Exhibit 99.1

Public Lender Presentation

March 18, 2014

CooperStandard

PASSION FOR PERFORMANCE

Forward-Looking Statements

This presentation includes “forward-looking statements” within the meaning of U.S. federal securities laws, and we intend that such forward-looking statements be subject to the safe harbor created thereby. We make forward-looking statements in this presentation and may make such statements in future filings with the SEC. We may also make forward-looking statements in our press releases or other public or stockholder communications. These forward-looking statements include statements concerning our plans, objectives, goals, strategies, future events, future revenue or performance, capital expenditures, financing needs, plans or intentions relating to acquisitions, business trends, and other information that is not historical information. When used in this presentation, the words “estimates,” “expects,” “anticipates,” “projects,” “plans,” “intends,” “believes,” “forecasts,” or future or conditional verbs, such as “will,” “should,” “could,” or “may,” and variations of such words or similar expressions are intended to identify forward-looking statements. All forward-looking statements, including, without limitation, management’s examination of historical operating trends and data are based upon our current expectations and various assumptions. Our expectations, beliefs, and projections are expressed in good faith and we believe there is a reasonable basis for them. However, no assurances can be made that these expectations, beliefs and projections will be achieved. Forward-looking statements are not guarantees of future performance and are subject to significant risks and uncertainties that may cause actual results or achievements to be materially different from the future results or achievements expressed or implied by the forward-looking statements.

There are a number of risks and uncertainties that could cause our actual results to differ materially from the forward-looking statements contained in this presentation. Important factors that could cause our actual results to differ materially from the forward-looking statements we make herein include, but are not limited to: cyclicality of the automotive industry with the possibility of further material contractions in automotive sales and production effecting the viability of our customers and financial condition of our customers; global economic uncertainty, particularly in Europe; loss of large customers or significant platforms; our ability to generate sufficient cash to service our indebtedness, and obtain future financing; operating and financial restrictions imposed on us by our bond indentures and credit agreement; our underfunded pension plans; supply shortages; escalating pricing pressures and decline of volume requirements from our customers; our ability to meet significant increases in demand; availability and increasing volatility in cost of raw materials or manufactured components; our ability to continue to compete successfully in the highly competitive automotive parts industry; risks associated with our non-U.S. operations; foreign currency exchange rate fluctuations; our ability to control the operations of joint ventures for our benefit; the effectiveness of our continuous improvement program and other cost savings plans; product liability and warranty and recall claims that may be brought against us; work stoppages or other labor conditions; natural disasters; our ability to meet our customers’ needs for new and improved products in a timely manner or cost-effective basis; the possibility that our acquisition strategy may not be successful; our legal rights to our intellectual property portfolio; environmental and other regulations; the possible volatility of our annual effective tax rate; significant changes in discount rates and the actual return on pension assets; the possibility of future impairment charges to our goodwill and long-lived assets; and the interests of our major stockholders may conflict with our interests.

There may be other factors that may cause our actual results to differ materially from the forward-looking statements. All forward-looking statements attributable to us or persons acting on our behalf apply only as of the date of this presentation and are expressly qualified in their entirety by the cautionary statements included herein. We undertake no obligation to update or revise forward-looking statements to reflect events or circumstances that arise after the date made or to reflect the occurrence of unanticipated events.

PASSION FOR PERFORMANCE 2

Today’s Presentation

Transaction Overview

- Deutsche Bank

Cooper Standard Overview

- Jeff Edwards, Chairman and Chief Executive Officer, Cooper Standard

Financial Overview and Guidance

- Allen Campbell, Executive Vice President and Chief Financial Officer, Cooper Standard

Syndication Overview

- Deutsche Bank

PASSION FOR PERFORMANCE 3

Transaction Overview

Deutsche Bank

PASSION FOR PERFORMANCE 4

Transaction Overview

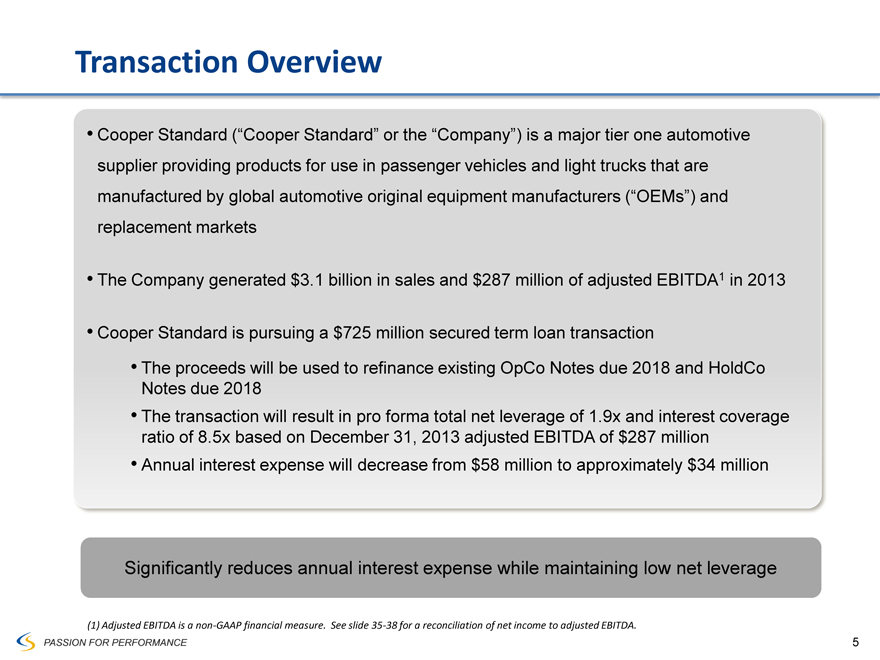

Cooper Standard (“Cooper Standard” or the “Company”) is a major tier one automotive supplier providing products for use in passenger vehicles and light trucks that are manufactured by global automotive original equipment manufacturers (“OEMs”) and replacement markets

The Company generated $3.1 billion in sales and $287 million of adjusted EBITDA1 in 2013

Cooper Standard is pursuing a $725 million secured term loan transaction

The proceeds will be used to refinance existing OpCo Notes due 2018 and HoldCo Notes due 2018

The transaction will result in pro forma total net leverage of 1.9x and interest coverage ratio of 8.5x based on December 31, 2013 adjusted EBITDA of $287 million

Annual interest expense will decrease from $58 million to approximately $34 million

Significantly reduces annual interest expense while maintaining low net leverage

(1) Adjusted EBITDA is a non-GAAP financial measure. See slide 35-38 for a reconciliation of net income to adjusted EBITDA.

PASSION FOR PERFORMANCE 5

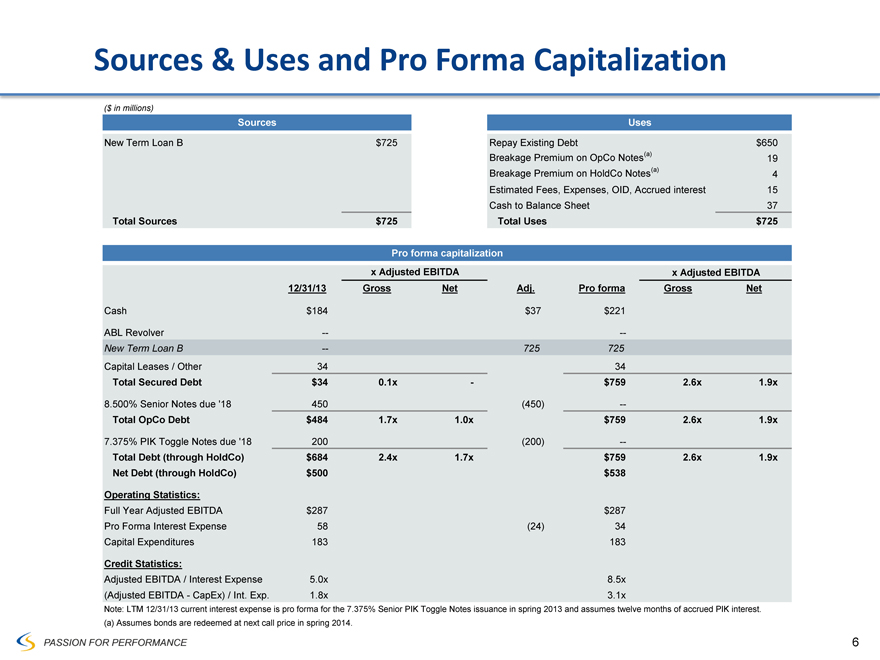

Sources & Uses and Pro Forma Capitalization

($ in millions)

Sources

New Term Loan B $725

Total Sources $725

Uses

Repay Existing Debt $650

Breakage Premium on OpCo Notes(a) 19

Breakage Premium on HoldCo Notes(a) 4

Estimated Fees, Expenses, OID, Accrued interest 15

Cash to Balance Sheet 37

Total Uses $725

Pro forma capitalization

x Adjusted EBITDA x Adjusted EBITDA

12/31/13 Gross Net Adj. Pro forma Gross Net

Cash $184 $37 $221

ABL Revolver -- --

New Term Loan B -- 725 725

Capital Leases / Other 34 34

Total Secured Debt $34 0.1x - $759 2.6x 1.9x

8.500% Senior Notes due ‘18 450 (450) --

Total OpCo Debt $484 1.7x 1.0x $759 2.6x 1.9x

7.375% PIK Toggle Notes due ‘18 200 (200) --

Total Debt (through HoldCo) $684 2.4x 1.7x $759 2.6x 1.9x

Net Debt (through HoldCo) $500 $538

Operating Statistics:

Full Year Adjusted EBITDA $287 $287

Pro Forma Interest Expense 58 (24) 34

Capital Expenditures 183 183

Credit Statistics:

Adjusted EBITDA / Interest Expense 5.0x 8.5x

(Adjusted EBITDA - CapEx) / Int. Exp. 1.8x 3.1x

Note: LTM 12/31/13 current interest expense is pro forma for the 7.375% Senior PIK Toggle Notes issuance in spring 2013 and assumes twelve months of accrued PIK interest. (a) Assumes bonds are redeemed at next call price in spring 2014.

PASSION FOR PERFORMANCE 6

Jeff Edwards

Chairman and Chief Executive Officer

Cooper Standard Overview

PASSION FOR PERFORMANCE 7

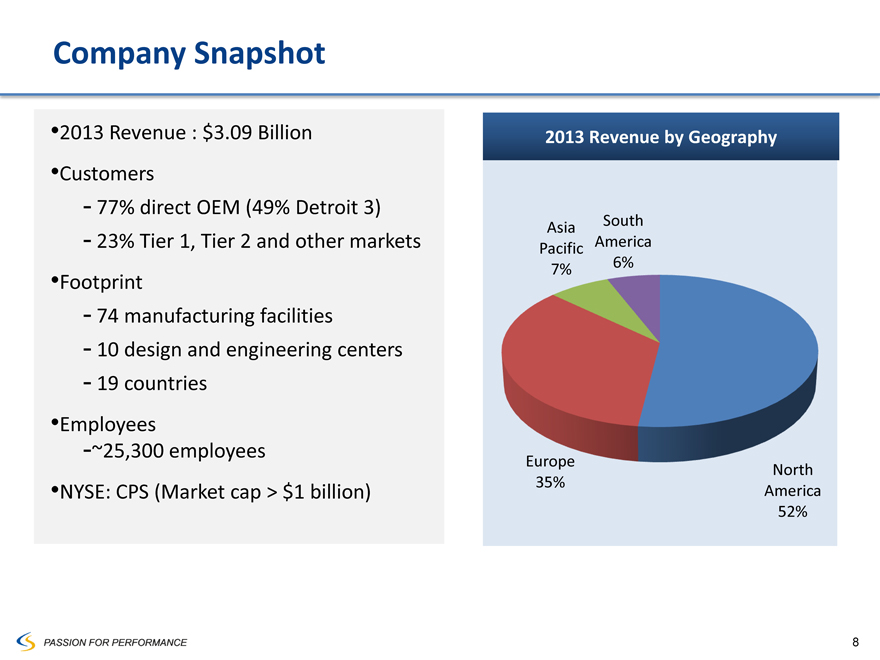

Company Snapshot

2013 Revenue : $3.09 Billion

Customers

- 77% direct OEM (49% Detroit 3)

- 23% Tier 1, Tier 2 and other markets

Footprint

- 74 manufacturing facilities

- 10 design and engineering centers

- 19 countries

Employees -~25,300 employees

NYSE: CPS (Market cap > $1 billion)

2013 Revenue by Geography

Asia Pacific 7%

South America 6%

Europe 35%

North America 52%

PASSION FOR PERFORMANCE 8

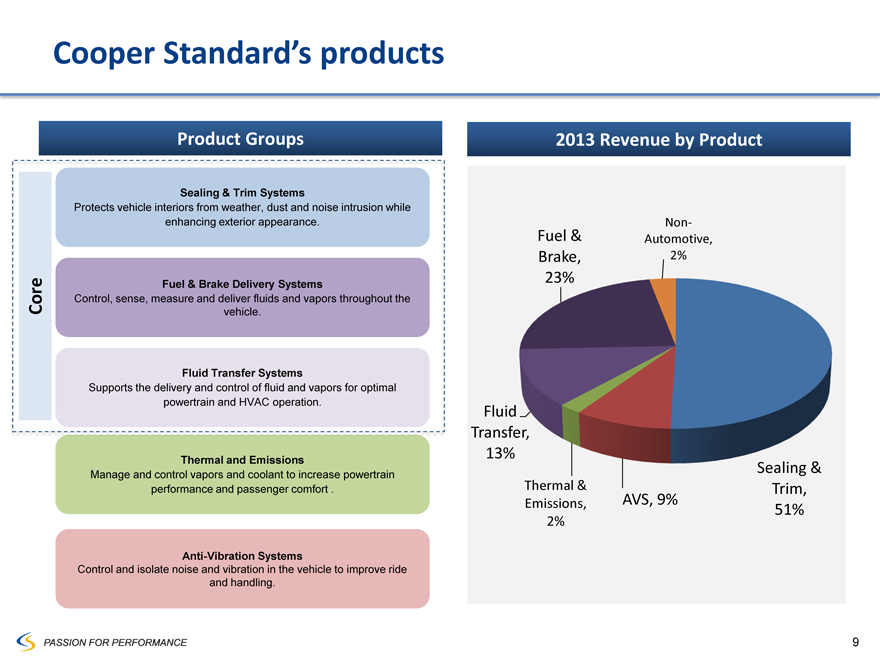

Cooper Standard’s products

Core

Product Groups

Sealing & Trim Systems

Protects vehicle interiors from weather, dust and noise intrusion while enhancing exterior appearance.

Fuel & Brake Delivery Systems

Control, sense, measure and deliver fluids and vapors throughout the vehicle.

Fluid Transfer Systems

Supports the delivery and control of fluid and vapors for optimal powertrain and HVAC operation.

Thermal and Emissions

Manage and control vapors and coolant to increase powertrain performance and passenger comfort .

Anti-Vibration Systems

Control and isolate noise and vibration in the vehicle to improve ride and handling.

2013 Revenue by Product

Fuel & Brake, 23%

Non-Automotive, 2%

Fluid Transfer, 13%

Thermal & Emissions, 2%

AVS, 9%

Sealing & Trim, 51%

PASSION FOR PERFORMANCE 9

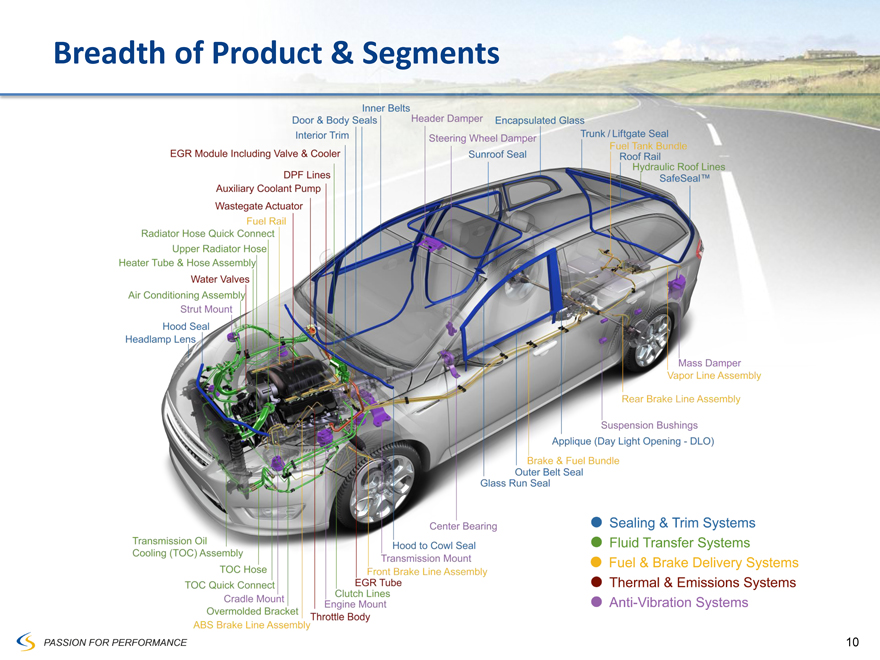

Breadth of Product & Segments

Inner Belts

Door & Body Seals

Interior Trim

EGR Module Including Valve & Cooler

DPF Lines

Auxiliary Coolant Pump

Wastegate Actuator

Fuel Rail

Radiator Hose Quick Connect

Upper Radiator Hose

Heater Tube & Hose Assembly

Water Valves

Air Conditioning Assembly

Strut Mount

Hood seal

Headlamp Lens

Transmission Oil

Cooling (TOC) Assembly

TOC Hose

TOC Quick Connect

Cradle Mount

Overmolded Bracket

ABS Brake Line Assembly

Throttle Body

Engine Mount

Clutch Lines

EGR Tube

Front Brake Line Assembly

Transmission Mount

Hood to Cowl Seal

Center Bearing

Glass Run Seal

Outer Belt Seal

Brake & Fuel Bundle

Applique (Day Light Opening - DLO)

Suspension Bushings

Rear Brake Line Assembly

Vapor Line Assembly

Mass Damper

SafeSealTM

Hydraulic Roof Lines

Roof Tail

Fuel Tank Bundle

Trunk / Liftgate Seal

Encapsulated Glass

Sunroof Seal

Steering Wheel Damper

Header Damper

Sealing & Trim Systems

Fluid Transfer Systems

Fuel & Brake Delivery Systems

Thermal & Emissions Systems

Anti-Vibration Systems

PASSION FOR PERFORMANCE 10

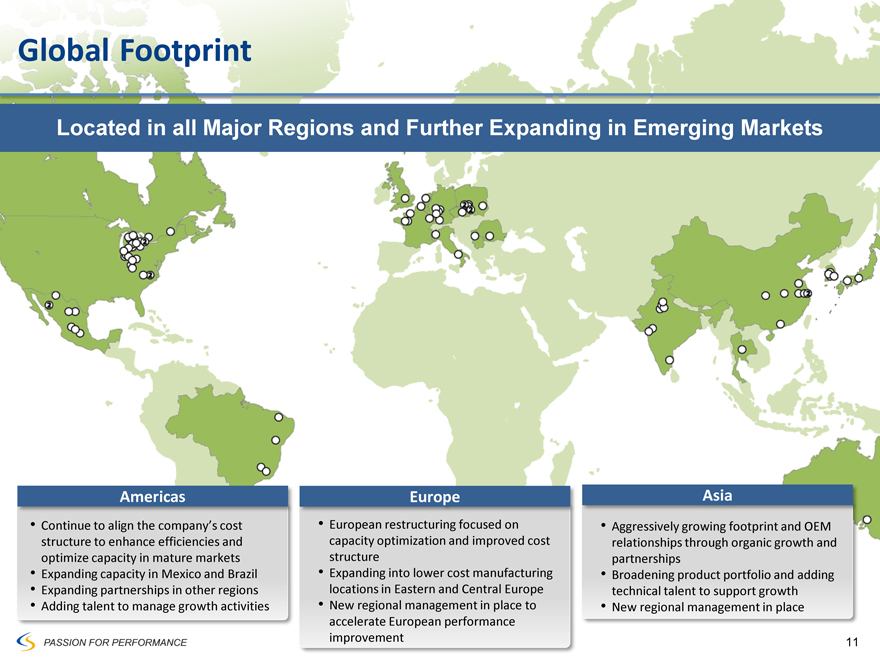

Global Footprint

Located in all Major Regions and Further Expanding in Emerging Markets

Americas

Continue to align the company’s cost structure to enhance efficiencies and optimize capacity in mature markets

Expanding capacity in Mexico and Brazil

Expanding partnerships in other regions

Adding talent to manage growth activities

Europe

European restructuring focused on capacity optimization and improved cost structure

Expanding into lower cost manufacturing locations in Eastern and Central Europe

New regional management in place to accelerate European performance improvement

Asia

Aggressively growing footprint and OEM relationships through organic growth and partnerships

Broadening product portfolio and adding technical talent to support growth

New regional management in place

PASSION FOR PERFORMANCE 11

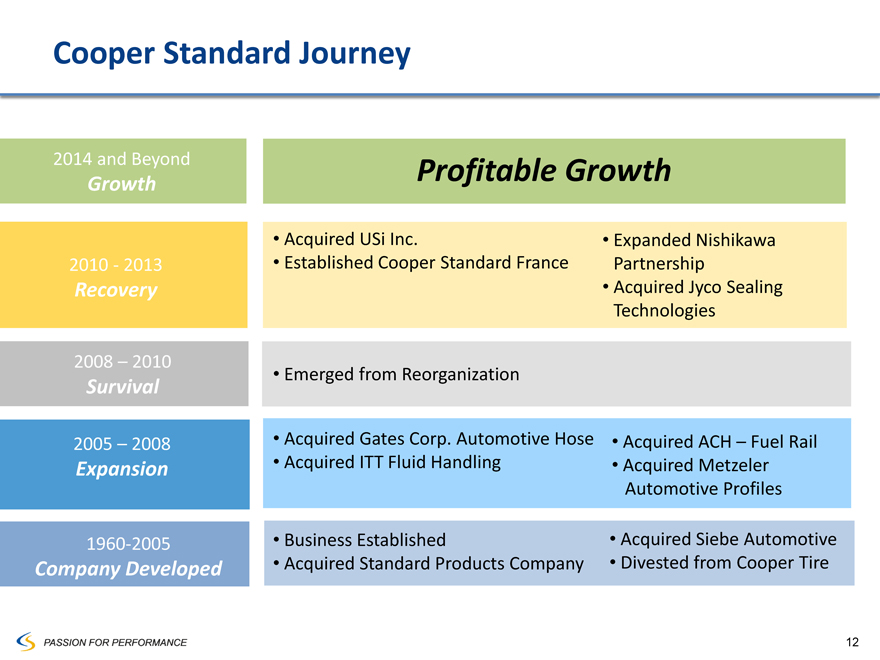

Cooper Standard Journey

2014 and Beyond Growth Profitable Growth

2010 - 2013 Recovery

Acquired USi Inc.

Expanded Nishikawa Partnership

Established Cooper Standard France

Acquired Jyco Sealing Technologies

2008 – 2010 Survival

Emerged from Reorganization

2005 – 2008 Expansion

Acquired Gates Corp. Automotive Hose

Acquired ACH – Fuel Rail

Acquired ITT Fluid Handling

Acquired Metzeler Automotive Profiles

1960-2005 Company Developed

Business Established

Acquired Siebe Automotive

Acquired Standard Products Company

Divested from Cooper Tire

PASSION FOR PERFORMANCE 12

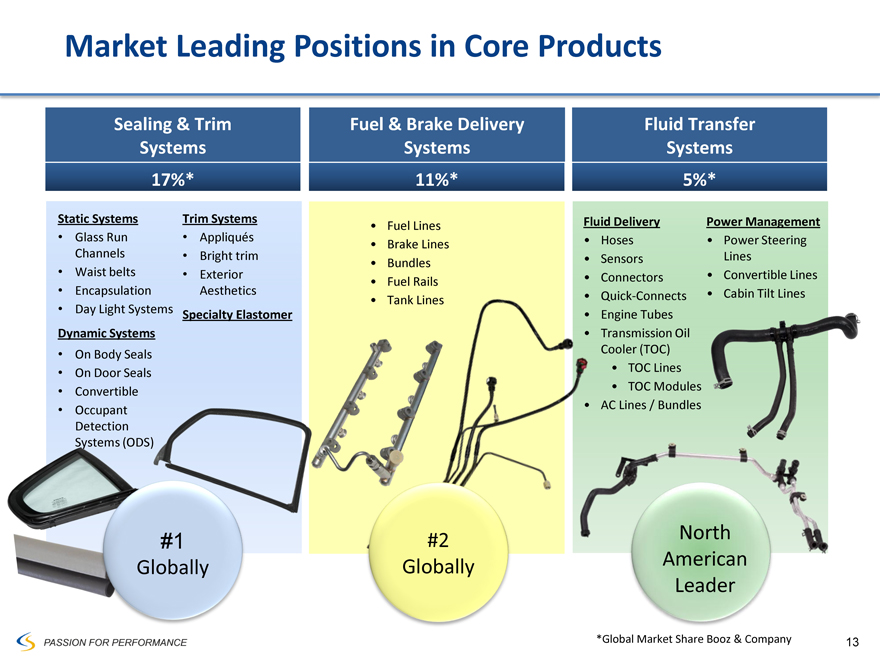

Market Leading Positions in Core Products

Sealing & Trim Systems 17%*

Static Systems

Glass Run Channels

Waist belts

Encapsulation

Day Light Systems

Dynamic Systems

On Body Seals

On Door Seals

Convertible

Occupant Detection Systems (ODS)

Trim Systems

Appliqués

Bright trim

Exterior Aesthetics

Specialty Elastomer

#1

Globally

Fuel & Brake Delivery Systems 11%*

Fuel Lines

Brake Lines

Bundles

Fuel Rails

Tank Lines

#2 Globally

Fluid Transfer Systems 5%*

Fluid Delivery

Hoses

Sensors

Connectors

Quick-Connects Engine Tubes Transmission Oil Cooler (TOC)

TOC Lines

TOC Modules

AC Lines / Bundles

Power Management

Power Steering Lines

Convertible Lines

Cabin Tilt Lines

North

American Leader

PASSION FOR PERFORMANCE *Global Market Share Booz & Company 13

Cooper Standard Products Well Represented on Global Platforms 2013

Cooper Standard products are found on 18 of the top 20 models in the U.S. and Europe

10 of Cooper Standard’s top 20 models are global platforms

Denotes Global Platform

#1 Ford #2 GM #3 Ford #4 Ford #5 Ford

F-150 Silverado/Sierra/Tahoe Explorer /Taurus Focus/Escape Fiesta /Ecosport

Yukon/Escalade

#6 GM #7 Chrysler #8 Chrysler #9 PSA #10 PSA

LaCrosse / Malibu Ram 200 Mid - Size CUV Picasso/C3 408 / C4

#11 GM #12 Ford #13 Volvo* #14 Fiat #15 Ford

Cruze/Volt/Astra Fusion/Mondeo/MKZ S60/V70 Giulietta / Dart F-Series Super Duty

#16 Chrysler #17 Chrysler #18 VW #19 Chrysler #20 Ford

Dodge Town &Country/Jetta Jeep Wrangler Expedition /Navigator

Challenger/Charger Dodge Caravan

Cooper Standard Products are Consistently on the Top Selling Global Platforms

| | |

PASSION FOR PERFORMANCE | | *This particular Volvo model is not global but the platform was designed |

| | | as part of Ford’s global platform |

14

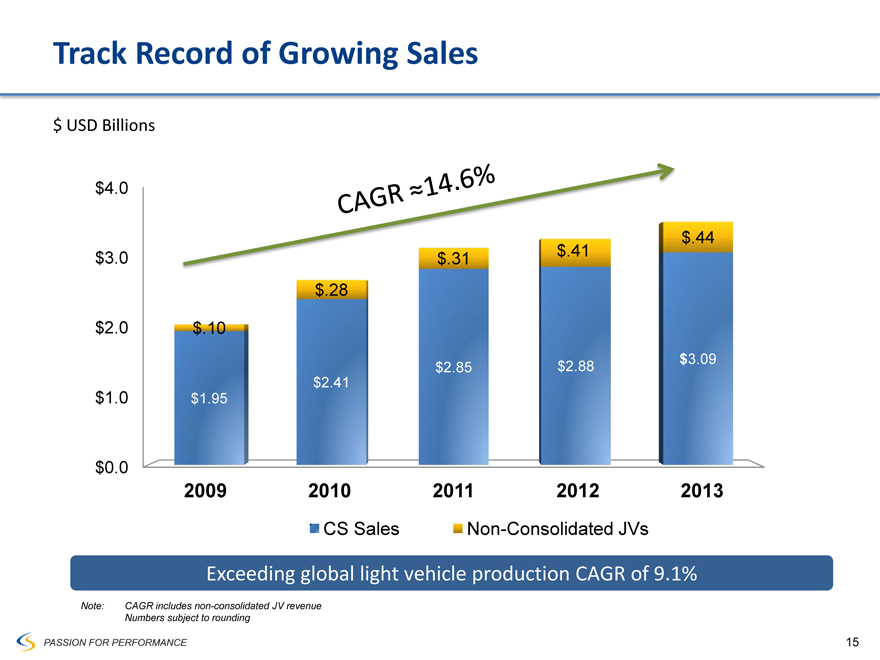

Track Record of Growing Sales

CAGR=14.6%

$ USD Billions

$4.0

$3.0

$2.0

$1.0

$0.0

$.44 $.41 $.31 $.28

$.10

$3.09

$2.85 $2.88

$2.41

$1.95

2009 2010 2011 2012 2013

CS Sales Non-Consolidated JVs

Exceeding global light vehicle production CAGR of 9.1%

Note: CAGR includes non-consolidated JV revenue Numbers subject to rounding

15

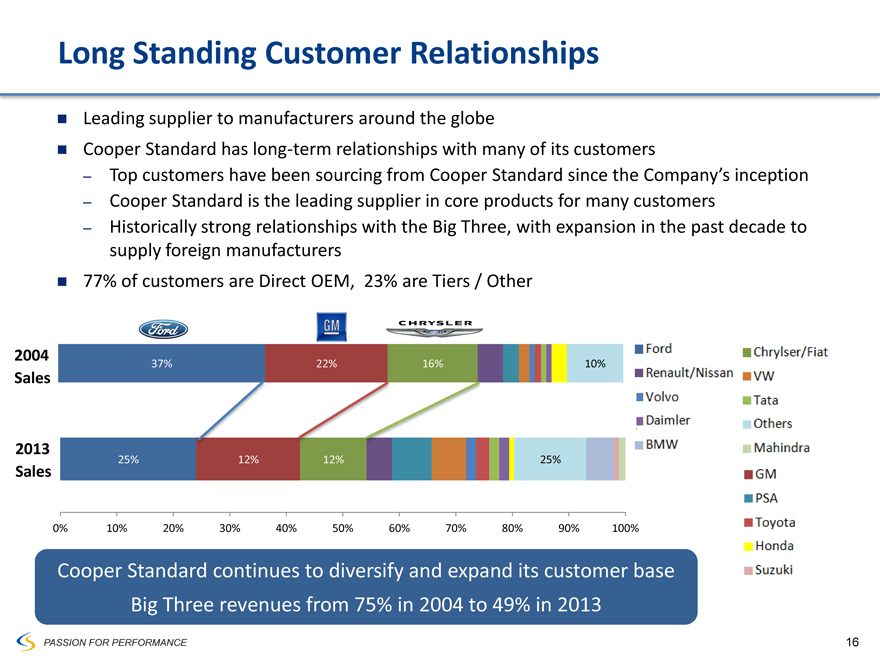

Long Standing Customer Relationships

Leading supplier to manufacturers around the globe

Cooper Standard has long-term relationships with many of its customers

– Top customers have been sourcing from Cooper Standard since the Company’s inception

– Cooper Standard is the leading supplier in core products for many customers

– Historically strong relationships with the Big Three, with expansion in the past decade to supply foreign manufacturers

77% of customers are Direct OEM, 23% are Tiers / Other

| | | | | | | | |

2004 | | 37% | | 22% | | 16% | | 10% |

Sales | | | | | | | | |

2013 | | | | | | | | |

| | | 25% | | 12% | | 12% | | 25% |

Sales | | | | | | | | |

0% 10% 20% 30% 40% 50% 60% 70% 80% 90% 100%

Ford

Renault/Nissan

Volvo

Daimler

BMW

Chrysler

VW

Tata

Others

Mahindra

GM

PSA

Toyota

Honda

Suzuki

Cooper Standard continues to diversify and expand its customer base Big Three revenues from 75% in 2004 to 49% in 2013

PASSION FOR PERFORMANCE

16

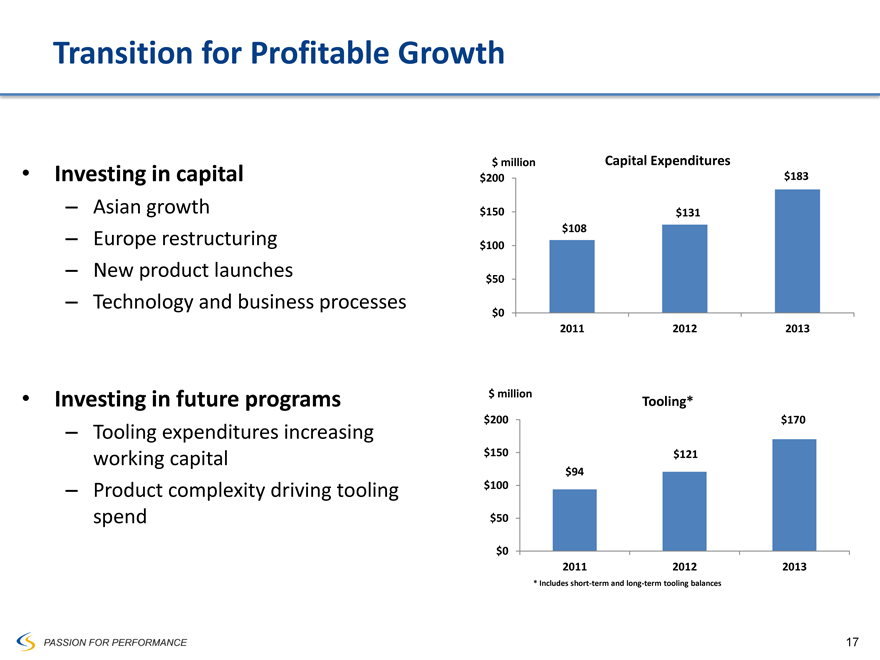

Transition for Profitable Growth

Investing in capital

– Asian growth

– Europe restructuring

– New product launches

– Technology and business processes

Investing in future programs

– Tooling expenditures increasing working capital

– Product complexity driving tooling spend

$ million Capital Expenditures $200 $183

$150 $131 $108 $100

$50

$0

2011 2012 2013

$ million

Tooling* $200 $170

$150 $121 $94 $100

$50

$0

2011 2012 2013

* Includes short-term and long-term tooling balances

PASSION FOR PERFORMANCE

17

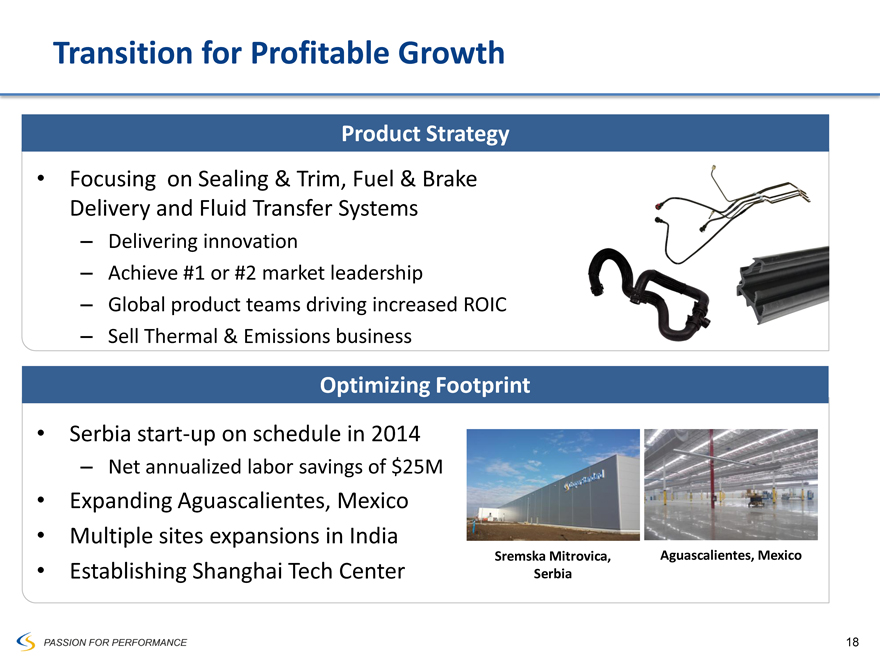

Transition for Profitable Growth

Product Strategy

Focusing on Sealing & Trim, Fuel & Brake Delivery and Fluid Transfer Systems

– Delivering innovation

– Achieve #1 or #2 market leadership

– Global product teams driving increased ROIC

– Sell Thermal & Emissions business

Optimizing Footprint

Serbia start-up on schedule in 2014

– Net annualized labor savings of $25M

Expanding Aguascalientes, Mexico

Multiple sites expansions in India

Establishing Shanghai Tech Center

Sremska Mitrovica,

Aguascalientes, Mexico

Serbia

PASSION FOR PERFORMANCE

18

Allen Campbell

Executive Vice President and

Chief Financial Officer

Financial Overview and Guidance

PASSION FOR PERFORMANCE

19

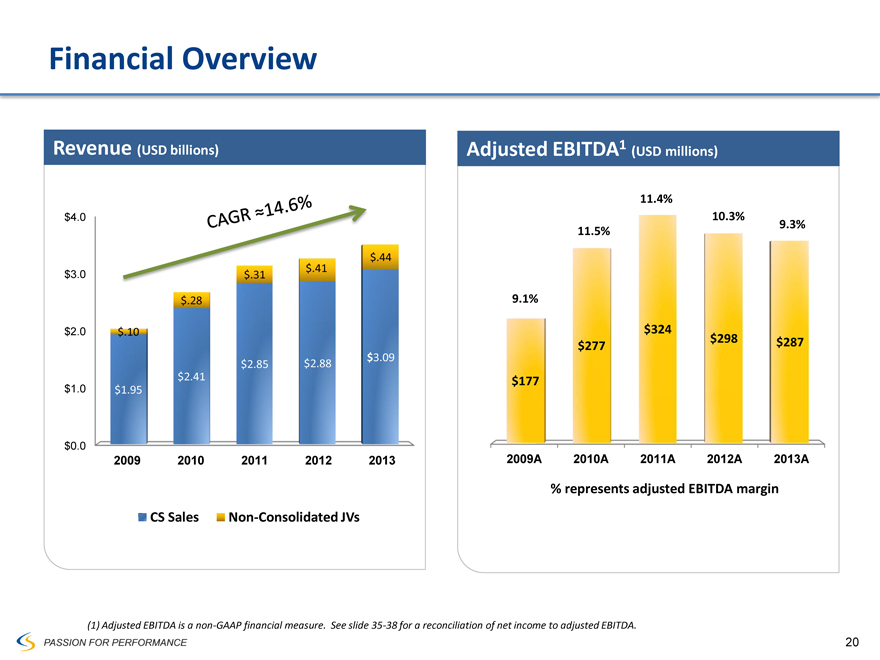

Financial Overview

Revenue (USD billions)

CAGR=14.6%

$4.0

$3.0

$2.0

$1.0

$0.0

$.44

$.31 $.41

$.28

$.10

$2.85 $2.88 $3.09

$2.41

$1.95

2009 2010 2011 2012 2013

CS Sales Non-Consolidated JVs

Adjusted EBITDA1

(USD millions)

11.4%

10.3%

9.3%

11.5%

9.1%

$324 $298 $287 $277

$177

2009A 2010A 2011A 2012A 2013A

% represents adjusted EBITDA margin

(1) Adjusted EBITDA is a non-GAAP financial measure. See slide 35-38 for a reconciliation of net income to adjusted EBITDA.

20 PASSION FOR PERFORMANCE

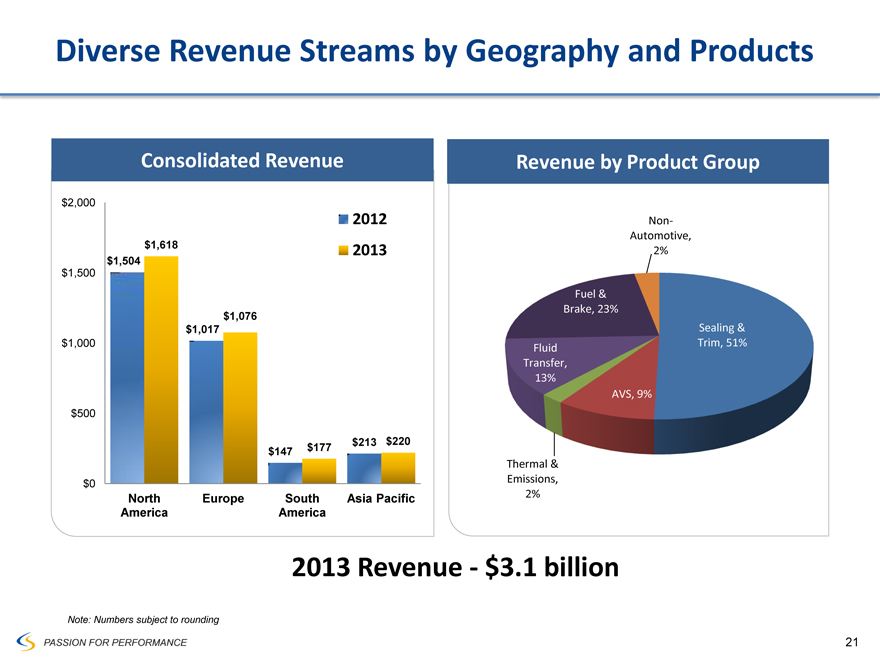

Diverse Revenue Streams by Geography and Products

Consolidated Revenue

2012

2013

$2,000 $1,500 $1,000 $500 $0

$1,618 $1,504

$1,076 $1,017

$213 $220 $147 $177

North Europe South America Asia Pacific America

Revenue by Product Group

Non-Automotive, 2%

Fuel & Brake, 23%

Sealing & Trim, 51% Fluid Transfer, 13% AVS, 9%

Thermal & Emissions, 2%

2013 Revenue - $3.1 billion

Note: Numbers subject to rounding

PASSION FOR PERFORMANCE

21

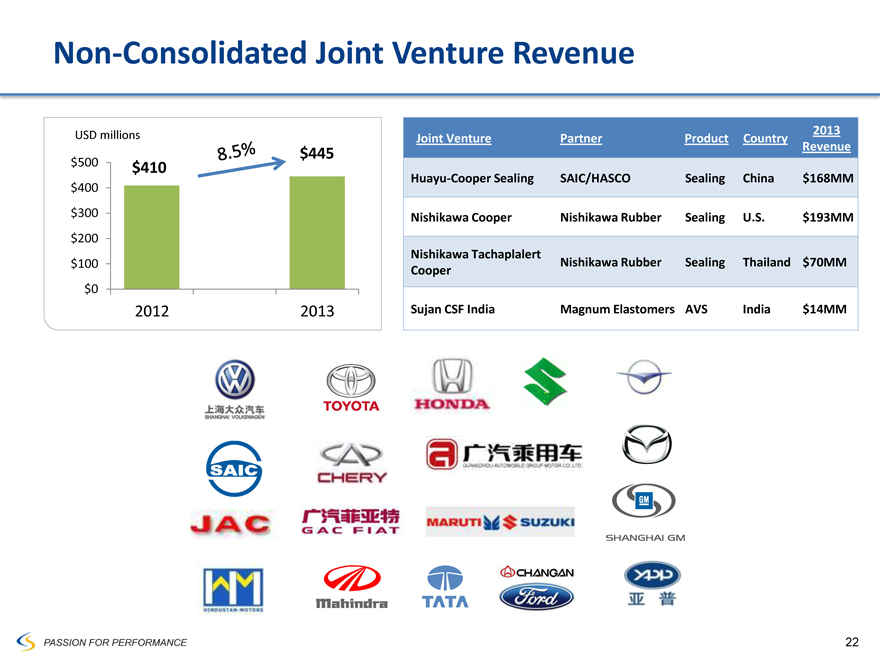

Non-Consolidated Joint Venture Revenue

8.5%

USD millions

$445

$500 $410 $400

$300 $200 $100

$0

2012 2013

Joint Venture

Partner

Product

Country

2013 Revenue

Huayu-Cooper Sealing

SAIC/HASCO

Sealing

China

$168MM

Nishikawa Cooper

Nishikawa Rubber

Sealing

U.S.

$193MM

Nishikawa Tachaplalert Cooper

Nishikawa Rubber

Sealing

Thailand

$70MM

Sujan CSF India

Magnum Elastomers

AVS

India

$14MM

SHANGHAI VOLKSWAGEN

TOYOTA

HONDA

SAIC

CHERY

JAC

GAC FIAT

MARUTI SUZUKI

SHANGHAI GM

HINDUSTAN-MOTORS

Mahindra

TATA

CHANGAN Ford

PASSION FOR PERFORMANCE

22

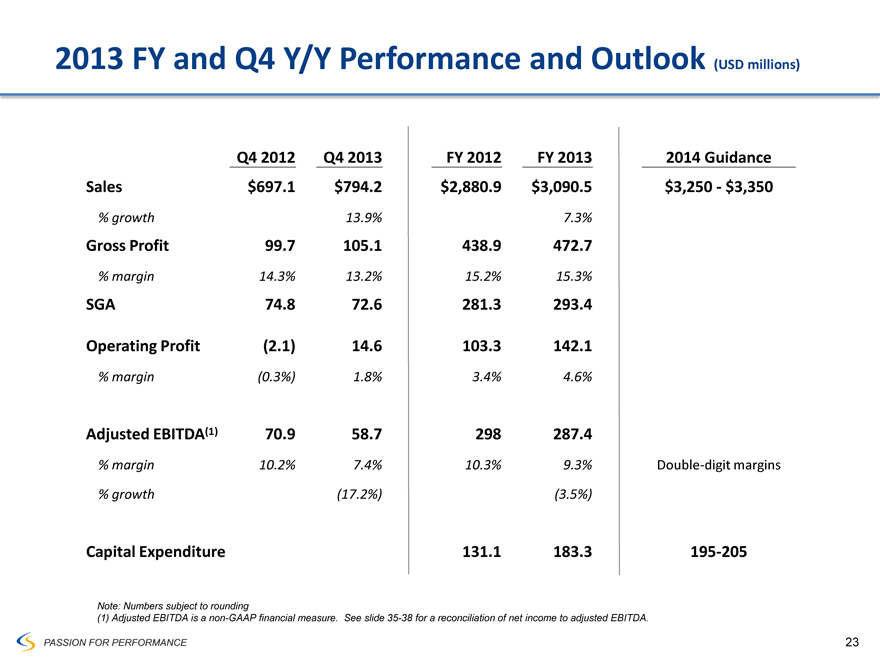

2013 FY and Q4 Y/Y Performance and Outlook (USD millions)

Q4 2012 Q4 2013 FY 2012 FY 2013 2014 Guidance

Sales $697.1 $794.2 $2,880.9 $3,090.5 $3,250 - $3,350

% growth 13.9% 7.3%

Gross Profit 99.7 105.1 438.9 472.7

% margin 14.3% 13.2% 15.2% 15.3%

SGA 74.8 72.6 281.3 293.4

Operating Profit (2.1) 14.6 103.3 142.1

% margin (0.3%) 1.8% 3.4% 4.6%

Adjusted EBITDA(1) 70.9 58.7 298 287.4

% margin 10.2% 7.4% 10.3% 9.3%Double-digit margins

% growth (17.2%) (3.5%)

Capital Expenditure 131.1 183.3 195-205

Note: Numbers subject to rounding

(1) Adjusted EBITDA is a non-GAAP financial measure. See slide 35-38 for a reconciliation of net income to adjusted EBITDA.

PASSION FOR PERFORMANCE

23

2013 Performance and Path Forward

Cooper Standard global sales grew by 7.3% year-over-year

Full year adjusted EBITDA margin of 9.3% of sales

2013 challenges

– New Sealing and Trim launch issues in North America and Europe created increased scrap, additional labor and other costs

– Unanticipated one-time costs approximately $17MM in Q4 2013

– Ramp-up North American volumes

Return to double digit EBITDA margins

– Increased product development and tooling investment address product launch complexity

– Migration to lower-cost areas (Serbia wage rate $5/hr vs. >$30/hr in Western Europe)

– Continued focus on core products with better margin profile

– Exit of non-core, low-margin segments

Capital expenditure at 5.9% of sales as we invest for future growth

Asia Pacific 9.2% North America and others 4.8% South America 7.4% Europe 6.8%

PASSION FOR PERFORMANCE

24

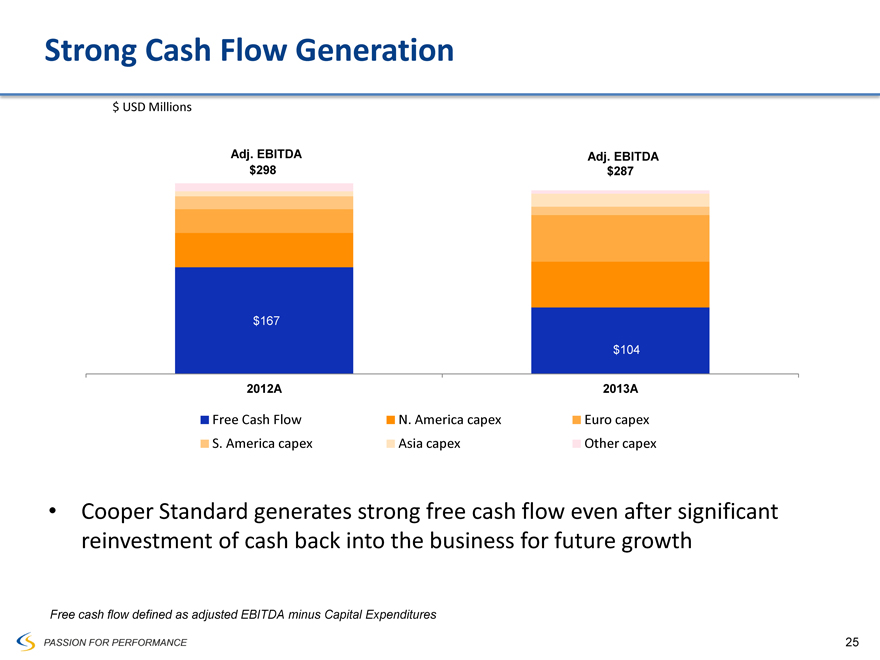

Strong Cash Flow Generation

$ USD Millions

Adj. EBITDA $298

$167

2012A

Adj. EBITDA $287

$104

2013A

Free Cash Flow N. America capex Euro capex S. America capex Asia capex Other capex

Cooper Standard generates strong free cash flow even after significant reinvestment of cash back into the business for future growth

Free cash flow defined as adjusted EBITDA minus Capital Expenditures

PASSION FOR PERFORMANCE

25

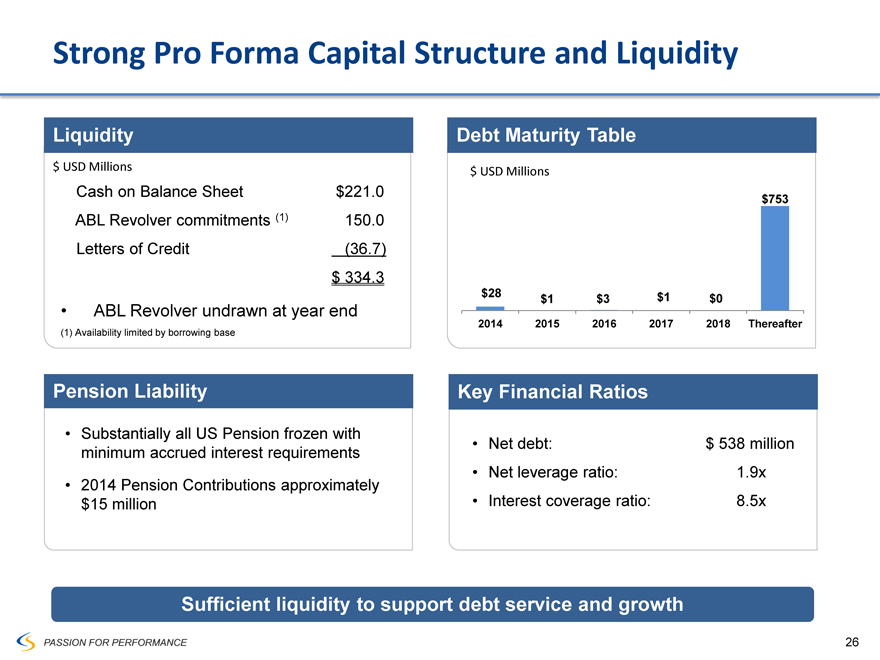

Strong Pro Forma Capital Structure and Liquidity

Liquidity

$ USD Millions

Cash on Balance Sheet

$221.0

ABL Revolver commitments (1)

150.0

Letters of Credit

(36.7)

$334.3

ABL Revolver undrawn at year end

(1) Availability limited by borrowing base

Debt Maturity Table

$ USD Millions

$753

$28 $1 $0

$1 $3

2014 2015 2016 2017 2018 Thereafter

Pension Liability

Substantially all US Pension frozen with minimum accrued interest requirements

2014 Pension Contributions approximately $15 million

Key Financial Ratios

Net debt: $ 538 million

Net leverage ratio: 1.9x

Interest coverage ratio: 8.5x

Sufficient liquidity to support debt service and growth

PASSION FOR PERFORMANCE

26

Summary

Focused on our customers to win global platform via footprint and technical center alignment

– Building centers of excellence

Stabilization of North America and Europe businesses performance

– Addressing launch and product complexity in Sealing & Trim business

– Successfully executing new launches

Continue to make necessary infrastructure / capacity investments

– Asia production strategy (China, India, SE Asia)

– Serbia expansion and optimizing European manufacturing footprint (Romania and Poland)

Evaluate partnerships, especially in Asia, to advance our strategic plan

Focused on returning to double-digit adjusted EBITDA margins

PASSION FOR PERFORMANCE 27

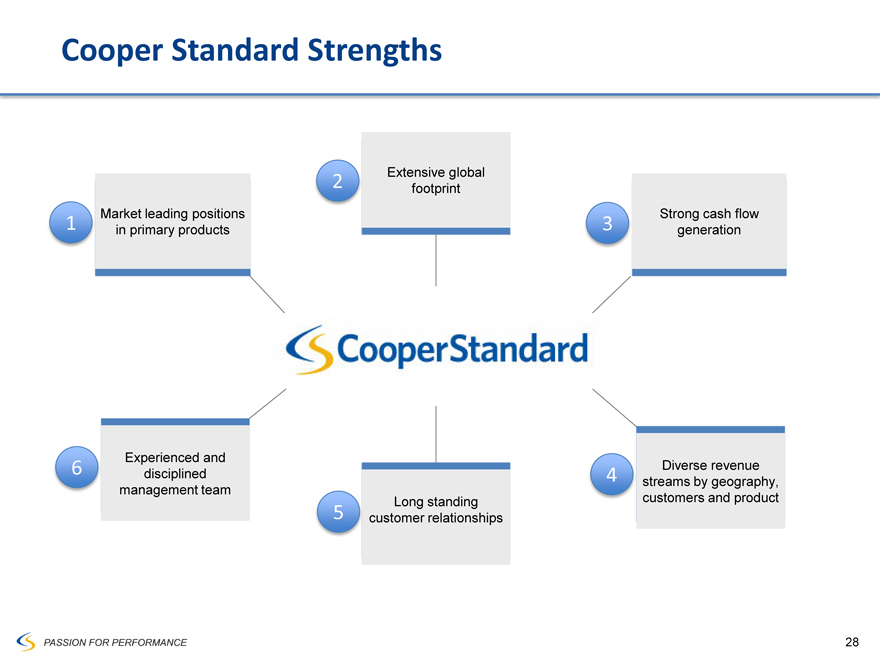

Cooper Standard Strengths

1 Market leading positions in primary products

2 Extensive global footprint

3 Strong cash flow generation

4 Diverse revenue streams by geography, customers and product

5 Long standing customer relationships

6 Experienced and disciplined management team

CooperStandard

PASSION FOR PERFORMANCE 28

Syndication Overview

Deutsche Bank

29

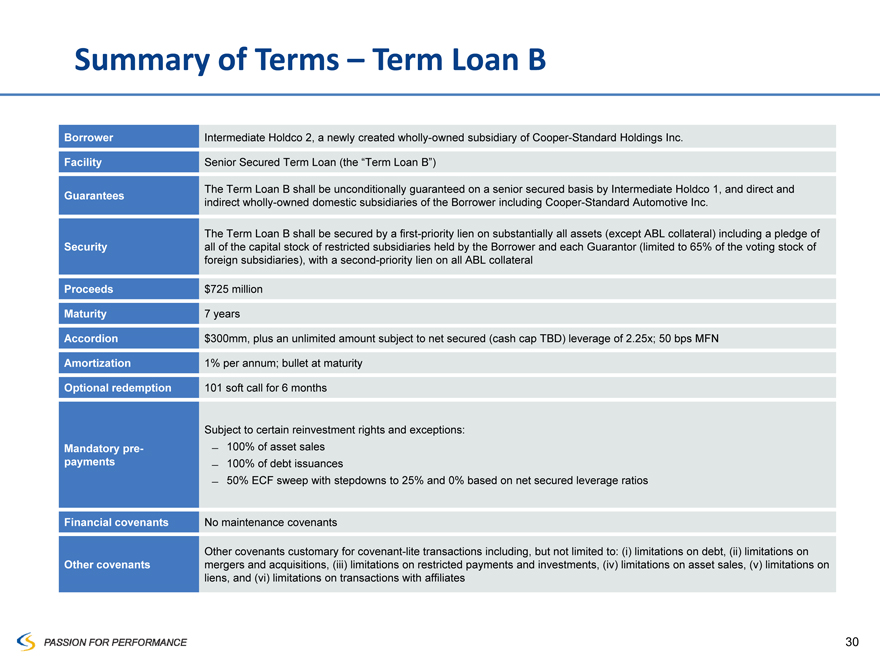

Summary of Terms – Term Loan B

Borrower Intermediate Holdco 2, a newly created wholly-owned subsidiary of Cooper-Standard Holdings Inc.

Facility Senior Secured Term Loan (the “Term Loan B”)

The Term Loan B shall be unconditionally guaranteed on a senior secured basis by Intermediate Holdco 1, and direct and

Guarantees indirect wholly-owned domestic subsidiaries of the Borrower including Cooper-Standard Automotive Inc.

The Term Loan B shall be secured by a first-priority lien on substantially all assets (except ABL collateral) including a pledge of

Security all of the capital stock of restricted subsidiaries held by the Borrower and each Guarantor (limited to 65% of the voting stock of foreign subsidiaries), with a second-priority lien on all ABL collateral

Proceeds $725 million

Maturity 7 years

Accordion $300mm, plus an unlimited amount subject to net secured (cash cap TBD) leverage of 2.25x; 50 bps MFN

Amortization 1% per annum; bullet at maturity

Optional redemption 101 soft call for 6 months

Subject to certain reinvestment rights and exceptions:

Mandatory pre- 100% of asset sales

payments 100% of debt issuances

50% ECF sweep with stepdowns to 25% and 0% based on net secured leverage ratios

Financial covenants No maintenance covenants

Other covenants customary for covenant-lite transactions including, but not limited to: (i) limitations on debt, (ii) limitations on

Other covenants mergers and acquisitions, (iii) limitations on restricted payments and investments, (iv) limitations on asset sales, (v) limitations on liens, and (vi) limitations on transactions with affiliates

30

Transaction Timeline

March 2014

S M T W T F S 1

2 3 4 5 6 7 8

9 10 11 12 13 14 15

16 17 18 19 20 21 22

23 24 25 26 27 28 29

30 31

April 2014

S M T W T F S

1 2 3 4 5

6 7 8 9 10 11 12

13 14 15 16 17 18 19

20 21 22 23 24 25 26

27 28 29 30

Denotes holiday Denotes key date

Date

March 18 March 28 Week of March 31st

Description of Events

– Lenders meeting

– Commitments due

– Close and fund

31

Q&A

32

Appendix

PASSION FOR PERFORMANCE 33

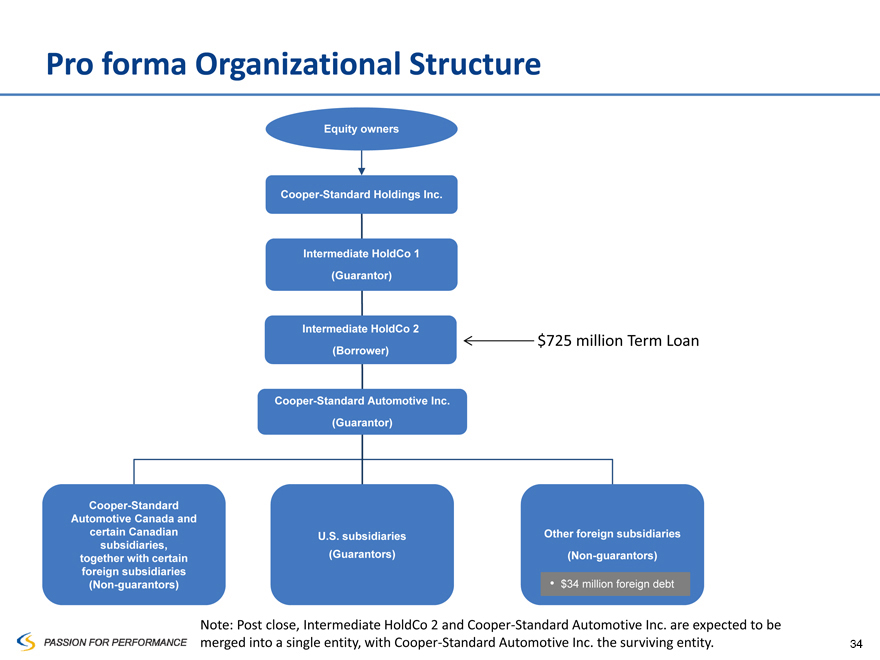

Pro forma Organizational Structure

Equity owners

Cooper-Standard Holdings Inc.

Intermediate HoldCo 1 (Guarantor)

Intermediate HoldCo 2 $725 million Term Loan

(Borrower)

Cooper-Standard Automotive Inc. (Guarantor)

Cooper-Standard Automotive Canada and certain Canadian U.S. subsidiaries Other foreign subsidiaries subsidiaries, together with certain (Guarantors) (Non-guarantors) foreign subsidiaries (Non-guarantors) $34 million foreign debt

Note: Post close, Intermediate HoldCo 2 and Cooper-Standard Automotive Inc. are expected to be merged into a single entity, with Cooper-Standard Automotive Inc. the surviving entity.

33

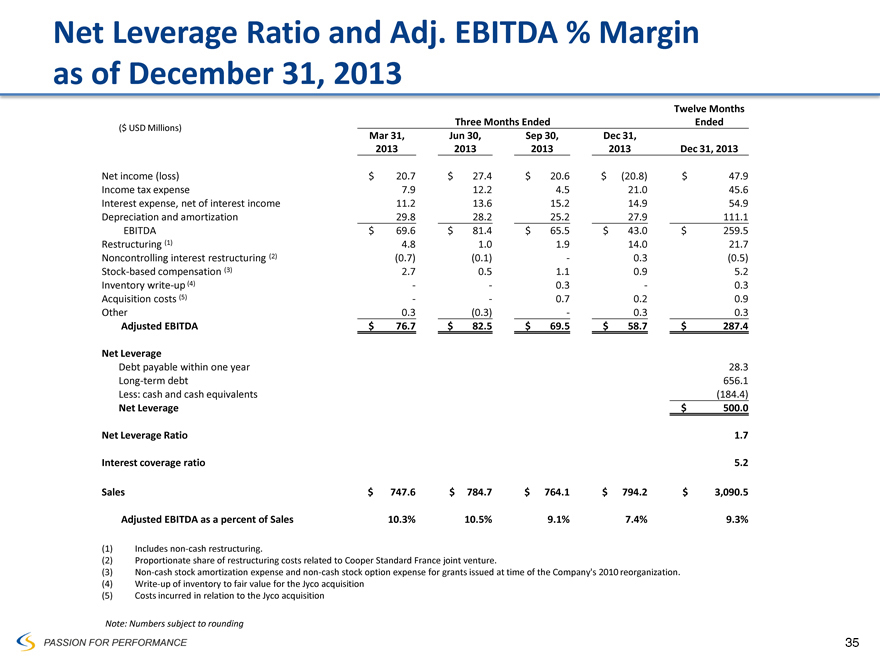

Net Leverage Ratio and Adj. EBITDA % Margin as of December 31, 2013

Three Months Ended Twelve Months Ended

($ USD Millions)

Mar 31, 2013 Jun 30, 2013 Sep 30, 2013 Dec 31, 2013 Dec 31, 2013

Net income (loss) $ 20.7 $ 27.4 $ 20.6 $ (20.8) $ 47.9

Income tax expense 7.9 12.2 4.5 21.0 45.6

Interest expense, net of interest income 11.2 13.6 15.2 14.9 54.9

Depreciation and amortization 29.8 28.2 25.2 27.9 111.1

EBITDA $ 69.6 $ 81.4 $ 65.5 $ 43.0 $ 259.5

Restructuring (1) 4.8 1.0 1.9 14.0 21.7

Noncontrolling interest restructuring (2) (0.7) (0.1) - 0.3 (0.5)

Stock-based compensation (3) 2.7 0.5 1.1 0.9 5.2

Inventory write-up (4) - - 0.3 - 0.3

Acquisition costs (5) - - 0.7 0.2 0.9

Other 0.3 (0.3) - 0.3 0.3

Adjusted EBITDA $ 76.7 $ 82.5 $ 69.5 $ 58.7 $ 287.4

Net Leverage

Debt payable within one year 28.3

Long-term debt 656.1

Less: cash and cash equivalents (184.4)

Net Leverage $ 500.0

Net Leverage Ratio 1.7

Interest coverage ratio 5.2

Sales $ 747.6 $ 784.7 $ 764.1 $ 794.2 $ 3,090.5

Adjusted EBITDA as a percent of Sales 10.3% 10.5% 9.1% 7.4% 9.3%

(1) Includes non-cash restructuring.

(2) Proportionate share of restructuring costs related to Cooper Standard France joint venture.

(3) Non-cash stock amortization expense and non-cash stock option expense for grants issued at time of the Company’s 2010 reorganization.

(4) Write-up of inventory to fair value for the Jyco acquisition

(5) Costs incurred in relation to the Jyco acquisition

Note: Numbers subject to rounding

PASSION FOR PERFORMANCE 34

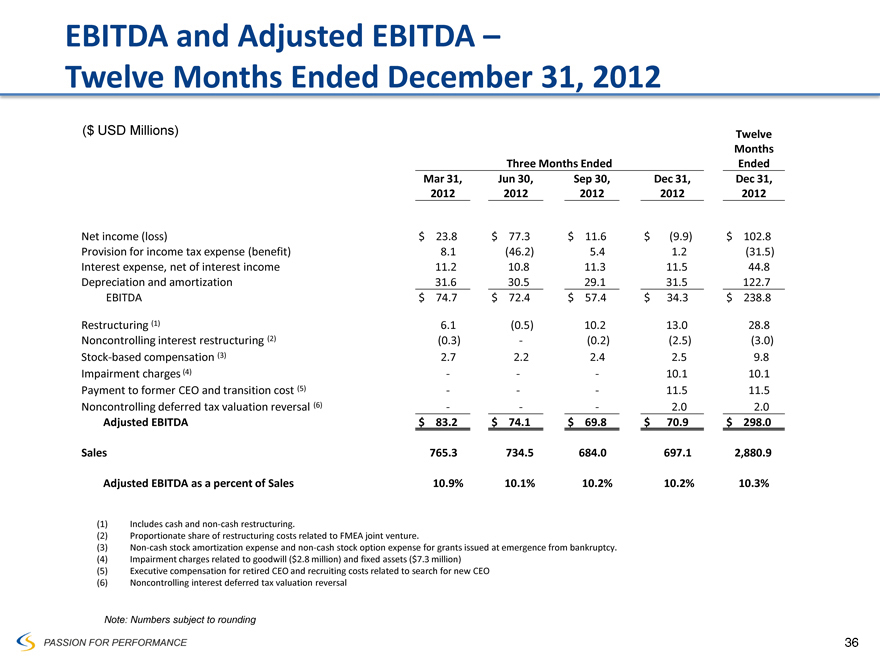

EBITDA and Adjusted EBITDA –

Twelve Months Ended December 31, 2012

($ USD Millions) Three Months Ended Twelve Months Ended

Mar 31, 2012 Jun 30, 2012 Sep 30, 2012 Dec 31, 2012 Dec 31, 2012

Net income (loss) $ 23.8 $ 77.3 $ 11.6 $ (9.9) $ 102.8

Provision for income tax expense (benefit) 8.1 (46.2) 5.4 1.2 (31.5)

Interest expense, net of interest income 11.2 10.8 11.3 11.5 44.8

Depreciation and amortization 31.6 30.5 29.1 31.5 122.7

EBITDA $ 74.7 $ 72.4 $ 57.4 $ 34.3 $ 238.8

Restructuring (1) 6.1 (0.5) 10.2 13.0 28.8

Noncontrolling interest restructuring (2) (0.3) - (0.2) (2.5) (3.0)

Stock-based compensation (3) 2.7 2.2 2.4 2.5 9.8

Impairment charges (4) - - - 10.1 10.1

Payment to former CEO and transition cost (5) - - - 11.5 11.5

Noncontrolling deferred tax valuation reversal (6) - - - 2.0 2.0

Adjusted EBITDA $ 83.2 $ 74.1 $ 69.8 $ 70.9 $ 298.0

Sales 765.3 734.5 684.0 697.1 2,880.9

Adjusted EBITDA as a percent of Sales 10.9% 10.1% 10.2% 10.2% 10.3%

(1) Includes cash and non-cash restructuring.

(2) Proportionate share of restructuring costs related to FMEA joint venture.

(3) Non-cash stock amortization expense and non-cash stock option expense for grants issued at emergence from bankruptcy. (4) Impairment charges related to goodwill ($2.8 million) and fixed assets ($7.3 million) (5) Executive compensation for retired CEO and recruiting costs related to search for new CEO

(6) Noncontrolling interest deferred tax valuation reversal

Note: Numbers subject to rounding

PASSION FOR PERFORMANCE 36

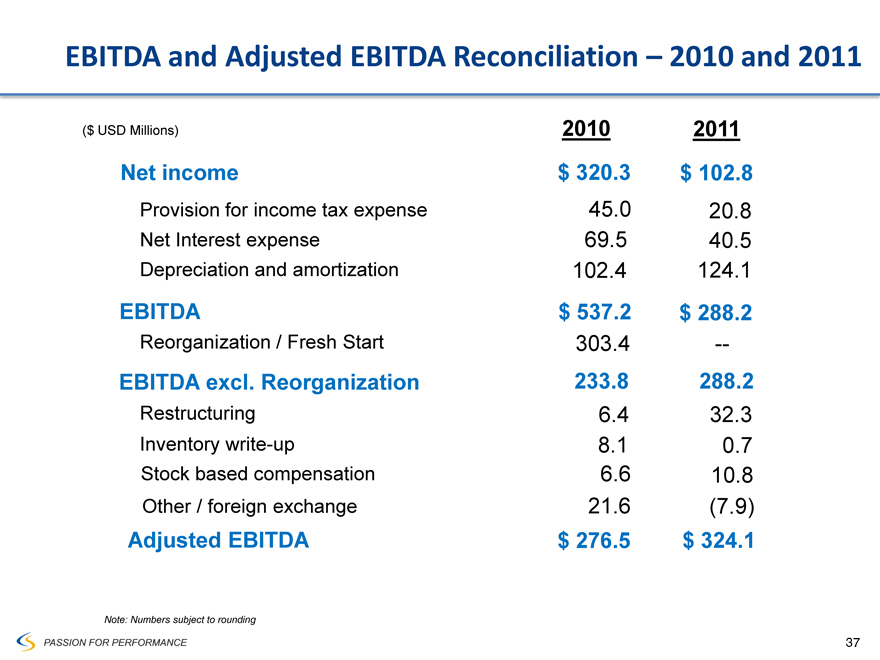

EBITDA and Adjusted EBITDA Reconciliation – 2010 and 2011

($ USD Millions) 2010 2011

Net income $ 320.3 $ 102.8

Provision for income tax expense 45.0 20.8

Net Interest expense 69.5 40.5

Depreciation and amortization 102.4 124.1

EBITDA $ 537.2 $ 288.2

Reorganization / Fresh Start 303.4 -

EBITDA excl. Reorganization 233.8 288.2

Restructuring 6.4 32.3

Inventory write-up 8.1 0.7

Stock based compensation 6.6 10.8

Other / foreign exchange 21.6 (7.9)

Adjusted EBITDA $ 276.5 $ 324.1

Note: Numbers subject to rounding

PASSION FOR PERFORMANCE 37

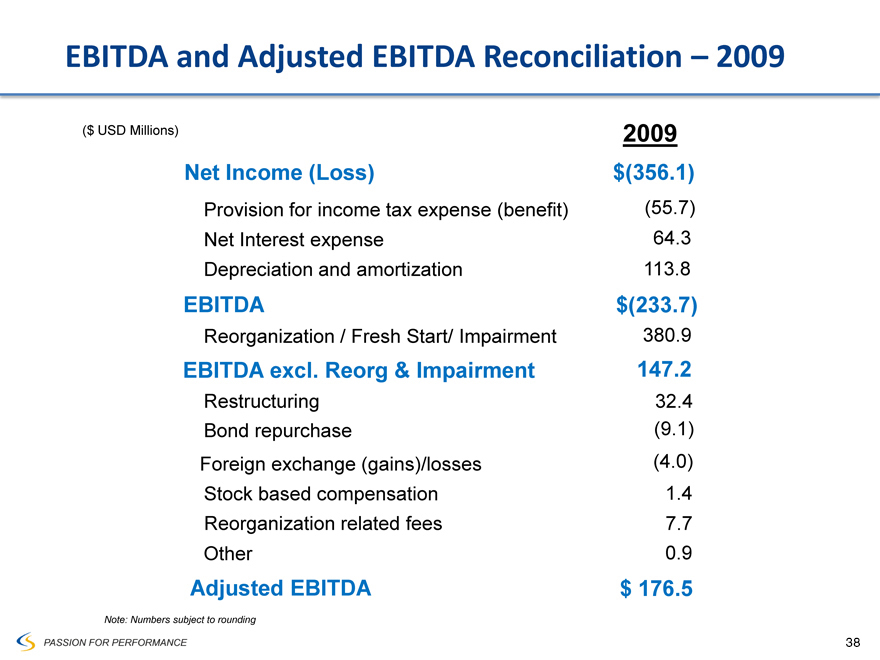

EBITDA and Adjusted EBITDA Reconciliation – 2009

($ USD Millions) 2009

Net Income (Loss) $(356.1)

Provision for income tax expense (benefit) (55.7)

Net Interest expense 64.3

Depreciation and amortization 113.8

EBITDA $(233.7)

Reorganization / Fresh Start/ Impairment 380.9

EBITDA excl. Reorg & Impairment 147.2

Restructuring 32.4

Bond repurchase (9.1)

Foreign exchange (gains)/losses (4.0)

Stock based compensation 1.4

Reorganization related fees 7.7

Other 0.9

Adjusted EBITDA $ 176.5

Note: Numbers subject to rounding

PASSION FOR PERFORMANCE 38

Non-GAAP Financial Measures

EBITDA and adjusted EBITDA are measures not recognized under Generally Accepted Accounting Principles (GAAP) which exclude certain non-cash and non-recurring items.

When analyzing the company’s operating performance, investors should use EBITDA and adjusted EBITDA in addition to, and not as alternatives for, net income (loss), operating income, or any other performance measure derived in accordance with GAAP, or as an alternative to cash flow from operating activities as a measure of the company’s performance. EBITDA and adjusted EBITDA have limitations as analytical tools and should not be considered in isolation or as substitutes for analysis of the company’s results of operations as reported under GAAP. Other companies may report EBITDA and adjusted EBITDA differently and therefore Cooper Standard’s results may not be comparable to other similarly titled measures of other companies.

PASSION FOR PERFORMANCE 39