Filed by Albemarle Corporation

(Commission File No.: 1-12658)

Pursuant to Rule 425 of the Securities Act of 1933

Subject Company: Rockwood Holdings, Inc.

(Commission File No: 1-32609)

Albemarle Corporation Investor Presentation October 2014 Albemarle |  |

Forward Looking Statements Some of the information presented in this document and discussions that follow, including, without limitation, statements with respect to the transaction and the anticipated consequences and benefits of the transaction, the targeted close date for the transaction, product development, changes in productivity, market trends, price, expected growth and earnings, cash flow generation, costs and cost synergies, portfolio diversification, economic trends, outlook and all other information relating to matters that are not historical facts may constitute forward-looking statements within the meaning of the Private Securities Litigation Reform Act of 1995. There can be no assurance that actual results will not differ materially. Factors that could cause actual results to differ materially include, without limitation: the receipt and timing of necessary regulatory approvals; the ability to finance the transaction; the ability to successfully operate and integrate Rockwood's operations and realize estimated synergies; changes in economic and business conditions; changes in financial and operating performance of our major customers and industries and markets served by us; the timing of orders received from customers; the gain or loss of significant customers; competition from other manufacturers; changes in the demand for our products; limitations or prohibitions on the manufacture and sale of our products; availability of raw materials; changes in the cost of raw materials and energy; changes in our markets in general; changes in laws and government regulation impacting our operations or our products; the occurrence of claims or litigation; the occurrence of natural disasters; political unrest affecting the global economy; political instability affecting our manufacturing operations or joint ventures; changes in accounting standards; changes in the jurisdictional mix of our earnings and changes in tax laws and rates; volatility and substantial uncertainties in the debt and equity markets; technology or intellectual property infringement; decisions we may make in the future; and the other factors detailed from time to time in the reports we file with the SEC, including those described under "Risk Factors" in our Annual Report on Form 10-K and our Quarterly Reports on Form 10-Q. These forward-looking statements speak only as of the date of this communication. We expressly disclaim any obligation or undertaking to disseminate any updates or revisions to any forward-looking statement contained herein to reflect any change in our expectations with regard thereto or any change in events, conditions or circumstances on which any such statement is based. Information with respect to Rockwood, including non-GAAP information is taken or derived from Rockwood's public filings and management estimates and we take no responsibility for the accuracy or completeness of such information. It should be noted that this presentation contains certain financial measures, including Net Sales, and Segment Income, that are not required by, or presented in accordance with, accounting principles generally accepted in the United States, or GAAP. These measures are presented here to provide additional useful measurements to review our operations, provide transparency to investors and enable period-to-period comparability of financial performance. A description of non-GAAP financial measures that we use to evaluate our operations and financial performance, and reconciliation of these non-GAAP financial measures to the most directly comparable financial measures calculated and reported in accordance with GAAP, can be found in the Investors section of our website at www.albemarle.com, under "Non-GAAP Reconciliations" under "Financials." Albemarle 2 |  |

Albemarle Acquisition of Rockwood: A Compelling Transaction

o Creates a premier specialty chemicals company with

leading positions in attractive end markets around the

world

o Accelerates Albemarle's strategy of bringing lithium

and bromine together

o Strengthens growth potential across four, high-margin

businesses - lithium, catalysts, bromine and surface

treatment

o Differentiated, performance-based, technologies driving

innovative solutions

o Capacity in place to serve future growth to drive

improved profitability

o Outstanding cash generation capacity supports rapid

deleveraging, ongoing dividend and investments to drive

future growth

Enhanced growth, expanded margins and improved cash flow

drive shareholder value

Albemarle 3

|  |

Summary

Strategic Rationale

o Combined company will be a leading specialty chemical

company with industry-leading growth and EBITDA margins

o Accelerates Albemarle's growth and enhances its margin

profile

o Creates the potential for more consistent and

predictable earnings growth for ALB shareholders

o Creates a leader in four attractive growth markets

o ROC acquisition enables ALB to accelerate its strategy

of bringing lithium and bromine businesses together and

leverage technology to exploit its brine resources

o Lithium and Bromine are a natural fit in several ways

o Both leverage chemistry to derivatize key molecules

o Similarity in extraction processes

o Presence in Fine Chemistry (Agriculture /

Pharmaceuticals) and Polymers (Plastics / Synthetic

Rubbers)

o Common end markets and cross-selling opportunities

o ALB has long been aware of the complementary fit and

has been pursuing an expansion into lithium

o In 2011, announced plans to extract lithium from its

Arkansas brine - key challenge was to extract at

competitive costs

o Evaluated acquisition opportunities even before

discussions with ROC had begun

Anticipated Financial Benefits

o Accretive to cash EPS in year one, adjusted EPS in year

two and substantially accretive to EPS thereafter

o Estimated $100 million in cost synergies across both

companies to be realized in first 2 years

o Capital cost avoidance and improved market access for

Albemarle's lithium development

o Exceptional cash flow generation ($500 million every

year) enables rapid deleveraging

o Continued investment grade rating to ensure low funding

costs

Valuation and Stock Price Performance

o The purchase premium of 13.7% to the prior close and

4.8% to the 52-week high at signing compares favorably

to premiums paid on precedent transactions

o Implied EV/EBITDA 2014E multiple of 14.1x (1) and with

synergies 11.3x (1); compares favorably with other high

growth, specialty chemical deals

o The transaction value was within BofAML's DCF valuation

before synergies, and below DCF valuation with

synergies

o Fixed share exchange ratio set at signing is not

impacted by subsequent share price movements

(1) 2014E EBITDA pro forma for Talison acquisition; Assumes

synergies of $100M

Albemarle 4

|  |

Both Boards Long Recognized The Value of a Combination

o Discussions between Albemarle and Rockwood regarding a

possible transaction date back to May 2012

o Initial discussions involved purchase of lithium,

potential sale of Albemarle or merger of equals

o In the spring of 2014, Rockwood received interest from

multiple parties, including Albemarle, to acquire all

or part of the company

o Indications of interest were received for Rockwood's

surface treatment business and for the company as a

whole

o Albemarle's board, together with management and outside

advisors, regularly reviews alternatives to deliver

shareholder value and determined the acquisition of

Rockwood to be in the best interests of Albemarle

shareholders

o Albemarle's offer to acquire Rockwood for $50.65 in

cash and 0.4803 in Albemarle shares was the most

favorable received by Rockwood

Albemarle 5

|  |

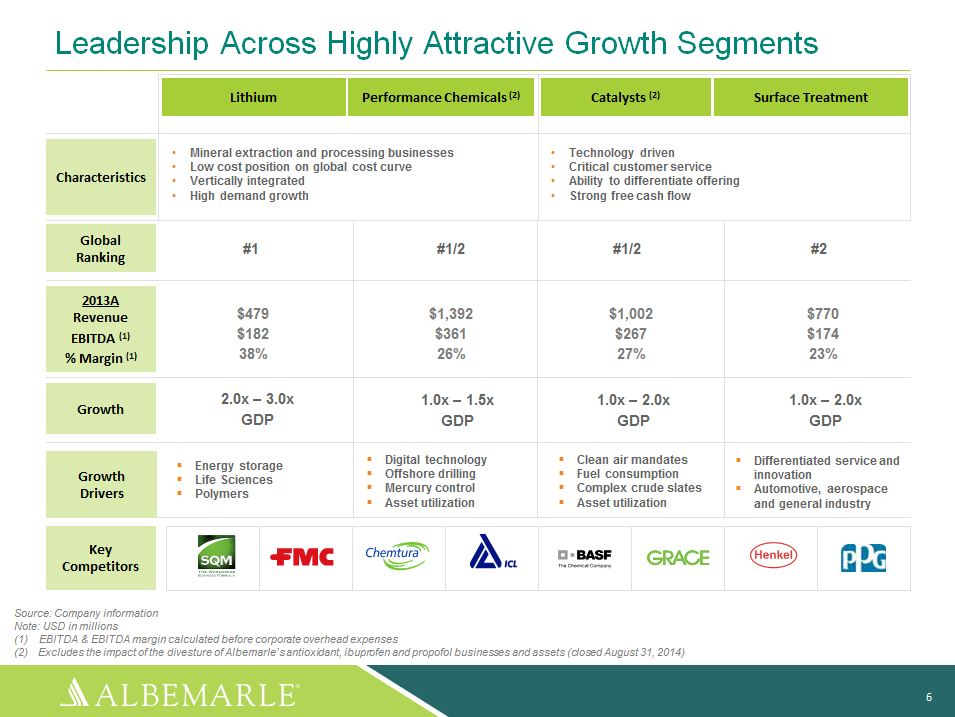

Leadership Across Highly Attractive Growth Segments

Lithium

Performance Chemicals (2)

Catalysts (2)

Surface Treatment

Characteristics

o Mineral extraction and processing businesses

o Low cost position on global cost curve

o Vertically integrated

o High demand growth

o Technology driven

o Critical customer service

o Ability to differentiate offering

o Strong free cash flow

Global Ranking

#1

#1/2

#1/2

#2

2013A

Revenue

EBITDA (1)

% Margin (1)

$479

$182

38%

$1,392

$361

26%

$1,002

$267

27%

$770

$174

23%

Growth

2.0x - 3.0x GDP

1.0x - 1.5x GDP

1.0x - 2.0x GDP

1.0x - 2.0x GDP

Growth Drivers

o Energy storage

o Life Sciences

o Polymers

o Digital technology

o Offshore drilling

o Mercury control

o Asset utilization

o Clean air mandates

o Fuel consumption

o Complex crude slates

o Asset utilization

o Differentiated service and innovation

o Automotive, aerospace and general industry

Key Competitors

Source: Company information

Note: USD in millions

(1) EBITDA and EBITDA margin calculated before corporate

overhead expenses

(2) Excludes the impact of the divesture of Albemarle's

antioxidant, ibuprofen and propofol businesses and

assets (closed August 31, 2014)

Albemarle 6

|  |

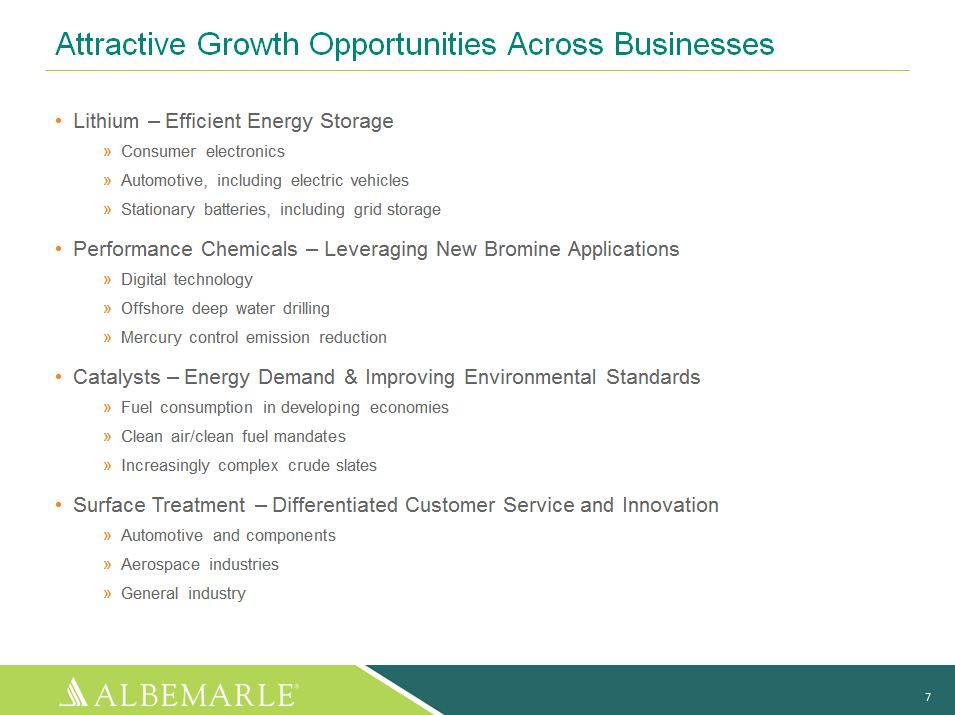

Attractive Growth Opportunities Across Businesses

o Lithium - Efficient Energy Storage

Consumer electronics

Automotive, including electric vehicles

Stationary batteries, including grid storage

o Performance Chemicals - Leveraging New Bromine Applications

Digital technology

Offshore deep water drilling

Mercury control emission reduction

o Catalysts - Energy Demand and Improving Environmental Standards

Fuel consumption in developing economies

Clean air/clean fuel mandates

Increasingly complex crude slates

o Surface Treatment - Differentiated Customer Service and Innovation

Automotive and components

Aerospace industries

General industry

Albemarle 7

|  |

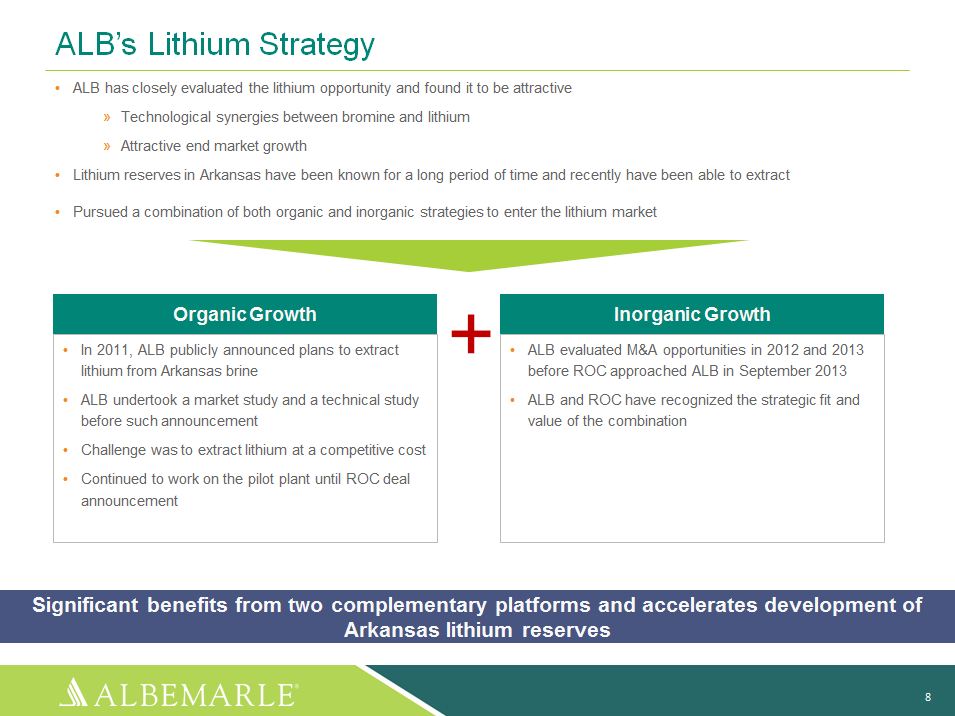

ALB's Lithium Strategy

o ALB has closely evaluated the lithium opportunity and

found it to be attractive

o Technological synergies between bromine and lithium

o Attractive end market growth

o Lithium reserves in Arkansas have been known for a long

period of time and recently have been able to extract

o Pursued a combination of both organic and inorganic

strategies to enter the lithium market

Organic Growth

o In 2011, ALB publicly announced plans to extract

lithium from Arkansas brine

o ALB undertook a market study and a technical study

before such announcement

o Challenge was to extract lithium at a competitive cost

o Continued to work on the pilot plant until ROC deal

announcement

+

Inorganic Growth

o ALB evaluated M and A opportunities in 2012 and 2013

before ROC approached ALB in September 2013

o ALB and ROC have recognized the strategic fit and value

of the combination

Significant benefits from two complementary platforms and

accelerates development of Arkansas lithium reserves

Albemarle 8

|  |

Complementary Fit - Especially Between Lithium and Bromine

Low Cost Sourcing and Processing

o Best sourcing and most diverse locations in the world

due to long term reserves and highest concentration

levels

o Chile, Australia, Nevada and Arkansas for lithium

o Arkansas and the Dead Sea for Bromine

o Chile, Nevada, Arkansas and the Dead Sea all extracted

from brine

Value-Added Derivatization

o Lithium converted into products used in electronic

chemicals, pharma, energy storage, plastics, rubber,

etc.

o Bromine converted into products used in electronics,

automotive, oilfield, mercury control, agriculture,

pharma, etc.

o Process and product technology leadership with in-house

R and D

Global End Market Overlap

Albemarle Rockwood

End Market Overlap

Consumer Electronics

o Flame Retardants

o Custom Organic Chemicals

o High Purity Metal Organics for LED applications

o Batteries

o High Purity Metal Organics

o Organometallics

Automotive

Flame Retardants

Batteries

Lubricants

Greases

Metal Treatment

Polymers

Polyolefins and Synthetic Elastomers

Bromobutyl rubber for use in tires

Synthetic Elastomers

Polyolefins

Agriculture, Pharma

Custom and Generic Active and intermediate Pharmaceutical

and Ag Ingredients

Custom manufacturing

Lithium Active Ingredient in Pharma

Organo lithium in pharma and Ag

Albemarle 9

|  |

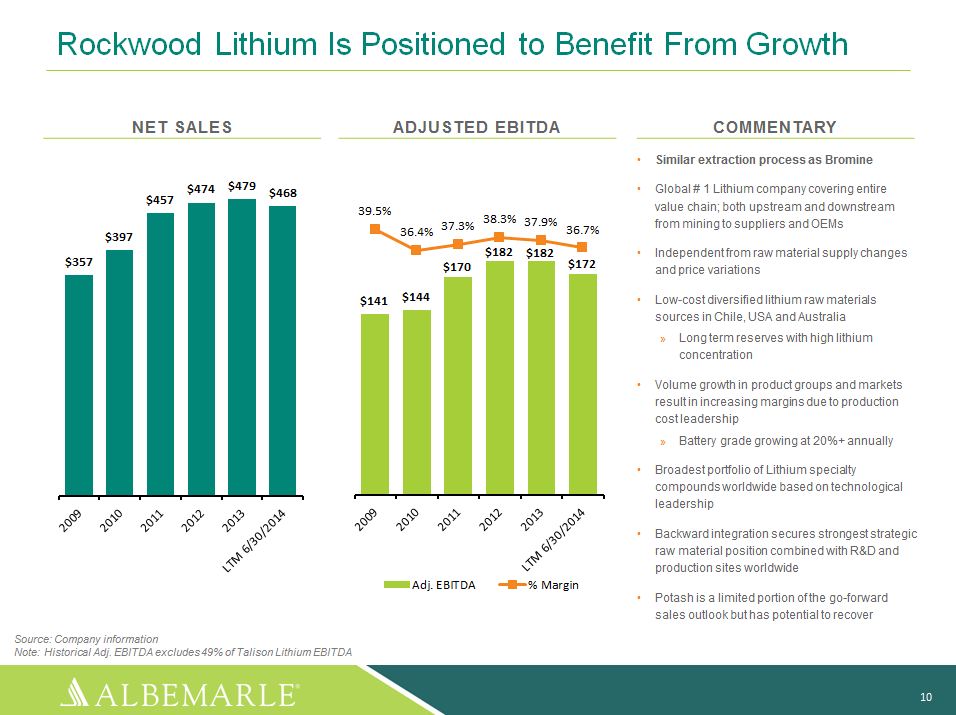

Rockwood Lithium Is Positioned to Benefit From Growth NET SALES $357 $397 $457 $474 $479 $468 2009 2010 2011 2012 2013 LTM 6/30/2014 ADJUSTED EBITDA 39.5% 36.4% 37.3% 38.3% 37.9% 36.7% $141 $144 $170 $182 $182 $172 2009 2010 2011 2012 2013 LTM 6/30/2014 COMMENTARY Similar extraction process as Bromine Global # 1 Lithium company covering entire value chain; both upstream and downstream from mining to suppliers and OEMs Independent from raw material supply changes and price variations Low-cost diversified lithium raw materials sources in Chile, USA and Australia Long term reserves with high lithium concentration Volume growth in product groups and markets result in increasing margins due to production cost leadership Battery grade growing at 20%+ annually Broadest portfolio of Lithium specialty compounds worldwide based on technological leadership Backward integration secures strongest strategic raw material position combined with R and D and production sites worldwide Potash is a limited portion of the go-forward sales outlook but has potential to recover Source: Company information Note: Historical Adj. EBITDA excludes 49% of Talison Lithium EBITDA Albemarle 10 |  |

Potential Lithium Demand Delivers Significant Upside Lithium Carbonate Equivalent in Metric tons 350,000 300,000 250,000 200,000 150,000 100,000 50,000 0 2012 2013 2014 2015 2016 2017 2018 2019 2020 Application Lithium Carbonate Content Cell Phone 3 grams ~ 0.1 oz Notebook 30 grams ~ 1.0 oz Power Tool 30-40 grams ~ 1.0-1.4 oz Hybrid (HEV) 3kWh 3.5 lbs Plug-in Hybrid (PHEV) 15 kWh 26 lbs Electrical Vehicle (BEV) 25 kWh 44 lbs Tesla 85 kWh 112 lbs Grid Storage: Potential Demand Could Exceed Electric Vehicle Automotive High Automotive Low Automotive Average Portable Batteries Other Applications Lubricating Greases Glass and Ceramics Rockwood expects to capture 50% of Lithium growth Source: Rockwood Lithium estimates and market surveys from BCG, Bloomberg, Avicenne, Roland Berger, Pike Research, Frauenhofer IST, Deutsche Bank Research, McKinsey, CTI, Anderman, JD Powers Albemarle 11 |  |

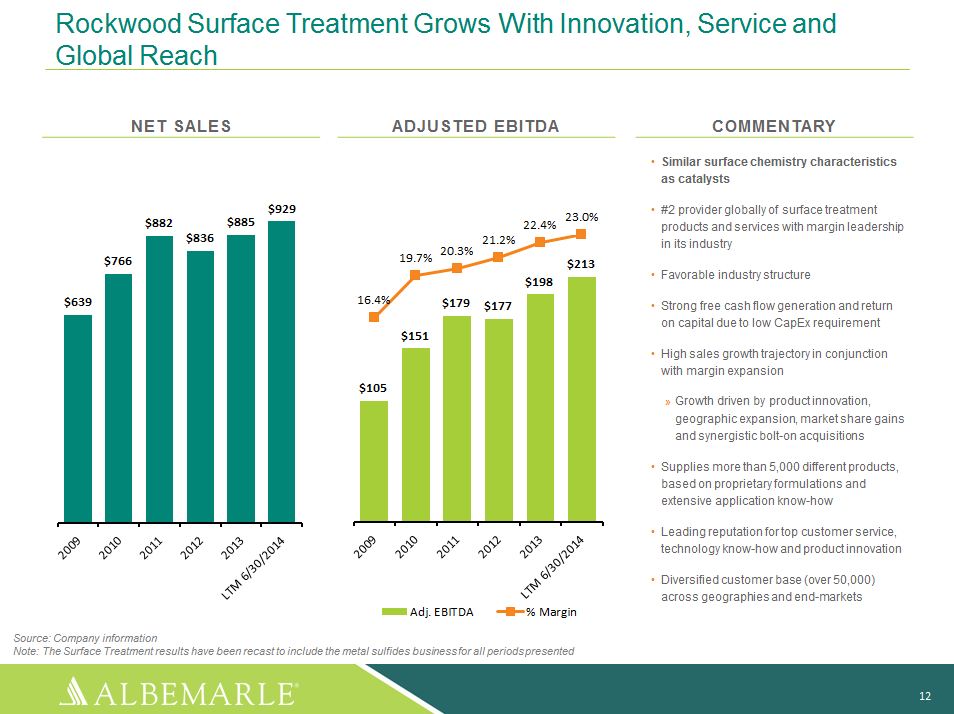

Rockwood Surface Treatment Grows With Innovation, Service and Global Reach NET SALES $639 $766 $882 $836 $885 $929 2009 2010 2011 2012 1013 LTM 6/30/2014 ADJUSTED EBITDA 16.4% $105 19.7% $151 20.3% $179 21.2% $177 22.4% $198 23.0% $213 2009 2010 2011 2012 1013 LTM 6/30/2014 Adj. EBITDA % Margin COMMENTARY Similar surface chemistry characteristics as catalysts #2 provider globally of surface treatment products and services with margin leadership in its industry Favorable industry structure Strong free cash flow generation and return on capital due to low CapEx requirement High sales growth trajectory in conjunction with margin expansion Growth driven by product innovation, geographic expansion, market share gains and synergistic bolt-on acquisitions Supplies more than 5,000 different products, based on proprietary formulations and extensive application know-how Leading reputation for top customer service, technology know-how and product innovation Diversified customer base (over 50,000) across geographies and end-markets Source: Company information Note: The Surface Treatment results have been recast to include the metal sulfides business for all periods presented Albemarle 12 |  |

Meaningful, Highly Executable Synergies

Cost synergies of ~$100 million to be fully realized in 2016

Go to market strategies and resources (e.g. Sales, R and D,

Marketing) do not change

Eliminate redundant corporate overhead costs

Transition back office services to low cost shared service

centers

Improve sourcing costs based on increased scale

Leverage expertise to drive production efficiency in

extracting Bromine and Lithium

High throughput experimentation capabilities in surface

treatment and catalysts businesses to innovate more rapidly

Day 1 synergies of $30 million+

Ahead of Plan

Albemarle 13

|  |

Integration Update Three months in on detailed integration planning Established joint integration teams with dedicated members from both companies Functional - real estate, logistics, supply chain, finance, shared services, tax, IT, legal, manufacturing Cross-functional - Day 1 readiness, communications, organizational design Engaged one of the top integration consulting teams to assist with integration planning and execution Building on best practices from both companies Team is dedicated to identify, quantify and execute synergies in the following areas: Reduce Costs - corporate costs, operational process, real estate footprint, non-raw material sourcing, shared services centers Accelerate Growth - leverage R and D capabilities, new product development, cross-selling opportunities Albemarle 14 |  |

Benefits of Using Albemarle Stock in Transaction Allows Albemarle to maintain its investment grade ratings and optimize capital structure All-cash deal would have resulted in substantially higher leverage resulting in non-investment grade rating and significantly higher financing costs Levered capital structure would have limited financial flexibility and ability of management to capitalize on growth opportunities Fixed exchange ratio of 0.4803x implies that Albemarle is issuing shares to Rockwood shareholders at attractive trading level Exchange ratio was agreed upon at an Albemarle share price of $71.52 locking in the number of shares Albemarle would issue to Rockwood shareholders Current share price performance has no impact on EPS accretion Enables Rockwood shareholders to participate in the upside of the combination (growth and synergies) Use of our cash / debt capacity to acquire Rockwood delivers higher long term value to our shareholders than short term stock buy-backs Our past stock buybacks reflected best use of our cash at that point; value-accretive transforming acquisition opportunities such as Rockwood were not available then Albemarle 15 |  |

BofA Merrill Lynch Valuation Analyses Discounted Cash Flow Analysis $110.00 $100.00 $90.00 $80.00 $70.00 Mixed Consideration Implied Premiums Analysis (1) $110.00 $100.00 $90.00 $80.00 $70.00 The purchase premium of 13.7% to the prior close and 4.8% to the 52-week high at signing compares favorably to premiums paid on precedent transactions ROC shares traded at ~12x 2014E EBITDA prior to transaction announcement of 14x 2014E EBITDA The transaction is expected to be accretive to cash EPS in year one, adjusted EPS in year two and substantially accretive to EPS thereafter The Albemarle Board of Directors reviewed financial analyses and received a fairness opinion from BofA Merrill Lynch Source: S-4 Filing Note. USD per share (1) Premiums offered for selected mixed cash and stock consideration transactions in the United States completed or pending since January 1, 2010 with transaction values over $1.0 billion (2) Represented a 13.7% premium to Rockwood closing price on July 10, 2014 and a 4.8% premium to Rockwood 52-week high Albemarle 16 |  |

ALB Share Price Performance in line With Market

Ph-1: Initial reaction to the deal

Ph-2: Initial fall triggered by earnings then stock performs

in line with peers

Ph-3: Broad market selloff

1 2 3

120%

110%

100%

90%

Dow Jones US Specialty

Chemicals Index

Post Announcement

LTM 6-M onth 2-Month Phase 1 Phase 2 Phase 3

5% (3%) (7%) (0%) 0% (8%)

Catalysts Index (7%) (13%) (13%) (2%)

2% (12%) Bromine Index (14%) (17%) (13%)

(1%) (5%) (12%) Albemarle (16%) (18%)

(12%) (6%) (8%) (15%)

80%

10/15/13 01/14/14 04/15/14 07/15/14

10/15/14

(1) (2)

Albemarle Catalysts Index Bromine Index Dow Jones Specialty

Chemicals Index

Source: FactSet as of October 15, 2014

Note: Phase 1 reflects stock price performance from

7/14/2014 to 7/23/2014, Phase 2 from 7/23/2014 to 9/22/2014

and Phase 3 from 9/22/2014 to 10/15/2014

(1) Catalysts Index includes W.R. Grace

(2) Bromine Index Includes Chemtura and ICL

Albemarle 17

|  |

Positive Reactions From The Street to Proposed Transaction Increases Growth Profile "[W]e believe base ALB remains on track to generate 9% EPS recovery this year, and the potential new ALB with ROC boosts its growth potential longer term." - KeyBanc, 7/31/2014 "We believe ALB is well positioned for growth as it continues to invest in R and D for new products in its Performance Chemicals unit and should enter the lithium market through the acquisition of ROC." - RW Baird, 9/26/2014 "Albemarle's proposed $6B acquisition of Rockwood adds high growth, high margin and high multiple Lithium and Surface Treatment businesses while diluting the bromine business, itself a deterrent to some investors." - Deutsche, 8/1/2014 Creates Market Leader in Attractive Industries "[S]ubsequent completion of the proposed ROC acquisition would create a solid asset base of high-margin businesses with strong leadership positions in concentrated industries: lithium, bromine, catalysts and surface treatment." - GS, 8/11/2014 "On balance, we think the deal would create a premier producer of specialty chemicals, second only to DuPont among diversified specialty names, i.e. ex industrial gases and coatings pure-plays." - BofA Merrill Lynch, 7/16/2014 "We are upgrading our rating on ALB to Buy from Hold, on favorable portfolio implications associated with the proposed Rockwood acquisition, a perceived positive inflection in bromine, the potential for several positive catalysts near-term, and an anticipated valuation re-rating for the new post-merger Albemarle." - Topeka, 7/29/2014 "The acquisition gives Albemarle more direct leverage to electric vehicles and diversifies the portfolio away from bromine (in transition between growth cycles, at best) and catalysts (very lumpy order patterns)." - Jefferies, 7/15/2014 "ALB will possess a collection of high-margin specialty chemical businesses with leadership positions in industries with attractive, concentrated markets." - GS, 8/11/2014 "The weak performance in 2014 is a timely demonstration of ALB's need for portfolio diversification into businesses with a higher growth profile. The ROC acquisition is just what the doctor ordered." - SunTrust, 7/31/2014 Provides Compelling Synergy Opportunity "[T]argeted synergies of $100m are 7% of ROC's sales, which seems achievable to us since the average targeted synergies in a specialty chemical transaction has been 7% historically with most actual achieved synergies coming in higher than the initial estimate." - GS, 7/15/2014 "In particular, we are more comfortable with the $100 million in potential synergies from corporate costs, shared services, raw material purchasing, and asset base optimization. We note ALB's internal synergy target is higher than $100 million." - First Analysis, 8/5/2014 "For additional perspective, the $100mm synergy number represents well under 3% of the combined Company's pro forma annualized revenue run-rate, which implies the target could prove conservative, in our view. [ ... ] We also believe synergies extracted from the ALB/ROC combination will improve the combined firm's financial profile and return metrics." - Topeka, 7/29/2014 Source: Wall Street Research as of October 15, 2014 Albemarle 18 |  |

Significant Financial Benefits Improved Revenue Growth Consistent, predictable growth significantly above GDP Industry- leading Margins Pro-forma EBITDA margins of 25%+ Earnings Accretive Accretive to cash EPS in year one and adjusted EPS in year two Substantially accretive thereafter Strong Free Cash Flow Focus on rapid deleveraging in near term before share repurchases Expect to grow current annualized dividend of $1.10 per share Albemarle 19 |  |

Strong Free Cash Flow Allows De-leveraging Free Cash Flow $1,000 800 600 400 200 0 FCF Yield 10.0% 9.0% 8.0% 7.0% 6.0% 5.0% 4.0% 3.0% $275 $365 $500 $600 - $900 2013A(1) 2014PF(1) 2015PF (2) 3 - 5 years (2) Net-Debt-to-EBITDA Available for dividend increases, investments and share repurchases ALB Target leverage 2.0 - 2.5x FCF growth driven by earnings growth and low CAPEX requirements $500M+ annual free cash flow before one time tax payment in 2015 to repatriate ~$4B in existing and future cash NPV of tax benefit of cash repatriation strategy is greater than $750M Focus on rapidly reducing leverage achieving target by 2017 CAPEX in the range of 4-6% of revenue Remain committed to previously announced working capital reduction of $100M by 2015 Expect to maintain current annualized dividend of $1.10 per share and annual increases (1) 2013A and 2014PF FCF excludes the impact of rare earth and the divestiture of antioxidant, ibuprofen and propofol businesses and assets (closed August 31, 2014) (2) 2015PF and Next 3-5 years FCF yield calculated using pro-forma market capitalization post Rockwood acquisition Albemarle 20 |  |

Albemarle Acquisition of Rockwood: A Compelling Transaction Creates a premier specialty chemicals company with leading positions in attractive end markets around the world Accelerates Albemarle's strategy of bringing lithium and bromine together Strengthens growth potential across four, high-margin businesses - lithium, catalysts, bromine and surface treatment Differentiated, performance-based, technologies driving innovative solutions Capacity in place to serve future growth to drive improved profitability Outstanding cash generation capacity supports rapid deleveraging, ongoing dividend and investments to drive future growth Enhanced growth, expanded margins and improved cash flow drive shareholder value Albemarle 21 |  |

Appendix Albemarle |  |

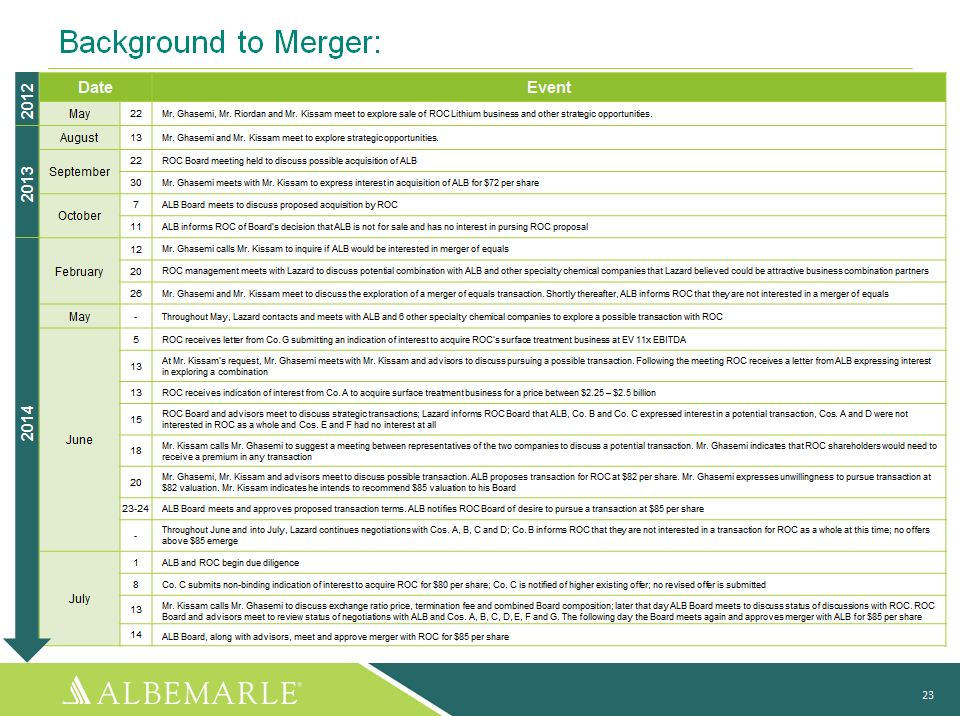

Background to Merger: Date Event 2012 May 22 Mr. Ghasemi, Mr. Riordan and Mr. Kissam meet to explore sale of ROC Lithium business and other strategic opportunities. 2013 August 13 Mr. Ghasemi and Mr. Kissam meet to explore strategic opportunities. September 22 ROC Board meeting held to discuss possible acquisition of ALB 30 Mr. Ghasemi meets with Mr. Kissam to express interest in acquisition of ALB for $72 per share October 7 ALB Board meets to discuss proposed acquisition by ROC 11 ALB informs ROC of Board's decision that ALB is not for sale and has no interest in pursing ROC proposal 2014 February 12 Mr. Ghasemi calls Mr. Kissam to inquire if ALB would be interested in merger of equals 20 ROC management meets with Lazard to discuss potential combination with ALB and other specialty chemical companies that Lazard believed could be attractive business combination partners 26 Mr. Ghasemi and Mr. Kissam meet to discuss the exploration of a merger of equals transaction. Shortly thereafter, ALB informs ROC that they are not interested in a merger of equals May - Throughout May, Lazard contacts and meets with ALB and 6 other specialty chemical companies to explore a possible transaction with ROC June 5 ROC receives letter from Co. G submitting an indication of interest to acquire ROC's surface treatment business at EV 11x EBITDA 13 At Mr. Kissam's request, Mr. Ghasemi meets with Mr. Kissam and advisors to discuss pursuing a possible transaction. Following the meeting ROC receives a letter from ALB expressing interest in exploring a combination 13 ROC receives indication of interest from Co. A to acquire surface treatment business for a price between $2.25 - $2.5 billion 15 ROC Board and advisors meet to discuss strategic transactions; Lazard informs ROC Board that ALB, Co. B and Co. C expressed interest in a potential transaction, Cos. A and D were not interested in ROC as a whole and Cos. E and F had no interest at all 18 Mr. Kissam calls Mr. Ghasemi to suggest a meeting between representatives of the two companies to discuss a potential transaction. Mr. Ghasemi indicates that ROC shareholders would need to receive a premium in any transaction 20 Mr. Ghasemi, Mr. Kissam and advisors meet to discuss possible transaction. ALB proposes transaction for ROC at $82 per share. Mr. Ghasemi expresses unwillingness to pursue transaction at $82 valuation. Mr. Kissam indicates he intends to recommend $85 valuation to his Board 23-24 ALB Board meets and approves proposed transaction terms. ALB notifies ROC Board of desire to pursue a transaction at $85 per share - Throughout June and into July, Lazard continues negotiations with Cos. A, B, C and D; Co. B informs ROC that they are not interested in a transaction for ROC as a whole at this time; no offers above $85 emerge July 1 ALB and ROC begin due diligence 8 Co. C submits non-binding indication of interest to acquire ROC for $80 per share; Co. C is notified of higher existing offer; no revised offer is submitted 13 Mr. Kissam calls Mr. Ghasemi to discuss exchange ratio price, termination fee and combined Board composition; later that day ALB Board meets to discuss status of discussions with ROC. ROC Board and advisors meet to review status of negotiations with ALB and Cos. A, B, C, D, E, F and G. The following day the Board meets again and approves merger with ALB for $85 per share 14 ALB Board, along with advisors, meet and approve merger with ROC for $85 per share Rockwood Lithium - Significant Recent Investments Have Positioned The Business for Growth Albemarle 23 |  |

Rockwood Lithium - Significant Recent Investments Have Positioned The Business for Growth CAPEX $24 $30 $76 $98 $145 $148 COMMENTARY Well invested global business Access to the highest quality and lowest cost Lithium raw materials (Brine in Chile and the U.S. and spodumene in Australia) Infrastructure supports growth in China market In 2011 and 2012, Rockwood Lithium invested approximately $50M in its high-purity lithium hydroxide plant at Kings Mountain, North Carolina for advanced batteries In 2012 and 2013, Rockwood Lithium invested $140M in its new 20,000 metric ton lithium carbonate plant at its La Negra, Chile facility Closed geologic basins resulting in some of the highest lithium concentrations globally In 2014, Rockwood acquired a 49% interest in Talison Lithium Talison owns the largest spodumene mine worldwide with 61.5 Mt of proven and probable mineral reserves at 2.8% LI2O with current mine life of 40 years Lowest cost producer of technical and chemical grade lithium concentrates Source: Company information Note: USD in millions Albemarle 24 |  |

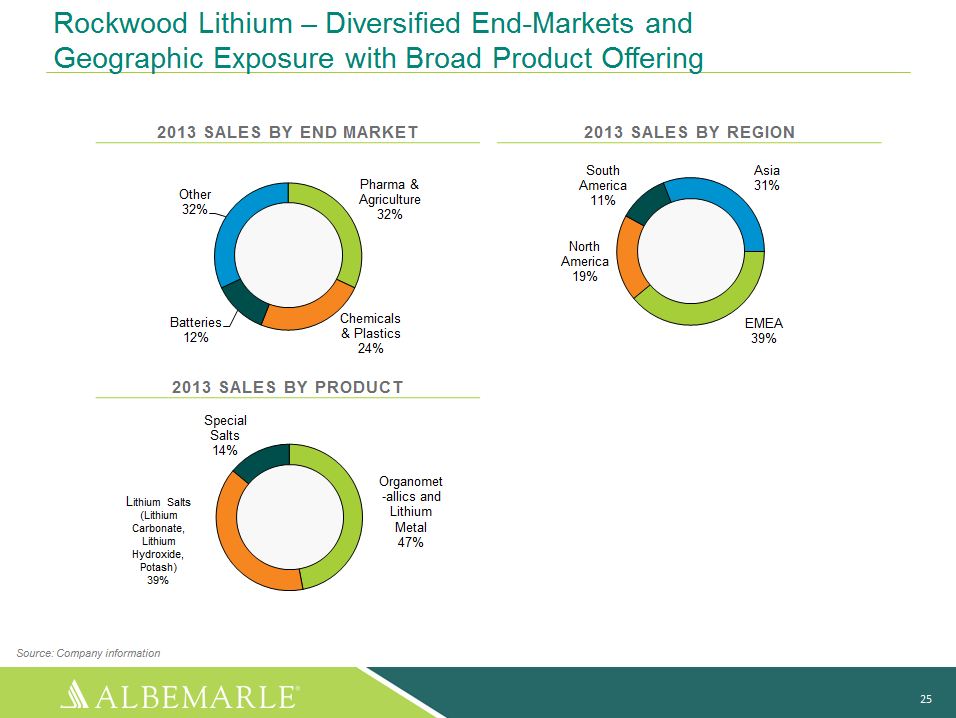

Rockwood Lithium - Diversified End-Markets and

Geographic Exposure with Broad Product Offering

2013 SALES BY END MARKET 2013 SALES BY REGION

Other

32%

Pharma and Agriculture

32%

South

America

11%

Asia

31%

North

America

19%

Batteries

12%

Chemicals

and Plastics

24%

EMEA

39%

2013 SALES BY PRODUCT

Special

Salts

14%

Lithium Salts (Lithium Carbonate, Lithium Hydroxide, Potash)

39%

Organomet

-allics and Lithium Metal

47%

Source: Company information

Albemarle 25

|  |

Rockwood Lithium - Low-Cost Lithium Brine Sources Resources in Chile and USA Desert environment to evaporate water and concentrate lithium salts enabling use of solar evaporation Closed geologic basins resulting in some of the highest lithium concentrations globally Good chemistry to allow further concentration and processing at low cost Atacama, CHILE Silver Peak, NEVADA Source: Company information Albemarle 26 |  |

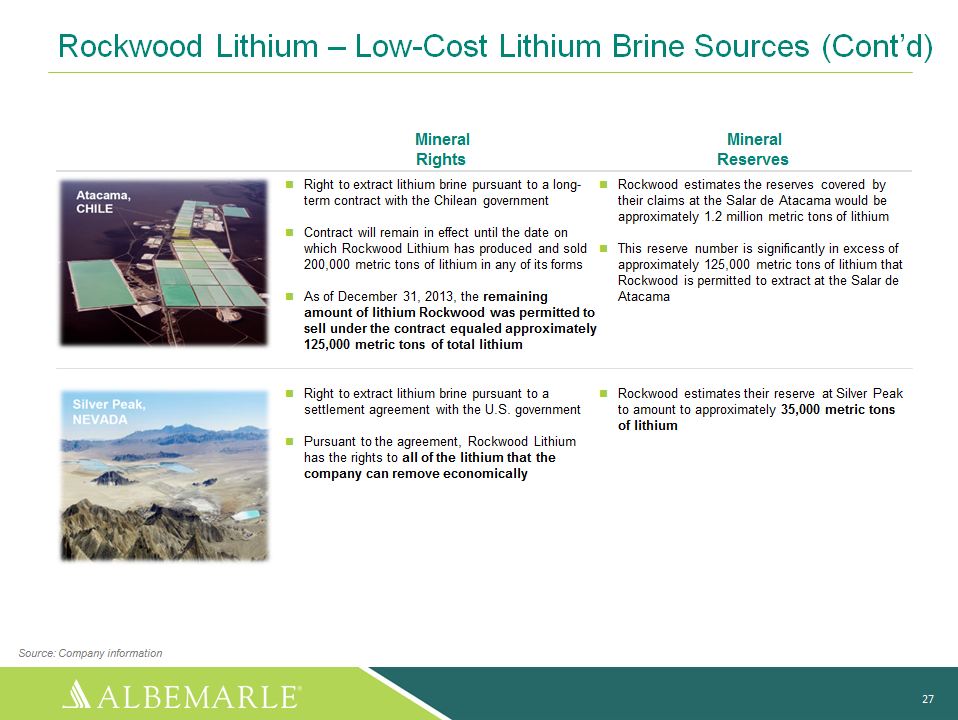

Rockwood Lithium - Low-Cost Lithium Brine Sources (Cont'd) Mineral Rights Right to extract lithium brine pursuant to a long- term contract with the Chilean government Contract will remain in effect until the date on which Rockwood Lithium has produced and sold 200,000 metric tons of lithium in any of its forms As of December 31, 2013, the remaining amount of lithium Rockwood was permitted to sell under the contract equaled approximately 125,000 metric tons of total lithium Mineral Reserves Rockwood estimates the reserves covered by their claims at the Salar de Atacama would be approximately 1.2 million metric tons of lithium This reserve number is significantly in excess of approximately 125,000 metric tons of lithium that Rockwood is permitted to extract at the Salar de Atacama Right to extract lithium brine pursuant to a settlement agreement with the U.S. government Pursuant to the agreement, Rockwood Lithium has the rights to all of the lithium that the company can remove economically Rockwood estimates their reserve at Silver Peak to amount to approximately 35,000 metric tons of lithium Source: Company information Albemarle 27 |  |

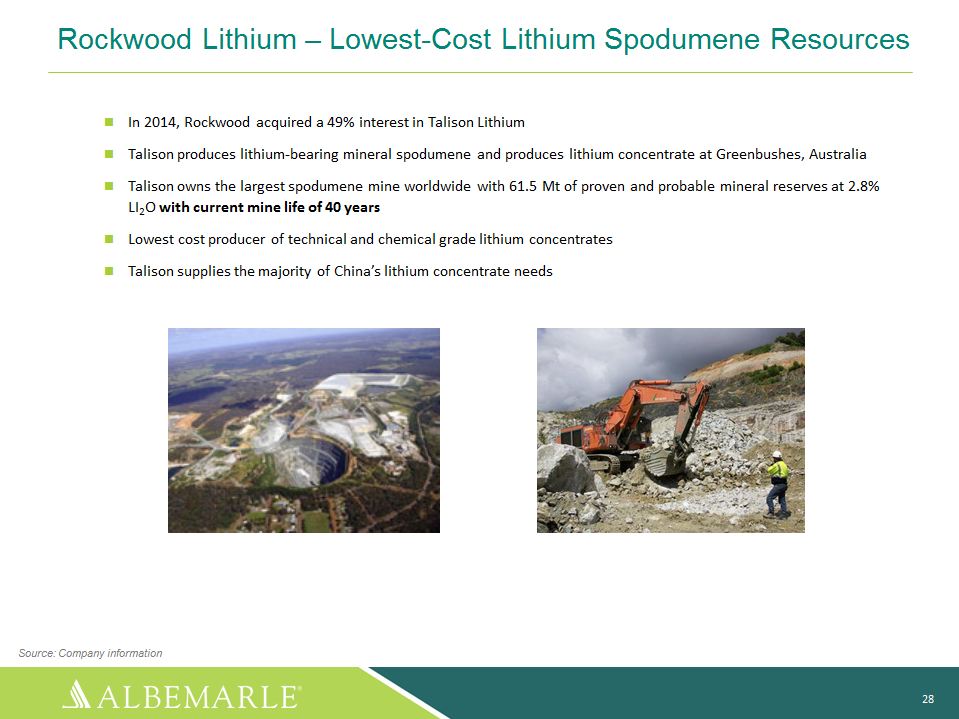

Rockwood Lithium - Lowest-Cost Lithium Spodumene Resources In 2014, Rockwood acquired a 49% interest in Talison Lithium Talison produces lithium-bearing mineral spodumene and produces lithium concentrate at Greenbushes, Australia Talison owns the largest spodumene mine worldwide with 61.5 Mt of proven and probable mineral reserves at 2.8% LI2O with current mine life of 40 years Lowest cost producer of technical and chemical grade lithium concentrates Talison supplies the majority of China's lithium concentrate needs Source: Company information Albemarle 28 |  |

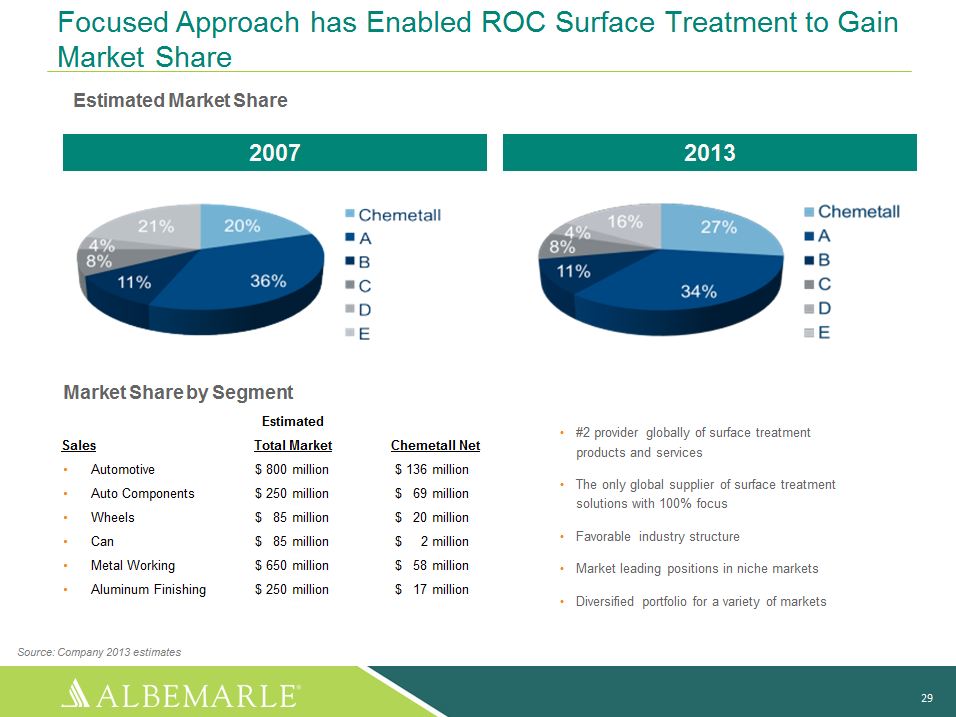

Focused Approach has Enabled ROC Surface Treatment to Gain

Market Share

Estimated Market Share

2007

2013

Market Share by Segment

Estimated

#2 provider globally of surface treatment

Sales

Estimated

Total Market Chemetall Net

Automotive $ 800 million $ 136 million

Auto Components $ 250 million $ 69 million

Wheels $ 85 million $ 20 million

Can $ 85 million $ 2 million

Metal Working $ 650 million $ 58 million

Aluminum Finishing $ 250 million $ 17 million

The only global supplier of surface treatment

solutions with 100% focus

Favorable industry structure

Market leading positions in niche markets

Diversified portfolio for a variety of markets

Source: Company 2013 estimates

Albemarle 29

|  |

Surface Treatment Markets

Automotive OEM

Globally harmonized technologies available for

NDT products, inhibitors, conversion coatings,

cleaners, coolants, activating and passivating

agents and maintenance chemicals. Aerospace

Sealants and sealant removers, NDT products and

equipment, corrosion protection, cleaners,

pretreatment and paint strippers for airframe,

aircraft operation and aero-engine applications.

Automotive Components

Broad portfolio of technologies from cleaners to

conversion coatings for all kinds of components

and substrates, such as steel or aluminium

wheels, bumpers or diesel injection systems. Coil

A variety of technologies for coil coating and

galvanizing processes. Prepainted and passivated

metal sheets are used in automotive, building,

electrical and packaging industries. Metal (Cold)

Forming

Tube industry (from the blank tube to the

precision tube), wire industry (from cold heading

to spring steel wire) and cold extrusion (complex

geometries extruded net shape).

General Industry

Broad portfolio of metal pretreatment technologies for all

kinds of applications such as furniture, garden fences,

trains, electrical cabines and many more. Heavy Equipment

Eco-friendly and efficient technologies ensure an

excellent and long- term surface quality for off-road

vehicles, construction equipment, industrial machines

and agricultural vehicles.

Appliances, HVAC

Broad portfolio eco-friendly, nickel-free and chrome-free

processes -

from cleaners, conversion coatings, paint detackification to

maintenance chemicals.

Metal Packaging

High efficient cleaners, conversion treatments and

mobility enhancers for the aluminium beverage can

manufacturing.

Aluminium Finishing

Pretreatment technologies, anodizing processes and

service products ensure an excellent surface in the

architectural and construction industry.

Albemarle 30

|  |

Surface Treatment - Net Sales

ROC Net Sales by End-Market

Aluminium

Finishing

2%

Cold Forming

7%

Competitors

Henkel AG and Co. KGaA Nihon Parkerizing Co., Ltd. PPG

Industries, Inc. Nippon Paint Co., Ltd.

Coi

10%

Automotive

11%

Aerospace

15%

General

Industry

37%

Automotive

OEM

17%

Major Customers Daimler AG ArcelorMittal Volkswagen AG

European Aeronautic Defense and Space Company (EADS) N.V.

Ford

Renault-Nissan

Source: Company 2013 estimates

Albemarle 31

|  |

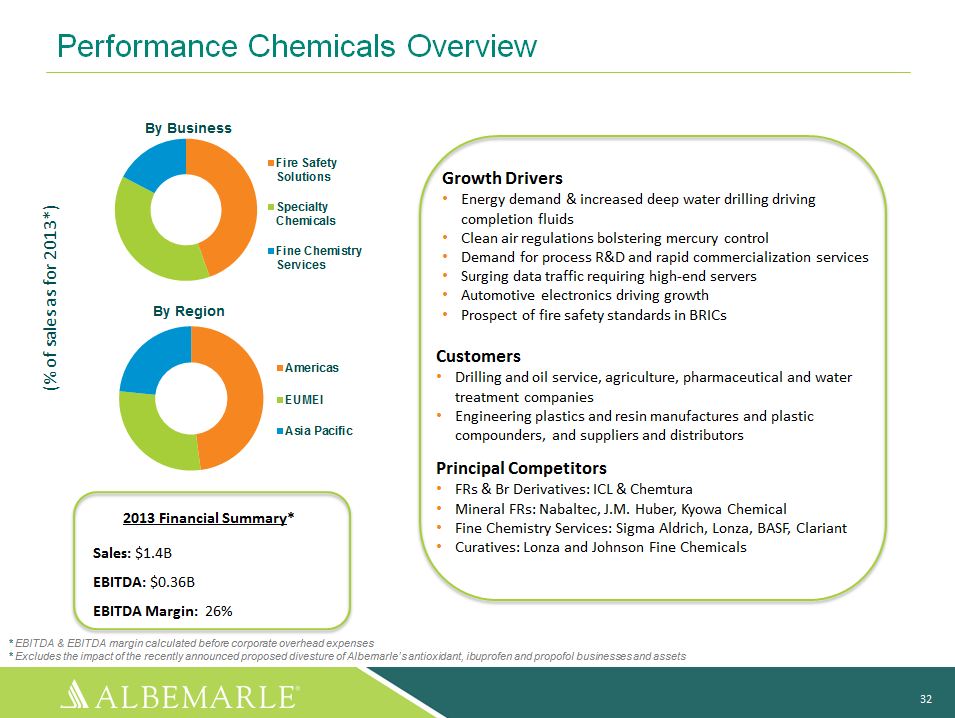

Performance Chemicals Overview

By Business

By Region

Fire Safety

Solutions

Specialty

Chemicals

Fine Chemistry

Services

Growth Drivers

Energy demand and increased deep water drilling driving

completion fluids Clean air regulations bolstering mercury

control Demand for process R and D and rapid

commercialization services Surging data traffic requiring

high-end servers Automotive electronics driving growth

Prospect of fire safety standards in BRICs

Americas

EUMEI

Asia Pacific

2013 Financial Summary* Sales: $1.4B

EBITDA: $0.36B

EBITDA Margin: 26%

Customers

Drilling and oil service, agriculture, pharmaceutical and

water treatment companies Engineering plastics and resin

manufactures and plastic compounders, and suppliers and

distributors

Principal Competitors

FRs and Br Derivatives: ICL and Chemtura

Mineral FRs: Nabaltec, J.M. Huber, Kyowa Chemical Fine

Chemistry Services: Sigma Aldrich, Lonza, BASF, Clariant

Curatives: Lonza and Johnson Fine Chemicals

* EBITDA and EBITDA margin calculated before corporate

overhead expenses * Excludes the impact of the recently

announced proposed divesture of Albemarle's antioxidant,

ibuprofen and propofol businesses and assets

Albemarle 32

|  |

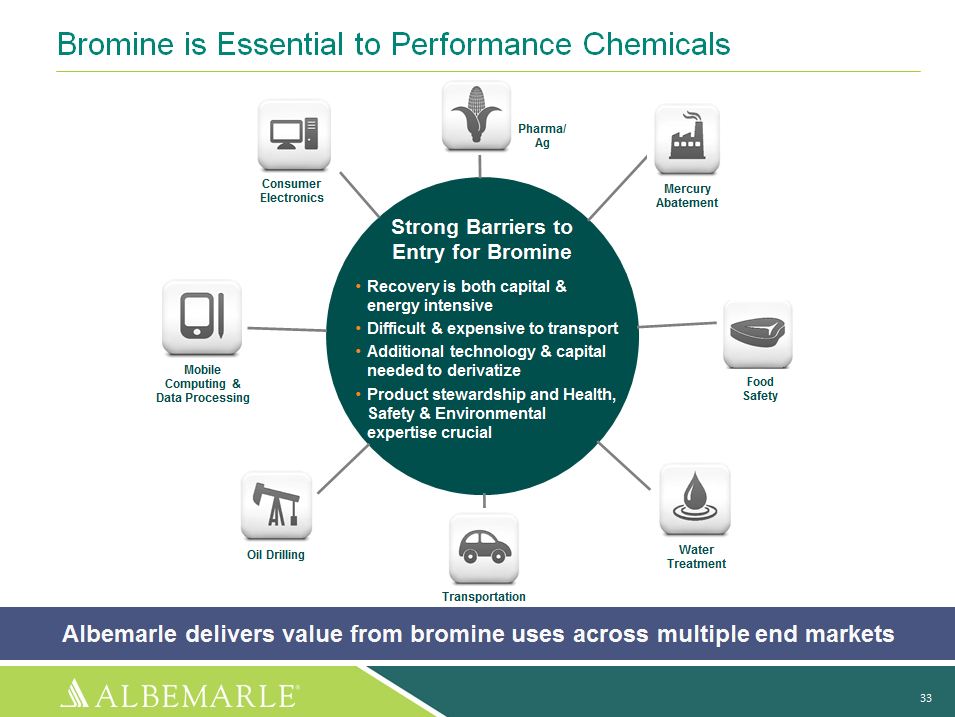

Bromine is Essential to Performance Chemicals Pharma/ Ag Mobile Computing and Data Processing Consumer Electronics Strong Barriers to Entry for Bromine Recovery is both capital and energy intensive Difficult and expensive to transport Additional technology and capital needed to derivatize Product stewardship and Health, Safety and Environmental expertise crucial Mercury Abatement Food Safety Oil Drilling Water Treatment Transportation Albemarle delivers value from bromine uses across multiple end markets Albemarle 33 |  |

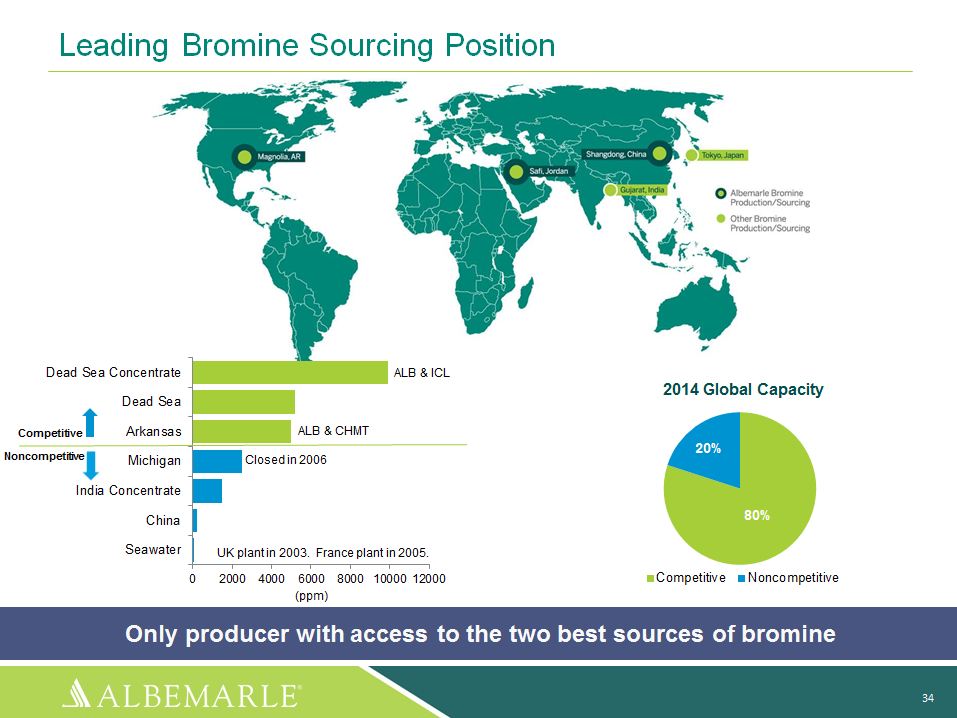

Leading Bromine Sourcing Position Dead Sea Concentrate Dead Sea ALB and ICL 2014 Global Capacity Competitive Noncompetitive Arkansas Michigan ALB and CHMT Closed in 2006 20% India Concentrate China 80% Seawater UK plant in 2003. France plant in 2005. 0 2000 4000 6000 8000 10000 12000 (ppm) Competitive Noncompetitive Only producer with access to the two best sources of bromine Albemarle 34 |  |

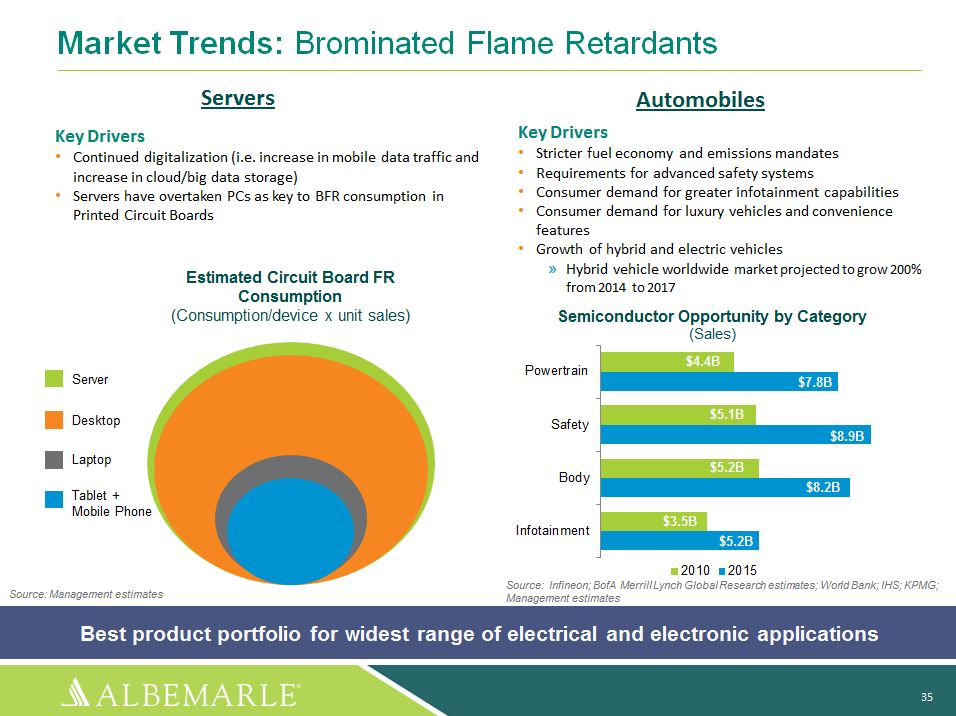

Market Trends: Brominated

Flame Retardants

Key Drivers

Servers

Key Drivers

Automobiles

Continued digitalization (i.e. increase in mobile data

traffic and increase in cloud/big data storage) Servers

have overtaken PCs as key to BFR consumption in

Printed Circuit Boards

Estimated Circuit Board FR Consumption

(Consumption/device x unit sales)

Stricter fuel economy and emissions mandates

Requirements for advanced safety systems

Consumer demand for greater infotainment capabilities

Consumer demand for luxury vehicles and convenience features

Growth of hybrid and electric vehicles

Hybrid vehicle worldwide market projected to grow 200%

from 2014 to 2017

Semiconductor Opportunity by Category

(Sales)

$4.4B

Server Desktop Laptop

Tablet +

Mobile Phone

Powertrain

Safety Body Infotainment

$3.5B

$5.1B

$5.2B

$5.2B

$7.8B

$8.9B

$8.2B

Source: Management estimates

2010 2015

Source: Infineon; BofA Merrill Lynch Global Research

estimates; World Bank; IHS; KPMG; Management estimates

Best product portfolio for widest range of electrical

and electronic applications

Albemarle 35

|  |

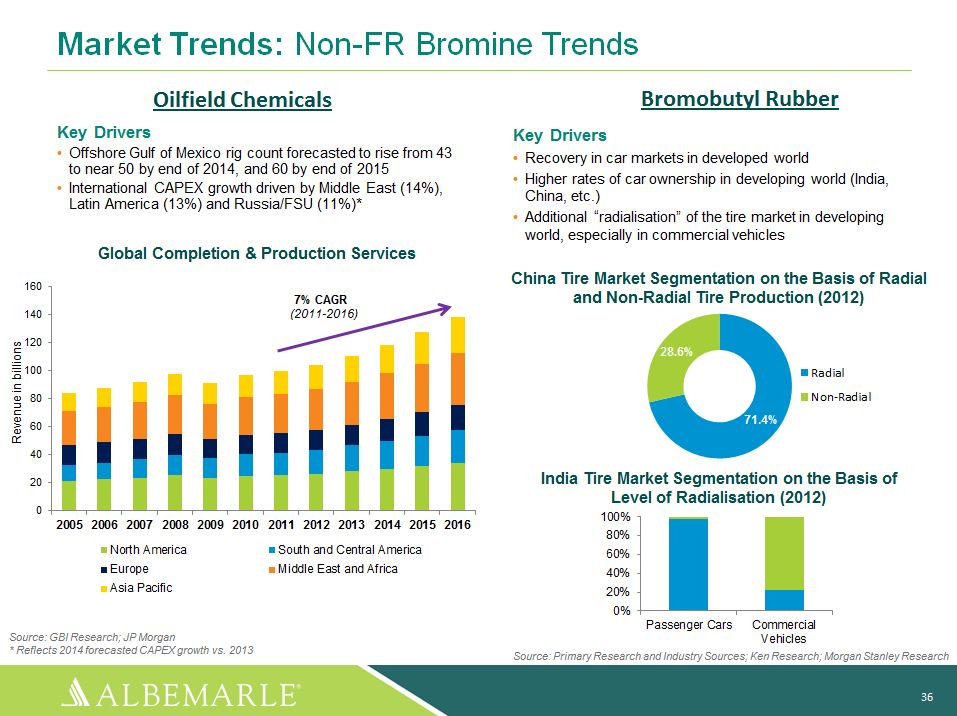

Key Drivers

Market Trends: Non-FR Bromine Trends

Oilfield Chemicals Bromobutyl Rubber

Key Drivers

160

140

Offshore Gulf of Mexico rig count forecasted to rise from 43

to near 50 by end of 2014, and 60 by end of 2015

International CAPEX growth driven by Middle East (14%),

Latin America (13%) and Russia/FSU (11%)* Global

Completion and Production Services

7% CAGR

(2011-2016)

Recovery in car markets in developed world

Higher rates of car ownership in developing world (India,

China, etc.)

Additional "radialisation" of the tire market in developing

world, especially in commercial vehicles China Tire Market

Segmentation on the Basis of Radial and Non-Radial Tire

Production (2012)

Revenue in billions

120

100

80

60

28.6%

71.4%

Radial

Non-Radial

40

20

0

2005 2006 2007 2008 2009 2010 2011 2012 2013 2014 2015 2016

North America South and Central America

Europe Middle East and Africa

Asia Pacific

India Tire Market Segmentation on the Basis of

Level of Radialisation (2012)

100%

80%

60%

40%

20%

0%

Source: GBI Research; JP Morgan

* Reflects 2014 forecasted CAPEX growth vs. 2013

Passenger Cars Commercial

Vehicles

Source: Primary Research and Industry Sources;

Ken Research; Morgan Stanley Research

Albemarle 36

|  |

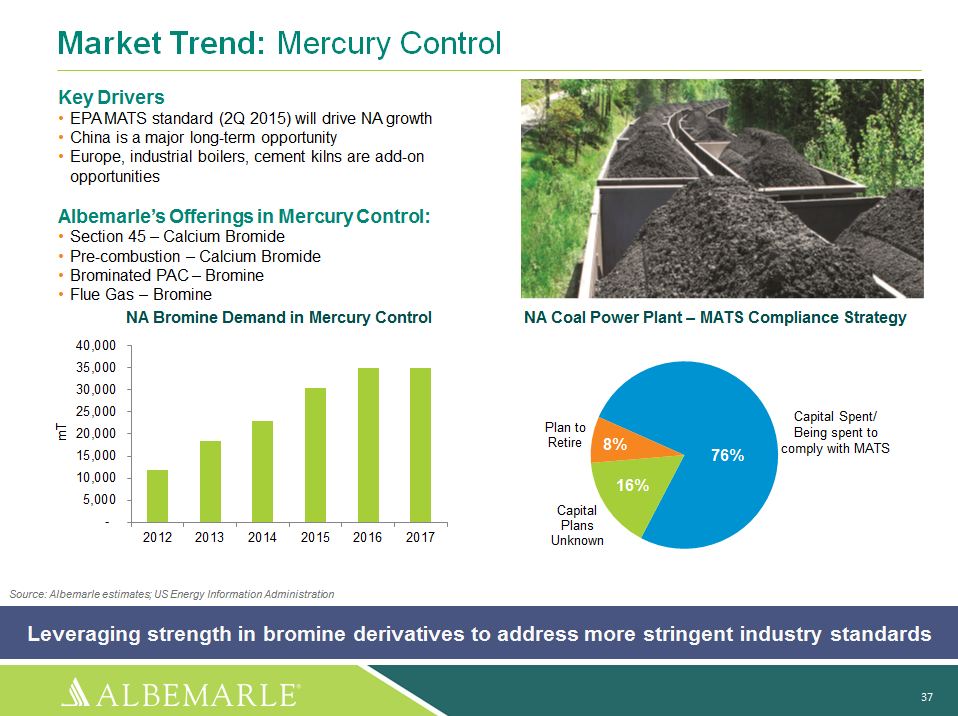

Market Trend: Mercury Control

Key Drivers

EPA MATS standard (2Q 2015) will drive NA growth

China is a major long-term opportunity

Europe, industrial boilers, cement

kilns are add-on opportunities

Albemarle's Offerings in Mercury Control:

Section 45 - Calcium Bromide

Pre-combustion - Calcium Bromide

Brominated PAC - Bromine

Flue Gas - Bromine

NA Bromine

Demand in

Mercury

Control

NA Coal Power Plant - MATS Compliance

Strategy

40,000

35,000

30,000

25,000

MT

20,000

15,000

10,000

5,000

-

Plan to

Retire

Capital

Plans Unknown

8%

16%

76%

Capital Spent/ Being spent to comply with MATS

2012 2013 2014 2015 2016 2017

Source: Albemarle estimates; US Energy Information

Administration Leveraging strength in bromine derivatives

to address more stringent industry standards

Albemarle 37

|  |

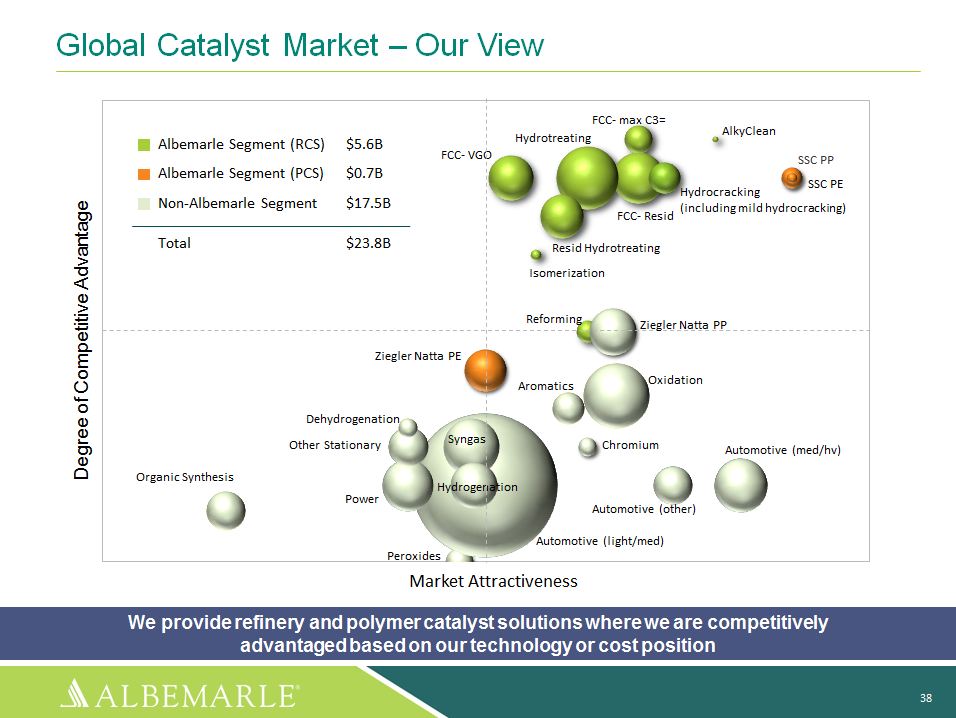

Global Catalyst Market - Our View

Albemarle Segment (RCS) Albemarle Segment (PCS)

$5.6B

$0.7B

FCC- VGO

Hydrotreating

FCC- max C3=

AlkyClean

Hydrocracking

SSC PP SSC PE

Non-Albemarle Segment

Total

$17.5B

$23.8B

FCC- Resid (including mild hydrocracking) Resid Hydrotreating

Isomerization

Degree of Competitive Advantage

Reforming

Ziegler Natta PP

Ziegler Natta PE

Aromatics Oxidation

Organic

Synthesis

Dehydrogenation

Other Stationary

Power

Syngas

Hydrogenation

Chromium

Automotive (other)

Automotive (med/hv)

Peroxides

Automotive (light/med)

Market Attractiveness

We provide refinery and polymer catalyst solutions

where we are competitively advantaged

based on our technology or cost position

Albemarle 38

|  |

Catalyst Solutions Overview

Refinery Catalyst Solutions (RCS)

Heavy Oil Upgrading (HOU)

FCC catalysts for resid

FCC catalysts for max propylene

FCC catalysts for vacuum gas oil

Clean Fuels Technologies (CFT)

Hydroprocessing catalysts

Isomerization

Technology licensing

Performance Catalyst Solutions (PCS)

Polyolefin catalysts and components

Organometallics and co-catalysts

Electronic materials - high purity metal organics

($ in millions)

$1,200

$1,000

$800

$600

$400

$200

$-

Net Sales*

2010 2011 2012 2013

By Business

Net Sales Distribution*

By Region

($ in millions)

$300

$250

Segment Income*

Segment Income

Segment Margin

35%

30%

76%

24%

PCS RCS

21%

35%

44%

Americas

EUMEI

Asia Pacific

$200

$150

$100

$50

25%

20%

15%

10%

5%

2013 Net

Sales:

$1B

$- 0%

2010 2011 2012 2013

*Financial data for 2010 - 2013 excludes the impact of rare

earth and the recently announced proposed

divesture of Albemarle's antioxidant,

ibuprofen and propofol businesses and assets

Albemarle 39

|  |

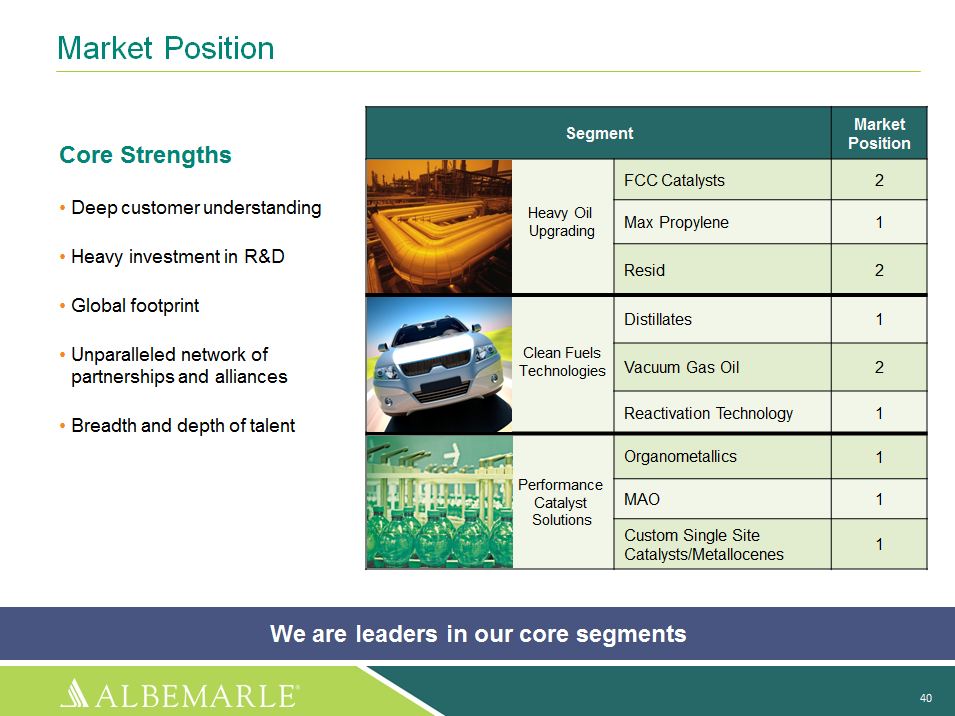

Market Position

Core Strengths

Deep customer understanding

Heavy investment in R and D

Global footprint

Unparalleled network of partnerships and alliances

Breadth and depth of talent

Segment

Market

Position

Heavy Oil

Upgrading

FCC Catalysts

2

Max Propylene

1

Resid

2

Clean Fuels

Technologies

Distillates

1

Vacuum Gas Oil

2

Reactivation Technology

1

Performance Catalyst Solutions

Organometallics

1

MAO

1

Custom Single Site

Catalysts/Metallocenes

1

We are leaders in our core segments

Albemarle 40

|  |

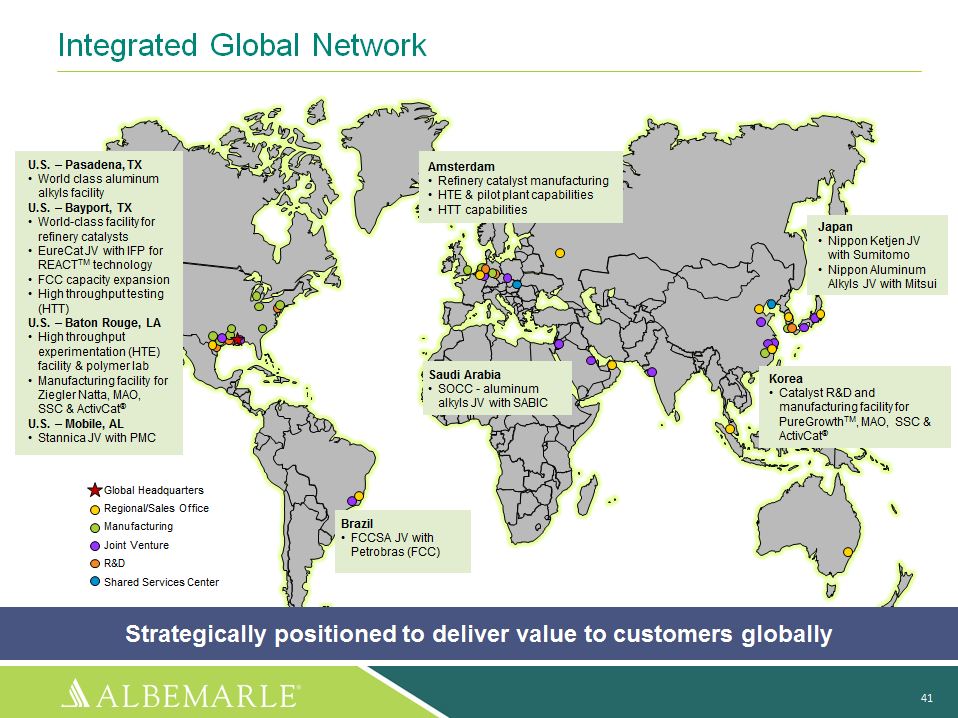

Integrated Global Network

U.S. - Pasadena, TX

World class aluminum alkyls facility

U.S. - Bayport, TX

World-class facility for refinery catalysts

EureCat JV with IFP for

REACTTM technology

FCC capacity expansion

High throughput testing

(HTT)

U.S. - Baton Rouge, LA

High throughput experimentation (HTE) facility and polymer lab

Manufacturing facility for

Amsterdam

Refinery catalyst manufacturing

HTE and pilot plant capabilities

HTT capabilities

. i , i

i,

Saudi Arabia

Korea

Japan

Nippon Ketjen JV

with Sumitomo

Nippon Aluminum

Alkyls JV with Mitsui

Ziegler Natta, MAO, SSC and ActivCat(R)

U.S. - Mobile, AL

Stannica JV with PMC

SOCC - aluminum

alkyls JV with SABIC

Catalyst R and D and manufacturing facility for PureGrowthTM,

MAO, SSC and ActivCat(R)

Global Headquarters Regional/Sales Office Manufacturing

Joint Venture

R and D

Shared Services

Center

Brazil

FCCSA JV with

Petrobras (FCC)

Strategically positioned to deliver value to

customers globally

Albemarle 41

|  |

Additional Information Important Information for Stockholders and Investors Nothing in this document or the discussions that follow shall constitute a solicitation to buy or subscribe for or an offer to sell any securities of Albemarle or Rockwood or a solicitation of any vote or approval. In connection with the proposed transaction, Albemarle filed with the SEC a Registration Statement on Form S-4 (the "Registration Statement") on August 27, 2014, which includes the preliminary joint proxy statement of Albemarle and Rockwood and which also constitutes a preliminary prospectus of Albemarle. The definitive joint proxy statement/prospectus has been mailed to stockholders of Albemarle and Rockwood. INVESTORS AND SECURITY HOLDERS ARE URGED TO READ THE REGISTRATION STATEMENT AND JOINT PROXY STATEMENT/PROSPECTUS (INCLUDING ANY AMENDMENTS OR SUPPLEMENTS THERETO) AND ANY OTHER RELEVANT DOCUMENTS FILED WITH THE SEC, BECAUSE THEY CONTAIN IMPORTANT INFORMATION. Investors and security holders may obtain a free copy of the Registration Statement and joint proxy statement/prospectus, as well as other documents filed by Albemarle and Rockwood, at the SEC's website (www.sec.gov). Copies of the Registration Statement and joint proxy statement/prospectus and the SEC filings that are be incorporated by reference therein may also be obtained for free by directing a request to either: Albemarle Corporation, 451 Florida Street, Baton Rouge, Louisiana 70801, USA, Attention: Investor Relations, Telephone: +1 (225) 388-7322, or to Rockwood Holdings, Inc., 100 Overlook Center, Princeton, New Jersey 08540, USA, Attn: Investor Relations, Telephone +1 (609) 524-1101. Albemarle 42 |  |