UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM N-CSR

CERTIFIED SHAREHOLDER REPORT OF REGISTERED MANAGEMENT INVESTMENT COMPANIES

Investment Company Act file number 811-21719

INVESTMENT MANAGERS SERIES TRUST

(Exact name of registrant as specified in charter)

235 W. Galena Street

Milwaukee, WI 53212

(Address of principal executive offices) (Zip code)

Diane J. Drake

Mutual Fund Administration, LLC

2220 E. Route 66, Suite 226

Glendora, CA 91740

(Name and address of agent for service)

(626) 385-5777

Registrant's telephone number, including area code

Date of fiscal year end: December 31

Date of reporting period: December 31, 2021

Item 1. Report to Stockholders.

| (a) | The registrant’s annual report transmitted to shareholders pursuant to Rule 30e-1 under the Investment Company Act of 1940, as amended (the “Investment Company Act”), is as follows: |

Aristotle/Saul Global Equity Fund

Class I Shares (ARSOX)

Aristotle International Equity Fund

Class I Shares (ARSFX)

Aristotle Strategic Credit Fund

Class I Shares (ARSSX)

Aristotle Value Equity Fund

Class I Shares (ARSQX)

Aristotle Small Cap Equity Fund

Class I Shares (ARSBX)

Aristotle Core Equity Fund

Class I Shares (ARSLX)

ANNUAL REPORT

December 31, 2021

Aristotle Funds

Each a series of Investment Managers Series Trust

Table of Contents

| Aristotle/Saul Global Equity Fund | |

| Shareholder Letter | 1 |

| Fund Performance | 10 |

| Schedule of Investments | 12 |

| Aristotle International Equity Fund | |

| Shareholder Letter | 16 |

| Fund Performance | 24 |

| Schedule of Investments | 25 |

| Aristotle Strategic Credit Fund | |

| Shareholder Letter | 29 |

| Fund Performance | 37 |

| Schedule of Investments | 39 |

| Aristotle Value Equity Fund | |

| Shareholder Letter | 46 |

| Fund Performance | 54 |

| Schedule of Investments | 55 |

| Aristotle Small Cap Equity Fund | |

| Shareholder Letter | 59 |

| Fund Performance | 67 |

| Schedule of Investments | 68 |

| Aristotle Core Equity Fund | |

| Shareholder Letter | 73 |

| Fund Performance | 82 |

| Schedule of Investments | 83 |

| Statements of Assets and Liabilities | 87 |

| Statements of Operations | 89 |

| Statements of Changes in Net Assets | 91 |

| Financial Highlights | 97 |

| Notes to Financial Statements | 103 |

| Report of Independent Registered Public Accounting Firm | 118 |

| Supplemental Information | 119 |

| Expense Examples | 131 |

This report and the financial statements contained herein are provided for the general information of the shareholders of the Aristotle Funds. This report is not authorized for distribution to prospective investors in the Funds unless preceded or accompanied by an effective prospectus.

www.aristotlefunds.com

Dear Fellow Shareholders,

Markets Review

In a year filled with uncertainty, global economies proved largely resilient. Even in the face of supply-chain disruptions and multiple variants of the COVID-19 virus, global recovery continued throughout the period. Themes from 2020, such as central bank policy decisions and vaccine distribution, persisted.

Overall, the MSCI ACWI Index (Net) had a full-year return of 18.54%, while the Bloomberg Global Aggregate Bond Index had a calendar-year return of -4.71%. In terms of style, value stocks outperformed their growth counterparts during the year, with the MSCI ACWI Value Index (Net) outperforming the MSCI ACWI Growth (Net) by 2.52%.

Throughout the year, investors focused on the progress of the global recovery. Although corporate revenues and earnings continued to rebound during the fourth quarter, the IMF announced a slight downward revision to its 2021 global real GDP growth projections due to continued supply disruptions and uncertain pandemic dynamics. These conditions have caused shortages of key inputs, lowered manufacturing activity and fueled inflation across the globe.

In addition to a global shipping crisis and semiconductor shortages, the energy sector also captured numerous headlines as robust demand outpaced supply, causing prices to surge. After a historic drop in energy consumption in 2020, the global economic recovery and a long and cold winter in the Northern Hemisphere have driven a strong rebound in demand, while the ongoing shift to renewables has impacted production and future investments in fossil fuels. Although OPEC and countries such as Russia have pledged to boost supply, the energy crunch has highlighted issues in long-term production. Furthermore, rising energy prices have contributed to an inflation loop as the prices of energy-intensive materials like nickel, steel and silicon have all risen.

Increased inflation, combined with an uncertain recovery, has created policy challenges for central banks. On one hand, the rhetoric on inflation being “transitory” softened as many central banks took a hawkish approach. During the quarter, the European Central Bank announced a gradual phaseout of its bond purchase program and the Federal Reserve started tapering its bond purchases, while countries like the U.K., Russia and Mexico raised interest rates. On the other hand, policy in Southeast Asia was largely unchanged, and China announced an easing of its monetary policy that will likely include further cuts to lending rates.

On the COVID front, the Omicron variant became the dominant strain in areas such as the U.K. and the U.S. The number of new daily cases reached as high as ~1,750,000, the highest reported figure during the pandemic, with Europe and the Americas reporting the greatest number of cases.

Performance data quoted here represents past performance. Past performance is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call (844) 274-7868.

FOR MORE INFORMATION, PLEASE CONTACT:

Phone: (888) 661-6691 | Email: funds@aristotlecap.com | Web: www.aristotlefunds.com

| 1 |

Although we are happy to report another strong year, the constant twists, turns and pivots of this past year are a reminder of the fragility of the short term. Factors such as the possibility of new variants, the timing of a full recovery, fiscal and monetary policy decisions, and market sentiment are topics better left for reporters. We believe investment managers (and their clients) are best positioned to create lasting value by minimizing distractions and focusing on the long term.

Performance Review

The Aristotle/Saul Global Equity Fund posted a total return of 19.54% at NAV for the year ending December 31, 2021, while the MSCI ACWI Index (Net) returned 18.54% and the MSCI World Index (Net) returned 21.82% over the same period.

The Fund’s outperformance relative to the MSCI ACWI Index (Net) over the year can be attributed to security selection, while sector allocation detracted from relative performance. Security selection in Consumer Discretionary and Materials as well as an underweight in Communication Services contributed the most to relative performance. Conversely, security selection in Industrials, Communication Services and Information Technology detracted the most from relative performance.

Compared to the Index, the Fund remains underweight Emerging Markets and U.S. equities and overweight Japanese equities; this relative positioning is the result of bottom-up, fundamental analysis and not an expression of a top-down macro view. Security selection in Europe & Middle East and Japan as well as an underweight in Emerging Markets contributed the most to relative performance for the year, while security selection in Emerging Markets as well as an overweight to Japan and an underweight to U.S. equities detracted the most from relative performance.

2021 Top Contributors to Relative Fund Return | 2021 Top Detractors from Relative Fund Return | |

| Nemetschek | Samsung | |

| Martin Marietta Materials | ||

| Lennar | AIA Group | |

| Penske Automotive | PayPal | |

| Danaher | FANUC |

Aggregates producer Martin Marietta Materials was one of the top contributors for the year, as it delivered year-to-date records for revenues and gross profit. A unique combination of higher organic volumes and price increases was able to offset significantly higher energy-related costs. The company also completed its acquisition of Lehigh Hanson’s West Region business, the second-largest acquisition in its history, increasing the firm’s presence in California and Arizona. Past acquisitions, including Texas Industries and Bluegrass Materials, have been, in our opinion, successfully integrated and have positioned the company with a coast-to-coast footprint and meaningful presence in states with high population inflows and what we think are solid underlying economies (i.e., Texas, Colorado, California, North Carolina, Georgia and Florida). Consistent with its acquisition practices, the company is committed to lowering its debt within the next 18 months. We believe the firm’s prudent capital spending, value-enhancing acquisitions, FREE cash flow generation and “value over volume” pricing strategy position the company to continue to benefit from secular demand trends, including single-family housing and federal and state-level infrastructure investment, as well as non-residential construction (e.g., warehouse and data centers).

| 2 |

Lennar, one of the nation’s largest homebuilders, was a primary contributor for the year. Despite supply-chain challenges affecting everything from the ability to source garage doors, windows and paint, to labor shortages impacting numerous installations, Lennar was able to deliver nearly 60,000 homes during the year, a 13% year-over-year growth in deliveries, while also achieving gross and net margin improvements. Such results highlight management’s focus and ability to execute amidst challenging short-term conditions while continuing to deliver on its longer-term strategic plan. To that effect, the firm made progress toward its asset-light model, where currently it controls more than half of its land through the use of options (up from 39% in 2020). This has enhanced the company’s FREE cash flow generation, allowing for the retirement of $850 million of debt and the repurchase of nearly $1 billion in stock in the most recent quarter. Furthermore, as part of its long-time efforts to incorporate technology into its business, Lennar announced commitments with Veev, a vertically integrated end-to-end panelized building technology company, and ICON, a 3D printing construction technology company, to build new communities utilizing their innovative technologies.

Twitter, the digital news platform, was one of the largest detractors this year. Despite recording positive results, concerns regarding the company’s growth and execution weighed on Twitter’s share price. Furthermore, during the fourth quarter, Jack Dorsey, Chairman and CEO of Twitter announced his resignation from both roles. Mr. Dorsey is succeeded by Parag Agrawal as CEO and Bret Taylor (CEO of Salesforce) as Chairman. Mr. Agrawal has been with Twitter for more than a decade and has served as CTO since 2017. We look forward to meeting with Mr. Agrawal and learning more about his leadership style and vision for Twitter.

AIA Group, a pan-Asian life insurance company headquartered in Hong Kong, was one of the largest detractors for the year. Shares declined despite continued improvements in fundamentals and progress further establishing AIA Group’s direct presence in mainland China, a catalyst we previously identified. AIA Group has benefited from an increasingly technology-enabled and productive agency salesforce; we believe this has helped the company deftly navigate pandemic-related travel restrictions. In fact, the company’s VONB* advanced 15% in the first nine months of 2021, with all areas outside of Hong Kong exceeding pre-pandemic levels. In our opinion, the advances in mainland China are more notable than the interim results. With the recent approval from the China Banking and Insurance Regulatory Commission to begin operations in the Hubei province, AIA Group now has operations in eight provinces, providing what we consider to be a unique platform to further penetrate this increasingly large market.

| * | Value of New Business (VONB) is an insurance term for the present value of new business written during a period. |

| 3 |

Investment Activity

During the year, we made the following purchases and sales in the Fund.

| 2021 Fund Purchases | 2021 Fund Sales | |||

| GlaxoSmithKline | 1Q2021 | Pioneer Natural Resources | 1Q2021 | |

| Nemetschek | 1Q2021 | ORIX | 1Q2021 | |

| Rational | 2Q2021 | Toray | 1Q2021 | |

| Pan Pacific International | 2Q2021 | Hoshizaki | 2Q2021 | |

| Honeywell | 2Q2021 | Novartis | 2Q2021 | |

| FirstCash | 3Q2021 | Penske Automotive | 4Q2021 | |

| Rentokil Initial | 4Q2021 | |||

One of our objectives is to clearly articulate the thought process behind our investments to our fellow shareholders. Below is an example of a sale (Penske Automotive) and a purchase (Rentokil Initial) we made in the Fund this year. Those securities were the last sale and purchase for the year.

Sale

We first became owners in Penske, one of the world’s largest automotive dealership groups, during the second quarter of 2016. During our holding period, the company executed on many of the catalysts we initially identified, including benefiting from industry consolidation, as well as its high-margin parts and service business capitalizing on increased car complexity. Though we will continue to admire Penske’s growing global presence and efforts to enhance the customer experience at its predominately luxury-focused dealerships, we decided to exit our position to fund what we believe is a more optimal investment in Rentokil.

Purchase

Founded in 1925, Rentokil Initial is a U.K.-based global provider of pest control, commercial hygiene and property care services. The company primarily operates in Europe and North America and recorded over £2.8 billion ($3.8 billion) of revenue in 2020.

In 2008, when current CEO Andy Ransom joined Rentokil, the company began a significant transformation. Less-attractive segments were shed, and proceeds were focused into the higher-margin Pest Control business. Most recently, Rentokil announced a $6.7 billion acquisition of Terminix, a leading residential and commercial pest control services provider in the U.S. The merger is expected to close in the second half of 2022, and we believe the financial and strategic rationales to be sound. The proforma entity will be the largest pest control company in North America, the world’s largest pest control market, and establishes the company as the leading global pest control company.

| 4 |

As a result, Rentokil will derive the vast majority of revenue from its Pest Control (~75% of sales) and Hygiene (~20%) segments. Pest Control provides services that protect customers from pest infestations (e.g., bedbugs, roaches, mice, termites), while the Hygiene segment, through its Initial brand, is one of the largest providers of commercial bathroom products and services in the industry. These businesses provide critical services that protect the health and well-being of people, as well as the reputation of customers’ brands.

High-Quality Business

Some of the quality characteristics we have identified for Rentokil include:

| · | Global scale, with operations in more than 80 countries and well-recognized global (and local) brands. Rentokil is one of the largest companies in the pest control industry, with number one or two positions in many of the geographies where it competes; |

| · | Significant exposure to stable, consistent businesses that can provide high recurring revenues (e.g., ~85% retention rates); and |

| · | Strong profitability profile coupled with low capital intensity, which has resulted in a consistently high ROIC (return on invested capital). |

Attractive Valuation

Given the company’s stability, return profile and future opportunities, we believe Rentokil’s current stock price is offered at a discount to our estimate of the company’s intrinsic value. In addition, we believe Rentokil’s normalized operating margins are several hundred basis points higher than current levels, and that margins can be increased in part due to the catalysts noted below.

Compelling Catalysts

Catalysts we have identified for Rentokil, which we believe will cause its stock price to appreciate over our three- to five-year investment horizon, include:

| · | Margin improvements, particularly in the large and growing North American Pest Control business, as scale is increased, acquisitions such as that of Terminix are integrated, further in-market densification is achieved and cost-reducing technology is increasingly leveraged; |

| · | Share gains through organic efforts and opportunistic acquisitions as the pest control industry continues to consolidate; and |

| · | Continued paring of non-core businesses and increased focus on its core Pest Control and Hygiene businesses can result in a higher-returning and more optimal FREE cash flow-generating business model. |

This information is for illustrative purposes only and is not a recommendation to buy or sell a particular security. There is no guarantee that the securities discussed will prove to be profitable. Please refer to disclosures at the end of this document.

| 5 |

Outlook

As we turn the page on another year, we are reminded of the fleeting nature of headline news. Our focus is not on factors that will change in the coming months, but rather on the fundamentals of businesses that may persist for years.

Rather than attempting the impossible task of predicting the unpredictable, we remain steadfast in abiding by our investment philosophy and process that have been in place for nearly 25 years. By utilizing a long-term approach and identifying what we perceive to be high-quality businesses, trading at discounts to our estimates of their intrinsic value, that possess catalysts within management’s control, we believe we can withstand short-term swings and add lasting value for our clients.

|  |  |

| Gregory Padilla, CFA | Alberto Jimenez Crespo, CFA | Howard Gleicher, CFA |

| Principal, Portfolio Manager | Principal, Portfolio Manager | CEO & Chief Investment Officer |

| Aristotle Capital Management, LLC |

| 6 |

Aristotle/Saul Global Equity Fund (Class I)

| Performance Update | December 31, 2021 | ||||||

| Total Return | 4Q21 | 1 Year | 3 Years | 5 Years | 7 Years | Annualized Since Inception (3/30/12) | Gross/Net Expense Ratio |

| ARSOX Class I | 6.34% | 19.54% | 21.17% | 13.16% | 10.93% | 8.99% | 1.07%/0.80% |

| MSCI ACWI Index (Net) | 6.68% | 18.54% | 20.38% | 14.40% | 10.90% | 10.88% | N/A |

| MSCI World Index (Net) | 7.77% | 21.82% | 21.70% | 15.03% | 11.53% | 11.77% | N/A |

Performance results for periods greater than one year have been annualized.

Performance data quoted here represents past performance. Past performance is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call (844) 274-7868.

The Fund’s advisor has contractually agreed to waive certain fees and/or absorb expenses, through April 30, 2022, to the extent that the total annual operating expenses do not exceed 0.80% of average daily net assets of the Fund. The Fund’s advisor may seek reimbursement from the Fund for waived fees and/or expenses paid for three years from the date of the waiver or payment. Without these reductions, the Fund’s performance would have been lower. A redemption fee of 1.00% will be imposed on redemptions of shares within 30 days of purchase.

On May 1, 2020, the Fund’s name changed from Aristotle/Saul Global Opportunities Fund to Aristotle/Saul Global Equity Fund. Also, on May 1, 2020, the Fund’s Principal Investment Strategies changed and performance prior to May 1, 2020 represents a different fund strategy.

Important Information:

There can be no guarantee that any strategy (risk management or otherwise) will be successful. All investing involves risk, including potential loss of principal.

The views in this letter were as of December 31, 2021 and may not necessarily reflect the same views on the date this letter is first published or any time thereafter. These views are intended to help shareholders in understanding the Fund’s investment methodology and do not constitute investment advice.

Past performance is not indicative of future results. You should not assume that any of the securities transactions, sectors or holdings discussed in this report are or will be profitable, or that recommendations Aristotle Capital makes in the future will be profitable or equal the performance of the securities listed in this report. There is no assurance that any securities, sectors or industries discussed herein will be included in or excluded from the Fund. The opinions expressed are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Aristotle Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. This is not a recommendation to buy or sell a particular security. Holdings in the last 12 months are available upon request.

| 7 |

An investment in the Fund is subject to risks, and you could lose money on your investment in the Fund. The principal risks of investing in the Fund include, but are not limited to, market risk, equity risk, foreign investment risk, currency risk, emerging market risk, small-cap, mid-cap and large-cap company risk, exchange-traded funds (ETFs) risk, liquidity risk, management and strategy risk and cybersecurity risk. Market Turbulence Resulting from COVID-19 – The outbreak of COVID-19 has negatively affected the worldwide economy, individual countries, individual companies and the market in general. The future impact of COVID-19 is currently unknown, and it may exacerbate other risks that apply to the Fund. To learn more about the Principal Risks of Investing in the Fund, please reference the prospectus.

Foreign securities have additional risks, including currency rate changes, political and economic instability, lack of comprehensive company information, less market liquidity, less-efficient trading markets, and differing auditing controls and legal standards.

Investments in emerging markets involve even greater risks. The use of short sales and ETFs may cause the Fund to have higher expenses than those of other equity funds. Short sales are speculative transactions and involve special risks, including a greater reliance on the investment team’s ability to accurately anticipate the future value of a security. The Fund’s losses are potentially unlimited in a short sale transaction. The Fund’s use of short sales and futures contracts leverages the Fund’s portfolio. The Fund’s use of leverage can make the Fund more volatile and magnify the effect of any losses. There is no assurance that a leveraging strategy will be successful.

The Fund may invest in derivatives, which can be highly volatile, illiquid and difficult to value, and changes in the value of a derivative may not correlate with the underlying securities or other securities held directly by the Fund. Such risks include gains or losses that, as a result of leverage, can be substantially greater than the derivatives’ original cost. There is also a possibility that derivatives may not perform as intended, which can reduce opportunity for gain or result in losses by offsetting positive returns in other securities the Fund owns.

Definitions:

| · | The MSCI All Country World Index (ACWI) captures large and mid capitalization representation across 23 developed markets and 27 emerging markets countries. With over 3,000 constituents, the Index covers approximately 85% of the global investable equity opportunity set. |

| · | The MSCI ACWI Value Index captures large and mid cap securities exhibiting overall value style characteristics across 23 developed markets countries and 27 emerging markets countries. |

| · | The MSCI World Index is a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance in 23 developed market countries. The MSCI World Index includes the following countries: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom and the United States. |

| · | The MSCI ACWI Growth Index captures large and mid cap securities exhibiting overall growth style characteristics across 23 developed markets countries and 27 emerging markets countries. |

| · | The Bloomberg Global Aggregate Bond Index is a flagship measure of global investment grade debt from 24 local currency markets. This multi-currency benchmark includes treasury, government-related, corporate and securitized fixed-rate bonds from both developed and emerging markets issuers. |

| · | FREE cash flow is generally calculated as cash flow from operations less capital expenditures. |

| · | Return on invested capital (ROIC) is a ratio that seeks to measure the amount of money a company makes that is above the average cost it pays for its debt and equity capital. |

| 8 |

The volatility (beta) of the Fund may be greater or less than that of the benchmarks. An investor cannot invest directly in these indices.

Portfolio composition will change due to ongoing management of the Fund. References to specific securities or sectors should not be construed as recommendations by the Fund, its Advisor or Distributor.

The companies identified herein are examples of holdings and are subject to change without notice. The companies have been selected to help illustrate the investment process described herein. A complete list of holdings is available upon request. This information should not be considered a recommendation to purchase or sell any particular security. It should not be assumed that any of the holdings listed have been or will be profitable, or that investment decisions made in the future will be profitable. Aristotle Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs.

As of December 31, 2021, the 10 largest holdings in the Fund and their weights as a percent of total net assets were: Microsoft Corp., 4.46%; Martin Marietta Materials, Inc., 4.08%; Danaher Corp., 3.93%; Lennar Corp., 3.67%; Sony Group Corp., 3.35%; Microchip Technology, Inc., 3.35%; Adobe, Inc., 3.11%; Nemetschek, SE, 3.04%; Samsung Electronics, 2.92%; Qualcomm, Inc., 2.71%.

| 9 |

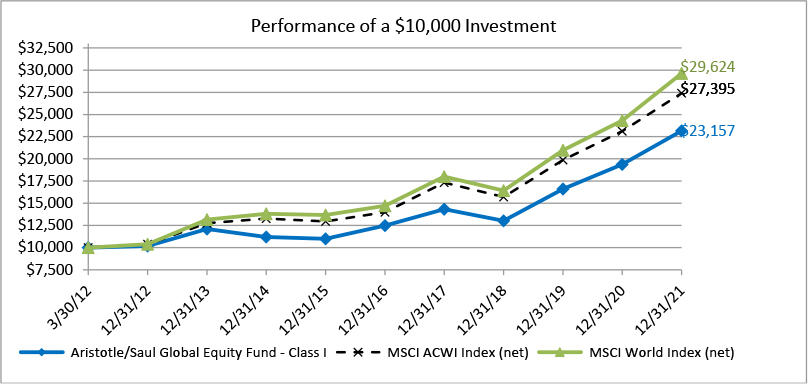

Aristotle/Saul Global Equity Fund

FUND PERFORMANCE at December 31, 2021 (Unaudited)

This graph compares a hypothetical $10,000 investment in the Fund’s Class I shares, made at its inception, with a similar investment in the MSCI All Country World Index (net) (MSCI ACWI Index (net)) and in the MSCI World Index (net). Results include the reinvestment of all dividends and capital gains.

The MSCI World Index captures large and mid cap representation across 23 Developed Markets (DM) countries. With 1,600 constituents, the index covers approximately 85% of the free float-adjusted market capitalization in each country. The MSCI All Country World Index (ACWI) captures large and mid capitalization representation across 23 developed markets and 24 emerging markets countries. With over 2,700 constituents, the Index covers approximately 85% of the global investable equity opportunity set. The index does not reflect expenses, fees, or sales charge, which would lower performance. This index is unmanaged and it is not available for investment.

| Average Annual Total Returns as of December 31, 2021 | 1 Year | 5 Years | Since Inception | Inception Date |

| Aristotle/Saul Global Equity Fund – Class I | 19.54% | 13.16% | 8.99% | 03/30/12 |

| MSCI ACWI Index (net) | 18.54% | 14.40% | 10.88% | 03/30/12 |

| MSCI World Index (net) | 21.82% | 15.03% | 11.77% | 03/30/12 |

The performance data quoted here represents past performance and past performance is not a guarantee of future results. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. The most recent month end performance may be obtained by calling (888) 661-6691.

Gross and net expense ratios for the Class I shares were 1.07% and 0.80%, respectively, which were the amounts stated in the current prospectus dated May 1, 2021. For the Fund’s current one year expense ratios, please refer to the Financial Highlights section of this report. The Fund’s Advisor has contractually agreed to waive its fees and/or pay for operating expenses of the Fund to ensure that total annual fund operating expenses do not exceed 0.80% of the Fund’s average daily net assets. This agreement is in effect until April 30, 2022, and it may be terminated before that date only by the Trust’s Board of Trustees. In the absence of such waivers, the Fund’s returns would be lower.

| 10 |

Aristotle/Saul Global Equity Fund

FUND PERFORMANCE at December 31, 2021 (Unaudited)

Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of the Fund shares. Shares redeemed within 30 days of purchase will be charged a 1.00% redemption fee.

| 11 |

Aristotle/Saul Global Equity Fund

SCHEDULE OF INVESTMENTS

As of December 31, 2021

Number | Value | |||||||

| COMMON STOCKS — 97.0% | ||||||||

| AUSTRIA — 1.2% | ||||||||

| 24,500 | Erste Group Bank A.G. | $ | 1,148,504 | |||||

| CANADA — 3.9% | ||||||||

| 71,300 | Cameco Corp. | 1,554,509 | ||||||

| 26,300 | Magna International, Inc. | 2,128,722 | ||||||

| 3,683,231 | ||||||||

| FRANCE — 6.2% | ||||||||

| 30,800 | Dassault Systemes S.E. | 1,834,185 | ||||||

| 2,400 | LVMH Moet Hennessy Louis Vuitton S.E. | 1,986,339 | ||||||

| 39,200 | TotalEnergies S.E. | 1,991,685 | ||||||

| 5,812,209 | ||||||||

| GERMANY — 6.8% | ||||||||

| 21,678 | Nemetschek S.E. | 2,771,677 | ||||||

| 1,670 | Rational A.G. | 1,707,918 | ||||||

| 12,900 | Symrise A.G. | 1,907,730 | ||||||

| 6,387,325 | ||||||||

| HONG KONG — 1.5% | ||||||||

| 144,000 | AIA Group Ltd. | 1,451,524 | ||||||

| IRELAND — 1.7% | ||||||||

| 15,150 | Medtronic PLC | 1,567,267 | ||||||

| JAPAN — 13.5% | ||||||||

| 7,000 | FANUC Corp. | 1,487,934 | ||||||

| 51,000 | KDDI Corp. | 1,491,430 | ||||||

| 79,700 | Kubota Corp. | 1,772,213 | ||||||

| 50,800 | Marui Group Co., Ltd. | 956,620 | ||||||

| 115,300 | Mitsubishi UFJ Financial Group, Inc. | 627,494 | ||||||

| 15,600 | Nidec Corp. | 1,845,393 | ||||||

| 20,600 | Otsuka Holdings Co., Ltd. | 749,447 | ||||||

| 53,000 | Pan Pacific International Holdings Corp. | 730,544 | ||||||

| 24,200 | Sony Corp. | 3,055,934 | ||||||

| 12,717,009 | ||||||||

| KOREA (REPUBLIC OF-SOUTH) — 2.8% | ||||||||

| 44,500 | Samsung Electronics Co., Ltd. | 2,660,462 | ||||||

| 12 |

Aristotle/Saul Global Equity Fund

SCHEDULE OF INVESTMENTS - Continued

As of December 31, 2021

Number | Value | |||||||

| COMMON STOCKS (Continued) | ||||||||

| NETHERLANDS — 1.4% | ||||||||

| 11,400 | Heineken N.V. | $ | 1,283,019 | |||||

| SINGAPORE — 2.0% | ||||||||

| 75,946 | DBS Group Holdings Ltd. | 1,840,603 | ||||||

| SWEDEN — 1.3% | ||||||||

| 40,800 | Assa Abloy A.B. - Class B | 1,243,624 | ||||||

| SWITZERLAND — 3.8% | ||||||||

| 22,400 | Alcon, Inc. | 1,975,799 | ||||||

| 8,000 | Chubb Ltd. | 1,546,480 | ||||||

| 3,522,279 | ||||||||

| UNITED KINGDOM — 4.2% | ||||||||

| 87,600 | GlaxoSmithKline PLC | 1,904,956 | ||||||

| 260,000 | Rentokil Initial PLC | 2,055,225 | ||||||

| 3,960,181 | ||||||||

| UNITED STATES — 46.7% | ||||||||

| 5,000 | Adobe, Inc.* | 2,835,300 | ||||||

| 7,800 | Amgen, Inc. | 1,754,766 | ||||||

| 31,400 | Axalta Coating Systems Ltd.* | 1,039,968 | ||||||

| 49,000 | Bank of America Corp. | 2,180,010 | ||||||

| 30,600 | Carnival PLC* | 573,067 | ||||||

| 27,900 | Coca-Cola Co. | 1,651,959 | ||||||

| 10,900 | Danaher Corp. | 3,586,209 | ||||||

| 20,900 | FirstCash, Inc. | 1,563,529 | ||||||

| 6,000 | General Dynamics Corp. | 1,250,820 | ||||||

| 7,400 | Honeywell International, Inc. | 1,542,974 | ||||||

| 28,800 | Lennar Corp. - Class A | 3,345,408 | ||||||

| 8,450 | Martin Marietta Materials, Inc. | 3,722,394 | ||||||

| 35,100 | Microchip Technology, Inc. | 3,055,806 | ||||||

| 12,100 | Microsoft Corp. | 4,069,472 | ||||||

| 19,100 | Oshkosh Corp. | 2,152,761 | ||||||

| 8,300 | PayPal Holdings, Inc.* | 1,565,214 | ||||||

| 9,600 | Procter & Gamble Co. | 1,570,368 | ||||||

| 13,500 | QUALCOMM, Inc. | 2,468,745 | ||||||

| 17,700 | RPM International, Inc. | 1,787,700 | ||||||

| 31,500 | Twitter, Inc.* | 1,361,430 | ||||||

| 13 |

Aristotle/Saul Global Equity Fund

SCHEDULE OF INVESTMENTS - Continued

As of December 31, 2021

Number | Value | |||||||

| COMMON STOCKS (Continued) | ||||||||

| UNITED STATES (Continued) | ||||||||

| 16,200 | Walgreens Boots Alliance, Inc. | $ | 844,992 | |||||

| 43,922,892 | ||||||||

| Total Common Stocks | ||||||||

| (Cost $59,824,047) | 91,200,129 | |||||||

Principal | ||||||||

| SHORT-TERM INVESTMENTS — 3.0% | ||||||||

| $ | 2,818,491 | UMB Bank demand deposit, 0.01%1 | 2,818,491 | |||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $2,818,491) | 2,818,491 | |||||||

| TOTAL INVESTMENTS — 100.0% | ||||||||

| (Cost $62,642,538) | 94,018,620 | |||||||

| Other Assets in Excess of Liabilities — 0.0% | 10,016 | |||||||

| TOTAL NET ASSETS — 100.0% | $ | 94,028,636 | ||||||

PLC – Public Limited Company

| * | Non-income producing security. |

| 1 | The rate is the annualized seven-day yield at period end. |

See Accompanying Notes to Financial Statements.

| 14 |

Aristotle/Saul Global Equity Fund

SUMMARY OF INVESTMENTS

As of December 31, 2021

| Security Type/Sector | Percent of Total Net Assets | |||

| Common Stocks | ||||

| Technology | 27.8 | % | ||

| Industrials | 14.0 | % | ||

| Health Care | 12.3 | % | ||

| Financials | 11.0 | % | ||

| Consumer Discretionary | 9.6 | % | ||

| Materials | 9.0 | % | ||

| Consumer Staples | 6.5 | % | ||

| Energy | 3.8 | % | ||

| Communications | 3.0 | % | ||

| Total Common Stocks | 97.0 | % | ||

| Short-Term Investments | 3.0 | % | ||

| Total Investments | 100.0 | % | ||

| Other Assets in Excess of Liabilities | 0.0 | % | ||

| Total Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

| 15 |

Dear Fellow Shareholders,

Markets Review

In a year filled with uncertainty, global economies proved largely resilient. Even in the face of supply-chain disruptions and multiple variants of the COVID-19 virus, global recovery continued throughout the period. Themes from 2020, such as central bank policy decisions and vaccine distribution, persisted.

After declining in the third quarter of 2021, global equity markets rebounded during the fourth quarter. Overall, the MSCI ACWI Index (Net) finished with a full-year return of 18.54%. In terms of style, for the full year, the MSCI ACWI Value (Net) outperformed the MSCI ACWI Growth (Net) by 2.52%.

Throughout the year, investors focused on the progress of the global recovery. Although corporate revenues and earnings continued to rebound during the period, the IMF announced a slight downward revision to its 2021 global real GDP growth projections due to continued supply disruptions and uncertain pandemic dynamics. These conditions have caused shortages of key inputs, lowered manufacturing activity and fueled inflation across the globe.

In addition to a global shipping crisis and semiconductor shortages, the energy sector also captured numerous headlines as robust demand outpaced supply, causing prices to surge. After a historic drop in energy consumption in 2020, the global economic recovery and a long and cold winter in the Northern Hemisphere have driven a strong rebound in demand, while the ongoing shift to renewables has impacted production and future investments in fossil fuels. Although OPEC and countries such as Russia have pledged to boost supply, the energy crunch has highlighted issues in long-term production. Furthermore, rising energy prices have contributed to an inflation loop as the prices of energy-intensive materials like nickel, steel and silicon have all risen.

Increased inflation, combined with an uncertain recovery, has created policy challenges for central banks. On one hand, the rhetoric on inflation being “transitory” softened as many central banks took a hawkish approach. During the fourth quarter, the European Central Bank announced a gradual phaseout of its bond purchase program, while countries like the U.K., Russia and Mexico raised interest rates. On the other hand, policy in Southeast Asia was largely unchanged, and China announced an easing of its monetary policy that will likely include further cuts to lending rates.

On the COVID front, the Omicron variant became the dominant strain in areas such as the U.K. and the U.S. The number of new daily cases reached as high as ~1,750,000, the highest reported figure during the pandemic, with Europe and the Americas reporting the greatest number of cases.

Although we are happy to report another strong year, the constant twists, turns and pivots of this past year are a reminder of the fragility of the short term. Factors such as the possibility of new variants, the timing of a full recovery, fiscal and monetary policy decisions, and market sentiment are topics better left for reporters.

Performance data quoted here represents past performance. Past performance is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call (844) 274-7868.

FOR MORE INFORMATION, PLEASE CONTACT:

Phone: (844) 274-7868 | Email: funds@aristotlecap.com | Web: www.aristotlefunds.com

| 16 |

We believe investment managers (and their clients) are best positioned to create lasting value by minimizing distractions and focusing on the long term.

Performance Review

For the year, the Aristotle International Equity Fund returned 15.79% at NAV, outperforming the 11.26% total return of the MSCI EAFE Index (Net).

The Fund’s outperformance for the year relative to the MSCI EAFE Index (Net) can be attributed to security selection. Relative sector weights, the by-product of our bottom-up stock selection decisions, also added to relative performance. Security selection in the Information Technology, Consumer Discretionary and Energy sectors positively impacted returns, while security selection in Financials, Consumer Staples and Materials detracted from relative performance.

Additionally, security selection in Europe & Middle East, as well as an overweight in Canada and an underweight in Asia contributed the most to relative performance. Security selection in Asia as well as an overweight to Emerging Markets and an underweight to Europe & Middle East detracted from relative performance.

2021 Top Contributors to Relative Fund Return | 2021 Top Detractors to Relative Fund Return | |

| Ashtead Group | Credicorp | |

| Accenture | Pan Pacific International | |

| Nemetschek | Samsung | |

| Brookfield Asset Management | FANUC | |

| Dassault Systèmes | Safran |

Ashtead Group, a U.K.-headquartered construction, industrial and general equipment rental company, was the top contributor for the year. As a result of the unprecedented conditions in 2020, management made what we consider to be the prudent decision of sourcing liquidity by pausing greenfield openings, bolt-on acquisitions and the company’s share buyback program. However, after weathering the uncertain market, Ashtead resumed all plans and launched a new share buyback program of $1.4 billion over the next two years during the first half of the year. Additionally, the company unveiled its Sunbelt 3.0 strategic plan that will further expand Ashtead’s location network, improve operational efficiency and solidify market share. Through this difficult period, we believe the company has demonstrated its resiliency, forward-looking and opportunistic mindset, and focus on continuously improving

| 17 |

Nemetschek, a European provider of software solutions for architectural and building construction projects, was a leading contributor for the year. The company reported strong results throughout the year, with both margins and revenue well above expectations. We believe margin improvement was due to its transition toward the more profitable licensing of its software, a catalyst we previously identified, in addition to COVID-related cost savings. Revenue growth was largely driven by its Design and Build segments as international cross-selling rose. Importantly, Bluebeam, its building collaboration software, achieved record levels of growth in new users. Nemetschek’s Build segment also benefited from the continued favorable environment for the construction sector. Furthermore, during its annual user event, the company announced new product features that it plans to release in the first half of 2022 that aim to increase office to field collaboration and connectivity – the fastest-growing area within construction software.

Pan Pacific International, the Japanese discount and general merchandise retailer, was one of the year’s largest detractors. Operating profits declined more than 30% year-over-year in the most recent quarter. This was in part due to lower foot traffic during a rainy season in Japan, coupled with a recently more difficult pandemic environment. Spending on technology investments, renovations and new store openings also compressed margins. However, we view these headwinds as temporary, and the investments, renovations and new openings as appropriate capital allocation, and continue to focus on the long-term strength of the business. Pan Pacific’s Don Quijote stores create a sense of treasure hunt that elicits high entertainment value—a unique business model that we believe will allow for organic market share gains in Japan, as well expansion overseas. With the company’s demonstrated ability to turn around competitors’ stores, in our opinion, it also stands to benefit from the ongoing conversion of its acquired UNY locations.

Safran, a France-based international aerospace propulsion and equipment supplier, was one of the main detractors for the year. Although the company continues to report recovering levels of sales and profitability, the uncertainty caused by the pandemic and supply chain issues continued to weigh on shares. Nevertheless, Safran has demonstrated its ability to efficiently manage costs, its supply chain, and inventories in this challenged environment. The company remains committed in investing for organic growth, actively managing its portfolio of products, keeping low leverage, and returning capital to its shareholders. We believe Safran remains well positioned to meet the evolving needs of the aerospace industry through its leadership positions and technological expertise.

| 18 |

Investment Activity

During the year, we made the following purchases and sales in the Fund.

| 2021 Fund Purchases | 2021 Fund Sales | |||

| GlaxoSmithKline | 1Q2021 | Compass Group | 1Q2021 | |

| Nemetschek | 1Q2021 | UBS Group | 1Q2021 | |

| Michelin | 1Q2021 | |||

| Pan Pacific International | 3Q2021 | |||

One of our objectives is to clearly articulate the thought process behind our investments to our fellow shareholders. Below is an example of a sale (Compass Group) and a purchase (GlaxoSmithKiline) we made in the Fund this year.

Sale

We first invested in Compass Group in the fourth quarter of 2012 in our International strategy. During our more than nine-year holding period, the company executed on a number of catalysts, including growing market share in North America and the Emerging Markets, restructuring its European operations, and continuing to consolidate the fragmented global market for contract catering via acquisitions. Like many companies, Compass Group’s operations have been significantly impacted by the COVID-19 pandemic. Although we believe management has taken the necessary (and correct) actions to position the company for long-term success, we have questions regarding the normalized earnings power over the next three to five years. While we decided to exit our position this quarter, we continue to closely monitor Compass Group.

Purchase

GlaxoSmithKline was formed in 2000 following the merger of British pharmaceutical companies Glaxo Wellcome and SmithKline Beecham. The company develops, manufactures and commercializes innovative medicines (~50% of revenue - HIV, respiratory, immune-inflammation, etc.), vaccines (~20% - shingles, meningitis, influenza, etc.), and consumer health products (~30% - oral health, pain, digestive health, etc.).

| 19 |

With origins dating as far back as 1715, U.K.-headquartered GlaxoSmithKline and its predecessors have been at the forefront of innovation, resulting in one of the strongest portfolios of commercialized products in the industry. The company currently operates in 150 countries and boasts an extensive network of manufacturing and research sites that spans over 36 countries, including major centers in the U.K., U.S., Spain, Belgium and China.

In early 2020, GlaxoSmithKline’s relatively new management team announced that the company will undergo a demerger, creating standalone biopharmaceutical and consumer healthcare companies in 2022. This ongoing strategic change is one we view positively.

High-Quality Business

Some of the quality characteristics we have identified for GlaxoSmithKline include:

| • | Global scale and a diverse product offering across various end markets and regions; |

| • | Leading market positions and a robust portfolio of recognizable brands (e.g., Advair, Triumeq, Shingrix, Bexsero, Advil, Sensodyne); and |

| • | Extensive history of developing innovative and relevant medicines (e.g., discovery of amoxicillin and Retrovir, the first treatment for HIV). |

Attractive Valuation

Given our estimates of normalized earnings, we believe GlaxoSmithKline’s current stock price is offered at a discount to our estimate of the company’s intrinsic value. We believe normalized earnings power is underappreciated given continued market share gains of commercialized products and the business’s improving FREE cash flow generation.

Compelling Catalysts

Catalysts we have identified for GlaxoSmithKline, which we believe will cause its stock price to appreciate over our three- to five-year investment horizon, include:

| • | Benefits from the upcoming separation of the biopharmaceutical and consumer health businesses, creating two standalone companies; |

| • | Continued market share advances by Shingrix, a leading vaccine for shingles (aka herpes zoster); and |

| • | Further market share gains for the oncology franchise, including Zejula, a treatment for ovarian cancer. |

This information is for illustrative purposes only and is not a recommendation to buy or sell a particular security. There is no guarantee that the securities discussed will prove to be profitable. Please refer to disclosures at the end of this document.

| 20 |

Outlook

As we turn the page on another year, we are reminded of the fleeting nature of headline news. Our focus is not on factors that will change in the coming months, but rather on the fundamentals of businesses that may persist for years.

Rather than attempting the impossible task of predicting the unpredictable, we remain steadfast in abiding by our investment philosophy and process that have been in place for nearly 25 years. By utilizing a long-term approach and identifying what we perceive to be high-quality businesses, trading at discounts to our estimates of their intrinsic value, that possess catalysts within management’s control, we believe we can withstand short-term swings and add lasting value for our clients.

|  |  |

Sean Thorpe Principal, Portfolio Manager | Geoffrey Stewart, CFA Principal, Portfolio Manager | Howard Gleicher, CFA CEO & Chief Investment Officer Aristotle Capital Management, LLC |

| 21 |

Aristotle International Equity Fund (Class I)

| Performance Update | December 31, 2021 | |||||

| Total Return | 4Q21 | 1 Year | 3 Years | 5 Years | Annualized Since Inception (3/31/14) | Gross/Net Expense Ratio |

| ARSFX Class I | 5.64% | 15.79% | 16.59% | 11.86% | 6.27% | 1.05% / 0.80% |

| MSCI EAFE Index (Net) | 2.69% | 11.26% | 13.54% | 9.55% | 5.31% | N/A |

Performance results for periods greater than one year have been annualized.

Performance data quoted here represents past performance. Past performance is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call (844) 274-7868.

The Fund’s advisor has contractually agreed to waive certain fees and/or absorb expenses, through April 30, 2022, to the extent that the total annual operating expenses do not exceed 0.80% of average daily net assets of the Fund. The Fund’s advisor may seek reimbursement from the Fund for waived fees and/or expenses paid for three years from the date of the waiver or payment. Without these reductions, the Fund’s performance would have been lower. A redemption fee of 1.00% will be imposed on redemptions of shares within 30 days of purchase.

Important Information:

There can be no guarantee that any strategy (risk management or otherwise) will be successful. All investing involves risk, including potential loss of principal.

The views in this letter were as of December 31, 2021 and may not necessarily reflect the same views on the date this letter is first published or any time thereafter. These views are intended to help shareholders in understanding the Fund’s investment methodology and do not constitute investment advice.

Past performance is not indicative of future results. You should not assume that any of the securities transactions, sectors or holdings discussed in this report are or will be profitable, or that recommendations Aristotle Capital makes in the future will be profitable or equal the performance of the securities listed in this report. There is no assurance that any securities, sectors or industries discussed herein will be included in or excluded from the Fund. The opinions expressed are as of the date of publication and are subject to change due to changes in the market or economic conditions and may not necessarily come to pass. Aristotle Capital reserves the right to modify its current investment strategies and techniques based on changing market dynamics or client needs. This is not a recommendation to buy or sell a particular security. Holdings are available within the last 12 months.

An investment in the Fund is subject to risks, and you could lose money on your investment in the Fund. The principal risks of investing in the Fund include, but are not limited to, investing in foreign securities, emerging markets, small-capitalization and mid-capitalization companies. Market Turbulence Resulting from COVID-19 – The outbreak of COVID-19 has negatively affected the worldwide economy, individual countries, individual companies and the market in general. The future impact of COVID-19 is currently unknown, and it may exacerbate other risks that apply to the Fund. To learn more about the Principal Risks of Investing in the Fund, please reference the prospectus.

| 22 |

Foreign securities have additional risks, including currency rate changes, political and economic instability, lack of comprehensive company information, less market liquidity, less-efficient trading markets, and differing auditing controls and legal standards. Investments in emerging markets involve even greater risks. The securities of small-capitalization and mid-capitalization companies may be subject to more abrupt or erratic market movements and may have lower trading volumes or more erratic trading than securities of larger, more established companies or market averages in general.

Definitions:

| · | The MSCI ACWI Index (All-Country World Index) captures large and mid cap representation across 23 developed market countries and 27 emerging markets countries. With approximately 3,000 constituents, the Index covers approximately 85% of the global investable equity opportunity set. |

| · | The MSCI EAFE Index (Europe, Australasia, Far East) is a free float-adjusted market capitalization-weighted index that is designed to measure the equity market performance of developed markets, excluding the United States and Canada. The MSCI EAFE Index consists of the following 21 developed market countries: Australia, Austria, Belgium, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland and the United Kingdom. |

| · | The MSCI ACWI Value Index captures large and mid cap securities exhibiting overall value style characteristics across 23 developed markets countries and 27 emerging markets countries. |

| · | The MSCI ACWI Growth Index captures large and mid cap securities exhibiting overall growth style characteristics across 23 developed markets countries and 27 emerging markets countries. |

| · | FREE cash flow is generally calculated as cash flow from operations less capital expenditures. |

The volatility (beta) of the Fund may be greater or less than its respective benchmarks. It is not possible to invest directly in these indices.

Portfolio composition will change due to ongoing management of the Fund. References to specific securities or sectors should not be construed as recommendations by the Fund, its Advisor or Distributor.

As of December 31, 2021, the 10 largest holdings in the Fund and their weights as a percent of total net assets were: Accenture plc, 5.62%; Sony Corp., 4.77%; Brookfield Asset Management, Inc., 4.46%; Nemetschek, SE, 4.26%; Dassault Systemes SE, 4.16%; Ashtead Group Plc., 4.05%; Magna International Inc., 2.99%; LVMH Moet Hennessy Louis Vuitton SE, 2.98%; Alcon, Inc., 2.88%; Cie Generale des Etablissements Michelin SCA, 2.87%.

| 23 |

Aristotle International Equity Fund

FUND PERFORMANCE at December 31, 2021 (Unaudited)

This graph compares a hypothetical $10,000 investment in the Fund’s Class I shares, made at its inception, with a similar investment in the MSCI Europe, Australia, Far East Index (net) (MSCI EAFE Index). Results include the reinvestment of all dividends and capital gains.

The MSCI EAFE Index is a free float-adjusted market capitalization index that is designed to measure the equity market performance of developed markets, excluding the US & Canada. The index does not reflect expenses, fees or sales charge, which would lower performance. This index is unmanaged and it is not available for investment.

| Average Annual Total Returns as of December 31, 2021 | 1 Year | 5 Years | Since Inception | Inception Date |

| Aristotle International Equity Fund – Class I | 15.79% | 11.86% | 6.27% | 03/31/14 |

| MSCI EAFE Index (net) | 11.26% | 9.55% | 5.31% | 03/31/14 |

The performance data quoted here represents past performance and past performance is not a guarantee of future results. Investment return and principal value will fluctuate so that an investor's shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. The most recent month end performance may be obtained by calling (888) 661-6691.

Gross and net expense ratios for the Class I shares were 1.05% and 0.80%, respectively, which were the amounts stated in the current prospectus dated May 1, 2021. For the Fund’s current one year expense ratios, please refer to the Financial Highlights section of this report. The Fund’s Advisor has contractually agreed to waive its fees and/or pay for operating expenses of the Fund to ensure that total annual fund operating expenses do not exceed 0.80% of the Fund’s average daily net assets. This agreement is in effect until April 30, 2022, and it may be terminated before that date only by the Trust’s Board of Trustees. In the absence of such waivers, the Fund’s returns would be lower.

Returns reflect the reinvestment of distributions made by the Fund, if any. The graph and performance table above do not reflect the deduction of taxes that a shareholder would pay on Fund distributions or the redemption of the Fund shares. Shares redeemed within 30 days of purchase will be charged a 1.00% redemption fee.

| 24 |

Aristotle International Equity Fund

SCHEDULE OF INVESTMENTS

As of December 31, 2021

Number | Value | |||||||

| COMMON STOCKS — 97.1% | ||||||||

| AUSTRIA — 2.1% | ||||||||

| 174,900 | Erste Group Bank A.G. | $ | 8,198,915 | |||||

| CANADA — 8.8% | ||||||||

| 280,600 | Brookfield Asset Management, Inc. - Class A | 16,944,691 | ||||||

| 285,400 | Cameco Corp. | 6,222,397 | ||||||

| 140,500 | Magna International, Inc. | 11,367,727 | ||||||

| 34,534,815 | ||||||||

| FRANCE — 15.6% | ||||||||

| 98,700 | Amundi S.A.1 | 8,151,964 | ||||||

| 66,400 | Cie Generale des Etablissements Michelin SCA | 10,896,585 | ||||||

| 265,700 | Dassault Systemes S.E. | 15,822,822 | ||||||

| 13,700 | LVMH Moet Hennessy Louis Vuitton S.E. | 11,338,684 | ||||||

| 58,600 | Safran S.A. | 7,182,236 | ||||||

| 147,000 | TotalEnergies S.E. | 7,468,818 | ||||||

| 60,861,109 | ||||||||

| GERMANY — 6.5% | ||||||||

| 126,700 | Nemetschek S.E. | 16,199,440 | ||||||

| 63,000 | Symrise A.G. | 9,316,821 | ||||||

| 25,516,261 | ||||||||

| HONG KONG — 2.0% | ||||||||

| 758,600 | AIA Group Ltd. | 7,646,707 | ||||||

| IRELAND — 8.2% | ||||||||

| 51,500 | Accenture PLC - Class A | 21,349,325 | ||||||

| 216,900 | Experian PLC | 10,662,978 | ||||||

| 32,012,303 | ||||||||

| JAPAN — 18.4% | ||||||||

| 42,800 | FANUC Corp. | 9,097,653 | ||||||

| 271,500 | KDDI Corp. | 7,939,672 | ||||||

| 354,200 | Kubota Corp. | 7,876,010 | ||||||

| 329,000 | Marui Group Co., Ltd. | 6,195,432 | ||||||

| 84,700 | Nidec Corp. | 10,019,536 | ||||||

| 156,600 | Otsuka Holdings Co., Ltd. | 5,697,254 | ||||||

| 516,900 | Pan Pacific International Holdings Corp. | 7,124,869 | ||||||

| 143,600 | Sony Corp. | 18,133,558 | ||||||

| 72,083,984 | ||||||||

| 25 |

Aristotle International Equity Fund

SCHEDULE OF INVESTMENTS - Continued

As of December 31, 2021

Number | Value | |||||||

| COMMON STOCKS (Continued) | ||||||||

| KOREA (REPUBLIC OF-SOUTH) — 2.5% | ||||||||

| 148,600 | Samsung Electronics Co., Ltd. | $ | 9,759,301 | |||||

| NETHERLANDS — 5.0% | ||||||||

| 89,900 | Akzo Nobel N.V. | 9,876,309 | ||||||

| 85,900 | Heineken N.V. | 9,667,662 | ||||||

| 19,543,971 | ||||||||

| PERU — 1.9% | ||||||||

| 62,300 | Credicorp Ltd. | 7,604,961 | ||||||

| SINGAPORE — 2.3% | ||||||||

| 374,300 | DBS Group Holdings Ltd. | 9,071,414 | ||||||

| SWEDEN — 2.1% | ||||||||

| 265,400 | Assa Abloy A.B. - Class B | 8,089,651 | ||||||

| SWITZERLAND — 4.5% | ||||||||

| 124,000 | Alcon, Inc. | 10,937,461 | ||||||

| 77,900 | Novartis A.G. | 6,845,232 | ||||||

| 17,782,693 | ||||||||

| UNITED KINGDOM — 16.5% | ||||||||

| 191,500 | Ashtead Group PLC | 15,401,909 | ||||||

| 325,200 | Close Brothers Group PLC | 6,180,033 | ||||||

| 152,900 | Coca-Cola European Partners PLC | 8,551,697 | ||||||

| 480,700 | GlaxoSmithKline PLC | 10,453,338 | ||||||

| 75,800 | Reckitt Benckiser Group PLC | 6,506,816 | ||||||

| 1,283,800 | Rentokil Initial PLC | 10,148,067 | ||||||

| 138,600 | Unilever N.V. | 7,424,662 | ||||||

| 64,666,522 | ||||||||

| UNITED STATES — 0.7% | ||||||||

| 144,200 | Carnival PLC* | 2,700,530 | ||||||

| Total Common Stocks | ||||||||

| (Cost $306,080,922) | 380,073,137 | |||||||

| 26 |

Aristotle International Equity Fund

SCHEDULE OF INVESTMENTS - Continued

As of December 31, 2021

Principal | Value | |||||||

| SHORT-TERM INVESTMENTS — 2.4% | ||||||||

| $ | 9,478,383 | UMB Bank demand deposit, 0.01%2 | $ | 9,478,383 | ||||

| TOTAL SHORT-TERM INVESTMENTS | ||||||||

| (Cost $9,478,383) | 9,478,383 | |||||||

| TOTAL INVESTMENTS — 99.5% | ||||||||

| (Cost $315,559,305) | 389,551,520 | |||||||

| Other Assets in Excess of Liabilities — 0.5% | 1,924,983 | |||||||

| TOTAL NET ASSETS — 100.0% | $ | 391,476,503 | ||||||

PLC – Public Limited Company

| * | Non-income producing security. |

| 1 | Security exempt from registration under Rule 144A of the Securities Act of 1933. These securities are restricted and may be resold in transactions exempt from registration normally to qualified institutional buyers. The total value of these securities is $8,151,964, which represents 2.1% of total net assets of the Fund. |

| 2 | The rate is the annualized seven-day yield at period end. |

See Accompanying Notes to Financial Statements.

| 27 |

Aristotle International Equity Fund

SUMMARY OF INVESTMENTS

As of December 31, 2021

| Security Type/Sector | Percent of Total Net Assets | |||

| Common Stocks | ||||

| Technology | 26.0 | % | ||

| Financials | 16.3 | % | ||

| Industrials | 14.8 | % | ||

| Consumer Discretionary | 10.9 | % | ||

| Consumer Staples | 10.0 | % | ||

| Health Care | 8.7 | % | ||

| Materials | 6.5 | % | ||

| Communications | 2.0 | % | ||

| Energy | 1.9 | % | ||

| Total Common Stocks | 97.1 | % | ||

| Short-Term Investments | 2.4 | % | ||

| Total Investments | 99.5 | % | ||

| Other Assets in Excess of Liabilities | 0.5 | % | ||

| Total Net Assets | 100.0 | % | ||

See Accompanying Notes to Financial Statements.

| 28 |

Dear Fellow Shareholders,

Summary

U.S. corporate credit markets finished the year strong, led by high yield bonds and bank loans. For the calendar year, bank loans outperformed as the Credit Suisse Leveraged Loan Index gained 5.40%. High yield bonds also had a strong year, gaining 5.28% as measured by the Bloomberg U.S. Corporate High Yield Bond Index. Investment grade corporate bonds underperformed, falling 1.04% as measured by the Bloomberg U.S. Corporate Bond Index.

Risk markets performed well throughout 2021, led by the U.S. equity market. The S&P 500 Index gained 28.71% for the calendar year as the market continued to rebound from the pandemic-driven selloff in the first half of 2020. Despite the emergence of both the Delta and Omicron variants of COVID-19 during the year, strong consumer spending, robust corporate earnings, still accommodative monetary policy and additional fiscal stimulus all helped to underpin risk markets during the year. On the U.S. economic data front, the unemployment rate declined to 4.2% in November, its lowest level since February 2020, despite a smaller than expected increase in nonfarm payrolls. Meanwhile, inflation remained in focus as November Consumer Price Index (CPI) rose by 6.8% year-over-year, the fastest rate since 1982, and Core CPI rose by 4.9% year-over-year, the largest annual increase since June 1991. At its November meeting, the Federal Reserve (Fed) announced it would begin tapering asset purchases at a pace of $15 billion a month, as expected, then proceeded to double the pace at the December meeting while abandoning the term “transitory”. In line with the shift in policy, new projections based on the median forecast by Fed officials signaled the possibility of three interest rate increases in the new year.

Market Environment

U.S. Treasury yields climbed in 2021 as the yield curve flattened further through the end of the year. Short-term yields rose sharply with the yield on U.S. 2-Year and 5-Year notes climbing roughly 61 and 90 basis points, respectively. The yield on the U.S. 10-Year Treasury Note climbed roughly 60 basis points as well, while the long-end outperformed in the second half of 2021. Higher quality bonds underperformed as the Bloomberg U.S. Aggregate Bond Index returned -1.54% for the calendar year.

Corporate credit spreads continued tightening in 2021, falling to near the lowest levels in over 10 years. High yield bond spreads ended the year roughly 76 basis points tighter as measured by the Bloomberg U.S. Corporate High Yield Bond Index. Conversely, investment grade corporate bond spreads ended the year roughly unchanged, tightening 3 basis points as measured by the Bloomberg U.S. Corporate Bond Index.

Performance data quoted here represents past performance. Past performance is no guarantee of future results. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain performance information current to the most recent month-end, please call (844) 274-7868.

FOR MORE INFORMATION, PLEASE CONTACT:

Phone: (844) 274-7868 | Email: funds@aristotlecap.com | Web: www.aristotlefunds.com

| 29 |

Total high yield bond issuance in 2021 topped $468 billion and surpassed 2020’s record annual supply. Investment grade corporate bond issuance totaled more than $1 trillion for the full year, falling short of 2020’s record. Driven by robust private equity buyout activity and record collateralized loan obligation (CLO) sales, leveraged loan supply topped $600 billion in 2021, the highest since at least 2013.

On the demand side, investors continued to favor investment grade corporate bond and bank loan funds in the fourth quarter. For the year, high yield bond funds experienced more than $13 billion in outflows while bank loan funds experienced inflows of around $45 billion.

Within the high yield universe, lower quality bonds outperformed for the calendar year as ‘CCC’s (+8.59%) outperformed ‘B’s (+4.85%) and ‘BB’s (+4.61%). From an industry perspective, cyclicals outperformed led by Energy (+13.50%), while Financial Institutions (-0.30%) trailed the broader high yield bond market. Additionally, default activity remained very benign as the U.S. high yield bond default rate declined to a record-low 0.29% at the end of the year.

Performance Review

The Aristotle Strategic Credit Fund, Class I (ARSSX), which primarily invests in high yield bonds, investment grade corporate bonds and bank loans, returned 2.56% at NAV for the calendar year, underperforming the 2.99% return of its blended benchmark of one-third Bloomberg U.S. High Yield Ba/B 2% Issuer Capped Bond Index, one-third Bloomberg U.S. Intermediate Corporate Bond Index and one-third Credit Suisse Leveraged Loan Index.

The Fund’s underperformance during the year was led by an underweight in bank loans and the allocation to cash. This was partially offset by the Fund’s overweight in high yield bonds and underweight in investment grade corporate bonds. Over the course of 2021, the Fund’s overweight in high yield bonds gradually increased while the allocation from investment grade corporate bonds was reduced from an overweight at the end of 2020 to an underweight by the end of the 2nd quarter of 2021. The Fund was underweight bank loans throughout the year.

Over the course of the first half of 2021, we reduced the Fund’s effective duration by over one year as we shifted out of investment grade corporate bonds into shorter duration high yield bonds. In our view, shorter duration high yield bonds were more attractive than bank loans from a quality perspective; nonetheless, significant inflows into bank loan funds and the strong performance of risk markets helped to underpin bank loan outperformance during the year. We believe the Fund’s allocation shift during the year from investment grade corporate bonds to high yield bonds highlights its flexible design.

| 30 |

The Aristotle Strategic Credit Fund, Class I (ARSSX) has an inception date of December 31, 2014.

Annual Attribution Summary

Security selection was the primary detractor from the Fund’s relative performance during the year, led by holdings in Energy and Pipelines & Distributors. This was partially offset by security selection in Banking and Media & Entertainment.

Sector rotation also detracted from relative performance as an underweight in bank loans was partially offset by an overweight in high yield bonds.

Industry allocation had a marginally positive effect on relative performance as overweights in Pipelines & Distributors and Finance Companies were largely offset by underweights in Industrials and Diversified Manufacturing & Construction Machinery.

| Top Five Contributors | Top Five Detractors |

| Quad/Graphics | CVS Health |

| RR Donnelley & Sons | Lumen Technologies |

| United Airlines | Meredith Corporation |

| MetLife | Presidio Holdings |

| American Airlines | CSC Holdings |

| 31 |

Outlook and Strategy

We believe corporate credit markets should remain strong in the first half of 2022, especially relative to higher quality fixed income market segments given expected interest rate pressures. In our opinion, solid fundamentals and the positive momentum in the global economy should overshadow the negative impact of a shift to tighter financial conditions.

While U.S. economic growth has moderated from the torrid pace seen in the middle of 2021, we believe 2022 should still see above-trend growth despite greater uncertainty on the monetary and fiscal policy fronts. The tides have turned as the Fed embarks on its well-telegraphed tapering process and is set to begin hiking rates soon, while additional fiscal stimulus meets resistance ahead of the mid-term elections in 2022. Despite these headwinds, we believe strong consumer spending, robust corporate earnings and solid balance sheets should be supportive of growth.

We believe U.S. Treasury yields should continue to push higher with the Fed backstop going from a tailwind to a headwind over the next several months. In our opinion, the lack of price-insensitive central bank demand in the bond market will have a significant impact on the yield curve, leading to higher rates across the curve and potential steepening. Furthermore, we expect real rates to move out of significantly negative territory, especially as global central banks begin following the Fed on the road to tighter monetary policy.

Following a record year for supply in the high yield market, we still expect above-average issuance in 2022. We believe companies will continue to take advantage of historically low rates to refinance, especially amidst the ongoing hunt for yield. Nonetheless, we expect to see a pickup in more aggressive issuance as companies fund share repurchases and mergers and acquisitions (M&A). We anticipate further growth in the loan market on the back of strong demand for floating-rate instruments ahead of the Fed hiking cycle.

With credit spreads entering 2022 within striking distance of the all-time lows, we believe the key to performance this year will come from carry. In our opinion, company balance sheets continue to improve and profitability remains strong. We acknowledge the outlook is more opaque than it has been for some time. In addition to the most apparent risks, we are monitoring additional risks including heightened geopolitical risk and broader, more persistent inflationary pressures that negatively impact consumers and corporate balance sheets.

In the Fund, from an overall perspective, we did not make any major changes to asset allocation during the second half of the year. We maintained an overweight in high yield bonds alongside underweights in investment grade corporate bonds and bank loans. The Fund also continues to hold a duration underweight relative to the blended benchmark.

With short-term interest rates in the U.S. already beginning to price in the Fed’s rate hikes this year, we are beginning to see better opportunities in the bank loan market and plan to gradually reduce the Fund’s underweight during the first quarter. Nonetheless, we still favor shorter duration high yield bonds relative to bank loans in the Fund, particularly from a quality perspective.

| 32 |

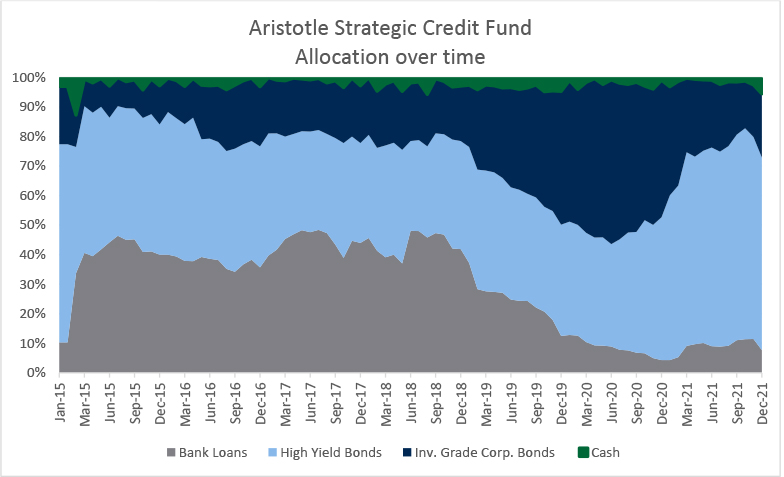

As of December 31, the Fund was composed of 65.3% high yield bonds, 21.5% investment grade corporate bonds and 7.7% bank loans. Roughly 5.5% was held in cash. At the end of the year, the Fund held overweights in Energy, Transportation and Lodging & Leisure alongside underweights in Technology, Industrials and Food, Beverage & Tobacco.

|  |

Douglas Lopez, CFA Principal, Portfolio Manager | Terence Reidt, CFA Principal, Portfolio Manager |

| 33 |

Aristotle Strategic Credit Fund (Class I)

| Performance Update | December 31, 2021 |

| Total Return | 4Q21 | YTD | 1 Year | 3 Years | 5 Years | Since Inception (12/31/14) | Gross/Net Expense Ratio |

| ARSSX Class I | 0.13% | 2.56% | 2.56% | 7.11% | 4.77% | 4.57% | 3.22% / 0.62% |

| Blended Benchmark* | 0.31% | 2.99% | 2.99% | 6.67% | 4.91% | 4.73% | N/A |

| Bloomberg U.S. Aggregate Bond Index | 0.01% | -1.54% | -1.54% | 4.79% | 3.57% | 3.00% | N/A |

| Bloomberg U.S. High Yield Ba/B 2% Issuer Capped Bond Index | 0.75% | 4.65% | 4.65% | 9.07% | 6.36% | 6.07% | N/A |

Performance data quoted here represents past performance. Past performance is no guarantee of future results. There can be no guarantee that any strategy (risk management or otherwise) will be successful. All investing involves risk, including potential loss of principal. Returns over one year are annualized. Investment return and principal value will fluctuate so that an investor’s shares, when redeemed, may be worth more or less than their original cost. Current performance may be lower or higher than the performance information quoted. To obtain current performance information to the most recent month-end, please call (844) 274-7868.

The Fund’s advisor has contractually agreed to waive its fees and/or pay expenses, through April 30, 2022, to the extent that the total annual operating expenses do not exceed 0.62% of average daily net assets of the Fund. The Fund’s advisor may seek reimbursement from the Fund for waived fees and/or expenses paid for three years from the date of the waiver or payment. Without these reductions, the Fund’s performance would have been lower. A redemption fee of 1.00% will be imposed on redemptions of shares within 30 days of purchase.

| * | The blended benchmark represents a blend of 1/3 Bloomberg U.S. High Yield Ba/B 2% Issuer Capped Bond Index, 1/3 Bloomberg U.S. Intermediate Corporate Bond Index and 1/3 Credit Suisse Leveraged Loan Index. The Bloomberg Barclays U.S. High Yield Loans Index was retired on September 30, 2016 and was replaced with the Credit Suisse Leveraged Loan Index effective October 1, 2016. |

Important Information:

There can be no guarantee that any strategy (risk management or otherwise) will be successful. All investing involves risk, including potential loss of principal.

The views in this commentary were as of the date stated and may not necessarily reflect the same views on the date this letter is first published or any time thereafter. These views are intended to help shareholders in understanding the Fund’s investment methodology and do not constitute investment advice.