Table of Contents

Filed Pursuant to Rule 424(b)(3)

Registration No. 333-191270

PROSPECTUS

NCL CORPORATION LTD.

OFFER TO EXCHANGE

$300,000,000 aggregate principal amount of NCL Corporation Ltd.’s 5.00% Senior Notes Due 2018, which have been registered under the Securities Act of 1933 (CUSIP No. 62886H AK7) for $300,000,000 aggregate principal amount of NCL Corporation Ltd.’s outstanding 5.00% Senior Notes Due 2018 (CUSIP Nos. 62886H AJ0 and G6436Q AD8).

We hereby offer, upon the terms and subject to the conditions set forth in this prospectus and the accompanying letter of transmittal (which together constitute the “exchange offer”), to exchange up to $300,000,000 aggregate principal amount of our registered 5.00% Senior Notes Due 2018, which we refer to as the “Exchange Notes”, for a like principal amount of our outstanding 5.00% Senior Notes Due 2018, which we refer to as the “Old Notes”. We refer to the Old Notes and the Exchange Notes collectively as the “Notes”. The terms of the Exchange Notes are identical to the terms of the Old Notes in all material respects, except for the elimination of certain transfer restrictions, registration rights and additional interest provisions relating to the Old Notes. The issuer of the Notes is NCL Corporation Ltd.

We will exchange any and all Old Notes that are validly tendered and not validly withdrawn prior to 5:00 p.m., New York City time, on November 7, 2013, unless extended.

We have not applied, and do not intend to apply, for listing of the Notes on any national securities exchange or automated quotation system.

Each broker-dealer that receives Exchange Notes for its own account pursuant to the exchange offer must acknowledge that it (i) has not entered into any arrangement or understanding with the Issuer (as defined below) or an affiliate of the Issuer to distribute such Exchange Notes and (ii) will deliver a prospectus in connection with any resale of such Exchange Notes. The letter of transmittal states that by so acknowledging and delivering a prospectus, a broker-dealer will not be deemed to admit that it is an “underwriter” within the meaning of the Securities Act of 1933, as amended, or the Securities Act. This prospectus, as it may be amended or supplemented from time to time, may be used by a broker-dealer in connection with resales of Exchange Notes received in exchange for Old Notes where such Old Notes were acquired by such broker-dealer as a result of market-making activities or other trading activities. We have agreed that, for a period of 180 days after the consummation of the exchange offer, we will make this prospectus available to any broker-dealer for use in connection with any such resale. See “Plan of Distribution.”

See “Risk Factors” beginning on page 20 of this prospectus for a discussion of certain risks that you should consider before participating in this exchange offer.

Neither the Securities and Exchange Commission nor any state securities commission has approved or disapproved of these securities or passed upon the adequacy or accuracy of this prospectus. Any representation to the contrary is a criminal offense.

The date of this prospectus is October 9, 2013.

Table of Contents

| ii | ||||

| v | ||||

| 1 | ||||

| 20 | ||||

| 33 | ||||

| 35 | ||||

| 44 | ||||

| 45 | ||||

| 46 | ||||

MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS | 48 | |||

| 59 | ||||

| 82 | ||||

| 88 | ||||

| 106 | ||||

SECURITY OWNERSHIP OF CERTAIN BENEFICIAL OWNERS AND MANAGEMENT | 107 | |||

| 112 | ||||

| 117 | ||||

| 124 | ||||

| 176 | ||||

| 179 | ||||

| 180 | ||||

| 182 | ||||

| 184 | ||||

| 185 | ||||

| 186 | ||||

| 187 | ||||

| 189 | ||||

| 190 | ||||

| F-1 |

We have not authorized anyone to give you any information or to make any representations about us or the transactions we discuss in this prospectus other than those contained in this prospectus. If you are given any information or representations about these matters that is not discussed in this prospectus, you must not rely on that information. This prospectus is not an offer to sell or a solicitation of an offer to buy securities anywhere or to anyone where or to whom we are not permitted to offer or sell securities under applicable law. The delivery of this prospectus does not, under any circumstances, mean that there has not been a change in our affairs since the date of this prospectus. Subject to our obligation to amend or supplement this prospectus as required by law and the rules of the Securities and Exchange Commission, or the SEC, the information contained in this prospectus is correct only as of the date of this prospectus, regardless of the time of delivery of this prospectus or any sale of these securities.

Until January 7, 2014, broker-dealers that effect transactions in these securities, whether or not participating in this offering, may be required to deliver a prospectus. This is in addition to the broker-dealers’ obligation to deliver a prospectus when acting as underwriters and with respect to their unsold allotments or subscriptions.

Table of Contents

Unless otherwise indicated or the context otherwise requires, references in this prospectus to (i) the “Company,” the “Issuer,” “we,” “our,” “us” and “NCLC” refer to NCL Corporation Ltd. and its subsidiaries and predecessors, (ii) “NCLH” refers to Norwegian Cruise Line Holdings Ltd. and/or its subsidiaries (iii) “Norwegian Cruise Line” or “Norwegian” refers to the Norwegian Cruise Line brand and its predecessors and “NCL America” or “NCLA” refers to our U.S.-flagged operations, (iv) “Apollo” refers to Apollo Global Management, LLC and its subsidiaries and the “Apollo Funds” refers to one or more of AIF VI NCL (AIV), L.P., AIF VI NCL (AIV II), L.P., AIF VI NCL (AIV III), L.P., AIF VI NCL (AIV IV), L.P., AAA Guarantor – Co-Invest VI (B), L.P., Apollo Overseas Partners (Delaware) VI, L.P., Apollo Overseas Partners (Delaware 892) VI, L.P., Apollo Overseas Partners VI, L.P. and Apollo Overseas Partners (Germany) VI, L.P., (v) “TPG Global” refers to TPG Global, LLC, “TPG” refers to TPG Global and its affiliates and the “TPG Viking Funds” refers to one or more of TPG Viking, L.P., TPG Viking AIV I, L.P., TPG Viking AIV II, L.P., and TPG Viking AIV III, L.P. and/or certain other affiliated investment funds, each an affiliate of TPG, (vi) “Genting HK” refers to Genting Hong Kong Limited and/or its affiliates (formerly Star Cruises Limited and/or its affiliates), and (vii) “Affiliate(s)” or “Sponsor(s)” refers to Genting HK, the Apollo Funds and/or the TPG Viking Funds. References to the “U.S.” are to the United States of America, “dollars” or “$” are to U.S. dollars and “euros” or “€” are to the official currency of the Eurozone. For a reconciliation of our non-GAAP financial measures we refer you to “Management’s Discussion and Analysis of Financial Condition and Results of Operations—Results of Operations” and “Prospectus Summary—Summary Consolidated Financial Data.” Unless otherwise indicated in this prospectus, the following terms have the meanings set forth below (all principal amounts refer to the original principal amount incurred or issued, as applicable):

| • | $1.3 billion Senior Secured Credit Facility. $1.3 billion credit agreement, dated May 24, 2013, by and among NCL Corporation Ltd., as borrower, Deutsche Bank Trust Company Americas, as administrative agent and as collateral agent, and various lenders, and related guarantee by Norwegian Dawn Limited, Norwegian Gem, Ltd., Norwegian Pearl, Ltd., Norwegian Spirit, Ltd., Norwegian Star Limited and Norwegian Sun Limited, providing for a $675 million term loan facility and a $625 million revolving credit facility. |

| • | $334.1 million Norwegian Jewel loan. $334.1 million secured loan agreement, dated as of April 20, 2004, as amended and restated on June 21, 2013, by and among Norwegian Jewel Limited, as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | Adjusted EBITDA. EBITDA adjusted for other income (expense) and other supplemental adjustments. |

| • | Adjusted EBITDA Margin. Adjusted EBITDA as a percentage of total revenue. |

| • | Adjusted Net Cruise Cost Excluding Fuel. Net Cruise Cost less fuel expense adjusted for supplemental adjustments. |

| • | Adjusted Net Income. Net income adjusted for supplemental adjustments. |

| • | Berths. Double occupancy capacity per cabin (single occupancy per studio cabin) even though many cabins can accommodate three or more passengers. |

| • | Breakaway Class Ships. Norwegian Breakaway delivered in April 2013 and Norwegian Getaway scheduled for delivery in January 2014. |

| • | Breakaway Export Credit Facility. €529.8 million credit agreement, dated November 18, 2010, as amended, by and among Breakaway One, Ltd., as borrower, and a syndicate of international banks and a related guarantee by NCL Corporation Ltd. |

| • | Breakaway/Getaway Credit Facilities. Our Breakaway Export Credit Facility, Getaway Export Credit Facility and Breakaway/Getaway Term Loan Facilities. |

| • | Breakaway/Getaway Term Loan Facilities. €126.1 million Pride of Hawai’i Credit Agreement, dated November 18, 2010, as amended and restated on June 21, 2013, by and among Pride of Hawaii LLC and a syndicate of international banks and a related guarantee by NCL Corporation Ltd. and €126.1 million Norwegian Jewel Credit Agreement, dated November 18, 2010, as amended and restated on June 21, 2013, by and among Norwegian Jewel Limited and a syndicate of international banks and a related guarantee by NCL Corporation Ltd. |

ii

Table of Contents

| • | Breakaway Plus Class Ships. Two ships on order with Meyer Werft for delivery in the fourth quarter of 2015 and the first quarter of 2017, respectively, which will be approximately 163,000 Gross Tons and 4,200 Berths each and will be similar in design and innovation to our Breakaway Class Ships. |

| • | Breakaway Plus Newbuild Export Credit Facilities. €590.5 million credit agreement, dated October 12, 2012, by and among Breakaway Three, Ltd. and KfW IPEX-Bank GmBH and a related guarantee by NCL Corporation Ltd. and €590.5 million credit agreement, dated October 12, 2012, by and among Breakaway Four, Ltd. and KfW IPEX-Bank GmBH and a related guarantee by NCL Corporation Ltd. |

| • | Capacity Days. Available Berths multiplied by the number of cruise days for the period. |

| • | Charter. The hire of a ship for a specified period of time. |

| • | CLIA. Cruise Lines International Association, a non-profit marketing and training organization formed in 1975 to promote cruising. |

| • | Constant Currency. A calculation whereby foreign currency-denominated revenue and expenses in a period are converted at the U.S. dollar exchange rate of a comparable period in order to eliminate the effects of the foreign exchange fluctuations. |

| • | Dry-dock. A process whereby a ship is positioned in a large basin where all the fresh/sea water is pumped out in order to carry out cleaning and repairs of those parts of a ship which are below the water line. |

| • | EBITDA. Earnings before interest, taxes and depreciation and amortization. |

| • | €258.0 million Pride of America loan. Euro 258.0 million secured loan agreement, dated as of April 4, 2003, as amended and restated on June 21, 2013, by and among Pride of America Ship Holding, LLC, as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | €308.1 million Pride of Hawai’i loan. Euro 308.1 million Pride of Hawai’i loan, dated as of April 20, 2004, as amended and restated on June 21, 2013, by and among Pride of Hawaii, LLC, as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | €662.9 million Norwegian Epic loan. Euro 662.9 million syndicated loan facility, dated September 22, 2006, as amended and restated on June 1, 2012, by and among Norwegian Epic, Ltd., as borrower, and a syndicate of international banks, and related guarantee by NCL Corporation Ltd. |

| • | Existing Senior Secured Credit Facilities. Our $1.3 billion Senior Secured Credit Facility, our Breakaway Plus Newbuild Export Credit Facilities, our Breakaway/Getaway Credit Facilities, our €308.1 million Pride of Hawai’i loan, our $334.1 million Norwegian Jewel loan, our €258.0 million Pride of America loan and our €662.9 million Norwegian Epic loan. |

| • | GAAP. Generally accepted accounting principles in the U.S. |

| • | Getaway Export Credit Facility. €529.8 million Breakaway Two Credit Agreement, dated as of November 18, 2010, as amended, by and among Breakaway Two, Ltd., as borrower, and a syndicate of international banks and a related guarantee by NCL Corporation Ltd. |

| • | Gross Cruise Cost. The sum of total cruise operating expense and marketing, general and administrative expense. |

| • | Gross Tons. A unit of enclosed passenger space on a cruise ship, such that one gross ton = 100 cubic feet or 2.831 cubic meters. |

| • | Gross Yield. Total revenue per Capacity Day. |

| • | IMO. International Maritime Organization, a United Nations agency that sets international standards for shipping. |

iii

Table of Contents

| • | IPO. The initial public offering of 27,058,824 ordinary shares, par value $.001 per share, of NCLH, which was consummated on January 24, 2013. |

| • | Jewel Class Ships. Norwegian Gem, Norwegian Jade, Norwegian Jewel and Norwegian Pearl. |

| • | Major North American Cruise Brands. Norwegian Cruise Line, Carnival Cruise Lines, Royal Caribbean International, Holland America, Princess Cruises and Celebrity Cruises. |

| • | Management NCL Corporation Units. NCLC’s previously outstanding profits interests issued to management (or former management) of NCLC which have been converted into units in NCLC in connection with the Corporate Reorganization. |

| • | Net Cruise Cost. Gross Cruise Cost less commissions, transportation and other expense and onboard and other expense. |

| • | Net Cruise Cost Excluding Fuel. Net Cruise Cost less fuel expense. |

| • | Net Revenue. Total revenue less commissions, transportation and other expense and onboard and other expense. |

| • | Net Yield. Net Revenue per Capacity Day. |

| • | Norwegian Sky Agreement. Memorandum of agreement, dated June 1, 2012, between Ample Avenue Limited, as seller, and Norwegian Sky, Ltd., as buyer, related to our purchase of Norwegian Sky. |

| • | Occupancy Percentage or Load Factor. The ratio of Passenger Cruise Days to Capacity Days. A percentage in excess of 100% indicates that three or more passengers occupied some cabins. |

| • | Passenger Cruise Days. The number of passengers carried for the period, multiplied by the number of days in their respective cruises. |

| • | SEC. U.S. Securities and Exchange Commission. |

| • | Ship Contribution. Total revenue less total cruise operating expense. |

| • | Shipboard Retirement Plan. An unfunded defined benefit pension plan for certain crew members which computes benefits based on years of service, subject to certain requirements. |

iv

Table of Contents

MARKET AND INDUSTRY DATA AND FORECASTS

This prospectus includes market share and industry data and forecasts that we obtained from industry publications, third-party surveys and internal company surveys. Industry publications, including those from CLIA (as defined below), and surveys and forecasts generally state that the information contained therein has been obtained from sources believed to be reliable. All CLIA information, obtained from the CLIA website “cruising.org,” relates to CLIA member lines, which currently represents 26 of the major North American cruise lines including Norwegian, which together represent 97% of the North American cruise capacity. All other references to third party information are publicly available at nominal or no cost. We use the most currently available industry and market data to support statements as to our market position.

Although we believe that the industry publications and third-party sources are reliable, we have not independently verified any of the data from industry publications or third-party sources. Similarly, while we believe our internal estimates with respect to our industry are reliable, our estimates have not been verified by any independent sources. While we are not aware of any misstatements regarding any industry data presented herein, our estimates, in particular as they relate to market share and our general expectations, involve risks and uncertainties and are subject to change based on various factors, including those discussed under “Risk Factors,” “Cautionary Statement Concerning Forward-Looking Statements” and “Management’s Discussion and Analysis of Financial Condition and Results of Operations” in this prospectus.

v

Table of Contents

The following summary includes highlights of the more detailed information and consolidated financial statements included elsewhere in this prospectus. This summary sets forth the material terms of the offering but does not contain all of the information that you should consider before investing in the Notes. For a more complete understanding of us, our business and the Notes, we urge you to read this prospectus carefully, including the sections entitled “Risk Factors,” “Cautionary Statement Concerning Forward-Looking Statements” and “Additional Information” and our consolidated financial statements and related notes included elsewhere in this prospectus, before making an investment.

Our Company

We are a leading global cruise line operator, offering cruise experiences for travelers with a wide variety of itineraries in North America (including Alaska and Hawaii), the Mediterranean, the Baltic, Central America, Bermuda and the Caribbean. We strive to offer an innovative and differentiated cruise vacation with the goal of providing our guests the highest levels of overall satisfaction on their cruise experience. In turn, we aim to generate the highest guest loyalty and greatest numbers of repeat guests. We created a distinctive style of cruising called “Freestyle Cruising” onboard all of our ships, which we believe provides our guests with the freedom and flexibility associated with a resort style atmosphere and experience as well as more dining options than a traditional cruise. We established the very first private island developed by a cruise line in the Bahamas with a diverse offering of activities for guests. We are also the only cruise line operator to offer an entirely inter-island itinerary in Hawaii.

By providing such a distinctive experience and appealing combination of value and service, we straddle both the contemporary and premium segments. As a result, we have been recognized for our achievements as the recipient of multiple honorary awards mainly consisting of reviews tabulated from the readers of travel periodicals such as Travel Weekly, Condé Nast Traveler, and Travel + Leisure. We were rated as the favorite cruise line by Budget Travel, and best for family cruises by Family Circle, Yahoo! Travel, and Today Travel. In addition, we were recognized as Europe’s leading cruise line six years in a row by the World Travel Awards and identified as the cruise line with the best use of a social media platform by Travel + Leisure. Norwegian Epic, which was launched in 2010, was recognized as “Best Overall Individual Cruise Ship” by the Travel Weekly Readers’ Choice Awards two years in a row.

We offer a wide variety of cruises ranging in length from one day to three weeks. During 2012, we docked at 114 ports worldwide, with itineraries originating from 15 ports of which 11 are in North America. In line with our strategy of innovation, many of these North American ports are part of our “Homeland Cruising” program in which we have homeports that are close to major population centers, such as New York, Boston and Miami. This reduces the need for vacationers to fly to distant ports to embark on a cruise and helps reduce our guests’ overall vacation cost. We offer a wide selection of exotic itineraries outside of the traditional cruising markets of the Caribbean and Mexico; these include cruises in Europe, including the Mediterranean and the Baltic, Bermuda, Alaska, and the industry’s only entirely inter-island itinerary in Hawaii with our U.S.-flagged ship, Pride of America. This itinerary is unparalleled in the cruise industry, as all other vessels from competing cruise lines are registered outside the U.S. and are required to dock at a distant foreign port when providing their guests with a Hawaii-based cruise itinerary.

Each of our 12 modern ships has been purpose-built to consistently deliver our “Freestyle Cruising” product offering across our entire fleet, which we believe provides us with a competitive advantage. By focusing on “Freestyle Cruising,” we have been able to achieve higher onboard spend levels, greater customer loyalty and the ability to attract a more diverse clientele.

As a result of our strong operating performance over the last four years, the growing demand we see for our distinctive cruise offering and the rational supply outlook for the industry, we believe that it is an optimal time to add new ships to our fleet. In 2010, we launched a newbuild program for the next generation of Freestyle Cruising vessels. We placed an order with Meyer Werft GmbH of Papenburg, Germany (“Meyer Werft”) for two new cruise ships: Norwegian Breakaway, which was delivered in April 2013 and Norwegian Getaway, which is scheduled for delivery in January 2014. This ship will be approximately 144,000 Gross Tons with 4,000 Berths at an aggregate cost of approximately €625.9 million, or $814.3 million based on the euro/U.S. dollar exchange rate as of June 30, 2013. We have also ordered two additional cruise ships from Meyer Werft for delivery in the fourth quarter of 2015 and the first quarter of 2017, respectively. These new Breakaway Plus Class Ships will be the largest in our fleet at approximately 163,000 Gross Tons and 4,200 Berths each and will be similar in design and innovation to our Breakaway Class Ships. The combined contract cost of the two Breakaway Plus Class Ships is approximately €1.4 billion, or $1.8 billion based on the euro/U.S. dollar exchange rate as of June 30, 2013. We have export credit financing in place for these ships that provides financing for 80% of their contract price.

1

Table of Contents

As of June 30, 2013, we have one of the most modern fleets of cruise ships in the industry among the Major North American Cruise Brands, with a weighted-average age of 7.5 years. Following the delivery of Norwegian Getaway, we will have the youngest fleet among the Major North American Cruise Brands. Norwegian Getaway joins Norwegian Breakaway as the latest generation of “Freestyle Cruising” ships and includes some of the most popular elements of our recently delivered ships together with new and differentiated features.

Our senior management team has delivered consistent growth and has driven measurable improvements in operating metrics and cash flow generation across several different operating environments. Under the leadership of our President and Chief Executive Officer, Kevin M. Sheehan, we significantly differentiated the Norwegian brand, largely with the “Freestyle Cruising” concept that accelerated revenue growth and contributed to improving our operating income margins by approximately 1,370 basis points since the beginning of 2008 through the end of 2012. Our management team was augmented in key areas such as Sales, Marketing, Hotel Operations and Finance and has since implemented major initiatives such as enhancing onboard service and amenities across the fleet, expanding our European presence and overseeing a newbuild program that included the successful launch in April 2013 of our most innovative ship to date, Norwegian Breakaway.

For the twelve months ended June 30, 2013, we generated total revenue of $2,349.6 million, Net Revenue of $1,748.5 million, net income of $27.7 million, Adjusted EBITDA of $580.3 million and an Adjusted EBITDA Margin of 24.7%. For the six months ended June 30, 2013, we generated total revenue of $1,172.1 million, Net Revenue of $872.8 million, net loss of $101.5 million, Adjusted EBITDA of $253.3 million and an Adjusted EBITDA Margin of 21.6%. For the six months ended June 30, 2012, we generated total revenue of $1,098.7 million, Net Revenue of $816.1 million, net income of $39.3 million, Adjusted EBITDA of $228.6 million and an Adjusted EBITDA Margin of 20.8%. This represents an increase of approximately 80 basis points in period over period Adjusted EBITDA Margin as a result of improved ticket pricing and onboard spending coupled with various business improvement, product enhancement and cost reduction initiatives. We refer you to note 5 under “Prospectus Summary—Summary Consolidated Financial Data” included elsewhere in this prospectus for a reconciliation of Adjusted EBITDA to net income.

Our Industry

We believe that the cruise industry demonstrates the following positive fundamentals:

Strong Growth with Low Penetration and Significant Upside

Cruising is a vacation alternative with broad appeal, as it offers a wide range of products and services to suit the preferences of vacationing guests of all ages, backgrounds and interests. Since 1980, cruising has been one of the fastest growing segments of the North American vacation market. According to CLIA, in 2012 approximately 17.2 million passengers took cruises on CLIA member lines versus 7.2 million passengers in 2000, representing a compound annual growth rate of approximately 7.5%. Based on CLIA’s research, we believe that cruising is under-penetrated and represents approximately 12% of the North American vacation market. As measured in Berths, the cruise industry is relatively nascent compared to the wide variety of much more established vacation travel destinations across North America.

According to the Orlando/Orange County Convention & Visitors Bureau and the Las Vegas Convention and Visitors Authority, there are approximately 267,000 rooms in just Orlando and Las Vegas combined. By comparison, the estimated Major North American Cruise Brands’ capacity in terms of Berths is approximately 241,000. In addition, according to industry research, only 24% of the U.S. population has ever taken a cruise and we believe this percentage should increase. The European vacation market, the fastest growing market globally, remains under-penetrated by the cruise industry, with approximately 1% of Europeans having taken a cruise in a given year, compared with 3% of the population in the U.S. and Canada. We believe that improving leisure travel trends along with a relatively low supply outlook in the near term from the Major North American Cruise Brands lead to an attractive business environment for our Company to operate in.

Attractive Demographic Trends to Drive Cruising Growth

The cruise market is comprised of a broad spectrum of guests and appeals to virtually all demographic categories. Based on CLIA’s 2011 Cruise Market Profile Study, the target North American cruise market, defined as households with income of $40,000 or more headed by a person who is at least 25 years old, is estimated to be 132.9

2

Table of Contents

million people. Also according to the study, the average cruise customer has a household income of $109,000. It is our belief that “Freestyle Cruising” will help us attract the younger generations who we believe are more likely to enjoy greater levels of freedom from our “Freestyle Cruising” product offering than was traditionally offered within the cruise industry.

Significant Value Proposition and High Level of Guest Satisfaction

We believe that the cost of a cruise vacation, relative to a comparable land-based resort or hotel vacation in Orlando or Las Vegas, offers an exceptional value proposition. When one considers that a typical cruise, for an all-inclusive price, offers its guests transportation to a variety of destinations, hotel-style accommodations, a generous diversity of food choices and a selection of daily entertainment options, this is compelling support for the cruise value proposition relative to other leisure alternatives. Cruises have become even more affordable for a greater number of North American guests over the past few years through the introduction of “Homeland Cruising,” which eliminates the cost of airfare commonly associated with a vacation. According to CLIA’s 2011 study, approximately 70% of persons who have taken a cruise rate cruising as a high-value vacation alternative. In this same survey, CLIA reported that approximately 80% of cruise passengers agree that a cruise vacation is a good way to sample various destinations that they may visit again on a land-based vacation.

High Barriers to Entry

The cruise industry is characterized by high barriers to entry, including the existence of several established and recognizable brands, the large investment to build a new, sophisticated cruise ship, the long lead time necessary to construct new ships and limited newbuild shipyard capacity. Based on new ship orders announced over the past several years, the cost to build a cruise ship can range from approximately $500 million to $1.4 billion or approximately $200,000 to $425,000 per Berth, depending on the ship’s size and quality of product offering. The construction time of a newbuild ship is typically between 27 and 36 months and requires significant upfront cash payments to fund construction costs before revenue is generated. In addition, the shipbuilding industry is experiencing tightened capacity as the size of ships increases and the industry consolidates, with virtually all new capacity added in the last 20 years having been built by one of three major European shipbuilders.

Varied Segments and Brands

The different cruise lines that make up the global cruise vacation industry have historically been segmented by product offering and service quality into “contemporary,” “premium” and “luxury” brands. The contemporary segment generally includes cruises on larger ships that last seven days or less, provides a casual ambiance and is less expensive on average than the premium or luxury segments. The premium segment is generally characterized by cruises that last from seven to 14 nights with a higher quality product offering than the contemporary segment, appealing to a more affluent demographic. The luxury segment generally offers the highest level of service and quality, with longer cruises on the smallest ships. In classifying our competitors within the Major North American Cruise Brands, the contemporary segment has historically included Carnival Cruise Lines and Royal Caribbean International. The premium segment has historically included Celebrity Cruises, Holland America and Princess Cruises. We believe that we straddle the contemporary and premium segments as well as offer a unique combination of value and leisure services to cruise guests. Our brand offers our guests a rich stateroom mix, which includes single studios, private balconies, and luxury suites with personal butler and concierge service as more recently enhanced by The Haven. As part of our “Freestyle Cruising” experience, we also offer various specialty dining venues, some of which are exclusive to our suite and The Haven guests. Based on fleet counts as of June 30, 2013, the Major North American Cruise Brands together represent approximately 90% of the North American cruise market as measured by total Berths.

Our Competitive Strengths

We believe that the following business strengths will enable us to execute our strategy:

Leading Cruise Operator with High-Quality Product Offering

We believe that our modern fleet provides us with operational and strategic advantages as our entire fleet has been purpose-built for “Freestyle Cruising” with a wider range of passenger amenities relative to many of our competitors.

We believe that in recent years the distinction has been blurred between segments of the market historically known as premium and contemporary, with the Major North American Cruise Brands each offering a wide range of

3

Table of Contents

onboard experiences across their respective fleets. With the completion of our fleet renewal initiative, we believe that based on a number of different metrics that directly impact a guest’s onboard experience, we compare favorably against the other Major North American Cruise Brands, with many product attributes that are more in line with the premium segment.

| • | Modern Fleet. With a weighted-average age of 7.5 years as of June 30, 2013 and no ships built before 1998, we have one of the most modern fleets among the Major North American Cruise Brands, which we believe allows us to offer a high-quality passenger experience with a significant level of consistency across our entire fleet. |

| • | Rich Stateroom Mix. As of June 30, 2013, 51% of our staterooms had private balconies representing a higher mix of outside balcony staterooms than the other contemporary brands. In addition, six of our ships offer The Haven, with suites of up to 570 square feet each. Guests staying in The Haven are provided with personal butler service and exclusive access to a private courtyard area with a private pool, sundecks, hot tubs, and a fitness center. Six of our ships also offer luxury garden suites of up to 6,694 square feet, making them the largest accommodations at sea. |

| • | High-Quality Service. We believe we offer a very high level of onboard service and to further enhance this service we have implemented the Norwegian Platinum Standards program. This program introduces specific standards emphasizing dedicated service, consistency in execution, and overall guest satisfaction which we believe will promote customer loyalty. |

| • | Diverse Selection of Premium Itineraries. In 2012, approximately 50% of our itineraries, by Capacity Days, were in more exotic, under-penetrated and less traditional locations, including Alaska, Hawaii, Bermuda and Europe, compared to the other contemporary brands which are focused primarily on itineraries in the Caribbean and Mexico. This mix of destinations is more consistent with the brands in the premium segment, and these itineraries typically attract higher Net Yields than Caribbean and Mexico sailings. We believe that this high-quality product offering positions us well in comparison to the other Major North American Cruise Brands and provides an opportunity for continued Net Yield growth. |

“Freestyle Cruising”

The most important differentiator for our brand is the “Freestyle Cruising” concept onboard all 12 of our ships. The essence of “Freestyle Cruising” is to provide a cruise experience that offers more freedom and flexibility than any other traditional cruise alternative. While many cruise lines have historically required guests to dine at assigned group tables and at specified times, “Freestyle Cruising” offers the flexibility and choice to our guests who prefer to dine when they want, with whomever they want and without having to dress formally. Additionally, we have increased the number of activities and dining facilities available onboard, allowing guests to tailor their onboard experience to their own schedules, desires and tastes.

All of our ships have been custom designed and purpose-built for “Freestyle Cruising,” which we believe differentiates us significantly from our major competitors. We further believe that “Freestyle Cruising” attracts a passenger base that prefers the less structured, resort-style experience of our cruises. Building on the success of “Freestyle Cruising,” we implemented across our fleet “Freestyle 2.0” featuring significant enhancements to our onboard product offering. These enhancements include a major investment in the total dining experience; upgrading the stateroom experience across the ship; new wide-ranging onboard activities for all ages; and additional recognition, services and amenities for premium-priced balcony, suite and The Haven guests. With Norwegian Epic and Norwegian Breakaway, we have enhanced “Freestyle Cruising” by offering what we believe to be unmatched flexibility in entertainment, offering guests a wide variety of activities and performances to choose from at any time of day or night.

Established Brand Recognition

The Norwegian Cruise Line brand is well established in the cruise industry with a long track record of delivering a world class cruise product offering to its guests. We achieve high-quality feedback scores from our guests in the areas of overall service, physical ship attributes, onboard products and services, food and beverage offerings and overall entertainment and land-based excursion quality. Based on recent guest experience and loyalty reports, the quality of our guests’ experience generates high levels of customer loyalty, as demonstrated by the fact that approximately 35% of our guests are repeat guests and 80% say they would recommend Norwegian Cruise Line to their friends and family. Brand recognition is also strong with over 93% of cruisers reporting familiarity with Norwegian. Additionally, our brand is known for freedom, flexibility and choice, all highly valued benefits within the cruise industry demographic.

4

Table of Contents

Strong Cash Flow

Nearly all of our capital expenditures, other than those related to our newbuild projects (which are substantially financed) and the recent renovation of our private island, relate to the maintenance of our modern fleet and shoreside operations, which includes investments in our IT infrastructure and business intelligence systems. We have export credit financing in place for the Breakaway Plus Class Ships and Norwegian Getaway which will fund approximately 80% to 90% of the required pre-delivery and delivery date construction payments; as such, we expect the cost of our newbuild projects to have a minimal impact on our cash flow in the near term.

We are able to generate significant levels of cash flow due to our ability to pre-sell tickets and receive customer deposits with long lead times ahead of sailing. We also offer our guests the ability to advance book and prepay for certain services. In addition, we believe that the favorable U.S. federal income tax regime applicable to international shipping income enhances our cash flow from operations which continues to contribute significantly to deleveraging our balance sheet.

Highly Experienced Management Team

Our senior management team is comprised of executives with an average of 16 years in the cruise, travel, leisure and hospitality-related industries. Our executive team has streamlined our organization and instilled a results-driven management philosophy that promotes direct accountability and a more nimble decision-making culture that contributed in driving approximately 1,370 basis points of operating income margin expansion since the beginning of 2008 through the end of 2012. We believe our incentive plans closely align the interest of our management team and our shareholders.

Strong Sponsors with Extensive Industry Expertise

Our Sponsors or their affiliates have extensive experience investing in the cruise, leisure and travel-related industries. Affiliates of the Apollo Funds have invested significant equity and resources to the cruise and leisure industry with its investment in Prestige Cruises International, Inc. which operates through two distinct upscale cruise brands, Oceania Cruises and Regent Seven Seas Cruises. In addition, affiliates of both Apollo and TPG have investments in Caesars Entertainment Corporation (“Caesars Entertainment”), with whom we have created a marketing alliance. Affiliates of TPG are also significant investors in Sabre Holdings, a leading GDS (global distribution system) and parent of Travelocity.com. Genting HK, headquartered in Hong Kong, operates a leading Asian cruise line through its subsidiary, Star Cruises Asia Holding Ltd., with destinations in Malaysia, Singapore, Hong Kong, Taiwan, Japan, Vietnam, China and Thailand. We believe that the synergies and purchasing power obtained through these affiliates have resulted in better price negotiations for us and our affiliates for selected supplies and services.

Our Business Strategies

We seek to attract vacationers by offering new products and services and creating differentiated itineraries in new markets through new and existing modern ships with the aim of delivering a better, value-added, vacation experience to our guests relative to other broad-based or land-based leisure alternatives. Our business strategies include the following:

Attractive Product Offerings

We have a long history of product development and innovation within the cruise industry as one of the most established consumer brands. We became the first cruise operator to purchase a private island in the Bahamas and offer a private beach experience to our guests; and we were the first to introduce a 2,000-Berth megaship into the Caribbean market in 1980. More recently, we pioneered new concepts in cruising over the last decade with the development of “Homeland Cruising” and the launch of “Freestyle Cruising.”

We continued to enhance our product offering with the delivery of Norwegian Epic in June 2010, which offers 21 dining options, a diverse range of accommodations and what we believe is the widest array of entertainment at sea. In addition to several differentiated full-service complimentary dining rooms, Norwegian Epic also features specialty restaurants including a classic steakhouse, sushi, Japanese teppanyaki, Brazilian churrascaria, Asian noodle bar, traditional Chinese, fine French and Italian offerings. Guest accommodations on Norwegian Epic include the groundbreaking Studios, 128 staterooms designed for solo travelers centered around the Studio Lounge, a private

5

Table of Contents

two-story lounge for Studio guests. On its top decks, Norwegian Epic offers a “ship within a ship” in the largest suite complex at sea; The Haven includes two decks with 60 suites and penthouses, a private pool with multiple hot tubs and sundecks, a private fitness center and steam rooms, fine dining in the Epic Club restaurant, casual outdoor dining at the Courtyard Grill, and 24-hour concierge service, all exclusively for guests of The Haven. Entertainment onboard Norwegian Epic includes a wide variety of branded entertainment for guests to choose from, including exclusive engagements with Blue Man Group, Cirque Dreams & Dinner, Legends in Concert, Nickelodeon and the improvisational comedy troupe, The Second City.

Building on the success of Norwegian Epic, Norwegian Breakaway includes many of her most popular elements, while maintaining the innovative spirit of “Freestyle Cruising” by introducing new and differentiated features. These include The Haven and a quarter-mile oceanfront boardwalk, The Waterfront, which creates outdoor seating areas for many dining venues and lounges, including our first seafood restaurant, “Ocean Blue by Geoffrey Zakarian.” The centrally located “678 Ocean Place” connects three entire decks of daytime and nighttime entertainment. Master Baker Buddy Valastro, of the popular TLC series “Cake Boss,” opened an extension of Carlo’s Bake Shop onboard. We offer our guests many of the popular entertainment venues of Norwegian Epic such as the dueling pianos of “Howl at the Moon” and new jazz and blues venues, and we also feature the 80’s-inspired rock musical “Rock of Ages,” ballroom dance experience “Burn the Floor” and “Cirque Dreams & Dinner Jungle Fantasy.” We have a strategic partnership with the Radio City Rockettes®, who christened Norwegian Breakaway. This relationship includes a marketing partnership that names Norwegian as the official cruise line of the Rockettes and Radio City Music Hall® and an exhibit showcasing the Rockettes is integrated into the ship. This relationship also includes two Rockettes sailing on select voyages and offering special fitness classes and photo opportunities.

We have completed a $25 million renovation to our private island, Great Stirrup Cay, which includes a new marina, dining and bar facility to enhance the guest experience, as well as offers new activities such as wave runners and private cabanas. The enhancements provide us with additional revenue-generating opportunities on the island.

Maximize Net Yields

We are focused on growing our revenue through various initiatives aimed at increasing our ticket prices and occupancy as well as onboard spending to drive higher overall Net Yields. To maximize passenger ticket revenue, our revenue management strategy is focused on optimizing pricing and generating demand throughout the booking curve. We utilize a base-loading strategy to fill our capacity by booking guests as early before sailing as possible. Base-loading is a strategy that focuses on selling inventory further from the cruise departure date by utilizing certain sales and marketing tactics which generate business with longer booking windows. Base-loading allows us to fill our ships earlier, which prevents discounting close to sailing dates, in order to achieve our targeted Occupancy Percentages. Our specific initiatives to achieve this include:

| • | Casino Player Strategy. As part of this strategy, we have non-exclusive arrangements with approximately 130 casino partners worldwide including Caesars Entertainment, in which affiliates of both Apollo and TPG have investments, whereby loyal gaming guests are offered cruise reward certificates redeemable for cruises on our ships. Through property sponsored events and joint marketing programs, we have the opportunity to market cruises to Caesars Entertainment’s guests. These arrangements with our casino partners have the dual benefit of filling open inventory and reaching guests expected to generate above average onboard revenue through the casino and other onboard spending. |

| • | Strategic Relationships. Our base-loading strategy also includes strategic relationships with travel agencies and international tour operators, who commit to purchasing a certain level of inventory with long lead times. |

| • | Meetings, Incentives and Charters. We are increasing our focus on the meetings, incentives and charters channel, which typically books very far in advance and can represent a significant portion of the ship, or even an entire sailing, in one transaction. |

We continue to focus on various initiatives to drive increased onboard revenue across a variety of areas. From the year ended December 31, 2007 to the twelve months ended June 30, 2013, our net onboard and other revenue yield increased by approximately 30% from $40.58 to $52.68 primarily due to strong performance in casino, beverage sales, shore excursions and specialty dining. Our strategy for further driving increased onboard revenue includes, among other things, generating additional casino revenue through our arrangements with our casino partners, including Caesars Entertainment and Genting HK. These arrangements incorporate marketing resources to deliver

6

Table of Contents

cross-company advertising and marketing campaigns to promote our brand. We also focus on optimizing the utilization of our specialty restaurants and pre-booking and pre-selling additional onboard activities. In addition, Norwegian Epic and Norwegian Breakaway have created additional onboard revenue opportunities based on our premium entertainment offerings.

Brand Expansion Through Disciplined Newbuild Program

Norwegian Getaway is under construction with Meyer Werft and is scheduled for delivery in January 2014. This ship will be approximately 144,000 Gross Tons with 4,000 Berths at an aggregate cost of approximately €625.9 million, or $814.3 million based on the euro/U.S. dollar exchange rate as of June 30, 2013. We have export credit financing in place for this ship that provides financing for 90% of its contract price.

We have also ordered two additional cruise ships from Meyer Werft for delivery in the fourth quarter of 2015 and the first quarter of 2017. These new Breakaway Plus Class Ships will be the largest in our fleet at approximately 163,000 Gross Tons and 4,200 Berths each and will be similar in design and innovation to our Breakaway Class Ships. The combined contract cost of these Breakaway Plus Class Ships is approximately €1.4 billion, or $1.8 billion based on the euro/U.S. dollar exchange rate as of June 30, 2013. We have export credit financing in place for these ships that provides financing for 80% of their contract price.

We believe that these ships will allow us to continue to expand the reach of our brand while driving shareholder value by positioning our Company for accelerated growth with an optimized return on invested capital.

Improve Operating Efficiency and Lower Costs

We are continually focused on driving financial improvement through a variety of business improvement initiatives. These initiatives are focused on reducing costs while at the same time improving the overall product we deliver to our guests. Since the beginning of 2008, we have significantly reduced our operating cost base through various programs including contract renegotiations, overhead rationalization, and fuel consumption reduction initiatives. We hedge our fuel purchases in order to provide greater visibility of our fuel expense. As of June 30, 2013, we had hedged approximately 93%, 63% and 51% of our projected metric tons of fuel purchases for 2013, 2014 and 2015, respectively. We have also reduced our maintenance expense as a result of our fleet renewal program, as younger, more modern ships are typically less costly to maintain than older ships. Adjusted EBITDA grew to $580.3 million for the twelve months ended June 30, 2013, from $332.3 million for the year ended 2009 with an increase in Adjusted EBITDA Margin to 24.7% from 17.9%, respectively, (we refer you to note 5 under “Prospectus Summary—Summary Consolidated Financial Data” for a calculation of Adjusted EBITDA). In addition, we expect the economies of scale from Norwegian Breakaway, Norwegian Getaway and the Breakaway Plus Class Ships to drive further operating efficiencies over the long term.

Expand and Strengthen Our Product Distribution Channels

As part of our growth strategy, we are continually looking for ways to deepen and expand our customer sales channels. We continue to invest in our brand by enhancing our website and our reservation department where our travel agents and guests have the ability to book cruise vacations. We also restructured our sales and marketing organization, which included the recruiting of a new executive leadership team, to provide better focus on distribution through our primary channels: “Retail/Travel Agent,” “International,” and “Meetings, Incentives and Charters.”

| • | Retail/Travel Agent. We introduced our “Partners First” program, in which we have invested in travel partners’ success with additional booking technology improvements and new marketing tools, improved communication and cooperative marketing initiatives. We also have implemented close to 100 individual projects specifically designed to improve our efficiency with the travel agency channels and our guests, ranging from more timely commission payments to aggressive call center quality monitoring. We restructured our travel agent sales force with specific expertise and we also have gained access to a significantly larger number of travel partners through an outbound call center based in our Miami headquarters. We believe that our travel agent partners have witnessed a material improvement in our business practices and overall communication. |

| • | International. We have an international sales presence in Europe and representatives covering Latin America, Australia and Asia. We are primarily focused on increasing our business in the European market, which has grown significantly in recent years but remains under-penetrated. In Europe, we offer local itineraries year-round and our “Freestyle Cruising” has been well received. We expanded our sales force in Europe which |

7

Table of Contents

allows us to develop our distribution in Europe in a manner similar to our U.S. operation. In support of this European strategy, we deployed Norwegian Epic in Europe for an extended summer season in 2013. We are forging a closer distribution partnership with Genting HK to develop product distribution across the Asia Pacific region. |

| • | Meetings, Incentives and Charters. This channel focuses on full ship Charters as well as corporate meeting and incentive travel. These sales often have very long lead times and can fill a significant portion of the ship’s capacity, or even an entire sailing, in one transaction. In addition, this channel strengthens base-loading, which allows us to fill our ships earlier, rather than discounting close to sailing dates, in order to achieve our targeted Occupancy Percentages. In addition, we acquired Sixthman, a company specializing in developing and delivering music-oriented charters, including productions from KISS, Kid Rock and the Cayamo festival, a cruise featuring a wide variety of popular and emerging songwriters. |

Across every distribution channel we are undertaking a major effort to grow demand with a targeted sales and marketing program for our premium stateroom categories, including our balcony and other premium stateroom categories, with a particular emphasis on our suites and The Haven, which have increased as a percentage of our total inventory as a result of our fleet renewal.

Our Fleet

Our ships are purpose-built ships that enable us to provide our guests with the ultimate “Freestyle Cruising” experience. Our ships have state-of-the-art passenger amenities, including up to 28 dining options together with hundreds of private balcony staterooms on each ship. As of June 30, 2013, 51% of our staterooms have private balconies representing a higher mix of outside staterooms with balconies than the other contemporary brands. Private balcony staterooms are very popular with guests and offer the opportunity for increased revenue by allowing us to charge a premium. Six of our ships offer accommodations in The Haven, with suites up to 570 square feet, which provide personal butler service and exclusive access to a private courtyard area with private pool, sundecks, hot tubs, and fitness center. In addition, six of our ships have luxury garden suites with up to 6,694 square feet, making them the largest accommodations at sea. These luxury garden suites offer three separate bedroom areas, spacious living and dining room areas, as well as 24-hour, on call butler and concierge service.

We place the utmost importance on the safety of our guests and crew. Every crew member is well trained in the Company’s stringent safety protocols and participates in weekly safety drills onboard every one of our ships. In addition, our ships utilize operational closed circuit television systems, and we use an advanced, intranet-based Safety and Environmental Management System (“SEMS”) for shipboard and shoreside procedures and self-improvement standards.

Our new ships on order are the next-generation of “Freestyle Cruising” ships and include some of the most popular elements of our recently delivered ships together with new and differentiated features. One such feature is The Haven, which consists of luxury suites included on our Jewel Class Ships, as well as Norwegian Epic and Norwegian Breakaway. We are also introducing The Waterfront, a quarter-mile oceanfront boardwalk which creates outdoor seating areas for many dining venues and lounges. The centrally located “678 Ocean Place” connects three entire decks of daytime and nighttime entertainment.

Continuing our tradition of new product development and the extension of the Norwegian Cruise Line brand, Norwegian Breakaway offers our guests many of the popular entertainment venues of Norwegian Epic such as the dueling pianos of “Howl at the Moon” and new jazz and blues venues, and also features the 80’s-inspired rock musical “Rock of Ages,” ballroom dance experience “Burn the Floor” and “Cirque Dreams & Dinner Jungle Fantasy.” Norwegian Breakaway homeports year-round in New York City with many elements of New York incorporated into its offerings.

The hull art design is by famed New York artist Peter Max, New York-based celebrity chef Geoffrey Zakarian has created our first seafood-centric dining venue, “Ocean Blue by Geoffrey Zakarian” and Master Baker Buddy Valastro of the popular TLC Series “Cake Boss,” opened an extension of Carlo’s Bake Shop onboard. The Radio City Rockettes® christened Norwegian Breakaway and an exhibit showcasing the Rockettes is integrated into the ship. This relationship also includes two Rockettes sailing on select voyages and offering special fitness classes and photo opportunities. Continuing our commitment to Miami, Norwegian Getaway, sister ship to Norwegian Breakaway, with hull artwork designed by Miami artist David “LEBO” LeBatard, will homeport year-round in Miami along with Norwegian Sky.

8

Table of Contents

Our Sponsors

Apollo

Apollo is a leading global alternative investment manager with offices in New York, Los Angeles, Houston, London, Frankfurt, Luxembourg, Singapore, Hong Kong and Mumbai. As of June 30, 2013, Apollo had assets under management of $113.1 billion invested in its private equity, capital markets and real estate businesses. Apollo owns a controlling interest in Prestige Cruises International, Inc. which operates through two distinct upscale cruise brands, Oceania Cruises and Regent Seven Seas Cruises. Investment funds managed by Apollo also have current and past investments in other travel and leisure companies, including Caesars Entertainment, Great Wolf Resorts, Vail Resorts, AMC Entertainment, Wyndham International and other hotel properties.

TPG

TPG is a leading global private investment firm founded in 1992 with more than $55.3 billion of assets under management as of June 30, 2013. TPG has extensive experience with global public and private investments executed through leveraged buyouts, recapitalizations, spinouts, joint ventures and restructurings. TPG seeks to invest in world-class franchises across a range of industries. Prior and current investments include Alltel, Burger King, Caesars Entertainment, Continental, Fairmont Raffles, Hotwire, J. Crew, Neiman Marcus, Sabre, Seagate, Texas Genco, Energy Future Holdings (formerly TXU) and Univision.

Genting HK

Genting HK was founded in 1993 and through its subsidiary, Star Cruises Asia Holding Ltd., operates a leading cruise line in the Asia-Pacific region. Its headquarters are located in Hong Kong and it is represented in more than 20 locations worldwide, with offices and representatives in Asia, Australia, Europe, United Arab Emirates and the U.S. Genting HK currently has a fleet of six ships, which offer various cruise itineraries in the Asia Pacific region.

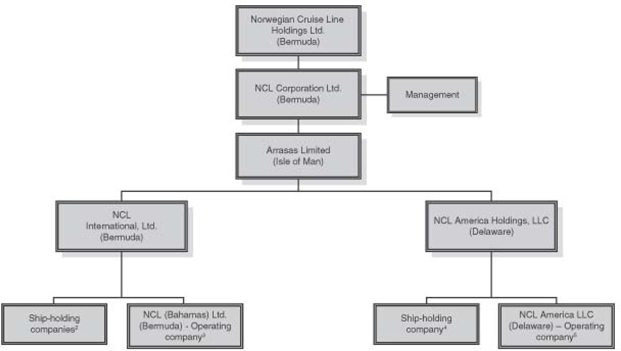

Corporate Reorganization

In February 2011, NCLH, a Bermuda limited company, was formed with the issuance to the Sponsors of, in aggregate, 10,000 ordinary shares, with a par value of $.001 per share. On January 24, 2013, NCLH completed the IPO. In connection with the consummation of the IPO, the Sponsors’ ordinary shares in NCLC were exchanged for the ordinary shares of NCLH, and NCLH became the owner of 100% of the ordinary shares (representing a 97.3% economic interest as of June 30, 2013) and parent company of NCLC (the “Corporate Reorganization”). The Corporate Reorganization was effected solely for the purpose of reorganizing our corporate structure. NCLH had not prior to the completion of the Corporate Reorganization conducted any activities other than those incidental to the formation and to preparations for the Corporate Reorganization and IPO.

NCLC is treated as a partnership for U.S. federal income tax purposes, and the terms of the partnership (including the economic rights with respect thereto) are set forth in an amended and restated tax agreement for NCLC. Economic interests in NCLC are represented by the partnership interests established under the tax agreement, which we refer to as “NCL Corporation Units.” The NCL Corporation Units held by NCLH (as a result of its ownership of 100% of the ordinary shares of NCLC) represent a 97.3% economic interest in NCLC as of June 30, 2013.

In connection with the Corporate Reorganization, NCLC’s outstanding profits interests granted under the Profits Sharing Agreement to management (or former management) of NCLC, including the Ordinary Profits Units described below in “Compensation Discussion and Analysis,” were exchanged for an economically equivalent number of NCL Corporation Units. We refer to the NCL Corporation Units exchanged for profits interests granted under the Profits Sharing Agreement as Management NCL Corporation Units. The Management NCL Corporation Units received upon the exchange of outstanding profits interests are subject to the same time-based vesting requirements and performance-based vesting requirements applicable to the profits interests for which they were exchanged. The Management NCL Corporation Units issued in exchange for the profits interests represent a 2.7% economic interest in NCLC as of June 30, 2013.

NCL Corporation Units are not transferrable without NCLH’s prior consent and do not entitle the holders to any voting, pre-emptive, or sinking fund rights. Any distributions (other than the tax distributions described below) made by NCLC are allocated on a pro rata basis to NCLH and the holders of the Management NCL Corporation Units, based upon the total number of NCL Corporation Units (including Management NCL Corporation Units) outstanding. Distributions by NCLC to NCLH or holders of Management NCL Corporation Units do not entitle holders of ordinary shares of NCLH to any portion of such distribution or to any additional distribution by NCLH.

9

Table of Contents

NCLC does not have any current plans to make any distributions, other than tax distributions which may occur in the future. To the extent funds are legally available, NCLC will make cash distributions, which we refer to as “tax distributions,” to holders of the NCL Corporation Units (including the Management NCL Corporation Units) if ownership of the NCL Corporation Units gives rise to U.S. taxable income for the holder. The U.S. taxable income attributable to NCLH’s ownership of NCL Corporation Units may be different from the relative U.S. taxable income attributable to the Management NCL Corporation Units. In that case, tax distributions may be made on a non-pro rata basis with the holders of Management NCL Corporation Units possibly receiving relative tax distributions greater than the tax distributions received by NCLH.

Holders of NCL Corporation Units (including the Management NCL Corporation Units prior to exchange for ordinary shares of NCLH, as described below) may be entitled to recover on account of the economic interest represented by those units in a bankruptcy or other insolvency event of NCLC or NCLH (even if NCLH incurs debt or other claims that are senior to its ordinary shares). In contrast, the rights of the holders of NCLH’s ordinary shares will be potentially junior to the debt or senior claims (if any) incurred by NCLH in a bankruptcy or other insolvency event. In this respect, the NCL Corporation Units (including the Management NCL Corporation Units) may be considered, in some cases, to be potentially structurally superior to those of the holders of ordinary shares of NCLH in a bankruptcy or other insolvency event for NCLH and NCLC.

Subject to certain procedures and restrictions (including the vesting schedules applicable to the Management NCL Corporation Units and any applicable legal and contractual restrictions), each holder of Management NCL Corporation Units has the right to cause NCLC and NCLH to exchange the holder’s Management NCL Corporation Units for ordinary shares of NCLH at an exchange rate equal to one ordinary share for every Management NCL Corporation Unit (or, at NCLC’s election, a cash payment equal to the value of the exchanged Management NCL Corporation Units), subject to customary adjustments for stock splits, subdivisions, combinations and similar extraordinary events. Any non-pro rata tax distributions made to a Management NCL Corporation Unit holder will reduce the amount of NCLH’s ordinary shares (or cash) that the holder would otherwise receive upon exchange. The exchange right described above is subject to (i) the filing and effectiveness of an applicable registration statement by NCLH that, in its determination, contains all the information which is required to effect a registered sale of its ordinary shares and (ii) all applicable legal and contractual restrictions. NCLH has reserved for issuance a number of its ordinary shares corresponding to the number of Management NCL Corporation Units to be outstanding. On August 19, 2013, NCLH filed a registration statement with the SEC to register on a continuous basis the issuance of the ordinary shares to be received by the holders of Management NCL Corporation Units who elect to exchange.

When any holder of a Management NCL Corporation Unit exchanges such unit for one of NCLH’s ordinary shares (or a cash payment equal to the value of one of such ordinary shares), the relative economic interests of the exchanging NCL Corporation Unit holder and the holders of ordinary shares of NCLH will not be altered. No new NCLC profits interests or Management NCL Corporation Units will be issued; however, NCLH has granted, and expects to continue to grant, options to acquire its ordinary shares to our management team under its new long-term incentive plan.

As a result of the Corporate Reorganization, a non-controlling interest was created within NCLH and NCLH’s financial statements and financial results will differ from NCLC’s in certain respects.

See also “Management,” “Security Ownership of Certain Beneficial Owners and Management,” “Certain Relationships and Related Party Transactions—The Shareholders’ Agreement” and “Certain Relationships and Related Party Transactions—Tax Agreement and Exchange Agreement.”

Corporate Information

NCL Corporation Ltd. is incorporated under the laws of Bermuda. Our registered offices are located at Cumberland House, 9th Floor, 1 Victoria Street, Hamilton HM 11, Bermuda. Our principal executive offices are located at 7665 Corporate Center Drive, Miami, Florida 33126. Our telephone number is (305) 436-4000. Our website is located at www.investor.ncl.com. The information that appears on our websites is not part of, and is not incorporated by reference into this prospectus. Daniel S. Farkas, the Company’s Senior Vice President and General Counsel, is our agent for service of process at our principal executive offices.

Recent Developments

In July 2013, we confirmed an order with Meyer Werft to proceed with the construction of the second Breakaway Plus Class Ship to be delivered in the first quarter of 2017. The contract cost of this second Breakaway Plus Class Ship is approximately €698.4 million, or $908.6 million based on the euro/U.S. dollar exchange rate as of June 30, 2013. We have export credit financing in place for this ship that provides financing for 80% of its contract price.

10

Table of Contents

Summary of the Terms of the Exchange Offer

In connection with the issuance of the Old Notes on February 6, 2013, we entered into a registration rights agreement (as more fully described below) with the initial purchasers of the Old Notes, under which we agreed to deliver to you this prospectus and to consummate the exchange offer. The exchange offer entitles you to exchange your Old Notes for Exchange Notes which are identical in all material respects to the Old Notes except that:

| • | the Exchange Notes have been registered under the Securities Act and will be freely tradable by persons who are not affiliated with us; |

| • | the Exchange Notes are not entitled to registration rights which are applicable to the Old Notes under the registration rights agreement; and |

| • | our obligation to pay additional interest on the Old Notes due to the failure to consummate the exchange offer by a specified date does not apply to the Exchange Notes. |

| The Exchange Offer | We are offering to exchange up to $300,000,000 aggregate principal amount of our registered 5.00% Senior Notes Due 2018 (the “Exchange Notes”), for a like principal amount of our 5.00% Senior Notes Due 2018, which were issued on February 6, 2013 (the “Old Notes”). Old Notes may be exchanged only in denominations of $2,000 and integral multiples of $1,000. For a more complete description of the exchange offer, see “The Exchange Offer.” | |

| Resales of the Exchange Notes | Based on an interpretation by the staff of the SEC set forth in “no-action” letters issued to third parties, we believe that the Exchange Notes issued pursuant to the exchange offer in exchange for Old Notes may be offered for resale, resold and otherwise transferred by you (unless you are our “affiliate” within the meaning of Rule 405 under the Securities Act) without compliance with the registration and prospectus delivery provisions of the Securities Act, provided that you: | |

• are acquiring the Exchange Notes in the ordinary course of business; and | ||

• have not engaged in, do not intend to engage in, and have no arrangement or understanding with any person or entity, including any of our affiliates, to participate in, a distribution of the Exchange Notes. | ||

| In addition, each participating broker-dealer that receives Exchange Notes for its own account pursuant to the exchange offer in exchange for Old Notes that were acquired as a result of market-making or other trading activity must also acknowledge that it (i) has not entered into any arrangement or understanding with the Issuer or an affiliate of the Issuer to distribute the Exchange Notes and (ii) will deliver a prospectus in connection with any resale of the Exchange Notes. For more information, see “Plan of Distribution.” | ||

| Any holder of Old Notes, including any broker-dealer, who | ||

• is our affiliate, | ||

• does not acquire the Exchange Notes in the ordinary course of its business, or | ||

• tenders in the exchange offer with the intention to participate, or for the purpose of participating, in a distribution of Exchange Notes, | ||

| cannot rely on the position of the staff of the SEC expressed in Exxon Capital Holdings Corporation, Morgan Stanley & Co., Incorporated or similar no-action letters and, in the absence of an exemption, must comply with the registration and prospectus delivery requirements of the Securities Act in connection with the resale of the Exchange Notes. | ||

11

Table of Contents

| Expiration Date; Withdrawal of Tenders | The exchange offer will expire at 5:00 p.m., New York City time, on November 7, 2013, or such later date and time to which we extend it. We do not currently intend to extend the expiration date. A tender of Old Notes pursuant to the exchange offer may be withdrawn at any time prior to the expiration date. Any Old Notes not accepted for exchange for any reason will be returned without expense to the tendering holder promptly after the expiration or termination of the exchange offer. | |

| Conditions to the Exchange Offer | The exchange offer is subject to customary conditions, some of which we may waive. For more information, see “The Exchange Offer—Certain Conditions to the Exchange Offer.” | |

| Procedures for Tendering Old Notes | If you wish to accept the exchange offer, you must complete, sign and date the accompanying letter of transmittal, or a copy of the letter of transmittal, according to the instructions contained in this prospectus and the letter of transmittal. You must also mail or otherwise deliver the letter of transmittal, or the copy, together with the Old Notes and any other required documents, to the exchange agent at the address set forth on the cover of the letter of transmittal. If you hold Old Notes through The Depository Trust Company (“DTC”) and wish to participate in the exchange offer, you must comply with the Automated Tender Offer Program procedures of DTC, by which you will agree to be bound by the letter of transmittal. | |

| By signing or agreeing to be bound by the letter of transmittal, you will represent to us that, among other things: | ||

• any Exchange Notes that you receive will be acquired in the ordinary course of your business; | ||

• you have no arrangement or understanding with any person or entity, including any of our affiliates, to participate in the distribution of the Exchange Notes; | ||

• if you are a broker-dealer that will receive Exchange Notes for your own account in exchange for Old Notes that were acquired as a result of market-making activities, that you (i) have not entered into any arrangement or understanding with the Issuer or an affiliate of the Issuer to distribute Exchange Notes and (ii) will deliver a prospectus, as required by law, in connection with any resale of the Exchange Notes; and | ||

• you are not our “affiliate” as defined in Rule 405 under the Securities Act, or, if you are an affiliate, you will comply with any applicable registration and prospectus delivery requirements of the Securities Act. | ||

| Guaranteed Delivery Procedures | If you wish to tender your Old Notes and your Old Notes are not immediately available or you cannot deliver your Old Notes, the letter of transmittal or any other documents required by the letter of transmittal or comply with the applicable procedures under DTC’s Automated Tender Offer Program prior to the expiration date, you must tender your Old Notes according to the guaranteed delivery procedures set forth in this prospectus under “The Exchange Offer—Guaranteed Delivery Procedures.” | |

| Effect on Holders of Old Notes | As a result of the making of, and upon acceptance for exchange of all validly tendered Old Notes pursuant to the terms of, the exchange offer, we will have fulfilled a covenant contained in the registration rights agreement and, accordingly, we will not be obligated to pay additional interest as described in the registration rights agreement. If you are a holder of Old Notes and do not tender your Old Notes in the exchange offer, you will continue to hold such Old Notes and you will be entitled to all the rights and limitations applicable to the Old Notes in the indenture, except for any rights under the registration rights agreement that by their terms terminate upon the consummation of the exchange offer. | |

12

Table of Contents

| Consequences of Failure to Exchange | All untendered Old Notes will continue to be subject to the restrictions on transfer provided for in the Old Notes and in the indenture. In general, the Old Notes may not be offered or sold unless registered under the Securities Act, except pursuant to an exemption from, or in a transaction not subject to, the Securities Act and applicable state securities laws. Other than in connection with the exchange offer, we do not currently anticipate that we will register the Old Notes under the Securities Act. | |

| Material Tax Consequences | The exchange of Old Notes for Exchange Notes in the exchange offer should not be a taxable event for U.S. federal income tax purposes. For more information, see “Certain U.S. Federal Income Tax Consequences.” See also “Certain Bermuda Tax Consequences.” | |

| Use of Proceeds | We will not receive any cash proceeds from the issuance of the Exchange Notes in the exchange offer. | |

| Registration Rights Agreement | We entered into a registration rights agreement with the initial purchasers of the Notes on February 6, 2013. The registration rights agreement requires us to file this exchange offer registration statement and contains customary provisions with respect to registration procedures, indemnity and contribution rights. The offering of the Exchange Notes is intended to satisfy certain of our obligations under the registration rights agreement. | |

| Exchange Agent | U.S. Bank National Association is the exchange agent for the exchange offer. The address and telephone number of the exchange agent are set forth in the section captioned “The Exchange Offer—Exchange Agent.” | |

13

Table of Contents

Summary of the Terms of the Exchange Notes

The summary below describes the principal terms of the Exchange Notes. Certain of the terms and conditions described below are subject to important limitations and exceptions. The “Description of Notes” section of this prospectus contains more detailed descriptions of the terms and conditions of the Exchange Notes. We urge you to read this entire prospectus, including the “Risk Factors” section and the consolidated financial statements and related notes.

| Issuer | NCL Corporation Ltd., a company incorporated under the laws of Bermuda. | |

| Exchange Notes Offered | $300,000,000 aggregate principal amount of 5.00% Senior Notes due February 15, 2018. | |

| Maturity Date | The Exchange Notes will mature on February 15, 2018. | |

| Interest Rate | The Exchange Notes will bear interest at a rate of 5.00% per annum. | |

| Holders of Old Notes whose Old Notes are accepted for exchange in the Exchange Offer will receive the same interest payment on February 15, 2014 (the next interest payment date with respect to the Old Notes) that they would have received if they had not accepted the Exchange Offer. | ||

| Interest Payment Dates | Interest on the Exchange Notes will be payable semi-annually in arrears on February 15 and August 15 of each year, beginning on the first interest payment date following the completion of the exchange offer. | |

| Ranking | The Exchange Notes will constitute our senior unsecured obligations. They will: | |

• rank senior in right of payment to all of our future indebtedness that is expressly subordinated in right of payment to the Exchange Notes; | ||

• rank equally in right of payment with all of our existing and future liabilities that are not so subordinated (including, without limitation, guarantees of indebtedness of our subsidiaries); | ||