | shares | |||||

Shares of common stock outstanding after this offering | shares | |||||

Percentage of outstanding common stock represented by shares offered after this offering | % | |||||

Use of proceeds | We estimate that our net proceeds from this offering, after deducting underwriting discounts and estimated offering expenses, will be approximately $236.8 million, assuming the shares are offered at $ per share, which is the mid-point of the estimated offering price range set forth on the cover page of this prospectus. | |||||

We intend to: | ||||||

• | indirectly contribute approximately $130.8 million of the net proceeds to New Skies Satellites B.V., in the form of an intercompany loan, which proceeds will then be used to repay a portion of the outstanding borrowings under the term loan facility and pay accrued interest thereon; | |||||

• | indirectly contribute approximately $99.5 million of the net proceeds to an indirect subsidiary of the Issuer, which proceeds will then be loaned to the Issuer to pay a dividend to existing shareholders; and | |||||

• | indirectly contribute approximately $6.5 million of the net proceeds to New Skies Satellites B.V., which proceeds will then be used to pay a termination fee to Blackstone Management Partners IV L.L.C. in connection with the anticipated termination of the transaction and monitoring fee agreement. See "Certain Relationships and Related Part Transactions—New Arrangements—Transaction and Monitoring Fee Agreement." | |||||

We also intend to use any net proceeds we receive from any shares sold pursuant to the underwriters' over-allotment option to pay a dividend to existing shareholders. See "Use of Proceeds." | ||||||

Dividend policy | Our board of directors has adopted a dividend policy, effective upon the closing of this offering, which reflects an intention to distribute a substantial portion of the cash generated by our business in excess of operating expenses and working capital requirements, interest and principal payments on our indebtedness and capital expenditures as regular quarterly dividends to our shareholders. | |||||

10

In February 2005, we paid our existing shareholders a dividend of $88.0 million. In addition, we expect to pay a dividend of $99.5 million to existing shareholders from the net proceeds of this offering (excluding any dividend that may be paid to them if and when the underwriters exercise their over-allotment option). | ||||||

Proposed New York Stock Exchange symbol | ||||||

Unless we specifically state otherwise, all information in this prospectus:

- •

- assumes no exercise by the underwriters of their option to purchase additional shares; and

- •

- excludes shares of common stock that we plan to reserve for issuance under the New Skies Satellites Stock Incentive Plan (the "Stock Incentive Plan"), none of which have been issued as of the date of this prospectus.

Investing in our common stock involves substantial risk. You should carefully consider all of the information set forth in this prospectus and, in particular, should evaluate the specific factors set forth under "Risk Factors" in deciding whether to invest in our common stock.

11

SUMMARY HISTORICAL AND PRO FORMA FINANCIAL, OPERATING AND OTHER DATA

Set forth below is summary consolidated historical financial and other data of New Skies Investments S.a.r.l. and summary consolidated pro forma financial and other data of New Skies Satellites Holdings Ltd. at the dates and for the periods indicated. The Issuer is a recently formed Bermuda holding company which does not have any independent external operations other than through the indirect ownership of the New Skies Satellites business. Accordingly, no separate historical financial statements of the Issuer on a stand-alone basis are included in this prospectus. For the purposes of this prospectus, all financial and other information herein relating to periods prior to the completion of the Transactions, including certain of the summary consolidated historical financial and other operating data presented below, is that of New Skies Satellites N.V., as the predecessor accounting entity to New Skies Investments S.a.r.l. The summary consolidated historical statement of operations data and summary consolidated historical statement of cash flow data for the fiscal years ended December 31, 2002 and 2003, the period January 1, 2004 to November 1, 2004 and the period November 2, 2004 to December 31, 2004 and the summary consolidated historical balance sheet data as of December 31, 2003 and 2004 were derived from the audited consolidated historical financial statements of New Skies Investments S.a.r.l. and related notes included elsewhere in this prospectus.

The summary unaudited pro forma consolidated financial and other data for New Skies Satellites Holdings Ltd. have been prepared to give effect to the Transactions, the Reorganization, the amended agreement for NSS-8, this offering and the application of the estimated net proceeds therefrom as if they had occurred on January 1, 2004, in the case of the unaudited pro forma consolidated statement of operations data, and to the Reorganization, the amended agreement for NSS-8, this offering and the application of the estimated net proceeds therefrom as if they had occurred on December 31, 2004, in the case of unaudited pro forma consolidated balance sheet data. The proceeds from the amended agreement for NSS-8, along with cash on hand, were used to repay a portion of the outstanding borrowings under the term loan facility and pay a dividend to existing shareholders. Assumptions underlying the pro forma adjustments are described in the notes to the unaudited pro forma condensed consolidated financial statements appearing elsewhere in this prospectus, which should be read in conjunction with these unaudited pro forma condensed consolidated financial statements.

The pro forma adjustments are based upon available information and certain assumptions that we believe are reasonable. Please see the notes to our unaudited pro forma condensed consolidated financial statements for a more detailed discussion of how pro forma adjustments are presented in our unaudited pro forma condensed consolidated financial statements. The unaudited pro forma condensed consolidated financial information is provided for informational purposes only. The summary unaudited pro forma consolidated financial data do not purport to represent what our results of operations or financial position actually would have been if the Transactions, the Reorganization, the amended agreement for NSS-8, this offering and the application of the estimated net proceeds therefrom had occurred at any date, nor do such data purport to project the results of operations for any future period.

The summary consolidated historical and pro forma financial, operating and other data should be read in conjunction with "Unaudited Pro Forma Condensed Consolidated Financial Information," "Selected Consolidated Historical Financial Data," "Management's Discussion and Analysis of Financial Condition and Results of Operations" and the audited consolidated financial statements of New Skies Investments S.a.r.l. and related notes included elsewhere in this prospectus.

12

| | Predecessor | | | ||||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Successor | ||||||||||||||||

| | Year Ended December 31, | | |||||||||||||||

| | Period from January 1, 2004 to November 1, 2004 | Period from November 2, 2004 to December 31, 2004 | Pro Forma Year Ended December 31, 2004 | ||||||||||||||

| | 2002 | 2003 | |||||||||||||||

| | (In millions (other than per share data, operating data and percentages)) | ||||||||||||||||

| Statement of Operations Data: | |||||||||||||||||

| Revenues from telecommunication services | $ | 200.5 | $ | 214.9 | $ | 175.4 | $ | 35.3 | $ | 210.7 | |||||||

Operating expenses: | |||||||||||||||||

| Cost of operations | 50.7 | 53.2 | 45.4 | 10.9 | 56.3 | ||||||||||||

| Selling, general and administrative | 39.5 | 42.1 | 35.8 | 18.0 | 53.6 | ||||||||||||

| Transaction related expenses | — | — | 26.4 | — | 26.4 | ||||||||||||

| Depreciation | 80.6 | 99.9 | 86.4 | 16.0 | 96.9 | ||||||||||||

| Total operating expenses | 170.8 | 195.2 | 194.0 | 44.9 | 233.2 | ||||||||||||

| Gain arising on frequency coordination(1) | — | — | 32.0 | — | 32.0 | ||||||||||||

Operating income (loss) | 29.7 | 19.7 | 13.4 | (9.6 | ) | 9.5 | |||||||||||

| Interest expense, net | 0.5 | 1.2 | 1.4 | 9.8 | 39.2 | ||||||||||||

Income (loss) before income tax expense (benefit) | 29.2 | 18.5 | 12.0 | (19.4 | ) | (29.7 | ) | ||||||||||

| Income tax expense (benefit) | 10.5 | 6.7 | 4.3 | (5.4 | ) | (9.1 | ) | ||||||||||

| Income (loss) before cumulative effect of change in accounting principle | 18.7 | 11.8 | 7.7 | (14.0 | ) | (20.6 | ) | ||||||||||

| Cumulative effect of change in accounting principle, relating to goodwill, net of taxes(2) | (23.4 | ) | — | — | — | — | |||||||||||

| Net income (loss) | $ | (4.7 | ) | $ | 11.8 | $ | 7.7 | $ | (14.0 | ) | $ | (20.6 | ) | ||||

| Net Income (Loss) Per Share Data(3): | |||||||||||||||||

| Basic and diluted net income (loss) per share: | |||||||||||||||||

| Net income (loss) per share | $ | (0.04 | ) | $ | 0.10 | $ | 0.06 | $ | (322.61 | ) | $ | ||||||

| Weighted average shares—basic (in thousands) | 130,342 | 119,499 | 118,099 | 43 | |||||||||||||

| Weighted average shares—diluted (in thousands) | 130,342 | 120,678 | 119,850 | 43 | |||||||||||||

Balance Sheet Data (end of year): | |||||||||||||||||

| Cash and cash equivalents | $ | 8.3 | $ | 23.3 | n/a | $ | 38.0 | $ | 30.0 | ||||||||

| Total current assets | 58.5 | 79.9 | n/a | 84.9 | 77.0 | ||||||||||||

| Communications, plant and other property | 1,058.1 | 1,026.6 | n/a | 895.9 | 727.9 | ||||||||||||

| Total assets | 1,128.0 | 1,115.8 | n/a | 1,030.3 | 847.8 | ||||||||||||

| Total debt(4) | 10.0 | — | n/a | 909.3 | 526.2 | ||||||||||||

| Total shareholders' equity (deficiency) | 1,019.0 | 1,001.8 | n/a | (11.8 | ) | 191.9 | |||||||||||

Statement of Cash Flow Data: | |||||||||||||||||

| Net cash provided by operating activities | $ | 113.0 | $ | 109.8 | $ | 111.2 | $ | 30.0 | n/a | ||||||||

| Net cash used in investing activities | (231.4 | ) | (43.5 | ) | (7.7 | ) | (866.1 | ) | n/a | ||||||||

| Net cash (used in) provided by financing activities | (11.7 | ) | (51.9 | ) | (6.4 | ) | 873.7 | n/a | |||||||||

13

| | Predecessor | | ||||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, | | Successor | |||||||||||

| | Period from January 1, 2004 to November 1, 2004 | Period from November 2, 2004 to December 31, 2004 | ||||||||||||

| | 2002 | 2003 | ||||||||||||

Other Data: | ||||||||||||||

| Adjusted EBITDA(5) | $ | 115.2 | $ | 127.0 | $ | 100.6 | $ | 19.9 | ||||||

| Capital expenditures: | ||||||||||||||

| New satellites | 210.2 | 38.1 | 3.3 | 3.4 | ||||||||||

| Non-satellite | 21.2 | 5.4 | 4.4 | 1.0 | ||||||||||

| Contractual backlog (at year end)(6) | 706.1 | 672.1 | n/a | 517.0 | ||||||||||

Operating Data (at end of period): | ||||||||||||||

| Number of satellites in commercial operation (station-kept) | 4 | 5 | 5 | 5 | ||||||||||

| Number of transponders(7): | ||||||||||||||

| C-band | 123 | 178 | 178 | 178 | ||||||||||

| Ku-band | 74 | 146 | 146 | 146 | ||||||||||

| Satellite fleet fill rate(8) | 67 | % | 48 | % | n/a | 55 | % | |||||||

- (1)

- Reflects a one-time payment from Intelsat LLC following the successful resolution of certain longstanding frequency coordination matters.

- (2)

- As of January 1, 2002, we adopted Statement of Financial Accounting Standard ("SFAS") No. 142,Goodwill and Other Intangible Assets ("SFAS No. 142"). This standard eliminates goodwill amortization from the Consolidated Statement of Operations and requires an evaluation of goodwill for impairment upon adoption of this standard, as well as subsequent evaluations on an annual basis, and more frequently if circumstances indicate a possible impairment. Upon adoption of SFAS No. 142, we performed a transitional impairment test on the goodwill resulting from the purchase of New Skies Networks Pty Ltd. in March 2000. As a result of this impairment test, we recorded an impairment charge of approximately $23.4 million, which is classified as a cumulative effect of a change in accounting principle.

- (3)

- Basic net income (loss) per share is calculated by dividing net income (loss) by the weighted average shares outstanding. The computation of diluted net income (loss) per share is similar to basic net income (loss) per share, except that it assumes the potentially dilutive securities were converted to shares as of the beginning of the period. Unaudited pro forma basic and diluted net income (loss) per share has been calculated in accordance with the Securities and Exchange Commission, or the SEC, rules for initial public offerings. These rules require that the weighted average share calculation give retroactive effect to any changes in our capital structure, the number of shares whose sale proceeds will be used to repay any debt as well as to pay a dividend as reflected in the pro forma adjustments. Therefore, pro forma weighted average shares for purposes of the unaudited pro forma basic net income (loss) per share calculation has been adjusted to reflect the shares expected to be issued in this offering.

- Since

- we had a pro forma net loss for the year ended December 31, 2004, shares issuable pursuant to previously existing options would have had an antidilutive effect, and therefore have been excluded from the computation of net income (loss) per share for this period.

- (4)

- Total debt is calculated as the sum of short-term and long-term third-party debt (including borrowings under the senior secured credit facilities, fixed and floating rate notes, and the preferred equity securities subject to mandatory redemption). We pay a portion of the purchase price for each of our satellites (100% in the case of NSS-8) as in-orbit performance incentives. Our obligation to pay in-orbit performance incentives depends upon the satisfactory performance of each satellite during its contractual design life. Total debt does not include short-term and long-term satellite performance incentives, which liabilities are contingent and were $36.9 million as of December 31, 2004. Pro forma total debt reflects the assumed use of a portion of proceeds from this offering to repay $130.8 million of the term loan facility as well as the use of a portion of the refund of milestone construction payments under the amended agreement for NSS-8 to repay an additional $88.8 million of the term loan facility. Additionally, pro forma total debt also assumes the reclassification to shareholders' equity of the par value of the preferred equity securities subject to mandatory redemption as well as the reclassification to accrued liabilities of the related accrued interest.

- (5)

- Adjusted EBITDA is defined as EBITDA (i.e., earnings before interest, taxes, depreciation and amortization), further adjusted to give effect to adjustments required in calculating covenant ratios and compliance under the indentures governing the notes and the senior secured credit facilities. We use Adjusted EBITDA to give effect to adjustments required in calculating covenant ratios and compliance under the indentures governing the notes and the senior secured credit facilities. For instance, both the indentures governing the notes and the senior secured credit facilities contain financial ratios that are calculated by reference to Adjusted

14

EBITDA. Non-compliance with the financial ratio maintenance covenants contained in the senior secured credit facilities could result in the requirement to immediately repay all amounts outstanding under such facilities, while non-compliance with the debt incurrence ratio contained in the indentures governing the notes would prohibit us from being able to incur additional indebtedness other than pursuant to specified exceptions. Adjusted EBITDA is not presented as an alternative measure of operating results or cash flows provided by operating activities, as determined in accordance with generally accepted accounting principles in the U.S. Adjusted EBITDA as presented in this prospectus may not be comparable to similarly titled measures reported by other companies. The following table sets forth the reconciliation of net cash provided by operating activities and net income (loss) to EBITDA and Adjusted EBITDA for the periods indicated.

Reconciliation of Net Cash Provided by Operating Activities to Net Income (Loss):

| | Predecessor | | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Year Ended December 31, | | Successor | ||||||||||

| | Period from January 1, 2004 to November 1, 2004 | Period from November 2, 2004 to December 31, 2004 | |||||||||||

| | 2002 | 2003 | |||||||||||

(in millions) | |||||||||||||

| Net cash provided by operating activities | $ | 113.0 | $ | 109.8 | $ | 111.2 | $ | 30.0 | |||||

| Depreciation | (80.6 | ) | (99.9 | ) | (86.4 | ) | (16.0 | ) | |||||

| Cumulative effect of change in accounting principle | (23.4 | ) | — | — | — | ||||||||

| Deferred taxes | (1.4 | ) | (0.9 | ) | (1.7 | ) | 5.6 | ||||||

| Stock compensation expense | (1.0 | ) | (2.2 | ) | (5.9 | ) | — | ||||||

| Amortization of debt issuance costs | (1.0 | ) | (0.6 | ) | (0.3 | ) | (0.9 | ) | |||||

| Change in operating assets and liabilities, net of effects of acquisition | (10.3 | ) | 5.6 | (9.2 | ) | (32.7 | ) | ||||||

| Net Income (loss) | $ | (4.7 | ) | $ | 11.8 | $ | 7.7 | $ | (14.0 | ) | |||

Reconciliation of Net Income (Loss) to EBITDA

| | Predecessor | | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Successor | ||||||||||||

| | Year Ended December 31, | | |||||||||||

| | Period from January 1, 2004 to November 1, 2004 | Period from November 2, 2004 to December 31, 2004 | |||||||||||

| | 2002 | 2003 | |||||||||||

(in millions) | |||||||||||||

| Net income (loss) | $ | (4.7 | ) | $ | 11.8 | $ | 7.7 | $ | (14.0 | ) | |||

| Income tax expense (benefit) | 10.5 | 6.7 | 4.3 | (5.4 | ) | ||||||||

| Interest expense, net | 0.5 | 1.2 | 1.4 | 9.8 | |||||||||

| Depreciation | 80.6 | 99.9 | 86.4 | 16.0 | |||||||||

| EBITDA | $ | 86.9 | $ | 119.6 | $ | 99.8 | $ | 6.4 | |||||

15

Reconciliation of EBITDA to Adjusted EBITDA

| | Predecessor | | ||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| | Successor | |||||||||||

| | Year Ended December 31, | | ||||||||||

| | Period from January 1, 2004 to November 1, 2004 | Period from November 2, 2004 to December 31, 2004 | ||||||||||

| | 2002 | 2003 | ||||||||||

(in millions) | ||||||||||||

| EBITDA | $ | 86.9 | $ | 119.6 | $ | 99.8 | $ | 6.4 | ||||

| Cumulative effect of change in accounting principle | 23.4 | — | — | — | ||||||||

| Gain arising on frequency coordination(a) | — | — | (32.0 | ) | — | |||||||

| Costs related to the Transactions(b) | — | — | 26.4 | — | ||||||||

| Unused satellite capacity leased from third party(c) | 3.9 | 5.2 | 4.6 | 0.2 | ||||||||

| One-time customer settlements | — | — | — | 10.3 | ||||||||

| Expense incurred with respect to employee severance | — | — | — | 2.8 | ||||||||

| Costs related to non-cash stock compensation | 1.0 | 2.2 | 1.8 | — | ||||||||

| Monitoring fee paid to Blackstone Management Partners IV L.L.C. | — | — | — | 0.2 | ||||||||

| Adjusted EBITDA | $ | 115.2 | $ | 127.0 | $ | 100.6 | $ | 19.9 | ||||

- (a)

- Reflects a one-time payment from Intelsat LLC following the successful resolution of certain longstanding frequency coordination matters.

- (b)

- Represents non-recurring costs incurred in connection with the Transactions.

- (c)

- For all periods presented, the respective amount reflects costs related to unused capacity on leased transponders, with the underlying contract terminating in November 2004.

- (6)

- Contractual backlog represents the actual dollar amount (without discounting for present value) of the expected future cash payments to be received from customers under all long-term contractual satellite service agreements, which may extend to the end of the life of the satellite or beyond to a replacement satellite. Contractual backlog is attributable to both satellites currently in orbit and those planned for future launch.

- (7)

- Number of transponders reflects transponder capacity available for service and is calculated based upon the total number of transponders, stated in 36 MHz equivalents. See "Business—Our Satellites—Overview of satellite fleet" for additional information.

- (8)

- Satellite fleet fill rate is defined as the number of our revenue-generating transponders (expressed in 36 MHz units) divided by our transponder capacity available for service. In April 2002, NSS-7 was launched, and following the transition of traffic from NSS-K and NSS-5, entered commercial service in August 2002. NSS-5 was then drifted to the Pacific Ocean region and entered commercial service in January 2003 at its new orbital location. Following the launch of NSS-6 in December 2002, it entered commercial service in February 2003. Our 2002 and 2003 satellite fleet fill rates do not include our NSS-513 satellite, which we operated in an inclined orbit and removed from service in 2003. See also "Business—Our Satellites—Overview of satellite fleet."

16

An investment in our common stock involves risks. You should carefully consider the risks described below, together with the other information in this prospectus, before you make a decision to purchase our common stock.

Risks Relating to Our Dividend Policy

You may not receive any dividends, and the reduction or elimination of dividends would negatively affect the market price of our common stock.

While we expect to pay quarterly dividends on our common stock, we have no obligation to do so. Dividend payments are within the absolute discretion of our board of directors and will depend on, among other things, our results of operations, working capital requirements, capital expenditure requirements, financial condition, contractual restrictions, business opportunities, anticipated cash needs, provisions of applicable law and other factors that our board of directors may deem relevant. For example, we may not generate sufficient cash from operations in the future, or we might suffer an uninsured loss of a satellite requiring significant and unplanned capital expenditures, resulting in an inability to pay dividends on our common stock in the intended amounts or at all. In addition, New Skies Satellites B.V. is subject to certain restrictions on payment of dividends under the senior secured credit facilities and the indentures governing the notes which, if triggered, may result in our modification or elimination of dividends. Additionally, our need for cash to fund capital expenditures to replace our existing satellites is projected to significantly increase in 2010. Under those circumstances, our board of directors may decide to use cash from operations for increased capital expenditures or to take advantage of new growth opportunities. Absent the incurrence of additional debt or increased net cash provided by operating activities, higher capital expenditures will restrict our ability to pay dividends. Restrictions under the laws of The Netherlands, Bermuda, Luxembourg and Ireland may also limit our ability to make dividend payments. See "Dividend Policy and Restrictions." Any reduction or elimination of dividends would adversely affect the market price of our common stock.

Higher capital expenditures in the future may require us to borrow funds for dividend payments and such borrowed funds may not be available to us.

In the future we will need to start replenishing our satellite fleet, which will require significantly increased capital expenditures. Of our five in-orbit satellites, NSS-5 and NSS-7 are scheduled to be taken out of service in 2014, and NSS-806 is scheduled to be taken out of service in 2015. As a result, we expect that our need for cash to replenish satellites will significantly increase beginning in 2010. Higher capital expenditures for satellite construction will reduce our excess cash flow and, without incurring additional indebtedness, we may be unable to finance our dividends. Cash outlays for satellite construction will impede our excess cash flow and, absent additional debt, our ability to pay dividends will be severely restricted.

Our ability to fund dividends during a high cost capital expenditure period will depend on our ability to incur additional indebtedness. Our ability to incur additional indebtedness and refinance existing indebtedness in the future will depend on our financial and operating performance; our ability to comply with restrictions in our existing debt agreements; market, financial and other economic factors beyond our control; and the ability to refinance our subsidiary's debt agreements on terms no less favorable than our subsidiary's existing debt agreements. Additionally, the senior secured revolving credit facility and senior secured term loan facility mature in 2010 and 2011, respectively. Further, depending on market conditions, even if we are able to obtain financing for our capital expenditures or to refinance the existing indebtedness, the terms of the financing may limit, or even prohibit, our ability to pay dividends.

17

The Issuer is a holding company with no operations, and unless it receives dividends, distributions, advances, transfers of funds or other payments from its subsidiaries, it will be unable to pay dividends on its common stock and meet its other obligations, if any.

The Issuer is a holding company and conducts all of its operations through its subsidiaries. It does not have, apart from its indirect ownership of New Skies Satellites B.V. (through its other subsidiaries, which are intermediary holding companies of New Skies Satellites B.V.), any independent operations. As a result, it will rely on dividends and other payments or distributions from New Skies Satellites B.V. and its other subsidiaries to pay dividends on its common stock and other obligations, if any. The ability of New Skies Satellites B.V. and our other subsidiaries to pay dividends or make other payments or distributions to their shareholders will depend on New Skies Satellites B.V.'s operating results and may be restricted by, among other things, laws of The Netherlands, the covenants contained in the senior secured credit facilities and the indentures governing the notes, and the covenants of any future outstanding indebtedness the Issuer or its subsidiaries incur. The ability of our Luxembourg subsidiaries to pay dividends or make other payments or distributions to its shareholders may be restricted by the laws of Luxembourg. See "Dividend Policy and Restrictions."

We may not receive sufficient cash from our Dutch subsidiaries, which could limit our ability to pay dividends.

Pursuant to Dutch law and under the provisions of the senior secured credit facilities and the indentures governing the notes, our Dutch subsidiaries may make distributions to its shareholders only to the extent that its shareholder's equity exceeds the aggregate of its paid up nominal share capital and the amount of mandatory reserves that must be maintained under Dutch law (such excess, if any, constituting "freely distributable reserves"). If either of these companies does not have sufficient freely distributable reserves, it will limit their ability to pay dividends.

We have considered several strategies for distributing cash out of each of these companies in the absence of sufficient freely distributable reserves. For example, each of these companies will, subject to the corporate benefit test (as described in the paragraph below) and general rules of Dutch law concerning fraudulent conveyance and/or tort, be permitted to make distributions in respect of interest and principal repayment on the Subordinated Shareholder PIK Loans and the indirect intercompany loans that we will make with a portion of the offering proceeds, as discussed in "Use of Proceeds" (collectively, the "Subordinated Loans"), even if there are no freely distributable reserves. Other strategies that we have considered include loans from the Issuer's subsidiaries to the Issuer (the "upstream loans"), additional capital raising transactions and disposals of appreciated assets. These other strategies, however, may not be available or we may not choose to pursue them. As a result, once the Subordinated Loans are repaid, these companies may no longer be able to make distributions unless there are sufficient profits. Furthermore, all of these strategies (including any upstream loans) will be subject to certain general principles of Dutch law (and any other applicable law) stipulating, among other things, that they be carried out in line with the corporate benefit of the company and taking into account the position of creditors as well as the view of the management board.

We anticipate that any such upstream loans will be made indirectly by our Irish subsidiaries on an interest-free basis. Indirect lending activities using our Irish subsidiaries, however, will require compliance with applicable Irish law. We may not be able, under applicable Irish law, to use our Irish subsidiaries for purposes of making these upstream loans, or to structure these upstream loans in a manner that ensures that none of our Irish or Dutch subsidiaries realizes taxable interest income.

We may also take the position that our Dutch subsidiaries will have freely distributable reserves to the extent of the value of our Irish subsidiaries, which will be transferred to our Dutch subsidiaries immediately following the initial public offering. The decision as to whether to take the position that our Dutch subsidiaries' freely distributable reserves will be increased by the value of our Irish subsidiaries will not be made until we have produced audited financial statements for our Dutch subsidiaries for fiscal 2005. Until this time, we cannot determine whether (and to what extent) the

18

value of our Irish subsidiaries will increase the freely distributable reserves of our Dutch subsidiaries. If we were to take the position that our Dutch subsidiaries' freely distributable reserves were increased by the value of our Irish subsidiaries, it is possible that any distributions made on that basis may be challenged before a Dutch court by interested parties (notably creditors or a receiver in bankruptcy) should it be demonstrated that the value of our Irish subsidiaries could not have been (fully) recognized by our Dutch subsidiaries for purposes of determining the amount of the distributable reserves.

Our Dutch subsidiaries may become subject to the structure regime under Dutch law, which could affect their decisions about whether to fund future dividends or to enter into future intercompany loans or other arrangements.

Under Dutch law, the shareholders of an ordinary B.V. company have substantial power over the company and its management board through their right to appoint and dismiss the managing directors. Although our Dutch subsidiaries each currently qualify as an ordinary Dutch B.V. company, any one of them may become subject to the "structure regime" under Dutch law in 2008. Once subject to the structure regime, the company would be required to amend its articles of association and institute a mandatory supervisory board, which would limit the ability of shareholders to appoint and dismiss its managing directors, which could adversely affect the payment of dividends to the Issuer.

The structure regime obliges the company to install a supervisory board consisting of at least three members in addition to its management board. The supervisory board is a non-executive board that has the duty to supervise the policy of the management board and the general course of affairs of the company and has the exclusive right to appoint (and dismiss) members of the management board. In addition, the supervisory board has the right of prior approval of important management decisions pertaining to, among other things, the issuance or acquisition of shares in the company or debt instruments issued by the company, the entry into or termination of significant long-term joint venture agreements, material participations in other businesses or investments, and employment reorganizations or change in working conditions. The supervisory board members are appointed by the general meeting of shareholders following a recommendation by the supervisory board itself. A company's Works Council (which is discussed below) has the right to make sub-recommendations for a maximum of one-third of the total number of the supervisory board members, which recommendations the supervisory board must follow. If the general meeting of the shareholders loses confidence in the supervisory board, it has the right to remove the entire supervisory board. In that case, the Dutch court will appoint an interim supervisory board, which then will make a binding recommendation to form a new supervisory board.

New Skies Satellites B.V.'s formation of a Works Council under Dutch law may affect its decisions about whether to fund future dividends or to enter into future intercompany loans or major investments.

In 2004, New Skies Satellites B.V. established a "Works Council" in accordance with the Dutch Works Councils Act (Wet op de ondernemingsraden), pursuant to which an employer of at least 50 persons must form a Works Council. A Works Council is a group of employees, elected by their peers, who liaise with company management on certain business, employment and employee benefit matters. New Skies Satellites B.V.'s Works Council includes seven of its Netherlands-based employees. New Skies Satellites B.V. must seek the Works Council's advice or consent on certain business matters that affect the company or its Netherlands-based employees and must consider the Works Council's views before concluding any such matters. Such business matters include, among others: (1) a transfer of control of the undertaking or any division thereof; (2) a significant change in the organization of the undertaking or in the division of powers within the undertaking; (3) the taking up of a significant credit on behalf of the undertaking (such as any future intercompany loans); (4) the granting of a significant credit (including any upstream loans entered into as part of the cash distribution policy of New Skies Satellites B.V.) or (5) the making of a major investment. If the Works Council does not support the

19

distribution of cash by New Skies Satellites B.V., this could adversely impact the Issuer's ability to pay dividends on its common stock.

Our dividend policy may limit our ability to pursue growth opportunities.

Our board of directors has adopted a dividend policy, effective upon the closing of this offering, which reflects an intention to distribute a substantial portion of the cash generated by our business in excess of operating expenses and working capital requirements, interest and principal payments on our subsidiary's indebtedness and capital expenditures as regular quarterly dividends to our shareholders. In developing this policy, we have made assumptions for and judgments about the first four full fiscal quarters following the closing of this offering as to our expected results of operations, anticipated levels of capital expenditures, cash interest expense, income taxes and working capital, and the continued availability of borrowings under our subsidiary's revolving credit facility. As a result of the dividend policy, our ability to finance any material expansion of our business or to fund our operations may be more limited than if we had retained all of our net cash provided by operating activities. In addition, our ability to pursue any material expansion of our business, including through acquisitions or increased capital spending, will depend more than it otherwise would on our ability to obtain third party financing. Such financing may not be available to us at an acceptable cost, or at all. See "Dividend Policy and Restrictions."

Risks Relating to Our Indebtedness

Our subsidiary has a substantial amount of indebtedness, which may adversely affect our cash flow and our ability to operate our business, support our dividend policy, comply with our subsidiary's debt covenants and repay our subsidiary's indebtedness.

As of December 31, 2004 on a pro forma basis after giving effect to the Transactions, the Reorganization, the amended agreement for NSS-8, this offering and the application of the estimated net proceeds therefrom, New Skies Satellites B.V. would have had outstanding indebtedness of $526.2 million and availability of $71.9 million (including standby letters of credit of $2.3 million) under the revolving credit facility.

The substantial indebtedness of New Skies Satellites B.V. could have important consequences to you. For example, it could:

- •

- make it more difficult for us to pay dividends on our common stock;

- •

- make it more difficult for us to satisfy our obligations with respect to the indebtedness of New Skies Satellites B.V., and any failure to comply with the obligations of any of the debt instruments of New Skies Satellites B.V., including financial and other restrictive covenants, could result in an event of default under the indentures governing the notes and the agreements governing such other indebtedness, which could lead to, among other things, cross default and acceleration of our indebtedness;

- •

- require New Skies Satellites B.V. to dedicate a substantial portion of its cash flow to pay principal and interest on its debt, which will reduce the funds available for working capital, capital expenditures, payment of dividends, acquisitions and other general corporate purposes;

- •

- limit our flexibility in planning for and reacting to changes in our business and in the industry in which we operate;

- •

- make us more vulnerable to adverse changes in general economic, industry and competitive conditions and adverse changes in government regulation;

- •

- limit our ability to borrow additional amounts for working capital, capital expenditures, acquisitions, debt service requirements, execution of our growth strategy or other purposes; and

- •

- place us at a disadvantage compared to our competitors who have less debt.

Any of the above listed factors could materially and adversely affect our business and results of operations. Furthermore, the interest expense of New Skies Satellites B.V. could increase if interest

20

rates increase because the entire amount of debt under the senior floating rate notes and the senior secured credit facilities bears interest at floating rates. See "Description of Indebtedness—Senior Secured Credit Facilities" and "—Senior Floating Rate Notes due 2011." Based on the outstanding floating rate indebtedness as of December 31, 2004 and giving pro forma effect to the use of proceeds of this offering, a 1% increase in the average interest rate would increase future interest expense by approximately $5.0 million per year. If New Skies Satellites B.V. does not have sufficient earnings to service its debt, it may be required to refinance all or part of its existing debt, reduce or eliminate dividend payments, sell assets, borrow more money or sell securities, which it may not be able to do. If any of these situations were to occur, the Issuer may not be able to pay dividends to its shareholders.

We will be able to incur significant additional indebtedness in the future. Although the indentures governing the notes and the credit agreement governing the senior secured credit facilities contain restrictions on the incurrence of additional indebtedness, these restrictions are subject to a number of important qualifications and exceptions and the indebtedness incurred in compliance with these restrictions could be substantial. If new debt is added to our anticipated debt levels, the related risks that we now face, including those described above, could intensify.