UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

☒ Annual Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the fiscal year ended February 2, 2019

Or

☐ Transition Report Pursuant to Section 13 or 15(d) of the Securities Exchange Act of 1934

For the transition period from to

Commission File Number: 000-51315

CITI TRENDS, INC.

(Exact name of registrant as specified in its charter)

Delaware | | 52-2150697 |

(State or other jurisdiction of | | (I.R.S. Employer Identification No.) |

incorporation or organization) | | |

| | |

104 Coleman Boulevard, Savannah, Georgia | | 31408 |

(Address of principal executive offices) | | (Zip Code) |

Registrant’s telephone number, including area code (912) 236-1561

Securities registered pursuant to Section 12(b) of the Act:

Title of each class | | Name of each exchange

on which registered |

Common Stock, $.01 Par Value | | NASDAQ Stock Market |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. Yes ☐ No ☒

Indicate by check mark if the registrant is not required to file reports pursuant to Section 13 or Section 15(d) of the Act. Yes ☐ No ☒

Indicate by check mark whether the registrant (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. Yes ☒ No ☐

Indicate by check mark whether the registrant has submitted electronically every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the registrant was required to submit such files). Yes ☒ No ☐

Indicate by check mark if disclosure of delinquent filers pursuant to Item 405 of Regulation S-K (§ 229.405 of this chapter) is not contained herein, and will not be contained, to the best of registrant’s knowledge, in definitive proxy or information statements incorporated by reference in Part III of this Form 10-K or any amendment to this Form 10-K. ☒

Indicate by check mark whether the registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definitions of “large accelerated filer,” “accelerated filer,” “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

Large accelerated filer ☐ | | Accelerated filer ☒ | | Non-accelerated filer ☐ | |

Smaller Reporting Company ☐ | | Emerging growth company ☐ | | | |

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial account standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). Yes ☐ No ☒

State the aggregate market value of the voting and non-voting common equity held by non-affiliates computed by reference to the price at which the common equity was last sold, or the average bid and asked price of such common equity, as of the last business day of the registrant’s most recently completed second fiscal quarter: $345,865,178 as of August 4, 2018.

Indicate the number of shares outstanding of each of the registrant’s classes of common stock, as of the latest practicable date: Common Stock, par value $.01 per share, 12,132,535 shares outstanding as of April 2, 2019.

DOCUMENTS INCORPORATED BY REFERENCE

Part III incorporates information from the registrant’s definitive proxy statement, to be filed with the Securities and Exchange Commission within 120 days after the close of the registrant’s fiscal year covered by this Annual Report on Form 10-K, with respect to the Annual Meeting of Stockholders to be held on June 5, 2019.

FORM 10-K REPORT INDEX

Table of Contents

PART I

Some statements in, or incorporated by reference into, this Annual Report on Form 10-K (this “Report”) of Citi Trends, Inc. (“we,” “us,” or the “Company”) may constitute “forward-looking statements” within the meaning of Section 27A of the Securities Act of 1933, as amended, and Section 21E of the Securities Exchange Act of 1934, as amended (the “Exchange Act”). All statements other than historical facts contained in this Report, including statements regarding our future financial position, business policy and plans, objectives and expectations of management for future operations and capital allocation expectations, are forward-looking statements. The words “believe,” “anticipate,” “project,” “plan,” “expect,” “estimate,” “objective,” “forecast,” “goal,” “intend,” “could,” “will likely result,” or “will continue” and similar expressions, as they relate to us, are intended to identify forward-looking statements, although not all forward-looking statements contain such language. We have based these forward-looking statements largely on our current expectations and projections about future events, including, among other things: our ability to anticipate and respond to fashion trends, competition in our markets, consumer spending patterns, general economic conditions, actions of our competitors or anchor tenants in the strip shopping centers where our stores are located, anticipated fluctuations in our operating results and expected cash position.

These forward-looking statements are subject to a number of risks, uncertainties and assumptions, including those described in Item 1A. Risk Factors and elsewhere in this Report and the other documents we file with the Securities and Exchange Commission (“SEC”), including our reports on Form 8-K and Form 10-Q, and any amendments thereto. Because forward-looking statements are inherently subject to risks and uncertainties, some of which cannot be predicted or quantified, you should not rely upon forward-looking statements as predictions of future events. The events and circumstances reflected in the forward-looking statements may not be achieved or occur and actual results could differ materially from those projected in the forward-looking statements. These forward-looking statements speak only as of the date of such statements. Except as required by applicable law, including the securities laws of the United States and the rules and regulations of the SEC, we do not plan to publicly update or revise any forward-looking statements contained in this Report, whether as a result of any new information, future events or otherwise.

Information is provided herein with respect to our operations related to our fiscal years ended on February 2, 2019 (“fiscal 2018”), February 3, 2018 (“fiscal 2017”) and January 28, 2017 (“fiscal 2016”).

ITEM 1.BUSINESS

Overview and History

We are a value-priced retailer of urban fashion apparel and accessories for the entire family. Our merchandise offerings are designed to appeal to the fashion preferences of value-conscious consumers, particularly African-Americans. We believe that we provide merchandise at compelling values. Our goal is to provide merchandise at discounts to department and specialty stores’ regular prices of 20% to 70%. Our stores average approximately 11,000 square feet of selling space and are typically located in neighborhood shopping centers that are convenient to low and moderate income customers. As of February 2, 2019, we operated 562 stores in both urban and rural markets in 32 states.

Our predecessor, Allied Department Stores, was founded in 1946 and grew into a chain of family apparel stores operating in the Southeast. In 1999, the Company, then consisting of 85 stores, was acquired by a private equity firm. Following this acquisition, management implemented several strategies to focus on the growing urban market and improve our operating and financial performance. After the successful implementation of these strategies and the successful growth of our chain from 85 stores to 212 stores, we completed an initial public offering of our common stock on May 18, 2005.

We are a Delaware corporation, and our executive offices are located at 104 Coleman Boulevard, Savannah, Georgia 31408 and our telephone number is (912) 236-1561. Our Internet address is http://www.cititrends.com. The reference to our web site address in this Report does not constitute the incorporation by reference of the information contained at the web site into this Report. We make available, free of charge through publication on our web site, copies of our Annual Report on Form 10-K, quarterly reports on Form 10-Q, current reports on Form 8-K, and amendments to those reports, as soon as reasonably practicable after we have filed such materials with, or furnished such materials to, the SEC. In addition, you may read and print any materials we file with the SEC on the SEC’s web site at http://www.sec.gov.

Company Strengths and Strategies

Our goal is to be the leading value-priced retailer of urban fashion apparel and accessories. We believe the following business strengths differentiate us from our competitors and are important to our success:

Focus on Urban Fashion Mix. We focus our merchandise on urban fashions, which we believe appeal to our core customers. We do not attempt to dictate trends, but rather devote considerable effort to identifying emerging trends and ensuring that our apparel assortment is considered timely and fashionable in the urban market. Our merchandising staff tests new emerging merchandise trends before reordering and actively manages the mix of fashion and branded products in the stores to keep our offering fresh and minimize markdowns.

Superior Value Proposition. As a value-priced retailer, we seek to offer top quality, fashionable merchandise at compelling prices in relation to department and specialty stores. We also offer products under our proprietary brands such as “Citi Steps” and “Red Ape.” These private brands enable us to expand our product selection, offer fashion merchandise at lower prices and enhance our product offerings.

Merchandise Mix that Appeals to the Entire Family. We merchandise our stores to create a destination environment capable of meeting the fashion needs of the entire value-conscious family. Each store offers a wide variety of products for men and women, as well as children. Our stores feature sportswear, dresses, outerwear, footwear, intimate apparel, accessories, scrubs, beauty and home. We believe that the breadth of our merchandise distinguishes our stores from many competitors that offer urban apparel primarily for women, and reduces our exposure to fashion trends and demand cycles in any single category.

Strong and Flexible Sourcing Relationships. We maintain strong sourcing relationships with a large group of suppliers. We have purchased merchandise from approximately 1,700 vendors in the past 12 months. Purchasing is controlled by a 50 member buying team located in one of our three buying offices - New York, New York; Los Angeles, California; and our Savannah, Georgia headquarters. We purchase merchandise through planned programs with vendors at reduced prices and opportunistically through close-outs, with the majority of our merchandise purchased for the current season and a lesser quantity held for sale in future seasons. To foster vendor relationships, we pay vendors promptly and do not ask for typical retail concessions, such as promotional and markdown allowances.

Attractive Fashion Presentation and Store Environment. We seek to provide a fashion-focused shopping environment that is similar to a specialty apparel retailer, rather than a typical off-price store. Products are prominently displayed by style, rather than by size, on dedicated, four-way fixtures featuring multiple sizes and styles. The remaining merchandise is arranged on hanging racks. The stores are carpeted and well-lit, with most featuring a sound system that plays urban adult and urban contemporary music throughout the store.

Cost-Effective Store Locations. We locate stores in high traffic strip shopping centers that are convenient to low and moderate income neighborhoods. We generally utilize previously occupied store sites which enables us to obtain attractive rents. Similarly, advertising expenses are low as we do not rely on promotion-driven sales but rather seek to build our reputation for value through everyday low prices. At the same time, from an investment perspective, we seek to design stores that are inviting and easy to shop, while limiting startup and fixturing costs.

Product Merchandising and Pricing

Products. Our merchandising strategy is to offer fashionable urban apparel and accessories at attractive prices for the entire value-conscious family. We seek to maintain a diverse assortment of first quality, in-season merchandise that appeals to the distinctive tastes and preferences of our core customers. Approximately 20% of our net sales in fiscal 2018 were represented by nationally recognized brands. We also offer a wide variety of products from less recognized brands and a lesser amount representing private label products under our proprietary brands.

Our merchandise includes apparel, accessories and home. Within apparel, we offer fashion sportswear for men, women and children, including offerings for newborns, infants, toddlers, boys and girls. Accessories include handbags, jewelry, footwear, belts, intimate apparel, scrubs and sleepwear. Home includes functional bedroom, bathroom and kitchen products, as well as beauty and toys.

The following table sets forth the merchandise assortment by classification as a percentage of net sales for fiscal 2018, 2017 and 2016.

| | | | | | | |

| | Percentage of Net Sales | |

| | 2018 | | 2017 | | 2016 | |

Accessories | | 32 | % | 32 | % | 31 | % |

Children’s | | 23 | % | 23 | % | 23 | % |

Ladies’ | | 22 | % | 23 | % | 24 | % |

Men’s | | 17 | % | 17 | % | 17 | % |

Home | | 6 | % | 5 | % | 5 | % |

Pricing. We purchase our merchandise at attractive prices and mark prices up less than department or specialty stores. We seek to provide nationally recognized brands at prices that are 20% to 70% below regular retail prices available in department stores and specialty stores. Further, we consider the price-to-value relationships of our non-branded products to be exceptionally strong. Both branded and non-branded offerings validate our value and fashion positioning to our customers. We review each department in our stores at least monthly for possible markdowns based on sales rates and fashion seasons to promote faster turnover of inventory and to accelerate the flow of current merchandise. In late 2019, we plan to implement a Markdown Optimization System, which is expected to improve our ability to determine optimal price reductions and timing, minimize end-of-season inventory and provide the ability to execute markdowns at the store level.

Sourcing and Allocation

The merchandising department oversees the sourcing, planning and allocation of merchandise to our stores, which allows us to utilize volume purchase discounts and maintain control over our inventory. We source our merchandise from approximately 1,700 vendors, consisting of domestic manufacturers and importers. Our merchandising department consists of a buying team of 50 merchants and a planning and allocation team, which is comprised of over 30 associates.

The buyers on our buying team have, on average, 15 years of experience in the retail business and have developed long-standing relationships with many of our vendors, including those controlling the distribution of branded apparel. Our buyers, who are based in New York, Los Angeles and Savannah, travel regularly to the major United States apparel markets, visiting major manufacturers and attending national and regional trade shows, including urban-focused trade shows.

Our buyers purchase merchandise in styles, sizes and quantities to meet inventory levels developed by the planning staff. The buying staff utilizes several purchasing techniques that enable us to offer to customers branded and non-branded fashion merchandise at everyday low prices. The majority of the nationally recognized branded products we sell are purchased in-season, and we generally purchase later in the merchandising buying cycle than department and specialty stores. This allows us to take advantage of imbalances between retailers’ demands for specific merchandise and manufacturers’ supply of that merchandise. We also purchase merchandise from some vendors in advance of the selling season at reduced prices and purchase merchandise on an opportunistic basis near the end of the selling season, which we then store in our distribution centers for sale three to nine months later. Where possible, we seek to purchase items based on style or color in limited quantities on a test basis with the right to reorder as needed. Finally, we purchase private brand merchandise that we source to our specifications.

We allocate merchandise across our store base according to sales and merchandise plans that are created by our planning and allocation teams. The merchandising staff utilizes a centralized management system to monitor merchandise purchasing, planning and allocation in order to maximize inventory turnover, identify and respond to changing product demands and determine the timing of markdowns to our merchandise. The recent addition of a store-level planning system assists our team in their efforts to allocate merchandise to individual stores based on local customer preferences. The buyers also regularly review the age and condition of the merchandise and manage both the reordering and clearance processes. In addition, the merchandising team communicates with regional, district and store managers to ascertain regional and store-level conditions and to better ensure that our product mix meets our consumers’ demands in terms of quality, fashion, price and overall value.

We accept payment from our customers for merchandise at time of sale. Payments are made to us by cash, check, Visa™, MasterCard™, American Express™, or Discover™. We do not extend credit terms to our customers; however, we do offer a layaway service.

Seasonality

The nature of our business is seasonal. Historically, sales in the first and fourth quarters have been higher than sales achieved in the second and third quarters of the fiscal year. Expenses and, to a greater extent, operating income, vary by quarter. Results of a period shorter than a full year may not be indicative of results expected for the entire year. Furthermore, the seasonal nature of our business may affect comparisons between periods.

Store Operations

Store Format. The average selling space of our 562 stores is approximately 11,000 square feet, which allows us the space and flexibility to departmentalize our stores and provide directed traffic patterns. We arrange most of our stores in a racetrack format with ladies’ sportswear in the center of each store and complementary categories adjacent to those items. Men’s and boy’s apparel and footwear are displayed on one side of the store, while dresses, ladies’ footwear and accessories are displayed on the other side. Merchandise for

infants, toddlers, boys and girls, as well as home goods, are displayed along the back of the store. Impulse items, such as jewelry and sunglasses, are featured near the checkout area. Products from nationally recognized brands and other current fashion styles are prominently displayed on four-way racks at the front of each department. The remaining merchandise is displayed on hanging racks and occasionally on table displays. Large hanging signs identify each category location. The unobstructed floor plan allows the customer to see virtually all of the different product areas from the store entrance and provides us the flexibility to easily expand and contract departments in response to customer demand, seasonality and merchandise availability. Virtually all of our inventory is displayed on the selling floor.

Store Management. Store operations are managed by our Senior Vice President of Store Operations, four regional vice presidents and 51 district managers, each of whom manages eight to fifteen stores. The typical store is staffed with a store manager, two or three assistant managers and seven to eight part-time sales associates, all of whom rotate work days on a shift basis. Store managers and assistant store managers participate in a bonus program based on achieving predetermined levels of sales and inventory shrinkage. District managers participate in bonus programs based on achieving targeted levels of sales, profits, inventory shrinkage and payroll costs. Regional Vice Presidents participate in a bonus program based partly on a roll-up of the district managers’ bonuses and partly on the Company’s profit performance in relation to budget. Sales associates are compensated on an hourly basis with incentives. Moreover, we recognize individual performance through internal promotions and provide opportunities for advancement.

We place significant emphasis on loss prevention in order to control inventory shrinkage. Initiatives include electronic tags on many of our products, training and education of store personnel on loss prevention issues, digital video camera systems, alarm systems and motion detectors in the stores. We also visually monitor the stores throughout the day using sophisticated camera systems, capture extensive point-of-sale data and maintain systems that monitor returns, voids and employee sales, and produce trend and exception reports to assist in identifying shrinkage issues. We have a centralized loss prevention team that focuses exclusively on implementation of these initiatives and specifically on stores that have experienced above average levels of shrinkage. We also maintain an independent, third party administered, toll-free line for reporting shrinkage concerns and any other employee concerns.

Employee Training. Our employees are critical to achieving our goals, and we strive to hire employees with high energy levels and motivation. We have well-established store operating policies and procedures and an extensive 30-day in-store training program for new store managers and assistant managers. Sales associates also participate in a 14-day customer service and store procedures training program, which is designed to enable them to assist customers in a friendly, helpful manner.

Layaway Program. We offer a layaway program that allows customers to purchase merchandise by initially paying a 20% deposit and a $2 service charge, although at various times, we have reduced the deposit requirement to 10% and waived the service charge in connection with promotional events. The customer then makes additional payments every two weeks and has 60 days within which to complete the purchase. If the purchase is not completed, the customer receives a Citi Trends gift card for amounts paid less a re-stocking and layaway service fee.

Site Selection. Cost-effective store locations are an important part of our store profitability model. Accordingly, we look for second and third use store locations that offer attractive rents, but also meet our demographic and economic criteria. We have a dedicated real estate management team responsible for new store site selection. In selecting a location, we target both urban and rural markets. Demographic criteria used in site selection include concentrations of our core consumers. In addition, we require convenient site accessibility, as well as strong co-tenants, such as food stores, dollar stores and rent-to-own stores.

Shortly after we sign a new store lease and complete the necessary leasehold improvements to the building, we prepare the store over a three to four week period by installing fixtures, signs, dressing rooms, checkout counters and cash register systems and merchandising the initial inventory.

Advertising and Marketing

Our marketing goals are to build the “Citi Trends” brand, promote customers’ association of the “Citi Trends” brand with value, quality, fashion and everyday low prices, and drive traffic into our stores. We generally focus our advertising efforts during the first quarter (Spring/Easter), back-to-school and Christmas through the use of hip-hop radio stations, social media and influencer marketing. In addition, we promote fashion trends and exciting deals in our window signage and through in-store announcements. In 2011, we started a Facebook page which has grown to nearly 600,000 followers.

Distribution

All merchandise sold in our stores is shipped directly from our distribution centers in Darlington, South Carolina and Roland, Oklahoma, utilizing various express package distributors. Our stores receive multiple shipments of merchandise from our distribution centers each week. The Darlington distribution center has 550,000 square feet of space, while the Roland distribution center has 565,000 square feet of space.

We have engaged a consulting firm to help us identify more efficient and less costly distribution alternatives. Likely opportunities include implementing a transportation management system; leveraging the consultant’s relationships with transportation service providers; expanding the number of in-bound trucking options; and evaluating the current out-bound to store model. This project has begun and is expected to continue into 2020. Benefits from these efforts are expected to begin in the second quarter of 2019 and continue to grow throughout the life of the project.

Information Technology and Systems

We have information systems in place to support our core business functions, using a combination of industry-standard third party products and internally developed applications. These systems support purchase order management, price and markdown management, merchandise planning and allocation, general ledger, accounts payable, sales audit, loss prevention and supply chain functions. We continue to evaluate and implement new technologies to enhance the execution of our merchandising strategies, improve our operating efficiencies and maintain financial control.

In 2018, we completed the rollout of our store-level planning system which allows for improved allocations at each level of the merchandise hierarchy. In addition, we launched a new retail analytics solution which provides transaction based reporting to assist with loss prevention activities.

Our 2019 projects include:

| · | | Markdown Optimization System – expected to determine optimal price reductions and timing, minimize end-of-season inventory, and provide the ability to execute markdowns at the store level |

| · | | Transportation Management System – expected to optimize in-bound and out-bound shipments resulting in transportation cost savings |

| · | | Warehouse Packing System – expected to improve merchandise packing efficiency, leading to an expected reduction in payroll costs |

| · | | Point-of-Sale System replacement – initiation of a project to replace our existing point-of-sale environment which is expected to improve operational and transactional processes, establish an enterprise return management system to reduce return fraud, and provide the foundation for future business initiatives. |

The security of our information technology systems is critical to us. We use commercially available security systems to protect Company, employee, customer and vendor information, and we employ a cybersecurity program to address ongoing security threats. Our program includes, but is not limited to, routine penetration and vulnerability testing, network segmentation, strong encryption protocols, virus and malware protection, email security scanning, simulation training, vendor assessments, and ongoing monitoring and patching activities. Within our stores, we use external chip-accepting pin pad devices which employ point-to-point encryption technology for the protection of our customer’s payment information. We do not retain encrypted, hashed, or tokenized payment information within our internal systems. In addition, we are subject to the Payment Card Industry’s Data Security Standards (PCI DSS) to which we attest compliance annually.

We believe that our information systems, with upgrades and updates over time, are adequate to support our operations for the foreseeable future.

Growth Strategy

Drive Comparable Store Sales Growth. We have a number of strategies in place that are focused on continuing to increase our comparable store sales, including the following:

| · | | Continued push toward lines of business that have proven to be consistent sales drivers over extended periods of time, including, among other things, accessories and home merchandise, |

| · | | Improvement of our fashion assortments within apparel to meet the demands of our unique customer base, |

| · | | Recent addition of internal store planning resources and the implementation of a store-level planning system, which we expect will improve our ability to allocate inventory at each level of the merchandise hierarchy, |

| · | | Future implementation of a markdown optimization system which is expected to improve our ability to determine the optimal amount and timing of markdowns, as well as provide us with the ability to take markdowns at the store level, |

| · | | Continued testing and introduction of new categories of merchandise that meet the needs of our customers, and |

| · | | Continued evolution of our marketing strategies through the use of digital advertising and influencers |

Increase Store Base. We believe that our store potential for the existing concept is up to 800 stores. This concept, which has historically done well in predominantly African-American markets, has proven to be portable across much of the country. In fact, of the twenty Citi Trends stores with the highest level of profit, sixteen are located in different cities. Also, only six of our stores are not profitable on a four-wall basis.

After opening nineteen new stores in fiscal 2018, we plan to open approximately twenty new stores in fiscal 2019, including our first test stores in markets that are predominantly Hispanic. We already serve the Hispanic consumer in many of our stores, although not at the same level as the African-American consumer. We currently have 36 stores with at least 40% Hispanic population within three miles. These stores, on average, have sales that are approximately 9% higher than our average store, while attaining profit levels that are virtually identical to the average store. As a result, we have a sampling of existing stores that we can use as guides in determining how to appropriately merchandise stores in Hispanic markets.

Competition

The markets we serve are highly competitive. The principal methods of competition in the retail business are fashion, assortment, pricing and presentation. We believe we have a competitive advantage in our offering of fashionable merchandise at everyday low prices. We compete against a diverse group of retailers, including national off-price retailers, mass merchants, smaller specialty retailers and dollar stores. The off-price retail companies with which we compete include TJX Companies, Inc. (“TJX Companies”), Ross Stores, Inc. (“Ross Stores”), The Cato Corporation (“Cato”), and Burlington Stores, Inc. (“Burlington”). In particular, Ross Stores’ “dd’s DISCOUNTS” stores, and Cato’s “It’s Fashion Metro” stores target lower and moderate income consumers. We believe our strategy of appealing to African-American consumers and offering urban apparel products allows us to compete successfully with these retailers. We also believe we offer a more inviting store format than the traditional off-price retailers, including our use of carpeted floors and more prominently displayed brands. In addition, we compete with a group of smaller specialty retailers that sell only women’s products, such as Rainbow, as well as value-oriented retailers, such as Forman Mills and Variety Wholesalers. Our mass merchant competitors include Wal-Mart, Target and Kmart. These chains do not focus on fashion apparel and, within their apparel offering, lack the urban focus that we believe differentiates our offering and appeals to our core customers. Similarly, while some of the dollar store chains offer apparel, they typically offer a more limited selection focused on basic apparel needs. As a result, we believe there is significant demand for a value-priced retailer that addresses the market of low and moderate income consumers generally and, particularly, African-American and other consumers who seek value-priced, urban fashion apparel, accessories and home goods. See Item 1A. Risk Factors in this Report for additional information regarding competition in our markets.

Intellectual Property

We regard our trademarks and service marks as having significant value and as being important to our marketing efforts. We have registered “Citi Trends” as a trademark with the U.S. Patent and Trademark Office on the Principal Register for retail department store services. We have also registered the following trademarks with the U.S. Patent and Trademark Office on the Principal Register for various apparel: “Citi Steps,” “Citi Trends Fashion for Less,” “Lil Ms Hollywood,” “Red Ape,” and “Vintage Harlem.” Our policy is to pursue registration of our marks and to oppose vigorously infringement of our marks.

Employees

As of February 2, 2019, we had approximately 2,800 full-time and approximately 2,700 part-time employees. Of these employees, approximately 4,700 are employed in our stores and the remainder are employed in our distribution centers, buying offices and corporate office. We are not a party to any collective bargaining agreements, and none of our employees are represented by a labor union.

ITEM 1A.RISK FACTORS

You should carefully consider the following risk factors, together with the other information contained or incorporated by reference into this Report. The risks and uncertainties described below are not the only ones we face. Additional risks and uncertainties not presently known to us or that we deem to be currently immaterial also may impair our business operations. The occurrence of any of the following risks could have a material adverse effect on our business, financial condition and results of operations.

Our success depends on our ability to anticipate, identify and respond rapidly to changes in consumers’ fashion tastes, and our failure to adequately evaluate fashion trends could have an adverse effect on our business, financial condition and results of operations.

The apparel industry in general and our core customer market in particular are subject to rapidly evolving fashion trends and shifting consumer demands. Accordingly, our success is heavily dependent on our ability to anticipate, identify and capitalize on emerging fashion trends, including products, styles and materials that will appeal to our target consumers. A failure on our part to anticipate, identify or react appropriately and timely to changes in styles, trends, brand preferences or desired image preferences is likely to lead to lower demand for our merchandise, which could cause, among other things, sales declines, excess inventories and higher markdowns.

If we are unsuccessful in competing with our retail apparel competitors, our market share could decline or our growth could be impaired and, as a result, our business, financial condition and results of operations could be negatively impacted.

The retail apparel and home fashion businesses are highly competitive with few barriers to entry. We compete against a diverse group of retailers, including national off-price apparel chains such as TJX Companies, Ross Stores, Cato, and Burlington; mass merchants such as Wal-Mart, Target and Kmart; smaller discount retail chains that sell only women’s products, such as Rainbow; and general merchandise discount stores and dollar stores, which offer a variety of products, including apparel, home fashions and other merchandise we sell, for the value-conscious consumer. We also compete against local off-price and specialty retail stores, regional retail chains, traditional department stores, web-based retail stores and other direct retailers.

The level of competition we face from these retailers varies depending on the product segment, as many of our competitors do not offer apparel for the entire family. Our greatest competition is generally in women’s apparel. Many of our competitors are larger than we are and have substantially greater resources than we do and, as a result, may be able to adapt better to changing market conditions, exploit new opportunities and exert greater pricing pressures on suppliers than we can. Many of these retailers have better name recognition among consumers than we do and purchase significantly more merchandise from vendors. These retailers may be able to purchase merchandise that we cannot purchase because of their name recognition and relationships with suppliers, or they may be able to purchase merchandise with better pricing concessions than we can. Our local and regional competitors have extensive knowledge of the consumer base and may be able to garner more loyalty from customers than we can. If the consumer base we serve is satisfied with the selection, quality and price of our competitors’ products, consumers may decide not to shop in our stores. Additionally, if our existing competitors or other retailers decide to focus more on our core customers, we may have greater difficulty in competing effectively. As a result of this competition, we may experience pricing pressures, increased marketing expenditures, increased costs to open new stores, as well as loss of market share, which could materially and adversely affect our business, financial condition and results of operations.

Our ability to attract consumers to our stores depends on the success of the strip shopping centers where our stores are located.

We locate our stores primarily in strip shopping centers where we believe our consumers and potential consumers shop. The success of an individual store can depend on favorable placement within a given strip shopping center and from the volume of traffic generated by the other destination retailers and the anchor stores in the strip shopping centers where our stores are located. We cannot control the development of alternative shopping destinations near our existing stores or the availability or cost of real estate within existing or new shopping destinations. If our store locations fail to attract sufficient consumer traffic or we are unable to locate replacement locations on terms acceptable to us, our business could suffer. If one or more of the destination retailers or anchor stores located in the strip shopping centers where our stores are located close or leave, or if there is significant deterioration of the surrounding areas in which our stores are located, our business may be adversely affected.

We may not be able to sustain our growth plans or successfully implement our long-term strategic goals.

Our growth strategy includes successfully opening and operating new stores and expanding our value-priced model within our current markets and into new geographic regions, as well as potentially branching out into some new store concepts. There are significant risks associated with our ability to continue to expand successfully and managing the implementation of this growth effectively. If any aspect

of our expansion strategy does not achieve the success we expect, in whole or in part, we may fail to meet our financial performance expectations, slow our planned growth or close stores or operations. For example, we intend to open approximately 20 new stores in fiscal 2019, while refreshing, remodeling or relocating a portion of our existing store base. The success of opening new stores is dependent upon, among other things, the current retail environment, the identification of suitable markets and the availability of real estate that meets our criteria for traffic, square footage, co-tenancies, lease economics, demographics, and other factors, the negotiation of acceptable lease terms, construction costs, the hiring, training and retention of competent sales personnel, and the effective management of inventory to meet the needs of new and existing stores on a timely basis. We may not be able to execute our growth strategies successfully, on a timely basis, or at all. If we fail to implement these strategies successfully, or if these strategies do not yield the desired outcomes, our financial condition and results of operations would be adversely affected.

We could experience a reduction in sales if we are unable to fulfill our current and future merchandising needs.

We depend on our suppliers for the continued availability and satisfactory quality of our merchandise. Most of our suppliers could discontinue selling to us at any time. Additionally, if the manufacturers or other owners of brands or trademarks terminate the license agreements under which some of our suppliers sell our products, we may be unable to obtain replacement merchandise of comparable fashion appeal or quality, in the same quantities or at the same prices. In addition, a number of our suppliers are smaller, less capitalized companies and are more likely to be impacted by unfavorable general economic and market conditions than larger and better capitalized companies. These smaller suppliers may not have sufficient liquidity during economic downturns to properly fund their businesses, and their ability to supply their products to us could be negatively impacted. If we lose the services of one or more of our significant suppliers or one or more of them fail to meet our merchandising needs, we may be unable to timely or adequately replace the merchandise we currently source with merchandise provided elsewhere, which could negatively impact our sales and results of operations.

Failure to properly manage and allocate our inventory could have an adverse effect on our business, sales, margins, financial condition, and results of operations.

In order to better serve our customers and maximize sales, we must properly execute our inventory management strategies by appropriately allocating merchandise among our stores, timely and efficiently distributing inventory to such locations, maintaining an appropriate mix and level of inventory in such locations, appropriately changing the allocation of floor space of stores among product categories to respond to customer demand, and effectively managing pricing and markdowns, and there is no assurance we will be able to do so. In addition, as we implement new inventory allocation initiatives, there could be disruptions in inventory flow and placement. Failure to effectively execute our opportunistic inventory buying and inventory management strategies could adversely affect our business, financial condition and results of operations.

If we are unable to provide frequent replenishment of fresh, quality, attractively priced merchandise in our stores, it could adversely affect traffic to our stores as well as our sales and margins. We base our purchases of inventory, in part, on our sales forecasts. If our sales forecasts do not match customer demand, we may experience higher inventory levels and need to markdown excess or slow-moving inventory, leading to decreased profit margins, or we may have insufficient inventory to meet customer demand, leading to lost sales, either of which could adversely affect our financial performance. We need to purchase inventory sufficiently below conventional retail to maintain our pricing differential to regular department and specialty store prices, and to attract customers and sustain our margins, which we may not achieve at various times and which could adversely affect our business, financial condition and results of operations.

Our sales could decline as a result of general economic and other factors outside of our control, such as changes in consumer spending patterns and declines in employment levels.

Downturns, or the expectation of a downturn, in general economic conditions, including the effects of unemployment levels, salaries and wage rates, interest rates, levels of consumer debt, inflation in food and energy prices, taxation (including delays in the distribution of tax refunds), government stimulus, consumer confidence, and other macroeconomic factors, could adversely affect consumer spending patterns, our sales and our results of operations. Consumer confidence may also be affected by domestic and international political unrest, acts of war or terrorism, natural disasters or other significant events outside of our control, any of which could lead to a decrease in spending by consumers. Because apparel generally is a discretionary purchase, declines in consumer spending patterns may have a more negative effect on apparel retailers than some other retailers. In addition, since many of our stores are located in the southeastern United States, our operations are more susceptible to regional factors than the operations of our more geographically diversified competitors. Therefore, any adverse economic conditions that have a disproportionate effect on the southeastern United States could have a greater negative effect on our sales and results of operations than on retailers with a more geographically diversified store base.

We do not sell our products through the internet. As the retail industry experiences an increase in online sales, our sales could be adversely affected.

The retail landscape is changing with consumers’ shopping habits shifting away from the traditional brick-and-mortar stores to online retailers. Internet sales have been obtaining an increasing percentage of retail sales over the past few years and this trend is expected to continue. Although we have tested the sale of products through the internet, we no longer have any items available on our company’s website. The continued growth of online sales could have a negative impact on our sales, as our customers may decide to make purchases through online retailers.

Adverse trade restrictions may disrupt our supply of merchandise. We also face various risks because much of our merchandise is imported from abroad.

We do not own or operate any manufacturing or production facilities. We purchase the products we sell directly from approximately 1,700 vendors, and a substantial portion of this merchandise is manufactured outside of the United States and imported by our vendors from countries such as China and other areas of the Far East. The countries in which our merchandise currently is manufactured or may be manufactured in the future could become subject to new trade restrictions imposed by the United States or other foreign governments. There is increased uncertainty with respect to trade relations between the United States and other countries, especially China. Trade restrictions, including increased customs restrictions and tariffs or quotas against apparel or home items, as well as United States or foreign labor strikes, work stoppages or boycotts, could increase the cost or reduce the supply or impede the timely delivery of merchandise available to us and have an adverse effect on our business. In addition, our merchandise supply could be impacted if our vendors’ imports become subject to existing or future duties and quotas, or if our vendors face increased competition from other companies for production facilities, import quota capacity and shipping capacity.

We also face a variety of other risks generally associated with relying on vendors that do business in foreign markets and import merchandise from abroad, such as:

| · | | political or labor instability, natural disasters, or the threat of terrorism, in particular in countries where our vendors source merchandise; |

| · | | increases in merchandise costs due to raw material price inflation or changes in purchasing power caused by fluctuations in currency exchange rates; |

| · | | enhanced security measures at United States and foreign ports, which could delay delivery of imports; |

| · | | imposition of new or supplemental duties, taxes, and other charges on imports; |

| · | | compliance with new or changing import/export controls; |

| · | | delayed receipt or non-delivery of goods due to the failure of foreign-source suppliers to comply with import regulations, organized labor strikes or congestion at United States ports; and |

| · | | local business practice and political issues, including issues relating to compliance with domestic or international labor and environmental standards. |

We rely on numerous third parties in the supply chain to produce and deliver the products that we sell, and our business may be negatively impacted by their failure to comply with applicable law.

Merchandise we sell in our stores is subject to regulatory standards set by various governmental authorities with respect to quality and safety. Regulations in this area may change from time to time. We rely on numerous third parties to supply quality merchandise that complies with applicable product safety laws and other applicable laws, but they may not comply with their obligations to do so. Violations of law by our importers, suppliers, manufacturers or distributors could result in delays in shipments and receipt of goods or damage our reputation, thus causing our sales to decline. Although our arrangements with our vendors frequently provide for indemnification for product liabilities, the vendors may fail to honor those obligations to an extent we consider sufficient or at all. Issues with the quality and safety of merchandise we sell in our stores, regardless of our fault, or customer concerns about such issues, could result in damage to our reputation, lost sales, uninsured product liability claims or losses, merchandise recalls, increased costs, and regulatory, civil or criminal fines or penalties, any of which could have a material adverse effect on our financial results. Further, we are

susceptible to the receipt of counterfeit brands, infringing products or unlicensed goods. We could incur liability with manufacturers or other owners of the brands or trademarked products if we receive and sell counterfeit brands, infringing products or unlicensed goods, even inadvertently, and, therefore, it is important that we establish relationships with reputable vendors to reduce the risk that we may inadvertently receive counterfeit brands, infringing products or unlicensed goods. Although we have a quality assurance team to check merchandise in an effort to assure that we purchase only authentic brands and licensed goods and are careful in selecting our vendors, we may receive products that we are prohibited from selling or incur liability for selling counterfeit brands, infringing products or unlicensed goods, which could adversely impact our results of operations.

A significant disruption to our distribution process or southeastern retail locations could have an adverse effect on our business, financial condition and results of operations.

Our ability to distribute our merchandise to our store locations in a timely manner is essential to the efficient and profitable operation of our business. We have distribution centers located in Darlington, South Carolina and Roland, Oklahoma. Any natural disaster or other disruption to the operation of either of these facilities due to fire, accidents, weather conditions or any other cause could damage a significant portion of our inventory and impair our ability to stock our stores adequately.

In addition, the southeastern United States, where the Darlington distribution center and many of our stores are located, is vulnerable to significant damage or destruction from hurricanes and tropical storms. Although we maintain insurance on our stores and other facilities, the economic effects of a natural disaster that affects our distribution centers and/or a significant number of our stores could have an adverse effect on our business, financial condition and results of operations.

Additionally, any disruption to the efficient or timely transportation of merchandise to our distribution centers or stores could adversely affect our business, financial condition and results of operations.

If we fail to protect our name and brand in the marketplace, there could be a negative effect on our business and limitations on our ability to penetrate new markets.

We believe that our “Citi Trends” trademark is integral to our store design and our success in building consumer loyalty to our brand. We have registered this trademark with the U.S. Patent and Trademark Office. We have also registered, or applied for registration of, additional trademarks with the U.S. Patent and Trademark Office that we believe are important to our business. We cannot assure you that these registrations will prevent imitation of our name, merchandising concept, store design or private label merchandise or the infringement of our other intellectual property rights by others. Imitation of our name, concept, store design or merchandise in a manner that projects lesser quality or carries a negative connotation of our brand image could have an adverse effect on our reputation, business, financial condition and results of operations.

In addition, we cannot assure you that others will not try to block the manufacture or sale of our private label merchandise by claiming that our merchandise violates their trademarks or other proprietary rights since other entities may have rights to trademarks that contain the word “Citi” or may have rights in similar or competing marks for apparel and/or accessories. Although we cannot currently estimate the likelihood of success of any such lawsuit or ultimate resolution of such a conflict, such a controversy could have an adverse effect on our business, financial condition and results of operations.

If we fail to implement and maintain effective internal controls in our business, there could be an adverse effect on our business, financial condition, results of operations and stock price.

Section 404 of the Sarbanes Oxley Act of 2002 requires annual management assessments of the effectiveness of our internal controls over financial reporting and an audit of such controls by our independent registered public accounting firm. If we fail to maintain the adequacy of our internal controls, we may be unable to conclude on an ongoing basis that we have effective internal controls over financial reporting. Moreover, effective internal controls, particularly those related to revenue recognition and accounting for inventory/cost of sales, are necessary for us to produce reliable financial reports and are important in our effort to prevent financial fraud. If we cannot produce reliable financial reports or prevent fraud, our business, financial condition and results of operations could be harmed, investors could lose confidence in our reported financial information, the market price of our stock could decline significantly and we may be unable to obtain additional financing to operate and expand our business.

Failure to attract, train, assimilate and retain skilled personnel could have an adverse effect on our financial condition.

Like most retailers, we experience significant employee turnover rates, particularly among store sales associates and managers. We therefore must continually attract, hire and train new personnel to meet our staffing needs. We constantly compete for qualified

personnel with companies in our industry and in other industries. A significant increase in the turnover rate among our store sales associates and managers would increase our recruiting and training costs and could cause us to be unable to service our customers effectively, thus reducing our ability to operate our stores as profitably as we have in the past.

In addition, we rely heavily on the experience and expertise of our senior management team and other key management associates, and accordingly, the loss of their services could have a material adverse effect on our business strategy and results of operations.

Our business could be negatively affected as a result of a proxy fight and the actions of activist shareholders.

If we become engaged in a proxy contest with activist shareholders in the future, our business could be adversely affected because:

Responding to proxy contests, litigation and other actions by activist stockholders can be costly and time-consuming, disrupt our operations and divert the attention of management and our employees.

Perceived uncertainties as to our future direction may result in the loss of potential business opportunities and harm our ability to attract new investors and to retain and attract experienced executives and employees.

If individuals are elected to our board of directors with a specific agenda, it may adversely affect our ability to retain and attract experienced directors, executives and employees, to effectively and timely implement our business strategy and create additional value for stockholders.

We may experience a significant increase in legal fees, administrative, advisor and associated costs incurred in connection with responding to a proxy contest or related action. For example, we incurred $2.5 million in expenses as a result of the proxy contest in connection with our 2017 annual meeting.

These factors could adversely impact our results of operations and could also cause our stock price to experience periods of volatility or stagnation.

Increases in the minimum wage could have an adverse effect on our operating costs, financial condition and results of operations.

Wage rates for many of our employees are slightly above the federal minimum wage. As federal and/or state minimum wage rates increase, we may need to increase not only our employees’ wage rates that are under the new minimum, but also the wages paid to our other hourly employees. Any increase in the cost of our labor could have a material adverse effect on our operating costs, financial condition and results of operations.

Failure to comply with legal requirements could have an adverse effect on our financial condition and results of operations.

Compliance risks in our business include areas such as employment law, taxation, securities laws, consumer protection laws, licensing, customer relations and personal injury claims, among others. If we fail to comply with these laws, rules and regulations, we may be subject to judgments, fines or other costs or penalties, which could have an adverse effect on our financial condition and results of operations.

Changes in government regulations could have an adverse effect on our financial condition and results of operations.

Our business is subject to numerous federal, state and local laws and regulations. New legal requirements in any number of areas could result in higher compliance costs. Changes in areas, such as workplace-regulation and other labor or employment benefits laws, supply chain, privacy and information security, or environmental regulation may require extensive structural and organizational changes that could be difficult to implement, disrupt our business, cause reputational harm and materially adversely affect our operations and financial results.

Any failure of our management information systems or the inability of third parties to continue to upgrade and maintain our systems could have an adverse effect on our business, financial condition and results of operations.

We depend on the accuracy, reliability and proper functioning of our management information systems, including the systems used to track our sales and facilitate inventory management. We also rely on our management information systems for merchandise planning, replenishment and markdowns, as well as other key business functions. These functions enhance our ability to optimize sales while limiting markdowns and reducing inventory risk through properly marking down slow-selling styles, reordering existing styles and effectively distributing new inventory to our stores. We do not currently have redundant systems for all functions performed by our

management information systems. Any interruption in these systems could impair our ability to manage our inventory effectively, which could have an adverse effect on our business.

We depend on third-party suppliers to maintain and periodically upgrade our management information systems. Due to ever-evolving cybersecurity threats, we and our third-party service providers and vendors must continually evaluate and adapt our respective systems and processes and overall security environment. If any of these suppliers is unable to continue to maintain and upgrade these software programs and/or if we are unable to convert to alternate systems in an efficient and timely manner, it could result in an adverse effect on our business.

Failure to maintain the security of employee, customer or vendor information could expose us to litigation, government enforcement actions and materially impact our reputation and business operations.

Over the normal course of business operations, we obtain certain private or confidential information of our employees, customers, and vendors. This information may be stored within our internal information technology environments or hosted by third party service providers. We have implemented security procedures and technology that are intended to safeguard this information from cybersecurity attacks and data breaches. These safeguards include, but are not limited to, routine penetration and vulnerability testing, network segmentation, strong encryption protocols, virus and malware protection, email security scanning, simulation training, vendor assessments, and on-going monitoring and patching activities. There is no guarantee that these measures will be adequate to safeguard against all data security breaches, system compromises or misuses of data.

As we accept debit and credit card payments in our stores, we are subject to the Payment Card Industry’s Data Security Standards (“PCI DSS”) to which we attest compliance annually. For the protection of our customer’s payment information, we utilize chip enabled pin pads with point-to-point encryption technology. In addition, we do not retain the customer’s encrypted, hashed, or tokenized payment information within our internal systems. However, even as we comply with PCI DSS and employ point-to-point encryption technology, we may not be able to prevent or detect a compromise of cardholder data. In addition, as the regulatory environment related to information security, data collection and use, and privacy becomes increasingly rigorous, with new and constantly changing requirements, compliance with those requirements could also result in additional costs.

Cyberattacks continue to evolve and there can be no assurance that an attacker would be unable to gain access to the information we collect. These attacks can come in many forms, including computer hacking, acts of vandalism or theft, malware, computer viruses or other malicious codes, phishing, employee error or malfeasance, catastrophes, unforeseen events or other cyber-attacks. Additionally, a failure of a third party service provider to monitor and secure their environment could lead to unauthorized access of our private or confidential information. A cyberattack or a breach of our data could expose us to costly fines, private litigation and response measures, credit card brand assessments, government enforcement actions, disruption of business operations, negative publicity and decrease our customers’ willingness to shop in our stores which could adversely affect our business and financial conditions.

Our sales, inventory levels and earnings fluctuate on a seasonal basis, which makes our business more susceptible to adverse events that occur during the first and fourth quarters.

Our sales and earnings are significantly higher during the first and fourth quarters each year due to the importance of the spring selling season, which includes Easter, and the fall selling season, which includes Christmas. Factors negatively affecting us during the first and fourth quarters, including adverse weather, unfavorable economic conditions, reduced governmental assistance, and tax refund patterns for our customers, will have a greater adverse effect on our financial condition than if our business was less seasonal.

Seasonal fluctuations also affect our inventory levels. In order to prepare for the spring and fall selling seasons, we must order and keep in stock significantly more merchandise than during other parts of the year. Merchandise must be ordered well in advance of the applicable selling season and before trends are confirmed by sales. If we are not able to accurately predict customers’ preferences for our fashion items, we may have too much inventory which may result in increased markdowns. If we are unable to accurately predict demand for our merchandise during these periods, we could also end up with inventory shortages resulting in missed sales. In either event, our sales may be lower and our cost of sales may be higher than historical levels, which could have a material adverse effect on our business, financial condition and results of operations.

If we fail to successfully implement our various marketing efforts or if our competitors are more effective with their programs than we are, our revenue or results of operations may be adversely affected.

Customer traffic and demand for our merchandise may be influenced by our marketing efforts. Although we use marketing to drive customer traffic through various media including radio, print, digital/social media and e-mail, some of our competitors expend more for

their marketing programs than we do, or use different approaches than we do, which may provide them with a competitive advantage. Further, we may not effectively implement strategies with respect to rapidly evolving Internet-based and other digital or mobile communication channels, including social media. Our programs may not be or remain effective or could require increased expenditures, which could have a significant adverse effect on our revenue and results of operations.

We experience fluctuations and variability in our comparable store sales and quarterly results of operations and, as a result, the market price of our common stock may fluctuate substantially.

Our comparable store sales and quarterly results have fluctuated significantly in the past based on a number of economic, seasonal and competitive factors, and we expect them to continue to fluctuate in the future. Since the beginning of fiscal 2014, our quarter-to-quarter comparable store sales have ranged from a decrease of 5.0% to an increase of 13.9%. This variability could cause our comparable store sales and quarterly results to fall below the expectations of securities analysts or investors, which could result in a decline in the market price of our common stock.

Our stock price is subject to volatility.

Our stock price has been volatile in the past and may be influenced in the future by a number of factors, including:

| · | | actual or anticipated fluctuations in our operating results; |

| · | | changes in securities analysts’ recommendations or estimates of our financial performance; |

| · | | changes in market valuations or operating performance of our competitors or companies similar to ours; |

| · | | announcements by us, our competitors or other retailers; |

| · | | additions and departures of key personnel; |

| · | | changes in accounting principles; |

| · | | the passage of legislation or other developments affecting us; |

| · | | the trading volume of our common stock in the public market; |

| · | | changes in economic or financial market conditions; |

| · | | natural disasters, terrorist acts, acts of war or periods of civil unrest; and |

| · | | the realization of some or all of the risks described in this section entitled “Risk Factors.” |

In addition, the stock markets have experienced significant price and trading volume fluctuations from time to time, and the market prices of the equity securities of retailers have been extremely volatile and have recently experienced sharp price and trading volume changes. These broad market fluctuations may adversely affect the market price of our common stock.

We cannot provide any guaranty of future cash dividend payments or that we will continue to actively repurchase our common stock pursuant to a share repurchase program.

Any determination to declare and pay cash dividends on our common stock in the future (quarterly or otherwise) will be based, among other things, upon our financial condition, results of operations, business and cash requirements and our board of directors’ conclusion in each instance that the declaration and payment of a cash dividend is in the best interest of our stockholders and is in compliance with all laws and agreements applicable to the dividend. In addition, there can be no assurance that our existing share repurchase authorization will be completed or that our board of directors will approve another repurchase program in the future.

Provisions in our certificate of incorporation and by-laws and Delaware law may delay or prevent our acquisition by a third party.

Our third amended and restated certificate of incorporation and our third amended and restated by-laws contain several provisions that may make it more difficult for a third party to acquire control of us without the approval of our board of directors. These provisions include, among other things, advance notice for raising business or making nominations at stockholder meetings and “blank check” preferred stock. Blank check preferred stock enables our board of directors, without stockholder approval, to designate and issue additional series of preferred stock with such dividend, liquidation, conversion, voting or other rights, including convertible securities with no limitations on conversion, as our board of directors may determine, including rights to dividends and proceeds in a liquidation that are senior to the common stock. Additionally, we are in the process of phasing out our classified board of directors, so only three directors will be up for election at the next annual meeting.

We are also subject to several provisions of the Delaware General Corporation Law that could delay, prevent or deter a merger, acquisition, tender offer, proxy contest or other transaction that might otherwise result in our stockholders receiving a premium over the market price for their common stock or may otherwise be in the best interests of our stockholders.

ITEM 1B.UNRESOLVED STAFF COMMENTS

None.

ITEM 2.PROPERTIES

Store Locations

As of February 2, 2019, we operated 562 stores located in 32 states. Our stores average approximately 11,000 square feet of selling space and are typically located in neighborhood strip shopping centers that are convenient to low and moderate income customers.

We have no franchising relationships, and all of the stores are company operated. All existing 562 stores, totaling 7.5 million total square feet and 6.2 million selling square feet, are leased under operating leases. The typical store lease is for five years with options to extend the lease term for three additional five-year periods. Nearly all store leases provide us the right to cancel following an initial three-year period in the event the store does not meet pre-determined sales levels. The table below sets forth the number of stores in each of the 32 states in which we operated as of February 2, 2019:

Alabama—31

Arkansas—13

California—9

Connecticut—4

Delaware—2

Florida—52

Georgia—64

Illinois—20

Indiana—17

Iowa—2

Kansas—1

Kentucky—6

Louisiana—35

Maryland—5

Massachusetts—2

Michigan—23

Minnesota—2

Mississippi—26

Missouri—7

Nebraska—1

Nevada—2

New York—9

North Carolina—48

Ohio—28

Oklahoma—7

Pennsylvania—7

Rhode Island—2

South Carolina—44

Tennessee—17

Texas—49

Virginia—21

Wisconsin—6

Support Center Facilities

We own a facility in Savannah, Georgia totaling approximately 70,000 square feet, which serves as our headquarters and, to a lesser extent, as a storage facility. We also own an approximately 550,000 square-foot distribution center in Darlington, South Carolina and a 565,000 square-foot distribution center in Roland, Oklahoma. In addition, we currently lease an 11,500 square-foot office in New York City and an 1,800 square-foot office in Los Angeles which are used for buyer operations and meetings with vendors.

ITEM 3.LEGAL PROCEEDINGS

We are from time to time involved in various legal proceedings incidental to the conduct of our business, including claims by customers, employees or former employees. Once it becomes probable that we will incur costs in connection with a legal proceeding and such costs can be reasonably estimated, we establish appropriate reserves. While legal proceedings are subject to uncertainties and the outcome of any such matter is not predictable, we are not aware of any legal proceedings pending or threatened against us that we expect to have a material adverse effect on our financial condition, results of operations or liquidity.

ITEM 4.MINE SAFETY DISCLOSURES

Not applicable.

PART II

ITEM 5. MARKET FOR THE REGISTRANT’S COMMON EQUITY, RELATED STOCKHOLDER MATTERS AND ISSUER PURCHASES OF EQUITY SECURITIES

Our common stock is traded on The NASDAQ Stock Market under the symbol “CTRN.” On April 2, 2019, there were 38 holders of record and approximately 2,500 beneficial holders of our common stock.

In 2018, we paid a quarterly dividend of $0.08 per common share on March 20, 2018, June 19, 2018, September 18, 2018 and December 26, 2018.

On February 12, 2019, the Company’s Board of Directors declared a quarterly dividend of $0.08 per common share, which was paid on March 19, 2019 to stockholders of record as of March 5, 2019. We currently anticipate continuing our $0.08 quarterly dividend. However, any determination to declare and pay cash dividends on our common stock in the future (quarterly or otherwise) will be based, among other things, upon our financial condition, results of operations, business and cash requirements and our board of directors’ conclusion in each instance that the declaration and payment of a cash dividend is in the best interest of our stockholders and is in compliance with all laws and agreements applicable to the dividend.

Recent Sales of Unregistered Securities.

None.

Purchases of Equity Securities by the Issuer and Affiliated Purchasers.

The number of shares of common stock that we repurchased during the fourth quarter of fiscal 2018 and the average price paid per share are as follows:

| | | | | | | | | | | |

| | | | | | | Total number of | | Maximum number (or | |

| | | | | | | shares purchased as | | approximate dollar value) | |

| | | | | | | part of publicly | | of shares that may yet be | |

| | Total number of | | Average price | | announced plans or | | purchased under the plans | |

Period | | shares purchased | | paid per share (1) | | programs (2) | | or programs (2) | |

November (11/4/18 - 12/1/18) | | — | | $ | — | | — | | $ | 25,000,000 | |

December (12/2/18 - 1/5/19) | | 547,464 | | | 19.65 | | 547,464 | | | 14,256,141 | |

January (1/6/19 - 2/2/19) | | 221,094 | | | 20.86 | | 221,094 | | | 9,649,697 | |

Total | | 768,558 | | | | | 768,558 | | | | |

(1) Includes commissions for the shares repurchased under the stock repurchase program.

(2) On November 28, 2018, the Company’s Board of Directors approved a $25.0 million stock repurchase program, under which approximately $9.6 million of shares remained available as of February 2, 2019. Repurchases under the stock repurchase program could be made at management’s discretion from time to time on the open market, in privately negotiated transactions or otherwise, and could be made in part under one or more Rule 10b5-1 plans. The stock repurchase program does not have an expiration date.

Equity Compensation Plan Information.

See Item 12 of this Report.

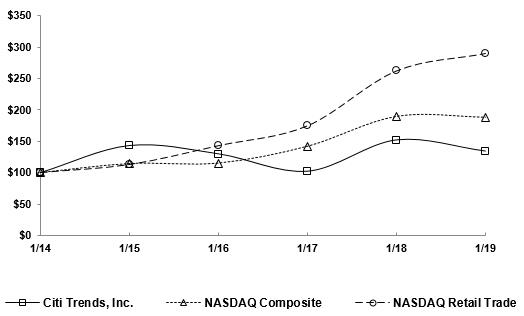

Stock Performance Graph

Set forth below is a line graph comparing the last five years’ percentage change in the cumulative total stockholder return on shares of our common stock against (i) the cumulative total return of companies listed on The NASDAQ Stock Market and (ii) the cumulative total return of the NASDAQ Retail Trade Index. This graph assumes that $100 was invested on January 31, 2014 in our common stock and in each of the market index and the industry index, and that all cash distributions were reinvested. Our common stock price performance shown on the graph is not indicative of future price performance.

COMPARISON OF 5 YEAR CUMULATIVE TOTAL RETURN*

Among Citi Trends, Inc., the NASDAQ Composite Index and the NASDAQ Retail Trade Index

*$100 invested on 1/31/14 in stock or index, including reinvestment of dividends.

Fiscal year ending on or about January 31.

| | | | | | | | | | | | | |

Total Return Analysis | | 1/14 | | 1/15 | | 1/16 | | 1/17 | | 1/18 | | 1/19 | |

| | | | | | | | | | | | | |

Citi Trends, Inc. | | 100.00 | | 143.06 | | 129.80 | | 102.19 | | 152.00 | | 134.20 | |

NASDAQ Composite | | 100.00 | | 114.30 | | 115.10 | | 141.84 | | 189.26 | | 187.97 | |

NASDAQ Retail Trade | | 100.00 | | 112.78 | | 142.83 | | 174.47 | | 261.97 | | 289.77 | |

ITEM 6.SELECTED FINANCIAL DATA

Selected Financial and Operating Data